Conference Theatre Day One - 6 July

321

UK AD & BIOGAS TRADESHOW 6-7 JULY 2016 NEC BIRMINGHAM

-

Upload

gayle-brandon-kirby-mcipr -

Category

Environment

-

view

243 -

download

2

Transcript of Conference Theatre Day One - 6 July

UK AD & BIOGAS

TRADESHOW

6-7 JULY 2016NEC BIRMINGHAM

WELCOME AND

INTRODUCTION

BUILDING A WORLD CLASS AD INDUSTRY

CHARLOTTE MORTONADBA CEO

IAN FARRHEAD OF SALES – BIOGAS , EDINA GROUP

DRIVING WORLD CLASS PERFORMANCE:

LAUNCHING AN INDUSTRY BEST PRACTISE

SCHEME

CHARLOTTE MORTON, ADBA CEO

JESS ALLAN, ENVIRONMENT AND REGULATION MANAGER, ADBA

FRAN LOWE, ENVIRONMENT AND BUSINESS MANAGER, ENVIRONMENT AGENCY

CARL GURNEY, RENEWABLE ENERGY DIRECTOR, JELF INSURANCE BROKERS

DAVID WOOLGAR, DIRECTOR OF TECHNOLOGY, BIOGEN

AMAYA ARIAS-GRACIA, TECHNICAL DIRECTOR, GOALS PROJECT MANAGEMENT &

ENGINEERING SUPPORT

BEST PRACTICE SCHEME

FOR AD

JESS ALLANENVIRONMENT AND REGULATION MANAGER

AMAYA ARIAS-GARCIATECHNICAL DIRECTOR (GOALS PROJECT MANAGEMENT AND ENGINEERING)

Overview

• Aims

• Industry Engagement

• Steering Group

• Delivery Plan

• Best Practice Checklists

• Next Steps

• Get Involved

Aims

The Best Practice Scheme aims to help the industry to:

• Improve environmental performance.

• Improve safety performance.

• Improve operational performance.

Industry Engagement

• Member survey

• Steering Group

• Operator Groups

• Working Groups

• Stakeholder Meeting – May 2016

• Updates at ADBA events – Regulatory Forum, Members Meeting

Steering Group

Chaired by Amaya Arias-Garcia (Goals-PME)ADBA

Chartered Institute of Wastes Management (CIWM)

Chartered Institute of Water and Environmental Management (CIWEM)

CNA Hardy (insurer)

Country Land and Business Association (CLA)

Energy Networks Association (ENA)

Environmental Services Association (ESA)

Institute of Chemical Engineers (IChemE)

Jelf (insurance broker)

NFU

NFU Cymru

NFU Scotland

Renewable Energy Association (REA)

Water UK

WRAP

Zero Waste Scotland

Plus input from regulators:

APHA, EA, HSE, NRW, SEPA

Steering Group Conclusions

• Priority topics identified included: odour management, containment, digestate quality,

risk management, training and competence.

• Scheme should improve awareness of existing guidance, standards and legislation

and make it more accessible.

• Checklists were proposed as a first step towards a certification scheme.

Delivery Plan

Step 2: Best Practice Certification Scheme

(July 2017)Develop a certification scheme, informed by the

checklists.

Step 1: Best Practice Checklists

(July 2016)Develop a series of Best Practice checklists which bring together regulations, guidance,

standards relating to best practice.

Best Practice Checklists

• Checklist-style guides on key topics identified through industry engagement:

Operational Performance

Risk Management

Procurement

• Raise awareness of existing guidance, regulations and standards that contribute to

best practice.

• Collate guidance to make it more accessible.

• Provide a foundation for a certification scheme.

Risk Management

• Covers identifying and managing risks to:

- Health and safety

- Environment

• Explains benefits of effective risk management.

• Promotes instilling risk awareness for all individuals involved in operating a plant,

from senior management to site operatives and contractors.

• Encompasses risk management at different stages of an AD project.

• Guide to making procurement decisions for items of plant, equipment or

machinery, and services such as maintenance contracts.

• Focuses on ensuring:

- Compliance with legislative requirements

- Safety and environmental protection

- Suitability for intended purpose

- Cost-effectiveness

Procurement

Operational Performance

• Focuses on identifying and overcoming barriers to good performance.

• Features guidance and tips on:

- Monitoring operational performance

- Ensuring competence

- Managing digester biology

- Understanding feedstock

- Making the most of digestate

Next Steps

• July 2016 – end year

• Will be seeking feedback andactively engaging with individualorganisations and working groups.

Test the checklists

• July 2016 – throughout 2017

• Will entail devising suitableassessment criteria, working withUKAS and third party accreditationbodies.

Design the certification

scheme

• Intention is to start from summer 2017

• Will be looking for operators to helpus pilot the scheme.

Pilot the certification

scheme

Get Involved

• Stakeholder Meeting – this afternoon (15:00, Piazza Suite)

• Food Waste Operator Group

• Crop Operator Group

• Training, Safety and Environment Working Group

• Finance Forum

• Visit ADBA website

• AD & Bioresources News

• ADBA events

• Get in touch with Jess

Industry Best Practice Scheme for AD- an Environment Agency perspective

UK AD & Biogas 2016

Fran Lowe – Environment & Business Manager

The Environment Agency

Established in 1996 to:protect and improve the environment

promote sustainable development, using resources wisely

Main roles, environmental:regulator – scrapyards to nuclear power stations, farms to fishing licences, main regulator for waste-fed AD

operator – managing flood risk, responding to emergencies

advisor – independent, to Govt, LAs & others

The Environment Agency and AD

AD was a newly emerging industry (non water UK) in 2010 when we introduced standard rules for AD

AD often the best environmental option for certain biowastes

We have continued to support the growth of AD through appropriate regulation:

that reflects both risks and benefits to the environment

isn’t unnecessarily burdensome

is responsive to new developments and issues

20

What and how we regulate AD

Determine environmental permit applications and assessing compliance/enforcing against issued permits

Various types of environmental permits for waste-fed AD plants and combustion of biogas – on-farm, merchant, standard rules and bespoke, waste operations and installations

Light touch regulation - registered exemptions for smaller scale waste-fed facilities and RPS

Sewage sludge AD at STWs – currently only permit biogas combustion and co-digestion AD plants

Crop-fed and other non-waste AD plants – don’t currentlyregulate

21

Pollution incidents at permitted AD sites

The biowaste treatment sector has had the highest proportion of serious and

significant pollution incidents of any sector we regulate and AD has been the worst

performer.

22Anaerobic digestionCompostingTreatmentWWTW

2.6 3.7 9.0 21.9Pollution incidents per 100

permits for 2013,

3 year average of serious pollution incidents, by sector and normalised per 100 permits in the sector

Number of incidents

Number per 100 permits

All other FAR Sectors not shown have a 3 year average of 0.7 incidents per 100

permits or less and fewer than 15 incidents in total

70 6 9 3 0.3 0.3 54 1 33 6 2 0.3 43

0.3 0.8 0.8 0.9 1.0 1.1 1.3 1.4 1.5 1.6 1.9 2.6 7.0

3 y

ear

avera

ge 2

012 -

2014Most of these have been preventable – causes can be grouped under poor design,

construction, maintenance or management/competence

Best Practice Scheme

Promotes well built, well-managed, profitable AD plants

Helps improve the environmental performance of the AD industry, giving confidence to the public, investors and insurers, supporting further growth of AD

Complements our permitting approach for those sites we do regulate – permit conditions largely focus on the outcomes to be achieved, NOT How

We no longer produce comprehensive guidance on the ‘how to’ elements – a role for industry, best practice will help to fill the gaps; covering areas outside our remit

Help new entrants go into AD with their eyes wide open!

23

Best Practice scheme

Whole heartedly support the introduction of this new scheme

It is much needed

Phase 1 is a great start and we await phase 2 with anticipation

24

Best Practice from an Insurers Perspective

Carl Gurney

Renewable Energy Director

Jelf Group

Best practice | Page 26

over £3.7 million paid out in claims over the last 3 years

Environmental claims in excess of £800K over last 18 months

Continuing incidents means premiums will continue to rise and insurers will, if not already, pull out of the market

Claims and insurance industry trends

Best practice | Page 27

Continuing Claims

Poor Practice

No insurance

& no investment

Claims and insurance industry trends

Best practice | Page 28

Causes of

claims

Operator error

Poor design

Over foaming

Poor upkeep

Storms

Claims

Best practice | Page 29

Best practice

Best practice

ADBA guidance

Insurer involvement

Investor and stakeholder confidence

Better ROI

Best Practice Scheme

Insurer / Investor /

Stakeholder Confidence

Industry growth (safely!)

Best practice | Page 30

Conclusion

Food waste to renewable energy 31

ADBA Best Practice Guidance

David Woolgar

Food waste to renewable energy 32

Introduction

• David Woolgar Director of

Technology at Biogen

• Responsible for design and

commissioning farm, crop and

foodwaste plants over the past

10 years

• The best practice guidance is

based on ADBA colleagues

sharing the pain and learning

• Highlight very quickly some key

topics. Come back with

questions

Food waste to renewable energy 33

Specification

What do you want the plant to do

• Feedstocks – what types, how much, storage, processing

• Plant construction – tanks, pipework, buildings

• Gas usage – CHP, Heat, Biomethane

• Digestate usage – liquid, solid, biofertiliser, treatment

• Regulation – EA, Ofgem

Food waste to renewable energy 34

UK Legislation

UK legislation is specific

• EU suppliers may not be familiar with UK

legislation.

• England, Scotland, Wales and NI have different

rules.

• CE marked equipment meets harmonised

standards.

• Owner is responsible for compliant site

Food waste to renewable energy 35

Gas Safety

ATEX

ATEX is the overall EU regulation.

DSEAR

DSEAR is the UK regulation and covers defining

hazardous zones and formal risk assessment.

BS EN 60079

International standard covering definition of

hazardous zones and the design and installation of

appropriate equipment.

IGEM Guidance

There is not a lot of specific legislation or guidance

for biogas pipework design, however IGEM natural

gas guidance is applicable. There is specific

guidance for biomethane pipework

These are areas where expert advice is

recommended

Food waste to renewable energy 36

Lightning Protection

Lightning protection

Recent photos in press about AD plant that was struck by

lightning.

Key is good earth path from strike point

Guidance in BS 62305 – specialist area

Earthing

Earthing generally is important

for personnel safety and for plant safety

Not just the power circuits but the structures and pipework

Food waste to renewable energy 37

Maintenance

Maintenance

The AD plant will be working hard and will require to be

maintained. Most equipment suppliers will provide

training on their equipment. Develop a maintenance

schedule

Critical spares

These are items required for safe, compliant and

effective operation of the AD plant.

Identify key items, know how to get them quickly

Consider holding spares on site.

Food waste to renewable energy 38

Thank You

www.biogen.co.uk

QUESTIONS AND COMMENTS FROM THE FLOOR

CIRCULAR SOLUTIONS FOR

GLOBAL CHALLENGERS

THE FIFTH CARBON BUDGET AND THE

POLICIES NEEDED FROM THE UK

GOVERNMENT TO MEET IT

DR DAVID JOFFETEAM LEADER: BUILDINGS & INDUSTRY, COMMITTEE ON CLIMATE CHANGE

41

The fifth carbon budget and the policies needed from the UK

government to meet it

Dr. David Joffe

ADBA Conference

6 July 2016

42

The Climate Change Act sets a framework to drive change

Requirement that Government brings forward policies

Committee on Climate Change to monitor progress and suggest

changes

Carbon budgets

2050 Emissions Target

A toolkit

A monitoringframework

A pathway

A goal1

2

3

4

The Climate Change Act

43

The Committee recommended for the fifth carbon budget (2028-32) that emissions fall by 57% vs. 1990, on the path to a reduction by 2050 of at least 80% - the Government has accepted this

44

Progress reducing emissions since 2012 has been almost entirely due to the power sector

45

Electricity

Buildings

Transport

Industry

Non-CO2

Aviation & shipping

45

Further expansion and decarbonise mid-merit/peak

Low-carbon electrified heatCommercial Residential Hard-to-treat

Roll out low-carbon vehicles to fleet

More on-farm measures, F-gases, reduce waste and improve diet?

Efficiency

Decarbonise baseload

EV penetration up;Early H2 adoption

Efficiency

CCS, electrification and other fuel switching? Product substitution?

Efficiency

Efficiency on farms, divert waste from landfill

Operational measures, new plane/ship efficiency, whilst demand grows (though possibly constrained)

The broad story behind our scenarios to 2050

2010s 2020s 2030s 2040s

46

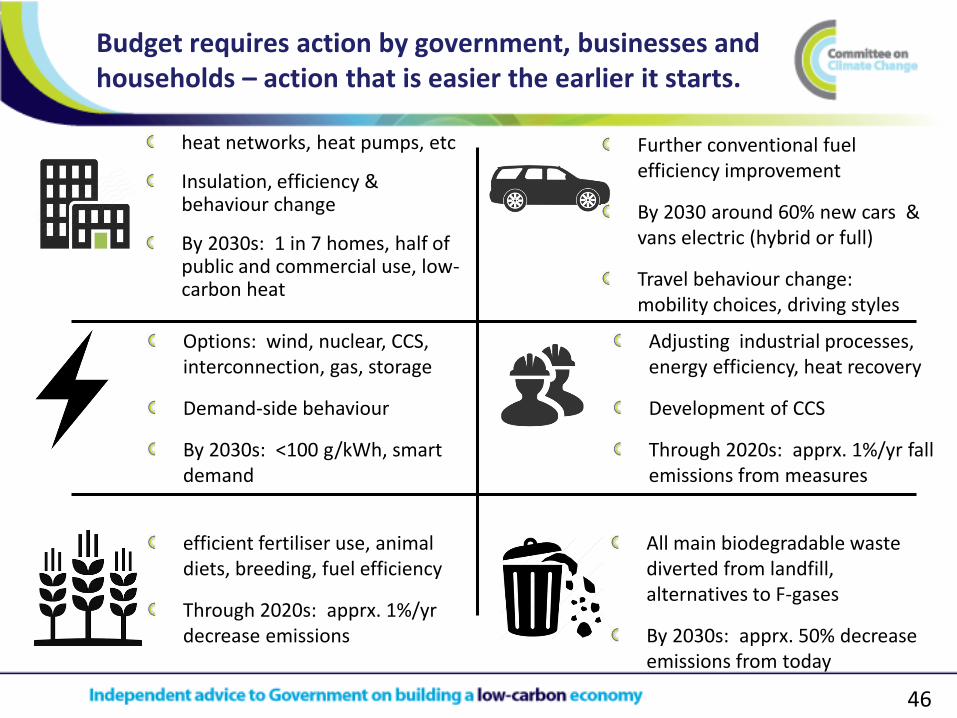

Budget requires action by government, businesses and households – action that is easier the earlier it starts.

heat networks, heat pumps, etc

Insulation, efficiency & behaviour change

By 2030s: 1 in 7 homes, half of public and commercial use, low-carbon heat

Further conventional fuel efficiency improvement

By 2030 around 60% new cars & vans electric (hybrid or full)

Travel behaviour change: mobility choices, driving styles

Options: wind, nuclear, CCS, interconnection, gas, storage

Demand-side behaviour

By 2030s: <100 g/kWh, smart demand

Adjusting industrial processes, energy efficiency, heat recovery

Development of CCS

Through 2020s: apprx. 1%/yr fall emissions from measures

efficient fertiliser use, animal diets, breeding, fuel efficiency

Through 2020s: apprx. 1%/yr decrease emissions

All main biodegradable waste diverted from landfill, alternatives to F-gases

By 2030s: apprx. 50% decrease emissions from today

47

Assessment of current policies against the cost-effective path to meet carbon budgets and the 2050 target

48

Why is there a policy gap?

In part the policy gap reflects mixed progress in developing the policy framework in those areas in the last year:

– Some areas have progressed, for example: funding available for offshore wind has been extended to 2026, for renewable heat to 2020/21 and for electric vehicles to 2018.

– There have been backward steps in other areas: cancellation of the Commercialisation Programme for carbon capture and storage (CCS), a reduction in funding for energy efficiency and cancellation of the zero carbon homes standard.

– Other priorities have not moved forward: no further auctions have been run or planned for the cheapest low-carbon generation (e.g. for onshore wind and solar in windy/sunny sites that are locally acceptable), there is no action plan for low-carbon heat or energy efficiency and there are no vehicle efficiency standards beyond 2020.

Given the need for progress across the economy, it is important that policy gaps are addressed in all areas.

49

Priority areas (1): Low-carbon heat

50

Priority areas (2): Transport through the 2020s

51

Priority areas (3): Power – carbon capture and storage and mature low-carbon generation

52

The Committee has a full work programme over the coming months

Post-Paris: net zero emissions and well below 2ºC

Deep dive on heat and energy efficiency, including consideration of the future of the gas grid

Implications of Brexit for the policy framework [may not be a stand-alone report]

Land use and agriculture – opportunities for climate adaptation and mitigation

53

Thank you for your attention

QUESTIONS AND COMMENTS FROM THE FLOOR

WHAT WILL BREXIT MEAN FOR BIOGAS?

MATT HINDLE, HEAD OF POLICY, ADBA

CHRIS HUHNE, STRATEGIC ADVISOR, ADBA

DAVID NEWMAN, PRESIDENT, ISWA

JONATHAN SCURLOCK, CHIEF ADVISOR, RENEWABLE ENERGY AND CLIMATE

CHANGE, NFU

NICHOLAS WHYTE & JULIE KJESTRUP, APCO WORLDWIDE

STUART HAYWARD-HINGHAM, TECHNICAL DIRECTOR, SUEZ

Brexit: the fall outThe implications of the 23 June 2016 referendum

UK AD & Biogas, Birmingham, 6 July 2016

Chris Huhne, Strategic Adviser, ADBA

Overview

Political uncertainty

Policy uncertainty

Economic uncertainty

What next?

Uncertainty and resolution

Political uncertainty over UK leadership and

policy options will slowly clear

Policy uncertainty could continue for some

time, as it depends on EU partners too

Recession likely, though more modest than

1992 or 2008

But AD is an essential part of domestic and

EU policy goals

Brexit effects

Worst ever two-day fall in sterling

More than £100 billion off share prices

Loss of UK’s AAA rating: now AA

Commercial property funds off 5 per cent

Residential property price mark-downs

HSBC: 1000 jobs to Paris; JP Morgan 4,000

Vodafone, Easyjet consider relocation in EU

Sharp rise in UK hate crimes

Sterling’s worst ever fall

Sterling volatility over time

British politics and Article 50

Continuity or radicalism? Theresa May is

continuity. Andrea Leadsom is safer Brexiteer.

Michael Gove is the radical.

Everyone will say respect the referendum, but

range of possible outcomes is EU membership

and Norway (limited immigration control) to WTO

(and full immigration control)

May knows more net immigration is from outside

the EU (188,000 last year) than inside (184,000)

Short-term: economic pressure

Average forecast for growth in 2017 down from 2.1

per cent to 0.3 per cent: recession by year end

Boards will defer investment, consumers defer big-

ticket spending, until outlook is clearer

Fall in pound to 31-year lows against dollar will

raise import prices and cut real incomes

Historic payments deficit of nearly 7% of GDP

Sterling constrains Bank of England rate freedom

AD? Public finance threat to RHI

Long-term: trade uncertainty

Half of UK trade with EU: trade determined by

distance and income

Best case: EEA/EU access to single market

Worst case: CET of 6.7% (+2% admin)

This matters to AD because of living standards

and the public finances (eg Renewable Heat

Incentive)

Openness also determines productivity growth

But most Brexit voters wanted barriers, not

openness

Single market boosts UK trade

Trade means lower prices

Timing

Speed resolves uncertainty, but may worsen long-

term outcome for the UK. Allow tempers to cool.

EU position: conclude two years of article 50

negotiations on withdrawal BEFORE trade deal

EEA/EU access only with free movement of labour

Uncertainty could last for 9 years (2 + 7) on

Canadian precedent

Can Germany, Scandinavia and Visegrad speed it

up and find more concessions on free movement?

Effects on AD deployment

AD could lose support of EU renewables target (15

per cent of UK’s PEC in 2020)

Waste directives also in the air

Fiscal weakness limits capacity to fund Renewable

Heat Incentive

Legislative overload of Whitehall

But fifth carbon budget is agreed, and in principle

provides a similar framework to EU targets

Favourable view of EU: contagion?

Summary

Business needs speed, but politics cannot deliver

British politics looks unstable and juvenile: House

of Cards meets Game of Thrones

Likely recession will increase Brexit remorse

Possible disintegration of EU: see bond markets

Limited room for EU fudge for fear of populism

Norway (40%), EU (20%), or WTO (40%)?

Economics is not a zero-sum game: all can lose

QUESTIONS AND COMMENTS FROM THE FLOOR

THE GLOBAL DRIVERS

FOR AD

ENERGY SYSTEMS-HOW BIG COULD ADS

ROLE BE?

CHRIS HUHNE, STRATEGIC ADVISOR, ADBA

HENRY FERLAND, CO-DIRECTOR, GLOBAL METHANE INITIATIVE

SECRETARIAT

MIKE MASON, CHAIRMAN, TROPICAL POWER

THE GLOBAL DRIVERS FOR

AD

WHERE DOES AD FIT IN THE FUTURE

GLOBAL ENERGY SYSTEMS?

CHRIS HUHNESTRATEGIC ADVISOR, ADBA

The future for biogasThe global and UK role for anaerobic digestion

UK AD & Biogas, Birmingham, 6 July 2016

Chris Huhne, Strategic Adviser, ADBA

Overview

COP 21 and 5th

carbon budgetTargets will

tighten

Short term problems,

long-term gains

Most important roles

for biogas

Paris COP 21

Goal is “well below” 2º warming and hope for 1.5º

Business as Usual is estimated at 3.6º to 4.5º

Estimated INDCs varies from 2.7º to 3.5º if fully

implemented

COP21 is a process, not a destination

So was 1987 Montreal Protocol on CFCs: first hard

evidence last week that ozone hole is closing

We do not have time: 5 to 10 years maximum

No silver bullet: need many actions to attain goal

EU carbon price since Paris

UK Climate Change Act

Climate Change Act 2008 mandates 80% cut in

emissions by 2050 (from 1990 levels)

Fifth carbon budget (2028 to 2032) recommended

by CCC in November: 1.725 MtCO2e

Acceptance by HMG on 30th June 2016

Demanding target assessed in annual reports by

independent Climate Change Committee

But any Act can be repealed and amended...

UK carbon emissions and targets...despite income drops

UK carbon emissions by sector

The benefits of biogas

Biogas turbines can generate electricity when and

where needed (despatchable power)

Power can be for baseload or for peak-lopping

Biogas in the grid can be stored cheaply through

pressure changes

Green biogas can be used in heating from grid

without retiring equipment

Biogas is one low carbon solution for HGVs

AD can help to decarbonise agriculture

Short term problems

EU target of 15% of energy consumption from

renewables by 2020 will no longer operate in UK

Major uncertainty for renewables organisations as

much less direct link with outcomes

Waste directives are EU law (like much else in the

environment)

DECC was relying on interconnectors to import

power: may be more difficult

Look at the alternative uses

Transport

Electricity generation (power)

Heat

Agriculture (either heat or power or both)

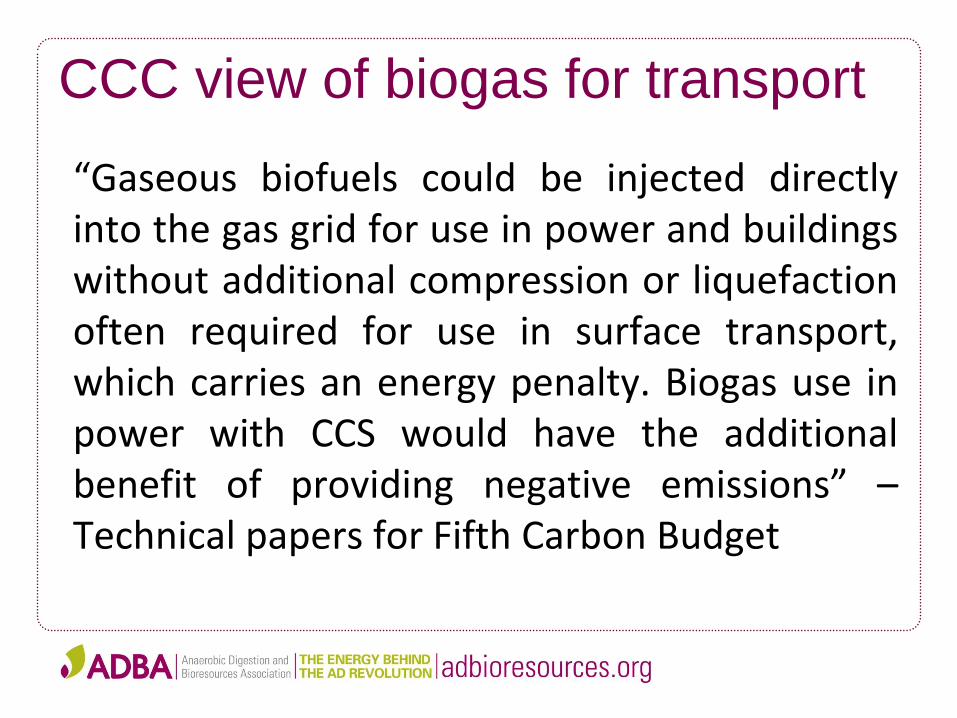

CCC view of biogas for transport

“Gaseous biofuels could be injected directlyinto the gas grid for use in power and buildingswithout additional compression or liquefactionoften required for use in surface transport,which carries an energy penalty. Biogas use inpower with CCS would have the additionalbenefit of providing negative emissions” –Technical papers for Fifth Carbon Budget

Remember the competition: solar

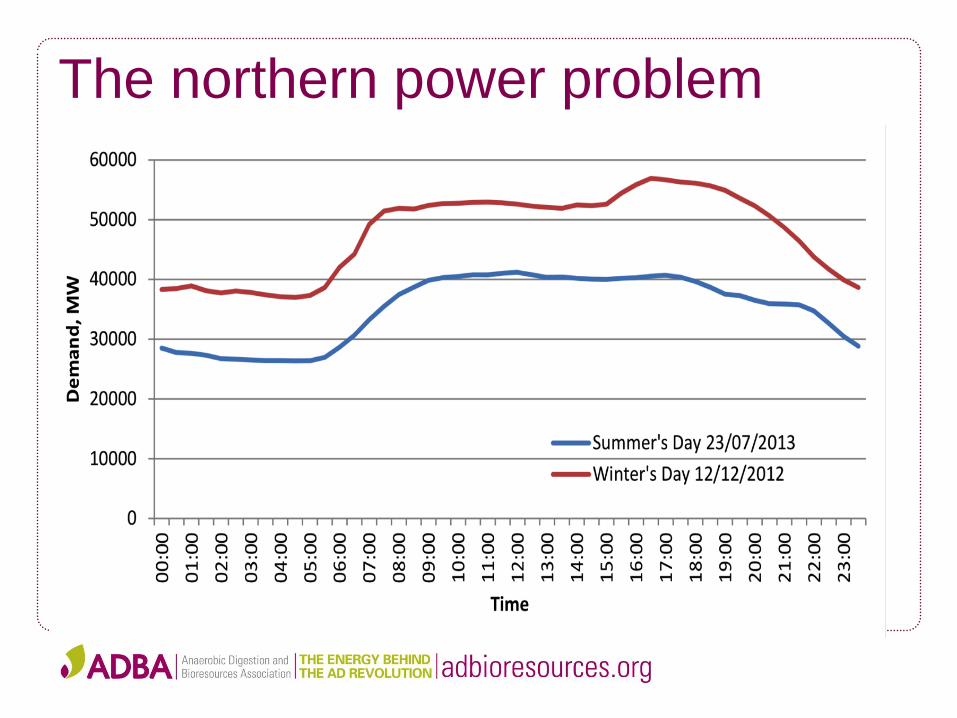

The northern power problem

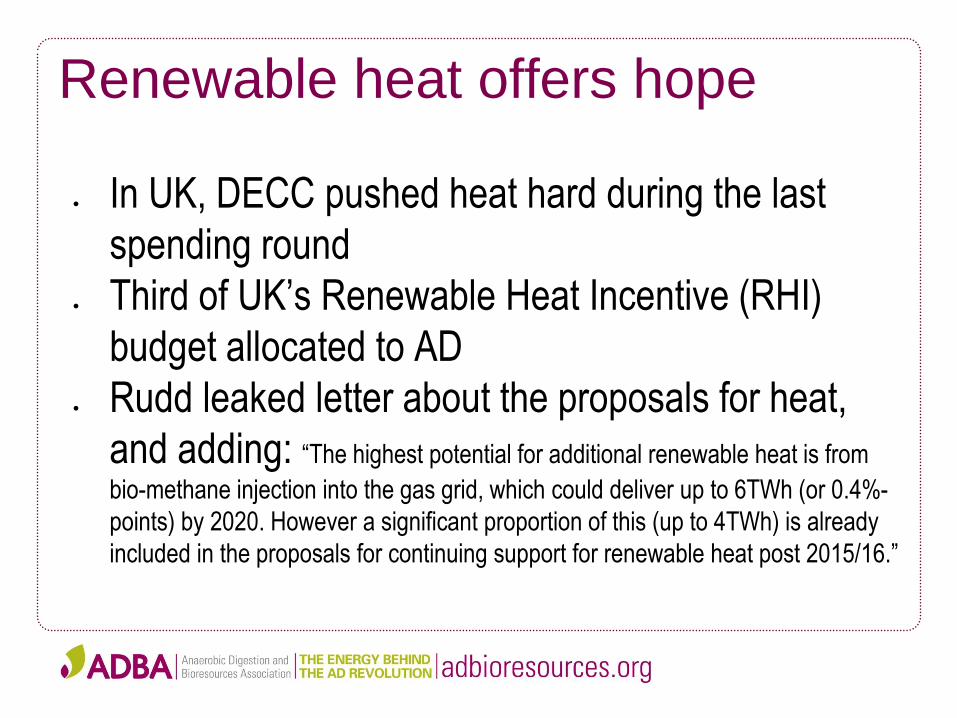

Renewable heat offers hope

In UK, DECC pushed heat hard during the last

spending round

Third of UK’s Renewable Heat Incentive (RHI)

budget allocated to AD

Rudd leaked letter about the proposals for heat,

and adding: “The highest potential for additional renewable heat is from

bio-methane injection into the gas grid, which could deliver up to 6TWh (or 0.4%-

points) by 2020. However a significant proportion of this (up to 4TWh) is already

included in the proposals for continuing support for renewable heat post 2015/16.”

UK case: agriculture

GHG from agriculture are 9.5% of total (2013)

Joint work with CCC and Irish equivalent (40%)

Projected fall from 53.5 MtCO2e in 2013 to 46

MtCO2e in 2030

2 MtCO2e from livestock diet, health and breeding

1.3 MtCO2e from manure management, energy

efficiency and on-farm AD

2.7 MtCO2e from cuts in N2O from crops through

better or less nitrous fertiliser

AD: making progress Ministers want farm decarbonisation, but

restrictions on crop AD

Third of RHI budget to AD

Movement on tariff guarantees

Increase in biomethane tariff

AD is always in MACC curves

But big uncertainties – EU renewables

targets for 2020, EU waste law, policy resets,

abolition of CCA

AD capacity in the UK

0

100

200

300

400

500

600

700

800

900

1000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

MW

e-e

Projected cumulative electrical-equivalent (electrical plus biomethane) capacity

Actual Projected 'High' Projected 'Low'

THE GLOBAL DRIVERS FOR

AD

UTILISING METHANE FOR ENERGY AND

MAXIMISING CARBON ABATEMENT

HENRY FERLANDCO-DIRECTOR, GLOBAL METHANE INITIATIVE SECRETARAIT

93

Global Methane Initiative Reducing Global Methane

Emissions – Biogas Approach

Henry Ferland, Co-Director of GMI

Administrative Support Group

UK AD & Biogas – July 6, 2016

94

Why Methane Matters

95

Mitigation Benefits

96

Targeted Sectors

GMI-targeted sectors contribute more than half of total global

methane emissions.

97

Partners

98

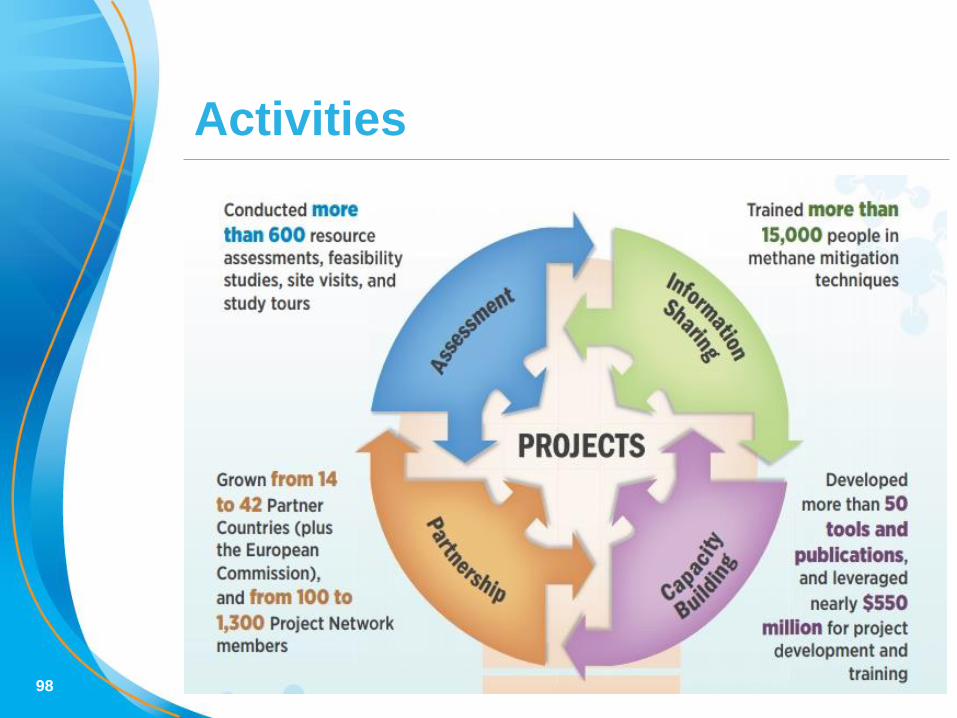

Activities

99

By 2017, GMI-supported projects are projected to yield

cumulative methane emission reductions of more than 430

MMtCO2e.

Accomplishments

MMTCO2e = Million metric tons of carbon dioxide equivalent, with methane GWP = 25

100

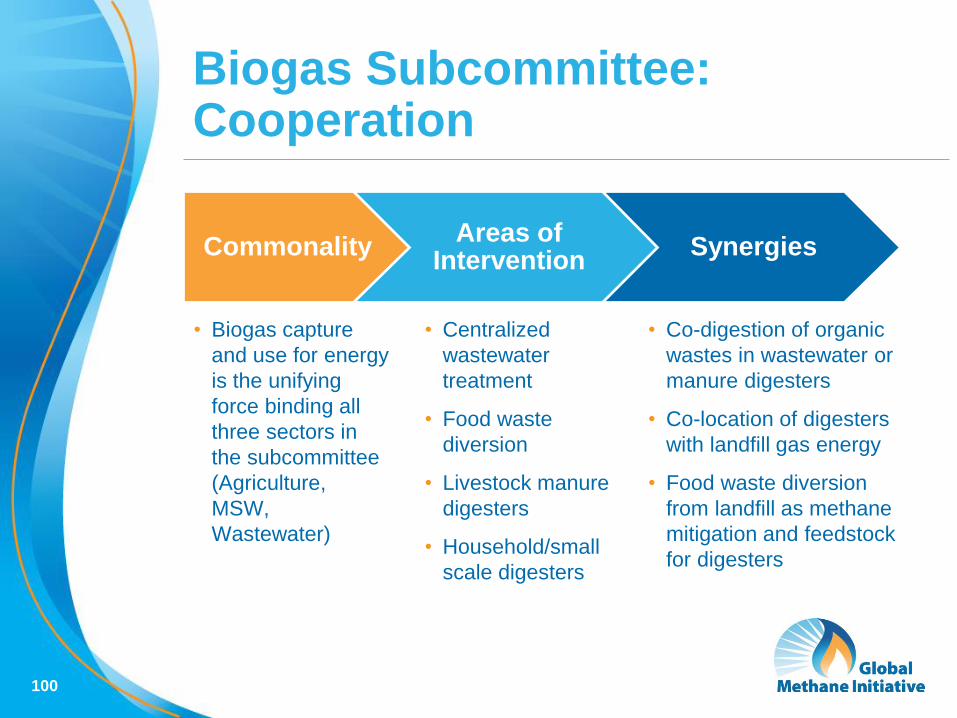

Biogas Subcommittee: Cooperation

CommonalityAreas of

InterventionSynergies

• Biogas capture

and use for energy

is the unifying

force binding all

three sectors in

the subcommittee

(Agriculture,

MSW,

Wastewater)

• Centralized

wastewater

treatment

• Food waste

diversion

• Livestock manure

digesters

• Household/small

scale digesters

• Co-digestion of organic

wastes in wastewater or

manure digesters

• Co-location of digesters

with landfill gas energy

• Food waste diversion

from landfill as methane

mitigation and feedstock

for digesters

101

Biogas Subcommittee:Sector Sources of Methane

Agriculture Municipal Solid Waste Municipal Wastewater

Livestock waste

management:

Anaerobic

management

of manure

• Anaerobic

decomposition of

organic waste

portion of municipal

solid waste

• Anaerobic

decomposition of

wastewater during

collection, handling,

and treatment.

102

Biogas Subcommittee:Sector Methane Reductions

Agriculture Municipal Solid Waste Municipal Wastewater

• Managing manure in

anaerobic digesters

or covered lagoons.

• Modifying how the

waste is treated, for

example:• Diverting organic

waste from

landfills to

anaerobic

digestion.

• Diverting organic

waste to

composting.

• Collecting landfill

gas and using it as

fuel.

• Modifying how

wastewater is treated,

for example:• Switching from a

latrine or septic

tank to an aerobic

treatment plant.

• Operating existing

plants more efficiently

• Installing anaerobic

digestion systems at

wastewater treatment

plants.

indicates options that have the potential to produce electricity

103

Biogas Subcommittee: Anaerobic Digestion and Biogas Use

104

Biogas Subcommittee:Renewable Energy from Biogas

Biogas from

animal waste

anaerobic digester

used as cooking

fuel (Philippines)

Biogas from

wastewater

sludge treated

and sold to gas

plant (Chile)

Biogas from a

landfill used in IR

heater (Bosnia

and Herzegovina)

105

Biogas Subcommittee: Emissions/Reductions in 2020

Based on data from EPA, 2013. Global Mitigation of Non-CO2 Greenhouse Gases: 2010-2030

Total from All Biogas Sectors:

2020 Total Estimated Emissions: 1,832 MMTCO2e

2020 Potential Emissions Reductions: 979 MMTCO2e

0 200 400 600 800 1000

Municipal Solid Waste

Wastewater

Manure Management

2020 Total Estimated Emissions and Potential Emissions Reductions, MMTCO2e

Potential Emissions Reductions

Total Estimated Emissions

106

Biogas Subcommittee: Energy Potential in 2020

-

2,000

4,000

6,000

8,000

10,000

12,000

Agriculture Municipal SolidWaste

Wastewater

2020 Potential Electricity Generation Capacity, MW

Total from All Biogas Sectors:

2020 Electricity Generation Capacity: 15 GW

Based on data from EPA, 2013. Global Mitigation of Non-CO2 Greenhouse Gases: 2010-2030

107

Future GMI/CCAC Work

GMI is enhancing its focus on building knowledge platforms

and developing policy guidance in the future.

– Less project directed work

Key opportunity to support GMI and CCAC Partner Countries

with their Nationally Determined Contributions (NDCs) to

include methane reduction as an important element of climate

mitigation strategy.

Work jointly with Ag, MSW, Oil and Gas Initiatives and CCAC

SNAP initiative to target our efforts on joint knowledge platform

and policy guidance in particular sectors.

The GMI Biogas Subcommittee is currently developing a work

plan to determine future work products and focus areas.

108

Of the 188 country Nationally Determined Contributions

(NDCs) developed, 27 have specifically addressed short-lived

climate pollutants (SLCPs) and integrated mitigation co-

benefits into their submissions

Many others included projects and activities directly relevant

to the work of GMI, CCAC, and SLCP reductions

64 countries included activities in the Waste Sector, nine are

in GMI Partner Countries:

China Mongolia

European Union Turkey

Ghana United States

Japan Vietnam

Jordan

Biogas Opportunities: NDCs

109

Thank You!

GMI maintains an extensive website at:

www.globalmethane.org

Social Media:

ASG Co-Directors:– Monica Shimamura

Phone: (202) 343-9337

Email: [email protected]

– Henry Ferland

Phone: (202) 343-9330

Email: [email protected]

110

APPENDIX

111

MSW Initiative Synergies Example

GMI CCAC Synergy

Country-focused

approach

City-focused approach Coordination can help scale

up action in both national

and municipal jurisdictions

Pipeline of projects

and tools

development

Small scale projects

and tool development

Joint tools development,

financing assistance, policy

guidance

Focus on methane

and biogas cross-

sector solutions

Focus on source

separation and basic

best practices

Anaerobic Digesters, cross-

sector solutions, methane

abatement and reduction

ideas.

New Biogas

Subcommittee

(national policy

discussions)

Regional workshops

(targeted capacity

building)

Future joint work on

workshops, policy guidance

and cross-sector biogas

solutions

112

This Nicaraguan wastewater treatment

plant has an anaerobic digester which:

– Reduces 2,520 MtCO2e/year of emissions

– Has electricity capacity of 655 kW

Biogas Project Example: Managua WWTP

113

Biogas PotentialCountry Example: Mexico

0 20 40 60

Municipal SolidWaste

Wastewater

Agriculture

2020 Potential Emissions Reductions, MMtCO2e

Total from All Biogas Sectors:

2020 Emissions Reductions: 75 MMtCO2e

2020 Electricity Generation Capacity: 944 MW

- 400 800

Municipal SolidWaste

Wastewater

Agriculture

2020 Potential Energy Generation Capacity, MW

114

Global Mitigation of Non-CO2 Greenhouse

Gases: 2010-2030

https://www3.epa.gov/climatechange/Downloads/EPAactivities/MAC_Report_2013.pdf

Biogas Subcommittee:Emissions Reductions and Energy

THE GLOBAL DRIVERS FOR

AD

TURNING AD INTO A GLOBAL PLAYER

MIKE MASONCHAIRMAN, TROPICAL POWER

3rd Generation Bioenergy

Moving from ‘fuel OR food’ to

‘fuel and MORE food’

The case for Biogas

Ethanol Methane

Feedstock (kg) 1,000 1,000

Gross fuel yield (kg) 227

Gross fuel yield (m3) 327

Gross Energy Yield (MJ/tonne) 5,176 10,791

Useful energy @40% efficiency (MJ) 2,070 4,316

Surplus/(Parasitic) electricity (MJ) 670 (302)

NET USEFUL ENERGY (MJ/tonne) 2,740 4,014

Relative yield 100% 143%

Maximising the value of Biogas

Three challenges

• Get the cost of bioenergy low enough to compete with coal

• Get the scale up so it is large enough to matter

• Make sure it adds to food security and doesn’t detract from it

Biogas – the key technology

• Massive potential to reduce costs

• Biogas is a cheaper and more efficient energy store than batteries. Perfect for grid or off-grid applications

• Perfect to hybridise with solar – use gas when the sun doesn’t shine.

Cutting the cost – bio-mimicry of cows

• A cow can digest 150 kg of biomass per m3 of rumen per day

• An AD plant can digest 4-6 kg of biomass per m3 of reactor per day

• Both use the same bacteria and chemistry

• Mimicking the cow could make digesting agricultural waste as cheap as burning coal

Getting the scale up

• Use agricultural waste not energy crops on good land ≈4 bn tonnes/yr at 1.2MWh/tonne

• Use hyper-water efficient CAM plants. There are ≈3 bn ha of under-used semi-arid land

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Oil AgResiduesHydro Gas CAMPlants Coal

Annualgen

era

onPWh/yr

Solarcomplement

AD

• Hybridise AD with solar to make large scale solar grid friendly. Biogas is a cheap energy store, batteries are expensive

Fuel and MORE food

• The liquid that comes out from AD is warm and nutrient rich

• Lemna are the world’s fastest growing plants, and will grow on AD digestate

• Lemna can produce 10x as much protein/ha as soy beans

• With CAM plants as the crop this can happen in semi-deserts

So how can we do it?

Or “why is a cow so unreasonably good at cellulolysis?”

Saliva – a key?

Cow

Cow

Sheep

Kangaroo

Human

0%

100%

200%

300%

400%

500%

600%

HCO3- PO4 pH N Na K Ca Mg Cl

Rela

veconcentra

ons-nromalised

tosheep

Sharma’s experiment

0%

20%

40%

60%

80%

100%

120%

0 20 40 60 80 100 120 140 160 180

Rela

verateofgasevolu

onperunitsurfacearea

Rela vesurfaceareapergramofpar cles(1forlargest,157forsmallest)

Gasevolu onperunitofsurfacearea,asf(par clesize)

Ini alreac onrate

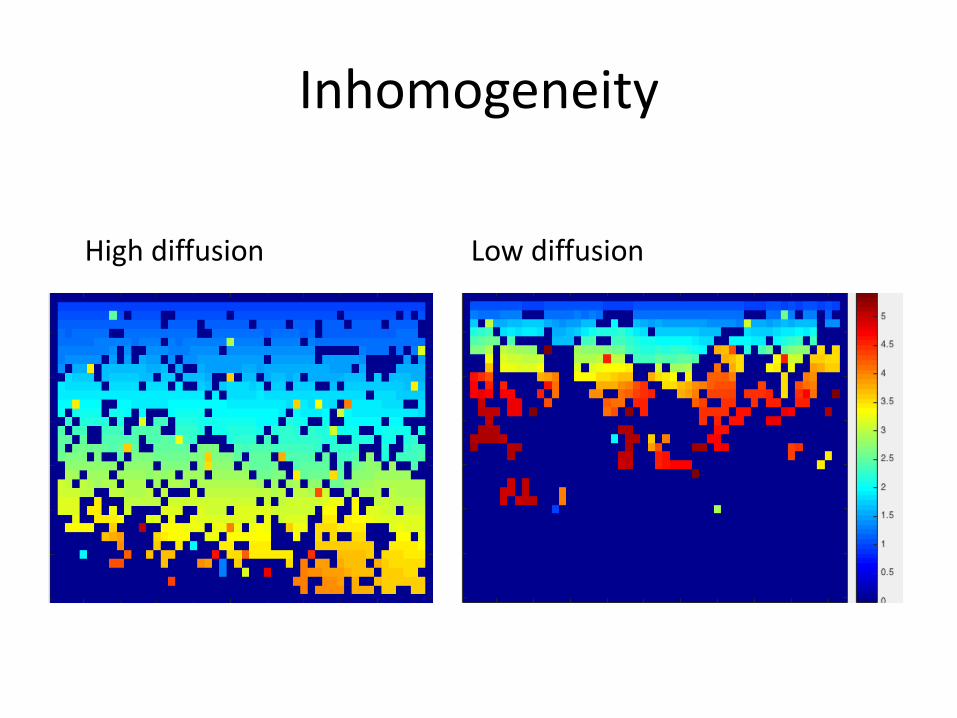

Biofilms are heterogeneous and ever changing

Inhomogeneity

High diffusion Low diffusion

Effect of Boundary Layers.

QUESTIONS AND COMMENTS FROM THE FLOOR

THE GLOBAL DRIVERS FOR

AD

RECYCLING NUTRIENTS AND SAVING

FOOD WASTE

CHARLOTTE MORTON, CEO, ADBA

MARK VARNEY, DIRECTOR OF FOOD, FARESHARE

DR RICHARD SWANNELL, DIRECTOR OF SUSTAINABLE FOOD SYSTEMS,

WRAP

THE GLOBAL DRIVERS FOR

AD

DELIVERING THE FOOD EFFICIENCY

FRAMEWORK

MARK VARNEYDIRECTOR OF FOOD, FARESHARE

FareShare is a UK-wide charity fighting hunger and

food waste. We redistribute surplus food to

frontline charities and community groups that

support vulnerable people.

Food Poverty in the UK

people struggle to afford a meal –

equivalent to the entire

population of London(Voices of the Hungry, Food & Agriculture Organisation

of the United Nations, 2016)

people are destitute - meaning they

cannot afford essentials such as food (Destitution in the UK, Joseph Rowntree, 2016)

8.4

million

1.3

million

How FareShare Works

FareShare in the CommunityFareShare redistributes food to a wide

range of charities and community

groups across the UK.

• Lunch clubs for older people

• Breakfast clubs for disadvantaged

children

• Homeless hostels

• Domestic violence refuges

Partnerships and collaboration with a

number of Local Authorities across the

UK in a broad range of ways

• Access to storage and warehousing

• Hosting “Local Collection Points”

• Collaborating on food provision for

vulnerable people

FareShare’s Work in 2016

Food Surplus in the UK Food Supply Chain

Farms

Processing & Manufacture

Wholesale & Distribution

Retail

Typic

al Pro

duct

Lif

e R

em

ain

ing Good life

7 – 28 days

5 – 30 days

1 – 3 days

100,000 – 500,000**

300,000+ locations

At least 160 000*

2,128 Large locations

80– 120 000**

1,000+ locations

47-110 000*

30 – 40,000 locations

Tonnes Surplus

* Quantification of food surplus, waste and related materials in the grocery supply chain, WRAP, 2016

** FareShare estimates

Supporting the food industry to

follow the Food Use Hierarchy

Funding support to help ensure the Food Use

Hierarchy is respected…?

Food businesses are

encouraged to take

“reasonable steps”

to follow the waste

hierarchy.

But it is often

neither cheaper nor

easier to do so for

many large food

manufacturers

Our aim is to grow the

volume of surplus food

that is redistributed to

charity to

100,000 tonnes

per yearand save the voluntary

sector > £150m per

year

Industry Testimonials

“They have immaculate codes of

practice. I kind of refer to FareShare

as a social distributer, a partner, it’s

not someone who takes our waste,

they are a means by which we fulfil

one of our commitments to society”

Bruce Learner - Kellogg Europe

“No surplus food from our stores that can

be eaten should go to waste - this will help

to provide millions of meals to feed people

in need. Helping to fight food waste with

FareShare FoodCloud is, undoubtedly, one

of the things I’m most proud of at Tesco.”

Dave Lewis - Tesco

“Yes, supporting FareShare was

initially a decision from the

heart, it seemed the right thing

to do, but we’ve quickly learned

that our involvement has helped

us to be a better business and it

is something that all of those

involved are very proud to be a

part of.”

Chris Mack - Fresca Group

“You might just be surprised

how simple it can be to turn

your waste into something that

delivers so much more for so

many people.”

Suzie McIntyre - Kettle Produce

“The best commercial decision I can make

with that waste product that I cannot sell is

to absolutely donate it to charity.”

Mike Coupe - Sainsbury’s

THE GLOBAL DRIVERS FOR

AD

AD AND WASTE – WHY SHOULD AD BE AT

THE HEART OF ALL WASTE RECYCLING

INITIATIVES

DR RICHARD SWANNELLDIRECTOR OF SUSTAINABLE FOOD SYSTEMS, WRAP

AD & Waste – why AD is key to food waste recycling

Richard Swannell

Director of Sustainable Food Systems

@R_Swannell

6th July 2016

WRAP’s

vision is a

world in which

resources

are used

sustainably

WHAT WRAP DOES

Research & evidence

Collaboration through voluntary

agreements

CampaignsGrant-

making & investment

Evaluation of impact

HOW WRAP WORKS

© WRAP 2016

WRAP works

with governments,

businesses and

communities to deliver

practical solutions to

improve resource

efficiency

By 2030 the world will need 40-50% more water, food and energy. Interdependence will increase volatility. More energy needs more water, more food and water need more energy. To meet those needs, business as usual will not be an option – we require business unusual.

Peter Voser

CEO

Royal Dutch Shell

Why do we need to act?

www.wrap.org.uk/foodquantification

The opportunityPost-farm gate food waste in UK

7.0 mt

1.7 mt

0.2 mt

0.9 mt0.1mt 0.02 mt

Tonnage (mt)

Household

Manufacturing

Retail

Hospitality & food service

Food waste in litter

Wholesale

AD growth to 2016

Sources of feedstock

Driving

Change

Opportunities in household

• Preventing food remains priority,

• Almost 3 Mt is unavoidable

• 40% of UK local authorities do not collect food

waste

• Only 12% of UK food waste is recycled by

local authorities

Helping to increase food waste recycling

• Updated WRAP food waste collections guide

for local authorities

• Refreshed Recycle Now communications

materials

• Improved householder engagement in

collections

• Greater consistency in household recycling

collections

Food Waste Recycling Action Plan

Aims to:

• Increase the amount of food waste collected

• Provide long term sustainable feedstocks for operators

Food Waste Recycling Action Plan

Increases capture of food waste…

Benefits to treatment plant operators from profit made

from increased feedstock

Benefits to local authorities from avoided residual

disposal costs

Find out more at the launch of the

Food Waste Recycling Action Plan,

UK AD & Biogas 2016, 1000 tomorrow

www.wrap.org.uk/foodwasterecycling

Supporting market development

• DC-Agri – supports the confident use of digestates by

farmers and growers as renewable fertilisers

• Increased focus on sustainable soil management

• More precision farming

• Adding more value to products

… delivered face-to-face

training to

3,526 people, increasing farmer

awareness of digestate and

it’s fertiliser value…

… and produced

training materials and

resources, including the

bulletins that have been

downloaded over

6,000times.

Conclusion

• Need to drive improvements in food

system sustainability

• Driving a more resource efficient more

circular approach will drive:

• Less material inputs

• Less waste

• More recycling and more innovative

uses of collected waste

Thank you

WRAP

Second Floor,

Blenheim Court,

19 George Street,

Banbury,

OX16 5BH

UK

www.wrap.org.uk

Dr Richard Swannell

@R_Swannell

+44 (0)1295 819900

QUESTIONS AND COMMENTS FROM THE FLOOR

THE GLOBAL DRIVERS FOR

AD

FARMING, SOIL AND FOOD SECURITY –

FEEDING THE WORLD AND FARMING

SUSTAINABLY

CHARLOTTE MORTON, CEO, ADBA

GUY HILDRED, FARMER, GREEN GAS OXON

DR STEPHEN RAMSDEN, UNIVERSITY OF NOTTINGHAM

THE GLOBAL DRIVERS FOR

AD

THE ROLE OF ENERGY CROPS IN

SUPPORTING FOOD SECURITY

GUY HILDREDFARMER, GREEN GAS OXON

Food Security:

a farmer’s view

Guy Hildred

Background

2 MW equivalent AD plant gas to grid

Fed on crops and some pig slurry

6,000 arable acres and 2,000 ewes on

1,500 acres

Degree in mechanical engineering

Land use pressures

Food

Medicinal

Fibre

Biomass

Leisure

Energy

Environment

Housing and infrastructure

Commodity volatility

1992 wheat price was £100 per ton. 2016

wheat price is…. £100 per ton

But price ranged in same period from £59

to £212 per ton

Energy crops help reduce this volatility

Increasing demand when prices are low

Suppressing demand when prices are high

Encourages investment

Soil health

Organically derived fertilizers

More varied cropping

Compaction

Erosion

Ignorance

Food versus fuel

Four crops in three years

Two energy

Two food

Digestate gives huge saving in GHG

A fuel crop is just another land use

Which is more important?

THE GLOBAL DRIVERS FOR

AD

SUSTAINABLE FARMING PRACTICES AND

AGRICULTURAL ECONOMICS

DR STEPHEN RAMSDENASSOCIATE PROFESSOR IN MANAGEMENT AND DIRECTOR OF UNIVERSITY

FARM, FACULTY OF SCIENCE, UNIVERSITY OF NOTTINGHAM

Sustainable Farming Practices and Agricultural Economics

Dr Stephen RamsdenSchool of Biosciences

University of Nottingham

Overview

1. What is Agricultural Economics?

2. Sustainable farming

3. The components of a sustainable system

4. Lessons and conclusions

What is Agricultural Economics?

http://onlinelibrary.wiley.com/journal/

10.1111/(ISSN)1477-9552

http://www.aes.ac.uk/

What is Agricultural Economics? In the UK, a Society and a Journal

What is Agricultural Economics?

• How to allocate scarce resources (land) productively and efficiently

• Where are the trade-offs?

• Agri-environment (physical, biological)

• Understand markets: farmers are price takers (and sometimes risk averse) and unit cost reducers (for commodities)

• Better policy (“value for money” – David Pannell)

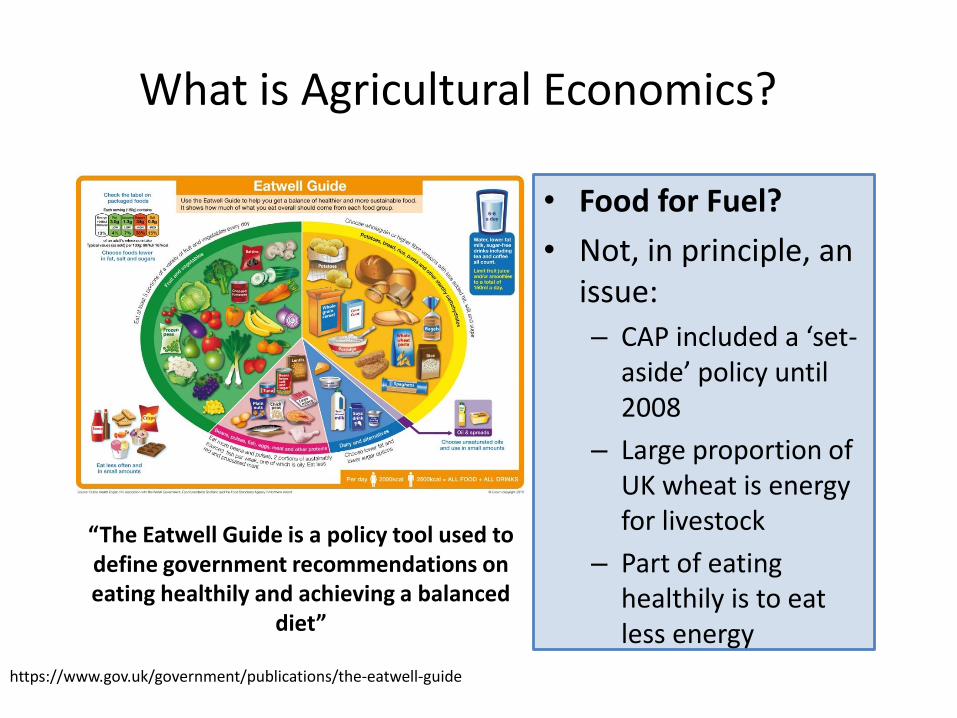

• Food for Fuel?

• Not, in principle, an issue:

– CAP included a ‘set-aside’ policy until 2008

– Large proportion of UK wheat is energy for livestock

– Part of eating healthily is to eat less energy

What is Agricultural Economics?

https://www.gov.uk/government/publications/the-eatwell-guide

“The Eatwell Guide is a policy tool used to define government recommendations on eating healthily and achieving a balanced

diet”

• Food for Fuel?

• Not, in principle, an issue:

– More diversified portfolio (risk)

– Miscanthus fertiliser and sprays: £25/ha

– Winter wheat fertiliser and sprays: £480/ha (Nix, 2015)

What is Agricultural Economics?

Crop Diversification at the University of Nottingham Farm

+ Environment- Environment

× 2×

× 1

×

× 𝐹𝑎𝑟𝑚𝑠:1 = Organic?

2 = Conventional?

× 𝐸𝑓𝑓𝑖𝑐𝑖𝑒𝑛𝑡 𝐹𝑎𝑟𝑚𝑠?

Greater productivity in both ‘E’ and ‘P’

Productivity and Efficiency

𝑃𝑟𝑜𝑑𝑢𝑐𝑡𝑖𝑜𝑛Possibility

Frontier

Production

𝑃𝑟𝑜𝑑𝑢𝑐𝑡𝑖𝑜𝑛Possibility

Frontier

Yield 14.50 t/hacv Kielder Sown 14th Sept

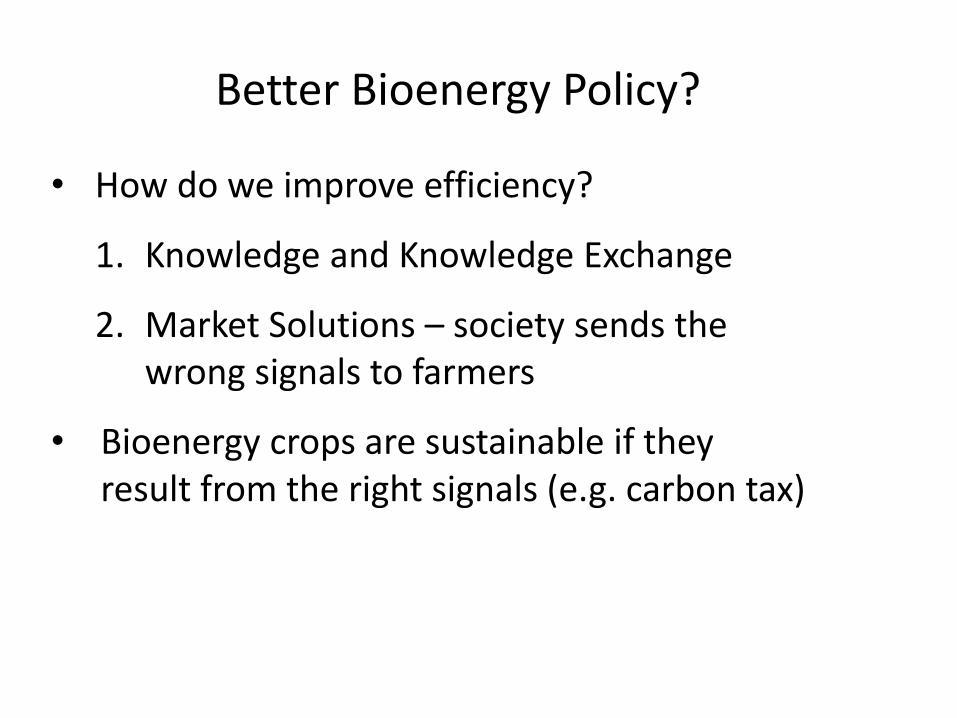

• How do we improve efficiency?

1. Knowledge and Knowledge Exchange

2. Market Solutions – society sends the wrong signals to farmers

• Bioenergy crops are sustainable if they result from the right signals (e.g. carbon tax)

Better Bioenergy Policy?

Sustainable farming –some example

sustainable intensification metrics

for cereal farms

Winter Wheat, 50.9%

Winter Oilseed Rape, 20.6%

Sugar Beet , 9.9%

Beans, 3.6%

Spring Barley , 2.7%

Winter Barley, 2.5%

Spring Wheat, 1.2%

Legumes and Potatoes, 0.9%

Other, 7.7%

Sample Cereal Farms: Land Use

0

5

10

15

20

25

30

35

40

0 5 10 15 20 25 30 35 40Nit

rate

Lo

ss k

g p

er

ha

Farm

Water Quality

Not so

good

Better

Nutrient Loss: N everywhere

• Nitrate

– Indicator of water quality

• Nitrous Oxide

– Indicator of global warming

• Ammonia

– Indicator of air quality

𝑵𝑶𝟑−

𝑵𝟐O

𝑵𝑯𝟑

0

2000

4000

6000

8000

10000

12000

14000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36

Co

st p

er

farm

£

Farm (ranked by cost)

Cost of N loss to the farmer

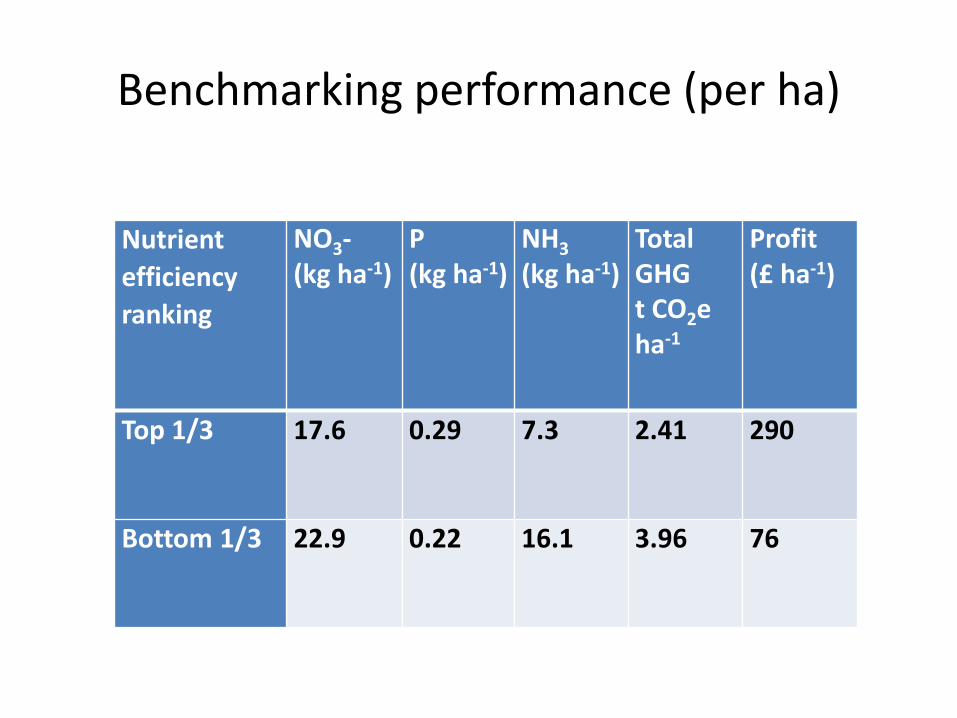

Benchmarking performance (per ha)

Nutrient

efficiency

ranking

NO3-(kg ha-1)

P(kg ha-1)

NH3

(kg ha-1)Total GHG t CO2e ha-1

Profit (£ ha-1)

Top 1/3 17.6 0.29 7.3 2.41 290

Bottom 1/3 22.9 0.22 16.1 3.96 76

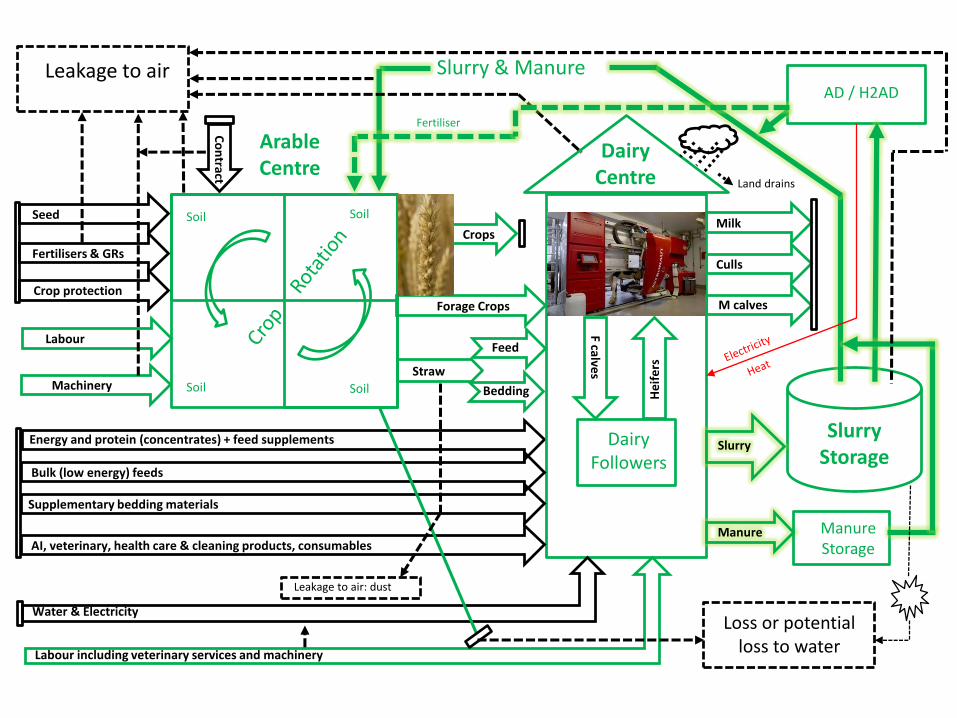

The components of a sustainable agricultural

system

Forage Crops

Crops

Arable Centre

Energy and protein (concentrates) + feed supplements SlurryStorage

AI, veterinary, health care & cleaning products, consumables

Bulk (low energy) feeds

Machinery

Labour

Crop protection

Fertilisers & GRs

Seed

Water & Electricity

Supplementary bedding materials

Labour including veterinary services and machinery

Straw

Feed

Bedding

Milk

Culls

M calves

DairyFollowers

F calves

He

ife

rs

Slurry

DairyCentre

Co

ntract

Manure ManureStorage

AD / H2AD

Slurry & Manure

Loss or potential loss to water

Leakage to air

Leakage to air: dust

Soil

Soil

Soil

Soil

Fertiliser

Land drains

How do we cultivate in England? Reduced Tillage (RT)

• Survey: 249 English arable farmers

• 32% of arable land was established under RT

• 46% of farms using some form of RT

• Main crops: wheat and oilseed rape

• How ‘reduced’ is reduced?

Cultivations and Drilling

‘Reduced Cultivation’

1 pass with 3m ‘Sumo’ discs and tines1 pass with 5m ‘Vaderstad Carrier’ discs

1 pass with 6m ‘Horsch Sprinter’ seed drill

Photos courtesy of James Beeby

Soil Use and Management

Volume 32, Issue 1, pages 106-117, 11 DEC 2015 DOI: 10.1111/sum.12241

http://onlinelibrary.wiley.com/doi/10.1111/sum.12241/full#sum12241-fig-0002

Tillage depths still quite deep with RT

Effects of Reduced Tillage: yields, costs and margins

Soil Use and Management

Volume 32, Issue 1, pages 106-117, 11 DEC 2015 DOI: 10.1111/sum.12241

Put RT into a (simplified!) model

Zero Tillage – lower emissions per unit of biomass produced by profit maximising farm…

MAX PROFIT Conventional Tillage Zero Tillage

Net energy (GJ farm− 1) 25,700 28,000

GHG emissions (t CO2-eq farm− 1)

1,767 1,567

Kg CO2-eq GJ − 1 69 56

MIN EMISSIONS Conventional Tillage Zero Tillage

Net energy (GJ farm− 1) 20,900 22,400

GHG emissions (t CO2-eq farm− 1)

764 639

Kg CO2-eq GJ − 1 37 29

… but greater scope when farm objective = minimise emissions

Agricultural Systems 146, 91-102. 10.1016/j.agsy.2016.04.005

Lessons and Conclusions

Sustainable Farming Practices- what can we learn from Ag Econ

1. There is scope to become more sustainable –e.g. RT

2. We need ways of measuring what is sustainable…

3. … and we need models (= understanding) of what happens when we intervene (there will be trade-offs)

Forage Crops

Crops

Arable Centre

Energy and protein (concentrates) + feed supplements SlurryStorage

AI, veterinary, health care & cleaning products, consumables

Bulk (low energy) feeds

Machinery

Labour

Crop protection

Fertilisers & GRs

Seed

Water & Electricity

Supplementary bedding materials

Labour including veterinary services and machinery

Straw

Feed

Bedding

Milk

Culls

M calves

DairyFollowers

F calves

He

ife

rs

Slurry

DairyCentre

Co

ntract

Manure ManureStorage

AD / H2AD

Slurry & Manure

Loss or potential loss to water

Leakage to air

Leakage to air: dust

Soil

Soil

Soil

Soil

Fertiliser

Land drains

References and further reading

• BUCKWELL et al., 2014. The Sustainable Intensification of European Agriculture. A review sponsored by the RISE Foundation. http://www.ieep.eu/assets/1404/111120_BROCH_SUST_INTENS_DEF.pdf.

• GLITHERO, N., RAMSDEN, S.J. and WILSON, P. 2012. Farm systems assessment of bioenergy feedstock production: Integrating Bio-economic models and Life Cycle Analysis approaches, Agricultural Systems 109, 53-64. 10.1016/j.agsy.2012.02.005

• GLITHERO, NJ, WILSON, P and RAMSDEN, SJ, 2015. Optimal combinable and dedicated energy crop scenarios for marginal land, Applied Energy 147, 82-91. 10.1016/j.apenergy.2015.01.119

• PANNELL, D. 2003. Value for Money in Environmental Policy and Environmental Economics. http://ageconsearch.umn.edu/bitstream/146501/2/WP130004.pdf

• TOWNSEND, T.J., RAMSDEN, S.J. and WILSON, P. 2015. How do we cultivate in England? Tillage practices in crop production systems, Soil Use and Management 36, 106-117. 10.1111/sum.12241

• TOWNSEND, T.J., RAMSDEN, S.J. and WILSON, P. 2016. Analysing reduced tillage practices within a bio-economic modelling framework, Agricultural Systems 146, 91-102. 10.1016/j.agsy.2016.04.005

QUESTIONS AND COMMENTS FROM THE FLOOR

THE GLOBAL DRIVERS FOR

AD

OPPORTUNITIES IN A GLOBAL MARKET

DR SARIKA JAIN, MARKET RESEARCH ANALYST, ADBA

PATRICK SERFASS, AMERICAN BIOGAS COUNCIL

JAKE DEBRUYN, ONTARIO MINISTRY OF AGRICULTURE

JORGE ANTONIO HILBERT, NATIONAL AGRICULTURAL TECHNOLOGY

INSTITUTE

DIARMID JAMEISON, SLR CONSULTING

CONRAD BURKE, DUPONT INDUSTRIAL BIOSCIENCES

LORENZO MAGGIONI, CIB

EDUARDO GRIFFONI, THAIS OLIVERIA, FCO

THE GLOBAL DRIVERS FOR

AD

AN OVERVIEW OF GLOBAL AD MARKET

POTENTIAL AND ITS DRIVERS

DR SARIKA JAINMARKET RESEARCH ANALYST, ADBA

GLOBAL AD MARKET

POTENTIAL AND ITS DRIVERS

Dr. Sarika JainMARKET RESEARCH ANALYST, ADBA

Global Overview

• Established as a renewable energy generation technology

• Benefits beyond electricity production recognised –

greenhouse gas abatement, waste management, sanitation,

vehicular fuel, domestic cooking fuel,

• Waste based potential (Animal manure, human waste and

food waste) - £150 billion or installed capacity of 300GW.

Animal Manure• Global livestock is responsible for 14.5% of all anthropogenic greenhouse gas

emissions

• Role AD can play:

─ Greenhouse gas (GHG) abatement AD can reduce the methane and nitrous

oxide emissions significantly from manure storage and fertiliser production.

─ Women empowerment, indoor quality and health By substituting the

traditionally used biomass as domestic fuel, biogas can have multiple social

benefits in the developing countries

• There is a market potential of £133 billion on an annual basis with a much larger

environmental and social impact

• Special mention: Micro-digesters in India, China, Bangladesh and other emerging

markets and the large scale digesters at US dairy farms.

Food Waste• World food production: 4 billion tonnes p.a. of which a third is wasted or lost.

• Role AD can play:

─ Pressure on the planet– Digesting food waste aids in nutrient recycling,

reduction of emissions and thereby reducing the pressure on the planet.

─ Waste management –Food waste often ends up in a landfill or with municipal

solid waste causing emissions.

─ Energy generation – Food waste with its high calorific value can be digested

to produce electricity, heat or upgraded biogas and also make digestion of

other feed stocks more feasible.

• Market potential for digestion of food waste is £15 billion

• Special mention: South Korea food collection and disposal system

Human waste• Out of a population of 7 billion people, 2.4 billion people don’t have access to

improved sanitation facility. Of which 950 million people still practice open

defecation.

• Role AD can play:

─ Sanitation: community based toilets that are connected to a digester. The

biogas produced can be used as fuel or used to electrify the facility

─ Wastewater treatment plants: Improving the economics of operational WWTP

by covering some part of the electricity and heat requirements.

• Market potential of £700 million with a much larger social impact.

• Special mention: Co-digestion of food waste with wastewater in the US

Energy generation potential

Drivers• GHG commitments

• Regulatory support

─ Feed in tariffs

─ Renewable Heat Incentive

─ Subsidies

─ Mandatory renewable fuel mix

• Waste management

• Social drivers like domestic fuel, sanitation

THE GLOBAL DRIVERS FOR

AD

INSIGHT INTO UNITED STATES OF

AMERICA

PATRICK SERFASSAMERICAN BIOGAS COUNCIL

US Biogas Market3 Challenges | 3 Opportunities

Patrick Serfass - American Biogas Council6 July 2016| NEC, Birmingham, UK

American Biogas Council: The Voice of the US Biogas Industry

The only U.S. organization representing the biogas and anaerobic digestion industry

Over 200+ Organizations from the U.S., Germany, Italy, Canada, Sweden, Belgium and the UK

All Industry Sectors Represented:

project developers/owners

anaerobic digestion designers

equipment dealers

waste managers

waste water companies

farms

utilities

consultants and EPCs

financiers, accountants, lawyers and engineers

Non-profits, universities and government agencies

Join Us! www.AmericanBiogasCouncil.org OR [email protected] OR 202.640.6595

213

0

50

100

150

200

250

300

2010 2011 2012 2013 2014 2015

ABC Membership

Organizations Linear (Organizations)

247on Farm

(Dairy AND Swine)

1,241Wastewater

(860 using their biogas)

645at Landfills

2,100+Operational

Biogas Systems

11,000+Potential

Biogas Systems

8,241on Farm

(Dairy AND Swine)

2,400Wastewater

(incl. 381 making biogas but not using it)

440 at Landfills

U.S. Biogas Market – Current and Potential

Wastewater Sector

U.S. Biogas Market – Potential Impact

Enough energy to power 3.5 million American

homes

Emission reductions equivalent to removing

up to 11 million passenger vehicles from the road

13,000+Biogas Systems

$33 Billion in construction spending, creating

approximately 275,000 short –term construction jobs and

18,000 permanent jobs

3 Challenges: Project Permitting

Selling Products (Elec., Gas, Digestate)

andFew/Unstable Incentives

218

3 Opportunities: Adding Food WasteMaking Vehicle Fuel

andMaking Products from Digestate

219

220

Food Waste

What wastes are BEST for making biogas?

25x manure

10x manure

35x manure

70% of the electricity from food waste

Manure Digester + Food Waste

222

10% food waste can DOUBLE

biogas production

5 States + 5 Cities: Food Waste Recycling PoliciesMunicipalities: San Francisco, Seattle, Austin, Vancouver, New York City, most starting in

2009-10

2011: Connecticut, Public Act 11-217 (updated in 2013)

2012: Vermont, Universal Recycling Law, Act 148—all organics, largest generators first, effective 7/1/2016

2013

• CT: Public Act 13-285 (update to 2011)—Commercial organics, effective 1/1/14

• NYC: Local Law 146-2013—Commercial organics, effective 7/1/2015

2014

• Massachusetts: 310 CMR 19.000 regulations—Commercial organics, effective 10/1/14

• Rhode Island: Act Relating to Health and Safety—Commercial organics, eff. Jan 2016

• California AB 1826: Mandatory Commercial Food Waste Recycling, effective 1/1/2016

2016: Maryland? New Jersey? New York (state)?

223

3 Opportunities: Adding Food WasteMaking Vehicle Fuel

andMaking Products from Digestate

225

Vehicle Fuel and Plastic• Greening fleets

• Garbage truck collects enough food waste to fuel the daily route

• Making RNG generates RINs worth $0.75 - $1.30/gallon

• Greening product packaging with bioplastic (Dell computer bags)

3 Opportunities: Adding Food WasteMaking Vehicle Fuel

andMaking Products from Digestate

227

Chesapeake Bay Phosphorus Risk Map

228

Red and pink areas: no more fertilizers containing phosphorus

Green and yellow areas: can continue to use manure or unseparated digested material

Chesapeake Bay Foundation

Summary of Systems

229Frear,C. (2013) Review of Emerging Nutrient Recovery Technologies and Discussion on Performance/Cost Structures for WSU/DVO Integrated Approach -Capturing Valuable Nutrients from Manure: Part 2

230

Soil Products (liquid/solids)

Digester PRODUCTS market potential*

$2.9 Billion

*agricultural sector only

231

Policies to Help US Project Development

• Make permitting and interconnection easier. Less time to develop = less expensive installations

• Buy the digestate. Revenue for the project, easier to get financing.

• Make long-term feedstock contracts with waste generators easier to obtain by project developers:

• Help project developers sell their gas/energy. Revenue for the project, easier to get financing:– FIT (Feed In Tariff)

– Get gas utilities to buy pipeline quality RNG from new projects and offer local “green gas” to their gas customers

Thank You!

• Learn More• Sign up for the FREE Biogas News• www.AmericanBiogasCouncil.org

• Become a Member• Application online, or contact us

Patrick Serfass, Executive DirectorAmerican Biogas Council1211 Connecticut Ave NW #650Washington, DC [email protected] [email protected]

THE GLOBAL DRIVERS FOR

AD

INSIGHT INTO CANADA

JAKE DEBRUYNONTARIO MINISTRY OF AGRICULTURE, FOOD AND RURAL AFFAIRS

Jake DeBruyn

Ontario Ministry of Agriculture,

Food and Rural Affairs

UK ADBA Conference, July 6 & 7, 2016

Canadian Biogas

Update

Today’s Presentation

• Introduction to biogas opportunity in Canada

– Key provincial initiatives

– Areas where UK leadership may have direct application to Canada

– Contact information to engage further with Canada

Ontario Quick Fact• 152 million consumers within a

day’s drive of Toronto

238

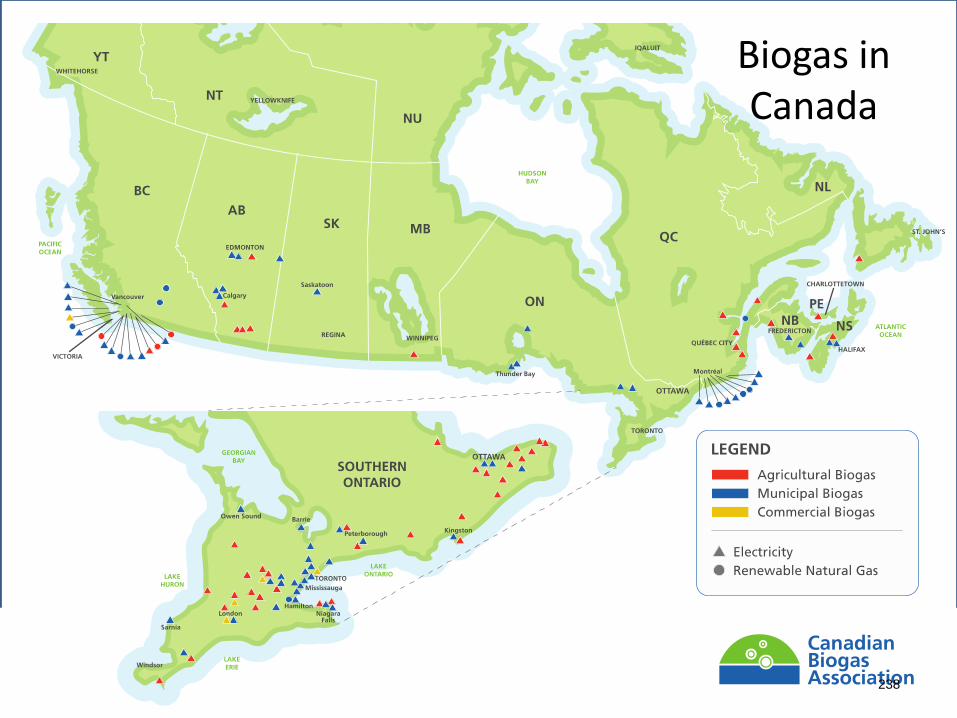

Biogas in Canada

Biogas Policies Across Canada• British Columbia

– Voluntary RNG program, carbon tax, low carbon fuels standard

• Alberta

– Carbon price and emitters regulation, biogas offset protocols, localized organics bans

• Quebec

– Ban on organics in landfill by 2022, municipal capital incentives, carbon tax, RNG momentum project by project

– Canada’s largest landfill in Quebec started selling Renewable Natural Gas (RNG) to California in 2015

• Nova Scotia

– Ban on organics in landfill, community feed-in-tariff program (on hold)

239

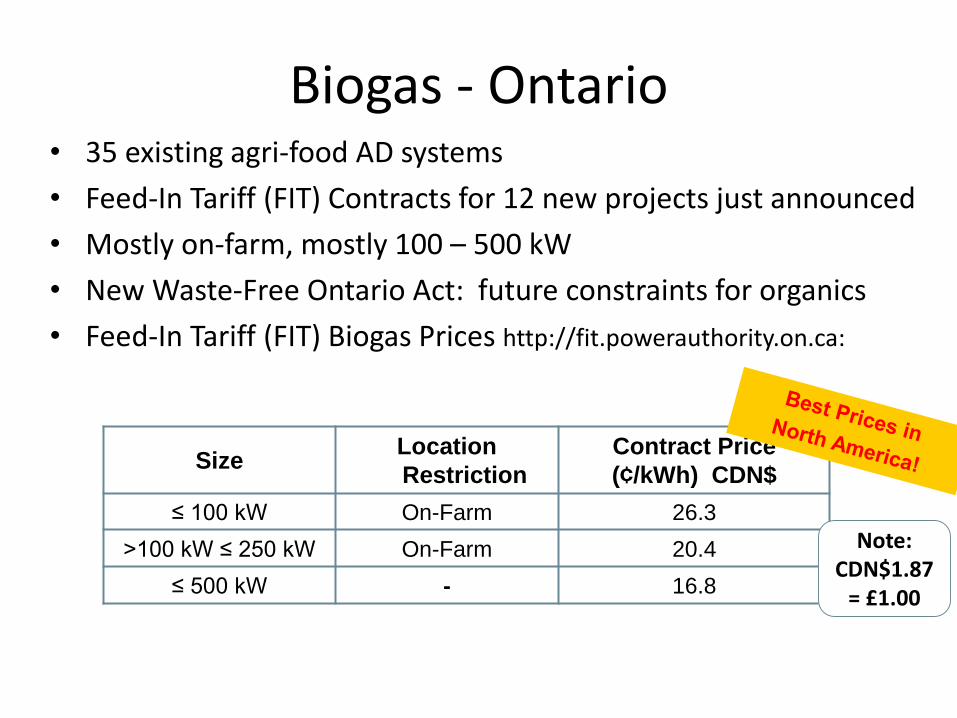

Biogas - Ontario• 35 existing agri-food AD systems

• Feed-In Tariff (FIT) Contracts for 12 new projects just announced

• Mostly on-farm, mostly 100 – 500 kW

• New Waste-Free Ontario Act: future constraints for organics

• Feed-In Tariff (FIT) Biogas Prices http://fit.powerauthority.on.ca:

SizeLocation

Restriction

Contract Price

(¢/kWh) CDN$

≤ 100 kW On-Farm 26.3

>100 kW ≤ 250 kW On-Farm 20.4

≤ 500 kW - 16.8

Note: CDN$1.87

= £1.00

Ontario – Climate Change Action Plan

• Cap and trade program

– 5 year plan to fight climate change, reduce greenhouse gas pollution and transition to a low-carbon economy.

– Emissions reductions targets

Ontario’s Climate Change Action Plan:

Anaerobic Digestion Opportunities:

1.3 Pilot waste and agricultural methane as a fuel source

– Biogas from agricultural materials or food wastes for transportation purposes, with funding for commercial-scale demonstration projects.

4.1 Green Commercial Vehicle Program

– Incentives to buy low-carbon commercial vehicles and technologies

4.2 Build a network of low-emission fuelling stations

– Establish a network of natural gas and low- or zero carbon fuelling stations.

6.1 Establish low-carbon content for natural gas

– Renewable content requirement for natural gas

UK Biogas Opportunities in Canada

• Canadian biogas companies experienced in international partnerships

• UK programs (Renewable Heat Incentive, Low Carbon Truck Demo) give UK companies experience for new biomethane opportunities in Canada

• Similar business culture and language

Next Steps for UK Companies

• Summary: Why do Biogas Business in Canada?

1. Ontario Climate Change Action Plan: exciting pathway forward

2. Ontario: Best Feed-In Tariff in North America

• Contact the Canadian Trade Commissioner Service

– Rachel Soares, Trade Commissioner | SustainableTechnologies

– Tel: 020 7004 6219 [email protected]

• Business Immigration to Ontario: www.investinontario.com/bi/

Come to Toronto March 2017!

www.biogasassociation.ca

• Ontario Ministry of Agriculture Food and Rural Affairs (OMAFRA) www.ontario.ca/biogas

• OMAFRA Biogas contacts:• [email protected]• [email protected]

THE GLOBAL DRIVERS FOR

AD

INSIGHT INTO ARGENTINA

JORGE ANTONIO HILBERTNATIONAL AGRICULTURAL TECHNOLOGY INSTITUTE

INSIGHTS INTO ARGENTINA

Jorge Antonio Hilbert

The law prioritizes projects that accomplish the following criteria:

Sponsored by small and medium sized companies. Belong to farming producers. Located in regional and rural economies. New law imposes renewable targets for the private sector

* Law 26.093 extends benefits to sugar plants, sugarcane and ethanol producers

LAW 26.093/2006: PROMOTES THE PRODUCTION AND USE OF BIOFUELS(Implemented by Decree 109/07).Mandatory use 7% bioethanol and 9% biodieselDefinition of domestic prices for biofuelsQuality standardsLAW 26.190/2006 8 % Renewables in Electric energy generationLAW 27.191/2015 20% 2020 Under regulation process

PROMOTION OF RENEWABLE ENERGY

Agriculture Sector

Livestock Sector

Forestry Sector

Argentina is a main producer of raw materials and manufactures

Based on WISDOM, power installed capacity could be increased up to 1,325 MW of total electricity capacity and by 1,325 MW of thermal generation by 2030

Industries

BIOENERGY FROM RESIDUES IN ARGENTINA

*

Program to promote the use of biomass for energy production in Argentina (PROBIOMASA)

Implemented by the Government of Argentina through the Ministries of Agriculture and Energy, with technical

assistance from FAO.

0

20

40

60

80

100

120

140

160

180

200

220

240

260

280

300

40% 35% CC TV CC Pulveriz IGCC

VIENTO MINI HIDRO GEOTÉRM. SOLAR (CSP) GASNATURAL

FUEL OIL DIESEL CARBÓN NUCLEAR

US$/MWh

CO2 @ 20 US$/ton

Combustible

O&M

Costo Capital

Cost of competitive MWh

Costo Combustible.: Gas Natural @ 12 US$/MMBTU

Petróleo @ 100 US$/bbl

Carbón CIF @ 150 US$/ton

Costo de Capital (US$/kW) / Viento 2000/40% Mini Hidro 2200/50%

Factor de Carga (%): Solar CSP 4000/30% Geotérmica 3900/85%

CC (gas) 900 Carbón Pulv. 2000

Nuclear 4000 Carbón IGCC 3000

Rentabilidad: TIR 10% después de IG

sobre activos (i.e. sin leverage)

Sin IVA. Contratos de 20 años .

Prices payed by consumers 3 to 10 US$/MWh

251

80PROJECTS UNDER

CONSTRUCTION

35PROJECTS

UNDER

EVALUATION

16PROJECTS IN

OPERATION

FIRST SURVEY OF BIOGAS PROJECTS

49

14

37

PLANTS SIZE

Small less than 1 to100 m3 Medium 100 to 1000 m3 Big over 1000 m3

Technology Providers

Empresa Provincia LocalidadEtapa del

proyectoSector Actividad

Capacidad

instalada

Origen de la

biomasa

Biogás Argentina Buenos Aires Carlos Tejedor ConstrucciónEnergía termica o

eléctrica

Biodigestion de

efluentes0,4 MW Feedlot

Bio4/Bioeléctrica Córdoba Rio Cuarto Construcción Energía eléctricaProducción de

biogás1 MW

Cereales &

Oleaginosas

Alimentos Magros

S.A. (ACA)San Luis Juan Llerena Construcción Cogeneración

Producción de

biogás1,5 MW

Industria

porcina

Gral. Pirán Biogás

guano aviarBuenos Aires General Pirán Cartera

Biogás- energía

eléctricacama de pollos 0,6 MW

Industria

avícola

Proyecto RSU

Cooperativa Rocío

(Gral. Rodríguez)

Buenos AiresGeneral

RodriguezCartera

Biogás- energía

eléctricaRSU - biomasa 11 MW? RSU

Adecoagro Tambos

La LacteoCórdoba

Capilla de los

RemediosCartera

Biogás- energía

eléctricatambo bovino 1-3 MW Tambo

Avícola Las Camelias

S.A.Entre Ríos San José Cartera Energía Eléctrica

Motor con

biogás0,6 MW

Industria

avícola

Don Guillermo S.R.L Misiones El dorado CarteraBiogás- energía

eléctrica

Producción de

biogás100 kw

Feedlot,

Cerdos

Solamb SRL Santa Fe Timbúes Cartera Energía eléctricaMotor con

biogás1 MW

Efluentes

biodiesel

Cooperativa Agricola

e Industrial San

Alberto (Puerto

Rico)

Misiones Puerto Rico Cartera Energía térmicaProducción de

biogás

10000

m3/día

biogás

Paladini Santa Fe Arroyo Seco Cartera Energia termicaBiodigestión de

efluentes

FIRST SURVEY OF BIOGAS PROJECTS

RESOURCES FOR BIOGASPRODUCTION

DEPTH OF STUDIES

NATIONAL

PROVINCIAL

LOCAL

CASE STUDIES

BIOMASS SOURCES STUDIED BY INTA

biogas from whine industry

biogas from vinace from sugarcane bioethanol

biogas from fruit juices

AGROINDUSTRY biogas from dairy industry

biogas from fruit and vegetable processing

biogas from beer industry

biogas from bread and other flour industries

SLAUGHTERHOUSESbiogas from slaughterhouses and meat processing

FISHERIES biogas from fish transforming chain

ANIMAL RESIDUES biogas from feedlots and dairies

biogas from confines swine production

biogas from chicken and egg production

CROP RESIDUES …

Implementation

of an

Geographic

Information

System on

Biomass

Resources

WISDOM-FAO

MethodologyWoodfuel Integrated

Supply/Demand Overview

Mapping

IDENTIFICATION OF RAW MATERIALS THAT COULD

BE USED

STUDY OF WASTE-GENERATING

AGRICULTURAL CHAINS

LOCALIZATION OF THE INFORMATION IN THE GEOGRAPHICAL SPACE

AGROINDUSTRIAL RESIDUOS DE CULTIVOS PODA

METHODOLOGY

Argentinean Crop Residue Supply E F M A M J J A S O N D

Vineyard pruning X X X X

Grape pomace X X X X

Olive pruning X X X

Olive Pomace X X X X X X

Sugaarcane--RAC X X X X X X X

Sugarcane-Bagaze X X X X X X X

Wheat X X X

Maize X X X X

SUrveyed projects 2016

Surveyed projects 2016

Research at experimental stations

YANQUETRUZ 1300 Mothers

SUBSTRATES Pig manure: 150 m3/day Corn/sorghum silage: 50 ton/day

PLANTA CONFIGURATION two Primary Biodigestrs 3619 m3 c/u Two secundary Biodigesters 2897 m3 c/u Two CATERPILLAR engines 756 kw Electric power= 1,53 Mw Heating system Emergency Torch 800 m3 / h Blowers 400 mbar y 390 m3/h

BIOGÁS PRODUCTION12.887 m3/day8.000 Mw/year

BIOELECTRICA FINISHED FIRST DIGESTER WITH PLANS TO CONSTRUCT 60 PLANTS OF 1 Mw

Investors 29 farmers

FIRST FEEDLOT IN THE PROVINCE OF BUENOS AIRES

281

New Plants 2015

Feedlot biogás plant in Buenos Aires province

Wet residue plant in San Luis Urban + agroindustrial residues Santa Fe

WORLD CONFERENCE BUENOS AIRES 23 AL 25 SEPTEMBER 2016

Workshop (1)

Merida

Workshop (2)

Buenos Aires

Conference (3)

Brazil

Workshop (4)

Houghtona. Community

impacts,

b. water /

energy

nexus,

c. biodiversity /

ecosystems

d. energy policy,

e. life cycle

assessment,

f. food and other

systems,

g. biogeochemical

cycles, and

h. biomass supply

transportation

logistics.

http://www.aiche.org/panamrcn/events/rcn-conference-on-pan-american-

biofuels-and-bioenergy-sustainability

283

Former Agriculture Subcommittee

The Subcommittee has:

– Hosted meetings and workshops in more than a

dozen countries.

– Assisted in the development of 13 country-

specific action plans and 10 resource

assessments.

– Showcased more than 30 project opportunities

and success stories at the 2010 Expo.

– Developed international guidance for evaluating

and reporting Anaerobic Digestion system

performance

284

Subcommittees Commonality

Municipal Wastewater

Municipal Solid Waste

Agriculture

Biogas

285

Biogas Subcommittee

Municipal Solid Waste

Subcommittee

Agriculture

Subcommittee

Municipal Wastewater

Subcommittee

Biogas

Subcommittee

286

Subcommittee Cooperation

• Biogas capture and

use for energy is the

unifying force binding

all 3 sectors in the

Biogas

Subcommittee

• Centralized

wastewater

treatment

• Food waste

diversion

• Livestock manure

digesters

• Household/small

scale digesters

• Co-digestion of organic

wastes in wastewater or

manure digesters

• Co-location of digesters

with landfill gas energy

• Food waste diversion

from landfill as methane

mitigation and feedstock

for digesters

CommonalityAreas of

InterventionSynergies

287

288

http://inta.gob.ar/bioenergia

Ing.Agr. M.Sc. Jorge A. Hilbert

› INTA y UTN

› Tel +54 11 4665-0495 0450

› Mail [email protected]

› http://inta.gob.ar/bioenergia

THE GLOBAL DRIVERS FOR

AD

INSIGHT INTO SOUTH AFRICA

DIARMID JAMEISONSLR CONSULTING

THE GLOBAL DRIVERS FOR

AD

CASE STUDY FROM DUPONT

CONRAD BURKEDUPONT INDUSTRIAL BIOSCIENCES

Bioscience in Biogas

© DuPont 2016

Page 293

Bioscience in Action All Around Us

Animal Nutrition

Home Care and Cleaning

© DuPont 2016

Page 294

Bioscience in Action All Around Us

Sustainable Textiles

Sustainable Deicing Fluids

© DuPont 2016

Of the 900 million solar panels installed in the past 40 years,

½ of them contain DuPont materials

In the past 12 years, solar cell improvements,

with our materials, have yielded

30% higher efficiencies

i.e. same power with

fewer solar panels

Page 295© DuPont 2016

DuPont Not New to Renewable Energy

Page 296

Bioscience transforming today’s fuel supply

© DuPont 2016

297