Looking for the Cradle of Life Sergio Branciamore DBAG- University of Florence - Italy.

DRIV ING EXPANSION.ENSURING

CONTINUIT Y.M A K I N G S T R O N G

C O M P A N I E S S T R O N G E R .

A N N U A L R E P O R T

2 0 1 3 / 1 4

www.deutsche-beteiligung.de

ISSN

161

9-12

26

De

uts

che

Be

teil

igu

ng

s A

GA

nn

ua

l R

ep

ort

20

13

/14

C O N T E N T SA N N U A L R E P O R T 2 0 13 / 1 4

LONG-TERM PERFORMANCE I

2013/14 HIGHLIGHTS I I

T O O U R S H A R E H O L D E R S 2

LETTER FROM THE BOARD OF MANAGEMENT 2

BOARD OF MANAGEMENT 3

REPORT OF THE SUPERVISORY BOARD 4

CORPORATE GOVERNANCE 10

SHARES 14

O U R P O R T F O L I O 22

5 0 Y E A R S O F D B AG 40

C O M B I N E D M A N AG E M E N T R E P O R T 52

BUSINESS OVERVIEW 54

THE GROUP AND UNDERLYING CONDITIONS 55

BUSINESS REVIEW OF THE GROUP 69

FINANCIAL REVIEW OF

DEUTSCHE BETEIL IGUNGS AG (COMMENTARY BASED

ON THE GERMAN COMMERCIAL CODE – HGB) 94

SIGNIFICANT EVENTS AFTER THE END

OF THE REPORTING PERIOD 100

ADDITIONAL STATUTORY INFORMATION

AND COMMENTARY 101

OPPORTUNITIES AND RISKS 108

REPORT ON EXPECTED DEVELOPMENTS 124

C O N S O L I DAT E D F I N A N C I A L S TAT E M E N T S 130

CONSOLIDATED STATEMENT OF

COMPREHENSIVE INCOME 132

CONSOLIDATED STATEMENT OF CASH FLOWS 133

CONSOLIDATED STATEMENT OF FINANCIAL POSIT ION 134

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY 135

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 136

M I S C E L L A N E O U S I N F O R M AT I O N 196

STATEMENT OF RESPONSIBIL ITY 196

AUDITOR’S REPORT 197

CONTACT 198

IMPRINT 198

TEN-YEAR FINANCIAL SUMMARY I I I

F INANCIAL CALENDAR IV

F I N A N CI A L C A L EN DA R

2 2 J A N UA RY 2 015

Annual press conference 2013/14, Frankfurt / Main

2 2 J A N UA RY 2 015

Analysts’ conference, Frankfurt / Main

11 F E B R UA RY 2 015

Listed Private Equity Day, Zurich

18 /19 F E B R UA RY 2 015 Road Show Great Britain, London/Edinburgh

16 M A R C H 2 015

Report on the first quarter 2014/15, Analysts’ conference call

21 M A R C H 2 015 Börsentag Munich (SdK Stock Forum), Munich

2 4 M A R C H 2 015

Annual Meeting, Frankfurt /Main

2 5 M A R C H 2 015

Dividend payment 2015

14 A P R I L 2 015 Solventis Stock Forum, Frankfurt/Main

15 J U N E 2 015

Report on the second quarter 2014/15, Analysts’ conference call

14 S E P T E M B E R 2 015

Report on the third quarter 2014/15, Analysts’ conference call

I V

D R I V I N G E X PA N S I O N . E N S U R I N G C O N T I N U I T Y. I D R I V I N G E X PA N S I O N . E N S U R I N G C O N T I N U I T Y. I I

LO N G -T ER M P ER F O R M A N CE 2013 /14 H I G H L I G H T S

Net asset value rose after paying a dividend of 1.20 euros in March 2014 to 22.18 euros per share at 31 October 2014. This equates to a gain of 1.82 euros, or a return of 15.8 percent in financial year 2013/14. Thus, we exceeded both the cost of equity and the long-term average: over the past ten-year period, we generated an average return on net asset value per share of 15.3 percent.

More information on the historical return trend on page 88.

R E T U R N O N N E T A S S E T VA L U E P E R S H A R E (%)

60

50

40

30

20

10

0

(10)

(20)

04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

20.0

36.4

56.2

7.3 12.7

(6.2)

16.811.5

15.8

(17.5)

In financial year 2013/14, the price of DBAG shares rose to 21.83 euros, up from 19.36 euros. Including the dividend of 1.20 euros that we paid per share in March 2014, we delivered a total return to our shareholders of 19.5 percent.Thus, DBAG shares outperformed the S-Dax – the benchmark index for German companies of a comparable size – and the LPX Direct – the benchmark index for directly investing private equity firms. Over a ten-year period, DBAG shares generated an average total return for our shareholders of 16.2 percent annually. That is roughly twice the return delivered by the benchmark indices.

More information on DBAG shares on page 14.

P E R F O R M A N C E O F D B A G S H A R E S A N D B E N C H M A R K I N D I C E S

(1 November 2004 to 31 October 2014, indexed to 1 November 2004 = 100)

450

400

350

300

250

200

150

100

50

DBAG

Dax

S-Dax

LPX Direct

1 Nov. 04 1 Nov. 06 1 Nov. 08 1 Nov. 10 1 Nov.12 1 Nov. 14

The consolidated net income of 47.8 million euros (previous year: 32.3 million euros) reflects profits from attractive divestments to strategic investors, very satisfactory progress on the part of most portfolio companies and higher fee income from investment services to funds.The net result of investment activity reached 54.5 million euros (previous year: 41.0 million euros); fee income from fund management and advisory services totalled 21.7 million euros (previous year: 18.9 million euros).

More information on the consolidated net income on page 75.

C O N S O L I D AT E D N E T I N C O M E (€mn)

120

100

80

60

40

20

0

(20)

(40)

04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

136.5

(51.1)

82.7

19.6

(16.6)

34.144.5

32.3

47.841.3

D R I V I N G E X PA N S I O N . E N S U R I N G C O N T I N U I T Y. I I I

T EN -Y E A R F I N A N CI A L SU M M A RY

€mn 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14

Development of portfolio and value

New investment 24 22 40 14 4 8 9 22 42 20

“Portfolio value” (31 Oct.) 1 197 121 189 127 123 118 84 143 173 153

Number of investments (31 Oct.) 35 32 30 21 19 17 16 18 20 19

Earnings position

EBIT 41.6 89.1 150.8 (60.5) 20.4 36.8 (23.0) 46.2 33.6 48.2

EBT 42.3 90.9 155.6 (55.3) 22.4 37.6 (19.9) 47.0 33.8 48.5

Consolidated net income/(loss) for the year 41.3 82.7 136.5 (51.1) 19.6 34.1 (16.6) 44.5 32.3 47.8

Consolidated retained profit 35.5 57.2 118.2 29.2 52.6 73.1 37.3 70.8 86.7 118.1

Financial position

Cash flows from operating activities (35.6) (4.1) (2.6) 3.0 (3.5) (12.8) 0.9 (9.6) (12.0) (1.4)

Cash flows from investing activities 132.2 169.3 65.4 11.2 28.8 36.3 34.1 (17.8) 18.7 70.8

thereof proceeds from disposals of financial assets 156.5 191.0 106.1 25.7 33.0 44.5 43.6 3.8 60.4 90.8

thereof purchase of financial assets (24.1) (21.7) (40.7) (14.5) (4.3) (8.2) (9.4) (21.6) (41.7) (20.0)

Cash flows from financing activities (57.1) (40.7) (71.4) (57.3) (5.5) (13.7) (19.1) (10.9) (16.4) (16.4)

Change in cash funds 2 39.5 124.0 (9.0) (50.5) 10.6 (70.9) 14.9 (38.7) (9.7) 52.4

Asset position

Non-current assets 201.1 124.6 211.3 147.2 161.2 244.3 228.6 238.7 233.6 243.9

thereof long-term securities 0 0 0 0 14.5 102.9 123.1 83.0 50.5 81.0

Current assets 65.2 195.5 183.0 125.1 127.1 71.8 51.3 59.5 77.1 103.2

thereof cash and short-term securities 40.7 164.7 155.8 105.2 109.5 37.8 32.5 27.8 47.8 69.7

Equity 246.6 289.0 353.6 244.8 256.8 273.9 238.9 266.2 278.4 303.4

Liabilities/provisions 19.7 31.1 40.8 27.4 31.5 42.2 41.0 32.8 32.2 43.7

Total assets 266.3 320.1 394.4 272.3 288.3 316.1 279.9 299.0 310.7 347.1

Key indicators

Return on NAV per share after taxes 3 (%) 18.1 36.4 56.2 (17.5) 7.3 12.7 (6.2) 16.7 11.5 15.8

Equity as a percentage of total assets 92.6 90.3 89.7 89.9 89.1 86.7 85.3 89.0 89.6 87.4

Information on shares 4

Earnings per share (€) 1.79 5.02 9.20 (3.73) 1.44 2.50 (1.22) 3.25 2.36 3.49

NAV per share (€) 14.64 19.07 25.09 17.90 18.77 20.03 17.47 19.46 20.36 22.18

Dividend per share (€; 2013/14: recommended) 0.33 0.50 1.00 0.40 0.40 0.40 0.40 0.40 0.40 0.40

Surplus dividend/bonus per share (€; 2013/14: recommended) 0.33 2.50 2.50 – 0.60 1.00 0.40 0.80 0.80 1.60

Total amount distributed 5 (2013/14: recommended) 11.1 45.5 47.9 5.5 13.7 19.1 10.9 16.4 16.4 27.4

Number of shares (end of FY) 16,837,329 15,153,864 14,403,864 13,676,359 13,676,359 13,676,359 13,676,359 13,676,359 13,676,359 13,676,359

thereof held by the Company 313.367

Share price (€; end of FY) 13.25 17.35 24.10 10.45 15.55 20.79 15.50 19.49 19.36 21.83

Market capitalisation (end of FY) 223.1 262.9 347.1 142.9 212.7 284.3 212.0 266.6 264.8 298.6

Number of employees 50 44 47 48 49 51 53 54 55 56

The table above contains data as originally reported in the respective annual consolidated financial statements. 1 Without interests in shelf companies and companies that are mainly attributable to third parties 2 Cash as well as short- and long-term securities3 Change in net asset value per share relative to opening net asset value per share at beginning of reporting period, less dividends per share4 Partly adjusted; earnings and cash flow per share relative to weighted average number of shares outstanding 5 Relates to respective financial year

C O N S O L I DAT E D N E T I N C O M E reaches

M I L L I O N E U R O S

R E T U R N O N N E T A S S E T VA L U E per share

P E R C E N T

T O TA L R E T U R N to shareholders

P E R C E N T

47.8

15.8

19.5

DRIV ING EXPANSION.ENSURING

CONTINUIT Y.M A K I N G S T R O N G

C O M P A N I E S S T R O N G E R .

A N N U A L R E P O R T

2 0 1 3 / 1 4

www.deutsche-beteiligung.de

ISSN

161

9-12

26

De

uts

che

Be

teil

igu

ng

s A

GA

nn

ua

l R

ep

ort

20

13

/14

C O N T E N T SA N N U A L R E P O R T 2 0 13 / 1 4

LONG-TERM PERFORMANCE I

2013/14 HIGHLIGHTS I I

T O O U R S H A R E H O L D E R S 2

LETTER FROM THE BOARD OF MANAGEMENT 2

BOARD OF MANAGEMENT 3

REPORT OF THE SUPERVISORY BOARD 4

CORPORATE GOVERNANCE 10

SHARES 14

O U R P O R T F O L I O 22

5 0 Y E A R S O F D B AG 40

C O M B I N E D M A N AG E M E N T R E P O R T 52

BUSINESS OVERVIEW 54

THE GROUP AND UNDERLYING CONDITIONS 55

BUSINESS REVIEW OF THE GROUP 69

FINANCIAL REVIEW OF

DEUTSCHE BETEIL IGUNGS AG (COMMENTARY BASED

ON THE GERMAN COMMERCIAL CODE – HGB) 94

SIGNIFICANT EVENTS AFTER THE END

OF THE REPORTING PERIOD 100

ADDITIONAL STATUTORY INFORMATION

AND COMMENTARY 101

OPPORTUNITIES AND RISKS 108

REPORT ON EXPECTED DEVELOPMENTS 124

C O N S O L I DAT E D F I N A N C I A L S TAT E M E N T S 130

CONSOLIDATED STATEMENT OF

COMPREHENSIVE INCOME 132

CONSOLIDATED STATEMENT OF CASH FLOWS 133

CONSOLIDATED STATEMENT OF FINANCIAL POSIT ION 134

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY 135

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 136

M I S C E L L A N E O U S I N F O R M AT I O N 196

STATEMENT OF RESPONSIBIL ITY 196

AUDITOR’S REPORT 197

CONTACT 198

IMPRINT 198

TEN-YEAR FINANCIAL SUMMARY I I I

F INANCIAL CALENDAR IV

F I N A N CI A L C A L EN DA R

2 2 J A N UA RY 2 015

Annual press conference 2013/14, Frankfurt / Main

2 2 J A N UA RY 2 015

Analysts’ conference, Frankfurt / Main

11 F E B R UA RY 2 015

Listed Private Equity Day, Zurich

18 /19 F E B R UA RY 2 015 Road Show Great Britain, London/Edinburgh

16 M A R C H 2 015

Report on the first quarter 2014/15, Analysts’ conference call

21 M A R C H 2 015 Börsentag Munich (SdK Stock Forum), Munich

2 4 M A R C H 2 015

Annual Meeting, Frankfurt /Main

2 5 M A R C H 2 015

Dividend payment 2015

14 A P R I L 2 015 Solventis Stock Forum, Frankfurt/Main

15 J U N E 2 015

Report on the second quarter 2014/15, Analysts’ conference call

14 S E P T E M B E R 2 015

Report on the third quarter 2014/15, Analysts’ conference call

I V

D R I V I N G E X PA N S I O N . E N S U R I N G C O N T I N U I T Y. I D R I V I N G E X PA N S I O N . E N S U R I N G C O N T I N U I T Y. I I

LO N G -T ER M P ER F O R M A N CE 2013 /14 H I G H L I G H T S

Net asset value rose after paying a dividend of 1.20 euros in March 2014 to 22.18 euros per share at 31 October 2014. This equates to a gain of 1.82 euros, or a return of 15.8 percent in financial year 2013/14. Thus, we exceeded both the cost of equity and the long-term average: over the past ten-year period, we generated an average return on net asset value per share of 15.3 percent.

More information on the historical return trend on page 88.

R E T U R N O N N E T A S S E T VA L U E P E R S H A R E (%)

60

50

40

30

20

10

0

(10)

(20)

04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

20.0

36.4

56.2

7.3 12.7

(6.2)

16.811.5

15.8

(17.5)

In financial year 2013/14, the price of DBAG shares rose to 21.83 euros, up from 19.36 euros. Including the dividend of 1.20 euros that we paid per share in March 2014, we delivered a total return to our shareholders of 19.5 percent.Thus, DBAG shares outperformed the S-Dax – the benchmark index for German companies of a comparable size – and the LPX Direct – the benchmark index for directly investing private equity firms. Over a ten-year period, DBAG shares generated an average total return for our shareholders of 16.2 percent annually. That is roughly twice the return delivered by the benchmark indices.

More information on DBAG shares on page 14.

P E R F O R M A N C E O F D B A G S H A R E S A N D B E N C H M A R K I N D I C E S

(1 November 2004 to 31 October 2014, indexed to 1 November 2004 = 100)

450

400

350

300

250

200

150

100

50

DBAG

Dax

S-Dax

LPX Direct

1 Nov. 04 1 Nov. 06 1 Nov. 08 1 Nov. 10 1 Nov.12 1 Nov. 14

The consolidated net income of 47.8 million euros (previous year: 32.3 million euros) reflects profits from attractive divestments to strategic investors, very satisfactory progress on the part of most portfolio companies and higher fee income from investment services to funds.The net result of investment activity reached 54.5 million euros (previous year: 41.0 million euros); fee income from fund management and advisory services totalled 21.7 million euros (previous year: 18.9 million euros).

More information on the consolidated net income on page 75.

C O N S O L I D AT E D N E T I N C O M E (€mn)

120

100

80

60

40

20

0

(20)

(40)

04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

136.5

(51.1)

82.7

19.6

(16.6)

34.144.5

32.3

47.841.3

D R I V I N G E X PA N S I O N . E N S U R I N G C O N T I N U I T Y. I I I

T EN -Y E A R F I N A N CI A L SU M M A RY

€mn 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14

Development of portfolio and value

New investment 24 22 40 14 4 8 9 22 42 20

“Portfolio value” (31 Oct.) 1 197 121 189 127 123 118 84 143 173 153

Number of investments (31 Oct.) 35 32 30 21 19 17 16 18 20 19

Earnings position

EBIT 41.6 89.1 150.8 (60.5) 20.4 36.8 (23.0) 46.2 33.6 48.2

EBT 42.3 90.9 155.6 (55.3) 22.4 37.6 (19.9) 47.0 33.8 48.5

Consolidated net income/(loss) for the year 41.3 82.7 136.5 (51.1) 19.6 34.1 (16.6) 44.5 32.3 47.8

Consolidated retained profit 35.5 57.2 118.2 29.2 52.6 73.1 37.3 70.8 86.7 118.1

Financial position

Cash flows from operating activities (35.6) (4.1) (2.6) 3.0 (3.5) (12.8) 0.9 (9.6) (12.0) (1.4)

Cash flows from investing activities 132.2 169.3 65.4 11.2 28.8 36.3 34.1 (17.8) 18.7 70.8

thereof proceeds from disposals of financial assets 156.5 191.0 106.1 25.7 33.0 44.5 43.6 3.8 60.4 90.8

thereof purchase of financial assets (24.1) (21.7) (40.7) (14.5) (4.3) (8.2) (9.4) (21.6) (41.7) (20.0)

Cash flows from financing activities (57.1) (40.7) (71.4) (57.3) (5.5) (13.7) (19.1) (10.9) (16.4) (16.4)

Change in cash funds 2 39.5 124.0 (9.0) (50.5) 10.6 (70.9) 14.9 (38.7) (9.7) 52.4

Asset position

Non-current assets 201.1 124.6 211.3 147.2 161.2 244.3 228.6 238.7 233.6 243.9

thereof long-term securities 0 0 0 0 14.5 102.9 123.1 83.0 50.5 81.0

Current assets 65.2 195.5 183.0 125.1 127.1 71.8 51.3 59.5 77.1 103.2

thereof cash and short-term securities 40.7 164.7 155.8 105.2 109.5 37.8 32.5 27.8 47.8 69.7

Equity 246.6 289.0 353.6 244.8 256.8 273.9 238.9 266.2 278.4 303.4

Liabilities/provisions 19.7 31.1 40.8 27.4 31.5 42.2 41.0 32.8 32.2 43.7

Total assets 266.3 320.1 394.4 272.3 288.3 316.1 279.9 299.0 310.7 347.1

Key indicators

Return on NAV per share after taxes 3 (%) 18.1 36.4 56.2 (17.5) 7.3 12.7 (6.2) 16.7 11.5 15.8

Equity as a percentage of total assets 92.6 90.3 89.7 89.9 89.1 86.7 85.3 89.0 89.6 87.4

Information on shares 4

Earnings per share (€) 1.79 5.02 9.20 (3.73) 1.44 2.50 (1.22) 3.25 2.36 3.49

NAV per share (€) 14.64 19.07 25.09 17.90 18.77 20.03 17.47 19.46 20.36 22.18

Dividend per share (€; 2013/14: recommended) 0.33 0.50 1.00 0.40 0.40 0.40 0.40 0.40 0.40 0.40

Surplus dividend/bonus per share (€; 2013/14: recommended) 0.33 2.50 2.50 – 0.60 1.00 0.40 0.80 0.80 1.60

Total amount distributed 5 (2013/14: recommended) 11.1 45.5 47.9 5.5 13.7 19.1 10.9 16.4 16.4 27.4

Number of shares (end of FY) 16,837,329 15,153,864 14,403,864 13,676,359 13,676,359 13,676,359 13,676,359 13,676,359 13,676,359 13,676,359

thereof held by the Company 313.367

Share price (€; end of FY) 13.25 17.35 24.10 10.45 15.55 20.79 15.50 19.49 19.36 21.83

Market capitalisation (end of FY) 223.1 262.9 347.1 142.9 212.7 284.3 212.0 266.6 264.8 298.6

Number of employees 50 44 47 48 49 51 53 54 55 56

The table above contains data as originally reported in the respective annual consolidated financial statements. 1 Without interests in shelf companies and companies that are mainly attributable to third parties 2 Cash as well as short- and long-term securities3 Change in net asset value per share relative to opening net asset value per share at beginning of reporting period, less dividends per share4 Partly adjusted; earnings and cash flow per share relative to weighted average number of shares outstanding 5 Relates to respective financial year

C O N S O L I DAT E D N E T I N C O M E reaches

M I L L I O N E U R O S

R E T U R N O N N E T A S S E T VA L U E per share

P E R C E N T

T O TA L R E T U R N to shareholders

P E R C E N T

47.8

15.8

19.5

O U R M I S S I O N

S T A T E M E N T

Stock exchange-listed Deutsche Beteiligungs AG invests

in well-positioned mid-sized companies with potential

for growth.

For many years, we have focused on industrial business

models in selected sectors. With our experience, expertise

and equity, we support our portfolio companies in

implementing their sustainable, value-creating corporate

strategies.

Our entrepreneurial approach to investing has made us a

sought-after investment partner in the German-speaking

world. We have achieved superior performance over

many years – for our portfolio companies as well as for

our shareholders and investors.

A N N U A L R E P O R T 2 0 1 3 / 1 4 1

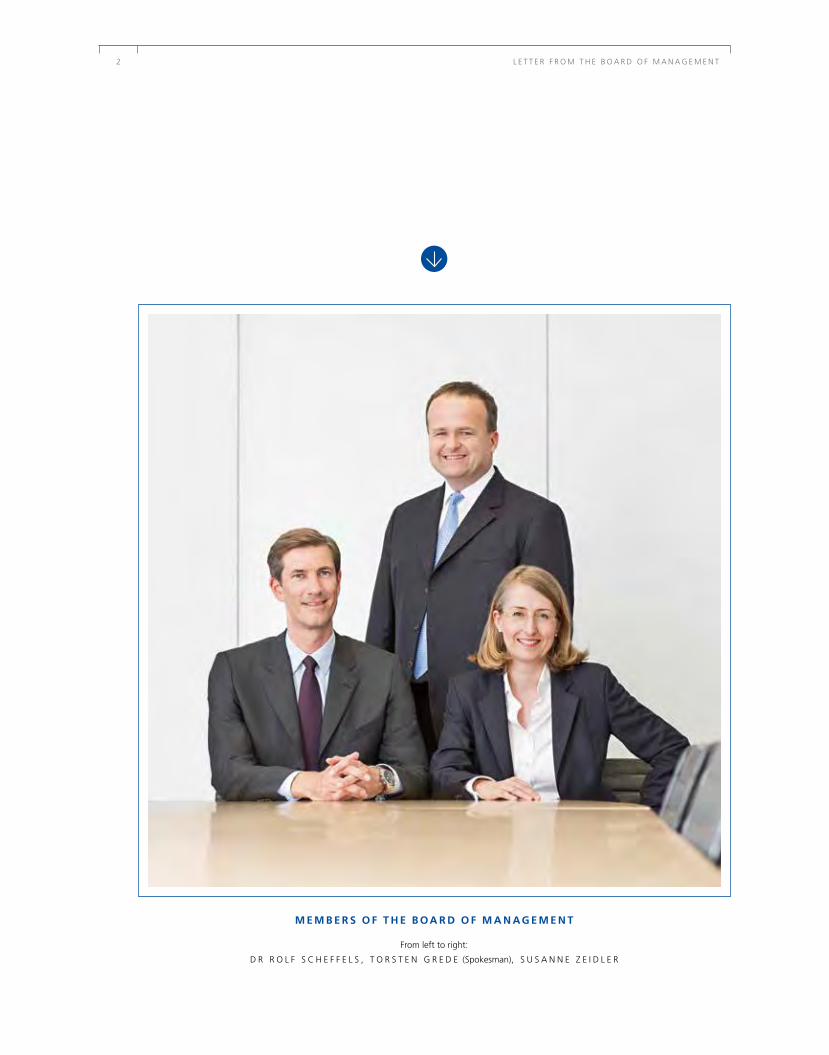

M E M B E R S O F T H E B OA R D O F M A N AG E M E N T

From left to right:

D R R O L F S C H E F F E L S , T O R S T E N G R E D E (Spokesman), S U S A N N E Z E I D L E R

2 L E T T E R F R O M T H E B O A R D O F M A N A G E M E N T

For Deutsche Beteiligungs AG, 2015 will be a very special year. This autumn, we will be looking back on 50 years of investing in Germany’s “Mittelstand”. Five decades during which we have financed growth through customised equity solutions and have driven change processes. Five decades during which we have backed farsighted entrepreneurs and courageous managers in developing their companies. In other words, five decades during which DBAG has played a leading role in private equity in Germany. We, too, have moved forward over time. With our successful investment activities as a point of departure, we have developed a growing fund business in recent years. The result is that we now create value in two ways: by providing investment services to private equity funds and, as always, by investing in portfolio companies.

DBAG today is one of Germany’s most successful private equity companies, and there are surely a number of reasons for that. One of them is that we have remained true to our investment principles: we invest in strong companies that have growth potential, an excellent market position and seasoned management.

Investing, developing and, finally, realising created value – that is the triad that defines our business. In 2013/14, we exited two long-standing investments, realising the value that had been built over many years. Our “young” portfolio is developing much to our satisfaction: most of our portfolio companies made good progress and very satisfactory value contributions. That is actually what we expect of the companies in which we recently invested. Please allow us to expound here on the three aspects of our business:

To begin with, the realisations. As has so often been the case in the past, we were able to draw the attention of buyers for whom our investments had a strategic value. And that was clearly reflected in the purchase prices. DBAG invested in Homag Group AG in 1997. In 2007, we led

Frankfurt/Main, 20 January 2015

— 1 —

A N N U A L R E P O R T 2 0 1 3 / 1 4 1

the company to an IPO; the proceeds from that alone considerably exceeded the invested capital. In finalising the disinvestment this past summer, we completed a transaction that – measured in absolute terms – was one of the most profitable in DBAG’s history. It provides the basis for the surplus dividend, which we are again recommending – for the ninth time in ten years. In October 2014, we divested another successful investment after 39 years in our portfolio: automotive dealership Dr. Vogler. Once again, the company was sold to a strategic buyer.

As for the development of the portfolio, it encompassed 15 active investments at the end of the period: ten management buyouts and five expansion capital investments. Two figures illustrate how well the companies have performed overall. They increased revenues by an average of nine percent compared with the preceding year. The improvement in their earnings power was even more impressive: an average of twelve percent. This was a key reason for the past financial year’s good valuation result. The recent additions to the portfolio in particular made good on their potential. Eight of the 15 active investments have been in the portfolio for less than two years – representing some 45 percent of the portfolio value. Momentum also came from the stock market: part of the value gain comes from higher valuation multiples.

Finally, the investments. These lay the foundation for positive value contributions in coming years. In 2013/14, we invested 20 million euros from DBAG’s balance sheet. We acquired a stake in a bakery chain and provided further funding to our portfolio companies for their expansion plans. “Unser Heimatbäcker” is one of the ten largest bakery chains in Germany. The company is growing rapidly and is proactively driving change in its market. After “Schülerhilfe” last year, this is the second company whose development is fuelled to a large degree by Germany’s domestic market and consumer demand. Both sectors – tutoring services and bakeries – are generally considered non-cyclical. This represents a positive change to the risk profile of our portfolio, which is also more balanced in terms of size now that we have exited what was our largest investment by far.

The investment team considered many interesting companies in 2013/14, and we would have liked to invest more. Yet one principle remains unchanged: we do not want to invest in as many companies as possible, but in the best companies possible. Additionally, competition has intensified. Strategic investors are expanding their companies through add-on acquisitions. Driven by low interest rates, players such as foundations and family offices are approaching attractive companies. Our response is to continuously improve our processes. Moreover, we have expanded our investment team once again.

— 2 —

2 L E T T E R F R O M T H E B O A R D O F M A N A G E M E N T

We are very pleased with financial year 2013/14. The consolidated net income of 47.8 mil lion euros exceeds our expectations. It represents a return on net asset value of 15.8 percent, nearly doubling our forecast of at least eight percent. 2013/14 is another in a series of successful financial years: over a ten-year period, we increased the net asset value per share by an average of 15.3 percent per year.

In addition to realisation profits and the portfolio companies’ value growth, a significant contributor to consolidated net income was fee income from fund management and advisory services – which increased yet again and is now almost double the amount it was five years ago. Within a decade, it has more than tripled. These developments show the value institutional investors attach to the “Deutsche Beteiligungs AG” brand, its investment team and its wealth of experience. The assets we manage and advise amount to nearly one billion euros – not counting the capital that you, the shareholders, have entrusted to us. This, too, represents a significant increase compared to 2004.

You have profited time and again from our investment activity in the form of sizeable distributions. Our policy is to be able to pay a base dividend even in years when we do not generate special realisation profits. Successful realisations of the kind seen in 2013/14 then make surplus dividends possible. The Supervisory Board and the Board of Management therefore recommend distributing 2.00 euros per share, which includes a surplus dividend of 1.60 euros per share.

We will be celebrating another anniversary this year: December 2015 will mark the 30th anniversary of the initial stock market listing of DBAG shares. Anyone who has held DBAG shares since 1985 and who reinvested the dividends in DBAG will be very pleased about the annual return of some 9.6 percent which DBAG shares delivered. Those who became DBAG shareholders later on were also well rewarded. Over the past ten-year period, DBAG shares returned an average of 16 percent annually, or nearly double the amount of investments in the Dax or S-Dax. This past financial year, DBAG shares delivered a total return of nearly 20 percent.

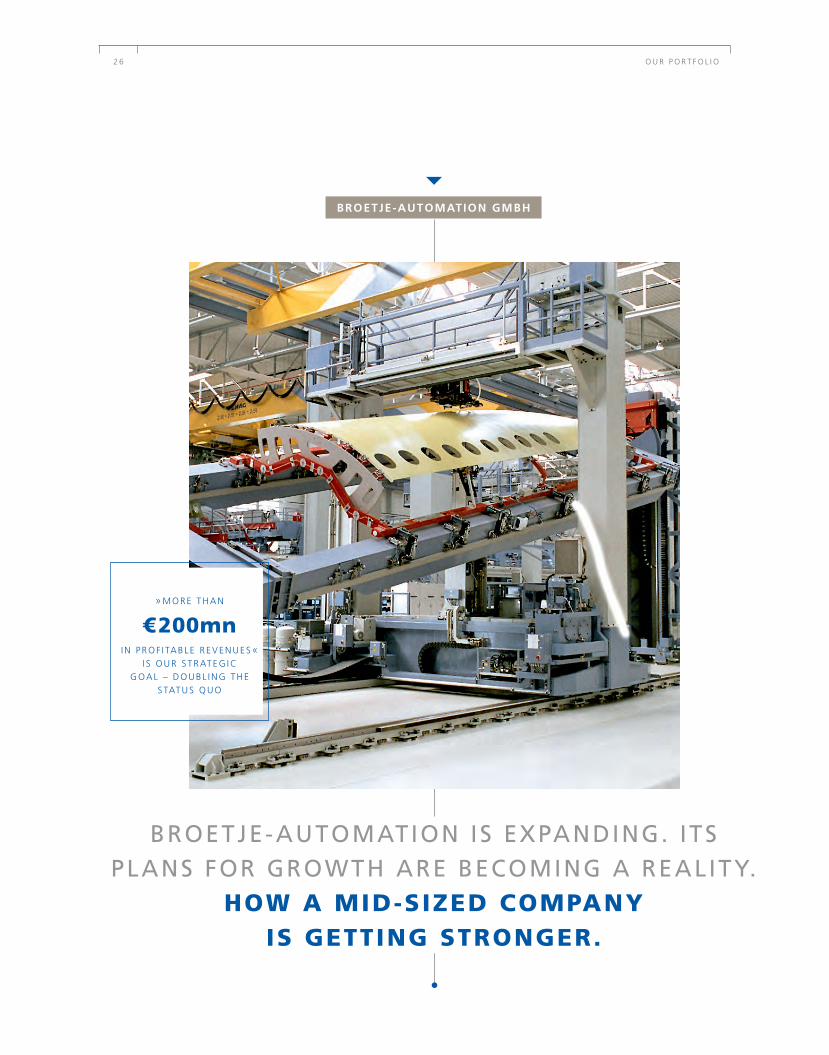

To continue this development, the companies in our portfolio will keep to the course mutually agreed at the outset of our investment. One of the key objectives was often growth. For that reason, the motto of this year’s Annual Report is “Driving expansion, ensuring continuity”. What this means is illustrated by looking at Broetje-Automation, a mechanical

— 3 —

A N N U A L R E P O R T 2 0 1 3 / 1 4 3

M I T G L I E D E R D E S VO R S TA N D S

Von links nach rechts:

D R . R O L F S C H E F F E L S , S U S A N N E Z E I D L E R , T O R S T E N G R E D E (Sprecher)

engineering and plant construction company (page 26). In a magazine, you can retrace 50 years of Deutsche Beteiligungs AG (page 40). Looking back, one thing becomes evident: DBAG has always been committed to Germany’s “Mittelstand”.

That commitment endures. We frequently find our investments in sectors for which the “Mittelstand” is known throughout the world. The investments we agreed at the beginning of the new financial year are prime examples. The three companies have a more than 100-year history: a manufacturer of specialised films and a mechanical engineering com pany can now take advantage of growth opportunities, unfettered by corporate constraints; and a foundry will develop its potential with support from DBAG. All in all, a solid start on the investment side.

What can you expect of DBAG in its anniversary year 2014/15? As always, great dedication on the part of the investment team to augmenting the value of the existing portfolio companies and to investing in new ones. Also as in the past, a steady flow of transparent information – with the stock market as a watchful motivator. And consolidated net income which, on a comparable basis, should slightly exceed that of the previous year – that is, without the effects of the Homag realisation. Disinvestments can rarely be planned in our business, neither the timing, nor the price. For that reason, we have based our one-year forecast on our costing, the expected fee income from investment services to funds, and the valuation contribution of our portfolio. The latter component is the least certain of the three since portfolio companies are not immune to cyclical influences. Distortions or a shift in sentiment in the stock markets can change company valuations quickly and significantly, thereby greatly impacting our annual net income. Both risks have, in our estimation, increased.

We measure the performance of each investment at the end of the holding period, which is not one year, but usually from four to seven years. During that time, we aim to make our portfolio companies more valuable – thereby continuing to create value for you. Our 50 years of success are no reason for us to sit back and relax. Instead, they are a reason – a mandate – to press on, ensuring that the next 50 are equally rewarding.

Torsten Grede Dr Rolf Scheffels Susanne Zeidler

— 4 —

2 L E T T E R F R O M T H E B O A R D O F M A N A G E M E N T

BOA R D O F M A N AG EM EN T

T O R S T E N G R E D E

Spokesman

Strategy and Business Development, Corporate Communication, Com pliance, Investment Business, Investor Relations (fund investors)

D R R O L F S C H E F F E L S

Investment Business, Investment Team Development

S U S A N N E Z E I D L E R

Chief Financial Officer

Finance and Accounting, Legal and Fiscal, Investor Relations (stock market), Investment Controlling, Internal Audit, Personnel, IT and Organisation

Torsten Grede studied business administration in Cologne and St Gallen, following a traineeship in banking. After earning his degree, he started his career in 1990 at Deutsche Beteiligungs AG; he now has more than 20 years of experience in private equity. Torsten Grede was named Senior Vice President in 1995 and was initially appointed to the Board of Management in 2001.

After completing a traineeship as an industrial administrator at Braun AG, Dr Rolf Scheffels studied business administration at the Goethe University in Frankfurt/Main, where he received his degree. His career began in 1992 with the audit firm C&L Deutsche Revision AG, Frankfurt/Main. In 1996, Dr Rolf Scheffels earned his doctorate (Dr. rer. pol.) at the Goethe University. He joined Deutsche Beteiligungs AG in 1997. Dr Rolf Scheffels was named Senior Vice President in 2000 and was initially appointed to the Board of Management in 2004.

Susanne Zeidler studied business administration at the University of Münster. She began her professional career in 1987 with an audit partnership that specialised in midsized companies. She moved into the area of corporate finance at an audit firm in 1990, where she was responsible, until 1999, for valuations of midsized and listed companies operating in various sectors. After becoming a partner in 2000, Susanne Zeidler headed the internal audit review and other back office activities at the audit firm’s largest German office. Beginning in 2005, she built the firm’s activities with foundations and other nonprofit organisations. In 2011, she joined a worldwide fundraising organisation, where she served as director at its international headquarters.

Born 1964. Spokesman of the Board of Management since March 2013; member of the Board of Management since January 2001; appointed until December 2018.

Born 1966. Member of the Board of Management since January 2004; appointed until March 2016.

Born 1961. Member of the Board of Management since November 2012; appointed until October 2020.

A N N U A L R E P O R T 2 0 1 3 / 1 4 3

Posting an excellent consolidated net

income, Deutsche Beteiligungs AG

recorded yet another year of success

in its long history. In 2013/14, our

working relationship with the Board

of Management was again both

effective and trustful.

A N D R E W R I C H A R D S

Chairman of the Supervisory Board

4 R E P O R T O F T H E S U P E R V I S O R Y B O A R D

R EP O RT O F T H E SU P ERV I SO RY BOA R D

In the reporting year, we again consistently and conscientiously discharged the duty of overseeing the managerial activities of the Board of Management required of us by law, the Articles of Association and the rules of procedure. The Board of Management regularly provided the Supervisory Board with comprehensive and prompt information, both in writing and verbally, about the Company’s course of business, its asset, financial and earnings position, the competitive environment and the prospects, as well as the risk management and compliance systems installed at Deutsche Beteiligungs AG. We discussed these issues in depth. Any divergences from the planned course of business were elucidated and substantiated by the Board of Management. The Board of Management also reported on strategic and major operational decisions as well as on the business policies it intends to pursue.

In financial year 2013/14, the Supervisory Board held eight meetings, three of which were telephone conferences. In several instances, the Supervisory Board met without the attendance of the Board of Management.

An integral part of all our Board meetings were detailed reports on current developments in individual portfolio companies. We received comprehensive quarterly reports in writing on those issues from the Board of Management. We were informed promptly and in depth about investments that were not performing as expected. We were also regularly informed about new investments in, and planned realisations from the portfolio.

At our first regular meeting on 28 NOVEMBER 2013, we dealt with the investment progress of the DBAG Expansion Capital Fund. The Board of Management informed us about the preliminary results for the preceding 2012/13 financial year and the potential for a dividend payment. The 2013/14 budget was also presented, which was drawn up based on a new methodology. In the November meeting, we were involved in and contributed to the Corporate Governance Statement (§ 289a of the German Commercial Code – HGB), and submitted the Declaration of Conformity as well as the joint report by the Board of Management and the Supervisory Board on the corporate governance practised at Deutsche Beteiligungs AG.

At our regular meeting on 24 JANUARY 2014, the auditors reported on the results of their audit of the separate financial statements and the consolidated financial statements at 31 October 2013. We adopted the separate financial statements of Deutsche Beteiligungs AG and approved the consolidated financial statements. We passed a joint dividend recommendation and the agenda for the 2014 Annual Meeting. We also discussed issues concerning potential conflicts of interest of Supervisory Board members.

A N N U A L R E P O R T 2 0 1 3 / 1 4 5

At our meeting following the Annual Meeting on 27 MARCH 2014, the Board of Management reported in depth on the market and competitive situation of Deutsche Beteiligungs AG; both fundraising issues and investment opportunities were comprehensively elucidated. We also dealt with the registration of DBAG as an AIF management company in accordance with the German Investment Code (Kapitalanlagegesetzbuch).

In addition to the reports on the portfolio companies and investment projects that are regularly dealt with at every meeting, the topics discussed at our meeting on 12 JUNE 2014 also pertained to the two disposals that were completed in the latter part of the financial year.

In the two telephone conferences on 30 JUNE 2014 and 9 JULY 2014, we were informed in detail about the progress of the negotiations concerning the disinvestment of Homag Group AG, before granting our consent to the sale of this investment.

At our meeting on 11 SEPTEMBER 2014, the Board of Management reported on the status of the compliance system at Deutsche Beteiligungs AG. According to that, there were no breaches in compliance. The Board of Management also reported on the status of the compliance systems at the portfolio companies of DBAG. At this meeting, the Board of Management’s presentations on the Company’s strategic development played a prominent role. We agreed that we again want to review the efficacy of our work practices in financial year 2014/15.

Between meetings, the Board of Management’s spokesman promptly informed the Chairman of the Supervisory Board about significant business issues, after which the complete Supervisory Board was briefed accordingly. In view of its magnitude, the disinvestment of Homag Group AG required our approval. There were no other transactions requiring our consent in financial year 2013/14.

All members of the Supervisory Board attended all of the Board’s meetings this past financial year, except when – as in one instance – there was a conflict of interest regarding an item dealt with on the agenda. The meeting of the Executive Committee was attended by all of its members. The Audit Committee also met in the presence of all members, with one exception.

CO R P O R AT E G OV ER N A N C E

We regularly evaluate the efficacy of our work on the Supervisory Board; we did so most recently in October 2013. We also continually follow the changes in corporate governance practices taking place in Germany. Management’s report on the Company’s corporate governance is also presented on behalf of the Supervisory Board; we adhere to the practice of publishing this report in the Annual Report (pages 10 to 13), and it is also accessible at the Company’s website together with the Corporate Governance Statement. The Board of Management and the Supervisory Board jointly submitted an updated Declaration of Conformity in November 2014 based on the German Corporate Governance Code as amended on 13 May 2013 (§ 161

6 R E P O R T O F T H E S U P E R V I S O R Y B O A R D

German Stock Corporation Act – AktG), which is permanently accessible to any interested party at the Company’s website.

To disseminate its responsibilities and increase efficiency, the Supervisory Board formed an Executive Committee, which also performs the functions of a Nominations Committee, as well as an Audit Committee.

In accordance with the recommendations of the Code, every Supervisory Board member is required to disclose to the Supervisory Board any conflict of interest that may possibly arise. There was one notice of a conflictofinterest issue this past financial year.

W O R K O F T H E E X EC U T I V E CO M M I T T EE

The Executive Committee convened once this past financial year: at its meeting on 21 November 2013, it determined the shortterm performancerelated and the longterm remuneration component for the members of the Board of Management for financial year 2012/13. The Supervisory Board approved the recommendation following an indepth discussion in a telephone conference on 25 November 2013. Since Mr von Hodenberg, in his capacity as a former member of the Board of Management and thereby as a recipient of that performancelinked component, had a personal interest in this decision, he declared that he had a conflict of interest on his own behalf and also pointed to a possible conflict of interest over a decision on the performancelinked component for the other members of Board of Management at that time. He therefore took part neither in the discussion, nor in the vote concerning the performancelinked component for the members of the Board of Management for financial year 2012/13.

The bonus payments for 2013/14 were discussed in a telephone conference at the beginning of the new financial year on 14 November 2014 and recommended to the Supervisory Board. The Supervisory Board approved the recommendation following an indepth discussion in a telephone conference on 18 November 2014. A further meeting in the new financial year (13 January 2015) dealt with Ms Zeidler’s reappointment and her service contract.

W O R K O F T H E AU D I T CO M M I T T EE

In six meetings held during the reporting year, the Audit Committee addressed issues concerning the separate and consolidated financial statements, the halfyearly financial report and the quarterly financial reports, all of which were discussed with the Board of Management prior to their publication. Additionally, the Committee discussed miscellaneous accounting issues, such as the effects of the new accounting standard IFRS 10 on the group of consolidated companies and

A N N U A L R E P O R T 2 0 1 3 / 1 4 7

on the asset, financial and earnings position of the DBAG Group. We monitored the accounting process as well as the effectiveness of the internal control system. From our point of view, there were no grounds for objections to the Company’s current practice.

We reviewed the required independence and objectivity of the Company’s auditors and the additional services the auditors provided. We also discussed the assignment of the audit to the auditors, the determination of the audit’s focal points and audit fees.

We continue to comply in multiple ways with the requirements under §§ 100 (5), 107 (4) German Stock Corporation Act (AktG), which stipulate that at least one independent member of the Supervisory Board or Audit Committee must have expert knowledge of accounting or auditing. In particular the Chairman of the Audit Committee has profound knowledge of and experience in the application of accounting principles and internal control processes.

The Chairmen regularly reported to the Supervisory Board on the work of their committees.

S EPA R AT E A N D CO N S O L I DAT ED F I N A N C I A L S TAT EM EN T S EN D O R S ED

Prior to recommending KPMG AG Wirtschaftsprüfungsgesellschaft (KPMG), Frankfurt/Main, for election as auditors to shareholders at the Annual Meeting, the Supervisory Board requested and received an independency statement from KPMG. Subsequent to the 2014 Annual Meeting, at which our recommendation was adopted, and in my capacity as the Chairman of the Supervisory Board, I commissioned KPMG with the audit. The auditors were required to immediately report all major findings and occurrences to us that may come to light during the audit.

KPMG audited the separate financial statements of Deutsche Beteiligungs AG for financial year 2013/14 and management’s combined report on Deutsche Beteiligungs AG and the Group, including the underlying accounting, and endorsed them with an unqualified certificate. The same applies to the consolidated financial statements for financial year 2013/14. The consolidated financial statements were drawn up in conformity with the International Financial Reporting Standards (IFRS). The auditors confirmed that the consolidated financial statements comply with the IFRS, as adopted by the European Union, and the additional requirements of German commercial law pursuant to § 315a (1) of the German Commercial Code (Handelsgesetzbuch – HGB) and that the consolidated financial statements in their entirety present a true and fair view of the position of the Group as well as the opportunities and risks involved in its future development.

8 R E P O R T O F T H E S U P E R V I S O R Y B O A R D

The Supervisory Board received the audited and certified financial statements of Deutsche Beteiligungs AG for the year ended 31 October 2014 and the combined management report on the state of Deutsche Beteiligungs AG and the Group in due time, reviewed them in conjunction with the report of the Audit Committee Chairman and the auditors, and discussed these documents in detail with the Board of Management in the presence of the auditors. The same applies to the consolidated financial statements as well as to the recommendation for the appropriation of profits.

The auditors explained the findings gathered within the scope of the preaudit at our meeting on 27 November 2014. At our meeting of 20 January 2015 as well as the meeting of the Audit Committee on the same day, the auditors reported on the results of their audit. There were no grounds for objections. The auditors also reported on the services they rendered in addition to performing the audit. The auditors provided detailed answers to our inquiries. After its own indepth review of all documents, the Supervisory Board found no grounds for objection. We approved the results of the audit. On 20 January 2015, we followed the Audit Committee’s recommendation and approved the consolidated financial statements and adopted the separate financial statements of Deutsche Beteiligungs AG.

The Supervisory Board reviewed the Board of Management’s recommendation on the appropriation of the retained profit. After its review, the Supervisory Board agreed to the Board of Management’s recommendation to distribute the sum of 27.4 million euros to shareholders and carry forward the residual retained profit of 64.9 million euros to new account.

Posting an excellent result this past financial year again, Deutsche Beteiligungs AG completed another chapter in its long story of success. We wish to express our greatest appreciation to everyone concerned. Our thanks to the Board of Management and the staff of Deutsche Beteiligungs AG for their outstanding performance and commitment this past financial year.

Frankfurt/Main, 20 January 2015

Andrew Richards Chairman of the Supervisory Board

A N N U A L R E P O R T 2 0 1 3 / 1 4 9

CO R P O R AT E GOV ER N A N CE

Corporate governance refers to the way a company is responsibly managed and controlled. The Supervisory Board and the Board of Management acknowledge and endorse the principles of good corporate governance. We have therefore set out the central values and guiding principles for Deutsche Beteiligungs AG in a Code of Conduct. Our intention is to give every member of our staff a set of fundamental rules and to communicate to our business partners and investors that our dealings are firmly rooted in ethical principles and that we will always interact fairly in good partnership. Our guiding principles also encompass the avoidance of conflicts of interest and acknowledgement of our social responsibility. We act politically neutrally, but support social projects and commit to fair competition.

Our Corporate Governance Statement sets out the basic principles behind the conduct of our business; it is published on the Internet and is accessible there together with this report.

Consistent with the recommendation of the German Corporate Governance Code, the following is a combined report by the Supervisory Board and the Board of Management on the corporate governance practised at Deutsche Beteiligungs AG. Further information can be found in the Corporate Governance Statement and the Report of the Supervisory Board (page 4ff.); that information is an integral part of our combined Corporate Governance Report. We will refer to other sections of this Annual Report on particular issues, if appropriate.

CO M P L I A N C E: EM P LOY EES , T R A N S AC T I O N P RO C ES S , P O R T F O L I O CO M PA N I ES

Compliance by the management and staff with all legal requirements applicable to Deutsche Beteiligungs AG and its subsidiaries and with all internal rules has long been a Company objective and an integral part of our corporate culture. However, as a private equity firm, that objective extends not just to our own Company. DBAG also endorses the installation and ongoing development of compliance schemes at current and future portfolio companies. The compliance system of DBAG therefore consists of three components:

> compliance for DBAG staff

> compliance in transactions

> compliance at portfolio companies

Code of Conduct, Corporate Governance Statement and Corporate Governance Report www.deutsche-beteiligung.de/corporate-governance

1 0 C O R P O R AT E G O V E R N A N C E

A compliance manager oversees adherence by DBAG STAFF to the Code of Conduct and the rules set out in the compliance guideline. He is independent in his role and reports directly to the Spokesman of the Board of Management. Practical effects and changes over past practice have occurred, for example, in the acceptance of invitations and gifts.

DBAG acts as a responsible investor. Compliance aspects have therefore also been integrated into the TRANSACTION PROCESS, specifically in the due diligence process and in purchase agreements. An examination of compliance issues is required as an integral part of every due diligence process to ensure that potential portfolio companies also fulfil DBAG’s values. The basis for this is a questionnaire which, depending on the situation, can be integrated into the due diligence process in collaboration with the legal consultant for the transaction or with the assistance of a specialised compliance adviser, who may be commissioned additionally, if required. To minimise the liability risk for DBAG in connection with compliance issues, warranty clauses to that effect will be included in every purchase agreement for a portfolio company.

DBAG employees who hold offices on a supervisory board or in an advisory council at a PORTFOLIO COMPANY or act on behalf of a shareowner of a portfolio company are required to firmly endorse the introduction or ongoing development of a compliance system within the portfolio company. The “DBAG Compliance Standard for Portfolio Companies” serves as guidance.

CO M P O S I T I O N O F T H E SU P E RV I S O RY BOA R D: O P ER A B I L I T Y I S K E Y O B J EC T I V E

The German Corporate Governance Code recommends that the Supervisory Board specify concrete objectives regarding its composition and report on these and on their implementation.

The key objective is the Supervisory Board’s operability; this objective is best addressed when the majority of its members are independent and not exposed to conflicts of interest and when its members are experienced in the multifaceted operations of DBAG and have expert knowledge of applicable accounting principles. The Supervisory Board is also of the opinion that the majority – or four – of its members should be independent, and the Chairman of the Supervisory Board should be one of them.

The current composition of the Supervisory Board reflects this objective. A further objective of more appropriately considering women in the Supervisory Board’s composition has not yet been reached. Achieving that objective will be the duty of the Nominations Committee when preparing for the next elections to the Supervisory Board. The Supervisory Board will stand for reelection at the 2016 Annual Meeting.

A N N U A L R E P O R T 2 0 1 3 / 1 4 1 1

The members of the Supervisory Board do not have business or personal relationships to the Company or its boards, or to a controlling shareholder or a company with which that shareholder is affiliated, which could constitute a significant and not merely temporary conflict of interest. Should, contrary to expectations, conflicts of interest arise in individual instances, these are disclosed and dealt with appropriately by the Supervisory Board. The members of the Supervisory Board bring with them a wide spectrum of professional and personal experience, including management responsibility abroad or in international companies in Germany. The age limit of 70 means that the Company can benefit as much as possible from these skills on the one hand; on the other hand, it is conducive to introducing changes in the Board’s composition.

I N D EP EN D EN C E O F CO R P O R AT E BO D I ES : N O CO N FL I C T S O F I N T ER ES T

Conflicts of interest on the part of members of the Board of Management and the Supervisory Board requiring immediate disclosure to the Supervisory Board did not come to our attention.

P R I N C I P L E O F EQ UA L T R E AT M EN T: T I M ELY I N F O R M AT I O N TO A L L I N T ER ES T ED PA R T I ES

The principle of simultaneously directing information to all interested parties ranks high in our communication policy. All major reports, announcements and presentations are accessible on the Internet synchronously with the respective event. The key presentations we prepare for meetings with investors are also available on our website. Any interested individual can take note of the dates and locations of roadshows and investors’ conferences that we attend.

Our complete Annual Meeting is webcast live on the Internet. Shareholders may elect to exercise their voting rights personally or through a proxy of their choice or through a proxy appointed by the Company who is bound by their directives. Postal voting is also possible. All documents and information on the Annual Meeting are accessible in German and in English on our website.

R EM U N E R AT I O N O F T H E BOA R D O F M A N AG EM EN T: L I N K E D TO CO R P O R AT E P ER F O R M A N C E

The remuneration paid to the Board of Management is composed of fixed and performancerelated components, most of which have a longterm incentive. We issue an individualised statement of emoluments paid to the members of the Board of Management. Shareholders at the 2011 Annual Meeting approved the remuneration scheme with a vote of approximately 92 percent.

Since the beginning of financial year 2013/14, the remuneration paid to Supervisory Board members is solely composed of a fixed fee.

Details on the remuneration for the members of the Board of Management and the Supervisory Board page 101

1 2 C O R P O R AT E G O V E R N A N C E

S T R I C T RU L ES O N S H A R E OW N ER S H I P

Apart from participating in the employee stock ownership plan once a year (see page 91), members of the staff and the corporate bodies may only purchase shares in Deutsche Beteiligungs AG within a limited frame. Shares may only be purchased and sold during specified periods of time. These periods largely begin subsequent to publication of the Annual Report and interim reports and to the Annual Meeting. They are announced on the website of Deutsche Beteiligungs AG.

Based on the nature of the business operations of Deutsche Beteiligungs AG, there are further rules that apply to trading in securities for DBAG staff. Irrespective of the trading restrictions for shares in Deutsche Beteiligungs AG, it is not permitted for members of the staff – or for members of the corporate bodies – to deal in shares of portfolio companies of Deutsche Beteiligungs AG, or of companies undergoing the due diligence process or whose portfolio contains companies in which Deutsche Beteiligungs AG is considering an investment.

R E P O R TA B L E S EC U R I T I ES T R A N S AC T I O N S (“D I R EC TO R S’ D E A L I N G S”)

The members of the Board of Management and the Supervisory Board of DBAG as well as related parties are required to report transactions in DBAG shares (§ 15a WpHG (German Securities Trading Act)).

Reporting individualCorporate body

Date of transaction Transaction

Number of shares

Price €

Susanne Zeidler Board of Management 29 Sept. 2014 Purchase 1,000 21.50

The members of the Board of Management held a total of 32,613 nopar value shares as at 31 October 2014, or less than one percent of the subscribed capital of Deutsche Beteiligungs AG.

The members of the Supervisory Board held a total of 33,000 nopar value shares as at 31 October 2014, or less than one percent of the subscribed capital of Deutsche Beteiligungs AG.

D EC L A R AT I O N O F CO N F O R M I T Y P U R SUA N T TO S EC T I O N 161 O F T H E G E R M A N S TO C K CO R P O R AT I O N AC T ( A K T I EN G ES E T Z – A K TG)

The Board of Management and the Supervisory Board declare that, since issuance of the last Declaration of Conformity, Deutsche Beteiligungs AG has complied with the recommendations of the “German Corporate Governance Code” as amended on 13 May 2013 in their entirety and will continue to do so. We have also followed all of the suggestions in the Code and will also follow them in the future.

Frankfurt/Main, November 2014

Deutsche Beteiligungs AG The Board of Management Supervisory Board

A N N U A L R E P O R T 2 0 1 3 / 1 4 1 3

SH A R ES

C A P I TA L M A R K E T CO M M U N I C AT I O N

We foster an open ongoing dialogue with private and institutional investors and with financial analysts. In the past financial year, we met with numerous institutional investors in Germany and other major European financial centres. We also presented DBAG to private investors at two events. In addition, we make use of the customary electronic communication channels.

A key objective of our investor relations communication is to achieve a fair valuation of our shares. Our efforts to promote trading in DBAG shares also serve that purpose, since the pricesetting process is more efficient for liquid stocks. Frequently, the difference between the share price and net asset value per share is used when assessing private equity companies. A gain in net asset value per share is considered an indicator of the value growth that companies create for their shareholders with their own portfolio. Dividends are also considered, since distribution policies can vary greatly from company to company. One of the particular strengths of our business model, moreover, is that we additionally earn substantial fee income from management and advisory services to funds. Our efforts are focused on having this unique aspect of our business model adequately taken into account when DBAG shares are assessed.

SH A R E P ER F O R M A N CE A N D A N A LYS T S’ R ECO M M EN DAT I O N S

N E T A S S E T VA LU E P ER S H A R E: G A I N O F 15 . 8 P E RC EN T I N F I N A N C I A L Y E A R

In financial year 2013/14, we again successfully created value for our shareholders: net asset value per share increased from 19.16 euros (after a dividend payment of 1.20 euros per share) at the beginning of the financial year to 22.18 euros, a gain of 3.02 euros or 15.8 percent.

Maintaining close relations with our shareholders and investors remains a priority. For information on our current investor relations activities, www.deutsche-beteiligung.de/investor-relations/

1 4 S H A R E S

1 Net asset value per share at a (quarterly) reporting date relative to the value at the preceding (quarterly) reporting date. In the event that a dividend was paid in a quarter, that amount is added to the net asset value per share at the reporting date.

Very satisfactory returns have also been delivered to shareholders over more extended periods of time: on 1 November 2004, net asset value per share was 12.54 euros. The base and surplus dividends that have been paid since then total 13.49 euros per share. Adding these dividend payments to the net asset value of 22.18 euros per share at the current reporting date results in an increase of 23.13 euros or about 235 percent on the initial amount ten years ago.1 This corresponds to an average annual return of 12.9 percent.

DBAG shares, including reinvested dividends

DBAG net asset value per share, including dividends (“total return”)

Dax, indexed

LPX Direct TR, indexed

SDax, indexed

SHARE PERFORMANCE AND NET ASSET VALUE PER SHARE

(1 November 2004 – 31 October 2014, total return, indexed to 1 November 2004 = 100)

500

450

400

350

300

250

200

150

100

50

01 Nov. 2004 1 Nov. 2006 1 Nov. 2008 1 Nov. 2010 1 Nov. 2012 1 Nov. 2014

The significant rise in net asset value per share this past financial year contributed towards the positive price movement of DBAG shares. In financial year 2013/14, they largely traded within a narrow band around the net asset value per share. Initially trading at a discount to NAV of up to five percent at the beginning of the financial year, they were quoted at a premium of, at times, up to twelve percent following the announcement of the preliminary results for 2012/13 and the dividend recommendation. As in previous years, after the dividend payment the share price fell to below net asset value per share. Towards the end of the financial year, prices again closely reflected net asset value. This distinguishes DBAG from other private equity firms: the stocks of 16 of the 23 listed private equity companies in Europe that also hold direct investments trade at discounts of more than ten percent, another three at discounts of between five and ten percent.

A N N U A L R E P O R T 2 0 1 3 / 1 4 1 5

DIFFERENCE BETWEEN SHARE PRICE AND NET ASSET VALUE PER SHARE

(1 November 2013 to 31 October 2014; %)

15

10

5

0

(5)

(10)1 Nov. 2013 1 Feb. 2014 1 March 2014 1 Aug. 2014 1 Nov. 2014

R ES E A RC H : H O L D R ECO M M EN DAT I O N S C U R R EN T LY P R ED O M I N AT E

Analysts frequently also consider the difference between the current share price and the net asset value per share in their opinions. In view of the market’s continued very favourable – from analysts’ perspective – assessment of our shares on a sector comparison, hold recommendations currently predominate. As previously mentioned, we want to call more attention to the role that fee income for investment services to funds plays for the performance generated by DBAG.

Analysts’ recommendations are regularly documented on our website in the section “Investor Relations/Research” as soon as they come to our attention. The table below presents analysts’ ratings at the beginning of financial year 2014/15. DBAG shares are also tracked by other analysts who exclusively assess listed private equity firms and comparable companies.

ANALYSTS’ RATINGS FOR DEUTSCHE BETEIL IGUNGS AG

ODDO SEYDLER BANK November 2014 “Hold”

Edison Investment Research September 2014 –

HSBC Trinkaus July 2014 “Neutral”

J.P. Morgan Cazenove September 2014 “Underweight”

Landesbank BadenWürttemberg December 2014 “Hold”

Solventis Wertpapierhandelsbank March 2014 “Buy”

Warburg Research (M.M.Warburg) November 2014 “Hold”

1 6 S H A R E S

On 31 October 2014, LPX Direct consisted of 30 constituents with a market capitalisation of 46.9 billion euros. DBAG shares are the only German component in the index, with a weighting of 0.64 percent.

SH A R E P R I CE M OV EM EN T A N D L I Q U I D I T Y

S H A R E P R I C E C L E A R LY O U T P E R F O R M ED BEN C H M A R K I N D I C ES

In financial year 2013/14, DBAG shares clearly outpaced key benchmark indices. Driven by a strong trend at the beginning of the financial year, they reached their peak price of 22.82 euros in Xetra trading in January 2014 and then largely moved sideways. Following the Annual Meeting, the share price declined, as has often been the case with our shares. The year’s low of 18.50 euros was reached in midApril, from which the shares quickly rebounded. After that, DBAG shares benefitted from the announced Homag realisation and fluctuated only within a narrow range of between 21 euros and 22 euros in a highly volatile market. At the end of the financial year, DBAG shares closed at 21.83 euros in Xetra trading.

DBAG

Dax

SDax

LPX Direct

PERFORMANCE OF DBAG PORTFOLIO OVER

ONE, F IVE AND TEN YEARS

(Initial investment of 10,000 euros on 1 November of the years 2013, 2009 and 2004; €)

1 year

5 years

10 years

44,984

17,484

22,597

23,244

11,952

18,964

21,246

19,606

17,174

10,852

9,998

10,324

A N N U A L R E P O R T 2 0 1 3 / 1 4 1 7

In March 2014, a dividend of 0.40 euros per share and a surplus dividend of 0.80 euros per share were paid for financial year 2012/13, a total of 16.4 million euros. This corresponds to a dividend yield of 6.6 percent based on the net asset value per share at the outset of the financial year (less the dividend paid for the previous year), or 6.2 percent measured by the opening share price at the beginning of the year. The share price movement and dividend payment result in a total return of 19.5 percent for DBAG shareholders this financial year. DBAG shares thus outperformed major benchmark indices. Over this period, the Dax merely gained 3.2 percent, the SDax, in net terms, remained unchanged and the LPX Direct, an index of other private equity stocks, grew by 8.5 percent. Over longer periods of time, an investment in DBAG shares has also – in part significantly – outperformed investments in the LPX Direct, or the Dax and SDax.

S H A R E L I Q U I D I T Y: T R A D I N G VO LU M E AT H I G H ES T L E V EL I N F I V E Y E A R S

One particularly gratifying aspect is that the price movement of DBAG shares was accompanied by significantly improved share liquidity. At 7.2 million shares, compared with 6.1 million shares in the previous year, trading volume on German stock exchanges reached its highest level since the financial market crisis in 2008. This is all the more noteworthy since overthecounter trading clearly gained in importance during the same period. The Bloomberg Information System identified another 2.4 million DBAG shares traded directly between buyers and sellers in financial year 2013/14. That means that almost one quarter of trading in DBAG shares took place over the counter. Five years ago, this platform was hardly ever used, whereas in 2012/13, OTC transactions accounted for almost 29 percent.

Apart from the turnover peak that is frequently observed in March, the month in which the Annual Meeting is held, monthly turnovers in DBAG shares were balanced more equally in 2013/14 than in the preceding year. Consistent marketability is an important feature for many institutional investors in assessing the quality of stocks. An average of 28,741 shares (previous year: 24,155) were traded daily on German stock exchanges. Some 72 percent of the turnover (previous year: 76 percent) was Xetratraded. Relative to the freefloat market capitalisation, shares in float ownership had a turnover rate of 1.00 (2012/13: 0.90).2

2 Stock exchange turnover and OTC turnover, calculated with a freefloat proportion of 70.0 percent

1 8 S H A R E S

Overview of dividend policy – management report: objectives and strategy, page 61

R ECO M M EN D E D A P P RO P R I AT I O N O F P RO F I T D I V I D EN D P O L I C Y U N C H A N G ED: SU R P LU S D I V I D EN D F O L LOW I N G SU CC ES S FU L H O M AG R E A L I S AT I O N

One of our major financial objectives is to have the shareholders of Deutsche Beteiligungs AG participate in the Company’s performance through regular dividends. In pursuit of that objective, our dividend policy has remained unchanged for many years. It consists of two components: a base dividend and a surplus distribution which is disbursed in instances of particularly high realisation proceeds and sufficient liquidity. That policy will again be maintained for financial year 2013/14.

In accordance with the legal framework in Germany, the separate financial statements of Deutsche Beteiligungs AG drawn up in conformity with the German Commercial Code (Handelsgesetzbuch – HGB) are decisive in determining DBAG’s ability to pay dividends. The HGBformatted annual profit is largely based on realised disposals. Apart from permanent value impairment, unrealised valuation movements are not considered in HGB accounting.

Following the profitable realisation of the investment in Homag, the base dividend is to remain unchanged at 0.40 euros per share. In addition, a surplus dividend of 1.60 euros is to be distributed to shareholders. In total, the Board of Management and the Supervisory Board will therefore recommend paying a dividend of 2.00 euros per share, or 27.4 million euros, to shareholders at the Annual Meeting. This equates to a dividend yield relative to net asset value per share at the outset of the financial year (less dividends paid for the previous year) of 10.4 percent. The average dividend yield for the past ten financial years – the period for which the present dividend policy has been in effect – is 9.3 percent.

A N N U A L R E P O R T 2 0 1 3 / 1 4 1 9

SH A R EH O L D ER P RO F I L E

Since the conversion to registered shares on 1 July 2013, we have more precise information available on the structure of our shareholder base. That puts us in a position to communicate with our shareholders specifically and directly. We want to expand on this in the future, in particular by using electronic means. At 20 October 2014, more than 11,400 private shareholders were invested in Deutsche Beteiligungs AG, holding approximately 42.9 percent of the shares at that date. Approximately one quarter of DBAG shares were held by institutional investors. Since most institutional investors – both German and international – are not listed directly in share registers, but through nominee shareholders (banks, brokerages), we obtain further information on our shareholder profile through disclosures several times each year. According to the voting rights notifications we have received, 69.96 percent of DBAG shares are in freefloat ownership, as defined by Deutsche Börse.

Private shareholders Germany

Private shareholders international

Rossmann Beteiligungs GmbH

Anpora Patrimonio

Institutional investors Germany

Institutional investors Europe

Institutional investors USA

Other

SHAREHOLDER PROFILE AS AT 31 OCTOBER 2014

%

2.5

4.3

41.0

12.0

8.3

5.0

25.0 1.9

2 0 S H A R E S

SHARE PROFILE

WKN/ISIN A1TNUT/DE000A1TNUT7

Symbol DBAGn (Reuters)/DBAN (Bloomberg)

Listings Frankfurt (Xetra and trading floor), BerlinBremen, Dusseldorf, Hamburg, Hanover, Munich, Stuttgart

Market segment Prime Standard

Index affiliation (selection)

SDax (rank 40 1); Classic All Share; CDax; Prime All Share; Deutsche Börse sector indices: DAXsector All Financial Services, DAXsubsector Private Equity & Venture Capital, LPX Direct, LPX Europe, LPX50; Stoxx Private Equity 20

Designated sponsors ODDO SEYDLER BANK AG, M.M.Warburg & CO (AG & Co.) KGaA

Share capital 48,533,334.20 euros

Number of shares issued 13,676,359

thereof outstanding 13,676,359

First traded 19 December 1985

1 At 31 October 2014, measured by market capitalisation (liquidity measure ranking: 38)

SHARE DATA

2013/14 2012/13 2011/12

Closing rate 1 € 21.83 19.36 19.49

Financial year high 1 € 22.82 21.93 20.21

Financial year low 1 € 18.50 17.27 14.01

Financial year average rate 1 € 21.05 19.25 16.57

Annual performance 2 % 19.5 7.6 33.3

Market capitalisation 1,3 €mn 298.6 264.8 266.5

thereof in free float 4 €mn 208.9 180.6 186.3

Average daily trading value 5 €mn 0.608 0.476 0.242

Dividend per share 6 € 0.40 0.40 0.40

Surplus dividend per share 6 € 1.60 0.80 0.80

Distribution sum 6 €mn 27.4 16.4 16.4

Dividend yield 7 % 10.4 6.6 7.2

Earnings per share € 3.49 2.36 3.25

NAV per share 3 € 22.18 20.36 19.46

Price/NAV per share 3 0.98 0.95 1.00

1 Xetra closing rate2 Adjusted for dividends 3 At end of period4 As defined by Deutsche Börse AG5 According to Deutsche Börse AG data 6 2013/14 recommended7 Relative to NAV per share at start of financial year (less dividend paid for previous year)

www.dirk.org

www.lpeq.com

DBAG is a member of:

www.dai.de

A N N U A L R E P O R T 2 0 1 3 / 1 4 2 1

2 2 O U R P O R T F O L I O

O U RP O R T F O L I O

A N N U A L R E P O R T 2 0 1 3 / 1 4 2 3

VA L UAT I O N

7.3T I M E S E B I T D A

Our portfolio companies’ valuation is based on 7.3 times their earnings on average, or to be more precise, 7.3 times their expected EBITDA for 2014 (or their financial year ending in 2014). Two companies were not valuated with the multiples method due to their strong growth. The remaining 13 companies were included in the calculation for the average figure weighted by their share of the portfolio value.

D E B T

2.4T I M E S E B I T D A

Our portfolio companies have debts amounting to less than 2.4 times their EBITDA on average. Two companies with no net liabilities were not considered in the calculation. The remaining 13 companies were included in the calculation for the average figure weighted by their share of the portfolio value. The calculation is based on the companies’ expected EBITDA and their net debt for 2014 (or their financial year ending in 2014).

R E V E N U E S

9.3P E R C E N T G R O W T H

The 14 companies that were part of our portfolio throughout the financial year increased their revenues by 9.3 percent. This was calculated by comparing the companies’ expected revenues for 2014 (or their financial year ending in 2014) with revenues generated in 2013. The respective growth rate was weighted by the company’s share in the value of our portfolio. This increase is predominantly due to organic growth.

E A R N I N G S

12.1P E R C E N T G R O W T H

The companies in the portfolio improved their earnings by 12.1 percent on average within one year. The indicator used is EBITDA (earnings before interest, tax, depreciation and amortisation) on tangible and intangible fixed assets. This was calculated by comparing the companies’ expected EBITDA for 2014 (or their financial year ending in 2014) with their EBITDA in 2013. The 14 companies that were in our portfolio throughout the financial year were included in the (weighted) calculation.

OU

R P

OR

TF

OL

IO

2 4 O U R P O R T F O L I O

DBAG offers the capital market shares that grant interest in a portfolio with currently 15 investments. We provide tailored equity solutions for the managers and partners of our portfolio companies. They can count on us in two ways: on the one hand, we give them scope to implement their business ideas and concepts that create value in the long term; on the other, thanks to our industry expertise and experience, we are sought after as a partner for supporting growth strategies and change processes. Just as the motto of this Annual Report says: Driving expansion. Ensuring continuity.

But what exactly does that mean? Why not take a look at our portfolio. For example, Broetje-Automation: the manufacturer of machinery and plants for aircraft assembly has boosted its expansion by acquiring two companies (see page 26). Stephan Machinery is using additional equity to expand its range of machines for the food industry and establishing an international service and distribution network (see page 38). Finally “Unser Heimatbäcker“: the company that we added to our portfolio in the 2013/14 financial year is continuing its course with DBAG as a partner to consolidate its market and expand its position (see page 39).

»

O U R P O R T F O L I O

CO M PA N I E S A R E G R O W I N G

A N D B ECO M I N G

M O R E P R O F I TA B L E .

«

In the past financial year, our portfolio companies have developed well overall, as their average increase in revenues and earnings in 2014 shows. Our portfolio investments are growing and becoming more profitable. They are improving their strategic position in the market to secure existing jobs and create new ones. Their average growth in revenues and earnings far exceeds general economic trends. That shows what great potential the companies that our investment team has identified and reviewed. The 23 members of this team together combine more than 200 years of experience from investments in mid-sized German companies. We will use this experience to continue supporting our portfolio companies.

O U R P O R T F O L I O

Stephan Machinery is one of the companies in the portfolio that make

classical industrial goods and sell them worldwide.

The bakery chain operates regionally: "Unser Heimatbäcker" is the market leader

in northeast Germany with more than 500 outlets.

15active

investments

A N N U A L R E P O R T 2 0 1 3 / 1 4 2 5

Company Revenues 2014 ¤mn Employees Core business

Broetje-Automation GmbH, Wiefelstede (Germany)

89(FY 2013/141) 550

Developer and manufacturer of machines and plants used to automate the assembly of aircraft for customers worldwide

Clyde Bergemann Group, Wesel (Germany) / Glasgow (UK) / Delaware (USA)

545(US$, FY 2013/14) 1,800

Developer and manufacturer of components for power plants on three continents as well as global service business

DNS:NET Internet Service GmbH, Berlin (Germany) 101 30

Telecommunications and IT services based on high-quality fibre-optic infrastructure in Berlin and Brandenburg

FDG S.A.,Orly (France) 1111 760

Services for supermarkets in France and other neighbouring countries

Formel D GmbH, Troisdorf (Germany) 1571 4,500 Services for car manufacturers and their suppliers worldwide

Grohmann GmbH, Prüm (Germany) 951 790

Developer and manufacturer of plants for industrial automation worldwide

Heytex Bramsche GmbH, Bramsche (Germany) 751 305

Manufacturer of textile print media and technical textiles for customers worldwide

Inexio KGaA, Saarlouis (Germany)

34(FY 2013/141) 170

Telecommunications and IT services based on high-quality optic-fibre infrastructure in Southwest Germany

JCK KG, Quakenbrück (Germany) 5751 1,050 Textile retail business, mainly for discounters in Germany

Plant Systems & Services PSS GmbH, Bochum (Germany) 281 190

Industrial services for the energy and process industries in Germany and neighbouring countries

Romaco GmbH, Karlsruhe (Germany)

113(FY 2013/141) 450