Consumer Lending GSB · 8/7/2018 · Bankers Management, Inc. Public Records & Collection Items...

26

RETAIL BANKING “Consumer Lending” David Kemp President Bankers Management, Inc. McDonough, GA [email protected] 770-909-6004 August 7, 2018

Transcript of Consumer Lending GSB · 8/7/2018 · Bankers Management, Inc. Public Records & Collection Items...

RETAIL BANKING

“Consumer Lending”

David Kemp President

Bankers Management, Inc. McDonough, GA

[email protected] 770-909-6004

August 7, 2018

Graduate School of Banking2018

Presented By: David L. Kemp: BMI

1

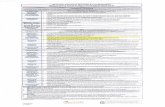

2016 2015 2014 2013 2012 2007

# Charters 6,111 6,238 6,570 6,874 7,149 7,787

Loan Growth 7.26% 7.02% 7.10% 4.15% 2.84% 9.76%

Past Due 1.68% 1.78% 2.23% 2.53% 3.14% 2.20%

Cost Staff $ 73,130 72,08069,99068,30066,76058,120

Eff Ratio 69.3% 70.4% 71.3% 72.2% 71.6% 68.9%

ROA 0.82% 0.80% 0.77% 0.73% 0.71% 0.80%

Source: BKD

2

Direct contact with large depositors◦ Have branch personnel contact CD holders prior to

maturity of deposits Pass on information about maturity procedures Discuss the availability of Wealth Management staff Ascertain if any additional funds exist Ask for referrals

3

Retail Loans◦ Have lending staff contact recently paid-off borrowers

to thank them for their handling of the loan: Inquire about any additional needs Inform about the collateral release process Inform about the array of different loan products Seek referrals (friends & associates)◦ Preapprove loans for current applicants Review current applicants use of additional loan products Contact current mortgage holders for HIP’s & HELOC’s,

for new opportunities

4

Bank sells are nationally at a very slow pace. This continues to be a buyers market:

Sellers are being driven by the following forces:◦ Tight margins◦ Weak loan demand◦ Loss of fee income◦ Higher compliance cost◦ Additional Capital requirements ◦ Change in generational ownership

Bankers Management, Inc.

5

Bankers Management, Inc.

Bank’s make loans to borrowers with the Demonstrated Willingness and Capacity to pay !!

Demonstrated◦ Track record (they have done it before)

Willingness◦ Credit History, have they paid other creditors?

Capacity $$$◦ DTI, Residual Income

6

Bankers Management, Inc.

What is the Consumer Loan Process?◦ Properly taking the Application◦ Investigating the application◦ Making the final decision

The Marginal Borrower◦ How do we make the close call ? The lender must apply their judgment to the facts &

policy

7

Bankers Management, Inc.

Common Sense of the Lender◦ Can you spot what does not fit ?◦ Does the loan fit the bank’s objectives ?

Loan Officer Responsibilities◦ Increased loan volume◦ Improved Risk Management Credit Files – Pre Approval Documents◦ Proper Loan Pricing

8

Bankers Management, Inc.

Can I read your credit file and understand the following?

The Purpose of the Loan◦ To assist in loan structuring◦ To review loan policy

The Basis of the Credit◦ Secured or Unsecured◦ Collateral Valuation, $, Source

9

Bankers Management, Inc.

Conformity to Credit Policy (FDICIA)◦ Written Credit Reasons for Exceptions◦ Exception Policy & Procedures

Identification of Risk◦ What are the Risk ? Why are they Acceptable ?

Completeness of Documents◦ Documentation Exception Reports◦ Responsible officer, Date of Exception

10

Bankers Management, Inc.

Credit Scores are statistical models that try to predict the likelihood of debt being repaid in the future.

They are based on data that is in the borrowers credit report

Not included :◦ Income◦ Assets◦ Collateral◦ Down Payment

11

Bankers Management, Inc.

Scoring Products◦ Beacon◦ FICO◦ Emprica

Scoring Range◦ 350 - 850

12

Bankers Management, Inc.

Credit Reports◦ Identifying Information DOB, Address, Name, Employment, SS#

◦ Trade Lines Date Opened, Payment Status, Credit Limit, Balance,

High Credit, Paid Accounts

◦ Inquiries 5 Inquiries @ 6 months – Hi Risk: *7 – Day Rule Any inquires within the same seven day calendar period

will be scored as one inquiry

13

Bankers Management, Inc.

Public Records & Collection Items◦ The Fair Debt Reporting Act Derogatory Credit must drop from the credit report

after seven years, except bankruptcy (10 years)

Bankruptcy, Liens, Collections, Judgments, Foreclosure

72 months – Low risk

14

Bankers Management, Inc.

Severity, Days past due 30 60 90 120

How Recent*◦ 0 -11 months : High Risk◦ 72 months: Low Risk *An account must be 30 days or more past due

Frequency ◦ % of accounts with late payments

15

Bankers Management, Inc.

Number of accounts recently opened◦ New Accounts: 2 Years or less: High Risk 10 Year rule; If the oldest opening date on any credit

account is 10 years or more: improves score

Average balance across all trade lines◦ % of accounts with 0 balance

Relationship between balance & limits◦ Revolving debt 20% < Low Risk 80% > High Risk

16

Bankers Management, Inc.

Bank Cards◦ Visa◦ MasterCard◦ Discover

Risk Matrix◦ 0 High Risk◦ 1 Lower Risk◦ 2 Lowest Risk◦ 3 Higher Risk◦ 4 Still Higher Risk◦ 7 Highest Risk

17

Bankers Management, Inc.

Travel & Entertainment Cards◦ Diners Club◦ American Express 0 Neutral 1 Low Risk 2 High Risk

Department Store & Gas Cards◦ More than one: High risk

18

Bankers Management, Inc.

Personal Finance Companies◦ High Risk

Installment Loans◦ 1 Open & 1> paid out: Low Risk◦ 2 or more open: High Risk

19

FICO has announced a change to its current consideration of Medical Collections:◦ Medical collections currently account for ½ of all

consumer collections◦ Paid medical collections will not be weighed at all◦ Unpaid medical collections will carry less weight

than before◦ Any amount under $100 will be ignored◦ Many scores will rise by more than 25 points

Bankers Management, Inc.

20

Bankers Management, Inc.

Credit scoring can not predict if an individual applicant will repay a loan.

If you make 100 loans with a 600 beacon score: 1:8 will default or go 60 days past due,◦ 12% (12 out of 100) will not pay◦ 88% (88 out of 100) will pay: You can’t tell WHO !

21

1. Does the borrower have the capacity to repay the loan ?

2. Has the borrower demonstrated the willingness to pay ?

3. What consideration should be given to Collateral ?

Bankers Management, Inc.

22

Bankers Management, Inc.

Is income sufficient to repay the loan ?◦ Debt to Income ratio◦ Residual Income

Is income dependable ?◦ Same line of work◦ Education related to work & high income potential

Is current debt level manageable ?◦ Limited credit user

Does the borrower demonstrate the ability to manage their debt?◦ Consolidation Loan

23

Bankers Management, Inc.

Credit history◦ Cut off Credit Score◦ Underwriting guidelines

Are you willing to be paid in the same manner that other creditors have been paid ?◦ Is a little slow OK ?

24

Bankers Management, Inc.

Has value been independently established ?◦ What is the source of the information?◦ Market value vs. Liquidation value

Is loan- to- value sufficient to pay out loan ?◦ Can the collateral be sold for enough ?

Is the collateral marketable ? (By the bank)

Can you gain possession if needed ?