constellation energy 2003 10K

140

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended DECEMBER 31, 2003 Commission IRS Employer file number Exact name of registrant as specified in its charter Identification No. 1-12869 CONSTELLATION ENERGY GROUP, INC. 52-1964611 1-1910 BALTIMORE GAS AND ELECTRIC COMPANY 52-0280210 MARYLAND (States of incorporation) 750 E. PRATT STREET BALTIMORE, MARYLAND 21202 (Address of principal executive offices) (Zip Code) 410-783-2800 (Registrants’ telephone number, including area code) SECURITIES REGISTERED PURSUANT TO SECTION 12(B) OF THE ACT: Name of Each Exchange on Title of each class Which Registered New York Stock Exchange, Inc. Constellation Energy Group, Inc. Common Stock—Without Par Value Chicago Stock Exchange, Inc. Pacific Exchange, Inc. 6.20% Trust Preferred Securities ($25 liquidation amount per preferred security) issued by BGE Capital Trust II, fully and unconditionally guaranteed, based on several obligations, by New York Stock Exchange, Inc. Baltimore Gas and Electric Company SECURITIES REGISTERED PURSUANT TO SECTION 12(G) OF THE ACT: Not Applicable Indicate by check mark whether the registrants (1) have filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months, and (2) have been subject to such filing requirements for the past 90 days. Yes No . Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrants’ knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Indicate by check mark whether Constellation Energy Group, Inc. is an accelerated filer Yes No . Indicate by check mark whether Baltimore Gas and Electric Company is an accelerated filer Yes No . Aggregate market value of Constellation Energy Group, Inc. Common Stock, without par value, held by non-affiliates as of June 30, 2003 was approximately $5,698,266,202 based upon New York Stock Exchange composite transaction closing price. CONSTELLATION ENERGY GROUP, INC. COMMON STOCK, WITHOUT PAR VALUE 168,103,732 SHARES OUTSTANDING ON FEBRUARY 27, 2004. DOCUMENTS INCORPORATED BY REFERENCE Part of Form 10-K Document Incorporated by Reference III Certain sections of the Proxy Statement for Constellation Energy Group, Inc. for the Annual Meeting of Shareholders to be held on May 21, 2004. Baltimore Gas and Electric Company meets the conditions set forth in General Instruction I(1)(a) and (b) of Form 10-K and is therefore filing this Form in the reduced disclosure format.

-

Upload

finance12 -

Category

Economy & Finance

-

view

178 -

download

0

Transcript of constellation energy 2003 10K

UNITED STATESSECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OFTHE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended DECEMBER 31, 2003Commission IRS Employerfile number Exact name of registrant as specified in its charter Identification No.

1-12869 CONSTELLATION ENERGY GROUP, INC. 52-1964611

1-1910 BALTIMORE GAS AND ELECTRIC COMPANY 52-0280210

MARYLAND

(States of incorporation)

750 E. PRATT STREET BALTIMORE, MARYLAND 21202

(Address of principal executive offices) (Zip Code)

410-783-2800

(Registrants’ telephone number, including area code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(B) OF THE ACT:

Name of Each Exchange onTitle of each class Which Registered

New York Stock Exchange, Inc.Constellation Energy Group, Inc. Common Stock—Without Par Value � Chicago Stock Exchange, Inc.

Pacific Exchange, Inc.

6.20% Trust Preferred Securities ($25 liquidation amount per preferred security) issued by BGECapital Trust II, fully and unconditionally guaranteed, based on several obligations, by New York Stock Exchange, Inc.Baltimore Gas and Electric Company

�SECURITIES REGISTERED PURSUANT TO SECTION 12(G) OF THE ACT:

Not Applicable

Indicate by check mark whether the registrants (1) have filed all reports required to be filed by Section 13 or 15(d) of theSecurities Exchange Act of 1934 during the preceding 12 months, and (2) have been subject to such filing requirements for thepast 90 days. Yes � No �.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, andwill not be contained, to the best of registrants’ knowledge, in definitive proxy or information statements incorporated by referencein Part III of this Form 10-K or any amendment to this Form 10-K. �

Indicate by check mark whether Constellation Energy Group, Inc. is an accelerated filer Yes � No �.Indicate by check mark whether Baltimore Gas and Electric Company is an accelerated filer Yes � No �.

Aggregate market value of Constellation Energy Group, Inc. Common Stock, without par value, held by non-affiliates as ofJune 30, 2003 was approximately $5,698,266,202 based upon New York Stock Exchange composite transaction closing price.

CONSTELLATION ENERGY GROUP, INC. COMMON STOCK, WITHOUT PAR VALUE 168,103,732 SHARESOUTSTANDING ON FEBRUARY 27, 2004.

DOCUMENTS INCORPORATED BY REFERENCE

Part of Form 10-K Document Incorporated by Reference

III Certain sections of the Proxy Statement for Constellation Energy Group, Inc. for the Annual Meeting ofShareholders to be held on May 21, 2004.

Baltimore Gas and Electric Company meets the conditions set forth in General Instruction I(1)(a) and (b) of Form 10-K andis therefore filing this Form in the reduced disclosure format.

TABLE OF CONTENTS

Page

Forward Looking Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1PART I

Item 1 — Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Merchant Energy Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Baltimore Gas and Electric Company . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Other Nonregulated Businesses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Consolidated Capital Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Environmental Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Employees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

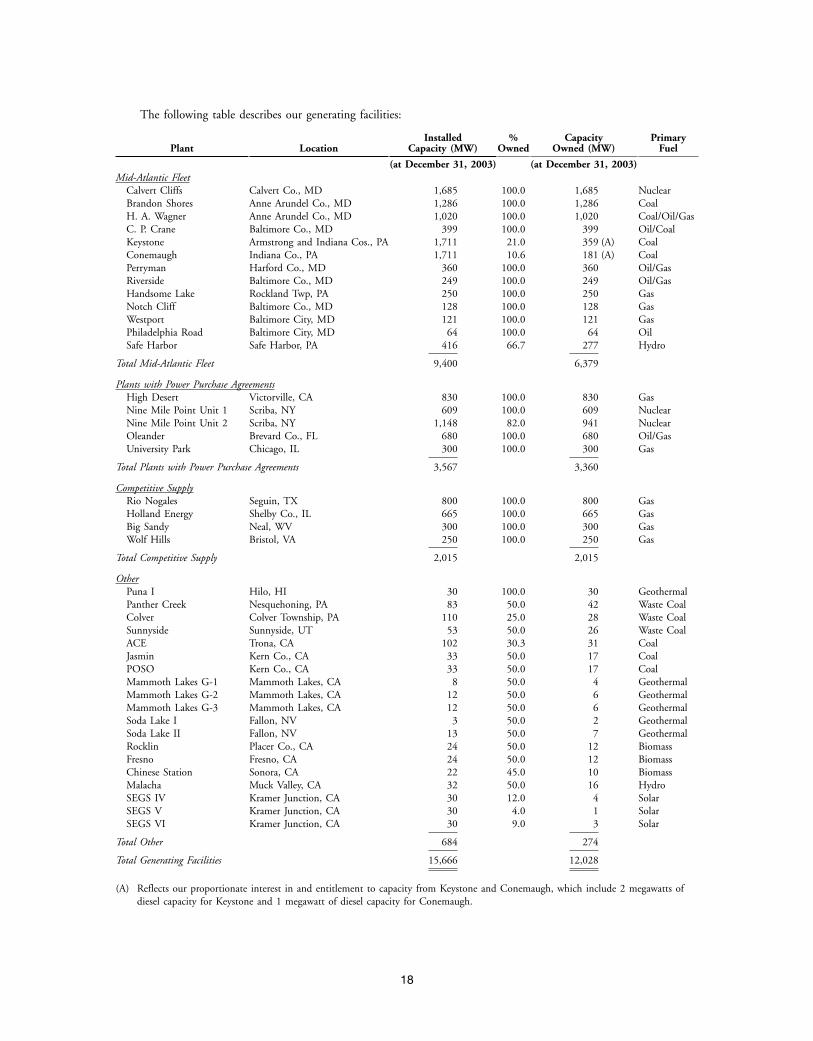

Item 2 — Properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Item 3 — Legal Proceedings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Item 4 — Submission of Matters to Vote of Security Holders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Executive Officers of the Registrant (Instruction 3 to Item 401(b) of Regulation S-K) . . . . . . . . . 19

PART II

Item 5 — Market for Registrant’s Common Equity and Related Shareholder Matters . . . . . . . . . . . . . . . . . . . 21

Item 6 — Selected Financial Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Item 7 — Management’s Discussion and Analysis of Financial Condition and Results of Operations . . . . . . 24

Item 7A — Quantitative and Qualitative Disclosures About Market Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

Item 8 — Financial Statements and Supplementary Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

Item 9 — Changes in and Disagreements with Accountants on Accounting and Financial Disclosure . . . . . . 119

Item 9A — Controls and Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119

PART III

Item 10 — Directors and Executive Officers of the Registrant . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119

Item 11 — Executive Compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119

Item 12 — Security Ownership of Certain Beneficial Owners andManagement and Related Shareholder Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

Item 13 — Certain Relationships and Related Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

Item 14 — Principal Accountant Fees and Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

PART IV

Item 15 — Exhibits, Financial Statement Schedules and Reports on Form 8-K . . . . . . . . . . . . . . . . . . . . . . . . . . 121

Signatures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 127

♦ the inability of BGE to recover all its costsForward Looking Statementsassociated with providing electric retailWe make statements in this report that are consideredcustomers service during the electric rate freezeforward looking statements within the meaning of theperiod,Securities Exchange Act of 1934. Sometimes these

♦ the effect of weather and general economic andstatements will contain words such as ‘‘believes,’’business conditions on energy supply, demand,‘‘anticipates,’’ ‘‘expects,’’ ‘‘intends,’’ ‘‘plans,’’ and otherand prices,similar words. We also disclose non-historical

♦ regulatory or legislative developments that affectinformation that represents management’s expectations,deregulation, transmission or distribution rateswhich are based on numerous assumptions. Theseand revenues, demand for energy, or increasesstatements and projections are not guarantees of ourin costs, including costs related to nuclearfuture performance and are subject to risks,power plants, safety, or environmentaluncertainties, and other important factors that couldcompliance,cause our actual performance or achievements to be

♦ the actual outcome of uncertainties associatedmaterially different from those we project. These risks,with assumptions and estimates using judgmentuncertainties, and factors include, but are not limitedwhen applying critical accounting policies andto:preparing financial statements, including factors♦ the timing and extent of changes in commoditythat are estimated in determining the fair valueprices and volatilities for energy and energyof energy contracts, such as the ability torelated products including coal, natural gas, oil,obtain market prices and in the absence ofelectricity, and emission allowances,verifiable market prices the appropriateness of♦ the timing and extent of deregulation of, andmodels and model inputs (including, but notcompetition in, the energy markets in Northlimited to, estimated contractual load

America, and the rules and regulations adoptedobligations, unit availability, forward

on a transitional basis in those markets,commodity prices, interest rates, correlation and♦ the conditions of the capital markets, interest volatility factors),

rates, availability of credit, liquidity, and general ♦ changes in accounting principles or practices,economic conditions, as well as Constellation ♦ the ability to attract and retain customers inEnergy Group’s (Constellation Energy) and our competitive supply activities and toBaltimore Gas and Electric Company’s (BGE) adequately forecast their energy usage,ability to maintain their current credit ratings, ♦ losses on the sale or write down of assets due♦ the effectiveness of Constellation Energy’s and to impairment events or changes inBGE’s risk management policies and procedures management intent with regard to eitherand the ability and willingness of our holding or selling certain assets, andcounterparties to satisfy their financial and ♦ cost and other effects of legal andperformance commitments, administrative proceedings that may not be

♦ the liquidity and competitiveness of wholesale covered by insurance, including environmentalmarkets for energy commodities, liabilities.

♦ operational factors affecting commercial Given these uncertainties, you should not placeoperations of our generating facilities (including undue reliance on these forward looking statements.nuclear facilities) and BGE’s transmission and Please see the other sections of this report and ourdistribution facilities, including catastrophic other periodic reports filed with the Securities andweather related damages, unscheduled outages Exchange Commission (SEC) for more information onor repairs, unanticipated changes in fuel costs these factors. These forward looking statementsor availability, unavailability of gas represent our estimates and assumptions only as of thetransportation or electric transmission services, date of this report.workforce issues, terrorism, liabilities associated Changes may occur after that date, and neitherwith catastrophic events, and other events Constellation Energy nor BGE assume responsibility tobeyond our control, update these forward looking statements.

Constellation Energy was incorporated inPART IItem 1. Business Maryland on September 25, 1995. On April 30, 1999,

Constellation Energy became the holding company forOverviewBGE and its subsidiaries through a share exchange.

Constellation Energy is a North American energyReferences in this report to ‘‘we’’ and ‘‘our’’ are to

company which includes a merchant energy business Constellation Energy and its subsidiaries, collectively.and BGE, its regulated electric and gas public utility in References in this report to the ‘‘utility business’’ are tocentral Maryland. BGE.

1

Our merchant energy business is a competitive Constellation Energy maintains a website atprovider of energy solutions for large customers in constellation.com where copies of our annual reports onNorth America. It has electric generation assets located Form 10-K, quarterly reports on Form 10-Q, currentin various regions of the United States and provides reports on Form 8-K, and any amendments may beenergy solutions to meet customers’ needs. Our obtained free of charge. These reports are posted on ourmerchant energy business focuses on serving the full website the same day they are filed with the SEC. Theenergy and capacity requirements (load-serving) of, and website address for BGE is bge.com. Both websiteproviding other energy risk management services for addresses are inactive textual references and the contentsvarious customers, such as utilities, municipalities, of these websites are not part of this Form 10-K.cooperatives, retail aggregators, and commercial and In addition, the website for Constellation Energyindustrial customers. includes copies of our Corporate Governance

Our merchant energy business includes: Guidelines, Principles of Business Integrity, Corporate♦ a generation operation that owns, operates, and Compliance Program and Insider Trading Policy, and

maintains fossil, nuclear, and hydroelectric the charters for the Audit, Compensation andgenerating facilities and interests in qualifying Nominating and Corporate Governance Committees offacilities, fuel processing facilities and power the Board of Directors. Copies of each of theseprojects in the United States, documents may be printed from the website or may be

♦ a marketing and risk management operation obtained from Constellation Energy upon writtenthat provides energy products and services to request to the Corporate Secretary.wholesale customers, The Principles of Business Integrity is a code of

♦ an electric and gas retail operation that provides ethics which applies to all of our directors, officers, andenergy services to commercial and industrial employees, including the chief executive officer, chiefcustomers, and financial officer, and chief accounting officer. We will

♦ a generation and consulting services operation. post any amendments to, or waivers from, theBGE is a regulated electric transmission and Principles of Business Integrity applicable to our chief

distribution utility company and a regulated gas executive officer, chief financial officer, or chiefdistribution utility company with a service territory that accounting officer on our website.covers the City of Baltimore and all or part of ten

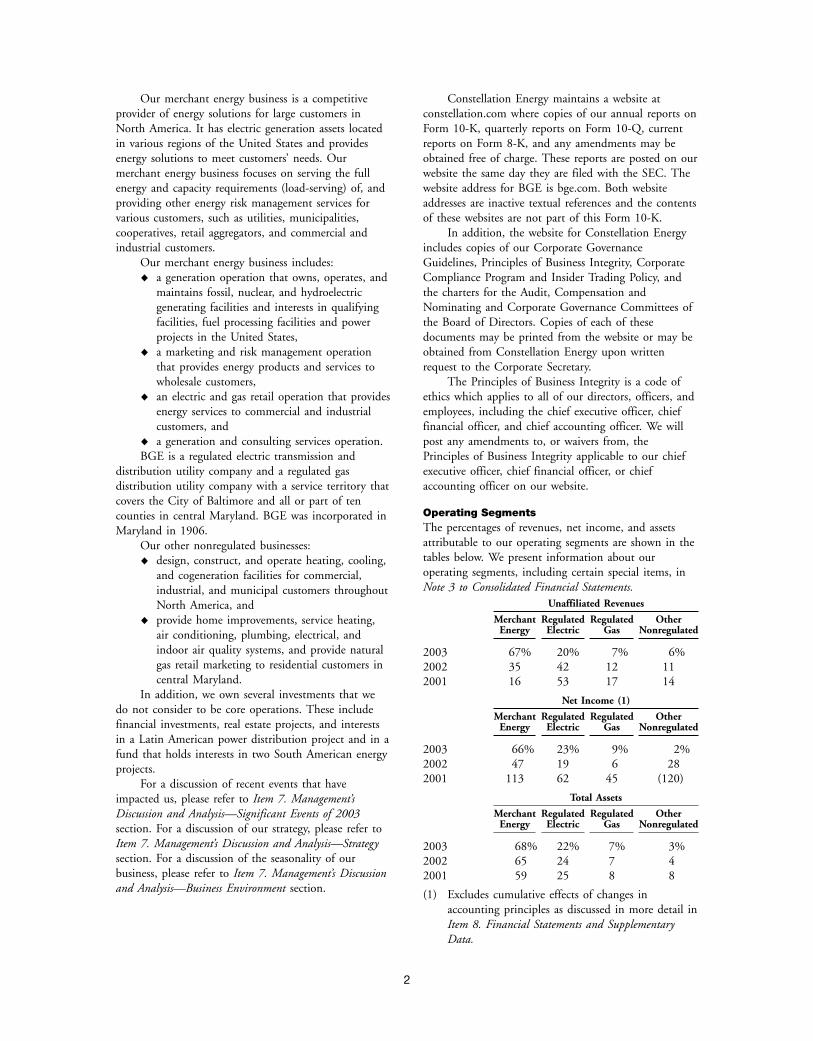

Operating Segmentscounties in central Maryland. BGE was incorporated inThe percentages of revenues, net income, and assetsMaryland in 1906.attributable to our operating segments are shown in theOur other nonregulated businesses:tables below. We present information about our♦ design, construct, and operate heating, cooling,operating segments, including certain special items, inand cogeneration facilities for commercial,Note 3 to Consolidated Financial Statements.industrial, and municipal customers throughout

Unaffiliated RevenuesNorth America, andMerchant Regulated Regulated Other♦ provide home improvements, service heating,

Energy Electric Gas Nonregulatedair conditioning, plumbing, electrical, andindoor air quality systems, and provide natural 2003 67% 20% 7% 6%gas retail marketing to residential customers in 2002 35 42 12 11central Maryland. 2001 16 53 17 14

In addition, we own several investments that we Net Income (1)do not consider to be core operations. These include

Merchant Regulated Regulated Otherfinancial investments, real estate projects, and interests Energy Electric Gas Nonregulatedin a Latin American power distribution project and in a

2003 66% 23% 9% 2%fund that holds interests in two South American energy2002 47 19 6 28projects.2001 113 62 45 (120)For a discussion of recent events that have

Total Assetsimpacted us, please refer to Item 7. Management’sMerchant Regulated Regulated OtherDiscussion and Analysis—Significant Events of 2003

Energy Electric Gas Nonregulatedsection. For a discussion of our strategy, please refer toItem 7. Management’s Discussion and Analysis—Strategy 2003 68% 22% 7% 3%section. For a discussion of the seasonality of our 2002 65 24 7 4business, please refer to Item 7. Management’s Discussion 2001 59 25 8 8and Analysis—Business Environment section. (1) Excludes cumulative effects of changes in

accounting principles as discussed in more detail inItem 8. Financial Statements and SupplementaryData.

2

We present details about our generating propertiesMerchant Energy BusinessIntroduction in Item 2. Properties.Our merchant energy business integrates electricgeneration assets with the marketing and risk Mid-Atlantic Fleetmanagement of energy and energy-related commodities, We own 6,379 MW of fossil, nuclear and hydroelectricallowing us to manage energy price risk over geographic generation capacity in the PJM region. The output ofregions and over time. Constellation Power Source, our these plants is managed by our wholesale marketing andwholesale marketing and risk management operation, risk management operation and is hedged through adispatches the energy from our generating facilities, combination of power sales to wholesale and retailmanages the risks associated with selling the output and market participants.obtaining fuels, and structures transactions to meet BGE transferred all of these facilities to ourcustomers’ energy and risk management requirements. merchant energy generation subsidiaries on July 1, 2000Constellation NewEnergy, our electric and gas retail as a result of the implementation of electric customeroperation, provides energy services to commercial and choice and competition among suppliers in Maryland,industrial customers. Generation capacity supports these except for the Handsome Lake project that commencedmarketing operations by providing a source of reliable operations in mid-2001. The assets transferred frompower supply that provides a physical hedge for some of BGE are subject to the lien of BGE’s mortgage.our load-serving activities. Our merchant energy business provides standard

Our merchant energy business: offer service to BGE as discussed in the Baltimore Gas♦ provided service to distribution utilities, and Electric Company—Standard Offer Service section.

municipalities, and commercial and industrial Our merchant energy business meets the load-servingcustomers with approximately 24,000 requirements of this contract using the output from themegawatts (MW) of peak load in the aggregate Mid-Atlantic Fleet and from purchases in the wholesaleduring 2003, market. For 2003, the peak load supplied to BGE was

♦ provided approximately 195,000 million British approximately 5,270 MW.Thermal Units (mmBTUs) of natural gas tocommercial and industrial customers during Plants with Power Purchase Agreements2003, and We own 3,360 MW of nuclear and natural gas/oil

♦ owns approximately 12,030 MW of generation generation capacity with power purchase agreements forcapacity. their output. Our facilities with power purchase

We analyze the results of our merchant energy agreements consist of:business as follows: ♦ the Nine Mile Point facility,

♦ Mid-Atlantic Fleet—our fossil, nuclear, and ♦ the High Desert Power Project, whichhydroelectric generating facilities and commenced operations in early 2003,load-serving activities in the PJM ♦ the Oleander project, which commencedInterconnection (PJM) region for which the operations in mid-2002, andoutput is primarily used to serve BGE. This ♦ the University Park project, which commencedalso includes active portfolio management of operations in mid-2001.the generating assets and associated physical We purchased 100% of Nine Mile Point Unit 1and financial arrangements. (609 MW) and 82% of Unit 2 (941 MW) in

♦ Plants with Power Purchase Agreements—our November 2001. The remaining interest in Nine Milegenerating facilities with long-term power Point Unit 2 is owned by a subsidiary of the Longpurchase agreements, including our Nine Mile Island Power Authority. Unit 1 entered service in 1969Point Nuclear Station (Nine Mile Point), and Unit 2 in 1988. Nine Mile Point is located withinOleander, University Park, and High Desert the New York Independent System Operator (NYISO)generating facilities. region.

♦ Competitive Supply—our wholesale marketing We sell 90% of our share of Nine Mile Point’sand risk management operation that provides output to the former owners of the plant at an averageenergy products and services to distribution price of nearly $35 per megawatt-hour (MWH) underutilities and other wholesale customers. We also agreements that terminate between 2009 and 2011. Theprovide electric and gas energy services to retail agreements are unit contingent (if the output is notcommercial and industrial customers. available because the plant is not operating, there is no

♦ Other—our investments in qualifying facilities requirement to provide output from other sources). Theand domestic power projects and our remaining 10% of Nine Mile Point’s output is managedgeneration and consulting services. by our wholesale marketing and risk management

operation and sold into the wholesale market.

3

Competitive SupplyAfter termination of the power purchaseWe are a leading supplier of energy products andagreements, a revenue sharing agreement with theservices in North America to wholesale customers andformer owners of the plant will begin and continueretail commercial and industrial customers. Ourthrough 2021. Under this agreement, which appliescompetitive supply activities include 2,015 MW fromonly to Unit 2, a predetermined price is compared toour Rio Nogales, Holland Energy, Big Sandy, and Wolfthe market price for electricity. If the market priceHills natural gas-fired generating facilities. These fourexceeds the strike price, then 80% of this excess amountfacilities are not sold forward under long-termis shared with the former owners of the plant. Theagreements, and their output is used to serve customerrevenue sharing agreement is unit contingent and isrequirements.based on the operation of the unit.

We have an operating agreement with the Long Origination of Structured TransactionsIsland Power Authority subsidiary to exclusively operate We structure transactions that serve the full energy andUnit 2. The Long Island Power Authority subsidiary is capacity requirements of various customers outside theresponsible for 18% of the operating costs (and PJM region such as distribution utilities, municipalities,decommissioning costs) of Unit 2 and has cooperatives, and retail aggregators that do not ownrepresentation on the Nine Mile Point Unit 2 sufficient generating capacity or in-house supplymanagement committee which provides certain functions to meet their own load requirements. We alsooversight and review functions. structure transactions to supply full energy and capacity

The license on Nine Mile Point’s Unit 1 expires in requirements and provide other energy products and2009 and in 2026 on Unit 2. We have commenced a services to retail commercial and industrial customers.license extension initiative for both units with the These activities typically occur in regional marketsobjective of obtaining up to 20 years of additional in which end user customers’ electricity rates have beenoperations. We expect to submit the license extension deregulated and thereby separated from the cost ofapplication to the NRC in the spring of 2004. generation supply. These markets include:

The High Desert Power Project has a long-term ♦ the New England, New York, and Mid-Atlanticpower sales agreement with the California Department regions,of Water Resources (CDWR). The contract is a ♦ Texas,‘‘tolling’’ structure, under which the CDWR pays a ♦ the Mid-West region,fixed amount of $12.1 million per month and provides ♦ the West region, andCDWR the right, but not the obligation, to purchase ♦ certain areas of Canada.power from the project at a price linked to the variable Contracts with these customers generally extendcost of production. During the term of the contract, from one to ten years, but some can be longer. Wewhich runs until December 2010, the project will currently have approximately 22,800 MW of load underprovide energy exclusively to the CDWR. contract for 2004.

We have sold portions of the output of the In 2003, we acquired Blackhawk Energy ServicesOleander and University Park facilities ranging from and Kaztex Energy Management and in 2002, we50% to 100% under tolling contracts for terms ending acquired NewEnergy and Alliance. These acquisitionsin 2005 through 2009. Under these tolling contracts, expand our business in the competitive supply marketour respective counterparties will pay a fixed amount by providing electricity, natural gas, transportation, andper month and have the right, but not the obligation, other energy related services to retail commercial andto purchase power from us at prices linked to the industrial customers throughout North America.variable fuel and other costs of production. To meet our customers’ load-serving requirements,

On November 25, 2003, we announced an our merchant energy business obtains energy fromagreement with Rochester Gas & Electric (RG&E) to various sources, including:acquire the 495 megawatt R.E. Ginna Nuclear Power ♦ bilateral power purchase agreements with thirdPlant (Ginna) located north of Rochester, New York. parties,The transaction is contingent upon regulatory approvals ♦ our generation assets,including license extension. The acquisition includes a ♦ regional power pools, orlong-term unit contingent power purchase agreement ♦ tolling contracts with generation companies,where we will sell 90% of the plant’s output and which provide us the right, but not thecapacity to RG&E for 10 years at an average price of obligation, to purchase power at a price linked$44.00 per MWH. The remaining 10% of the plant’s to the variable cost of production, includingoutput will be managed by our wholesale marketing fuel, with terms that generally extend fromand risk management and will be sold into the several months to several years but can bewholesale market. longer.

4

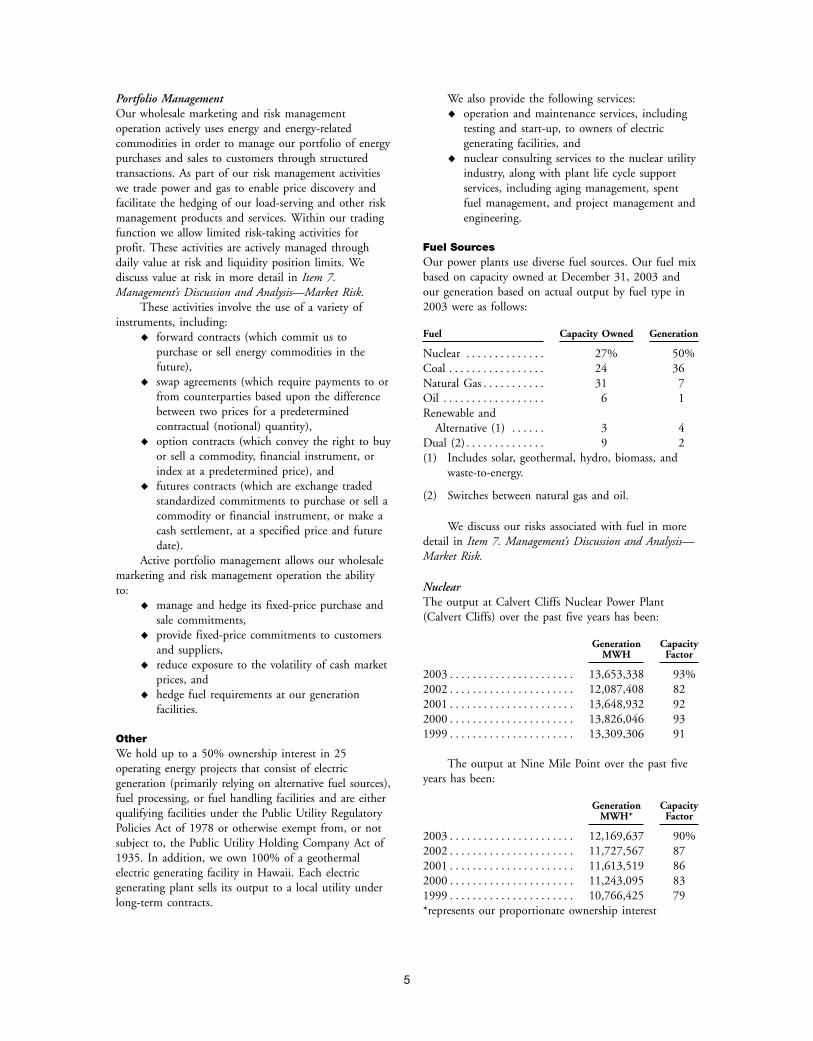

Portfolio Management We also provide the following services:Our wholesale marketing and risk management ♦ operation and maintenance services, includingoperation actively uses energy and energy-related testing and start-up, to owners of electriccommodities in order to manage our portfolio of energy generating facilities, andpurchases and sales to customers through structured ♦ nuclear consulting services to the nuclear utilitytransactions. As part of our risk management activities industry, along with plant life cycle supportwe trade power and gas to enable price discovery and services, including aging management, spentfacilitate the hedging of our load-serving and other risk fuel management, and project management andmanagement products and services. Within our trading engineering.function we allow limited risk-taking activities for

Fuel Sourcesprofit. These activities are actively managed throughOur power plants use diverse fuel sources. Our fuel mixdaily value at risk and liquidity position limits. Webased on capacity owned at December 31, 2003 anddiscuss value at risk in more detail in Item 7.our generation based on actual output by fuel type inManagement’s Discussion and Analysis—Market Risk.2003 were as follows:These activities involve the use of a variety of

instruments, including:Fuel Capacity Owned Generation♦ forward contracts (which commit us to

purchase or sell energy commodities in the Nuclear . . . . . . . . . . . . . . 27% 50%future), Coal . . . . . . . . . . . . . . . . . 24 36

♦ swap agreements (which require payments to or Natural Gas . . . . . . . . . . . 31 7from counterparties based upon the difference Oil . . . . . . . . . . . . . . . . . . 6 1between two prices for a predetermined Renewable andcontractual (notional) quantity), Alternative (1) . . . . . . 3 4

♦ option contracts (which convey the right to buy Dual (2) . . . . . . . . . . . . . . 9 2or sell a commodity, financial instrument, or (1) Includes solar, geothermal, hydro, biomass, andindex at a predetermined price), and waste-to-energy.

♦ futures contracts (which are exchange traded(2) Switches between natural gas and oil.standardized commitments to purchase or sell a

commodity or financial instrument, or make aWe discuss our risks associated with fuel in morecash settlement, at a specified price and future

detail in Item 7. Management’s Discussion and Analysis—date).Market Risk.Active portfolio management allows our wholesale

marketing and risk management operation the abilityNuclearto:The output at Calvert Cliffs Nuclear Power Plant♦ manage and hedge its fixed-price purchase and(Calvert Cliffs) over the past five years has been:sale commitments,

♦ provide fixed-price commitments to customersGeneration Capacityand suppliers, MWH Factor

♦ reduce exposure to the volatility of cash market2003 . . . . . . . . . . . . . . . . . . . . . . 13,653,338 93%prices, and2002 . . . . . . . . . . . . . . . . . . . . . . 12,087,408 82♦ hedge fuel requirements at our generation2001 . . . . . . . . . . . . . . . . . . . . . . 13,648,932 92facilities.2000 . . . . . . . . . . . . . . . . . . . . . . 13,826,046 931999 . . . . . . . . . . . . . . . . . . . . . . 13,309,306 91Other

We hold up to a 50% ownership interest in 25The output at Nine Mile Point over the past fiveoperating energy projects that consist of electric

years has been:generation (primarily relying on alternative fuel sources),fuel processing, or fuel handling facilities and are either

Generation Capacityqualifying facilities under the Public Utility Regulatory MWH* FactorPolicies Act of 1978 or otherwise exempt from, or not

2003 . . . . . . . . . . . . . . . . . . . . . . 12,169,637 90%subject to, the Public Utility Holding Company Act of

2002 . . . . . . . . . . . . . . . . . . . . . . 11,727,567 871935. In addition, we own 100% of a geothermal

2001 . . . . . . . . . . . . . . . . . . . . . . 11,613,519 86electric generating facility in Hawaii. Each electric

2000 . . . . . . . . . . . . . . . . . . . . . . 11,243,095 83generating plant sells its output to a local utility under

1999 . . . . . . . . . . . . . . . . . . . . . . 10,766,425 79long-term contracts.

*represents our proportionate ownership interest

5

The supply of fuel for nuclear generating stations The nuclear fuel markets are competitive andincludes the: although prices for uranium and conversion are

♦ purchase of uranium (concentrates, and increasing, we do not anticipate any problem inuranium hexafluoride) meeting our future requirements.

♦ conversion of uranium concentrates to uraniumStorage of Spent Nuclear Fuel—Federal Facilities

hexafluoride,One of the issues associated with the operation and♦ enrichment of uranium hexafluoride, anddecommissioning of nuclear generating facilities is♦ fabrication of nuclear fuel assemblies.disposal of spent nuclear fuel. There are no facilities for

Uranium: We have under contract sufficient the reprocessing or permanent disposal of spent nuclearquantities of uranium (concentrates and fuel currently in operation in the United States, and theuranium hexafluoride) to meet 100% of Nuclear Regulatory Commission (NRC) has notboth Calvert Cliffs’ and Nine Mile Point’s licensed any such facilities. The Nuclear Waste Policyrequirements through 2004, 45% for Act of 1982 (NWPA) required the federal governmentboth plants in 2005, 60% for both plants through the Department of Energy (DOE), to developin 2006, and 25% for both plants in a repository for, and disposal of, spent nuclear fuel and2007. In late 2003, the federally high-level radioactive waste.designated Russian export agent As required by the NWPA, we are a party toresponsible for nuclear fuel terminated contracts with the DOE to provide for disposal of spenttheir contract with one of our key nuclear fuel from our nuclear generating plants. Theuranium hexafluoride suppliers located in NWPA and our contracts with the DOE requirethe United States. This action will likely payments to the DOE of one tenth of one cent (oneimpact uranium hexafluoride deliveries mill) per kilowatt hour on nuclear electricity generatedfrom this supplier throughout the term of and sold to pay for the cost of long-term nuclear fuelour agreement. Prices have increased due storage and disposal. We continue to pay those fees intoto this event and will adversely impact the DOE’s Nuclear Waste Fund for Calvert Cliffs andour future costs of uranium hexafluoride. Nine Mile Point. The NWPA and our contracts withThe uranium hexafluoride that was the DOE required the DOE to begin taking possessionscheduled to be delivered from this of spent nuclear fuel generated by nuclear generatingsupplier in 2004 represents approximately units no later than January 31, 1998.27% of our requirements for that year. The DOE has stated that it will not meet thatWe are currently evaluating our options obligation until 2010 at the earliest. This delay hasto acquire alternate uranium hexafluoride required that we undertake additional actions related tosupplies to meet our requirements. on-site fuel storage at Calvert Cliffs and Nine Mile

Conversion: We have contractual commitments Point, including the installation of on-site dry fuelproviding for the conversion of all of our storage capacity at Calvert Cliffs, as described in moreuranium concentrates into uranium detail below. In January 2004, we filed a complainthexafluoride for Calvert Cliffs and Nine against the federal government in the United StatesMile Point through 2004. We do not Court of Federal Claims seeking to recover damageshave requirements for conversion beyond caused by the DOE’s failure to meet its contractual2004 because we currently do not expect obligation to begin disposing of spent nuclear fuel byto purchase uranium concentrates beyond January 31, 1998.2004.

Storage of Spent Nuclear Fuel—On-Site FacilitiesEnrichment: We have contractual commitments thatCalvert Cliffs has a license from the NRC to operate anprovide 100% of Calvert Cliffs’ and Nineon-site independent spent fuel storage installation thatMile Point’s uranium enrichmentexpires in 2012. We have storage capacity at Calvertrequirements through 2006 and 25% ofCliffs that will accommodate spent fuel from operationsthese requirements for both plants inthrough 2008. In addition, we can expand our2007 and 2008.temporary storage capacity at Calvert Cliffs to meetFuel Assemblyfuture requirements until approximately 2025.Fabrication: We have contracted for the fabrication ofCurrently, Nine Mile Point does not have independentfuel assemblies for reloads requiredspent fuel storage capacity. Rather, Nine Mile Point’sthrough 2013 at Calvert Cliffs andUnit 1 has sufficient storage capacity within the plantthrough 2008 for Nine Mile Point.until the end of its current operating license in 2009. Iflicense renewal is obtained, independent spent fuelstorage capability will need to be developed. Nine Mile

6

Point’s Unit 2 has sufficient storage capacity within the decommissioning Nine Mile Point to a greenfield statusplant until 2012. After that time independent spent fuel (restoration of the site so that it substantially matchesstorage capability may need to be developed. the natural state of the surrounding properties and the

site’s intended use). At December 31, 2003, the NineCost for Decommissioning Uranium Enrichment Facilities

Mile Point trust fund assets were $451.2 million.The Energy Policy Act of 1992 contains provisions

Upon the closing of the Ginna acquisition, therequiring domestic nuclear utilities to contribute to a

seller will transfer approximately $202 million infund for decommissioning and decontaminating

decommissioning funds. In return, we will assume alluranium enrichment facilities that had been operated by

liability for the costs to decommission the unit. TheDOE. These contributions are generally payable over a

amount of the decommissioning trust fund transfer is15-year period with escalation for inflation and are

subject to regulatory approval. We believe that thisbased upon the amount of uranium enriched by DOE

transfer will be sufficient to cover our responsibility forfor each utility through 1992. The 1992 Act provides

decommissioning Ginna to a greenfield status.that these costs are recoverable through utility servicerates. BGE is solely responsible for these costs as they Coalrelate to Calvert Cliffs. The sellers of the Nine Mile We purchase the majority of our coal under supplyPoint plant and a subsidiary of the Long Island Power contracts with mining operators, and we acquire theAuthority are responsible for the costs relating to the remainder in the spot or forward coal markets. WeNine Mile Point plant. believe that we will be able to renew supply contracts as

they expire or enter into contracts with other coalCost for Decommissioning

suppliers. Our primary coal burning facilities have theWe are obligated to decommission our nuclear plants at

following requirements:the time these plants cease operation. Both CalvertCliffs and Nine Mile Point are required by the NRC to Approximate

Annual Coaldemonstrate reasonable assurance that funds will beRequirement Special Coalavailable to decommission the sites. When BGE (tons) Restrictions

transferred all of its nuclear generating assets to ourBrandon Shores Sulfur content lessmerchant energy business, it also transferred the trust

Units 1 and 2 than 1.20 lbs perfund established to pay for decommissioning Calvert(combined) . . . 3,500,000 mmBTUCliffs. At December 31, 2003, the trust fund assets

C. P. Cranewere $284.9 million.Units 1 and 2 Low ash meltingUnder the Maryland Public Service Commission’s

(combined) . . . 850,000 temperature(Maryland PSC) order regarding the deregulation ofH. A. Wagnerelectric generation, BGE ratepayers must pay a total of

Units 2 and 3 Sulfur content no more$520 million, in 1993 dollars, adjusted for inflation, to(combined) . . . 1,100,000 than 1%decommission Calvert Cliffs through fixed annual

collections of approximately $18.7 million until Coal deliveries to these facilities are made by railJune 30, 2006, and thereafter in an annual amount and barge. The primary source of coal we use isdetermined by reference to specified factors. BGE is produced from mines located in central and northerncollecting this amount on behalf of Calvert Cliffs. Any Appalachia. During 2003, we expanded our coal sourcescosts to decommission Calvert Cliffs in excess of this including restructuring our rail contracts, increasing the$520 million must be paid by Calvert Cliffs. If BGE range of coals we can consume, adding synthetic fuel asratepayers have paid more than this amount at the time an alternate source, and finding potential other coalof decommissioning, Calvert Cliffs must refund the supply sources including shipments from areas includingexcess. If the cost to decommission Calvert Cliffs is less Columbia, Venezuela, and South Africa.than the amount BGE’s ratepayers are obligated to pay, All of the Conemaugh and Keystone plants’ annualCalvert Cliffs may keep the difference. coal requirements are purchased from regional suppliers

The sellers of Nine Mile Point transferred a on the open market by the plant operators. The sulfur$441.7 million decommissioning trust fund at the time restrictions on coal are approximately 2.3% for theof sale. In return, Nine Mile Point assumed all liability Keystone plant and approximately 5.3% for thefor the costs to decommission Unit 1 and 82% of the Conemaugh plant.cost to decommission Unit 2. We believe that thisamount is adequate to cover our responsibility for

7

The annual coal requirements for the ACE, having varying levels of experience, financial and humanJasmin, and POSO plants, which are located in resources, and differing strategies.California, are supplied under contracts with mining We face competition in the market for energy,operators. The Jasmin and POSO plants are restricted capacity, and ancillary services. In our merchant energyto coal with sulfur content less than 4.0% and ACE is business, we compete with international, national, andrestricted to less than 2.0%. regional full service energy providers, merchants and

All of our requirements reflect historical levels. The producers, to obtain competitively priced supplies fromactual fuel quantities required can vary substantially a variety of sources and locations, and to utilize efficientfrom historical levels depending upon the relationship transmission or transportation. We principally competebetween energy prices and fuel costs, weather on the basis of the price, customer service, reliability,conditions, and operating requirements. and availability of our products.

With respect to power generation, we compete inthe operation of energy-producing projects, and ourGascompetitors in this business are both domestic andWe purchase natural gas, storage capacity, andinternational organizations, including various utilities,transportation, as necessary, for electric generation atindustrial companies and independent power producerscertain plants. Some of our gas-fired units can use(including affiliates of utilities), some of which haveresidual fuel oil or distillates instead of gas. Gas isfinancial resources that are greater than ours.purchased under contracts with suppliers on the spot

During the transition of the energy industry tomarket and forward markets, including financialcompetitive markets, it is difficult for us to assess ourexchanges and bilateral agreements. The actual fueloverall position versus the position of existing powerquantities required can vary substantially from year toproviders and new entrants because each company mayyear depending upon the relationship between energyemploy widely differing strategies in their fuel supplyprices and fuel costs, weather conditions, and operatingand power sales contracts with regard to pricing, termsrequirements. However, we believe that we will be ableand conditions. Further difficulties in makingto obtain adequate quantities of gas to meet ourcompetitive assessments of our company arise fromrequirements.states considering different types of regulatory initiativesconcerning competition in the power industry.Oil

Increased competition that resulted from some ofUnder normal burn practices, our requirements forthese initiatives in several states contributed in someresidual fuel oil (No. 6) amount to approximatelyinstances to a reduction in electricity prices and put1.5 million to 2.0 million barrels of low-sulfur oil perpressure on electric utilities to lower their costs,year. Deliveries of residual fuel oil are made from theincluding the cost of purchased electricity. Some statessuppliers’ Baltimore Harbor marine terminal forthat were considering deregulation have slowed theirdistribution to the various generating plant locations.plans or postponed consideration of deregulation. InAlso, based on normal burn practices, we requireaddition, other states are reconsidering deregulation.approximately 5.0 million to 6.0 million gallons of

We believe there is adequate growth potential indistillates (No. 2 oil and kerosene) annually, but thesethe current deregulated market. However, in response torequirements can vary substantially from year to yearregional market differences and to promote competitivedepending upon the relationship between energy pricesmarkets, the Federal Energy Regulatory Commissionand fuel costs, weather conditions, and operating(FERC) proposed initiatives promoting the formation ofrequirements. Distillates are purchased from theRegional Transmission Organizations and a standardsuppliers’ Baltimore truck terminals for distribution tomarket design. If approved, these market changes couldthe various generating plant locations. We haveprovide additional opportunities for our merchantcontracts with various suppliers to purchase oil at spotenergy business.prices, and for future delivery, to meet our

As the economy continues to recover and therequirements.market for commercial and industrial supply continuesto grow, we have experienced increased competition inCompetitionour retail commercial and industrial supply activities.Market developments over the past several years haveThe increase in retail competition may affect thechanged the nature of competition in the merchantmargins that we will realize from our customers.energy business. Certain companies within the merchantHowever, we believe that our experience and expertiseenergy sector have curtailed their activities, withdrawnin assessing and managing risk will help us to remaincompletely from the business, or returned to acompetitive during volatile or otherwise adverse markettraditional utility business. However new competitorscircumstances.(i.e., financial investors) are entering the market. We

encounter competition from companies of various sizes,

8

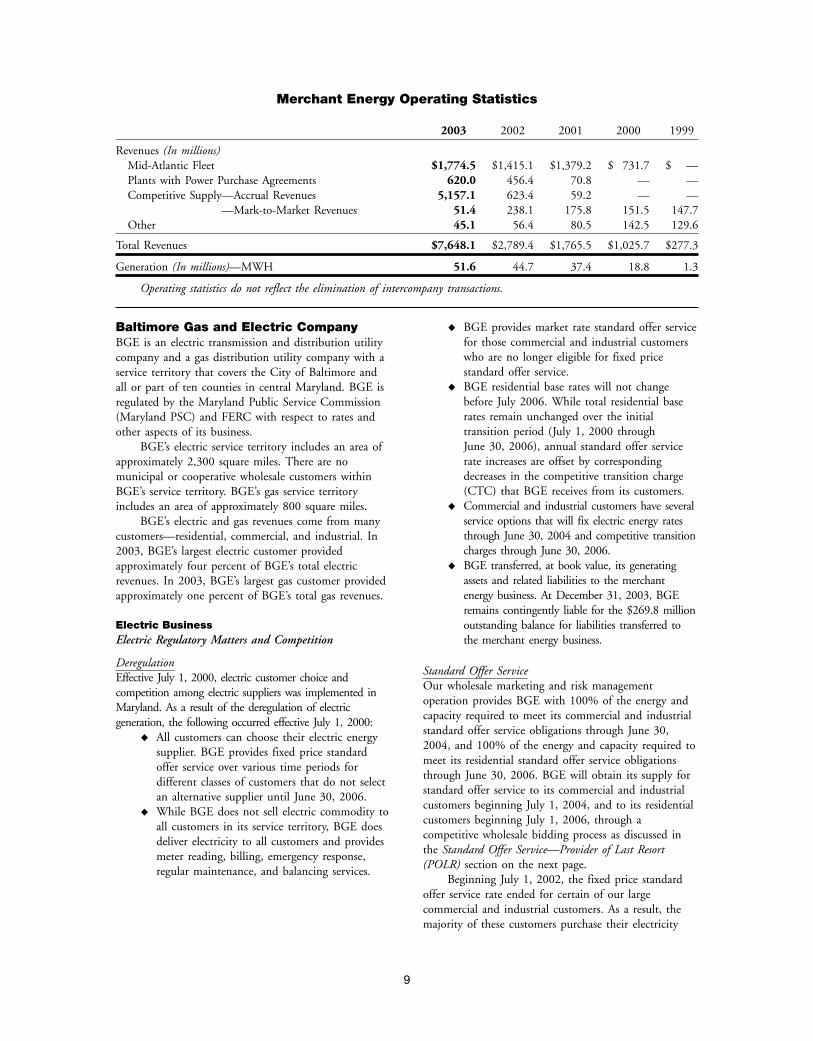

Merchant Energy Operating Statistics

2003 2002 2001 2000 1999

Revenues (In millions)Mid-Atlantic Fleet $1,774.5 $1,415.1 $1,379.2 $ 731.7 $ —Plants with Power Purchase Agreements 620.0 456.4 70.8 — —Competitive Supply—Accrual Revenues 5,157.1 623.4 59.2 — —

—Mark-to-Market Revenues 51.4 238.1 175.8 151.5 147.7Other 45.1 56.4 80.5 142.5 129.6

Total Revenues $7,648.1 $2,789.4 $1,765.5 $1,025.7 $277.3

Generation (In millions)—MWH 51.6 44.7 37.4 18.8 1.3

Operating statistics do not reflect the elimination of intercompany transactions.

♦ BGE provides market rate standard offer serviceBaltimore Gas and Electric Companyfor those commercial and industrial customersBGE is an electric transmission and distribution utilitywho are no longer eligible for fixed pricecompany and a gas distribution utility company with astandard offer service.service territory that covers the City of Baltimore and

♦ BGE residential base rates will not changeall or part of ten counties in central Maryland. BGE isbefore July 2006. While total residential baseregulated by the Maryland Public Service Commissionrates remain unchanged over the initial(Maryland PSC) and FERC with respect to rates andtransition period (July 1, 2000 throughother aspects of its business.June 30, 2006), annual standard offer serviceBGE’s electric service territory includes an area ofrate increases are offset by correspondingapproximately 2,300 square miles. There are nodecreases in the competitive transition chargemunicipal or cooperative wholesale customers within(CTC) that BGE receives from its customers.BGE’s service territory. BGE’s gas service territory

♦ Commercial and industrial customers have severalincludes an area of approximately 800 square miles.service options that will fix electric energy ratesBGE’s electric and gas revenues come from manythrough June 30, 2004 and competitive transitioncustomers—residential, commercial, and industrial. Incharges through June 30, 2006.2003, BGE’s largest electric customer provided

♦ BGE transferred, at book value, its generatingapproximately four percent of BGE’s total electricassets and related liabilities to the merchantrevenues. In 2003, BGE’s largest gas customer providedenergy business. At December 31, 2003, BGEapproximately one percent of BGE’s total gas revenues.remains contingently liable for the $269.8 million

Electric Business outstanding balance for liabilities transferred toElectric Regulatory Matters and Competition the merchant energy business.

DeregulationStandard Offer ServiceEffective July 1, 2000, electric customer choice andOur wholesale marketing and risk managementcompetition among electric suppliers was implemented inoperation provides BGE with 100% of the energy andMaryland. As a result of the deregulation of electriccapacity required to meet its commercial and industrialgeneration, the following occurred effective July 1, 2000:standard offer service obligations through June 30,♦ All customers can choose their electric energy2004, and 100% of the energy and capacity required tosupplier. BGE provides fixed price standardmeet its residential standard offer service obligationsoffer service over various time periods forthrough June 30, 2006. BGE will obtain its supply fordifferent classes of customers that do not selectstandard offer service to its commercial and industrialan alternative supplier until June 30, 2006.customers beginning July 1, 2004, and to its residential♦ While BGE does not sell electric commodity tocustomers beginning July 1, 2006, through aall customers in its service territory, BGE doescompetitive wholesale bidding process as discussed indeliver electricity to all customers and providesthe Standard Offer Service—Provider of Last Resortmeter reading, billing, emergency response,(POLR) section on the next page.regular maintenance, and balancing services.

Beginning July 1, 2002, the fixed price standardoffer service rate ended for certain of our largecommercial and industrial customers. As a result, themajority of these customers purchase their electricity

9

from alternate suppliers, including subsidiaries of June 30, 2004 began in February 2004. The sameConstellation Energy. The remaining large commercial bidding procedures will be used for supplying BGE’sand industrial customers that continue to receive their standard offer service to residential customers for theelectric supply from BGE are charged market-based period after June 30, 2006.standard offer service rates through June 30, 2004. We discuss the market risk of our regulated electric

Beginning July 1, 2004, all other commercial and business in more detail in Item 7. Management’sindustrial customers that receive their electric supply Discussion and Analysis—Market Risksection.from BGE will be charged market-based standard offerservice rates. Beginning July 1, 2006, BGE’s current Electric Load Managementobligation to provide fixed price standard offer service BGE has implemented various programs for use whento residential customers ends and all residential system-operating conditions or market economicscustomers that receive their electric supply from BGE indicate that a reduction in load would be beneficial.will be charged market-based standard offer service We refer to these programs as active load managementrates. programs. These programs include:

♦ customer-owned generation and curtailableStandard Offer Service—Provider of Last Resort (POLR)service for large commercial and industrial

In April 2003, the Maryland PSC approved acustomers,

settlement agreement reached by BGE and parties ♦ air conditioning control for residential andrepresenting customers, industry, utilities, suppliers, the

commercial customers, andMaryland Energy Administration, the Maryland PSC’s ♦ residential water heater control.Staff, and the Office of People’s Counsel which, among

BGE generally activates these programs on summerother things, extends BGE’s obligation to supply

days when demand and/or wholesale prices are relativelystandard offer service for a second transition period.

high. The reduction in the summer 2003 peak loadUnder the settlement agreement, BGE is obligated to

from active load management was approximatelyprovide market-based standard offer service to

342 MW.residential customers until June 30, 2010, and forcommercial and industrial customers for one, two or

Transmission and Distribution Facilitiesfour year periods beyond June 30, 2004, depending onBGE maintains approximately 250 substations andcustomer load. The POLR rates charged during this1,300 circuit miles of transmission lines throughouttime will recover BGE’s wholesale power supply costscentral Maryland. BGE also maintains nearly 22,900and include an administrative fee.circuit miles of distribution lines. The transmissionIn September 2003, the Maryland PSC approved afacilities are connected to those of neighboring utilitysecond settlement agreement. This phase deals with thesystems as part of the PJM Interconnection. Under thebid procurement process that utilities must follow toPJM Tariff and various agreements, BGE and otherobtain wholesale power supply to serve retail customersmarket participants can use regional transmissionon standard offer service during the second transitionfacilities for energy, capacity and ancillary servicesperiod. The settlement contains a model request fortransactions including emergency assistance.proposals, a model wholesale power supply contract,

We discuss FERC’s initiatives in implementing aand various requirements pertaining to, among otherstandard market design for wholesale electric markets inthings, bidder qualifications and bid evaluation criteria.more detail in Item 7. Management’s Discussion andBidding to supply BGE’s standard offer service toAnalysis—FERC Regulation section.commercial and industrial customers beyond

10

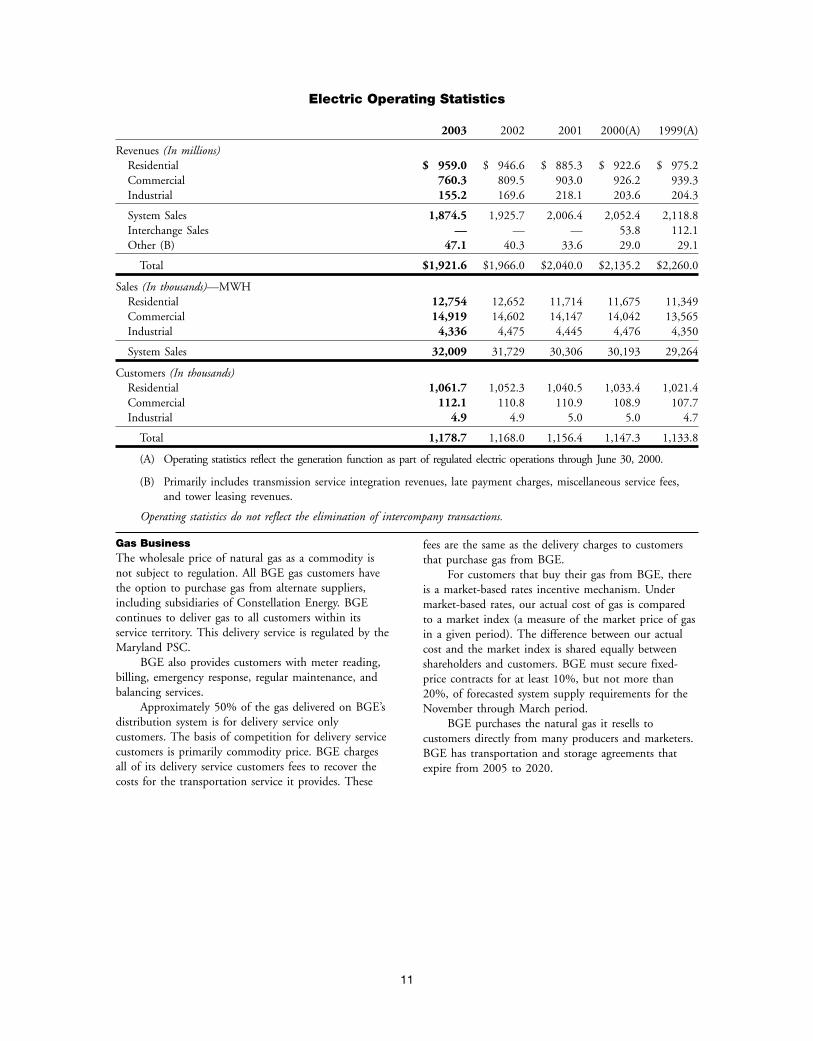

Electric Operating Statistics

2003 2002 2001 2000(A) 1999(A)

Revenues (In millions)Residential $ 959.0 $ 946.6 $ 885.3 $ 922.6 $ 975.2Commercial 760.3 809.5 903.0 926.2 939.3Industrial 155.2 169.6 218.1 203.6 204.3

System Sales 1,874.5 1,925.7 2,006.4 2,052.4 2,118.8Interchange Sales — — — 53.8 112.1Other (B) 47.1 40.3 33.6 29.0 29.1

Total $1,921.6 $1,966.0 $2,040.0 $2,135.2 $2,260.0

Sales (In thousands)—MWHResidential 12,754 12,652 11,714 11,675 11,349Commercial 14,919 14,602 14,147 14,042 13,565Industrial 4,336 4,475 4,445 4,476 4,350

System Sales 32,009 31,729 30,306 30,193 29,264

Customers (In thousands)Residential 1,061.7 1,052.3 1,040.5 1,033.4 1,021.4Commercial 112.1 110.8 110.9 108.9 107.7Industrial 4.9 4.9 5.0 5.0 4.7

Total 1,178.7 1,168.0 1,156.4 1,147.3 1,133.8

(A) Operating statistics reflect the generation function as part of regulated electric operations through June 30, 2000.

(B) Primarily includes transmission service integration revenues, late payment charges, miscellaneous service fees,and tower leasing revenues.

Operating statistics do not reflect the elimination of intercompany transactions.

Gas Business fees are the same as the delivery charges to customersThe wholesale price of natural gas as a commodity is that purchase gas from BGE.not subject to regulation. All BGE gas customers have For customers that buy their gas from BGE, therethe option to purchase gas from alternate suppliers, is a market-based rates incentive mechanism. Underincluding subsidiaries of Constellation Energy. BGE market-based rates, our actual cost of gas is comparedcontinues to deliver gas to all customers within its to a market index (a measure of the market price of gasservice territory. This delivery service is regulated by the in a given period). The difference between our actualMaryland PSC. cost and the market index is shared equally between

BGE also provides customers with meter reading, shareholders and customers. BGE must secure fixed-billing, emergency response, regular maintenance, and price contracts for at least 10%, but not more thanbalancing services. 20%, of forecasted system supply requirements for the

Approximately 50% of the gas delivered on BGE’s November through March period.distribution system is for delivery service only BGE purchases the natural gas it resells tocustomers. The basis of competition for delivery service customers directly from many producers and marketers.customers is primarily commodity price. BGE charges BGE has transportation and storage agreements thatall of its delivery service customers fees to recover the expire from 2005 to 2020.costs for the transportation service it provides. These

11

BGE’s current pipeline firm transportation during the summer months for operations of itsentitlements to serve BGE’s firm loads are 284,053 liquefied natural gas facility during winter emergencies.dekatherms (DTH) per day during the winter period BGE historically has been able to arrangeand 259,053 DTH per day during the summer period. short-term contracts or exchange agreements with other

BGE’s current maximum storage entitlements are gas companies in the event of short-term disruptions to235,080 DTH per day. To supplement its gas supply at gas supplies or to meet additional demand.times of heavy winter demands and to be available in BGE also participates in the interstate markets bytemporary emergencies affecting gas supply, BGE has: releasing pipeline capacity or bundling pipeline capacity

♦ a liquefied natural gas facility for the with gas for off-system sales. Off-system gas sales areliquefaction and storage of natural gas with a low-margin direct sales of gas to wholesale suppliers oftotal storage capacity of 1,092,977 DTH and a natural gas outside BGE’s service territory. Earningsdaily capacity of 311,500 DTH, and from these activities are shared between shareholders

♦ a propane air facility with a mined cavern with and customers. BGE makes these sales as part of aa total storage capacity equivalent to 564,200 program to balance our supply of, and cost of, naturalDTH and a daily capacity of 85,000 DTH. gas.

BGE has under contract sufficient volumes ofpropane for the operation of the propane air facility andis capable of liquefying sufficient volumes of natural gas

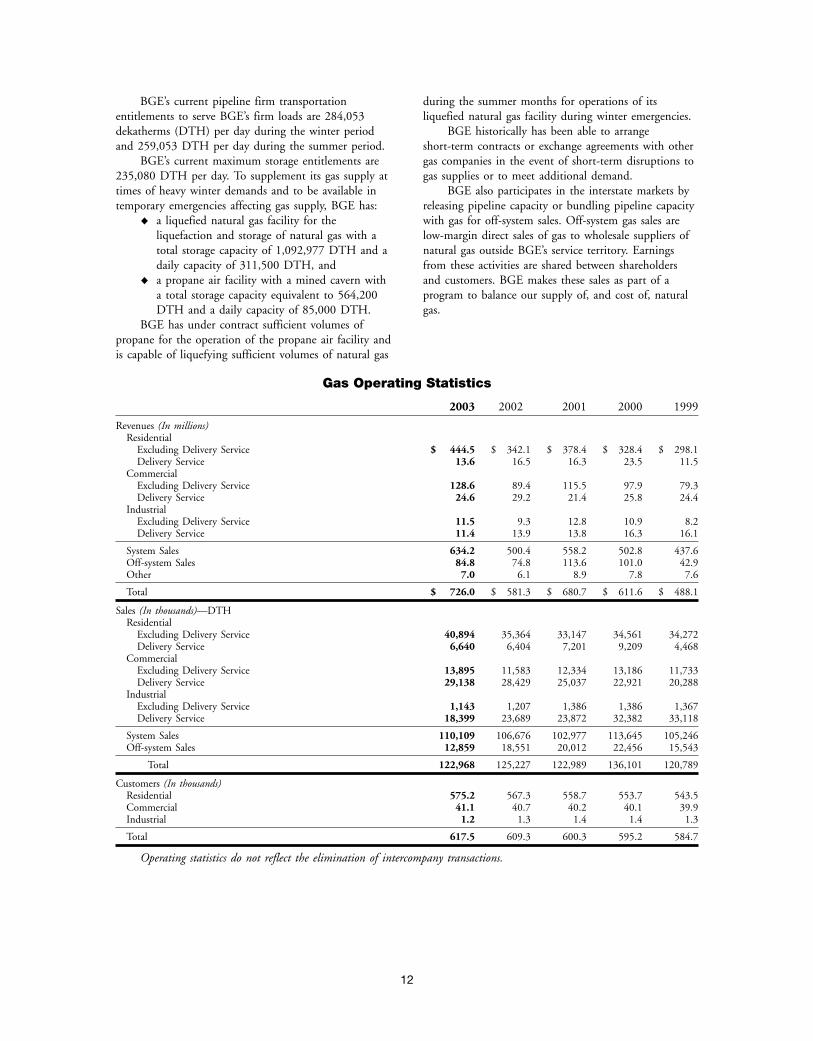

Gas Operating Statistics

2003 2002 2001 2000 1999

Revenues (In millions)Residential

Excluding Delivery Service $ 444.5 $ 342.1 $ 378.4 $ 328.4 $ 298.1Delivery Service 13.6 16.5 16.3 23.5 11.5

CommercialExcluding Delivery Service 128.6 89.4 115.5 97.9 79.3Delivery Service 24.6 29.2 21.4 25.8 24.4

IndustrialExcluding Delivery Service 11.5 9.3 12.8 10.9 8.2Delivery Service 11.4 13.9 13.8 16.3 16.1

System Sales 634.2 500.4 558.2 502.8 437.6Off-system Sales 84.8 74.8 113.6 101.0 42.9Other 7.0 6.1 8.9 7.8 7.6

Total $ 726.0 $ 581.3 $ 680.7 $ 611.6 $ 488.1

Sales (In thousands)—DTHResidential

Excluding Delivery Service 40,894 35,364 33,147 34,561 34,272Delivery Service 6,640 6,404 7,201 9,209 4,468

CommercialExcluding Delivery Service 13,895 11,583 12,334 13,186 11,733Delivery Service 29,138 28,429 25,037 22,921 20,288

IndustrialExcluding Delivery Service 1,143 1,207 1,386 1,386 1,367Delivery Service 18,399 23,689 23,872 32,382 33,118

System Sales 110,109 106,676 102,977 113,645 105,246Off-system Sales 12,859 18,551 20,012 22,456 15,543

Total 122,968 125,227 122,989 136,101 120,789

Customers (In thousands)Residential 575.2 567.3 558.7 553.7 543.5Commercial 41.1 40.7 40.2 40.1 39.9Industrial 1.2 1.3 1.4 1.4 1.3

Total 617.5 609.3 600.3 595.2 584.7

Operating statistics do not reflect the elimination of intercompany transactions.

12

FranchisesBGE has nonexclusive electric and gas franchises to use sufficient to permit them to engage in their presentstreets and other highways that are adequate and business. Conditions of the franchises are satisfactory.

Other Nonregulated BusinessesDistrict Cooling ServicesEnergy Products and ServicesWe provide cooling services using a central chilled waterWe offer energy products and services designeddistribution system to commercial and municipalprimarily to provide solutions to the energy needs ofcustomers in the City of Baltimore.commercial and industrial customers. These energy

products and services include:Other♦ designing, constructing, and operating heating,Our other nonregulated businesses include investmentscooling, and cogeneration facilities,that we do not consider to be core operations. These♦ energy consulting and power-quality services,include financial investments, real estate projects, and♦ services to enhance the reliability of individualinterests in a Latin American distribution project and inelectric supply systems, anda fund that holds interests in two South American♦ customized financing alternatives.energy projects. While our intent is to dispose of theseassets, market conditions and other events beyond ourHome Products and Gas Retail Marketingcontrol may affect the actual sale of these assets. InWe offer services to customers including:addition, a future decline in the fair value of these♦ home improvements,assets could result in additional losses.♦ the service of heating, air conditioning,

plumbing, electrical, and indoor air qualitysystems, and

♦ natural gas retail marketing to residentialcustomers.

Consolidated Capital RequirementsWe continuously review and change our capitalOur total capital requirements for 2003 were

expenditure programs, so actual expenditures may vary$761 million. Of this amount, $472 million was usedfrom the estimate above. We discuss our capitalin our nonregulated businesses and $289 million wasrequirements further in Item 7. Management’s Discussionused in our utility operations. We estimate our totaland Analysis—Capital Resources section.capital requirements to be $760 million in 2004.

Environmental MattersOur activities require complex and often lengthyWe are subject to regulation by various federal, state,

processes to obtain approvals, permits, or licenses forand local authorities with regard to:new, existing, or modified facilities. Additionally, the♦ air quality,use and handling of various chemicals or hazardous♦ water quality, andmaterials (including wastes) requires preparation of♦ disposal of hazardous substances.release prevention plans and emergency responseThe development (involving site selection,procedures. We continuously monitor federal and stateenvironmental assessments, and permitting),environmental initiatives in order to provide input asconstruction, acquisition, and operation of electricwell as to maintain a proactive view of the future whichgenerating and distribution facilities are subject tois key to effective strategic planning. Additionally, asextensive federal, state, and local environmental andnew laws or regulations are promulgated, we assess theirland use laws and regulations. From the beginningapplicability and implement the necessary modificationsphases of siting and developing, to the ongoingto our facilities or their operation, as required.operation of existing or new electric generating and

Our capital expenditures (excluding allowance fordistribution facilities, our activities involve compliancefunds used during construction) were approximatelywith diverse laws and regulations that address emissions$260 million during the five-year period 1999-2003 toand impacts to air and water, special, protected andcomply with existing environmental standards andcultural resources (such as wetlands, endangered species,regulations.and archeological/historical resources), chemical, and

waste handling and noise impacts.

13

Clean Air Act the area failed to meet the deadline. The exact methodThe Clean Air Act affects both existing generating of computing these fees has not been established andfacilities and new projects. The Clean Air Act and will depend in part on state implementing regulationsmany state laws impose significant requirements relating that have not been finalized.to emissions of sulfur dioxide (SO2), nitrogen oxide The current deadline for most severe(NOx), particulate matter, and other pollutants that nonattainment areas is 2005, including those in whichresult from burning fossil fuels. The Clean Air Act also our generating facilities are located. Assessment of feescontains other provisions that could materially affect would commence in 2006 if the current effective date issome of our projects. Various provisions may require maintained. However, there is significant uncertaintypermits, inspections, or installation of additional regarding the date when fees would be assessed in lightpollution control technology or may require the of pending federal legislation and anticipated EPApurchase of emission allowances. Certain of these rulemaking. Currently, we are unable to estimate theprovisions are described in more detail below. ultimate timing or financial impact of the standard in

On October 27, 1998, the Environmental light of the uncertainty surrounding its effective dateProtection Agency (EPA) issued a rule requiring 22 and the methodology that will be used in calculatingEastern states and the District of Columbia to reduce the fees.emissions of NOx. The EPA rule requires states to The EPA and several states have filed suits againstimplement controls sufficient to meet their NOx budget a number of coal-fired power plants in Mid-Westernby May 30, 2004. However, the Northeast states and Southern states alleging violations of the Preventiondecided to require compliance in 2003. Coal-fired of Significant Deterioration and non-attainmentpower plants are a principal target of NOx reductions provisions of the Clean Air Act’s new source reviewunder this initiative. requirements. The EPA requested information relating

Many of our generation facilities are subject to NOx to modifications made to our Brandon Shores, Crane,reduction requirements under the EPA rule, including and Wagner plants in Baltimore, Maryland. The EPAthose located in Maryland and Pennsylvania. At the also sent similar, but narrower, information requests toBrandon Shores and Wagner facilities, we installed two of our newer Pennsylvania waste-coal burningemission reduction equipment for our coal-fired units to plants. We have responded to the EPA, and as of themeet Maryland regulations issued pursuant to the EPA’s date of this report the EPA has taken no further action.rule. The owners of the Keystone plant in Pennsylvania Based on the level of emissions control that the EPAcompleted the installation of emissions reduction and states are seeking in these new source reviewequipment by July 2003 to meet Pennsylvania regulations enforcement actions, we believe that material additionalissued pursuant to the EPA’s rule. Our total cost of the costs and penalties could be incurred if the EPA wasemissions reduction equipment at the Keystone plant was successful in any future actions regarding our facilities.approximately $37 million. On October 27, 2003, the EPA’s new source review

The EPA established new National Ambient Air rule on routine maintenance was published in the FederalQuality Standards for very fine particulates and revised Register. The new regulations would establish anstandards for ozone attainment that were upheld after equipment replacement cost threshold for determiningvarious court appeals. While these standards may when major new source review requirements are triggered.require increased controls at some of our fossil Plant owners may spend up to 20% of the replacementgenerating plants in the future, implementation could value of a generation unit on certain improvements eachbe delayed for several years. We cannot estimate the year without triggering requirements for new pollutioncost of these increased controls at this time because the controls. Parties had until December 26, 2003, thestates, including Maryland, Pennsylvania, and effective date of the rule, to appeal the agency’s decision inCalifornia, still need to determine what reductions in court. An appeal was filed with the United States Court ofpollutants will be necessary to meet the EPA standards. Appeals. The effective date of the rule has been delayed

We may be impacted by the EPA’s designation of pending review.certain areas as severe ozone nonattainment areas. These The Clean Air Act required the EPA to evaluateare areas where air pollution levels severely exceed the public health impacts of emissions of mercury, anational air quality standards. We own several hazardous air pollutant, from coal-fired plants. The EPAgenerating facilities in severe ozone nonattainment areas decided to control mercury emissions from coal-firedin Maryland and California. The Clean Air Act requires plants. On December 15, 2003, the EPA proposed twostates to assess fees against every major stationary source alternatives for controlling mercury emissions fromof NOx and volatile organic chemicals in severe ozone generating facilities. The EPA may require thenonattainment areas if national air quality standards are installation of mercury reduction equipment.not achieved by a specified deadline. If implemented, Alternatively, the EPA may revise standards to allow forthe fee would be assessed based on the magnitude of a the purchase of allowances. Compliance could besource’s emissions as compared to its emissions when required as soon as 2007, or by 2010 depending on

14

which alternative is selected. We believe final regulations Metal Bankcould be issued in 2004 and could affect all oil-fired In the early 1970s, BGE shipped an unknown numberand coal-fired boilers. The cost of compliance with the of scrapped transformers to Metal Bank of America, afinal regulations could be material. metal reclaimer in Philadelphia. Metal Bank’s scrap and

Future initiatives regarding greenhouse gas storage yard has been found to be contaminated withemissions and global warming continue to be the oil containing high levels of PCBs (hazardous chemicalssubject of much debate. As a result of our diverse fuel frequently used as a fire resistant coolant in electricalportfolio, our contribution to greenhouse gases varies by equipment). On December 7, 1987, the EPA notifiedplant type. Fossil fuel-fired power plants are significant BGE and nine other utilities that they are consideredsources of carbon dioxide emissions, a principal potentially responsible parties (PRPs) with respect to thegreenhouse gas. Our compliance costs with any clean-up of the site. BGE, along with the other PRPs,mandated federal greenhouse gas reductions in the submitted a remedial investigation and feasibility studyfuture could be material. to the EPA on October 14, 1994, and the EPA issued

its Record of Decision (ROD) recommending clean-upClean Water Act for the site on December 31, 1997. On June 26, 1998,Our facilities are subject to a variety of federal and state the EPA ordered BGE, the other utility PRPs, and theregulations governing existing and potential water/ owner/operator to implement the requirements of thewastewater and storm water discharges. ROD. The utility PRPs have submitted the remedial

In April 2002, the EPA proposed rules under the design to EPA. Based on the ROD, BGE’s share of theClean Water Act that require that cooling water intake reasonably possible clean-up costs, estimated to bestructures reflect the best technology available for approximately 15.47%, could be as much asminimizing adverse environmental impacts. In February $1.3 million higher than amounts we believe are2004, the proposed rules were finalized. The final rules probable and have recorded as a liability in ourrequire the installation of additional intake screens or Consolidated Balance Sheets.other protective measures, as well as extensivesite-specific study and monitoring requirements. We are Kane and Lombard Streetscurrently reviewing the final rules and their potential A suit was originally filed by the EPA under CERCLAimpact to us. Our compliance costs associated with the in October 1989 against BGE and several otherfinal rules could be material. defendants in the U.S. District Court for the District of

Under current provisions of the Clean Water Act, Maryland, seeking to recover past and future clean-upexisting permits must be renewed at least every five costs at the Kane and Lombard Street site located inyears, at which time permit limits come under extensive Baltimore City, Maryland. The State of Maryland filedreview and can be modified to account for more a similar complaint in the same case and court instringent regulations. In addition, the permits can be February 1990. The complaints alleged that BGEmodified at any time. Changes to the water discharge arranged for coal fly ash to be deposited on the site.permits of our coal or other fuel suppliers due to The Court dismissed these complaints infederal or state initiatives may increase the cost of fuel, November 1995. Maryland began additionalwhich in turn could have a significant impact on our investigation on the remainder of the site for the EPA,operations. but never completed the investigation. BGE, along with

three other defendants, agreed to complete a remedialComprehensive Environmental Response, investigation and feasibility study of groundwaterCompensation and Liability Act (Superfund contamination around the site in a July 1993 consentstatute) order. The remedial investigation report and a draftThis law, or CERCLA, among other things, imposes feasibility study were submitted to the EPA inclean-up requirements for threatened or actual releases February 2002. In December 2002, the EPA released itsof hazardous wastes that may endanger public health or proposed remedy for the site and estimated the totalwelfare of the environment. Under CERCLA, joint and clean-up cost for the site to be $6.2 million.several liability may be imposed on waste generators, The EPA issued its ROD for the Kane andsite owners and operators and others regardless of fault Lombard Drum site on September 30, 2003. The RODor the legality of the original disposal activity. Many specifies the clean-up plan for the site, consisting ofstates have enacted laws similar to CERCLA. Although enhanced reductive dechlorination, a soil managementmost wastes generated by our facilities are generally not plan, and institutional controls. The ROD wasregarded as hazardous wastes, some products used in the consistent with the proposed remedy the EPA releasedoperations and the disposal of those materials are in December 2002. We expect the EPA to approach thegoverned by CERCLA and similar state statutes. potentially responsible parties regarding implementation

of the plan in 2004. The total clean-up costs are

15

estimated to be $7.3 million. We estimate our current Environment that required BGE to implement remedialshare of site-related costs to be 11.1% of the action plans for contamination at and around the$7.3 million. Our share of these future costs has not Spring Gardens site. BGE submitted the requiredbeen determined and it may vary from the current remedial action plans, and they have been approved byestimate. In December 2002, we recorded a liability in the Maryland Department of the Environment. Basedour Consolidated Balance Sheets for our share of the on these plans, the costs BGE considers to be probableclean-up costs that we believe is probable. to remedy the contamination are estimated to total

$47 million. BGE recorded these costs as a liability inits Consolidated Balance Sheets and deferred these costs,68th Street Dumpnet of accumulated amortization and amounts itIn July 1999, the EPA notified BGE, along with 19recovered from insurance companies, as a regulatoryother entities, that it may be a potentially responsibleasset. Through December 31, 2003, BGE spentparty at the 68th Street Dump/Industrial Enterprisesapproximately $39 million for remediation at this site.Site, also known as the Robb Tyler Dump, located in

BGE also is required by accounting rules toBaltimore, Maryland. The EPA indicated that it isdisclose additional costs it considers to be less likelyproceeding with plans to conduct a remedialthan probable, but still ‘‘reasonably possible’’ of beinginvestigation and feasibility study. In April 2003, EPAincurred at this site. Based on the results of studies atre-proposed the 68th Street site for listing as a federalthis site, it is reasonably possible that these additionalSuperfund site, but decided not to include the site incosts could exceed the $47 million BGE recognized byits September 2003 update. BGE and other potentiallyapproximately $14 million.responsible parties are pursuing alternatives to listing as