Consolidated Financial Statements - Itaú...

88

1 Consolidated Financial Statements 1 st Quarter 2001

Transcript of Consolidated Financial Statements - Itaú...

11111

ConsolidatedFinancial

Statements1st Quarter 2001

2

Management Report

To our Stockholders:

We are pleased to present the Management Report andfinancial statements of Banco Itaú S.A. and its controlledcompanies for the first quarter of 2001 in accordance withthe regulations established by the Central Bank of Brazil(BACEN) and the Brazilian Securities and ExchangeCommission (Comissão de Valores Mobiliários) - CVM.

Relevant Events

Note of Condolence

It is with great sadness that we have to report the death on April18, 2001 of Dr. Eudoro Villela, Vice-chairman of the AdministrativeCouncil of Banco Itaú and Chairman of the Administrative Councilof Itaúsa, the holding company of the Itaú Group. Dr. Villellaplayed a key role as Chairman of Itaú between 1961 and 1975,and also as founder of Duratex S.A. and as an active counselor ofone of the largest companies in the Group.

His biography is one of impressive achievements in businessand medicine, having ren-dered important services to thecommunity in medical research. Particularly notable was Dr.Villela's time at the Curie Foundation, where he worked underthe direct guidance of Madame Curie herself.

In recognizing the debt of gratitude we owe to him, we cannotunderestimate the immense loss his absence will mean to allof us.

Changes in the Administrative Council

On April 23, 2001, at the Annual General Meeting and theExtraordinary General Meeting, tributes were paid to Dr. EudoroVillela, whose dedication and work for the Bank were un-derlined. A portrait of this leading figure in the Group's historywas unveiled in the stock-holders' meeting room and it wasfurther decided to name the fifth office block of the CEI -Centro Empresarial Itaúsa (The Itaúsa Business Center) - tobe occupied by Banco Itaú - after Dr Villela.

The Administrative Council will be strengthened by theelection of new well-known mem-bers with no previousconnections to the organization and prominent in their fieldsof busi-ness: Pérsio Arida, with a PhD from the MassachussetsInstitute of Technology and an ex-president of the CentralBank of Brazil and Roberto Teixeira da Costa, economist andfirst president of the CVM.

José Vilarasau Salat, president of the Caja de Ahorros yPensiones de Barcelona ("la Caixa") - with a 3% stake in Itaú- also becomes a member of the Administrative Council.

The contribution of these new members is a clear indicationof the priority the Bank is plac-ing on its model of corporategovernance, which is line with modern methods of administra-tion and underlines the importance placed on the creationof stockholder value.

Alfredo Egydio Arruda Villela Filho and Roberto Egydio Setubalwere elected as vice-chairmen of the Administrative Council.

Tributes were also paid to Counselors Mauricio Libânio Villelaand Jairo Cupertino, retiring members of the Council, bothof whom have contributed much to the development of theBank.

Creation of a Specialized Structure for SmallBusinesses

Banco Itaú has set up a Small Business Unit (UPE) to providespecialized services in the small business segment (sales ofup to R$ 4 million). Plans have been made to establishexclusive areas in the branches located in the principalBrazilian cities to provide complete privacy and a tailor madeservice.

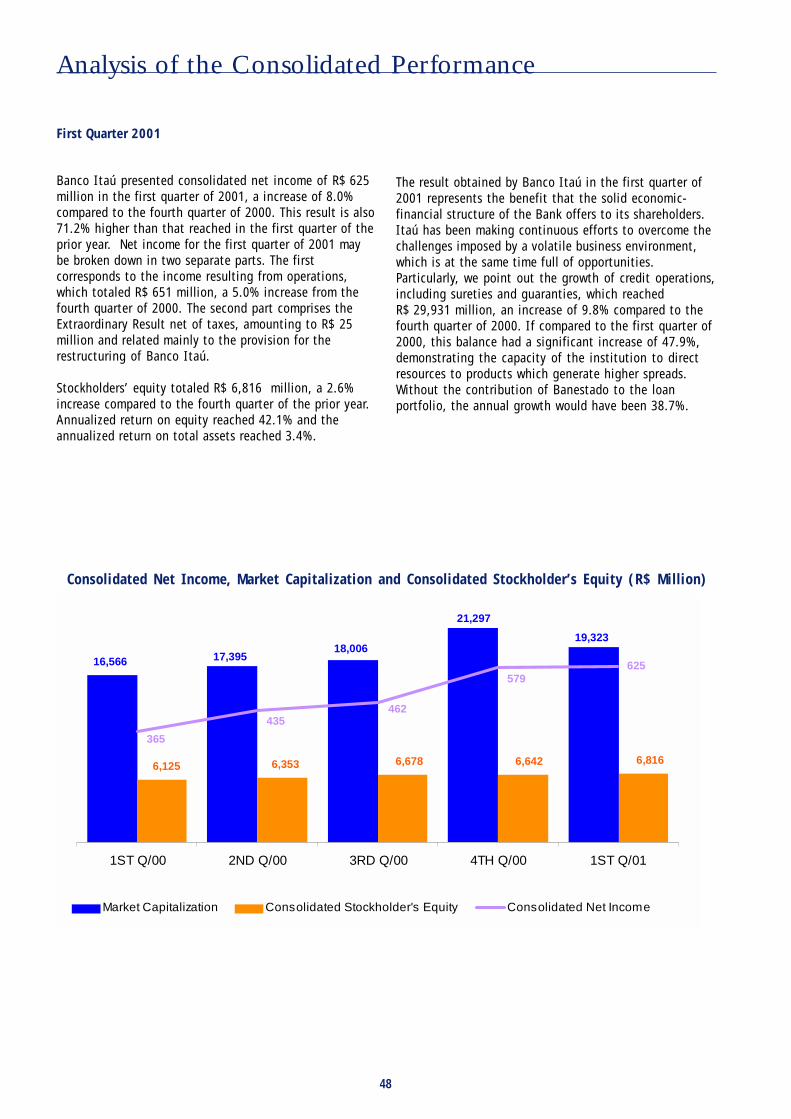

Results, Stockholders' Equity and MarketCapitalization

Banco Itaú posted an accumulated net income on aconsolidated basis of R$625 million for the quarter, anannualized return on consolidated stockholders' equity of42.1% and growth of 71.2% compared to the same period in2000. This profit incorporates the positive impact of R$154million, a reflection of the exchange rate gain (10.6%) netof the basic Selic inter-est rate (3.6%) on unhedged overseasinvestments.

Consolidated net income per batch of one thousand shareswas R$5.51 a year on year growth of 77.7% (and 9.6%compared to the fourth quarter 2000). The book value wasR$60.06. The consolidated stockholders' equity was R$6,816million, an evolution of 11.3% in relation to March 2000(2.6% over December 2000).

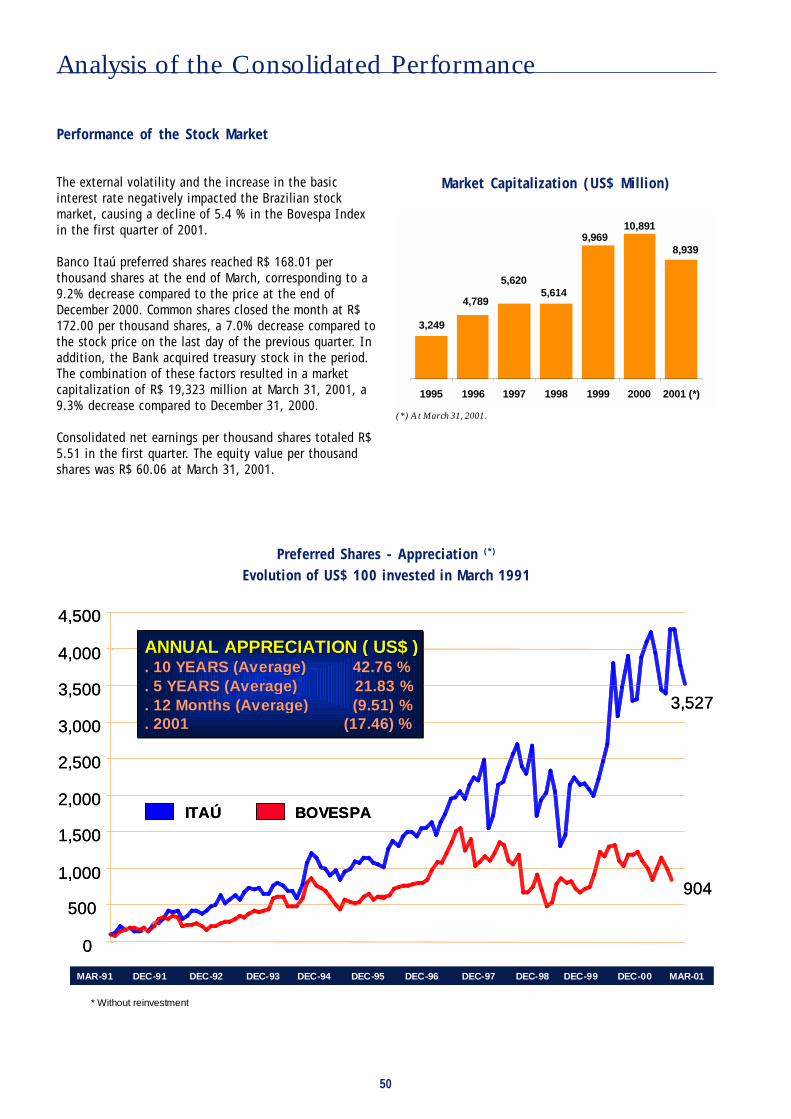

Banco Itaú's preferred shares traded at R$168.01 per batchof one thousand shares at the end of the first quarter 2001,an appreciation of 8.4% against a depreciation of 19.0%registered by the Bovespa index compared with March 2000.Thanks to this, market capitalization totaled R$19,323 million(US$8,939 million), the largest among the entire universe ofLatin American banks.

Third Party Funding and Fund Management

At the end of the period, Itaú reported R$103,422 million inconsolidated own free funds plus those funded from thirdparties or managed by the bank 33.7% higher than in March2000 (4.6% over the period ending December 2000). Of thistotal, R$44,366 million corre-sponded to mutual funds andother managed funds which in turn grew by 30.0%.

During the quarter, the Bank raised a total of US$766 millionin the international capital markets, of particular note beingan 18 month Eurobond issue amounting to US$125 mil-lion

First quarter 2001

3

Management Report

and a Syndicated Loan Facility of US$275 million withmaturities of one and three years.

Assets and Loans

Itaú's consolidated assets were R$74,563 million at the endof the quarter, an increase of 37.8% over March 2000 (and7.2% compared to December 2000).

The credit portfolio grew by 47.9% over March 2000 (9.8%compared to December 2000). The portfolio of majorcorporates continued to grow strongly reporting an increaseof 48.7% over March 2000 (14.2% compared to December2000). The small business and middle market portfolio grewby 68.8% over March 2000 (-3.1%, compared to December2000). The private individual credit segment posted anincrease of 79.2% over March 2000 (20.5% over December2000), with a particularly strong demand coming frompersonal credit operations and consumer goods finance.

There was a 6.0% increase in the number of credit cardsissued while the number of clients accessing the bank viahome or office banking rose by 11.2%. The Itaú-AOL, servicelaunched in January had already surpassed 100,000subscribers by the end of the quarter.

The International structure continued to operate on the basisof separate structures for trade finance and operations fundedthrough overseas lines of credit. The consolidatedportfolio amounted to R$5,603 million (US$ 2,592 million),an increase of 41.5% in relation to March 2000.

Credit portfolio quality remained unchanged. Managementadopted a conservative policy and opted to increase the excessprovision for overdue credits by R$27 million to R$630million. The cost of provisioning for overdue credits fellcompared to the previous quarter in spite of the overallincrease in the outstanding balance of the portfolio.

Insurance, Private Pension Plans andCapitalization

Itauseg and its subsidiaries posted a net income of R$38million for the quarter, an annual-ized return of 23.3%.Earnings from insurance premiums registered R$375 millionwhile technical reserves stood at R$942 million. Itauseg'sclaims index was 59.6%, against 60.9% posted for the sameperiod in 2000. Thanks to this, the combined ratio was 93.2%,an improvement of 4.3 percentage points.

Itaucap and Itauprev posted technical reserves at the end ofthe period of R$821 million and R$971 million, respectively.

International Presence

Banco Itaú Buen Ayre (IBA) closed the period with US$728million in assets and US$319 million in loans. Due to theArgentine economic crisis and a revision of the Bank's creditportfolio using risk management monitoring, IBA decided toadopt a more restrictive ap-proach to credit. This decisionhowever, in no way reflected any relevant event related to adeterioration in the bank's credit portfolio. IBA continues tohave an extremely low expo-sure to the public sector andenjoy very high levels of liquidity. Deposits were US$510mil-lion, an increase of 3.5% over the same period in 2000.

Banco Itaú Europa, S.A. (BIE), controlled by Itaúsa Portugaland regulated by the Bank of Portugal, continues to focuson trade finance and provide support to European companiesinvesting in Brazil. The bank closed the quarter with totalassets of Eur. 1,686 million (US$1,483 million) andstockholders' equity of Eur. 194 million (US$171 million), ayear-on-year growth of 37.3% and 6.7%, respectively. Netincome was Eur. 5 million (US$4 million), an increase of69.3%, representing an annualized return of 10.9% onstockholders' equity.

Banco Itaú Europa Luxembourg, also controlled by Itaúsa Portugaland regulated by the Central Bank of Luxembourg, - a bankwhich operates exclusively in the area of private banking -reported net profits of Eur. 1.9 million (US$1.7 millions) withan annualized return of 28.8% on stockholders' equity. Totalfunds managed by the Bank were in excess of US$796 million.

Human Resources

Payroll (fixed and variable) together with labor charges andfringe benefits amounted to R$612 million. Of this amount,spontaneous benefits were R$34 million, the most notableitem of which were contributions to the SupplementaryPension Plan provided by the Itaubanco Foundation at a totalcost in the quarter of R$7 million.

Acknowledgements

We wish to thank our stockholders and clients for the supportand trust which are indispensable for Itaú's continueddevelopment. To our employees and service suppliers, wealso wish to express our appreciation for their endeavor, whichhas enabled the Bank to achieve outstanding results inaddition to the constant improvement in our products andservices.

(Approved at the Meeting of the AdministrativeCouncil of May 2, 2001)

4

Board of Directors

Administrative Council

Chairman

Olavo Egydio Setubal

Vice Chairmen

Alfredo Egydio Arruda Villela Filho (*)

Eudoro Villela (in Memoriam)

José Carlos Moraes Abreu

Roberto Egydio Setubal

Directors

Ana Lúcia de Mattos Barretto Villela

Carlos da Câmara Pestana

Henri Penchas

Jairo Cupertino

José Vilarasau Salat (*)

Luiz Assumpção Queiroz Guimarães

Luiz de Moraes Barros

Maria de Lourdes Egydio Villela

Maurício Libanio Villela

Pérsio Arida (*)

Roberto Teixeira da Costa (*)

Sergio Silva de Freitas

Executive Board

I - Executive Committee

President and CEO

Roberto Egydio Setubal

Senior Vice Presidents

Henri Penchas

Sergio Silva de Freitas

Executive Vice Presidents

Alberto Dias de Mattos Barretto

Alfredo Egydio Setubal

Antonio Jacinto Matias

Humberto Fábio Fischer Pinotti

Milton Luís Ubach Monteiro

Renato Roberto Cuoco

Legal Advisor

Luciano da Silva Amaro

Executive Officers

Antonio Carlos Barbosa De Oliveira

João Jacó Hazarabedian

Luiz Cristiano de Lima Alves

Rodolfo Henrique Fischer

Ronald Anton de Jongh

Ruy Villela Moraes Abreu

Silvio Aparecido de Carvalho

II - Managing Directors

Senior Managing Directors

Carlos Henrique Mussolini

Cláudio Rudge Ortenblad

Marco Ambrogio Crespi Bonomi

Osvaldo do Nascimento

Paulo Roberto Soares

Managing Directors

Alberto Fernandes

Aldous Albuquerque Galletti

Alexandre de Barros

Alexandre Zákia Albert

Aluísio Paulino da Costa

Anibal Malgueiro Moreira

Antonio Carlos Morelli

Antonio Pedro da Costa

Antonio Sivaldi Roberti Filho

Arnaldo Pereira Pinto

Dieter Rudloff (*)

Edelver Carnovali

Fernando Antonio Neves Lima

Fernando de Assis Pereira

Gian Paolo Aslan

Heli de Andrade

Hitoshi Suzuki

Jackson Ricardo Gomes

Jaime Augusto Chaves

João Antonio Dantas Bezerra Leite

João Batista Videira Martins

João Costa

Joaquim Marcondes De Andrade Westin

José Antonio Lopes

José Caruso Cruz Henriques

5

Board of Directors

José Cláudio Arouca

José Geraldo Borges Ferreira

José Valério Macucci (*)

Júlio Abel de Lima Tabuaço

Luiz Antonio Fernandes Valente

Luiz Antonio Nogueira de França

Luiz Antonio Ribeiro

Luiz Antonio Rodrigues

Luiz Eduardo Zago

Luiz Fernando de Assumpção Faria

Luiz Henrique Campíglia

Manoel Antonio Granado

Marcelo Habice da Motta

Marco Antonio Antunes

Marco Antonio Monteiro Sampaio

Marcus Aurélio Mangini

Maria Cristina Lass

Maria Elizabete Vilaça Lopes

Marta Alves

Máximo Hernández González

Paschoal Pipolo Baptista

Patrick Pierre Delfosse

Pedro de Alcântara Nabuco De Abreu

Ricardo Reisen de Pinho

Ronaldo Fiorini

Vilson Gomes de Brito

Audit Committee

Sitting Members

Gustavo Jorge Laboissiere Loyola

Alberto Sozin Furuguem

Iran Siqueira Lima

Respective Substitute Members

José Marcos Konder Comparato

José Roberto Brant de Carvalho

Walter Dos Santos

Advisory Committee

Daniel Machado de Campos

Fernando de Almeida Nobre Filho

Joaquim Francisco Monteiro De Carvalho

Lício Meirelles Ferreira

Luiz Eduardo Campello

Olavo de Queiroz Guimarães Filho

International Advisory Committee

Olavo Egydio Setubal

Roberto Egydio Setubal

Alberto Dias de Mattos Barretto

Antonio Carlos Barbosa de Oliveira

Artur Eduardo Brochado dos Santos Silva (*)

Carlos da Câmara Pestana

Dieter Rampl

Henri Penchas

Isidro Fainé Casas (*)

José Carlos Moraes Abreu

Keiji Yokooji

Lorenzo David Weisman

Maria de Lourdes Egydio Villela

Renato Roberto Cuoco

Roberto Teixeira da Costa (*)

Sergio Silva De Freitas

Itaubanco Share Options Committee

Chairman

Olavo Egydio Setubal

Sitting Members

Carlos Da Câmara Pestana

José Carlos Moraes De Abreu

Roberto Egydio Setubal

Roberto Teixeira Da Costa (*)

Internal Control Committee

Chairman

Carlos Da Câmara Pestana

Sitting Members

Henri Penchas (*)

Jairo Cupertino

Luiz Assumpção Queiroz Guimarães

(*) Effected by the Shareholder' Meeting and the Board of Directors on April 23, 2001. Awaiting formed registration by the Central Bank of Brazil.

6

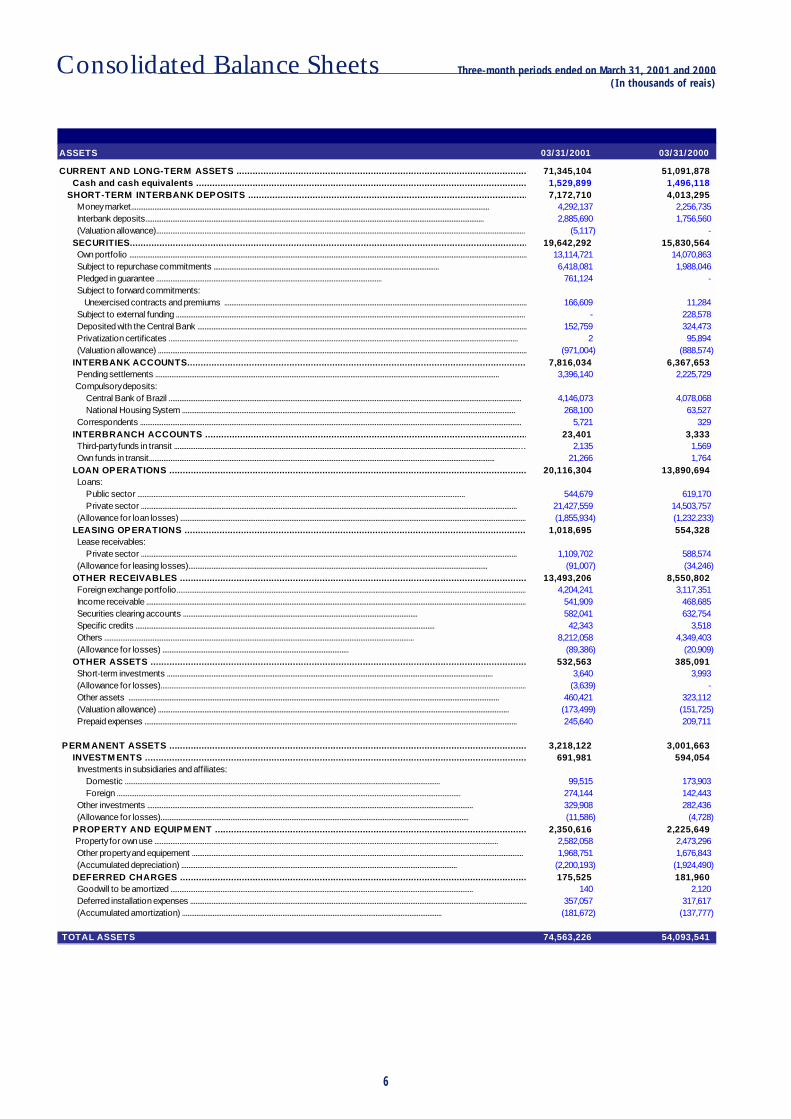

Consolidated Balance Sheets Three-month periods ended on March 31, 2001 and 2000(In thousands of reais)

ASSETS 03/31/2001 03/31/2000

CURRENT AND LONG-TERM ASSETS ............................................................................................................ 71,345,104 51,091,878 Cash and cash equivalents ........................................................................................................................... 1,529,899 1,496,118 SHORT-TERM INTERBANK DEPOSITS ........................................................................................................ 7,172,710 4,013,295 Money market........................................................................................................................................................................................................ 4,292,137 2,256,735 Interbank deposits............................................................................................................................................................................................. 2,885,690 1,756,560 (Valuation allowance).............................................................................................................................................................................................................. (5,117) - SECURITIES.................................................................................................................................................... 19,642,292 15,830,564 Own portfolio .............................................................................................................................................................................................................................. 13,114,721 14,070,863 Subject to repurchase commitments .............................................................................................................................. 6,418,081 1,988,046 Pledged in guarantee .............................................................................................................................. 761,124 - Subject to forward commitments: Unexercised contracts and premiums ......................................................................................................................................................................... 166,609 11,284 Subject to external funding ................................................................................................................................................................................................... - 228,578 Deposited with the Central Bank ........................................................................................................................................................................................ 152,759 324,473 Privatization certificates ................................................................................................................................................................................................... 2 95,894 (Valuation allowance) .............................................................................................................................................................................................................. (971,004) (888,574) INTERBANK ACCOUNTS............................................................................................................................... 7,816,034 6,367,653 Pending settlements ................................................................................................................................................................................................ 3,396,140 2,225,729 Compulsory deposits: Central Bank of Brazil ..................................................................................................................................................................................................... 4,146,073 4,078,068 National Housing System .......................................................................................................................................................................................... 268,100 63,527 Correspondents ..................................................................................................................................................................................................................... 5,721 329 INTERBRANCH ACCOUNTS ........................................................................................................................ 23,401 3,333 Third-party funds in transit ................................................................................................................................................................................................… 2,135 1,569 Own funds in transit................................................................................................................................................................................................. 21,266 1,764 LOAN OPERATIONS ..................................................................................................................................... 20,116,304 13,890,694 Loans: Public sector ....................................................................................................................................................................................... 544,679 619,170 Private sector .................................................................................................................................................................................................................. 21,427,559 14,503,757 (Allowance for loan losses) .................................................................................................................................................................................................. (1,855,934) (1,232,233) LEASING OPERATIONS ................................................................................................................................ 1,018,695 554,328 Lease receivables: Private sector .................................................................................................................................................................................................................. 1,109,702 588,574 (Allowance for leasing losses)....................................................................................................................................................................... (91,007) (34,246) OTHER RECEIVABLES ................................................................................................................................. 13,493,206 8,550,802 Foreign exchange portfolio.................................................................................................................................................................................................... 4,204,241 3,117,351 Income receivable .................................................................................................................................................................................................................... 541,909 468,685 Securities clearing accounts ................................................................................................................................... 582,041 632,754 Specific credits ....................................................................................................................................................................... 42,343 3,518 Others ............................................................................................................................................................................. 8,212,058 4,349,403 (Allowance for losses) ........................................................................................................ (89,386) (20,909) OTHER ASSETS ............................................................................................................................................ 532,563 385,091 Short-term investments ...................................................................................................................................................................................... 3,640 3,993 (Allowance for losses)............................................................................................................................................................................................................. (3,639) - Other assets ............................................................................................................................................................................................................... 460,421 323,112 (Valuation allowance) .................................................................................................................................................................................................... (173,499) (151,725) Prepaid expenses ................................................................................................................................................................................................................ 245,640 209,711

PERM ANENT ASSETS ..................................................................................................................................... 3,218,122 3,001,663 INVESTM ENTS .............................................................................................................................................. 691,981 594,054 Investments in subsidiaries and affiliates: Domestic ................................................................................................................................................................................ 99,515 173,903 Foreign ................................................................................................................................................................................................ 274,144 142,443 Other investments ...................................................................................................................................................................................... 329,908 282,436 (Allowance for losses)............................................................................................................................................................................ (11,586) (4,728) PROPERTY AND EQUIPM ENT .................................................................................................................... 2,350,616 2,225,649 Property for own use ................................................................................................................................................................................................ 2,582,058 2,473,296 Other property and equipement ......................................................................................................................................................................................... 1,968,751 1,676,843 (Accumulated depreciation) .......................................................................................................................................................... (2,200,193) (1,924,490) DEFERRED CHARGES ................................................................................................................................. 175,525 181,960 Goodwill to be amortized ......................................................................................................................................................................... 140 2,120 Deferred installation expenses ............................................................................................................................................................................................ 357,057 317,617 (Accumulated amortization) ................................................................................................................................................. (181,672) (137,777)

TOTAL ASSETS 74,563,226 54,093,541

7

Consolidated Balance Sheets Three-month periods ended on March 31, 2001 and 2000(In thousands of reais)

LIA B ILIT IES A N D ST OC KH OLD ER S' EQUIT Y 03/ 31 / 2001 03/ 31 / 2000

C UR R EN T A N D LON G-T ER M LIA B ILIT IES ..................................................................................................... 64,714 ,650 45,527 ,219

D EP OSIT S ...................................................................................................................................................... 27,158 ,852 22,131 ,021

Demand deposits ..................................................................................................................................................................................................................... 5,875,044 4,163,950

Savings deposits ...................................................................................................................................................................................................................... 15,751,315 14,674,345

Interbank deposits ................................................................................................................................................................................................................... 354,357 16,696

Time deposits ........................................................................................................................................................................................................................... 5,178,136 3,276,030

D EP OSIT S R EC EIVED UN D ER SEC UR IT Y R EP UR C H A SE A GR EEM EN T ............................................... 10,278 ,877 4 ,289,307

Own portfo lio ............................................................................................................................................................................................................................. 6,951,280 2,425,951

Third-party portfo lio ................................................................................................................................................................................................................ 3,327,597 1,863,356

F UN D S F R OM A C C EP T A N C ES A N D ISSUE OF SEC UR IT IES .................................................................. 3 ,114,557 3 ,139,584

M ortgage notes ............................................................................................................................................................................................................... 384,961 -

Debentures............................................................................................................................................................................................................... 742,787 1,140,486

Foreign borrowings in securities ............................................................................................................................................................................. 1,986,809 1,999,098

IN T ER B A N K A C C OUN T S .............................................................................................................................. 3 ,326,220 2 ,170,674

Pending settlement .........................................................................................................................................................................… 3,208,718 2,064,035

Interbank on-lending ...................................................................................................................................................................................... 647 1,026

Correspondents ....................................................................................................................................................................................... 116,855 105,613

IN T ER B R A N C H A C C OUN T S ........................................................................................................................ 427 ,496 332 ,899

Third-party funds in transit ................................................................................................................................................................................................... 420,331 321,753

Own funds in transit ................................................................................................................................................................................................. 7,165 11,146

B OR R OWIN GS ............................................................................................................................................... 5 ,284,300 3 ,570,308

Domestic - public institutions ....................................................................................................................................… 6,498 -

Domestic - other institutions .......................................................................................................................................... 684,774 460,748

Foreign currency trade finance borrowings .................................................................................................................................................................... 4,593,028 3,109,560

ON -LEN D IN G B OR R OWIN GS F R OM P UB LIC IN ST IT UT ION S ............................................................ 3 ,276,598 1 ,899,840

Federal Development Bank - BNDES .............................................................................................................................................................................. 2,324,886 1,226,497

CEF ............................................................................................................................................................................................................................... 131,239 1

Federal Capital Goods Financing Agency - FINAM E ................................................................................................................................................ 819,848 672,535

Other institutions ....................................................................................................................................................................................................................... 625 807

F OR EIGN ON -LEN D IN G................................................................................................................................. - 161

Foreign on-lending ................................................................................................................................................................................................................ - 161

OT H ER LIA B ILIT IES ...................................................................................................................................... 11,847 ,750 7 ,993,425

Co llection of taxes and contributions .............................................................................................................................................................................. 601,636 456,771

Foreign exchange portfo lio ................................................................................................................................................................................................... 2,382,366 1,989,092

Corporate and statutory contributions ............................................................................................................................................................................ 205,127 174,200

Taxes and social security contributions .......................................................................................................................................................................... 1,198,019 817,239

Negotiation and intermediation o f securities ............................................................................................................................................................... 1,111,743 503,904

Technical provisions for insurance, pension plan and capitalization operations - restricted ................................................................... 444,531 331,980

Financial and Development Funds..................................................................................................................................................................................... - 98

Others ........................................................................................................................................................................................................................................... 5,904,328 3,720,141

T EC H N IC A L P R OVISION S F OR IN SUR A N C E, P EN SION P LA N A N D

C A P IT A LIZ A T ION OP ER A T ION S - N ON -R EST R IC T ED ................................................................................. 2 ,344,225 1 ,904,201

D EF ER R ED IN C OM E ......................................................................................................................................... 116 ,609 142 ,581

Deferred income ...................................................................................................................................................................................................................... 116,609 142,581

M IN OR IT Y IN T ER EST IN SUB SID IA R IES ....................................................................................................... 572 ,116 394 ,722

ST OC KH OLD ER S' EQUIT Y ................................................................................................................................ 6 ,815,626 6 ,124,818

Capital:

Domestic ................................................................................................................................................................................................................................. 2,423,350 1,975,208

Foreign ..................................................................................................................................................................................................................................... 576,650 524,792

Capital reserves ....................................................................................................................................................................................................................... 202,219 264,394

Revaluation reserves ............................................................................................................................................................................................................. - 12,434

Retained income ...................................................................................................................................................................................................................... 3,792,455 3,458,703

(Treasury shares)....................................................................................................................................................................................................................... (179,048) (110,713)

T OT A L LIA B ILIT IES A N D ST OC KH OLD ER S' EQUIT Y 74,563 ,226 54,093 ,541

8

Consolidated Balance Sheets Three-month periods ended on March 31, 2001 and 2000(In thousands of reais)

Consolidated Statementsof Income

Three-month periods ended on March 31, 2001 and 2000(In of thousands of reais)

01.01 to 01.01 to03.31.2001 03.31.2000

INCOME FROM FINANCIAL OPERATIONS ....................................................................................................... 3,676,492 1,614,332 Loans.................................................................................................................................................................. 1,823,039 767,978

Leases ............................................................................................................................................................... 180,993 144,576

Securities portfolio ............................................................................................................................................. 1,584,943 651,629

Foreign exchange portfolio ................................................................................................................................ 20,082 1,622

Compulsory deposits ....................................................................................................................................... 67,435 48,527

EXPENSES ON FINANCIAL OPERATIONS ......................................................................................................... (2,446,237) (663,258) Deposits, money market and interbank funds .................................................................................................... (1,615,174) (370,081)

Borrow ings and assignments and on-lendings ................................................................................................. (454,925) (26,622)

Leases ............................................................................................................................................................... (141,856) (115,967)

Provision for loan losses ...................................................................................... (234,282) (150,588)

GROSS PROFIT FROM FINANCIAL OPERATIONS ........................................................................................... 1,230,255 951,074

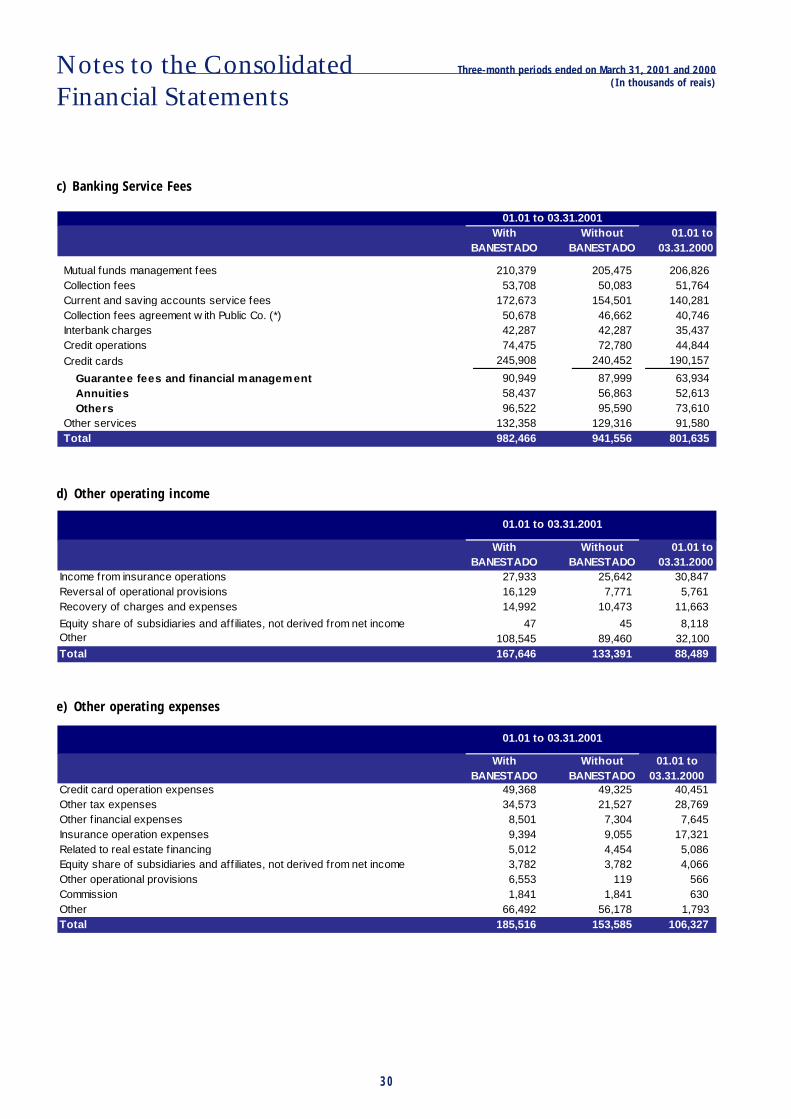

OTHER FINANCIAL INCOME (EXPENSES) ........................................................................................................ (448,382) (410,056) Banking service fees ......................................................................................................................................... 982,466 801,635

Capitalization, insurance and pension plan premiums ....................................................................................... 624,770 465,884

Expenses on Technical provisions for insurance, pension plan and capitalization operations ........................ (196,557) (103,480)

Insurance Claims ................................................................................................................................................ (199,699) (181,952)

Selling expenses ................................................................................................................................................ (43,182) (50,260)

Pension plan benefit expenses .......................................................................................................................... (53,618) (41,796)

Salaries and benefits to employees ................................................................................................................... (612,390) (516,626)

Other administrative expenses ....................................................................................................................... (789,282) (636,007)

Tax expenses .................................................................................................................................................... (152,616) (141,141)

Equity in income of subsidiaries and aff iliates ........................................................................................... 9,596 11,525

Other operating income ............................................................................................................... 167,646 88,489

Other operating expenses ................................................................................................................ (185,516) (106,327)

OPERATING INCOME ......................................................................................................................................... 781,873 541,018

NON-OPERATING INCOME ................................................................................................................................ 36,043 10,053

INCOME BEFORE INCOME TAX AND SOCIAL CONTRIBUTION AND PROFIT SHARING .................................................................................................................................................... 817,916 551,071

INCOME TAX AND SOCIAL CONTRIBUTION Due on operations for the period .........................................................................................… (163,118) (163,311)

Deferred related to temporary additions ..................................................................................... 86,459 3,864

EXTRAORDINARY RESULTS (Note 15) ........................................................................................................... (25,454) -

PROFIT SHARING ............................................................................................................................................... Employees ...................................................................................................................................................... (53,854) (23,150)

Directors - Statutories ..................................................................................................................................... (6,597) (5,381)

MINORITY INTEREST .................................................................................................................................… (30,139) 2,182

NET INCOME ..................................................................................................................................................... 625,213 365,275

NUMBER OF OUTSTANDING SHARES ............................................................................................................. 113,484,949,140 117,844,337,341 NET INCOME PER THOUSAND SHARES - R$ .............................................................................................. 5.51 3.10 STOCKHOLDERS' EQUITY PER THOUSAND SHARES - R$ ................................................................ 60.06 51.97

RECURRING NET INCOME ...................................................................................... 650,667 365,275

EXTRAORDINARY RESULT ......................................................................................... (25,454)

TOTAL - parent + company 625,213 365,275

9

Notes to the ConsolidatedFinancial Statements

Three-month periods ended on March 31, 2001 and 2000(In thousands of reais)

The financial statements of Banco Itaú S.A. and its subsidiaries(ITAÚ CONSOLIDATED) have been prepared in accordance withaccounting policies derived from the Brazilian Corporate Lawand instructions issued by the Brazilian Securities andExchange Commission (CVM) and the Central Bank of Brazil(BACEN), which include the use of estimates necessary tocalculate accounting provisions.

The consolidated financial statements have been presentedwithout the classification of balances between current andlong-term amounts, consistent with the presentation withthe comparable period.

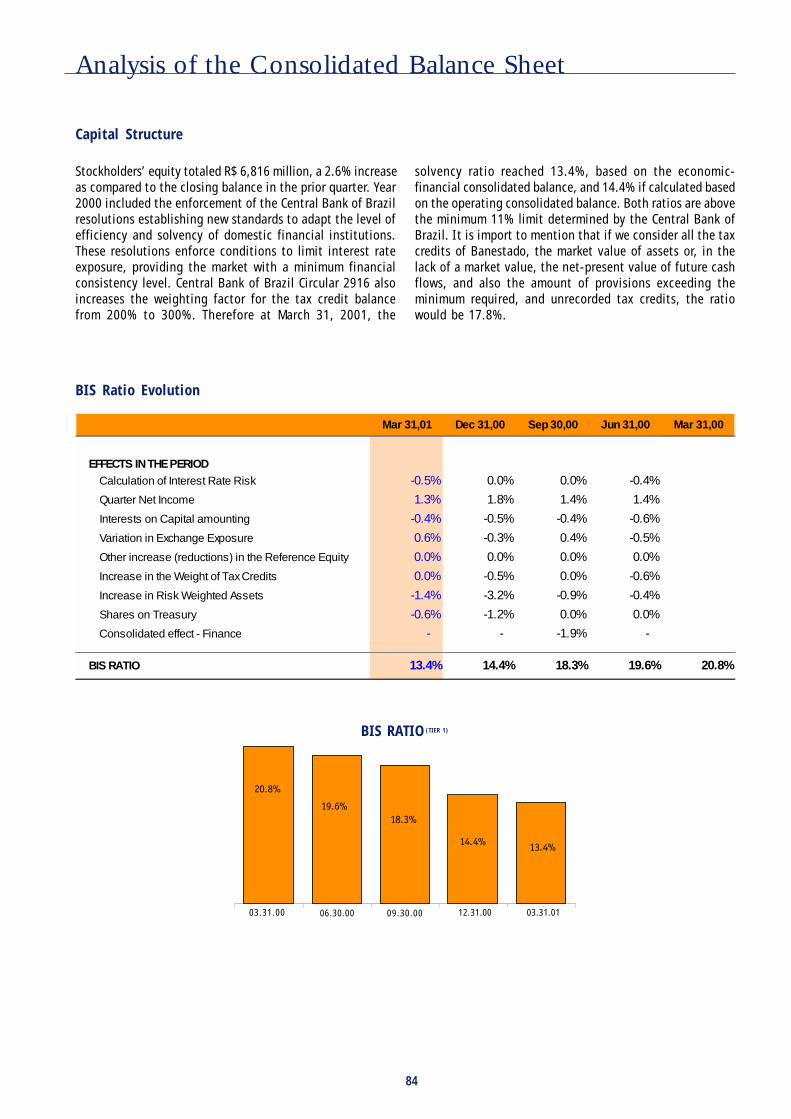

Management considers the current risk based capital ratio(13.4% based on economic-financial consolidated) to beadequate, considering that:

a) It is higher than the minimum required by authorities(11%);

b) This rate increases to 14.7%, when all of the tax credits ofBANESTADO are recorded in the financial statements basis(ITAÚ) used to establish limits;

c) This ratio would increase to 17.8% after considering theremaining realization values of assets (Note 13 b) and theprovision in excess to the minimum requirements and thetax credits not recorded.

Note 1 - Presentation of the Financial Statements

For comparison purposes, the notes to the financialstatements include information on ITAÚ CONSOLIDATED "withBANESTADO" and "without BANESTADO", with the lattercomparable with the balances at March 31, 2000.

The main indicators at March 31, 2001 obtained from thenon-consolidated financial statements (the initial basis fordetermination of the financial system consolidated amountsand pro forma economic-financial consolidated amounts),according to current legislation are as follows:

(1) In accordance with Note 1 II(2) In accordance with Note 1 III

Financial system Economic-financial

amounts (1) amounts (1)

Stockholders’ equity (2) 7,906,912 7,835,628

Risk based capital ratio 14.4 13.4

Fixed asset ratio 66.5 47.7

Excess capital in relation to f ixed assets 272,776 1,742,778

10

Notes to the ConsolidatedFinancial Statements

Three-month periods ended on March 31, 2001 and 2000(In thousands of reais)

Evolution of Basle rate

(1) In accordance with Note 1 II.(2) In accordance with Note 1 III.(3) In effect as from July 2000.(4) Because of the increased volatility of the interest rate market.

I- Risk based capital ratio (Basle ratio)

At March 31, 2001, the risk based capital ratio was 14.4%(20.8% at March 31, 2000) based on the Financial SystemConsolidated financial statements and 13.4%, based onEconomic-Financial Consolidated financial statementamounts.

The effects resulting from the changes during the last fourquarters, due to changes in the legislation or variation inthe balances are shown below:

Economic-financial consolidated (1) (3)

Referential Weighted Referential Weighted

equity (2) asset Effect equity (2) asset Effect

Rate of March 2000 6,511,659 31,310,707 20.8%

Calculation of interest rate risk (117,152) - -0.4%Quarterly results 427,217 - 1.4%Interest on ow n capital (187,040) - -0.6%Increase in foreign exchange exposure (172,047) - -0.5%Other increases (reductions) in referential equity (1,089) - 0.0%Increase in w eighted tax credit from 200% to 250% - 1,006,305 -0.6%Increase in w eighted asset - 590,830 -0.4%

Rate of June 2000 6,461,548 32,907,842 19.6%

Quarterly results 470,775 - 1.4%Interest on ow n capital (127,947) - -0.4%Increase in foreign exchange exposure 128,841 - 0.4%Other increases (reductions) in referential equity (2,150) - 0.0%Increase in w eighted asset - 1,397,276 -0.9%

Rate of September 2000 6,931,067 34,305,118 20.2% 6,854,989 37,360,184 18.3%

Quarterly results 627,234 - 1.8% 655,085 - 1.8%Interest on ow n capital (175,160) - -0.5% (175,160) - -0.5%Increase in foreign exchange exposure (122,873) - -0.4% (122,873) - -0.3%Purchase of treasury shares (454,842) - -1.3% (454,842) - -1.2%Other increases (reductions) in referential equity 36,619 - 0.1% 18,580 - 0.0%Increase in w eighted tax credit from 250% to 300% - 956,182 -0.5% - 1,107,819 -0.5%Increase in w eighted asset - 8,381,560 -3.7% - 8,652,424 -3.2%

Rate of December 2000 6,842,045 43,642,860 15.7% 6,775,779 47,120,427 14.4%

Quarterly results 602,880 - 1.4% 613,726 - 1.3%Interest on ow n capital (163,369) - -0.4% (163,369) - -0.4%Increase in interest rate risk (4) (252,404) - -0.6% (252,404) - -0.5%Reduction in foreign exchange exposure (5) 297,013 - 0.7% 297,013 - 0.6%Purchase of treasury shares (288,297) - -0.7% (288,297) - -0.6%Other increase (reductions) in referential equity (6,642) - 0.0% (22,462) - 0.0%Increase in w eighted asset - 5,107,794 -1.7% - 4,972,872 -1.4%

Rate of March 2001 7,031,266 48,750,654 14.4% 6,959,986 52,093,299 13.4%

Financial system consolidated (1)

11

Notes to the ConsolidatedFinancial Statements

Three-month periods ended on March 31, 2001 and 2000(In thousands of reais)

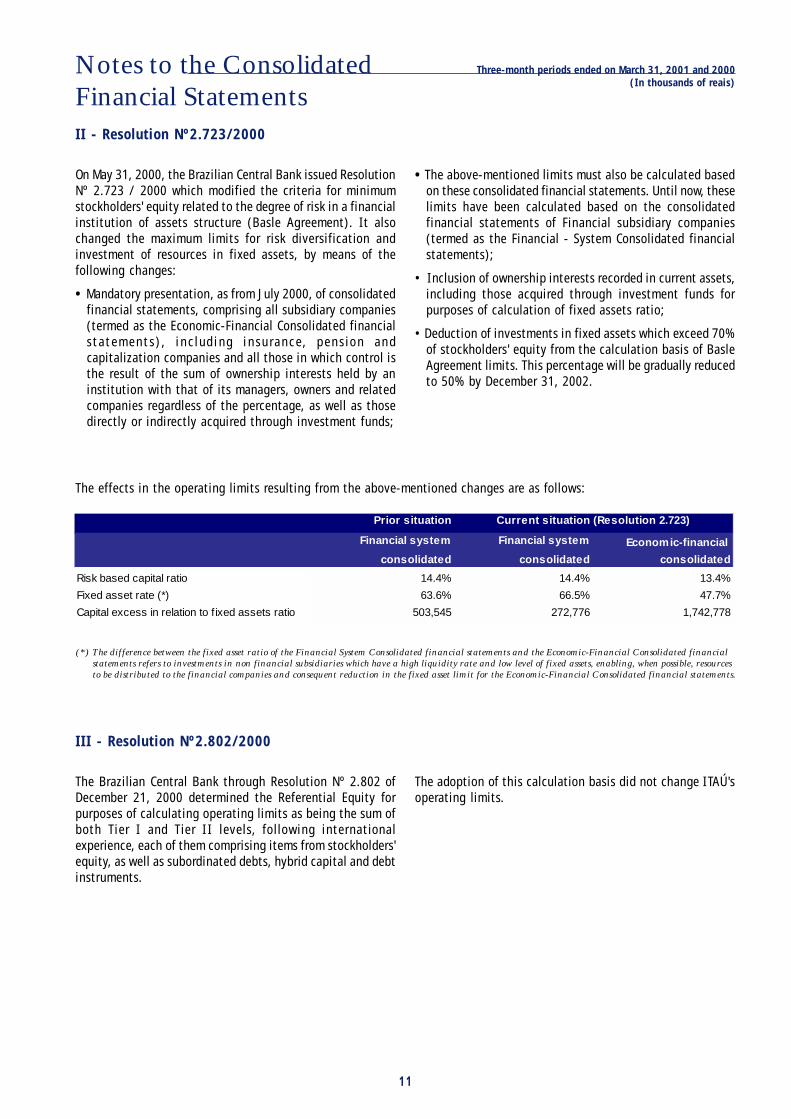

II - Resolution Nº2.723/2000

On May 31, 2000, the Brazilian Central Bank issued ResolutionNº 2.723 / 2000 which modified the criteria for minimumstockholders' equity related to the degree of risk in a financialinstitution of assets structure (Basle Agreement). It alsochanged the maximum limits for risk diversification andinvestment of resources in fixed assets, by means of thefollowing changes:

• Mandatory presentation, as from July 2000, of consolidatedfinancial statements, comprising all subsidiary companies(termed as the Economic-Financial Consolidated financialstatements), including insurance, pension andcapitalization companies and all those in which control isthe result of the sum of ownership interests held by aninstitution with that of its managers, owners and relatedcompanies regardless of the percentage, as well as thosedirectly or indirectly acquired through investment funds;

The effects in the operating limits resulting from the above-mentioned changes are as follows:

• The above-mentioned limits must also be calculated basedon these consolidated financial statements. Until now, theselimits have been calculated based on the consolidatedfinancial statements of Financial subsidiary companies(termed as the Financial - System Consolidated financialstatements);

• Inclusion of ownership interests recorded in current assets,including those acquired through investment funds forpurposes of calculation of fixed assets ratio;

• Deduction of investments in fixed assets which exceed 70%of stockholders' equity from the calculation basis of BasleAgreement limits. This percentage will be gradually reducedto 50% by December 31, 2002.

III - Resolution Nº2.802/2000

The Brazilian Central Bank through Resolution Nº 2.802 ofDecember 21, 2000 determined the Referential Equity forpurposes of calculating operating limits as being the sum ofboth Tier I and Tier II levels, following internationalexperience, each of them comprising items from stockholders'equity, as well as subordinated debts, hybrid capital and debtinstruments.

The adoption of this calculation basis did not change ITAÚ'soperating limits.

(*) The difference between the fixed asset ratio of the Financial System Consolidated financial statements and the Economic-Financial Consolidated financialstatements refers to investments in non financial subsidiaries which have a high liquidity rate and low level of fixed assets, enabling, when possible, resourcesto be distributed to the financial companies and consequent reduction in the fixed asset limit for the Economic-Financial Consolidated financial statements.

Prior situation

Financial system Financial system Economic-financial

consolidated consolidated consolidated

Risk based capital ratio 14.4% 14.4% 13.4%

Fixed asset rate (*) 63.6% 66.5% 47.7%

Capital excess in relation to f ixed assets ratio 503,545 272,776 1,742,778

Current situation (Resolution 2.723)

12

Notes to the ConsolidatedFinancial Statements

Three-month periods ended on March 31, 2001 and 2000(In thousands of reais)

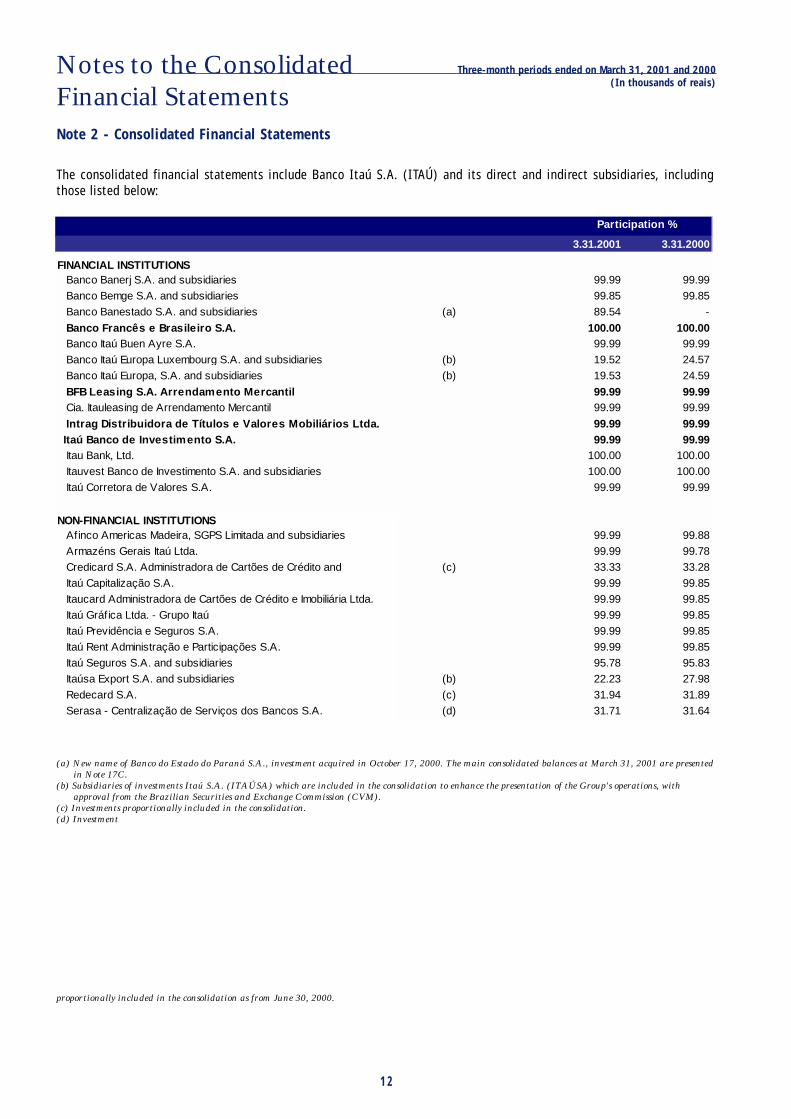

The consolidated financial statements include Banco Itaú S.A. (ITAÚ) and its direct and indirect subsidiaries, includingthose listed below:

Note 2 - Consolidated Financial Statements

(a) New name of Banco do Estado do Paraná S.A., investment acquired in October 17, 2000. The main consolidated balances at March 31, 2001 are presentedin Note 17C.

(b) Subsidiaries of investments Itaú S.A. (ITAÚSA) which are included in the consolidation to enhance the presentation of the Group's operations, withapproval from the Brazilian Securities and Exchange Commission (CVM).

(c) Investments proportionally included in the consolidation.(d) Investment

proportionally included in the consolidation as from June 30, 2000.

3.31.2001 3.31.2000

FINANCIAL INSTITUTIONS Banco Banerj S.A. and subsidiaries 99.99 99.99

Banco Bemge S.A. and subsidiaries 99.85 99.85

Banco Banestado S.A. and subsidiaries (a) 89.54 -

Banco Francês e Brasileiro S.A. 100.00 100.00 Banco Itaú Buen Ayre S.A. 99.99 99.99

Banco Itaú Europa Luxembourg S.A. and subsidiaries (b) 19.52 24.57

Banco Itaú Europa, S.A. and subsidiaries (b) 19.53 24.59

BFB Leasing S.A. Arrendamento Mercantil 99.99 99.99 Cia. Itauleasing de Arrendamento Mercantil 99.99 99.99

Intrag Distribuidora de Títulos e Valores Mobiliários Ltda. 99.99 99.99 Itaú Banco de Investimento S.A. 99.99 99.99 Itau Bank, Ltd. 100.00 100.00

Itauvest Banco de Investimento S.A. and subsidiaries 100.00 100.00

Itaú Corretora de Valores S.A. 99.99 99.99

NON-FINANCIAL INSTITUTIONS Afinco Americas Madeira, SGPS Limitada and subsidiaries 99.99 99.88

Armazéns Gerais Itaú Ltda. 99.99 99.78

Credicard S.A. Administradora de Cartões de Crédito and (c) 33.33 33.28

Itaú Capitalização S.A. 99.99 99.85

Itaucard Administradora de Cartões de Crédito e Imobiliária Ltda. 99.99 99.85

Itaú Gráf ica Ltda. - Grupo Itaú 99.99 99.85

Itaú Previdência e Seguros S.A. 99.99 99.85

Itaú Rent Administração e Participações S.A. 99.99 99.85

Itaú Seguros S.A. and subsidiaries 95.78 95.83

Itaúsa Export S.A. and subsidiaries (b) 22.23 27.98

Redecard S.A. (c) 31.94 31.89

Serasa - Centralização de Serviços dos Bancos S.A. (d) 31.71 31.64

Participation %

13

Notes to the ConsolidatedFinancial Statements

Three-month periods ended on March 31, 2001 and 2000(In thousands of reais)

a) Basis of consolidation - All material intercompany profits,transactions and balances have been eliminated onconsolidation.

The difference between Itaú and Itaú Consolidated in netincome and Shareholders' Equity results from the effectson the differing policies for the amortization of goodwillon acquisitions, the recognition of deferred tax assetsand the elimination of unrealized results of a transactionsanong group companies, together with correspondingdeferred taxation effects.

b) Interbank funds applied, loans, discounted tradereceivables, financing, remunerated deposits, fundsobtained in the open market and other receivablesand payables - Transactions subject to monetarycorrection or foreign exchange rates are recorded at presentvalue, calculated "pro rata die" based on the variation ofcontracted index. Real estate loans are adjusted to presentvalue of future installments. Transactions withpredetermined remuneration rates are recorded at theirredemption value, adjusted for any unearned income/expenses.

Note 3 - Summary of Significant Accounting Policies

c) Securities - These are recorded at restated cost andadjusted by a provision to reflect its market value, whenthis is lower.

d) Allowance for loan losses - The balance of the allowancefor loan losses was constituted based on an analysis ofthe credit risk in the loan portfolio, in amounts consideredsufficient to cover loan losses.

e) Investments - In subsidiary and associated companies,investments are using the equity method. The financialstatements of foreign branches and subsidiaries, includedin ITAÚ CONSOLIDATED, are adapted to comply withBrazilian accounting policies and converted into reais.Other investments are recorded at cost, restated up toDecember 31, 1995.

f) Fixed assets - These are stated at cost of acquisition orconstruction, less accumulated depreciation, restated upto December 31, 1995. For insurance operations, privatepension and capitalization, property and equipment areadjusted to market value supported by appraisal reports.Depreciation is calculated using the straight line method,based on monetarily corrected cost at the following annualrates:

g) Deferred expenses - Deferred organization and expansionexpenses represent improvements in third party propertiesand are amortized on a straight line over the respectiverental periods, and acquisition and development of logisticare amortized on a straight line basis over five years.

h) Income tax and social contribution, PIS and COFINSThe provisions were calculated according to the currentlegislation at the rates shown below.

(*) Period from May 1, 1999 to January 31, 2000 calculated at the rate of4%. As from February 1, 2000 up to December 31, 2002 the rate wasreduced to 1%.

Amounts subject to litigation have been fully provided.

%

Buildings in use 4

Installations, furnishings, equipment and security and communication systems 10 to 25

EDP systems 20 to 50

Income tax 15.00%

Additional income tax 10.00%

Social contribution 8.00%

Additional social contribution (*) 1.00%

PIS 0.65%

COFINS 3.00%

14

Notes to the ConsolidatedFinancial Statements

Three-month periods ended on March 31, 2001 and 2000(In thousands of reais)

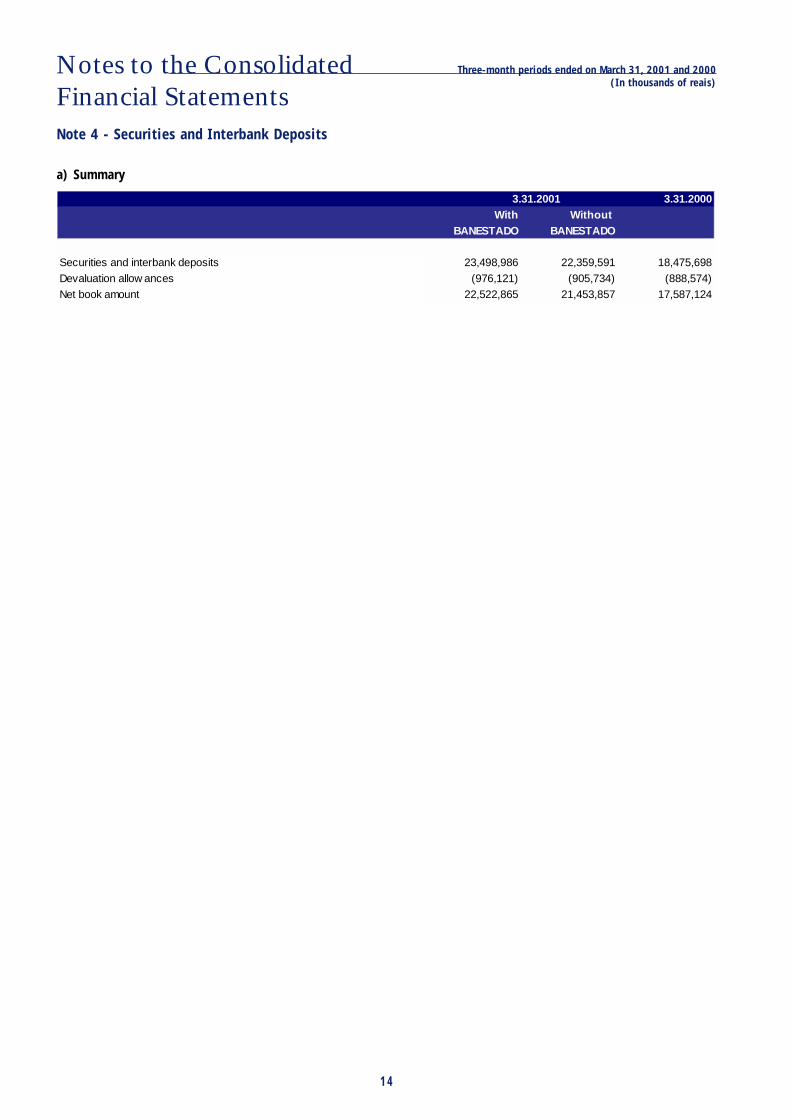

a) Summary

Note 4 - Securities and Interbank Deposits

3.31.2001 3.31.2000With Without

BANESTADO BANESTADO

Securities and interbank deposits 23,498,986 22,359,591 18,475,698

Devaluation allow ances (976,121) (905,734) (888,574)

Net book amount 22,522,865 21,453,857 17,587,124

15

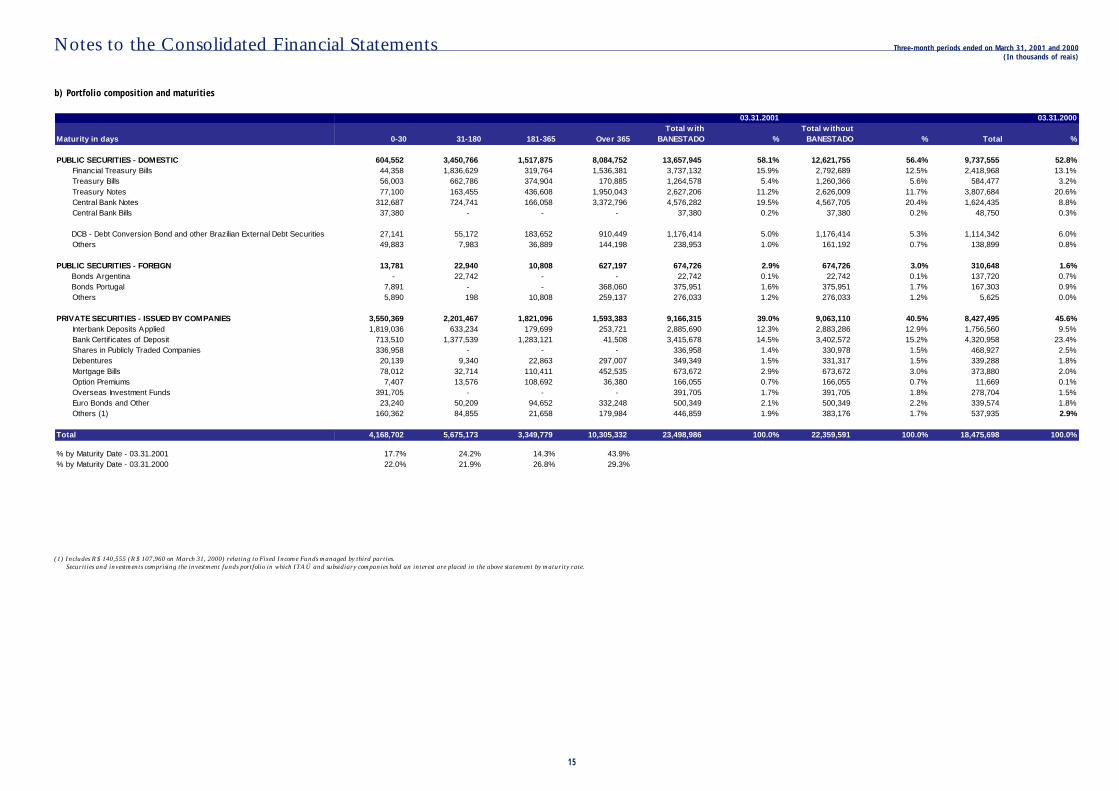

b) Portfolio composition and maturities

Notes to the Consolidated Financial Statements

(1) Includes R$ 140,555 (R$ 107,960 on March 31, 2000) relating to Fixed Income Funds managed by third parties.Securities and investments comprising the investment funds portfolio in which ITAÚ and subsidiary companies hold an interest are placed in the above statement by maturity rate.

Maturity in days

PUBLIC SECURITIES - DOMESTIC Financial Treasury Bills Treasury Bills Treasury Notes Central Bank Notes Central Bank Bills

DCB - Debt Conversion Bond and other Brazilian External Debt Securities Others

PUBLIC SECURITIES - FOREIGN Bonds Argentina Bonds Portugal Others

PRIVATE SECURITIES - ISSUED BY COMPANIES Interbank Deposits Applied Bank Certif icates of Deposit Shares in Publicly Traded Companies Debentures Mortgage Bills Option Premiums Overseas Investment Funds Euro Bonds and Other Others (1)

Total

% by Maturity Date - 03.31.2001% by Maturity Date - 03.31.2000

Total w ith Total w ithout0-30 31-180 181-365 Over 365 BANESTADO % BANESTADO % Total %

604,552 3,450,766 1,517,875 8,084,752 13,657,945 58.1% 12,621,755 56.4% 9,737,555 52.8%44,358 1,836,629 319,764 1,536,381 3,737,132 15.9% 2,792,689 12.5% 2,418,968 13.1%56,003 662,786 374,904 170,885 1,264,578 5.4% 1,260,366 5.6% 584,477 3.2%77,100 163,455 436,608 1,950,043 2,627,206 11.2% 2,626,009 11.7% 3,807,684 20.6%

312,687 724,741 166,058 3,372,796 4,576,282 19.5% 4,567,705 20.4% 1,624,435 8.8%37,380 - - - 37,380 0.2% 37,380 0.2% 48,750 0.3%

27,141 55,172 183,652 910,449 1,176,414 5.0% 1,176,414 5.3% 1,114,342 6.0%49,883 7,983 36,889 144,198 238,953 1.0% 161,192 0.7% 138,899 0.8%

13,781 22,940 10,808 627,197 674,726 2.9% 674,726 3.0% 310,648 1.6%- 22,742 - - 22,742 0.1% 22,742 0.1% 137,720 0.7%

7,891 - - 368,060 375,951 1.6% 375,951 1.7% 167,303 0.9%5,890 198 10,808 259,137 276,033 1.2% 276,033 1.2% 5,625 0.0%

3,550,369 2,201,467 1,821,096 1,593,383 9,166,315 39.0% 9,063,110 40.5% 8,427,495 45.6%1,819,036 633,234 179,699 253,721 2,885,690 12.3% 2,883,286 12.9% 1,756,560 9.5%

713,510 1,377,539 1,283,121 41,508 3,415,678 14.5% 3,402,572 15.2% 4,320,958 23.4%336,958 - - - 336,958 1.4% 330,978 1.5% 468,927 2.5%20,139 9,340 22,863 297,007 349,349 1.5% 331,317 1.5% 339,288 1.8%78,012 32,714 110,411 452,535 673,672 2.9% 673,672 3.0% 373,880 2.0%7,407 13,576 108,692 36,380 166,055 0.7% 166,055 0.7% 11,669 0.1%

391,705 - - - 391,705 1.7% 391,705 1.8% 278,704 1.5%23,240 50,209 94,652 332,248 500,349 2.1% 500,349 2.2% 339,574 1.8%

160,362 84,855 21,658 179,984 446,859 1.9% 383,176 1.7% 537,935 2.9%

4,168,702 5,675,173 3,349,779 10,305,332 23,498,986 100.0% 22,359,591 100.0% 18,475,698 100.0%

17.7% 24.2% 14.3% 43.9%22.0% 21.9% 26.8% 29.3%

03.31.2001 03.31.2000

Three-month periods ended on March 31, 2001 and 2000(In thousands of reais)

Notes to the ConsolidatedFinancial Statements

Three-month periods ended on March 31, 2001 and 2000(In thousands of reais)

16

c) Changes in the valuation allowance for securities

Note 5 - Loan and Lease Portfolio

a) Summary

(1) Includes honored endorsements and sureties, receivables from advances, commissions from co-obligations receivable, debtors on purchase of assets andreceivables.

(2) Recorded in other liabilities.(3) Recorded in memorandum accounts.

(*) Additional allowance was recorded to cover risks of future price fluctuation.

With Without

BANESTADO BANESTADO

Balance at December 31, 1999 902,301 902,301Write-offs (13,727) (13,727)

Reversal (11,695) (11,695)

Losses on sales (2,032) (2,032)

Balance at March 31, 2000 888,574 888,574 Minimum allow ance required 142,674 142,674

Additional allow ance (*) 745,900 745,900

Balance at December 31, 2000 972,774 905,247Increase 6,565 3,703

Write-offs (3,218) (3,216)

Reversal (2,083) (2,081)

Loss on sales (1,135) (1,135)

Balance at March 31, 2001 976,121 905,734 Minimum allow ance required 321,121 250,734

Additional allow ance (*) 655,000 655,000

03.31.2000

With Without

BANESTADO BANESTADO Loan operations 21,972,238 20,717,601 15,122,927

Leasing operations 1,109,702 1,080,992 588,574

Other receivables (1) 685,650 141,392 168,491

Advances on exchange contracts (2) 1,739,754 1,734,487 1,512,988

Total 25,507,344 23,674,472 17,392,980

Endorsements and sureties (3) 4,423,856 4,406,682 2,847,560

Total w ith endorsements and sureties 29,931,200 28,081,154 20,240,540

03.31.2001

Notes to the ConsolidatedFinancial Statements

Three-month periods ended on March 31, 2001 and 2000(In thousands of reais)

17

I - Composition by type of operation and risk level

(1) Comprises honoured endorsements and sureties, receivables from advances, commissions,(2) Recorded under other liabilities

b) Loan and Lease portfolio by risk level

II - Composition by maturity and risk level

03.31.2001 03.31.2000

Maturity (days) AA A B C D E F G H Total%

Falling due - - 449,266 518,995 319,462 40,802 132,937 39,613 180,101 1,681,176 6.6%01 to 30 - - 97,724 14,483 16,435 1,784 10,303 1,866 15,265 157,860 0.6%

31 to 60 - - 10,761 12,633 17,320 1,517 7,420 3,205 7,027 59,883 0.2%61 to 90 - - 10,027 11,427 13,225 2,113 6,396 1,481 6,231 50,900 0.2%

91 to 180 - - 74,674 39,301 35,349 5,745 30,137 5,994 24,825 216,025 0.8%181 to 360 - - 91,386 60,652 48,568 5,957 25,479 5,872 33,173 271,087 1.1%More than 360 - - 164,694 380,499 188,565 23,686 53,202 21,195 93,580 925,421 3.6%

Overdue - - 200,736 91,856 125,538 67,345 93,828 62,573 409,219 1,051,095 4.1%01 to 14 - - 2,749 4,388 5,418 975 7,109 1,436 15,018 37,093 0.1%15 to 30 - - 196,334 9,941 27,709 5,968 7,523 1,229 4,674 253,378 1.0%

31 to 60 - - 799 76,257 28,942 4,030 8,950 2,593 11,085 132,656 0.5%61 to 90 - - 87 822 61,695 4,787 7,458 2,484 9,111 86,444 0.3%

91 to 180 - - 767 315 1,774 51,030 61,385 52,879 39,118 207,268 0.8%181 to 360 - - - 133 - 555 1,387 1,952 249,822 253,849 1.0%

More than 360 - - - - - - 16 - 80,391 80,407 0.3%

SUBTOTAL - - 650,002 610,851 445,000 108,147 226,765 102,186 589,320 2,732,271 10.7%

% 0.0% 0.0% 2.5% 2.4% 1.7% 0.4% 0.9% 0.4% 2.3%

Falling due 7,070,423 6,511,880 6,531,889 1,154,395 762,803 148,215 235,823 89,076 88,257 22,592,761 88.6%01 to 30 866,651 943,597 2,600,782 274,695 213,722 3,714 28,197 458 6,487 4,938,303 19.4%31 to 60 1,115,720 824,926 499,474 137,890 75,673 5,384 18,870 208 3,460 2,681,605 10.5%61 to 90 485,850 310,283 328,241 99,591 38,677 14,353 17,661 208 4,134 1,298,998 5.1%91 to 180 1,216,942 630,716 604,326 146,347 86,212 50,150 43,186 422 10,969 2,789,270 10.9%181 to 360 1,065,410 1,011,641 776,499 221,968 128,832 52,949 53,843 570 17,639 3,329,351 13.1%More than 360 2,319,850 2,790,717 1,722,567 273,904 219,687 21,665 74,066 87,210 45,568 7,555,234 29.6%

Overdue up to 14 days 31,241 36,588 60,324 21,127 25,063 389 6,081 118 1,381 182,312 0.7%

SUBTOTAL 7,101,664 6,548,468 6,592,213 1,175,522 787,866 148,604 241,904 89,194 89,638 22,775,073 89.3%% 27.8% 25.7% 25.8% 4.6% 3.1% 0.6% 0.9% 0.3% 0.4%

TOTAL 7,101,664 6,548,468 7,242,215 1,786,373 1,232,866 256,751 468,669 191,380 678,958 25,507,344 100.0%% 27.8% 25.7% 28.4% 7.0% 4.8% 1.0% 1.8% 0.8% 2.7%

CLASSIFICATION OF CLIENTS

NORMAL SITUATION

ABNORMAL SITUATION

Risk Levels AA A B C D E F G HWith

BANESTADO%

Without BANESTADO

%

Loans Operations 6,061,093 5,146,870 6,586,755 1,605,426 1,128,519 242,599 447,341 185,539 568,096 21,972,238 86.1% 20,717,601 87.5% Loans and discounted trade receivables 4,038,522 2,775,523 4,462,497 779,874 703,298 61,944 318,317 72,983 373,680 13,586,638 53.3% 13,114,662 55.4% Financing 1,685,730 1,442,050 701,694 220,338 66,993 16,524 16,083 2,614 13,128 4,165,154 16.3% 4,112,141 17.4% Farm and agrobusiness industries 316,841 369,811 174,068 43,825 12,198 107,232 6,825 77,994 10,585 1,119,379 4.4% 1,042,244 4.4% Real estate financing 20,000 559,486 1,248,496 561,389 346,030 56,899 106,116 31,948 170,703 3,101,067 12.2% 2,448,554 10.3%Securities financing - - - - - - - - - - 0.0% - 0.0%

Leasing Operations 13,756 665,323 201,182 79,552 82,467 5,943 15,571 4,472 41,436 1,109,702 4.4% 1,080,992 4.6%

Other receivables (1) 29,183 485,627 82,317 11,835 7,955 1,840 3,439 1,064 62,390 685,650 2.7% 141,392 0.6%

Advances on Exchange Contracts (2) 997,632 250,648 371,961 89,560 13,925 6,369 2,318 305 7,036 1,739,754 6.8% 1,734,487 7.3%

Total 7,101,664 6,548,468 7,242,215 1,786,373 1,232,866 256,751 468,669 191,380 678,958 25,507,344 100.0% 23,674,472 100.0%

03.31.2001

% Total %

87.5% 15,122,927 86.9%55.4% 8,857,375 50.9%17.4% 2,490,339 14.3%4.4% 884,884 5.1%

10.3% 2,888,760 16.6%0.0% 1,569 0.0%

4.6% 588,574 3.4%

0.6% 168,491 1.0%

7.3% 1,512,988 8.7%

100.0% 17,392,980 100.0%

Notes to the ConsolidatedFinancial Statements

Three-month periods ended on March 31, 2001 and 2000(In thousands of reais)

18

c) Composition by Business Sector

With BANESTADO %

Without BANESTADO % Sectors %

PUBLIC SECTOR 1,012,813 4.0% 516,254 2.2% 658,782 3.8% INDUSTRY 1,012,813 4.0% 516,254 2.2% 658,782 3.8% Chemical and Petrochemical 491,420 1.9% 491,420 2.1% 658,325 3.8% Other 521,393 2.0% 24,834 0.1% 457 0.0%PRIVATE SECTOR 24,494,531 96.0% 23,158,218 97.8% 16,734,198 96.2% INDUSTRY 6,248,384 24.5% 6,183,919 26.1% 4,899,589 28.2% Steel, Metallurgy and Heavy Industry 1,064,487 4.2% 1,058,363 4.5% 861,091 5.0% Chemical and Petrochemical 1,110,782 4.4% 1,107,692 4.7% 778,873 4.5% Food and Beverages 1,066,407 4.2% 1,053,827 4.5% 1,011,415 5.8% Paper and Pulp 573,329 2.2% 568,350 2.4% 487,818 2.8% Light and Heavy Vehicles 371,499 1.5% 371,421 1.6% 274,673 1.6% Electrical and Eletronic 496,087 1.9% 493,944 2.1% 298,617 1.7% Textiles and Clothing 236,500 0.9% 229,760 1.0% 176,178 1.0% Autoparts and Accessories 118,832 0.5% 117,766 0.5% 108,907 0.6% Fertilizers, Insecticides and Crop Protection 245,767 1.0% 239,850 1.0% 198,669 1.1% Pharmaceuticals 49,894 0.2% 49,738 0.2% 90,951 0.5% Other 914,800 3.6% 893,208 3.8% 612,397 3.5% COMMERCE 1,635,385 6.4% 1,579,920 6.7% 870,749 5.0% SERVICES 5,120,335 20.1% 4,937,883 20.9% 3,087,641 17.8% Financial 632,475 2.5% 629,871 2.7% 771,907 4.4% Telecommunications 1,774,070 7.0% 1,773,664 7.5% 632,028 3.6% Public Services Concessionaires 637,252 2.5% 636,853 2.7% 395,584 2.3% Holding and Service Companies 990,707 3.9% 952,917 4.0% 378,691 2.2% Civil Construction 285,746 1.1% 214,133 0.9% 400,949 2.3% Contractors and Real Estate Agents 265,035 1.0% 237,237 1.0% 174,931 1.0% Transportation 137,899 0.5% 124,308 0.5% 89,989 0.5% Others 397,151 1.6% 368,900 1.6% 243,562 1.4% PRIMARY SECTOR 865,958 3.4% 859,530 3.6% 656,847 3.8% Farming and Livestock 436,343 1.7% 431,243 1.8% 348,505 2.0% Mining 429,615 1.7% 428,287 1.8% 308,342 1.8% OTHER - INDIVIDUALS 10,225,137 40.1% 9,228,815 39.0% 6,923,345 39.8% Credit Cards 2,006,812 7.9% 1,974,819 8.3% 1,441,690 8.3% Real estate f inancings 2,815,321 11.0% 2,234,421 9.4% 2,487,811 14.3% Consumer Loans/Vehicles/Overdraft 5,403,004 21.2% 5,019,575 21.2% 2,993,844 17.2% OTHER - CORPORATE ENTITIES 399,332 1.6% 368,151 1.6% 296,027 1.7%

TOTAL 25,507,344 100.0% 23,674,472 100.0% 17,392,980 100.0%

03.31.2001 03.31.2000

Notes to the ConsolidatedFinancial Statements

Three-month periods ended on March 31, 2001 and 2000(In thousands of reais)

19

d) Concentration of credit (*)

(*) Amounts include endorsements and sureties.

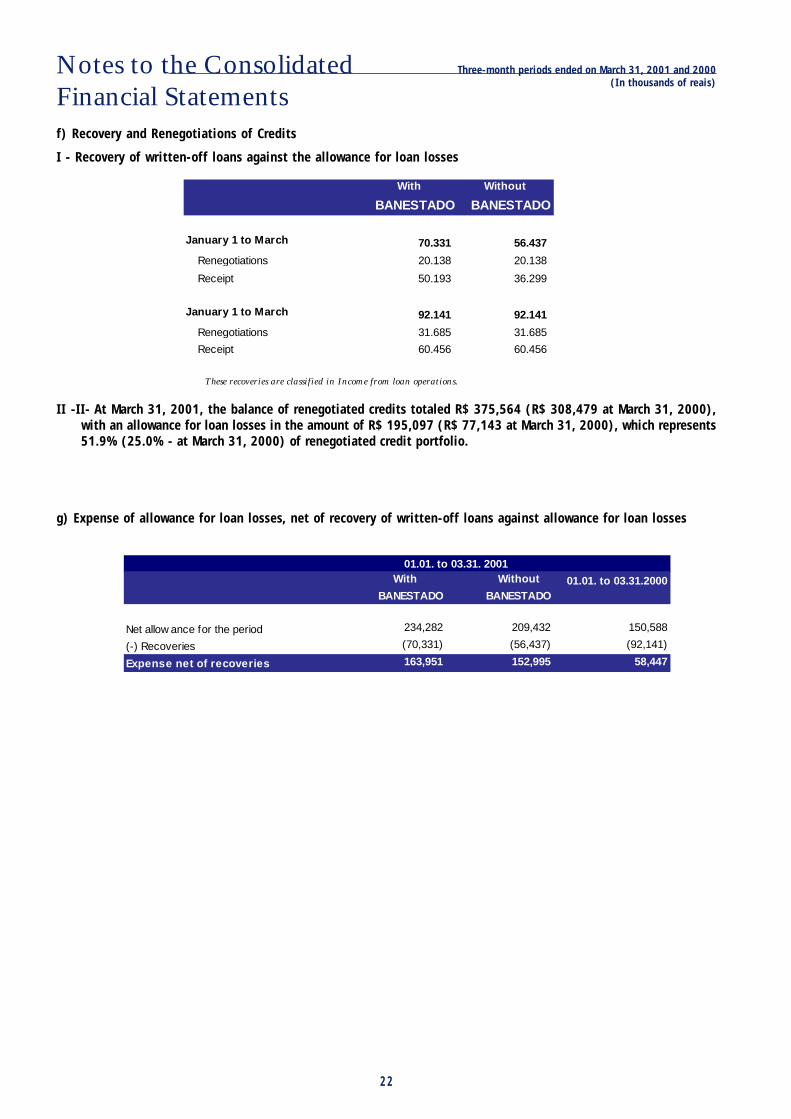

e) Allowance for loan losses

The allowance for loan losses complies with the rulesdetermined by BACEN Resolution No. 2.682 of December 21,1999, among which are:

• Provisions are recorded from the date of the loandisbursements, based on periodic analysis of the qualityof the client/loan and not just in the event of default;

I- Changes in the allowance for loan losses

• Based exclusively on delinquency, write-offs can be made360 days after the due date of the credit or 720 days foroperations that mature after a period of 36 months. Otherfactors related to analysis of the quality of the client/loanmay generate write-offs before these periods, however,never before 180 days of the due date.

At March 31, 2001, the balance of the allowance was equivalent to 8.0% of the loan portfolio in ITAÚ CONSOLIDATED withBANESTADO and 7.4% in ITAÚ CONSOLIDATED without BANESTADO (7.4% at March 31, 2000).

(1) For operations for which installments are overdue more than 14 days, with renegotiations made or under the responsibility of companies in the process of debtrehabilitation or bankruptcy.

(2) For operations not covered by the previous item due to the classification of the client or the operation.(3) Refers to the provision in excess of the minimum requirement, recorded based on the conservative criteria adopted by management, in accordance with good

banking practice, in order to cover any unexpected losses resulting from oscillations in the credit risks quantified based on historic data considering marketvolatility and economic casis situations.

Risk w ith % of Total Risk w ithout % of Total Risk % of Total

BANESTADO BANESTADO

Largest debtor 658,831 2.2% 658,831 2.3% 695,469 3.4%

20 largest debtors 6,803,122 22.7% 6,488,693 23.1% 4,128,400 20.4%

50 largest debtors 9,993,303 33.4% 9,599,681 34.2% 6,398,700 31.6%

100 largest debtors 12,532,042 41.9% 12,088,821 43.0% 8,279,648 40.9%

03.31.2001 03.31.2000

With Without

BANESTADO BANESTADO

Balance at December 31, 1999 1,253,371 1,253,371

Increase in the period 150,588 150,588

Write-offs (116,571) (116,571)

Balance at March 31, 2000 1,287,388 1,287,388

Specif ic allow ance (1) 321,599 321,599

Generic allow ance (2) 341,162 341,162

Excess allow ance (3) 624,627 624,627

Specif ic allow ance (1) 929,374 647,517

Generic allow ance (2) 501,101 430,632

Excess allow ance (3) 602,616 602,616

Balance at December 31, 2000 2,033,091 1,680,765

Increase in the period 234,282 209,432

Write-offs (231,046) (126,654)

Balance at March 31, 2001 2,036,327 1,763,543

Specif ic allow ance (1) 876,003 669,930

Generic allow ance (2) 530,324 463,613

Excess allow ance (3) 630,000 630,000

20

Three-month periods ended march 31, 2001 and 2000(In of thousands of reais)

Notes to the Consolidated Financial Statements

II- Allowance for Loan Losses by Risk Levels at December 31, 2000

(1) Operations in abnormal situation are considered to be those with installments overdue for more than 14 days, assumed by or theresponsibility of companies undergoing debt rehabilitation or in process of bankruptcy.

(2) At Bacen's request, the provision was allocated to make explicit, in each risk level, the exceeding amounts quantified using thestatistical models so as to evaluate the "stressed" portfolios in the market.

Risk Levels % Minimum Normal Situation

Provision RequiredFalling Due

Operations and Installments

Overdue Installments

Subtotal Falling Due Operations

AA 0.0% - - - 6,407,430 6,407,430 A 0.5% - - - 5,526,513 5,526,513 B 1.0% 138,158 183,732 321,890 6,636,677 6,958,567 C 3.0% 362,586 90,691 453,277 1,282,482 1,735,759 D 10.0% 334,381 109,319 443,700 1,003,212 1,446,912 E 30.0% 47,987 63,355 111,342 163,169 274,511 F 50.0% 211,548 93,628 305,176 119,513 424,689 G 70.0% 36,088 55,712 91,800 100,535 192,335 H 100.0% 172,887 445,050 617,937 89,224 707,161

Total 1,303,635 1,041,487 2,345,122 21,328,755 23,673,877

Portfolio Balance

Abnormal Situation (1)

Total Falling Due Overdue Subtotal

Excess Allow ance (2)

Existing Allowance

- - - - - - - - - - 27,633 27,633 20,509 48,142 1,381 1,837 3,218 66,366 69,584 124,817 194,401 10,878 2,720 13,598 38,474 52,072 91,315 143,387 33,438 10,932 44,370 100,321 144,691 231,355 376,046 14,396 19,007 33,403 48,951 82,354 45,851 128,205 105,774 46,814 152,588 59,757 212,345 59,282 271,627 25,262 38,998 64,260 70,375 134,635 29,487 164,122 172,887 445,050 617,937 89,224 707,161 - 707,161 364,016 565,358 929,374 501,101 1,430,475 602,616 2,033,091

Total Allowance BACEN Resolution 2682/1999

Specific

Total Generic

Risk Levels % Minimum Normal Situation

Provision RequiredFalling Due

Operations and Installments

Overdue Installments

Subtotal Falling Due Operations

AA 0.0% - - - 6,316,369 6,316,369 A 0.5% - - - 4,839,339 4,839,339 B 1.0% 113,717 181,555 295,272 6,416,823 6,712,095 C 3.0% 316,573 82,330 398,903 1,007,603 1,406,506 D 10.0% 144,797 91,184 235,981 980,160 1,216,141 E 30.0% 37,203 60,521 97,724 137,707 235,431 F 50.0% 158,716 77,461 236,177 81,137 317,314 G 70.0% 25,398 50,436 75,834 99,941 175,775 H 100.0% 91,020 317,490 408,510 62,183 470,693

Total 887,424 860,977 1,748,401 19,941,262 21,689,663

Total

Portfolio Balance

Abnormal Situation (1)

Falling Due Overdue Subtotal

Excess Allow ance (2)

Existing Allowance

- - - - - - - - - - 24,197 24,197 20,509 44,706 1,137 1,816 2,953 64,168 67,121 127,817 191,938 9,497 2,470 11,967 30,228 42,195 91,315 133,510 14,480 9,118 23,598 98,016 121,614 231,355 352,969 11,161 18,156 29,317 41,312 70,629 4,585 116,480 79,358 38,730 118,088 40,569 158,657 59,282 217,939 17,779 35,305 53,084 69,959 123,043 29,487 152,530 91,020 317,490 408,510 62,183 470,693 - 470,693 224,432 423,085 647,517 430,632 1,078,149 602,616 1,680,765

Specific

Generic Total

Total Allowance BACEN Resolution 2682/1999

21

III- Alowance for Loan Losses by Risk Levels

(1) Operations in abnormal situation are considered to be those with installments overdue for more than 14 days, assumed by or theresponsibility of companies undergoing debt rehabilitation or in process of bankruptcy.

(2) At Bacen's request, the provision was allocated to make explicit, in each risk level, the exceeding amounts quantified using thestatistical models so as to evaluate the "stressed" portfolios in the market.

Risk % Minimum Normal Situation

At levels Allowance

RequiredFalling Due

Operations and installments

Overdue installments

Subtotal Falling Due Operations

03.31.2000

AA 0.0% - - - 7,101,664 7,101,664 4,906,983 A 0.5% - - - 6,548,468 6,548,468 6,021,657 B 1.0% 449,266 200,736 650,002 6,592,213 7,242,215 3,506,932 C 3.0% 518,995 91,856 610,851 1,175,522 1,786,373 1,530,268 D 10.0% 319,462 125,538 445,000 787,866 1,232,866 723,475 E 30.0% 40,802 67,345 108,147 148,604 256,751 90,347 F 50.0% 132,937 93,828 226,765 241,904 468,669 298,218 G 70.0% 39,613 62,573 102,186 89,194 191,380 39,920 H 100.0% 180,101 409,219 589,320 89,638 678,958 275,180

Total 1,681,176 1,051,095 2,732,271 22,775,073 25,507,344 17,392,980

At 03.31.2001

Portfolio balance

Abnormal Situation (1)

Total

Exceeding 03.31.2001 03.31.2000

Specific At 03.31.2000 At 03.31.2000

Falling Due Overdue Subtotal Generic TotalExces Allowance

(2) Existing

Allowance Existing

Allowance