Company Progress FIX Banget

51

Module Assignment – Accounting Information System I Page 34 PT Pelni (Persero) 2014 PREFACE First of all, give thanks for God’s love and the gracious that enable authors to accomplish this end of term assignment for the Accounting Information System I subject which talk about Internal audit, Internal Control, Revenue cycle, and also Data Management in PT Pelni. Thanks to God for helping us and give us chance to finish this assignment periodically. This module assignment is arranged to complete our task in Accounting Information System I subject. Authors would like to say thank you to people who guides us in completing this Module Assignment. 1. Mr. James Situmorang Akt., MBA., MM. as the lecturer that always teach and give us much knowledge about Accounting Information System I 2. Mr. Junaidi as source information about PT Pelni 3. Our beloved family especially our parents for supporting and motivating us to complete this task 4. And also our friends for their support and help. Authors realized this assignment is not perfect. The authors apologize if in this Module Assignment there are some mistaken on writing or mistaken in providing information to the reader. But we hope it can be useful for us. Critics and suggestion is needed here to make this assignment be better. December 4 th , 2014

-

Upload

triasekarprestisha -

Category

Documents

-

view

233 -

download

1

description

hmm

Transcript of Company Progress FIX Banget

PT Pelni (Persero) 2014

PREFACE

First of all, give thanks for God’s love and the gracious that enable authors to accomplish this end of term assignment for the Accounting Information System I subject which talk about Internal audit, Internal Control, Revenue cycle, and also Data Management in PT Pelni. Thanks to God for helping us and give us chance to finish this assignment periodically.

This module assignment is arranged to complete our task in Accounting Information System I subject. Authors would like to say thank you to people who guides us in completing this Module Assignment.

1. Mr. James Situmorang Akt., MBA., MM. as the lecturer that always teach and give us much knowledge about Accounting Information System I

2. Mr. Junaidi as source information about PT Pelni

3. Our beloved family especially our parents for supporting and motivating us to complete this task

4. And also our friends for their support and help.

Authors realized this assignment is not perfect. The authors apologize if in this Module Assignment there are some mistaken on writing or mistaken in providing information to the reader. But we hope it can be useful for us. Critics and suggestion is needed here to make this assignment be better.

December 4th, 2014

Authors

Page 1Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

Table of ContentsPREFACE................................................................................................................................................1

Table of Contents..................................................................................................................................2

BAB I

Introductions.........................................................................................................................................4

A. Background...................................................................................................................................4

B. Purpose of Writing........................................................................................................................4

C. Methodology.................................................................................................................................4

D. Systematization............................................................................................................................5

BAB II

Theories.................................................................................................................................................6

1. Information System...........................................................................................................................6

1.1 What is Information System?.....................................................................................................6

1.2 Information Objectives...............................................................................................................6

1.3 Information System....................................................................................................................6

2. Transactions Processing Models........................................................................................................8

3. Internal Control.................................................................................................................................9

3.1 COSO Internal Control Framework...........................................................................................10

4. Revenue Cycle.................................................................................................................................11

4.1 Basic Technology of Revenue Cycle..........................................................................................11

5. Database..........................................................................................................................................12

BAB III

Analysis................................................................................................................................................13

1. About PT Pelni (Persero)..................................................................................................................13

1.1 History of PT Pelni.....................................................................................................................13

1.2 Company’s Profile.....................................................................................................................14

1.3 Vision and Mission....................................................................................................................15

1.4 Core Values...............................................................................................................................15

1.5 Core Business............................................................................................................................16

2. Company’s Structure.......................................................................................................................17

2.1 Organizational Charts...............................................................................................................17

2.2 Job Description..........................................................................................................................18

Page 2Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

2.2.1 Accounting and Finance Department..................................................................................18

2.3 Internal Audit............................................................................................................................19

2.3.1 DPA (Design Person Ashore)...............................................................................................19

2.3.2 SPI (Satuan Pengawas Internal)..........................................................................................19

2.4 Comment of the Group.............................................................................................................20

3. General Activities.............................................................................................................................21

4. Chart of Account..............................................................................................................................22

4.1 Chart..........................................................................................................................................22

4.1.1 Asset (100.000 – 299.9999)................................................................................................22

4.1.2 Kewajiban (300.000 – 499.9999)........................................................................................22

4.1.3 Ekuitas (500.000 – 599.9999).............................................................................................22

4.1.4 Pendapatan (600.000 – 699.9999).....................................................................................22

4.1.5 Beban Pokok (700.000 – 799.9999)...................................................................................23

4.1.6 Beban Usaha / Overhead (800.000 – 899.9999)................................................................23

4.1.7 Pendapatan & Beban lain-lain (900.000 – 999.9999)........................................................23

4.2 Comment of the Group.............................................................................................................24

5. Revenue Cycle.................................................................................................................................25

5.1 PT Pelni Revenue Cycle Flowchart............................................................................................25

5.2 Comment of the Group.............................................................................................................26

6. Accounting Records.........................................................................................................................27

6.1 Ticket Coupon...........................................................................................................................27

6.2 Distribution of Blank Ticket......................................................................................................28

6.3 Comment of the Group.............................................................................................................31

7. Internal Control...............................................................................................................................32

7.1 Comment of the Group.............................................................................................................33

8. Database Management...................................................................................................................34

8.1 Comment of the Group.............................................................................................................35

BAB IV

Conclusion and Suggestion..................................................................................................................36

A. Conclusion...................................................................................................................................36

B. Suggestion...................................................................................................................................36

Page 3Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

Page 4Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

BAB IIntroductions

A. Background

Accounting Information System (AIS) is the whole of the related components that are cooperate together to collect,store, and disseminate data for the purpose of planning, control, coordination, analysis and decision-making which relevant outsiders and external parties. AIS is designed to make the accomplishment of the service function that seeks to provide the users with quantitative information (accounting function) possible.

AIS processes data and transactions to provide users with the information they need to plan, control, and operate their businesses. AIS can be a manual system, or a computerized system using computers. Regardless of the type, AIS is designed to collect, enter, process, store, and report data and information that can be used in the decision-making process, and perform precise control of the assets of the organization.

B. Purpose of Writing

The aim of this study is to analyze about AIS theory that we are already study and implement the aplication about AIS in a Company. The Discussion of our research that we’ve been working on including company’s Operational Activities, company’s Internal Audit, company’s Revenue Cycle, and also Internal Control contained in the Revenue Cycle.

C. Methodology

The methodology that used to accomplish this module assignment report is by :

Doing interview, survey, and observation to PT PELNI.

Study literature from text book, “Introduction to Accounting Information System by

James A. Hall” and “Accounting Information System by Marshall B. Romney and Paul

J. Steinbart”

Comparison on the result of the observation and the study literature also done to analyze

the implementation of the theories. Additionally, We also ask to the lecturers who always

give the information to us and help us along the way.

Page 5Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

D. Systematization

The format of our module assignment is as follows:

Chapter 1 : INTRODUCTION; consists of:

Background;

Purpose of Writing;

Methodology;

Systematization.

Chapter 2 : THEORIES; consists of:

Information System

Transaction Processing Models

Internal Control

Revenue Cycle

Database

Chapter 3 : ANALYSIS; consists of:

Analysis of The Implementation

Chapter 4 : CONCLUSION AND SUGGESTIONS; consists of:

Conclusion

Suggestion.

Page 6Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

BAB IITheories

1. Information System

1.1 What is Information System?

Information system is a group interrelated component that working together toward a common goal by accepting input and process output in an organized process transformation.

1.2 Information Objectives

Specific information objectives will differ from firm to firm as specific user need vary. Three fundamental objectives are, however, common to all organizations:

a. To support the stewardship function of managementb. To support management decision makingc. To support the firm’s day-to-day operation

1.3 Information System

The Information system is the set of formal procedures by which data are collected, stored, processed into information, and distributed to users.

Notice that two board classes of systems emerge from decomposition:

a. The Accounting Information System (AIS)

b. The Management Information System (MIS)

More often, MIS and AIS functions are integrated within physical systems to achieve operational efficiency.

a. The Accounting Information System

AIS subsystem process financial transactions and nonfinancial transactions that directly affect the processing of financial statement.

Page 7Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

The AIS is composed of three major subsystems:

1. The Transaction Processing System (TPS)

Which support daily business operations with numerous report, documents, and message for users throughout the organization.

2. The General Ledger / Financial Reporting System (GL / FRS)

Which produces the traditional financial statements, such as the income statement, balance sheet, statement of cash flows, tax returns, and other reports required by law.

3. The Management Reporting System (MRS)

Which provides internal management with special-purpose financial reports and information needed for decision making such as budgets, variance report, and responsibility reports.

b. The Management Information System

Management often requires information that goes beyond the capability of AIS. As organizations grow in size and complexity, specialized functional areas emerge requiring additional information for production planning and control, sales forecasting, inventory warehouse planning, market research, and so on. The MIS process nonfinancial transactions that are not normally processed by additional AIS.

Page 8Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

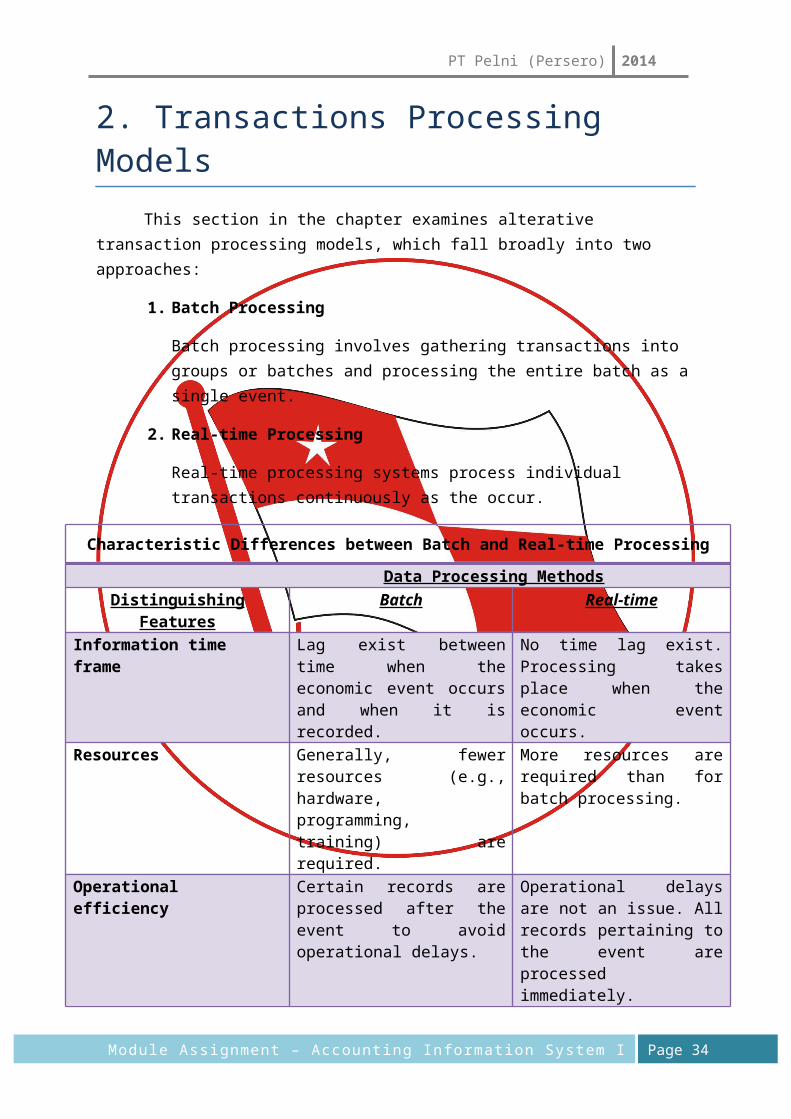

2. Transactions Processing Models

This section in the chapter examines alterative transaction processing models, which fall broadly into two approaches:

1. Batch Processing

Batch processing involves gathering transactions into groups or batches and processing the entire batch as a single event.

2. Real-time Processing

Real-time processing systems process individual transactions continuously as the occur.

Characteristic Differences between Batch and Real-time Processing

Data Processing Methods

Distinguishing Features Batch Real-time

Information time frame Lag exist between time when the economic event occurs and when it is recorded.

No time lag exist. Processing takes place when the economic event occurs.

Resources Generally, fewer resources (e.g., hardware, programming, training) are required.

More resources are required than for batch processing.

Operational efficiency Certain records are processed after the event to avoid operational delays.

Operational delays are not an issue. All records pertaining to the event are processed immediately.

Page 9Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

3. Internal Control

The internal control system comprises policies, practices, and procedures employed by the organization to achieve four board objectives:

1. To safeguard assets of the firm.2. To ensure the accuracy and reliability of accounting records and information.3. To promote efficiency in the firm’s operations.4. To measure compliance with management’s prescribed policies and

procedures.

Modifying Assumptions

Inherent in these control objectives are four modifying assumptions that guide designers and auditors of internal control.

1. Management Responsibility

This concept holds that the establishment and maintenance of a system of internal control is a management responsibility.

2. Reasonable Assurance

The internal control system should provide reasonable assurance that the four broad objectives of internal control are met in a cost-effective manner. This means that no system of internal control is perfect and the cost of achieving improved control should not outweigh its benefit.

3. Methods of Data Processing

Internal controls should achieve the four broad objectives regardless of the data processing method used. The control techniques used to achieve these objectives will, however, vary with different types of technology.

4. Limitations

Every system of internal control has limitations on its effectiveness. These include:

(1) The possibility of error – no system is perfect(2) Circumvention – personnel may circumvent the system

through collusion or other means.(3) Management override – management is subordinate to do so(4) Changing conditions – conditions may change over time and

render existing controls ineffective

Page 10Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

3.1 COSO Internal Control Framework

The phsycal control of COSO framework consist of six components:

Physical Control

This class of controls relates to the human activities employed in accounting systems. Physical controls do not relate to the computer logic that actually performs accounting tasks. Six categories physical control activities:

i. Transaction Authorization

The purpose of transaction authorization is to ensure that all material transactions processed by the information system are valid and in accordance with management’s objectives.

ii. Segregation of Duties

One of the most important control activities is the segregation of employee duties to minimize incompatible function. Segregation of duties can take many forms, depending on the specific duties to be controlled.

iii. Supervision

Implementing adequate segregation of duties requires that a firm employ a sufficiently large number of employee. Achieving adequate segregation of duties often presents difficulties for small organizations. Therefore, in small organizations or in functional areas that lack sufficiently personnel, management must compensate for the absence of segregation controls with close supervision. For this reason, supervision is often called a compensating controls.

iv. Accounting Records

The accounting records of an organization consist of sources documents, journals, and ledgers. These records capture the economic essence of transactions and provide an audit trail of economic events

v. Access Control

The purpose of access controls is to ensure that only authorized personnel have access to the firm’s assets. Unauthorized access exposes assets to misappropriation, damage, and theft.

vi. Independent Verification

Verification procedures are independent checks of the accounting system to identify errors and misrepresentations. Verification differs from supervision because it takes place after the fact, by an individual who is not directly involved with the transaction or task being verified.

Page 11Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

4. Revenue Cycle

Revenue cycle management (RCM) is the process that manages claims processing, payment and revenue generation. It entails using technology to keep track of the claims process at every point of its life, so the healthcare provider doing the billing can follow the process and address any issues, allowing for a steady stream of revenue.

The process includes keeping track of claims in the system, making sure payments are collected and addressing denied claims, which can cause up to 90 percent of missed revenue opportunity.

RCM encompasses everything from determining patient insurance eligibility and collecting co-pays to properly coding claims using ICD-10. Time management and efficiency play large elements in RCM, and a physician’s or hospital’s choice of an EMR can be largely centered around how their RCM is implemented.

4.1 Basic Technology Revenue Cycle

The computers used in these systems are independent (non-networked) PSc. Therefore, information flows between departments are communicated via hard-copy documents. In addition, in such systems, maintaining physical files of source documents is critical to the audit trail. As we walk through the various flowcharts notice that in many departments, after an individual completes his or her assigned task, documents are files a evidence that the tasks were performed.

Page 12Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

5. Database

Most modern organizations use some form of distributed processing and networking to process their transactions. Some companies process all of their transaction in this way. An important consideration in planing distributed system is the location of the organization’s database. In addressing this issue, the planner has two basic options:

1. Centralized Database

Under the centralized database approach, remote users send requests via terminals for data to the central site, which processes the requests and transmits the data back to the user. The central site, performs the functions of a file manager that services the data needs of the remote users.

2. Distributed Database

Distributed database can be distributed using either the partitioned or replicated techniques.

Partitioned Database

The partitioned database approach splits the central database into segments or partitions that are distributed to their primary users.

Replicated Database

Replicated database are effective in companies in which there exists a high degree of data sharing but no primary user. Because common data are replicated at each site, the data traffic between sites is reduced considerably. The primary justification for a replicated database is to support read-only queries. With data replicated at every site, data access for query puposed is ensured, and lockouts and delays because of network traffic are minimized. Because each site processes only its local transactions, different transactions will update the common data attributes that are replicated at each site, and thus, each site will process uniquely differentvalues after the respectives updates.

Page 13Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

BAB IIIAnalysis

1. About PT Pelni (Persero)

1.1 History of PT Pelni

The company was incorporated in 1950 under the name of Yayasan Penguasaan Pusat Kapal-kapal (PEPUSKA/Foundation of Main Authority for Ships) by legally from Surat Keputusan Bersama (SKB/Joining Letter) by the Minister of Transportation and Minister of Public Development.

During the years before 1950s, The Netherlands Government refused Indonesia's concept to convert their Ships Company by the name of N.V. K.P.M (Koninklijke Paketvaart Matschappij) into a private company. The concept also mentioned that all operational ships must using Indonesia National Flag. This idea was totally rejected by The Netherlands Government.

Onwards, the rejection does not decrease the spirit for Indonesia. In spite of, consist with 8 ships with total 4800 DWT (death weight ton), PEPUSKA story was such a success that the business was continuing and expanded. PEPUSKA ships sails together with N.V. K.P.M ships that already had experienced more than half century. That was some unfair business. N.V. K.P.M had more ships than PEPUSKA does, and also N.V. K.P.M already monopoly some business contract in shipment.

Finally, On April 28th 1952, in addition to its operation, management recognized growing opportunities in the shipment business. On that date, PEPUSKA being dismissed and Indonesia opened its first state shipment private company called PT. PELNI based on three legal letters Surat Keputusan Menteri Perhubungan (Minister of Transportation) No. M.2/1/2 dated February 28th 1952, No. A.2/1/2 dated April 19th 1952, and Berita Negara Republik Indonesia No. 50 dated June 20th 1952. PT PELNI appointed its first President Director is Mr. R. Ma'moen Soemadipraja (1952-1955)

The Company (PT. PELNI) found it difficult to compete with only 8 boats from PEPUSKA as a beginning. So, Export Import Indonesia Bank lending funds for PELNI to bought 45 coasters from Western Europe. As the company wait for those coasters arrival, PELNI rented some overseas flag ships. This procedure was taken to fulfill empty route inherit from KPM. After that one by one the rented ships was replaced by the coasters and some of them also fulfilled by the Japanese boats taken from war action.

Page 14Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

As time goes by and competition, in the late 1975 the company changed their status based on Akta Pendirian No. 31 dated October 30th, 1975 and Akte Perubahan No. 22 dated March 4th, 1998. This changing is published on Berita Negara Republik Indonesia dated April 16th, 1999 and addendum No. 2203.

1.2 Company’s Profile

PT Pelayaran Nasional Indonesia (PT.PELNI) was established by the Government on 28 April 1952 with the overall activities are controlled by the Government. However, its was recently announced two days later on 30 April 1952 by Ministry of Transportation IR. H. Junda. The establishment of PT. Pelayaran Nasional Indonesia was part of the Government's policy to manage cruise in Indonesia.

To implement government’s policy, then they opened a branch office of PT. Pelayaran Nasional Indonesia in some ports in Indonesia, including in Semarang. Semarang Branch Office was established in 1953. At the moment, 90% of the ship of PT. Pelayaran Nasional Indonesia has entered the harbor with 61 offices.

As time goes by, PT. Pelayaran Nasional Indonesia managed to obtain recognition from the International Community with a certificate of the International Safety Management Code (ISM Code) Awards, that consists of certificate DOC (Document Of Complience) for Land Management (Headquarters) or SMC (Safety Management Certificate) to KM Bukit Siguntang. The awarding was conducted on 10 July 1998 by the Directorate General of Sea Transportation.

Page 15Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

1.3 Vision and Mission

1.4 Core Values

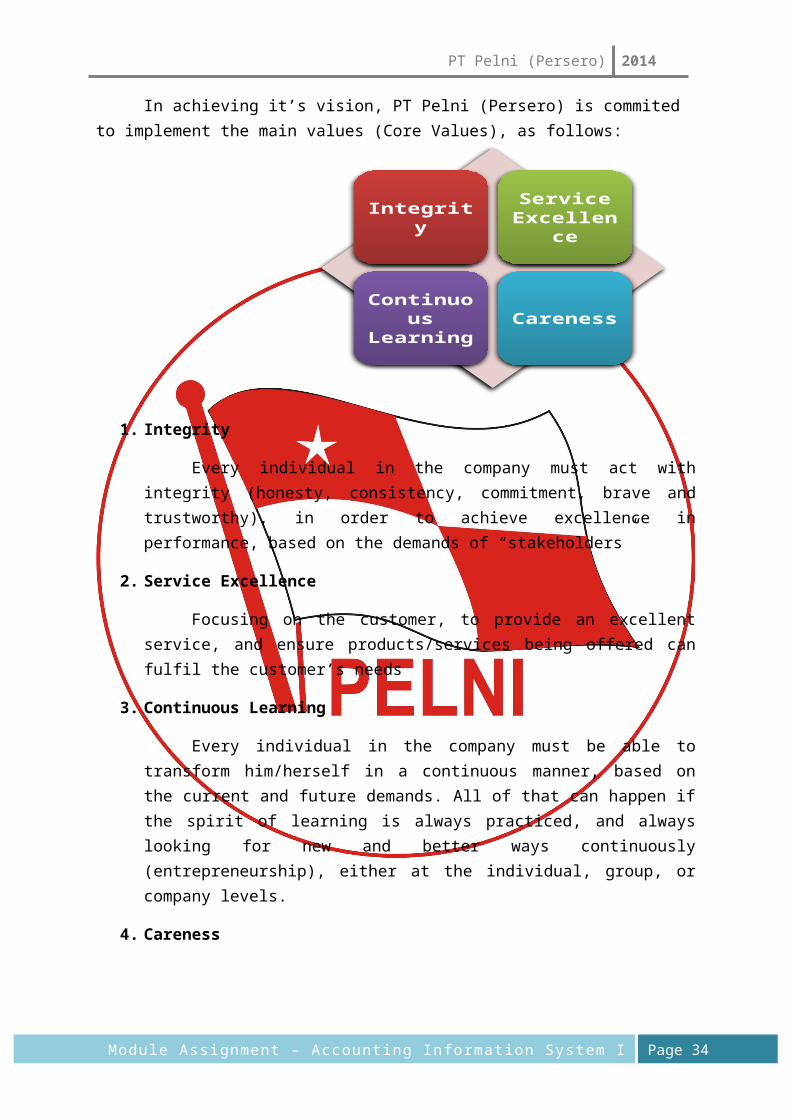

In achieving it’s vision, PT Pelni (Persero) is commited to implement the main values (Core Values), as follows:

Integrity Service Excellence

Continuous Learning Careness

Page 16Module Assignment – Accounting Information System I

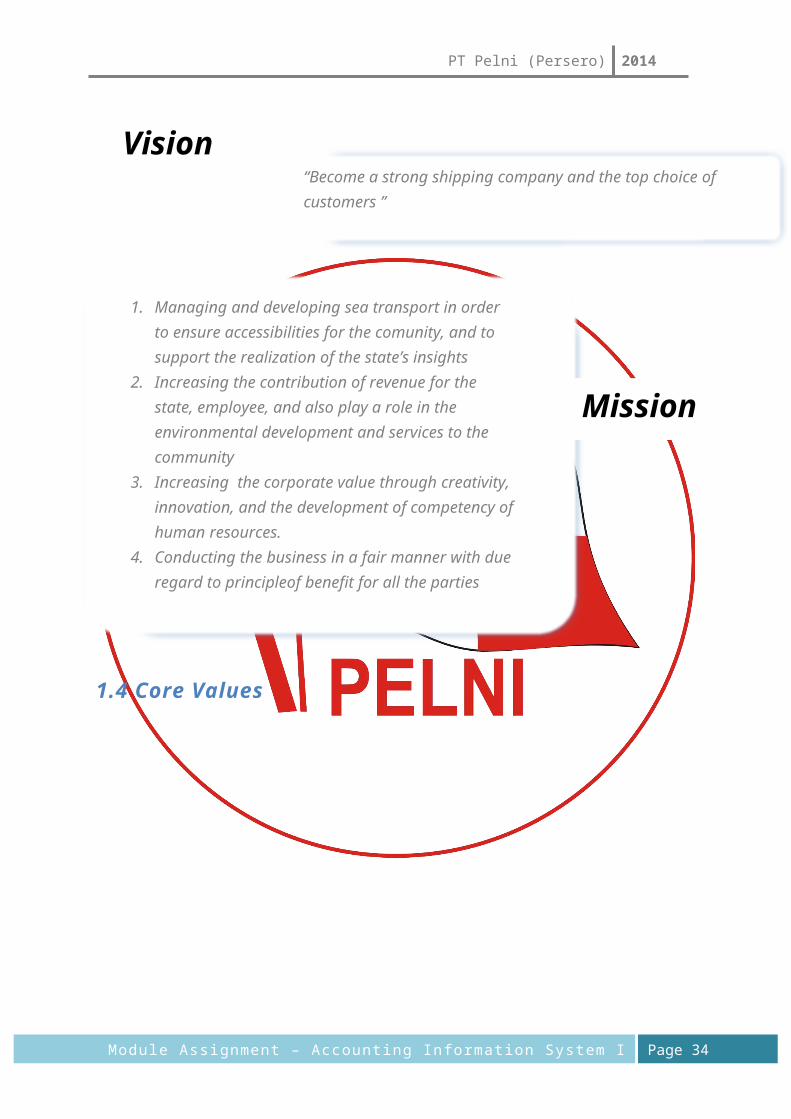

“Become a strong shipping company and the top choice of customers ”Vision

1. Managing and developing sea transport in order to ensure accessibilities for the comunity, and to support the realization of the state’s insights

2. Increasing the contribution of revenue for the state, employee, and also play a role in the environmental development and services to the community

3. Increasing the corporate value through creativity, innovation, and the development of competency of human resources.

4. Conducting the business in a fair manner with due regard to principleof benefit for all the parties involved (stakeholders), and applying the principles of Good Corporate Governance (GCG)

Mission

PT Pelni (Persero) 2014

1. Integrity

Every individual in the company must act with integrity (honesty, consistency, commitment, brave and trustworthy), in order to achieve excellence in performance, based on the demands of “stakeholders”

2. Service Excellence

Focusing on the customer, to provide an excellent service, and ensure products/services being offered can fulfil the customer’s needs

3. Continuous Learning

Every individual in the company must be able to transform him/herself in a continuous manner, based on the current and future demands. All of that can happen if the spirit of learning is always practiced, and always looking for new and better ways continuously (entrepreneurship), either at the individual, group, or company levels.

4. Careness

Maintaining the safety, security, and environmental health for the employees, partners, and customers, or the community in general.

1.5 Core Business

The company’s business activities held are:

1. Business activities in the service of cargo and passenger transport, with a network of scheduled shipping as well as shipping to cater to specific requests.

2. Business activity of shipping agency3. Business activity in terminal operation services, warehousing, rede

transportation, and expedition/forwarding. 4. Business activity in ship maintenance services and ship repair or dock business.5. Charter activities and ship brokerage6. Consulting services activities, education, training, and health care services.

In addition to carrying out commercial business, PT PELNI also carry out social mission assigned by the Government and business function, because of that PELNI decided on policy that will not only be the main field of business, which is sea transport between islands, but also developing supporting business, side businesses, and set up subsidiaries. This policy is to provide a synergy that can support each other for the future of the company

Page 17Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

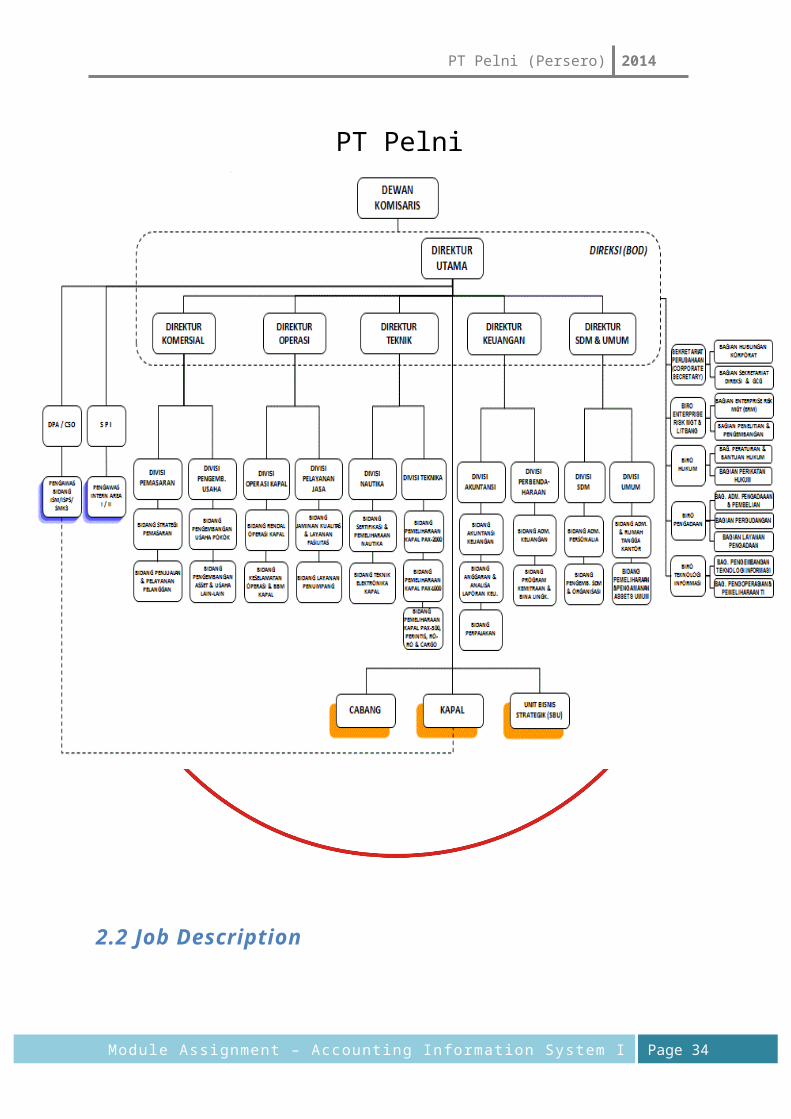

2. Company’s Structure

2.1 Organizational Charts

Page 18Module Assignment – Accounting Information System I

PT Pelni (Persero)

PT Pelni (Persero) 2014

2.2 Job Description

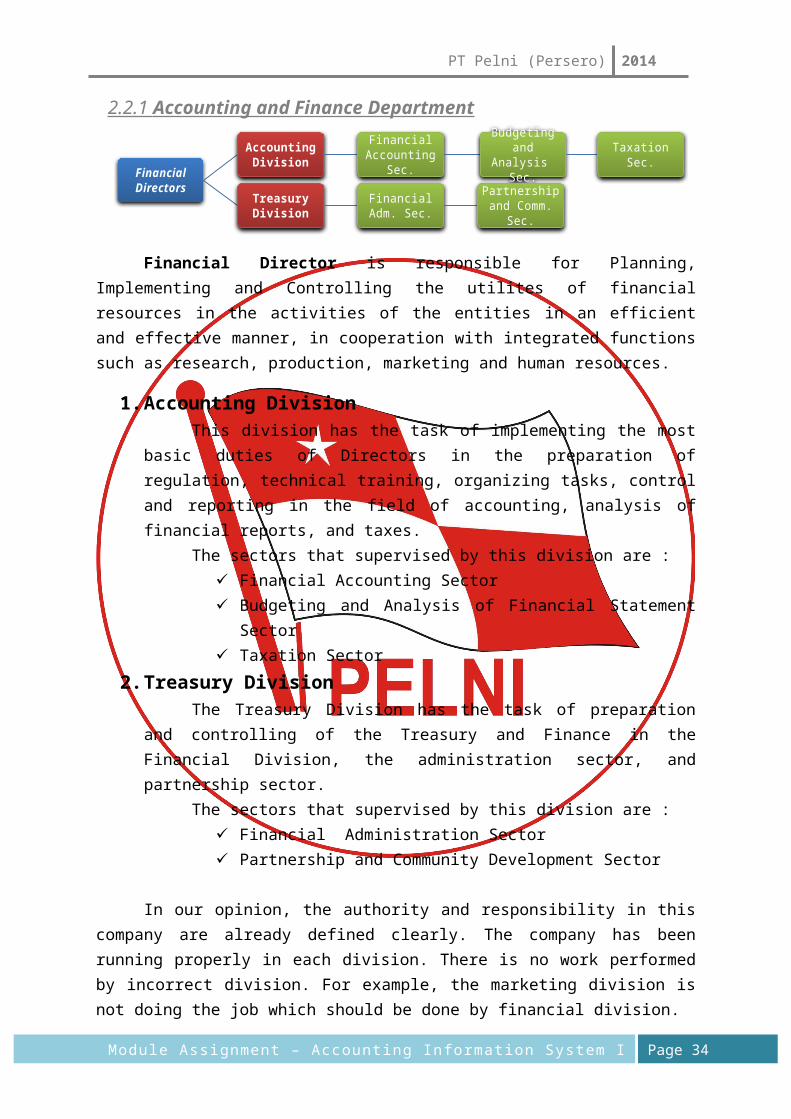

2.2.1 Accounting and Finance Department

Financial Director is responsible for Planning, Implementing and Controlling the utilites of financial resources in the activities of the entities in an efficient and effective manner, in cooperation with integrated functions such as research, production, marketing and human resources.

1. Accounting DivisionThis division has the task of implementing the most basic duties of Directors

in the preparation of regulation, technical training, organizing tasks, control and reporting in the field of accounting, analysis of financial reports, and taxes.

The sectors that supervised by this division are : Financial Accounting Sector Budgeting and Analysis of Financial Statement Sector Taxation Sector

2. Treasury DivisionThe Treasury Division has the task of preparation and controlling of the

Treasury and Finance in the Financial Division, the administration sector, and partnership sector.

The sectors that supervised by this division are : Financial Administration Sector Partnership and Community Development Sector

In our opinion, the authority and responsibility in this company are already defined clearly. The company has been running properly in each division. There is no work performed by incorrect division. For example, the marketing division is not doing the job which should be done by financial division.

Financial Directors

Accounting Division

Financial Accounting Sec.

Budgeting and Analysis Sec. Taxation Sec.

Treasury Division

Financial Adm. Sec.

Partnership and Comm. Sec.

Page 19Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

2.3 Internal Audit

2.3.1 DPA (Design Person Ashore) DPA unit is a unit or a person appointed as an independent evaluator, who is a part

of the company’s internal control structure that has a function to improve efficiency related to the supervision of verification, safety, security, and prevention of pollution in accordance to ISM-Code.

DPA/CSO/K3 Unit is in charge to assist the management in carrying out their duties, and to provide assistance in the form of assessment, analysis, recommendation, consultation, and information, as well as support regarding activities reviewed related to other units, through the company’s leadership, in accordance to SOLAS (ISM-Code) Audit Standard, and the Government’s Regulation of the Republic of Indonesia No. 50 Year 2012 regarding the implementation of SMK3, as well as ethical professional behavior. This responsibilities also covers the implementation of audit coordination carried out by external auditor, in order for the aim of the audit of all parties are achieved in parallel to the company’s objective (DOC and SMS certification).

2.3.1.1 Functions of DPA

DPA is responsible for the execution and maintenance of the company’s Safety Management System (SMS). The aim for this appointment is to ensure the safety of ship operations, and in this matter to connect the company to those on board the ship.

2.3.2 SPI (Satuan Pengawas Internal) Internal auditors (Internal Control Unit / SPI) is the company’s internal regulatory

authorities, led by a chief who is appointed and is responsible to the President Director. Internal Control Unit has a function in the operation of theinternal control activities and providing constructive suggestionsabout implementation of corporate transaction in order for the implementation of company’s activities can be conducted in. Accordance to the regulation in force, so that the company’s performance can be achieved according to plan.

2.3.2.1 Functions of SPI

1. Assist the President Director in carrying out inspection of the State Owned Enterprise’s operations and finances; assess control, management and implementation to the SOE as well as providing suggestions for improvement.

2. Provide information or inspection result of the implementation of internal auditor duties as referred to point a to the President Director with a copy to the Audit Commitiee.

3. Create and implement the Annual Internal Audit Plan

Page 20Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

4. Test and evaluate the implemention of internal control in accordance with the company’s policy.

5. Perform inspetion and assessment of the effi ciency and effectiveness in the finance, accounting, operations, human resources, marketing, information technology, and other activities.

6. Suggest improvement and objective information regarding the activities inspected at all levels of management.

7. Create audit report and submit the report to the President Director and BOC.

8. Monitor, analyze and report on implementation of the improvements that have been suggested.

9. Cooperate with Audit Commitee.

10. Create a program to evaluate the quality of the audit activity.

11. Conduct a special inspection if necessary.

2.4 Comment of the Group

In the structure organization shown on previous chapter, position of Internal Audit is placed directly under the Board of Directors. This is a wise decision by PT Pelni because the Internal Audit can’t be interverted by other departments. Internal Audit in PT Pelni has the authority to access all of information from every division. It should report the inspection results to the Boards of Directors.

DPA is an internal audit besides SPI. DPA is an Internal Audit who only oversee the ships. DPA will check whether the ship’s condition according to standard established by BKI (Biro Klasifikasi Indonesia. If there is damage occurred in the ship, DPA will provide reports about the damage of the ship. In the Organization Structure, DPA is also placed directly under the Board of Directors. So the DPA can report all the results of the ship inspection. DPA can also give an advice to the Board of Directors about the feasibility or standards that must be prepared to qualify from BKI.

Overall, the internal audit in PT Pelni is very good. PT Pelni has two internal audits. Not only for auditing in PT Pelni company, but also there is also auditing for the feasibility of the ship. Internal Audit position has also been very nice, because it is directly under the Board of Directors.

Page 21Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

3. General Activities

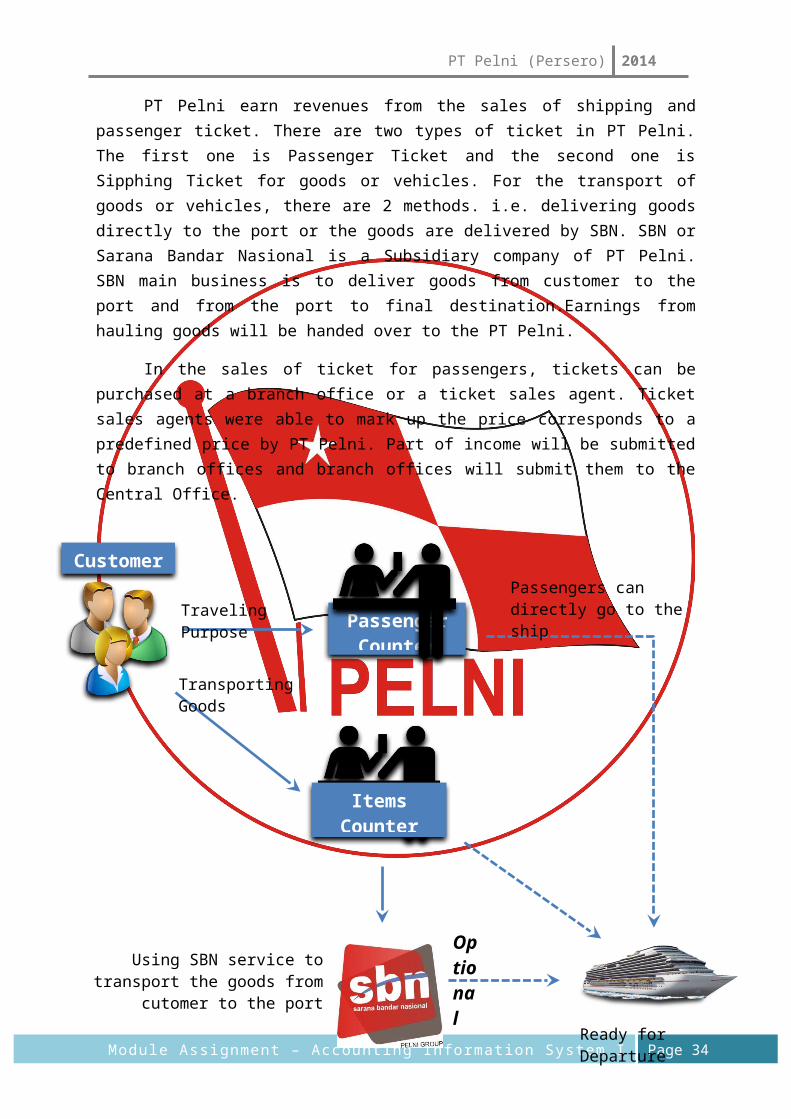

PT Pelni earn revenues from the sales of shipping and passenger ticket. There are two types of ticket in PT Pelni. The first one is Passenger Ticket and the second one is Sipphing Ticket for goods or vehicles. For the transport of goods or vehicles, there are 2 methods. i.e. delivering goods directly to the port or the goods are delivered by SBN. SBN or Sarana Bandar Nasional is a Subsidiary company of PT Pelni. SBN main business is to deliver goods from customer to the port and from the port to final destination.Earnings from hauling goods will be handed over to the PT Pelni.

In the sales of ticket for passengers, tickets can be purchased at a branch office or a ticket sales agent. Ticket sales agents were able to mark up the price corresponds to a predefined price by PT Pelni. Part of income will be submitted to branch offices and branch offices will submit them to the Central Office.

Page 22Module Assignment – Accounting Information System I

Passenger Counter

ItemsCounter

Traveling Purpose

Using SBN service to transport the goods from cutomer to the port

Passengers can directly go to the ship

Ready for Departure

Customer

Optional

Transporting Goods

PT Pelni (Persero) 2014

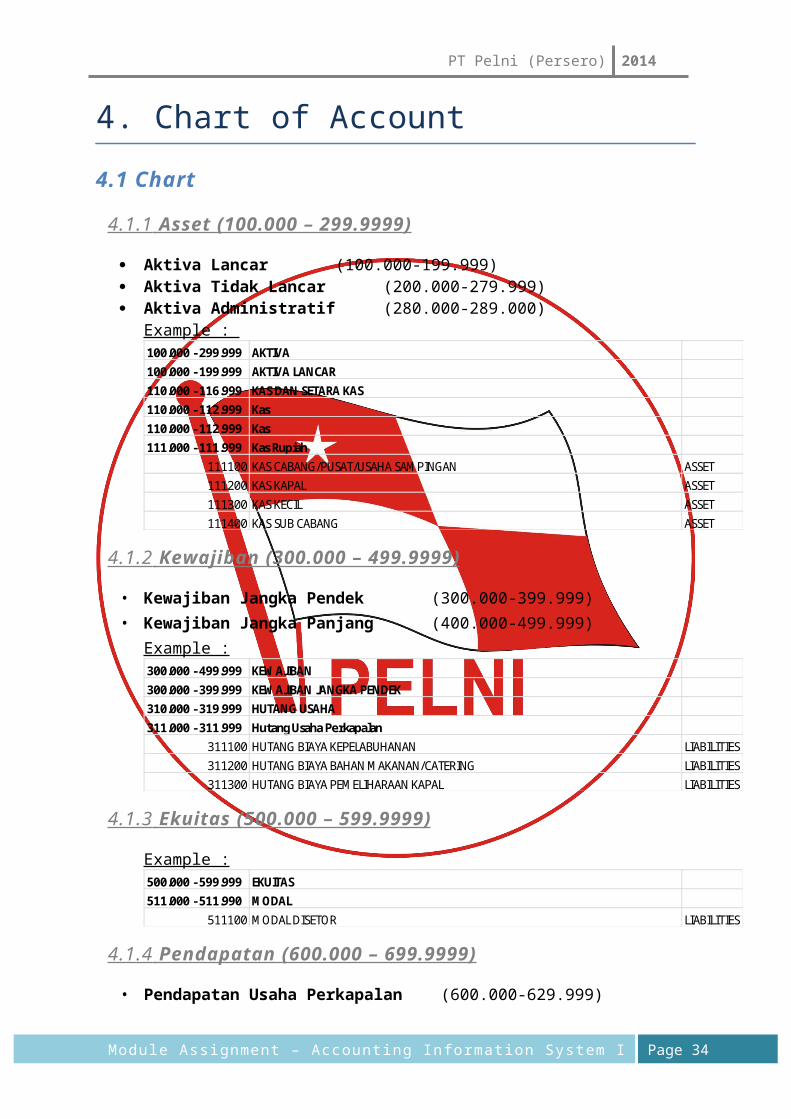

4. Chart of Account

4.1 Chart

4.1.1 Asset (100.000 – 299.9999)

Aktiva Lancar (100.000-199.999) Aktiva Tidak Lancar (200.000-279.999) Aktiva Administratif (280.000-289.000)

Example : 100.000 - 299.999 AKTIVA100.000 - 199.999 AKTIVA LANCAR110.000 - 116.999 KAS DAN SETARA KAS110.000 - 112.999 Kas110.000 - 112.999 Kas111.000 - 111.999 Kas Rupiah

111100 KAS CABANG/PUSAT/USAHA SAMPINGAN ASSET111200 KAS KAPAL ASSET111300 KAS KECIL ASSET111400 KAS SUB CABANG ASSET

4.1.2 Kewajiban (300.000 – 499.9999)

• Kewajiban Jangka Pendek (300.000-399.999)• Kewajiban Jangka Panjang (400.000-499.999)

Example :300.000 - 499.999 KEWAJIBAN300.000 - 399.999 KEWAJIBAN JANGKA PENDEK310.000 - 319.999 HUTANG USAHA311.000 - 311.999 Hutang Usaha Perkapalan

311100 HUTANG BIAYA KEPELABUHANAN LIABILITIES311200 HUTANG BIAYA BAHAN MAKANAN/CATERING LIABILITIES311300 HUTANG BIAYA PEMELIHARAAN KAPAL LIABILITIES

4.1.3 Ekuitas (500.000 – 599.9999)

Example :500.000 - 599.999 EKUITAS511.000 - 511.990 MODAL

511100 MODAL DISETOR LIABILITIES

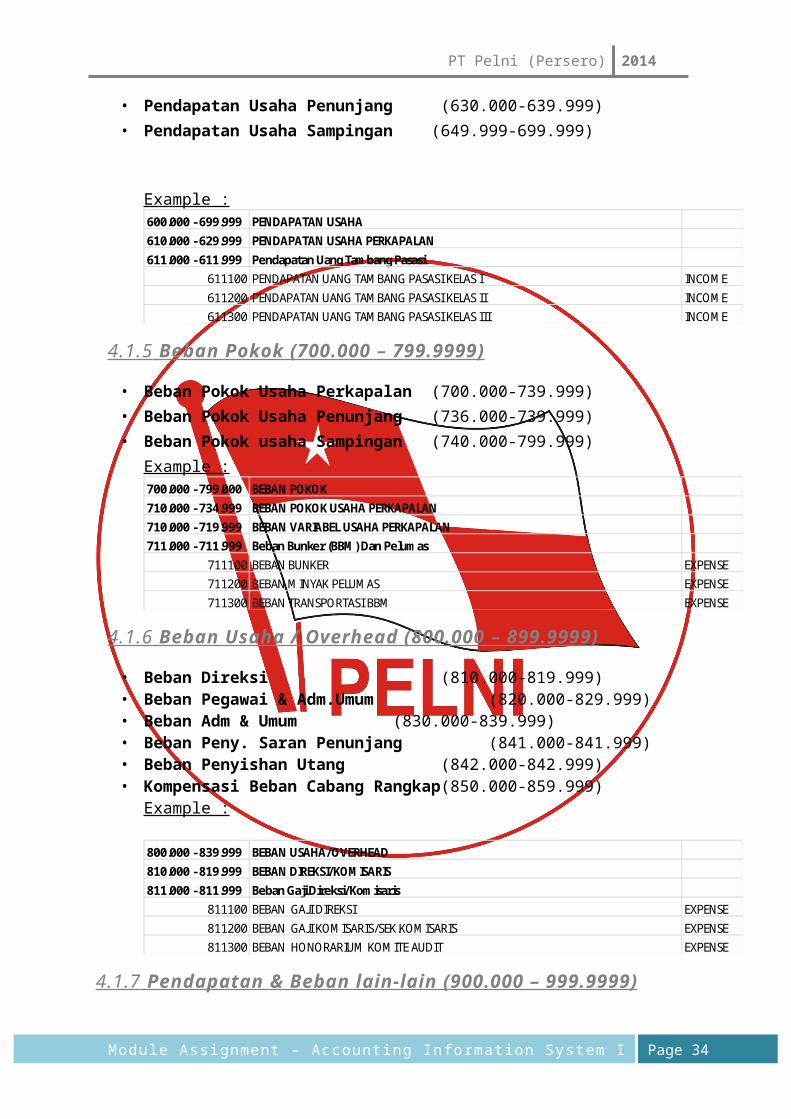

4.1.4 Pendapatan (600.000 – 699.9999)

• Pendapatan Usaha Perkapalan (600.000-629.999)• Pendapatan Usaha Penunjang (630.000-639.999)• Pendapatan Usaha Sampingan (649.999-699.999)

Page 23Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

Example :600.000 - 699.999 PENDAPATAN USAHA610.000 - 629.999 PENDAPATAN USAHA PERKAPALAN611.000 - 611.999 Pendapatan Uang Tambang Pasasi

611100 PENDAPATAN UANG TAMBANG PASASI KELAS I INCOME611200 PENDAPATAN UANG TAMBANG PASASI KELAS II INCOME611300 PENDAPATAN UANG TAMBANG PASASI KELAS III INCOME

4.1.5 Beban Pokok (700.000 – 799.9999)

• Beban Pokok Usaha Perkapalan (700.000-739.999)• Beban Pokok Usaha Penunjang (736.000-739.999)• Beban Pokok usaha Sampingan (740.000-799.999)

Example :700.000 - 799.000 BEBAN POKOK710.000 - 734.999 BEBAN POKOK USAHA PERKAPALAN710.000 - 719.999 BEBAN VARIABEL USAHA PERKAPALAN711.000 - 711.999 Beban Bunker (BBM) Dan Pelumas

711100 BEBAN BUNKER EXPENSE711200 BEBAN MINYAK PELUMAS EXPENSE711300 BEBAN TRANSPORTASI BBM EXPENSE

4.1.6 Beban Usaha / Overhead (800.000 – 899.9999)

• Beban Direksi (810.000-819.999)• Beban Pegawai & Adm.Umum (820.000-829.999)• Beban Adm & Umum (830.000-839.999)• Beban Peny. Saran Penunjang (841.000-841.999)• Beban Penyishan Utang (842.000-842.999)• Kompensasi Beban Cabang Rangkap(850.000-859.999)

Example :

800.000 - 839.999 BEBAN USAHA/OVERHEAD810.000 - 819.999 BEBAN DIREKSI/KOMISARIS811.000 - 811.999 Beban Gaji Direksi/Komisaris

811100 BEBAN GAJI DIREKSI EXPENSE811200 BEBAN GAJI KOMISARIS/SEK.KOMISARIS EXPENSE811300 BEBAN HONORARIUM KOMITE AUDIT EXPENSE

4.1.7 Pendapatan & Beban lain-lain (900.000 – 999.9999)

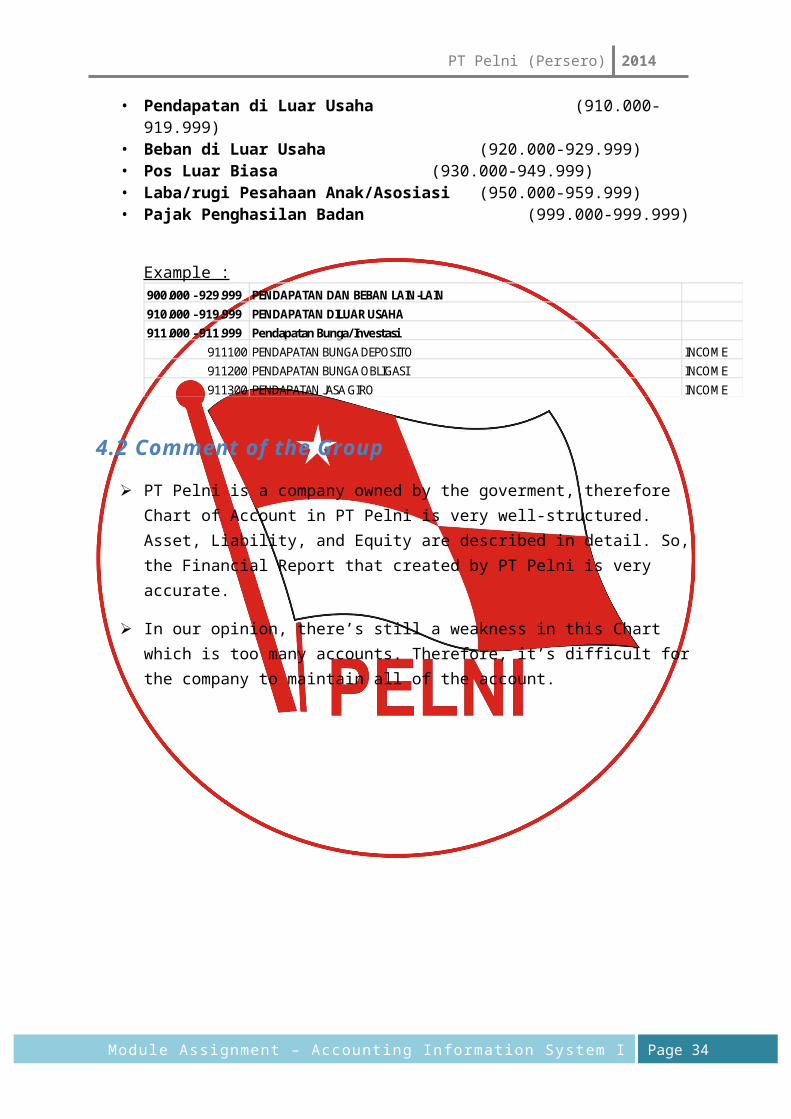

• Pendapatan di Luar Usaha (910.000-919.999)• Beban di Luar Usaha (920.000-929.999)• Pos Luar Biasa (930.000-949.999)• Laba/rugi Pesahaan Anak/Asosiasi (950.000-959.999)• Pajak Penghasilan Badan (999.000-999.999)

Page 24Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

Example :900.000 - 929.999 PENDAPATAN DAN BEBAN LAIN-LAIN910.000 - 919.999 PENDAPATAN DILUAR USAHA911.000 - 911.999 Pendapatan Bunga/Investasi

911100 PENDAPATAN BUNGA DEPOSITO INCOME911200 PENDAPATAN BUNGA OBLIGASI INCOME911300 PENDAPATAN JASA GIRO INCOME

4.2 Comment of the Group

PT Pelni is a company owned by the goverment, therefore Chart of Account in PT Pelni is very well-structured. Asset, Liability, and Equity are described in detail. So, the Financial Report that created by PT Pelni is very accurate.

In our opinion, there’s still a weakness in this Chart which is too many accounts. Therefore, it’s difficult for the company to maintain all of the account.

Page 25Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

5. Revenue Cycle

5.1 PT Pelni Revenue Cycle Flowchart

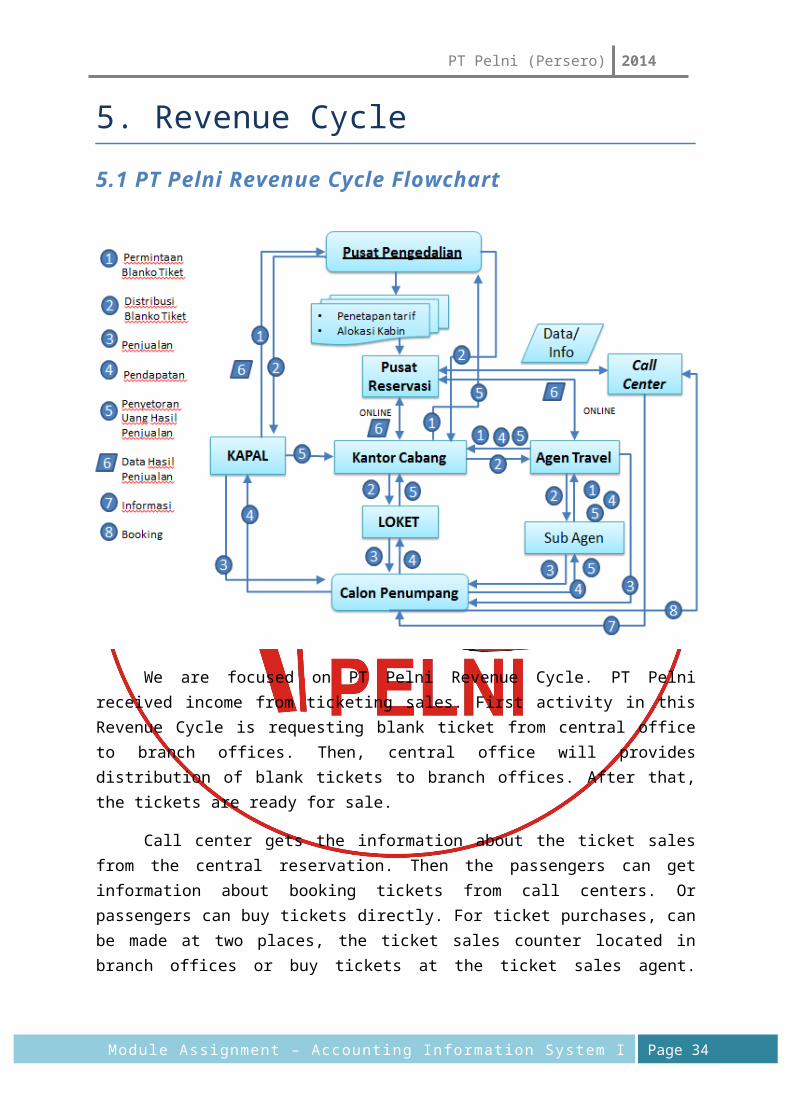

We are focused on PT Pelni Revenue Cycle. PT Pelni received income from ticketing sales. First activity in this Revenue Cycle is requesting blank ticket from central office to branch offices. Then, central office will provides distribution of blank tickets to branch offices. After that, the tickets are ready for sale.

Call center gets the information about the ticket sales from the central reservation. Then the passengers can get information about booking tickets from call centers. Or passengers can buy tickets directly. For ticket purchases, can be made at two places, the ticket sales counter located in branch offices or buy tickets at the ticket sales agent. Ticket sales agents were able to mark up the price according to a predefined price by PT Pelni.

Sales data will be sent by the agent ticket sales and branch offices to a central reservation through the online system.

Page 26Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

All revenues will be deposited to the Central Office. Revenues from agency branches will be deposited to the Branch Office. And revenue from the Branch Office will be deposited directly to the Central Office through the transfer to the bank.

In certain situations, PT Pelni can sell tickets on board. For example, when the ship will departed from Papua, passengers are too much so it's hard to be controled, there is even a passenger climbs aboard the Ship to come off. When there's a ticket inspection, for passengers who did not have tickets can buy tickets on board. Data from the results of ticket sales on the ship will be sent directly to the Central Office.

5.2 Comment of the Group

Based on theory of revenue cycle that we've learned, the revenue cycle in PT Pelni is not same as the existing theories in the James Hall’s Book. It is because the theory in the book is the Retail Company, while PT Pelni is a Service Company.

Alhough the theory is different than we’ve learned, PT Pelni Revenue Cycle flowchart is very communicative. Just by looking at the flowchart, we can instantly understand wherever the direction from this flowchart. The flowchart is also very simple and easy to understand.

However, this flowchart also has weakness. It is not clearly explained who makes the documents, where the documents will be delivered, and how many copies of document will be distributed. A flow about document controls are built in another flowchart. Flowchart about document control has to be made along with flowchart of Revenue Cycle.

In the revenue cycle in PT Pelni, we conclude the passengers can buy tickets through 3 ways. The direct purchase in the counters at branch offices, by ticketing agency, and on board. All revenues are directly assigned to branch offices, while the central office or central control received no Cash at all. Central Office only accepts the documents of sales going on.

Page 27Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

6. Accounting Records

6.1 Tickets Coupon

1. Audit Coupon

2. Agent Coupon

3. Ship Coupon

4. Passenger Coupon

5. Meal Control

Page 28Module Assignment – Accounting Information System I

PT Pelni has 4 coupons that will be directly distributed to each department as evidence and for the recording of each department.

Audit Coupon is the first Coupon. Audit coupon will be recorded in the Branch Office and will be given to the Central Office.

The second coupon is Agent Coupon. Agent Coupon is a coupon that will be retained by the Travel Agency.

The third coupon is Ship Coupon. Ship Coupon is a coupon that will be saved to the shipping section.

And the last coupon is Passenger Coupon. Passenger Coupon will be saved by the passenger, coupon will be used as evidence or sign of entry to the ship. There is a record in the passenger coupon for a meal, so passengers will not get double the food, because if it is eaten is recorded.

This is a listing of meals passengers, each passenger already taking food, will be given a tick, as a sign that the passenger had taken his food.

PT Pelni (Persero) 2014

6.2 Distribution of Blank Ticket

1. Blank Ticket request from Branch Office to Central Office

Ticket distribution begins with blank ticket request from Branch Office to Central Office. Branch Office sends the request document as shown above. When the ticket stock in the Branch Office reach reorder point, Branch Office will send the information about how much the ticket stock left, and how many tickets needed for sales order process.

Because the sales order only available in Branch Office, so the Blank Ticket Request is important. If the ticket has been sold out, then sales ticket process will be disturbed and might cause loss for company.

There are some important things in this document:

1. Type of Ticket

2. Stock left

3. The amount of Blank Ticket requested

Page 29Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

2. Sending the Blank Ticket to Branch Office

After the Central Office receive the Blank Ticket request from Branch Office, Central Office will prepare the Blank Ticket requested from Branch Office. Central Office will only send the Blank Ticket to the Branch Office based on information given by Branch Office. And the, Central Office will send the Blank Ticket with the documents that contains information about how many Blank Ticket has been sent.

The document contains information about Type of Ticket, Serial Number, and the amount. It also contains signature of the Head of Finance and the person who receive the Blank Ticket.

This is the implementation of a good Independent Verification. The Accounting Record is also very good because the Blank Ticket has been sent by a very accurate information.

Page 30Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

3. Blank Ticket Request from Travel Agent and Ship

Other than Blank Ticket request from Branch Office, Travel Agent is also requesting Blank Ticket. Ticket purchasing in PT Pelni is not only available in counter, but also can be purchased in Travel Agent.

Travel Agent is requesting the Blank Ticket from Branch Office based on their needs. Other than Branch Office and Travel Agent, Central Office is also received Blank Ticket request from the ship. Ticket selling from the ship is only happened is certai situation, e.g. if there are some illegal passangers, the ticket will be sold to them. The ship clerk will send the ticket selling data to Central Office.

Blank Ticket requesting from Travel Agent and ship basically are same as blank ticket requesting from Branch Office. The difference is only from signature or authorization. For the Blank Ticket request from Travel Agent , the document will be signed by agency. While, Blank Ticket request from the ship will be signed by ship clerk.

4. Sending the Blank Ticket to Travel Agent and Ship

Blank Ticket Sending format from Central Office to Travel Agent, ship, and Branch Office are having a similar format. This document contains type of ticket, serial number and amount of ticket that will be sent. All of the data are sent according to request information received.

The document is also signed by the Head of Finance. He will also verified the accuracy and completeness of documents.

Page 31Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

6.3 Comment of the Group

Pelni has 4 coupons in the ticket. Each coupon will be recorded in each Division. The recording system in PT Pelni was very good because each Division has its own records so the errors that occur in each Division was very rare. Pelni tickets also have a serial number and a hologram, so counterfeiting the ticket will be hard to do. Pelni also has The Pelni Stamp at a back of all coupon.

Internal Control in requesting and deliverying Blank Ticket works very well and conveniently because these documents were authorized by each department manager, e.g. Branch Ticket manager, Traveling Agent manager, Central manager, and Ship manager.

Overall, Accounting Record in PT Pelni is being conducted well. Fraudulents that occur in PT Pelni could be handled properly because there are authorization, independent verification, and access control. Every document is signed by the person who in charge, e.g. Head of Finance, Branch Office Manager, Ship Captain, and Blank Ticket receiver.

Page 32Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

7. Internal Control

• Transaction Authorization

On distributing ticket to the Branch Offices, Central Office of PT Pelni will receive a Blank Form filled with the amount-of-ticket requested by the branches, which then will be authorized by Head of Finance. Authorization in this process aims to control and ensure that only company’s official branches received ticket which has been dealt before. Through this transaction authorization process, company could reconcile amount of revenue they have earned.

• Segregation of Duties

PT Pelni forms 2 (two) Internal Auditor, they are Designed Person Ashored (DPA) and Satuan Pengawasan Internal (SPI). They are the example of Segregation of Duties within PT Pelni. DPA is an Internal Auditor whose responsible to check and monitor maintenance of PT Pelni’s ships to get an eligibility license to sailing from Badan Kelayakan Indonesia (BKI). On the otherhand, SPI responsible in auditing company’s internal both in financial and non-financial activity.

• Supervision

The supervision in PT Pelni is done by the manager. Each department has a different manager whose responsible in supervise every individual within the company. Manager responsible in monitoring whether each department has done their duties conveniently.

One of the technology which supports Supervision is CCTV. CCTV system is applied within the ship to make sure that only certain people allowed to entering the ship. This CCTV is also aimed to know whether the people on board are legal passenger who paid the ticket, not intruder.

• Accounting Records

PT Pelni has 4 copy of transaction records, consist of Audit Coupon, Agent Coupon, Ship Coupon, and Passenger Coupon.

o The Audit Coupon will be sent to Accounting Division in Central Office, with this Audit Coupon, the employee will input the data of sales to the software system of bill of lading.

o Agent Coupon will be given to Travel Agent, if only the ticket was purchased through Travel Agent.

Page 33Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

o Ship Coupon will be clinged by customer to be checked when they’re going to aboard

• Access Control

There is limitation on accessing the databse system in PT Pelni. Only limited people have the access to database system.

The employee attendance system of PT Pelni is Fingerprint System. This system is customized and intend to control the employee’s attendance.

The ships of PT Pelni only have 2 (two) main doors that built in purpose to restrict and control the passengers that will go aboard.

• Independent Verification

There’s a National Classification Board (Badan Klasifikasi Nasional), independent and responsible in classifying Indonesian commercial ships, which regularly operated in Indonesia’s Ocean Territory or commonly known as Badan Klasifikasi Indonesia (BKI). BKI determine whether PT Pelni and other Indonesian Ships are able to operate.

7.1 Comment of the Group

PT Pelni has Internal Control that similiar with COSO theory. The theory consist of transaction authorization, segregation of duties, supervision, accounting records, access control, and independent verification. Because the Internal Control is similiar with COSO theory, therefore it will be a positive impact for the company.

It also will reduce the fraudlent done by other irresponsible parties. The better company’s Internal Control, the greater company’s performance. Therefore, it will impact to company’s future prospect.

Page 34Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

8. Database Management

PT Pelni is using Oracle software on every system. The storagement of all existing data is using Centralized Database.This Database only exist in the Central Office. Every branch Office throughout Indonesia can access and enter data into the Central Server and input the data to the Central Office via Internet. All data will be stored in the Database. PT Pelni has established cooperation with PT Telkom Indonesia to customize a specific network only for PT Pelni.

PT Pelni has an independent VPN (Virtual Private Protocol), that built for accesing-data purpose. Only the employee could access the system which located in Central Office. The operation process of VPN is like a global-scale Wi-fi. Leakage and theft of data that may occur, could be avoided because PT Pelni has its own firewall to protect data. Firewall will identify if there is an unrecognized IP accessing data of PT Pelni.

PT Pelni is using real-time for its data recording system. When transaction of ticket-selling occurs, the transaction will then be recorded and the data will be directly given to the Central Office.

Page 35Module Assignment – Accounting Information System I

Oracle( Data Master )

Finance System Sales System etc

Centralized

PT Pelni (Persero) 2014

8.1 Comment of the Group

A database management system that has been used by PT Pelni is pretty good. They are using a Centralized-System for data input from various branches throughout Indonesia. The data is not accumulated in any particular branch, but directly inputted to the Central Server at the time when transaction occurs.

In our opinion, a management system like this is a good decision because the accumulation data in one place would not happen. The implementation of Real-Time System in data inputting will also reduce the risk of fraud. Manipulation of data could happened if the company use Batch System to input data.

On its implementation, real-time system could also shorten the time in making the Financial Statements Report. Data which is needed to prepare the Financial Statement has already available at that time. Another impact on implementing Real-Time System is time efficiency.

Page 36Module Assignment – Accounting Information System I

PT Pelni (Persero) 2014

BAB IVConclusion and Suggestion

A. Conclusion

As we have explained above, we conclude PT Pelni has already implementing a good Internal Control. Segregation of Duties, Supervision, Accounting Record and other Internal Control can be implemented according its functions. Internal Control that PT Pelni has implemented can help them to oversee the business process and give a positive impact to PT Pelni.

For Internal Audit, we conclude PT Pelni has two Independent Internal Audit which is good for company’s auditing. They segregate this Internal Audit because it makes the auditing more accurate and effective.

Although the Revenue Cycle in PT Pelni is different from theory that we’ve learned in James Hall and Romney, the flowchart is already defined quite cleary, easy to understand, and very comunicative. Eventhough, it is not clearly explained where the documents will be delivered, how the delivering process, and by whom the documents will be sent.

B. Suggestion

PT Pelni has a weakness on its payment ticket system, which still use manual-system. The risk of fraudulent that might happen is quite high. All transaction record and the cash revenue will be collected in Branch Office to be sent to Central Office every month. This system could cause theft of cash or inaccurate data recording. Moreover, Pelni’s ticket also sold by Pander. This may cause inflict a financial loss for the company. Therefore, to overcome things that may harm the company, PT Pelni is planning to using online-system to all of its business transaction to reduce risk. The online-payment system will make payment system more efficient, systemized, and simple.

We suggest PT Pelni has to tighten the supervision in the Ship. So there are no passengers who come aboard ilegally.

Pelni’s ticket should not have much coupon. They should change the couponing system to one-ticket system. Beside to reduce cost, it is also simpler.

Page 37Module Assignment – Accounting Information System I