CONSOLIDATED ANNUAL AUDIT REPORT - World …documents.worldbank.org/curated/en/... · CONSOLIDATED...

55

VO Republic of the Philippines COMMISSION ON AUDIT Commonwealth Avenue, Quezon City CONSOLIDATED ANNUAL AUDIT REPORT ON THE PHILIPPINE STATISTICS AUTHORITY For the Year Ended December 31, 2015 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of CONSOLIDATED ANNUAL AUDIT REPORT - World …documents.worldbank.org/curated/en/... · CONSOLIDATED...

VO

Republic of the PhilippinesCOMMISSION ON AUDIT

Commonwealth Avenue, Quezon City

CONSOLIDATEDANNUAL AUDIT REPORT

ON THE

PHILIPPINE STATISTICSAUTHORITY

For the Year Ended December 31, 2015

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Republic of the Philippines

COMMISSION ON AUDITCommonwealth Avenue, Quezon City, Philippines

INDEPENDENT AUDITOR'S REPORT

The National Statistician and Civil Registrar GeneralPhilippine Statistics Authority (PSA)East Avenue, Quezon City

We have audited the accompanying financial statements of the Philippine StatisticsAuthority (PSA), which comprise the Statement of Financial Position as at December 31,2015, and the Statement of Financial Performance, Statement of Comparison of Budget

and Actual Amounts, Statement of Cash Flows and Statement of Changes in Net

Assets/Equity for the year then ended, and a summary of significant accounting policies

and other explanatory information,

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financialstatements in accordance with Philippine Public Sector Accounting Standards (PPSAS),and for such internal control as management determines is necessary to enable the

preparation of financial statements that are free from material misstatements, whether due

to fraud or error.

Auditor's Responsibiliy

Our responsibility is to express an opinion on these financial statements based on our

audit. We conducted our audit in accordance with Philippine Public Sector Standards onAuditing. Those standards require that we comply with ethical requirements and plan and

perform the audit to obtain reasonable assurance that the financial statements are free

from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and

disclosures in the financial statements. The procedures selected depend on the auditor's

judgment, including the assessment of the risks of material misstatement of the financialstatements, whether due to fraud or error. in making those risk assessments, the auditor

considers internal control relevant to the entity's preparation and fair presentation of the

financial statements in order to design audit procedures that are appropriate in the

circumstances, but not for the purpose of expressing an opinion on the effectiveness of

the entity's internal control. An audit also includes evaluating the appropriateness of

accounting policies used and the reasonableness of accounting estimates made by

management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence that we have obtained is sufficient and appropriate to

provide a basis for our qualified audit opinion.

Basis for Qualified Opinion

The combined effect of the following audit observations which are discussed in detail in

Part It of this report, had affected the fair presentation of the financial statements:

I. The carrying amount of the Inventory accounts of P38,437,134.72 is unreliable due to

(a) non-reconciliation of physical count with the accounting records in NCR and

Regional Oflice (RO) VII; (b) recognition of purchases of inventories as outright

expense in NCR and ROs IX and X; (c) non-updating and non-maintenance of Stock

Ledger Cards (SLCs) and Stock Cards (SCs) in NCR, ROs VI, IX and XIII; (d) non-

conduct of physical inventory taking and non-preparation/non-submission of Report

on the Physical Count of Inventory (RPCI) in ROs V, VI, VII and IX; (e) non-

preparation of Requisition and Issue Slip (RIS) and Report of Supplies and Materials

Issued (RSMI) in RO IX; and (f) non-recognition of accountable forms as Inventories

in RO X.

2. The carrying amount of PPE of P731,236,468.28 is unreliable due to (a) erroneous

computation of depreciation in the CO and NCR; (b) unrecognized PPE totaling

-502,795.00 in CO, ROs 1, II, 111 and V and the unrecognized transfer of PPE from

CO in RO V; (c) lost/missing/unaccounted PPE of P130,709.00 in NCR; (d) non-

preparation/erroneous preparation of the Report on the Physical Count of PPE

(RPCPPE); and non-maintenance of Property Cards (PCs) and PPE Ledger Cards

(PPELCs) in NCR, ROs I, I, V, VI, VII, IX and X. Moreover, proper practices were

not observed in the management and tracking of PPE.

3. Out of the balance of the Due from GOCCs account of P93,595,255.10 as of

December 31, 2015, P86,859,771.37 pertains to the fund transferred to Philhealth,which remained unliquidated for over seven years now, thus, depriving the

government and the public of the benefits of the project to which the fund had been

released, contrary to the rules and regulations prescribed under COA Circular No. 94-

013 dated December 13, 1994 and the Memorandum of Agreement (MOA).

4. The balance of the Trust Liabilities account of P270,563,000.47 as of December 31,2015 is unreliable due to (a) non-accrual of income to the Accumulated Surplus of the

General Fund; (b) disbursements of Civil Registry System-Information Technology

Project (CRS-ITP) government share and Office of the Civil Registrar General

(OCRO) trust funds without authority from the Permanent Committee; (c) defects in

the administration of the OCRG trust funds; and (d) non-recognition of expenses.

Moreover, excess collections from sale of bid documents were not remitted to the

BTr.

2

Opinion

in our opinion, except for the effects of the matter described in the Basis for Qualified

Opinion paragraph, the financial statements present fairly, in all material respects, the

financial position of Philippine Statistics Authority as at December 31, 2015, and its

financial performance and its cash flows for the year then ended in accordance with

Philippine Public Sector Accounting Standards.

COMMISSION ON AUDIT

By:

MELINDAR. BARCIALState Auditor IV

OIC-Supervising AuditorNEDA Audit Group

May 24, 2016Commission on AuditNational Economic and Development AuthorityPasig City

3

Republic of the Philippines

Philippine Statistics Authority

Reference No. 16FASO3 152

STATEMENT OF MANAGEMENT'S RESPONSIBILITYFOR FINANCIAL STATEMENTS

(Consolidated)

The management of PHILIPPINE STATISTICS AUTHORITY is responsible for t11

information and representations contained in the accompanying Statement of Financial

Position as of December 31, 2015 and the related Statements of Financial Performance,

Statement of Cash Flows, Statement of Comparison of Budget and Actual Amounts,

Statement of Changes in Net Assets/Equity and Notes to Financial Statements for the

year then ended. The financial statements have been prepared in conformity with the

Philippine Public Sector Accounting Standards and generally accepted state accounting

principles and reflect amounts that are based on the best estimates and informed

judgment of management with an appropriate consideration to materiality.

In this regard, management maintains a system of accounting and reporting which

provides for the necessary internal controls to ensure that transactions are properly

authorized and recorded, assets are safeguarded against unauthorized use or disposition

and liabilities are recognized.

EVELYN . TOLENTINO ATTY. MARIBETH C. PILIMPINAS

Chief, Accounting Division Assistant National Statistician

Finance and Administrative Services

April 28, 2016 April 28, 2015

Date signed Date signed

CFTModlb

PSA-CVEA Building, East Avenue, Diliman, Quezon City, Philippines 1101

Telephone: (632) 462-6600 loc. 822 and 805 * Fax (632) 462 6600 loc. 825 -

www.ps.aov.ph

4

PHILIPPINE STATISTICS AUTHORITYSTATEMENT OF FINANCIAL POSITION

All FundsAs of December 31, 2015

Tn Philippine Peso

Note Amount

ASSETSCurrent Assets

Cash and Cash Equivalent 4 259,962,536.45Receivables 5 245,683,915.40

Inventories 6 38,437,134.72Other Assets 9 52,001,439.71

Total Current Assets 596,085,026.28

Non-Current Assets

Property, Plant and Equipment 7 731,236,468.28

Intangible Assets 8 158,956.43

Other Non-Current Assets 9 16,362,817.72

Total Non-Current Assets 747,758,242.43

Total Assets 1,343,843,268.71

LIABILITIES

Current Liabilities

Financial Liabilities 10 609,577,978.69

Inter-Agency Payables 11 24,194,717.23

Trust Liabilities 12 270,563,000.47

Other Payables 13 1,267,478.48

Total Current Liabilities 905,603,174.87

Total Liabilities 905,603,174.87

NET ASSETS/EQUITY

Accumulated Surplus/(Deficit) 438,240,093.84

Total Liabilities and Net Assets/Equity 1,343,843,268.71

This statement should be read in conjunction with the accompanying notes.

5

Note Amount

6

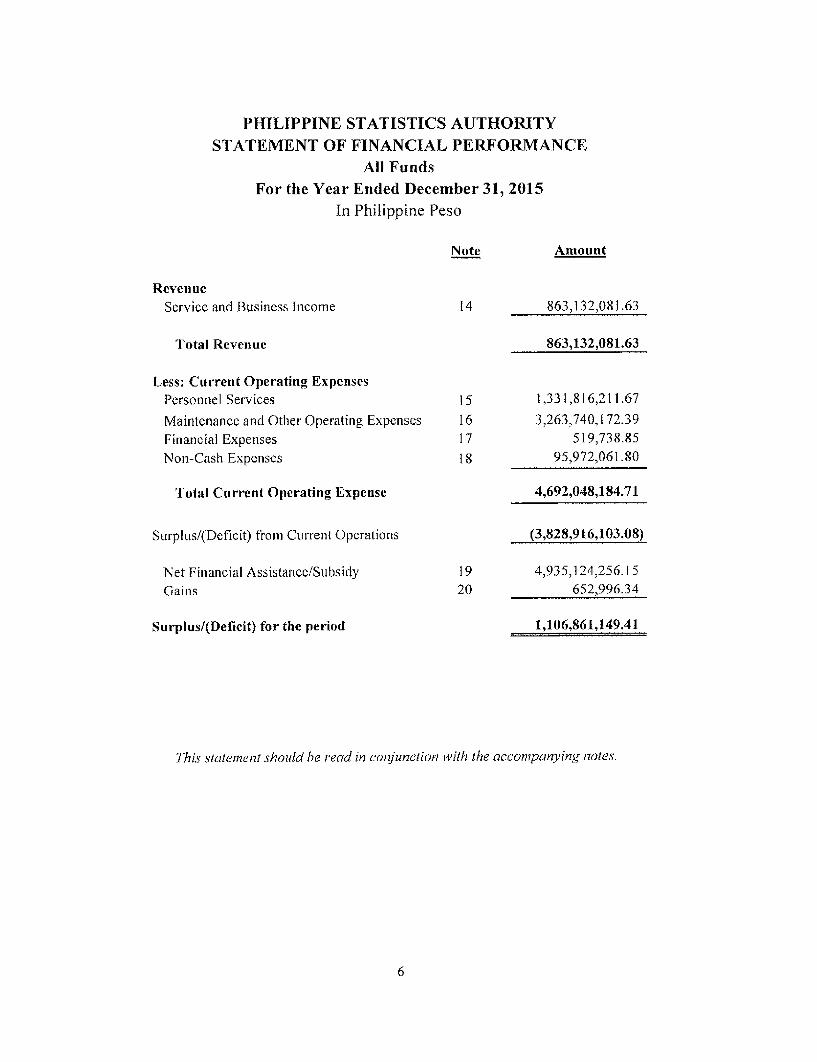

PHILIPPINE STATISTICS AUTHORITYSTATEMENT OF FINANCIAL PERFORMANCE

All FundsFor the Year Ended December 31, 2015

In Philippine Peso

Note Amount

RevenueService and Business Income 14 863,132,081.63

Total Revenue 863,132,081.63

Less: Current Operating Expenses

Personnel Services 15 1,331,816,211.67

Maintenance and Other Operating Expenses 16 3,263,740,172.39

Financial Expenses 17 519,738.85

Non-Cash Expenses 18 95,972,061.80

Total Current Operating Expense 4,692,048,184.71

Surplus/(Deficit) from Current Operations (3,828,916,103.08)

Net Financial Assistance/Subsidy 19 4,935,124,256.15

Gains 20 652,996.34

Surplus/(Deficit) for the period 1,106,861,149.41

This statement should be read in conjunction with the accompanying notes.

6

PHILIPPINE STATISTICS AUTHORITYSTATEMENT OF CASH FLOWS

All FundsFor the Year Ended December 31, 2015

tn Philippine Peso

Amount

Cash Flow from Operating ActivitiesCash Inflows

Receipt of Notice of Cash Allocation 5,430,754,717.00Collection of Income/Revenue 863,653,184.66Constructive receipt of TRA 212,723,477.92Collection of Receivables 120,175.15Receipt of Inter-Agency Fund Transfers 82,939,850.00Receipt of Intra-Agency Fund Transfers 83,497,198.63Trust Receipts 2,751,058,076.88Other Receipts 31,075,023.03Adjustments 5,356,100.85

Total Cash Inflows 9,461,177,804.12

Cash OutflowsRevert Treasury/Agency DepositsPayment of Operating Expenses 1,326,195,300.87Purchases of Inventories 26,159.50

Grant of Cash Advances 120,630,095.81Prepayments 153,777,467.53Payment of Deposits 50,000.00Payment of Accounts Payables 69,755,448.86Remittance of Personnel Benefit Contributions and Mandatory

Deductions 651,260,563.26Grant of Financial Assistance/Subsidy 2,821,948,377.00

Release of Intra-Agency Fund Transfers 71,968,081.63

Payments for trust liabilities and fund transfers 2,326,500,270.38Remittances to BTr 72,930.02

Other Disbursements 4,351,189.16Adjustments 1,724,073,613.56

Total Cash Outflows 9,270,609,497.58

Net Cash Provided by (Used in) Operating Activities 190,568,306.54

7

Amount

Cash Flows from Investing Activities:

Cash OutflowsPurchase/Construction of Property, Plant and Equipment 25,322,874.88

Total Cash Outflows 25,322,874.88

Net Cash Provided by (Used in) Investing Activities (25,322,874.88)

Increase (Decrease) in Cash and Cash Equivalents 165,245,431.66

Cash and Cash Equivalents, January 1, 2015 94,717,104.79

Cash and Cash Equivalents, December 31, 2015 259,962,536.45

8

PSA-NATIONAL STATISTICS OFFICESTATEMENT OF CHANGES IN NET ASSETS/EQUITY

All FundsFor the Year Ended December 31, 2015

In Philippine Peso

Amount

Balance at January 1, 2015 427,142,861.77

Changes in accounting policy (10,454,098.60)

Prior year adjustment/unrecorded income and expenses (485,811.35)

Restated Balance 416,202,951.82

Changes in Net Assets/Equity for Calendar Year

Adjustment of net revenue recognized directly in net assets/equity (1,037,884,768.64)Surplus for the period 1,106,861,149.41

Total Recognized revenue and expenses for the period 68,976,380.77

Others (46,939,238.75)

Balance at December 31, 2015 438,240,093.84

9

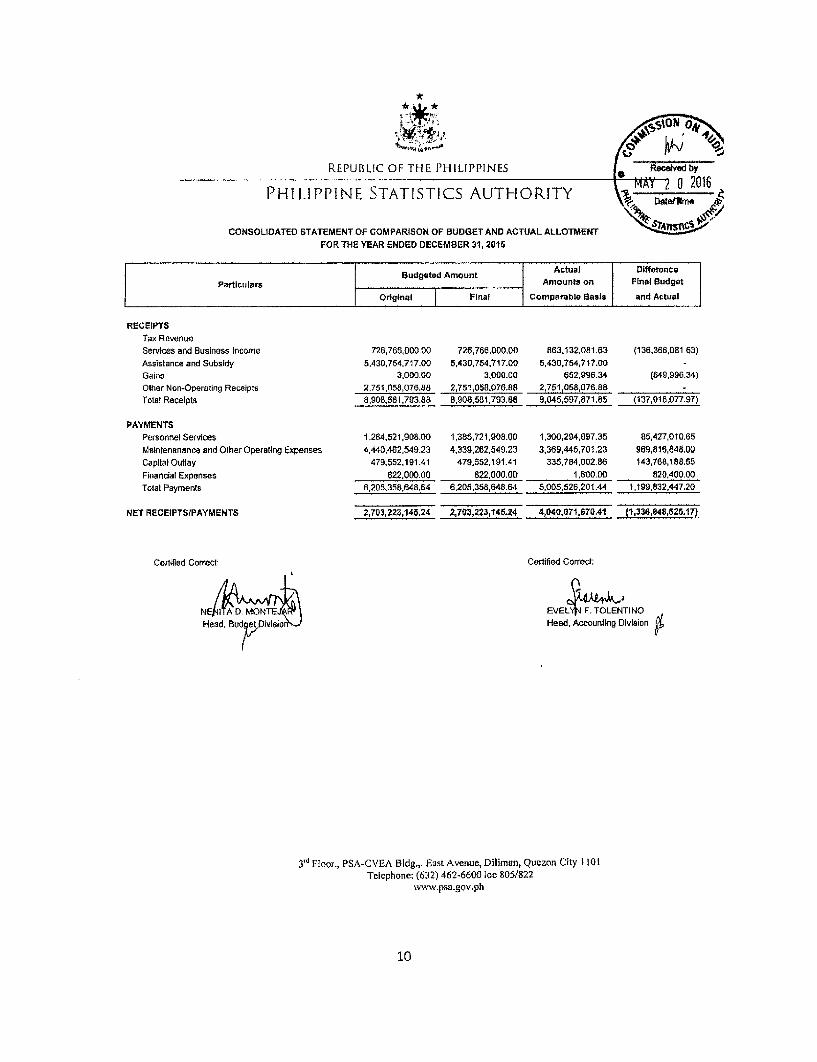

REPuBuiC OF THE PHILIPPINES -Recived by

PHILIPPINE STATISTICS AUTHORITY M S

CONSOLIDATED STATEMENT OF COMPARISON OF BUDGET AND ACTUAL ALLOTMENTFOR THE YEAR ENDED DECEMBER 31, 2015

Budgeted Amount Actual Difference

Particulars Amounts on Final Budget

Original Final Comparable Basis and Actual

RECEIPTSTax RevenueServices and Business Income 72,766,000 00 726,766,000,00 883.132.081.83 (136.366,081.63)Assistance and Subsidy 5,430,754,717,00 5,430,754,717.00 5,430,754,717.00 -

Gains 3,000.00 3,000.00 r42,996.34 (549,996.34)Oher Non-Operating Receipts 2,751,058,07B.88 2,7!1,058.076.88 2,751,058,076.88 -

Total Receipts 8,908.581,793.88 8,908,581.793.88 9,045,597,871.85 (137,016,077.97)

PAYMENTSPersonnel ServIces 1,284,521908.00 1,385,721,908.00 1,300.294,897,35 85,427,010,65Maintenanance and Other Operating Expenses 4,440,462,549.23 4,339,262,549.23 3,369,445,701.23 969,816,848.90Capital Outlay 479,552,191.41 479,552,191.41 335,784,002.86 143,768,188,55Financial Expenses 822,000.00 822,000.00 1,600.00 820,400.00Total Payments 6,205,358,648.54 6,205,368,648.64 5,005,526,201.44 1,199,832,447.20

NET RECEPTSIPAYMENTS 2,703,223,145,24 ,703,223,14.24 4,040,071.670.41 (1,336,848,525.17)

Certified Correct: Certified Correct:

N IAD MONTE EVEL F. TOLNTI NO

Head, Bud Division Head, Accounting Division

3C Floor., PSA-CVEA Bldg., East Avenue, Diliman, Quezon City 1101Telephone: (632) 462-6600 loc 805/822

www.psa.gov.ph

10

t Republic of the Philippines

Philippine Statistics Authority

NOTES TO CONSOLIDATED FINANCIAL STATEMENTSFor the Year ended December 31, 2015

General Information/Agency Profile

The consolidated financial statements of the Philippine Statistics Authority (PSA) wereauthorized for issue on April 28, 2016 as shown in the Statement of ManagementResponsibility for Financial Statements signed by Atty. Maribeth C. Pilimpinas,Assistant National Statistician - Financial and Administrative Service, Civil

Registration and Central Support Office.

The PSA, pursuant to its mandate as the primary statistical agency of the governmentand its functions as stipulated in Republic Act No. 10625 and its Implementing Rules

and Regulations, produced timely, reliable and relevant official statistics, and provided

statistical products and services to support the formulation of development plans and

programs, decision making, research and public policy discussion.

It shall plan, develop, prescribe, disseminate and enforce policies, rules and regulations

and coordinate government-wide programs governing the production of official

statistics, general purpose-statistics, and civil registration services.

It shall primarily responsible for all national censuses and surveys, sectoral statistics,

consolidation of selected administrative recording systems and compilation of national

accounts.

In addition, pursuant to Article 7 of the Family Code, the PSA also issues certificates of

registration of authority to solemnize marriage to solemnizing officers.

The Agency's registered address is CVEA Bldg., East Avenue, Diliman, Quezon City,1101.

2. Statement of Compliance and Basis of Preparation of Financial Statements

The consolidated financial statements have been prepared in accordance with and

comply with the Philippine Public Sector Accounting Standards (PPSAS) issued by the

Commission on Audit per COA Resolution No. 2014-003 dated January 24, 2014,

The consolidated financial statements have been prepared on the basis of historical cost.

The Statement of Cash Flows is prepared using the direct method.

11

3. Summary of Significant Accounting Policies

3.1 Basis of accounting

The consolidated financial statements are prepared on an accrual basis in

accordance with the Philippine Public Sector Accounting Standards (PPSAS),

3.2 Consolidation

* Consolidated Entities

The consolidated financial statements reflect the assets, liabilities, revenues,and expenses of the Central and Regional Offices.

3.3 Financial instruments

a. Financial assets

Initial recognition and measurement

Financial assets within the scope of IPSAS 29 Financial Instruments:

Recognition and Measurement are classified as financial assets at fair value

through surplus or deficit, loans and receivables, held-to-maturity

investments or available-for-sale financial assets, as appropriate. PSA

determines the classification of its financial assets at initial recognition.

PSA's financial assets include: cash and short-term deposits and other

receivables.

Subsequent measurement

The subsequent measurement of financial assets depends on their

classification.

Derecognition

PSA derecognizes a financial asset or, where applicable, a part of a financial

asset or part of PSA of similar financial assets when:

* The rights to receive cash flows from the asset have expired or is waived.

* PSA has transferred its rights to receive cash flows from the asset or has

assumed an obligation to pay the received cash flows in full without

material delay to a third party; and either (a) PSA has transferred

substantially all the risks and rewards of the asset; or (b) PSA has neither

transferred nor retained substantially all the risks and rewards of the

12

asset, but has transferred control of the asset.

Impairment oJfinancial assets

PSA assesses at each reporting date whether there is objective evidence that a

financial asset or a group of financial assets is impaired. A financial asset or

a group of financial assets is deemed to be impaired if, and only if, there is

objective evidence of impairment as a result of one or more events that has

occurred after the initial recognition of the asset (an incurred 'loss event')

and that loss event has an impact on the estimated future cash flows of thefinancial asset or the group of financial assets that can be reliably estimated.Evidence of impairment may include the following indicators:

* The debtors or a group of debtors are experiencing significant financial

difficulty

* Default or delinquency in interest or principal payments

* The probability that debtors will enter bankruptcy or other financialreorganization

* Observable data indicates a measurable decrease in estimated future cash

flows (e.g. changes in arrears or economic conditions that correlate with

defaults)

b. Financial liabilities

Initial recognition and measurement

Financial liabilities within the scope of PPSAS 29 are classified as financial

liabilities at fair value through surplus or deficit or loans and borrowings, as

appropriate. PSA determines the classification of its financial liabilities at

initial recognition.

All financial liabilities are recognized initially at fair value and, in the case of

loans and borrowings, plus directly attributable transaction costs.

The PSA's financial liabilities include trade and other payables.

Subsequent measurement

The measurement of financial liabilities depends on their classification.

13

Derecognition

A financial liability is derecognized when the obligation under the liability is

discharged or cancelled or expires.

When an existing financial liability is replaced by another from the same

lender on substantially different terms, or the terms of an existing liability are

substantially modified, such an exchange or modification is treated as a

derecognition of the original liability and the recognition of a new liability,

and the difference in the respective carrying amounts is recognized in surplus

or deficit.

c. Offsetting of financial instruments

Financial assets and financial liabilities are offset and the net amount

reported in the consolidated statement of financial position if, and only if,

there is a currently enforceable legal right to offset the recognized amounts

and there is an intention to settle on a net basis, or to realize the assets and

settle the liabilities simultaneously.

3.4 Cash and Cash Equivalents

Cash and cash equivalents comprise cash on hand and cash at bank, deposits on

call and highly liquid investments with an original maturity of three months or

less, which are readily convertible to known amounts of cash and are subject to

insignificant risk of changes in value. For the purpose of the consolidated

statement of cash flows, cash and cash equivalents consist of cash and short-term

deposits as defined above, net of outstanding bank overdrafts.

3.5 Inventories

Inventory is measured at cost upon initial recognition. To the extent that

inventory was received through non-exchange transactions (for no cost or for a

nominal cost), the cost of the inventory is its fair value at the date of acquisition.

Inventories are recognized as an expense when deployed for utilization or

consumption in the ordinary course of operations of the PSA.

3.6 Property, Plant and Equipment (PPE)

Recognition

An item is recognized as PPE if it meets the characteristics and recognition

criteria as such. The characteristics of PPE are as follows:

14

* tangible items;

* are held for use in the production or supply of goods or services, for rental toothers, or for administrative purposes; and

* are expected to be used during more than one reporting period.

An item of PPE is recognized as an asset if:

* It is probable that future economic benefits or service potential associatedwith the item will flow to the entity; and

* The cost or fair value of the item can be measured reliably.

Measurement at Recognition

An item recognized as PPE is measured at cost.

A PPE acquired through non-exchange transaction is measured at its fair value asat the date of acquisition.

The cost of the PPE is the cash price equivalent or, for PPE acquired through

non-exchange transaction its cost is its fair value as at recognition date.

Cost includes the following:

* Its purchase price, including import duties and non-refundable purchase

taxes, after deducting trade discounts and rebates;

* expenditure that is directly attributable to the acquisition of the items; and

* initial estimate of the costs of dismantling and removing the item and

restoring the site on which it is located, the obligation for which an entity

incurs either when the item is acquired, or as a consequence of having used

the item during a particular period for purposes other than to produce

inventories during that period.

Measurement After Recognition

After recognition, all PPE are stated at cost less accumulated depreciation and

impairment losses.

When significant parts of PPE are required to be replaced at intervals, PSA

recognizes such parts as individual assets with specific useful lives and

depreciates them accordingly. Likewise, when a major repair/replacement is

done, its cost is recognized in the carrying amount of the PPE as a replacement if

15

the recognition criteria are satisfied. All other repair and maintenance costs are

recognized as expense in surplus or deficit as incurred.

Depreciation

Each part of an item of PPE with a cost that is significant in relation to the total

cost of the item is depreciated separately.

The depreciation charge for each period is recognized as expense unless it is

included in the cost of another asset.

Initial Recognition of Depreciation

Depreciation of an asset begins when it is available for use such as when it is in

the location and condition necessary for it to be capable of operating in the

manner intended by management.

For simplicity and to avoid proportionate computation, the depreciation is for

one month if the PPE is available for use on or before the 1 5th of the month.

However, if the PPE is available for use after the 15th of the month, depreciation

is for the succeeding month.

Depreciation Method

The straight line method of depreciation is adopted unless another method is

more appropriate for agency operation.

Estimated Useful Life

PSA uses the Schedule on the Estimated Useful Life of PPE by classification

prepared by COA.

The PSA uses a residual value equivalent to at least 10 percent of the cost of the

PPE.

Impairment

An asset's carrying amount is written down to its recoverable amount, or

recoverable service amount, if the asset's carrying amount is greater than its

estimated recoverable service amount.

Derecognition

PSA derecognizes items of PPE and/or any significant part of an asset upon

disposal or when no future economic benefits or service potential is expected

from its continuing use. Any gain or loss arising on derecognition of the asset

16

(calculated as the difference between the net disposal proceeds and the carrying

amount of the asset) is included in the surplus or deficit when the asset is

derecognized.

3.7 Changes in accounting policies and estimates

PSA recognizes the effects of changes in accounting policy retrospectively. The

effects of changes in accounting policy are applied prospectively, if

retrospective, application is impractical.

PSA recognizes the effects of changes in accounting estimates prospectively by

including in surplus or deficit.

The PSA corrects material prior period errors retrospectively in the first set of

financial statements authorized for issue after their discovery by:

* Restating the comparative amounts for prior period(s) presented in which the

error occurred; or

* If the error occurred before the earliest prior period presented, restating the

opening balances of assets, liabilities and net assets/equity for the earliest

prior period presented.

3.8 Foreign currency transactions

Transactions in foreign currencies are initially recognized by applying the spot

exchange rate between the function currency and the foreign currency at the

transaction.

At each reporting date:

* Foreign currency monetary items are translated using the closing rate;

* Nonmonetary items that are measured in terms of historical cost in a foreign

currency shall be translated using the exchange rate at the date of the

transaction; and

* Nonmonetary items that are measured at fair value in a foreign currency shall

be translated using the exchange rates at the date when the fair value was

determined.

Exchange differences arising (a) on the settlement of monetary items, or (b) on

translating monetary items at rates different from those at which they were

translated on initial recognition during the period or in previous financial

statements, are recognized in surplus or deficit in the period in which they arise,

except as those arising on a monetary item that forms part of a reporting entity's

17

net investment in a foreign operation.

3.9 Revenue from non-exchange transactions

Recognition and Measurement ofAssets from Non-Exchange Transactions

An inflow of resources from a non-exchange transaction, other than services in-

kind, that meets the definition of an asset are recognized as an asset if the

following criteria are met:

* It is probable that the future economic benefits or service potential associated

with the asset will flow to the entity; and

* The fair value of the asset can be measured reliably.

An asset acquired through a non-exchange transaction is initially measured at

its fair value as at the date of acquisition.

Recognition of Revenue from Non-Exchange Transactions

An inflow of resources from a non-exchange transaction recognized as an asset

is recognized as revenue, except to the extent that a liability is also recognized in

respect of the same inflow.

Fees and fines not related to taxes

PSA recognizes revenues froin fees and fines, except those related to taxes,

when earned and the asset recognition criteria are met, Deferred income is

recognized instead of revenue if there is a related condition attached that would

give rise to a liability to repay the amount.

Other non-exchange revenues are recognized when it is probable that the future

economic benefits or service potential associated with the asset will flow to the

entity and the fair value of the asset can be measured reliably.

Transfers

PSA recognizes an asset in respect of transfers when the transferred resources

meet the definition of an asset and satisfy the criteria for recognition as an asset,

except those arising from services in-kind.

Transfersfron other government entities

Revenues from non-exchange transactions with other government entities and

the related assets are measured at fair value and recognized on obtaining control

of the asset (cash, goods, services and property) if the transfer is free from

18

conditions and it is probable that the economic benefits or service potentialrelated to the asset will flow to the PSA and can be measured reliably.

3.10 Revenue from Exchange Transactions

Afeasurement of Revenue

Revenue shall be measured at the fair value of the consideration received orreceivable.

Interest income

Interest income pertains to interest earned from bank accounts maintained byPSA Central, Regional and Provincial Offices. It is accrued using the simpleinterest method.

3.11 Budget information

The annual budget is prepared on a cash basis and is published in the

government website.

As a result of the adoption of the cash basis for budgeting purposes, a separate

Statement of Comparison of Budget and Actual Amounts is presented showing

the basis, timing or entity differences.

3.12 Impairment of Non-Financial Assets

Impairment of cash-generating assets

At each reporting date, PSA assesses whether there is an indication that an asset

may be impaired. If any indication exists, or when annual impairment testing for

an asset is required, PSA estimates the asset's recoverable amount. An asset's

recoverable amount is the higher of an asset's or cash-generating unit's fair value

less costs to sell and its value in use and is determined for an individual asset,unless the asset does not generate cash inflows that are largely independent of

those from other assets or groups of assets.

Where the carrying amount of an asset or the cash-generating unit (CGU)

exceeds its recoverable amount, the asset is considered impaired and is written

down to its recoverable amount.

In assessing value in use, the estimated future cash flows are discounted to their

present value using a discount rate that reflects current market assessments of the

time value of money and the risks specific to the asset. In determining fair value

less costs to sell, recent market transactions are taken into account, if available.

If no such transactions can be identified, an appropriate valuation model is used.

19

For assets, an assessment is made at each reporting date as to whether there isany indication that previously recognized impairment losses may no longer existor may have decreased. If such indication exists, PSA estimates the asset's orcash-generating unit's recoverable amount.

A previously recognized impairment loss is reversed only if there has been achange in the assumptions used to determine the asset's recoverable amountsince the last impairment loss was recognized. The reversal is limited so that thecarrying amount of the asset does not exceed its recoverable amount, nor exceed

the carrying amount that would have been determined, net of depreciation, had

no impairment loss been recognized for the asset in prior years. Such reversal is

recognized in surplus or deficit.

Impairment of non-cash-generating assets

PSA assesses at each reporting date whether there is an indication that a non-

cash-generating asset may be impaired. If any indication exists, or when annual

impairment testing for an asset is required, PSA estimates the asset's recoverable

service amount. An asset's recoverable service amount is the higher of the non-

cash generating asset's fair value less costs to sell and its value in use.

Where the carrying amount of an asset exceeds its recoverable service amount,

the asset is considered impaired and is written down to its recoverable service

amount.

PSA classifies assets as cash-generating assets when those assets are held with

the primary objective generating a commercial return. Therefore, non-cash

generating assets would be those assets from which PSA-NSO does not intend

(as its primary objective) to realize a commercial return.

3.13 Employee benefits

The employees of PSA are members of the Government Service Insurance

System (GSIS), which provides life and retirement insurance coverage.

PSA recognizes the undiscounted amount of short term employee benefits, like

salaries, wages, bonuses, allowance, etc., as expense unless capitalized, and as a

liability after deducting the amount paid.

PSA recognizes expenses for accumulating compensated absences when these

are paid (commuted or paid as terminal leave benefits). Unused entitlements that

have accumulated at the reporting date are not recognized as expense. Non-

accumulating compensated absences, like special leave privileges, are not

recognized.

20

4. Cash and Other Cash Equivalent

Accounts Amount

Cash on Hand 4a 2,031,228.62Cash in Bank - Local Currency 210,799,462.37Cash in Bank - Foreign Currency 3,994,723.14

Cash - Treasury/Agency Deposits, Trust 43,137,122.32

Total P259,962,536.45

4.1 Cash on hand

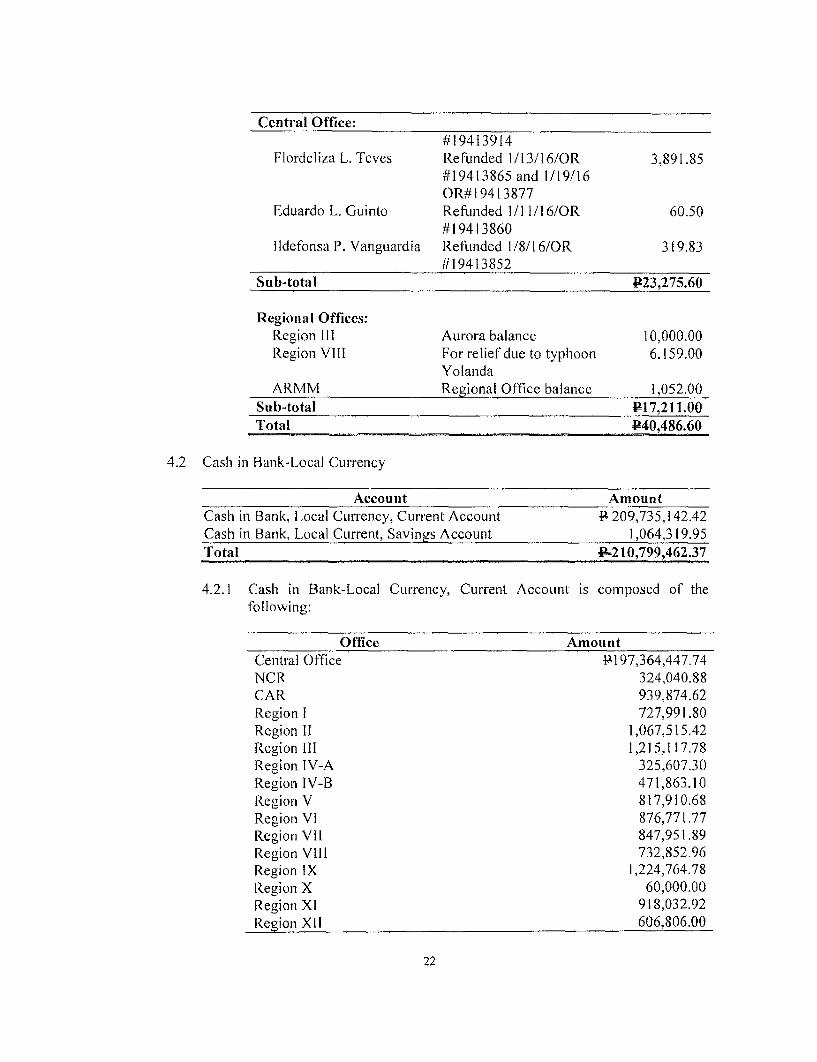

Account AmountCash - Collecting Officer P1,990,742.02Petty Cash 40,486.60

Total $2,031,228.62

4.1.1 Cash-Collecting Officers account is composed of collections from the

refund of cash advances, sale of publications, data request, sale of civil

registry forms and Census Serbilis Outlets as follows:

Office Amount

Central Office R1,845,066.97NCR 10,420.00

CAR 3,655.09Region I 11,330.00Region 11 3,000.00Region 111 80,305.00Region VII 28,836.79Region VIII 8,128.17

Total P1,990,742.02

4.1.2 Petty Cash Fund account is composed of balances as of year-end which

were refunded as follows:

Central Office:Amelita D. Abalos Refunded 3/2/16 3,806.00

OR#1 9413987Joseph P. Cajita Refunded 1/18/16/ OR9 2,469.25

1119413873Marisol T. Fallarme On maternity leave 2,035.80Edward Eugenio P.Lopez Dee Refunded 1/6/ 16/OR 6,979.50

#19413880MaribethC. Pilimpinas Refunded 1/16/16/ OR 1.82

#19413843Dulce A. Regala Refunded 2/1/16/OR 3,711.05

21

Central Office:#19413914

Flordeliza L. Teves Refunded 1/13/16/OR 3,891.85#19413865 and 1/19/16OR#19413877

Eduardo L. Guinto Refunded I/I 1/16/OR 60.50#19413860

Ildefonsa P. Vanguardia Refunded 1/8/16/OR 319.83#19413852

Sub-total P23,275.60

Regional Offices:Region III Aurora balance 10,000.00Region Vill For relief due to typhoon 6,159.00

YolandaARMM Regional Office balance 1,052,00

Sub-total P17,211.00Total P40,486.60

4.2 Cash in Bank-Local Currency

Account Amount

Cash in Bank, Local Currency, Current Account 4209,735,142.42Cash in Bank, Local Current, Savings Account 1,064,319.95Total P-210,799,462.37

4.2.1 Cash in Bank-Local Currency, Current Account is composed of thefollowing:

Office AmountCentral Office P197,364,447.74NCR 324,040.88CAR 939,874.62Region 1 727,991.80Region II 1,067,515.42Region 111 1,215,117.78Region IV-A 325,607.30Region IV-B 471,863.10Region V 817,910.68Region VI 876,771.77Region VII 847,951.89Region Vill 732,852.96Region IX 1,224,764.78Region X 60,000.00Region XI 918,032.92Region XII 606,806.00

22

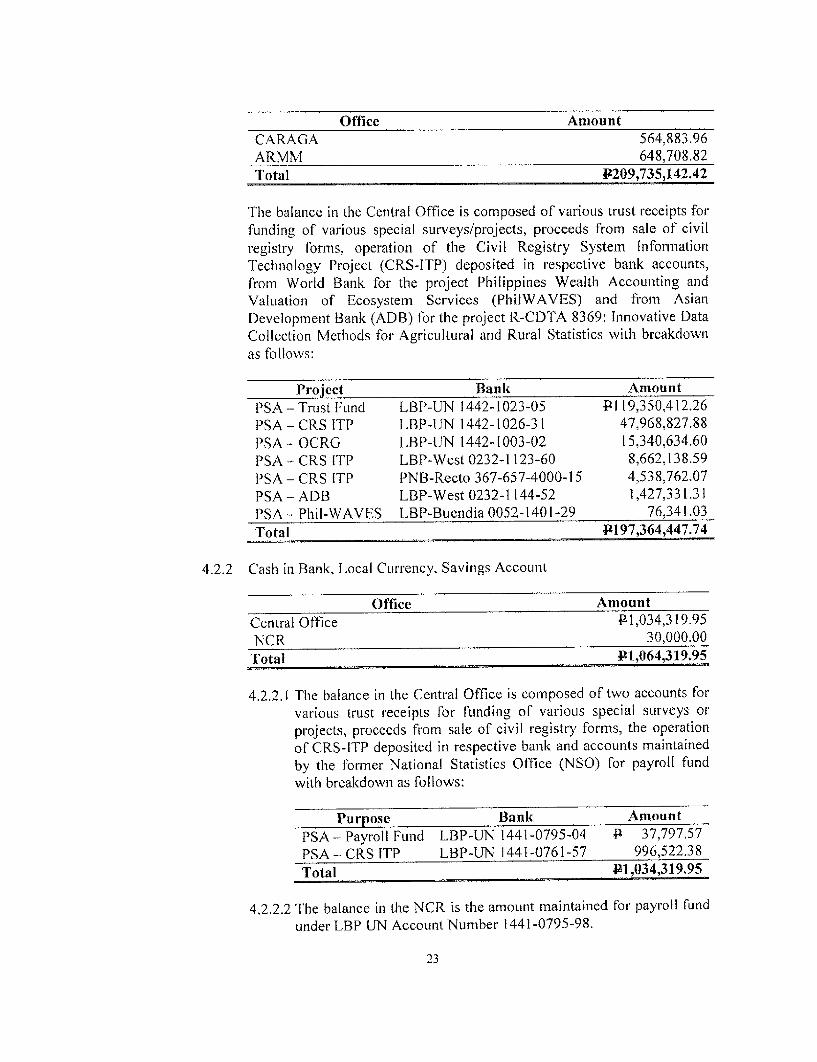

Office AmountCARAGA 564,883.96ARMM 648,708.82

Total P209,735,142.42

The balance in the Central Office is composed of various trust receipts for

funding of various special surveys/projects, proceeds from sale of civil

registry forms, operation of the Civil Registry System Information

Technology Project (CRS-ITP) deposited in respective bank accounts,from World Bank for the project Philippines Wealth Accounting and

Valuation of Ecosystem Services (PhilWAVES) and from Asian

Development Bank (ADB) for the project R-CDTA 8369: Innovative Data

Collection Methods for Agricultural and Rural Statistics with breakdown

as follows:

Project Bank Amount

PSA - Trust Fund LBP-UN 1442-1023-05 P119,350,412.26

PSA - CRS ITP LBP-UN 1442-1026-31 47,968,827.88

PSA - OCRG LBP-UN 1442-1003-02 15,340,634.60

PSA - CRS ITP LBP-West 0232-1123-60 8,662,138.59

PSA - CRS ITP PNB-Recto 367-657-4000-15 4,538,76207

PSA - ADB LBP-West 0232-1 144-52 1,427,331.31

PSA - Phil-WAVES LBP-Buendia 0052-1401-29 76,341.03

Total P197,364,447.74

4.2.2 Cash in Bank, Local Currency, Savings Account

Office Amount

Central Office P1,034,319.95

NCR 30,000.00

Total P1,064,319.95

4.2.2.1 The balance in the Central Office is composed of two accounts for

various trust receipts for funding of various special surveys or

projects, proceeds from sale of civil registry forms, the operation

of CRS-ITP deposited in respective bank and accounts maintained

by the former National Statistics Office (NSO) for payroll fund

with breakdown as follows:

Purpose Bank Amount

PSA - Payroll Fund LBP-UN 1441-0795-04 P 37,797.57

PSA - CRS ITP LBP-UN 1441-0761-57 996,522.38

Total R1,034,319.95

4.2.2.2 The balance in the NCR is the amount maintained for payroll fund

under LBP UN Account Number 1441-0795-98.

23

4.3 Cash in Bank-Foreign Currency

4.3.1 Cash in Bank-Foreign Currency, Savings account is composed of three

bank accounts, namely: (a) account maintained by the former NSO for

overseas remittances of payments for requests of civil registry documents,

(b) account maintained by the former Bureau of Agricultural Statistics

(BAS) for R-CDTA 8369: Innovative Data Collection Methods for

Agricultural and Rural Statistics Project, and (c) account maintained by

the former National Statistical Coordination Board (NSCB) for

PhilWAVES Project. In the case of the account previously maintained by

NSO, after deducting payment for the document, any excess

amount/balance is being withdrawn and transferred to the account of the

Treasurer of the Philippines as income.

Purpose Bank Amount

PSA - CRS ITP LBP West 0234-0026-35 $ 1,522.97

PSA - ADB LBP West 0234-0052-27 110.82

PSA - Phil WAVES LBP Buendia 0054-0025-30 90,721.31

Total $92,355.10

4.4 Treasury/Agency Cash

Account Amount

Cash - Treasury/Agency Deposits, Trust R 28,594,487.30

Cash - Modified Disbursement Scheme (MDS) 14,083,236.18

Cash - Tax Remittance Advice 459,398.84

Total a43,137,122.32

44.1 Cash - Treasury/Agency Deposits, Trust is the balance of Central Office

as of year-end.

4.4.2 Cash - Modified Disbursement System (MDS), Regular is composed of

the following:

Office Amount

Central Office 9 771,856.67

CAR 8,764,543.05

Region V 39,278.95

Region VI 7,525.00

Region VII 3,949,568.63

Region IX 485,100,00

ARMM 65,363.88

Total 4A14,083,236.18

24

4.4.3 Cash - Tax Remittance Advice account represents CARAGA'swithholding taxes for the month of December for remittance to BIR in thenext month.

5. Receivables

5.1 Inter-agency Receivables

Account AmountDue from NGAs $150,802,993.00Due from GOCCs 93,595,255.10Due from LGUs 259,270.00Total P244,657,518.10

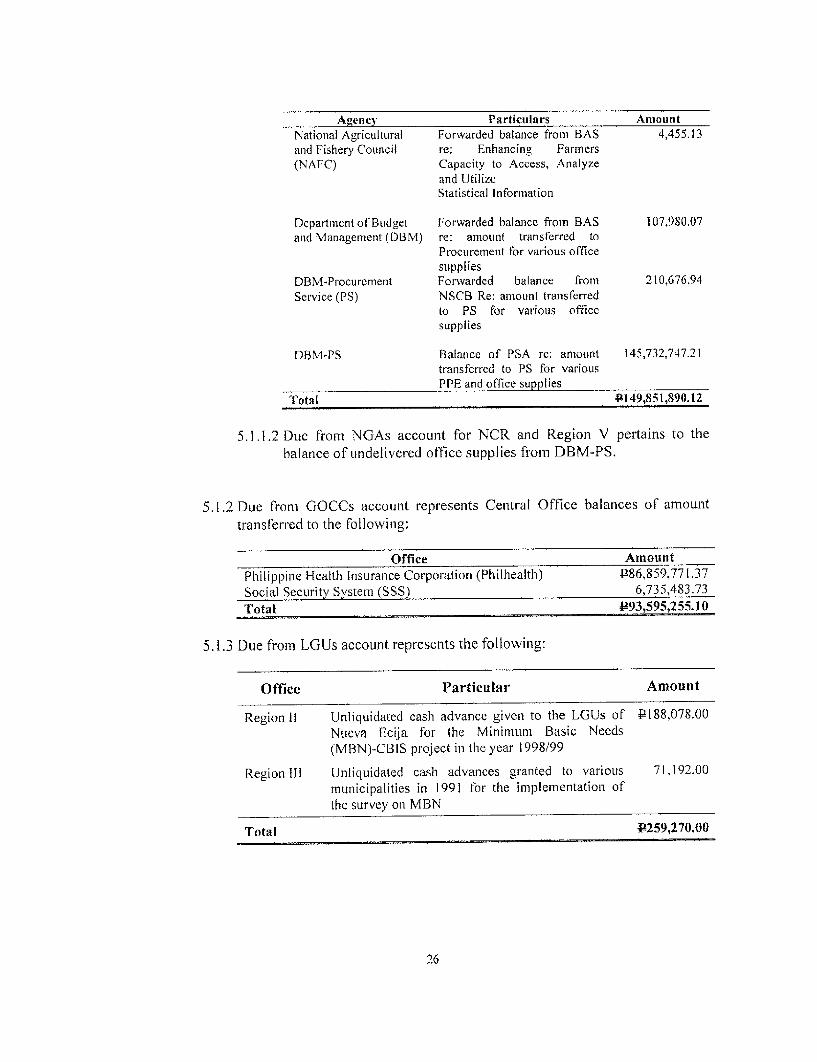

5.1.1 Due from NGAs account represents the following balances:

Office AmountCentral Office P149,851,890.12NCR 843,238.97Region V 107,863.91Total P150,802,993.00

5. 1.1.1 Due from NGAs account for Central Office is composed of thefollowing balances:

Agency Particulars Amount

Securities and Exchange Forwarded balance from P 1,315.14

Commission (SEC) NSCB re: Corporate StatisticsProject

Philippine Statistical Forwarded balance from 1,070.84

Research and Training NSCB re: StatisticalInstitute (PSRTI) Manpower Development

Program (SNDP)

PSRTI Forwarded balance from 2,051.01NSCB re: Research andDevelopment Grants underPSS Data and ServiceImprovement (RDGPDSI)

PSRTI Forwarded balance from BAS 3,791,593.78re: Livestock and Poultryinformation and EarlyWarning System for CY 2015(LPI-EWS)

25

Agency Particulars Amount

National Agricultural Forwarded balance from BAS 4,455.13

and Fishery Council re: Enhancing Farmers(NAFC) Capacity to Access, Analyze

and UtilizeStatistical Information

Department of Budget Forwarded balance from BAS 107,980.07

and Management (DBM) re: amount transferred toProcurement for various officesupplies

DBM-Procurement Forwarded balance from 210,676.94

Service (PS) NSCB Re: amount transferredto PS for various officesupplies

DBM-PS Balance of PSA re: amount 145,732,747.21transferred to PS for variousPPE and office supplies

Totai P149,851,890.12

5.1.1.2 Due from NGAs account for NCR and Region V pertains to the

balance of undelivered office supplies from DBM-PS.

5.1.2 Due from GOCCs account represents Central Office balances of amount

transferred to the following:

office Amount

Philippine Health Insurance Corporation (Philhealth) P86,859,771.37

Social Security System (SSS) 6,735,483,73

Total P93,595,255.10

5.1.3 Due from LGUs account represents the following:

Office Particular Amount

Region 11 Unliquidated cash advance given to the LGUs of P188,078.00

Nueva Ecija for the Minimum Basic Needs

(MBN)-CBIS project in the year 1998/99

Region Ill Unliquidated cash advances granted to various 71,192.00municipalities in 1991 for the implementation of

the survey on MBN

Total P259,270.00

26

5.2 Other Receivables

Account AmountReceivables-Disallowances/Charges 4- 845,160.32Due from Officers and Employees 44,043.38Other Receivables 137,193.60Total P1,026,397.30

5.2.1 Receivable-Disallowance/Charges

Office AmountCentral Office 42718,284.91Region 1 45,300.00Region IX 81,575.41Total P845,160.32

5.2.1.1 Receivable-Disallowance/Charges for Central Office is composedof the following balances:

Name Particulars AmountNSIC I Forwarded balance from A. Torres PI11,925.58

(previous NSCB Accountant)1993 PlA 72.47Rogelio Glorioso 4,119.66Rigor Magtanong 167.20Various BAS employces Consultant services of BAS 702,000.00Total P718,284.91

5.2.1.2 Receivables-Disallowance/Charges for Regions I and IX iscomposed of the following balances:

Office Particulars AmountRegion I Service allowance and training P45,300.00

allowanceRegion IX Service allowance, traveling and 81,575.41

electricity expenses disallowedTotal P126,875.41

5.2,2 Due from Officers and Employees

Office AmountCentral Office P43,143.38

Region V 900,00

Total P44,043.38

27

5.2.2.1 Due from Officers and Employees Central Office pertains to theforwarded balance from BAS with details as follows:

Name Amount RemarksMorano, Eduardo P40,203.38 With Letters to COARamirez, Roy 2,940.00 for the relief

Total P43,143.38

5.2.2.2 Due from Officers and Employees of Region V pertains to the

receivable balance from Bookkeeper of Sorsogon with details as

follows:

Name Remarks Amount

Carol Labanan Unrecorded bank service charge P420.00for snapshot last November 2012

Overpayment of Check no. 808408 480.00dated March 4, 2013, corrected perbooks but the checks was alreadyencashed by the payee, paymentwill be made in 2016.

Total P900.00

5.2.3 Other Receivables

Office Amount

Central Office P 55,505.70Region V 81,687.90

Total P137,193.60

5.2.3.1 Other Receivables account of Central Office pertains to the

forwarded balance from NSCB with details as follows:

Name Amount RemarksBaban, Jimmy P 1,890.00 Coordinated with

Nefulda, Jaime 10,798.67 Regional Directors

Roscom, Brigida 6,964.00 (RDs)Reala, Jeremias 1,890,00Nimeno, Romeo 2,051.97 DeceasedEstrella, Domingo 31,174.95 DeceasedPenpillo, Presentacion 736.11 Coordinated with RDs

Total P55,505.70

28

5.2.3.2 Other Receivables account of Region V pertains to the forwardedbalance from Albay Electric Cooperative (ALECO) with details asfollows:

Office Particulars AmountRegional Office Security Deposit for P58,062.20

Albay electricity expense from 23,625.70ALECO

Total P81,687.90

6. Inventories Held for Consumption

Account Amount

Ofice Supplies Inventory P31,586,306.25Accountable Forms Inventory 85,746.60

Other Supplies and Materials Inventory 6,765,081.87

Total P38,437,134.72

6.1 Office Supplies Inventory

Office Amount

Central Office R 1,373,126.66

NCR 1,975,040.43

CAR 1,580,582.61

Region I 317,313.21

Region II 3,130,521.36

Region 111 1,845,094.23

Region IV-A 2,636,042.34

Region IV-B 781,362.93

Region V 2,353,931.29

Region VI 2,714,76119

Region ViI 1,627,636.39

Region VIII 4,879,186.62

Region X 111,539.30

Region XI 2,476,902.16

Region XII 1,503,036.66

CARAGA 2,280,228.87

Total P31,586,306.25

6.2 Accountable Forms, Plates and Stickers Inventory is the balance of CO Official

Receipts for distribution to the field offices.

29

6.3 Other Supplies and Materials Inventory

Office Amount

Central Office P 370,303.09

CAR 61,978.34

Region 1 449,209.11

Region Ill 1,764,348.91

Region IV-A 2,970.00

Region V 474,967.20

Region VIII 69,917.00

Region IX 1,981,684.86

Region X 5,340.45

Region XI 917,531.50

Region XlI 605,463.86

CARAGA 61,367.55

Total P6,765,081.87

7. Property, Plant and Equipment

n iulding and Pamnn e as Assets Construwttr Toall':itteal,e ladolah Oiie ielry and TerAin'olnvinn Flnin u1w An I'Mperty, Plat

PAr-giculars andSncurs IEqFquipmn Equipment Soaks ImprvenMtts in PrngArsn and Eqipmet

Carryint Amount, 12 245,245 42 7,017,44R I 102,41,41133 69 297.904,75S 25 50p01,595 45 45.322,673 45 365,11680 176,591,711 52 23,849009 85 705765,039 64

Jaauary I, 20 15AddeiiosA ddtioqai- Ln 137,086 646 02 1,8c7,531 74 10.25,996 91 2,661,962 03 R6,356,455 06 5,106,568 04 25,145.150 0

Total 2,245.25 42 7.037,442 18 102,433.4556) 424,99[,3207 51,821,127 19 56,148,670 39 3,027,07R 83 262,950.166 58 28,55.77 89 951,610,100 24

Di5posal1 (388,4919 61) (108,686,118 1I) (12,440,10284) (1,77 .45 865 (40,05000) (1,461,011 86) (124.807,8093)

Deprecimanon (525.923 52) (2,586,%07 88) (70.362.o0 66) (D424,403 79) (0.127,260 13) (1,f591.87 57) (4,64672 II 9.565,913 00)

Carrying

DA,cen ber 3t,2015 A; (e r 12,245,295.42 6,123,02.03 99,846,465.51 245,942,673.30 31,956,460.56 48,050,256.40 1,295,141.26 262,950,166.58 22,926,03,52 731,236,468.28

Sitenent ofFinancialPNsilion)Grss Cost (AssItacouunI balhnce 12,245.29 42 11,635,06 22 114,768,410 19 667,034,167 31 150,326.112 15 10.667,777 10 2.211,769 55 262,950,166 50 5,601.38648 1,165,440,160 08

per Statenie ofFinaniaal Posttion

De 01treao 5,512,041 19 14,)21,953 30 421,091,494 01 118,369.051 59 42.617,i2078 916.62829 30,774,40250 6142205,631 0

Allownne forInipairmwntCwrryingAmo-nt,lece.AbA,ee 31,

20V0 (As per 12,245,295.42 6.123,025.03 99,846,465.81 245,942,673.30 31,956,460.56 48.050.256.40 1,295,141.26 262,950.166.55 22,826,93.92 731,236,448.28

Smatemen ofFinanciialPanlian)

7.1 Land account represents the value and related costs of NSO lot at East Avenue,

Dilirnan, Quezon City with a total area of 20,001 square meters as per TCT No.

40608.

7.2 Land Improvements

Office Cost Accumulated Carrying AmountDepreciation

Central Office P 8,184,854.49 P3,923,001.01 P4,261,853.48

30

AccumulatedOffice Cost Carrying Amount

DepreciationRegion I 1t052,640.76 492,786.23 559,854.53

Region 111 2,397,570.97 1,096,253.95 1,301,317.02

Total P11,635,066.22 P5,512,041.19 46,123,025.03

7.3 Buildings

AccumulatedOffice Cost Carrying Amount

Depreciation

Central Office A 86,634,930.24 P11,598,003.01 P75,036,927.23

Region 111 28,133,488.95 3,323,950.37 24,809,538.58

Total P114,768,419.19 P14,921,953.38 $99,846,465.81

7.4 Machineries and Equipment

Accumulated Carrying

Depreciation Amount

Office Equipment P115,694,549.08 P 64,273,659.52 P 51,420,889.56

Information and 534,461,047.83 349,227,932.63 185,233,115.20

CommunicationTechnology Equipment

Communication Equipment 13,850,197.90 6,426,276.77 7,423,921.13

Disaster Response and 70,153.00 52,297.56 17,855.44

Rescue EquipmentMedical Equipment 601,907.00 475,361.89 126,545,11

Sports Equipment 274,116.50 95,610.46 178,506.04

Technical and Scientific 2,082,196.00 540,355.18 1,541,840.82

EqUipmnentTotal P667,034,167.31 P421,091,494.01 P245,942,673.30

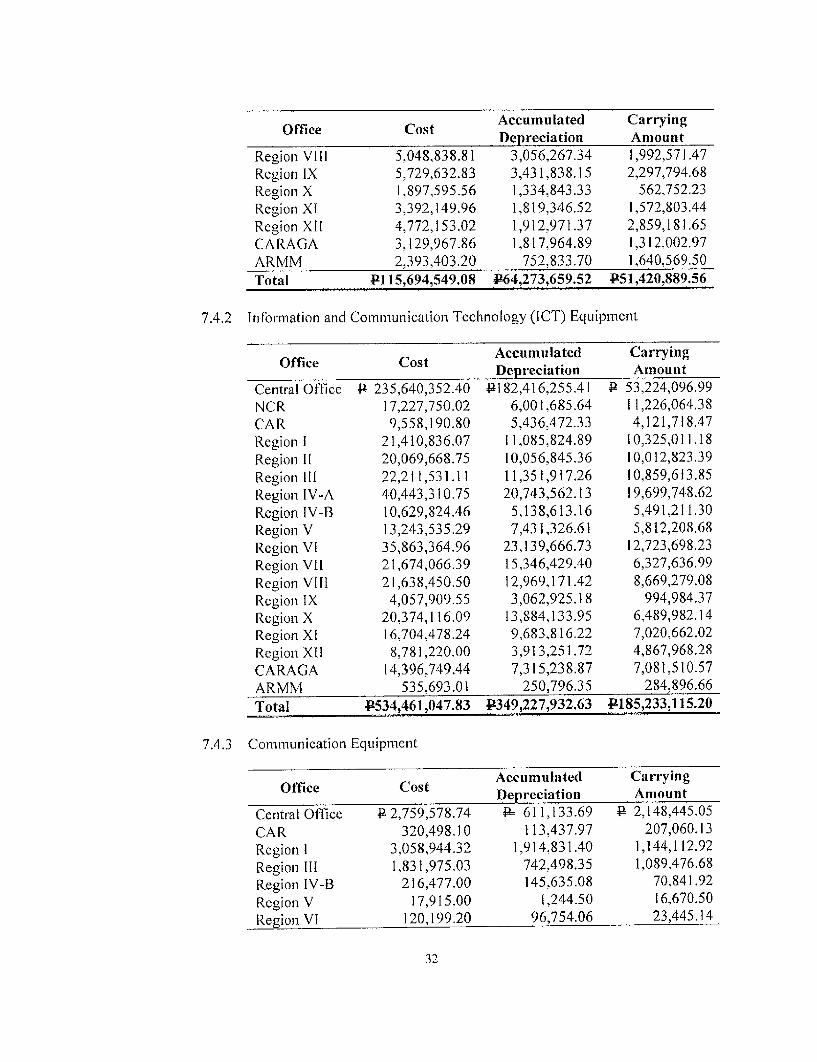

7.4.1 Office Equipment

Accumulated CarryingDepreciation Amount

Central Office 933,616,763.43 P20,898,574.57 P12,718,188.86

NCR 9,218,308.23 4,231,000.96 4,987,307.27

CAR 2,722,768.71 1,415,324.92 1,307,443.79

Region 1 4,375,305.56 1,733,302.36 2,642,003.20

Region I! 6,075,776.34 3,119,461.78 2,956,314.56

Region 111 5,445,286.08 2,241,043.50 3,204,242.58

Region IV-A 7,656,779.29 5,037,807.25 2,618,972.04

Region IV-B 4,827,860.36 3,090,988.35 1,736,872.01

Region V 4,162,882.58 1,761,622.89 2,401,259.69

Region VI 4,689,431.57 2,856,939.01 1,832,492.56

Region VIl 6,539,645.69 3,761,528.63 2,778,117.06

31

Accumulated CarryingDepreciation Amount

Region VIII 5,048,838.81 3,056,26734 1,992,571.47

Region IX 5,729,632.83 3,431,838.15 2,297,794.68Region X 1,897,595.56 1,334,843.33 562,752.23

Region XI 3,392,149.96 1,819,346.52 1,572,803.44

Region XII 4,772,153.02 1,912,971.37 2,859,181.65CARAGA 3,129,967.86 1,817,964.89 1,312,002.97

ARMM 2,393,403.20 752,833.70 1,640,569.50

Total P115,694,549.08 64,273,659.52 P51,420,889.56

7.4.2 Information and Communication Technology (ICT) Equipment

Accumulated CarryingDepreciation Amount

Central Office A 235,640,352.40 P182,416,255.41 P 53,224,096.99

NCR 17,227,750.02 6,001,685.64 11,226,064.38

CAR 9,558,190.80 5,436,472.33 4,121,718.47

Region I 21,410,836.07 11,085,824.89 10,325,011.18

Region lI 20,069,668.75 10,056,845,36 10,012,823.39

Region Ill 22,211,531.11 11,351,917.26 10,859,613.85

Region IV-A 40,443,310.75 20,743,562.13 19,699,748.62

Region IV-B 10,629,824.46 5,138,613.16 5,491,211.30

Region V 13,243,535.29 7,431,326.61 5,812,208.68

Region VI 35,863,364.96 23,139,666.73 12,723,698.23

Region VIl 21,674,066.39 15,346,429.40 6,327,636.99

Region VIII 21,638,450.50 12,969,171.42 8,669,279.08

Region IX 4,057,909.55 3,062,925.18 994,984.37

Region X 20,374,116.09 13,884,133.95 6,489,982.14

Region Xl 16,704,478.24 9,683,816.22 7,020,662.02

Region XII 8,781,220.00 3,913,251.72 4,867,968.28

CARAGA 14,396,749.44 7,315,238.87 7,081,510.57

ARMM 535,693.01 250,796.35 284,896.66

Total P534,461,047.83 P349,227,932.63 P185,233,115.20

7.4.3 Communication Equipment

Accumulated CarryingDepreciation Amount

Central Office P 2,759,578.74 P- 611,133.69 P 2,148,445.05

CAR 320,498.10 113,437.97 207,060.13

Region I 3,058,944.32 1,914,831.40 1,144,112.92

Region ill 1,831,975.03 742,498,35 1,089,476.68

Region IV-B 216,477.00 145,635.08 70,841.92

Region V 17,915.00 1,244.50 16,670.50

Re1on VI I20,199.20 96,754.06 23,445.14

32

Accumulated CarryingDepreciation Amount

Region VII 967,963.07 720,531.65 247,431.42

Region VIII 1,534,285.68 513,336.62 1,020,949.06

Region IX 73,420.00 66,078.00 7,342,00

Region X 67,464.00 58,282.61 9,181.39Region XI 1,362,001.89 970,610.85 391,391.04

Region XII 229,656.44 67,769.14 161,887.30CARAGA 1,289,819.43 404,132.85 885,686.58

Total P13,850,197.90 P6,426,276.77 P7,423,921.13

7.4.4 Disaster Response and Rescue Equipment

Accumulated CarryingDepreciation Amount

Central Office P10,000.00 P 9,500.00 P 500.00

Region III 9,720.00 8,747.86 972.14

Region VIII 50,433.00 34,049.70 16,383.30

Total P70,153.00 P52,297.56 P 17,855.44

7.4.5 Medical Equipment

Office Cost Accumulated CarryingDepreciation Amount

Central Office P 542,710.00 P459,211.72 P 83,498.28

Region IV-A 52,800.00 10,392.83 42,407.17

Region VIII 6,397.00 5,757.34 639.66

Total P601,907.00 4475,361.89 U126,545.11

7.4.6 Sports Equipment

Office Cost Accumulated CarryingDepreciation Amount

Central Office P 24,365.00 415,654.59 P 8,710.41

Region III 184,669.00 48,475.70 136,193.30

Region IV-A 65,082.50 31,480.17 33,602.33

Total P274,116.50 P95,610.46 P178,506.04

7.4.7 Technical and Scientific Equipment account with carrying amount of

P1,541,840.82 pertains to the balance of CAR GPS Receiver received

from Central Office in CY 2013 which was reclassified from the account

Office Equipment with cost of 42,082,196.00 and accumulated

depreciation of P540,355.18.

33

7.5 Transportation Equipment

Accumulated CarryingDepreciation Amount

Motor Vehicles P150,280,513.40 P118,331,478.20 P31,949,035.20Other Transportation

Equipm-ent 45,598,75 38,173139 7,425.36Total P150,326,112,15 P118,369,651.59 P31,956,460.56

7.5.1 Motor Vehicles

Accumulated Carrying

O Depreciation AmountCentral Office P 40,829,626.96 P 23,823,958.38 P 17,005,668.58NCR 6,867,100.00 5,996,532.68 870,567.32CAR 6,231,756.15 5,677,975.00 553,781.15Region 1 6,232,607.10 5,614,410.65 618,196.45Region 1I 6,389,244.00 5,959,138.80 430,105.20Region 111 8,906,649.40 8,098,036.48 808,612.92Region IV-A 7,733,381.75 6,916,026,03 817,355.72Region IV-B 5,943,296.24 5,184,512.13 758,784.11Region V 6,219,172.40 4,746,590.05 1,472,582.35Region VI 7,881,820.60 6,777,291.36 1,104,529.24Region VII 7,158,154.80 5,589,454.50 1,568,700.30Region VIII 6,715,446.80 5,901,424.15 814,022.65Region IX 4,889,888.40 4,335,110.75 554,777.65Region X 6,430,444.00 4,841,184.71 1,589,259.29Region XI 5,855,976.00 5,126,080.97 729,895.03Region XII 4,889,797.20 4,422,329.28 467,467.92CARAGA 5,890,214.00 5,062,177.80 828,036.20ARMM 5,215,937.60 4,259,244.48 956,693.12

Total P150,280,513.40 P118,331,478.20 131,949,035.20

7.5.2 Other Transportation Equipment account pertains to the balance of RegionVIII as of year-end with cost of P45,598.75 less depreciation of

238,173.39 and carrying amount of P7,425.36.

7.6 Furniture and Fixtures

Account Cost Carrying AmountDepreciation

Furniture and Fixtures P90,563,336.33 A 42,534,713.53 P48,028,622.80Books 104,440.85 82,807.25 21,63360

Total P90,667,777.18 P 42,617,520.78 P48,050,256.40

34

7.6.1 Furniture and Fixtures

Accumulated CarryingDepreciation Amount

Central Office 423,801,772.17 413,565,352.60 410,236,419.57NCR 8,558,121.82 4,677,355.48 3,880,766.34CAR 3,620,475.97 1,352,591.05 2,267,884.92Region 1 3,747,829.46 1,408,854.78 2,338,974.68Region I 3,787,586.38 1,562,105.27 2,225,481.11

Region 1II 6,980,904.84 2,697,696.57 4,283,208.27

Region IV-A 9,803,186.47 4,237,226.71 5,565,959.76

Region IV-B 2,736,076.69 589,959.92 2,146,116.77Region V 3,487,767.18 1,751,468.65 1,736,298.53

Region VI 4,111,220.72 1,855,275.61 2,255,945.11Region VII 3,465,783.69 1,826,573.23 1,639,210.46

Region VIII 3,870,152.40 1,971,000.84 1,899,151.56Region IX 1,740,897.10 969,968.36 770,928.74

Region X 2,329,510.69 1,103,701.02 1,225,809.67Region XI 1,824,895.05 841,283.42 983,611.63

Region XII 2,478,887.79 776,033.06 1,702,854.73CARAGA 2,909,318.31 1,168,893.68 1,740,424.63

ARMM 1,308,949.60 179,373.28 1,129,576.32

Total P90,563,336.33 P42,534,713.53 P48,028,622.80

7.6.2 Books

Accumulated CarryingDepreciation Amount

Central Office P 79,076.00 # 75,122.20 P 3,953.80

Region IV-A 6,128.85 4,240.20 1,888.65

Region V 1,867.00 0.00 1,867.00

Region VIl 7,693.00 0.00 7,693.00

Region VIII 3,524.00 3,171.60 352.40

Region IX 5,840.50 0.00 5,840.50

CARAGA 311.50 273.25 38.25

Total 104,440.85 R82,807.25 P21,633.60

7.7 Leased Assets Improvements

7.7.1 Leased Assets Improvements - Building

Accumulated CarryingDepreciation Amount

Region I P 993,765.45 P 748,432.99 P 245,332.46

Region.IV-A 1,218,004.10 168,195.30 1,049,808.80

Total P2,211,769.55 P916,628.29 P1,295,141.26

35

7.8 Construction in Progress

Particulars Remarks Amount

Construction in Pathway and perimeter fence around at P 18,160,000.00Progress - Land PSA, East Avenue, Dilirnan, QuezonImprovements City

Construction in Remaining amount for the construction 175,764,516.27Progress - of PSA-CVEA building at PSA, EastInfrastructure Assets Avenue, Diliman, Quezon City

Construction in Consulting services for the architectural 69,025,650.31

Progress - Buildings and engineering design for the proposedand Other Structures construction of a 23 storey PSA Building

at East Avenue, Diliman, Quezon City

Total P262,950,166.58

7.9 Other Property Plant and Equipment

Office Cost Accumulated Carrying AmountDepreciation

Central Office P32,907,026.65 R19,191,212.15 P13,715,814.50NCR 38,750.00 34,875.00 3,875.00CAR 454,122.55 179,570.06 274,552.49Region IT 207,613.68 0.00 207,613.68Region Ill 811,043.75 203,950.85 607,092.90Region IV-A 10,1 58,362.52 5,374,499.02 4,783,863.50Region IV-B 216,309.40 0.00 216,309.40Region V 1,926,361.72 1,280,649.52 645,712.20Region VIT 709,743.55 601,042.78 108,700.77Region IX 1,095.00 65.70 1,029.30Region X 3,177,145.01 2,154,614.69 1,022,530.32Region XI 1,836,227.77 1,212,764.26 623,463.51Region XII 1,000,00 180.00 820.00

CARAGA 1,011,769.88 514,911.89 496,857.99ARMM 144,815.00 26,066.64 118,748.36

Total P53,601,386.48 430,774,402.56 P22,826,983.92

8. Intangible Asset

8.1 Computer Software

AccumulatedOffice Cost Amortizato Carrying Amount

Amortization

Central Office P794,126.00 4635,169.57 P158,956.43

36

9. Other Assets

Account Amnount

Advances R 1,333,253.23

Prepayments 48,859,714.74

Deposits 1,808,471,74

Other Assets 16,362,817.72

Total P68,364,257.43

9.1 Advances

Account Amount

Advances for Operating Expenses R 16,923.31

Advances for Payroll 659,917.13

Advances to Special Disbursing Officers 580,942.32

Advances to Officers and Employees 75,470.47

Total R1,333,253.23

9. 1.1 Advances for Operating Expenses account consists of the following

balances:

Office Amount

Central Office P14,406.26

Region VII 2,517.05

Total 9l6,923.31

9. 1. 1.1 Advances for Operating Expenses account for Central Office

Name Amount Remarks

Saimah P. Ringia 4 1,409.00 Petty cash erroneously posted as cashadvance. With letter sent to COA for

write-off dated Jan, 22, 2015 due to the

sudden death of Ms. Ringia.

Eduardo L. Guinto 3,997.26 Refunded 2/11/16 w/ OR #19413939

Eduardo L. Guinto 9,000.00 Refunded 3/3/16 w/ OR #19413990

Total P14,406.26

9.1.1.2 Advances For Operating Expenses account of Region VII is the

balance of cash advance for Regional Planning Workshop last

December 2015 by Myrna Trinidad Cataluna, Statistical Officer I.

It was refunded on January 12, 2016 with OR# 17810685.

37

9.1.2 Advances for Payroll

Office AmountRegion V P555,400.00

Region VIll 104,517.13Total $659,917.13

9.1.2.1 Advances for Payroll account of Region V

Office Particulars AmountCamarines Norte Cash advance for payment of P423,000.00

honorarium of barangay chairmen for2015 POPCEN

Carnarines Sur Cash advance for payment of I19,000.00cellphone load allowanceCash advance for Fixed Travelling 13,400.00

ExpensesTotal 4z555,400,00

9.1.2.2 Advances for Payroll account of Region VIll is Leyte balance forrelief due to typhoon Yolanda.

9.1.3 Advances to Special Disbursing Officers

Office AmountCentral Office P407,603.32ARMM 173,339.00

Total 4580,942.32

9.1.3.1 Advances to Special Disbursing Officers account for CentralOffice

Name Amount RemarksBernadette B. P 0.59 Still for refindBalamban balance of cash

advance for variousexpenses ofTechnical WorkshopWriteshop for 2012SAE Poverty Project

Candido J. 1,739.60 Refunded 1/11/16 v/Astrologo, Jr. OR #19413859Agustin S. Blanco 40.00 Still for refund

balance of cashadvance for various

expenses for BAS-

38

Name Amount RemarksADB Project

Eduardo L. Guinto 358,117.25 Partially LiquidatedCash Advance forvarious expenses forBAS-ADB Project

Aurora T. Reolalas 47,705.88 Partially Liquidatedcash advance foriniscellaneous

expenses for CRD-VSD

Total 9407,603.32

9.1.3.2 Advances to Special Disbursing Officers account for ARMM

pertain to advances for travelling expenses from previous years

since 2014 which were already liquidated but were not reported in

the books due to the negligence of the previous accountants. These

balances were adjusted in March 2016 with supporting liquidation

reports.

9.1.4 Advances to Officers and Employees

Office Amount

Central OfficeRegion 1 10,000.00

Region VI 7,176.70

Region VII 1,770.40

Region IX 30,000.00Total P75,470.47

9.1.4.1 Advances to Officers and Employees account for Central Office

Name Amount Remarks

From Regular Fund:Candido J. Astrologo, 4 607.40 Various expenses of Region X

Jr. for PSA First AnniversarySO0192-14-RD 10On-study leave - Mastcrts Degree

Gerald Junne L. Clarino 600.00 Program in Public Management,Japan

RoyTraveling expenses for

Riotomihe 3 1 ,202.00 Estimation Regional DomesticDifontorumProduct

Wilma A. Guillen 20,698.15 Refunded as of 1/7/16 w/OR#19413851

39

Name Amount Remarks

From Trust Fund:

Lourdes.J. Flufana 776.82 Refunded as of 1/6/16 w/OR#19413842

Delilah G. Bassig 2,639.00 Refunded as of 1/10/16 wIOR#19413881

Total P 26,52337

9.1.4.2 Advances to Officers and Employees account for various Regional

Offices

Office Particulars Amount

Region I Cash advance by Alejandro Rapacon, OIC- 410,000,00PSSO of IlocosNorte for hauling fortransfer of POPCEN documents liquidatedon January 4, 2016.

Region VI Undeposited cash advances for 2015 7,176.70Regional Planning Workshop and 2015General Assembly activities. Since these

were prior year transactions, the balances

were deposited back to the Bureau of

Treasury on February 12, 2016.

Region VII Cash advance by Teresita Seno, Utility 1,770.40Worker 11 for Retirement Seminar in

Cagayan de Oro last November 24-27,2015.

Region IX Cash advance by Ronaldo Taghap for 5,000.00

various Maintenance and Other OperatingExpenses.Cash advance by Belinda Garcia for 25,000.00

various Maintenance and Other OperatingExpenses

Total P48,947.10

9.2 Prepayments

Account Amount

Advances to Contractor P11,789,014.23

Prepaid Rent 34,196,288.75

Prepaid Registration 296,665.06

Prepaid Insurance 1,830,100.30

Other Prepaymnents 747,646.40

Total #48,859,714.74

40

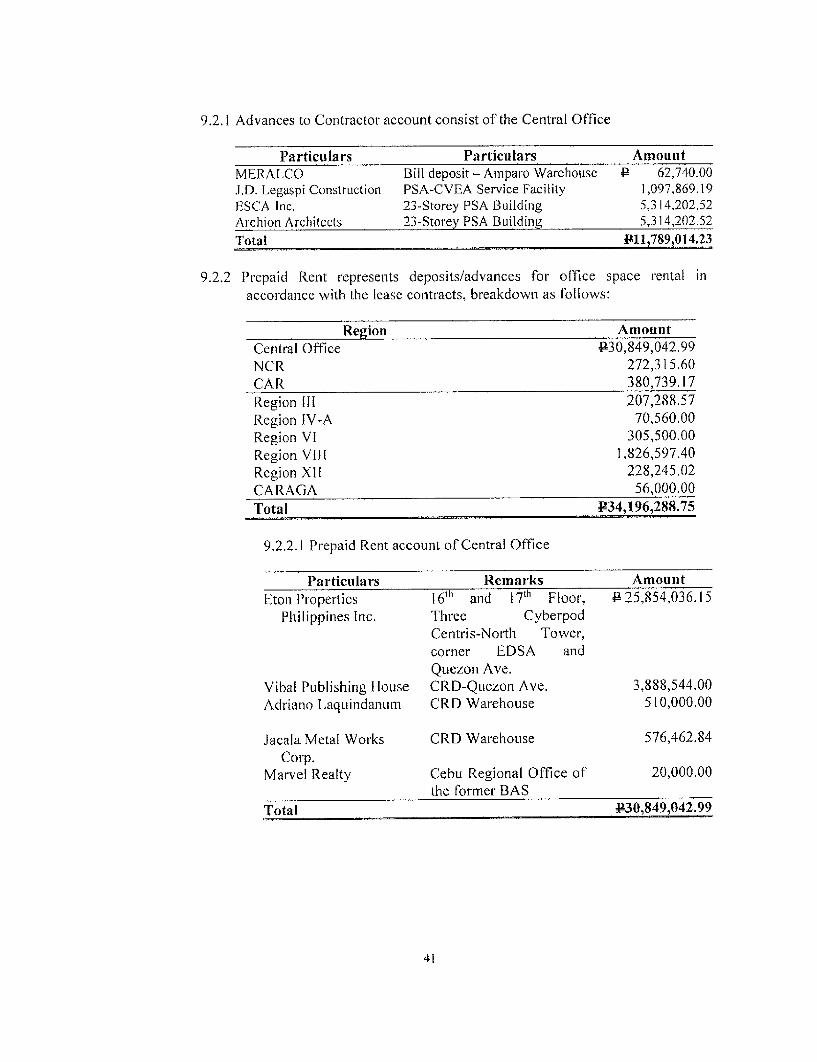

9.2.1 Advances to Contractor account consist of the Central Office

Particulars Particulars AmountMERALCO Bill deposit - Aniparo Warehouse P 62,740.00J.D. Legaspi Construction PSA-CVEA Service Facility 1,097,869.19ESCA Inc. 23-Storey PSA Building 5,314,202,52Archion Architects 23-Storey PSA Building 5,314,202.52

Total P1 1,789,014.23

9.2.2 Prepaid Rent represents deposits/advances for office space rental inaccordance with the lease contracts, breakdown as follows:

Region Amount

Central Office P30,849,042.99NCR 272,315.60CAR 380,739.17

Region ill 207,288.57Region IV-A 70,560.00Region VI 305,500.00Region VIll 1,826,597.40Region XII 228,245,02CARAGA 56,000.00

Total P34,196,288.75

9.2.2.1 Prepaid Rent account of Central Office

Particulars Remarks Amount

Eton Properties 16' and 17t Floor, P25,854,036.15Philippines Inc. Three Cyberpod

Centris-North Tower,corner EDSA andQuezon Ave.

Vibal Publishing House CRD-Quezon Ave. 3,888,544.00

Adriano Laquindanum CRD Warehouse 510,000.00

Jacala Metal Works CRD Warehouse 576,462.84Corp.

Marvel Realty Cebu Regional Office of 20,000.00the former BAS

Total V30,849,042.99

41

9.2.3 Prepaid Registration

Office AmountCentral Office P290,835.35CARAGA 5,829.71Total P296,665.06

9.2.3.1 Prepaid Registration account for Central Office representsprepayments to Land Transportation Office for registration offormer BAS vehicles and motorcycles.

9.2.3.2 Prepaid Registration account for CARAGA represents year-endbalance.

9.2.4 Prepaid Insurance consists of premiums paid for insurance of government

service vehicles and for fidelity bonds of Accountable Officers

Office AmountCentral Office P1,537,382.48NCR 12,643.12CAR 84,724.07

Region 1 4,167.83Region II 10,384.47Region V 3,973.31Region Vil 13,027.79Region VIII 43,120.30Region IX 13,488.71Region X 22,651.44Region XI 19,223.43Region XII 35,303.90CARAGA 30,009.45

Total 41,830,100.30

9.2.5 Other Prepayments

Office Amount

Central Office 4201,233.88

Region II 720.00Region VillI 506,009.07Region X 16,207.82CARAGA 23,475.63

Total P747,646.40

42

9.3 Deposits

Account AmountGuaranty Deposits P1,752,751.74Other Deposits 55,720.00Total P1,808,471.74

9.3.1 Guaranty Deposits consists of the following balances:

Office AmountCentral Office R 42,051.90CAR 704,900.00Region 1 328,400.00

Region Ill 83,498.46Region IV-A 148,760.00Region XI 82,381.38Region XII 362,760.00Total P1,752,751.74

9.3.2 Other Deposits consists of year-end balance of Central Office for gasoline,

meter and electricity consumption.

9.4 Other Assets

Other Assets account represents the value of fully depreciated, obsolete and

unserviceable properties awaiting final disposition:

Office Amount

Central Office P 8,697,188.23CAR 895,772.47Region 1 772,091.46Region IV-A 894,368.42

Region IV-B 53,947.88Region V 1,088,347.32Region VI 116,689.59Region VII 185,825.48Region VIII 2,096,315.94Region IX 530,189.70Region X 93,053.44

Region XI 23,390.17

Region XII 630,855.02CARAGA 67,697.11

ARMM 217,085.49

Total P16,362,817.72

43

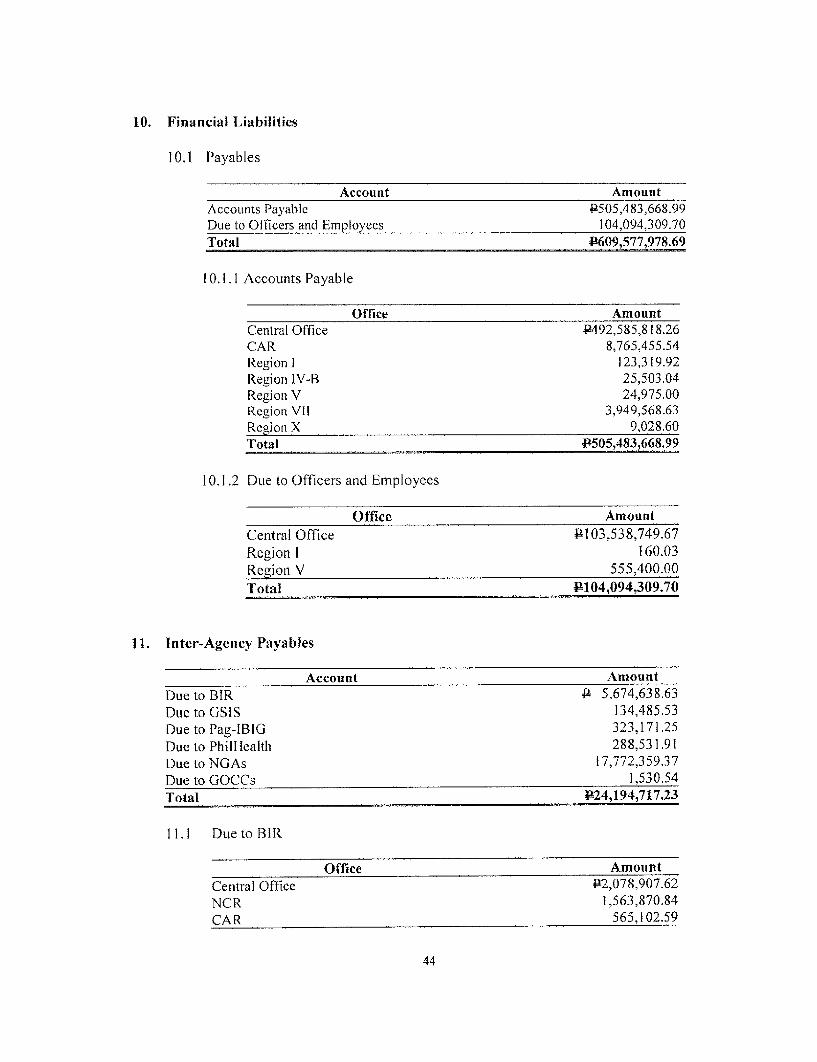

10. Financial Liabilities

10.1 Payables

Account AmountAccounts Payable P505,483,668.99Due to Officers and Employees 104,094,309.70Total P609,577,978.69

10.1.1 Accounts Payable

Office AmountCentral Office P492,585,818.26CAR 8,765,455.54Region 1 123,319.92Region IV-B 25,503.04Region V 24,97500Region VIl 3,949,568.63Region X 9,028.60Total P505,483,668.99

10.1.2 Due to Officers and Employees

Office AmountCentral Office P103,538,749.67Region I 160,03Region V 555,400.00Total 4104,094,309.70

11. Inter-Agency Payables

Account Amount

Due -toBIR A 5,674,638.63Due to GSIS 134,485.53Due to Pag-[BIG 323,171.25Due to PhilHealth 288,531.91Due to NGAs 17,772,359.37Due to GOCCs 1,530.54Total P24,194,717.23

11.1 Due to BIR

Office AmountCentral Office P2,078,907.62NCR 1,563,870.84CAR 565,102.59

44

Office AmountRegion I 52,147.40Region II 288.10Region III 13,685.05Region IV-B 28,141.04Region VI 433,663.03Region VII 284,605.42Region IX 1,806.00Region XII 140.00CARAG A 459,248.90ARMM 193,032.64Total P5,674,638.63

11.2 Due to GSIS

Office AmountCentral Office & 15,464.98Region VII 1,265.03Region VIII (2,424.56)Region XII 31.45ARMM 120,148.63Total P134,485.53

11.3 Due to Pag-IBIG

Office AmountCentral Office &300,521.43Region Il1 200.00Region VII 181.82Region VIII (0.62)CARAGA 200.00ARMM 22,068.62Total P323,171.25

11.4 Due to Phillealth

Office Amount

Central Office P286,437.41Region II 275.00Region VII 212.50CARAGA 462.50ARMM 1,144.50

Total P288,531.91

45

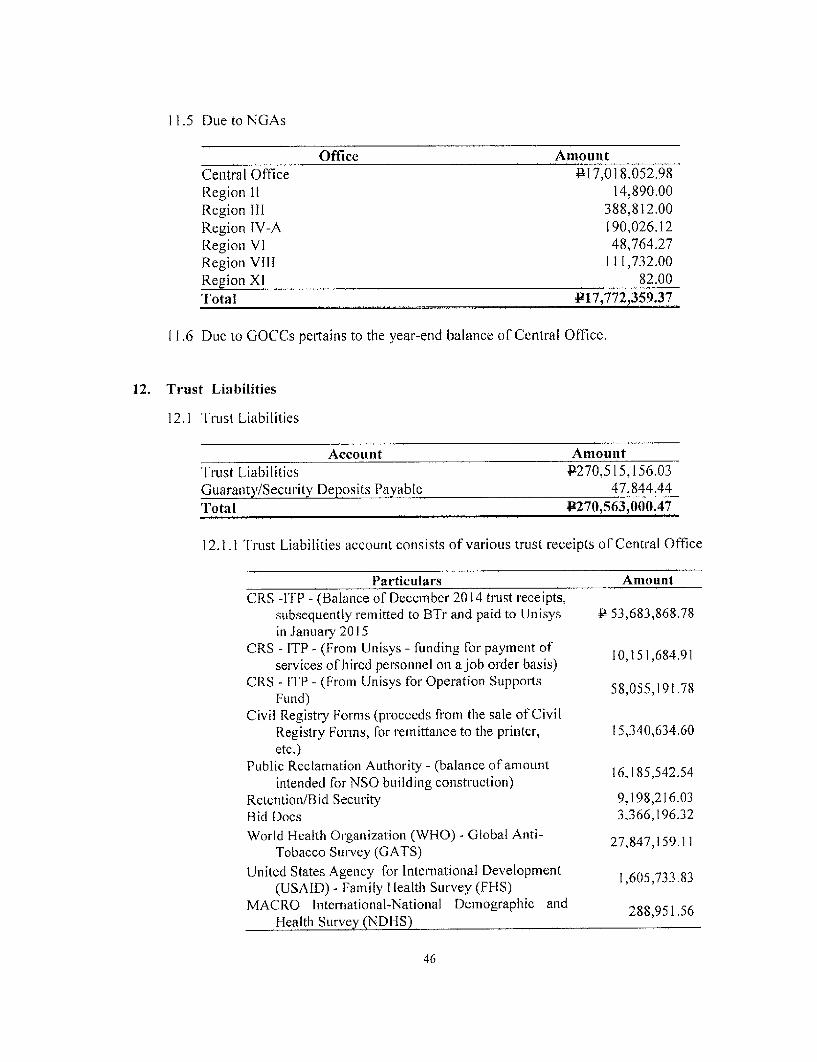

11.5 Due to NGAs

Office AmountCentral Office P17,018,052.98Region II 14,890.00Region Ill 388,812,00Region IV-A 190,026.12Region VI 48,764.27Region VIII 111,732,00

Region XI 82.00Total P17,772,359.37

11.6 Due to GOCCs pertains to the year-end balance of Central Office.

12. Trust Liabilities

12.1 Trust Liabilities

Account Amount

Trust Liabilities P270,515,156.03Guaranty/Security Deposits Payable 47,844.44

Total P270,563,000.47

12.1.1 Trust Liabilities account consists of various trust receipts of Central Office

Particulars AmountCRS -ITP - (Balance of December 2014 trust receipts,

subsequently remitted to BTr and paid to Unisys P 53,683,868.78in January 2015

CRS - ITP - (From Unisys - funding for payment of 10,151,684.91services of hired personnel on ajob order basis)

CRS - ITP - (From Unisys for Operation Supports 58,055,191.78Fund)

Civil Registry Forms (proceeds from the sale of CivilRegistry Forms, for remittance to the printer, 15,340,634.60etc.)

Public Reclamation Authority - (balance of amount 16,185,542.54intended for NSO building construction)

Retention/Bid Security 9,198,216.03Bid Does 3,366,196.32World Health Organization (WHO) - Global Anti- 27,847,159.11

Tobacco Survey (GATS)United States Agency for International Development 1,605,733.83

(USAID) - Family Health Survey (FHS)MACRO International-National Demographic and 288,951.56

Health Survey (NDHS)

46

Particulars AmountSSS - Matching Data Project 2,289,418.00Brightscreen 1,897,400.00Remittance from CRS-ITP and OCRG for tax 34,095,899.63

paymentSurvey of Food Demand 6,262,458.00Livestock and Poultry Information (LPI) 15,000,000.00Philippine Carabao 1,500,000.00Evidence Data for Gender Equality (EDGE) 2,005,156.53Consumer Expectation Survey (CES) 2,634,974.54Department of Health (DOH) - Development of the

Vital Registration Framework for Health 911,203.66Workers

International Labour Organization (ILO) / PILOT 2,186,411.80PhilWAVES 3,967,328.14ADB - R-CDTA 8369: Innovative Data Collection

Methods for Agricultural and Rural Statistics 1,427,331.31Project

Various Trust Receipts 614,394.96

Total P270,515,156.03

12.1.2 Guaranty/Security Deposits Payable account is composed of the following

balances:

Office Amount

Region I 41 8,900.00

Region VII 17,944.44Region X1 21,000.00

Total P47,844.44

13. Other Payables

Office Amount

Central Office P 240,045.36NCR 120,000.00CAR 30,000.00Region 1 35,418.20Region II 10,036.00Region Ill 221,018.44Region IV-A 27,472.53Region IV-B 71,378.32Region V 82,687.00

Region VI 121,456.95

47

Office Amount

Region VIl 91,247.10

Region VIII 13,950.00

Region IX 13,571.52

Region X 40,000.00

Region XI 4,000.00

Region XII 40,100.00

CARAGA 49,868.00

ARMM 55,229.06

Total P1,267,478.48

13.1 The PSA Central Office has other payables to agencies pertaining to current salary

deductions for Philippine Statistics Authority Employees Multi-purpose

Cooperative amounting to P240,045.36 remitted in January 2016.

14. Service and Business Income

Account Amount

Service IncomeRegistration Fees P 4,773,410.00

Licensing Fees 1,874,320.00

Verification and Authentication Fees 852,149,755.54

Business IncomeIncome from Printing and Publication 779,353.77

Interest Income 428,454.84

Fines and Penalties - Business Income 1,380,911.84

Other Business Income 1,745,875.64

Total P 863,132,081.63

15. Personnel Services - P1,331,816,211.67

15.1 Salaries and Wages

Account Amount

Salaries and Wages - Regular f670,870,705.39

Salaries and Wages - Casual/Contractual 20,130,747.83

Total 4691,001,453.22

48

15.2 Other Compensation

Account AmountPersonal Economic Relief Allowance (PERA) P 69,856,882.99Representation Allowance (RA) 8,275,943.21Transportation Allowance (TA) 3,063,191.49Clothing/Uniform Allowance 14,591,194.03Subsistence Allowance 29,341.04Laundry Allowance 11,293.00Productivity Incentive Allowance 4,263,204.55Honoraria 386,870.00Hazard Pay 116,947.81Longevity Pay 1,135,000.00Overtime and Night Pay 35,673,753,22Year End Bonus 58,487,918.68Cash Gift 15,446,065.45Other Bonuses and Allowances 132,930,785.72Total P344,268,391.19

15.3 Personnel Benefit Contributions

Account Amount

Retirement and Life Insurance Premiums P82,11 8,100.37Pag-IBIG Contributions 3,493,207.66

Phil-Iealth Contributions 7,960,518.61Employees Compensation Insurance Premiums 3,467,205.84Total P97,039,032.48

15.4 Other Personnel Benefits

Account Amount

Retirement Gratuity - Civilian P 3,208,454.90Terminal Leave Benefits 38,145,546.77Other Personnel Benefits 158,153,333.11Total P199,507,334.78

16. Maintenance and Other Operating Expenses - P3,263,740,172.39

16.1 Traveling Expenses

Account Amount

Traveling Expenses - Local P290,088,062.76Traveling Expenses - Foreign 3,350,04211

Total -P293,438,104.87

49

16.2 Training and Scholarship Expenses

Account AmountTraining Expenses P 227,528,787.47

16.3 Supplies and Materials Expenses

Account AmountOffice Supplies Expenses 4 I13,840,128.38Accountable Forms Expenses 436,226.32Drugs and Medicines Expenses 35,016.82Medical, Dental and Laboratory Supplies Expenses 130,840.42Fuel, Oil and Lubricants Expenses 11,173,340.32Other Supplies and Materials Expenses 254,771,631.03Total V 380,387,183.29

16.4 Utility Expenses

Account AmountWater Expenses 9 12,311,107.44Electricity Expenses 74,655,731.27Total R 86,966,838.71

16.5 Communication Expenses

Account Amount

Postage and Courier Services P 9,769,816.14Telephone Expenses 19,575,165.97Internet Subscription Expenses 5,680,862.35Cable, Satellite, Telegraph and Radio Expenses 245,477.14

Total R 35,271,321.60

16.6 Awards/Rewards and Prizes

Account Amount

Awards/Rewards Expenses P 110,000.00Prizes 436,970.00Total P 546,970,00

16.7 Confidential, Intelligence and Extraordinary Expenses

Account Amount

Extraordinary and Miscellaneous Expenses P 3,124,421.95

50

16.8 Professional Services

Account AmountLegal Services & 994,775.00Auditing Services 638,192.43Consultancy Services 1,909,000.00Other Professional Services 5,140,158.60Total P 8,682,126.03

16.9 General Services

Account Amount

Janitorial Services P 6,654,627.02Security Services 49,531,233.47Other General Services 1,118,516,084.04Total R 1,174,701,944.53

16.10 Repairs and Maintenance

Account AmountRepairs and Maintenance - Buildings and Other Structures 4 720,659.00Repairs and Maintenance - Machinery and Equipment 63,5 13,984.72Repairs and Maintenance - Transportation Equipment 10,905,372.97Repairs and Maintenance - Furniture and Fixtures 2,620,347.97Repairs and Maintenance - Leased Assets 104,611.34

Repairs and Maintenance - Leased Assets Improvements 4,338,505.55Repairs and Maintenance - Other Property, Plant and 306,682.38

EquipmentTotal P82,510,163.93

16.11 Taxes, Insurance Premiums and Other Fees

Account Amount

Taxes, Duties and Licenses R 114,895.15Fidelity Bond Premiums 2,199,920.54

Insurance Expenses 3,238,842.03

Total P 5,553,657.72

16.12 Labor and Wages

Account Amount

Labor and Wages P 716,472.20

51

16.13 Other Maintenance and Operating Expenses