Comprehensive Annual Financial Reportgfoa.net/cafr/COA2012/MoraineValleyCommunityCollegeIL.pdf ·...

147

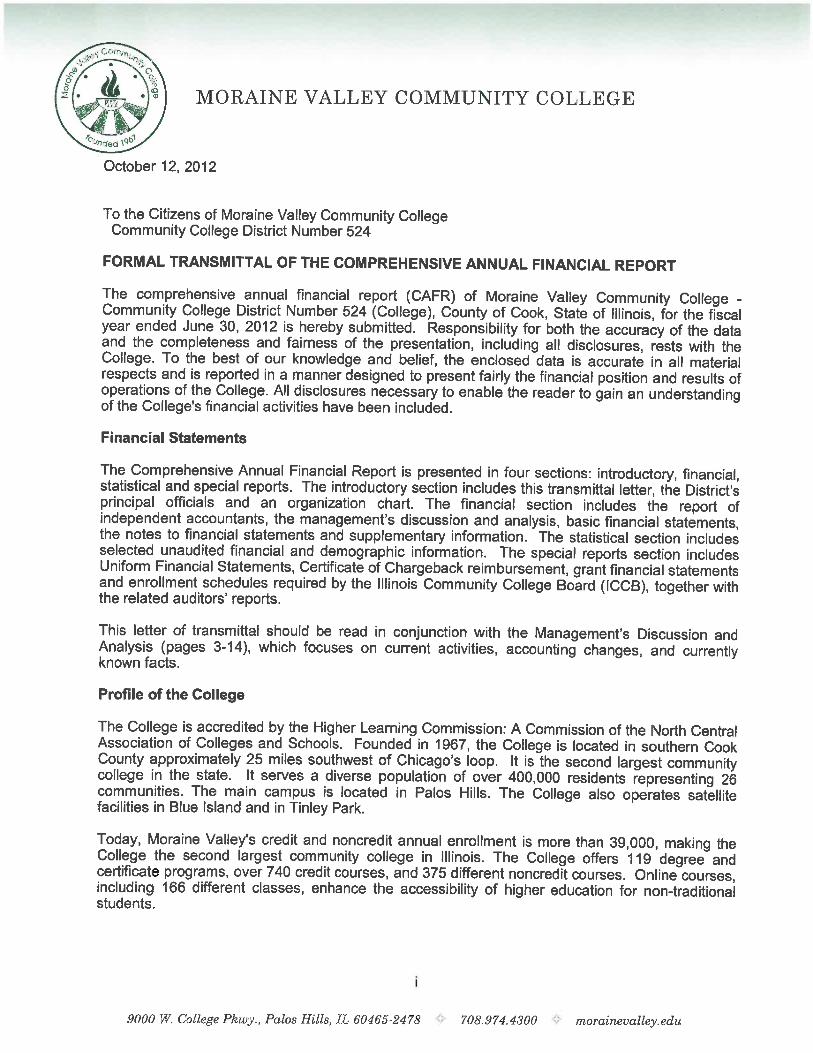

Comprehensive Annual Financial Report Fiscal Year Ended June 30, 2012 Community College District Number 524 Palos Hills, IL

Transcript of Comprehensive Annual Financial Reportgfoa.net/cafr/COA2012/MoraineValleyCommunityCollegeIL.pdf ·...

Comprehensive AnnualFinancial Report

Fiscal Year EndedJune 30, 2012

Community CollegeDistrict Number 524Palos Hills, IL

MORAINE VALLEY COMMUNITY COLLEGE COMMUNITY COLLEGE DISTRICT NUMBER 524

PALOS HILLS, ILLINOIS

10/08/2011

COMPREHENSIVE ANNUAL FINANCIAL REPORT

FISCAL YEAR ENDED JUNE 30, 2012

Prepared by:

Division of Finance

Robert J. Sterkowitz Chief Financial Officer / Treasurer

Theresa O’Carroll

Controller

William Corrello Internal Auditor

MORAINE VALLEY COMMUNITY COLLEGE COMMUNITY COLLEGE DISTRICT NUMBER 524

Palos Hills, Illinois

COMPREHENSIVE ANNUAL FINANCIAL REPORT June 30, 2012

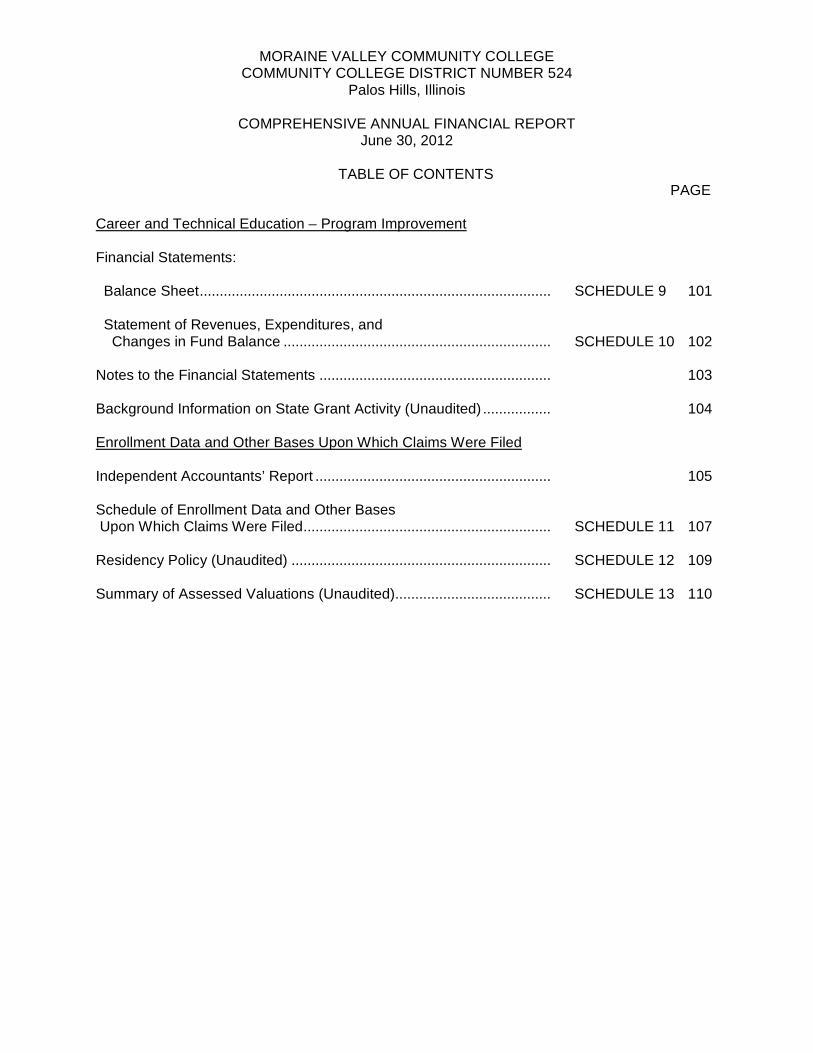

TABLE OF CONTENTS

PAGE INTRODUCTORY SECTION (UNAUDITED)

Transmittal Letter ..................................................................................... i Principal Officials ..................................................................................... xx Organization Chart ................................................................................... xxi Certificate of Achievement for Excellence in Financial Reporting (GFOA) xxii Certificate of Excellence in Financial Reporting (ASBO) ........................ xxiii

FINANCIAL SECTION Independent Auditors’ Report .................................................................. 1 Management Discussion and Analysis .................................................... 3 BASIC FINANCIAL STATEMENTS: Statement of Net Assets ........................................................................ STATEMENT 1 15 Statement of Revenues, Expenses, and Changes in Net Assets ......... STATEMENT 2 16 Statement of Cash Flows ..................................................................... STATEMENT 3 17 Notes to Basic Financial Statements ..................................................... 19 SUPPLEMENTARY INFORMATION: Schedule of Management Information – Detail of Operating Expenses By Function and Object ......................................................................... EXHIBIT 1 43 Schedule of Expenditures for Tort Immunity Purposes ........................ EXHIBIT 2 44

STATISTICAL SECTION (UNAUDITED) Net Assets by Component ....................................................................... TABLE 1 45 Changes in Net Assets ............................................................................ TABLE 2 47 Assessed Value and Actual Value of Taxable Property ......................... TABLE 3 49 Property Tax Levies and Collections ....................................................... TABLE 4 51

MORAINE VALLEY COMMUNITY COLLEGE COMMUNITY COLLEGE DISTRICT NUMBER 524

Palos Hills, Illinois

COMPREHENSIVE ANNUAL FINANCIAL REPORT June 30, 2012

TABLE OF CONTENTS

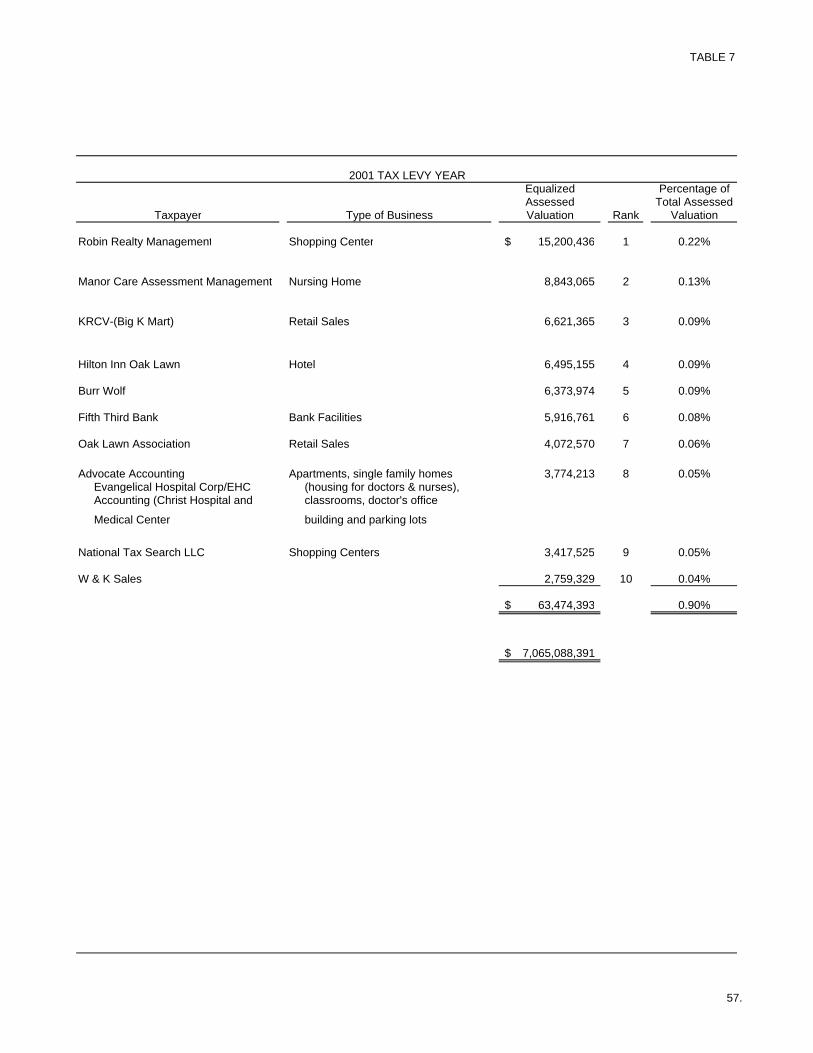

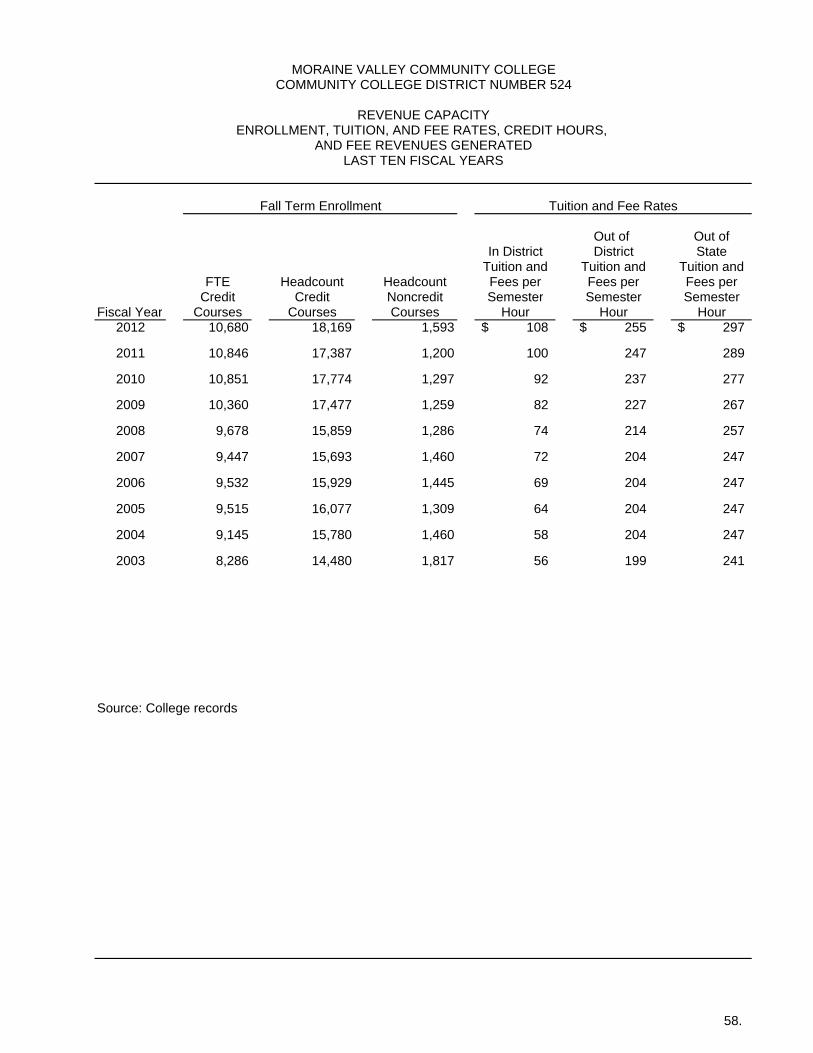

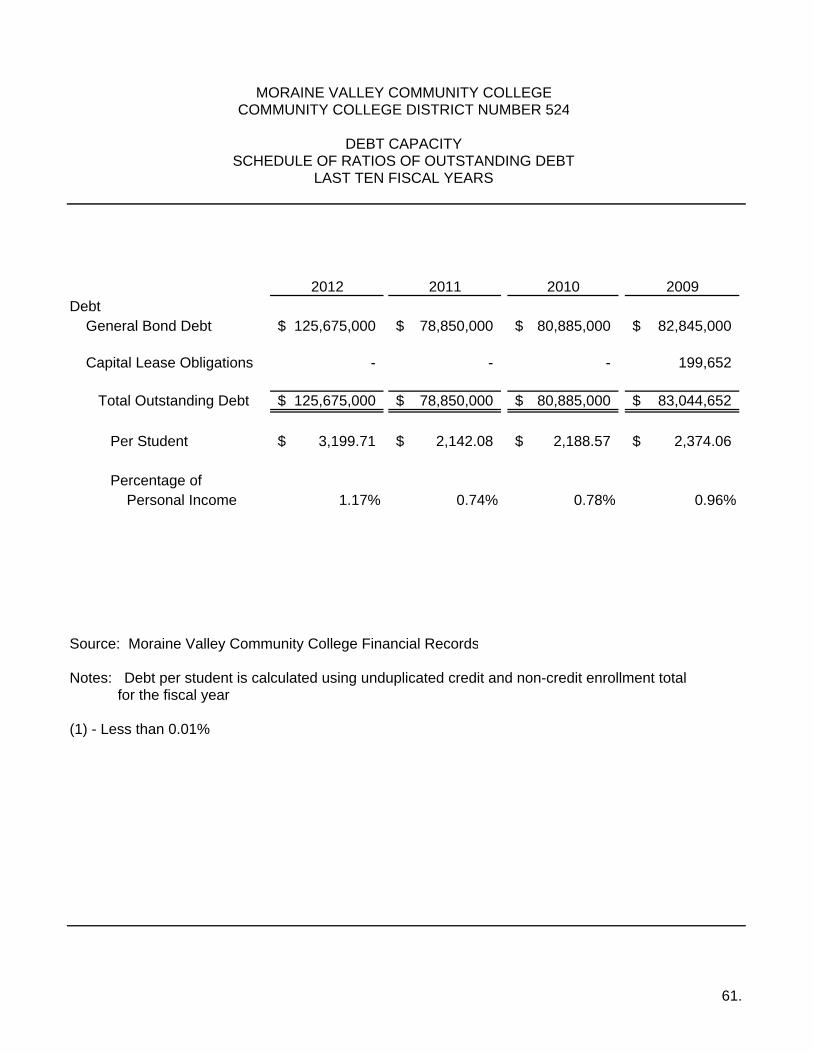

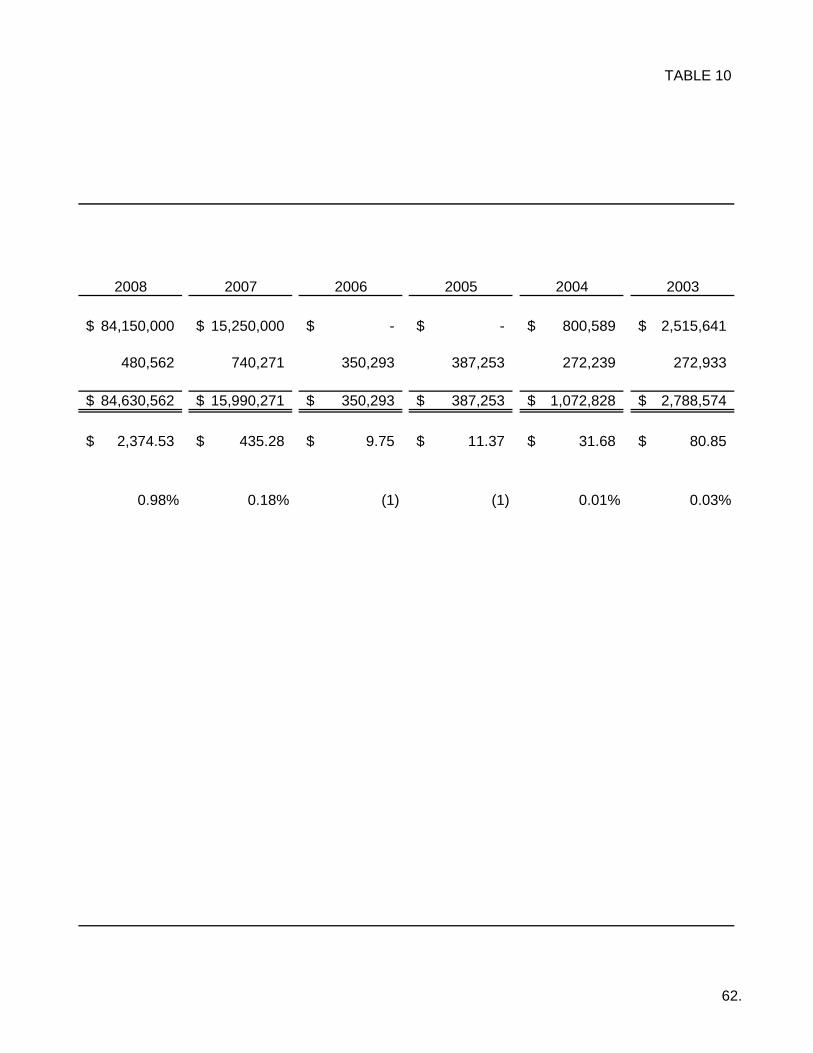

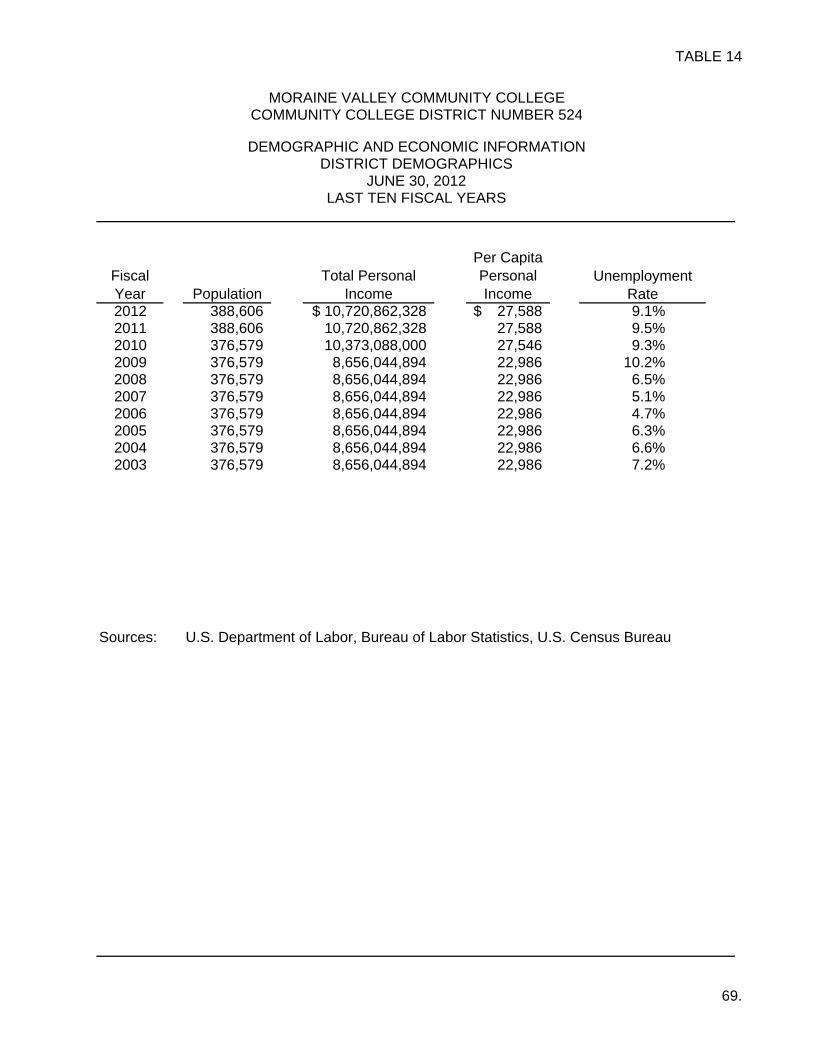

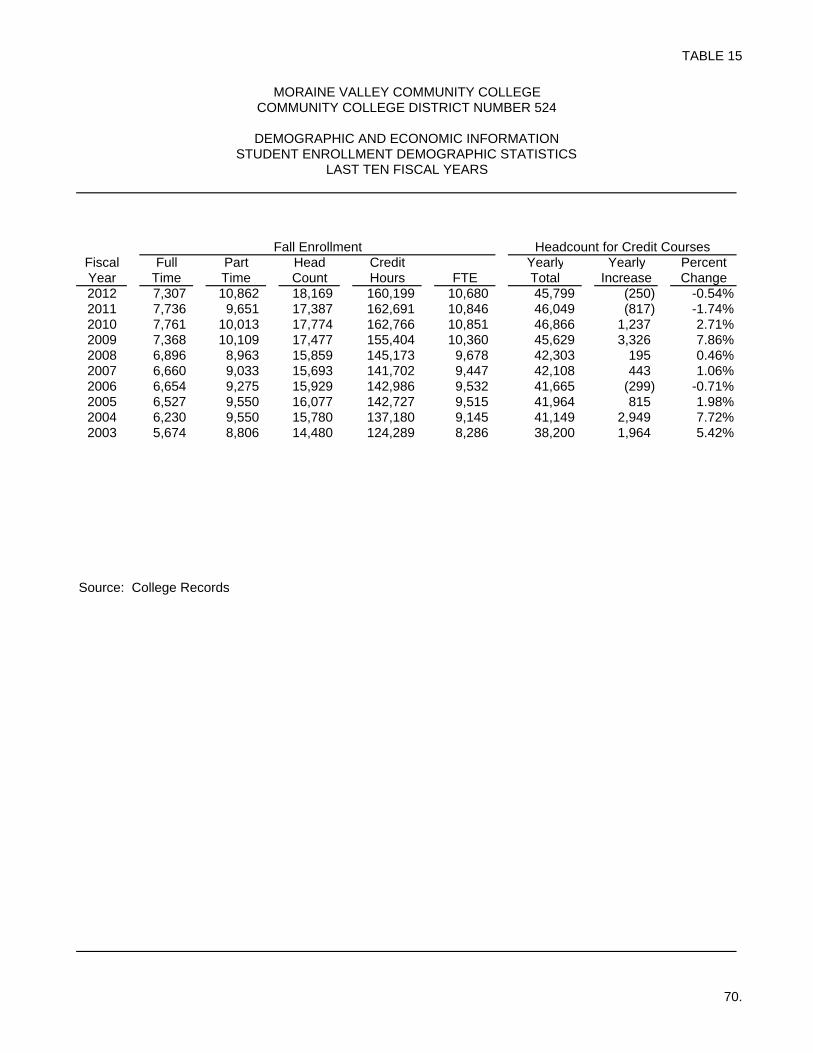

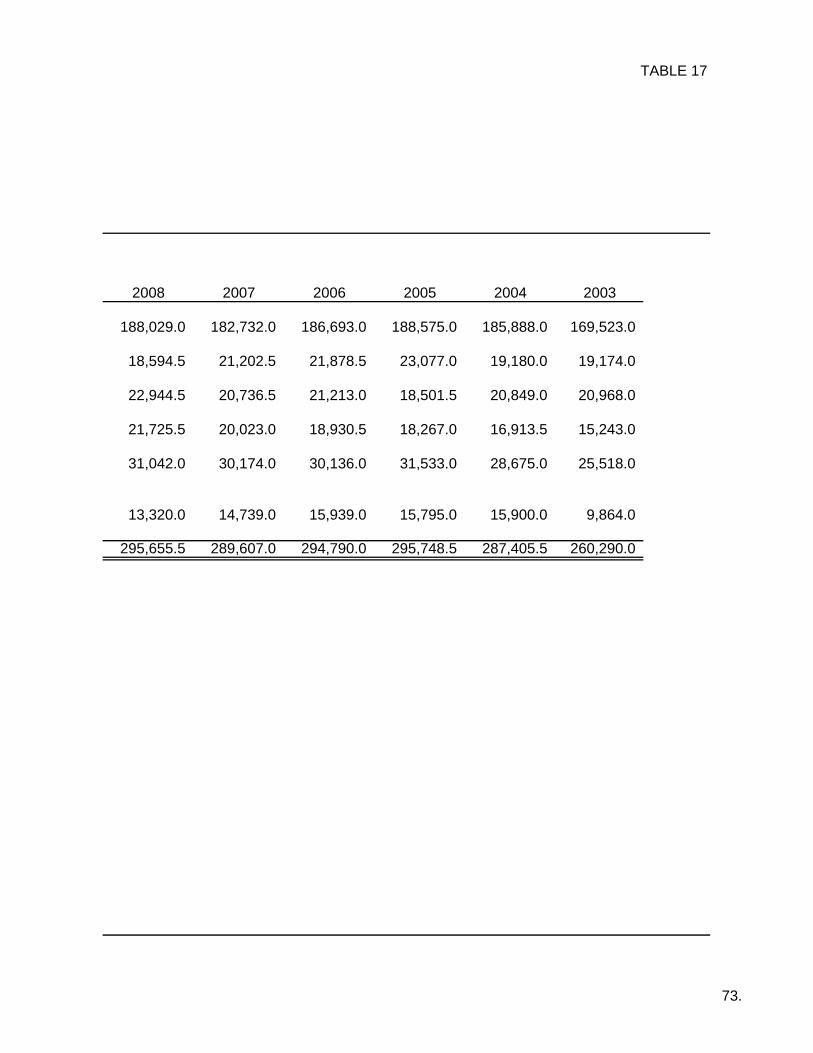

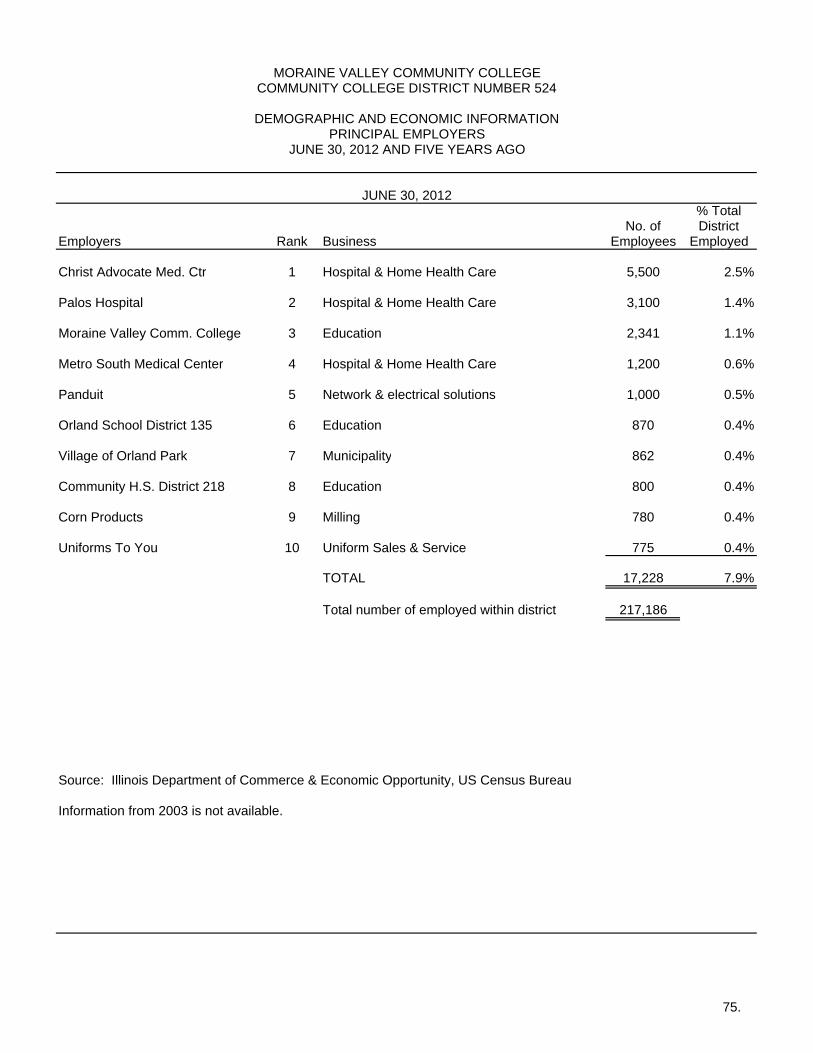

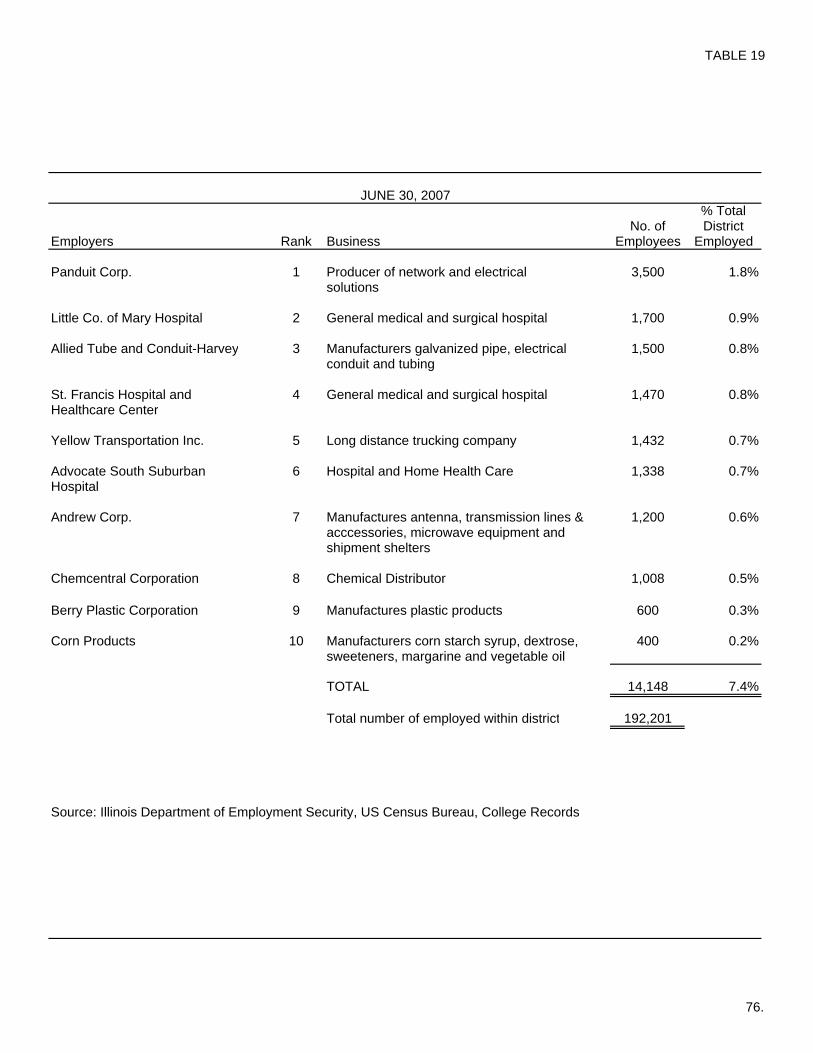

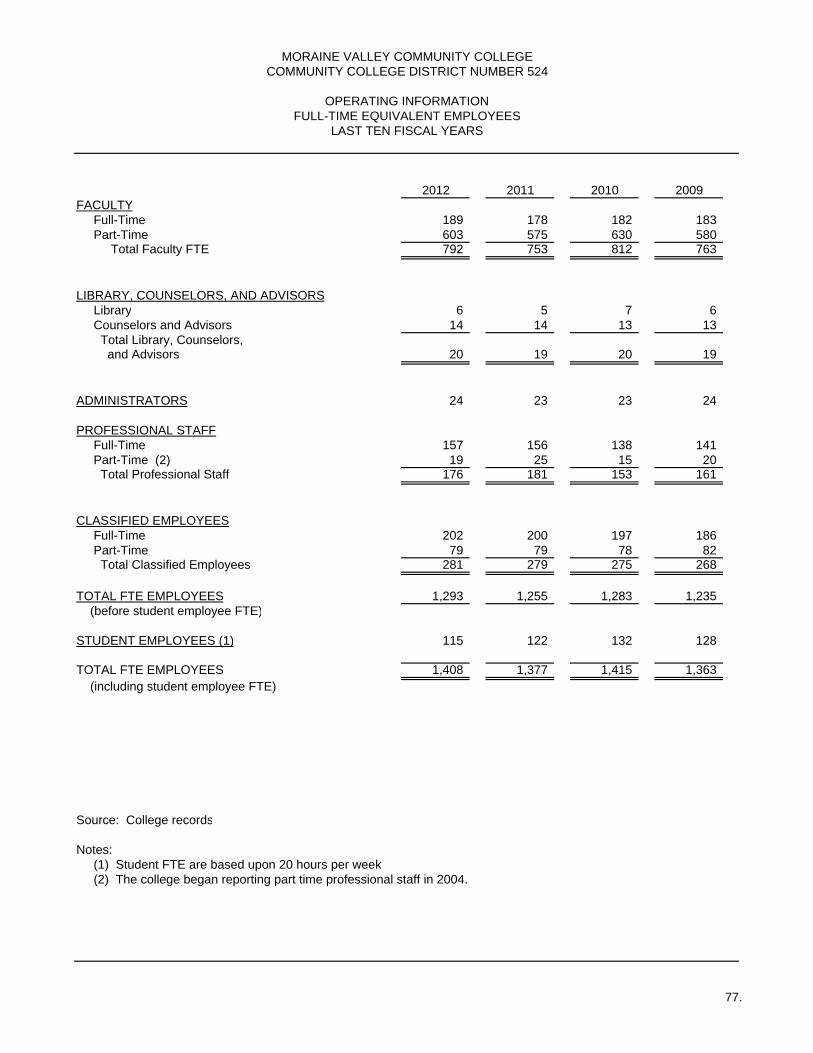

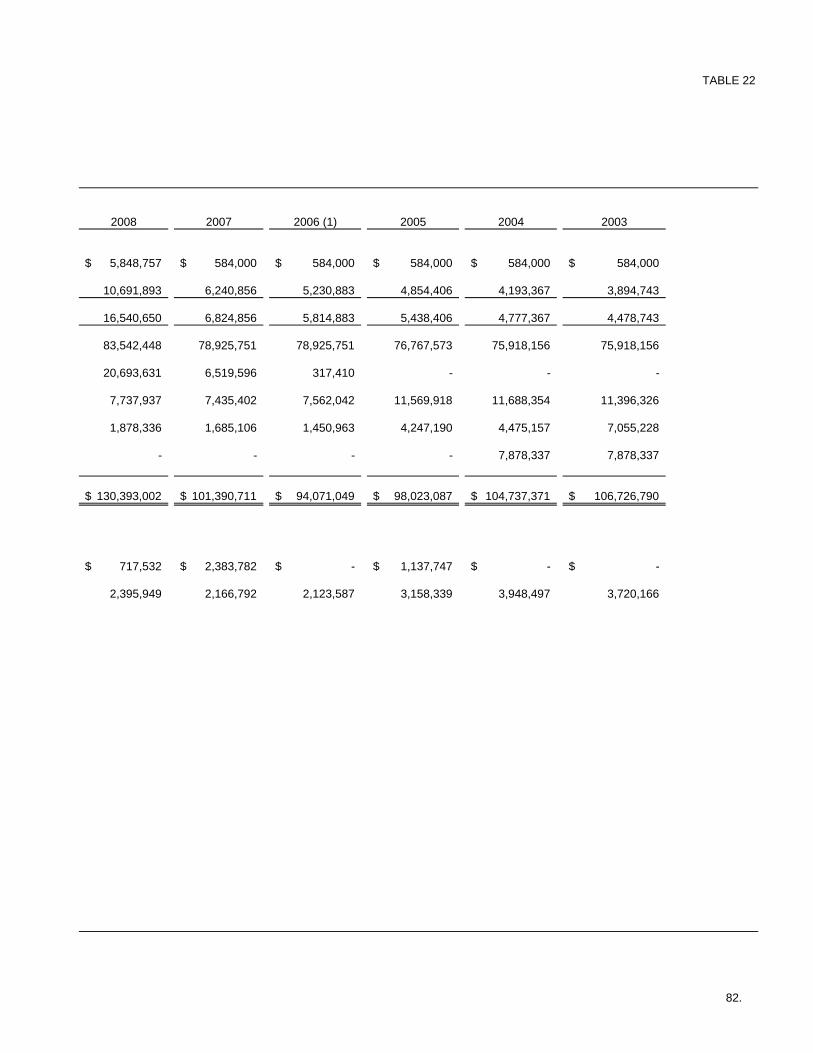

PAGE Assessed Valuations, Taxes Extended and Tax Rates .......................... TABLE 5 52 Property Tax Rates-Direct and Overlapping Governments .................... TABLE 6 54 Principal Property Taxpayers .................................................................. TABLE 7 56 Enrollment, Tuition, and Fee Rates, Credit Hours, and Fee Revenues Generated .............................................................................................. TABLE 8 58 Ratio of Net General Bonded Debt to Assessed Value and Personal Income and Net General Obligation Bonded Debt per Capita .............. TABLE 9 60 Schedule of Ratios of Outstanding Debt ................................................ TABLE 10 61 Computation of Direct and Overlapping Debt ......................................... TABLE 11 63 Legal Debt Margin Information ................................................................ TABLE 12 66 Pledged Revenue Coverage ................................................................... TABLE 13 68 District Demographics .............................................................................. TABLE 14 69 Student Enrollment Demographic Statistics ............................................ TABLE 15 70 Student Enrollment and Miscellaneous Statistics Annual Unduplicated Enrollment....................................................................... TABLE 16 71 Credit Hours Eligible for Funding by Illinois Community College Board Reimbursement Categories ........................................................ TABLE 17 72 College Demographics ............................................................................ TABLE 18 74 Principal Employers ................................................................................. TABLE 19 75 Full-Time Equivalent Employees ............................................................. TABLE 20 77 Capital Asset Statistics - Volume............................................................. TABLE 21 79 Capital Asset Statistics - Value ................................................................ TABLE 22 81

MORAINE VALLEY COMMUNITY COLLEGE COMMUNITY COLLEGE DISTRICT NUMBER 524

Palos Hills, Illinois

COMPREHENSIVE ANNUAL FINANCIAL REPORT June 30, 2012

TABLE OF CONTENTS

PAGE SPECIAL REPORTS SECTION Uniform Financial Statements ................................................................. SCHEDULE 1 83 Certification of Chargeback Reimbursement .......................................... SCHEDULE 2 90 Independent Auditors’ Report .................................................................. 91 Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Grant Program Financial Statements Performed in Accordance with Government Auditing Standards ............................................................. 93 Workforce Development – Business/Industry Grant Program Financial Statements: Balance Sheet………………………………………………………… ....... SCHEDULE 3 95 Statement of Revenues, Expenditures, and Changes in Fund Balance ................................................................... SCHEDULE 4 96 ICCB Compliance Statement for the Workforce Development Business & Industry Grant .............................................. SCHEDULE 5 97 State Adult Education Restricted Funds Financial Statements: Combined Balance Sheet ...................................................................... SCHEDULE 6 98 Combined Statement of Revenues, Expenditures, and Changes in Fund Balances ................................................................. SCHEDULE 7 99 ICCB Compliance Statement for the Adult Education and Family Literacy Grant ........................................................................... SCHEDULE 8 100

MORAINE VALLEY COMMUNITY COLLEGE COMMUNITY COLLEGE DISTRICT NUMBER 524

Palos Hills, Illinois

COMPREHENSIVE ANNUAL FINANCIAL REPORT June 30, 2012

TABLE OF CONTENTS

PAGE Career and Technical Education – Program Improvement Financial Statements: Balance Sheet ........................................................................................ SCHEDULE 9 101 Statement of Revenues, Expenditures, and Changes in Fund Balance ................................................................... SCHEDULE 10 102 Notes to the Financial Statements .......................................................... 103 Background Information on State Grant Activity (Unaudited) ................. 104 Enrollment Data and Other Bases Upon Which Claims Were Filed Independent Accountants’ Report ........................................................... 105 Schedule of Enrollment Data and Other Bases Upon Which Claims Were Filed .............................................................. SCHEDULE 11 107 Residency Policy (Unaudited) ................................................................. SCHEDULE 12 109 Summary of Assessed Valuations (Unaudited)....................................... SCHEDULE 13 110

Introductory SectionFiscal Year EndedJune 30, 2012

Community CollegeDistrict Number 524Palos Hills, IL

ii

Economic Condition and Outlook The College is located on over 300 acres of land and covers 139 square miles representing a population over 400,000. The College district is in all or part of the following 26 communities: Alsip Forest View Palos Heights Bedford Park Hickory Hills Palos Hills Blue Island Hometown Palos Park Bridgeview Justice Robbins Burbank Merrionette Park Summit Calumet Park Oak Forest (11%) Tinley Park (40%) Chicago Ridge Oak Lawn Willow Springs (80%) Crestwood Orland Hills Worth Evergreen Park Orland Park Mission The College’s mission is guided by the Illinois Public Community College Act, which established the statewide community college system. Simply stated, that mission is to serve the post-secondary educational needs of the residents of District 524. The mission of our college is to educate the whole person in a learning-centered environment, recognizing our responsibilities to one another, to our community, and to the world we share. We value excellence in teaching, learning, and service as we maintain sensitivity to our role in a global, multicultural community. We are committed to continuous improvement and dedicated to providing accessible, affordable, and diverse learning opportunities and environments. We promise to provide a student-centered environment and to focus all College staff and resources on student learning, student development, and student success. The College fulfills its educational mission through:

General Education—Courses and concepts integrated into the curriculum that foster critical thinking and enable informed judgment and decision making

Transfer Programs—Courses in arts, sciences, and business leading to an associate’s degree and fulfilling the first two years of a bachelor’s degree

Career Education—Occupational courses and skill development that respond to industry and community needs and lead to professional credentials, a certificate or an Associate in Applied Science degree

Community Enrichment—Opportunities for residents to engage in lifelong education and cultural enrichment in a learning community

Workforce Development—Partnerships with and customized training for business, government, social, and civic institutions resulting in organizational and economic improvement

Student Development—Programs and services to support and enhance academic, career, and personal growth and success for our diverse student population

Developmental and Enrichment Education—Courses, programs, and services to support and advance academic success leading to high school equivalency, English language proficiency, or entry to college-level courses

iii

Core Values

Integrity Responsibility Respect Fairness Diversity

Service Statement

We promise to provide a student-centered environment and to focus all College staff and resources on student learning, student development, and student success.

Promise Statement

We value the members of our college community and recognize that each individual is entitled to respect, understanding and positive communication. We recognize that Moraine Valley Community College employees are the College's most valuable resources.

In support of the College's strategic directions, we are committed to providing quality service to students, including prospective, currently enrolled and graduates; community residents; fellow staff members; and others who come in contact with the College.

Vision

We envision a world-class college that meets current and emerging community needs for education and training through excellent service and outstanding programs offered in stimulating learning environments. Strategic Priorities As a learning-centered college, we dedicate all programs, services and resources to student success, with a commitment to continuously monitor, assess, and improve our performance. Moraine Valley will:

• Emphasize and Promote Student Success • Enhance Community Awareness, Connections and Partnerships • Embrace Diversity • Plan, Achieve, and Manage Growth • Build Organizational Capability Through Continuous Improvement

Opportunities Support Student Growth and Success At Moraine Valley Community College, we provide unique learning experiences for our students in and out of the classroom to enable them to grow professionally and personally. Our exceptional faculty and staff, up-to-date technology, and welcoming atmosphere make Moraine Valley a learning-centered environment where all students can achieve their highest potential.

iv

Enrollment Remains High Moraine Valley provides our students with an exceptional education at an affordable price. We offer a host of extracurricular activities that allow them to pursue new interests, make friends and develop skills such as leadership, time management and communication. And, our campus is beautiful and inviting. All of this combines to make Moraine Valley a wonderful place for our district residents to begin or continue their college education. This year, our enrollment was again outstanding. Our total fall 2011 enrollment was up more than 6 percent compared to the previous fall, with 19,762 students. Credit student enrollment was at a record high, 4.5 percent higher than fall 2010, while noncredit enrollment was up an astonishing 33 percent. Plus, one third of area public high school graduates enrolled at Moraine Valley. We awarded 2,644 degrees and certificates to 2,187 graduates in 2011-2012, and the total number of degrees and certificates awarded to date is 51,870. Health Care Students Have Outstanding Pass Rates Students in our health care programs routinely exceed national pass rates on their licensure and certification tests. This year, they again did exceptionally well. Here is a sample of the pass rates of our graduates who challenged their state or national exams: • 100 percent passed for addictions studies • 100 percent passed for medical assistant • 100 percent passed for polysomnography • 94 percent passed for nursing • 94 percent passed for phlebotomy • 89 percent passed for health information technology • 82 percent passed for emergency medical technician • 80 percent passed for respiratory therapy • 79 percent passed for radiologic technology Agree to Degree Inspires Students to Strive for Program Completion Moraine Valley always has encouraged our students to work toward attaining their degree or certificate with a high level of success. In fact, according to Community College Week’s annual “Top 100 Associate Degree Producers Report,” we are in the top 3 percent in degrees conferred among the nation’s 2,839 two and four-year institutions granting associate degrees. And, we are third in the country in the multi-interdisciplinary studies (science transfer) associate’s degree category. Also, we enacted several Graduation and Completion Rate initiatives and launched our campus wide Agree to Degree campaign. This effort, which encourages our students to sign a pledge that they will commit to earning their associate’s degree or certificate, was enthusiastically embraced by students, faculty and staff. In the spring, a graduation/transfer event was held. Academic advisors completed degree audits with students to verify they had completed the necessary credits to graduate. Students also had an opportunity to meet with over a dozen universities for a possible on-the-spot transfer admission with no application charge. More than 50 of our students applied, and 45 were immediately admitted.

v

All of our efforts have been paying off! This year, we experienced a one-year increase of 18 percent and a five-year increase of 60 percent in the number of degrees and certificates we awarded. Illinois Lt. Gov. Sheila Simon visited Moraine Valley as part of her tour of the state’s 48 community colleges to see completion efforts at each campus. She met with administrators and students, and learned more about our initiative. She was given an Agree to Degree T-shirt by one of the student leaders. In addition, the Agree to Degree campaign materials received a Gold award in the National Council of Marketing and Public Relations’ annual Paragon Awards competition. New Programs and Courses Enhance Opportunities By expanding the programs and courses we offer, Moraine Valley continually meets the ever-changing needs of our students. New Certificates and Programs • Android Developer Certificate • Associate Database Administrator Certificate • Gerontology Certificate • IPhone Developer Certificate • Pharmacy Technician Review Program (noncredit) • PHP Programmer Certificate Our Fire Service Management Program offered its first Fire Academy, which prepares participants to complete specific objectives required by the Illinois State Fire Marshal’s Office. All 13 students in the inaugural session met the objectives and participated in a graduation ceremony that was attended by area fire service professionals and Moraine Valley staff members. Also, the Nursing Department graduated its first cohort from the revised Associate Degree Nursing Program, which gives graduates the option to sit for their licensed practical nurse boards after their second semester. New Courses • Android Programming I and II • Discrete Mathematics • IPhone Programming I and II • Law and Ethics in Healthcare • Oracle Database Management • PHP Programming I and II In addition, the Office Systems and Applications certificate curriculum was revised to better reflect current trends. Celebrating Our Students’ Success The College’s chapter of Phi Theta Kappa, the international honor society for two-year and junior colleges, received Five-Star Status, which is the highest level that can be attained. The chapter also received two Illinois Regional Awards for Service Hallmark and College Project and nominated two students for the All-Illinois Academic Team for Community Colleges.

vi

An Honors Program student was accepted at the prestigious Ivy League institution Cornell University. The Gilman Scholarship Program awarded a Moraine Valley student a $3,000 scholarship to allow him to pursue his studies at Canterbury Christ Church University in England. A Travel-Tourism and Meeting Planning student received a Skål International scholarship from this worldwide organization of tourism executives. Our students participated in the annual Skyway Art, Jazz, STEM, and Writing competitions, as well as in the annual League for Innovation in the Community College’s Art and Writing competitions. Four Moraine Valley students were recognized as Outstanding Soloists and two received Honorable Mentions at the Jazz competition; one student received a second place in poetry at the Writing competition; six students had their artwork selected for the Skyway Art Show; and three teams, made up of 11 students, were recognized with medals for their work in the STEM poster competition. The Glacier student newspaper won numerous awards at the Associated Collegiate Press/College Media Matters National College Newspaper Conference. The paper’s student staff also hosted the Illinois Community College Journalism Association’s sectionals competition. The Moraine Valley Percussion Ensemble performed with the Elmhurst College Percussion Ensemble at their November 2011 concert. They also participated in the 2012 Lincoln-Way Central Day of Percussion, where the group received excellent comments from clinician and noted percussionist, Rich Holly of Northern Illinois University. Four literacy students serve as president, vice president, secretary, and treasurer on the governing board of New Readers for New Life, a network of past and current adult literacy students affiliated with Literacy Volunteers of Illinois. At the Phi Rho Pi National Speech and Debate Tournament, our Forensics team took home the Bronze award, and individual team members received one Gold, six Silver, and three Bronze awards. Moraine Valley hosted the event, which attracted more than 600 student competitors from over 60 community colleges and four-year institutions from across the nation. Student Success – Our Number-One Commitment Moraine Valley’s mission statement says that we “educate the whole person in a learning-centered environment.” By offering numerous programs and services to meet our students’ individual needs, we strive to accomplish this each day. Orientation Our orientation programs provide students with the tools and information they need to make a successful start in college. To ensure our student veterans and their family members properly receive their military educational benefits, we offer the Mandatory Veteran Advising Session and Veteran Orientation programs. More than 670 students were advised on the correct programs and courses they should take to receive their maximum benefits.

vii

New Student Orientation sessions for Developmental Reading and part-time students were implemented to assist these unique populations in identifying appropriate college resources and selecting courses. Each student attending New Student Orientation received a USB flash drive that contains orientation information, along with College practices and procedures. Students can utilize the drives during their College 101 education-planning meeting and during future academic advising sessions. Tutoring Students sometimes need extra help gaining knowledge and abilities necessary to succeed in college, preparing for tests or mastering specific skills. Our various tutoring opportunities give them the assistance they need. This year, we expanded offerings, locations and the number of tutors.

• The Literacy Program increased their tutoring sites from 22 to 28 locations in our district.

• More than 40 new adult volunteer tutors were trained for the Literacy Program.

• Tutors were designated to work specifically with GED students preparing to take their GED exam.

• Group, peer and drop-in tutoring were established, and online videos were added, to allow students more options when seeking assistance.

• Members of the Honors Program and Phi Theta Kappa served as tutors. Learning Opportunities Beyond Moraine Valley’s Campus We also support our students’ learning beyond the confines of our campus to provide hands-on experiences that will translate into important job skills.

• Culinary Arts students attended the annual National Restaurant Association Show in Chicago.

• Recreation Therapy students attended the Illinois Recreational Therapy Annual Conference

and hosted a Teen Sports Night.

• Travel and Tourism students went to the Motivation Show at McCormick Place and the Hospitality Sales and Marketing Association International’s Meet Mid-America at Navy Pier. They also volunteered at the National Restaurant Association Show.

• Members of the Meeting Planning and Travel Club planned and executed a familiarization

trip to Springfield, Ill. They gained experience making reservations, inspecting convention centers, and planning meals.

• Students in the Special Events Management class helped with the popular annual

Magnificent Mile Lights Festival Parade in Chicago.

viii

• The Psychology Club visited a mental health courthouse to learn about forensic psychology in a real-life situation.

• Students in Introduction to Sociology classes participated in the Sociology in the Global

Village Project, which lets students research a variety of non-Western countries to gain knowledge regarding differences in socioeconomic, cultural, and social aspects of various societies.

• Future teachers and paraprofessionals attended the Experiencing Autism Program, which

gave them the opportunity to see what it would be like to be autistic and to learn strategies for working with autistic children.

• Students in the Older Adult Recreation and Wellness course organized a Good Old Times

event with activities surrounding New York, Las Vegas, and Hollywood themes to learn all aspects of event planning for senior citizens. They also presented a holiday program for residents at a senior residence.

• Students in the Recreation for Special Populations class arranged a Snow Flurries event for

more than 300 elementary school students to promote self-esteem and team building.

• In addition, approximately 8,500 students participated in more than 150 events that were presented by the Student Life Office that helped develop skills in leadership, team building, communication, community awareness, and more.

Improved Instruction Means More Learning The Center for Teaching and Learning offered more than 160 professional development workshops to faculty and staff on topics such as Avoiding Cheating and Plagiarism, Creating Effective Collaboration in the Classroom, Understanding the Digital Generation, and more. Over 1,100 attendees took advantage of these opportunities. As one of the action projects for the Academic Quality Improvement Program, the College developed an assessment plan to measure and improve student learning across the General Education Core Curriculum. These courses foster complex learning across a wide array of disciplines and satisfy the Illinois Articulation Initiative, making it convenient for our students to transfer to other schools in Illinois. The College also created a set of six rubrics that will be used to score student work and determine areas of improvement in our curriculum and instruction. The Nursing Program piloted the American Testing Institute’s Comprehensive Assessment and Review Program System. This online product enhances nursing theory with online remediation, practice, and proctored assessments that are aligned with current licensing exams. It also allows faculty to analyze student learning to best target instructional improvements. Honors Program The number of Honors classes was increased from six to nine in the fall and spring semesters. Two new courses were also developed. Several faculty and students spoke at breakout sessions at the National Collegiate Honors Council annual conference in Phoenix, Ariz., which was the first time in the program’s nine-year history that students and faculty presented at an out-of-state conference.

ix

Athletic Achievement Highlights Our student-athletes worked hard on and off the field. We had 14 who were nominated for the National Junior College Athletic Association’s (NJCAA) Academic All-American awards. Two received the NJCAA Pinnacle Award for Academic Excellence for achieving a 4.0 grade point average after completing 45 semester hours. And, Moraine Valley’s Cyclones led the Illinois Skyway Collegiate Conference in academic achievement with 32 student-athletes named to the Conference All-Academic team. They also won the Illinois Skyway Collegiate Conference All Sports Trophy. The Cyclones qualified for berths in the national tournaments in men’s basketball, men’s cross country, men’s golf, and men’s and women’s tennis. Nearly 60 student-athletes received Skyway Conference and All-Region awards. And, two students were named NJCAA Athletic All-Americans, one from our men’s basketball team and one from our men’s golf team. A member of the women’s tennis team won the Novo Nordisk Donnelly Award, which is part of a student scholarship program established by Billie Jean King to encourage youth with diabetes to lead active lives and participate in tennis. The student also met Billie Jean King at the World Team Tennis Pro League championship. There are only two national scholarships given through this program each year. The same student also was named Region IV Player of the Year. The men’s basketball coach was named Co-Coach of the Year in NJCAA Division II by the Illinois Basketball Coaches Association, and also was named the Illinois Skyway Collegiate Conference Coach of the Year. Community Connections and Partnerships Continue to Thrive With a firm commitment to our role as a community college, Moraine Valley routinely connects with organizations, businesses and individuals to provide services and resources that will best serve our students and all district residents. Partnerships Provide Opportunities for Current and Potential Students Moraine Valley faculty and staff worked with the School of the Art Institute to develop an articulation agreement between the two institutions. Moraine Valley and DePaul University signed the Dual Admission Partnership Program. The partnership also includes a scholarship opportunity for our students. The College partnered with the Palos-Orland Chapter of the American Association of University Women to host their annual Math/Science Conference for fifth grade girls and their parents. The Glacier student-run newspaper partnered with the Illinois Press Association to hold a workshop on video editing for Illinois high school journalism educators. Faculty from the Health Sciences Department participated in a Health Care Career Day, which was sponsored by the Moraine Area Career System. Approximately 100 high school students who had expressed an interest in pursuing a career in health care learned about the College’s health care programs and asked questions about the education necessary to be eligible for employment.

x

Work Experience Opportunities for Our Students The Job Resource Center worked with students to identify internships that would give them practical job skills. Our students gained experience in their respective fields of study, including Restaurant/Hotel Management, Culinary Arts, Travel/Tourism, Office Systems and Applications, Legal Office Assistant, and Mechanical Design and Drafting/CAD. The Fire Service Program partnered with the Alsip Fire Department and Frankfort Fire Protection District to help our students in the fire academy program master psychomotor objectives. The two departments authorized our fire academy instructors and students to use the burn towers at their training facilities to hone their skills. The Fire Service Program also worked with the Burbank Fire Department, North Palos Fire Protection District, Roberts Park Fire Protection District, and Willow Springs Fire Department to offer student internships as part of our Fire Service Operations A.A.S. degree program. We had 27 students who participated in the Disney College Program and served as interns at one of the Disney properties. The College partnered with Espo Systems to provide Information Technology students with internship opportunities. Supporting Our Veterans - AmeriCorps VISTA Volunteers Offer Assistance Two Volunteers in Service to America (VISTA) volunteers worked at the College to help improve services to our increasing veteran population and coordinate services provided by community organizations to meet the needs of student veterans both inside and outside of the classroom. Moraine Valley Gives Back to Community Moraine Valley’s staff and students volunteered to work in the College’s community garden. Many of the vegetables and herbs that were harvested were donated to the Moraine Valley Community Church food pantry. Two of our academic advisors planted a tree in Bridgeview’s Commissioners Park as part of a community service project of the Arab-American Family Services to recognize military service members. The Library donated books that were withdrawn from its collection to area nonprofit organizations rather than throw them away. This helped the various organizations raise funds through the sale of these materials and is a more sustainable option. College employees participated in the annual Employee Giving Campaign that raised more than $40,000 to benefit Moraine Valley Community College and its students, Southwest Suburban United Way and Community Health Charities of Illinois. Student Groups and College Staff Hold Numerous Events to Help Others Our students and staff volunteered their time, collected donations of money and basic necessities, and organized events to support individuals and organizations in need of assistance.

xi

• The Culinary Arts Program faculty and students prepared a meal for the residents, workers and guests at the Ronald McDonald House in Oak Lawn.

• Students in the Travel-Tourism Program helped with the Professional Convention Management Association’s charitable projects. They washed mini blinds for Housing Opportunities and Maintenance for the Elderly, an organization dedicated to improving the quality of life for Chicago’s low-income elderly. They also worked with the Off-the-Street Club, a Boys and Girls Club, in one of Chicago’s neediest, high-crime neighborhoods.

• Students in our Recreation Therapy and Recreation Management programs, our Education Program, and students from Stagg, Andrew, Chicago Christian, and Rich East high schools volunteered at the 28th Annual Illinois Special Olympic Motor Activity Program, held in the Moraine Business and Conference Center. More than 150 special athletes participated, which is the largest number of athletes in attendance since the event began.

• Students in Social Sciences classes participated in the global education event titled “Is the U.S. Falling Behind Educationally?” which discussed educational systems in the United States, China, India, and across the world. Attendees reflected upon the differences in these educational systems.

• Approximately 150 units of blood were donated through two blood drives sponsored by the Student Government Association.

• More than $3,000 was raised for St. Baldrick’s Foundation to help children with cancer. • The Music Club hosted a haunted house and collected nonperishable food that was

donated to the Greater Chicago Food Depository. • The Student Government Association and Gay, Lesbian, or Whatever (GLOW) Club

sponsored Change for Change to educate students about the Invisible Children movement, which provides support to war-affected communities in Africa.

• The Combat to College Student Veterans’ Organization held a holiday Toys for Tots collection to donate to the less fortunate in the community.

• The Alliance of Latin American Students sold candy and flowers to raise money for autism. • The Recreation Therapy/Management Club made and sold holiday ornaments to raise

money for Special Olympics. • The Arab Student Union held a winter coat drive. • Phi Theta Kappa held a food drive for Together We Cope. • Women Empowered participated in an Eye4Style event to raise money for the South

Suburban Family Shelter in Tinley Park. Providing Help for Those Seeking Work With many unemployed and underemployed people in our district, Moraine Valley offered programs and assistance to many students and community members. Secretary of Labor Hilda L. Solis and Under Secretary of Education Martha J. Kanter announced a national consortium of community colleges, including Moraine Valley, for training and workforce development to help unemployed workers who are changing careers. More than 200 community colleges around the country applied, and only 32 were selected by the U.S. Department of Labor in coordination with the U.S. Department of Education. The new National Information, Security and Geospatial Technology Consortium will focus on training workers for the information, security and geospatial technologies industries. Moraine Valley will take the lead on developing a virtual learning environment, updating and disseminating cybersecurity curriculum, as well as enhancing our current information technology program by developing a geospatial certificate/degree program. The College’s Job Resource Center hosted two Job and Internship Fairs, which attracted 110 employers and more than 900 job seekers. To help students understand the importance of

xii

dressing properly for a job fair, the center created displays across campus with mannequins dressed in professional attire. They also acquired professional outfits through a second-hand clothing store to lend to job fair attendees who came dressed in non-business clothing. More than 30 job seekers took advantage of this opportunity. More than 40 community college counselors attended the Counselors Consortium for the C-4 Counselors, which provided training on best practice when working with underemployed and unemployed students who have been out of work for extended periods of time. The new Career Paths and Coffee series, designed to help adults improve job-seeking skills or prepare for a new career, presented speaker Ziggy Letheby from the U.S. Department of Labor at an event which was attended by more than 80 community residents. Moraine Valley’s Police Department Offers Training and Programs to Ensure the Safety of our Students and Community Members Some of the department’s efforts included:

• Facilitated the staging and training of the South Suburban Regional Field Force Team in preparation for the NATO conference in Chicago. The team was designated as the primary Emergency Operations Center for the unit, representing 60 south and southwestern communities. This vital mutual aid unit provides regional communities with crowd control, emergency response and disaster response units, and ensures the protection of members of the campus community and our district residents in times of need.

• Offered eight free domestic violence training sessions for law enforcement personnel from

neighboring communities. The sessions were put on by the Domestic Violence Coalition and resulted in the training of more than 300 officers on current domestic violence procedures.

• Began a child safety seat program and installed child seats for students, community

residents and College staff. This program allows new parents and grandparents to have a certified representative properly install the seat and instruct them on its proper usage.

• Conducted a communications tabletop drill to test our external disaster response with our

South Metropolitan Higher Education Consortium partners. Moraine Valley Police Dispatch procedures were used as an example of preferred practices.

Expanding Community Awareness Moraine Valley embraces our role as a resource for all residents of District 524, and we offer educational programs, cultural events, and entertaining performances to fulfill this role. College Programs Educate, Enlighten and Entertain District Residents and Students Arts and History Guest poet Dr. Matthew Brennan, professor of English at Indiana State University, gave a poetry reading.

xiii

Dr. Theodore Karamanski, a history professor at Loyola University and consultant to the National Park Service, discussed Chicago’s role in the Civil War. Business and Careers The Economic Development Council for the Southwest Suburbs hosted a Business Resource Fair and Expo—“Be Responsible, Be Safe, Stay Profitable!” It featured guest speaker Maria Wynne, CEO of the Girl Scouts of Greater Chicago and Northwest Indiana, and introduced business leaders to useful resources in our community. The Criminal Justice Club invited Jeremy Hirst, a former Army Ranger, to speak about leadership and ways to manage emergency situations. Health and Safety More than 600 students and community members gained information on state-of-the-art medical treatments at lectures that were presented in partnership with Northwestern Memorial Hospital. Topics covered included “Cutting-Edge Therapies for Diabetes,” “Sleep: The Gentle Tyrant,” “Scars and Plastic Surgery: What’s New?” and more. The College’s Earth Month Celebration focused on health issues and included seminars such as “Flexitarians: Healthy You and Healthy Planet,” “Plastics and You: Is Convenience Worth the Cost?” and “A Conversation about Being Beautiful: Cosmetics for Men and Women.” The College hosted a Children’s Mental Health Conference. During Mental Health Month, a panel on eating disorders was presented and featured Dr. Jan Hart, Ph.D., a local clinical psychologist. Two student-run clubs hosted a self-defense workshop. More than 300 students attended a panel discussion on sex trafficking that included representatives from the Chicago Police Department, Chicago Alliance Against Sexual Exploitation and the Salvation Army’s STOP-IT Program. Fine and Performing Arts Center Gets Rave Reviews The Fine and Performing Arts Center presented 12 mainstage performances during its 2011-2012 season. The center again broke revenue and attendance records with more than 7,000 patrons attending the eclectic performances. Fun Under the Stars The College hosts family-friendly performances at our Gateway, such as summer productions of Shakespeare and the Movie in the Moonlight event. Enriching College Culture through Diversity At Moraine Valley, we are proud of our diverse student population, and we believe that each of us is enriched by learning about different cultures, being exposed to opposing ideas, and sharing our unique perspectives with others.

xiv

Discussion Explores Diversity More than 100 people from the 26 communities we serve, including elected officials, staff from local school districts, members of law enforcement, along with our faculty and staff, participated in the Community Dialogue on Promoting Diversity and Inclusion seminar and discussed thought-provoking questions and situations around diversity and inclusion. Fine and Performing Arts Center Showcases Music and Dance of Various Cultures • Juan Siddi Flamenco Theatre Company featured music, singing and dancing from Spain • Singer-songwriter Cathie Ryan performed Celtic music • Ragamala Dance highlighted art, music and dance from the Warli people of western India Sharing with Educators from Around the World Representatives from the Shanghai Institute of Health Sciences visited our campus. The College has a new relationship with this institution, and we received three transfer nursing students from it. The Automotive Technology Program hosted a delegation of Chinese automotive educators and administrators to share ideas on educating students and discuss our curriculum and practices with them. A professor in our Child Care Program traveled to Guatemala to observe a Montessori school and a preschool. She brought what she learned back to familiarize her students with the educational systems and philosophies of different cultures. Events Focus on Diversity Topics The College partnered with the Palos Fine Arts Association to present the One Book, One College and Palos Reads Program on the book Between Two Worlds: My Life and Captivity in Iran. The book’s author, Roxana Saberi, visited campus and discussed her experiences after she was accused of being an American spy in Tehran. The Blue Island Education Center offered a piñata demonstration for Hispanic Heritage Month and a line dance demonstration for African-American History Month. The College offered workshops and a webinar to promote minority student success including, “Building for Success: A Model for Improving African-American Male Retention”, “Success and Diversity, Collaborations for First-Generation Hispanic Student Success,” and “Understanding the Arab/Arab-American Student Population on Campus.” At the College’s annual Staff Recognition Dinner, a new Embracing Diversity Award was announced. College president Dr. Vernon O. Crawley received the inaugural award, which will be given annually. Emphasis on Language Improves and Expands Learning The International/U.S. Conversation Partners Program was implemented to increase friendship and interaction between local students and international students. More than 180 students participated and spent time communicating with each other, attending events together, and sharing their life experiences, in an effort to gain cross-cultural knowledge and awareness.

xv

The Children’s Learning Center added Spanish language instruction to its curriculum. The center also invited members of the Arab Student Union to teach the children Arabic for a day. Student Life Office Sponsors Numerous Events to Promote Understanding and Acceptance of Diverse Populations

• GLOW Club sponsored National Coming Out Day • Alliance of Latin American Students celebrated the Day of the Dead • Combat to College Student Veterans’ Organization and GLOW held a luncheon to honor

the repeal of the Don’t Ask, Don’t Tell policy • Arab Student Union celebrated Arab Heritage Month, with cultural displays including food,

henna tattoos, music, and dance • Phi Theta Kappa sponsored Unity in the Community Week to improve student engagement

on campus • The Alliance of African-American Students celebrated Black History Month with “Soul

Valley”—a fashion show and Soul Train Line where historical facts were shared • Women Empowered recognized Women’s History Month by viewing Miss Representation, a

film that explores how the media’s misrepresentations of women has led to the underrepresentation of women in positions of power and influence

• Women Empowered hosted a session that included information about the styling and care of natural black hair, and promoted safety, health and money-saving tips

Energizing and Enhancing College Growth With an unrelenting commitment to excellence, Moraine Valley utilizes our resources to grow and maximize our students’ opportunities. Continuous Improvement—A College Focal Point Moraine Valley is committed to continuous improvement in all areas of the College—our programs, services and processes—to ensure we are giving our students the best education possible and providing our community with the exceptional community college it deserves. Saving Money for Our Students and Taxpayers We have a strong commitment to fiscal responsibility and continually look for ways to provide excellent service while protecting the interests of the taxpayers in our district.

• We joined a consortium with two other community colleges to save approximately $120,000 in health care insurance costs by jointly purchasing health insurance. The consortium is hoping to attract more colleges and reduce costs even further in the future.

• We ceased using the College’s mainframe computer server, which brings an annual cost savings of $222,000.

• We began automatically shutting down computers in common areas. Previously, these PCs may have been left on throughout the week or night.

• We joined forces with seven other South Metropolitan Higher Education Consortium colleges and universities to reduce our electricity costs. The schools worked together and secured a rate that will reduce monthly expenses by $25,000. The College hopes to apply some of the cost savings to future sustainability efforts.

xvi

Tip-Top Technology Moraine Valley has always had a strong commitment to providing the latest technology for our students. This year, we were ranked ninth among large-size community colleges with 10,000 or more enrollment by e.Republic’s Center for Digital Education and Converge Online’s Seventh Annual Digital Community Colleges Survey, which recognizes colleges that have made significant advances in utilizing information technology. Here are some of the technology enhancements and additions we made over the past year: The Education Department acquired 20 iPads for use in our Technology for Educators and Students with Disabilities in School classes. Currently, Moraine Valley is the only community college in Illinois using iPads in their education courses. The Heating and Air Conditioning Program received donations of two state-of-the-art direct digital control systems. A Mobile Technology Program was developed to utilize mobile devices as strategic instructional and office tools. Dr. Vernon O. Crawley Leadership Academy Launches The Leadership Academy was created to help employees of all levels develop and improve their leadership skills. Workshops that focused on delegation, communication and conflict management were offered. Plus, the Leadership Assembly, an intensive two-and-a-half day program, was introduced. Interested employees must apply to participate in this annual session, which features speakers and activities related to leadership. Green Efforts Lead to Platinum and Gold Moraine Valley’s dedication to being a leader in sustainability was evident this year. Every area of the College was encouraged to identify ways to be more green in our everyday practices. We also focused on educating our students and community members on the value of being good citizens in environmental sustainability. Our efforts were noticed. The Southwest Education Center was awarded platinum certification by the U.S. Green Building Council’s Leadership in Energy and Environmental Design (LEED). Platinum is the highest LEED ranking possible. The College also was recognized as a Gold Level Compact School by the Illinois Campus Sustainability Compact Program. Here is a sampling of the projects that led to these prestigious honors: With online class schedules offering up-to-the-minute data, we eliminated the printing of two class schedules, significantly reducing paper and postage costs. We recycled over three tons of nonfunctional computer, network, and multimedia equipment through a green recycling company. Campus monitors were updated with flat-screen models, which eliminated all remaining high-energy-use CRTs at the College.

xvii

Our Economic Development Council for the Southwest Suburbs hosted a Green Economy Action Roadshow, which brought together businesses, governmental agencies, nonprofits, and individuals to promote the local green economy. We partnered with the Illinois Department of Commerce and Economic Opportunity, Illinois EPA, Illinois Clean Cities, and American Lung Association of Illinois to host an electric vehicle forum. A member of the College staff designed the Governor’s Illinois Green Governments Coordinating Council’s gold, silver and bronze awards. Students in a Three-Dimensional Design class completed a sculpture entitled “Trash People” using discarded items, which they displayed in the Fine and Performing Arts Center. The Child Care Program and the Children’s Learning Center developed a children’s garden. The Fine and Performing Arts Center presented performances of Trash and Recycle Show with Steve Trash: Rockin’ Eco Hero. Exceptional Efforts Receive Acknowledgment Our Dreamkeepers Emergency Financial Assistance Program received the First Runner-Up Award in the Illinois Council of Community College Administrators’ 2011 Innovation Award Competition. An audit of the ACT Testing Centers for High Stakes Testing was conducted by the American College Testing program, and Moraine Valley’s center exceeded the national average in all four areas of valuation. The College received over 20 awards in regional and national competitions for excellence in our various marketing and advertising materials from the Educational Advertising Awards, National Council for Marketing and Public Relations, University College Designers Association, University Photographers Association of America, and Videographer Awards. FINANCIAL INFORMATION The College maintains its accounts and prepares its financial statements in accordance with accounting principles generally accepted in the United States of America (GAAP) as set forth by the Governmental and Financial Accounting Standards Boards (GASB and FASB), National Association of College and University Business Officers (NACUBO) and the Illinois Community College Board (ICCB). The financial records of the College are maintained on the accrual basis of accounting whereby all revenues are recorded when earned and all expenses are recorded when an obligation has been incurred. The notes to the financial statements expand and explain the financial statements and the accounting principles applied. Internal Controls Management of the College is responsible for establishing and maintaining an internal control structure designed to ensure that the assets of the College are protected from loss, theft, or misuse and to ensure that adequate accounting data are compiled to allow for the preparation of financial statements in conformity with generally accepted accounting principles. The internal control

xviii

structure is designed to provide reasonable, but not absolute, assurance that these objectives are met. The concept of reasonable assurance recognizes that: (1) the cost of a control should not exceed the benefits likely to be derived; and (2) the valuation of costs and benefits requires estimates and judgments by management. Tests are made by the College's independent auditors to determine the adequacy of the internal control structure, including that portion related to federal financial assistance programs, as well as to determine that the College has complied with applicable laws and regulations. The results of the tests for the fiscal year ended June 30, 2012 provided no instances of material weaknesses in the internal control structure. Budgetary Controls In addition, the College maintains budgetary controls. The objective of the budgetary controls is to ensure compliance with legal provisions embodied in the annual appropriated budget approved by the College's Board of Trustees. Activities of the funds are included in the annual appropriated budget. The President is authorized to transfer budgeted amounts between programs within any fund; however, the Board of Trustees must approve any revisions that alter the total expenditures of any fund in a manner consistent with the original budget adoption process. Activities of the following fund groups and individual funds are included in the annual budget.

Fund Group Fund General Fund Education Operations and Maintenance of Plant Special Revenue Restricted Purposes Liability, Protection, and Settlement Audit Grants and Contracts Social Security/Medicare Debt Service Fund Bond and Interest Capital Projects Operations and Maintenance (Restricted) Proprietary Fund Auxiliary Enterprises

The level of budgetary control (that is, the level at which expenditures cannot exceed the appropriated amount) is established for each individual fund. The College also maintains an encumbrance accounting system as one technique of accomplishing budgetary control. Encumbered amounts lapse at year-end. However, encumbrances generally are re-authorized as part of the following year’s budget. As demonstrated by the statements and supplementary financial information included in the financial section of this report, the College continues to meet its responsibility for sound financial management. Financial Planning Long-term financial planning is performed on an ongoing basis. The controlling document is the College’s 5-year financial plan which includes reserves by fund. Along with the adoption of the 2013 budget, certain tuition and fee increases were approved by the board of trustees. The board of trustees approved a three year tuition rate increase of $5 per credit hour each academic year

xx

MORAINE VALLEY COMMUNITY COLLEGE COMMUNITY COLLEGE DISTRICT NUMBER 524

PRINCIPAL OFFICIALS JUNE 30, 2012

BOARD OF TRUSTEES

Position Term Expires Joseph P. Murphy Chairman 2013 Patrick D. Kennedy Vice Chairman 2015 Susan Murphy Secretary 2017 John R. Coleman Trustee 2017 Lisa Szynalski Trustee 2013 Sandra S. Wagner Trustee 2013 Mark D. Weber Trustee 2015 Taylor Geraghty Student Trustee 2013

OFFICERS OF THE COLLEGE

Dr. Vernon O. Crawley President Dr. Margaret Lehner Interim Vice President, Institutional Advancement and Executive Assistant to the President Mr. Andrew Duren Executive Vice President, Administrative Services Dr. Sylvia Jenkins Vice President, Academic Affairs Dr. Normah Salleh-Barone Vice President, Student Development Mr. Robert J. Sterkowitz Chief Financial Officer/Treasurer

OFFICIALS ISSUING REPORT

Mr. Robert J. Sterkowitz Chief Financial Officer/Treasurer Ms. Theresa O’Carroll Controller Mr. William Corrello Internal Auditor

DIVISION ISSUING REPORT

Finance Division

Dir

ecto

rA

uxili

ary

Serv

ices

Dir

ecto

rC

ampu

s O

pera

tions

Dir

ecto

rH

uman

Res

ourc

es

Exe

cutiv

e D

irec

tor/

CIO

Info

rmat

ion

Tec

hnol

ogy

Chi

efP

olic

e D

epar

tmen

t

Dir

ecto

rP

urch

asin

g

Dir

ecto

rSu

stai

nabi

lity

EX

EC

UT

IVE

VIC

E P

RE

SID

EN

TA

dmin

istr

ativ

e Se

rvic

esA

ndre

w D

uren

Dea

n, A

cade

mic

Dev

elop

men

tan

d L

earn

ing

Res

ourc

es C

ente

r

Dea

n, A

cade

mic

Ini

tiativ

esan

d A

ccou

ntab

ility

Dea

nC

aree

r Pr

ogra

ms

Dea

n, E

nric

hmen

tP

rogr

ams

and

Serv

ices

Dea

nL

iber

al A

rts

Dea

n, S

cien

ce, B

usin

ess

and

Com

pute

r T

echn

olog

y

Dea

n, C

orpo

rate

, Com

mun

ityan

d C

ontin

uing

Edu

catio

n

VIC

E P

RE

SID

EN

TA

cade

mic

Aff

airs

Dr.

Syl

via

Jenk

ins

Dea

nE

nrol

lmen

t Ser

vice

s

Dea

nSt

uden

t Ser

vice

s

Dea

nC

ouns

elin

g &

Adv

isin

g

Dir

ecto

rA

thle

tics

Dir

ecto

rC

hild

rens

Lea

rnin

g C

ente

r

VIC

E P

RE

SID

EN

T S

tude

nt D

evel

opm

ent

Dr.

Nor

mah

Sal

leh-

Bar

one

INT

ER

NA

L A

UD

ITO

RW

illi

am C

orre

lloC

ontr

olle

rA

ccou

ntin

g; G

rant

s; A

sset

s

Dir

ecto

rP

ayro

ll

Supe

rvis

orC

ashi

ers

CH

IEF

FIN

AN

CIA

L O

FFIC

ER

Fina

nce

and

Acc

ount

ing

Rob

ert S

terk

owitz

Dir

ecto

r, R

esou

rce

Dev

elop

men

tan

d In

stitu

tiona

l Eff

ectiv

enes

s

Dir

ecto

rIn

stitu

tiona

l Res

earc

h an

d Pl

anni

ng

Dir

ecto

rM

arke

ting

and

Cre

ativ

e Se

rvic

es

Dir

ecto

rC

olle

ge &

Com

mun

ity

Rel

atio

ns

INT

ER

IM V

ICE

PR

ESI

DE

NT

& E

XE

C. A

SS

IST

AN

T T

O P

RE

SID

EN

TIn

stitu

tiona

l Adv

ance

men

tD

r. M

arga

ret L

ehne

r

SPE

CIA

L A

SSIS

TA

NT

TO

TH

E P

RE

SID

EN

TD

r. T

erry

Lud

wig

PR

ES

ID

EN

T

Dr. V

ern

on

Craw

ley

BO

AR

D O

F T

RU

ST

EE

S

MO

RA

INE

VA

LLEY

CO

MM

UN

ITY

CO

LLEG

E D

IVIS

ION

S O

VER

VIE

WEx

ecut

ive

Lead

ersh

ip T

eam

an

d A

dmin

istra

tive

and

Prof

essi

onal

Sta

ff 2

012

borast

Typewritten Text

borast

Typewritten Text

borast

Typewritten Text

borast

Typewritten Text

borast

Typewritten Text

borast

Typewritten Text

xxi

borast

Typewritten Text

borast

Typewritten Text

borast

Typewritten Text

borast

Typewritten Text

xxii

This

Cer

tific

ate

of E

xcel

lenc

e in

Fin

anci

al R

epor

ting

is p

rese

nted

to

M

OR

AIN

E VA

LLEY

CO

MM

UN

ITY

CO

LLEG

E

For

its

Com

preh

ensi

ve A

nnua

l Fin

anci

al R

epor

t (C

AFR

) Fo

r the

Fis

cal Y

ear E

nded

June

30,

201

1

Upo

n re

com

men

datio

n of

the

Asso

ciat

ion’

s Pa

nel o

f Rev

iew

whi

ch h

as ju

dged

that

the

Rep

ort

subs

tant

ially

con

form

s to

prin

cipl

es a

nd s

tand

ards

of A

SBO

’s C

ertif

icat

e of

Exc

elle

nce

Prog

ram

Pr

esid

ent

Ex

ecut

ive

Dire

ctor

borast

Typewritten Text

xxiii

borast

Typewritten Text

Financial SectionFiscal Year EndedJune 30, 2012

Community CollegeDistrict Number 524Palos Hills, IL

1.

Crowe Horwath LLP Independent Member Crowe Horwath International

INDEPENDENT AUDITORS’ REPORT

The Board of Trustees Moraine Valley Community College – Community College District Number 524 Palos Hills, Illinois

We have audited the accompanying basic financial statements of Moraine Valley Community College – Community College District No. 524 (the College) as of and for the year ended June 30, 2012 as listed in the table of contents. These financial statements are the responsibility of the College’s management. Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and the significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion. In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the College, as of June 30, 2012, and the respective changes in financial position and cash flows, where applicable, thereof for the year then ended in conformity with accounting principles generally accepted in the United States of America. In accordance with Government Auditing Standards, we have also issued our report dated October 12, 2012 on our consideration of the College’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be considered in assessing the results of our audit.

2.

Accounting principles generally accepted in the United States of America require that Management’s Discussion and Analysis on pages 3 through 14 be presented to supplement the financial statements. Such information, although not a part of the financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the financial statements, and other knowledge we obtained during our audit of the financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Our audit was conducted for the purpose of forming an opinion on the financial statements that collectively comprise the College’s financial statements. The introductory section, supplementary information, statistical section, and special reports section information included in schedules 1 and 2 (special reports section) are presented for purposes of additional analysis and are not a required part of the financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The special reports section is required by the Illinois Community College Board and is presented on the modified accrual basis of accounting. The special reports section and the supplementary information have been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the special reports section and the supplementary information are fairly stated in all material respects in relation to the financial statements as a whole. The introductory and statistical sections have not been subjected to the auditing procedures applied in the audit of the financial statements and, accordingly, we express no opinion on them.

Crowe Horwath LLP Oak Brook, Illinois October 12, 2012

3.

MANAGEMENT’S DISCUSSION AND ANALYSIS

INTRODUCTION AND BACKGROUND This section of Moraine Valley Community College District 524’s (the College) Comprehensive Annual Financial Report presents management’s discussion and analysis (MD&A) of the College’s financial activity during the fiscal year ended June 30, 2012. Since this MD&A is designed to focus on current activities, resulting changes and currently known facts, please read it in conjunction with the Transmittal Letter (pages i - xix), the College’s basic financial statements (pages 15 - 18) and the notes to the financial statements (pages 19 - 41). Responsibility for the completeness and fairness of this information rests with the College.

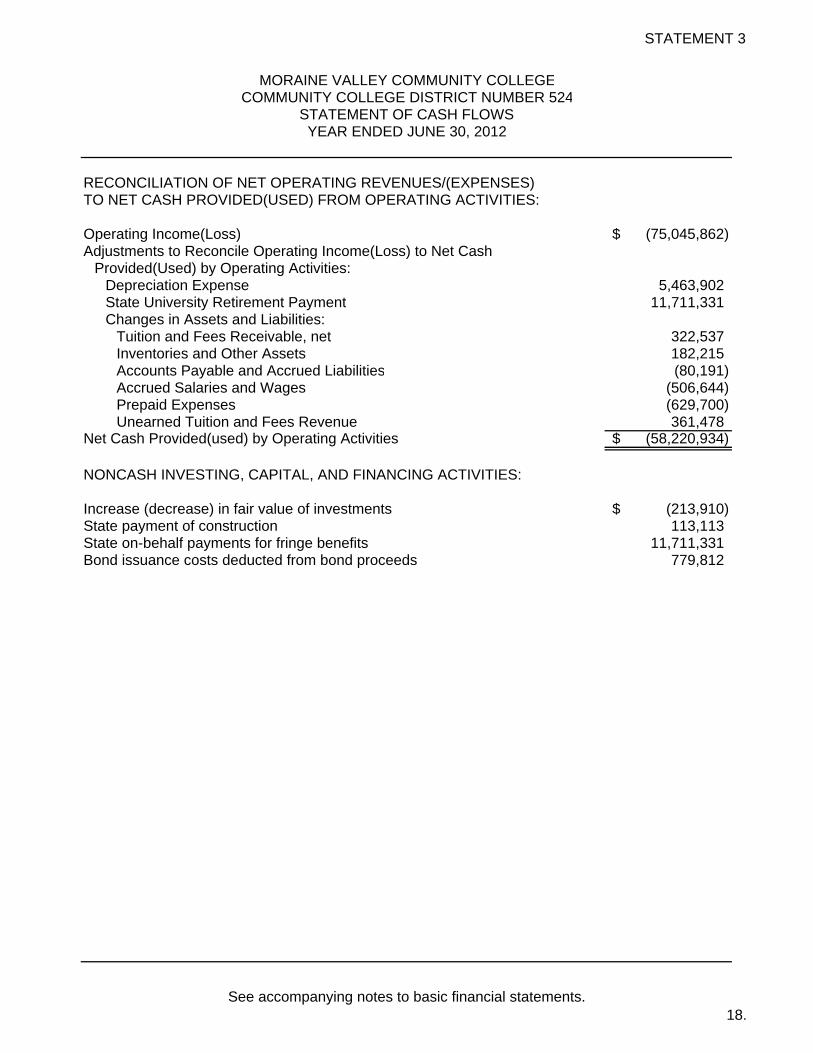

USING THIS ANNUAL REPORT The financial statements focus on the College as a whole and are designed to emulate corporate presentation models whereby all College activities are consolidated into one total. The financial statements consist of four primary parts: (1) the statement of net assets, (2) statement of revenue, expenses, and changes in net assets, (3) statement of cash flows and (4) notes to the financial statements. The financial statements are prepared on the accrual basis of accounting and economic resources measurement focus. Under the accrual basis of accounting, expenses are recorded when incurred and revenues are recognized when earned in accordance with generally accepted accounting principles. The Statement of Net Assets is presented in the format where assets equal liabilities plus net assets. Assets and liabilities are presented in order of liquidity and are classified as current (convertible into cash within one year) and noncurrent. This statement combines and consolidates current financial resources (short-term spendable resources) with long-term capital assets. The focus on this statement is to show the overall liquidity and health of the College as of the end of the fiscal year. The Statement of Revenues, Expenses, and Changes in Net Assets focuses on both the gross and net costs of College activities, which are supported substantially by property taxes, state and federal grants, student tuition and fees and auxiliary enterprises revenues. This approach is intended to summarize and simplify the user’s analysis of the financial results of the various College services to students and the public. The statement of Cash Flows discloses net cash provided by or used for operating, non-capital financing and related financing activities. This statement shows the College’s cash flows are sufficient to pay current liabilities. The notes to the financial statements are an integral part of the basic statements and describe the College’s significant accounting policies. The reader is encouraged to review notes in conjunction with the management discussion and analysis of the financial statements.

4.

FINANCIAL HIGHLIGHTS

STATEMENT OF NET ASSETS The major components of Moraine Valley’s assets, liabilities, and net assets as of June 30, 2012 and 2011 are as follows (in millions of dollars):

Fiscal Year 2012 Compared to 2011 Assets Total current and other assets increased by approximately $45.9 million as compared to prior year. The primary reason for this increase is attributable to an increase of $49.1 million in restricted investments from bond proceeds held in escrow to advance refund a portion of the College’s outstanding General Obligation Bonds, Series 2007B and an increase of $2.0 million in accrued revenue due the College from the State offset by a decrease of $5.7 million in cash and cash equivalents. Net Assets See net assets section on page 6 for the discussion of the $1.5 million increase in net assets.

Increase Percent2012 2011 (Decrease) Change

AssetsCurrent and other assets $ 175.9 $ 130.0 $ 45.9 35.3%Capital assets, net of depreciation 155.9 153.0 2.9 1.9%Total assets 331.8 283.0 48.8 17.2%

LiabilitiesCurrent liabilities 36.6 35.5 1.1 3.1%Non-current liabilities 127.0 80.8 46.2 57.2%Total liabilities 163.6 116.3 47.3 40.7%

Net AssetsInvested in capital assets, net of debt 76.6 71.5 5.1 7.1%Restricted expendable 25.1 27.7 (2.6) (9.4%)Unrestricted 66.5 67.5 (1.0) (1.5%)Total Net Assets $ 168.2 $ 166.7 $ 1.5 0.9%

5.

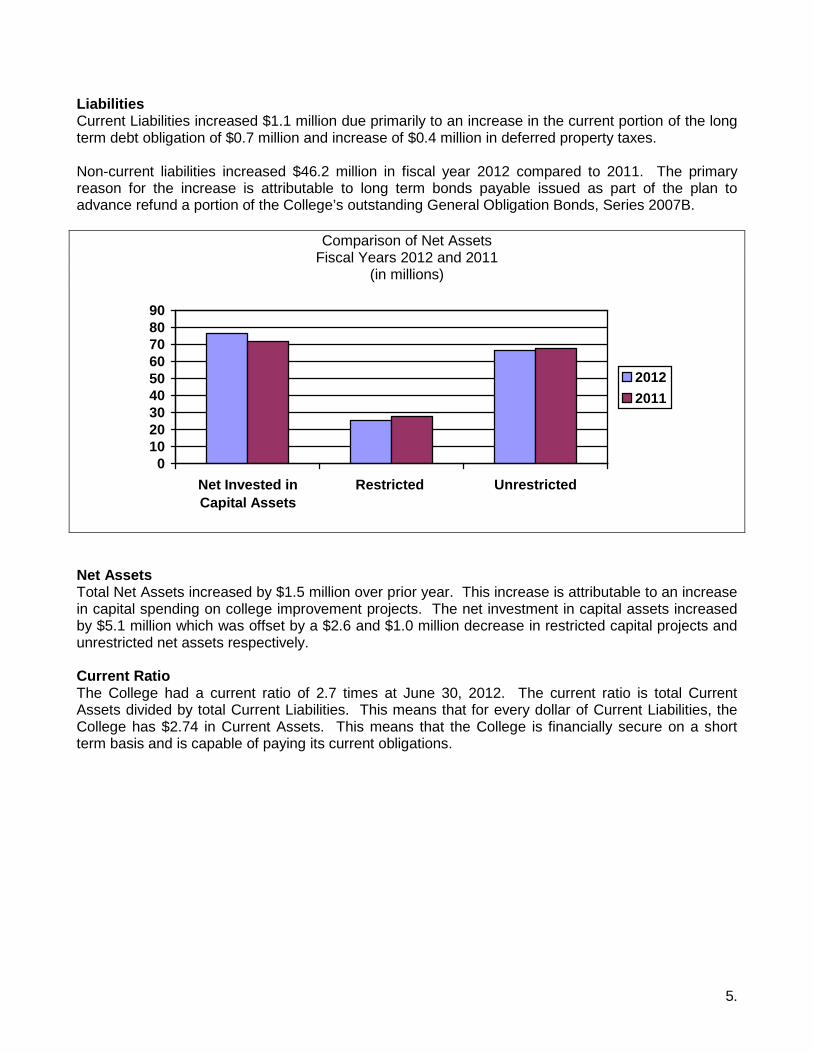

Liabilities Current Liabilities increased $1.1 million due primarily to an increase in the current portion of the long term debt obligation of $0.7 million and increase of $0.4 million in deferred property taxes. Non-current liabilities increased $46.2 million in fiscal year 2012 compared to 2011. The primary reason for the increase is attributable to long term bonds payable issued as part of the plan to advance refund a portion of the College’s outstanding General Obligation Bonds, Series 2007B.

Comparison of Net Assets Fiscal Years 2012 and 2011

(in millions)

0102030405060708090

Net Invested inCapital Assets

Restricted Unrestricted

20122011

Net Assets Total Net Assets increased by $1.5 million over prior year. This increase is attributable to an increase in capital spending on college improvement projects. The net investment in capital assets increased by $5.1 million which was offset by a $2.6 and $1.0 million decrease in restricted capital projects and unrestricted net assets respectively. Current Ratio The College had a current ratio of 2.7 times at June 30, 2012. The current ratio is total Current Assets divided by total Current Liabilities. This means that for every dollar of Current Liabilities, the College has $2.74 in Current Assets. This means that the College is financially secure on a short term basis and is capable of paying its current obligations.

6.

ANALYSIS OF NET ASSETS

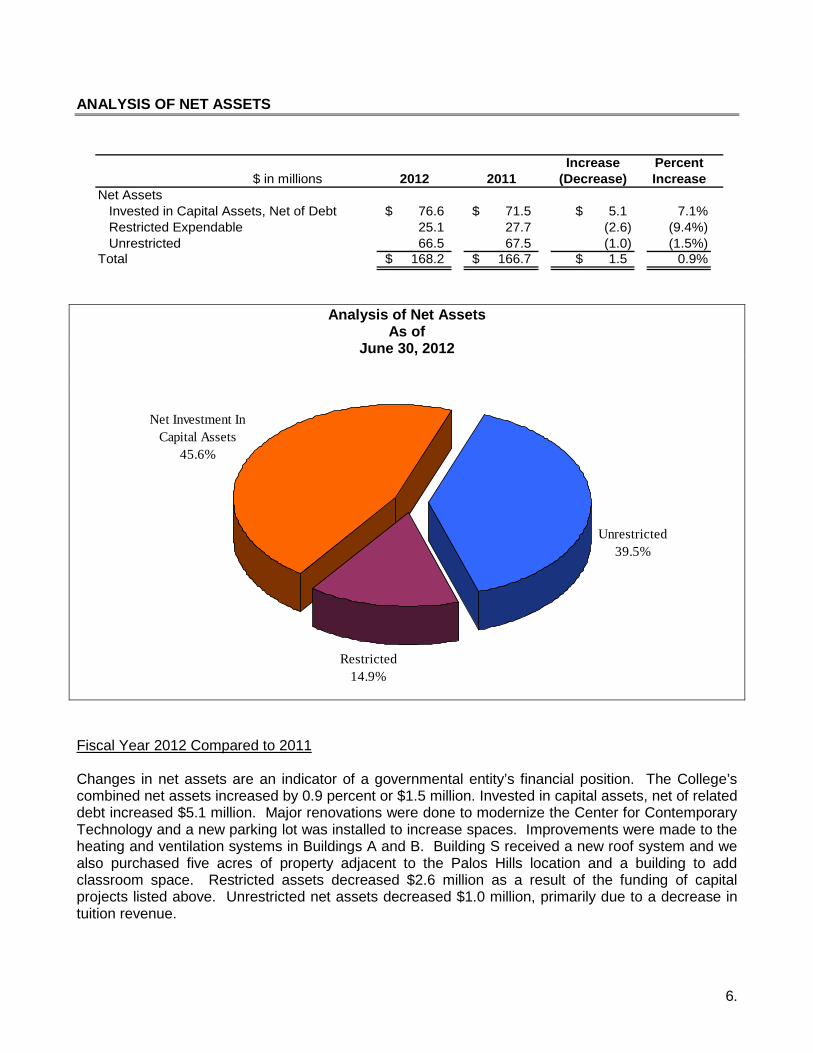

Increase Percent $ in millions 2012 2011 (Decrease) IncreaseNet Assets

Invested in Capital Assets, Net of Debt $ 76.6 $ 71.5 $ 5.1 7.1%Restricted Expendable 25.1 27.7 (2.6) (9.4%)Unrestricted 66.5 67.5 (1.0) (1.5%)

Total $ 168.2 $ 166.7 $ 1.5 0.9%

Analysis of Net Assets

As of June 30, 2012

Unrestricted39.5%

Restricted14.9%

Net Investment In Capital Assets

45.6%

Fiscal Year 2012 Compared to 2011 Changes in net assets are an indicator of a governmental entity’s financial position. The College’s combined net assets increased by 0.9 percent or $1.5 million. Invested in capital assets, net of related debt increased $5.1 million. Major renovations were done to modernize the Center for Contemporary Technology and a new parking lot was installed to increase spaces. Improvements were made to the heating and ventilation systems in Buildings A and B. Building S received a new roof system and we also purchased five acres of property adjacent to the Palos Hills location and a building to add classroom space. Restricted assets decreased $2.6 million as a result of the funding of capital projects listed above. Unrestricted net assets decreased $1.0 million, primarily due to a decrease in tuition revenue.

7.

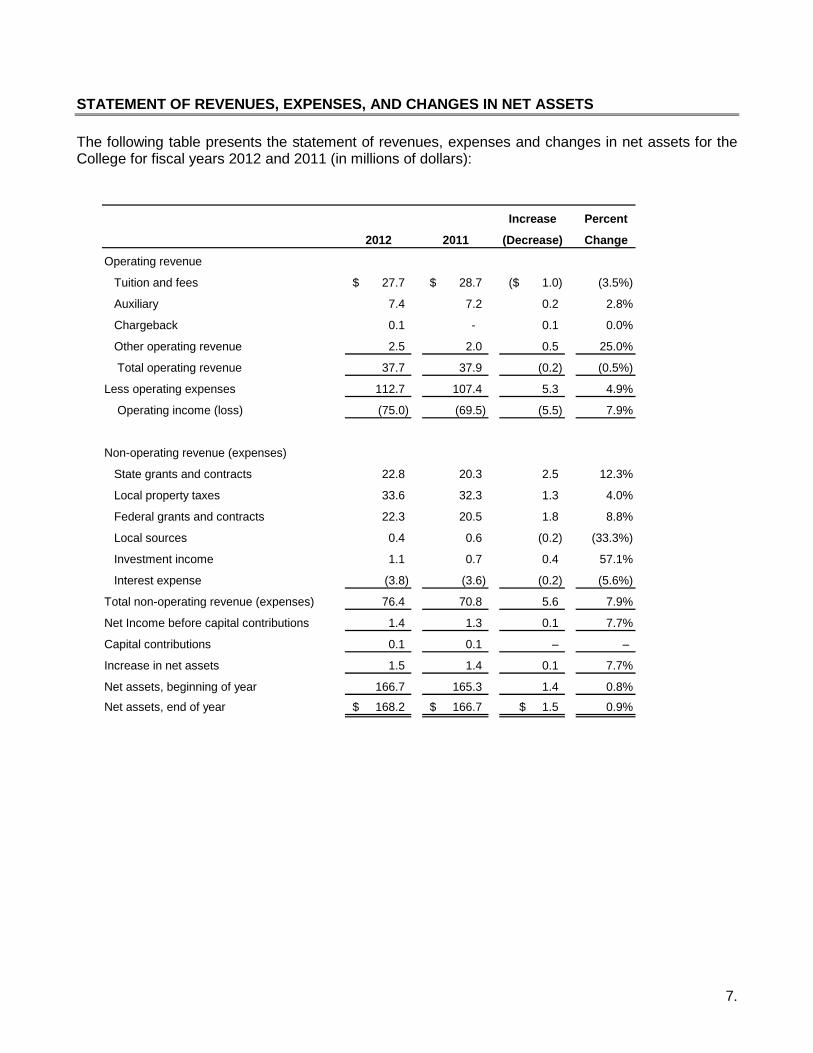

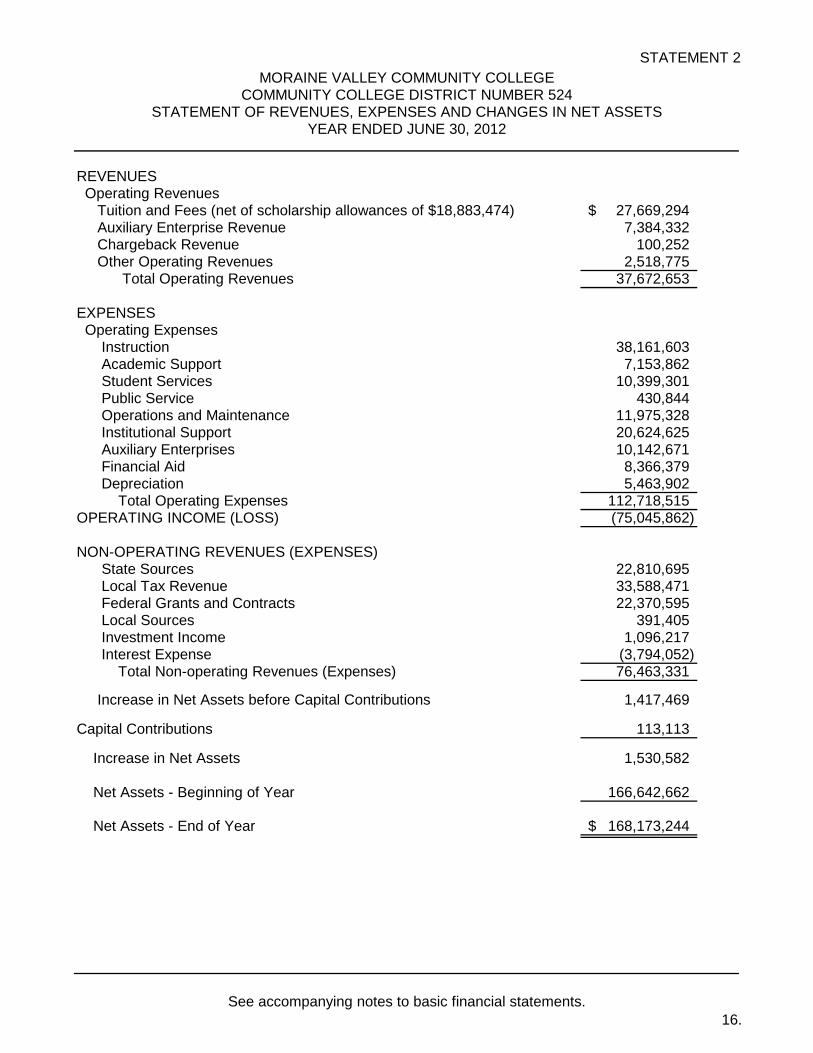

STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN NET ASSETS The following table presents the statement of revenues, expenses and changes in net assets for the College for fiscal years 2012 and 2011 (in millions of dollars):

Increase Percent

2012 2011 (Decrease) Change

Operating revenue

Tuition and fees $ 27.7 $ 28.7 ($ 1.0) (3.5%)

Auxiliary 7.4 7.2 0.2 2.8%

Chargeback 0.1 - 0.1 0.0%

Other operating revenue 2.5 2.0 0.5 25.0%

Total operating revenue 37.7 37.9 (0.2) (0.5%)

Less operating expenses 112.7 107.4 5.3 4.9%

Operating income (loss) (75.0) (69.5) (5.5) 7.9%

Non-operating revenue (expenses)

State grants and contracts 22.8 20.3 2.5 12.3%

Local property taxes 33.6 32.3 1.3 4.0%

Federal grants and contracts 22.3 20.5 1.8 8.8%

Local sources 0.4 0.6 (0.2) (33.3%)

Investment income 1.1 0.7 0.4 57.1%

Interest expense (3.8) (3.6) (0.2) (5.6%)

Total non-operating revenue (expenses) 76.4 70.8 5.6 7.9%

Net Income before capital contributions 1.4 1.3 0.1 7.7%

Capital contributions 0.1 0.1 – –

Increase in net assets 1.5 1.4 0.1 7.7%

Net assets, beginning of year 166.7 165.3 1.4 0.8%

Net assets, end of year $ 168.2 $ 166.7 $ 1.5 0.9%

8.

REVENUES: Fiscal Year 2012 Compared to 2011 Operating and non-operating revenue total $117.9 million for fiscal year 2012, an increase of $5.6 million over fiscal year 2011. The largest component of revenue, $33.6 million, is from local property taxes which comprises 28.5% of total revenues. Revenues from student tuition and fees were $27.7 million in fiscal year 2012 and represent the second largest component of total revenues at 23.5%. State and Federal revenues were $22.8 million and $22.3 million respectively each accounting for approximately 19% of total fiscal year 2012 revenues. Operating revenue from tuition and fees decreased $1.0 million from the previous year. This decrease is attributable to the offsetting increase in financial aid. Generally Accepted Accounting Principles (GAAP) require colleges to report tuition and fees funded by state and federal financial awards as nonoperating revenue and not as tuition. The amount of state and federal scholarships applied to tuition was $18.9 million in fiscal year 2012 compared to $15.7 million in fiscal year 2011, an increase of $3.2 million which is classified in non-operating revenues. The table below summarizes total gross tuition and fee revenues before reclassifying the federal and state financial aid awards to non-operating revenue. As shown in the table below, student tuition and fees before adjustment were $46.6 million, or $2.2 million higher than fiscal year 2011.

Change % ChangeFY2012 FY2011 2012-11 2012-11

Student tuition and fees 46.6$ 44.4$ 2.2$ 5.0%Federal and State Awards (18.9) (15.7) 3.2 20.4%Student tuition and fees, net 27.7$ 28.7$ (1.0)$ (3.5%)

Non-operating revenue and expenses increased $5.6 million overall. State revenue increased $2.5 million due to an increase in the total pension plan contributions made by the State of Illinois on behalf of employees participating in the State University Retirement System (SURS) plan. According to the Governmental Accounting Standards Board (GASB), the employer of these members must disclose the on-behalf payments as revenues and expenditures in the financial statements. Local property tax revenue increased by $1.3 million due to an increase in the property tax levy. Revenues from federal grants increased $1.8 million primarily due to increases in student federal financial aid. Investment income increased $0.4 million due to an increase in investment returns related to bond proceeds used to advance refund a portion of the College’s series 2007B bonds. Interest on capital related debt decreased $0.2 million.

9.

Operating and Non-Operating Revenues June 30, 2012

Tuition & Fees23.6%

Investment0.9%

Local Tax Revenue28.6%

Federal Grants /Contracts

19.0%

State Grants/Contracts

19.4%

Other2.1%

Auxiliary6.3%

Chargeback Revenue

0.1%

Auxiliary Enterprise revenue increased $0.2 million over the prior year primarily due to an increase in sales and service fee revenue. The Continuing Education program had an increase in non-credit enrollment for fiscal year 2012 compared to 2011 which resulted in a $0.4 million increase in revenue. The bookstore revenue decreased by $0.2 million in revenue due to a decrease in the volume of books sold.

10.