Comparison Methods Part 2. Copyright © 2006 Pearson Education Canada Inc. 5-2 5.1 Introduction...

27

Comparison Methods Part 2

-

Upload

merilyn-morgan -

Category

Documents

-

view

216 -

download

0

Transcript of Comparison Methods Part 2. Copyright © 2006 Pearson Education Canada Inc. 5-2 5.1 Introduction...

Comparison Methods Part 2

Copyright © 2006 Pearson Education Canada Inc. 5-2

5.1 Introduction

• Chapter 4 introduced the Present Worth and Annual Worth comparison methods

• This chapter introduces another commonly used comparison method called the internal rate of return

Copyright © 2006 Pearson Education Canada Inc. 5-3

Example 5-1

• Suppose $100 is invested today and it returns $110 in one year from now.

• The internal rate of return (IRR) for this investment is the interest rate at which $100 today is equivalent to $110 one year from now:

• Solve for i* in:

P = F(P/F,i*,1)

100 = 110/(1+i*)1

i * = 0.10 or, 10%.• The internal rate of return (IRR) is 10%

Copyright © 2006 Pearson Education Canada Inc. 5-4

The Internal Rate of Return (con’t)

• The IRR is the interest rate at which the project “breaks even”

• It is the interest rate such that:

PW = 0, or PW(receipts) = PW(disbursements)

FW = 0, or FW(receipts) = FW(disbursements)

AW = 0, or AW(receipts) = AW(disbursements)

• The “internal” in IRR refers to the fact that the return is due to the cash flows “internal” to the project being evaluated.

Copyright © 2006 Pearson Education Canada Inc. 5-5

Example 5-2 (Very Important)

• New windows at University of Saskatoon are expected to save $400 per year in energy over their 30 year life. The windows have an initial cost of $8000 and will have a zero salvage value.

a) Plot the Present Worth of this investment as a function of the interest rate. What is the IRR?

Copyright © 2006 Pearson Education Canada Inc. 5-6

Example 5-2: Answera) Use a spreadsheet to calculate and plot PW

PW = -8000 + 400(P/A,i,30)i PW(windows)

0.00 40000.01 23230.02 9590.03 -160

-1800

-800

200

1200

2200

3200

0.00 0.01 0.02 0.03 0.04 0.05

Interest Rate

Pres

ent W

orth

($)

Copyright © 2006 Pearson Education Canada Inc. 5-7

Compound Interest FactorsDiscrete Cash Flow, Discrete Compounding

To Find Given Name of Factor Factor

A P Capital Recovery Factor

P APresent Worth Factor (uniform series)

A G

Arithmetic Gradient Conversion Factor (to uniform series)

P G

Arithmetic Gradient Conversion Factor (to present value)

1)1(

)1(

n

n

i

ii

n

n

ii

i

)1(

1)1(

]1)1[(

)1()1(

n

n

ii

nii

2

)1)(1(1

i

ini n

Copyright © 2006 Pearson Education Canada Inc. 5-8

Capital Recovery Factor

$120,000

1 2 3 8

A A A A A

(1 )

(1 ) 1

n

n

i iA P

i

30

30

(1 ) 1$8000

(1 )

(1 0.01) 1$8000 $400

0.01(1 0.01)

$2323

n

n

iP A

i i

Copyright © 2006 Pearson Education Canada Inc. 5-9

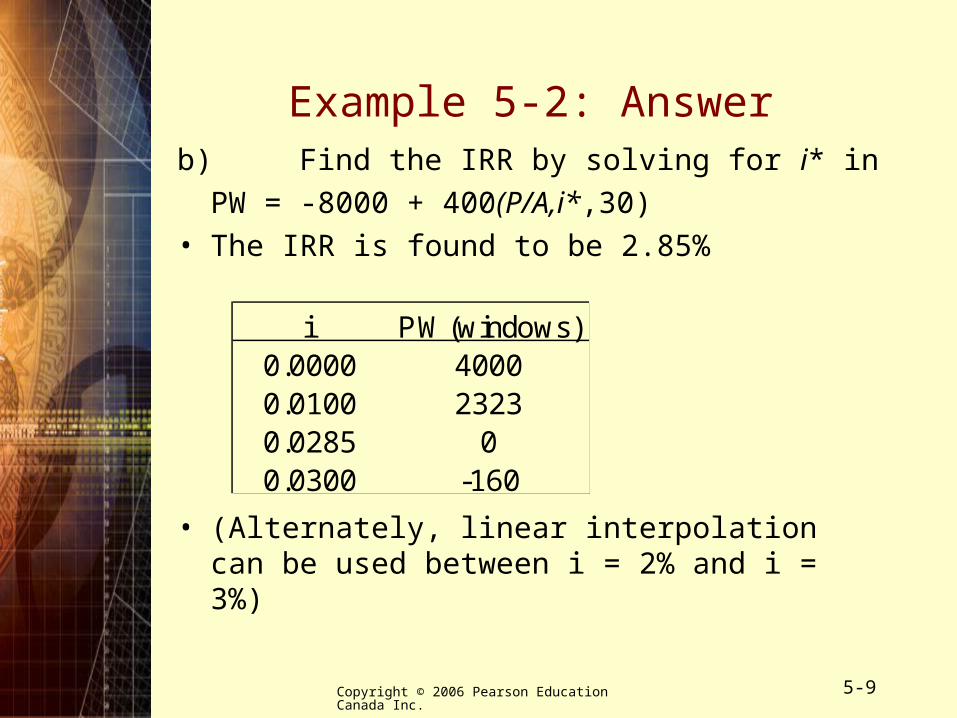

Example 5-2: Answerb) Find the IRR by solving for i* in

PW = -8000 + 400(P/A,i*,30)• The IRR is found to be 2.85%

• (Alternately, linear interpolation can be used between i = 2% and i = 3%)

i PW(windows)0.0000 40000.0100 23230.0285 00.0300 -160

Copyright © 2006 Pearson Education Canada Inc. 5-10

5.3 Internal Rate of Return Comparisons

• This section demonstrates how to use the Internal Rate of Return to decide whether a project should be accepted

– IRR for Independent Projects– IRR for mutually exclusive projects– Potential for multiple IRRs– External Rate of Return ERR

Copyright © 2006 Pearson Education Canada Inc. 5-11

5.3.1 IRR for Independent Projects

• For Independent Projects: Select any project which has an IRR which is at least the MARR.

• Similar to the evaluation of independent projects where any project with a PW or AW ≥ 0 is acceptable.

Copyright © 2006 Pearson Education Canada Inc. 5-12

Example 5-2 (Revisited)

• New windows at the University of Saskatoon are expected to save $400 per year in energy over their 30 year life. The windows have an initial cost of $8000 and will have a zero salvage value.

• The MARR is 8%. Using an IRR analysis, should the investment be made?

• NO – we saw that the IRR = 2.85% < MARR.

Copyright © 2006 Pearson Education Canada Inc. 5-13

5.3.2 IRR for Mutually Exclusive Projects

• The analysis gets a bit more complex than for independent projects.

• We will start with a comparison of two projects.

Copyright © 2006 Pearson Education Canada Inc. 5-14

Example 5-3

• Consider two mutually exclusive investments. The first costs $10 today and returns $20 in one year. The second costs $1000 and returns $1200 in one year. Your MARR is 12%

• Which is your preferred investment?

(P.S. You cannot take “multiples” of the investments.)

Copyright © 2006 Pearson Education Canada Inc. 5-15

Example 5-3: Answer

• First project:

Rate of return = 100%

PW = -10 + 20 (P/F,12%,1) = $7.86• Second Project:

Rate of Return = 20%

PW = -1000 + 1200(P/F,12%,1) = $71.42

• The IRR for the first project is higher than the second, but the second has a higher PW…

• The preferred project is the second. Why?

Copyright © 2006 Pearson Education Canada Inc. 5-16

IRR for Mutually Exclusive Projects

• If the two projects in Example 5-3 were independent, we would do both (both have an IRR > MARR).

• If they are mutually exclusive, it is tempting to pick the one with the higher IRR, but this is incorrect because it can overlook projects whose IRR is at least the MARR, but don’t have the highest IRR.

• It is important that each incremental investment earn at least the MARR. (each part makes money)

Copyright © 2006 Pearson Education Canada Inc. 5-17

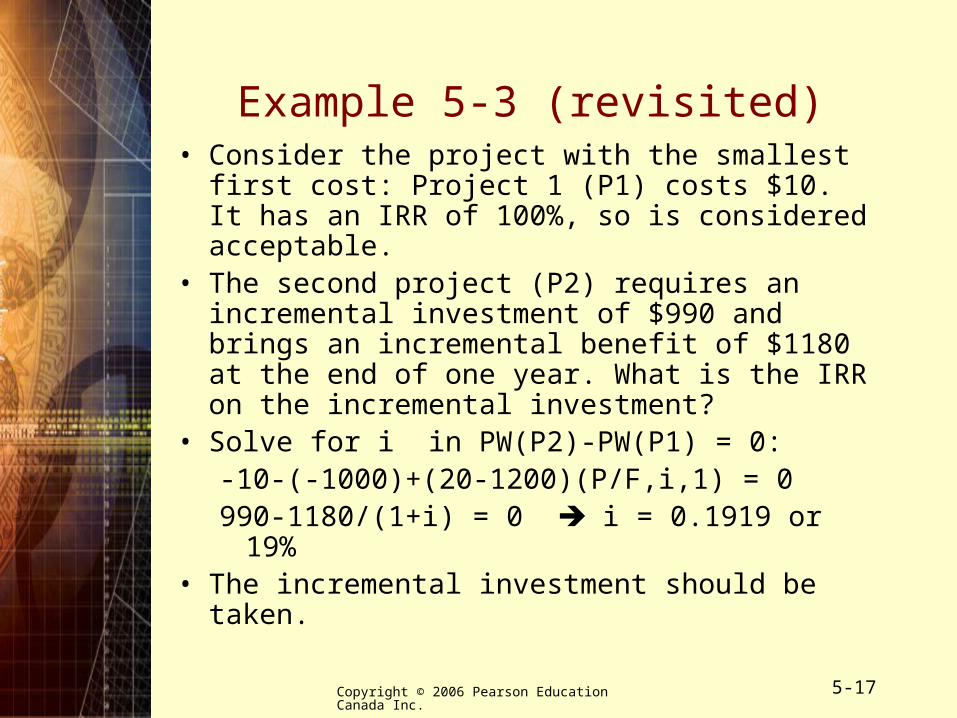

Example 5-3 (revisited)• Consider the project with the smallest first cost:

Project 1 (P1) costs $10. It has an IRR of 100%, so is considered acceptable.

• The second project (P2) requires an incremental investment of $990 and brings an incremental benefit of $1180 at the end of one year. What is the IRR on the incremental investment?

• Solve for i in PW(P2)-PW(P1) = 0:-10-(-1000)+(20-1200)(P/F,i,1) = 0990-1180/(1+i) = 0 i = 0.1919 or 19%

• The incremental investment should be taken.

Copyright © 2006 Pearson Education Canada Inc. 5-18

5.5.3 Multiple IRRs: Example 5-5• Suppose that a project pays $2500 today,

costs $12 500 one year from now and pays $15 000 in two years. What is the IRR?

• Solve for i* in:

2500–12 500(P/F,i*,1)+15 000(P/F, i*, 2)=0

• i* = 100% or 200%. Which is correct?

0)2*i)(1*i(

02*i3*i

0*)i1(

6

*i1

51

2

2

Copyright © 2006 Pearson Education Canada Inc. 5-19

Multiple IRRs (con’t)

-200

0

200

400

600

800

1000

0.00

Interest Rate

Pre

se

nt

Wo

rth

($

)

200%100%

Copyright © 2006 Pearson Education Canada Inc. 5-20

Descartes’ Rule of Signs• gives an upper limit on the number of positive,

real roots of a polynomial with real coefficients (e.g. PW(i) = 0).

The number of positive, real IRRs is less than or equal to the number of sign changes in the cash flow series.

• There were 2 sign changes in Example 5-5 – Descartes’ rule says that there can be 0, 1

or 2 positive real IRRs.

Copyright © 2006 Pearson Education Canada Inc. 5-21

Project Balances

• Consider Example 5-5 again

Project Balance Project BalanceYear at i = 100% at i = 200%0 2500 25001 2500(1+1) – 12500= –7500 2500(1+2) – 12 500 = –

50002 –7500(1+1) + 15 000 = 0 –5000(1+2) + 15 000 = 0

• Positive project balances are invested elsewhere – probably at the MARR (Minimum Acceptable Rate of Return), but not at 100% or 200%.

Copyright © 2006 Pearson Education Canada Inc. 5-22

5.4 IRR and PW/AW Methods Compared

• IRR: commonly used, facilitates comparisons of projects of different sizes, difficult to calculate, multiple IRR may exist.

• PW and AW: difficult to compare projects of different sizes. PW gives explicit measure of profit. AW may be more meaningful.

• All are equivalent and thus lead to the same decision.

Copyright © 2006 Pearson Education Canada Inc. 5-23

5.3.4 External Rate of Return Methods

• What return is earned by money associated with a project that is not invested in the project?– The usual assumption is that the funds are invested

elsewhere and earn an explicit rate of return (usually the MARR – a “conservative” assumption).

• The external rate of return (ERR) is the rate of return on a project where any “excess” cash from a project is assumed to earn interest at a pre-determined explicit rate — usually the MARR.

Copyright © 2006 Pearson Education Canada Inc. 5-24

Approximate ERR

• Computing an exact ERR is difficult: The ERR affects project balances, which affect the ERR.

• To get an approximate ERR:

1. Take all net receipts forward at the MARR to the time of the last cash flow.

2. Take all net disbursements forward at the unknown rate iea* (approximate ERR) to the time of the last cash flow.

3. Set FW(receipts) = FW(disbursements) and solve for iea*.

Copyright © 2006 Pearson Education Canada Inc. 5-25

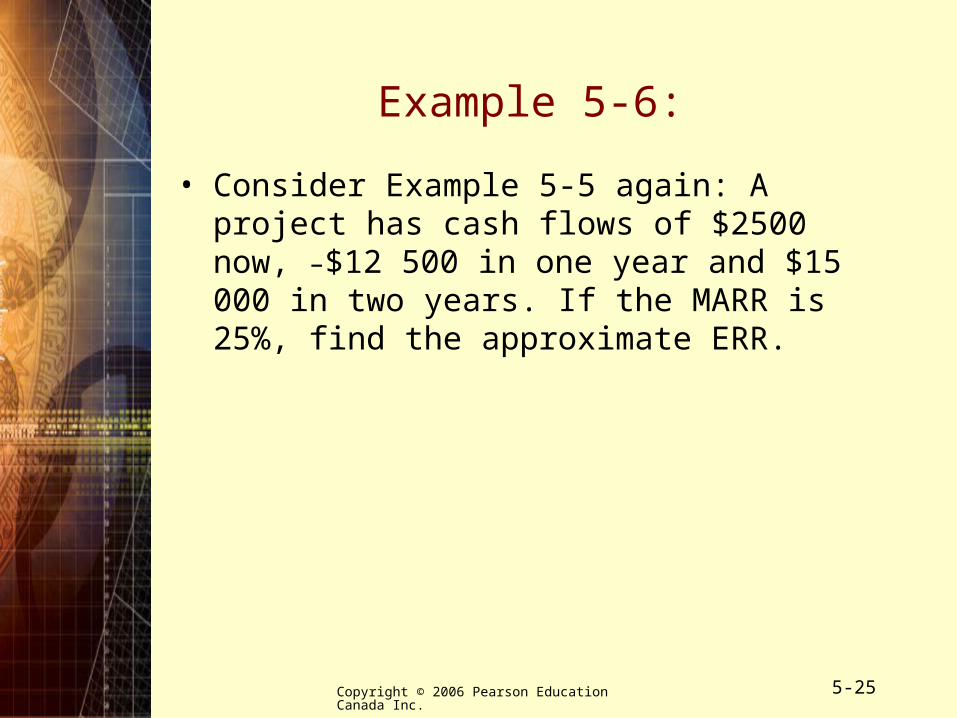

Example 5-6:

• Consider Example 5-5 again: A project has cash flows of $2500 now, –$12 500 in one year and $15 000 in two years. If the MARR is 25%, find the approximate ERR.

Copyright © 2006 Pearson Education Canada Inc. 5-26

Example 5-6: Answer

• Taking net receipts forward at the MARR and equating to net disbursements taken forward at the unknown rate () gives:

2500(F/P,25%,2) + 15 000 = 12 500(F/P,i*,1)

(F/P,i*,1) = 1.5125

(1+ i*) = 1.5125

• The approximate ERR is 51.25%.

Copyright © 2006 Pearson Education Canada Inc. 5-27

Summary

• Internal Rate of Return (IRR) Defined• IRR comparisons for independent projects• IRR comparisons for mutually exclusive

projects• External Rate of Return (ERR) Methods• Comparison of IRR and PW/AW Methods