Breakout Microinsurance, Michael McCord, Microinsurance Centre

[email protected] www.e-mfp.eu

Microinsurance and MFIs

Craig Churchill Microinsurance Innovation Facility

International Labour Organization

[email protected] www.e-mfp.eu

Outline of the presentation

1. Should an MFI offer microinsurance?

2. If so, through what institutional structure?

3. If they partner with an insurance company,

how to manage that relationship effectively?

4. What products should the MFI offer?

5. Concluding thoughts

[email protected] www.e-mfp.eu

1. Should MFIs offer insurance?

Commercial Lower credit risk Enhance client retention Bolster product

profitability Diversify income streams Reach out to new markets

Social Help clients to reduce their

vulnerability Improve client welfare

For those that do, their primary motivations are:

[email protected] www.e-mfp.eu

Inefficient or expensive way of addressing the risk of client death

Requires a different skill sets from savings and credit

Do not want to be distracted from core competencies

Wise to separate credit and insurance risks

Possible reasons for not offering insurance:

1. Should MFIs offer insurance?

[email protected] www.e-mfp.eu

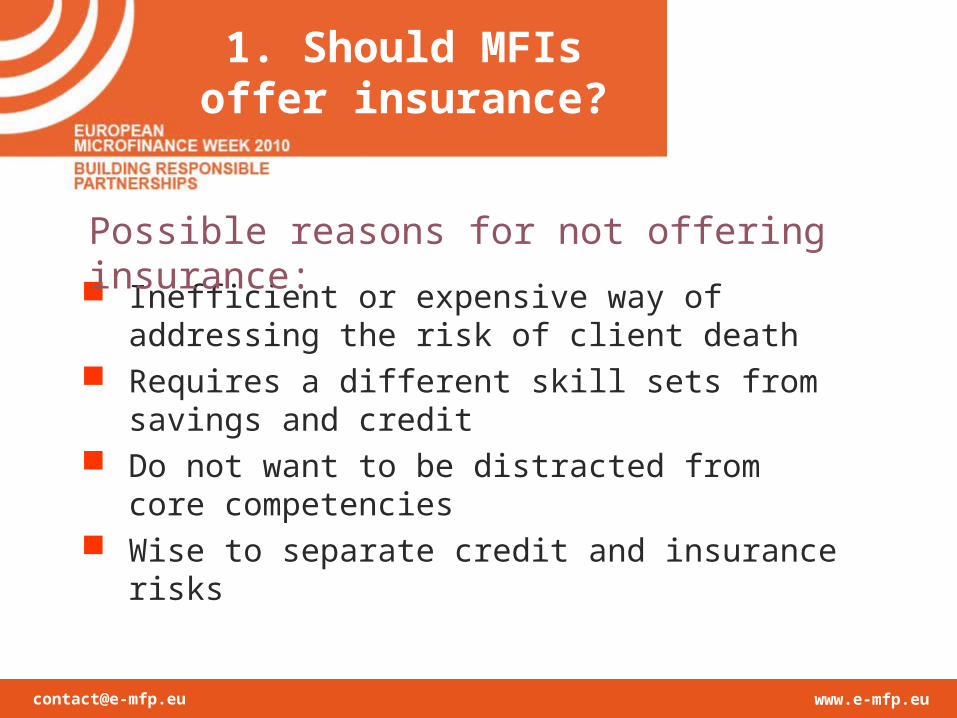

ReinsurerRisk CarrierPolicyholders(low-incomehouseholds)

DeliveryChannel

Administration platform

Broker

Microinsurance supply chain

2. Institutional options

[email protected] www.e-mfp.eu

1. Self-insurance

2. Partner-agent model

3. Microinsurance broker

4. Create an insurance company

2. Institutional options

[email protected] www.e-mfp.eu

1. Self-insurancea) only for basic products

b) if the MFI has > 10K clients

c) and technical assistance

d) and catastrophe cover for large losses

2. Partner-agent model

3. Microinsurance broker

4. Create an insurance company

2. Institutional options

[email protected] www.e-mfp.eu

3. Making the Partner-agent model work

1. Tell them what you want

2. Choose a trustworthy insurer

3. Involve the insurer in understanding customer needs

4. Manage claims*

5. Create a review committee

[email protected] www.e-mfp.eu

3. Making the Partner-agent model work

6. Eliminate exclusions

7. Maintain and analyse data

8. Determine the costs

9. Own the clients

10. Share the profits

[email protected] www.e-mfp.eu

4. Products

Credit life Perhaps the best opportunity to expose

large number of low-income people to insurance

It is a lost opportunity if they did not know that they were covered, or if they had a bad experience with the product

It needs to cover more than just the loan to increase the chances that policyholders will have a positive experience with it

[email protected] www.e-mfp.eu

Integrated vs. stand-alone products More efficient to “piggyback” insurance

transaction onto another transaction Link with credit limits value because

people do not always want to be in debt

Links with savings have high potential Does the MFI want to develop the

capacity to deliver stand-alone insurance products?

4. Products

[email protected] www.e-mfp.eu

Health Often the product for which there is the

greatest demand Illnesses can cause a significant problem

for the MFI’s loan portfolio If MFIs do offer health, perhaps focus on

more basic products like hospital cash Can MFIs offer health savings accounts for

small, frequent health expenses?

4. Products

[email protected] www.e-mfp.eu

Insurance for the MFI?• MFIs should consider their broader

insurance needs when negotiating with insurers

• If frontline employees have the same coverage, it will be easier for them sell it to clients

• Other coverage to consider: vehicles, property, fidelity, money storage and handling

4. Products

[email protected] www.e-mfp.eu

5. Concluding thoughts

MFIs need to: Reflect on their objectives Develop in-house expertise Actively manage their microinsurance

scheme, even in a P-A model, because their reputation is at risk

Consider how ensure that low-income households appreciate insurance and are willing to pay for additional benefits

Persuade front line staff that insurance provides value for clients and the MFI

[email protected] www.e-mfp.eu

Thank you!

Craig [email protected]

Tel +41 22 799 6242www.ilo.org/microinsurance

www.microinsurancenetwork.org

A member of the