Community Services Block Grant Administrative Expenses

41

February 2012 Prepared by Erwin de Leon Sarah Pettijohn Carol J. De Vita Urban Institute Fe Fe Fe Fe Fe Fe Fe Fe Fe Fe F b b br br br br br br b ua u u u u u u u u u ry r r r r 2012 Community Services Block Grant Administrative Expenses

Transcript of Community Services Block Grant Administrative Expenses

February 2012

Prepared by

Erwin de LeonSarah PettijohnCarol J. De VitaUrban Institute

FeFeFeFeFeFeFeFeFeFeF bbbrbrbrbrbrbrb uauuuuuuuuu ryrrrr 2012

Community ServicesBlock GrantAdministrativeExpenses

Prepared by

Erwin de Leon

Sarah Pettijohn

Carol J. De Vita

Urban Institute

February 28, 2012

This publication was created by the Urban Institute in the performance of the U.S. Department of Health and Human

Services, Administration for Children and Families, Office of Community Services, Community Services Block

Grant contract number HHSP23320095654WC. Any opinion, findings, and conclusions, or recommendations

expressed in this material are those of the author(s) and do not necessarily reflect the views of the U.S. Department

of Health and Human Services, Administration for Children and Families, Office of Community Services, or of the

Urban Institute, its trustees, or its sponsors.

ii

CONTENTS

Executive Summary ...................................................................................................................................... iii

Accountability and Administrative Expenses ................................................................................................ 1

Definitions of Administrative Expenses ........................................................................................................ 2

Administrative Expenses as a Proxy for Efficiency ........................................................................................ 4

Efforts to Assess Nonprofits by Their Administrative Expenses ............................................................... 5

HHS Administrative Efficiency Measures for CSBG ................................................................................... 6

Strengths and Limitations of Financial Ratios ........................................................................................... 6

Implications for Organizational Capacity .................................................................................................. 8

State CSBG Administrative Expenses ............................................................................................................ 9

CSBG Eligible Entities’ Administrative Expenses ......................................................................................... 12

Types of Expenses Allocated to Administration ..................................................................................... 12

Staff time ............................................................................................................................................. 12

Other types of administrative expenses ............................................................................................. 13

Use of CSBG Funds .................................................................................................................................. 14

Perspectives on Allocating Administrative Expenses .............................................................................. 16

Comparisons of CAAs and Other Nonprofits .............................................................................................. 17

Administrative Expenses of CAAs and Comparable Nonprofits .............................................................. 19

Findings ................................................................................................................................................... 20

Conclusions ................................................................................................................................................. 21

Technical Notes ........................................................................................................................................... 24

References .................................................................................................................................................. 25

Appendix A: CSBG Administrative Expenditures by State, FY 2008 ............................................................ 27

Appendix B: Methodology for the Phone Interviews ................................................................................. 29

Appendix C: Methodology for the Regression Analysis .............................................................................. 31

iii

EXECUTIVE SUMMARY

All funders—both government and private donors—want to know that their funds are being used

for the purposes intended and are being spent efficiently and effectively. This is especially true

when resources are constrained. To learn more about administrative expenses and financial

efficiency measures, the Office of Community Services, Administration for Children and

Families, Department of Health and Human Services (OCS/ACF/HHS) commissioned the Urban

Institute to review literature on measuring administrative expenses and analyze the

administrative expenses associated with the Community Services Block Grant (CSBG).

The study addressed five research questions:

1. How are administrative costs defined by Federal government entities, particularly for

CSBG?

2. What percentage of State CSBG funds is spent on administrative expenditures?

3. What types of guidance do States receive in reporting CSBG administrative costs?

4. How do the administrative expenditures of CSBG-eligible entities (specifically

Community Action Agencies, or CAAs) compare to those of similar nonprofit

organizations?

5. How have administrative expenditures been used to assess the performance of nonprofit

organizations, including the strengths and limitations of these approaches?

Key Findings

Many definitions and guidelines relate to administrative expenses Administrative costs are generally defined as expenditures incurred by a nonprofit organization

to support its stated mission or purpose; they are associated with the organization’s overall

functions and management. These are often defined along three functional categories:

administrative, program, and fundraising.

There are multiple layers of guidance for reporting administrative expenses. For example, the

Financial Accounting Standards Board (FASB) establishes standards of financial accounting that

govern the preparation of financial reports by nongovernmental entities. In addition, individual

agencies issue guidelines specific to particular government programs or reporting forms. The

iv

Internal Revenue Service (IRS), for example, uses the same functional categories as FASB but

adds instructions for completing the Form 990—a financial reporting form that nonprofits file

annually with the IRS. Similarly, the Office of Management and Budget (OMB) issued Circular

A-122 in 1980, with subsequent updates, that set principles for determining costs of grants,

contracts, and other agreements with nonprofit organizations. The Office of Community Services

issued an Information Memorandum (IM 37) in 1999 to help CSBG grantees better understand

how to report their CSBG expenditures in programmatic reports required under the CSBG

legislation.

Interviews with CAA financial officials indicate that guidelines regarding CSBG administrative

expenses are complex and sometimes conflict with other directives. For example, some expenses

can be seen as both administrative and programmatic, depending on the regulatory authority

issuing the guidance and the purpose of the report being completed. IM 37 provides

administrative and programmatic definitions that sometimes differ from those identified under

OMB Circular A-122. Grantees must reconcile these differences.

State spending on CSBG administrative expenditures is restricted By law, States may spend no more than $55,000 or 5 percent of their CSBG grant on

administrative expenses (CSBG Act, Sec. 675C(b)(2)). The legislation also provides States the

authority to expend allocated funds within a 24-month time frame. Consequently, administrative

expenditures reported by a State over a one-year period may exceed the 5 percent threshold

because of the carryover of funds from the previous fiscal year.

In FY 2008, States’ CSBG administrative expenses ranged from 0.87 percent (South Dakota) to

6.61 percent (Alabama) of their total CSBG expenditures. Four States (South Dakota, Tennessee,

Missouri, and Indiana) reported CSBG administrative expenditures of less than 2 percent of their

total CSBG expenditures in FY 2008.

Eight States (Georgia, Massachusetts, New Mexico, Ohio, North Carolina, Arizona, New Jersey,

and Alabama) exceeded the 5 percent threshold in FY 2008 because of differences in the CSBG

reporting period and grant period.

v

Training and guidance on using and reporting CSBG funds is available The national CSBG Network provides training opportunities for State officials to learn how to

budget and allocate CSBG funds. The National Association for State Community Services

Programs (NASCSP) and other national associations conduct training through webinars; at

national meetings, orientations, and monitors’ training sessions; and by special request. Some of

these sessions have been conducted by large, highly respected accounting and consulting firms.

CAAs appear to be motivated to keep administrative expenses low

Unlike States, eligible entities (such as CAAs) do not have legislative restrictions on their use of

CSBG funds for administrative purposes. However, like all nonprofits, they are motivated to

keep overall administrative costs low and target resources toward their direct service programs

and their legislated mission to address the causes of poverty in local communities.

In FY 2009, OCS/HHS introduced an administrative efficiency measure for eligible entities that

receive CSBG funds and set as a target that 19 percent of a CAA’s (or other eligible entity’s)

total CSBG subaward could be spent on administrative expenditures in a year. Nationally,

eligible entities have been able to produce even more efficient results, reporting CSBG

administrative expenses, on average, just below 17 percent in FY 2009 and 16 percent in FY

2010. The efficiency measure applies only to CSBG funds, not administrative expenses for the

organization as a whole.

Based on an analysis of IRS Form 990 data, CAAs appear to be comparatively good stewards of

their financial resources. In FY 2008, CAAs spent, on average, somewhat less on agency-wide

administrative expenses (6.8 percent) than a comparable group of nonprofits (8.2 percent).

Factors to consider when developing Efficiency Measures

There is no generally accepted standard for designating an appropriate level of resources that

should be spent on administrative expenditures. In 2002, the U.S. General Accounting Office

(GAO) reported that nonprofits spent on average 13 percent of their budgets on general

management—namely, salaries, travel, professional fees, and other expenses not otherwise

designated to specific line items. About 85 percent of funds, on average, cover program

expenses, and about 3 percent is used for fundraising (percentages are rounded).

Efforts to create rating scales to assess the efficiency of nonprofit service providers typically are

based on the assumption that lower is better. Scholars note that such systems can lead to creative

vi

and inconsistent accounting procedures that underreport administrative expenses and lead to

underinvestment in an organization’s infrastructure.

Focusing solely on financial ratios to assess an organization’s efficiency and effectiveness can

miss the big picture of an organization’s performance. In addition to financial stability, it is

important to consider the outcomes an organization achieves in order to demonstrate success in

meeting community needs.

To fulfill CSBG’s legislative mandate of addressing the causes of poverty locally, CAAs and

other eligible entities coordinate a wide range of health and human services programs and

collaborate with community partners. Such activities are often considered administrative rather

than programmatic because they are not necessarily associated with the direct delivery of service.

This distinction needs to be considered when creating benchmarks and targets for CSBG

administrative expenditures.

Recommendations

Both funders and nonprofit organizations want public needs to be met in the best possible way, at

the least cost and with little waste. This analysis suggests three areas in which further attention is

needed.

First, government agencies that issue guidelines need to clarify the distinction between

administrative and program expenses. Expert review of guidelines across issuing

authorities is needed to reduce or eliminate ambiguous and conflicting guidelines and

improve the quality of reporting. In particular, attention might be given to clarifying how

facility costs, grant writing/development activities, and information technology services

are classified.

Second, training and technical assistance for States and eligible entities (CAAs),

particularly for smaller organizations, is needed to help financial officers prepare

reporting documents. Comparisons of financial ratios, such as percentage spent on

administrative expenses, are only valid if the data are comparable. Interviews with CAA

financial officers indicate that they do their best to comply with Federal directives but

that unclear and conflicting guidelines can be problematic.

vii

Third, because administrative costs, as a proportion of total expenses, decrease as a

nonprofit’s budget increases, funders might consider permitting a range of administrative

expense levels based on organization size, with smaller nonprofits allowed higher

percentages than larger ones. The literature is less clear about how the types of services

provided or the provider’s geographic location might affect administrative expenses.

These factors need further investigation before any policy recommendations can be made.

Information Sources

The report is based on the following sources of information:

legislative and administrative records,

CSBG Information System (IS) Survey data, provided by NASCSP,

telephone interviews with 23 CAA financial officers in eight States,

FY 2008 IRS Form 990 data, and

professional journal articles on efforts to create measures of administrative expenses as a

proxy for efficiency.

1

ACCOUNTABILITY AND ADMINISTRATIVE EXPENSES

All levels of government contract with nonprofit organizations to provide needed services.

According to a 2009 study, 33,000 nonprofit human service organizations in the United States

managed nearly 200,000 government contracts—an average of six government contracts per

organization. For 60 percent of these organizations, government funds represented the single

largest source of revenue. Three-quarters of these nonprofits managed grants and contracts from

two or more government agencies. Larger nonprofits with budgets of more than $1 million were

more likely than smaller ones to contract with government (Boris et al. 2010).

In a time of tight budgets and resource constraints, all funders—government and private

donors—want to know that their funds are being spent for the purposes intended and that funds

are being spent efficiently and effectively. This idea is not a new one. Nearly 20 years ago, the

1993 Government Performance and Results Act (GPRA) directed government contractors to

articulate their project goals and objectives and to measure performance. However, empirically

measuring the outcomes and effectiveness of nonprofit human service organizations is difficult

because outcomes are not easily defined or easily quantified, and definitions of effectiveness

may vary among different stakeholders (Hatry et al. 2003).

This paper examines the administrative costs associated with the Community Services Block

Grant (CSBG). It begins by presenting four definitions of administrative expenses used by

government entities. It then reviews the scholarly literature regarding how administrative

expenditures have been used to assess the performance of nonprofits, including the strengths and

limitations of these approaches. It also describes the HHS efficiency measures and targets

currently in place for CSBG. The third section looks at CSBG administrative expenses from the

perspective of the State agencies (hereafter referred to as “States”), including the guidance States

receive regarding statutory and regulatory requirements. The next section focuses on

administrative expenditures from the perspective of Community Action Agencies (CAAs),

namely, the groups responsible for implementing CSBG locally. A comparison of administrative

expenditures of CAAs and a comparable set of nonprofit organizations is provided in section five

to place the CAA experience in a broader context. Finally, the report summarizes the key points

2

of this study and suggests directions that might be considered for measuring and interpreting

CSBG’s administrative expenditures.

DEFINITIONS OF ADMINISTRATIVE EXPENSES

Administrative expenses are generally defined as expenditures a nonprofit organization incurs to

support its stated mission or purpose. Most funders, government agencies, and financial and

nonprofit experts associate these costs with the overall function and management of the

organization. Sometimes these expenditures are also referred to as overhead expenses or

management and general expenses.

While the broad functional categories for reporting allowable activities and expenses are similar,

the precise reporting instructions and definitions often differ, based upon the regulatory authority

publishing the guidance. For example:

1. The Financial Accounting Standards Board (FASB), the designated private-sector

organization that establishes standards of financial accounting that govern the preparation

of financial reports by nongovernmental entities,1 requires nonprofits to account for their

costs along three functional dimensions: administrative, program, and fundraising

expenses (Pindus and Nightingale 1994; Pollak, Rooney, and Hager 2001; Parson 2003).

The FASB guidelines (1993) categorize nonprofit activities such as “oversight, business

management, general recordkeeping, budgeting, financing, and related administrative

activities, and all management and administration except for direct conduct of program

services or fund-raising activities” under management and general expenses.

2. The Internal Revenue Service (IRS) uses the same functional categories, and instructs

nonprofits filing Form 990 (the annual reporting statement)2 to use the management and

general expenses line to report expenses “that relate to the organization’s overall

operations and management, rather than fundraising activities or program services.” The

1 Financial Accounting Standards Board, “Facts about FASB,”

http://www.fasb.org/jsp/FASB/Page/SectionPage&cid=1176154526495.

2 The IRS requires registered nonprofits to file an annual Form 990 if their gross receipts are greater than a

predetermined threshold. In 2008, organizations with gross receipts over $100,000 were required to file a Form 990

or 990EZ.

3

management and general expenses line should include salaries and expenses of the

nonprofit’s chief executive officer and his or her staff;3 expenses incurred managing

investments; lobbying costs; costs of board, committee, and staff meetings; general legal

and accounting expenses; office management; auditing, human resources, and other

centralized services; and preparation, publication, and distribution of the annual report.4

3. The Office of Management Budget (OMB) Circular A-122, which establishes principles

for determining costs of grants, contracts, and other agreements with nonprofits, defines

administrative expenses as “general administration and general expenses such as the

director's office, accounting, personnel, library expenses, and all other types of

expenditures not listed specifically as one of the subcategories of ‘Facilities.’”5

4. In addition to OMB Circular A-122, the Office of Community Services (OCS) issued an

Information Memorandum (IM 37) in 1999 to help grantees better understand how to

report their CSBG expenditures in the programmatic reports required under the block

grants legislation. Grantees are instructed to use two functional categories: direct program

expenses and administrative costs. Use of CSBG funds and reporting requirements adhere

to three criteria: meeting the program’s intended outcomes to address the causes of

poverty as stated in the CSBG legislation, achieving consistency with Health and Human

Services (HHS) audit and financial management standards, and ensuring a common basis

for relating expenditures to the CSBG Results Oriented Management and Accountability

(ROMA) System. The guidance in IM 37 specifically refers to CSBG administrative

expenditures, whereas the definitions listed in items 1–3 above apply to administrative

expenditures of the entire organization.

According to IM 37, administrative costs refer to central executive functions that do not directly

support a specific project or service. These costs are incurred for common objectives that benefit

3 Unless part of their time is spent directly supervising program services or fundraising activities.

4 From the IRS, “2010 Instructions for Form 990 Return of Organization Exempt from Income Tax,”

http://www.irs.gov/pub/irs-pdf/i990.pdf, accessed September 7, 2011.

5 From the Office of Management and Budget, “Circular No. A-122 Revised May 10, 2004,”

http://www.whitehouse.gov/omb/circulars_a122_2004/, accessed July 26, 2011. OMB Circular A-122 does not

apply to colleges and universities, which are covered by OMB Circular A-21, “Cost Principles for Educational

Institutions.”

4

multiple programs administered by the grantee organization, or the entity as a whole, and as such

are not readily assignable to a particular program funding stream. Administrative expenses relate

to the general management of the grantee organization, such as strategic planning, board

development, executive director functions, accounting, budgeting, personnel, procurement, and

legal services. In contrast, direct program costs are linked specifically to the delivery of a

specific program or service that is intended to achieve one of the funding outcomes or objectives

of CSBG.6

One example of conflicting guidance concerns the allocation of facility costs. OMB Circular A-

122 designates a separate line item for these costs; IM 37 allows CSBG grantees to allocate

facility costs between program expenses and administrative expenses. Another example concerns

development and grant writing activities. CSBG funds can be used to create new programs,

support existing ones, and coordinate and enhance a wide variety of programs or resources that

are responsive to the needs of the local community. The development/grant writing costs

associated with leveraging other resources and making programs self-sustaining are not

addressed in IM 37. In contrast, FASB and OMB Circular A-122 regard grant writing as a

fundraising expense. The IRS also considers grant writing a fundraising expense, unless the

grantor requires it to be reported as a program expense. The IRS does not consider

development/grant writing part of management and general expenses. IM 37, on the other hand,

is silent on this topic.

ADMINISTRATIVE EXPENSES AS A PROXY FOR EFFICIENCY

Funders, both public agencies and private donors, want to ensure that nonprofit organizations

that receive or are considered for funding use their resources prudently. Governments rely

heavily on nonprofits to deliver a range of critical human services through $100 billion in

contracts and grants (Boris et al. 2010). Given this volume of business, government officials

want to assure taxpayers that public dollars are being used wisely. Administrative expenditures

are often used as a proxy for fiscal responsibility.

6 From the U.S. Department of Health and Human Services, Administration for Children and Families, Office of

Community Services, “Community Services Block Grant Program, Information Memorandum No. 37,”

http://www.acf.hhs.gov/programs/ocs/csbg/guidance/im37.html, accessed July 26, 2011.

5

There is no generally accepted standard for designating an appropriate level of resources that

should be spent on administrative expenditures. The U.S. General Accounting Office (GAO)

reported in 2002 that nonprofits spent on average 13 percent of their budgets on general

management—namely, salaries, travel, professional fees, and other expenses not otherwise

designated to specific program line items. The majority of funds (85 percent, on average)

covered program expenses, and about 3 percent was used for fundraising.7

Efforts to Assess Nonprofits by Their Administrative Expenses

Financial information on nonprofit organizations is not as readily available and timely as

information about for-profit enterprises, which regularly provide quarterly reports to

shareholders and potential investors (Keating and Frumkin 2003). In the nonprofit sector, funders

rely mostly on annual IRS Form 990 filings, financial audits, and annual reports. Although the

IRS files are made available to the general public through services such as the National Center

for Charitable Statistics and GuideStar, data processing and release of this information by the

IRS generally takes a few years before it is publicly available. Administrative expenses are

extracted from these reports and factored into financial ratios that gauge the health of an

organization. This is a common and simple way to assess the efficiency of nonprofits; however, a

number of scholars have sharply criticized the method (Gregory and Howard 2009, Hager and

Greenlee 2004).

With increased demand for accountability, a number of efforts are under way to develop

mechanisms that assess and compare the efficiency and effectiveness of charitable organizations.

One of the early and better known efforts is Charity Navigator,8 an online nonprofit evaluator

that rates the financial health of organizations using financial ratios based on the IRS Form 990s

filed by nonprofits. An entity’s efficiency is analyzed through four performance categories:

program expenses, fundraising expenses, fundraising efficiency, and administrative expenses.

Under administrative expenses, Charity Navigator states that, “as with successful organizations

7 The 3 percent figure for fundraising is based on nonprofits that report their fundraising expenses. Percentages cited

here have been rounded.

8 Charity Navigator (http://www.charitynavigator.org) is an independent charity evaluator founded in 2002. Its

purpose is to direct philanthropic dollars to the most efficient and responsive nonprofits in the country. Using the

IRS Forms 990, it assesses charitable organizations along a number of dimensions, including administrative

expenditures, and then summarizes the scores into a four-star rating system.

6

in any sector, effective charities must recruit, develop, and retain talented people. At the same

time, they ensure that these administrative expenses remain reasonable and in line with the

organization’s total functional expenses.” For the Charity Navigator system, a nonprofit’s

administrative expenses are divided by total expenses to derive a percentage that can be checked

against Charity Navigator’s rating scale, which reflects the assumption that lower is better.9

Based on a study of 30 major metropolitan markets, Charity Navigator reports the typical (i.e.,

median) value for administrative expenses for public charities is 9.6 percent of total expenses.10

HHS Administrative Efficiency Measures for CSBG

In FY 2009, HHS ACF introduced an administrative efficiency measure for eligible entities that

receive CSBG subawards. The measure is intended to set priorities, monitor progress, and reduce

the proportion of CSBG funds subgrantees spend on administrative expenses. The measure is

calculated as the total amount of subgrantee CSBG administrative funds expended each year (the

numerator) divided by the total amount of subgrantee CSBG funds expended per year (the

denominator). The data for this measure are provided through the CSBG Information System

(CSBG IS) Survey, collected by NASCSP. This efficiency measure applies only to CSBG funds,

not administrative expenses for the organization as a whole.

The target for subgrantee’s CSBG administrative expenses, based on historical trend data, was

set at 19.00 percent for FYs 2009 and 2010. Subgrantees were able to produce even more

efficient results for these years, reporting CSBG administrative expenses of 16.96 percent in FY

2009 and 16.04 percent in FY 2010.

Strengths and Limitations of Financial Ratios

One strength of financial ratios is that they are simple and responsive to the needs of funders and

donors. Administrative expenses and other financial data tell funders how a nonprofit spends its

money and which organizations are likely to be “the most efficient stewards of their [resources]”

(Hager et al. 2005). These measures also help funders assess whether a nonprofit is financially

9 From Charity Navigator, “How Do We Rate Charities’ Financial Health?”

http://www.charitynavigator.org/index.cfm?bay=content.view&cpid=35, accessed September 7, 2011.

10 From Charity Navigator, “Metro Market Study 2010,”

http://www.charitynavigator.org/index.cfm?bay=studies.metro.main, accessed January 19, 2012.

7

viable and likely to sustain its operations. Such information can be linked to the scope and depth

of the organization’s programs. Further, financial measures (e.g., revenues, expenditures, assets,

and liabilities) are easier to obtain than measures of capacity and effectiveness. They provide

funders with a quick and common proxy for assessing and vetting nonprofits (Hager and

Greenlee 2004).

However, financial ratios also have shortcomings. For example, nonprofits tend to account for

fundraising and administrative expenditures in idiosyncratic ways (Hager and Greenlee 2004).

Some nonprofits ignore rules for allocating expenses that have both programmatic and

fundraising content, often charging no expenses to fundraising, keeping their fundraising ratio

low or nonexistent. Further, the rules for preparing financial records can vary. Audited financial

statements are prepared according to Generally Accepted Accounting Principles (GAAP), while

the IRS Form 990 is prepared according to IRS regulations, which differ somewhat from GAAP.

More important, “focusing on financials sometimes misses the big picture … it takes the place of

trying to determine whether the organization is doing a good job of fulfilling its mission or not”

(Hager and Greenlee 2004). By focusing only on a nonprofit’s financial performance, it

underplays other dimensions that may ultimately be important. A small nonprofit, for instance,

that reports high administrative expenses may be better suited to serve the community in which it

is embedded than a larger one with relatively low overhead costs but little knowledge of program

beneficiaries or community needs. An organization’s outcomes need to be considered as well as

its fiscal stability. Both elements must be strong to demonstrate success in meeting community

needs.

Financial ratios can be helpful in ascertaining a nonprofit’s efficient use of resources and solid

financial footing, but notions about the “right level” of administrative costs can result in some

nonprofits underreporting administrative expenses. This obscures the picture about what it takes

to run an effective organization. Results from the national Nonprofit Overhead Cost Study find

that nonprofit workers reiterate long-held beliefs about foundation support of overhead

expenses—that is, funders prefer to pay solely for program expenses and not administrative

expenses or a share of the overhead costs necessary for an organization to function (Center on

Philanthropy 2007). Nonprofits believe that funders are looking for low administrative expenses

as a sign of efficiency—an ideal perpetuated by Charity Navigator and others.

8

Research on nonprofit administrative expenses confirms the assumption that nonprofit

professionals have about funder bias for slim administrative budgets. In a competitive

fundraising environment, funders—public and private—are more likely to support organizations

that are deemed efficient, based on a relatively large percentage of funds being used for program

purposes versus administrative needs (Frumkin and Kim 2001; Pollak et al. 2001; Gregory and

Howard 2009). Such expectations can start “a vicious cycle” which “fuels the persistent

underfunding of overhead” (Gregory and Howard 2009). Nonprofits feel pressure to conform to

the mandate that administrative expenses be kept to a minimum and respond in two ways: they

spend too little on administrative costs, and they underreport their expenditures on tax forms and

in fundraising materials. This in turn perpetuates unrealistic expectations. Over time, funders

expect grantees to do a whole lot more for a whole lot less than it really costs an organization.

Data from the Nonprofit Overhead Cost Study indicate that roughly 10 to 13 percent of nonprofit

human service providers may be underreporting their administrative and fundraising costs based

on “plausible” management and general expenses as reported on the Form 990.11

Smaller

organizations are less likely than larger ones to file plausible expenditure information (Pollak et

al. 2001), suggesting that smaller nonprofits may need more training and technical assistance in

reporting administrative expenses than larger nonprofits.

Implications for Organizational Capacity

The tendency to pare down administrative expenses to the bare minimum has serious

implications for a nonprofit’s organizational capacity and ultimately its ability to deliver

programs and services to clients. An organization faced with scarce revenue sources and hobbled

by inadequate administrative budgets is left with few options for covering the full cost of

delivering its services and programs and can make decisions that compromise its ability to serve

its clientele. Low pay for administrative positions, for example, makes recruiting and retaining

skilled and experienced staff a challenge. Some executive directors ultimately do the

administrative tasks their staff cannot manage (Hager et al. 2005). Indeed, extremely low

administrative expenditures can be a signal that an organization is not investing in the

11

The researchers considered the following Form 990 entries as problematic and therefore not “plausible”: reporting

no management and general expenses –13 percent of all nonprofits did this; and reporting all expenses as

management and general expenses –2 percent of nonprofits did this. The percentages for nonprofit human service

providers are somewhat lower than these overall aggregate statistics.

9

infrastructure that will enable it to deliver a quality product in a reasonable and efficient manner.

As Tierney and Steele note, “Without the necessary investments in overhead, the organization

underperforms. It can't meet expectations, it becomes difficult to retain high-quality talent … it

might be hampered in attracting new funding and in ultimately serving the people it aims to

serve” (2011, 7).

The adverse effects of keeping administrative costs low are often felt most acutely in smaller

nonprofits. These organizations often can be cash strapped and have modest, if any, accounting

staff. Volunteers may be called upon to serve as part-time bookkeepers and work with

inexpensive, over-the-counter software packages that are not designed for nonprofits (Keating

and Frumkin 2003). In a study of nonprofit compliance with the Single Audit Act, findings

indicate that smaller nonprofits, those that are new to government grants, and those with prior

audit findings have a higher rate of adverse audit findings. The authors suggest that for cost or

other reasons, smaller nonprofits are being audited by less experienced auditors (Keating et al.

2003).

STATE CSBG ADMINISTRATIVE EXPENSES

In each State, one State agency is assigned to serve as the lead agency to carry out the duties set

forth by the CSBG Act. In addition to making subgrants to eligible entities and ensuring that

CSBG funds are used as intended, the State provides training and technical assistance, supports

communication among eligible entities, monitors the distribution of funds to ensure targeted

areas are reached, and supports other activities (CSBG Act Sec. 675C). Generally, States are to

distribute at least 90 percent of the CSBG funds to eligible entities to accomplish the goals of the

CSBG Act (see CSBG Act Section 672(2) for information regarding goals). In FY 2008, CSBG

expenditures reported by the 50 States and District of Columbia totaled $589.6 million.12

Expenditure amounts ranged from $2.5 million in Alaska to $58.0 million in California. Of the

51 jurisdictions in this analysis, CAAs in 46 States spent 90 percent or more of the State’s total

CSBG expenditures; CAAs in the remaining 5 States spent between 85.6 and 89.8 percent of the

12

This analysis uses data for FY 2008 because they reflect typical CSBG funding levels before the infusion of

CSBG ARRA funds in FY 2009.

10

State’s total CSBG expenditures. The remaining 10 percent of CSBG funds are used for other

functions, including administrative activities.

While the statute provides some flexibility on the percentage of funds that States must grant to

eligible entities, the language in the CSBG Act is stronger when discussing the requirements on

administrative expenses. “No State may spend more than the greater of $55,000, or 5 percent, of

the grant received…for administrative expenses, including monitoring activities” (CSBG Act,

Sec. 675C(b)(2)). The Act does not explicitly define administrative activities, but when the State

spends CSBG funds to support “Statewide coordination and communication among eligible

entities,” the State must categorize these funds as administrative expenses (CSBG Act, Sec.

675C(b)(1)(c)).

In FY 2008, States’ CSBG administrative expenses ranged from 0.87 percent (South Dakota) to

6.61 percent (Alabama) of their total CSBG expenditures.13

Indeed, South Dakota, Tennessee,

Missouri, and Indiana each reported using less than 2 percent of their CSBG expenditures for

administrative activities (Table 1).

Eight States (Georgia, Massachusetts, New Mexico, Ohio, North Carolina, Arizona, New Jersey,

and Alabama) reported administrative expenditures that exceeded 5 percent of their total CSBG

expenditures due to differences between the CSBG reporting period and the grant period. States

are able to spend up to 5 percent of their CSBG allocation on administrative expenditures.

However, they are also able to carry that money over to the next fiscal year, for a total authority

on the funds of 24 months. In other words, grantees report on a one-year period but have two

years in which to spend funds. The administrative percentages above that exceed 5 percent

include carryover funds from FY 2007 and do not take into account the funds distributed to

eligible entities that will be carried forward into 2009.

13

See Appendix A for the proportion of CSBG funds used for administrative purposes in each State and the District

of Columbia.

11

Table 1. States with the Lowest and Highest Shares of CSBG Expenditures Used for Administrative Activities, FY 2008

Rank State Percentage of CSBG expenditures spent on administrative expenses in FY 2008

States reporting less than 2 percent on administrative expenses

1 South Dakota 0.87

2 Tennessee 1.33

3 Missouri 1.34

4 Indiana 1.88

States reporting more than 5 percent on administrative expenses

44 Georgia 5.16

45 Massachusetts 5.18

46 New Mexico 5.20

47 Ohio 5.23

48 North Carolina 5.39

49 Arizona 5.88

50 New Jersey 6.07

51 Alabama 6.61

Sources: Data from the National Association for State Community Services Programs, Community Services Block Grant (Annual Report, 2008); calculations by the Urban Institute.

The national CSBG Network provides training opportunities for State officials to learn how to

budget and allocate CSBG funds. NASCSP staff conduct training through webinars, at national

meetings, orientations and monitors’ training sessions, and by special request. NASCSP also

contracts on occasion with WIPFLI, a large and highly respected CPA and consulting firm,14

to

provide training seminars to State agency officials. A 2011 session covered the purpose of CSBG

funding; the structure of a Federal program; sources of Federal regulation; examples of cost

allocation methods, including allowable methods and direct versus indirect costing; and tools for

budgeting and managing CSBG funds. In addition, CAPLAW (i.e., the Community Action

Program Legal Services) and the Community Action Partnership offer financial training to the

CSBG Network that generally focuses on issues related to OMB compliance and other related

14

Established in 1930, WIPFLI has more than 1,100 partners and associates worldwide. It ranks among the top 30

accounting and business consulting firms in the United States and is a member of PKF International, Ltd., the tenth

largest global accounting network in the world. WIPFLI’s client base includes both nonprofit organizations and

governmental units.

12

topics. These training programs, although voluntary, provide support and guidance to State

officials and CAA leaders responsible for managing CSBG funds.

CSBG ELIGIBLE ENTITIES’ ADMINISTRATIVE EXPENSES

Unlike States, the eligible entities (e.g., primarily CAAs) do not have legislative restrictions on

their use of CSBG funds for administrative purposes. However, like all nonprofits, they are

motivated to keep overall administrative costs low and target resources toward direct services to

address the underlying causes of poverty and strengthen communities.

To better understand how CAAs report administrative expenditures for their agencies, and how

CSBG funds are used locally, telephone interviews were conducted with the financial officers of

23 CAAs in eight States.15

The interviews were designed to learn how CAAs track and classify

agency-wide expenditures and the intrinsic value of CSBG funding for the organization.

Types of Expenses Allocated to Administration

Following guidelines from OMB Circular A-122 and OCS directives, CAAs allocate their

expenses between program and administrative cost categories. In general, CAAs report their

overall operations and management expenses as administrative costs. However, because OMB

and OCS guidelines are sometimes subject to interpretation, and definitions of program and

administrative costs differ depending on the regulatory authority and reporting purpose, the

financial reports submitted by eligible entities may not be completely comparable.

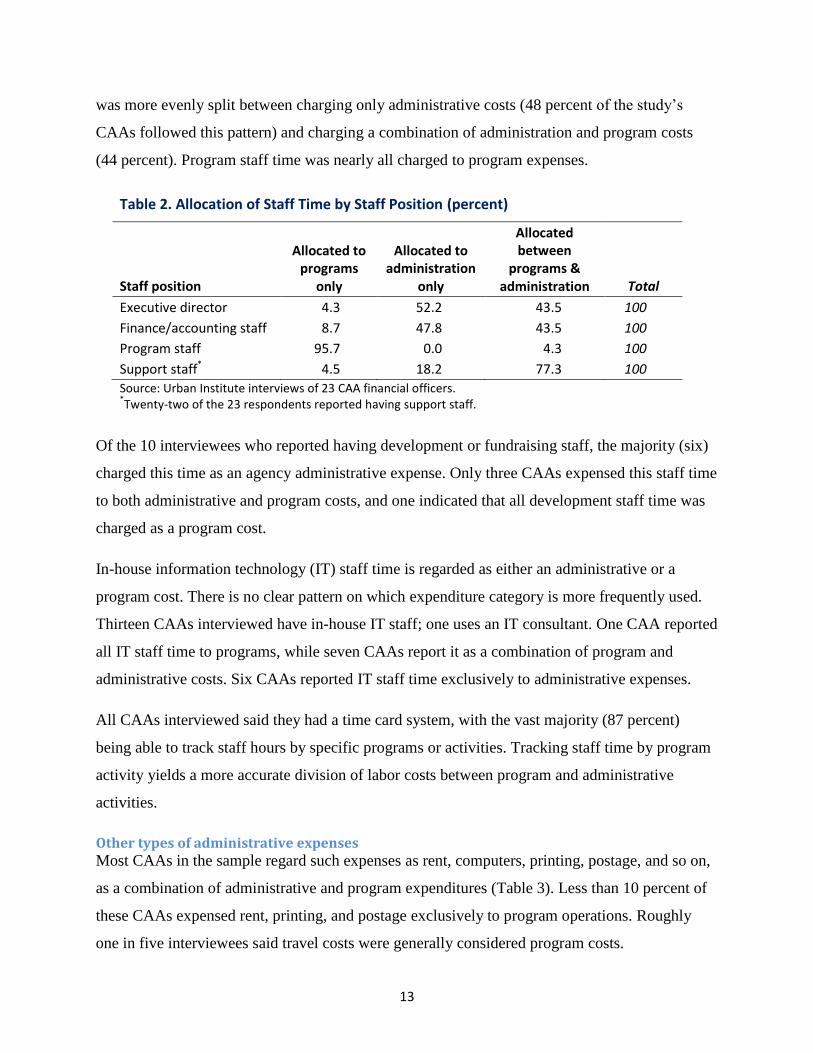

Staff time The vast majority of interviewees reported that the time of non-program staff is classified as

either administrative expenses or a combination of administrative and program expenses (Table

2). Half the CAAs interviewed (52 percent) charged their executive director’s time solely to

administration, while two-fifths (44 percent) attributed their director’s time to both

administration and programs. For finance and accounting personnel, the allocation of their time

15

The eight States selected (California, Georgia, Massachusetts, Minnesota, New York, Oklahoma, Virginia, and

Washington) correspond to those that participated in site visits as part of the larger CSBG ARRA Evaluation study.

See Appendix B for a description of the methodology used to select the States and CAAs, and the protocols used for

conducting the interviews.

13

was more evenly split between charging only administrative costs (48 percent of the study’s

CAAs followed this pattern) and charging a combination of administration and program costs

(44 percent). Program staff time was nearly all charged to program expenses.

Table 2. Allocation of Staff Time by Staff Position (percent)

Staff position

Allocated to programs

only

Allocated to administration

only

Allocated between

programs & administration Total

Executive director 4.3 52.2 43.5 100

Finance/accounting staff 8.7 47.8 43.5 100

Program staff 95.7 0.0 4.3 100

Support staff* 4.5 18.2 77.3 100

Source: Urban Institute interviews of 23 CAA financial officers. *Twenty-two of the 23 respondents reported having support staff.

Of the 10 interviewees who reported having development or fundraising staff, the majority (six)

charged this time as an agency administrative expense. Only three CAAs expensed this staff time

to both administrative and program costs, and one indicated that all development staff time was

charged as a program cost.

In-house information technology (IT) staff time is regarded as either an administrative or a

program cost. There is no clear pattern on which expenditure category is more frequently used.

Thirteen CAAs interviewed have in-house IT staff; one uses an IT consultant. One CAA reported

all IT staff time to programs, while seven CAAs report it as a combination of program and

administrative costs. Six CAAs reported IT staff time exclusively to administrative expenses.

All CAAs interviewed said they had a time card system, with the vast majority (87 percent)

being able to track staff hours by specific programs or activities. Tracking staff time by program

activity yields a more accurate division of labor costs between program and administrative

activities.

Other types of administrative expenses Most CAAs in the sample regard such expenses as rent, computers, printing, postage, and so on,

as a combination of administrative and program expenditures (Table 3). Less than 10 percent of

these CAAs expensed rent, printing, and postage exclusively to program operations. Roughly

one in five interviewees said travel costs were generally considered program costs.

14

Table 3. Allocation of Organizational Expenses (percent)

Organizational expense

Allocated to programs

only

Allocated to administration

only

Allocated between

programs & administration Total

Rent/mortgage* 9.5 0.0 90.5 100

Computers & IT-related 0.0 4.3 95.6 100

Printing/copying 8.7 0.0 91.3 100

Telephone 0.0 0.0 100.0 100

Postage 8.7 0.0 91.3 100

Supplies/miscellaneous 4.3 4.3 91.3 100

Travel** 18.2 4.5 77.3 100

Source: Urban Institute interviews of 23 CAA financial officers. *Twenty-one of the 23 respondents reported having rent or mortgage expenses. Two CAAs owned

the space they occupied. **

One respondent did not report travel expenses.

Ten of the 17 CAAs that reported capital expenses (e.g., building additions and major equipment

purchases) classified the expenses under both agency administration and programs. Six of the 17

attributed capital expenses to programmatic activities, and only one said its capital expenses fall

under administration.

Use of CSBG Funds

According to most interviewees, CSBG funds are used primarily for programmatic purposes. But

the flexibility of CSBG funds enables CAAs to use this support in various ways—similar to a

general program support grant that might be obtained from a private foundation. It may be used

to fill in funding gaps of other programs, start new and innovative efforts, or provide leverage for

securing other sources of revenue. One financial officer characterized CSBG as the “umbrella

program” that covers all the other programs of her agency. CSBG assists in supporting varied

expenses, including staffing and space for other services.

A common use of CSBG funds is to bolster programs and services. Twenty-one of the 23 CAAs

interviewed used their CSBG funds to help with other programs such as local homelessness

prevention, employment, child care, youth development, food and nutrition, education, and

energy programs. Part of the cost of these programs is covered through other Federal programs

such as Head Start, Weatherization, and The Emergency Food Assistance Program (TEFAP),

with CSGB filling in gaps and supplementing program activities. One in three interviewees said

15

their organizations allocated 60 percent or more of CSBG funds to help fund other programs,

which is an allowable use of CSBG funds under IM 37. Interviewees suggested that CSGB funds

provide an operational platform from which other programs and services may be delivered to

address the causes of poverty in local areas. One interviewee said that without CSBG, the CAA

would lose at least 10 of its 40 programs and be forced to lay off 150 to 200 people.

Other CAAs use CSBG to launch new programs or strengthen existing ones, which eventually

are funded from other sources. One interviewee characterized this as the “entrepreneurial spirit”

developed with CSBG. He said that without the initial infusion of CSBG funding, most of his

organization’s 35 programs would not have started. In fact, three-quarters of the interviewees

reported that they use CSBG funds to leverage additional revenue to meet critical, inadequately

funded needs (such as food banks, long-term care ombudsman programs, employment programs,

and homelessness prevention initiatives) and other services for low-income families and

children.

One CAA staffer indicated that the ability to use CSBG funds to support the agency’s homeless

shelter proved invaluable, as it demonstrated a financial base for this service and resulted in

securing funds from other revenue sources. Another interviewee recounted how his CAA used

CSBG funds to set up a health clinic and apply for grants from other Federal agencies. In this

case, staff time was covered by CSBG. The clinic eventually became a separate, independent

nonprofit.

When asked how much of CSBG funds were spent on administrative expenses in FY 2008, a

third of the CAAs interviewed (8 of 23) said 10 percent or less. The median share was 15

percent. A financial officer at one CAA said he really wanted all of his organization’s CSBG

funds to go toward programs. He noted that his CAA has such respect for CSBG funding that the

organization uses alternate funding (such as earned income and user fees) to cover administrative

costs. This tactic allows his CAA to spend 100 percent of CSBG funds on program services.

However, not all CAAs have alternate streams of revenue to cover administrative costs.

CSBG funds are meant to meet local needs and are designed to be more flexible than most other

government funds; as such, they can serve various organizational and community needs. One

CAA used CSBG funds to put in place the “appropriate infrastructure to administer our Federal

16

contracts correctly. It would have been very difficult otherwise as funding for such capacity-

building activities is rare.” Another noted that CSBG funds are critical to meet the different

needs of the community. CSBG allows this agency to develop programs that address those needs.

Perspectives on Allocating Administrative Expenses

A consistent theme throughout the interviews was the negative stigma associated with

administrative costs. Managers wanted to spend as much of their CSBG funds on programs as

possible; however, several expressed concern over balancing their program and administrative

costs. As one interviewee stated, “the reality is there is a level of admin[istrative] cost that needs

to exist.”

The organizations interviewed strive to present an honest and accurate picture of how they spend

their funds, but several interviewees noted that the guidelines regarding administrative expenses

are complex and sometimes conflicting. Some expenses can be seen as both administrative and

programmatic, depending on the regulatory authority issuing the guidance and the purpose of the

report being completed. For example, IM 37 provides administrative and programmatic

definitions that sometimes differ from those identified under OMB Circular A-122. According to

Circular A-122, grantees can include all facility costs as a separately identified category in

calculating their administrative expenditures. For CSBG, grantees may allocate facility costs

between direct program costs (i.e., those facility costs attributable to the operation of direct

program activities) and administrative costs (i.e., those facility costs associated with general

management of the organization).16

Eligible entities must comply with IM 37 when reporting

CSBG funds, but they also must comply with the requirements and definitions outlined under

Circular A-122.

This complexity requires CAAs to be cognizant of the differences among legislative and

regulatory guidelines in order to ensure accurate reporting of administrative expenditures.

Interviewees followed different strategies for resolving such issues. A few organizations said that

16

According to statute, CSBG funds cannot be used for “the purchase, construction, or permanent improvement

(other than low-cost residential weatherization or other energy-related home repairs) of any building or other

facility” (Sec. 678F, 42 USC 9918). In practice, this statutory language is generally interpreted to mean that

mortgage expenses are not an allowable expense under CSBG, while rental expenses are an allowable expense.

Circular A-122 does not provide specific guidance on this matter.

17

when they were unsure how to allocate costs, they tended to report such expenses as

administrative rather than program costs, which inflates their reported administrative costs.

Another interviewee said that “Technically, everything is related to programs. There really are

no admin expenses.” She noted, however, that her organization and auditors abide by contract

and grant regulations and guidelines, as they understand these rules. One CAA fiscal executive

explained that she felt the need to work closely with the State to make sure that the CAA is

following regulations. Several interviewees stressed the importance of following the rules and

maintaining transparency. As one interviewee stated, “Everything is very clean and very

transparent. Anyone can walk in and trace any line item expense.”

Overall, the CAA respondents share the goal of minimizing administrative expenses as best they

can. They want to be good stewards of the resources available to them. They also do not want to

provoke an audit or give the impression that they are wasting taxpayer and funder dollars. Many

interviewees feel that more guidance is needed to clarify financial reporting issues.

COMPARISONS OF CAAS AND OTHER NONPROFITS

CAAs are sometimes regarded as unique organizations, having been founded during the 1960s

and 1970s in response to President Johnson’s War on Poverty. Being charged with addressing

the causes of poverty in local communities, their activities are extremely broad and necessitate

coordination of a wide range of services to fulfill the purposes outlined under the CSBG

legislation. But since the 1960s and ’70s, other nonprofits have emerged that also address

poverty issues. How do CAA agency-wide administrative expenses compare to those of similar

nonprofit organizations? Are CAAs’ organization-wide administrative expenses higher or lower

than those of other nonprofits?

To answer this question, a sample of nonprofit organizations comparable to CAAs in size and

types of services provided was drawn from the National Center for Charitable Statistics (NCCS)

database, a national repository of IRS Forms 990. The sample was stratified by four size

categories (small, medium, large, and mega) based on total agency expenditures and by primary

18

type of service provided according to the National Taxonomy of Exempt Entities (NTEE)

classification system.17

Appendix C describes the methodology used for drawing the sample.

Table 4. Distribution of CAAs and Comparable Nonprofits by Total Expenditures, 2008

Size Expenditures

CAAs Comparable Nonprofits

No. Percent No. Percent

Small Less than $5 million 261 35.7 353 35.1

Medium $5–$50 million 463 63.3 594 59.0

Large $50.01–$100 million 4 0.5 36 3.6

Mega Greater than $100 million 4 0.5 17 1.7

Unknown Unknown 0 0.0 6 0.6

Total Total 732 100.0 1,006 100.0

Source: Urban Institute, National Center for Charitable Statistics, Core Files (Public Charities, 2008). Note: The CAAs in this study represent all CAAs that had a Form 990 on file with the IRS for FY 2008. CAAs not included may have requested reporting extensions from the IRS and do not appear in the NCCS database.

As Table 4 shows, the two groups are fairly similar in size, with comparable nonprofits slightly

larger than CAAs. About 5 percent of comparable nonprofits report annual total expenditures

over $50 million compared with 1 percent of CAAs. A somewhat higher share of CAAs than

comparable nonprofits fall in the medium-size category (63 percent versus 59 percent).

These size differences are also reflected in average and median annual expenditures. The average

(or mean) expenditures for the comparable group is almost two-thirds larger than expenditures

for the CAAs ($14.4 million versus $9.2 million, respectively). However, median expenditures

(i.e., the point where half the organizations are above or below this number) are much closer.

The median for CAAs is $6.3 million; for comparable nonprofits, it is $6.7 million.

The two groups are also statistically well matched based on their primary activity as defined by

NTEE codes (Table 5). Nearly 60 percent of each group is a human service nonprofit, while

almost 30 percent is community improvement and capacity-building organizations. The

17

The NTEE-CC classification system categorizes nonprofit organizations into 26 major groups under 10 broad

categories, including arts, culture, and humanities; education; environment and animals; health; human services;

international, foreign affairs; public, societal benefit; religion-related; mutual/membership benefit; and

unknown/unclassified.

19

remaining CAAs and comparable nonprofits are classified as “Other.” These organizations tend

to focus on such activities as employment, food, agriculture, nutrition, and housing and shelter.

Table 5. Distribution of CAAs and Comparable Nonprofits by Primary Services

NTEE Codes Mission

CAAs Comparable Nonprofits

No. Percent No. Percent

P Human Services 434 59.3 596 59.2

S Community Improvement and Capacity Building

213 29.1 279 27.7

J,K,L Other 85 11.6 131 13.0

Total Total 732 100.0 1,006 100.0

Source: Urban Institute, National Center for Charitable Statistics, Core Files (Public Charities, 2008).

In terms of geographic location, a slightly greater share of CAAs than comparable nonprofits is

located in the Midwest and South. In contrast, other nonprofits are more likely than CAAs to be

found in the West (Table 6). The concentration of CAAs in the Midwest and particularly the

South may reflect the historical origins of Community Action. Also, subsequent U.S. population

shifts to western States after the 1960s and ’70s may have encouraged the formation and growth

of other nonprofit organizations that address low-income needs.

Table 6. Distribution of CAAs and Comparable Nonprofits by Region

Census Region

CAAs Comparable Nonprofits

No. Percent No. Percent

Northeast 151 20.6 229 22.8

Midwest 205 28.0 235 23.3

South 273 37.3 331 32.9

West 103 14.1 211 21.0

Total 732 100.0 1,006 100.0

Source: Urban Institute, National Center for Charitable Statistics, Core Files (Public Charities, 2008).

Administrative Expenses of CAAs and Comparable Nonprofits

To understand how CAAs and a comparable group of nonprofits allocate their agency-wide

expenditures between program and administrative expenses, we looked at the percentage of total

expenditures an organization spent on administrative expenses as reported on its IRS Form 990.18

18

Percentage of administrative expenses is the total management and general expenses divided by total

expenditures. The Form 990 was extensively redesigned in 2008, and organizations had the option to use either the

20

This measure reflects administrative expenses for the whole organization, not just CSBG.

Because administrative expenses can vary by a number of organizational factors, the analysis

controlled for five factors, namely type of organization (CAA or comparable nonprofit), primary

type of service, organization size, location, and percentage of organizational funds received

through government grants. This last variable was included to facilitate comparisons because

many CAAs receive the bulk of their revenues from Federal funds.

Findings

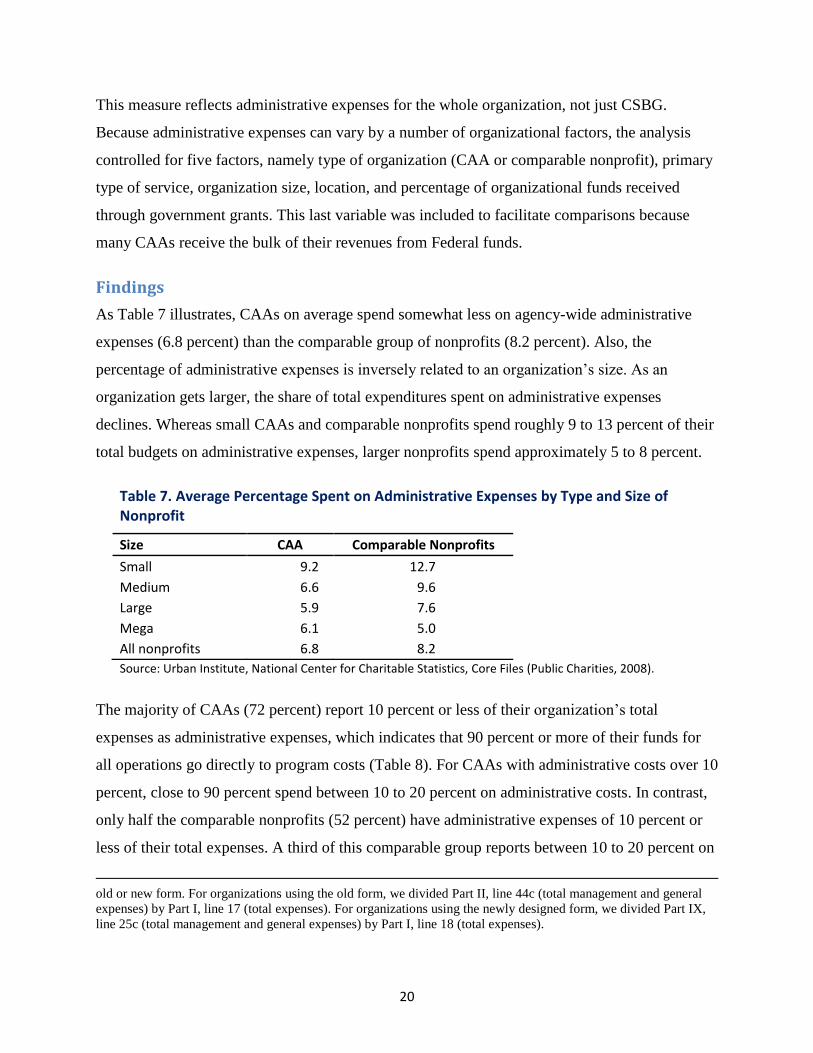

As Table 7 illustrates, CAAs on average spend somewhat less on agency-wide administrative

expenses (6.8 percent) than the comparable group of nonprofits (8.2 percent). Also, the

percentage of administrative expenses is inversely related to an organization’s size. As an

organization gets larger, the share of total expenditures spent on administrative expenses

declines. Whereas small CAAs and comparable nonprofits spend roughly 9 to 13 percent of their

total budgets on administrative expenses, larger nonprofits spend approximately 5 to 8 percent.

Table 7. Average Percentage Spent on Administrative Expenses by Type and Size of Nonprofit

Size CAA Comparable Nonprofits

Small 9.2 12.7

Medium 6.6 9.6

Large 5.9 7.6

Mega 6.1 5.0

All nonprofits 6.8 8.2

Source: Urban Institute, National Center for Charitable Statistics, Core Files (Public Charities, 2008).

The majority of CAAs (72 percent) report 10 percent or less of their organization’s total

expenses as administrative expenses, which indicates that 90 percent or more of their funds for

all operations go directly to program costs (Table 8). For CAAs with administrative costs over 10

percent, close to 90 percent spend between 10 to 20 percent on administrative costs. In contrast,

only half the comparable nonprofits (52 percent) have administrative expenses of 10 percent or

less of their total expenses. A third of this comparable group reports between 10 to 20 percent on

old or new form. For organizations using the old form, we divided Part II, line 44c (total management and general

expenses) by Part I, line 17 (total expenses). For organizations using the newly designed form, we divided Part IX,

line 25c (total management and general expenses) by Part I, line 18 (total expenses).

21

administrative expenses, and 13 percent indicate that they spend more than 20 percent of their

total operating budget on administrative expenses. These differences are statistically significant.

Table 8. Distribution of CAAs and Comparable Nonprofits by Percentage Spent on Administrative Expenses

Percentage Spent on Administrative Expenditures

CAAs Comparable Nonprofits

No. Percent No. Percent

0 24 3.3 69 6.9

0.01 to 5 188 25.7 199 19.8

5.01 to 10 316 43.2 258 25.6

10.01 to 20 181 24.7 341 33.9

Greater than 20 23 3.1 133 13.2

Unknown 6 0.6

Total 732 100.0 1,006 100.0

Source: Urban Institute, National Center for Charitable Statistics, Core Files (Public Charities, 2008).

Further analysis using Ordinary Least Squares (OLS) regression19

explored the strength of the

relationship between the percentage of revenues spent on administrative expenses and five

organizational characteristics: type of organization, primary type of service provided, size,

location, and percentage of funds received through government grants.

The results of the regression (see Technical Notes) provide additional evidence that CAAs spend

significantly less on agency-wide administrative expenses than the comparable group of

nonprofits. Size of the organization is statistically a strong and negative factor in explaining

levels of spending on administrative expenses—that is, as the size of the organization increases

the share of expenditures devoted to administrative expenses decreases. Economies of scale

come with greater size.

CONCLUSIONS

Administrative costs provide one measure of an organization’s efficient use of funds, although

they should not be viewed as the only measure for assessing performance. Many other factors—

19

Ordinary Least Squares regression is a procedure whereby the association between two values is represented by a

straight line drawn through the scatter of bivariate observations. The best-fitting line takes the most central path

through the scatter of observations.

22

such as the population served, types of services provided, location of the organization, and

program outcomes—are also important in assessing the efficiency and effectiveness of nonprofit

service providers.

This analysis focused on one aspect of organizational efficiency: administrative expenditures.

Based on an analysis of IRS Form 990 data, the study finds that CAAs, on average, tend to have

lower agency-wide administrative expenses than comparable nonprofit organizations. Moreover,

size matters: larger organizations achieve greater economies of scale and tend to use a smaller

percentage of their total operating budgets on administrative activities. These data support the

idea that CAAs are comparatively good stewards of Federal dollars.

While administrative expenses do not tell the whole story, they are an easy, accessible, and

nearly universal measure for gauging and comparing an organization’s efficiency. In a highly

competitive funding environment, nonprofits have much to gain by touting their efficiency

through financial data and metrics commonly used in the for-profit sector. But such financial

yardsticks must be accurately portrayed and comparably measured to be useful. If guidelines for

reporting financial information are unclear or conflicting, the resulting measures are likely to be

inconsistent across organizations, affecting one’s ability to compare and interpret results.

Both funders and nonprofit organizations want public needs to be met in the best possible way, at

the least cost, and with little waste. This analysis suggests three areas in which further attention

is needed:

First, the distinction between administrative and program expenses needs to be clarified

by government agencies that issue guidelines. Both the research literature and the CAAs

interviewed indicate that current guidelines from IRS, OMB, and OCS are not always

clear, and they are sometimes conflicting. Expert review of guidelines across issuing

authorities is needed to reduce or eliminate this ambiguity and improve the quality of

these financial measures. In particular, attention might be given to clarifying how facility

costs, grant writing/development activities, and information technology services are

classified.

Second, training and technical assistance for States and eligible entities (CAAs),

particularly for smaller organizations, is needed to help financial officers prepare

23

reporting documents. Comparisons of financial ratios, such as percentage of total

expenditures spent on administrative activities, are only valid if the data are comparable.

Interviews with CAA financial officers indicate that they do their best to comply with

Federal directives, but that unclear and conflicting guidelines can be problematic.

Third, because administrative costs, as a proportion of total expenses, decrease as a

nonprofit’s budget increases, funders might consider permitting a range of administrative

expense levels based on organizational size, with smaller nonprofits allowed higher

percentages than larger ones. The literature is less clear how the types of services

provided or the provider’s geographic location might affect administrative expenses.

These factors need further investigation before any policy recommendations can be made.

24

TECHNICAL NOTES

OLS Regression Results

Percentage Spent on Administrative Expenses by: Coefficient Standard

Error T score

Type -.094*** -0.017 -5.4

Mission:1

Human Services (P20) 0.004 -0.007 0.5

Community Improvement and Capacity Building (K) 0.002 -0.007 0.27

Other Human Services (other P) -0.001 -0.01 -0.1

Size -0.047*** -0.007 -6.66

Location:2

Northwest -0.005 -0.008 -1.27

Midwest -0.015 -0.008 -1.88

South 0.005 -0.008 0.63

Percent Government Grant 0.003 -0.006 0.55

Type*Size .023** -0.008 2.7

N 1,731

R squared 0.1097

Source: Urban Institute, National Center for Charitable Statistics, Core Files (Public Charities, 2008). Note: Robust standard error in parentheses. 1

Others is omitted category. 2

West is omitted category. Significance: *(0.05), **(0.01),***(0.001).

25

REFERENCES

Boris, Elizabeth, Erwin de Leon, Katie L. Roeger, and Milena Nikolova, 2010. “Human Service

Nonprofits and Government Collaboration: Findings from the 2010 National Survey of

Nonprofit Government Contracting and Grants.” Washington, DC: The Urban Institute.

Center on Philanthropy at Indiana University. 2007. “Paying for Overhead Study.” Indianapolis:

Indiana University–Purdue University Indianapolis.

Frumkin, Peter and Mark T. Kim. 2001. “Strategic Positioning and the Financing of Nonprofit

Organizations: Is Efficiency Rewarded in the Contributions Marketplace?” Public

Administration Review 61(3): 266–75.

General Accounting Office. 2002. “Tax-Exempt Organizations: Improvements Possible in

Public, IRS, and State Oversight of Charities.” Washington, DC: U.S. General

Accounting Office.

Gregory, Ann Goggins, and Don Howard. Fall 2009. “The Nonprofit Starvation Cycle.” The

Stanford Social Innovation Review: 49–53.

Gujarati, Damodar N., and Dawn Porter. 2008. Basic Econometrics, 5th

edition. New York:

McGraw-Hill.

Hager, Mark, and Janet Greenlee. 2004. “How Important Is a Nonprofit’s Bottom Line? The

Uses and Abuses of Financial Data.” In In Search of the Nonprofit Sector, edited by Peter

Frumkin and Jonathan B. Imber. New Brunswick, NJ: Transaction Publishers.

Hager, Mark, Patrick Rooney, Thomas Pollak, and Kennard Wing. 2005. “Paying for Not Paying

for Overhead.” Foundation News & Commentary 46(3).

http://www.foundationnews.org/CME/article.cfm?ID=3313.

Hatry, Harry P., Jake Cowan, Ken Weiner, and Linda M. Lampkin. 2003. “Developing

Community-wide Outcome Indicators for Specific Services.” Washington, DC: The

Urban Institute.

Keating, Elizabeth K., and Peter Frumkin. 2003. “Reengineering Nonprofit Financial

Accountability: Toward a More Reliable Foundation for Regulation.” Public

Administration Review 62(1): 3–15.

Keating, Elizabeth K., Mary Fischer, Theresa Gordon, and Janet Greenlee. 2003. “The Single

Audit Act: How Compliant Are Nonprofit Organizations.” John F. Kennedy School of

Government Faculty Research Working Paper Series. Cambridge, MA: Harvard

University.

26

Parsons, Linda M. 2003. “Is Accounting Information from Nonprofit Organizations Useful to

Donors? A Review of Charitable Giving and Value-Relevance.” Journal of Accounting

Literature 22:104–29.

Pindus, Nancy, and Demetra Smith Nightingale. 1994. “Administrative Cost Savings Resulting

from Federal Program Consolidation.” Washington, DC: The Urban Institute.

Pollak, Thomas H., Patrick Rooney, and Mark A. Hager. 2001. “Understanding Management and

General Expenses in Nonprofits.” Overhead Cost Study Working Paper presented at the

2001 Annual Meeting of the Association for Research on Nonprofit Organizations and

Voluntary Action.

Tierney, Thomas J., and Richard Steele. 2011. “The Donor-Grantee Trap: How Ineffective

Collaboration Undermines Philanthropic Results for Society and What Can Be Done

about It.” Boston, MA: The Bridgespan Group, Inc.

27

APPENDIX A: CSBG ADMINISTRATIVE EXPENDITURES BY STATE, FY 2008

State

State CSBG administrative

expenses Total CSBG expenses

Percent administrative

expenses

Rank by administrative

expenses

Number of CAAs in State,

FY 2008

Alabama 635,621 9,613,027 6.61 51 22 Alaska 119,465 2,537,843 4.71 30 1 Arizona 276,283 4,699,232 5.88 49 10 Arkansas 381,746 8,501,520 4.49 24 16 California 2,898,833 57,976,671 5.00 42 54 Colorado 272,442 5,448,843 5.00 40 3 Connecticut 317,854 7,615,778 4.17 22 12 Delaware 149,194 3,194,337 4.67 29 1 District of Columbia 417,402 10,642,350 3.92 18 1 Florida 911,643 19,601,665 4.65 28 31 Georgia 828,928 16,071,980 5.16 44 20 Hawaii 115,209 3,034,849 3.80 15 4 Idaho 144,299 3,410,002 4.23 23 6 Illinois 1,429,437 31,150,483 4.59 27 37 Indiana 176,174 9,347,663 1.88 4 24 Iowa 281,497 7,037,445 4.00 20 18 Kansas 249,979 5,144,692 4.86 34 8 Kentucky 226,746 10,316,479 2.20 6 23 Louisiana 755,861 15,267,581 4.95 35 42 Maine 73,129 3,481,397 2.10 5 10 Maryland 446,118 8,922,364 5.00 41 17 Massachusetts 810,392 15,653,155 5.18 45 24 Michigan 680,227 23,266,579 2.92 8 30 Minnesota 351,687 7,701,353 4.57 26 28 Mississippi 517,112 10,342,254 5.00 39 17 Missouri 239,744 17,827,420 1.34 3 19 Montana 157,963 3,159,269 5.00 37 10 Nebraska 116,596 4,495,353 2.59 7 9 Nevada 132,528 3,980,435 3.33 11 3 New Hampshire 120,735 3,172,205 3.81 16 6 New Jersey 584,604 9,628,343 6.07 50 25 New Mexico 185,184 3,558,791 5.20 46 8 New York 2,285,647 56,373,872 4.05 21 45 North Carolina 823,261 15,264,225 5.39 48 35 North Dakota 99,945 3,179,792 3.14 9 7 Ohio 1,350,208 25,830,444 5.23 47 52 Oklahoma 365,877 7,588,374 4.82 33 20 Oregon 203,470 5,117,804 3.98 19 17 Pennsylvania 921,127 27,558,455 3.34 12 42 Rhode Island 151,155 3,330,447 4.54 25 8 South Carolina 306,231 9,309,120 3.29 10 15 South Dakota 24,398 2,815,463 0.87 1 4 Tennessee 172,101 12,894,994 1.33 2 11 Texas 1,180,463 30,286,761 3.90 17 38 Utah 188,893 3,663,203 5.16 43 4 Vermont 173,382 3,654,349 4.74 31 5 Virginia 515,947 10,783,085 4.78 32 26

28

State

State CSBG administrative

expenses Total CSBG expenses

Percent administrative

expenses

Rank by administrative

expenses

Number of CAAs in State,

FY 2008

Washington 387,468 7,803,925 4.97 36 30 West Virginia 363,179 7,263,596 5.00 38 16 Wisconsin 278,114 7,850,539 3.54 14 16 Wyoming 110,397 3,241,136 3.41 13 5 Total 24,905,895 589,610,942 4.22 - 935

Source: National Association for State Community Services Programs. Community Services Block Grant (Annual Report, 2008). Note: Total CSBG Award combines State administrative, discretionary, and CAA amounts. CAAs counted above are only eligible nonprofit entities; other eligible entities such as public agencies and tribes are not shown.

29