Comprehensive school counseling programs: A review for policy ...

Portland

Sacramento

Las Vegas

Phoenix

DenverKansas City

DetroitChicago

Memphis

Tulsa

DallasFort Worth

San Antonio Houston

Atlanta

Nashville

Louisville

Indianapolis

Morgantown

Cincinnati

Philadelphia

Minneapolis

PittsburghColumbus

Seattle

San Francisco

Austin

Milwaukee

Dayton

Hartford

Savannah

Columbia

Charlotte

Orlando

MiamiSarasota

Tampa

Boston

New York CityNorthern New JerseyCoastal New Jersey

Washington D.C.Baltimore

Richmond

Naples

Providence

Los Angeles

San Diego Greenville

IRR de México

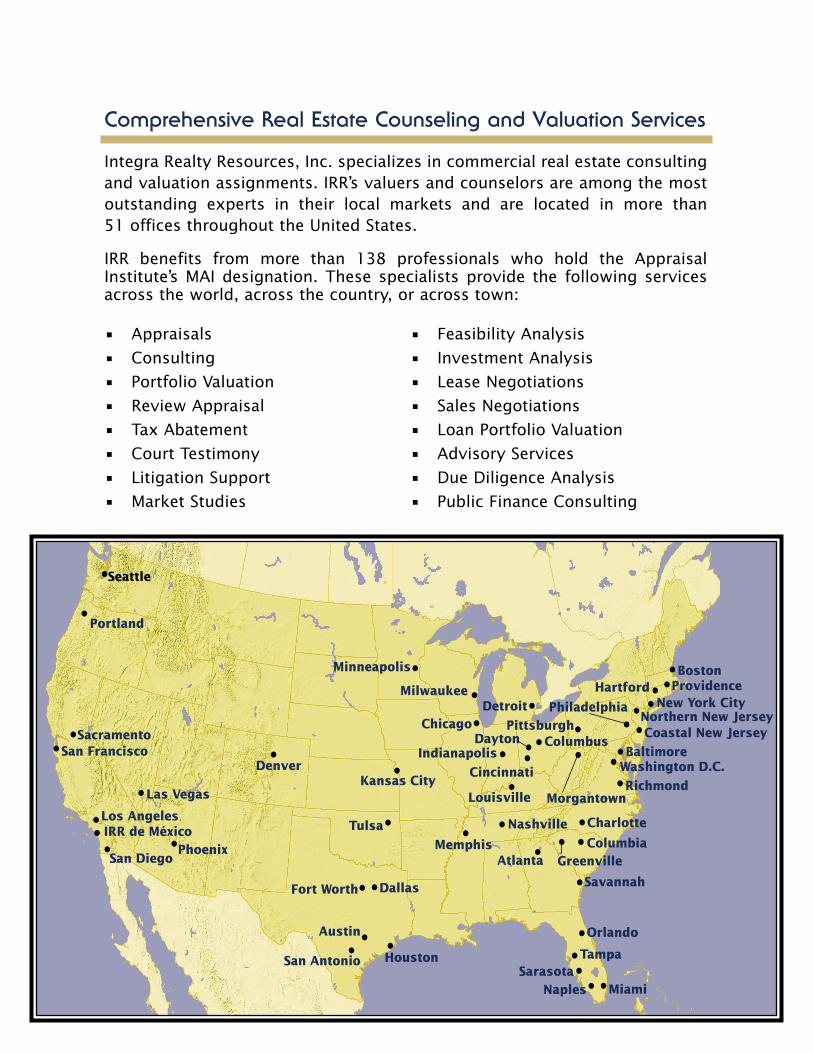

Comprehensive Real Estate Counseling and Valuation Services

Integra Realty Resources, Inc. specializes in commercial real estate consultingand valuation assignments. IRR’s valuers and counselors are among the mostoutstanding experts in their local markets and are located in more than 51 offices throughout the United States.

IRR benefits from more than 138 professionals who hold the AppraisalInstitute’s MAI designation. These specialists provide the following servicesacross the world, across the country, or across town:

• Appraisals

• Consulting

• Portfolio Valuation

• Review Appraisal

• Tax Abatement

• Court Testimony

• Litigation Support

• Market Studies

• Feasibility Analysis

• Investment Analysis

• Lease Negotiations

• Sales Negotiations

• Loan Portfolio Valuation

• Advisory Services

• Due Diligence Analysis

• Public Finance Consulting

VIEWPOINT 2005 INTEGRA REALTY RESOURCES, INC.

Dear Colleagues and Friends,

I am pleased to publish Viewpoint 2005, which is in its 15th consecu-tive year of print. Again this year we focus on the four food groups:office, retail, multifamily and industrial. Additional special reportswere prepared by Shelli Lowe and Anthony S. Graziano on gaming andJoe Pasquarella on lodging. This year we present our real estate trendsforecast in a similar format reflecting our views on the national realestate market and identifying where each major metropolitan area cur-rently is in the cycle.

We are pleased to announce that Jeffrey Rogers has been promotedfrom Chief Operating Officer to President of Integra Realty Resources.Jeffrey is responsible for the leadership of our 51 U.S. offices and twoin Mexico. We are proud of the fact that we continue our mantra “localexpertise nationally” providing services to financial institutions, cor-porations and the legal profession. Integra continues to focus on qual-ity control. In 2005 we will be launching integrated new softwarethroughout Integra that will allow the exchange of income andexpense data as well as lease and comparable sale informationthroughout our entire company.

Integra Realty Resources was further honored by the fact that I wasinvited to present to the Federal Reserve Board of Governors, includ-ing Alan Greenspan, Integra’s views on the residential real estate mar-ket for 2005. The presentation included forecasting potential bubblemarkets and the impact of those markets on the residential real estateindustry.

Finally, on behalf of Integra, I would like to wish each of you a healthyand prosperous 2005.

Very truly yours;

Kevin K. Nunnink, MAIEditor-in-ChiefChairman of the BoardIntegra Realty Resources, Inc.

CHAIRMAN’SLETTER

TABLE OF CONTENTS

National Real Estate Market..............2

Property Sector Cycles

New Investment Criteria ..5

Property Sector Cycles

Office, CBD & Suburban...9Gaming..........................14Lodging .........................15Retail .............................18Apartment .....................21Industrial .......................24

Demographic andEconomic Trends ..............27

Appendix .........................32

Local IRR Offices..back cover

NATIONAL REAL ESTATE

MARKETThe economic recovery is in full swing, but what itmeans for the real estate sector is the question. Lastyear IRR forecasted a “Yellow Flag Recovery.” IRRbelieves the economy is now hitting on all cylindersand IRR believes the GDP growth rate will range from3.5% – 4% in 2005. Reflecting on the last three months,approximately 300,000 jobs per month have been cre-ated in the U.S. decreasing the unemployment rate to5.4%.

When the economy is experiencing a “rising tide,” nor-mally one would expect the real estate sector to risewith all other boats. However, when dissecting the cap-ital markets IRR cautions both investors and lenders ofthe historical relationship of the 10-year treasury andthe Federal Funds rate. Reflecting on the recent FederalReserve actions, it is worthwhile to note the “Fed”reduced the Federal Funds rate 13 consecutive timesfrom 6.5% in May of 2000 to 1% in June of 2003.Considering inflation, this accommodative fiscal policycreated at times a zero cost of funds to borrowers dur-ing that period. Since June 2004, the Federal Reservehas increased rates from 1% to 2.25%. Presumably,these increases are in part to keep inflation in check asthe recovery heats up. While there are numerous exter-nalities affecting the 10-year treasury, a comparison ofthe direct relationship would suggest that the 10-yeartreasury will likely rise commensurate with the FederalFunds rate. Furthermore, it is widely speculated that

the equilibrium for the Federal Funds rate is approxi-mately 4%. In the early 1990’s the “delta” between thesetwo indices approximated 250 basis points. In the mid-dle to late 1990’s this spread narrowed to 50 to 100basis points. In the first portion of the 21st Century, thespread again widened to 250 to 300 basis points. Thus,Integra has forecasted that if the Federal Funds ratereturns to 4%, the 10-year treasury will range from4.75% to 5.25%, similar to the spreads observed duringthe mid to late 1990’s.

With most borrowing being pegged off the 10-year trea-sury and a median loan to value ratio of 75%, theimpact of the interest rates trends could be consider-able. Thus, Integra cautions investors and lenders tochart their debt course accordingly; either by hedgingtheir position or by locking in on a fixed rate mortgage.IRR counsels those investors that have “ridden theadjustable rate tide,” now is the time to “lock your rateor pay the price” in the years to come.

Other risks to consider when examining today’s econ-omy include:

• Energy: The U.S, which is an approximate $11.8Trillion dollar economy, imports approximately 4.5billion barrels of oil per year, thus every $10 per bar-rel (i.e. aggregate cost of $45 billion) increase in oilwould suggest a drop in the annual GDP growth rateof .4%. Threats of terrorism in the Middle East exposethe U.S. economy to this risk.

• Deficit: The current U.S. deficit is projected to be$422 billion in 2004, up from $375 billion in 2003.Financing the war in Iraq in the future will likely cause

0

1

2

3

4

5

6

7

8

9

10

Mar

-90

Mar

-91

Mar

-92

Mar

-93

Mar

-94

Mar

-95

Mar

-96

Mar

-97

Mar

-98

Mar

-99

Mar

-00

Mar

-01

Mar

-02

Mar

-03

Mar

-04

Mar

-05

Mar

-06

Effective Federal Funds Rate10 Year Treasury Yield

0

1

2

3

4

5

6

7

8

9

10

%%

Historical Projected

2 INTEGRA REALTY RESOURCES, INC. VIEWPOINT 2005

INTEREST RATETABLE 2

3.5

4

4.5

5

5.5

6

6.5

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

-400

-200

0

200

400

600

Rate Thousands of jobs

Nonfarm payroll employmentUnemployment Rate

SOURCE: Federal Reserve Bank

NEW JOBS CREATED BY THE ECONOMYTABLE 1

HISTORICAL SOURCE: Federal Reserve BankPROJECTED SOURCE: Integra Realty Resources, Inc.

the deficit to increase in the short term which couldbegin to substantially affect the price of debt instru-ments.

• Medical costs and funding retirement: Rising medicalcosts and the current underfunding of Social Securityare concerns and need to be dealt with before theseissues affect the economy on a go forward basis.

• Terrorism: Another catastrophic event in the U.S.could again cause another “economic flu” that is notpredictable in depth or impact.

ALTERNATIVE INVESTMENTS

CMBS MARKETU.S. volume was up 19.7% closing at $93.1 billion. Lastyear’s volume of $77.8 billion was also a record. Bankof America originated $11.6 billion and dethroned

-7

-6

-5

-4

-3

-2

-1

0

1

2

1970 1974 1978 1982 1986 1990 1994 1998 2002

-700

-600

-500

-400

-300

-200

-100

0

100

200

Percent Billions of $

Current Account

CA/GDP

NATIONAL REAL ESTATE MARKET

VIEWPOINT 2005 INTEGRA REALTY RESOURCES, INC. 3

J.P. Morgan Chase for first place in the league tables. J.P.Morgan lost first place by a meager $550 million.Morgan Stanley and Credit Suisse First Boston are virtu-ally in a dead heat for third and fourth place, both orig-inating approximately $10.5 billion.

REITSReal Estate Investment Trusts continue to dominate theinvesting sectors. The ALL REIT index returned 28.67%with the EQUITY REITS returning 29.88%. MORTGAGEREITs returned a respectable 16.01% while dealing withthe interest rate swing in 2004. IRR believes this REITsector will have difficulty continuing its recent returnsand investors should cautiously trade mortgage REITstocks.

Furthermore, IRR believes it will be difficult for theEquity REITs to continue the returns they have har-vested in the past five years; three-year average of22.32%, five-year 21.55%. IRR suggests the upside willbe selecting individual REIT stocks rather than theindexes. Attributes to look for in your favorite REITstock should be low debt levels, diversification of geo-graphic ownership that will insulate the REIT from cata-strophic events (hurricanes, terrorism, etc). IRR likesthe lodging and apartment sectors. The lodging sectorshould continue to benefit from the rebounding econ-omy and many of its gains are merely recovery from thepost-September 11th hangover. On the other hand, theapartment sector will benefit from the reboundingeconomy as well as the swing upward in interest rates.IRR believes the most challenged REIT sectors will beManufactured Homes, Health Care and MortgageFinancing.

INVESTMENT ALTERNATIVESYEAR S&P 500 BONDS* NCREIF** NAREIT

1994 1.3% 3.51% 6.4% 0.8%1995 37.5% 19.24% 7.7% 18.3%1996 23.0% 2.90% 10.3% 35.8%1997 33.2% 9.76% 10.9% 18.9%1998 28.58% 9.46% 16.14% -18.82%

1999 21.04% -2.15% 11.11% -6.48%

2000 -10.14% 11.84% 11.66% 17.74%

2001 -13.04% 8.5% 10.10% 12.83%

2002 -23.4% 9.15% 5.5% 3.6%

2003 26.4% 4.67% 7.84% 35.42%2004 9.0% 4.2% 12.42% 29.88%

SOURCE: *Lehman’s Government/Corporate Bond Index**NCREIF: Twelve-month return based on 3rd quarter 2004 reporting.

48.9

58.5

77.7

40.5

28.8

17.8

0

10

20

30

40

50

60

70

80

20001995 1996 1997 1998 1999

90

100

2001

74.4

2002

66.4

2003

77.8

2004

93.1

CMBS ISSUANCE ($ in Billions)

TABLE 5

SOURCE: Federal Reserve Bank

CURRENT ACCOUNT DEFICITTABLE 3

TABLE 4

SOURCE: CMSA & MBAA

NATIONAL REAL ESTATE MARKET

4 INTEGRA REALTY RESOURCES, INC. VIEWPOINT 2005

EXPECTATIONS FOR 2005Integra expects the office, industrial and apartmentsectors to continue their rebounding parallel with therecovery of the economy. Thus, expectations of signifi-cant gross revenue increases are expected. However,net yield to the investor will be a function of theamount of leverage in the transaction or pool of trans-actions. Gains in the top line revenue may be lost to thebottom line for properties with lots of leverage.

Owners of apartments seem to feel the worst is over.Generally, concessions are disappearing and increasinginterest rates in the single-family residential sector arecreating additional demand for rental units. Apartmentconversions to condos have also contributed to lesssupply. IRR acknowledges the office market is still softbut 2005 should provide the turning point for therecovery with corporations first absorbing under-utilized space followed by expansion in late 2005 and2006. However, due to the number of new buildingsunder construction in the major metropolitan areas IRRexpects a continued hangover for owners attempting tore-lease space that has been vacated. Tenants will stillperceive it as a tenant’s market and landlords will havedifficulty in pushing rents until late 2005 or early 2006.

This paradigm coupled with interest rate hikes will bechallenging in the office and industrial sectors.

In conclusion, IRR believes acceptable risk adjustedreturns will be commanded by the four main foodgroups in the real estate sector. However, apartmentsand retail will lead the recovery followed by industrialand then office. Those owners that are highly leveragedwill face some challenges of maintaining their bottomline, but generally the demand components willincrease as the economy gains momentum. IRRbelieves the cities with a 24-hour culture will continueto thrive as the empty nesters continue to leave the“burbs” for the vibrancy of the City. The hospitality andgaming sectors are both in for a banner 2005; however,the hospitality sector will primarily just recover some ofthe ground that it has lost during the past few years.The gaming sector on the other hand continues to caterto the “boomers” and the high risk adjusted returnscontinue to attract capital.

All in all the real estate “boat” should rise with the ris-ing tide of the economy, but Integra does not expect a“good times roll” mentality.

VIEWPOINT 2005 INTEGRA REALTY RESOURCES, INC. 5

PROPERTYSECTOR CYCLESNew Investment Criteria

Integra Realty Resources (IRR) takes a three-channelapproach in providing investors with appropriateinformation to make investment decisions. Our triad

of services — the Viewpoint publication, our website atwww.irr.com and market insights from our local IRRrepresentatives — help investors interpret the realestate environment, both nationally and locally.

Viewpoint provides a broad introduction to the currentnational real estate environment while selectively direct-ing a spotlight at several hot spots on the horizon.

Investors drill down more at www.irr.com where theycan access a collection of comprehensive, moredetailed and regularly updated data. In addition,updates for property type and submarket are availableat www.irr.com/IRR-Pulse.

Investors dig even deeper when they turn to local IRRrepresentatives for help in defining local and submar-ket risks and opportunities in all MSA’s. Examples ofspecialized information available from our representa-tives for some MSA’s and their submarkets are pre-sented in Quick Market Glance in the individualproperty sector segments in this section of Viewpoint.

Our broad look focuses on promising MSA’s that are inexpansion phases. However, even in those top markets,an isolated submarket could be in a recessionaryphase. We think this is important so we’ll say it again.To get more targeted information about specific sub-markets, consult a local IRR representative. To make themost informed real estate investment decision,investors ideally would use all resources made avail-able by IRR.

In the following pages, we discuss these designatedproperty sectors: CBD and suburban office, gaming,lodging, retail, apartment and industrial. We feature mar-ket cycle and cap rate trends charts in only four of thoseproperty sectors: office, retail, apartment and industrial.

MARKET CYCLE PHASESThe four market cycle phases include:

• Recovery: decreasing vacancy rates; low new con-struction; moderate absorption; and low to moderateemployment growth

• Expansion: decreasing vacancy rates; moderate tohigh new construction; high absorption; and moder-ate to high employment growth

• Hypersupply: increasing vacancy rates; moderate tohigh new construction; low to negative absorption;and moderate to low employment growth

• Recession: increasing vacancy rates; moderate tolow new construction; low absorption; and low tonegative employment growth

We determine the position of each market by analyzingvacancy rate trends, new construction starts, fore-

PROJECTED CAP RATE CHANGEProperty Type Decline (%) Increase (%) Stable (%)

CBD Office 17.0 8.5 74.5Suburban Office 22.4 10.2 67.3Regional Mall 20.0 8.9 71.1Community Mall 18.4 10.2 71.4Neighborhood Strip 18.4 14.3 67.3Manufacturing 4.3 14.9 80.9Bulk 12.5 4.2 83.3Office/Warehouse 22.4 6.1 71.4R&D 4.2 6.3 89.6Urban Multi Family 14.9 17.0 68.1Suburban Multi Family 16.3 18.4 65.3CBD Lodging 31.9 4.3 63.8Suburban Lodging 31.3 4.2 64.6Airport Lodging 30.4 4.3 65.2AVERAGE 18.9 9.4 71.7

TABLE 7

2004 CAP RATE RANKS2004 2004 Low 2004 High 2004 Avg.Rank Property Type (%) (%) (%)

1 Suburban Multi Family 5.0 9.5 7.492 Urban Multi Family 5.9 10.5 7.623 Regional Mall 6.0 10.0 7.984 Community Mall 7.0 10.0 8.295 Neighborhood Strip 6.5 10.8 8.376 CBD Office 6.8 10.5 8.717 Office/Warehouse 7.5 10.5 8.748 Suburban Office 6.6 11.0 8.799 Bulk 7.3 11.0 8.8210 R&D 7.0 10.5 9.1511 Manufacturing 7.5 11.0 9.3412 CBD Lodging 9.0 12.0 10.2313 Airport Lodging 9.0 12.0 10.4814 Suburban Lodging 8.5 12.0 10.48

TABLE 6

INVESTMENT CRITERIA

6 INTEGRA REALTY RESOURCES, INC. VIEWPOINT 2005

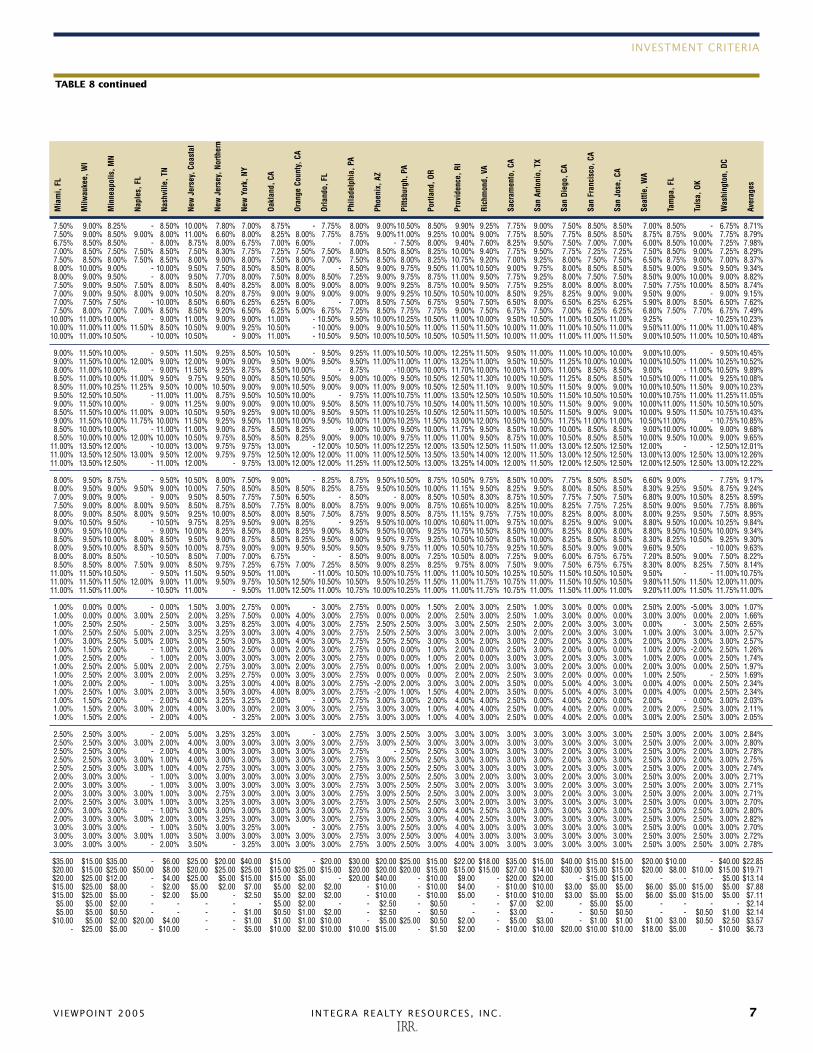

CBD Office 9.00% 9.00% 8.50% 8.00% 8.75% 7.50% 9.25% 9.00% 9.50% 9.00% 10.50% 8.00% 10.00% 9.00% 9.50% 9.25% 9.00% 10.00% 8.50% 8.50% 8.50% 9.00% 10.00%Suburban Office 8.50% 9.50% 8.50% 9.00% 9.00% 9.50% 9.50% 9.50% 9.50% 9.25% 9.50% 8.50% 9.00% 9.25% 9.80% 9.25% 8.50% 9.00% 8.00% 8.25% 8.00% 9.00% 9.00%Regional Mall 8.00% 8.00% 8.00% 8.00% 7.50% 7.50% 8.00% 8.50% 8.50% 7.75% 10.00% 7.50% 8.75% 8.00% 8.50% 8.00% 8.00% 9.00% 9.00% 7.75% 8.00% 8.00% -Community Mall 8.50% 8.50% 8.50% 8.50% 8.00% 8.00% 7.75% 8.75% 8.75% 8.75% 9.50% 8.00% 9.00% 8.75% 8.75% 9.00% 8.50% 9.50% 8.50% 8.00% 8.00% 9.00% 8.50%Neighborhood Strip 8.75% 9.50% 8.00% 8.50% 8.50% 8.50% 8.25% 8.25% 8.75% 9.00% 9.50% 8.50% 9.00% 9.00% 8.80% 9.25% 8.50% 9.50% 8.50% 8.00% 8.00% 8.00% 9.50%Manufacturing 9.50% 10.00% 9.00% 9.00% 9.25% 9.00% 9.00% 10.25%11.00% 9.00% 11.00% 9.00% 9.75% 9.00% 10.50% 11.00% 10.00% 10.50% 8.50% 9.25% 9.00% 9.80% 9.00%Bulk 9.00% 10.50% 8.00% 9.00% 9.00% 8.00% 8.75% 9.75% 9.50% 8.50% 10.50% 9.00% 9.75% 8.50% 9.50% 11.00% 8.00% 9.00% 8.50% 8.25% 8.00% 9.50% 8.50%Office/Warehouse 9.00% 10.50% 8.00% 9.00% 9.00% 8.00% 8.50% 9.50% 9.50% 8.50% 10.50% 8.80% 9.25% 8.50% 9.00% 10.50% 9.00% 9.50% 8.50% 8.50% 8.50% 9.00% 8.50%R&D 9.00% 10.00% 8.50% 9.00% - 9.00% 9.00% 10.25%10.00% 9.00% 10.50% 9.00% 8.75% 9.00% 9.50% 10.00% 9.00% 9.50% 8.50% 8.75% 8.50% 9.80% 9.00%Urban Multi Family 8.50% 8.50% 7.00% 8.00% 6.50% 7.00% 8.50% 8.50% 8.50% 7.00% 10.50% 6.00% 9.00% 7.25% 8.25% 8.50% 8.00% 9.50% 8.00% 8.25% 7.00% 8.50% 6.75%Suburban Multi Family 8.50% 8.50% 7.00% 7.00% 6.50% 7.00% 8.00% 8.00% 8.00% 7.25% 9.50% 6.50% 8.25% 7.50% 8.30% 9.25% 7.50% 8.50% 7.50% 6.75% 6.50% 8.00% 6.75%CBD Lodging 10.50% 11.00% 10.00% 10.00% 9.50% 10.50% 11.50% 10.50% 9.50% 10.00% 12.00% 9.50% 11.50% 10.00% 11.00% 9.50% 10.50% 11.00% 9.00% 9.25%10.00% 10.00% -Suburban Lodging 10.50% 11.00% 10.50% 10.00% 9.50% 11.50% 11.00% 10.50%10.50% 10.00% 11.50% 10.00% 11.50% 10.00% 11.00% 11.00% 11.00% 12.00% 9.00% 9.00%10.00% 12.00% -Airport Lodging 11.00% 11.00% 10.50% 10.00% 9.50% 10.50% 11.00% 10.50%10.50% 10.50% 12.00% 10.00% 10.50% 10.50% 10.50% 11.00% 10.75% 12.00% 9.00% 9.00%11.00% 10.00% -

CBD Office 11.00% 11.00% 10.50% 10.50%10.25% 10.00% 11.25% 11.25%10.50% 10.75% 12.50% 10.00% 10.50% 10.75% 12.00% 10.75% 10.50% 10.50% 11.00% 9.50%10.50% 10.50% 11.00%Suburban Office 10.50% 11.00% 10.50% 11.00%10.50% 11.00% 11.50% 11.00%10.50% 10.75% 11.50% 10.50% 10.25% 10.75% 13.00% 10.75% 10.00% 10.50% 11.00% 9.25%10.00% 10.50% 10.00%Regional Mall 9.00% 10.00% 10.00% 10.00% 9.00% 10.00% 10.00% 10.75% 9.00% 10.25% 12.00% 9.50% 10.50% 10.25% 10.00% 9.50% 9.50% 10.00% 11.00% 8.75%10.00% 10.00% -Community Mall 9.50% 11.00% 10.50% 10.00% 9.50% 10.50% 9.75% 11.00%10.00% 10.25% 11.50% 10.00% 10.50% 10.25% 10.50% 10.50% 9.50% 10.50% 11.00% 9.00%10.00% 9.80% 10.00%Neighborhood Strip 9.75% 11.00% 10.00% 10.00%10.00% 10.50% 10.25% 10.50%10.00% 10.50% 11.00% 10.25% 10.50% 10.50% 11.00% 10.75% 10.00% 11.50% 11.00% 9.00%10.00% 10.50% 11.00%Manufacturing 10.50% 11.50% 11.00% 10.50%10.75% 11.00% 11.00% 11.50%11.50% 11.00% 13.00% 11.00% 11.50% 11.00% 14.00% 12.50% 12.00% 12.50% 11.00% 10.00%11.00% 10.20% 11.00%Bulk 10.00% 11.50% 10.00% 10.50%10.50% 11.00% 10.75% 10.50%11.00% 10.25% 12.50% 10.50% 11.00% 10.50% 13.00% 12.00% 9.50% 11.00% 11.00% 9.00%10.00% 10.80% 10.50%Office/Warehouse 10.00% 11.00% 10.00% 10.50%10.50% 11.00% 10.50% 10.50%11.00% 10.25% 12.50% 10.00% 11.00% 10.50% 12.00% 12.00% 10.50% 11.00% 11.00% 9.25%10.50% 10.50% 10.50%R&D 10.00% 11.00% 10.50% 10.50% - 12.00% 11.00% 11.50%11.00% 11.00% 12.50% 10.50% 10.50% 11.00% 13.00% 11.50% 10.50% 11.50% 11.00% 9.50%10.50% 10.80% 11.00%Urban Multi Family 10.00% 10.00% 9.00% 10.00% 8.50% 9.00% 10.50% 10.50%10.00% 9.25% 12.50% 9.50% 9.50% 9.50% 10.50% 9.50% 9.50% 10.00% 11.00% 9.25% 9.50% 9.50% 10.00%Suburban Multi Family 10.00% 10.00% 9.00% 10.00% 8.50% 9.00% 10.00% 10.50%10.00% 9.50% 11.50% 9.50% 9.25% 9.75% 10.00% 10.75% 9.00% 9.00% 11.00% 9.00% 9.00% 8.80% 10.00%CBD Lodging 12.00% 12.00% 12.00% 12.50%11.75% 12.00% 13.50% 12.25%12.00% 12.00% 14.00% 11.75% 12.50% 12.00% 14.00% 11.00% 12.50% 12.50% 11.00% 9.50%12.00% 13.00% -Suburban Lodging 12.00% 12.00% 12.50% 12.50%11.75% 13.00% 13.00% 12.25%13.50% 12.00% 13.50% 11.75% 12.00% 12.00% 14.00% 13.00% 12.50% 13.50% 11.00% 9.25%12.00% 13.50% -Airport Lodging 12.50% 12.00% 12.50% 12.50%11.75% 10.50% 13.00% 12.25%13.50% 12.00% 14.00% 11.75% 11.50% 12.00% 13.50% 12.50% 12.50% 13.50% 11.00% 9.25%13.00% 13.00% -

CBD Office 9.50% 9.50% 9.50% 8.50% 9.25% 8.00% 9.50% 9.50%10.00% 9.50% 11.00% 8.50% 10.25% 9.50% 10.00% 9.75% 9.50% 10.50% 9.00% 9.00% 9.00% 9.50% 10.25%Suburban Office 9.50% 10.00% 9.50% 9.50% 9.50% 10.00% 9.75% 10.00%10.00% 9.75% 10.00% 9.00% 9.50% 9.75% 10.30% 9.75% 9.00% 9.50% 8.50% 8.75% 8.50% 9.50% 9.25%Regional Mall 8.75% 8.50% 9.00% 8.50% 8.00% 7.50% 8.25% 9.00% 9.00% 8.25% 12.00% 8.00% 9.25% 8.50% 9.00% 8.50% 8.50% 9.50% 9.50% 8.00% 8.50% 8.60% -Community Mall 9.00% 9.50% 9.50% 9.00% 8.50% 8.00% 8.00% 9.25% 9.25% 9.50% 10.00% 8.75% 9.50% 9.50% 9.00% 9.50% 9.00% 10.00% 9.00% 8.50% 8.50% 10.50% 8.75%Neighborhood Strip 9.25% 10.50% 9.00% 9.00% 9.00% 8.50% 8.50% 8.50% 9.25% 9.50% 10.00% 8.75% 9.50% 9.50% 9.30% 9.75% 9.00% 10.00% 9.00% 8.50% 8.50% 9.20% 9.75%Manufacturing 10.00% 10.50% 10.00% 9.50% 9.75% 9.50% 9.25% 10.75%11.50% 9.50% 11.50% 9.50% 10.00% 9.50% 11.00% 11.50% 11.00% 11.00% 9.00% 10.00% 9.50% 10.00% 9.50%Bulk 9.50% 11.00% 9.00% 9.50% 9.50% 8.50% 9.00% 10.00%10.00% 9.00% 11.00% 9.50% 10.00% 9.00% 10.00% 11.00% 8.50% 9.50% 9.00% 8.75% 8.50% 10.00% 9.00%Office/Warehouse 9.50% 11.00% 9.00% 9.50% 9.50% 8.50% 8.75% 9.75%10.00% 9.00% 11.00% 9.25% 9.75% 9.00% 9.50% 11.00% 9.50% 10.00% 9.00% 8.75% 9.00% 10.00% 9.00%R&D 9.50% 10.50% 9.50% 9.50% - 9.50% 9.25% 10.75%10.50% 9.50% 11.00% 9.50% 9.25% 9.50% 10.00% 11.00% 9.50% 10.00% 9.00% 9.00% 9.00% 10.20% 9.50%Urban Multi Family 9.50% 9.00% 8.00% 8.50% 7.25% 7.50% 8.75% 8.75% 9.00% 7.50% 11.00% 6.50% 9.25% 7.75% 8.80% 8.50% 8.50% 10.00% 8.50% 8.75% 7.50% 8.70% 7.00%Suburban Multi Family 9.50% 9.00% 8.00% 7.50% 7.25% 7.50% 8.25% 8.25% 9.00% 7.75% 10.00% 7.00% 9.00% 8.00% 8.80% 9.75% 8.00% 9.00% 8.00% 7.75% 7.00% 8.20% 7.00%CBD Lodging 11.00% 11.50% 11.00% 10.50% 9.75% 10.75% 11.75% 11.00%10.00% 11.00% 13.00% 10.00% 12.00% 11.00% 11.20% 10.00% 11.00% 11.50% 9.50% 9.50%10.50% 13.00% -Suburban Lodging 11.00% 11.50% 11.50% 10.50% 9.75% 11.75% 11.25% 11.00%11.00% 11.00% 12.50% 10.50% 12.00% 11.00% 11.50% 12.00% 11.50% 12.50% 9.50% 9.25%10.50% 12.50% -Airport Lodging 12.00% 11.50% 11.50% 10.50% 9.75% 10.75% 11.25% 11.00%11.00% 11.50% 13.00% 10.50% 11.00% 11.50% 11.00% 11.50% 11.25% 12.50% 9.50% 9.25%11.50% 10.50% -

CBD Office 2.00% 0.00% 2.00% 0.00% 0.00% 2.50% 0.00% 0.00% 3.00% 0.00% 2.00% 0.00% -2.00% 0.00% 0.00% 0.00% 1.00% 3.00% 2.00% 2.75% 1.00% 0.50% 1.00%Suburban Office 2.00% 0.00% 2.00% 0.00% 0.00% 0.00% 1.00% 0.00% 3.00% 0.00% 3.00% 0.00% 0.00% 2.00% 0.00% 0.00% 5.00% 2.00% 3.00% 2.75% 2.00% 0.50% 2.00%Regional Mall 2.00% 5.00% 3.00% 2.50% 2.50% 2.00% 2.00% 3.00% 3.00% 3.00% 2.00% 3.00% 0.00% 0.00% 3.00% 2.00% 2.50% 3.00% 3.00% 3.25% 3.00% 2.00% -Community Mall 2.00% 5.00% 3.00% 3.00% 2.50% 2.00% 2.00% 2.00% 3.00% 2.00% 2.00% 3.00% 0.00% 3.00% 0.00% 2.00% 2.50% 3.00% 3.00% 3.25% 2.50% 2.00% 2.00%Neighborhood Strip 2.00% 3.00% 3.00% 3.00% 2.50% 2.00% 2.00% 1.00% 3.00% 3.00% 3.00% 3.00% 0.00% 3.00% 0.00% 2.00% 2.50% 3.00% 3.00% 3.00% 2.50% 2.50% 2.00%Manufacturing 1.50% 0.00% 3.00% 0.00% 0.00% 2.00% 1.00% 0.00% 3.00% 2.50% 1.00% 3.00% -2.50% 2.50% 0.00% 0.00% 0.00% 0.00% 2.50% 2.75% 0.00% 1.00% 2.50%Bulk 1.50% 0.00% 3.00% 0.00% 0.00% 2.00% 0.00% 1.00% 3.00% 3.00% 1.00% 3.00% -2.00% 3.00% 0.00% 2.00% 1.50% 3.00% 2.50% 3.00% 2.00% 1.00% 2.50%Office/Warehouse 1.50% 0.00% 3.00% 1.50% 0.00% 2.00% 1.00% 1.00% 3.00% 3.00% 2.00% 3.00% 0.00% 3.00% 2.00% 2.00% 1.25% 2.00% 2.50% 3.00% 2.00% 1.00% 2.50%R&D 1.50% 0.00% 3.00% 0.00% - 2.00% 1.00% 1.00% 3.00% 0.00% 2.00% 3.00% 0.00% 0.00% 2.00% 2.00% 1.25% 2.00% 2.50% 2.75% 2.00% 1.00% 2.50%Urban Multi Family 2.00% 3.00% 2.50% 1.50% 0.00% 1.00% 2.00% 2.00% 3.00% 0.00% 2.00% 3.00% 0.00% 0.00% 3.00% 2.00% 5.00% 3.00% 5.00% 2.75% 3.00% 1.50% 2.00%Suburban Multi Family 2.00% 3.00% 2.50% 1.50% 0.00% 1.00% 2.00% 2.00% 3.00% 0.00% 2.00% 3.00% 1.50% 0.00% 4.00% 2.00% 5.00% 3.00% 5.00% 3.00% 3.00% 1.00% 0.00%CBD Lodging 3.50% 0.00% 3.00% 3.00% 0.00% 2.00% 2.00% 1.00% 3.00% 0.00% 2.00% 2.00% -1.50% 0.00% 5.00% 2.00% 2.50% 0.00% 1.00% 3.00% 1.00% 2.50% -Suburban Lodging 3.50% 0.00% 3.00% 3.00% 0.00% 2.00% 2.00% 1.00% 3.00% 0.00% 2.00% 2.00% 0.00% 0.00% 5.00% 0.00% 2.50% 0.00% 1.00% 3.25% 3.00% 2.00% -Airport Lodging 3.00% 0.00% 3.00% 3.00% 0.00% 2.00% 2.00% 1.00% 3.00% 0.00% 2.00% 2.00% 0.00% 0.00% 5.00% 0.00% 2.50% 0.00% 1.00% 3.00% 2.00% 2.50% -

CBD Office 2.50% 3.00% 3.00% 3.00% 2.75% 3.00% 2.00% 3.00% 3.00% 3.00% 2.00% 3.00% 2.50% 3.00% 3.00% 2.00% 2.75% 3.00% 3.00% 3.00% 3.00% 2.50% 2.00%Suburban Office 2.50% 3.00% 3.00% 3.00% 2.75% 2.00% 2.00% 3.00% 3.00% 3.00% 2.00% 3.00% 2.50% 3.00% 3.00% 2.00% 2.75% 3.00% 3.00% 2.75% 3.00% 3.00% 2.00%Regional Mall 2.50% 3.00% 3.00% 3.00% 2.50% 2.00% 2.00% 3.00% 3.00% 3.00% 2.00% 3.00% 2.50% 3.00% 3.00% 2.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% -Community Mall 2.50% 3.00% 3.00% 3.00% 2.50% 2.00% 2.00% 3.00% 3.00% 3.00% 2.00% 3.00% 2.50% 3.00% 3.00% 2.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.00%Neighborhood Strip 2.50% 3.00% 3.00% 3.00% 2.50% 2.00% 2.00% 3.00% 3.00% 3.00% 2.00% 3.00% 2.50% 3.00% 3.00% 2.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.00%Manufacturing 2.50% 3.00% 3.00% 3.00% 2.50% 2.00% 2.00% 3.00% 3.00% 3.00% 2.00% 3.00% 2.50% 3.00% 3.00% 2.00% 3.00% 3.00% 3.00% 2.75% 3.00% 3.00% 2.50%Bulk 2.50% 3.00% 3.00% 3.00% 2.50% 2.00% 2.00% 3.00% 3.00% 3.00% 2.00% 3.00% 2.50% 3.00% 3.00% 2.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.50%Office/Warehouse 2.50% 3.00% 3.00% 3.00% 2.50% 2.00% 2.00% 3.00% 3.00% 3.00% 2.00% 3.00% 2.50% 3.00% 3.00% 2.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.50%R&D 2.50% 3.00% 3.00% 3.00% - 2.00% 2.00% 3.00% 3.00% 3.00% 2.00% 3.00% 2.50% 3.00% 3.00% 2.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.50%Urban Multi Family 2.50% 3.00% 3.00% 3.00% 2.75% 2.00% 2.00% 3.00% 3.00% 3.00% 2.00% 3.00% 2.50% 3.00% 3.00% 2.00% 2.75% 3.50% 3.00% 3.25% 3.00% 3.00% 2.50%Suburban Multi Family 2.50% 3.00% 3.00% 3.00% 2.75% 2.00% 2.00% 3.00% 3.00% 3.00% 2.00% 3.00% 2.50% 3.00% 3.00% 2.00% 2.75% 3.00% 3.00% 3.00% 3.00% 3.00% 2.50%CBD Lodging 2.50% 3.00% 3.00% 3.00% 2.75% 3.00% 2.00% 3.00% 3.00% 3.00% 2.00% 2.00% 2.50% 3.00% 3.00% 2.00% 3.00% 0.00% 2.00% 3.00% 3.00% 3.00% -Suburban Lodging 2.50% 3.00% 3.00% 3.00% 2.75% 3.00% 2.00% 3.00% 3.00% 3.00% 2.00% 2.00% 2.50% 3.00% 3.00% 2.00% 3.00% 0.00% 2.00% 3.00% 3.00% 1.00% -Airport Lodging 2.50% 3.00% 3.00% 3.00% 2.75% 3.00% 2.00% 3.00% 3.00% 3.00% 2.00% 2.00% 2.50% 3.00% 3.00% 2.00% 3.00% 0.00% 2.00% 3.00% 3.00% 3.00% -

CBD Office $23.00 $20.00 $25.00 $20.00 $15.00 $35.00 $15.00 $20.00 $20.00 $20.00 $15.00 $25.00 $20.00 $20.00 $25.00 $20.00 $20.00 $30.00 $40.00 $25.00 $35.00 $30.00 $25.00Suburban Office $17.50 $17.00 $20.00 $10.00 $15.00 $25.00 $15.00 $15.00 $20.00 $20.00 $22.00 $25.00 $12.50 $20.00 $20.00 $15.00 $15.00 $25.00 $40.00 $20.00 $25.00 $25.00 $25.00Regional Mall - $20.00 - $2.00 - $10.00 $15.00 $15.00 - $25.00 $22.00 $2.00 $7.00 $25.00 $10.00 $25.00 $10.00 - $30.00 $25.00 $5.00 $50.00 -Community Mall $10.00 $10.00 - $2.00 - $10.00 $10.00 $10.00 - $15.00 $17.00 $4.00 $5.00 $17.00 $5.00 $12.00 $10.00 - $30.00 $5.00 $5.00 $20.00 $20.00Neighborhood Strip $10.00 $9.00 - $2.00 - $10.00 $5.00 $5.00 - $16.00 $15.00 $4.00 $7.00 $16.00 $5.00 $8.00 $5.00 - $30.00 $2.00 $5.00 $15.00 $20.00Manufacturing - $4.00 - - - $5.00 - - - $1.00 $8.00 $1.00 - $3.00 - - - - $30.00 - $2.50 - $1.00Bulk $1.00 $2.00 $1.00 - - $5.00 - - - $3.00 $8.00 $1.00 - $3.00 - - $0.50 - $30.00 - $1.50 $20.00 $1.00Office/Warehouse $2.00 $2.00 $2.00 - - $5.00 - - - $2.50 $8.00 $1.00 $3.00 $3.00 - $5.00 $1.00 - $30.00 - $2.50 - $1.00R&D - $5.00 $9.00 $5.00 - $5.00 - - - $5.00 $13.00 $5.00 $7.00 $5.00 - $4.00 $1.00 $5.00 $30.00 - $2.00 $25.00 $2.00

Atla

nta,

GA

Aust

in, T

X

Balti

mor

e, M

D

Bost

on, M

A

Char

lotte

, NC

Chic

ago,

IL

Cinc

inna

ti, O

H

Colu

mbi

a, S

C

Colu

mbu

s, O

H

Dalla

s, T

X

Dayt

on, O

H

Denv

er, C

O

Detro

it, M

I

Fort

Wor

th, T

X

Hartf

ord,

CT

Hous

ton,

TX

Indi

anap

olis

, IN

Kans

as C

ity, K

S/M

O

Las

Vega

s, N

V

Long

Isla

nd, N

Y

Los

Ange

les,

CA

Loui

svill

e, K

Y

Mem

phis

, TN

GOIN

G-IN

CAP

E RA

TE (%

)GO

ING-

IN D

ISCO

UNT

RATE

(%)

REVE

RSIO

NCA

PRA

TE (%

)M

ARKE

T RE

NT IN

FLAT

OR (%

)EX

PENS

EGR

OWTH

RATE

(%)

TENA

NT F

INIS

HAL

LOW

ANCE

($)

Property Types

CAPITALIZATION RATES, DISCOUNT RATES, REVERSION RATES, MARKET RENT CHANGE RATES, EXPENSE GROWTH RATES AND TENANT FINISH ALLOWANCES

TABLE 8

7.50% 9.00% 8.25% - 8.50% 10.00% 7.80% 7.00% 8.75% - 7.75% 8.00% 9.00%10.50% 8.50% 9.90% 9.25% 7.75% 9.00% 7.50% 8.50% 8.50% 7.00% 8.50% - 6.75% 8.71%7.50% 9.00% 8.50% 9.00% 8.00% 11.00% 6.60% 8.00% 8.25% 8.00% 7.75% 8.75% 9.00%11.00% 9.25% 10.00% 9.00% 7.75% 8.50% 7.75% 8.50% 8.50% 8.75% 8.75% 9.00% 7.75% 8.79%6.75% 8.50% 8.50% - 8.00% 8.75% 8.00% 6.75% 7.00% 6.00% - 7.00% - 7.50% 8.00% 9.40% 7.60% 8.25% 9.50% 7.50% 7.00% 7.00% 6.00% 8.50% 10.00% 7.25% 7.98%7.00% 8.50% 7.50% 7.50% 8.50% 7.50% 8.30% 7.75% 7.25% 7.50% 7.50% 8.00% 8.50% 8.50% 8.25% 10.00% 9.40% 7.75% 9.50% 7.75% 7.25% 7.25% 7.50% 8.50% 9.00% 7.25% 8.29%7.50% 8.50% 8.00% 7.50% 8.50% 8.00% 9.00% 8.00% 7.50% 8.00% 7.00% 7.50% 8.50% 8.00% 8.25% 10.75% 9.20% 7.00% 9.25% 8.00% 7.50% 7.50% 6.50% 8.75% 9.00% 7.00% 8.37%8.00% 10.00% 9.00% - 10.00% 9.50% 7.50% 8.50% 8.50% 8.00% - 8.50% 9.00% 9.75% 9.50% 11.00% 10.50% 9.00% 9.75% 8.00% 8.50% 8.50% 8.50% 9.00% 9.50% 9.50% 9.34%8.00% 9.00% 9.50% - 8.00% 9.50% 7.70% 8.00% 7.50% 8.00% 8.50% 7.25% 9.00% 9.75% 8.75% 11.00% 9.50% 7.75% 9.25% 8.00% 7.50% 7.50% 8.50% 9.00% 10.00% 9.00% 8.82%7.50% 9.00% 9.50% 7.50% 8.00% 8.50% 8.40% 8.25% 8.00% 8.00% 9.00% 8.00% 9.00% 9.25% 8.75% 10.00% 9.50% 7.75% 9.25% 8.00% 8.00% 8.00% 7.50% 7.75% 10.00% 8.50% 8.74%7.00% 9.00% 9.50% 8.00% 9.00% 10.50% 8.20% 8.75% 9.00% 9.00% 9.00% 9.00% 9.00% 9.25% 10.50% 10.50% 10.00% 8.50% 9.25% 8.25% 9.00% 9.00% 9.50% 9.00% - 9.00% 9.15%7.00% 7.50% 7.50% - 10.00% 8.50% 6.60% 6.25% 6.25% 6.00% - 7.00% 8.50% 7.50% 6.75% 9.50% 7.50% 6.50% 8.00% 6.50% 6.25% 6.25% 5.90% 8.00% 8.50% 6.50% 7.62%7.50% 8.00% 7.00% 7.00% 8.50% 8.50% 9.20% 6.50% 6.25% 5.00% 6.75% 7.25% 8.50% 7.75% 7.75% 9.00% 7.50% 6.75% 7.50% 7.00% 6.25% 6.25% 6.80% 7.50% 7.70% 6.75% 7.49%

10.00% 11.00% 10.00% - 9.00% 11.00% 9.00% 9.00% 11.00% - 10.50% 9.50% 10.00%10.25% 10.50% 11.00% 10.00% 9.50% 10.50% 11.00% 10.50% 11.00% 9.25% - - 10.25%10.23%10.00% 11.00% 11.00% 11.50% 8.50% 10.50% 9.00% 9.25% 10.50% - 10.00% 9.00% 9.00%10.50% 11.00% 11.50% 11.50% 10.00% 11.00% 11.00% 10.50% 11.00% 9.50%11.00% 11.00% 11.00%10.48%10.00% 11.00% 10.50% - 10.00% 10.50% - 9.00% 11.00% - 10.50% 9.50% 10.00%10.50% 10.50% 10.50% 11.50% 10.00% 11.00% 11.00% 11.00% 11.50% 9.00%10.50% 11.00% 10.50%10.48%

9.00% 11.50% 10.00% - 9.50% 11.50% 9.25% 8.50% 10.50% - 9.50% 9.25% 11.00%10.50% 10.00% 12.25% 11.50% 9.50% 11.00% 11.00% 10.00% 10.00% 9.00%10.00% - 9.50%10.45%9.00% 11.50% 10.00% 12.00% 9.00% 12.00% 9.00% 9.00% 9.50% 9.00% 9.50% 9.50% 11.00%11.00% 11.00% 13.25% 11.00% 9.50% 10.50% 11.25% 10.00% 10.00% 10.00%10.50% 11.00% 10.25%10.52%8.00% 11.00% 10.00% - 9.00% 11.50% 9.25% 8.75% 8.50% 10.00% - 8.75% -10.00% 10.00% 11.70% 10.00% 10.00% 11.00% 11.00% 8.50% 8.50% 9.00% - 11.00% 10.50% 9.89%8.50% 11.00% 10.00% 11.00% 9.50% 9.75% 9.50% 9.00% 8.50% 10.50% 9.50% 9.00% 10.00% 9.50% 10.50% 12.50% 11.30% 10.00% 10.50% 11.25% 8.50% 8.50% 10.50%10.00% 11.00% 9.25%10.08%8.50% 11.00% 10.25% 11.25% 9.50% 10.00% 10.50% 9.00% 9.00% 10.50% 9.00% 9.00% 11.00% 9.00% 10.50% 12.50% 11.10% 9.00% 10.50% 11.50% 9.00% 9.00% 10.00%10.50% 11.50% 9.00%10.23%9.50% 12.50% 10.50% - 11.00% 11.00% 8.75% 9.50% 10.50% 10.00% - 9.75% 11.00%10.75% 11.00% 13.50% 12.50% 10.50% 10.50% 11.50% 10.50% 10.50% 10.00%10.75% 11.00% 11.25%11.05%9.00% 11.50% 10.00% - 9.00% 11.25% 9.00% 9.00% 9.00% 10.00% 9.50% 8.50% 11.00%10.75% 10.50% 14.00% 11.50% 10.00% 10.50% 11.50% 9.00% 9.00% 10.00%11.00% 11.50% 10.50%10.50%8.50% 11.50% 10.00% 11.00% 9.00% 10.50% 9.50% 9.25% 9.00% 10.00% 9.50% 9.50% 11.00%10.25% 10.50% 12.50% 11.50% 10.00% 10.50% 11.50% 9.00% 9.00% 10.00% 9.50% 11.50% 10.75%10.43%9.00% 11.50% 10.00% 11.75% 10.00% 11.50% 9.25% 9.50% 11.00% 10.00% 9.50% 10.00% 11.00%10.25% 11.50% 13.00% 12.00% 10.50% 10.50% 11.75% 11.00% 11.00% 10.50%11.00% - 10.75%10.85%8.50% 10.00% 10.00% - 11.00% 11.00% 9.00% 8.75% 8.50% 8.25% - 9.00% 10.00% 9.50% 10.00% 11.75% 9.50% 8.50% 10.00% 10.00% 8.50% 8.50% 9.00%10.00% 10.00% 9.00% 9.68%8.50% 10.00% 10.00% 12.00% 10.00% 10.50% 9.75% 8.50% 8.50% 8.25% 9.00% 9.00% 10.00% 9.75% 11.00% 11.00% 9.50% 8.75% 10.00% 10.50% 8.50% 8.50% 10.00% 9.50% 10.00% 9.00% 9.65%

11.00% 13.50% 12.00% - 10.00% 13.00% 9.75% 9.75% 13.00% - 12.00% 10.50% 11.00%12.25% 12.00% 13.50% 12.50% 11.50% 11.00% 13.00% 12.50% 12.50% 12.00% - - 12.50%12.01%11.00% 13.50% 12.50% 13.00% 9.50% 12.00% 9.75% 9.75% 12.50% 12.00% 12.00% 11.00% 11.00%12.50% 13.50% 13.50% 14.00% 12.00% 11.50% 13.00% 12.50% 12.50% 13.00%13.00% 12.50% 13.00%12.26%11.00% 13.50% 12.50% - 11.00% 12.00% - 9.75% 13.00% 12.00% 12.00% 11.25% 11.00%12.50% 13.00% 13.25% 14.00% 12.00% 11.50% 12.00% 12.50% 12.50% 12.00%12.50% 12.50% 13.00%12.22%

8.00% 9.50% 8.75% - 9.50% 10.50% 8.00% 7.50% 9.00% - 8.25% 8.75% 9.50%10.50% 8.75% 10.50% 9.75% 8.50% 10.00% 7.75% 8.50% 8.50% 6.60% 9.00% - 7.75% 9.17%8.00% 9.50% 9.00% 9.50% 9.00% 10.00% 7.50% 8.50% 8.50% 8.50% 8.25% 8.75% 9.50%10.50% 10.00% 11.15% 9.50% 8.25% 9.50% 8.00% 8.50% 8.50% 8.30% 9.25% 9.50% 8.75% 9.24%7.00% 9.00% 9.00% - 9.00% 9.50% 8.50% 7.75% 7.50% 6.50% - 8.50% - 8.00% 8.50% 10.50% 8.30% 8.75% 10.50% 7.75% 7.50% 7.50% 6.80% 9.00% 10.50% 8.25% 8.59%7.50% 9.00% 8.00% 8.00% 9.50% 8.50% 8.75% 8.50% 7.75% 8.00% 8.00% 8.75% 9.00% 9.00% 8.75% 10.65% 10.00% 8.25% 10.00% 8.25% 7.75% 7.25% 8.50% 9.00% 9.50% 7.75% 8.86%8.00% 9.00% 8.50% 8.00% 9.50% 9.25% 10.00% 8.50% 8.00% 8.50% 7.50% 8.75% 9.00% 8.50% 8.75% 11.15% 9.75% 7.75% 10.00% 8.25% 8.00% 8.00% 8.00% 9.25% 9.50% 7.50% 8.95%9.00% 10.50% 9.50% - 10.50% 9.75% 8.25% 9.50% 9.00% 8.25% - 9.25% 9.50%10.00% 10.00% 10.60% 11.00% 9.75% 10.00% 8.25% 9.00% 9.00% 8.80% 9.50% 10.00% 10.25% 9.84%9.00% 9.50% 10.00% - 9.00% 10.00% 8.25% 8.50% 8.00% 8.25% 9.00% 8.50% 9.50%10.00% 9.25% 10.75% 10.50% 8.50% 10.00% 8.25% 8.00% 8.00% 8.80% 9.50% 10.50% 10.00% 9.34%8.50% 9.50% 10.00% 8.00% 8.50% 9.50% 9.00% 8.75% 8.50% 8.25% 9.50% 9.00% 9.50% 9.75% 9.25% 10.50% 10.50% 8.50% 10.00% 8.25% 8.50% 8.50% 8.30% 8.25% 10.50% 9.25% 9.30%8.00% 9.50% 10.00% 8.50% 9.50% 10.00% 8.75% 9.00% 9.00% 9.50% 9.50% 9.50% 9.50% 9.75% 11.00% 10.50% 10.75% 9.25% 10.50% 8.50% 9.00% 9.00% 9.60% 9.50% - 10.00% 9.63%8.00% 8.00% 8.50% - 10.50% 8.50% 7.00% 7.00% 6.75% - - 8.50% 9.00% 8.00% 7.25% 10.50% 8.00% 7.25% 9.00% 6.00% 6.75% 6.75% 7.20% 8.50% 9.00% 7.50% 8.22%8.50% 8.50% 8.00% 7.50% 9.00% 8.50% 9.75% 7.25% 6.75% 7.00% 7.25% 8.50% 9.00% 8.25% 8.25% 9.75% 8.00% 7.50% 9.00% 7.50% 6.75% 6.75% 8.30% 8.00% 8.25% 7.50% 8.14%

11.00% 11.50% 10.50% - 9.50% 11.50% 9.50% 9.50% 11.00% - 11.00% 10.50% 10.00%10.75% 11.00% 11.00% 10.50% 10.25% 10.50% 11.50% 10.50% 10.50% 9.50% - - 11.00%10.75%11.00% 11.50% 11.50% 12.00% 9.00% 11.00% 9.50% 9.75% 10.50% 12.50% 10.50% 10.50% 9.50%10.25% 11.50% 11.00% 11.75% 10.75% 11.00% 11.50% 10.50% 10.50% 9.80%11.50% 11.50% 12.00%11.00%11.00% 11.50% 11.00% - 10.50% 11.00% - 9.50% 11.00% 12.50% 11.00% 10.75% 10.00%10.25% 11.00% 11.00% 11.75% 10.75% 11.00% 11.50% 11.00% 11.00% 9.20%11.00% 11.50% 11.75%11.00%

1.00% 0.00% 0.00% - 0.00% 1.50% 3.00% 2.75% 0.00% - 3.00% 2.75% 0.00% 0.00% 1.50% 2.00% 3.00% 2.50% 1.00% 3.00% 0.00% 0.00% 2.50% 2.00% -5.00% 3.00% 1.07%1.00% 0.00% 0.00% 3.00% 2.50% 2.00% 3.25% 7.50% 0.00% 4.00% 3.00% 2.75% 0.00% 0.00% 2.00% 2.50% 3.00% 2.50% 1.00% 3.00% 0.00% 0.00% 3.00% 3.00% 0.00% 2.00% 1.66%1.00% 2.50% 2.50% - 2.50% 3.00% 3.25% 8.25% 3.00% 4.00% 3.00% 2.75% 2.50% 2.50% 3.00% 3.00% 2.50% 2.50% 2.00% 2.00% 3.00% 3.00% 0.00% - 3.00% 2.50% 2.65%1.00% 2.50% 2.50% 5.00% 2.00% 3.25% 3.25% 3.00% 3.00% 4.00% 3.00% 2.75% 2.50% 2.50% 3.00% 3.00% 2.00% 3.00% 2.00% 2.00% 3.00% 3.00% 1.00% 3.00% 3.00% 3.00% 2.57%1.00% 3.00% 2.50% 5.00% 2.00% 3.00% 2.50% 3.00% 3.00% 4.00% 3.00% 2.75% 2.50% 2.50% 3.00% 3.00% 2.00% 3.00% 2.00% 2.00% 3.00% 3.00% 2.00% 3.00% 3.00% 3.00% 2.57%1.00% 1.50% 2.00% - 1.00% 2.00% 3.00% 2.50% 0.00% 2.00% 3.00% 2.75% 0.00% 0.00% 1.00% 2.00% 0.00% 2.50% 3.00% 2.00% 0.00% 0.00% 1.00% 2.00% -2.00% 2.50% 1.26%1.00% 2.50% 2.00% - 1.00% 2.00% 3.00% 3.00% 3.00% 2.00% 3.00% 2.75% 0.00% 0.00% 1.00% 2.00% 0.00% 3.00% 3.00% 2.00% 3.00% 3.00% 1.00% 2.00% 0.00% 2.50% 1.74%1.00% 2.50% 2.00% 5.00% 2.00% 2.00% 2.75% 3.00% 3.00% 2.00% 3.00% 2.75% 0.00% 0.00% 1.00% 2.00% 2.00% 3.00% 3.00% 2.00% 3.00% 0.00% 2.00% 3.00% 0.00% 2.50% 1.97%1.00% 2.50% 2.00% 3.00% 2.00% 2.00% 3.25% 2.75% 0.00% 3.00% 3.00% 2.75% 0.00% 0.00% 0.00% 2.00% 2.00% 2.50% 3.00% 2.00% 0.00% 0.00% 1.00% 2.50% - 2.50% 1.69%1.00% 2.00% 2.00% - 1.00% 3.00% 3.25% 3.00% 4.00% 8.00% 3.00% 2.75% -2.00% 2.00% 3.00% 3.00% 2.00% 3.50% 0.00% 5.00% 4.00% 3.00% 0.00% 4.00% 0.00% 2.50% 2.34%1.00% 2.50% 1.00% 3.00% 2.00% 3.00% 3.50% 3.00% 4.00% 8.00% 3.00% 2.75% -2.00% 1.00% 1.50% 4.00% 2.00% 3.50% 0.00% 5.00% 4.00% 3.00% 0.00% 4.00% 0.00% 2.50% 2.34%1.00% 1.50% 2.00% - 2.00% 4.00% 3.25% 3.25% 2.00% - 3.00% 2.75% 3.00% 3.00% 2.00% 4.00% 4.00% 2.50% 0.00% 4.00% 2.00% 0.00% 2.00% - 0.00% 3.00% 2.03%1.00% 1.50% 2.00% 3.00% 2.00% 4.00% 3.00% 3.00% 2.00% 3.00% 3.00% 2.75% 3.00% 3.00% 1.00% 4.00% 4.00% 2.50% 0.00% 4.00% 2.00% 0.00% 2.00% 2.00% 2.50% 3.00% 2.11%1.00% 1.50% 2.00% - 2.00% 4.00% - 3.25% 2.00% 3.00% 3.00% 2.75% 3.00% 3.00% 1.00% 4.00% 3.00% 2.50% 0.00% 4.00% 2.00% 0.00% 3.00% 2.00% 2.50% 3.00% 2.05%

2.50% 2.50% 3.00% - 2.00% 5.00% 3.25% 3.25% 3.00% - 3.00% 2.75% 3.00% 2.50% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.50% 3.00% 2.00% 3.00% 2.84%2.50% 2.50% 3.00% 3.00% 2.00% 4.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.75% 3.00% 2.50% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.50% 3.00% 2.00% 3.00% 2.80%2.50% 2.50% 3.00% - 2.00% 4.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.75% - 2.50% 2.50% 3.00% 3.00% 3.00% 3.00% 2.00% 3.00% 3.00% 2.50% 3.00% 2.00% 3.00% 2.78%2.50% 2.50% 3.00% 3.00% 1.00% 4.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.75% 3.00% 2.50% 2.50% 3.00% 3.00% 3.00% 3.00% 2.00% 3.00% 3.00% 2.50% 3.00% 2.00% 3.00% 2.75%2.50% 2.50% 3.00% 3.00% 1.00% 4.00% 2.75% 3.00% 3.00% 3.00% 3.00% 2.75% 3.00% 2.50% 2.50% 3.00% 3.00% 3.00% 3.00% 2.00% 3.00% 3.00% 2.50% 3.00% 2.00% 3.00% 2.74%2.00% 3.00% 3.00% - 1.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.75% 3.00% 2.50% 2.50% 3.00% 2.00% 3.00% 3.00% 2.00% 3.00% 3.00% 2.50% 3.00% 2.00% 3.00% 2.71%2.00% 3.00% 3.00% - 1.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.75% 3.00% 2.50% 2.50% 3.00% 2.00% 3.00% 3.00% 2.00% 3.00% 3.00% 2.50% 3.00% 2.00% 3.00% 2.71%2.00% 3.00% 3.00% 3.00% 1.00% 3.00% 2.75% 3.00% 3.00% 3.00% 3.00% 2.75% 3.00% 2.50% 2.50% 3.00% 2.00% 3.00% 3.00% 2.00% 3.00% 3.00% 2.50% 3.00% 2.00% 3.00% 2.71%2.00% 2.50% 3.00% 3.00% 1.00% 3.00% 3.25% 3.00% 3.00% 3.00% 3.00% 2.75% 3.00% 2.50% 2.50% 3.00% 2.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.50% 3.00% 0.00% 3.00% 2.70%2.00% 3.00% 3.00% - 1.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.75% 3.00% 2.50% 3.00% 4.00% 2.50% 3.00% 3.00% 3.00% 3.00% 3.00% 2.50% 3.00% 2.50% 3.00% 2.80%2.00% 3.00% 3.00% 3.00% 2.00% 3.00% 3.25% 3.00% 3.00% 3.00% 3.00% 2.75% 3.00% 2.50% 3.00% 4.00% 2.50% 3.00% 3.00% 3.00% 3.00% 3.00% 2.50% 3.00% 2.50% 3.00% 2.82%3.00% 3.00% 3.00% - 1.00% 3.50% 3.00% 3.25% 3.00% - 3.00% 2.75% 3.00% 2.50% 3.00% 4.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.50% 3.00% 0.00% 3.00% 2.70%3.00% 3.00% 3.00% 3.00% 1.00% 3.50% 3.00% 3.00% 3.00% 3.00% 3.00% 2.75% 3.00% 2.50% 3.00% 4.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.50% 3.00% 2.50% 3.00% 2.72%3.00% 3.00% 3.00% - 2.00% 3.50% - 3.25% 3.00% 3.00% 3.00% 2.75% 3.00% 2.50% 3.00% 4.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 2.50% 3.00% 2.50% 3.00% 2.78%

$35.00 $15.00 $35.00 - $6.00 $25.00 $20.00 $40.00 $15.00 - $20.00 $30.00 $20.00 $25.00 $15.00 $22.00 $18.00 $35.00 $15.00 $40.00 $15.00 $15.00 $20.00 $10.00 - $40.00 $22.85$20.00 $15.00 $25.00 $50.00 $8.00 $20.00 $25.00 $25.00 $15.00 $25.00 $15.00 $20.00 $20.00 $20.00 $15.00 $15.00 $15.00 $27.00 $14.00 $30.00 $15.00 $15.00 $20.00 $8.00 $10.00 $15.00 $19.71$20.00 $25.00 $12.00 - $4.00 $25.00 $5.00 $15.00 $15.00 $5.00 - $20.00 $40.00 - $10.00 $9.00 - $20.00 $20.00 - $15.00 $15.00 - - - $5.00 $13.14$15.00 $25.00 $8.00 - $2.00 $5.00 $2.00 $7.00 $5.00 $2.00 $2.00 - $10.00 - $10.00 $4.00 - $10.00 $10.00 $3.00 $5.00 $5.00 $6.00 $5.00 $15.00 $5.00 $7.88$15.00 $25.00 $5.00 - $2.00 $5.00 - $2.50 $5.00 $2.00 $2.00 - $10.00 - $10.00 $5.00 - $10.00 $10.00 $3.00 $5.00 $5.00 $6.00 $5.00 $15.00 $5.00 $7.11$5.00 $5.00 $2.00 - - - - - $5.00 $2.00 - - $2.50 - $0.50 - - $7.00 $2.00 - $5.00 $5.00 - - - - $2.14$5.00 $5.00 $0.50 - - - - $1.00 $0.50 $1.00 $2.00 - $2.50 - $0.50 - - $3.00 - - $0.50 $0.50 - - $0.50 $1.00 $2.14

$10.00 $5.00 $2.00 $20.00 $4.00 - - $1.00 $1.00 $1.00 $10.00 - $5.00 $25.00 $0.50 $2.00 - $5.00 $3.00 - $1.00 $1.00 $1.00 $3.00 $0.50 $2.50 $3.57- $25.00 $5.00 - $10.00 - - $5.00 $10.00 $2.00 $10.00 $10.00 $15.00 - $1.50 $2.00 - $10.00 $10.00 $20.00 $10.00 $10.00 $18.00 $5.00 - $10.00 $6.73

Mia

mi,

FL

Milw

auke

e, W

I

Min

neap

olis

, MN

Napl

es, F

L

Nash

ville

, TN

New

Jer

sey,

Coa

stal

New

Jer

sey,

Nor

ther

n

New

Yor

k, N

Y

Oakl

and,

CA

Oran

ge C

ount

y, C

A

Orla

ndo,

FL

Phila

delp

hia,

PA

Phoe

nix,

AZ

Pitts

burg

h, P

A

Portl

and,

OR

Prov

iden

ce, R

I

Rich

mon

d, V

A

Sacr

amen

to, C

A

San

Anto

nio,

TX

San

Dieg

o, C

A

San

Fran

cisc

o, C

A

San

Jose

, CA

Seat

tle, W

A

Tam

pa, F

L

Tuls

a, O

K

Was

hing

ton,

DC

Aver

ages

TABLE 8 continued

INVESTMENT CRITERIA

VIEWPOINT 2005 INTEGRA REALTY RESOURCES, INC. 7

INVESTMENT CRITERIA

8 INTEGRA REALTY RESOURCES, INC. VIEWPOINT 2005

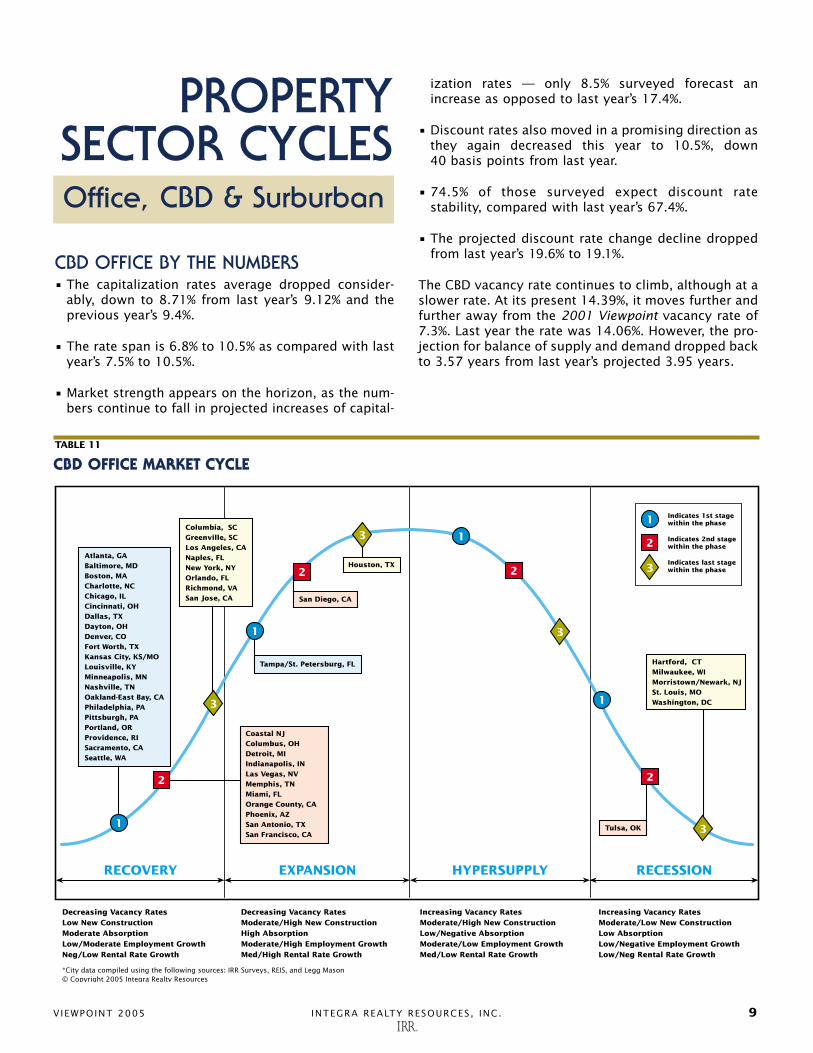

casted absorption figures and employment growthforecasts and by applying standard criteria to each sur-veyed city. The majority of reviewed markets for allproperty types were in various stages of the recession-ary or recovery phases of the market cycle. The viabil-ity of a MSA depends upon where it is in the cycle. If aMSA has entered the last stage of the recessionaryphase, it is expected that it will begin its recovery bythe end of the year.

OFFICE MARKET CYCLE 2004In the office sector cycle, many markets in the reces-sionary phase in last year’s report have moved into thefirst phase of recovery, including Boston, Chicago,Dallas, Minneapolis and Pittsburgh. Hartford,Milwaukee and St. Louis are those still stuck in the thirdphase of the recessionary stage. Houston, Tampa,

St. Petersburg and San Diego are all in some stage ofexpansion in the office property sector.

RETAIL MARKET CYCLE 2004Kansas City and Orange County have moved into thefirst phase of expansion for the retail property sector.Last year, Kansas City was in the third phase of reces-sion in this sector. The majority of the markets are invarious stages of the expansion or recovery phaseswith many more in the hypersupply phase. Last year,Austin was the lone MSA in the hypersupply phase.

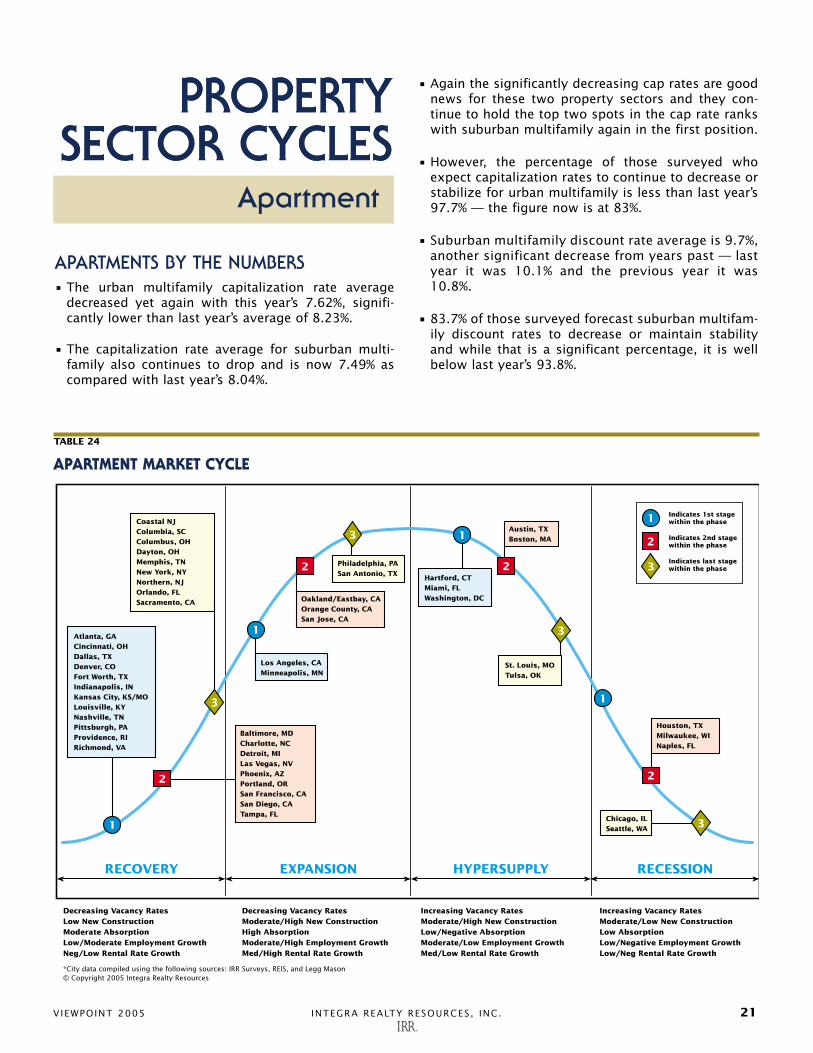

APARTMENT MARKET CYCLE 2004

In the apartment sector cycle, Washington, D.C., Hartford,Miami, Austin, Boston, St. Louis and Tulsa are in the hyper-supply phase. Last year no markets were in this phase.

INDUSTRIAL MARKET CYCLE 2004The majority of markets in the industrial property sec-tor are in various stages of recovery/expansion. Onlytwo markets are in hypersupply including Ft. Worth andAtlantic City, which was in this phase last year.Indianapolis, St. Louis and Tampa moved out of therecessionary phase.

CAPITALIZATION AND DISCOUNT RATESAlthough no crystal ball, capitalization and discountrates are important signposts on the real estate invest-ment landscape. When capitalization rates increase,caution is warranted. However, a drop in initial capital-ization rates usually indicates strength in future dura-bility, net income growth, capital costs and overall risks.Other factors in the macro-economic environment canskew this standard barometer, so it is wise to take ahard look at the declining rates to determine if they arebased on strong fundamentals or other market condi-tions. Caution is warranted here and IRR representativescan help you analyze any current market anomalies.

Discount rates are the annualized rates or expectedrates of return for property investments and they alsoprovide clues about the weakness or strength of a mar-ket. Basically, overall risk decreases when discountrates fall and risk increases as rates move up.

OVERALL YIELD RATESLast year’s projected capitalization rates were on aver-age 74.3% stable with 17.8% declining and 7.9%increasing. This year it hasn’t changed much with71.7% stable, 18.9% declining and 9.4% increasing.

The discount rates’ year-to-year change was greater. Lastyear IRR projected discount rates at 75.4% stable, 18.6%declining and 6% increasing. This year, the projectionsare 73.2% stable with 17.8% declining and 9% increasing.

PROJECTED DISCOUNT RATE CHANGEProperty Type Decline (%) Increase (%) Stable (%)

CBD Office 19.1 6.4 74.5Suburban Office 24.5 6.1 69.4Regional Mall 17.8 11.1 71.1Community Mall 16.3 10.2 73.5Neighborhood Strip 16.3 12.2 71.4Manufacturing 8.5 14.9 76.6Bulk 10.4 4.2 85.4Office/Warehouse 26.5 6.1 67.3R&D 16.7 6.3 77.1Urban Multi Family 10.6 17.0 72.3Suburban Multi Family 14.3 16.3 69.4CBD Lodging 21.3 6.4 72.3Suburban Lodging 22.9 4.2 72.9Airport Lodging 23.9 4.3 71.7AVERAGE 17.8 9.0 73.2

2004 DISCOUNT RATE RANKS2004 2004 Low 2004 High 2004 Avg.Rank Property Type (%) (%) (%)

1 Urban Multi Family 8.3 12.5 9.72 Suburban Multi Family 8.3 12.0 9.73 Regional Mall 8.0 12.0 9.94 Community Mall 8.5 12.5 10.15 Neighborhood Strip 8.5 12.5 10.26 CBD Office 8.5 12.5 10.57 Office/Warehouse 8.5 12.5 10.48 Bulk 8.5 14.0 10.59 Suburban Office 9.0 13.3 10.5

10 R&D 9.0 13.0 10.911 Manufacturing 8.8 14.0 11.012 CBD Lodging 9.5 14.0 12.013 Airport Lodging 9.3 14.0 12.214 Suburban Lodging 9.3 14.0 12.3

TABLE 9

TABLE 10

CBD OFFICE BY THE NUMBERS• The capitalization rates average dropped consider-

ably, down to 8.71% from last year’s 9.12% and theprevious year’s 9.4%.

• The rate span is 6.8% to 10.5% as compared with lastyear’s 7.5% to 10.5%.

• Market strength appears on the horizon, as the num-bers continue to fall in projected increases of capital-

ization rates — only 8.5% surveyed forecast anincrease as opposed to last year’s 17.4%.

• Discount rates also moved in a promising direction asthey again decreased this year to 10.5%, down 40 basis points from last year.

• 74.5% of those surveyed expect discount rate stability, compared with last year’s 67.4%.

• The projected discount rate change decline droppedfrom last year’s 19.6% to 19.1%.

The CBD vacancy rate continues to climb, although at aslower rate. At its present 14.39%, it moves further andfurther away from the 2001 Viewpoint vacancy rate of7.3%. Last year the rate was 14.06%. However, the pro-jection for balance of supply and demand dropped backto 3.57 years from last year’s projected 3.95 years.

VIEWPOINT 2005 INTEGRA REALTY RESOURCES, INC. 9

PROPERTYSECTOR CYCLESOffice, CBD & Surburban

RECOVERY EXPANSION HYPERSUPPLY RECESSION

Decreasing Vacancy RatesLow New ConstructionModerate AbsorptionLow/Moderate Employment GrowthNeg/Low Rental Rate Growth

Tulsa, OK

Indicates 1st stagewithin the phase

Indicates 2nd stagewithin the phase

Indicates last stagewithin the phase

1

2

3

Hartford, CTMilwaukee, WIMorristown/Newark, NJSt. Louis, MOWashington, DC

Decreasing Vacancy RatesModerate/High New ConstructionHigh AbsorptionModerate/High Employment GrowthMed/High Rental Rate Growth

Increasing Vacancy RatesModerate/High New ConstructionLow/Negative AbsorptionModerate/Low Employment GrowthMed/Low Rental Rate Growth

Increasing Vacancy RatesModerate/Low New ConstructionLow AbsorptionLow/Negative Employment GrowthLow/Neg Rental Rate Growth

*City data compiled using the following sources: IRR Surveys, REIS, and Legg Mason© Copyright 2005 Integra Realty Resources

Coastal NJColumbus, OHDetroit, MIIndianapolis, INLas Vegas, NVMemphis, TNMiami, FLOrange County, CAPhoenix, AZSan Antonio, TXSan Francisco, CA

Atlanta, GABaltimore, MDBoston, MACharlotte, NCChicago, ILCincinnati, OHDallas, TXDayton, OHDenver, COFort Worth, TXKansas City, KS/MOLouisville, KYMinneapolis, MNNashville, TNOakland-East Bay, CAPhiladelphia, PAPittsburgh, PAPortland, ORProvidence, RISacramento, CASeattle, WA

3

2

1

1

2

3 1

2

3

1

2

3

Tampa/St. Petersburg, FL

Houston, TX

San Diego, CA

Columbia, SCGreenville, SCLos Angeles, CANaples, FLNew York, NYOrlando, FLRichmond, VASan Jose, CA

TABLE 11

CBD OFFICE MARKET CYCLE

PROPERTY SECTORS – OFFICE, CBD & SURBURBAN

10 INTEGRA REALTY RESOURCES, INC. VIEWPOINT 2005

4

5

6

7

8

9

10

11

1994 1995 1996 1997 1998 1999 2000 2002

Office CBD10 Year Treasury (January Avg.)

Year

Per

cent

age

2001

3

2

120042003

10 Year Treasury (Annual Avg.)

TABLE 12

CAP RATE TRENDS—CBD OFFICE

Inventory grew. This year it was 1.37 billion squarefeet, as compared with last year’s 1.35 billion squarefeet. Development in the pipeline for 2004 – 2007 is 46million square feet. Last year about 54.6 million squarefeet in office space was under development for theperiod of 2003 – 2006.

QUICK MARKET GLANCE• CBD office continues to hold 6th place in the cap rate

ranks, but has moved up one slot in the discount rate ranks, from 7th to 6th.

• The continuing upward trend of vacancy rates, eventhough it appears to be slowing a bit, discouragesany thoughts of a quick turnaround in this sector, buta market recovery is on the horizon. Perhapsinvestors think it has bottomed out and are buyingon higher than normal vacancy rates.

• Although moving away from the projection to reachequilibrium in almost four years, it at last seems tobe moving in the right direction.

• The corporate hiring moratorium seems to be a stub-born mainstay of today’s economy and it will have toshake loose before this sector begins to fire on allcylinders.

• This sluggishness holds on in many MSA’s throughoutthe nation, with a few tentative bright spots, offeringa glimpse at a more promising future trend.

– In the Los Angeles market, recent construction anddevelopment have accelerated, but the anticipatedamount of available space expected within the nexttwo years is still considered minimal so the marketwill tighten up somewhat. However, the reductionof government employment will put a drag onabsorption of space in the market.

– In Miami, vacancy continues to decline and thetrend of slightly increased lease rates is expectedto continue for the next two years.

– The downtown Seattle market is steadily improv-ing, although gradually. In the third quarter, thedowntown Bellevue market improved significantlywhen three large tenants relocated to the area.

• Growth in low-wage and service sector jobs justwon’t pull this sector out of the doldrums. UntilCorporate America sees enough growth on the hori-zon to ignore escalating health care costs and beginsto generate jobs, recovery in this sector isn’t going tosurprise anyone with any speed records. In this sec-tor, the follow-up to the age-old maxim of “nothingever happens until someone sells something” is“nothing will really happen until someone hiressomeone.”

© 2005 Integra Realty Resources

VIEWPOINT 2005 INTEGRA REALTY RESOURCES, INC. 11

TABLE 13

OFFICE MARKET CONDITIONS AND FORECASTS: Central Business DistrictTOTAL FORECAST TOTAL FORECAST

AVG. ANNUAL UNDER AVG. ANNUAL VALUE TOTAL VALUE EST.VACANCY NET ABSORP. CONST. NET ABSORP. CHANGE CHANGE YEARS

INVENTORY1 RATE1 VACANCY1 2001-20041 2004-20071 2005-20071 2001-2004 2005-2007 TOMARKET AREA (SQ. FT.) (%) (SQ. FT.) (SQ. FT.) (SQ. FT.) (SQ. FT.) (%) (%) BALANCE

Atlanta, GA 15,500,000 19.50 3,022,500 -370,250 441,000 500,000 -9.50 4.10 3Austin, TX 8,456,130 23.40 1,978,734 6,391 1,391,970 217,333 -1.00 -5.00 3Baltimore, MD 19,069,000 13.00 2,478,970 44,500 725,000 225,000 9.00 7.00 3Boston, MA 60,000,000 15.00 9,000,000 -472,500 1,500,000 533,333 -10.00 5.00 3Charlotte, NC 14,295,000 9.00 1,286,550 337,250 3,927,000 340,000 -8.00 15.00 2Chicago, IL 115,400,000 15.93 18,378,000 -539,500 4,150,000 1,512,333 0.00 3.50 5Cincinnati, OH 13,000,000 13.00 1,690,000 -70,000 580,000 166,667 3.50 3.00 1.5Cleveland, OH 20,543,000 21.80 4,478,374 -402,250 0 319,333 - - -Columbia, SC 5,526,000 18.50 1,022,310 2,500 370,000 100,000 -8.00 0.00 4Columbus, OH 9,350,000 14.00 1,309,000 -14,750 160,000 225,000 -5.00 5.00 3Dallas, TX 33,299,499 27.70 9,223,961 -121,944 0 - -30.00 3.00 4Dayton, OH 7,124,295 14.30 1,018,774 44,755 20,000 1,667 7.00 6.00 1Denver, CO 23,300,000 17.00 3,961,000 -582,500 0 283,333 0.00 6.00 5Detroit, MI 13,000,000 23.00 2,990,000 -383,500 100,000 28,333 -1.00 0.00 7Fort Worth, TX 10,218,202 7.60 776,583 255,906 1,300,000 101,077 -10.00 6.00 1Hartford, CT 7,547,882 24.00 1,811,492 -40,858 93,000 -50,000 -5.00 0.00 5Houston, TX 43,300,000 22.00 9,526,000 -986,165 690,000 900,000 15.00 0.00 4Indianapolis, IN 10,328,000 16.00 1,652,480 51,250 0 0 1.00 1.00 2.5Kansas City, KS/MO 13,550,000 22.00 2,981,000 -140,000 500,000 166,667 -15.00 15.00 5Las Vegas, NV 2,960,151 5.20 153,928 83,000 392,000 50,000 9.00 6.00 1Los Angeles, CA 35,169,581 19.50 6,858,068 -401,512 697,000 557,535 10.00 4.00 5Louisville, KY 10,300,000 24.70 2,544,100 -20,486 380,000 166,667 -2.00 3.00 2Memphis, TN 2,792,870 22.90 639,567 -44,453 50,000 10,000 0.00 2.00 3Miami, FL 6,700,000 14.00 938,000 -28,889 0 74,500 - - 2.5Milwaukee, WI 11,931,000 14.70 1,753,857 -45,750 220,000 23,333 -7.00 0.00 4Minneapolis, MN 24,786,000 19.80 4,907,628 -505,750 941,000 665,667 3.00 1.00 5Nashville, TN 5,800,000 15.00 870,000 56,250 80,000 16,667 0.00 0.00 6New Jersey, Coastal 4,500,000 9.00 405,000 0 310,000 100,000 -10.00 5.00 -New Jersey, Northern 42,000,000 15.70 6,594,000 400,000 0 1,800,000 8.00 6.00 5New Orleans, LA 14,024,000 17.50 2,454,200 -44,000 0 -10,333 - - -New York, NY 365,000,000 10.50 38,325,000 -1,388,000 7,400,000 12,933,333 27.00 12.00 4Oakland, CA 12,139,000 13.03 1,582,000 179,000 177,000 145,667 0.00 10.00 4Orlando, FL 6,270,000 11.00 689,700 10,179 1,340,000 185,333 13.55 9.05 1Philadelphia, PA 54,464,441 11.50 6,263,411 -449,075 1,800,000 -262,018 7.00 0.00 5Phoenix, AZ 5,500,000 15.00 825,000 147,500 0 46,667 3.00 3.00 2Pittsburgh, PA 26,700,000 18.00 4,806,000 -295,000 460,000 133,333 -12.00 0.00 5Portland, OR 17,096,519 12.80 2,188,354 -158,987 40,980 200,000 2.50 7.50 2.5Providence, RI 6,200,000 9.70 601,400 - 300,000 116,667 6.00 6.00 3Richmond, VA 8,250,000 14.00 1,155,000 53,750 1,050,000 50,000 6.00 4.00 2Sacramento, CA 11,000,000 14.00 1,540,000 -6,500 360,000 150,000 9.00 2.00 2Salt Lake City, UT 7,612,000 16.10 1,225,532 -101,000 56,000 129,667 - - -San Antonio, TX 5,324,000 22.10 1,176,604 -146,000 0 134,667 12.50 10.00 4San Diego, CA 9,503,000 11.00 1,045,330 -79,000 1,299,000 288,667 30.00 10.00 1San Francisco, CA 49,673,000 16.72 8,305,000 -1,409,000 70,000 511,333 -5.00 10.00 5San Jose, CA 8,640,000 17.12 1,479,000 -194,500 149,000 243,667 -10.00 15.00 5Seattle, WA 43,184,820 14.11 6,091,229 25,716 2,174,500 780,000 30.00 20.00 4St. Louis, MO 11,982,000 19.80 2,372,436 -210,000 0 -42,000 - - -Tampa, FL 7,120,000 18.00 1,281,600 -94,268 1,750,000 258,333 5.50 6.00 2Tulsa, OK 7,900,000 24.50 1,935,500 -148,649 0 33,333 0.00 2.50 10Washington, DC 105,000,000 7.50 7,875,000 1,497,500 8,856,000 2,337,333 11.00 5.50 -

Total: Simple Avg Total: Total: Total: Total: Average: Average: Average:1,372,329,390 16.22 197,467,173 -6,335,729 46,300,450 27,398,094 1.78 5.20 3.57

Weighted Avg:14.39

1 Italicized Inventory (i.e. blue), Vacancy, Absorption and Under Construction figures were provided by REIS, Inc. 212-921-1122.

12 INTEGRA REALTY RESOURCES, INC. VIEWPOINT 2005

OFFICE MARKET CONDITIONS AND FORECASTS: Surburban Market AreaTOTAL FORECAST TOTAL FORECAST

AVG. ANNUAL UNDER AVG. ANNUAL VALUE TOTAL VALUE EST.VACANCY NET ABSORP. CONST. NET ABSORP. CHANGE CHANGE YEARS

INVENTORY1 RATE1 VACANCY1 2001-20041 2004-20071 2005-20071 2001-2004 2005-2007 TOMARKET AREA (SQ. FT.) (%) (SQ. FT.) (SQ. FT.) (SQ. FT.) (SQ. FT.) (%) (%) BALANCE

Atlanta, GA 120,000,000 19.60 23,520,000 475,000 3,922,000 1,833,333 -15.50 4.10 4Austin, TX 28,751,936 20.40 5,864,842 -479,534 352,672 733,333 -25.00 0.00 4Baltimore, MD 55,244,000 12.10 6,684,524 1,017,802 2,300,000 800,000 9.00 7.00 4Boston, MA 92,500,000 17.73 16,400,000 -1,837,500 2,100,000 666,667 -15.00 5.00 3Charlotte, NC 25,124,000 19.39 4,872,362 719,250 5,126,346 333,333 -13.00 5.00 4Chicago, IL 102,000,000 19.82 20,215,000 -2,730,500 1,707,000 1,869,000 5.00 6.00 5Cincinnati, OH 18,605,000 19.15 3,562,150 -216,250 2,050,000 483,333 1.50 4.00 2Cleveland, OH 16,557,000 18.30 3,029,931 81,500 672,500 349,000 - - -Columbia, SC 4,875,000 24.00 1,170,000 111,250 275,000 91,667 -10.00 0.00 5Columbus, OH 22,300,000 15.25 3,400,000 -156,750 975,000 556,667 -3.00 5.00 3Dallas, TX 169,311,978 20.85 35,302,669 -1,628,540 3,611,667 177,791 -20.00 0.00 3Dayton, OH 14,060,696 12.85 1,806,485 163,621 145,000 30,000 7.00 6.00 1Denver, CO 63,000,000 24.06 15,160,500 -482,750 4,300,000 1,000,000 0.00 6.00 4Detroit, MI 55,350,000 17.87 9,890,250 -962,401 1,750,000 -300,000 - 5.00 5Fort Worth, TX 39,620,070 14.06 5,572,398 220,321 1,101,293 644,667 -20.00 3.00 2Hartford, CT 16,280,796 16.45 2,678,432 -193,910 0 66,667 -10.00 0.00 5Houston, TX 170,177,000 14.92 25,391,730 669,124 940,000 2,500,000 10.00 5.00 1Indianapolis, IN 18,982,000 19.27 3,658,480 240,250 612,000 444,000 3.00 2.00 2.5Kansas City, KS/MO 27,350,000 18.91 5,173,000 -352,908 1,000,000 366,667 -15.00 10.00 4Las Vegas, NV 29,326,788 9.45 2,772,703 1,885,530 8,200,000 1,683,333 15.00 10.00 1Long Island, NY 46,200,000 10.80 4,989,600 460,000 935,000 475,000 14.00 9.00 3Los Angeles, CA 138,038,662 14.17 19,557,584 -1,047,888 2,178,947 2,078,798 11.00 6.00 2Louisville, KY 13,000,000 19.06 2,477,200 84,528 2,350,000 333,333 -4.00 3.00 2Memphis, TN 14,584,343 16.94 2,470,545 17,458 483,866 466,667 0.00 4.00 2Miami, FL 33,300,000 15.33 5,105,000 12,477 1,657,000 613,000 - - 2.5Milwaukee, WI 15,284,000 18.68 2,855,654 -108,750 100,000 33,333 -7.00 0.00 4Minneapolis, MN 43,661,000 18.30 7,988,140 -318,750 312,000 450,667 4.00 1.00 5Naples, FL 5,605,797 9.53 534,064 141,178 579,000 250,000 10.00 12.00 2Nashville, TN 19,400,000 15.08 2,926,250 242,547 930,000 216,667 7.50 5.00 1New Jersey, Coastal 17,721,765 12.24 2,168,275 -422,500 950,000 283,333 -8.00 3.00 2New Jersey, Northern 201,000,000 14.20 28,542,000 1,925,000 1,200,000 2,533,333 7.00 2.00 4New Orleans, LA 7,505,000 8.50 637,925 -14,750 620,000 168,000 - - -Oakland, CA 48,066,000 14.79 7,111,000 -481,000 673,000 839,333 0.00 10.00 4Orange County, CA 126,622,198 10.41 13,177,453 813,399 2,795,000 1,898,333 15.00 10.00 1Orlando, FL 24,153,000 16.54 3,994,327 711,196 2,859,000 832,667 10.60 7.10 1Philadelphia, PA 90,679,493 17.62 15,978,643 -328,411 3,329,445 638,693 5.00 6.00 2Phoenix, AZ 50,380,000 19.98 10,064,000 1,327,500 6,000,000 1,200,000 3.00 3.00 4Pittsburgh, PA 47,900,000 17.72 8,487,880 3,300 500,000 333,333 -4.00 4.00 3Portland, OR 24,281,137 16.03 3,892,948 343,880 1,987,973 750,000 -5.00 5.00 3.5Providence, RI 5,750,000 9.50 546,250 - 550,000 95,000 12.00 10.00 3Richmond, VA 17,550,000 11.24 1,973,250 118,750 1,240,000 270,000 10.00 6.00 2Sacramento, CA 37,075,000 14.11 5,231,250 356,250 4,050,000 1,150,000 11.00 2.00 2Salt Lake City, UT 17,788,000 19.30 3,433,084 -79,500 993,000 551,000 - - -San Antonio, TX 20,437,000 17.70 3,617,349 -201,706 841,000 614,000 12.50 10.00 4San Diego, CA 38,481,000 13.46 5,177,990 318,250 2,328,000 1,174,000 30.00 10.00 1San Francisco, CA 74,676,000 20.14 15,040,000 -354,750 554,000 1,340,667 -12.50 10.00 5San Jose, CA 56,634,000 15.97 9,044,000 -775,250 146,000 1,187,000 -10.00 15.00 5Seattle, WA 50,200,829 14.92 7,491,300 -209,692 677,083 733,333 -8.00 25.00 3St. Louis, MO 33,026,000 18.30 6,043,758 92,750 1,109,000 859,333 - - -Tampa, FL 33,555,000 16.02 5,375,293 999,326 2,350,000 250,000 7.00 6.00 2Tulsa, OK 12,000,000 17.23 2,067,500 -55,513 0 100,000 0.00 2.50 5Washington, DC 202,850,000 13.58 27,538,650 2,602,500 13,723,000 4,040,000 5.50 4.00 2

Total: Simple Avg Total: Total: Total: Total: Average: Average: Average:2,656,821,488 16.19 431,663,618 2,714,436 100,141,792 41,088,283 0.45 5.82 3.01

Weighted Avg:16.25

TABLE 14

1 Italicized Inventory (i.e. blue), Vacancy, Absorption and Under Construction figures were provided by REIS, Inc. 212-921-1122.

PROPERTY SECTORS – OFFICE, CBD & SURBURBAN CRITERIA

VIEWPOINT 2005 INTEGRA REALTY RESOURCES, INC. 13

SUBURBAN OFFICE BY THE NUMBERS• Capitalization rates continue to fall, decreasing from

last year’s 9.2% to this year’s 8.79%.

• Projected declines rose to 22.4% from last year’s18.8%.

• The discount rate average continues to decrease witha drop to 10.5% from last year’s 10.9%.

The vacancy rates took a decidedly welcome downwardturn, but it was still far from the 8.6% of four years ago.This year’s 16.25% is a decrease from both last year’s16.76% and the previous year’s 16.66%. Inventory lev-els were just a bit higher from last year’s 2.6 billion atalmost 2.66 billion square feet.

Suburban office space in the development pipelinemoved upwards to 100 million square feet from lastyear’s 93.8 million square feet under construction.However, it’s well under the radar of the 246 millionsquare feet reported in Viewpoint 2001.

This constriction of future supply alleviates some of thepressure in this sector, supporting the drop in the timespan to reach equilibrium. Last year’s estimated yearsto balance were 3.48 years and this year, the projectedyears to balance are 3.01 years.

QUICK MARKET GLANCE• Suburban again held down 8th place in the cap rate

ranks chart.

• Equilibrium moves closer, but tenants are still favoredwith a beneficial negotiating environment.

• Healthy discipline in controlling supply will aid thissector. Once demand returns, supply will be in bal-ance.

• The Tulsa suburban office submarket is showing asign of recovery as absorption was positive in 2004.The average vacancy rate also decreased in the sub-urban market.

• Tampa Bay is also experiencing a strengthening sub-urban office market with increasing rental rates andlower vacancies. The previous glut of sublease spacehas dissipated except for negative absorption of callcenter space. The Westshore office district, thelargest in Florida, is particularly strong and demandfor owner-occupied buildings has soared, with someprices over $200 per square feet.

4

5

6

7

8

9

10

11

1994 1995 1996 1997 1998 1999 2000 2002

10 Year Treasury (January Avg.)

Year

Per

cent

age

2001

3

2

1

Office Sub

20042003

10 Year Treasury (Annual Avg.)

TABLE 15

CAP RATE TRENDS—SURBURBAN OFFICE

© 2005 Integra Realty Resources

14 INTEGRA REALTY RESOURCES, INC. VIEWPOINT 2005

Last November, voters made the gaming equipmentmakers the real winners in several significant elec-tions.

• Voters passed the expansion of gaming in threestates. Florida, Oklahoma and Wisconsin all passedgaming initiatives.

• Voters in Florida approved the legalization of slotmachines at both Jai Alai games and racetracks.

• However, the voters in both Miami-Dade and BrowardCounties still need to pass a referendum early in2005 to secure the vote. If all goes as planned, theslot machines should be showing up in Florida some-time in early 2006.

• Oklahoma voters passed a proposal to allow race-tracks to have slot machines.

• Wisconsin voted to allow tribal casinos to developgaming properties on acquired land.

• California voters shot down two separate initiativesthat would have expanded Indian gaming. The indi-vidual tribes are trying to negotiate with the new gov-ernor on their individual pacts. They want to increaseslot machine numbers currently allowed. California isone of the strongest, if not the most explosive gam-ing market.

• Therefore, 46 states have some form of legalizedgaming and 35 states allow electronic gamingdevices. The American Gaming Association (AGA)reports legal gaming reported $73 billion spent byestimates of gross gaming revenue. The largest com-ponent is commercial casinos.

As of October 10, 2004, Nevada statewide reported a$10,189,484,000 win for all nonrestricted gaming loca-tions for 2004 thru August 31, 2004. This is up 6.59%.Total gaming win for the strip was up 8.08%. Nevadacasinos reported their best ever August winnings at$905.1 million. This is up 11.2% over the same monthlast year. September was $924.8 million, a 10% gainfrom last year.

Las Vegas has the 10 largest hotels in the United States.The average occupancy level overall is 88%. By 2006, thetotal room count will be approximately 140,000 rooms.

The new Wynn Resort is planned to open in April of2005. Sheldon Adelson is also building a new resortbetween the Venetian and the new Wynn property.

MGM Mirage announced a multi-billion dollar “UrbanMetropolis” on the strip between Bellagio and theMonte Carlo.

This will be a 66-acre project featuring an 18 millionsquare foot phase one. The resort will include a 4,000-room hotel and casino, three 400-room boutique hotelsand a 1,550-condominium development. There is also a550,000 square foot retail and entertainment spaceplanned. The first phase will cost approximately $4 bil-lion and create 7,000 construction jobs, and then12,000 permanent jobs. MGM Mirage states it shouldbe completed by 2010.

Interest has again peaked to see the latest and greatesthotels. The new financial sheets show that gamingincome as a percentage of total income is continuouslyhaving less of the total pie, as the other portions ofbusiness (dining, rooms, entertainment and retail) con-tinue to increase their contribution to the bottom line.

Atlantic City, New Jersey still maintains the “Avis” positionin the United States gaming industry and continues to tryharder. After a 10-year effort on the part of the redevel-opment agencies, state legislature and gaming industry, in2003 Atlantic City enjoyed opening the first new casinohotel in 13 years. The Borgata Hotel raised the bar andbrought new life to the gaming industry. As we reportedlast year, gaming revenues for the city in 2003 increasedby a modest 2.4%. A significant component of the winshifted from the existing casinos to the Borgata.

The year 2004 saw the first full year of operation forthe Borgata Hotel and the grand opening of the WalkOutlet Center at the foot of the Expressway. Resortsopened the 479-room Rendezvous Tower andShowboat opened a new 544-room tower. Morerecently, in November of this year, the $280-millionHavana Hotel Tower and The Quarter at the TropicanaCasino opened. The Quarter is a Cuban-themed non-gaming venue which features street entertainment,retail shops, restaurants and the IMAX Theatre. TheHavana Tower added an additional 500 rooms to theTropicana Complex which now is the second hotel inAtlantic City to boast over 2,000 hotel rooms. As weforecasted last year, Atlantic City will wrap up 2004with well over 15,000 hotel rooms and over 1,200,000square feet of casino gaming space.

Boosted by the success of the Borgata, anticipationthroughout the city was encouraged dramatically bythe same store sales January to October of 2003 vs.January to October of 2004 which showed a 7.4%growth in gaming revenue from approximately $3.8 bil-lion to $4.1 billion based on Casino Control Com-

PROPERTYSECTOR CYCLES

Gaming

PROPERTY SECTORS – GAMING

VIEWPOINT 2005 INTEGRA REALTY RESOURCES, INC. 15

PROPERTYSECTOR CYCLES

Lodging

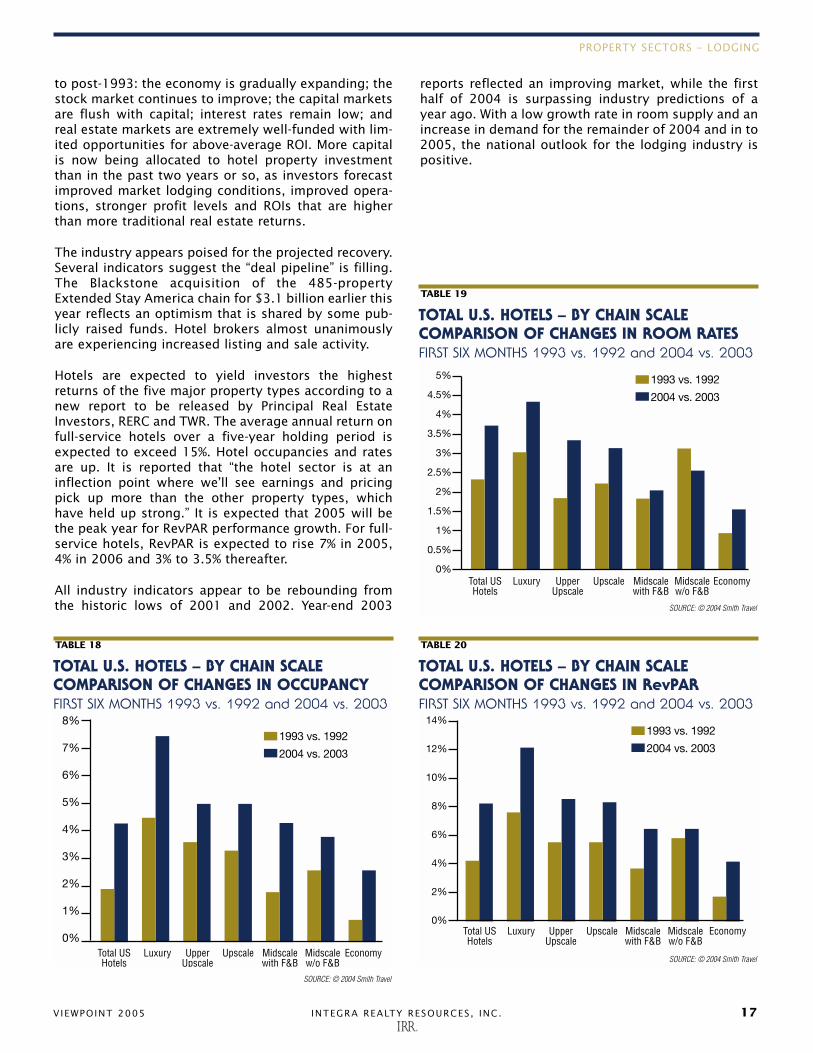

As we review national, regional and local lodgingtrends, we will primarily focus on conditionsaffecting the lodging’s specific market area and

competitive set. First, a review of national trends overthe past 10 years for a general perspective of the cycli-cal nature of the lodging industry, and a brief review ofthe anemic conditions surrounding the more recentpast and the current resurgence underway with therecovering economy.

NATIONAL TRENDS A review and comparison of the past 10 to 12 years ofthe industry is a useful tool for understanding thedirection the lodging industry is likely to take in thenear and intermediate term. A 10 year historical per-spective of pertinent lodging statistics compiled bySmith Travel Research for the U.S. lodging industry ispresented below.

mission reports. The Borgata continues to drive successand reports a win as of October 2004 at $528 million,second only to Bally’s win of $549 million for the sameperiod. Bally’s win, which is slightly over 3% higher thanBorgata, however, must be weighted against the realitythat Bally/Claridge Complex provides over 55% moregaming space. We are further impressed by the Borgataperformance in table win which totals over 35% of rev-enue when compared to the industry average inAtlantic City at about 25% of gaming revenue.

Enthusiasm in Atlantic City is running high. The Borgatahas announced plans for a $347 million expansion whichincludes 500 rooms, restaurants and non-gaming facilities.

The best evidence of the Atlantic City confidence is theincreasing investment from operators within the market.One of the commitments is the $9.4 billion Harrah'sacquisition of Caesars Entertainment. Once completed,Harrah's will be operating four world-class casino hotelproperties including Bally's, Caesars, Showboat and, ofcourse, the Harrah's Marina property. Even the new guyon the block, Colony Capital, who operates Resorts willbe closing shortly on their acquisition of the Atlantic CityHilton, a purchase which will include several large tractsof land at the west end of the city.

Atlantic City is even excited about a recently filed bank-ruptcy by the Trump Organization. As stated by DonaldTrump, the three Trump Casinos are in dire need ofmajor renovations and expansion to maintain a com-petitive position in this growing marketplace. Thebankruptcy offers Trump an opportunity to recapitalizeand upgrade the three properties.

Although Atlantic City will never challenge Las Vegas insize, merely for geographic reasons, it is clear that theindustry in Atlantic City will be in a strong second placewith a 2004 gross win close to $4.7 billion. All currentindications are that 2005 could be the year that the citybreaks the $5-billion threshold.

Redevelopment efforts throughout the city are continu-ing and all eyes now are focusing on the re-opening ofthe Million Dollar Pier (formerly Shops at Ocean I). Thisnew non-gaming venue will position the city as a truenational convention hub with gaming and non-gamingopportunities, including over one-million square feet ofnew upscale shopping.

The more we study the industry, the more we recognizethat the gaming industry provides a draw necessary tosupport the upscale hotel, resort, entertainment andshopping venues necessary to attract the Baby Boomersand Generation Xers. Clearly the ability to support andfund world-class boxing and top-line entertainmentwhile providing luxury hotel rooms at moderate pricingare the features that attract American and internationaltravelers to Las Vegas and Atlantic City. Continued

growth in the economy and the building of underlyingfamily wealth should bode well for the gaming industry.

As stated several years ago in the early planning stagesof the Borgata site, the various state initiatives andexpansion of the Indian gaming markets have helpedthe industry by legitimizing recreational gaming andexposing a larger segment of the population to thisform of recreation.

TABLE 16

U.S. LODGING INDUSTRY – KEY STATISTICSSupply Demand Fixed

% % % % ADR % RevPAR % GOP ExpensesChg Chg Occupancy Chg $ Chg $ Chg (RTS)* (RTS)

1992 0.8 2.1 62.6 1.3 59.17 1.5 37.06 2.8 29.5 25.61993 0.4 1.9 63.6 1.6 60.79 2.7 38.64 4.2 30.5 22.81994 1.2 3.1 64.7 1.7 63.19 3.9 40.91 5.9 36.2 24.01995 1.5 2.1 65.1 0.6 66.22 4.8 43.10 5.4 37.0 20.11996 2.4 2.32 64.9 -0.3 70.53 6.5 45.81 6.3 38.2 17.61997 3.6 2.8 64.4 -0.8 74.71 5.9 48.13 5.1 40.3 15.81998 4.2 3.1 63.8 -0.9 78.17 4.6 49.86 3.6 40.2 13.51999 4.1 3.0 63.2 -1.1 81.29 4.0 51.33 2.9 39.2 13.92000 3.1 3.7 63.5 0.6 85.24 4.9 54.15 5.5 40.9 13.52001 2.4 -3.4 60.0 -5.7 84.92 -1.3 50.96 -6.9 37.0 17.72002 1.8 0.8 59.1 -1.0 83.35 -1.5 49.24 -2.5 N/A N/A2003 1.3 1.6 59.2 0.2 83.28 -0.1 49.34 0.2 N/A N/A* Gross operating profit ratio to sales

SOURCE: © 2004 Smith Travel Research

PROPERTY SECTORS – LODGING

16 INTEGRA REALTY RESOURCES, INC. VIEWPOINT 2005

Before 2000, the lodging industry fared well with gen-erally stable occupancy rates and increasing ADR andRevPAR. In particular, IRR – Hospitality identifies severalkey forces that affected the expansion cycle of lodgingassets immediately before 2000 including:

• Improved hotel performance since 1993

• Financing availability at low interest rates

• Demand from real estate investment trusts (REITs)

• Growing economic trends

• Expansion of major franchise affiliations

However, the market sharply declined during the 2000-01 national recession, especially after September 11th.These forces culminated in a deep and protracted eco-nomic downturn following the wars in Afghanistan andIraq; reduced consumer confidence/spending; and cap-ital market instability. A reversal of the past trends sur-faced in late-2002 into early-2003. The following chartshows this observed turnaround. More pronouncedimprovement has been observed through most of2004. The following demonstrates the rate(s) of growthor decline having taken place before and after thedownturn. Note the slope of ADR and OCC lines aremarkedly improved beginning in the latter part of2002, with a slight flattening during 2003, and anothersurge reflecting consistent improving conditionsobserved through May 2004. (As will be noted below,these trends have continued to take place throughSeptember 2004.)

The growth recorded above is a result of an expandingeconomy and improving capital markets, causing amuch-anticipated recovery in the U.S. lodging industry.Actual RevPAR improvement in the first six months of

2004 was 9.5%, as reported by all companies that trackthese statistics, including Smith Travel. ADR increasedin the range of 3.2% during the same period, a growthrate similar to that reported during the post 1990-91recession. In relative terms, this increase is more posi-tive since the rate of inflation is noticeably less post-2003 when compared to the early-1990s. If this trendcontinues through the remainder of 2004 (data avail-able through September 2004 available through SmithTravel projections appears to support these estimates),the rate of recovery in RevPAR will be the highest inalmost 25 years. As a result of this recent and projectedgrowth, hotel operators are expecting a 17.9% increasein operating profits, also the highest rate in about 25 years.

In addition to the above, other major observations inthe broader market are as follows: