Conservation and Sustainability Center. Fundação Amazonas Sustentável.

2011REPORT

Conservation Sustainability Climate Change

Electric avenuesDriving home the case for electric vehicles in the UK March 2011

LiSt of aCronymS anD initiaLS

BAU Business as usual

BEV Battery electric vehicle

CCC The Committee on Climate Change

GHG Greenhouse gas

GWh Gigawatt hour (unit of energy) 1GWh = 106kWh

EV Electric vehicle (used as a generic term to refer to BEVs and PHEVs)

ICEV Internal combustion engine vehicle (used to refer to traditional cars)

kt Kilo tonne (one thousand tonnes)

kWh Kilowatt hour (unit of energy)

Mt Megatonne (one million tonnes)

MW Megawatt (unit of power)

NTS National Travel Survey

OEM Original equipment manufacturer

OLEV OfficeforLowEmissionVehicles

ONS OfficeforNationalStatistics

PHEV Plug-in hybrid electric vehicle

SMMT Society of Motor Manufacturers and Traders

R&D Research and development

UNFCCC United Nations Framework Convention on Climate Change

US ABC United States Advanced Battery Consortium

V2G Vehicle to grid

VED Vehicle excise duty

• AllUKfiguresincludeNorthernIreland.

• ‘Britain’or‘GreatBritain’referstoEngland,ScotlandandWales.

• Pleasealsonotethat,unlessotherwisestated,percentageemissionreductionsarerelativeto1990emissionlevels.

Acronyms

aCKnowLEDgEmEntS This report is based on research commissioned by WWF-UKandpreparedbyElementEnergyLtd.Itincludesthemainfindingsoftheconsultants’researchandpresentsourviewofwhatthesefindingsmean.The

consultants’researchreportcanbedownloadedfromwwf.org.uk/electricvehicles.Aseparatesummaryofthisreportisalsoavailableinhardcopyortodownload, asabove.

We’despeciallyliketothankShaneSlaterandMichaelDolmanofElementEnergyfor devising the three different scenarios to estimate the UK carbon savings potential ofEVsandtheirgridimpacts,andforwritingtheresearchreport.We’realsogratefultoDrJillianAnableoftheCentreforTransportResearch,UniversityofAberdeen,and Keith Buchan of the Metropolitan Transport Research Unit for acting as peer reviewers,providingtheirexpertiseandadviceatallstagesofthisproject.

Electric avenues page 3

Acknowledgements

© N

atioN

al G

eo

Gr

ap

hic

Sto

ck

/ Sa

ra

h le

eN

/ WW

F

100% rEnEwabLES by 2050WWF has a vision of a world that is powered by 100% renewable resources by the middle of thiscentury.Unlesswemakethistransition,theworldismostunlikelytoavoidpredictedescalatingimpactsofclimatechange. See wwf.org.uk/energyreport for more information

Contents

Key messages 06

exeCutive summary 07

1 introduCtion 131.1MeetingUKclimatechangeobligations 13 1.2CCCindicativefiguresforreducingcaremissions 13 1.3TheadvantagesofEVs 15 1.4TheemergingEVmarket 15

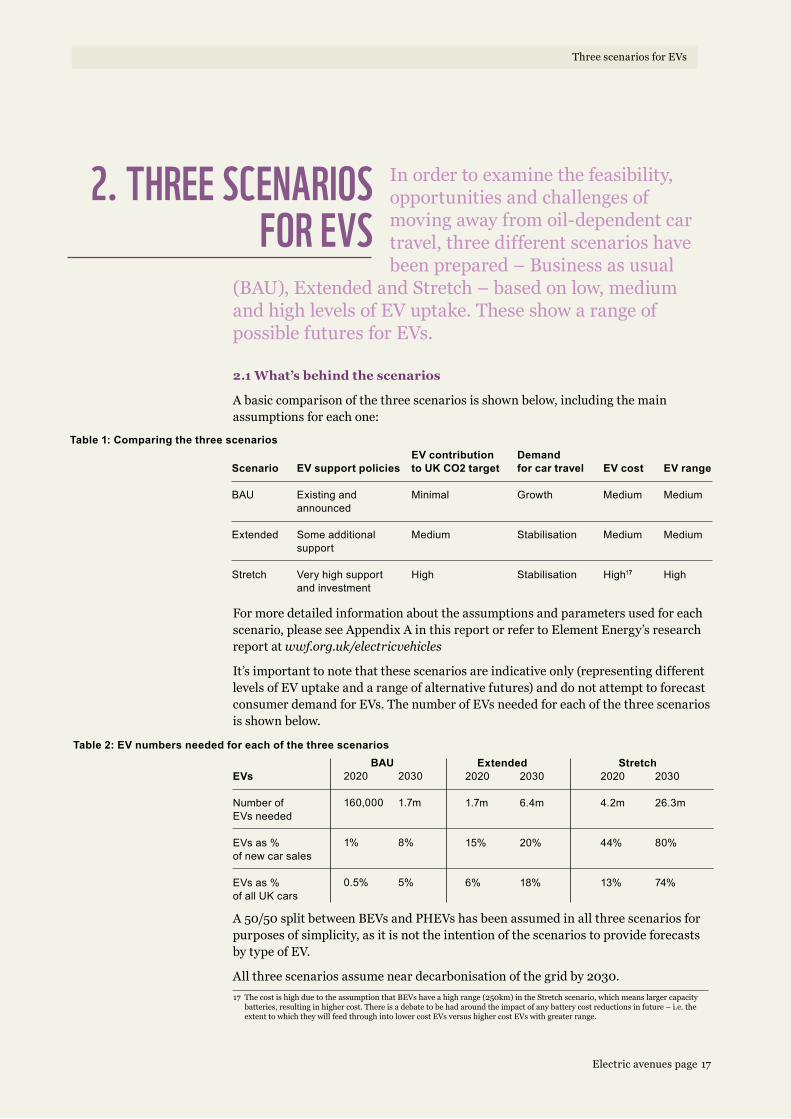

2 three sCenarios for evs 17 2.1What’sbehindthescenarios 17

2.2Thepurposeofthescenarios 18

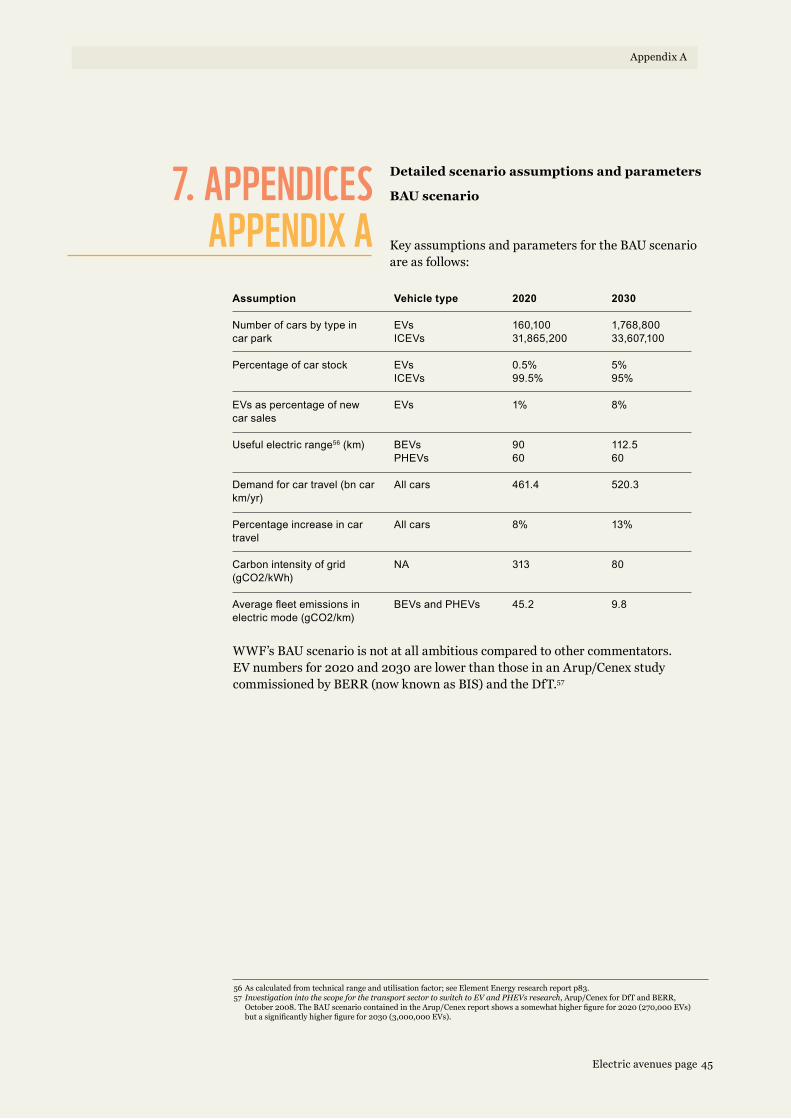

2.3TheBusinessasUsual(BAU)scenario 18

2.4TheExtendedscenario 19

2.5TheStretchscenario 19

2.6Scope 19

3 the role of evs in reduCing Carbon emissions 20 3.1EVsandCO2reduction 20

3.2Theimportanceofmanagingtraveldemand 22

3.3EVs’impactonfueldemand 25

4 the imPaCt of evs on the grid 28 4.1ChargingEVs 28

4.2Gridimpacts 28

5 Challenges and oPPortunities 35 5.1Challenges 35

5.2Opportunities 37

6 PoliCy reCommendations 39 6.1ReducingcaremissionsandsupportingEVgrowth 39

6.2Planningforgridimpacts 42

6.3Businessrecommendations 42

7 aPPendiCes 45

6Electric avenues page

Key Messages

KEy mESSagES • Electric vehicles (EVs) have an important role to play in decarbonisingroadtransportandreducingtheUK’sdependencyonoil.They’llalsobeessentialindeliveringthelevelofreductioninemissionsfromcarsthat’snecessarytoachievethetargetsrequiredundertheUKClimateChangeAct.

•EVshavestrategicimportancetotheUKeconomy:thousandsoffuturejobsareexpectedinthisindustry.Thedevelopmentofastrongdomesticmarketwillhelptoattractfutureinvestment.TheUKisalreadyaleaderincommercialEVsandbatterytechnologyand,withtheannouncementoftheNissanLeafmanufacturingfacilityinSunderland,canexpecttoplayaleadingroleintheinternationalEVmarket.

• WWF-UK supports the rapid introduction of EVs to replace petrol/diesel vehicles.However,thefullvalueofEVstoalow-carboneconomywillbedependent on decarbonising the power sector and reducing the amount we drive.

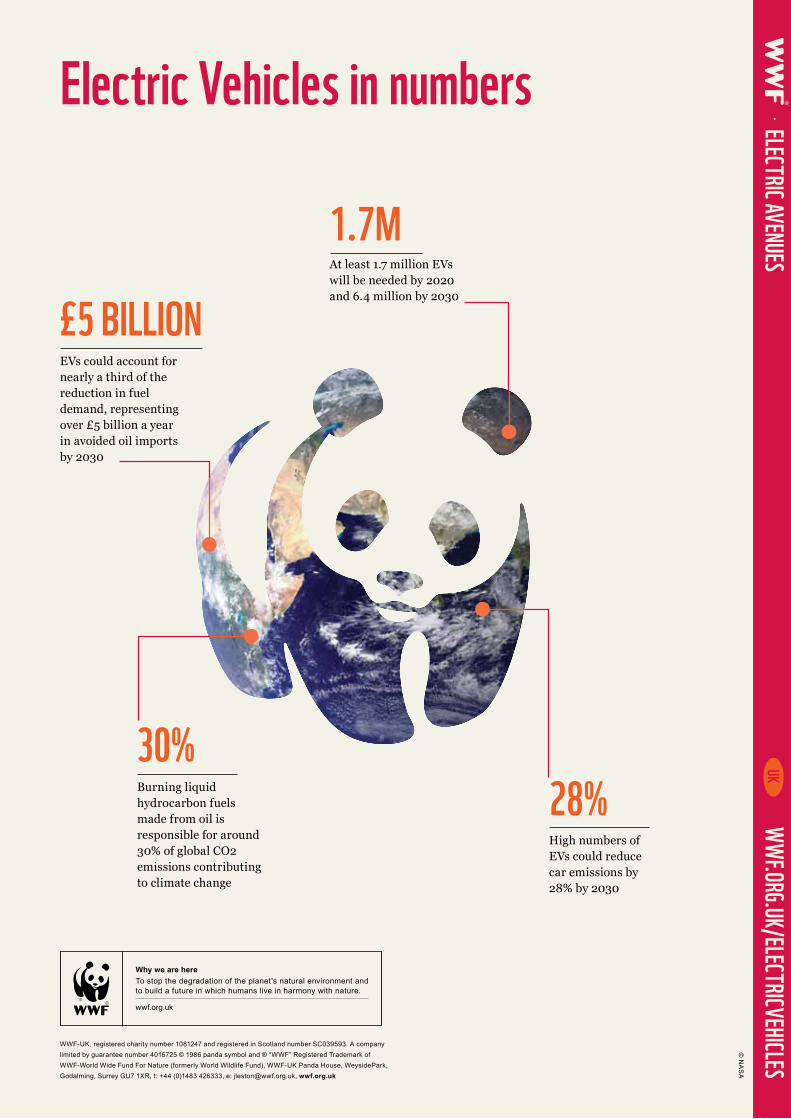

•Thisstudyshowsthatatleast1.7millionEVswillbeneededby2020and6.4millionby2030inordertoachievetheUK’sclimatechangetargets.EVswouldthenrepresent6%ofallUKcarsin2020and18%in2030.Capitalgrantsandother incentives to encourage an increase in numbers of EVs will be essential to stimulatethemarket.

•AcombinationofhighEVuptake,improvementsintheefficiencyofinternalcombustionenginevehicles(ICEVs),anddemandmanagementmeasurestoreducetheamountpeopledrivecouldpotentiallydelivera75%reductionincaremissionsby2030.EVscouldprovidenearlyathirdofthisemissionsreduction.

• This same combination of factors could also reduce UK fuel demand for cars by nearly80%by2030.EVscouldaccountfornearlyathirdofthereductioninUKfueldemand,representingover£5billionayearinavoidedoilimportsby2030.

• Grid impacts of EVs are manageable and within National Grid forecasts in termsofadditionalloadandpeakelectricitydemand,evenwithhighlevelsofEVuptake.However,EVscouldoverloadcurrentlocaldistributionsystemsandtransformers,sothesemayneedupgradingasthenumberofEVsincreases.

•EVssupporttherapidgrowthofrenewableenergy.Theycanhelpbalancethegridbycharginglateatnight,usingrenewablepowerwhenelectricitydemandisotherwiselow.UsingrenewablestorechargeEVsalsoreducestheircarbonimpact.Oncetechnicalissuesareresolved,there’salsopotentialforEVstofeedpowerbackintothegridattimesofhighdemand.

•ToensureEVsdeliversignificantcarbonsavingsinthe2020s,theUKneedstobecome‘EVready’now.Earlyactionsneededincludetheroll-outofcharginginfrastructure,encouragementofdelayedcharging,anddevelopmentof‘smartgrids’thatincludeintelligentmonitoring,controlandcommunicationstechnologies to optimise EV charging for grid stability and at times of lowest carbonintensity.

• Other priorities for innovation and investment are reducing the cost and improvingtheperformanceofEVbatteries,anddecarbonisingthegrid.AEurope-wide approach to grid infrastructure will also be needed if EVs are to be poweredbyadecarbonisedEuropeangrid,inordertodelivermaximumcarbonsavingsbothintheUKandonthecontinent.

at LEaSt 1.7 miLLion EVS wiLL bE nEEDED by

2020 anD 6.4 miLLion by 2030

EVS CoULD aCCoUnt for nEarLy a thirD of thE rEDUCtion in fUEL

DEmanD, rEprESEnting oVEr £5 biLLion a yEar in aVoiDED oiL importS

by 2030

1.7 miLLion

£5 biLLion

Electric avenues page 7

Executive Summary

ExECUtiVE SUmmary Electric vehicles (EVs) have an important role to play in decarbonising roadtransport.

To ensure they realise their full emissions-saving potential,wealsoneedtodecarbonisethepowersectorby 2030 and deliver demand management measures that willreducetheamountpeopledrive.

Why EVs are an important issue for WWF

Climate change is one of the greatest threats to the natural world and the people whodependonit.Astheprimarycauseofclimatechangeistheburningoffossilfuels(coal,oilandgas),reducinghumanity’scarbonfootprintmustbeapriorityiftheriseinglobaltemperaturesistobekeptbelowdangerouslevels.Thiswillrequireaggressiveactiontoimproveenergyefficiencyinallsectorsoftheeconomy.Inthetransportsector,itwillrequireareductioninthedemandforoil-derivedfuels.

WWF’sLivingPlanetReport2010showsthat,globally,we’recurrentlyusingnaturalresourcesataratethat’s50%higherthantheplanetcanreplenisheachyear.IfeveryonelivedaswedointheUK,we’dneed2.75planetsofresources.Thisovershootislargelyduetoourcarbonfootprint.Webelievethatamovetowardstransportationsystemspoweredbyrenewableelectricity,togetherwithimprovementsinconventionalvehicleefficiencyandareductionintheamountpeopledrive,canplayamajorroleinreducingourrelianceonoilandotherfossilfuels,therebycuttingcarbonemissionssignificantly. Helping to reduce our oil dependency

The world is running out of cheap and easily accessible sources of oil1.Thisreductionin affordable supply should focus our efforts on developing alternatives – yet we continuetoseekincreasinglyriskyandmorepollutingsourcesofoilintheArctic,deepwaterssuchastheMexicanGulfandthetarsandsofCanada.

Burning liquid hydrocarbon fuels made from oil is responsible for around 30% of globalCO2emissionscontributingtoclimatechange.2 We need to wean ourselves off oil and decarbonise our economies in order to ensure that average global temperaturesrisebynomorethan1.5ºCcomparedtopre-industriallevels.Thisisnecessaryifwewanttoensurethesafety,sustainabilityandprosperityofpeople,placesandwildlife.

In its recent report3,theIndustryTaskforceonPeakOilandEnergySecuritywarnedthatBritainwasunpreparedforoilpriceshockswhichcouldhappeninthenextfiveyears,placingtheUKeconomyatrisk.TaskforcememberJeremyLeggettsays:“Onlytwo things are standing in the way: a collective sense of urgency consistent with peak-oilrisk,andeffectiveyokingofindustryandgovernmentinstrategicharness.”

Burning liquid hydrocarbon fuels made from oil is respon-sible for around 30% of global

CO2 emissions contributing to climate change

1 The UK Energy Research Centre (UKERC) Global Oil Depletionreport(October2009)statesthatthereissignificantriskofpeakoiloccurringbefore2020;alsothatlargeresourcesofconventionaloilare‘unlikelytobeaccessedquickly’,ppix-x.

2 http://cdiac.ornl.gov/trends/emis/tre_glob.html,2007data(June2010).3 IndustryTaskforceonPeakOilandEnergySecurity,The Oil Crunch: a wake-up call for the British economy,February2010.

The growing danger of dirty oil

Energy companies are increasingly looking to meet continuing growth in energy demandbyexploitingriskyandhighlypollutingsourcesofoilandgas,suchasdeep-wateroilandunconventionaloilsliketarsands.Butthesecomeatanenormouscost,economicallyandenvironmentally,atatimewhenweshouldbeinvestinginrenewables.Manyoilreservesarelocatedinpristineplacesthatarevitalforbiodiversity–includingtropicalrainforestsandtheArctic.Extractingthemisdifficultanddangerous,andfurtherdisastersliketheDeepwaterHorizonoilspillintheGulfofMexicoareinevitable.

Closertohome,therearenowmovestolicensedeep-seadrillingforoilneartheShetland Islands and off the west coast of Scotland – vulnerable areas where environmentaldamagewouldbedifficulttocontainintheeventofablowout.

We’verecentlyhighlightedanobscurelegalityinCrownEstateleasesthatshowsaclear institutional bias towards offshore oil and gas exploration to the detriment of renewables.ButiftheuseofEVsandrenewableswereexpanded,thiswouldhelptoreducefueldemand,meaningtherewouldbelessneedtorelyonincreasinglyriskysourcesofoilandgas.

Webelievethere’sawayforward.Ourvisionisforalow-carbonfuturebasedonrenewableenergy,energyefficiencyanddemandreduction,wherefossilfuel-dependentcarsareincreasinglyreplacedbyEVs.

Thisisabigchallenge,butthere’snoreasonwhytheUKcannotplanforsuchafuture.ArecentreportfromtheEuropeanClimateFoundation(ECF)4 shows that Europe does not need to rely on nuclear energy or fossil fuels to meet ambitious carbontargetsorenergysecurityobjectives–andthatanelectricitysystembasedon100%renewableenergysourcesisaffordableandachievable.Moreover,theECFreportfoundthatthiscouldbeachievedalongsideverysubstantialelectrificationofroadtransport.

TheUK’sCommitteeonClimateChangehasalsorepeatedlycalledforneardecarbonisation of the power sector by 2030 as a critical milestone to achieving theClimateChangeActtargetofareductionintheUK’sgreenhousegasemissionsofatleast80%by2050.5Inordertoachievethistarget,theyrecommendastrongfocusonefficiencyanddemandreduction,adecarbonisedpowersector,andtheelectrificationoftransport.

Inourview,EVsonlymakesenseinthecontextofanew,moresustainableapproachtotransportwhichacceptstheneedtoreduceourrelianceonfossilfuels,managedemand,andpromotealternativestotravel.AsKeithAllott,WWF-UK’sHeadofClimateChangeexplains:“Beitoilandcoalorflightsandcarkilometres,peopleneed to consume and travel less – and more intelligently – if the UK is to meet its climatechangetargets.Businessasusual(BAU)practicesandanoverrelianceontechnologyimprovementswillnotbeenough.Weneedtomaketherightsetofchoicestobringaboutfundamentalchangeifwe’retoreduceouroildependency andmakethetransitiontoalow-carboneconomy.”

“Be it oil and coal or flights and car

kilometres, people need to consume and

travel less – and more intelligently – if the UK is to meet its climate change targets. We need to make the right set of choices to

bring about fundamental change if we’re to reduce

our oil dependency and make the transition to a

low-carbon economy”

keith allott, head of climate

change, WWF-Uk

4 Roadmap 2050: a practical guide to a prosperous, low-carbon Europe,EuropeanClimateFoundation,April2010.5 ForexampleintheCommitteeonClimateChangeletterfromAdairTurnertoChrisHuhne,9September2010,regardingthe

levelofrenewableenergyambitionto2020.

8Electric avenues page

Executive Summary

Energy companies are increasingly looking to meet continuing growth in energy demand by exploiting risky and highlypollutingsourcesofoilandgas,suchasdeep-wateroilandunconventionaloilsliketarsands.

© Jir

i re

za

c / W

WF-U

k

10Electric avenues page

Executive Summary

EVs as part of the solution, not a panacea

Ifwe’reseriousaboutreducingouroildependency,thenEVshavetobeanimportantpartofthesolutionastheyareamuchlowercarbonalternativetoconventionalcars,whichproduce14%ofCO2emissionsintheUK6.EVsarealsomoreenergyefficient,with75%efficiencycomparedtothe20%efficiencyoffossilfuel-poweredcars7.ButEVsarenotcarbonfree.Ultimately,thescaleofthecontributiontheycouldmake to a low-carbon transport sector depends on the carbon intensity of the electricity thatpowersthem.That’swhyEVsneedtogohandinhandwithdecarbonisation ofthegrid.

ItisalsoimportantthatEVsareusedtodriveless,notmore–whichwillbeachallengeasEVshaveloweroperatingcosts.IfEVscontributetoariseincarkilometres,we’llneedfarmoreofthemtoachievethesameresultasdrivinglessintermsofreducingfueldemandandcaremissions.Greatersupportforwalkingandcycling,carsharingandmoreattractivepublictransportoptionswouldallhelptobringdowncarkilometresbyreducingtheneedforprivatecartravel.Othermeasures such as road and congestion charges or higher parking charges would also helptocurbdemand.

EvenwithoutEVs,thereissignificantpotentialtoreducecaremissionsandoilconsumptionbyimprovingICEVengineefficiency.PressingforstrongerEUlegislationtoreduceaveragefleetemissionsfromICEVs8 needs to be a continuing priority,especiallybefore2020whileEVsareintheirinfancyandthegridisstillsubstantiallypoweredwithfossilfuels.Tighteremissionstargetswillbecriticalindrivingthewidespreadinvestmentinresearchanddevelopment(R&D)thatwillbringdownEVcostsandmakethemcommonplaceontheroads.

EVs offer a promising way of reducing our oil dependency and improving our ability tomeetclimatechangetargets.AthighlevelsofuptakeandtogetherwithICEVefficiencyimprovementsanddemandmanagement,EVscoulddeliverareductionofnearly80%infossilfueldemandfromcarsby2030,andatthesametimedelivera75%reductionincarbonemissionsfromcars. Replacing the need for biofuels

Another low-carbon alternative to EVs would be to opt for high levels of biofuel use inconventionalcars.Althoughwebelievethatbioenergycouldplayanimportantroleinmeetingtheworld’senergyneedsinfuture,it’simportanttorealisethatitisafiniteresourcewithnumerouspotentialimpactsonlanduse,foodandwatersecurityandbiodiversity.

Biofuels should therefore be considered a last resort for sectors where at present therearenopracticalalternativestofossilfuels–suchasaviation,shippingandheavygoodstransport.Incontrast,anattractiveandfeasiblealternative–electrification–isavailableforpassengercars,sotheuseofbiofuelsforthissectorshouldnotbeconsideredahighpriority.

6 CommitteeonClimateChange,www.theccc.org.uk/sectors/transport7 Seepp82-83ofWWF’sPlugged Inreportforanefficiencycomparisonofelectricalversusmechanicalpowertrains.Theenergy

efficiencyofEVsisheavilydependentonthe‘generationmix’oftheelectricityusedtopowerthem.Usingcoalorgas-firedplanttogeneratetheelectricityusedforchargingEVssignificantlyreducestheiroverallenergyefficiencyand,worstcase,canputthemnearlyonaparwithICEVs,asdiscussedinp95ofElementEnergy’sresearchreport.

8 TheEuropeanParliamentpassednewcarCO2legislationthatsetsanemissionscapof130gCO2/kmaveragedoverallnewvehiclesproducedbyeachmanufacturerby2015.Reachingthisgoalwillbephasedinoverthreeyears,from2012.Anextendedtargetissettobeanaverageof95gCO2/km/kmby2020.

EVs are also more energy efficient,with75%ef-

ficiencycomparedtothe20%efficiencyoffossil

fuel-powered cars

A rapid rise in EV numbers is needed

EVscouldstartdeliveringsubstantialcarbonsavingsby2020.Butweneedlotsofthem–atleast1.7millionEVsby2020and6.4millionby2030–iftheyaretomakeaseriousdentoncaremissions.Thiswillrequireahighlevelofpolicyinterventionby the government to both invest in the conditions and infrastructure that are neededforEVstosucceedandtohelp‘normalise’theiracceptancebyconsumers,andprovideincentivesfortheirpurchase,inordertoensurearapidriseinEVnumbersthatwillbeneededforthemtomakeadifference.

TherearethreemainreasonsfortakingearlyactiononEVs.SupportnowforUKmanufacturers will help to establish a market-leading EV industry and create green jobs.Acontinuationofthecapitalgrantscheme,andanincreaseinthetotalfundsavailable,willhelptostimulateearlypurchasesofEVs.Andplanningnowforgridimprovements and rolling out new charging infrastructure will ensure that these are readyintimetoaccommodatehighlevelsofEVs. Supporting the rapid growth in renewables

We’reconvincedthatafuturewherepeoplesharetheworld’snaturalresourcesmoresustainablyiswithinourgrasp,basedonmuchgreateruseofrenewableenergysources.AsignificantincreaseinelectricityfromrenewablesisrequirediftheUKistomeetthegovernment’srenewableenergytargetof15%by2020,andifwearetoachievea100%renewableenergyfutureby2050.EVscanhelptosupportthistransitionbychargingattimesoflowoveralldemandonthegrid,usingpowerfromrenewablesourceswhenitmightotherwisenotbeused.ChargingattimeswhentheCO2intensityofthegridislowalsohelpstoreducethecarbonimpactofEVs.

Itisencouragingthat,evenathighlevelsofuptake,EVs’impactonthegridisnotasgreatasperhapsfeared.Atanationallevel,theirimpactcanbecontainedwithintherangeofNationalGridforecasts.Longerterm,EVsalsohavethepotentialtofeedpowerbacktothegridattimesofpeakdemand.Butsuchvehicletogrid(V2G)applicationsmustfirstovercomesignificanttechnicalandeconomicchallengesifthisaspectofEVpotentialistoberealised. The importance of investing now to ensure the UK is ‘EV ready’

InorderforpeopletowanttodriveEVs,theyneedtogetusedtoseeingthem,perhapsinitiallyingovernmentorcorporatecarfleetsorcarsharingclubs.Theyalsoneedplentyofencouragement,fromfreeparkingspacestoexemptionfromcongestionchargingandVehicleExciseDuty(VED).ButcapitalgrantswillbemostimportantinordertoreducethehighupfrontcostofEVsrelativetoICEVs.ThisgovernmentfundingforEVsneedstocontinuewellbeyond2012,oncetheeconomyimproves,inordertoboostsales.Inaddition,newmodelsofownership,suchasleasingschemes,maybeneededthatshiftthecostofEVownershipovermanyyears.

Aflexiblechargingnetworkisalsorequired,involvingchargedelaydevicesandsmartgrids,sothatEVscanbechargedattimesoflowelectricitydemandandwhenthecarbonintensityofthegridislow.TheUKgovernment’ssupportforintegratedsmart grids and standardised charging points and compatible charging technology across Europe will be important if EVs are to provide more than a localised solution toreducingtransportemissions.Doingthisearlywillhelptoshapeanddevelopthefuture market for EVs and provide a consistent model for EV charging across the UK andEurope.

EVS Can hELp to SUpport thE tranSition to

rEnEwabLES by Charging at timES of Low oVEraLL

DEmanD on thE griD, USing powEr from

rEnEwabLE SoUrCES whEn it might othErwiSE

not bE USED

Electric avenues page 11

Executive Summary

Mostchargingpointswillbeneededathome,withdelayedovernightchargingtoputlesspressureonthegrid.Workplacechargingpointswillalsoberequired,althoughtraveltoworkbyprivatecarneedstoreduce.Chargingpointsatotherhighvisibilitylocationssuchassupermarketsorinfrontoftownhallswillalsobeimportant.

ThereisalsoapressingrequirementforR&DinvestmenttoimproveEVcostandperformance.Inparticular,reducingbatterycostsandincreasingtheirstoragecapacityandrangewouldmakeEVsmoreattractivetoconsumers.

Muchmarketlearningisstillneededfornewbusinessmodelstosucceed,suchasEV car sharing instead of ownership or (borrowing from the mobile phone business model)batteryleasingandswapping,perhapsatpetrolstationforecourts,tohelpreducethecostofEVsandincreasetheiruptake. Insights not forecasts

Thisreportpresentsthefeasibility,opportunitiesandchallengesofmovingawayfromoil-dependentcartravel.ItsetsoutthreedifferentscenariosforEVuptake:aBusinessasusualscenario(BAU)representinglowlevelsofEVs(1.7millionEVsby2030);anExtendedscenariowithmediumEVlevels(6.4millionEVsby2030);andaStretchscenariowhichstresstestsafuturewithveryhighEVuptake(26.3millionEVsby2030).

Our research builds on two other WWF reports: Plugged In,whichlookedattheimportanceofEVsinrelationtodecliningoilresources,andWatt Car,whichexaminedtheroleforEVsinScotland.Thisreport,ourfirsttofocusontheUKpotentialforEVsin2020and2030,usesasimilarmethodologytothatusedby Watt Car toestimateCO2savingsandgridimpactsfromEVs.

Itisimportanttonotethatthesescenariosareintendedtoprovideinsights,notforecasts.TheyaimtoprovideabetterunderstandingoftheroleEVscouldplay,aswellaswhathastohappeninorderforEVstorealisetheirpotential.Thefutureislikelytoliesomewherebetweenthescenariosthatthisreportdescribes.However,itisclearthatatleast1.7millionEVswillbeneededby2020and6.4millionby2030inordertoachievethelevelofambitionthatweneed.

+ –Weneedatleast1.7million EVs by 2020 and6.4millionby2030 if they are to make a serious dent on car emissions

EVs are a much lower carbon alternative to conventionalcars,whichproduce14%of CO2 emissions in the UK

We need to wean ourselves off oil and decarbonise our economies in order to ensure that average global temperatures rise by no more than 1.5Ccomparedto pre-industrial levels

12Electric avenues page

Executive Summary

1. introDUCtion EVs are needed to reduce car emissions to levels which are in line withUKclimatechangetargets.EVs

have many advantages over conventional cars and the UK already has a strong presence in this market.

1.1 Meeting UK climate change obligations

The UK is legally committed to reduce its greenhouse gas emissions by at least 80%by2050,from1990levels,undertheClimateChangeAct.Thegovernmenthasacceptedaninterimreductiontargetof34%for2020astheUK’scontributiontowardsachievinganEU-wideemissionsreductiontargetof20%.However,theCommitteeonClimateChange(CCC)hasrecommendedan‘intended’targetfor2020of42%–whichisinlinewithamoreambitious30%targetinEurope.WWFisalsosupportingaUKemissionsreductiontargetof42%by2020,whichwebelievecanandmustbeachievedthroughdomesticactionratherthanoffsetting.

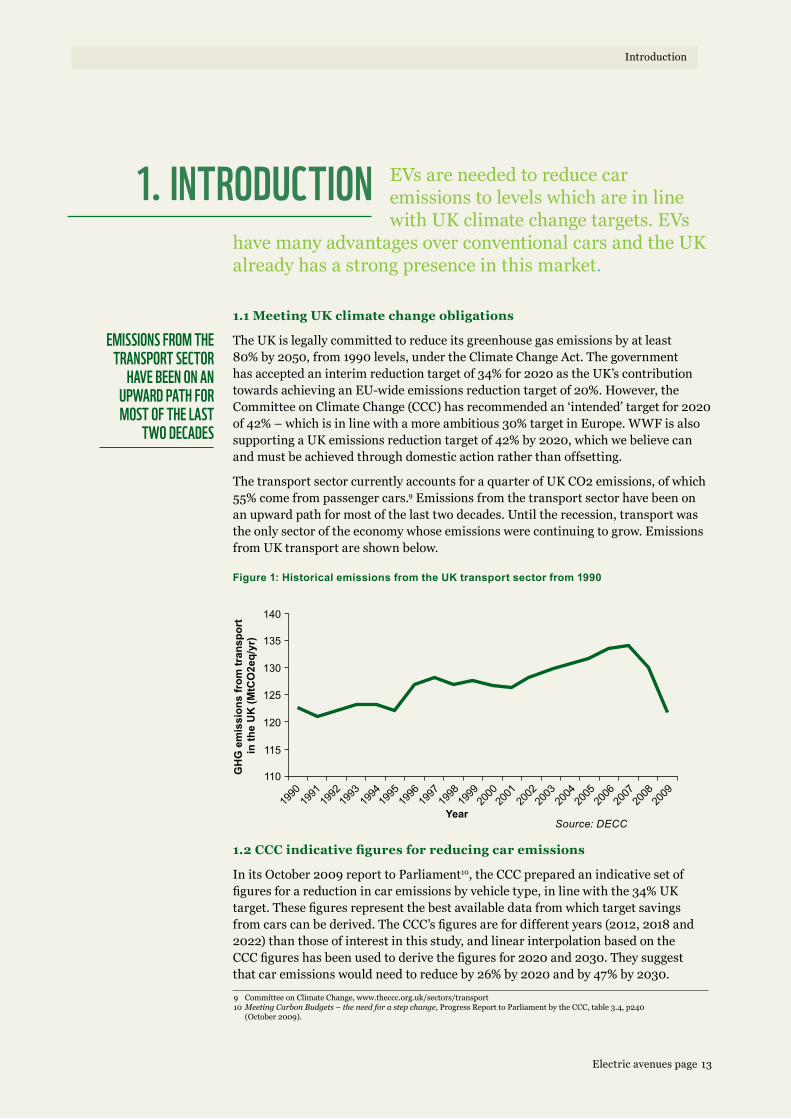

ThetransportsectorcurrentlyaccountsforaquarterofUKCO2emissions,ofwhich55%comefrompassengercars.9 Emissions from the transport sector have been on anupwardpathformostofthelasttwodecades.Untiltherecession,transportwastheonlysectoroftheeconomywhoseemissionswerecontinuingtogrow.EmissionsfromUKtransportareshownbelow.

Source: DECC

Figure 1: Historical emissions from the UK transport sector from 1990

1.2 CCC indicative figures for reducing car emissions

In its October 2009 report to Parliament10,theCCCpreparedanindicativesetoffiguresforareductionincaremissionsbyvehicletype,inlinewiththe34%UKtarget.Thesefiguresrepresentthebestavailabledatafromwhichtargetsavingsfromcarscanbederived.TheCCC’sfiguresarefordifferentyears(2012,2018and2022)thanthoseofinterestinthisstudy,andlinearinterpolationbasedontheCCCfigureshasbeenusedtoderivethefiguresfor2020and2030.Theysuggestthatcaremissionswouldneedtoreduceby26%by2020andby47%by2030.

9 CommitteeonClimateChange,www.theccc.org.uk/sectors/transport10 Meeting Carbon Budgets – the need for a step change,ProgressReporttoParliamentbytheCCC,table3.4,p240

(October2009).

EmiSSionS from thE tranSport SECtor

haVE bEEn on an UpwarD path for moSt of thE LaSt

two DECaDES

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

110

115

120

125

130

135

140

Year

GH

G e

mis

sion

s fr

om tr

ansp

ort

in th

e U

K (M

tCO

2eq/

yr)

Electric avenues page 13

Introduction

WethenaskedElementEnergytotakethefiguresdescribedaboveandadjustthemtobeinlinewithamoreambitious42%reductiontargetby2020,whichwebelievewillgivetheUKabetterchanceofmeetingits80%reductiontargetfor2050.Thismeansthatcaremissionswouldneedtocomedownby32%by2020and,usinglinearinterpolation,by51%in2030.11ThesehigherambitionfigureshavebeenusedastheemissionsmilestonesshowninChapter3ofthisreport.WehavelookedattheabilityofeachofourthreeEVscenariostomeettheseemissionsmilestones.

Lookingbeyond2030,theCCC’sindicativefiguresforthereductionofcaremissionssuggestthatcaremissionswillneedtofallby90%by2050inordertomeettheoverall80%emissionsreductiontarget.

The main types of EVs

Battery electric vehicles (BEVs)

BEVssuchastheNissanLeafuseanelectricmotor,oranumberofelectricmotorstopropelthevehicle.Theenergysuppliedisfrombatterieswithinthevehicle.ABEV’srangeislimitedbythestoragecapacityofthebattery.Insteadoffillingupatapetrolstation,thebatterymustberechargedfromanexternalsource. Plug-in hybrid electric vehicles (PHEVs)

PHEVs such as the Vauxhall Ampera use a combination of an electric motor andbatteriesalongwithaninternalcombustionengine(ICE).PHEVscomeintwomaintypes:parallelandseries.Inserieshybridsthesolesourceofmotivepowertothewheelscomesfromtheelectricmotor(s).Themotorissuppliedwith electricity from a battery or directly from a generator (driven by an internal combustionengine).Whentheengineisrunninganyexcesschargeisusedtorechargethebattery.

Parallel hybrids differ from series in that they can transmit power to drive the wheelsfromtwoseparatesources,suchasanICEandbattery-poweredelectricmotors.Somemanufacturersaredevelopingseries-parallelhybrids,whichareabletooperateineitherseriesorparallelmode.

HybridElectricVehicles(HEVs),suchastheToyotaPrius,differfromPHEVsinthattheycannotplugintorecharge,althoughbothHEVsandPHEVsareprimarilypoweredbypetrolordiesel.

Inthisreport,onlyBEVsandPHEVsareincludedinthefiguresforEVs,withourscenariosassuminganequalsplitbetweenthetwo.HEVsareincludedinthefiguresforInternalCombustionEngineVehicles(ICEVs).

Hybrid Electric Vehicles (HEVs) such as the Toyota Prius are different from PHEVsinthattheydonotrequirechargingfromthegridandusemotiveenergy,largelysuppliedthroughanICE,torechargethebattery.

WWFhasusedthetermEVsgenericallytoincludeBEVsandPHEVsonly.

11 AmoredetaileddescriptionofthemethodologyusedtoadjusttheCCC’sfigurescanbefoundinAppendix8.3.1toElementEnergy’sresearchreport.FollowingadditionalanalysisbytheCCContheimpactsoftherecession,theirFourthCarbonBudget(December2010)showsthattheachievementofthe42%target(intheExtendedAmbitionscenario)islookingmorelikely,atleastinthenon-tradedsector(includingtransport).

Car EmiSSionS nEED to ComE Down by 32% by 2020 anD 51% by 2030

-32%

14Electric avenues page

Introduction

1.3 The advantages of EVs

The main advantages of EVs over conventional cars are that they are less oil dependentandareconsiderablymoreenergyefficient.Theinternalcombustionengineisincrediblyinefficient,wastingoverthree-quartersoffuelenergy,whereasBEVsachievearound75%efficiency.12ThefuelefficiencyofPHEVsisalsobetterthanICEVs,althoughlessgoodthanBEVs.

ComparedtotheaverageICEV,EVsalsooffercarbonsavingsevenwithtoday’slargelyfossil-fuelpoweredenergygrid.Forexample,theaverageemissionsperformanceofallnewcarssoldinthefirsthalfof2010was145gCO2/km.13Thiscomparestojustover100gCO2/kmforaBEVchargedwithgridelectricity.14 As the electricity sector issteadilydecarbonised,whichisaprerequisiteforachievingourUKclimatechangetargets,EVswillgenerateevenloweremissionscomparedtoICEVs.

EVsreduceoreliminatemanyoftheissuesassociatedwithconventionalcars,including:

• Long-termsustainabilityissues–asfossilfuelsuppliesarelimitedandtheenvironmental impact of extracting these fuels from increasingly risky sources canbesevere.

• Carbonimpact–thecombustionoffossilfuelsreleasesCO2intotheatmosphere,contributingtoclimatechange.

• Pricevolatility–traditionaltransportationfuelpricesarelinkedtothepriceofoil,whichishighlyvolatileandexpectedtoincreaseinthemediumtolongtermassuppliesdiminish.

• Securityoffuelsupply–theworld’soilreservesareconcentratedinarelativelysmallnumberofcountries.

• Airqualityissues–theburningofpetrolanddieselcontributestoairpollution,especiallyincities,withsignificanthealthimpacts.

EVs can therefore not only help to reduce our oil dependency and the climate change impactsofconventionalcars,theycanalsoreduceairpollutionassociatedwithemissions.Airpollutionisassociatedwithrespiratoryandcardiacdiseases,whicharemajorcontributorstosicknessandmortality.AirqualityimprovementsthroughgreateruseofEVs,tougheremissionslegislation,anddemandreductionmeasureswouldbenefitthehealthoftheUKpopulationandcontributetohealthcaresavings. 1.4 The emerging EV market

EV manufacturers

Analysis by Frost and Sullivan15suggeststhatover47manufacturersareexpectedtocompeteintheglobalEVmarketwithover75modelsby2015.Chineseoriginalequipmentmanufacturers(OEMs)areexpectedtolaunch35EVmodelsinthenextthreetofiveyears.ThisemergingEVmarketwill,tostartwithatleast,remaindominatedbytraditionalOEMs.ManufacturerssuchasToyota,Ford,Volvo,BMW,VW,Nissan,Renault,GM,TataandSmartallhavemodelscomingtothemarketinthenearfuture.

12WWF,Plugged In:theendoftheoilage,pp79-83(2008)13 DatafromSMMT:www.smmt.co.uk14 EmissionsfromEVsbasedontypicalgridtowheelefficiencyof02.kWh/kmandanaveragegridCO2intensityof517gCO2 kWH,whichisthefigureusedinthegovernment’slatesttoolforassessingthecarbonimpactofnewdwellings.15 FrostandSullivan,Electric Vehicles: Market Opportunities and New Business Models for Industry Stakeholders,MaRSMarket

Insights,20September2010.

EVS not onLy hELp to rEDUCE oUr oiL

DEpEnDEnCy anD thE CLimatE ChangE impaCtS

of ConVEntionaL CarS, thEy Can aLSo rEDUCE air

poLLUtion aSSoCiatED with EmiSSionS

Electric avenues page 15

Introduction

IntheUK,theNissanLeaf,Mitsubishii-MiEVandnewplug-inToyataPriuswillallgoonsalein2011.Renault-Nissanhasannounceda£420millioninvestmentbothtoproducetheLeafandtobuildanewbatteryplantatSunderland,TyneandWear,where50,000EVswillbeproducedinitiallyasfrom2013.Some2,250peoplewillbeemployedatNissanandacrosstheUKsupplychain.Toyota’sAurishybridismanufacturedinBurnaston,Derbyshire.TheVauxhallAmpera(sisterEVtotheUSChevroletVolt)mayalsobemanufacturedinEllesmerePort,Merseyside.Inaddition,threeUKcompanies–SmithElectricVehicles,AlliedVehicles,andModec–arewellestablishedelectriccommercialvehiclemanufacturers.

UK manufacturers therefore have a head start in EV manufacture which should give themacompetitiveadvantageinthefuture,asthemarketgrows. Current number of EVs

TheEVmarketisstillinitsinfancy.Accordingtothelatestfigures,therearecurrently61,000HEVsand1,400BEVslicensedinGreatBritain.16 There are currentlynoPHEVsonthemarket.

SalesofBEVsin2009weretiny,withonly55newcarsregistered,incomparisonto397in2007.MostofthesewereG-Wizcars,manufacturedinIndia.Thissharpdrop in sales has been interpreted as due to the recession or because people are waitingforgovernmentgrantstoarrivebeforepurchasinganEV.CertainlyUKEVmanufacturersarebullish,asistheDfTwhichexpects8,600EVstobesoldin2011oncecapitalgrantsforEVsareavailable.

To move from thousands to millions of EVs in future will clearly be an enormous task,requiringsubstantialinvestmentandgovernmentsupport.ChallengesandopportunitiesforgrowingtheEVmarketarediscussedfurtherinChapter5.

16 DfT2009figuresforBEVsandPHEVs.Thisconcurswiththegovernment’sresponsetotheSecondAnnualProgressReportoftheCommitteeonClimateChange,p35,whichshows1,453EVsregisteredin2009.

16Electric avenues page

Introduction

2. thrEE SCEnarioS for EVS

Inordertoexaminethefeasibility,opportunities and challenges of moving away from oil-dependent car travel,threedifferentscenarioshavebeen prepared – Business as usual

(BAU),ExtendedandStretch–basedonlow,mediumandhighlevelsofEVuptake.TheseshowarangeofpossiblefuturesforEVs.

2.1 What’s behind the scenarios

Abasiccomparisonofthethreescenariosisshownbelow,includingthemainassumptions for each one:

For more detailed information about the assumptions and parameters used for each scenario,pleaseseeAppendixAinthisreportorrefertoElementEnergy’sresearchreport at wwf.org.uk/electricvehicles

It’simportanttonotethatthesescenariosareindicativeonly(representingdifferentlevels of EV uptake and a range of alternative futures) and do not attempt to forecast consumerdemandforEVs.ThenumberofEVsneededforeachofthethreescenariosisshownbelow.

A50/50splitbetweenBEVsandPHEVshasbeenassumedinallthreescenariosforpurposesofsimplicity,asitisnottheintentionofthescenariostoprovideforecastsbytypeofEV.

Allthreescenariosassumeneardecarbonisationofthegridby2030.

Table 1: Comparing the three scenarios

Scenario

BaU

extended

Stretch

EV support policies

existing and announced

Some additional support

Very high support and investment

EV contribution to UK CO2 target

Minimal

Medium

high

Demand for car travel

Growth

Stabilisation

Stabilisation

EV cost

Medium

Medium

high17

EV range

Medium

Medium

high

Table 2: EV numbers needed for each of the three scenarios

17 ThecostishighduetotheassumptionthatBEVshaveahighrange(250km)intheStretchscenario,whichmeanslargercapacitybatteries,resultinginhighercost.Thereisadebatetobehadaroundtheimpactofanybatterycostreductionsinfuture–i.e.theextenttowhichtheywillfeedthroughintolowercostEVsversushighercostEVswithgreaterrange.

Electric avenues page 17

Three scenarios for EVs

EVs

Number of eVs needed

eVs as % of new car sales

eVs as % of all Uk cars

BAU2020 2030

160,000 1.7m

1% 8%

0.5% 5%

Extended2020 2030

1.7m 6.4m

15% 20%

6% 18%

Stretch2020 2030

4.2m 26.3m

44% 80%

13% 74%

2.2 Purpose of the scenarios

The main purpose of the scenarios is to examine the impact of EVs on UK carbon emissions,aswellasfuelandelectricitydemand.TheStretchscenarioistheonlyonethat’sbeendesignedtomeetthehigher42%carbonreductiontargetfor2020,whichwesupport.However,we’veexaminedtheabilityofallthreescenariostomeetthismoreambitioustarget.

Thescenarioslookatpassengercarsonly.Theyincludeassumptionsonthedemandforcartravel,emissionreductionsthroughmeasuressuchaseco-driving18 and speed limitenforcement,andthespeedatwhichthemarketforEVstakesoffinfutureyears.We’vemadeotherassumptionsontheefficiencyofallcartypes,EVrange,andthecarbonintensityofthegrid.

Adescriptionofeachscenariofollows. 2.3 The business as usual (bau) scenario

The BAU scenario is a realistic one if current policies and behaviours remain unchanged.Underthisscenario,EVswillhaveminimalimpactinreducingUKcarbonemissions.

This scenario shows the level of EV uptake assuming that existing and announced policiesremaininplace,withnofurthersupportforEVs.TheseincludetheDfT’s‘Plugged-inPlaces’schemetoinstallchargingpointsinkeyUKcities,whichwasrecently extended from three to eight cities and regions19aspartofits£400millionfundingforlow-carbonvehicles,announcedintheComprehensiveSpendingReview.Thisfundingalsoincludes£43millionincapitalgrantsasfrom1January2011tosupporttheuptakeofEVs,withsubsidiesofupto£5,000pervehicle20.AreviewofthisfundingwilltakeplaceinJanuary2012.Ifnofurtherfundingismadeavailableasaresultofpublicspendingcuts,thelevelofEVuptakeintheBAUscenariowouldbeevensmallerthanthatshownhere.

InaBAUfuture,EVsonlyaccountforasmallpercentageofnewcarsalesandUKcars.Theyremainanicheproductforatleastadecadeandprovidelittleinthewayofcarbonsavings.

The BAU scenario assumes that ICEVs will remain the predominant vehicle and that theirefficiencywillimproveinlinewithEUlegislation,i.e.130gCO2/kmby2015,withafurtheratargetof95gCO2/kmproposedfor2020.TheseimprovementsmeanthatICEVswillhelptoreducecaremissions,evenwithoutmanyEVsontheroad.Buttheywillbeinsufficientontheirowntohittheemissionsmilestonesinlinewitha42%target,andstillleaveUKcartravelverydependentonoil.

Underthisscenario,thecarbonintensityofgridelectricityremainshighuntil2020,but by 2030 this will have reduced markedly as a result of less polluting sources of energycomingon-stream,inlinewiththeCCC’srecommendations.

18 Accordingtoa2010DfTconsultationoneco-drivingtraining,thedefinitionofeco-drivingincludesdrivingatefficientspeeds,fuelefficiencyandchoiceofgear,bestpracticeforaccelerationandbrakingandanticipationfortrafficanddrivingconditions.

19 London,MiltonKeynes,theNorthEast,Midlands,GreaterManchester,eastEngland,ScotlandandNorthernIreland.20The£43millionoffunding,whichwasannouncedbytheSecretaryofStateforTransportinJuly2010tosubsidiseEVpurchases,

at£5,000pervehicle,between2011and2012andconfirmedintheComprehensiveSpendingReviewinOctober2010,isagooddeallessthanthe£230millionallocatedbythepreviousgovernment.InDecember2010,thegovernmentannouncedthenineBEVsandPHEVsthatwillinitiallybeeligibleforthisgrant:theNissanLeaf,Mitsubishii-MiEV,Smartfortwoelectricdrive,PeugeotiOn,TataVista,CitroenCZero,VauxhallAmpera,ToyotaPriusPlug-inHybridandChevroletVolt.

18Electric avenues page

Three scenarios for EVs

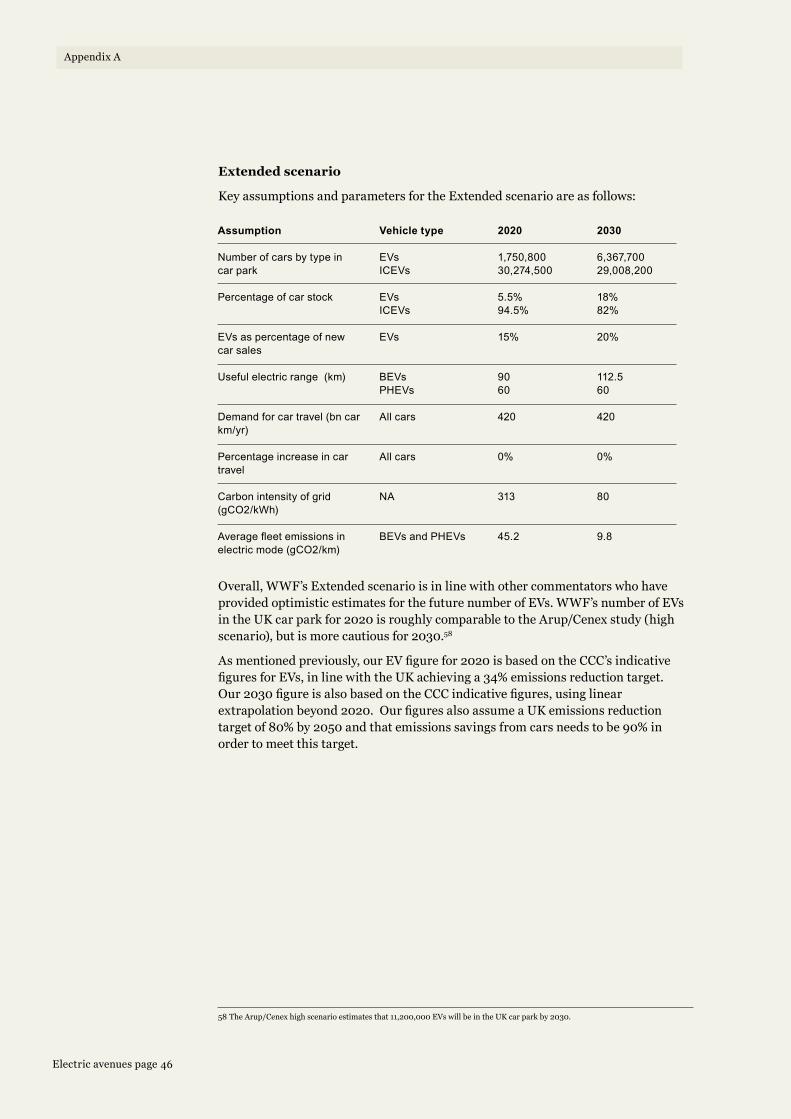

2.4 The extended scenario

Inthisscenario,we’veassumedmediumlevelsofEVuptake,andthatcarbonsavingsfromEVsstarttoberealised.

EVuptakeundertheExtendedscenarioissignificantlyabovethatoftheBAUscenario,with a relatively high increase in production capacity and demand within the next decade.Inthisscenario,EVsareestimatedtoaccountforaround15%ofnewcarsalesby2020,and20%by2030,correspondingto6%ofallUKcarsby2020,and18%by2030.RampingupEVpenetrationtothislevelrequiresadditionalpolicysupportfromgovernment,suchasadditionalfundingforlowcarbonvehiclesandacontinuationofthe£5,000pervehiclesubsidywellbeyond2012.

Inthisscenario,thereare1.7millionEVsby2020.ThisfigurematchestheCCC’srecommendedlevelofEVpenetrationinlinewiththeUKachievinga34%carbonreductiontargetby2020.

TheExtendedscenarioassumesstabilisationintrafficgrowthat2010levels,improvementsinICEVefficiency,andCO2savingsfromeco-drivingandspeedlimitenforcement.WeassumethesamecarbonintensityofthegridasintheBAUscenario. 2.5 The stretch scenario

The Stretch scenario is in line with the emissions reduction that we expect the car sector tocontributeinordertoachievea42%carbonreductiontargetby2020.ItassumestheveryhighestlevelofEVuptakeinordertoindicateEVs’maximumcarbonsavingspotentialand‘stresstests’theimpactofextremelyhighEVlevelsonthegrid.ItassumesarapidincreaseinEVnumbersoverthenextdecadeandbeyond,withtrafficstabilisedattoday’slevels.It’stheonlyoneofthethreescenariosthat’sbasedonmeetinga42%emissionsreductiontargetby2020.

Thisisnottosaythattheonlywaya42%targetcanbeachievedisbymeetingtheStretchscenario.Butifcaremissionsdonotfalltothelevelneededtomeetthistarget,thenothersectorswillhavetodecarbonisemore.

InordertoachievethislevelofEVuptake,arapidincreaseinEVproductionvolumesisneededtokeepupwithdemand.ContinuingsubsidiestoreducethecostofEVsandperformanceimprovementstoextendtheirrange,aswellasadditionalpolicysupport,arerequiredifthislevelofdemandistoberealised.

Sales of EVs start from a low base in the Stretch scenario but then follow a rapid growthtrajectory21whichistypicalofnewcartechnologiessuchastheToyotaPrius.Accordingtothisveryambitiousscenario,EVsaccountfor44%ofnewcarsalesby2020and80%by2030,faroutsellingICEVs.TheyalsorepresentthemajorityoftheUK’scarstockby2030. 2.6 Scope

The focus of this study is on passenger cars as this is the main market for EVs in the UK andthemainsourceofroadtransportemissions.AllsectionspertainingtoUKemissionssavingsandreductioninfueldemandfromEVsincludeNorthernIreland.However,gridimpactsandinfrastructureanalysisarefocussedonGreatBritain(includingEngland,WalesandScotland).ThisisbecauseNorthernIrelandandtheRepublicofIrelandbothshareaseparategridfromtherestofGreatBritain.Wedo,however,refertogridimpactsforNorthernIrelandandtheRepublicofIrelandinthetext.

21 Forfurtherinformationaboutgrowthtrajectoryassumptions,seeAppendix8.2.4inElementEnergy’sresearchreport.

Electric avenues page 19

Three scenarios for EVs

3. thE roLE of EVS in rEDUCing Carbon

EmiSSionS

EVscanmakeasignificantcontribution to helping the UK meet its emissions reduction targets andtoreducingouroildependency.

3.1 EVs and CO2 reduction

The importance of EVs in reducing emissions

If cars are to play their part in helping the UK to achieve a reduction in carbon emissionsof42%by2020andatleast80%by2050,thencaremissionsneedtofallbyaboutathirdby2020andbyhalfby2030.Thereisclearlyabigtaskaheadofus.

HighlevelsofEVuptakecanresultinsignificantemissionssavings,but:

• theelectricityusedtopowerEVsmustbesubstantiallydecarbonised;and

• theamountwedrivemustnotgrowfromcurrentlevelsandshoulddecline.

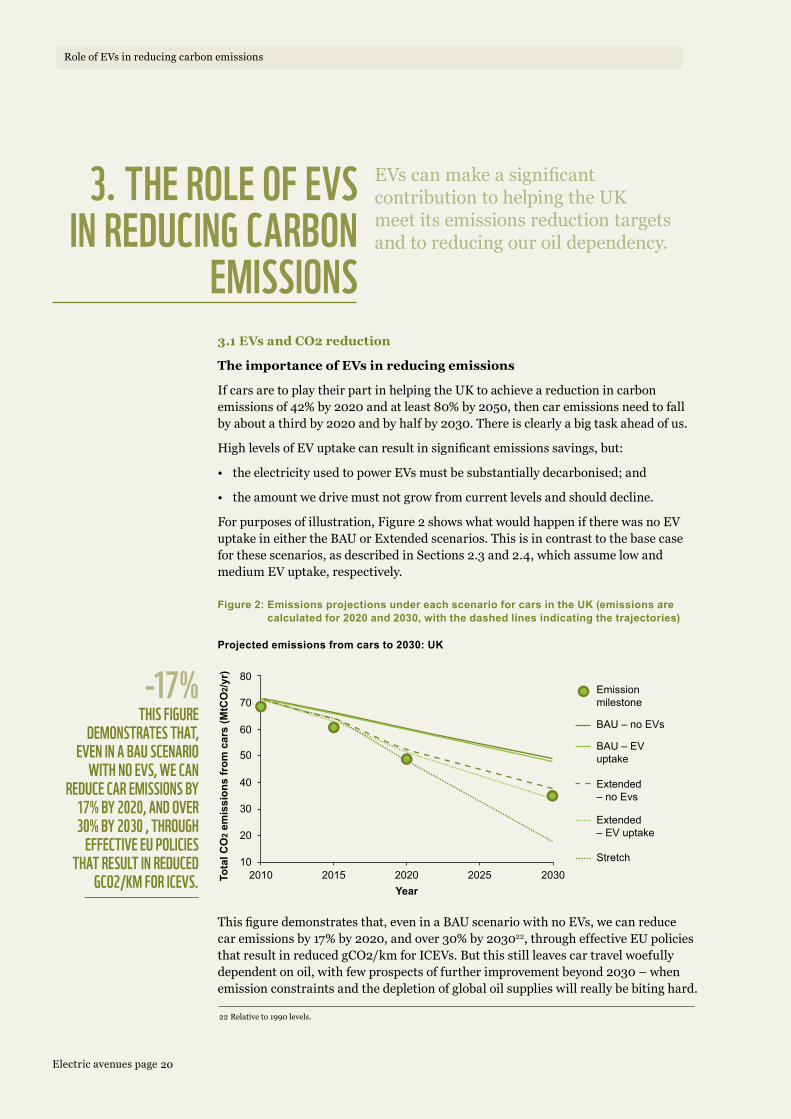

Forpurposesofillustration,Figure2showswhatwouldhappeniftherewasnoEVuptakeineithertheBAUorExtendedscenarios.Thisisincontrasttothebasecaseforthesescenarios,asdescribedinSections2.3and2.4,whichassumelowandmediumEVuptake,respectively.

Thisfiguredemonstratesthat,eveninaBAUscenariowithnoEVs,wecanreducecaremissionsby17%by2020,andover30%by203022,througheffectiveEUpoliciesthatresultinreducedgCO2/kmforICEVs.Butthisstillleavescartravelwoefullydependentonoil,withfewprospectsoffurtherimprovementbeyond2030–whenemissionconstraintsandthedepletionofglobaloilsupplieswillreallybebitinghard.

Projected emissions from cars to 2030: UK

Figure 2: Emissions projections under each scenario for cars in the UK (emissions are calculated for 2020 and 2030, with the dashed lines indicating the trajectories)

201010

20

30

40

50

60

70

80

2015 2020

Emissionmilestone

BAU – no EVs

BAU – EV uptake

Extended – no Evs

Extended – EV uptake

Stretch

Year

Tota

l CO

2 em

issi

ons

from

car

s (M

tCO

2/yr

)

2025 2030

22Relativeto1990levels.

thiS figUrE DEmonStratES that,

EVEn in a baU SCEnario with no EVS, wE Can

rEDUCE Car EmiSSionS by 17% by 2020, anD oVEr 30% by 2030 , throUgh

EffECtiVE EU poLiCiES that rESULt in rEDUCED

gCo2/Km for iCEVS.

-17%

20Electric avenues page

Role of EVs in reducing carbon emissions

Electric avenues page 21

Role of EVs in reducing carbon emissions

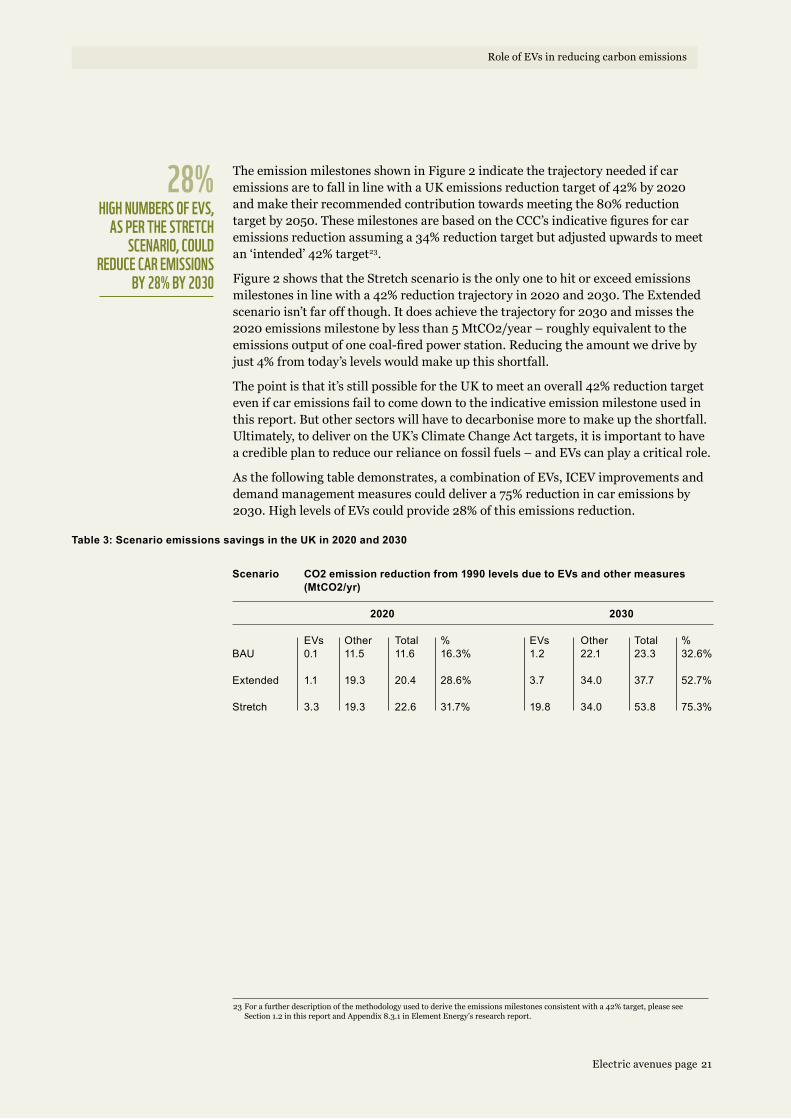

TheemissionmilestonesshowninFigure2indicatethetrajectoryneededifcaremissionsaretofallinlinewithaUKemissionsreductiontargetof42%by2020andmaketheirrecommendedcontributiontowardsmeetingthe80%reductiontargetby2050.ThesemilestonesarebasedontheCCC’sindicativefiguresforcaremissionsreductionassuminga34%reductiontargetbutadjustedupwardstomeetan‘intended’42%target23.

Figure 2 shows that the Stretch scenario is the only one to hit or exceed emissions milestonesinlinewitha42%reductiontrajectoryin2020and2030.TheExtendedscenarioisn’tfaroffthough.Itdoesachievethetrajectoryfor2030andmissesthe2020emissionsmilestonebylessthan5MtCO2/year–roughlyequivalenttotheemissionsoutputofonecoal-firedpowerstation.Reducingtheamountwedrivebyjust4%fromtoday’slevelswouldmakeupthisshortfall.

Thepointisthatit’sstillpossiblefortheUKtomeetanoverall42%reductiontargeteven if car emissions fail to come down to the indicative emission milestone used in thisreport.Butothersectorswillhavetodecarbonisemoretomakeuptheshortfall.Ultimately,todeliverontheUK’sClimateChangeActtargets,itisimportanttohaveacredibleplantoreduceourrelianceonfossilfuels–andEVscanplayacriticalrole.

Asthefollowingtabledemonstrates,acombinationofEVs,ICEVimprovementsanddemandmanagementmeasurescoulddelivera75%reductionincaremissionsby2030.HighlevelsofEVscouldprovide28%ofthisemissionsreduction.

Table 3: Scenario emissions savings in the UK in 2020 and 2030

Scenario

BaU

extended

Stretch

CO2 emission reduction from 1990 levels due to EVs and other measures (MtCO2/yr)

2020 2030

eVs0.1

1.1

3.3

other11.5

19.3

19.3

total11.6

20.4

22.6

%16.3%

28.6%

31.7%

eVs1.2

3.7

19.8

other22.1

34.0

34.0

total23.3

37.7

53.8

%32.6%

52.7%

75.3%

23Forafurtherdescriptionofthemethodologyusedtoderivetheemissionsmilestonesconsistentwitha42%target,pleaseseeSection1.2inthisreportandAppendix8.3.1inElementEnergy’sresearchreport.

high nUmbErS of EVS, aS pEr thE StrEtCh

SCEnario, CoULD rEDUCE Car EmiSSionS

by 28% by 2030

28%

The importance of other measures to reduce car emissions

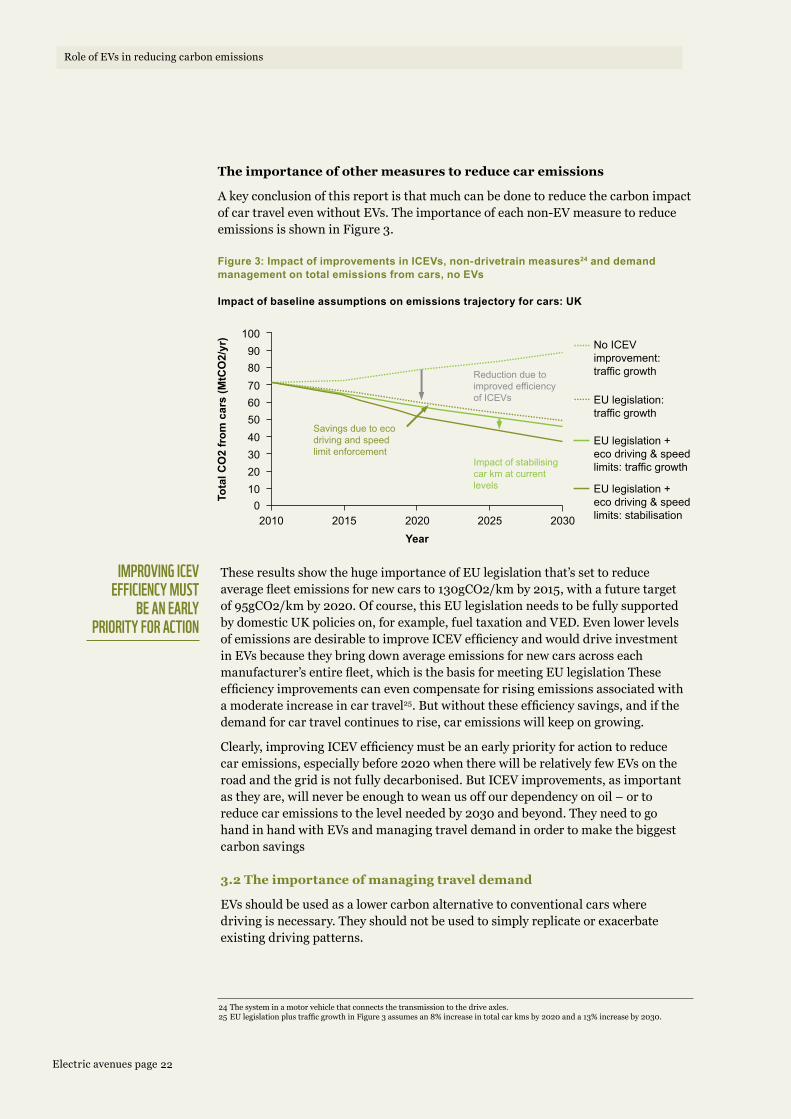

A key conclusion of this report is that much can be done to reduce the carbon impact ofcartravelevenwithoutEVs.Theimportanceofeachnon-EVmeasuretoreduceemissionsisshowninFigure3.

TheseresultsshowthehugeimportanceofEUlegislationthat’ssettoreduceaveragefleetemissionsfornewcarsto130gCO2/kmby2015,withafuturetargetof95gCO2/kmby2020.Ofcourse,thisEUlegislationneedstobefullysupportedbydomesticUKpolicieson,forexample,fueltaxationandVED.EvenlowerlevelsofemissionsaredesirabletoimproveICEVefficiencyandwoulddriveinvestmentin EVs because they bring down average emissions for new cars across each manufacturer’sentirefleet,whichisthebasisformeetingEUlegislationTheseefficiencyimprovementscanevencompensateforrisingemissionsassociatedwitha moderate increase in car travel25.Butwithouttheseefficiencysavings,andifthedemandforcartravelcontinuestorise,caremissionswillkeepongrowing.

Clearly,improvingICEVefficiencymustbeanearlypriorityforactiontoreducecaremissions,especiallybefore2020whentherewillberelativelyfewEVsontheroadandthegridisnotfullydecarbonised.ButICEVimprovements,asimportantastheyare,willneverbeenoughtoweanusoffourdependencyonoil–ortoreducecaremissionstothelevelneededby2030andbeyond.Theyneedtogohand in hand with EVs and managing travel demand in order to make the biggest carbon savings 3.2 The importance of managing travel demand

EVs should be used as a lower carbon alternative to conventional cars where drivingisnecessary.Theyshouldnotbeusedtosimplyreplicateorexacerbateexistingdrivingpatterns.

Impact of baseline assumptions on emissions trajectory for cars: UK

Figure 3: Impact of improvements in ICEVs, non-drivetrain measures24 and demand management on total emissions from cars, no EVs

24Thesysteminamotorvehiclethatconnectsthetransmissiontothedriveaxles.25EUlegislationplustrafficgrowthinFigure3assumesan8%increaseintotalcarkmsby2020anda13%increaseby2030.

improVing iCEV EffiCiEnCy mUSt

bE an EarLy priority for aCtion

2010 2015 2020 2025 20300

102030405060708090

100No ICEVimprovement:traffic growthReduction due to

improved efficiencyof ICEVs

Impact of stabilisingcar km at currentlevels

Savings due to ecodriving and speedlimit enforcement

EU legislation:traffic growth

EU legislation +eco driving & speedlimits: traffic growth

EU legislation +eco driving & speedlimits: stabilisation

Tota

l CO

2 fr

om c

ars

(MtC

O2/

yr)

Year

22Electric avenues page

Role of EVs in reducing carbon emissions

Electric avenues page 23

Role of EVs in reducing carbon emissions

Managing travel demand is especially important as EVs are cheaper to operate than conventionalcars,astheytendtohaverelativelylowoperatingcosts.26 There is thus apossible‘reboundeffect’–thatEVscouldbedrivenmorethanconventionalcars.An increase in total car kilometres as a result of EVs would not be either desirable or sustainable.ThisisbecausethemorethatEVsaredriven,themoreoftentheyneedcharging,whichproducesemissionsandincreasestotalenergydemand.Anincreasein EV driving could also generate pressure for new road building or discourage peoplefromusingpublictransport,whichwouldaddfurtherenvironmentalcosts.

Evenifwekeepcarkilometrespercapitastable,populationgrowthalonewilldriveuptotaldemand.TheUKpopulationisexpectedtogrowatabout0.7%perannum.27 Thereforeweneedareductioninpercapitacarkilometrestoachievestabilisation.

Demandreductionwillrequiresignificantchangesinconsumerbehaviourandareversalofhistoricaltrendstodecoupletrafficgrowthfromeconomicgrowth.Buttoreduce car kilometres still further will require a sustained effort and a strong set of governmentpolicymeasures.

Thegoodnewsisthatdemandreductionislessdifficulttoachievethanoftenassumed28:

• Sincethemid-1990s,therateofpassengertrafficgrowthintheUKhashalvedeventhougheconomicgrowthwas(untilrecently)50%higher–sotherehasalreadybeensomedecoupling.

• Baylissetal.(2008)29identifythatactualtrafficlevels(upto2006)havebeenwellbelowthemid-rangeforecastsprovidedbyboththe1989and1997NationalRoadTrafficForecasts.

• Theaverageannualtrafficgrowthratefrom2003-08wasonly0.1%.

• Totaldistancetravelledpercapitabyallmodeshaslevelledoffsince1999andtheshareofprivatetripsbycarisfalling.

• Recently,thenumberoftripsbycarhasstartedtofall.

• Althoughcarownershiphascontinuedtogrow,annualmileagepercarfellby10%duringthelastdecade.

As suggested in A low carbon transport policy for the UK30,suchmeasurescouldinclude:

• Additionalrailcapacity,reopeningofclosedlinesandlocallinesupport.

• IncreasingVEDforlessenergyefficientcars.

• Amoratoriumontheconstructionofmajorroads.

• Higherparkingcharges.

• Roadandcongestioncharging.

26AccordingtotheAA,aFordFocuscostsabout14ppermiletooperatecomparedto0.3ppermileforaNissanLeaf.27OfficeforNationalStatistics.28Source:DrJillianAnable,CentreforTransportResearch,UniversityofAberdeen29DavidBaylis,Travel demand and its causes,RoyalAutomobileClubFoundation,July2008.30KeithBuchan,MetropolitanTransportResearchUnit(MTRU),November2008;www.transportclimate.org.SeeTable1,p18for

proposedlowcarbontransportpolicies.

EVEn if wE KEEp Car KiLomEtrES pEr Capita

StabLE, popULation growth aLonE wiLL

DriVE Up totaL DEmanD. thErEforE

wE nEED a rEDUCtion in pEr Capita Car

KiLomEtrES to aChiEVE StabiLiSation.

• Governmentbackingforsmartertravelchoices31,includinggreateruseofpublictransport,carsharing,cyclingandwalking.

• Limitsonparkinginnewdevelopmentsandworkplaces.

• Planningofnewdevelopmentsclosertopublictransportlinks.

The UK Energy Research Centre (UKERC) stresses the importance of a future ‘lifecyclescenario’inreducingemissionsfromtransport32,wherecarbonemissionsreductionisnotdeliveredmerelythroughpublicpolicy,priceandtechnicalchange,butalsothroughsociallyledchange–i.e.throughindividualsandcommunitieschoosingtoliveinawaythathaslowerenvironmentalimpact.Accordingtothisviewofthefuture,sharedcarownershipwouldbeencouraged,whichiscorrelatedwithlowercaruse.Therewouldalsobeanincreaseinactivetravel,withmorewalkingandcycling,asaconsequenceofmorepeopleworking,shoppingandrelaxingclosertohome.Teleworkingandvideoconferencingwouldbeusedmoreoftentoreplacelongdistancecommutingorbusinesstravel.

Reducingtraveldemandthroughfewercarkilometreswouldalsomeanwedon’tneed as many EVs on the road to achieve the same result in terms of carbon savings.Demandreductionisalsocheaperanddoesn’trequiretheinvestmentininfrastructurenecessaryforEVs.

The impact of reducing car kilometres

Totestthedifferencethatreducingtraveldemandcouldmaketocarbonsavings,Element Energy ran a sensitivity analysis to see what would happen to car emissions in our three baseline scenarios if:

1) car kilometres were reduced by 16% by 2020 and stayed the same in 2030; or

2)carkilometreswerereducedby23%by2020and37%by2030,relativeto 2010levels.

We found that a reduction in demand at lower levels of EV uptake makes the greatestimpactonreducingcaremission,inpercentageterms.Forexample,intheBAUscenariowithlowlevelsofEVs(160,000by2020and1.7millionby2030),amoderatelevelofdemandreductionasper1)reducescaremissionsfrom16to36%by2020andfrom33to55%by2030.ButintheExtendedscenariowithmediumlevelsofEVs(1.7millionby2020and6.4millionby2030),amoderatelevelofdemandreductionwouldreducecaremissionsfrom29to40%by2020andfrom53to61%by2030.

More ambitious demand reduction in the BAU scenario as per 2) above would reducecaremissionsfrom16to41%by2020andfrom33to66%by2030.Greaterdemand reduction in the Extended scenario would reduce car emissions from 29to45%by2020andfrom53to71%by2030.Thishigherlevelofdemandreduction would allow us to meet the emission milestones consistent with a 42%reductiontrajectorywithoutanyEVsatall(assumingthatICEVefficiencyimprovementsarerealisedinlinewithEUlegislation).Only4%fewercarkilometresareneededfrom2010levelstoensurethat1.7millionEVsby2020,aspertheCCC’srecommendationtoachievea34%reductioninemissions,wouldalsobeenoughtohitthe42%target.

Forfurtherinformationaboutthissensitivityanalysis,pleaseseeSection8.6.2inElementEnergy’sresearchreport.

31 FormoreinformationabouttheDfT’ssupportforSmarterChoicesregardingtravel, seehttp://www.dft.gov.uk/pgr/sustainable/smarterchoices/

32UKERC,Making the transition to a secure and low-carbon energy system,Chapter6.

wE foUnD that a rEDUCtion in DEmanD

at LowEr LEVELS of EV UptaKE maKES thE

grEatESt impaCt on rEDUCing Car EmiSSion,

in pErCEntagE tErmS

24Electric avenues page

Role of EVs in reducing carbon emissions

Electric avenues page 25

Role of EVs in reducing carbon emissions

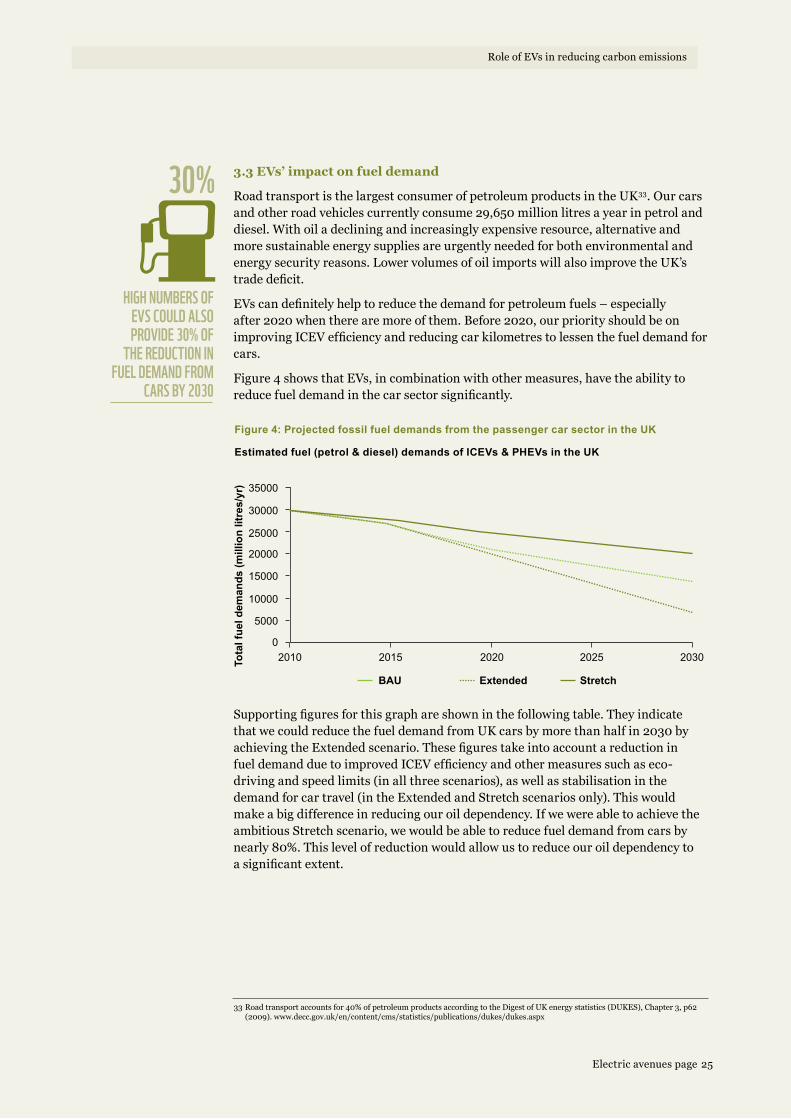

3.3 EVs’ impact on fuel demand

Road transport is the largest consumer of petroleum products in the UK33.Ourcarsandotherroadvehiclescurrentlyconsume29,650millionlitresayearinpetrolanddiesel.Withoiladecliningandincreasinglyexpensiveresource,alternativeandmore sustainable energy supplies are urgently needed for both environmental and energysecurityreasons.LowervolumesofoilimportswillalsoimprovetheUK’stradedeficit.

EVscandefinitelyhelptoreducethedemandforpetroleumfuels–especiallyafter2020whentherearemoreofthem.Before2020,ourpriorityshouldbeonimprovingICEVefficiencyandreducingcarkilometrestolessenthefueldemandforcars.

Figure4showsthatEVs,incombinationwithothermeasures,havetheabilitytoreducefueldemandinthecarsectorsignificantly.

Supportingfiguresforthisgraphareshowninthefollowingtable.Theyindicatethat we could reduce the fuel demand from UK cars by more than half in 2030 by achievingtheExtendedscenario.Thesefigurestakeintoaccountareductionin fueldemandduetoimprovedICEVefficiencyandothermeasuressuchaseco-drivingandspeedlimits(inallthreescenarios),aswellasstabilisationinthedemandforcartravel(intheExtendedandStretchscenariosonly).Thiswouldmakeabigdifferenceinreducingouroildependency.IfwewereabletoachievetheambitiousStretchscenario,wewouldbeabletoreducefueldemandfromcarsbynearly80%.Thislevelofreductionwouldallowustoreduceouroildependencyto asignificantextent.

Estimated fuel (petrol & diesel) demands of ICEVs & PHEVs in the UK

Figure 4: Projected fossil fuel demands from the passenger car sector in the UK

2010 2015 2020 2025 20300

5000

10000

15000

20000

25000

30000

35000

Tota

l fue

l dem

ands

(mill

ion

litre

s/yr

)

BAU Extended Stretch

33Roadtransportaccountsfor40%ofpetroleumproductsaccordingtotheDigestofUKenergystatistics(DUKES),Chapter3,p62(2009).www.decc.gov.uk/en/content/cms/statistics/publications/dukes/dukes.aspx

high nUmbErS of EVS CoULD aLSo proViDE 30% of

thE rEDUCtion in fUEL DEmanD from

CarS by 2030

30%

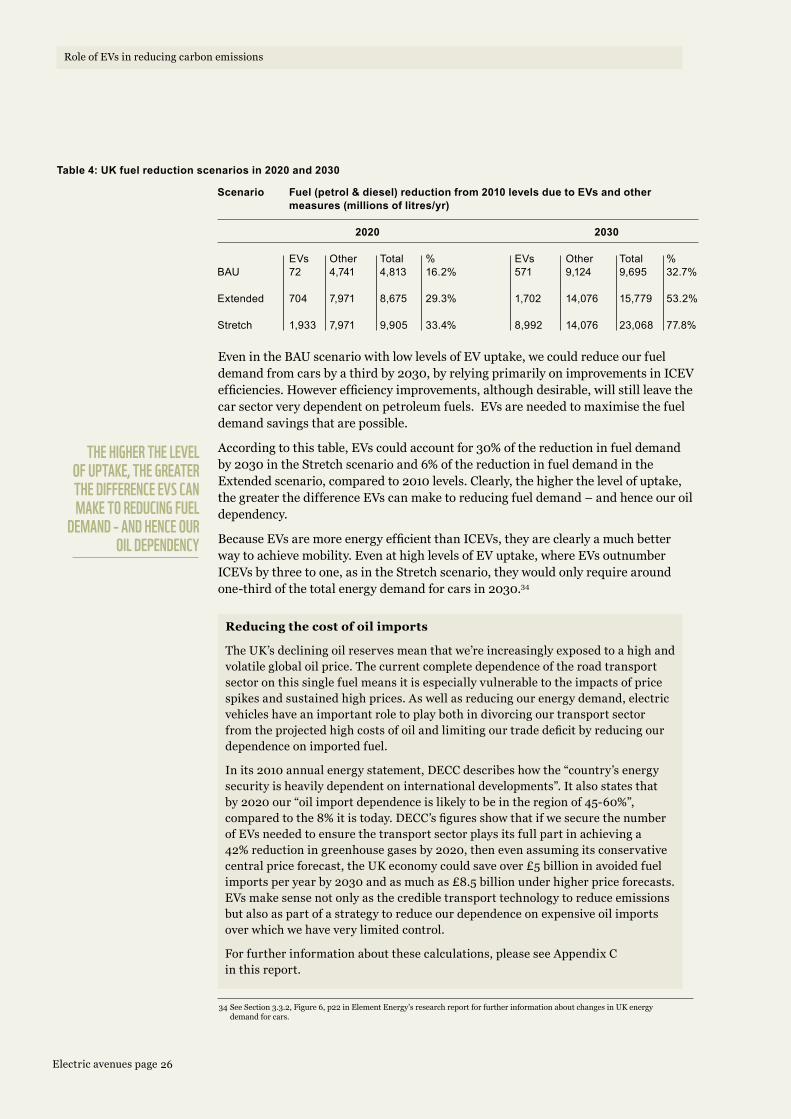

EvenintheBAUscenariowithlowlevelsofEVuptake,wecouldreduceourfueldemandfromcarsbyathirdby2030,byrelyingprimarilyonimprovementsinICEVefficiencies.Howeverefficiencyimprovements,althoughdesirable,willstillleavethecarsectorverydependentonpetroleumfuels.EVsareneededtomaximisethefueldemandsavingsthatarepossible.

Accordingtothistable,EVscouldaccountfor30%ofthereductioninfueldemandby 2030 in the Stretch scenario and 6% of the reduction in fuel demand in the Extendedscenario,comparedto2010levels.Clearly,thehigherthelevelofuptake,the greater the difference EVs can make to reducing fuel demand – and hence our oil dependency.

BecauseEVsaremoreenergyefficientthanICEVs,theyareclearlyamuchbetterwaytoachievemobility.EvenathighlevelsofEVuptake,whereEVsoutnumberICEVsbythreetoone,asintheStretchscenario,theywouldonlyrequirearoundone-thirdofthetotalenergydemandforcarsin2030.34

Table 4: UK fuel reduction scenarios in 2020 and 2030

Scenario

BaU

extended

Stretch

Fuel (petrol & diesel) reduction from 2010 levels due to EVs and other measures (millions of litres/yr)

2020 2030

eVs72

704

1,933

other4,741

7,971

7,971

total4,813

8,675

9,905

%16.2%

29.3%

33.4%

eVs571

1,702

8,992

other9,124

14,076

14,076

total9,695

15,779

23,068

%32.7%

53.2%

77.8%

Reducing the cost of oil imports

TheUK’sdecliningoilreservesmeanthatwe’reincreasinglyexposedtoahighandvolatileglobaloilprice.Thecurrentcompletedependenceoftheroadtransportsector on this single fuel means it is especially vulnerable to the impacts of price spikesandsustainedhighprices.Aswellasreducingourenergydemand,electricvehicles have an important role to play both in divorcing our transport sector fromtheprojectedhighcostsofoilandlimitingourtradedeficitbyreducingourdependenceonimportedfuel.

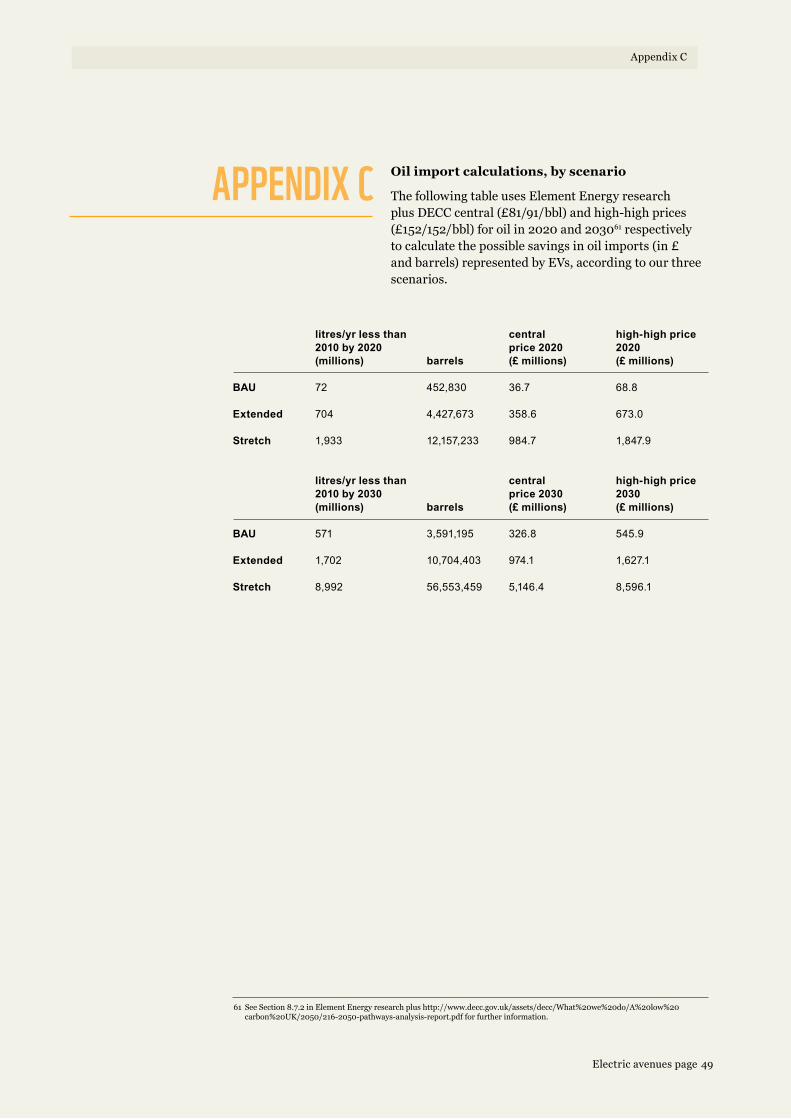

Inits2010annualenergystatement,DECCdescribeshowthe“country’senergysecurityisheavilydependentoninternationaldevelopments”.Italsostatesthatby2020our“oilimportdependenceislikelytobeintheregionof45-60%”,comparedtothe8%itistoday.DECC’sfiguresshowthatifwesecurethenumberof EVs needed to ensure the transport sector plays its full part in achieving a 42%reductioningreenhousegasesby2020,thenevenassumingitsconservativecentralpriceforecast,theUKeconomycouldsaveover£5billioninavoidedfuelimportsperyearby2030andasmuchas£8.5billionunderhigherpriceforecasts.EVs make sense not only as the credible transport technology to reduce emissions but also as part of a strategy to reduce our dependence on expensive oil imports overwhichwehaveverylimitedcontrol.

Forfurtherinformationaboutthesecalculations,pleaseseeAppendixC inthisreport.

34SeeSection3.3.2,Figure6,p22inElementEnergy’sresearchreportforfurtherinformationaboutchangesinUKenergy demandforcars.

thE highEr thE LEVEL of UptaKE, thE grEatEr thE DiffErEnCE EVS Can maKE to rEDUCing fUEL

DEmanD – anD hEnCE oUr oiL DEpEnDEnCy

26Electric avenues page

Role of EVs in reducing carbon emissions

EVs make sense not only as the credible transport technology to reduce emissions but also as part of a strategy to reduceourdependenceonexpensiveoilimportsoverwhichwehaveverylimitedcontrol.

© S

co

tt D

ick

er

So

N / W

WF-U

S

4. thE impaCt of EVS on thE griD

EVs can play an important role in helpingtobalancethegrid,which will encourage a greater use of renewables.TheimpactofEVson thegridisgenerallylessthanfeared,

but delayed charging will be important to spread peak demandfromEVs.

4.1 Charging EVs

The most important locations for charging EVs will be at homes and workplaces since thesearewhereEVsarelikelytobeparkedforthelongestperiodsoftime,asindicatedby the National Travel Survey (NTS)35.MostownersarelikelytowanttochargetheirEVsovernightusingachargingpointathome,perhapsnexttotheirproperty.

WWF’sresearchhasfoundthat,whileoff-streetchargepointsarelikelytobethe normforthenexttwodecades,on-streetchargepointswillincreasinglybeneededifEVsbecomethedominantvehicletypeinthepassengercarmarket.

Public charge points should be considered a lower priority than home or workplace chargingastheyarelikelytobeusedlessoftenandcostmoretoinstall,especiallyiftheyarefastcharging.ButtheydohaveavalueinhelpingtoincreasethepublicprofileofEVs,encouragetheiruse,andextendtheirrange.GoodlocationsforpublicchargepointswouldincludespecialEVparkingandchargingareaswithincongestionzones,orEVparkingspaceswithchargepointsclosetoshopentrances.

Ascarsarealsoparkedforlongerathomeoratwork,thissuggeststhatslowchargepointscouldbesufficientforchargingEVsintheirprimarylocations.However,fastercharging points are more likely to be needed in public locations so that EV drivers can rechargequicklywhentheyareoutandabout. 4.2 Grid impacts

BecauseEVswillbechargedfromthenationalgrid,theirimpactonthegridmustconsider:

• AdditionalannualelectricitydemandsfromEVs.

• TheimpactofEVsonpeakelectricitydemand.

The impacts that EVs will have on the grid have to be understood at both a national andlocallevel.Simultaneousdemandsonthegridcanaddtopeakloads,andgenerationcapacitymustbeplannedaccordingly.Butlocalisedpeaksindemandforpoweralsohaveanimpactonlocaldistributionsystemsandtransformers,whicharesmallerscaleandlowerspecificationthannationalleveltransmissionsystemsandthereforelessabletohandlesurgesindemand.

Any extra demands that EVs place on the grid must also be compatible with greaterelectrificationofothersectors,suchasheatpumpsfordomestichousingandrailelectrification–whicharealsoincreasinglyrelyingontheirenergyfromadecarbonisedelectricitygrid.

35 AccordingtotheNTS,acontinuoussurveyfortheDfT,vehiclesspend61%oftimeparkedathome,35%atworkand4%inotherplaces.Forfurtherinformation,see:www.dft.gov.uk/pgr/statistics/datatablespublications/personal/mtehodlolgoy/ntstechreports/

28Electric avenues page

The impact of EVs on the grid

Electric avenues page 29

The impact of EVs on the grid

Additional loads from EVs

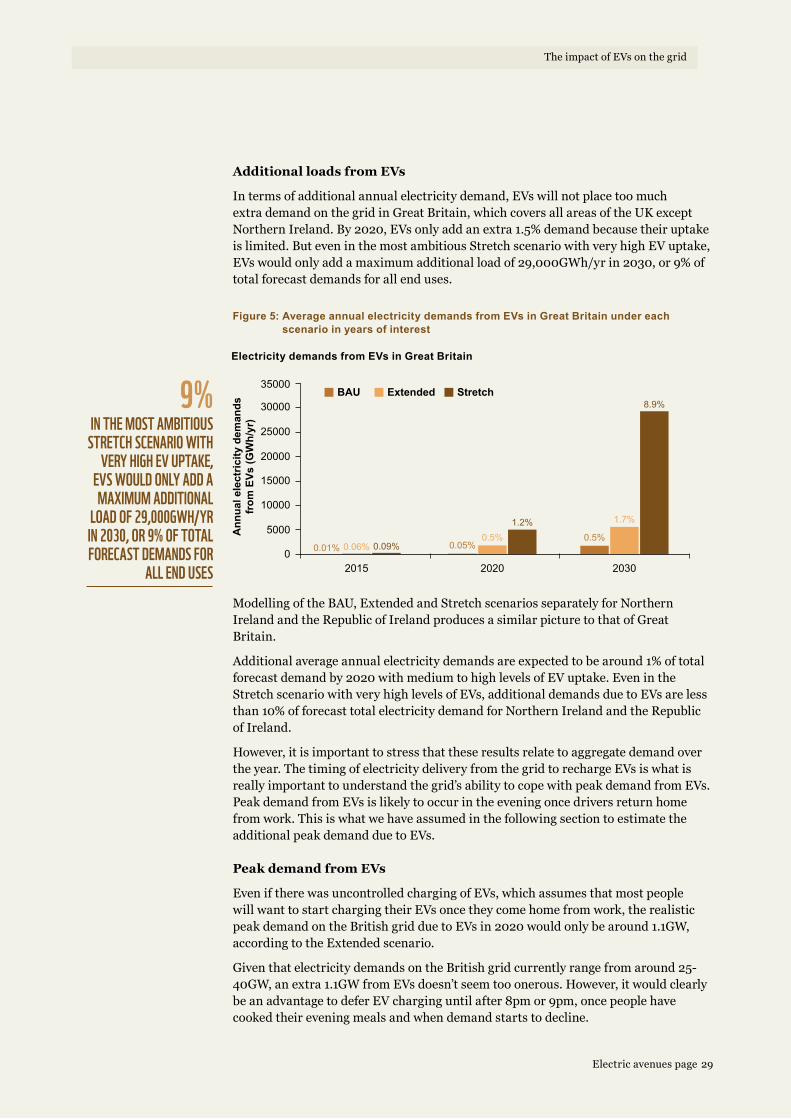

Intermsofadditionalannualelectricitydemand,EVswillnotplacetoomuchextrademandonthegridinGreatBritain,whichcoversallareasoftheUKexceptNorthernIreland.By2020,EVsonlyaddanextra1.5%demandbecausetheiruptakeislimited.ButeveninthemostambitiousStretchscenariowithveryhighEVuptake,EVswouldonlyaddamaximumadditionalloadof29,000GWh/yrin2030,or9%oftotalforecastdemandsforallenduses.

ModellingoftheBAU,ExtendedandStretchscenariosseparatelyforNorthernIreland and the Republic of Ireland produces a similar picture to that of Great Britain.

Additional average annual electricity demands are expected to be around 1% of total forecastdemandby2020withmediumtohighlevelsofEVuptake.EvenintheStretchscenariowithveryhighlevelsofEVs,additionaldemandsduetoEVsarelessthan 10% of forecast total electricity demand for Northern Ireland and the Republic ofIreland.

However,itisimportanttostressthattheseresultsrelatetoaggregatedemandovertheyear.ThetimingofelectricitydeliveryfromthegridtorechargeEVsiswhatisreallyimportanttounderstandthegrid’sabilitytocopewithpeakdemandfromEVs.Peak demand from EVs is likely to occur in the evening once drivers return home fromwork.ThisiswhatwehaveassumedinthefollowingsectiontoestimatetheadditionalpeakdemandduetoEVs. Peak demand from EVs

EveniftherewasuncontrolledchargingofEVs,whichassumesthatmostpeoplewillwanttostartchargingtheirEVsoncetheycomehomefromwork,therealisticpeakdemandontheBritishgridduetoEVsin2020wouldonlybearound1.1GW,accordingtotheExtendedscenario.

GiventhatelectricitydemandsontheBritishgridcurrentlyrangefromaround25-40GW,anextra1.1GWfromEVsdoesn’tseemtooonerous.However,itwouldclearlybeanadvantagetodeferEVcharginguntilafter8pmor9pm,oncepeoplehavecookedtheireveningmealsandwhendemandstartstodecline.

Electricity demands from EVs in Great Britain

Figure 5: Average annual electricity demands from EVs in Great Britain under each scenario in years of interest

0.5%

1.7%

8.9%

0.05%0.5%

1.2%

0.01% 0.06% 0.09%

2015 2020 20300

5000

10000

15000

20000

25000

30000

35000

Ann

ual e

lect

ricity

dem

ands

from

EVs

(GW

h/yr

)

BAU Extended Stretch

in thE moSt ambitioUS StrEtCh SCEnario with

VEry high EV UptaKE, EVS woULD onLy aDD a maximUm aDDitionaL

LoaD of 29,000gwh/yr in 2030, or 9% of totaL forECaSt DEmanDS for

aLL EnD USES

9%

Estimated peak demands on British grid in 2030 due to EVs under the Stretch scenario

Figure 6: Peak demands on the electricity grid in Great Britain with 25.5 million EVs in stock (Stretch scenario in 2030) based on average charging rate of 3kW per EV

The use of charge delay devices would help to smooth out the spikes of peak demand bypushingbackthetimewhenEVsarecharged,ideallytolateatnightwhendemandsonthegridarelow.Inconcept,theyarenotdissimilartousingstorageheaters,asbothconsumeandstorecheaperelectricityfordelayeduse.

EvenundertheStretchscenarioin2030,whereEVsmakeup75%ofallUKcars,arealisticworstcasepeakdemandduetoEVsisstillbelow10GW,whichiswithintherange of National Grid forecasts of load growth36.TheworstcasescenariorepresentsallEVsdemandingpoweratthesametime.ButthisisneverlikelytohappenasnotallEVsaredriveneachdayandtherearedifferentarrivaltimeshome.ChargedelaydevicescanalsohelptoreducepeakdemandduetoEVs,asshowninFigure637.

Widespread use of charge delay devices would also reduce potential strain on local distributionnetworksandtransformers,whicharelessabletocopewithpeaksindemandthanthenationalgrid,giventheirlowervoltageandthermalrating.38

Smartelectricitygridsthatincludeintelligentmonitoring,controlandcommunications technologies could also help to minimise the impact that EVs have onthegridbyhelpingtodetermineoptimumchargingtimes,atthelowestcarbonintensity.Theuseofsmartgridscould,forexample,shiftEVchargingtothemiddleofthenight,whentheoveralldemandforenergyislowerandthereforerenewableenergy sources are more likely to provide most of the electricity needed to charge EVs,atalowergridCO2intensity.Bycontrast,chargingEVsattimesofpeakdemandismorelikelytoinvolvehighcarbon‘peakingplant’(generatorsthatcomeonlineforshortperiodstomeetsurgesinelectricitydemand,whichareusuallypoweredbycoalorgas).ThiswouldreducethepotentialCO2savingsofEVs.

76.5

54.6

12.39.3

Worst case(theoretical only)

Adjusted for carsthat require charge

Theoretical worst case = all EVs demand power simultaneously

Reduction due to proportion of EVsnot driven on any particular day

Impact of diversity(spread time of arrival home)

Impact of simplecharge delay

Adjusted forarrival time

With loadshifting

0

10

20

30

40

50

60

70

80

90

Peak

dem

ands

due

to E

Vs (G

W)

36BasedonforwardextrapolationofmediumtermprojectionsfromtheNationalGrid.SeeSection5.3.4inElementEnergy’sresearchreportforfurtherinformation.

37 ForfurtherinformationabouthowtherealisticworstcasepeakdemandduetoEVswasderived,seeSection5.3.4inElementEnergy’sresearchreport.

38InStrategies for the uptake of electric vehicles and associated infrastructure implications,preparedbyElementEnergyfortheCCC(2009),itwasestimatedthatlocaldistributionnetworkscouldaccommodatereasonablelevelsofEVuptake(uptoathirdofhouseholdsowningEVs).Upgradingthelocaldistributionsystemsatthesametimeasthenationalgridtomaximisesynergieswouldalsohelptoreducelocalimpacts.

EVS Can pLay an important roLE in

hELping to baLanCE thE griD, whiCh wiLL

EnCoUragE a grEatEr USE of rEnEwabLES

30Electric avenues page

The impact of EVs on the grid

Electric avenues page 31

The impact of EVs on the grid

Althoughsmartgridsarenotlikelytobewidespreadintheshortterm,neitherareEVs.Thisgivestimeforfurtherinvestmentandresearch,whichneedstohappennowifsmartgridsaretobeinusebythetimetherearemillionsofEVs.

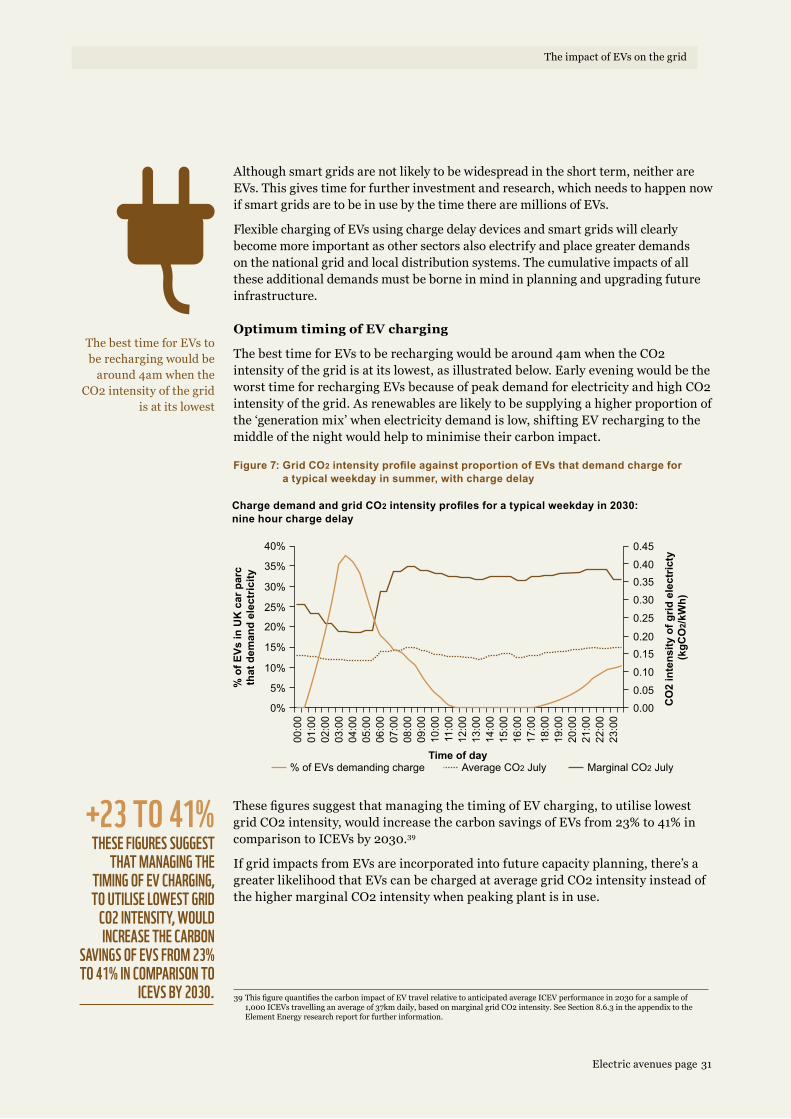

Flexible charging of EVs using charge delay devices and smart grids will clearly become more important as other sectors also electrify and place greater demands onthenationalgridandlocaldistributionsystems.Thecumulativeimpactsofallthese additional demands must be borne in mind in planning and upgrading future infrastructure. Optimum timing of EV charging

ThebesttimeforEVstoberechargingwouldbearound4amwhentheCO2intensityofthegridisatitslowest,asillustratedbelow.Earlyeveningwouldbetheworst time for recharging EVs because of peak demand for electricity and high CO2 intensityofthegrid.Asrenewablesarelikelytobesupplyingahigherproportionofthe‘generationmix’whenelectricitydemandislow,shiftingEVrechargingtothemiddleofthenightwouldhelptominimisetheircarbonimpact.

ThesefiguressuggestthatmanagingthetimingofEVcharging,toutiliselowestgridCO2intensity,wouldincreasethecarbonsavingsofEVsfrom23%to41%incomparisontoICEVsby2030.39

IfgridimpactsfromEVsareincorporatedintofuturecapacityplanning,there’sagreater likelihood that EVs can be charged at average grid CO2 intensity instead of thehighermarginalCO2intensitywhenpeakingplantisinuse.

Charge demand and grid CO2 intensity profiles for a typical weekday in 2030: nine hour charge delay

Figure 7: Grid CO2 intensity profile against proportion of EVs that demand charge for a typical weekday in summer, with charge delay

39ThisfigurequantifiesthecarbonimpactofEVtravelrelativetoanticipatedaverageICEVperformancein2030forasampleof1,000ICEVstravellinganaverageof37kmdaily,basedonmarginalgridCO2intensity.SeeSection8.6.3intheappendixtotheElementEnergyresearchreportforfurtherinformation.

The best time for EVs to be recharging would be around4amwhenthe

CO2 intensity of the grid is at its lowest

thESE figUrES SUggESt that managing thE

timing of EV Charging, to UtiLiSE LowESt griD

Co2 intEnSity, woULD inCrEaSE thE Carbon

SaVingS of EVS from 23% to 41% in CompariSon to

iCEVS by 2030.

+23 to 41%

0% 0.00

0.05

0.10

0.150.20

0.25

0.30

0.350.40

0.45

5%

10%

15%

20%

25%

30%

35%

00:0

001

:00

02:0

003

:00

04:0

005

:00

06:0

007

:00

08:0

009

:00

10:0

011

:00

12:0

013

:00

14:0

015

:00

16:0

017

:00

18:0

019

:00

20:0

021

:00

22:0

023

:00

40%

% o

f EVs

in U

K c

ar p

arc

that

dem

and

elec

tric

ity

CO

2 in

tens

ity o

f grid

ele

ctric

ty

(kgC

O2/

kWh)

Time of day% of EVs demanding charge Average CO2 July Marginal CO2 July

Storage potential of EVs

Infuture,highlevelsofEVscouldpotentiallystoreelectricitywhendemandislowandthenfeeditbacktothegridwhendemandishigh.However,furtherresearchisneededtoimprovebothbatteryandsmartgridtechnologies.Significantinvestmentwillthereforeberequiredifthispotentialistoberealised.

Driveracceptabilityisalsoanissue,assomeindividualswillwanttohaveaccesstotheirEVsatalltimes.Smartchargingtariffsthatrewarddriverswhoareprepared to surrender some of their battery capacity would help to encourage the storagepotentialofEVs.

ThetotalstoragecapacityofEVs,accordingtotheExtendedscenario,isequivalenttoaround30minutesoftheaveragenationalelectricitydemandby2020.InGreatBritain,themaximumstoragecapacityofEVsinthe2030Stretchscenariowouldbe417GWh,basedon90%ofEVsbeingparkedandpluggedintothegridatanyone time40.Thisisequivalentto46timestheUK’slargestpumpedhydrostoragefacility.

InNorthernIrelandandtheRepublicofIreland,themaximumstoragecapacityofEVsintheStretchscenariowouldbe41GWh,basedon90%ofEVsbeingparkedandpluggedintothegridatanyonetime.Thisisequivalentto26timestheenergyavailablefromtheRepublicofIreland’sonlypumpedhydrostoragefacilityatTurloughHill. Grid balancing and vehicle to grid (V2G) applications

Gridbalancingreferstomatchingtheamountofelectricitythat’sgeneratedatanypointintimewiththesimultaneousdemandforpowerfromthegrid.Vehicletogrid(orV2G)isaconceptthat’sstillinitsinfancy.Itinvolvesprovidingpowerto the grid from the batteries of grid-connected EVs at times of high overall electricitydemand,whenthepriceofelectricityisalsohigh.Thebatteriescanthenbechargedduringperiodsoflowerdemand,suchaslateatnightwhenelectricityshouldbecheaper.

Using V2G could potentially reduce the need for high carbon peaking plant byfeedingbackpowertothegridattimesofpeakdemand.Butfasterbatterychargingwillbeneeded,aswellassmartgridstohelpshiftdemandwhenEVsarebetterabletohelpbalancethegrid.Thesetechnologiesarenotlikelytobeavailableforsometime.

AnothersignificantbarriertoV2GisthecostofEVbatteries.Thiswilldeterminethe point at which it makes economic sense to provide electricity back to the grid fromEVs,especiallyasfeedingpowerbacktothegridreducesbatterylife.Ourresearchsuggeststhat,atcurrentbatterycosts,V2Gbecomesviableataround£500/MWh.IfEVbatterycostscomedown,V2Gwouldbecomeviableat£320/MWh.Butcomparisonswithpublishedforecastpricedurationcurvesfor2020suggest that the electricity price may only exceed this level for less than 1% of thetime.Clearly,EVbatterycostswillhavetofalllowerstillforV2Gtohavesignificantpotential.41 Consideration will also need to be given as to how best to structureconsumers’electricitybillingarrangementsiftheirEVsareabletofeedelectricitybacktothegrid. 40NationalTravelSurveyfiguressuggestthatatanyparticulartimeduringthedayornightthere’sahighchancethatatleast90%

ofcarsareparked.41 IfEVbatterycostsgetlowerstill,asisthetargetoftheUSAdvancedBatteryConsortium,V2Gwouldbeviableatanelectricity

priceof£170/MWh.

in fUtUrE, high LEVELS of EVS CoULD potEntiaLLy

StorE ELECtriCity whEn DEmanD iS Low anD thEn fEED it baCK to thE griD

whEn DEmanD iS high

32Electric avenues page

The impact of EVs on the grid

Electric avenues page 33

The impact of EVs on the grid

EVs and renewables

DecarbonisationofthegridisaprerequisiteifEVsaretoachievetheirmaximumcarbonsavingspotential.AthighlevelsofEVuptake,decarbonisationofthegridreducescaremissionsbyapproximately70%morethanifthegridispoweredbyfossilfuelsasitiscurrently.42

EVsarethereforehighlycompatiblewithgreateruseofrenewables.EVscanhelpto‘fillinthetroughs’ofelectricitydemand,byusingrenewablepowerwhenitmightotherwisenotbeused,Theycanalso‘shaveoffpeaks’bystoringexcessgenerationcapacityofrenewables.Infuture,EVsmaybeabletosupplypowerbacktothegridthroughV2Gatpeaktimesofdemand.

AsignificantincreaseinelectricityfromrenewablesisrequirediftheUKistomeetthegovernment’s15%renewableenergytargetby2020.Thiswillincludealargeincreaseinwindcapacityonthegrid.There’saneedformuchgreaterinvestmentinwindandothertypesofrenewableenergy,intheUKandtherestofEurope,ifwearetoachievea100%renewablesfutureby2050.Thispointwasfurthersupportedin a recent report from the European Climate Foundation (ECF)43.

Thevariabilityofwindpowerisoftencitedasacriticism.ButaccordingtotheECFreport,whichshowsthatafutureEuropeanenergysystembasedon100%renewable energy is technically feasible and at costs that are not substantially higher than other ways of decarbonising the power sector44,thebestwaytomanagethe variability of some forms of renewable energy power is by investing in new interconnection infrastructure and management systems between the different Europeangrids.

42SeeAppendixBtothisreportforasensitivityanalysisofcarCO2emissionsbylevelofcarbonintensityofthegrid.43ECF,Roadmap 2050: a practical guide to a prosperous, low-carbon Europe,2010.44Thesamereportfoundthatnuclearenergyandfossilfuelpowerstationswithcarboncaptureandstoragetechnologywerenot

essentialtodecarbonisethepowersectorwhileprotectingsystemreliability.

DECarboniSation of thE griD iS a prErEqUiSitE if EVS arE to aChiEVE

thEir maximUm Carbon SaVingS potEntiaL.

EVsarehighlycompatiblewithgreateruseofrenewables.EVscanhelpto‘fillinthetroughs’ofelectricitydemand,byusingusingrenewableenergywhenitmightnototherwisebeused.Theycanalso‘shaveoffthepeaks’bystoringexcessgenerationcapacity.Infuture,EVsmaybeabletosupplypowerbacktothegridthroughvehicletogrid(V2G)applicationsatpeaktimesofdemand.

©ADAMOSW

ELL/W

WF-C

ANON

5. ChaLLEngES anD opportUnitiES

Price,rangeandinfrastructurearethebiggest barriers to EVs being accepted byconsumers.Changestodriverattitudes will also be required for EVs to gain acceptance and to encourage

lessdriving.Governmentpolicyinterventionwillbeneeded to overcome these issues and help UK companies makethemostofEVmarketopportunities.

5.1 Challenges

TheintroductionofEVs,attheraterequiredbythetargetsundertheClimateChangeAct,willbeasignificantchallengeinitself,giventheverylowlevelsofEVsthatexistatpresent,asdiscussedinSection1.4.TomovefromthousandstomillionsofEVsinfuturewillclearlybeanenormoustask,requiringsubstantialinvestmentandgovernmentsupport.

Themainbarrierstotheeffectiveroll-outofEVsarediscussedbelow. Price

The most obvious and immediate barrier to the rapid take-up of EVs is their significantpricepremiumcomparedtoconventionalvehicles.45 According to FinancialTimesresearch,76%ofUKconsumerssaythattheywouldnotpaymoreforanEV.46

Muchofthispricedifferenceisassociatedwiththehighcostoflithiumbatteries.Asdemandincreasesandbatterytechnologyimproves,EVpriceswilldecline.Butinordertokick-startthemarket,asignificantlevelofsubsidywillberequired.TheCCChasindicatedthatthiscouldbeintheregionof£10,000pervehicleandmayneedtobeashighas£20,000.47

Althoughcapitalgrantsofupto£5,000pervehiclearebeingofferedbythegovernmentfrom2011to2012,worthupto£43million,thisfallswellshortofthe£230millionpromisedbythepreviousgovernment.Webelievethatadditionalfundingwillbeneeded,wellbeyond2012,ifEVsaretogainmarketshare.Asmostconsumers are unlikely to purchase EVs until the charging infrastructure is well establishedandtheeconomyimproves,it’sveryimportantthatthesesubsidiescontinueforsometime.