Connecticut Avenue Securities Investor Presentation · 2016 (our “2016 Form 10-K”), and Form...

79

© 2017 Fannie Mae. Trademarks of Fannie Mae. 1 December 2017 Connecticut Avenue Securities Program TM

Transcript of Connecticut Avenue Securities Investor Presentation · 2016 (our “2016 Form 10-K”), and Form...

© 2017 Fannie Mae. Trademarks of Fannie Mae. 1

December 2017

Connecticut Avenue Securities Program

TM

© 2017 Fannie Mae. Trademarks of Fannie Mae. 2

This presentation contains a number of estimates, forecasts, expectations,

beliefs, and other forward-looking statements, including statements regarding

economic and housing market conditions, Fannie Mae’s future dividend

payments to Treasury, and future issuances and the projected performance of

Connecticut Avenue SecuritiesTM. These estimates, forecasts, expectations,

beliefs and other forward-looking statements are based on the company’s

current assumptions regarding numerous factors and are subject to change.

Actual outcomes may differ materially from those reflected in these forward-

looking statements due to a variety of factors, including, but not limited to, those

described in “Executive Summary,” “Forward-Looking Statements” and “Risk

Factors” in our annual report on Form 10-K for the year ended December 31,

2016 (our “2016 Form 10-K”), and Form 10-Q for the quarter ended November

30, 2017.

Any forward-looking statements made by Fannie Mae speak only as of the date

on which they were made. Fannie Mae is under no obligation to, and expressly

disclaims any obligation to, update or alter its forward-looking statements,

whether as a result of new information, subsequent events, or otherwise.

Disclaimer

© 2017 Fannie Mae. Trademarks of Fannie Mae. 31/31/2018Connecticut Avenue Securities Investor Presentation

Fannie Mae’s business model 4

Credit risk management 10

CAS key features and deal highlights 16

Connecticut Avenue Securities deal structure overview 20

Historical loan performance 33

Investor distribution and security performance 48

Investor resources 54

Appendix 60

A. How mortgage insurance works-High LTV deals

B. CAS deal summaries and comparisons

C. Credit risk management

D. Additional resources 78

Contents

© 2017 Fannie Mae. Trademarks of Fannie Mae. 4

Fannie Mae’s business model

© 2017 Fannie Mae. Trademarks of Fannie Mae. 51/31/2018

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

Fir

st L

ien

Mo

rtg

ag

es

Ou

tsta

nd

ing

(B

illi

on

s)

Our size and scale

As of June 2017, U.S. 1st Lien mortgage debt outstanding totaled $9.8 trillion. Fannie Mae’s share stood at over $2.8 trillion, approximately 30% of the market.

The U.S. mortgage market is dominated by the 30-year Fixed-Rate Mortgage (FRM).

*Based on Fannie Mae, Freddie Mac and Ginnie Mae securitization data through Q3 2017. Data includes ARM and FRM.

Fannie Mae was the largest issuer of single-family mortgage securities year to date.*

Fannie Mae’s book of business is geographically dispersed across the United States

*Source: Federal Reserve’s Flow of Funds

Fannie Mae Total MDO

*Source: Fannie Mae Q3 2017 Credit Supplement

20%

64%

Other

California

Texas

6%

Florida

6%

New York

5%Third Quarter 2017 Issuance* by Institution

0

200

400

600

800

3Q2017 2016 2015 2014 2013

In B

illio

ns

Fannie Mae Issuance by Product Type

30-year FRM 15-year FRM 20-year FRM 10-year FRM Other Fixed ARM

© 2017 Fannie Mae. Trademarks of Fannie Mae. 6

LenderOriginates loans

Fannie MaeGuarantees MBS backed by loans

Interest RateInvestor

Purchases MBSMBS

Delivers loansServices loans

Pays guaranty fee

Securitizes loansGuarantees principal

& interest on MBS

Sold to investor

Proceeds from sale of MBS flow back to lender

Credit-Linked Debt

Credit InvestorAssumes portion of credit risk

Funding loans through issuance of Fannie Mae MBS

When Fannie Mae issues fully guaranteed single-family MBS, we retain all of the credit (mortgage default) risk associated with losses on the underlying mortgage loans. In return for taking on that risk, we receive a guaranty fee paid from a portion of the loans’ interest payments, which is passed through to us by the lender that delivered the loan to us. When we issue credit risk transfer securities, we transfer some of the retained credit risk to private market investors. However, thepurchasers of the credit-linked debt do not own the underlying loans. Such ownership interest belongs to the MBS investor.

Fannie Mae’s credit guaranty business model

Fannie Mae’s business model and industry-leading credit risk management capabilities facilitate the transfer of both interest rate risk and credit risk to the private markets.

© 2017 Fannie Mae. Trademarks of Fannie Mae. 7

Investors have shown an appetite for credit risk, and Fannie Mae’s credit risk in particular, given the

strong collateral characteristics and Fannie Mae’s role as a standard setter in the market

Investors in Fannie Mae’s CRT vehicles benefit from

Broad exposure to national U.S. housing market

Consistent high-quality underwriting standards

Fannie Mae’s comprehensive credit risk management process

Ongoing, programmatic issuance

Loan-level data disclosures and extensive historical datasets

Fannie Mae retains a portion of all risk transferred

To ensure the success of our Credit Risk Transfer (CRT) programs, Fannie Mae sets standards, provides credit risk management oversight, and maintains stability through all business cycles.

LENDER FANNIE MAE

Lenders leverage Fannie Mae’s proprietary suite of credit risk management tools to manufacture loans

Desktop Underwriter™ the most broadly used automated underwriting system in the industry

Collateral Underwriter® Fannie Mae’s proprietary appraisal valuation tool

Early Check™ assists lenders in identifying and correcting potential eligibility and/or data issues

Fannie Mae’s industry expertise ensures loan delivery quality and offers multiple avenues for credit risk sharing

Industry leading credit risk management technology and expertise

An established operational infrastructure and large scale aggregation capabilities

Robust strategy and development of a market for credit risk

Innovative credit risk sharing vehicles including Connecticut Avenue SecuritiesTM (CAS), and Credit Insurance Risk SharingTM (CIRTTM)

Credit Risk Transfer

As the largest guarantor in the U.S. housing market, Fannie Mae leads the industry in setting standards on managing and transferring credit risk.

INVESTOR

© 2017 Fannie Mae. Trademarks of Fannie Mae. 81/31/2018

About Fannie Mae

■ Government-Sponsored Enterprise (GSE) chartered by the United States Congress in 1938■ Our charter permits us to purchase and securitize mortgage loans secured by either a single-family or

multifamily property, but does not permit us to originate loans or lend money directly to consumers in the primary mortgage market

Background

■ Fannie Mae has a Single-Family guaranty business and a Multifamily guaranty business, both of which collect guarantee fees for assuming and managing the credit risk on our book of business, and a Capital Markets group that is responsible for managing the Company’s mortgage portfolio

Business

Conservatorship and United States (U.S.) Treasury agreement

■ Since September of 2008, Fannie Mae has been under Conservatorship with the Federal Housing Finance Agency (FHFA) acting as Conservator

■ Upon entering conservatorship, FHFA and the U.S. Treasury entered into a Senior Preferred Stock Purchase Agreement (SPSPA) on our behalf so that we could continue to fulfill our mission of providing liquidity and support to the housing market

1) Source: https://www.treasury.gov/press-center/press-releases/Pages/hp1131.aspx

Our public mission is to support liquidity and stability in the secondary mortgage market, where existing mortgage-related assets are purchased and sold, and to increase the supply of affordable housing.

■ Upon entering into the agreement, the U.S. Treasury stated that the holders of senior debt, subordinated debt, and mortgage backed securities issued or guaranteed by these GSEs are protected by the SPSPA without regard to when those securities were issued or guaranteed1

© 2017 Fannie Mae. Trademarks of Fannie Mae. 9

Payments under the Treasury agreement

■ Upon entering conservatorship Fannie Mae, through FHFA and the U.S. Treasury, entered into the SPSPA that permitted Fannie Mae to continue to fulfill our mission of providing liquidity and support to the housing finance market

■ Through this agreement, the U.S. Treasury stated that the holders of senior debt, subordinated debt, and mortgage backed securities issued or guaranteed by these GSEs are protected by the SPSPA without regard to when those securities were issued or guaranteed1

■ We received a total of $116.1B of funding from Treasury to support our operations and have $117.6B of funding remaining under the agreement. Fannie Mae has not received funds from Treasury under the SPSPA since the first quarter of 2012

■ The Director of FHFA has directed Fannie Mae to make dividend payments to Treasury on the senior preferred stock on a quarterly basis

Dividend payments do not offset funds drawn under the SPSPA Quarterly dividend payments equal any net worth as of the prior quarter end minus a capital

reserve amount, currently $600 million The capital reserve amount will be reduced to $0 in 2018

■ Through the third quarter of 2017, we have paid a total of $165.8 billion in dividends to Treasury, $49.7 billion more than the $116.1 billion we have received from Treasury to date

■ We paid Treasury $3.1 billion dividend in September 2017 due to FHFA declaring a dividend in this amount

1) Source: https://www.treasury.gov/press-center/press-releases/Pages/hp1131.aspx

© 2017 Fannie Mae. Trademarks of Fannie Mae. 10

Credit risk management

© 2017 Fannie Mae. Trademarks of Fannie Mae. 11

Fannie Mae’s comprehensive and proactive risk management approach aims to strengthen loan performance and reduce losses. This approach focuses on ensuring lender, loan, and servicing quality throughout the loan lifecycle.

Loans included in the CAS Reference Pools have all been securitized into Fannie Mae’s guaranteed MBS, and are therefore subject to the same origination, underwriting, quality control, and servicing standards as other loans guaranteed by Fannie Mae.

Loan Quality

Servicing Quality

Property Management

and Disposition

Lender Quality

Single-family credit risk management

In contrast to legacy Non-Agency RMBS transactions, investors in CAS deals benefit from Fannie Mae’s ongoing credit risk management.

© 2017 Fannie Mae. Trademarks of Fannie Mae. 12

Credit risk management overview

■ As the largest credit risk manager in the industry, we have built a comprehensive approach to credit risk management aided by cutting-edge analytical tools and grounded in cohesive end-to-end processes

■ Beginning in 2008, we took action to significantly strengthen our underwriting and eligibility standards to improve the quality of loans delivered to us

■ The changes we’ve made and continue to make help to make mortgage lending safer by providing more complete and accurate information about the key factors in underwriting a loan – from the value of the home being purchased to the borrower’s income and credit history

■ We have pioneered the industry-preferred automated underwriting system, a cutting-edge appraisal analytics tool, and built the largest loss mitigation platform in the industry

■ We leverage in-depth market data, research, and analysis to manage our book of business – and provide that information to our lenders in order to improve the end-to-end loan manufacturing process

We stand side-by-side with our credit risk investorsand strive to provide the greatest possible transparency into the tools and processes that make us the market leader in single-family residential mortgage credit risk management.

© 2017 Fannie Mae. Trademarks of Fannie Mae. 13

Our credit risk management approach■ Lenders undergo a rigorous approval process prior to doing business with Fannie Mae and

must meet ongoing net worth and business operational requirements

■ Lenders are subject to ongoing oversight through comprehensive operational reviews to assessthe effectiveness of their quality control procedures

■ Loans must be underwritten in accordance with Fannie Mae guidelines. Over 90%(1) of loansthat we acquire are evaluated through Desktop Underwriter®, DU®, the industry’s mostwidely used automated underwriting system

■ 100% of Fannie Mae’s single-family and condo appraisals are assessed through CollateralUnderwriter®, our proprietary appraisal risk assessment tool, to identify potential appraisalquality issues

■ Fannie Mae sets loan servicing standards, acts as Master Servicer, and provides oversight ofloan servicers

■ We set standards for loss mitigation and borrower workout options. Our proprietary servicingtool, Servicing Management Default UnderwriterTM (SMDUTM) automates our servicingpolicies

■ We conduct all property management and disposition in house, managing the industry’slargest real-estate owned portfolio – disposing of over 1.5 million homes since 2009

■ Our strategy is to sell non-distressed homes to owner-occupants, helping to maximize salesproceeds, stabilize neighborhoods, and preserve the value of our guaranty book

(1) Estimate of 2016 new acquisitions, excluding loans acquired under Fannie Mae’s Refi Plus and HARP initiatives

Our full range of credit risk management capabilities is driven by innovation and analytics and informed by continuous feedback across the loan lifecycle

Lender quality

Loan quality

Servicing quality

Propertymanagement

and disposition

© 2017 Fannie Mae. Trademarks of Fannie Mae. 14

Key credit risk management highlights

Loan Deliveries in

2016 thru DU®(1)

Desktop Underwriter®

approx. 1,861

Lenders/agents

USERS

Collateral Underwriter®

20,000+ Users

2,300+ Lenders/

agents

USERS since Jan.

2015

Over half of our lenders actively use CU™ during

origination process

100% of single-family and condominium loans

go through CU™ as part of our QC process

27 Million Appraisals collected to Date

Single Family Real Estate Servicing Management Default Underwriter™

100% of REO sales are managed

in-house: resulting in lower costs;

higher sales prices, and reduced severities

Beginning in Q4 2016, we offer Direct 3rd PartyData Validation of borrower income, assets,

and employment information

85% of ALLdelinquencies

covered

Allowed over 131,000 borrowers to start trial modifications in 2016

Created an interface that will give > 1,000 mid-size and smaller servicers system access

1-2 hoursper loan

New automated loss mitigation functionality

saves

>90%

(1) 2016 new acquisitions, excluding loans acquired under Fannie Mae’s Refi Plus and HARP initiatives

Best execution approach to sell real estate

based on an NPV comparison to a move-in

ready home sold to an owner occupant

>2 million Appraisals have been viewed by lenders since launch

Industry’s largest distressed portfolio disposed

of >1.5 million homes since 2009

11.8 Millionvisits in YTD 2017

Connecticut Avenue Securities Investor Presentation

Key credit risk management highlights

© 2017 Fannie Mae. Trademarks of Fannie Mae. 15

■ Changed guidelines to eliminate certain higher risk products such as interest-only loans and 40-year loans and to eliminate newly originated “Alt-A” and low documentation loans

■ Revised eligibility guidelines to reduce amount of risk layering (i.e., combining multiple higher risk elements on a single loan such as a low credit score with a high debt ratio)

■ Require homebuyer education and counseling for certain products

■ Revised servicing protocols to establish quality contact with delinquent borrowers more quickly

■ Introduced more effective modification programs for qualified distressed borrowers

■ Enhanced servicer training and oversight and implemented new servicer metrics, incentives and compensatory fees

■ Created industry’s largest platform for management and sale of Real Estate Owned properties, creating significant efficiencies in marketing and selling properties

■ Created cutting-edge data driven tools to support underwriting, property valuation, quality control, servicing and real estate owned management

■ Innovative analytics leverage Fannie Mae’s vast trove of data to improve loan manufacturing quality and identify defects earlier in the process

Underwriting andEligibility

Credit Loss Management

Innovation

Summary of single-family business changes since the global financial crisis

As the largest guarantor of U.S. mortgages, we play a major role in setting the standards for the housing finance market.

© 2017 Fannie Mae. Trademarks of Fannie Mae. 16

CAS key features and deal highlights

© 2017 Fannie Mae. Trademarks of Fannie Mae. 17

Fannie Mae’s Connecticut Avenue SecuritiesTM (CAS) program

Since 2013, our award-winning CAS program has grown to be the premier mortgage credit

risk transfer program in the industry, established through:

Industry-leading, innovative credit-risk management methodologies

Thoughtful issuance approach

Transparent and unique investor resources

Maturing and liquid market

The Benchmark for U.S. mortgage credit

Proprietary credit risk management tools and processes manage credit risk on the largest mortgage credit book in the industry

Innovative tools that improve the loan manufacturing process

A benchmark issuer with a transparent issuance calendar

$28.4 billion issued since 2013

Transferring a significant portion of risk on $942B in unpaid principal balance of mortgage loans

Historical research dataset of over 36 million loans

Transparent webpagesdetailing our comprehensive credit risk management process

Loan-level disclosures

Unique Data DynamicsTM

tool enabling analysis of loan-level data and deal performance

© 2017 Fannie Mae. Trademarks of Fannie Mae. 171/31/2018Connecticut Avenue Securities Investor Presentation

© 2017 Fannie Mae. Trademarks of Fannie Mae. 18

Program benefits and issuance volumes

• Large, geographically diversified loan pools provide broad exposure to U.S. housing market

• Fannie Mae acts as credit risk manager throughout the program – acting as an intermediary between the lender and investor to set standards, manage quality, mitigate losses, and maximize value

• Ongoing, programmatic issuance and consistent structures

• Broad Wall Street coverage, making daily markets and publishing research and analytics

• Pricing and trading volume available on TRACE and Bloomberg

• Active deal management – including seeking and receiving ratings on previously unrated CAS bonds

• Transparent investor resources – including our investor analytical tool – Data Dynamics® Fannie Mae has issued $28.4 BN under the CAS

program to date, and $22.4 BN in bonds remain outstanding as of November 21, 2017.

0

2000

4000

6000

8000

10000

2013 2014 2015 2016 2017 YTD

Dea

l Iss

uan

ce M

illio

ns

($)

CAS Issuance

M-1 M-2 B B-1

© 2017 Fannie Mae. Trademarks of Fannie Mae. 19

2018 issuance calendar

■ The calendar below highlights periods in 2018 during which Fannie Mae may issue Connecticut Avenue Securities

■ Fannie Mae may choose not to issue in some periods, or in certain limited issuance windows, may choose to issue up to two deals.

■ Issuance volumes and utilization of available issuance windows continue to be dependent on market conditions

*Issuance windows in which Fannie Mae may issue up to two CAS deals, subject to market conditions

Connecticut Avenue Securities Investor Presentation

Month Issuance Window

February/March* Early February to early March

April/May* Late April to late May

June Mid- to late June

July/August* Late July to late August

September/October* Late September to late October

December Early December

© 2017 Fannie Mae. Trademarks of Fannie Mae. 20

Connecticut Avenue Securities deal structure overview

© 2017 Fannie Mae. Trademarks of Fannie Mae. 21

Class

Loan

Group

Offered Notes

($MM)

Expected

Credit

Support (%)

Tranche

Thickness (%)

Expected Ratings

(Fitch/KBRA)

Expected WAL @

10 CPR (yrs)

Expected Principal

Window @ 10 CPR

2M-1 2 $107.666 3.40% 0.85% BBB-sf/BBB(sf) 1.42 1-28

2M-2 2 $303.996 1.00% 2.40% Bsf/B(sf) 6.10 28-120

2B-1 2 $63.333 0.50% 0.50% NR/NR 10.01 120-120

2B-2 2 $0.000 0.00% 0.50% NR/NR N/A N/A

Sample transaction overview

Loan Group 1: Loans with 60.01% - 80.00% original loan-to-value ratios

Loan Group 2: Loans with 80.01% - 97.00% original loan-to-value ratios

CAS 2017-C07 Group 2 collateral (April 2017-June 2017)

Class

Loan

Group

Offered Notes

($MM)

Expected

Credit

Support (%)

Tranche

Thickness (%)

Expected Ratings

(Fitch/KBRA)

Expected WAL

@ 10 CPR (yrs)

Expected Principal

Window @ 10 CPR

1M-1 1 $186.170 3.05% 0.95% BBB-sf/BBB+(sf) 2.06 1-39

1M-2 1 $401.734 1.00% 2.05% Bsf/BB-(sf) 6.66 39-120

1B-1 1 $97.984 0.50% 0.50% NR/NR 10.01 120-120

1B-2 1 $0.000 0.00% 0.50% NR/NR N/A N/A

CAS 2017-C07 Group 1 (February 2017-April 2017)$ 1.161 billion in offered notes(1)

(1)The Maturity Date for all classes will be February 2030.Note: WALs at 10 CPR to Optional Redemption

© 2017 Fannie Mae. Trademarks of Fannie Mae. 22

CAS 2017-C07 structural overview■ The Reference Pool is subdivided

into two loan groups by original LTV

■ Each loan group serves as a reference for a separate set of securities

■ Notes are par-priced uncapped LIBOR floaters

■ 12.5-year legal final maturity; Fannie Mae optional 10% clean up call and call starting in year 10

■ The minimum credit enhancement to unlock unscheduled principal is 4.50% for Group 1 and Group 2

■ Credit events are based on actual losses

■ 1M-2 and 2M-2 classes will offer exchange features with rated exchangeable notes

■ Fannie Mae will retain 100% of each first loss tranche and at least 5% of all offered tranches.

Reference Pool

February 2017* – April 2017 Acquisition for Loan Group 1

April 2017 – June 2017 Acquisition for Loan Group 2

Group 1 Loans

Original LTV 60.01 – 80.00%

Class 1A-H

96.00% thick

4.00% credit support

Class 1M-1

0.95% thick

3.05% credit support

Class 1M-2

2.05% thick

1.00% credit support

Class

1M-2H

(5% vertical

slice)

Class

1M-1H

(5% vertical

slice)

All H tranches are reference tranches only and will not be issued

Class 1B-1

0.50% thick

0.50% credit support

Class

1B-1H

(5% vertical

slice)

Class

1B-2H

0.50% thick; 0% credit support

Connecticut Avenue Securities Investor Presentation

Class 2A-H

95.75% thick

4.25% credit support

Class 2M-1

0.85% thick

3.40% credit support

Class 2M-2

2.40% thick

1.00% credit support

Class

2M-2H

(5% vertical

slice)

Class

2M-1H

(5% vertical

slice)

Class 2B-1

0.50% thick

0.50% credit support

Class

2B-1H

(5% vertical

slice)

Class

2B-2H

0.50% thick; 0% credit support

Group 2 Loans

Original LTV 80.01 – 97.00%

*February 2017 acquisitions targeted for CAS were randomly divided, with 50% allocated to CAS

2017-C06 and the remaining 50% allocated to CAS 2017-C07

© 2017 Fannie Mae. Trademarks of Fannie Mae. 23

CAS 2017-C07 exchangeable notes

1M-2A, 1M-2B and 1M-2C are LIBOR floaters with a margin that is equal to the 1-M2, and the 2M-2A, 2M-2B and 2M-2C are LIBOR floaters with a margin that is equal to the 2M-2

To reduce the coupon, each exchangeable class can be stripped down to exchange into four P&I tranches, each with a different margin and corresponding fixed IO

Multiple options to combine the floating rate and IO classes are available to meet various investor needs

Class 1M-2$401.734

Bsf / BB- (sf)

Credit Enhancement: 1.00%

1M-2A/1M-2B/1M-2C OptionClass 1M-2A

$133.258

BBsf / BBB(sf)

Credit Enhancement: 2.37%

Class 1M-2B

$133.258

BB-sf / BB+(sf)

Credit Enhancement: 1.69%

Class 1M-2C

$135.218

Bsf / BB-(sf)

Credit Enhancement: 1.00%

Prin

cip

al

Losses

Tranching and coupon stripping

to provide optionality to meet

investor needs

Exchangeable notes-upgrade to investment grade

Deal Exchangeable Class Rating agency At issuance Current rating

CAS 2016-C011M-2A Moody's/Kroll Ba1/BBB- Baa2 (upgrade)/BBB-

2M-2A Moody's/Kroll Ba1/BB+ Baa3 (upgrade)/BB+

CAS 2016-C02 1M-2A Moody's/Kroll Ba1/BBB Baa2 (upgrade)/BBB

Connecticut Avenue Securities Investor Presentation

Class 2M-2$303.996

Bsf / B (sf)

Credit Enhancement: 1.00%

2M-2A/2M-2B/2M-2C OptionClass 2M-2A

$101.332

BBsf / BBB-(sf)

Credit Enhancement: 2.60%

Class 2M-2B

$101.332

BB-sf / BB(sf)

Credit Enhancement: 1.80%

Class 2M-2C

$101.332

Bsf / B(sf)

Credit Enhancement: 1.00%

Prin

cip

al

Losses

Tranching and coupon stripping

to provide optionality to meet

investor needs

© 2017 Fannie Mae. Trademarks of Fannie Mae. 24

■ CAS cash flow structure is designed to be similar to typical RMBS transaction cash flows

■ Principal payments and losses applied to the notes mirror the principal payments and losses experienced on the loans in the underlying Reference Pool

■ Principal Payments are first allocated pro rata between the senior notes and the subordinate notes, then are applied sequentially to the subordinate notes starting with M-1

The deal must meet specified credit enhancement and delinquency tests in order for the subordinate notes to receive unscheduled principal payments (i.e., prepayments)

■ Losses are applied in reverse sequential order starting with class B-2

■ Principal payments and losses are allocated pro rata between the sold notes and the retained vertical slice

Loan Group 1 (60.01 – 80.00 LTV)

Senior Notes: A class | Subordinate Notes: M classes, B classes | Retained Vertical Slice: 1M-1H, 1M-2H, 1B-1H, 1B-2H, 2M-1H, 2M-2H, 2B-1H, 2B-2H

Cash flow waterfall

Prin

cip

al

Lo

sses

Class 1A-H

Class 1B-1H

Class 1M-1

Class 1M-2 Class 1M-2H

Class 1M-1H

Class 1B-1

Class 1B-2H

Connecticut Avenue Securities Investor Presentation

Loan Group 2 (80.01 – 97.00 LTV)

Prin

cip

al

Lo

sses

Class 2A-H

Class 2B-1H

Class 2M-1

Class 2M-2 Class 2M-2H

Class 2M-1H

Class 2B-1

Class 2B-2H

© 2017 Fannie Mae. Trademarks of Fannie Mae. 25

Credit events and allocation of losses

Allocation of principal loss amounts Allocation of modification loss amounts

Class B2 - Principal1 Class B2 - Interest1

Class B2 - Principal2

Class M2 - Interest5

Class M2 - Principal6

Class M1- Interest7

Class M1 - Principal8

Class M2 - Principal3

Class M1 - Principal4

Class B1 - Interest3

Class B1 - Principal4

Class B1 - Principal2

Connecticut Avenue Securities Investor Presentation

© 2017 Fannie Mae. Trademarks of Fannie Mae. 26

Actual loss calculation – principal losses

Losses at Disposition

(+) Loan Balance UPB at time of removal from reference pool (including any prior principal forgiveness

amount)

(+) Total Liquidation Costs Foreclosure Expense

Property Preservation Expense

Asset Recovery Expense

Miscellaneous Holding Expenses/Credits

Associated Taxes

(+) Accrued Interest Unpaid interest from Last Paid Installment date through Disposition Date on interest-

bearing UPB, based on net Note rate (Note Rate net of servicing fee or 35 bps,

whichever is greater)

(-) Total Proceeds Net Sales Proceeds

Credit Enhancement Proceeds (Mortgage Insurance Proceeds)

Repurchase/ Make Whole Proceeds

Other Proceeds

Expenses and proceeds associated with a credit event are passed through to noteholders 90 days after the disclosedDisposition Date (e.g., property sale date). Any remaining trailing expenses and proceeds are passed through on a monthlybasis thereafter as received.

Connecticut Avenue Securities Investor Presentation

© 2017 Fannie Mae. Trademarks of Fannie Mae. 27

Modification lossesModification Borrower Impact Loss to Investor

Interest Rate Reduction Reduces monthly interest rate borrower pays

on loan obligation

Losses passed through based on the

difference between the modified and

original note rate paid on the outstanding

loan balance

Principal Forbearance Mortgage payments are temporarily

suspended to reduce monthly mortgage

payments for a specific period of time; the

portion of suspended principal does not bear

interest and is due at termination of the loan

Loss reflects foregone interest on non

interest bearing portion of UPB

Term Extension The loan term is extended to reduce borrower

monthly payments

No loss impact to investor

Principal Forgiveness* The outstanding principal loan balance is

subject to a one time principal reduction based

on established eligibility criteria

At time of principal forgiveness, no

modification losses will be passed

through to noteholders

The forgiven UPB amount will be

treated as unscheduled principal at

the time of the modification

If the modified loan subsequently

becomes subject to a credit event, the

amount of the principal forgiveness

will be included in the credit event net

loss (realized loss calculation)

*Fannie Mae does not anticipate that any loans referenced in CAS deals will be eligible for Principal Forgiveness*Principal Forgiveness Eligibility Criteria: http://www.fhfa.gov/Media/PublicAffairs/Pages/FHFA-Announces-PRM-Program-and-Further-Enhancements-to-NPL-Sales-Reqts.aspx

Modification losses are passed through to noteholders on a monthly basis once a permanent modification takes effect. No losses are incurred during a modification trial period (typically 3 months).

Connecticut Avenue Securities Investor Presentation

© 2017 Fannie Mae. Trademarks of Fannie Mae. 28

Acquisition profile

Source: Fannie Mae Data, as of November 2017 activity date

Connecticut Avenue Securities Investor Presentation

© 2017 Fannie Mae. Trademarks of Fannie Mae. 29

Fully amortizing, generally 25-year and 30-year fixed rate**, 1-4 unit, first lien, conventional

Not subject to a repurchase request as of Cut-Off Date

In an MBS as of the cut-off date

Not Refi Plus™ / Not HARP

February 2017* – April 2017 Total Acquisitions of $109.0BN Original UPB

0 x 30 payment history since acquisition

Random Division

60% < Loan-to-Value < 80%

Reserved for

Reinsurance

*February 2017 acquisitions targeted for CAS were randomly divided, with 50% allocated to CAS 2017-C07**All loans will have terms greater than 240 months and less than or equal to 360 months. Other minimal exclusion criteria apply.*** Current UPB Reflects CAS 2017-C07 Sept 2017 Book Profile. Numbers may not foot due to rounding.

Fannie Mae acquires HARP loans under its Refi Plus™ initiative, which provides expanded refinance opportunities for eligible Fannie Mae borrowers.

CAS 2017-C07 G1 reference pool selection process

Connecticut Avenue Securities Investor Presentation

Connecticut Avenue Securities: $20.63BN Current UPB ***

Not subject to any form of risk sharing with the loan seller and/or servicer

Approximately 50% of February 2017 acquisitions + 100% of March 2017 – April 2017 (random division)

Not a hurricane-related exclusion loan

© 2017 Fannie Mae. Trademarks of Fannie Mae. 30

Fully amortizing, generally 25-year and 30-year fixed rate**, 1-4 unit, first lien, conventional

Not subject to a repurchase request as of Cut-Off Date

In an MBS as of the cut-off date

Not Refi Plus™ / Not HARP

April 2017 – June* 2017 Total Acquisitions of $121.34BN Original UPB

0 x 30 payment history since acquisition

Random Division

80% < Loan-to-Value < 97%

Reserved for

Reinsurance

*June 2017 acquisitions targeted for CAS were randomly divided, with 50% allocated to CAS 2017-C07**All loans will have terms greater than 240 months and less than or equal to 360 months. Other minimal exclusion criteria apply.*** Current UPB Reflects CAS 2017-C07 Sept 2017 Book Profile. Numbers may not foot due to rounding.

Fannie Mae acquires HARP loans under its Refi Plus™ initiative, which provides expanded refinance opportunities for eligible Fannie Mae borrowers.

CAS 2017-C07 G2 reference pool selection process

Connecticut Avenue Securities Investor Presentation

Connecticut Avenue Securities: $13.33BN Current UPB ***

Not subject to any form of risk sharing with the loan seller and/or servicer

100% of April 2017 - May 2017 + approximately 50% of June 2017 acquisitions

Not a hurricane-related exclusion loan

© 2017 Fannie Mae. Trademarks of Fannie Mae. 31

Private Mortgage Insurance on high LTV loans■ All loans in CAS deals with original loan-to-value ratios greater than 80% are required to have mortgage insurance

(MI) in place provided by one of 8 approved and active Mortgage Insurance Companies

Borrower-paid MI: the borrower makes a monthly payment as part of his/her mortgage payment

• Approximately 85%(1) of MI is borrower-paid. Monthly MI payment is typically 7% - 7.5%(2) of the borrower’s total mortgage payment at loan inception. MI can be canceled by borrower once loan reaches a certain LTV

Lender-paid MI: the lender pays for the MI upfront and charges the borrower a higher interest rate

• Approximately 15%(1) of MI is lender-paid. Lender-paid MI cannot be cancelled because the payment is built into the mortgage rate.

■ If a loan goes to disposition, the MI company is obligated to pay Fannie Mae a claim based on the MI coverage percentage. This payment is passed through to the CAS investor as additional disposition proceeds and reduces the loss

LTV Range Standard MI Coverage %

95.01 – 97.00 35.0%

90.01 – 95.00 30.0%

85.01 – 90.00 25.0%

80.01 – 85.00 12.0%

Note: most loans have “standard” coverage; however, levels may differ on some loans – this is disclosed on the loan-level deal file

■ If the MI company fails to pay a claim per their contractual obligation, Fannie Mae will step in and cover the MI contractual benefit amount on that loan. Investors are not exposed to MI Company counterparty risk

(1) Figures represent breakdown of MI payments from CAS 2017-C04 deal

(2) Given the following key assumptions: 90% LTV, 740 FICO, MGIC Mortgage Insurance rates (44 bps for a 740 FICO loan) No Curtailment

© 2017 Fannie Mae. Trademarks of Fannie Mae. 32

Guidelines for loans with LTV greater than 95%

Standard Guidelines:

■ Fannie Mae’s standard guidelines allow for LTV/CLTV up to 97% under the following circumstances:

Must be underwritten through DU; Loan purpose is for a purchase or a limited cash-out refinance (i.e., rate/term refinance) of an existing Fannie Mae loan; Property is a 1-unit primary residence

At least one borrower on the loan is a first-time homebuyer

HomeReady®:

■ Designed for creditworthy low- to moderate-income borrowers

■ Replaced Fannie Mae’s existing community lending program, My Community Mortgage, in late 2015

■ Allows for LTV up to 97% under the following circumstances:

Must be underwritten through DU; Loan purpose is for a purchase or a limited cash-out refinance (i.e., rate/term refinance) of an existing Fannie Mae loan; Property is a 1-unit primary residence

Borrower income is not more than 100% of area median income, or subject property is located in a low-income census tract

■ LTV>90% allows for lower MI coverage than standard loans to reduce borrowers’ monthly payments

■ Typically requires 25% MI for loans 90.01-97% LTV versus 30-35% MI coverage for standard loans

■ Fannie Mae charges lower loan-level price adjustments for HomeReady loans to help reduce cost to borrower

■ DU applies the same risk assessment to HomeReady as all other loans underwritten through DU

■ Some product flexibilities allowed with prudent underwriting (See Appendix)

Example: Documented income from non-borrower householder members may be considered as a compensating factor in DU to allow for DTI up to 50%

Note: non-borrower income is not included in the DTI ratio

Connecticut Avenue Securities Investor Presentation

© 2017 Fannie Mae. Trademarks of Fannie Mae. 33

Historical loan performance

© 2017 Fannie Mae. Trademarks of Fannie Mae. 34

Group 1 (60.01-80.00 OLTV) - historical acquisition profile

Source: Fannie Mae October 2017 Data ReleaseConnecticut Avenue Securities Investor Presentation

60-80 LTV Historical Loan Acquisition Profile

Orig year Loan Count Original UPB

WA Note

Rate WA Fico WA DTI WA OLTV WA OCLTV % 2nd Lien1 % Investor % Refi2 % TPO3 % CA

WA Risk

Layers4

1999 64,038 $8.4B 7.77% 705 32.9 75.9 76.0 0.7% 4.0% 35.2% 52.1% 15.0% 0.71

2000 549,663 $76.0B 8.09% 707 33.7 76.2 76.5 2.7% 4.3% 29.6% 57.1% 16.2% 0.69

2001 1,358,192 $211.3B 6.96% 709 32.4 75.1 75.6 3.8% 4.6% 67.7% 56.0% 20.1% 0.84

2002 1,401,199 $229.1B 6.48% 715 32.9 74.7 75.3 5.0% 5.0% 70.2% 57.5% 20.0% 0.84

2003 1,798,899 $309.1B 5.74% 717 32.6 74.2 75.0 7.0% 4.8% 75.5% 58.9% 20.6% 0.83

2004 726,741 $128.2B 5.83% 713 34.3 74.9 76.8 15.0% 4.1% 57.5% 60.6% 16.5% 0.93

2005 711,414 $137.2B 5.83% 717 36.9 75.0 77.5 20.3% 4.0% 56.8% 63.1% 11.5% 0.99

2006 566,515 $115.0B 6.41% 718 38.1 75.3 78.0 21.6% 5.3% 53.7% 64.7% 9.5% 1.03

2007 647,552 $138.3B 6.33% 720 37.9 75.3 77.9 20.6% 6.8% 58.7% 67.7% 10.4% 1.05

2008 697,327 $158.2B 6.03% 741 37.2 75.1 76.6 12.3% 8.5% 57.8% 62.7% 18.6% 0.82

2009 1,089,924 $260.4B 4.99% 760 34.5 74.5 75.6 9.0% 3.9% 70.8% 51.0% 20.5% 0.55

2010 779,816 $193.3B 4.74% 763 33.0 75.0 76.0 9.4% 6.3% 59.5% 56.3% 28.0% 0.36

2011 631,262 $148.0B 4.58% 761 33.3 75.1 76.2 8.7% 9.2% 55.8% 58.6% 29.4% 0.37

2012 1,019,597 $250.8B 3.85% 764 31.9 74.6 75.6 8.8% 8.8% 65.1% 56.3% 29.6% 0.32

2013 857,168 $204.5B 4.05% 757 33.2 75.1 76.2 8.9% 10.5% 53.2% 49.5% 29.7% 0.39

2014 581,444 $135.0B 4.47% 746 34.6 75.9 77.0 8.7% 11.5% 41.4% 46.4% 27.8% 0.48

2015 738,034 $179.6B 4.13% 748 34.1 75.3 76.3 8.0% 10.6% 51.5% 41.9% 27.3% 0.48

2016 535,256 $134.2B 3.95% 750 34.0 75.1 75.9 5.8% 8.7% 52.0% 40.9% 26.0% 0.46

Only loans with LTV between 60-80 are included. Excludes loans with CLTV >97

Statistics weighted by origination UPB

1Loans with CLTV more than 3 % greater than LTV are assumed to have second liens.

2Includes both Rate/Term and Cashout Refinances.

3Includes Broker and Correspondent originations.

4Risk Layers defined as: Investor Property, DTI>45, FICO<680, & Cash-out Refinance

© 2017 Fannie Mae. Trademarks of Fannie Mae. 35

Group 1: historical loss performance re-weighted to CAS 2017-C07 profile

Connecticut Avenue Securities Investor Presentation

Realized Loss Performance Default Pipeline ImplicationsCAS 2017-C07 G1 Equivalent Perf. (Not Including Default Pipeline)5

Orig YearRemaining

UPB Pool Factor12.5 Year Net Loss Mod Loss1 Total Loss

Rem. CAS Window

(Months)2

Rem. CAS Window %2

Unsold REO %3

Active D180 %4 Net Loss6 Mod Loss7

Total Comped

Loss

2000 0.4B 0.50% 0.13% 0.02% 0.15% 0.0 0.0% 0.01% 0.02% 0.08% 0.01% 0.09%

2001 1.9B 0.90% 0.19% 0.03% 0.22% 0.0 0.0% 0.01% 0.02% 0.12% 0.02% 0.13%

2002 4.4B 1.90% 0.28% 0.05% 0.33% 0.0 0.0% 0.02% 0.05% 0.20% 0.03% 0.23%

2003 15.3B 5.00% 0.49% 0.11% 0.60% 0.0 0.0% 0.03% 0.11% 0.38% 0.08% 0.46%

2004 8.7B 6.80% 1.18% 0.27% 1.45% 0.2 0.1% 0.06% 0.20% 0.79% 0.18% 0.97%

2005 12.3B 9.00% 3.01% 0.65% 3.66% 8.6 5.8% 0.12% 0.32% 2.12% 0.43% 2.55%

2006 9.7B 8.40% 4.52% 1.17% 5.69% 20.6 13.8% 0.15% 0.40% 2.99% 0.76% 3.76%

2007 12.9B 9.30% 4.04% 1.33% 5.37% 32.8 21.9% 0.18% 0.45% 2.50% 0.81% 3.30%

2008 11.1B 7.00% 1.61% 0.68% 2.29% 44.2 29.5% 0.12% 0.29% 1.17% 0.53% 1.70%

2009 35.2B 13.50% 0.23% 0.02% 0.25% 55.5 37.0% 0.04% 0.12% 0.31% 0.04% 0.35%

2010 40.3B 20.80% 0.07% 0.00% 0.07% 69.4 46.3% 0.03% 0.08% 0.13% 0.01% 0.14%

2011 40.9B 27.60% 0.03% 0.00% 0.03% 81.2 54.1% 0.02% 0.08% 0.06% 0.00% 0.06%

2012 137.2B 54.70% 0.01% 0.00% 0.01% 92.9 61.9% 0.01% 0.05% 0.03% 0.00% 0.03%

2013 117.2B 57.30% 0.01% 0.00% 0.01% 103.9 69.2% 0.01% 0.06% 0.01% 0.00% 0.01%

2014 72.3B 53.50% 0.00% 0.00% 0.00% 117.1 78.0% 0.01% 0.10% 0.00% 0.00% 0.00%

2015 135.6B 75.50% 0.00% 0.00% 0.00% 128.4 85.6% 0.00% 0.06% 0.00% 0.00% 0.00%

2016 120.9B 90.00% 0.00% 0.00% 0.00% 138.9 92.6% 0.00% 0.02% 0.00% 0.00% 0.00%

1. Reflects interest income forgone due to loan modifications (includes both interest rate and principal forbearance modifications)

2. Calculated as average loan age subtracted from 150 months (CAS maturity)

3. Calculated as default UPB for foreclosed loans that have yet to be disposed divided by total vintage origination UPB

4. Calculated as last UPB for loans that were in D180+ delinquency as of the last activity period in the public dataset divided by total vintage origination UPB

5. Reflects historical loss rates re-weighted to reflect the FICO, CLTV, & Risk Layer Count distribution of CAS 2017-C07 G1

6. In addition to the re-weighting, historical loss rates used in the comp process have been revised to reflect the ~4.38% WAC of the CAS pool

7. Reflects historical mod loss re-weighted to reflect the FICO, CLTV, & Risk Layer Count distribution of CAS 2017-C07 G1

© 2017 Fannie Mae. Trademarks of Fannie Mae. 36

0%

1%

2%

3%

4%

5%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

2017-C07 Group 1 Comped Loss Performance with Pipeline Consideration (60.01-80 LTV Loans)

Net Loss Mod Loss Comped Pipeline M2 Attach

M1 Attach M1 Detach B1 Attach Minimum CE

1. Bars reflect historical cum loss performance re-weighted to the CAS 2017-C07 G1 profile across FICO/CLTV/Risk Layer distribution

2. Mod Loss re-weighted to the CAS 2017-C07 G1 profile across FICO/CLTV/Risk Layer distribution (risk layers defined as: cashout refinance, investor property,

DTI>45 and single borrower)

3. Comped Pipeline equal to 25% of the previously defined loss pipeline re-weighted across the FICO/CLTV/Risk Layer distribution

Historical loss performance re-weighted to CAS 2017-C07 profile

Source: Fannie Mae Data Dynamics. http://www.fanniemae.com/DataDynamics

Connecticut Avenue Securities Investor Presentation

M1 Detach

M1 Attach

M2 Attach

B2 Attach

B1 Attach

3.05%

4.00%

0.50%

Minimum

Credit

Enhancement4.50%

© 2017 Fannie Mae. Trademarks of Fannie Mae. 37

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

0 12 24 36 48 60 72 84 96 108 120 132 144

% o

f O

rig

inati

on

UP

B

Months From First Payment

Group 1 (60.01-80.00 OLTV) Comped Historical Loss

y2000 y2001 y2002 y2003 y2004 y2005 y2006

y2007 y2008 y2009 y2010 y2011 y2012 y2013

M2 Attach M1 Attach M1 Detach B1 Attach Min CE

Group 1: historical loss performance re-weighted to CAS 2017-C07 profile

1. Curves reflect historical cum loss performance re-weighted to the CAS 2017-C07 Group 1 profile across FICO/CLTV/Risk Layer distribution2. Comped loan modification concession (mod loss) for a given vintage has been distributed evenly across each point on the respective curve3. A projected terminal loss has been calculated for all vintages with fewer than 150 months of activity. Projected terminal loss calculated by adding 25% of the

default pipeline to the cumulative loss (default pipeline defined as foreclosed loans without a property disposition and loans that were in D180 delinquency as of the most recent available activity record)

Source: Fannie Mae October 2017 Data ReleaseConnecticut Avenue Securities Investor Presentation

M1 Detach

M1 Attach

M2 Attach

B1 Attach

B2 Attach

Minimum

Credit

Enhancement

© 2017 Fannie Mae. Trademarks of Fannie Mae. 38

Historical loss performance re-weighted to Group 1 CAS profiles

1. Dots reflect historical total loss performance re-weighted to all of Group 1 CAS profiles across FICO/CLTV/Risk Layer distribution2. For deals up to and including CAS 2015 C03, total loss is calculated in accordance with the fixed severity schedule; for the others, total loss is

calculated from actual net, modification and pipeline losses

Source: Fannie Mae Data Dynamics. http://www.fanniemae.com/DataDynamics

Connecticut Avenue Securities Investor Presentation

Fixed severity Actual loss

© 2017 Fannie Mae. Trademarks of Fannie Mae. 39

Loss/Severity statistical summary (Group 1)

Source: Fannie Mae October 2017 Data ReleaseConnecticut Avenue Securities Investor Presentation

Loss/Severity Summary Characteristics by Origination Year (Group 1)(Reflects loan status in performance dataset for activity through June 2017)

Loan Population: loans with zero balance code of '02', '03', '09', '15' with non-null Disposition dates

1999 -

20012002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Total

Default UPB ($M)1 $1,812 $1,804 $4,312 $3,569 $8,712 $10,075 $11,459 $6,053 $1,795 $434 $163 $107 $53 $20 $7 $50,375

Default Rate (%) 0.6% 0.8% 1.4% 2.8% 6.3% 8.8% 8.3% 3.8% 0.7% 0.2% 0.1% 0.0% 0.0% 0.0% 0.0% 1.7%

EXPENSES:

Delinquent Interest 12% 12% 11% 11% 10% 11% 11% 11% 9% 8% 8% 6% 6% 6% 4% 11%

Total Liquidition Exp. 12% 13% 13% 12% 9% 8% 8% 9% 9% 11% 11% 10% 10% 9% 5% 10%

Foreclosure 5% 5% 4% 4% 3% 2% 2% 3% 2% 3% 3% 3% 3% 3% 3% 3%

Property

Preservation 4% 4% 4% 3% 3% 2% 2% 2% 3% 3% 4% 4% 4% 3% 1% 3%

Asset Recovery 0% 1% 1% 1% 1% 1% 1% 1% 1% 1% 1% 0% 1% 0% 0% 1%

Misc. Holding

Expenses/Credits1% 1% 1% 1% 1% 1% 1% 1% 1% 1% 1% 1% 0% 0% 0% 1%

Associated Taxes 3% 4% 4% 3% 3% 2% 2% 3% 3% 3% 3% 2% 2% 2% 1% 3%

Total Costs 124% 125% 124% 123% 119% 120% 120% 120% 118% 119% 119% 116% 116% 114% 109% 120%

PROCEEDS:

Net Sales Proceeds 76% 76% 82% 77% 69% 63% 63% 67% 77% 83% 84% 86% 90% 92% 91% 69%

Credit Enhancement 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

Repurchase/Make

Whole8% 5% 1% 1% 2% 4% 7% 10% 7% 4% 3% 1% 1% 0% 0% 5%

Other 6% 4% 3% 2% 1% 1% 1% 1% 1% 2% 1% 3% 2% 3% 7% 2%

Total Proceeds 91% 85% 86% 80% 72% 68% 71% 78% 85% 88% 88% 89% 93% 96% 99% 75%

Severity 33.4% 40.1% 37.7% 42.7% 47.4% 51.5% 48.7% 42.1% 32.6% 30.8% 31.3% 27.2% 23.0% 18.9% 10.2% 45.2%

Total Net Loss ($M) $605 $724 $1,626 $1,525 $4,132 $5,188 $5,584 $2,548 $586 $133 $51 $29 $12 $4 $1 $22,749

Origination Year

1 Default UPB, expenses and proceeds in this view are for completed foreclosures only. These are defined as loans with a zero balance code of '09', '03', '02', or '15' and non-null disposition dates. Default

rate is calculated as the sum of default UPB divided by the origination UPB. Expense and proceed line items are a percentage of default UPB.

© 2017 Fannie Mae. Trademarks of Fannie Mae. 40

Group 2 (80.01-97.00 OLTV) - historical acquisition profile

Source: Fannie Mae October 2017 Data ReleaseConnecticut Avenue Securities Investor Presentation

80-97 LTV Historical Loan Acquisition Profile

Orig year Loan Count Original UPB

WA Note

Rate WA Fico WA DTI WA OLTV WA OCLTV % 2nd Lien1 % Investor % Refi2 % TPO3 % CA

WA Risk

Layers4

1999 48,172 $6.0B 7.87% 690 34.6 92.1 92.1 0.0% 1.4% 12.2% 51.3% 11.2% 0.59

2000 393,070 $50.8B 8.21% 693 35.8 92.2 92.2 0.0% 1.9% 10.7% 54.7% 10.8% 0.62

2001 638,520 $89.0B 7.08% 694 34.6 91.2 91.2 0.1% 2.5% 38.4% 54.8% 10.9% 0.69

2002 521,034 $74.2B 6.65% 696 35.5 91.1 91.1 0.1% 3.5% 37.0% 56.9% 9.6% 0.75

2003 510,404 $75.5B 5.85% 698 35.1 90.9 90.9 0.3% 3.3% 42.3% 58.3% 7.7% 0.76

2004 213,038 $31.9B 5.97% 695 36.2 91.3 91.3 0.3% 3.9% 28.8% 57.7% 4.5% 0.89

2005 167,094 $26.8B 5.97% 701 38.6 90.8 90.8 0.3% 4.4% 34.2% 59.1% 2.3% 0.95

2006 131,247 $22.5B 6.55% 702 40.0 90.6 90.6 0.3% 4.9% 35.5% 61.0% 2.0% 1.00

2007 213,877 $41.1B 6.50% 702 40.5 90.6 90.6 0.4% 5.8% 43.4% 67.6% 4.6% 1.05

2008 261,651 $55.6B 6.19% 731 39.9 90.9 90.9 0.3% 3.4% 29.4% 62.9% 13.3% 0.64

2009 158,604 $34.5B 5.02% 755 33.6 89.9 89.9 0.5% 0.0% 41.1% 45.7% 8.9% 0.11

2010 120,206 $27.3B 4.72% 760 32.8 90.3 90.4 0.5% 0.0% 31.6% 54.8% 10.4% 0.03

2011 160,352 $35.8B 4.59% 758 33.5 91.3 91.3 0.3% 0.0% 26.4% 59.6% 12.4% 0.04

2012 319,013 $73.2B 3.87% 757 33.0 91.4 91.4 0.4% 0.0% 32.8% 55.1% 13.6% 0.05

2013 413,398 $93.5B 4.16% 751 34.2 92.1 92.1 0.4% 0.1% 21.9% 50.0% 13.2% 0.07

2014 376,434 $84.7B 4.49% 743 35.1 92.0 92.0 0.3% 0.2% 14.8% 45.1% 12.5% 0.12

2015 457,192 $107.1B 4.17% 744 34.7 92.0 92.0 0.3% 0.2% 17.1% 42.5% 11.8% 0.08

2016 326,788 $78.4B 3.95% 745 34.8 92.1 92.1 0.2% 0.2% 15.3% 40.3% 12.0% 0.09

Only loans with LTV between 80-97 are included. Excludes loans with CLTV >97

Statistics weighted by origination UPB

1Loans with CLTV more than 3 % greater than LTV are assumed to have second liens.

2Includes both Rate/Term and Cashout Refinances.

3Includes Broker and Correspondent originations.

4Risk Layers defined as: Investor Property, DTI>45, FICO<680, & Cash-out Refinance

© 2017 Fannie Mae. Trademarks of Fannie Mae. 41

Group 2: historical loss performance re-weighted to CAS 2017-C07 profile

Connecticut Avenue Securities Investor Presentation

Realized Loss Performance Default Pipeline ImplicationsCAS 2017-C07 G2 Equivalent Perf.(Not Including Default Pipeline)5

Orig YearRemaining

UPB Pool Factor12.5 Year Net Loss Mod Loss1 Total Loss

Rem. CAS Window

(Months)2

Rem. CAS Window %2

Unsold REO %3

Active D180 %4 Net Loss6 Mod Loss7

Total Comped

Loss

2000 0.3B 0.70% 0.14% 0.04% 0.18% 0.0 0.0% 0.02% 0.02% 0.04% 0.02% 0.06%

2001 1.2B 1.30% 0.27% 0.06% 0.33% 0.0 0.0% 0.02% 0.04% 0.11% 0.03% 0.14%

2002 2.1B 2.80% 0.48% 0.12% 0.60% 0.0 0.0% 0.04% 0.08% 0.24% 0.06% 0.29%

2003 4.9B 6.50% 0.89% 0.22% 1.11% 0.0 0.0% 0.09% 0.18% 0.52% 0.13% 0.65%

2004 2.7B 8.50% 1.75% 0.43% 2.18% 0.2 0.1% 0.18% 0.33% 0.94% 0.23% 1.17%

2005 2.9B 10.80% 3.55% 0.80% 4.35% 8.5 5.7% 0.26% 0.51% 1.95% 0.42% 2.37%

2006 2.3B 10.20% 4.72% 1.39% 6.11% 20.6 13.7% 0.37% 0.63% 2.44% 0.67% 3.11%

2007 4.9B 11.90% 4.85% 2.00% 6.85% 33.5 22.3% 0.46% 0.80% 2.30% 0.97% 3.27%

2008 5.0B 9.10% 1.97% 1.25% 3.22% 44.0 29.3% 0.27% 0.48% 0.98% 0.79% 1.77%

2009 4.8B 13.90% 0.28% 0.04% 0.32% 55.2 36.8% 0.07% 0.12% 0.30% 0.07% 0.37%

2010 6.2B 22.80% 0.06% 0.01% 0.07% 69.4 46.3% 0.05% 0.09% 0.08% 0.01% 0.09%

2011 10.4B 29.00% 0.02% 0.00% 0.02% 81.5 54.3% 0.05% 0.10% 0.02% 0.01% 0.03%

2012 38.6B 52.60% 0.01% 0.00% 0.01% 93.1 62.0% 0.04% 0.09% 0.01% 0.00% 0.01%

2013 50.0B 53.20% 0.01% 0.00% 0.01% 104.5 69.7% 0.04% 0.14% 0.01% 0.00% 0.01%

2014 47.8B 56.00% 0.00% 0.00% 0.00% 117.1 78.1% 0.04% 0.18% 0.00% 0.00% 0.00%

2015 86.0B 78.70% 0.00% 0.00% 0.00% 128.6 85.7% 0.02% 0.13% 0.00% 0.00% 0.00%

2016 74.1B 92.50% 0.00% 0.00% 0.00% 138.9 92.6% 0.00% 0.04% 0.00% 0.00% 0.00%

1. Reflects interest income forgone due to loan modifications (includes both interest rate and principal forbearance modifications)

2. Calculated as average loan age subtracted from 150 months (CAS maturity)

3. Calculated as default UPB for foreclosed loans that have yet to be disposed divided by total vintage origination UPB

4. Calculated as last UPB for loans that were in D180+ delinquency as of the last activity period in the public dataset divided by total vintage origination UPB

5. Reflects historical loss rates re-weighted to reflect the FICO, CLTV, & Risk Layer Count distribution of CAS 2017-C07 G2

6. In addition to the re-weighting, historical loss rates used in the comp process have been revised to reflect the ~4.39% WAC of the CAS pool

7. Reflects historical mod loss re-weighted to reflect the FICO, CLTV, & Risk Layer Count distribution of CAS 2017-C07 G2

© 2017 Fannie Mae. Trademarks of Fannie Mae. 421/31/2018

-1%

0%

1%

2%

3%

4%

5%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

2017-C07 Group 2 Comped Loss Performance with Pipeline Consideration (80.01-97 LTV Loans)

Net Loss Mod Loss Comped Pipeline M2 Attach

M1 Attach M1 Detach B1 Attach Minimum CE

1. Bars reflect historical cum loss performance re-weighted to the CAS 2017-C07 G2 profile across FICO/CLTV/Risk Layer distribution

2. Mod Loss re-weighted to the CAS 2017-C07 G2 profile across FICO/CLTV/Risk Layer distribution (risk layers defined as: cashout refinance, investor property,

DTI>45 and single borrower)

3. Comped Pipeline equal to 25% of the previously defined loss pipeline re-weighted across the FICO/CLTV/Risk Layer distribution

Historical loss performance re-weighted to CAS 2017-C07 profile

Source: Fannie Mae Data Dynamics. http://www.fanniemae.com/DataDynamics

Connecticut Avenue Securities Investor Presentation

M1 Detach

M1 Attach

M2 Attach

B2 Attach

B1 Attach

Minimum

Credit

Enhancement

© 2017 Fannie Mae. Trademarks of Fannie Mae. 43

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

0 12 24 36 48 60 72 84 96 108 120 132 144

% o

f O

rigin

ation U

PB

Months From First Payment

Group 2 (80.01-97.00 OLTV) Comped Historical Loss

y2000 y2001 y2002 y2003 y2004 y2005 y2006

y2007 y2008 y2009 y2010 y2011 y2012 y2013

M2 Attach M1 Attach M1 Detach B1 Attach Min CE

Group 2: historical loss performance re-weighted to CAS 2017-C07 profile

1. Curves reflect historical cum loss performance re-weighted to the CAS 2017-C07 Group 2 profile across FICO/CLTV/Risk Layer distribution2. Comped loan modification concession (mod loss) for a given vintage has been distributed evenly across each point on the respective curve3. A projected terminal loss has been calculated for all vintages with fewer than 150 months of activity. Projected terminal loss calculated by adding 25% of the

default pipeline to the cumulative loss (default pipeline defined as foreclosed loans without a property disposition and loans that were in D180 delinquency as of the most recent available activity record)

Source: Fannie Mae October 2017 Data ReleaseConnecticut Avenue Securities Investor Presentation

M1 Detach

M1 Attach

M2 Attach

B1 Attach

B2 Attach

Minimum Credit

Enhancement

© 2017 Fannie Mae. Trademarks of Fannie Mae. 44

Historical loss performance re-weighted to Group 2 CAS profiles

1. Dots reflect historical total loss performance re-weighted to all of Group 2 CAS profiles across FICO/CLTV/Risk Layer distribution2. For deals up to and including CAS 2015 C03, total loss is calculated in accordance with the fixed severity schedule; for the others, total loss is

calculated from actual net, modification and pipeline losses

Source: Fannie Mae Data Dynamics. http://www.fanniemae.com/DataDynamics

Connecticut Avenue Securities Investor Presentation

Fixed severity Actual loss

© 2017 Fannie Mae. Trademarks of Fannie Mae. 45

Loss/Severity statistical summary (Group 2)

Source: Fannie Mae October 2017 Data ReleaseConnecticut Avenue Securities Investor Presentation

Loss/Severity Summary Characteristics by Origination Year (Group 2)

(Reflects loan status in performance dataset for activity through June 2017)

Loan Population: loans with zero balance code of '02', '03', '09', '15' with non-null Disposition dates

1999 -

20012002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Total

Default UPB ($M)1 $2,596 $1,805 $2,729 $1,852 $2,846 $3,082 $6,474 $4,824 $571 $153 $96 $89 $99 $52 $14 $27,282

Default Rate (%) 1.8% 2.4% 3.6% 5.8% 10.6% 13.7% 15.8% 8.7% 1.7% 0.6% 0.3% 0.1% 0.1% 0.1% 0.0% 2.7%

EXPENSES:

Delinquent Interest 11% 11% 10% 11% 11% 12% 11% 10% 7% 6% 7% 5% 5% 5% 3% 11%

Total Liquidition Exp. 11% 12% 13% 13% 11% 10% 9% 8% 8% 9% 10% 10% 9% 8% 5% 10%

Foreclosure 4% 4% 4% 4% 3% 3% 3% 2% 2% 2% 3% 3% 3% 2% 2% 3%

Property

Preservation 3% 4% 4% 3% 3% 2% 2% 2% 2% 3% 4% 4% 3% 3% 1% 3%

Asset Recovery 0% 0% 1% 1% 1% 0% 0% 1% 1% 1% 1% 1% 0% 0% 0% 0%

Misc. Holding

Expenses/Credits1% 1% 1% 2% 2% 1% 1% 1% 1% 1% 1% 1% 1% 1% 0% 1%

Associated Taxes 2% 3% 3% 3% 3% 2% 2% 2% 2% 2% 2% 2% 2% 2% 1% 2%

Total Costs 122% 123% 123% 124% 122% 121% 120% 118% 115% 115% 116% 116% 115% 113% 108% 121%

PROCEEDS:

Net Sales Proceeds 75% 71% 71% 66% 60% 56% 56% 61% 73% 80% 82% 83% 80% 80% 85% 63%

Credit Enhancement 24% 23% 22% 23% 23% 24% 24% 22% 20% 21% 24% 24% 25% 24% 17% 23%

Repurchase/Make

Whole5% 4% 2% 2% 3% 5% 8% 10% 4% 2% 1% 1% 0% 0% 0% 6%

Other 3% 3% 2% 2% 2% 2% 2% 1% 1% 1% 1% 1% 2% 2% 2% 2%

Total Proceeds 107% 101% 97% 93% 88% 87% 90% 96% 98% 104% 107% 108% 108% 106% 104% 94%

Severity 15.1% 22.4% 26.2% 30.4% 33.5% 34.5% 30.8% 22.7% 16.9% 10.9% 9.0% 7.6% 6.8% 6.3% 4.2% 26.8%

Total Net Loss ($M) $391 $404 $716 $563 $952 $1,063 $1,993 $1,097 $96 $17 $9 $7 $7 $3 $1 $7,319

Origination Year

1 Default UPB, expenses and proceeds in this view are for completed foreclosures only. These are defined as loans with a zero balance code of '02', '03', '09', or '15' and non-null disposition dates.

Default rate is calculated as the sum of default UPB divided by the origination UPB. Expense and proceed line items are a percentage of default UPB.

© 2017 Fannie Mae. Trademarks of Fannie Mae. 46

Group 1/Group 2 loss comparison

*RMW = Repurchase Make Whole proceeds**Other = Amounts other than sales proceeds including redemption proceeds received from the mortgagor

Connecticut Avenue Securities Investor Presentation

0%

20%

40%

60%

80%

100%

120%

Group 1 Proceeds as % of Defaulted UPB

CE Proceeds Sales Proceeds Other** RMW*

0%

20%

40%

60%

80%

100%

120%

Group 2 Proceeds as % of Defaulted UPB

CE Proceeds Sales Proceeds Other** RMW*

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Default Rate

Group 1 Group 2

0%

10%

20%

30%

40%

50%

60%

Severity

Group 1 Group 2

© 2017 Fannie Mae. Trademarks of Fannie Mae. 47

Group 1/Group 2 loss comparison

Connecticut Avenue Securities Investor Presentation

2017-C07 Group 1 Comped loss performance with

pipeline consideration (60.01-80.00 LTV loans)

2017-C07 Group 2 Comped loss performance with

pipeline consideration (80.01-97.00 LTV loans)

0%

1%

2%

3%

4%

5%

0%

1%

2%

3%

4%

5%

3.05%

4.00%

0.50%

4.50%

3.40%

4.25%

0.50%

4.50%

1. Bars reflect historical cum loss performance re-weighted to the CAS 2017-C07 G1/G2 profile across FICO/CLTV/Risk Layer distribution2. Mod Loss re-weighted to the CAS 2017-C07 G1/G2 profile across FICO/CLTV/Risk Layer distribution (risk layers defined as: cashout refinance, investor property,

DTI>45 and single borrower)3. Comped Pipeline equal to 25% of the previously defined loss pipeline re-weighted across the FICO/CLTV/Risk Layer distribution

© 2017 Fannie Mae. Trademarks of Fannie Mae. 48

Investor distribution and security performance

© 2017 Fannie Mae. Trademarks of Fannie Mae. 49

83%

5% 11%

1%

81%

2%4% 12%

61%11%

18%

10%

35%

1%

63%

<1%<1%

Program to date investor distribution

*Includes pensions, mutual funds, sovereign wealth funds, state/local government**Data through CAS 2017-C07Source: Fannie Mae and dealers, primary issuance only

2013 2014 2015 2016

M-1

M-2

64%

5%

19%

12%

50%

6%

42%

<1%2%

37%

<1%

55%

<1%

7%

42%

48%

1%

8%

2013 2014 2015 2016 2017

Investor Type M1 M2 M1 M2 M1 M2 M1 M2 M1 M2

Asset Manager* 64% 35% 61% 50% 81% 37% 83% 42% 82% 41%

Depository Institution/Bank 5% 1% 11% 6% 2% <1% 0% 0% <1% 0%

Hedge Fund/Private Equity 19% 63% 18% 42% 4% 55% 5% 48% 7% 46%

Insurance Company 12% <1% 10% 0% 12% <1% 11% 1% 10% 3%

REIT 0% <1% 0% 2% 0% 7% 1% 8% 0% 10%

Connecticut Avenue Securities Investor Presentation

2017**

82%

<1% 7%

10%

41%

46%

3%10%

© 2017 Fannie Mae. Trademarks of Fannie Mae. 50

CRT monthly average trading volume

Connecticut Avenue Securities Investor Presentation

$22.6B of secondary trading in CAS bonds in the last 12 months, over one times float of approximately $21.3B.

Source: Fannie Mae Survey

0%

2%

4%

6%

8%

10%

12%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017 Q3 2017

$ M

illio

ns

Investment Grade Non-Investment Grade Total Volume/Outstanding UPB (RHS)

© 2017 Fannie Mae. Trademarks of Fannie Mae. 51

Connecticut Avenue Securities spreads

Source: JP Morgan Markets, Fannie Mae

*As of November 2017

Connecticut Avenue Securities Investor Presentation

0

50

100

150

200

250

300

350

400

450

500

Spre

ad O

ver

Index/B

enchm

ark

(bps)

1M1 (1mL) 1M2 (1mL) 2M1 (1mL)

2M2 (1mL) CMBS BBB (vs swaps) CDX 5Y HY (vs swaps)

BBB Corporates (vs swaps)

© 2017 Fannie Mae. Trademarks of Fannie Mae. 52

CAS Ratings Overview

M1 ratings distribution

M2 ratings distribution

Connecticut Avenue Securities Investor Presentation

All previously non-rated CAS M2 bonds are now rated.

0%

10%

20%

30%

40%

50%

60%

BBBB+BBB-BBBBBB+A-AA+AA-AAAA+AAA

Initial Ratings Distribution Current Ratings Distribution

0%

10%

20%

30%

40%

50%

Not RatedB-BB+BB-BBBB+BBB-BBBInitial Ratings Distribution Upgrade Ratings Distribution

© 2017 Fannie Mae. Trademarks of Fannie Mae. 53

NAIC Designations

Designation Class

NAIC 2 CAS 2015-C04 1M2

NAIC 2 CAS 2015-C04 2M2

NAIC 1 CAS 2016-C01 1M2

NAIC 2 CAS 2016-C01 2M2

NAIC 1 CAS 2016-C02 1M2

NAIC 2 CAS 2016-C03 1M2

NAIC 2 CAS 2016-C03 2M2

NAIC 2 CAS 2016-C04 1M2

NAIC 3 CAS 2016-C05 2M2

NAIC 2 CAS 2016-C06 1M2

NAIC 3 CAS 2016-C07 2M2

Designation Class

NAIC 1 CAS 2015-C04 1M1

NAIC 1 CAS 2015-C04 2M1

NAIC 1 CAS 2016-C01 1M1

NAIC 1 CAS 2016-C01 2M1

NAIC 1 CAS 2016-C02 1M1

NAIC 1 CAS 2016-C03 1M1

NAIC 1 CAS 2016-C03 2M1

NAIC 1 CAS 2016-C04 1M1

NAIC 1 CAS 2016-C05 2M1

NAIC 1 CAS 2016-C06 1M1

NAIC 1 CAS 2016-C07 2M1

M1 Classes M2 Classes

CAS transactions received favorable NAIC designations for the 2016 filing year.

Connecticut Avenue Securities Investor Presentation

© 2017 Fannie Mae. Trademarks of Fannie Mae. 54

New investor resources

© 2017 Fannie Mae. Trademarks of Fannie Mae. 55

Collateral UnderwriterTM

Desktop Underwriter®

Servicing Management

Default UnderwriterTM

Property Valuation and

Analytics

Web-based credit-risk sharing resources bolster transparency

Gain a comprehensive overview of our industry-leading credit risk management processes

Demo our industry-leading, cutting-edge tools

Sign-up to receive Fannie Mae’s Credit Risk Transfer Commentary and News – delivered directly to your inbox

Gain confidence in our approach – view consolidated third-party due diligence results

Interact with and analyze Fannie Mae’s historical loan performance data, deal issuance data, and ongoing disclosure data with Data DynamicsTM

Drillable analysis of:

Credit Risk Sharing Webpage: http://fanniemae.com/portal/funding-the-market/credit-risk/index.html

© 2017 Fannie Mae. Trademarks of Fannie Mae. 56

Data Dynamics illustrative analysis

HistoricalPerformance

Data

CAS geographical analysis Historical comparative analysis

Access Data Dynamics: www.fanniemae.com/datadynamics

Cohort Default UPB Foreclosure Property

Preservation Asset

Recovery Misc. Taxes

Forgone Interest

Net Sales Credit

Enhancement Repurchase / Make Whole

Other Proceeds

Net Loss

2006 $1,117M $41.7M $38.0M $2.9M $4.0M $22.0M $105.6M $869.8M $173.2M $54.8M $62.5M $170.3M

2007 $1,329M $48.4M $36.5M $3.6M $4.1M $28.1M $117.1M $1,015.7M $184.7M $46.1M $60.8M $259.7M

2008 $2,124M $58.9M $43.6M $5.9M $3.9M $40.3M $169.2M $1,516.6M $229.5M $92.3M $40.1M $566.9M

2009 $5,327M $107.0M $79.8M $16.5M $11.2M $82.7M $393.9M $3,356.9M $480.6M $418.4M $42.4M $1,719.7M

2010 $10,996M $238.6M $171.4M $44.1M $31.4M $178.0M $888.2M $6,818.7M $829.4M $957.5M $92.7M $3,849.9M

2011 $15,686M $348.6M $315.0M $79.8M $75.5M $286.9M $1,438.1M $9,224.1M $1,076.5M $1,241.6M $202.5M $6,485.4M

2012 $13,417M $333.6M $302.2M $85.6M $101.4M $294.8M $1,287.7M $8,546.4M $943.8M $652.8M $188.5M $5,490.9M

2013 $9,402M $290.7M $279.4M $65.8M $120.0M $278.8M $1,109.3M $6,699.6M $647.6M $248.1M $153.5M $3,797.0M

2014 $6,890M $280.0M $286.2M $47.4M $139.7M $276.9M $1,028.4M $5,141.6M $490.2M $61.4M $138.3M $3,117.3M

2015 $5,682M $273.0M $317.3M $38.3M $144.4M $275.9M $986.2M $4,458.1M $375.2M $24.8M $123.6M $2,735.4M

2016 $2,914M $129.2M $129.6M $16.3M $56.2M $125.2M $553.8M $2,295.5M $150.6M $11.5M $59.2M $1,407.1M

Fannie Mae Credit Insurance Risk Transfer (CIRT) Overview

© 2017 Fannie Mae. Trademarks of Fannie Mae. 57

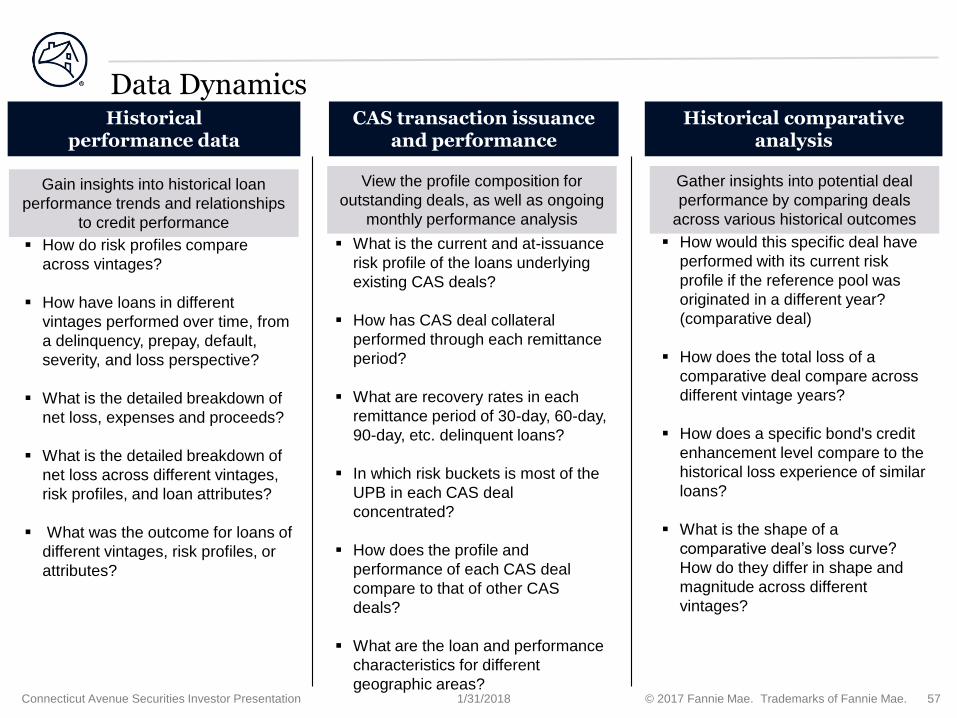

Data DynamicsHistorical

performance dataCAS transaction issuance

and performanceHistorical comparative

analysis

How do risk profiles compare

across vintages?

How have loans in different

vintages performed over time, from

a delinquency, prepay, default,

severity, and loss perspective?

What is the detailed breakdown of

net loss, expenses and proceeds?

What is the detailed breakdown of

net loss across different vintages,

risk profiles, and loan attributes?

What was the outcome for loans of

different vintages, risk profiles, or

attributes?

What is the current and at-issuance

risk profile of the loans underlying

existing CAS deals?

How has CAS deal collateral

performed through each remittance

period?

What are recovery rates in each

remittance period of 30-day, 60-day,

90-day, etc. delinquent loans?

In which risk buckets is most of the

UPB in each CAS deal

concentrated?

How does the profile and

performance of each CAS deal

compare to that of other CAS

deals?

What are the loan and performance

characteristics for different

geographic areas?

How would this specific deal have

performed with its current risk

profile if the reference pool was

originated in a different year?

(comparative deal)

How does the total loss of a

comparative deal compare across

different vintage years?

How does a specific bond's credit

enhancement level compare to the

historical loss experience of similar

loans?

What is the shape of a

comparative deal’s loss curve?

How do they differ in shape and

magnitude across different

vintages?

Gain insights into historical loan

performance trends and relationships

to credit performance

View the profile composition for

outstanding deals, as well as ongoing

monthly performance analysis

Gather insights into potential deal

performance by comparing deals

across various historical outcomes

1/31/2018Connecticut Avenue Securities Investor Presentation

© 2017 Fannie Mae. Trademarks of Fannie Mae. 58

■ Fannie Mae’s Single-Family Loan Performance Dataset provides historical monthly loan performance data on a portion of our single-family book of business to promote better understanding of the credit performance of Fannie Mae mortgage loans.

■ Includes a subset of our fully amortizing, full documentation, single-family, conventional fixed-rate mortgage acquisitions since January 2000, and is updated on a quarterly basis to include a new quarter of acquisitions (currently through Q3 2016) and performance (currently through Q2 2017)

■ Over 50 data elements per loan, including key loan risk factors, loan term characteristics, collateral characteristics, servicing data, and disposition data

■ Investor resources including file layout, glossary, FAQs, web tutorials, and statistical summaries support download of the dataset

Historical loan-level performance data

Appendix D: Loan level disclosure

Connecticut Avenue Securities Investor Presentation

■ One-click download feature to ease file-download experience

■ Inclusion of one million loans that were modified through HARP®, supporting market analysis of high loan-to-value refinance assistance programs

■ Inclusion of fixed-rate loans with 5 year to 25 year terms

■ Aggregate analysis of the loan-level historical data

■ Filter dataset across several dimensions to compare risk profiles and performance

■ View the HARP enhanced analysis at an aggregate level

Recent Enhancements Data Dynamics Features

www.fanniemae.com/loanperformance www.fanniemae.com/datadynamics

© 2017 Fannie Mae. Trademarks of Fannie Mae. 59

CAS loan-level data disclosure

Insert Presentation Title Here

■ Fannie Mae makes available nearly 90 loan-level disclosure fields to support analysis of its CAS deals and program

■ A one-click download feature in Data Dynamics enables users to download all available loan-level files at one time

■ Fields include key loan risk factors, loan term characteristics, collateral characteristics, servicing data, and disposition data, such as (not limited to):

Loan and Borrower

Characteristics

Property TypeHomeReady Program Indicator First Time Home Buyer Indicator

Number of Borrowers Original Debt to Income Ratio

Borrower FICO and Co-Borrower

FICO scores (at origination, deal

issuance, and ongoing)

Collateral

CharacteristicsNumber of Units

Original Loan to Value Ratio (LTV)

and Combined LTV Ratio (CLTV)Three digit zip code

Occupancy Type Metropolitan Statistical AreaProperty Inspection Waiver

Flag(1)

Servicing Data Servicer Name Loan Payment HistoryReason and Date as to why a loan

balance went to zero

Mortgage Insurance Cancellation

IndicatorModification Flag Current Loan Delinquency Status

Loan Term

CharacteristicsOriginal and Current Interest Rate Original Loan Term Loan Age

Original and Current UPB Origination Date Maturity Date

Disposition Data Last Paid Installment Date Foreclosure Date Detailed Proceed Fields

Original and Current List Price and

DateDisposition Date Detailed Expense Fields

Connecticut Avenue Securities Investor Presentation

(1) Available beginning with 2017-C07 forward

Appendix D: Loan level disclosure

© 2017 Fannie Mae. Trademarks of Fannie Mae. 60

A. How mortgage insurance works-High LTV loans 61

B. CAS deal summaries and comparisons 63

C. Credit risk management 67

D. Additional resources 78

Appendix

Connecticut Avenue Securities Investor Presentation

© 2017 Fannie Mae. Trademarks of Fannie Mae. 61

How Mortgage Insurance (MI) Works I: Possible Claim Outcomes

Appendix A: How does mortgage insurance work- Group 2 deals

Connecticut Avenue Securities Investor Presentation

© 2017 Fannie Mae. Trademarks of Fannie Mae. 62

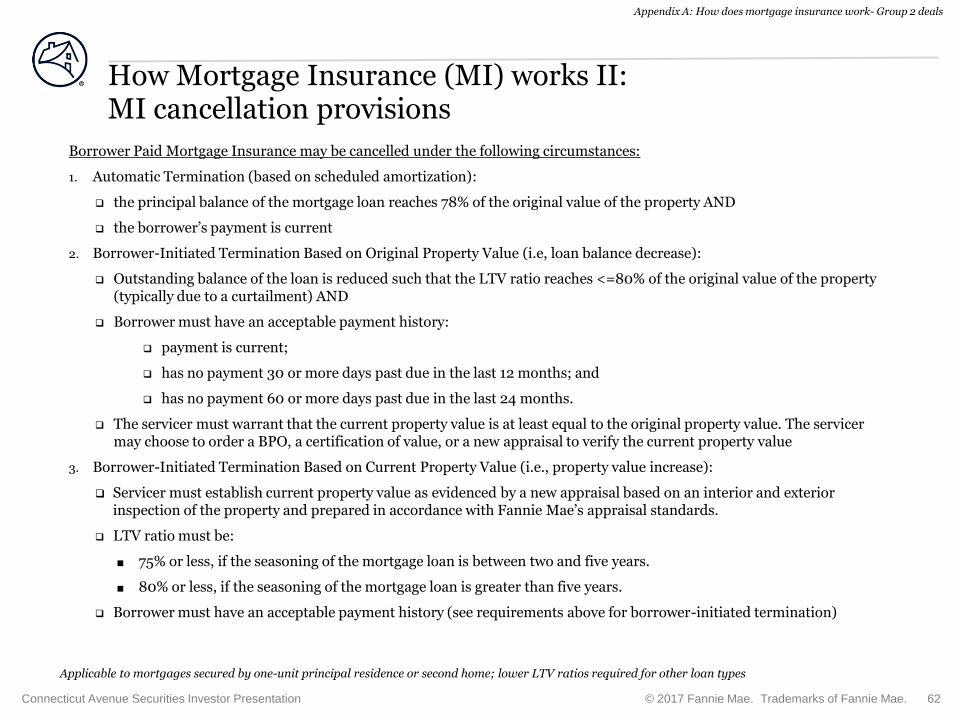

How Mortgage Insurance (MI) works II: MI cancellation provisions

Borrower Paid Mortgage Insurance may be cancelled under the following circumstances:

1. Automatic Termination (based on scheduled amortization):

the principal balance of the mortgage loan reaches 78% of the original value of the property AND

the borrower’s payment is current

2. Borrower-Initiated Termination Based on Original Property Value (i.e, loan balance decrease):

Outstanding balance of the loan is reduced such that the LTV ratio reaches <=80% of the original value of the property (typically due to a curtailment) AND

Borrower must have an acceptable payment history:

payment is current;

has no payment 30 or more days past due in the last 12 months; and

has no payment 60 or more days past due in the last 24 months.

The servicer must warrant that the current property value is at least equal to the original property value. The servicer may choose to order a BPO, a certification of value, or a new appraisal to verify the current property value

3. Borrower-Initiated Termination Based on Current Property Value (i.e., property value increase):

Servicer must establish current property value as evidenced by a new appraisal based on an interior and exterior inspection of the property and prepared in accordance with Fannie Mae’s appraisal standards.

LTV ratio must be:

■ 75% or less, if the seasoning of the mortgage loan is between two and five years.

■ 80% or less, if the seasoning of the mortgage loan is greater than five years.

Borrower must have an acceptable payment history (see requirements above for borrower-initiated termination)

Applicable to mortgages secured by one-unit principal residence or second home; lower LTV ratios required for other loan types

Appendix A: How does mortgage insurance work- Group 2 deals

Connecticut Avenue Securities Investor Presentation

© 2017 Fannie Mae. Trademarks of Fannie Mae. 63

Deal summaries & comparison – Group 1

Appendix B: CAS Deal Summaries and comparisons

Connecticut Avenue Securities Investor Presentation

2016-C01 2016-C02 2016-C03 2016-C04 2016-C06 2017-C01 2017-C03 2017-C05 2017-C06 2017-C07

Pricing Date 2/9/2016 3/22/2016 4/12/2016 7/19/2016 11/1/2016 1/18/2017 5/2/2017 7/18/2017 8/15/2017 11/14/2017

Pricing (1 Month

LIBOR +)

M1: 195 bps

M2: 675 bps

B: 1175 bps

M1: 215 bps

M2: 600 bps

B: 1225 bps

M1: 200 bps

M2: 530 bps

B: 1175 bps

M1: 145 bps

M2:425 bps

B: 1025 bps

M1: 130 bps

M2:425 bps

B: 925 bps

M1:130 bps

M2: 355 bps

1B-1: 575 bps

M1:95 bps

M2: 300 bps

1B-1: 485 bps

M1:55 bps

M2:220 bps

1B-1:360 bps

M1: 75 bps

M2: 265 bps

1B-1 415 bps

M1: 65 bps

M2: 240 bps

1B-1: 400 bps

SizeM1: $207.6 mm

M2: $333.9 mm

B: $94.9 mm

M1: $342.3 mm

M2: $599.1 mm

B: $90.1 mm