Conditional Expectation Functionsecon.ucsb.edu/~doug/241b/Lectures/01 Conditional Expectation... ·...

29

Conditional Expectation Functions Econometrics II Douglas G. Steigerwald UC Santa Barbara D. Steigerwald (UCSB) Expectation Functions 1 / 29

Transcript of Conditional Expectation Functionsecon.ucsb.edu/~doug/241b/Lectures/01 Conditional Expectation... ·...

Conditional Expectation FunctionsEconometrics II

Douglas G. Steigerwald

UC Santa Barbara

D. Steigerwald (UCSB) Expectation Functions 1 / 29

OverviewReference: B. Hansen Econometrics Chapters 1 and 2.0 - 2.8

most commonly applied econometrics toolI least-squares estimation (regression)

tool to estimateI approximate conditional mean of dependent variableI as a function of covariates (regressors)I (y , x1, . . . , xK ) :=

�y , xT�

data is observational not experimentalI causality is di¢ cult to infer

example - wagesI random variable before measurementI observed wages are outcomes of the random variableI underpins the application of statistics to economics

D. Steigerwald (UCSB) Expectation Functions 2 / 29

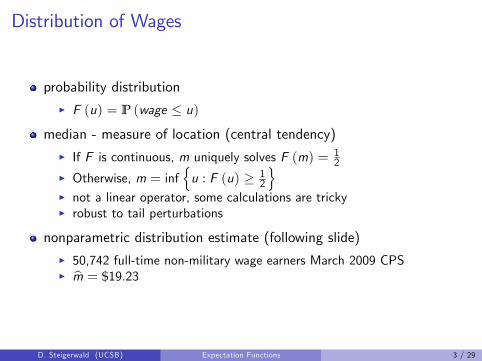

Distribution of Wages

probability distributionI F (u) = P (wage � u)

median - measure of location (central tendency)I If F is continuous, m uniquely solves F (m) = 1

2I Otherwise, m = inf

nu : F (u) � 1

2

oI not a linear operator, some calculations are trickyI robust to tail perturbations

nonparametric distribution estimate (following slide)I 50,742 full-time non-military wage earners March 2009 CPSI bm = $19.23

D. Steigerwald (UCSB) Expectation Functions 3 / 29

D. Steigerwald (UCSB) Expectation Functions 4 / 29

Quantiles

a useful way to summarize a probability distribution

for any α 2 (0, 1), the αth quantile isI If F is continuous, qα uniquely solves F (qα) = αI Otherwise, qα = inf fu : F (u) � αgI q0.5 = m

quantile function, qα, viewed as a function of α is the inverse of F

if α is represented in percentage terms (10% instead of .1), quantilesare referred to as percentiles

I q0.5 = m is called the 50th percentileI q0.9 is called the 90th percentile

D. Steigerwald (UCSB) Expectation Functions 5 / 29

Density of Wages

If F is di¤erentiable, density function exists

f (u) =dduF (u)

F (u) and f (u) contain the same information

density is easier to interpret visually

mean - measure of location (y denotes wage)I if F is continuous, µ := E (y) =

R ∞�∞ uf (u) du

I formal de�nition, 240A Lecture on Random Variables and DistributionsI linear operator, not robust

nonparametric density estimate (following slide)bµ = $23.90data are skew, 64% of workers earn less than bµD. Steigerwald (UCSB) Expectation Functions 6 / 29

D. Steigerwald (UCSB) Expectation Functions 7 / 29

Density of Log Wagegains can be made by taking the natural logarithm of wages

skewness and thick tails can be reducedbµ for log wage is a much better measure of central tendency

D. Steigerwald (UCSB) Expectation Functions 8 / 29

Toolkit: Log Di¤erences

key logic log (1+ x) � x

If y � is c% greater than y

y � =�1+

c100

�y

log y � � log y = log�1+

c100

�� c

example: logw � log z = bI then w is approximately b% larger than zI approximation is quite good for jbj � 10

Approximation Accuracy

D. Steigerwald (UCSB) Expectation Functions 9 / 29

Conditional ExpectationsIs the wage distribution the same for all workers?

Men versus women (43% of workers are women)I E (log (wage) jgender = man) = 3.05I E (log (wage) jgender = woman) = 2.81I 24% di¤erence in average wages between men and women

D. Steigerwald (UCSB) Expectation Functions 10 / 29

Gender and Race

conditional means reduce distributions to a single summary measureI primary focus of regression analysisI major focus of econometrics

Conditional MeansWhite Black Other

Men 3.07 2.86 3.03Women 2.82 2.73 2.86

male-female wage gapI 25% for whites 13% for blacks

black-white wage gapI 21% for men 9% for women

D. Steigerwald (UCSB) Expectation Functions 11 / 29

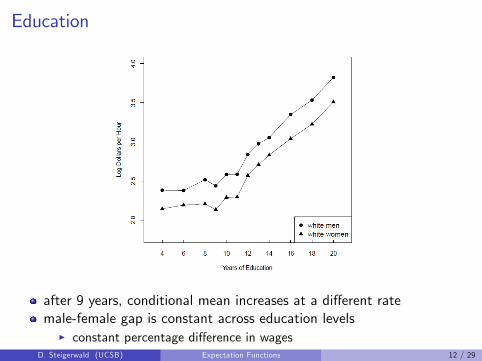

Education

after 9 years, conditional mean increases at a di¤erent ratemale-female gap is constant across education levels

I constant percentage di¤erence in wagesD. Steigerwald (UCSB) Expectation Functions 12 / 29

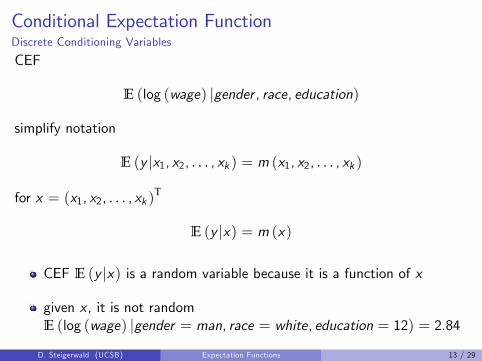

Conditional Expectation FunctionDiscrete Conditioning Variables

CEF

E (log (wage) jgender , race, education)

simplify notation

E (y jx1, x2, . . . , xk ) = m (x1, x2, . . . , xk )

for x = (x1, x2, . . . , xk )T

E (y jx) = m (x)

CEF E (y jx) is a random variable because it is a function of x

given x , it is not randomE (log (wage) jgender = man, race = white, education = 12) = 2.84

D. Steigerwald (UCSB) Expectation Functions 13 / 29

Conditional Expectation FunctionContinuous Variables with Joint Density Function

f (y , x) is the joint density function for (y , x)

y = log (wage) x = experience

for white men with 12 years of education contours of f (y , x) are

D. Steigerwald (UCSB) Expectation Functions 14 / 29

Conditional Densitya "slice" of the joint density contours yields the conditional density

shifts right and becomes more di¤use as experience increasesI little change as experience increases past 25 years

the conditional density is denoted fy jx (y jx) Conditional DensityD. Steigerwald (UCSB) Expectation Functions 15 / 29

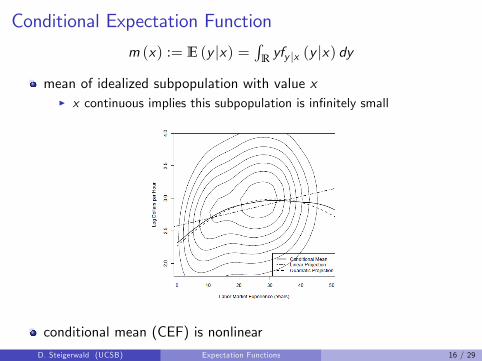

Conditional Expectation Function

m (x) := E (y jx) =R

Ryfy jx (y jx) dy

mean of idealized subpopulation with value xI x continuous implies this subpopulation is in�nitely small

conditional mean (CEF) is nonlinear

D. Steigerwald (UCSB) Expectation Functions 16 / 29

Toolkit: Law of Iterated Expectations

Simple Law

E (E (y jx)) = E (y) if E (y) < ∞

note E (E (y jx)) =R

RE (y jx) fx (x) dx

General Law (allows for 2 sets of conditioning variables)

E (E (y jx1, x2) jx1) = E (y jx1) if E (y) < ∞

"smaller information set wins"

D. Steigerwald (UCSB) Expectation Functions 17 / 29

Toolkit: Conditioning Theorem

condition on x ! e¤ectively treat x as constantSimple Property

E (g (x) jx) = g (x) for any function g (�)

example E (x jx) = x

General Property (allows for an additional random variable)

E (g (x) y jx) = g (x)E (y jx)

E (g (x) y) = E (g (x)E (y jx))

D. Steigerwald (UCSB) Expectation Functions 18 / 29

Error

de�ne: CEF error e = y �m (x)

y = m (x) + eE (ejx) = 0

note, E (ejx) = 0 is not a restriction, these equations hold by de�nition

Error Properties Theorem: (derived from f (y , x))

1 E (ejx) = 0) E (e) = 02 E (h (x) e) = 0 if E jh (x) ej < ∞3 E jy jr � ∞) E jejr � ∞ (r � 1)

D. Steigerwald (UCSB) Expectation Functions 19 / 29

Error Properties

1. E (ejx) = 0not a restriction, but a de�nition

called mean independenceI mean independence ; independenceI e = xε with ε � N (0, 1) independent of x ) ejx � N

�0, x2

�I empirics : e and x are rarely assumed independent

2. E (h (x) e) = 0

e is uncorrelated with any function of the covariates

3. E jy jr � ∞) E jejr � ∞

Ey2 < ∞ ) Var (e) < ∞

D. Steigerwald (UCSB) Expectation Functions 20 / 29

Proofs

1 Proof of Simple LIE2 Proof of General LIE3 Proof of Conditioning Theorems4 Proof of Error Properties Theorem

D. Steigerwald (UCSB) Expectation Functions 21 / 29

Review

Implication of observational data?

causality is di¢ cult to infer

Should we model E (y jx) as linear in x?no

What are the key properties of e = y �E (y jx)?E (ejx) = 0 (by construction)

uncorrelated with any function of x

D. Steigerwald (UCSB) Expectation Functions 22 / 29

Approximation AccuracyTaylor Series approximation

log(1+ x) = x � 12x2 + 1

3x3 � � � � = x +O

�x2�� x

highly accurate if jx j � .1

D. Steigerwald (UCSB) Expectation Functions 23 / 29

Landau Notation (Big O)

we say f (x) = O (g (x)) as x ! 0 if

jf (x)j � M jg (x)j for all x � x0

Consider f (x) = � 12x2 +13x3�����12x2 + 13x3

���� � 12

��x2��+ 13

��x3��for suitably chosen x0, if x � x0

12

��x2��+ 13

��x3�� � 12

��x2��+ 13

��x2�� = 56x2

so f (x) = O�x2�as x ! 0

Return to Log Wage

D. Steigerwald (UCSB) Expectation Functions 24 / 29

De�nition of Conditional Densityif (y , x) have joint density f (y , x) then

I x has marginal density

fx (x) =Z

Rf (y , x) dy

for any x such that fx (x) > 0, the conditional density of y given x isde�ned as

fy jx (y jx) =f (y , x)fx (x)

consider f (log(wage)jexperience = 5)f (y , x = 5)P (x = 5)

the "slice" the scale factor

I if their are fewer individuals with 5 years of experience than with 10years of experience, the higher conditional density could correspond toworkers with 5 years of experience, even if the joint density is higher forworkers with 10 years of experience

Return to Conditional DensityD. Steigerwald (UCSB) Expectation Functions 25 / 29

Proof of Simple Law of Iterated Expectations

Simple LIE: E (E (y jx)) = E (y)

assume (y , x) have joint density f (y , x) (for convenience)I E (y jx) is a function of the random variable x onlyI to calculate its expectation, integrate with respect to the density fx (x)of x

E (E (y jx)) =Z

RkE (y jx) fx (x) dx

I which equals (by substitution and by noting thatfy jx (y jx) fx (x) = f (y , x))Z

Rk

�ZRyfy jx (y jx) dy

�fx (x) dx =

ZRk

ZRyfy ,x (y , x) dydx

= E (y) ,

becauseR

Rk fy ,x (y , x) dx = fy (y). �

Return to Proofs

D. Steigerwald (UCSB) Expectation Functions 26 / 29

Proof of General Law of Iterated ExpectationsGeneral LIE: E (E (y jx1, x2) jx1) = E (y jx1)

assume (y , x1, x2) have joint density f (y , x1, x2) (for convenience)I E (y jx1, x2) is a function of the random variables x1 and x2I integrate with respect to the density of x2 given x1

E (E (y jx1, x2) jx1) =Z

Rk2E (y jx1, x2) f (x2 jx1) dx2

=Z

Rk2

�ZRyf (y jx1, x2) dy

�f (x2 jx1) dx2

I note that f (y jx1, x2) f (x2 jx1) = f (y ,x1,x2)f (x1,x2)

f (x1,x2)f (x1)

= f (y , x2 jx1), so

=Z

Rk2

ZRyf (y , x2 jx1) dydx2

= E (y jx1) ,

the mean of y given the value of x1. �Return to Proofs

D. Steigerwald (UCSB) Expectation Functions 27 / 29

Proof of Conditioning Theorems

Simple CT: E (g (x) y jx) = g (x)E (y jx)

assume (y , x1, x2) have joint density f (y , x1, x2) (for convenience)

E (g (x) y jx) =Z

Rg (x) yfy jx (y jx) dy

= g (x)Z

Ryfy jx (y jx) dy

= g (x)E (y jx) ,

where E jg (x) y j < ∞ is needed to ensure the �rst equality is wellde�ned. �

General CT: E (g (x) y j) = E (g (x)E (y jx))

Proof: application of simple LIE. �Return to Proofs

D. Steigerwald (UCSB) Expectation Functions 28 / 29

Proof of Error Properties Theorem

Parts 1 and 2 follow trivially

Part 3: E jy jr � ∞) E jejr � ∞ (r � 1)

e = y �m (x)(E jejr )1/r

= (E jy �m (x)jr )1/r

I�E jy �m (x)jr

�1/r ��E jy jr

�1/r+�E jm (x)jr

�1/r (Minkowski�sInequality)

F E jE (y jx)jr � E jy jr for any r � 1 (Conditional ExpectationInequality)

I the two parts on the right are �nite by E jy jr � ∞

(E jejr )1/r � ∞ implies E jejr � ∞. �Return to Proofs

D. Steigerwald (UCSB) Expectation Functions 29 / 29

![Understanding Conditional Expectation via Vector Projection › cschang › Talk01142008.pdf · † The conditional expectation of X given Y, denoted by E[XjY], is the function of](https://static.fdocuments.net/doc/165x107/5ed9f65928db2d5ca24928b9/understanding-conditional-expectation-via-vector-projection-a-cschang-a-a.jpg)

![Conditional Expectation and Prediction - Mark Irwin · = E[Y2jX = x]¡(E[YjX = x])2 Conditional Expectation 1. ... 0.0 0.2 0.4 0.6 0.8 1.0 Fuel Use Conditional Expectation 8. In the](https://static.fdocuments.net/doc/165x107/5b5cdad97f8b9ad2198d4454/conditional-expectation-and-prediction-mark-ey2jx-xeyjx-x2-conditional.jpg)