Computing the Market Price of Volatility Risk in the Energy Commodity Markets

20

Computing the Market Price of Volatility Risk in the Energy Commodity Markets James S. Doran Department of Finance Florida State University Ehud I. Ronn Department of Finance University of Texas at Austin January 2007

Transcript of Computing the Market Price of Volatility Risk in the Energy Commodity Markets

Computing the Market Price of Volatility Risk in the Energy

Commodity MarketsJames S. Doran

Department of FinanceFlorida State University

Ehud I. RonnDepartment of Finance

University of Texas at Austin

January 2007

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

2

Outline and Overview

The relationship between implied and realized volatility in energy marketsInstantaneous parameter sensitivities demonstrated via quasi‐Monte‐Carlo simulationMarket price of volatility risk estimation

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

3

Motivation and ContributionBridge two strands of literature and extend one:

Quantify the bias between implied volatility and realized volatility Relate the bias in Black‐Scholes to the underlying parametersExtend our understanding of risk premium in energy markets

Relate the Market Price of Volatility Risk (λσ) to F<E(ST) for equitiesWhy option traders like to be shortF>E(ST) for commodities

Demonstrate the differences between commodity and equity markets

Positive skew in commodities marketsRelationship between price and volatility

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

4

Literature ReviewData Generating Process

Black‐Scholes (1972)Hull and White (1987), Heston (1993)Bates (1994, 1996), Duffie, Pan and Singleton (2000), Pan (2002)

Market Price of Volatility RiskCoval and Sumway (2001)Buraschi and Jackwerth (2001)Carr and Wu (2004)Doran (2007)

Energy RiskSchwartz (1997), Schwartz and Smith (2000)Hilliard and Reis (1998)Pindyck (1999)Casassus and Collin Dufresne (2005)Doran and Ronn (2006)

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

5

Preview of Results

The inclusion of a market price of volatility risk appears necessary to capture the degree of bias in BSIV/BIVThe market price of volatility risk is negative and significant for natural gas, crude oil, and heating oil. There is a seasonality in the volatility risk premium for natural gas

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

6

Pricing Dynamics

This is not a test of spot and futures price relationship

i.e, Schwartz (1997)

This is an option on futures

Start with traditional equity literature

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

7

Data Generating Process

Must have two distinct price treesRisk Neutral Process

Real World Process

Jump arrives at γdt for risk-neutral processJump arrives at γ(1−λ)dt for real world processJump size is drawn from N~(μj∗,σ2) for risk-neutral processJump size is drawn from N~(μj,σ2) for real world process

SV‐ModelSVJ0‐Model

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

8

Monte Carlo & Quasi Monte Carlo

Simulate processes over n pathN=30,000Sobol Sequence

( )∑=

− −=N

iTi

rT KSeN

Call1

* )0,max(1

),0(~,,,252/1

** tNdzdzdzdzt

sS Δ

Δ

σσ

=

TSSN

N

iTi ])/[ln(1

101 ∑

=

−= μσ

)(11

2,2 ∑

=

−=t

ktkt rr

τ

τσ

Implied Volatility

Realized Volatility

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

9

Simulated Volatility DifferenceThis table highlights the simulated percentage difference in Black implied volatility (BIV) versus realized volatility using the SVJ (stochastic volatility with jumps) model and the SVJ0 (stochastic volatility with jump but no market price of volatility risk) model. In each case the simulation is conducted over 30 days (22‐trading days) using the given futures

contract and a corresponding ATM option.

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

10

Volatility SkewFigure 1 demonstrates the simulated volatility difference between implied and realized

volatility across the cross‐section of option prices using the SVJ model.

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

11

Data

Daily observations for natural gas, crude oil, and heating oil futures and optionsContracts expiring between January 1995 through December 2005Use only close to ATM optionsData comes from Bloomberg and NYMEX

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

12

Descriptive Statistics for Monthly Energy ContractsThe number of observations for natural gas, crude oil, and heating oil are 26,843, 27,065,

and 22,827 respectively.

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

13

Implied Volatility in Energy MarketsFigure 2 demonstrates the implied volatility of the near‐term contract for the three energy commodities and VIX, the weighted average of implied volatility on near‐term S&P 500 option contracts. The implied volatility for each energy commodity comes

from the contract that is closest to maturity up until 10‐days to expiration. The second near‐term month then is used instead. HO is the implied volatility from heating oil contracts, CO is from crude oil contracts, and NG is from natural gas contracts. The

period is from January 1994 through April 2004.

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

14

Solving for the Instantaneous Parameters

Estimate the risk‐neutral parameters

Reciprocal specification to capture TSOVSimilar to Dennis, Mayhew, and Stivers (2006)Alternatively, to capture monthly effects using December as the base month

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

15Risk Neutral ParametersThis table reports the parameter estimates of the mean‐reverting regression for three energy commodities: natural gas, crude oil, and heating oil. The period uses daily frequency from monthly contracts between 1994 through 2005, over the period January 1994 through April 2004. Each commodity is estimated using equations (15‐16), where equation (16) controls for potential year effects. Monthly dummies, MON, are included for each of the j contract months, using December as thebase month. The term‐structure control uses a reciprocal specification, where DM is the number of days until maturity

divided by 360

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

16

Solving for the Volatility Risk Premium

Calibrate the data generating process by minimizing the difference between the estimated and actual implied and realized volatility

Done in a similar spirit to Bakshi, Cao, and Chen (1997) and Bates (2000)Estimate volatilities using quasi‐Monte Carlo and the given data‐generated process

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

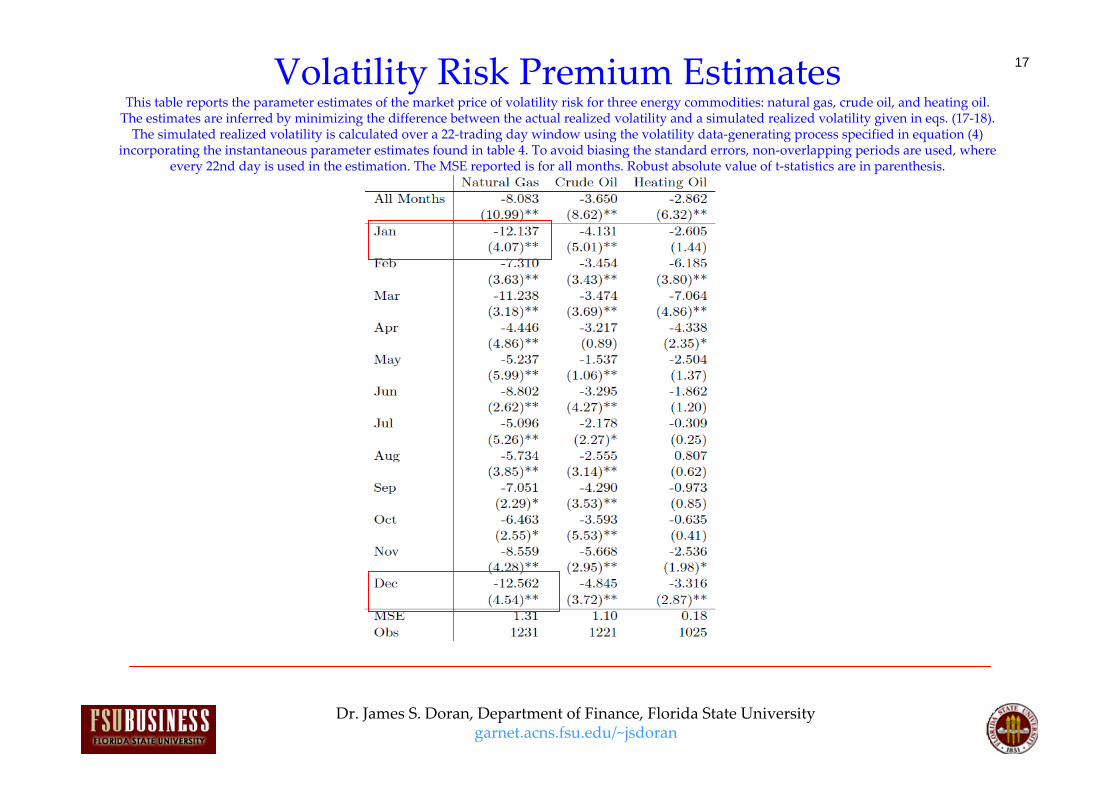

17Volatility Risk Premium EstimatesThis table reports the parameter estimates of the market price of volatility risk for three energy commodities: natural gas, crude oil, and heating oil. The estimates are inferred by minimizing the difference between the actual realized volatility and a simulated realized volatility given in eqs. (17‐18). The simulated realized volatility is calculated over a 22‐trading day window using the volatility data‐generating process specified in equation (4)

incorporating the instantaneous parameter estimates found in table 4. To avoid biasing the standard errors, non‐overlapping periods are used, where every 22nd day is used in the estimation. The MSE reported is for all months. Robust absolute value of t‐statistics are in parenthesis.

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

18

Robustness

Prior results place strong restrictions on the data generating processAdopt the Broadie, Chernov, and Johannes (2006) methodology, but ignore the jump premiumApply GMM methodology using both volatility and return

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

19

Risk Premium across Months

Dr. James S. Doran, Department of Finance, Florida State Universitygarnet.acns.fsu.edu/~jsdoran

20

Conclusions

A negative market price of volatility risk can explain the difference between implied and realized volatilityResults appear consistent with empirical observations

Additional supporting evidence for negative volatility risk premium

How important is the specificationPotential justification for option tradingOption price includes volatility premium