Comparitive Analysis of Market Players With Idbi

133

IDBI LTD: COMPARITIVE ANALYSIS OF MARKET PLAYERS WITH IDBI Submitted in partial fulfillment of the requirements for the award of the degree of Guided by: Submitted by:

-

Upload

vikashprabhu -

Category

Documents

-

view

112 -

download

5

Transcript of Comparitive Analysis of Market Players With Idbi

IDBI LTD: COMPARITIVE ANALYSIS OFMARKET PLAYERS WITH IDBI

Submitted in partial fulfillment of the requirementsfor the award of the degree of

Guided by: Submitted by:

ACKNOWLEDGEMENT

"Accomplishment of any task necessarily depends upon the willingness and

enthusiastic contribution of time and energy of many people."

I take this humble opportunity to express my special thanks and portray my deep

sense of gratitude to Mr. Raja Kumar whose invaluable guidance and supervision in

the project infused in me great inspiration and confidence in making this survey in

right earnest. His masterly guidance from time to time made the study interesting

and meaningful.

He was always there for our help and doing away all the difficulties and confusions

that arose during the project period. He also helped me to understand what was

actually required from the project and what was needed to be done.

I would like to thank our respondents for their kind response and their precious time

they provided me to carry our survey based on the data provided by them. I have

given some suggestions that would be surely beneficial for the company.

At last I would like to pay my word of thanks to my family members, all my

teachers and my friends who have indebted me by supporting and encouraging me to

go on with the project easily.

ABSTRACT

IDBI Ltd. Completed yet another year of strong performance with an operating

profit (before provisions and contingencies) of Rs.2921.83 crores and net turnover

of Rs.307.26 crores. The Earnings per share for the year stand at Rs.4.26. The results

of IDBI and its subsidiaries stand with operating profit of Rs.373.97 crores, net

turnover of Rs.318.57 crores and earning per share of Rs.4.42.

Products and Services of IDBI Ltd. at a glance

The erstwhile IDBI has played a pioneering role in fulfilling its mission of

promoting industrial growth through financing of medium and long-term projects, in

consonance with national plans and priorities. Over the years, IDBI has enlarged its

basket of products and services to industrial concerns, covering almost the entire

spectrum of industrial activities, including manufacturing and services. IDBI and its

successor entity IDBI Ltd. provides financial assistance, both in rupee and foreign

currencies, for green-field projects as also for expansion, modernization and

diversification purposes.

Further, in order to cater to the diverse and customized needs of its corporate clients,

IDBI Ltd. has structured suitable products like equipment finance, asset credit,

corporate loan, working capital loan and bills discounting to variously finance

acquisition of equipment and capital assets, besides meeting capital expenditure

and/or incremental long-term working capital requirements. It also offers structured

products like lines of credit to meet the funding requirements for execution of

turnkey contracts. Besides, IDBI Ltd. provides a wide array of fee- based services.

IDBI Ltd. also provides indirect financial assistance through refinancing of loans

extended by State-level financial institutions and banks and by way of rediscounting

of bills of exchange arising out of sale of indigenous machinery on deferred

payment terms.

INTRODUCTION

INDUSTRIAL DEVELOPMENT BANK OF INDIAOverview

IDBI is one of the All India Development Bank in India. In addition, it is the apex

banking institution in the field of long term industrial finance and functions as the

principal financial institution for coordinating the functions and activities of all India

term lending institutions and to some extent the public sector banks.

The merger of IDBI Bank with the IDBI Ltd. in the year 2004 had made the IDBI

Ltd. as the public sector bank (PSU) with the Government stake holding of 51.4%

and the new company has been incorporated on Sept.27, 2004 and the Registrar of

the companies, Mumbai issued the certificate for commencement of business to

IDBI Ltd. on Sept.28, 2004.

Consequently, the IDBI formally entered the portals of banking business as IDBIL

(Industrial Development Bank Of India Limited) from Oct.1, 2004 over and above

the business currently being transacted.

MILESTONES

July 1964: Set up under an Act of Parliament as a wholly owned

subsidiary of Reserve Bank of India.

February 1976: Ownership transferred to Government of India.

Designated Principal Financial Institution for coordinating the working of

institutions at national and State levels engaged in financing, promoting and

developing industry.

March 1982: International Finance Division of IDBI transferred

to Export-Import Bank of India, established as a wholly owned corporation of

Government of India, under an Act of Parliament.

April 1990: Set up Small Industries Development Bank of India (SIDBI)

under SIDBI Act as a wholly owned subsidiary to cater to specific needs of

small-scale sector. In terms of an amendment to SIDBI Act in September 2000,

IDBI divested 51% of its shareholding in SIDBI in favour of banks and other

institutions in the first phase. IDBI has subsequently divested 79.13% of its

stake in its erstwhile subsidiary to date.

January 1992: Accessed domestic retail debt market for the first time with

innovative Deep Discount Bonds; registered path-breaking success.

December 1993: Set up IDBI Capital Market Services Ltd. as a wholly owned

subsidiary to offer a broad range of financial services, including Bond Trading,

Equity Broking, Client Asset Management and Depository Services. IDBI

Capital is currently a leading Primary Dealer in the country.

September 1994: Set up IDBI Bank Ltd. in association with SIDBI as a

private sector commercial bank subsidiary, a sequel to RBI's policy of opening

up domestic banking sector to private participation as part of overall financial

sector reforms.

October 1994: IDBI Act amended to permit public ownership up to 49%.

July 1995: Made Initial Public Offer of Equity and raised over Rs.2000

crore, thereby reducing Government stake to 72.14%.

March 2000: Entered into a JV agreement with Principal Financial Group,

USA for participation in equity and management of IDBI Investment

Management Company Ltd., erstwhile a 100% subsidiary. IDBI divested its

entire shareholding in its asset management venture in March 2003 as part of

overall corporate strategy.

March 2000: Set up IDBI Intech Ltd. as a wholly owned subsidiary to

undertake IT-related activities.

June 2000: A part of Government shareholding converted to preference

capital, since redeemed in March 2001; Government stake currently 58.47%.

August 2000: Became the first All-India Financial Institution to obtain ISO

9002:1994 Certification for its treasury operations. Also became the first

organization in Indian financial sector to obtain ISO 9001:2000 Certification for

its forex services.

March 2001: Set up IDBI Trusteeship Services Ltd. to provide technology-

driven information and professional services to subscribers and issuers of

debentures.

February 2002: Associated with select banks/institutions in setting up Asset

Reconstruction Company (India) Limited (ARCIL), which will be involved with

the strategic management of non-performing and stressed assets of Financial

Institutions and Banks.

September 2003: IDBI acquired the entire shareholding of Tata Finance

Limited in Tata Home finance Ltd, signaling IDBI's foray into the retail finance

sector. The housing finance subsidiary has since been renamed 'IDBI Home

finance Limited'.

December 2003: On December 16, 2003, the Parliament approved The

Industrial Development Bank (Transfer of Undertaking and Repeal Bill) 2002 to

repeal IDBI Act 1964. The President's assent for the same was obtained on

December 30, 2003. The Repeal Act is aimed at bringing IDBI under the

Companies Act for investing it with the requisite operational flexibility to

undertake commercial banking business under the Banking Regulation Act 1949

in addition to the business carried on and transacted by it under the IDBI Act,

1964.

July 2004: The Industrial Development Bank (Transfer of Undertaking and

Repeal) Act 2003 came into force from July 2, 2004.

July 2004: The Boards of IDBI and IDBI Bank Ltd. take in-principle decision

regarding merger of IDBI Bank Ltd. with proposed Industrial Development

Bank of India Ltd. in their respective meetings on July 29, 2004.

September 2004: The Trust Deed for Stressed Assets Stabilization Fund

(SASF) executed by its Trustees on September 24, 2004 and the first meeting of

the Trustees was held on September 27, 2004.

September 2004: The new entity "Industrial Development Bank of India" was

incorporated on September 27, 2004 and the Registrar of Companies issued

Certificate of commencement of business on September 28, 2004.

September 2004: Notification issued by Ministry of Finance specifying

SASF as a financial institution under Section 2(h)(ii) of Recovery of Debts due

to Banks & Financial Institutions Act, 1993.

September 2004: Notification issued by Ministry of Finance on September

29, 2004 for issue of non-interest bearing GOI IDBI Special Security, 2024,

aggregating Rs.9000 crore, of 20-year tenure.

September 2004: Notification for appointed day as October 1, 2004, issued

by Ministry of Finance on September 29, 2004.

September 2004: RBI issues notification for inclusion of Industrial

Development Bank of India Ltd. in Schedule II of RBI Act, 1934 on September

30, 2004.

October 2004: Appointed day - October 01, 2004 - Transfer of undertaking of

IDBI to IDBI Ltd. IDBI Ltd. commences operations as a banking company.

IDBI Act, 1964 stands repealed.

January 2005: The Board of Directors of IDBI Ltd., at its meeting held on

January 20, 2005, approved the Scheme of Amalgamation, envisaging merging

of IDBI Bank Ltd. with IDBI Ltd. Pursuant to the scheme approved by the

Boards of both the banks, IDBI Ltd. will issue 100 equity shares for 142 equity

shares held by shareholders in IDBI Bank Ltd. EGM has been convened on

February 23, 2005 for seeking shareholder approval for the scheme.

OBJECTIVES

OBJECTIVES OF THE STUDY

1. To understand the corporate history and strategy of IDBI Ltd.

2. To understand the overall business strategies adopted by IDBI Ltd. for the

loan against securities business.

3. To make a comparative analysis of the product and business strategies of

IDBI Ltd. with respect to various private and public sector banks.

4. To formulate the unique and desired corrective measures and innovation to

increase market share and enhance the brand value of IDBI Ltd.

SCOPE OF THE STUDY

1. The project should be able to determine the right strategies to be

implemented in the process of designing the “marketing and product

development strategy for loan against securities division at IDBI Bank.

2. The research will enable the organization to understand and compare policies

and practices employed by various competitors in terms of product

Development considering customer’s choice and preferences across common

parameters like advertising and marketing, new schemes, rate of interest,

loan amount range, tenure of the loan and the whole package offered by the

Company etc.

3. Using the information gathered and with proper analysis carried out on it, we

can determine the most effective and efficient policies followed across the

industry and implement them at IDBI Bank to ensure better product

development, best product positioning & marketing strategy in their personal

loan division service.

4. Also by conducting interviews with former and present sales force (Territory

Sales Leaders) we can estimate the problem areas, the reasons for the less

development area, the reason of dissatisfaction with company’s present

strategy can be determined and effort towards correcting the problems faced

by them can be made so that such issues do not arise with the current and

future sales executives.

LITERATURE

REVIEW

By Surojit Chatterjee

New Delhi - Industrial and Development Bank of India (IDBI) which has won the

race for acquisition of ailing United Western Bank (UWB), held a board meeting on

September 21 to discuss the Reserve Bank of India's (RBI) draft scheme for

amalgamation, even as global rating agency Standard & Poor's has warned that

UWB's huge bad loans may affect the acquirer's financial profile negatively.

On September 12, India's central bank, the Reserve Bank of India (RBI)

proposed a draft scheme to IDBI for amalgamating the under-moratorium bank

with itself.

As per the draft scheme, IDBI will have to make an upfront payment in cash of Rs.

28 per share in respect of every fully paid-up share in UWB to investors as on

prescribed date, which will be decided by the government later. Market sources

said IDBI will have to pay Rs. 150.50 crores to the UWB shareholders and assume

the assets and liabilities of UWB according to the conditions in the proposal. This

is the first instance in India where an acquirer bank, IDBI, is required to

compensate the shareholders of a bank under moratorium. Payment made to UWB

investors will be considered as provision for bad debt, the scheme elaborated. IDBI

will discharge all payments to creditors and depositors of UWB while the

employees will continue in service and will be transferred to IDBI, the scheme said.

Both the banks have been given two weeks' time up to September 27 to consider

the draft scheme, after which RBI will take a view on the future set-up of UWB.

UWB too is likely to decide the date of its board meeting soon. UWB's huge pile of

bad debts may affect IDBI's financial profile negatively, Standard and Poor's (S&P)

has warned.However, the rating agency added that there is no immediate impact on

IDBI ratings after Reserve Bank cleared a merger proposal between UWB and

IDBI. The rating agency has a "BB+/Positive" rating on IDBI, a public sector bank.

S&P will continue to monitor the impact on IDBI's financial profile. UWB's branch

network in the affluent western Maharashtra region and its wide depositor base is

expected to boost IDBI's distribution network and grow its retail

portfolio.INDIA'S ICICI, SBI, IDBI TO PICK 24.5 PCT STAKE

EACH IN ARC.AsiaPulse News, June, 2002NEW DELHI, June 25 Asia Pulse -

ICICI Bank (BSE:ICBK), IDBI (BSE:IDBI) and State Bank of India (BSE:SBI)

will pick up 24.5 per cent stake each in the Asset Reconstruction Company of India

Ltd (ARCIL), which is slated to start operations with an

initial.RESEARCHME

THODOLOGYRESEARC

H METHODOLOGY Methodologically, marketing research uses four

types of research designs, namely:Qualitative marketing research -

generally used for exploratory purposes - small number of respondents - not

generalizable to the whole population - statistical significance and confidence not

calculated - examples include focus groups, depth interviews, and projective

techniques.Quantitative marketing research - generally used to draw

conclusions - tests a specific hypothesis - uses random sampling techniques so as to

infer from the sample to the population - involves a large number of respondents -

examples include surveys and questionnaires.Observational techniques - the

researcher observes social phenomena in their natural setting - observations can

occur cross-sectionally (observations made at one time) or longitudinally

(observations occur over several time-periods) - examples include product-use

analysis and computer cookie traces.Experimental techniques - the researcher

creates a quasi-artificial environment to try to control spurious factors, and then

manipulates at least one of the variables - examples include purchase laboratories

and test markets.The project report titled IDBI Ltd. has been prepared mainly on

the basis of secondary data.Secondary data is the data which is made available and

considered as the starting point for the report. This data can be obtained both

internally as well as externally. The following sources were the basis of this project

report:-Internal Sources The main internal source has been the library of our

institute i.e. MAIMS.

IDBI product manual

Annual report of IDBI

Journals of various banks

External Sources

Websites

Magazines

Newspapers

COMPANY’S PROFILE

Introduction to IDBI - History

The genesis of “Industrial Development Bank Of India Ltd” can be traced to the

establishment of the IDBI, its predecessor entity, in 1964, by an Act of Parliament to

provide credit and other facilities for the development of industry.

IDBI’s charter was later broad-based to also encompass the responsibilities of

principal financial institution for coordinating the working of National and State

level institutions engaged in financing, promoting and developing industry.

IDBI was established in 1964 as a wholly owned subsidiary of the Reserve Bank of

India (RBI). In February 1976 it was de-linked from the Reserve Bank and its entire

capital was transferred to the Central Government. In March 1994 the IDBI Act was

amended to empower the government provided the government holding does not fall

below 51%.

Consequently, the Bank made its first public issue of equity in July 1995, which was

the largest equity offering in the Indian Stock Market till then.

The majority of its shares are still held with Central Government though the

percentage holding of Government has declined to 58.47% as at the end of March

2002.

The authorized capital of Erstwhile IDBI stood at Rs.1500 crores in conformity with

the provision of Banking Regulation Act. The paid up capital of the company is at

Rs.653 crores.

During the four decades of its existence, IDBI has been instrumental not only in

establishing a well developed, diversified and efficient industrial and institutional

structure but also adding a qualitative dimension to the process of industrial

development in the country.

Cumulative assistance sanctioned and disbursed by IDBI, since inception up to the

end - September 2004 aggregated around Rs.22, 30,000 Crores and Rs. 1,78,000

Crores respectively. IDBI’s asset base stood in the vicinity of Rs. 63,850 Crores at

the end of September 2004.

Institution Building

IDBI has been actively involved in the development of a robust institutional

framework for the domestic financial sector. It played a significant role in the setting

up of several Financial Institutions viz. Export-Import Bank of India (EXIM Bank);

Small Industries Development Bank of India (SIDBI); North Eastern Development

Finance Corporation Ltd. (NEDFi); and the Asset Reconstruction Company (India)

Ltd. (ARCIL).

IDBI also participated in the setting up of various capital market-related institutions

viz. Securities & Exchange Board of India (SEBI); National Stock Exchange of

India Ltd. (NSE); Stock Holding Corporation of India Ltd. (SHCIL); Credit

Analysis & Research Ltd. (CARE); National Securities Depository Ltd. (NSDL);

IDBI Trusteeship Services Ltd.(ITSL) and Clearing Corporation Of India Limited

(CCIL).

IDBI played a key role in the development of the Jawaharlal Nehru Institute of

Development Banking (JNIDB) and the Entrepreneurship Development Institute of

India (EDII) as training institutes.

IDBI has also been associated with the Entrepreneurship Development in the

industrially less developed states of India. Thus it has performed the role of the

institution builder.

Subsidiaries of IDBI

After the de-linking of Small Industries Development Bank of India from the IDBI

with effect from March 27,2000. IDBI has the following three subsidiaries, viz IDBI

Bank Ltd. (commercial bank) (IDBI Ltd.'s shareholding: 55.38%); IDBI Capital

Market Services Ltd. (financial services/ primary dealership company) (IDBI Ltd's

shareholding: 100%) and IDBI Home finance Ltd. (housing finance company) (IDBI

Ltd's shareholding:100%).

SHAREHOLDING PATTERN AS ON SEPTEMBER 30, 2004

(%)Government 58.47Employees 0.09

Public 13.90HUF 0.16

Bodies Corporate 3.62Banks 5.06FIIs 8.29

SFCs 0.03Fis 0.67

MFs 2.52OCBs 0.07Trusts 0.06

Insurance Companies 5.76

NRIs 0.72Others 0.58Total 100.00

IDBI Bank Ltd.

IDBI Bank Ltd. is a commercial bank, set up by IDBI and SIDBI in September

1994.

It provides the complete range of banking facilities. During 1998-99, IDBI Bank

Ltd. issued 4 crores-equity shares of Rs.10 each at a premium of Rs.8 per share to

the public. Thus IDBI’s share in the equity capital of the bank has fallen from 80%

to 57%. SIDBI also holds shares in the IDBI Bank Ltd.

The IDBI Bank Ltd. has a robust business model which focuses on careful choice of

market segments having revenue potential, expansion of products suite for

supporting future growth and profitability, leveraging technology infrastructure for

enhanced customer services and strong risk management committed to high quality

assets and earnings.

IDBI Capital Market Services Ltd.

IDBI Capital Market Services Ltd (ICMS) was established in December 1993 as a

wholly owned subsidiary of IDBI Ltd. to offer a broad range of Capital Market

services. The Company's business activities include Bond Trading, Retail

Distribution, Broking, Client Asset Management and Depository Services.

ICMS is one of the Primary Dealers (PDs) accredited by the Reserve Bank of India

to act as a market maker in Government Securities. The Company has achieved the

highest outright turnover in Government Securities among all PDs for the past three

consecutive years. The Company is at the forefront in building the retail debt market

in India and is one of the few active institutional equity brokers having membership

of both BSE and NSE.

ICMS also acts as an arranger in the private placement market for institutional and

corporate debt and also markets products like equity, debt, mutual fund instruments,

RBI Relief Bonds, etc. through its nation-wide network of sub-agents.

IDBI Home Finance Ltd.

In order to make a foray into retail financing, the erstwhile IDBI, in September

2003, acquired the entire shareholding of Tata Finance Ltd. in Tata Home Finance

Ltd., at par for a total consideration of Rs.49.98 crore. The company has since been

renamed as "IDBI Home Finance Limited”

After becoming a subsidiary of IDBI Ltd., IHFL obtained an A1+ rating (highest

short-term rating) from ICRA, which facilitated the raising of funds at lower rates.

IHFL has implemented a Total Home Loan Solutions (THLS) system with

connectivity through leased lines with all its 16 branches. The system is scalable and

forms the foundation for future business growth.

Merger of IDBI Bank Ltd. with IDBI Ltd.

During the four decades of its existence, IDBI has been instrumental not only in

establishing a well developed, diversified and efficient industrial and institutional

structure but also adding a qualitative dimension to the process of industrial

development in the country. Cumulative assistance sanctioned and disbursed by

IDBI since inception up to end-September 2004 aggregated around Rs.2, 23,000

crores and Rs 1,78,000 crores respectively. IDBI's asset base stood in the vicinity of

Rs.63850 crores at end- September 2004.

As a considered response to changes in its operating environment following

initiation of reforms since the early nineties and the resultant concerns of IDBI's

sustained viability therein in its current avatar, IDBI, in consultation with the

Government of India, decided to transform into a commercial bank without

eschewing its secular development finance obligations. The migration to the new

business model of commercial banking, with its gateway to low-cost current/savings

bank deposits, it was felt, would help overcome most of the limitations of the current

business model of development finance while simultaneously enabling it to diversify

its client/asset base.

Towards this end, the IDBI (Transfer of Undertaking and Repeal) Act 2003 was

passed by Parliament on December 16, 2003 and received the President's assent on

December 30, 2003. The provisions of the Act came into force from July 2, 2004 in

terms of a Government Notification to this effect. The Notification enabled IDBI to

obtain the requisite statutory and regulatory approvals, including those from RBI,

for conversion into a banking company. The new company viz. "Industrial

Development Bank of India Limited" (IDBIL) was incorporated on September 27,

2004 and the Registrar of Companies, Mumbai, issued the certificate for

commencement of business to IDBI Ltd. on September 28, 2004. Subsequently, the

Central Government notified October 1, 2004 as the 'Appointed Date' and RBI

issued the requisite notification on September 30, 2004 incorporating IDBI Ltd. as a

'scheduled bank' under the RBI Act, 1934. Consequently, IDBI, the erstwhile

Development Financial Institution of the country, formally entered the portals of

banking business as IDBIL from October 1, 2004, over and above the business

currently being transacted.

IDBI Ltd. is registered as a company under the Companies Act, 1956 to carry out

banking business in accordance with the provisions of the Banking Regulation Act,

1949. The IDBI Repeal Act 2003 enabled IDBI to become a banking company

without the need to obtain a separate banking license under the Banking Regulation

Act, 1949. IDBI Ltd. will enjoy certain regulatory forbearance, including exemption

from compliance with SLR requirements (mandated under the Banking Regulation

Act) for the first five years. All existing shareholders of the erstwhile IDBI,

including the Central Government, have become pro-rata shareholders of IDBI Ltd.

from the 'appointed date'. Further, the provisions of the Memorandum and Articles

of Association of IDBI Ltd. require that the Central Government, as a shareholder of

the Company, shall, at all times, maintain not less than 51% of the issued capital of

the company.

The authorized capital of IDBI Ltd has been reduced to Rs.1250 crore from Rs.1500

crore (the authorized capital of erstwhile IDBI) in conformity with the provision of

the Banking Regulation Act. The paid-up capital of the Company, at Rs.653 crore,

however, remains the same as the paid-up capital of the erstwhile IDBI.

The merger of IDBI Bank with IDBI Ltd. seeks to consolidate businesses across the

value chain. The merger will provide a win-win situation for both the institutions

and also enable the merged entity to provide an array of customer-friendly services

to its existing and prospective clients. In a physical sense, this would enable IDBI to

complete the integration across the board.

Resource Management

IDBI Ltd's principal sources of outstanding funds comprise borrowings from the

GOI and RBI, borrowings by way of Government-guaranteed bonds, private

placement and public issues of unsecured bonds, market-related relatively short-term

domestic borrowings, foreign currency borrowings and internal generation.

With the initiation of domestic financial sector reforms in the early nineties, the

erstwhile IDBI's access to assured sources of long-duration/concessional funds from

GOI and RBI have been gradually phased out and IDBI Ltd. now overwhelmingly

depends on market borrowings - wholesale and retail, domestic and foreign - for its

resource mobilization

IDBI Ltd. now overwhelmingly depends on market borrowings - wholesale and

retail, domestic and foreign - for its resource mobilization. The Bank has a well-

diversified wholesale resource base, which includes banks, PSUs, corporate,

provident/pension funds, mutual funds, trusts and multilateral institutions. The

sizeable domestic retail segment is being tapped through innovatively packaged

offerings of unsecured bonds, under the brand-name 'Flexi-bonds', at periodic

intervals throughout the year as well as through competitively priced Fixed Deposits

of one year and above under the 'IDBI Suvidha' brand. The principal instruments of

Rupee funds from the wholesale market are Omni Bonds (private placement and on-

tap), Certificates of Deposit, Term Money Bonds, IDBI Corporate Deposits and

Commercial Paper.

On the international front, the erstwhile IDBI's sourcing of funds in various foreign

currencies (FC) for on-lending have, over the last few years, moved away from

multilateral/bilateral lines of credit and towards the External Commercial Borrowing

(ECB) route.

A hallmark of IDBI's resource management initiatives during the last few years has

been its concerted efforts at reducing the average and incremental cost of

borrowings, primarily through periodic retirement of high-cost debt contracted in the

past and refinancing thereof at finer rates.

Management and organization

IDBI Ltd. is a Board-managed institution. The responsibility of the day-to-day

management of operations of the Bank is vested with the Chairman, who draws

upon the support and expertise of a Top Management Team, comprising Executive

Directors and a Legal Adviser. IDBI Ltd.has a pool of around 1400 competent and

experienced professionals. The Bank, with its Head Office at Mumbai, operates

through a network of five Zonal Offices (Chennai, Guwahati, Kolkata, Mumbai and

New Delhi) and Branch Offices spread across the country.

Corporate Office Mumbai

Registered Office IndoreBranches 130

ATM’s 339

Extension Counters 8

Cities 92

The IDBI’s registered office is located at Indore. IDBI Ltd. has over 130 Branches

across 92 cities with 339 ATM’s and 8 Extension Counters.

Working results of IDBI Ltd.

(Rs. crore)2005-06

Total Income 6661Interest income 5381

Non-Interest income 1280

Total Expenses 5860Interest expenses 5001

Operating expenses 859

Operating Profit 801Provisions(net) 240

Net Profit 561

Functions of IDBI

Besides providing assistance to industries directly, IDBI also provides assistance to

industries through other financial institutions and banks. Thus, the assistance

provided by IDBI falls in two categories, viz.

1 Direct finance to large and medium enterprises and

2 Indirect finance through other financial institutions.

FunctionsDirect finance Indirect Finance

- Project Finance - Refinance of Term Loans

- Underwriting & subscription - Rediscounting of bills

to shares & debentures - Support to shares &

- Guarantees for deferred Bonds of other institutions

- Payments & Loans - Rehabilitation Financing

- Bills Discounting

- Equipment Finance Scheme

- Film Financing

Future Prospects

Although IDBI Ltd. commenced its foray into banking on a standalone basis, the

merger of IDBI Bank into IDBI Ltd., a mutually gainful proposition with positive

implications for all stakeholders and clients in terms of operational synergies,

logistics advantages, cost efficiencies and rationalization of business processes, is

expected to be in place before the end of the current financial year ended March 31,

2005. The Board of Directors of both IDBI and IDBI Bank accorded in-principle

approval for the same on July 29, 2004. The Board of IDBI Ltd. (IDBI's successor

entity) ratified the decision regarding merger of IDBI Bank with IDBI Ltd. at the

meeting held on October 1, 2004. The various preparatory steps leading up to the

proposed merger are already under way.

The Board of Directors of IDBI Limited, at its meeting held on January 20, 2005,

approved the Scheme of Amalgamation, envisaging merger of IDBI Bank Ltd with

IDBI Ltd. Pursuant to the Scheme approved by the Boards of both the banks, IDBI

Ltd. will issue 100 equity shares for 142 equity shares held by the shareholders in

IDBI Bank Ltd. IDBI Ltd. will transfer a portion of its current shareholding in IDBI

Bank Ltd., amounting to 2.5% of the merged entity's share capital, to a Special

Purpose Vehicle (SPV) and extinguish the balance shares currently held by it in the

Bank. Post-merger, the Central Government's shareholding in IDBI Ltd. will be at

51.4%. The appointed date for the merger has been fixed as October 1, 2004. The

Scheme of Amalgamation would need to be approved by the shareholders of each of

the banking companies viz. IDBI Ltd. and IDBI Bank Ltd. and will become effective

on subsequent receipt of final approval of the Reserve Bank Of India.

The merger of IDBI Bank with IDBI Ltd. seeks to consolidate businesses across the

value chain. The merger will provide a win-win situation for both the institutions

and also enable the merged entity to provide an array of customer-friendly services

to its existing and prospective clients. In a physical sense, this would enable IDBI to

complete the integration across the board. In a competitive sense, the merger would

create a firm foundation for IDBI to compete with other banks, supported by strong

operational synergies. The merger stood IDBI Ltd. in good stead in its quest for

market share in the intensely competitive financial system and facilitates its passage

to the upper echelons of the emerging financial architecture in India.

The proposed business model underpinning the new organization is one of Strategic

Business Units (SBUs), with one SBU focusing on development finance, with

accent on corporate finance, while the other would focus on commercial banking.

There could be more SBUs, depending on the space that IDBI Ltd. decides to

appropriate for itself going forward.

The transformation into a bank comes on the heels of the establishment of the

Stressed Assets Stabilization Fund (SASF), domiciled in a Special Purpose Vehicle

set up by the Central Government in the form of an Asset Management Trust, to

which stressed assets amounting to Rs. 9000 crore have been transferred. The above

initiative would go a long way in purging IDBI's legacy portfolio of Non-Performing

Assets. The Central Government has accorded SASF the status of a deemed

'financial institution' to enable it to press a claim for disposal of assets in its portfolio

under the aegis of Debt Recovery Tribunals (DRTs), wherever deemed necessary.

The off-balance sheet, cash-neutral proposition is expected to trigger a

concatenation of benefits: a clean and stronger balance-sheet, consequential positive

implication on the organization rating that would translate into more cost-effective

borrowing, both domestically and abroad, and overall upgrade in the organization’s

brand equity that would suitably reflect in its stock valuations, which is already

discernible.

IDBI Ltd. would continue to provide the extant products and services as part of its

development finance role even as a banking company. The Union Budget 2004-05,

presented on July 8, 2004, spelt out a number of positives for financial sector

participants, including IDBI. The focused pursuit of infrastructure development

through pooled investment of Rs. 40,000 crore by the proposed Inter-Institutional

Group (IIG), comprising IDBI Ltd. and select FIs and banks, is expected to stimulate

the Bank's business volumes. Further, the reform of the SARFAESI Act 2002,

making it more equitable for both lenders and borrowers (in the light of the Supreme

Court pronouncements on the subject and apprehension of potential dilution of

creditors' rights) and related enabling amendments in the Debt Recovery Act, 1993,

are expected to strengthen the legal framework for facilitating expeditious recovery

of the organization’s dues from delinquent accounts.

In addition to extant services, the new entity would also provide an array of

wholesale and retail banking products, designed to suit the specific needs/cash-flow

requirements of corporate and individuals. In particular, the Bank would leverage

the strong corporate relationships built up by the erstwhile IDBI over the years to

offer customized and total financial solutions for all corporate business needs,

single-window appraisal for term loans and working capital finance, strategic

advisory and "hand-holding" support at the implementation phase of projects, among

others.

IDBI's transformation into a commercial bank also provides a potential gateway to

low-cost banking deposits like Current and Savings Bank Deposits. This would have

a positive impact on the Bank's overall cost of funds and facilitate lending at more

competitive rates to its clients. The new entity would, in due course, offer various

retail liability products, leveraging upon its present relationship with retail investors

under its existing Suvidha/ Flexibond schemes.

IDBI Ltd. would aggressively leverage its strengths - both within and without - to

fashion an enduring improvement in the Bank's performance, quality of its portfolio

and its relative standing in the emerging financial infrastructure. Systems and

procedures have already been streamlined to facilitate the process while the hard and

soft infrastructure has been readied to address the deliverables of the new

organization.. Going forward, IDBI Ltd. seeks to emerge as a top-drawer

commercial bank, providing innovative financial and banking solutions for corporate

and individuals and a name to reckon with in the emerging configuration of

institutional finance, both at home and abroad, capitalizing on its intimate

knowledge of Indian industry and client requirements and large retail base on the

liability side in addition to the significant benefits expected to accrue from the

ensuing merger of IDBI Bank with IDBI Ltd.

The Bank has set a target of opening 500 branches and 500 ATMs by 2008. Idbi Ltd.

currently has 129 branches and 334 ATMs. It expects to grow 25% in business value

for the next three years. With the inauguration of main branch on Chapel Road,

IDBI Ltd. now has three branches at Hyderabad. Referring to the merger of IDBI

Bank with IDBI, the merger has positive implications for all stakeholders and clients

of these two entities from the viewpoint of operational synergies.

PRODUCTS AND SERVICES

Introduction To The Products And Services

In order to cater to the diverse and customized needs of its corporate clients, IDBI

Ltd. has structured suitable products like equipment finance, asset credit, corporate

loan, working capital loan and bills discounting to variously finance acquisition of

equipment and capital assets, besides meeting capital expenditure and/or incremental

long-term working capital requirements. It also offers structured products like lines

of credit to meet the funding requirements for execution of turnkey contracts.

Besides, IDBI Ltd. provides a wide array of fee-based services.

IDBI Ltd. also provides indirect financial assistance through refinancing of loans

extended by State-level financial institutions and banks and by way of rediscounting

of bills of exchange arising out of sale of indigenous machinery on deferred

payment term.

The Bank has a well-diversified wholesale resource base, which includes banks,

PSUs, corporate, provident/pension funds, mutual funds, trusts and multilateral

institutions. The sizeable domestic retail segment is being tapped through

innovatively packaged offerings of unsecured bonds, under the brand-name 'Flexi-

bonds', at periodic intervals throughout the year as well as through competitively

priced Fixed Deposits of one year and above under the 'IDBI Suvidha' brand. The

principal instruments of Rupee funds from the wholesale market are Omni Bonds

(private placement and on-tap), Certificates of Deposit, Term Money Bonds, IDBI

Corporate Deposits and Commercial Paper.

IDBI's transformation into a commercial bank also provides a potential gateway to

low-cost banking deposits like Current and Savings Bank Deposits.

The new entity would, in due course, offer various retail liability products,

leveraging upon its present relationship with retail investors under its existing

Suvidha /Flexi bond schemes.

IDBI Ltd - Role In Primary Market

1 Acting as collection Banker.

2 Funding IPO’S.

3 Rendering Depository Services.

IDBI Ltd. - Role In Secondary Market

1 Depository services to investors.

2 Helping/Guiding investors to invest in Mutual Funds.

3 CSGL Account to investors who deal in Government securities.

4 Providing Banking services to investors at very competitive price.

In Short, the following are the categories: -

1 Direct Finance

2 Indirect Finance

3 Corporate Banking

4 Retail Banking

5 Treasury Products

Direct Finance

Project Finance

IDBI provide long-term finance for new projects, expansion, diversification and

modernization of existing projects. Project finance is provided by the way of: -

i. Term loans in Indian rupees and foreign currencies.

ii. Underwriting.

iii. Direct subscription to equity capital.

iv. Deferred payment guarantees.

The Term loans are secured by a first charge on the movable and immovable fixed

assets of the industrial concerns. These loans are repayable in quarterly installments

depending upon the projected cash flows of the borrower. IDBI insists upon

minimum promoter’s contribution of 25% of the project cost and debt equity ratio of

1.5: 1. It charges upfront fee @ 1% of the loan amount and underwriting

commission @ 2.5% of the amount underwritten.

1. Guarantees For Deferred Payments And Loans

It includes the following categories: -

1. Corporate Loans

Corporate loans are provided in Indian and foreign currencies to financially

sound companies with net worth of not less than Rs.10 crore and having been

in commercial operation for 5 years and making profits consistently for last 3

years. Such loans are granted to finance capital expenditure and long term

working capital. Assistance is provided from a minimum of Rs.5 crore up to

70% of the cost of capital goods or raw materials, components, etc., to be

purchased.

Promoter’s contribution must be 30% of the cost of capital goods/ raw

materials, components to be purchased.

2. Working Capital Loans

Such loans are provided to meet the loan component of working capital

finance required by the companies already assisted by IDBI with net worth

of not less than Rs. 15 crores. Assistance is provided up to 805 of the

working capital gap with the minimum of Rs.2 crores. These loans are

repayable over a period of 12 to 18 months, with roll over facility at the

discretion of IDBI.

Other terms are debt equity ratio not more than 3:1, Current ratio not less

than 1.25:1 and Interest coverage not less than 2:1.

Bills Discounting

IDBI directly discounts the bills of exchange drawn by financially sound companies,

which have been in operation for at least 3 years and have not defaulted to financial

institutions, in connection with sale of machinery Equipment. IDBI fixes annual

limit for discounting of bills, which are repayable over a period of 2 to 7 years.

Assistance is provided up to 100% of the total value (including insurance, taxes and

freight). IDBI requires security in the form of bank guarantee co-acceptance by a

bank.

Equipment Finance

Equipment finance is also provided in Indian and foreign currencies for acquiring

specific machinery/ equipment. The eligible borrowing firm must be financially

sound company and should have been in operation for at least 5 years. It should have

earned profits during the last 3 years and must have dividend paying capacity of not

less than 2 years. The net worth of the company must be above Rs.5 crores.

Assistance is provided to the extent of 70% of the cost of equipment plus taxes/

duties, transportation and installation charges. The amount of loan ranges between

Rs.3 crores and Rs.25 crores. Loan is repaid over 6 tears including moratorium.

Management fee is charged @ 1.05% on the loan amount.

Film Financing

Objective is to provide finance for production of feature films as defined under the

Cinematograph (Certification) Rules, 1983. Advertisement films, short films,

documentaries, etc. are not eligible for financing.

The eligible borrowing concern should be a corporate entity, promoted by reputed

producers, backed by established directors & other technicians and possessing

satisfactory track record. In case the entity is recently corporative, track record of

the main promoter(s) is considered. The extent of assistance should be :

1 Not less than Rs.2 crore

2 Not exceeding 50% of the estimated cost of the film.

Promoter’s contribution is not less than 30% of the estimated cost of the film.

A part of the equity contribution (not exceeding 20% of th0e estimated cost of the

film) may be raised in the form of advances from distributors against sale of

territories, music/video rights, etc.

Indirect Finance

Re- Finance Of Term Loans

Objective is to finance medium scale industries. IDBI provides: -

i. Line of Credit (LOC) to all SFCs/SIDCs

ii. Refinance to banks only in States of Bihar, Himachal Pradesh, Jammu &

Kashmir, Orissa and States in the North East.

The eligible borrowing concerns should be:

i. Refinance of loans or advances granted by SFCs / SIDCs / SIICs, Financial

Institution, Banks etc.

ii. Should not be SSI

iii. Cost of project not to exceed Rs. 12 crore under LOC scheme.

iv. Proposals meeting the norms and parameters of Refinance Scheme

Promoter’s contribution is @ 25% of project cost and the up front fee is @ 1% on

each disbursement under LOC. The repayment period include:

i. LOC: Maximum 8 years

ii. Refinance: Maximum -10 years and Normal repayment period: 3-10 years

Re-Discounting Of Bills

Objective is to cover or promote sale of indigenous machinery / equipment. The

eligibility includes the bills / promissory notes made, drawn, accepted or endorsed

by any manufacturer, user or any person selling capital goods. The extent of

assistance is the minimum amount of rediscounting of bills/promissory notes is fixed

at Rs.10, 000 and 100% of value of invoice. The repayment period includes the

minimum and maximum deferred payment period covering a set of bills /

promissory notes is two years and 5½ years respectively and maximum period may

be extended up to 7 years, on selective basis, with the prior approval of IDBI.

Rehabilitation Financing

IDBI has in its portfolio certain potentially viable, weak and sick companies, which

can be revived by way of merger /takeover.

Rehabilitation Finance Department (RFD), a specialized department, created to

achieve the said objective, is on the lookout for resourceful parties interested in

takeover/merger or joining in as co-promoter. Industry-wise classification of such

companies is given ahead. Industries, where companies are presently available, are

given. Please click the industry of your interest to have access to such company

profiles.

In addition, IDBI has in its portfolio, other companies which can be revived by

undertaking various measures such as strengthening of management, up gradation of

technology, infusion of fresh funds, etc.

IDBI would like to interact with potential investors / clients who may be interested

in takeover, merger or joining as co-promoters etc. in order to achieve the said

objectives.

Corporate Banking

Lending Products

i. Working capital and Term Loans

ii. Supply Chain Management

Vendor financing

Dealers financing

iii. Loans Against Credit Card Receivables

iv. Loans Syndication

Government Business

i. Tax Collection

ii. Pension Disbursals

Cash Management

i. Current Account & Deposits

ii. Collection & Disbursement Solutions

iii. Debt Servicing

iv. E- Banking Solutions

Trade Finance

i. International / Domestic Letter Of Credit

ii. Performance & Financial Guarantee

iii. Import/ Export Remittance & Collections

iv. Trade Advisory

Retail Banking

At IDBI Bank, it’s not enough to offer a great banking experience. It’s equally

important to understand the various banking needs and answer them well in

advance. In just two years, IDBI has already launched more than 35 sophisticated

products. Some of these categories are: -

Choice Of Accounts

i. Instant Savings Account

ii. Roaming Current Account

iii. Demat Account

iv. NRI Services

v. Corporate Payroll Account

Anytime, Anywhere Banking

i. SMS Banking

ii. Internet Banking

iii. Phone Banking

iv. ATM Banking

Loans

i. Home Loans

ii. Personal Loans

iii. Loans Against Securities

iv. IPO Financing

v. ME Overdraft

Privilege Banking

i. Preferred Customer Banking

ii. Power Plus Saving Account

Investment Advisory Services

i. Mutual Funds

ii. Life Insurance

iii. Bonds & Debentures

Beyond Banking

i. ATM Next

ii. Talking ATMs

iii. Easy Fill Mobile Prepaid Services

iv. Bill Payment

Card Products/ Services

i. World Currency Card

ii. International Debit - cum - ATM Card

iii. Merchant Services

iv. Internet Payment Gateway

Treasury Products

Inward & Outward Remittance

Forward Contracts

Travellers Cheque, Currency

Currency Travel Card

Customized Risk Management Solutions

Interest Rate and Currency Swaps

INR and Foreign Currency Option

Exotic Swaps and Options

Constituent SGL Accounts

Structured Finance Solutions

Debt Syndication and Distribution

VARIOUS PLAYERS IN LOAN AGAINST SECURIT Y

Presenting Loans against Securities from IDBI Bank - A unique scheme that

guarantees the instant liquidity against the securities. To meet the personal needs of

the investment needs be it in the primary market or the secondary market

This is an easy to use overdraft facility up to Rs. 20 lakhs. A current account is

opened in your name (initially for a 1 year period), and you are provided with a

personalized cheque book, ATM card, and access to the Bank by Phone service. You

can then use these to withdraw and deposit money from / into your account, and,

access an exciting range of banking services. Of course, you pay interest only for the

amount and period for which your overdraft facility is utilized

Overdraft facility can be availed against:

1. Demat shares

2. RBI Relief Bonds

3. Mutual funds

4. LIC Policies

5. National Saving Certificate (NSC)

6. Kisan Vikas Patra (KVP)

Eligibility for LAS:

1 Individuals- Salaried, Professional, and Self employed individuals having

independent source of income

2 Should have a Demat account

3 Shares should be fully paid up

4 Shares should be in the approved list of bank.

Scrip’s in the name of corporate Firms, HUF, Minors and NRIs are not eligible for

individual LAS.

How to apply for LAS

1 After fulfilling the eligibility criteria (As mentioned above) LAS application

form is furnished.

2 Loan Document (Including Process note, pledge/ hypothecation

form/agreement for pledge cum guarantee and irrevocable power of attorney)

is signed.

Mode of Loan:

Loan is in the form of overdraft repayable on demand, renewable every year as per

the request of the Borrower.

Suitable drawing limit will be fixed within which the client can draw the overdraft

facility.

Loan limit

Rs.50,000 - Rs. 20,00,000.

Margin

1 On index (Nifty & Sensex) scrips margin @ 50% will be retained

2 Single scrip lending (only nifty & sensex scrips) attracts a margin of 60 %-

70%.

3 Mutual fund -margin @ 50%.

4 RBI Bonds- Margin 5% to 20%.

5 50% margin in case of multiple scrip (minimum 2 scrip)

6 60% margin in single scrip (category A: Pharma, FMCG etc.).

7 70% margin in single scrip (category B: IT Sector).

Interest is payable on monthly basis on the daily reducing balance, penalty of 2% is

charged on delayed payment.

Loan Against Shares

Sanction limit can be up to the value of pledged shares irrespective of Drawing

power, as drawing power can be up to the 50% of the Market value of the pledged

shares.

It is done on the request of the borrower because, Drawing power can be enhanced

up to the sanction limit by pledging more value of shares, instead of further new

documentation.

**Approved list of shares has been attached to the Annexure.

Steps involved in creation of pledge / hypothecation

a) Agreement (Loan document) is signed between borrower and IDBI BANK

branch, outside the NSDL system.

b) The borrower fills pledge creation request in specific format from his DP,

DP enters the request in the DPM.

c) Request is made to IDBI Bank DP cell Mumbai through NSDL.

d) Pledgee (IDBI Bank) is intimated by the borrower’s DP.

e) Pledgee (IDBI Bank branch) gives a Pledge creation confirmation to the

borrower’s DP who enters it in the DPM.

f) Securities are transferred from “ Free Balance” to “Pledged balance”

g) Loan is given by IDBI Bank Branch to borrower in overdraft account.

PLEDGE CLOSURE:

a) Borrower repays the loan to (IDBI Bank branch) pledgee.

b) Borrower gives a pledge closure request to his DP.DP forwards the request

to IDBI Bank DP Cell through NSDL

c) IDBI Bank DP gives a pledge closure confirmation form to the borrower’s

DP.DP confirms the closure on the system.

d) The pledge is closed and the securities are moved from “Pledged” balances

to “Free balances” in the pledger’s account.

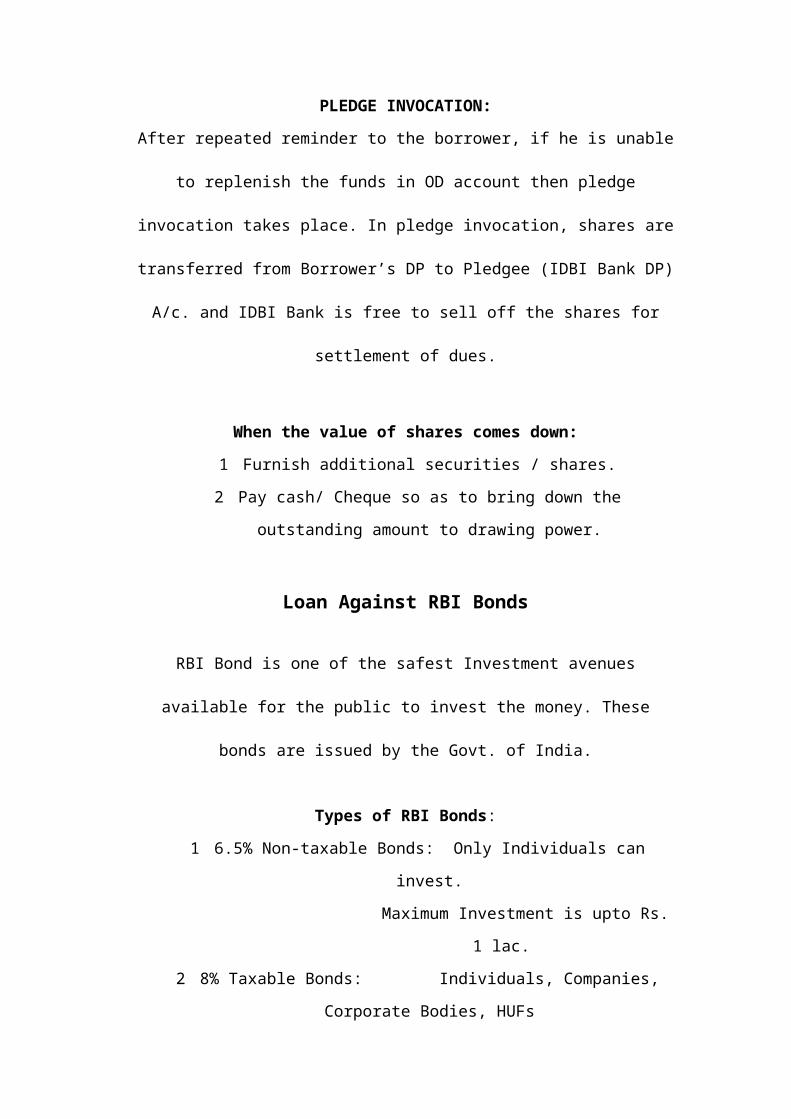

PLEDGE INVOCATION:

After repeated reminder to the borrower, if he is unable to replenish the funds in OD

account then pledge invocation takes place. In pledge invocation, shares are

transferred from Borrower’s DP to Pledgee (IDBI Bank DP) A/c. and IDBI Bank is

free to sell off the shares for settlement of dues.

When the value of shares comes down:

1 Furnish additional securities / shares.

2 Pay cash/ Cheque so as to bring down the outstanding amount to drawing

power.

Loan Against RBI Bonds

RBI Bond is one of the safest Investment avenues available for the public to invest

the money. These bonds are issued by the Govt. of India.

Types of RBI Bonds:

1 6.5% Non-taxable Bonds: Only Individuals can invest.

Maximum Investment is upto Rs. 1 lac.

2 8% Taxable Bonds: Individuals, Companies, Corporate Bodies,

HUFs

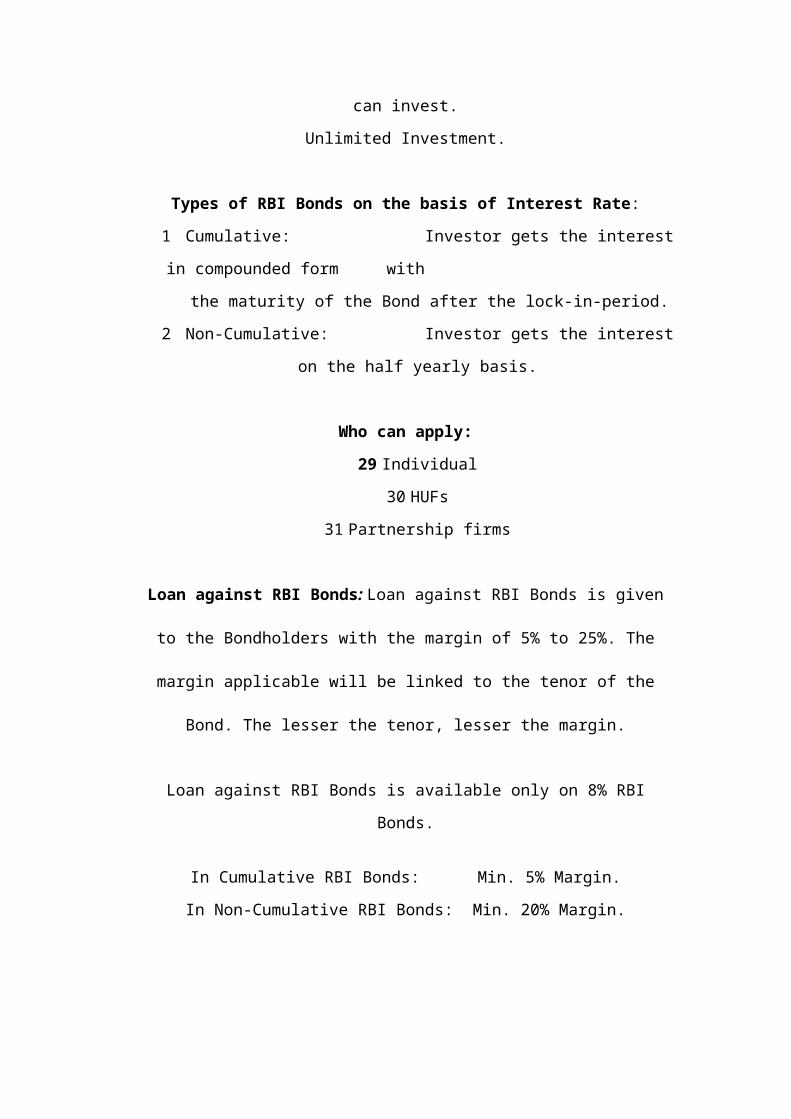

can invest.

Unlimited Investment.

Types of RBI Bonds on the basis of Interest Rate:

1 Cumulative: Investor gets the interest in compounded form

with the maturity of the Bond after the lock-

in-period.

2 Non-Cumulative: Investor gets the interest on the half yearly

basis.

Who can apply:

29 Individual

30 HUFs

31 Partnership firms

Loan against RBI Bonds: Loan against RBI Bonds is given to the Bondholders

with the margin of 5% to 25%. The margin applicable will be linked to the tenor of

the Bond. The lesser the tenor, lesser the margin.

Loan against RBI Bonds is available only on 8% RBI Bonds.

In Cumulative RBI Bonds: Min. 5% Margin.

In Non-Cumulative RBI Bonds: Min. 20% Margin.

Interest charged varies b/w 7.5 to 9.5% depends upon the Bond Value. Interest is

charged from the borrower on the monthly basis on the daily reducing Balance.

Tenure: This facility will be renewable at the end of every 12 months.

Loan Amount:

Minimum Rs 0.50 lac.

Maximum Unlimited.

(The limit depends upon the value of the bond & applicable margin).

Prerequisite: Borrower holds a Bond Ledger Account with any of the designated

bank, authorized by RBI for servicing the bonds.

‘Bond Ledger A/c’ is the A/c, from where the Bond is issued to the investor.

Loan Against Mutual Fund Units

Presently available only against IDBI Principal Mutual Fund units.

Eligibility

1 Individuals, salaried,

2 professional,

3 self-employed and

4 individuals having independent source of income.

Purpose of the loan

You can avail of the facility to meet contingencies and personal needs

Loan Limits

You can take a loan anywhere between a minimum of Rs.0.50 Lac to a maximum of

Rs.20.00 Lac. The limit depends on the valuation of the security, applicable margin,

and your ability to service and repay the loan, and other conditions as applicable

from time to time.

Margin

Margin @50% will be applicable based on the market value of units/ repurchase

price/ net asset value whichever is lower. Units of Mutual Fund will attract margin

of 50 %.

Interest Rate

The Interest rates charged by idbi bank are amongst the lowest in the market.

Withdrawals / swaps Rs.100 per request.

Approved list of Schemes of IDBI Principal Mutual Fund.

IDBI Principal Money Market FundIDBI Principal Index Fund

IDBI Principal Deposit Fund -54EAIDBI Principal Deposit Fund -54 EB

IDBI Principal Equity FundIDBI Principal Deposit Fund Bond Plan

IDBI Principal Growth FundIDBI Principal Income FundIDBI Principal Balance Fund

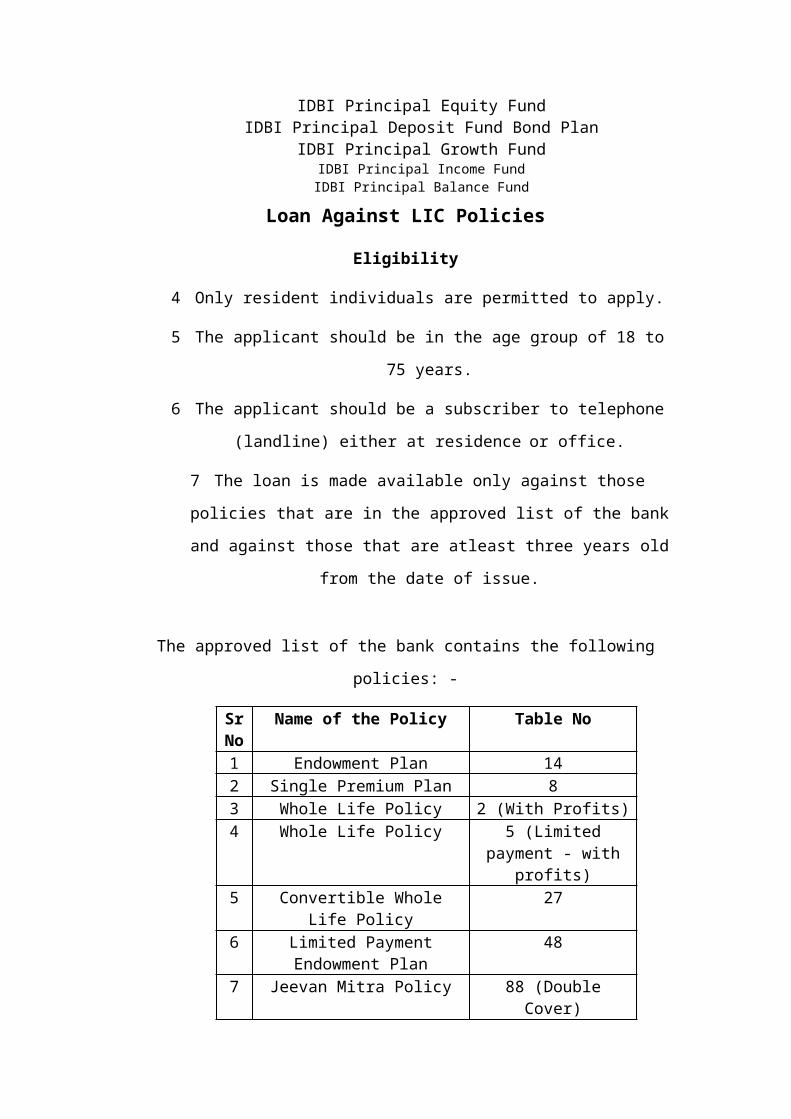

Loan Against LIC Policies

Eligibility

4 Only resident individuals are permitted to apply.

5 The applicant should be in the age group of 18 to 75 years.

6 The applicant should be a subscriber to telephone (landline) either at

residence or office.

7 The loan is made available only against those policies that are in the

approved list of the bank and against those that are atleast three years old

from the date of issue.

The approved list of the bank contains the following policies: -

Sr No

Name of the Policy Table No

1 Endowment Plan 142 Single Premium Plan 83 Whole Life Policy 2 (With Profits)4 Whole Life Policy 5 (Limited payment -

with profits)5 Convertible Whole Life Policy 276 Limited Payment Endowment

Plan48

7 Jeevan Mitra Policy 88 (Double Cover)8 Jeevan Mitra Policy 133 (Triple Cover)9 Jeevan Saathi 8910 New Janaraksha Policy 9111 Jeevan Anand 14912 New Bima Kiran 15013 New Jeevan Shree 15114 Bima Nivesh 13215 Bima Nivesh - Triple Cover 14316 Bima Nivesh 2002 15817 Bima Nivesh 2004 16618 Jeevan Shree 16219 Bima Kiran 11120 Jeevan Shree 11221 Bima Nivesh 2001 141

22 Bima Nivesh 142

Loan Limits

You can take a loan anywhere between a minimum of Rs.0.50 Lac to a maximum of

Rs.20.00 Lac. The limit depends on the valuation of the security, applicable margin,

and your ability to service and repay the loan, and other conditions as applicable

from time to time.

Process Involved In Availing The Loan Against Securities

In Case OF Shares

1. Submission of Documentation to the branch by BDE. Preliminary check and

credit investigation is done by the branch.

2. Verification of the customer is done and KYC duly signed and attached with the

documents by the authorized signatory.

3. Stamping and notarization of document by branch.

4. Credit approval and ROI approval is taken by branch from C.P.U.

5. Dispatch of loan documents to CPU LAS operation along with detail of demat

A/c and dematerlized shares to pledge.

6. Agreement number (Account number) is generated by C.P.U., which is forwarded

to customer for pledging of shares in favour of Idbi bank.

7. Customer pledges the share(s) in respective D.P. and submits the pledge master

report in respective branch along with the pledge forms of Idbi bank so as to

conform the created pledge.

8. Branch sends the details (pledge master report) of the share(s) along with the

pledge order number to the Depository participant cell; finally C.P.U. set the

Drawing power. accordingly with the current market value of the pledge shares.

In Case Of Bonds

1. Submission of Documentation to the branch by BDE. Preliminary check and

credit investigation is done by the branch.

2. BDE approaches to respective bank from where the bonds are issued and

where customer maintains his BLA (Bond Ledger Account) for transfer of

bonds in favour of Idbi bank.

3. Verification of the customer is done and KYC duly signed and attached with

the documents by the authorized signatory.

4. Stamping and notarization of document by branch.

5. Credit approval and ROI approval is taken by branch from C.P.U.

6. Dispatch of loan document to CPU Las operation along with transferred

original bonds.

7. After close verification of document by CPU LAS operation, Account is

open by CPU limit is being set as document and D.P. as per the value and

type of the bonds

In Case OF LIC

1. Submission of Documentation to the branch by BDE. Preliminary check and

credit investigation is done by the branch.

2. Getting the surrender value of LIC policy through LIC office.

3. Approach to the respective LIC office with the original LIC policies, assignment form,

notice of assignment and bank covering letter obtain from respective branch for assigning

the policies in favour of Idbi bank.

4. Assigned LIC policies are obtained back (by hand or by post).

5. Status report is taken from LIC office for conformation of assignment

6. Verification of the customer is done and KYC duly signed and attached with the

documents by the authorized signatory.

7. Stamping and notarization of document by branch.

8. Credit approval and ROI approval is taken by branch from C.P.U.

9. Dispatch of loan document to CPU Las operation along with original assigned LIC

policies, Status report and surrender value quotation.

10. After close verification of document by CPU LAS operation, Account is open by CPU

and drawing power is set as per documents and D.P. as per the credit approval.

In Case OF KVP/NSC

1. Submission of Documentation to the branch by BDE. Preliminary check and credit

investigation is done by the branch.

2. BDE approaches the respective post office along with original KVP/NSC, bank

covering letter FormNC-41 (issue by post office) and authority letter from branch

head for pledging KVP/NSC in favour of Idbi bank

3. Pledge KVP/NSC are obtained back

4. Verification of the customer is done and KYC duly signed and attached with the

documents by the authorized signatory.

5. Stamping and notarization of document by branch.

6. Credit approval and ROI approval is taken by branch from C.P.U.

7. Dispatch of loan document to CPU Las operation along with original KVP/NSC.

8. After close verification of document by CPU LAS operation, Account is open by

CPU and limit is set as per documents and D.P. as per the credit approval.

ICICI Bank was originally promoted in 1994 by ICICI Limited, an Indian financial

institution, and was its wholly owned subsidiary. ICICI was formed in 1955 at the

initiative of the World Bank, the Government of India and representatives of Indian

industry. The principal objective was to create a development financial institution

for providing medium-term and long-term project financing to Indian businesses.

In the 1990s, ICICI transformed its business from a development financial

institution offering only project finance to a diversified financial services group

offering a wide variety of products and services, both directly and through a number

of subsidiaries and affiliates like ICICI Bank. In 1999, ICICI become the first Indian

company and the first bank or financial institution from non-Japan Asia to be listed

on the NYSE.

In October 2001, the Boards of Directors of ICICI and ICICI Bank approved the

merger of ICICI and two of its wholly owned retail finance subsidiaries, ICICI

Personal Financial Services Limited and ICICI Capital Services Limited, with ICICI

Bank. Shareholders of ICICI and ICICI BANK approved the merger in January

2002, by the High Court of Gujarat at Ahmedabad in March 2002, and by the High

Court of Judicature at Mumbai and the Reserve Bank of India in April 2002.

Consequent to the merger, the ICICI group's financing and banking operations, both

wholesale and retail, have been integrated in a single.

The merger has enhance value for ICICI shareholders through the merged entity's

access to low-cost deposits, greater opportunities for earning fee-based income and

the ability to participate in the payments system and provide transaction-banking

services

Objective

The principal objective was to create a development financial institution for

providing medium-term and long-term project financing to Indian businesses.

1 Continuous technology up gradation while maintaining human values.

2 Progressive globalization and achieving international standards.

3 Efficiency and effectiveness built on ethical practices.

4 Customer Satisfaction through -

1. Providing quality service effectively and efficiently

2. Smile, it enhances your face value" is a service quality stressed on

3. Periodic Customer Service Audits

5 Maximization of Stakeholder value

6 Success through Teamwork, Integrity and People

Activities

ICICI Bank offers a wide range of banking products and financial services to

corporate and retail customers through a variety of delivery channels and through its

specialized subsidiaries and affiliates in the areas of investment banking, life and

non-life insurance, venture capital and asset management. ICICI Bank set up its

international banking group in fiscal 2002 to cater to the cross border needs of

clients and leverage on its domestic banking strengths to offer products

internationally.

Capital Structure

ICICI Bank is India's second-largest bank with total assets of about Rs.1, 67,659

crores at March 31, 2005 and profit after tax of Rs. 2,005 crores for the year ended

March 31, 2005 (Rs. 1,637 crores in fiscal 2004)

ICICI Bank's equity shares are listed in India on the Stock Exchange, Mumbai and

the National Stock Exchange of India Limited and its American Depositary Receipts

(ADRs) are listed on the New York Stock Exchange (NYSE).

At April 4, 2005, ICICI Bank, with free float market capitalization* of about Rs.

308.00 billion (US$ 7.00 billion) ranked third amongst all the companies listed on

the Indian stock exchanges.

Network

ICICI Bank has a network of about 560 branches and extension counters and over

1,900 ATMs. ICICI Bank currently has subsidiaries in the United Kingdom and

Canada, branches in Singapore and Bahrain and representative offices in the United

States, China, United Arab Emirates, Bangladesh and South Africa.

Loan Against Securities With ICICI Bank

Loans against Securities enable the borrower to obtain loans against his securities.

So that he gets the instant liquidity without having to sell his securities.

All he has to do is pledge his securities in favour of ICICI Bank. The Bank will then

grant an overdraft facility up to a value determined on the basis of the securities

pledged by the borrower. A current account will be opened and the borrower can

withdraw money as and when he require. Interest will be charged only on the

amount withdrawn and for the time span utilized

Overdraft facility can be availed against:

1. Demat shares

2. RBI Relief Bonds

3. Mutual funds

4. India Millennium Deposits (IMD’s)

5. ICICI Bank Bonds

6. LIC Policies (Single Premium)

Loan Amount

1. Shares

1 You are given a drawing power up to 50% of the value of the shares.

2 Since the market price of the scrip keeps fluctuating, the scripts are revalued

weekly (every friday), or more frequently if required, and the drawing power

will be revised accordingly. If the new drawing power is less than the

outstanding in the current account, the customer is required to put in the

difference amount or pledge more shares to regularize the account.

Alternately, if the drawing power rises, the limit available to the customer

also automatically increases.

3 Minimum loan amount is Rs 1 lakh.

4 Maximum loan amount is Rs 20 lakh.

5 The loan is applicable for a year and renewable at the end of each year.

2. Bonds

1 The loan amount will depend upon the value of bonds and also the period left

for maturity

2 Loan amount will be between 70% and 95% of the value of bonds.

3. Mutual Funds

1 50% lending on the NAV.

2 Minimum loan amount is Rs.1 lakh.

3 Maximum loan amount is Rs. 20 lakh.

4. India Millennium Deposits (IMDs)

1 90% of the face value in rupees.

2 Minimum loan amount is Rs.1 lakh.

5. ICICI Bank Bonds

1 Minimum Loan amount is Rs.50000

2 Maximum loan amount is Rs. 20 lakh

6. Life Insurance Policies (Single Premium)

1 Minimum Loan amount is Rs.50000

2 Maximum loan amount is Rs. 2 crores

Eligibility

1. Shares

1 Only resident individuals are permitted to apply.

2 Hindu Undivided Families (HUFs), Limited Companies, Partnerships, Sole

Proprietors & NRIs are excluded.

3 Loans are granted only against the list of approved scripts, as determined by

ICICI Bank.

4 The applicant should be in the age group of 18 to 75 years.

5 The applicant should be a subscriber to telephone (landline) either at

residence or office.

2. RBI Bonds

1 Resident Individuals, Hindu Undivided Families (HUFs), Limited

Companies and Partnerships are permitted to apply.

2 Non Resident Indians (NRIs) are excluded.

3 The applicant should be in the age group of 18 to 75 years.

4 The applicant should be a subscriber to telephone (landline) either at

residence or office.

3. Mutual Funds

1 Only resident individuals are permitted to apply.

2 HUFs, Limited Companies, Partnerships, Sole Proprietors and NRIs are

excluded.

3 The applicant should be in the age group of 18 to 75 years.

4 The applicant should be a subscriber to telephone (landline) either at

residence or office.

4. India Millennium Deposits (IMDs)

1 Only non-resident Indian individuals can apply. In case a resident has to

apply he should have a guarantee of bonds from the NRI for doing so.

2 The applicant should be in the age group of 18 to 75 years.

3 The applicant should be a subscriber to telephone (landline) either at

residence or office.

5. ICICI Bank Bonds

1 Only resident individuals are permitted to apply.

2 The applicant should be in the age group of 18 to 75 years.

3 The applicant should be a subscriber to telephone (landline) either at

residence or office.

6. Life Insurance Policies (Single Premium)

1 Only resident individuals are permitted to apply.

2 The applicant should be in the age group of 18 to 75 years.

3 The applicant should be a subscriber to telephone (landline) either at

residence or office.

4 For all the above the applicant should be in the age group of 18 to 75 years.

5 The applicant should be a subscriber to telephone (landline) either at

residence or office.

The Housing Development Finance Corporation Limited (HDFC) was amongst the

first to receive an 'in-principle' approval from the Reserve Bank of India (RBI) to set

up a bank in the private sector, as part of the RBI's liberalization of the Indian

Banking Industry in 1994. The bank was incorporated in August 1994 in the name

of 'HDFC Bank Limited', with its registered office in Mumbai, India. HDFC Bank

commenced operations as a Scheduled Commercial Bank in January 1995.

HDFC is India's premier housing finance company and enjoys an impeccable track

record in India as well as in international markets.

Since its inception in 1977, the Corporation has maintained a consistent and healthy

growth in its operations to remain a market leader in mortgages. Its outstanding loan

portfolio covers well over a million dwelling units.

Business Focus

HDFC Bank's mission is to be a World-Class Indian Bank. The Bank's aim is to

build sound customer franchises across distinct businesses so as to be the preferred

provider of banking services in the segments that the bank operates in and to achieve

healthy growth in profitability, consistent with the bank's risk appetite. The bank is

committed to maintain the highest level of ethical standards, professional integrity

and regulatory compliance. HDFC Bank's business philosophy is based on four core

values: Operational Excellence, Customer Focus, Product Leadership and people.

Activities of HDFC

HDFC has developed significant expertise in retail mortgage loans to different

market segments and also has a large corporate client base for its housing related

credit facilities. With its experience in the financial markets, a strong market

reputation, large shareholder base and unique consumer franchise, HDFC was

ideally positioned to promote a bank in the Indian environment.

HDFC Bank caters to a wide range of banking services covering both commercial

and investment banking on the wholesale side and transactional / branch banking on

the retail side.

The bank has three key business areas: -

a) Wholesale Banking Services

b) Retail Banking Services

c) Treasury Operations

Capital Structure

The authorized capital of HDFC Bank is Rs.450 crore (Rs.45 billion). The paid-up

capital is Rs.282 crore (Rs.28.2 billion). The HDFC Group holds 24.2% of the

bank's equity while about 13.1% of the equity is held by the depository in respect of

the bank's issue of American Depository Shares (ADS/ADR Issue). The Indian

Private Equity Fund, Mauritius (IPEF) and Indocean Financial Holdings Ltd.,

Mauritius (IFHL) (both funds advised by J P Morgan Partners, formerly Chase

Capital Partners) together hold about 5.5% of the bank's equity. Roughly 27.5% of

the equity is held by FIIs, NRIs/OCBs while the balance is widely held by about

214,000 shareholders.

The shares are listed on The Stock Exchange, Mumbai and the National Stock

Exchange. The bank's American Depository Shares are listed on the New York

Stock Exchange (NYSE) under the symbol "HDB".

Distribution Network

HDFC Bank is headquartered in Mumbai. The Bank at present has an enviable

network of over 484 branches spread over 217 cities across the country. All

branches are linked on an online real-time basis. Customers in 90 locations are also

serviced through Phone Banking. The Bank's expansion plans take into account the

need to have a presence in all major industrial and commercial centers where its

corporate customers are located as well as the need to build a strong retail customer

base for both deposits and loan products. Being a clearing/settlement bank to various