CONTENTITUOUS ISSUES UNDER EXCISE & SERVICE TAX. BY P.K.MITTAL B. Com, LLB, FCS ADVOCATE DELHI HIGH...

39

CONTENTITUOUS ISSUES UNDER EXCISE & SERVICE TAX. BY P.K.MITTAL B. Com, LLB, FCS ADVOCATE DELHI HIGH COURT CENTRAL COUNCIL MEMBER – THE INSTITUTE OF COMPANY SECRETARIES OF INDIA. CHIEF ADVISOR : PKMG LAW CHAMBERS Mobile 9811044365,9911044365 011-22540549,

Transcript of CONTENTITUOUS ISSUES UNDER EXCISE & SERVICE TAX. BY P.K.MITTAL B. Com, LLB, FCS ADVOCATE DELHI HIGH...

CONTENTITUOUS ISSUES UNDER EXCISE & SERVICE TAX.

BY P.K.MITTALB. Com, LLB, FCS ADVOCATEDELHI HIGH COURT

CENTRAL COUNCIL MEMBER – THE INSTITUTE OF COMPANY SECRETARIES OF INDIA.

CHIEF ADVISOR : PKMG LAW CHAMBERS

Mobile 9811044365,9911044365 011-22540549,

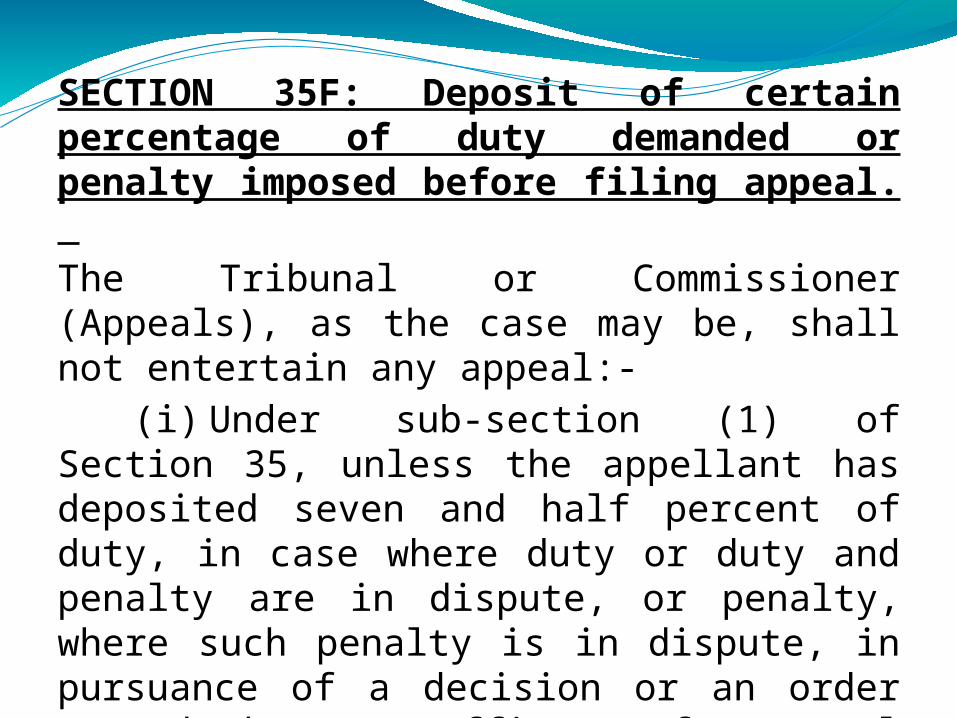

SECTION 35F: Deposit of certain percentage of duty demanded or penalty imposed before filing appeal. The Tribunal or Commissioner (Appeals), as the case may be, shall not entertain any appeal:-

(i) Under sub-section (1) of Section 35, unless the appellant has deposited seven and half percent of duty, in case where duty or duty and penalty are in dispute, or penalty, where such penalty is in dispute, in pursuance of a decision or an order passed by an officer of Central Excise lower in rank than the Commissioner of Central Excise.

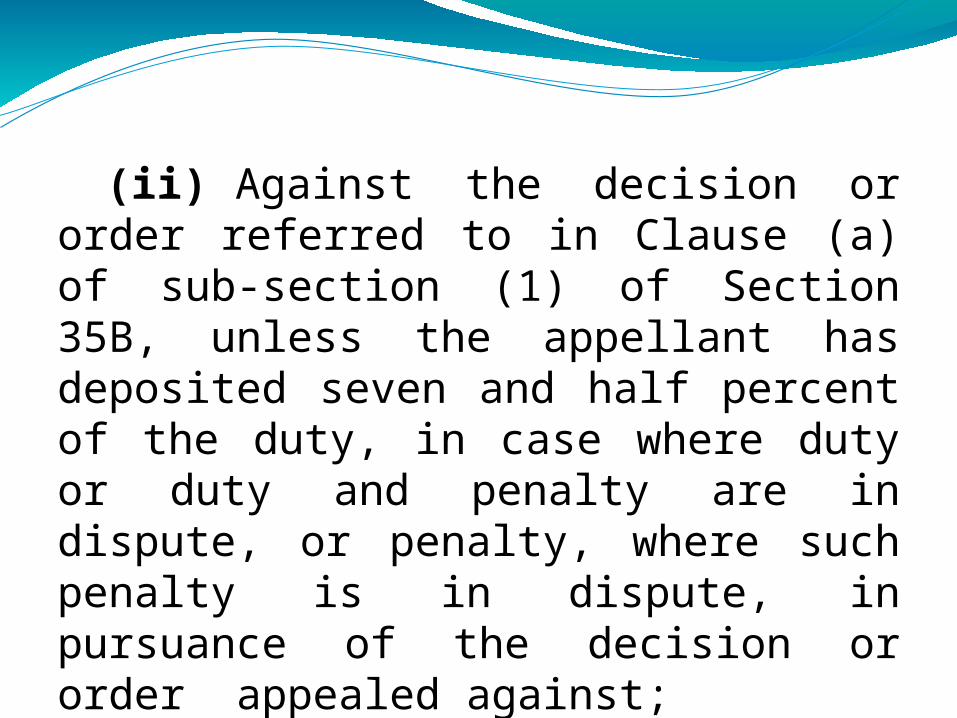

(ii) Against the decision or order referred to in Clause (a) of sub-section (1) of Section 35B, unless the appellant has deposited seven and half percent of the duty, in case where duty or duty and penalty are in dispute, or penalty, where such penalty is in dispute, in pursuance of the decision or order appealed against;

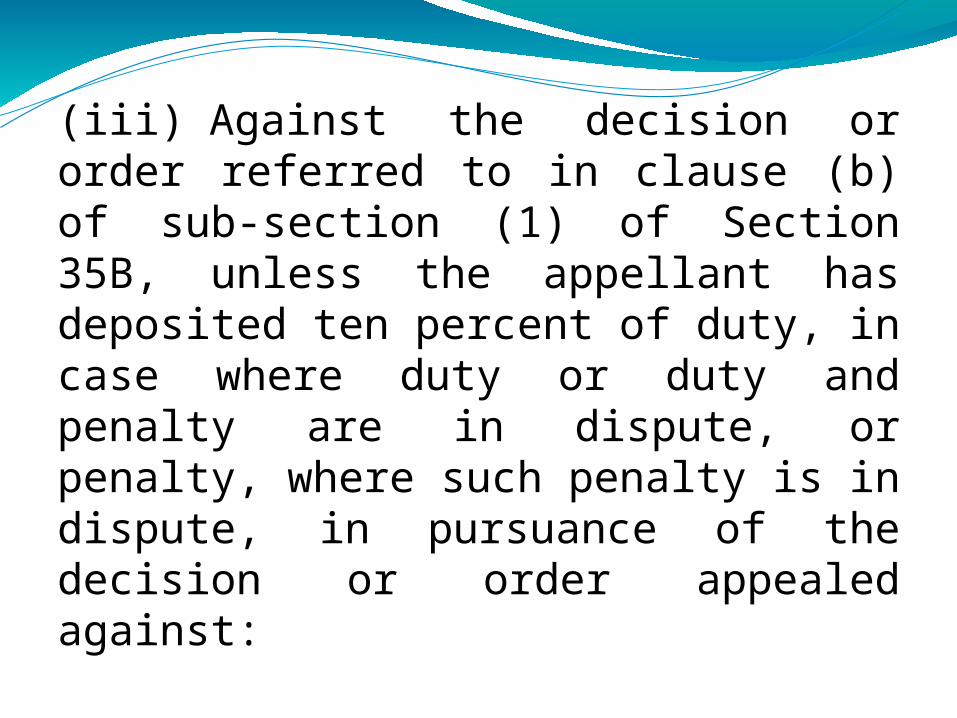

(iii) Against the decision or order referred to in clause (b) of sub-section (1) of Section 35B, unless the appellant has deposited ten percent of duty, in case where duty or duty and penalty are in dispute, or penalty, where such penalty is in dispute, in pursuance of the decision or order appealed against:

Provided that the amount required to be deposited under this section shall not exceed rupees ten crores;

Provided further that the provisions of this section shall not apply to the stay application and appeals pending before any appellate authority prior to the commencement of the Finance Act, 2014.

The Appellant shall have to comply with the mandatory deposit of 7.5% or 10%, as the case may be, by either deposit in cash or can reverse the credit by debit to Cenvat Credit Account, a proof of such cash deposit/reversal in the Cenvat Credit account along with a separate letter shall be required to be filed at the time of filing of an appeal either before (i) Commissioner (Appeal) or Tribunal. Upon such deposit having been made, there shall be automatic stay and there shall be no requirement of making a separate application for seeking stay either before the Commissioner (Appeals) or before Tribunal, as was the case previously. The automatic stay shall continue till the decision of the appeal. This would apply to the appeals filed after 06.08.2014.

However, stays granted prior to 06.08.2014 either by the Commissioner (Appeals) or by the Tribunal shall continue till the decision of the Appeal The Department would be very soon issuing circular to this effect.

The stay petition may be required in the following cases:

(i) Stay of operation of Order, may be required, even when there is no revenue involved, legal rights are involved like in cases of suspension, prohibition, revocation of licenses of CHAs or Department may require stay of operation of an order of Commissioner (Appeal) or Tribunal.

ii) Cases where, mere procedural contraventions have taken place like in cases of CENVAT credit being disallowed on grounds of some or other particulars found, missing. In this context it is important to note that for departmental authorities every procedure is sacrosanct and justice in such cases of procedural lapses, where transaction in substance is correct, is only done at the level of Tribunal and above. If the demands are made in such cases, the burden of getting the matter heard through mandatory deposit can be quite crushing for the assessee.

(iii) Department has to, as per instructions, issue protective demands, even when it does not agree with the Audit Paras made by the Officer of Comptroller and Auditor General (CAG). It takes years to decide such Audit Paras and burden on assessee can be exorbitant if it has to rush for filing an appeal with mandatory deposit in each case.

(iv) All the Departmental appeals against refund, normally seek Stay of operation of Order. However, if Stay is not even warranted at the Tribunal level all the refunds will be held in abeyance for years together, just on filing of Departmental appeal.

(v) In cases which are before BIFR making of stipulated mandatory deposit is also not feasible for a sick unit.

vi) It will be highly injudicious to expect an assessee who shell out 7.5% to 10% of the duty involved in cases with the Order-in-Original has been hurriedly passed by not providing Relied Upon Documents (RUDs) or Non-Relied upon Documents or by not affording cross-examination, etc. even when the same was warranted as per Section 9D. As per existing dispensation also, if the departmental officers err in this regard, the assessee is required to shell out market interest, even due to lack of competence of the adjudicating authority and now the assessee shall be additionally called upon to pay 7.5% to 10% just to get heard in the matter.

REGISTERED/HEAD OFFICE/CORPORATTE OFFICE AT “INPUT SERVICE DISTRIBUTOR:Rule 2 – Cenvat Credit Rules, 2004.

(l) “input service” means any service, -(i) used by a provider of (output service)

for providing an output service; or(ii) used by a manufacture, whether

directly or indirectly, in or in relation to the manufacture of final products and clearance of final products upto the place of removal,

and includes services used in relation to modernization, renovation or repairs of a factory, premises of provider of output service or an office relating to such factory or premises, advertisement or sales promotion, market research, storage upto the place of removal, procurement of inputs, accounting, auditing, financing, recruitment and quality control, coaching and training, computer networking, credit rating, share registry, security, business exhibition, legal services, inward transportation of inputs or capital goods and outward transportation upto the place of removal;

(m) “input service distributor” means an office of the manufacturer or producer of final products or provider of output service, which receives invoices issued under rule 4A of the Service Tax Rules, 1994 towards purchases of input services and issues invoice, bill or, as the case may be, challan for the purposes of distributing the credit of service tax paid on the said services to such manufacturer or producer or provider, as the case may be;

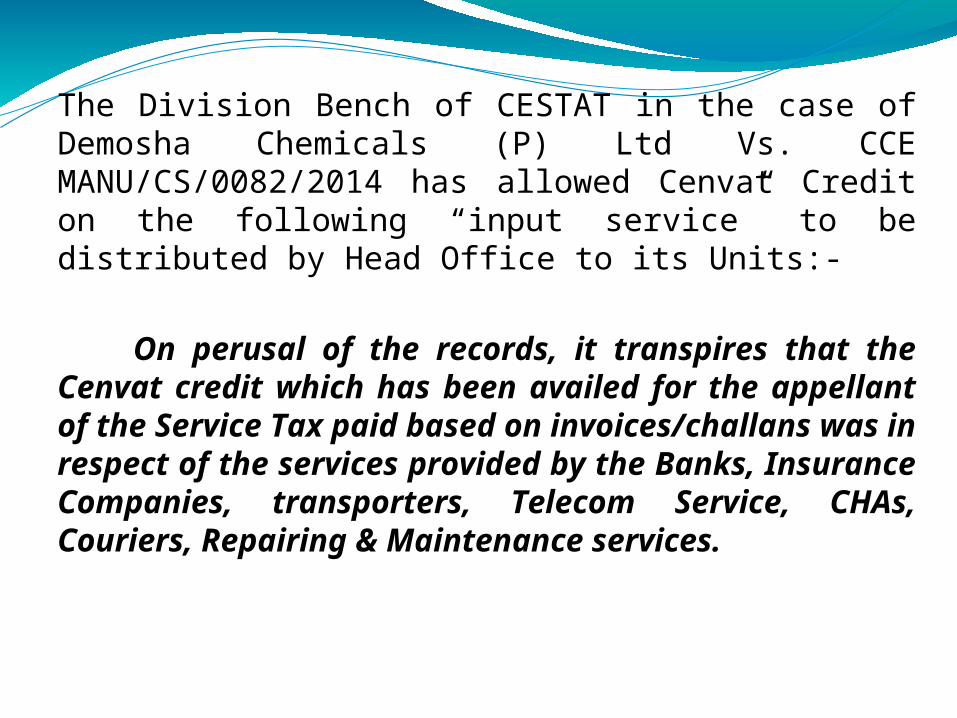

The Division Bench of CESTAT in the case of Demosha Chemicals (P) Ltd Vs. CCE MANU/CS/0082/2014 has allowed Cenvat Credit on the following “input service” to be distributed by Head Office to its Units:-

On perusal of the records, it transpires that the Cenvat credit which has been availed for the appellant of the Service Tax paid based on invoices/challans was in respect of the services provided by the Banks, Insurance Companies, transporters, Telecom Service, CHAs, Couriers, Repairing & Maintenance services.

The Division Bench of Karnataka High Court in the case of CCE Vs. ECOF Industries Ltd – MANU/KA/1106/2011 has observed as under:-

Merely because the input service tax is paid at a particular unit and the benefit is sought to be availed at another unit, the same is not prohibited under law. It is in this context, the manufacturer is expected to register himself as a input service distributor and thereafter, he is entitled to distribution of credit of such input in the manner prescribed under law. .

The Tribunal in the case of Greaves Cotton Ltd Vs. CCE MANU/CC/0072/2014 has held as under:-

FACTS OF THE CASE:The present appeals were filed by Unit-I. Five show cause notices were issued proposing to deny cenvat credit availed on input services on advertisement charges on the ground that Unit-I availed service tax credit on advertisement charges which was used in respect of the product manufactured by the other unit.

LAW POINT:

The inclusive part of definition of "input service" under Rule 2(l) of Cenvat Credit Rules, 2004, consists of advertisement or sales promotion...., activities relating to business". The Hon'ble Bombay High Court in the case of Manikgarh Cement (supra) as relied upon by the Ld. A.R., held that cenvat credit of input service is allowable only if nexus between relevant services and business of the assessee established. In the present case, it is apparent that input service credit on advertisement charges are related to the business of the assessee. Taking into account of the facts and circumstances of the present case, in so far as both the units are under the same manufacturer and the input service credit is related to the advertisement charges, "relating to business" of the same assessee, there is no reason to deny the input service credit to the appellants.

CENVAT CREDIT NOT ALLOWABLE IN CASE NON-REGISTRATION OF INPUT-SERVICE DISTRIBUTORS:

The CESTAT in the case of Market Creators Ltd Vs. CCE MANU/CS/0113/2014 has observed as under:-

In the case of present appellant, the service tax is not paid by the rented premises as Head Office for all the branches and no service tax registration is so taken by the appellant of such premises issuing credit taking document. In the facts and circumstances, appellant can not take credit of the document issued by a premises not registered as an Input Service Distributor under the service tax provisions.

The Division Bench of Tribunal, in a very interesting case, cited as Sunbell Alloys & Co Ltd Vs. CCE MANU/CM/030/2013 was pleased to observe:-FACTS OF THE CASE:The charge is that M/s. Merck Specialties Limited, Worli, who distributed the credit, did not have any manufacturing unit of their own and the appellants, M/s. Sunbell Alloys Co. of India Ltd. and M/s. Machsons Pvt. Ltd. are only job-workers who undertake repacking/re-labelling of goods imported/procured by M/s. Merck Specialties Ltd. As per the provisions of Rule 2(m) read with Rule 7 of CCR, 2004, the appellants being separate legal entities and not being a unit of Merck Specialties Ltd., were not entitled to such availment of Cenvat credit distributed by a different legal entity and therefore, the credit availed by them on the documents issued by Merck Specialties Ltd. was inadmissible.

LAW POINT:

Secondly, 'input service distributor' means an office of the manufacturer or producer of final products. The office of M/s. Merck cannot be considered as an office of the job-worker and, therefore, the definition of 'input service distributor' is not satisfied. Thirdly, Rule 7 deals with the manner of distribution, which specifically states that the input service distributor may distribute Cenvat credit of the service tax paid on the input service to its manufacturing units. The job-workers' factory is not the manufacturing unit of M/s. Merck Specialties Ltd. but they are independent legal entities by themselves and, therefore, the question of distribution of credit by M/s. Merck Specialties Ltd. to

the job-workers does not satisfy the condition that the credit is distributed to its manufacturing units. It is a settled position of law that job-workers who actually undertake the manufacturing process is the 'manufacturer' of goods and not the supplier of raw materials.

The Tribunal in the case of Punjab National Bank Vs. CCE MANU/CE/0691/2013 has observed:-

There is no dispute that the appellant are the Zonal Audit Head office of Punjab National Bank and though they are registered in respect of banking services since October 2004, they were actually responsible only for audit of the records of the Branches of PNB within their jurisdiction and it is the branches which were providing banking services and were individually registered for service tax payment. There is no dispute that the Appellant as Zonal Audit Office were not providing banking/financial services. The point of dispute is as to whether in this factual background, the appellant as Zonal Audit Office of PNB could take Cenvat credit on the basis of invoices issued in their name and distribute the same to the branches as input service distributor.

The Division Bench of CESTAT in the case of Thiru Arooran Sugars Ltd Vs. CCE MANU/CC/0131/2013 has observed:

FACTS OF THE CASE:

Rent-a-Cab Services, (ii) Telephone Services, and (iii) Contract Bus Services. The credit in question is taken by the corporate office at Chennai in their capacity as "input servicedistributor" as envisaged in Rule 2(m) of Cenvat Credit Rules, 2004 and passed on to their factory at Papanasam, Thanjavur for utilization for payment of excise duty.

LAW POINT:

The concept of "input service distributor" as defined in Rule 2(m) of the Cenvat Credit Rules, 2004 also implies allowing credit of services availed by an office which cannot utilize the credit as in the case of a corporate office. In the first place as per the definition, "input service" means service used by the manufacturer, whether directly or indirectly, in or in relation to the manufacture of final products. The Services would include "activities relating to business, such as accounting, auditing, financing, recruitment and quality control, coaching and training, computer networking, credit rating, share registry, and security, inward transportation of inputs or capital goods".

Here again the listing within this category cannot be taken to be exhaustive but only illustrative. The question arises whether (a) Rent-a-Cab (b) Telephone (c) Contract Bus Service will fall within the definition when received at the corporate office. In the matter of extending Cenvat credit in respect of above three services, no distinction can be made between the factory and Corporate Office where input services were received.

The Three Member Bench of CESTAT in the case of Telco Construction & Equipment Co Ltd Vs. CCE MANU/CB/0138/2013 has observed:- FACTS OF THE CASE: TCECL have their Corporate office at Bangalore registered with the Department as an 'Input Service Distributor' under Rule 4A of the Service Tax Rules, 1994, for distributing the credit of Service Tax paid and accounted at their Corporate office to its manufacturing units.. The show-cause notices had proposed to disallow Cenvat Credit on various taxable services such as 'air travel agents' service,

7/28/15

'management consultancy' service, 'goods transport agents' service, 'maintenance & repair service, 'car hiring' ('rent-a-cab') service, 'telephone and mobile' service, 'courier' service, 'recovery agent's' service, 'rail travel agent's' service, 'warranty handling' service, 'authorized service station' service, 'AMC of photocopier machines', 'club association' services, 'insurance' service, service tax paid on professional fees and packing expenses.

LAW POINTS:

By majority out of three member bench of the Tribunal, the adjudicating authority shall have to determine whether the said services involved activities integrally connected with the business of manufacture, of the assessee.

The above judgments is clearly contrary to the Division Bench Judgment of Hon’ble Bombay High Court in the case of Coca Cola India (P) Ltd Vs. CCE MANU/MH/0784/2009, wherein, it was observed:-

The expression Business is an integrated/continuous activity and is not confined restricted to mere manufacture of the product. Therefore, activities in relation to business can cover all the activities that are related to the functioning of a business. The term business therefore, in our opinion cannot be given a restricted definition to say that business of a manufacturer is to manufacture final products only

Credit is availed on the tax paid on the input service, which is advertisement and not on the contents of the advertisement. Thus it is not necessary that the contents of the advertisement must be that of the final product manufactured by the person advertising, as long as the manufacturer can demonstrate that the advertisement services availed have an effect of or impact on the manufacture of the final product and establish the relationship between the input service and the manufacture of the final product.

The Division Bench of Karnataka High Court in the case of CCE Vs. Stanzen Toyotetsu India (P) Ltd MANU/KA/0835/2011 has observed as under:-

The services mentioned in the Section are only illustrative and it is not exhaustive. Therefore when a particular service not mentioned in the definition clause is utilised by the Assessee/manufacturer and service tax paid on such service is claimed as CENVAT Credit, the question is what are the ingredients that are to be satisfied for availing such credit.

If the credit is availed by the manufacturer, then the said service should have been utilized by the manufacturer directly or indirectly in or in relation to the manufacture of final products or used in relation to activities relating to business. If any one of these two tests is satisfied, then such a service falls within the definition of "input service" and the manufacturer is eligible to avail CENVAT credit of the service tax paid on such service.

Hence, Cenvat Credit on (i) Canteen Services (ii) Rent-a-Cab/Transportation and (iii) Health Insurance/Insurance.

The Division Bench of Karnataka High Court in the case of CCE Vs. Millipore India (P) Ltd MANU/KA/2672/2011 has observed as under:-

It was observed that all elements of costs which are required to included as per CAS-4, the service tax paid on such elements, could be availed by the manufacturer. Therefore, it is clear that those factors have to be taken into consideration while fixing the costs of the final products. If services tax is paid in respect of any of those services which forms part of the costs of the final products certainly the assessee would be entitled to the cenvat credit of the tax so paid.

It is an inclusive and illustrative definition. Activities relating to business and any services rendered in connection therewith, would form part of the input services. The medical benefit extended to the employees, insurance policy to cover the risk of accidents to the vehicle as well as the person, certainly would be a part of the salary paid to the employees. Landscaping of factory or garden certainly would fall, within the concept of modernization, renovation, repair, etc., of the office premises.

The Division Bench of Bombay High Court in the case of CCE Vs. Ultratech Cements Ltd MANU/MH/1408/2010 has observed as under:-

We concur with the above decision of this Court in the case of Coco Cola India Pvt. Ltd. (supra). However, in that case, this Court has also held that the cost of any input service that forms part of value of final products would be eligible for CENVAT credit. Where the input service used is integrally connected with the business of manufacturing the final product and the cost of that input service forms part of the cost of the final product, then credit of service tax paid on such input service would be allowable.

THANK YOU