UBS 2004 Natural Gas & Electric Utilities Conference Gerry Anderson February 12, 2004 New York, NY.

Upload

vuongnguyetCategory

view

214download

0

1

Con Edison, Inc. UBS Natural Gas & ElectricUtilities Conference

New York, NYFebruary 28, 2007

2

Forward-Looking Statements

This presentation contains certain forward-looking statements of future expectations and financial measures not determined in accordance with Generally Accepted Accounting Principles (non-GAAP) financial measures. Actual results might differ materially from those projected in the forward-looking statements because of factors such as those identified in reports the company has filed with the Securities and Exchange Commission.

For more information, contact:

Jan Childress, Director, Investor Relations 1-212-460-6611Ellen Socolow, Manager, Investor Relations 1-212-460-4986

www.conEdison.com

3

Long Tradition, Solid Performance

Con Edison, Inc. Parent Net Loss: $32 million – (4)%

Con Edison of New YorkNet Income: $686 million – 93%

Orange and RocklandNet Income: $45 million – 6%

Con Edison SolutionsNet Income:

$8 million – 1%

Con Edison Energy

Net Income:$1 million – 0%

Con Edison Development

Net Income:$30 million – 4%

Regulated Utilities

Competitive Energy Businesses

Note: For the year ended December 31, 2006

4

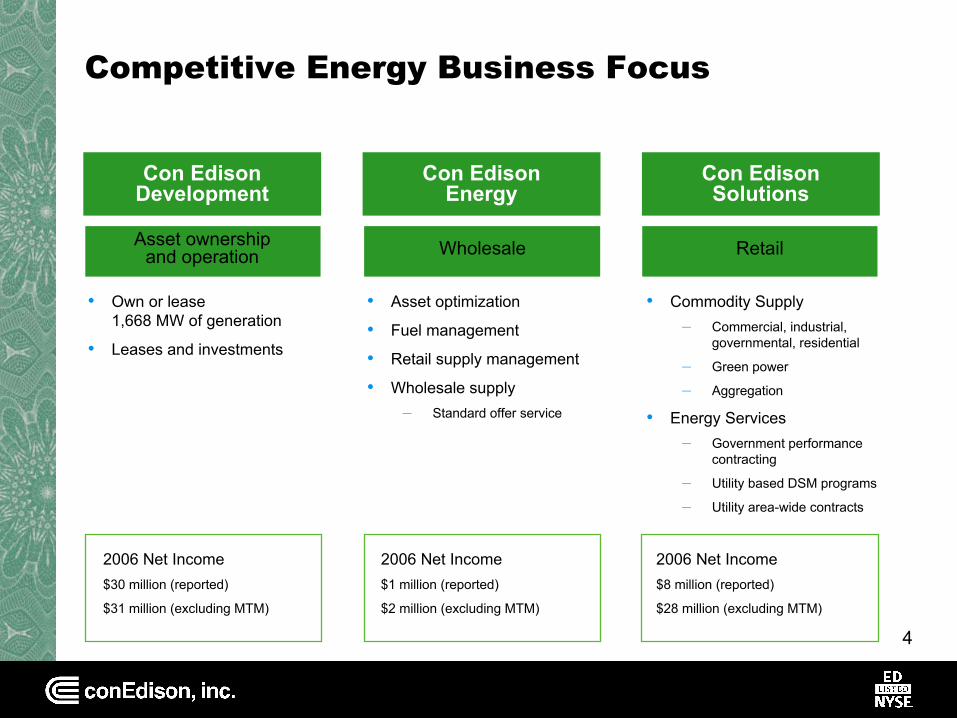

Competitive Energy Business Focus

• Own or lease1,668 MW of generation

• Leases and investments

Con Edison Development

• Asset optimization

• Fuel management

• Retail supply management

• Wholesale supply– Standard offer service

Con Edison Energy

• Commodity Supply– Commercial, industrial,

governmental, residential

– Green power

– Aggregation

• Energy Services– Government performance

contracting

– Utility based DSM programs

– Utility area-wide contracts

Con Edison Solutions

Asset ownershipand operation Wholesale Retail

2006 Net Income$8 million (reported)

$28 million (excluding MTM)

2006 Net Income$1 million (reported)

$2 million (excluding MTM)

2006 Net Income$30 million (reported)

$31 million (excluding MTM)

5

Overview of Con Edison DevelopmentCon Edison Development

1,6681,778Total Capacity

335335Gas100.0%PeakingMarylandRock Springs

330330Gas100.0%PeakingNew JerseyOcean Peaking

156156Gas/Oil100.0%PeakingMassachusettsCEEMI

189236 (c)Gas/Oil80.0%IntermediateNew JerseyLakewood

125125 (d)Gas/Oil/Hydro100.0%IntermediateMassachusettsCEEMI

2042Oil49.5%IntermediateGuatemalaGENOR

1429 (b)Gas48.0%BaseMichiganADA

499525Gas/Oil95.0%BaseNew HampshireNewington (a)

Owned Capacity(in MW)

Aggregate Capacity(in MW)

Fuel SourceOwnershipPower PlantTypeBase/Peak/Intermediate

LocationName

(a) Leased pursuant to a consolidated lease transaction.

(b) Subject to a power purchase agreement expiring in 2026.

(c) Subject to a power purchase agreement expiring in 2014.

(d) Includes 18MW from five small hydroelectric facilities.

Newington, NH1

West Springfield, MA2

Lakewood, NJ3

Rising Sun, MD4

12

3

4

NEISO

NYISO

PJMISO

6

Con Edison Solutions Highlights

• Ninth largest ESCO nationwide

• Profitable every year since 2001

• Provides commodity service in eight states and the District of Columbia

• 200,000 plus customers

• 10.6 million MWhrs sold in 2006 –7% greater than 2005

• Supplies green power in New York and Massachusetts

Con Edison Solutions

NY

DEMD

NJ

CT

NH

MA

TX

7

Regulated Business Service Area

• 3.2 million electric customers

• 1.1 million gas customers

• 1,800 steam customers

• 709 MW of regulated generation

• 36,000 miles of overhead transmission and distribution lines

• 93,000 miles of underground transmission and distribution lines

• 4,300 miles of gas mains

• 105 miles of steam mains and lines

Con Edison of New York

8

New York City Job Growth By Sector — 2006Con Edison of New York

16,300

8,200

6,900

6,200

5,200

3,300

3,200

(1,300)

(2,500)

Education and health services

Financial services

Leisure and hospitality

Professional and business services

Construction

Trade, transportation, and utility

Other services

Information

Manufacturing

Source: New York State Department of Labor

9

New York City and WestchesterHousing Permits

Con Edison of New York

2004

8,652

Represents New32-Year Record for

New York City

30,000

25,000

20,000

15,000

10,000

5,000

0

Number of New Dwelling Units

20032002200120001999199819971996 20062005

35,000

40-year average of 14,434 for New York City

Source: U.S. Census Bureau

30,927

2005 – 2006 marked the highest two-year stretch since the first reliable construction figures became available in 1965.

31,5991,006

1,493

New York City Westchester

1,364

10

New York City Is the Most Energy Efficient Large City in America

Con Edison of New York

4,696New York

Source: Energy Velocity; U.S. Census 2000

San Francisco

Chicago

Phoenix

Houston

Dallas

6,753

8,143

13,344

14,542

16,116

New York

San Francisco

Chicago

Philadelphia

Atlanta

Los Angeles

Houston

Dallas

53%

31%

26%

25%

15%

10%

6%

5%

Average annual residential electricity usage by city — 2000 – 2005

Incidence of commuters using public transportation — 2000

KWh/customer

11

Growth in Electric Peak Usage 2006 – 2011 Five-Year Compounded Annual Growth

Con Edison of New York

> 3.0%

> 1.5% and ≤ 3.0%

≤ 1.5%

New York City WestchesterCompounded Growth Rate

12

System Peak Demand ForecastCon Edison of New York

MW

20060

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

New York City Westchester

13,141

1,797

11,344

13,575

1,795

11,780

13,800

1,825

11,975

14,000

1,850

12,150

14,200

1,875

12,325

14,375

1,895

12,480

14,550

1,905

12,645

14,700

1,920

12,780

14,850

1,935

12,915

14,975

1,945

13,030

15,100

1,960

13,140

13

Major Substation Construction Program 1948 – 2016

Con Edison of New York

Planned Construction

Transmission Switching Station

DistributionSubstation

1948

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

14

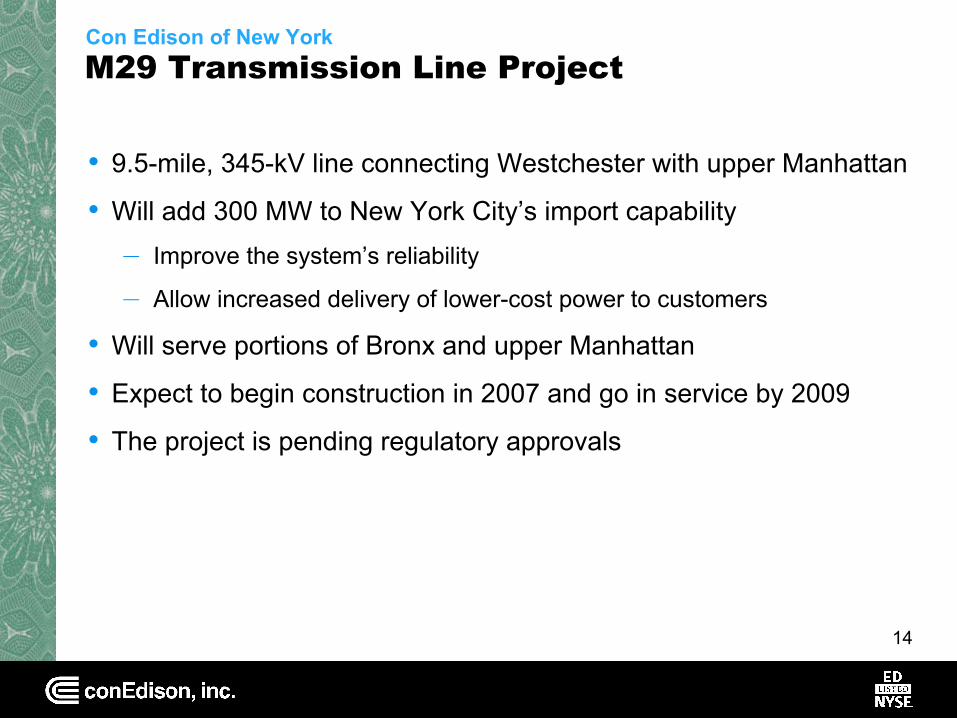

M29 Transmission Line Project

• 9.5-mile, 345-kV line connecting Westchester with upper Manhattan

• Will add 300 MW to New York City’s import capability– Improve the system’s reliability

– Allow increased delivery of lower-cost power to customers

• Will serve portions of Bronx and upper Manhattan

• Expect to begin construction in 2007 and go in service by 2009

• The project is pending regulatory approvals

Con Edison of New York

15

Unparalleled ReliabilityCon Edison of New York

Interruptions per 1,000 customers served, excluding major storms

National(USA)

1,200

1,000

200

0New York State

(w/o Con Edison of NY)Con Edison of NY

(non-network)Con Edison of NY

(overall)Con Edison of NY

(network)

2005 2006

800

600

400

16

System Challenges

• High cost of building and maintaining system

• Low equipment utilization

• Real estate scarcity and price

• Implementing emerging technology, including distributed generation

• Office buildings constructed in the 1960s planned for average loads of 4-5 watts per square foot

• Office buildings today are experiencing average loads of8-9 watts per square foot

Con Edison of New York

17

Evolution of Electric Delivery System

• 1900s – 1920s– Manhattan served by multiple electric

companies

• 1920s – 1940s– Creation of secondary 120V network

systems

– Motivation for network design: load management using substations

• 1940s – 1960s– Continued to break up Manhattan into

more, smaller networks

• 1960s – Today – Design networks and area substation

supplies as second contingency

– Manually alter network sizes as required to defer installing assets

• Today – Second contingency design of

34 networks in Manhattan supplied by24 area substations

Con Edison of New York

1900 1961 2006

Generating StationTransmission SubstationArea Substation

18

System of the FutureCon Edison of New York

Area Substation

Feeders

Network Customers

Transmission

Conventional Design System of the Future Concept

Switch

Shared Network Load

Shared Substation Transformers

19

Regulated Business Service Area

• 296,000 electric customers

• 126,000 gas customers

• 5,800 miles of transmission and distribution lines

• 1,830 miles ofgas mains

Orange and Rockland

Orange and Rockland

Rockland Electric

Pike County Light & Power

New York

Pennsylvania

New Jersey

Connecticut

New York City

20

New Development Spurs 2.3% Annual Growth in Electric Peak Usage

Orange and Rockland

Brigadoon housing development in Highland Mills, Orange County

Harbors at Haverstraw development in Rockland County

21

Major Substation Construction Program 1999 – 2014

Orange and Rockland

Planned Construction

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Transmission Switching Station

DistributionSubstation

22

Building Substations to Meet Growing DemandOrange and Rockland

Darlington Substation, Ramsey, NJ

Orangeburg Substation, Orangeburg, NYChester Substation, Chester, NY

23

Financial Overview

• Proven track record in regulatory relations– Current recovery of all energy costs

– Reconciliation of major uncontrollable costs

– Weather normalization for gas

• Stable balance sheet

• Earnings growth consistent with conservative,low-risk business model

Strategy Provide current income and consistent total returns for shareholders at low risk.

24

Infrastructure InvestmentCon Edison of New York

Millions

2008Forecast

$1,911

2003Actual$1,167

2005Actual$1,541

1,700

Common Plant

Steam

Gas

Electric

2006Actual$1,782

2004Actual$1,235

1,6001,5001,4001,3001,2001,1001,000

900800700600500400300200100

0

Depreciation

1,900

2007Budget$1,870

1,800

2009Forecast

$1,790

$2,000

25

Infrastructure InvestmentOrange and Rockland

Gas

Electric

2003Actual$71

2004Actual$79

2005Actual$87

2006Actual$110

110

90

80

70

60

50

40

30

20

10

0

Depreciation

2008Forecast

$127

Millions

100

2007Budget$125

120

$130

2009Forecast

$125

26

Growing Rate Base and Solid Balance Sheet(as of December 31, 2006)

Rate Base ($ millions)

Orange and Rockland

Pike Gas $ 1Pike Electric $ 9Rockland Electric $ 140O&R Gas $ 210O&R Electric $ 375

Con Edison of New York

Electric $ 10,415Gas $ 2,271Steam $ 1,340

Total Rate Base $ 14,761

Long-TermDebt

50.2%$8,298

Capital Structure ($ millions)

Target Equity Ratio 48%–50%

CommonEquity48.5%$8,004

Preferred Stock1.3%$213

• Expected issuances of new equity: $500 million - $700 million (above issuances through DRIP and employee stock plans).

• Expected issuances of new l-t debt: $900 million - $1.3 billion.

2007

27

Drivers for Change in Earnings Per Share

• Return to normal weather

• Queens outage

• Other non-recurring items

• Sales growth

• Rate increases

• Regulatory amortizations

• Incremental capital carrying charge

• Competitive energy businesses

• Dilution

2006 2007

$3.05

$3.25

High

$3.05

Low

28

A Compelling Dividend Record: 33 Consecutive Years of Dividend Increases

Annualized Dividend 1975 - 2007

$0.50

$1.00

$1.50

$2.00

$2.50

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

$0.30

$2.32One of two utilities in S&P 500 with 25 or more consecutive years of dividend increases

2005

2007

$0.00

29

Total Return to Shareholders

Source: Bloomberg

Average Annual Total Return for Period Ended December 31, 2006

10 Year 25 Year5 Year

9.1

6.2

11.1

8.4

14.613.4

Con Edison

S&P 5009.1

15.8

1 Year

30

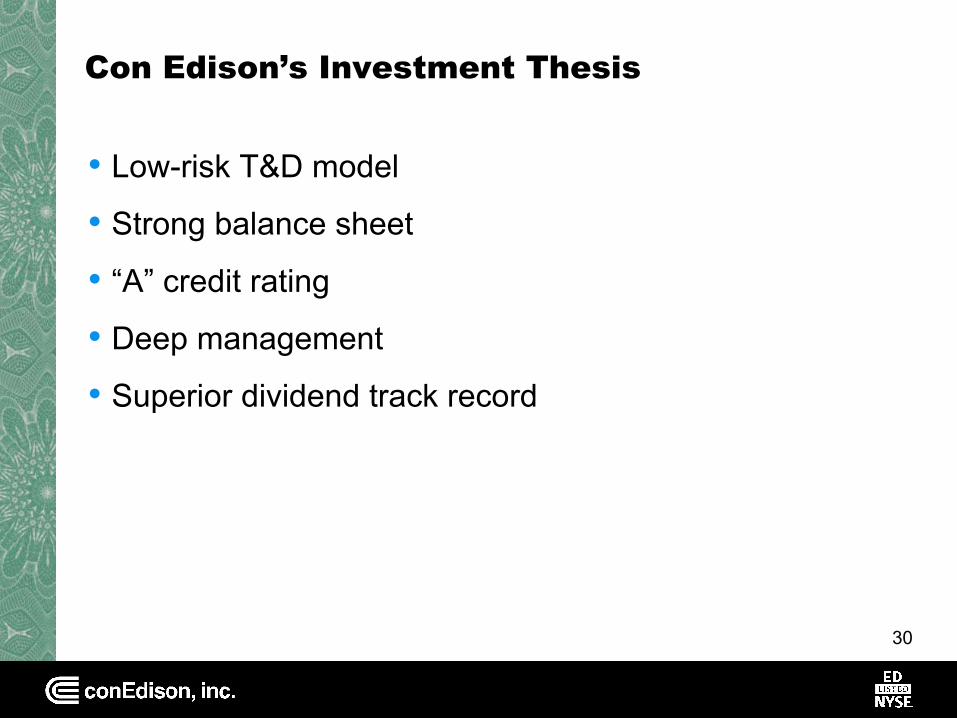

Con Edison’s Investment Thesis

• Low-risk T&D model

• Strong balance sheet

• “A” credit rating

• Deep management

• Superior dividend track record

31

Appendix

32

Con Edison of New York

Electric Apr. 2005 – Yr. 1 – $9.3 b Yr. 1 – $104.6 m Yr. 1 – $128 m $60 m of 11.40% 11.4% – 13% – 50/50Mar. 2008 Yr. 2 – $9.6 b Yr. 2 – None Yr. 2 – $173 m annual TCC >13% – 25/75

Yr. 3 – $10.3 b Yr. 3 – $220.4 m**** Yr. 3 – $249 m revenues

Gas Oct. 2004 – Yr. 1 – $2.0 b Yr. 1 – $46.8 m $41 m $35 m of 11.75% 50/50Sept. 2007 Yr. 2 – $2.1 b Yr. 2 – None over 3 yrs annual non-

Yr. 3 – $2.2 b Yr. 3 – None firm revenues

Steam Oct. 2006 – Yr. 1 – $1.3 b None $53 m — 11.00% 11% – 12% – 50/50 Sept. 2008 Yr. 2 – $1.3 b over 2 yrs >12% – 25/75

Orange and Rockland

Gas Nov. 2006 – Yr. 1 – $235 m Yr. 1 – $6.5 m $(3) m — 11.00% 11% – 12% – 50/50 Oct. 2009 Yr. 2 – $242 m Yr. 2 – $6.5 m over 3 yrs 12% – 14% – 35/65

Yr. 3 – $251 m Yr. 3 – $6.3 m >14% – 0/100

Summary of Rate Plans

Effective Rate Rate Amortization Other ROE Sharing Earnings Sharing Terms ***Period Base * Increases ** of Credits Increases Threshold (Shareholders/Customers)

* Under Con Edison of New York’s electric rate plan, the company is allowed to accrue a full return on increases in net electric transmission and distribution plant above the levels reflected in rates. For the period from April 1, 2005 through December 31, 2006, actual net transmission and distribution has exceeded the net transmission and distribution reflected in rates by $1 billion. The company accrued revenues of $115 million and $38 million in 2006 and 2005, respectively, to reflect the revenue requirement impact of net transmission and distribution difference.

** The Orange and Rockland gas rate plan provides for rate increases in base rates of $12 million in the first year, $0.7 million in the second year, and $1.1 million in the third year. To phase in the effect of the increase for customers, the rate plan provides for O&R to accrue revenues for, but defer billing to customers of, $5.5 million of the first rate year increase by establishing a regulatory asset which, together with interest, will be billed to customers in the second and third years. This chart reflects the phase-in of those rate increases.

*** Subject to limitation for cost reconciliations.

**** $60 million accrued to income in rate year two.

33

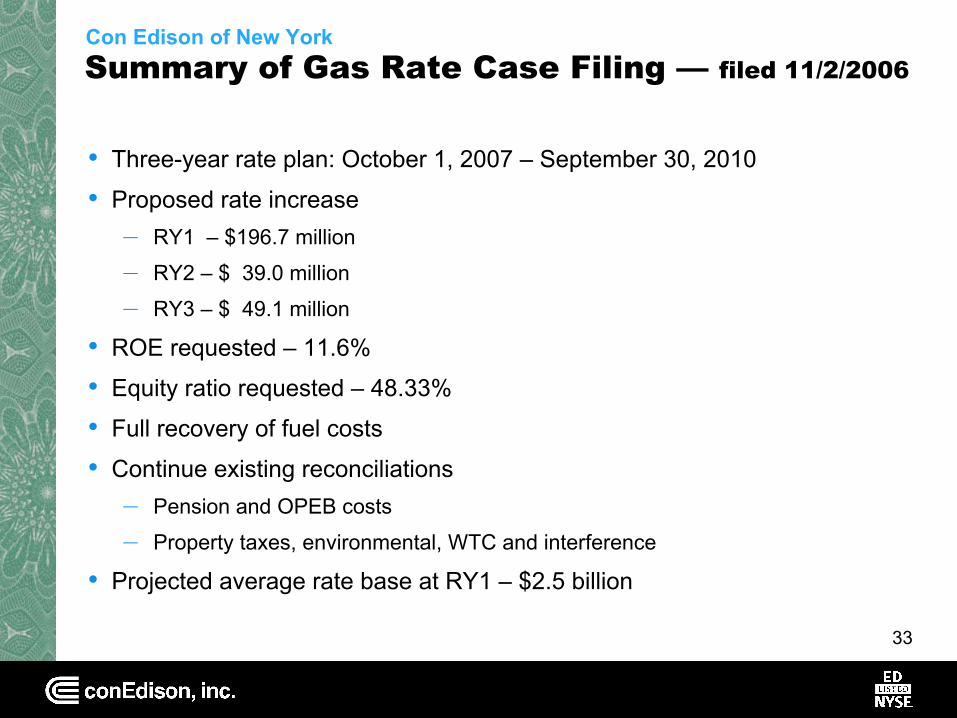

Summary of Gas Rate Case Filing — filed 11/2/2006

• Three-year rate plan: October 1, 2007 – September 30, 2010

• Proposed rate increase– RY1 – $196.7 million

– RY2 – $ 39.0 million

– RY3 – $ 49.1 million

• ROE requested – 11.6%

• Equity ratio requested – 48.33%

• Full recovery of fuel costs

• Continue existing reconciliations– Pension and OPEB costs

– Property taxes, environmental, WTC and interference

• Projected average rate base at RY1 – $2.5 billion

Con Edison of New York

34

Summary of Rockland Electric Rate Case Filing

• Filed on June 30, 2006 with New Jersey BPU

• One-year rate plan: April 2007 through March 2008

• Proposed rate increase of $13.2 million, or 7.5%

• ROE requested – 11.0%

• Equity ratio requested – 49.7%

• Proposed reconciliations– Pension and OPEB costs

• Projected T&D rate base at June 2007 – $153.2 million

Orange and Rockland

35

Summary of Gas Rate Plan

• Three year rate plan: November 1, 2006 – October 31, 2009

• Rate increases to be phased in over three years– RY1 – $6.5 million

– RY2 – $6.5 million

– RY3 – $6.3 million

• Continued full recovery of fuel costs

• Reconciliation of pension and OPEB costs, property taxes, and environmental costs

• 9.8% authorized ROE with earnings sharing threshold of 11%– Based on actual equity ratio – up to 50%

– Deferral limitation for earnings above 11%

• Potential penalties of $1.2 million geared toward gas safety performance and customer service

Orange and Rockland

36

Profit Model For a Cost-of-ServiceRate-Regulated Utility

• Capital spending leads to rate base growth, which generallyleads to net income growth

• Growth in rate base requires significant external financing

Debt Percent of Capital

Preferred Percent

of Capital

Common Percent

of Capital

Rate Base

Deferred taxes-Working capital+Regulatory items+/-

+

+

+

+

InterestRate

DividendRate

Cost ofEquity Net Income

Recovered

Recovered

Net Plant

37

Growing Earnings Through Infrastructure Investment — An Illustration

• We spend $1.8 billion each year in cap ex

• One-third, or nearly $600 million, is funded through depreciation

• The balance of $1.2 billion is funded 50/50 with debt/equity

• About one-third of the equity funding requirement is met with retained earnings

• Earnings on the total equity investment at 10% would be approximately $60 million

38

Con Edison’s Financing Activities

• Issued $447 million in common stock in September 2006

• Raised $120 million in equity through DRIP and employee stock plans

• Issued $1,200 million in Con Edison of New York bonds for general purposes

• Issued $500 million in Con Edison of New York bonds to redeem maturing bonds

• Issued $75 million of O&R bonds for general purposes

• Expected issuances of new equity: $500 million - $700 million (above issuances through DRIP and employee stock plans)

• Expected issuances of new l-t debt: $900 million - $1.3 billion

2006 2007

39

Unparalleled ReliabilityCon Edison of New York

2005 Customer Interruption Rate

0.00

0.140.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

0.410.50

0.64

0.79 0.81 0.84 0.90

1.11 1.13 1.18 1.21 1.24 1.261.37 1.39

1.811.88

2.41

Average Rate = 0.97

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19Con Edison

Major Utilities

Source: Salt River Project – Large City Survey

40

The Electric System

Generating Station(electricity generated at 13.8 to 22.0 kV)

Transformers(voltage stepped up to transmission voltage)

Transmission Substation

Area Substation(voltage stepped down to distribution voltage)

Transformers(voltage stepped down to 480, 208, or 120 V)

Feeders

Connection To Others

Network Customers(residential, commercial, industrial, hospitals, schools, and street and traffic lights)

Radial Customers

Transmission Distribution

Con Edison of New York

41

Meeting Customers’ Needs New York City Area Substation Capacity – 2006

Above 100%

95% to 100%

90% to 94%

below 90%

Con Edison of New York

42

Meeting Customers’ Needs New York City Area Substation Capacity – 2011

Con Edison of New York

Without Capital Projects With Capital Projects

Above 100%

95% to 100%

90% to 94%

below 90%

432002 – 2006 volumes are weather normalized

Firm Gas Delivery Volumes ForecastCon Edison of New York

BCF

2003 2004 2005 20062002 2007

98

101 101103 104

106

2008

109

Forecast

44

New York City EmploymentCon Edison of New York

2005

3,600

3,400

3,200

3,000

Thousands

20042003200220012000199919981997 2006

3,800

Source: New York State Department of Labor

45