Construction & Housing: Softwood Timber - New Forests global harvest of industrial roundwood, being...

17

Construction and Housing: Softwood Timber Sector Overview March 2017

Transcript of Construction & Housing: Softwood Timber - New Forests global harvest of industrial roundwood, being...

Construction and Housing: Softwood Timber

Sector Overview March 2017

2

Disclaimer © New Forests 2017. This presentation is issued by and is the property of New Forests Asset Management Pty Ltd (New Forests) and may not be reproduced or used in any form or medium without express written permission.

This document is dated 31 March 2017. Statements are made only as of the date of this document unless otherwise stated. New Forests is not responsible for providing updated information to any person.

The information contained in this document is of a general nature and is intended for discussion purposes only. The information set forth herein is based on information obtained from sources that New Forests believes to be reliable, but New Forests makes no representations as to, and accepts no responsibility or liability for, the accuracy, reliability or completeness of the information. Except insofar as liability under any statute cannot be excluded, New Forests, its associates, related bodies corporate, and all of their respective directors, employees and consultants, do not accept any liability for any loss or damage (whether direct, indirect, consequential or otherwise) arising from the use of this information.

The information contained in this document may include financial and business projections that are based on a large number of assumptions, any of which could prove to be significantly incorrect. New Forests notes that all projections, valuations, and statistical analyses are subjective illustrations based on one or more among many alternative methodologies that may produce different results. Projections, valuations, and statistical analyses included herein should not be viewed as facts, predictions or the only possible outcome.

New Forests Advisory Pty Limited (ACN 114 545 274) is registered with the Australian Securities and Investments Commission and is the holder of AFSL No 301556. New Forests Asset Management Pty Limited (ACN 114 545 283) is registered with the Australian Securities and Investments Commission and is an Authorised Representative of New Forests Advisory Pty Limited (AFS Representative Number 376306). New Forests Inc. has filed as an Exempt Reporting Adviser with the Securities and Exchange Commission.

• Softwood timber is supplied from a range of natural and plantation coniferous trees and represents a third of the global harvest of industrial roundwood, being 1.3 billion cubic metres out of a total global harvest of 4 billion cubic metres.

• Australia and New Zealand have 2.7 million hectares of softwood plantations, representing around 1% of the global plantation area of approximately 200 million hectares. These plantations produce around 44 million cubic metres of roundwood per annum representing approximately 3% of global softwood industrial roundwood production.

Softwood Timber

3

Sources: www.fao.org/3/a-i3274e.pdf, www.fao.org/faostat/en/#data/FO, RISI Global Tree Farm Study 2017,

www.nzfoa.org.nz/resources/publications/facts-and-figures, www.agriculture.gov.au/abares/forestsaustralia

Image: Softwood logs from New Forests’ Penola Plantations managed in

Australia’s Green Triangle region.

• Radiata Pine (Pinus radiata) has been widely established as a plantation species due to its relatively high biological growth rate in temperate climates and the wide range of uses of the timber it produces.

• Radiata Pine is a highly versatile species, used for structural and appearance applications, engineered wood products, plywood, reconstituted panels, pallets and packaging, furniture, posts, poles, paper, pellets and burnt as a source of commercial energy.

• Of the 4.2 million hectares of the species planted globally, over 3.9 million hectares are in the Southern Hemisphere.

• 2.3 million hectares of Radiata Pine plantations have been established in Australia (0.8 million hectares) and New Zealand (1.5 million hectares).

Radiata Pine in Australia and New Zealand

4 Source: www.fao.org/3/a-i3274e.pdf

Image: Penola Plantations 4 4

• In this presentation, New Forests focuses on how its Australian and New Zealand softwood assets supply the domestic construction and housing and the Asian export market.

• Further more, we discuss how the timber industry is seeking to optimise softwood utilisation and innovate beyond traditional forest products, extending product life cycles. This in turn improves diversification through value-added products and applications, and creates further market opportunities.

5

New Forests’ Softwood Assets

Image: Radiata Pine

Demand is shifting to Asia and supply sources are re-aligning

• Softwood supply sources have traditionally been Scandinavia, Russia, and North America selling into US, European and Japanese markets.

• Over the past 10 years economic growth and urbanisation occurring in China, and increasingly India, has been the driver of new demand for softwood.

• Northern hemisphere softwood timber has come from predominantly managed natural forests where available supply is reducing, most significantly in Canada.

• Australia and New Zealand have gradually increased production from planted Radiata Pine forests, taking advantage of reducing production from North America, geographic proximity to growing Chinese and Indian markets, favourable growing conditions and climate, and forest management certification.

Global Softwood Markets Are Tightening

6 Source: www.fao.org/faostat/en/#data/FO (calendar year)

0

50

100

150

200

250

300

350

199

5

199

7

199

9

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

Mill

ion

s C

ub

ic M

etr

es

Softwood Roundwood Producers

Australia & New ZealandCanadaScandinaviaRussian FederationUnited States of America

• Between 1982 and 2015 China’s urbanisation rate increased from 21% to 56%.

• China’s urbanisation rate is projected to increase to 60% by 2020 due to increased housing demand from an additional 100 million migrant workers.

Growth in Chinese Softwood Demand China’s urbanisation and construction drives softwood log imports

Sources: news.xinhuanet.com/english/2016-04/19/c_135294134.htm, www.bloomberg.com/view/articles/2016-07-19/has-china-reached-peak-urbanization, RISI China Timber Outlook Study 2015 (updated, calendar year)

7

0

10

20

30

40

50

60

70

80

Mill

ion

Cu

bic

Metr

es

Chinese Softwood Log and Lumber Imports

Logs Lumber (Roundwood Equivalent)

0

200

400

600

800

1000

1200

Mill

ion

Sq

uare

Metr

es

Chinese Completed Construction

Residential Non-Residential

RISI’s forecast of total Chinese floor space completion peaks in 2018-2020. Residential construction is expected to slow as urbanisation and the working age population declines. Diversification into other markets, e.g. furniture, and throughout the bio-economy will be an important driver of future demand.

Sources: RISI China Timber Outlook Study 2015 (updated), OandA (calendar year) 8

• In 2004, China imported 16 million cubic metres of softwood logs. By 2016, this had grown to 33.7 million cubic metres.

• The source of softwood logs has diversified. New Zealand overtook Russia as the largest softwood log supplier to China in 2013. (See graph on slide 9).

• Recent changes in currency exchange rates have reduced the competitiveness of US log exports, further supporting increasing market share for New Zealand as well as other countries, including Australia.

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

$1.20

2009 2010 2011 2012 2013 2014 2015 2016

AUD and NZD Exchange Rates

USD:AUD USD:NZD

Changing Chinese Softwood Log Supply Sources

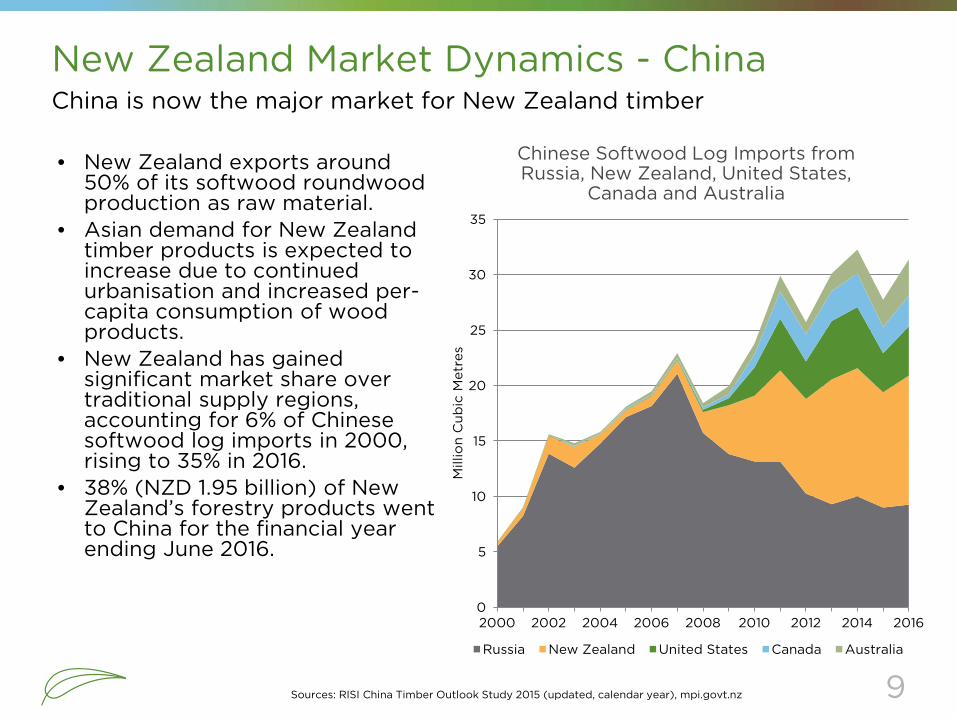

New Zealand Market Dynamics - China China is now the major market for New Zealand timber

Sources: RISI China Timber Outlook Study 2015 (updated, calendar year), mpi.govt.nz

• New Zealand exports around 50% of its softwood roundwood production as raw material.

• Asian demand for New Zealand timber products is expected to increase due to continued urbanisation and increased per-capita consumption of wood products.

• New Zealand has gained significant market share over traditional supply regions, accounting for 6% of Chinese softwood log imports in 2000, rising to 35% in 2016.

• 38% (NZD 1.95 billion) of New Zealand’s forestry products went to China for the financial year ending June 2016.

9

0

5

10

15

20

25

30

35

2000 2002 2004 2006 2008 2010 2012 2014 2016

Mill

ion

Cu

bic

Metr

es

Chinese Softwood Log Imports from Russia, New Zealand, United States,

Canada and Australia

Russia New Zealand United States Canada Australia

• India is one of the fastest growing economies in the world. India’s annual growth rate according to IMF 2016 estimates was 6.6% and the 2017-18 outlook is 7.2-7.7% (compared to China’s 6.5% and 6.0%, respectively).

• India is expected to become the third largest economy in the world by 2030. In 2016 it was ranked fifth.

• India’s urbanisation rate in 2015 was 33% and is expected to reach 39% in 2030.

• Approximately 110 million houses are forecast to be required by 2022 in urban and rural India.

• Between June 2006 and June 2016, New Zealand’s total forestry product exports to India increased from NZD 57.2 million to NZD 310.8 million.

New Zealand Market Dynamics - India Indian imports are trending upward and likely to continue due to economic growth and urbanisation

Sources: imf.org, assets.kpmg.com/content/dam/kpmg/in/pdf/2016/08/urban_realestate.pdf, statisticstimes.com/economy/projected-world-gdp-ranking.php, mpi.govt.nz

10

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Th

ou

san

d C

ub

ic M

etr

es

New Zealand Roundwood Exports to India

• Australia runs a softwood lumber deficit, part of an AUD 2.1 billion trade deficit in wood products, with domestic consumption outstripping production and imported softwood timber required to service the domestic construction and housing industry.

• Softwood production in Australia is focused on meeting the domestic deficit in lumber, with exports generally being of lower grades of logs unsuitable for structural or appearance lumber production.

11

Australian Softwood Market Dynamics

Source: ABARES Forest and Wood Product Statistics

Image: Timberlink Australia

• Australia exports around 25% of its softwood roundwood production as raw material, primarily to China.

-

1,000

2,000

3,000

4,000

5,000

Th

ou

san

d C

ub

ic M

etr

es

Australian Softwood Lumber Supply and Demand

Imports Exports

Annual Production Apparent Consumption

-

50,000

100,000

150,000

200,000

250,000

300,000

Oct-

01

Oct-

02

Oct-

03

Oct-

04

Oct-

05

Oct-

06

Oct-

07

Oct-

08

Oct-

09

Oct-

10

Oct-

11

Oct-

12

Oct-

13

Oct-

14

Oct-

15

Oct-

16

Building Approvals: Total Dwelling vs. Detached Dwellings

Dwelling Approvals - Moving Annual Totals

Detached Dwelling Approvals - Moving Annual Totals

12

Australian Residential Demand A strong residential housing sector will continue to support domestic softwood lumber demand supported by forecast immigration and population growth in Australia.

Source: BIS Shrapnel

Image: Young replant area at Penola Plantations

Australian Alterations and Additions Housing alterations and additions represent a less cyclical market (but more seasonally driven) than new housing construction for softwood lumber. Increasing house prices have increased equity in homes, allowing homeowners to re-invest in their property through renovations. Long-term growth is expected in this market.

Source: ABS Building Activity Value of Residential Building Work

Image: Timber grading at Timberlink Australia 13

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

Valu

e o

f W

ork

Do

ne, A

UD

Mill

ion

s

Total Residential Alterations, Additions, and Conversions (All Sectors)

Trend

Australian Softwood Exports to China China continues to import increasing volumes of timber, and the Australian timber market has responded to this sustained appetite. A declining AUD/USD has allowed Australia to direct small and low grade softwood logs to the export market. Around 25% of Australia’s softwood roundwood production is exported.

Source: ABARES Forest and Wood Product Statistics

Image: Harvest slash at Burbyng, Green Triangle

14

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Th

ou

san

d C

ub

ic M

etr

es

Australian Roundwood Exports to China

15

Innovating Towards a Bio-economy Bio-products are being developed as alternatives to non-renewable raw materials, such as fossil fuels, and allowing for sustainable use of biological natural resources to produce goods, energy, food, and services. These markets provide diversification opportunities for softwood investors.

• The bio-economy refers to a growing body of economic activity based on the use of biological inputs to develop sustainable materials and products, including those described in the image to the right. Timber fibre now provides sustainable inputs for a range of products in the bio-economy:

• Engineered materials such as plywood, glulam, cross laminated timber (CLT), and oriented strand boards (OSB) are sophisticated and viable building materials. Commercial tall-building projects are now starting to be constructed across the world with engineered wood products.

• Biomaterials include diverse materials, ranging from rayon for clothing to pseudo-plastics.

• Biomass can be used to create both bioenergy and refined biofuels; biomass must be sourced responsibly and total life cycle analysis is important for bioenergy and biofuels to be sustainable

• Biorefinery products can be created directly and as by-products of industrial processes, making more sustainable resins, chemicals, and polymers

Australia New Zealand

Country Risk

• Long track record; mature forestry industry

• Attractive and safe operating environment

• Open to foreign investment

• Long track record; mature forestry industry

• Attractive and safe operating environment

• Open to foreign investment

Timber Market Exposure

• Domestic-oriented market: softwood lumber is the major portion of apparent domestic consumption (over 90%). This is linked to domestic housing demand and population growth

• Net importer of wood products

• Timber market exposure through economic ties, e.g. Free Trade Agreements

• Exposed to Asian economic growth and urbanisation story

• The Australian market is structurally supportive of prices due to strong domestic demand and geographic isolation

• Innovation in forest products, technology and bio-economy increases applications and market opportunities

• Export-oriented market

• Linked to China and India‘s booming construction and housing markets

• Export industry is supported by good infrastructure, multiple ports, and a skilled workforce

• Softwood timber prices can be more volatile than in Australia due to its primary exposure to export markets

• Innovation in forest products, technology and bio-economy increases applications and market opportunities

Currency Risk

• Asian commodity demand and mining investment inflows helped drive a strong AUD between 2010 – 2014. Although the AUD has since eased, any future AUD strength changes the competitiveness of exports.

• As AUD weakens, softwood imports will become more expensive for Australian building industry, favoring domestic softwood timber suppliers.

• Linked to the USD

• A high NZD/USD affects competitiveness of exports. However, as the New Zealand currency has recently eased, exports have become more competitive.

Softwood Market Exposure and Opportunity

16

Want to Learn More? To learn more about New Forests’ investment programs related to softwood plantations in Australia and New Zealand, contact Radha Kuppalli at [email protected].

17 Image: Penola Plantations