Community and neighbourhood centres … Africa...1 Central London |Office Market Report Q3 2016...

9

1 Central London Office Market Report | Q3 2016 South Africa Retail Market Report Community and neighbourhood centres experience welcome growth in the quarter. Q4 2016

Transcript of Community and neighbourhood centres … Africa...1 Central London |Office Market Report Q3 2016...

1 CentralLondonOfficeMarketReport | Q3 2016

South Africa Retail Market ReportCommunityandneighbourhoodcentresexperiencewelcomegrowthinthequarter.

Q4 2016

Theretailsectorhasseenencouraginggrowthdespitethecurrenteconomicclimate.InQ42016wewitnessedtheriseofsmallershoppingcentres,withcommunityandneighbourhoodcentrescontributingtomuchoftheoverallincreaseintradingdensity,aswellasrecordinganaverage3.4%declineinvacancies.Theperformanceofthesecentreswillhavetobemonitoredtodeterminewhetherthisisalong-termtrend.

Regionalandsuper-regionalshoppingcentreshaveovertheyearsexperiencedexceptionalperformancewiththeabilitytothriveandconsistentlymaintainlowvacanciesdespiteunfavourableeconomicconditions.Itisthereforenotsurprisingthatnewdevelopmentsarebreakingground.However,withtherecentlyopenedMallofAfrica,thenewlyrenovatedMenlynParkShoppingCentre,andthecurrentperformanceofsmallercentres,one

wouldexpectcautioninincreasingregionalshoppingcentresprimarilyintheGautengarea.

2 SouthAfricaRetailMarketReport | Q4 2016

Overview

Innumbers

7.5%6.8%

3.7%

Interestrate

Inflationrate

Averagevacancyrate

SouthAfricaRetailMarketReport | Q4 2016 3

Totaldevelopmentpipeline

328,177m²

4 CentralLondonOfficeMarketReport | Q3 2016

Issue to watch :Cansmallershoppingcentressustaintheir

goodperformanceoverthelongterm?

5 SouthAfricaRetailMarketReport | Q4 2016

-0.5%0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%4.5%

50.0

55.0

60.0

65.0

70.0

75.0

80.0

85.0

90.0

95.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

y/y change 2014 2015 2016

November2016markedthesecondyearofBlackFridayinSouthAfrica,givingconsumerstheopportunitytoanticipateit.Themarketingscheme,whichseesretailersofferingmajorpricecuts,wasintroducedin2015withretailsalesreportinga7.8%m/mgrowthrateinthatmonth.ThepopularityofBlackFridaythisyearresultedinlargefootcountsacrossseveralretailstoresonadaywhenmanyemployeesreceivetheirsalaries.Retailsalesgrewbyanotable12.1%m/m(StatisticsSouthAfrica).

Reta

il tra

de sa

les i

n Ra

nds (

000m

²)

% Gr

owth

rat

e

Retailsalestrendatconstantprices

Source: Statistics South Africa

DemandDespiteincreasedfuelpricesandrisinginflationrateswhichinfluenceconsumerspend,theretailmarkethasseenencouraginggrowthinthelastquarterof2016.Retailsalesatconstantpriceswitnesseda3.8%increaseonay/ybasisforthetermendinginNovember–thehighestsalesinthepastsixyears.Necessitystoressuchasgeneraldealers,hardwareandpharmaceuticalstoreswerepositivecontributors.Duetoconstrainedspendingbyconsumers,furniturestoressawacontractionof0.8%y/yinthesametime-frame.

AccordingtoSAPOAdata,tradingdensityincreasedby5.4%y/yincurrentpricesduring2016.Therecordedgrowthismainlydrivenbysmallershoppingcentres,withcommunitycentresshowingagrowthrateof12.05%andneighbourhoodcentres,whichhaveinpreviousyearsbeentheunderperformers,recordingagrowthrateof7.32%attheendofSeptember.Increasedsalespersquaremetreinsmallercentresmaybeasaresultofconsumerspreferringconvenientlocationswithonlythenecessaryshopsratherthanthelargeshoppingexperienceinregionalandsuper-regionalcentres.

AlthoughretailsalesforDecemberhavenotyetbeenreleased,retailerssuchasWoolworthsandMrPricehavereportedpoorperformanceinDecemberonay/ybasiswhichweexpecttodampentheDecembersalesfigures.

6 SouthAfricaRetailMarketReport | Q4 2016

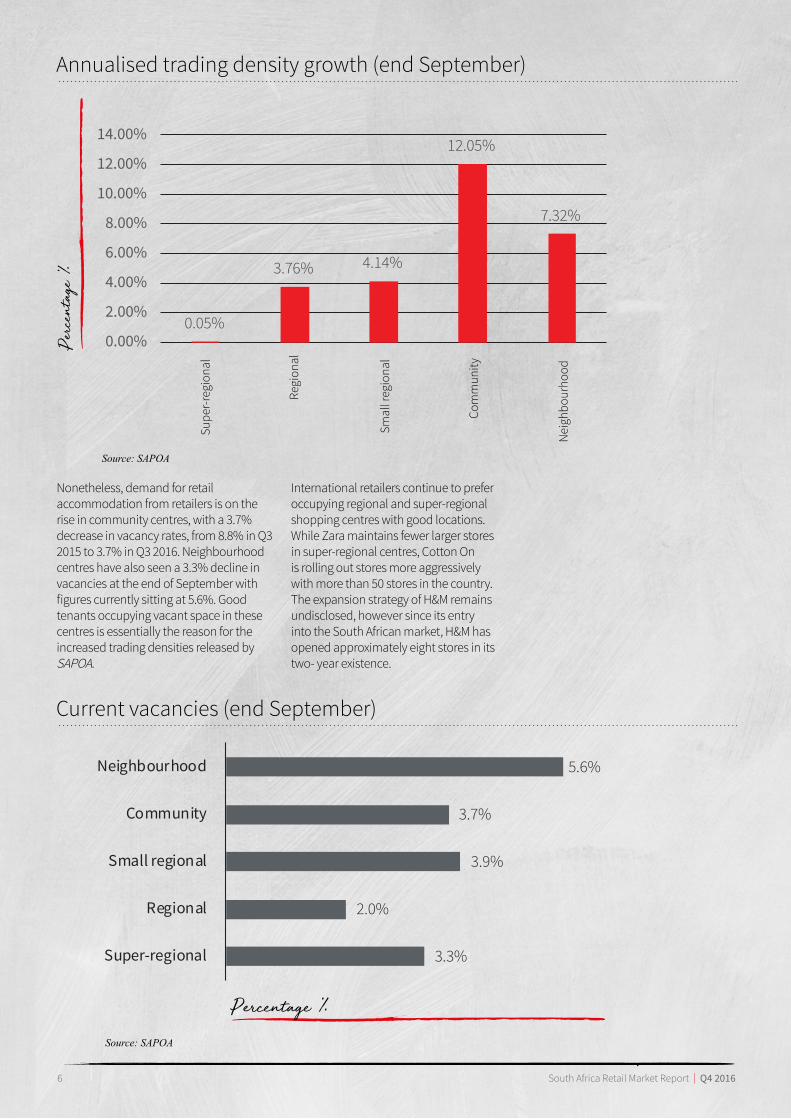

0.05%

3.76% 4.14%

12.05%

7.32%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Supe

r-reg

iona

l

Smal

l reg

iona

l

Com

mun

ity

Nei

ghbo

urho

od

Regi

onal

3.3%

2.0%

3.9%

3.7%

5.6%

Super-regional

Regional

Small regional

Community

Neighbourhood

Perce

ntage

%

Percentage %

Annualisedtradingdensitygrowth(endSeptember)

Currentvacancies(endSeptember)

Source: SAPOA

Internationalretailerscontinuetopreferoccupyingregionalandsuper-regionalshoppingcentreswithgoodlocations.WhileZaramaintainsfewerlargerstoresinsuper-regionalcentres,CottonOnisrollingoutstoresmoreaggressivelywithmorethan50storesinthecountry.TheexpansionstrategyofH&Mremainsundisclosed,howeversinceitsentryintotheSouthAfricanmarket,H&Mhasopenedapproximatelyeightstoresinitstwo-yearexistence.

Nonetheless,demandforretailaccommodationfromretailersisontheriseincommunitycentres,witha3.7%decreaseinvacancyrates,from8.8%inQ32015to3.7%inQ32016.Neighbourhoodcentreshavealsoseena3.3%declineinvacanciesattheendofSeptemberwithfigurescurrentlysittingat5.6%.GoodtenantsoccupyingvacantspaceinthesecentresisessentiallythereasonfortheincreasedtradingdensitiesreleasedbySAPOA.

Source: SAPOA

7 SouthAfricaRetailMarketReport | Q4 2016

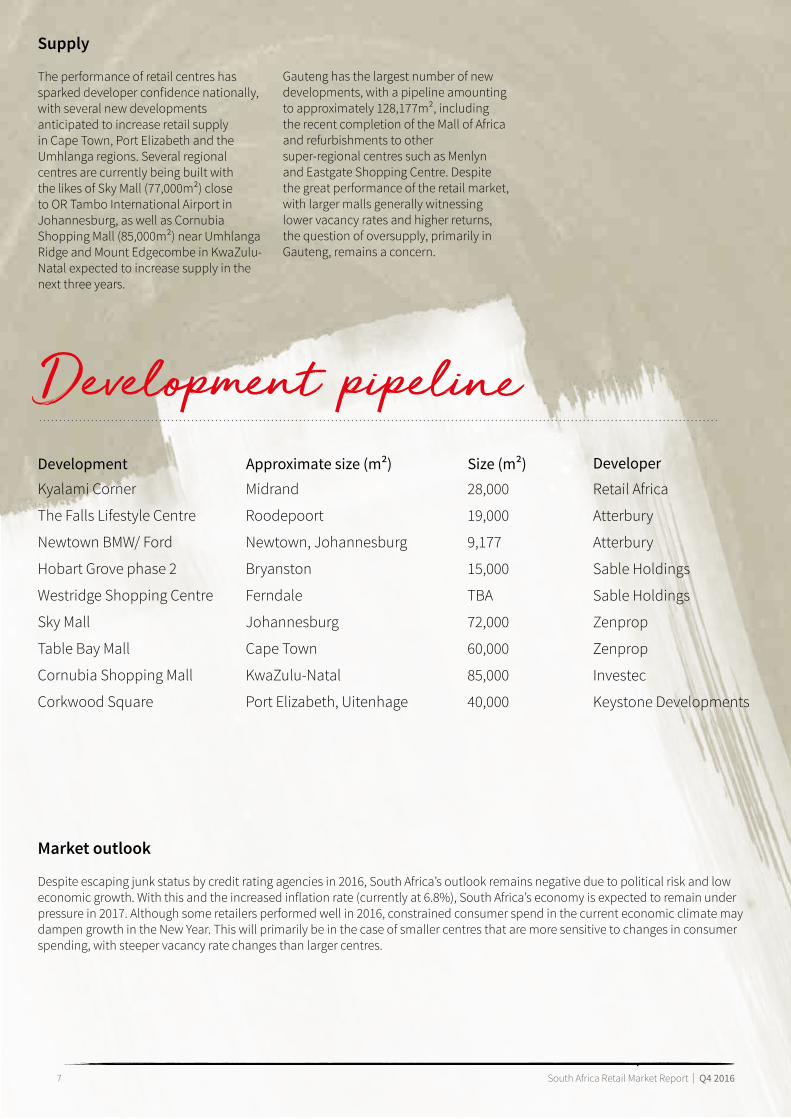

Supply

Theperformanceofretailcentreshassparkeddeveloperconfidencenationally,withseveralnewdevelopmentsanticipatedtoincreaseretailsupplyinCapeTown,PortElizabethandtheUmhlangaregions.SeveralregionalcentresarecurrentlybeingbuiltwiththelikesofSkyMall(77,000m²)closetoORTamboInternationalAirportinJohannesburg,aswellasCornubiaShoppingMall(85,000m²)nearUmhlangaRidgeandMountEdgecombeinKwaZulu-Natalexpectedtoincreasesupplyinthenextthreeyears.

Market outlook

Despiteescapingjunkstatusbycreditratingagenciesin2016,SouthAfrica’soutlookremainsnegativeduetopoliticalriskandloweconomicgrowth.Withthisandtheincreasedinflationrate(currentlyat6.8%),SouthAfrica’seconomyisexpectedtoremainunderpressurein2017.Althoughsomeretailersperformedwellin2016,constrainedconsumerspendinthecurrenteconomicclimatemaydampengrowthintheNewYear.Thiswillprimarilybeinthecaseofsmallercentresthataremoresensitivetochangesinconsumerspending,withsteepervacancyratechangesthanlargercentres.

Development pipelineKyalamiCorner

TheFallsLifestyleCentre

NewtownBMW/Ford

HobartGrovephase2

WestridgeShoppingCentre

SkyMall

TableBayMall

CornubiaShoppingMall

CorkwoodSquare

Midrand

Roodepoort

Newtown,Johannesburg

Bryanston

Ferndale

Johannesburg

CapeTown

KwaZulu-Natal

PortElizabeth,Uitenhage

28,000

19,000

9,177

15,000

TBA

72,000

60,000

85,000

40,000

RetailAfrica

Atterbury

Atterbury

SableHoldings

SableHoldings

Zenprop

Zenprop

Investec

KeystoneDevelopments

Development DeveloperApproximate size (m²) Size (m²)

Gautenghasthelargestnumberofnewdevelopments,withapipelineamountingtoapproximately128,177m²,includingtherecentcompletionoftheMallofAfricaandrefurbishmentstoothersuper-regionalcentressuchasMenlynandEastgateShoppingCentre.Despitethegreatperformanceoftheretailmarket,withlargermallsgenerallywitnessinglowervacancyratesandhigherreturns,thequestionofoversupply,primarilyinGauteng,remainsaconcern.

8 SouthAfricaRetailMarketReport | Q4 2016

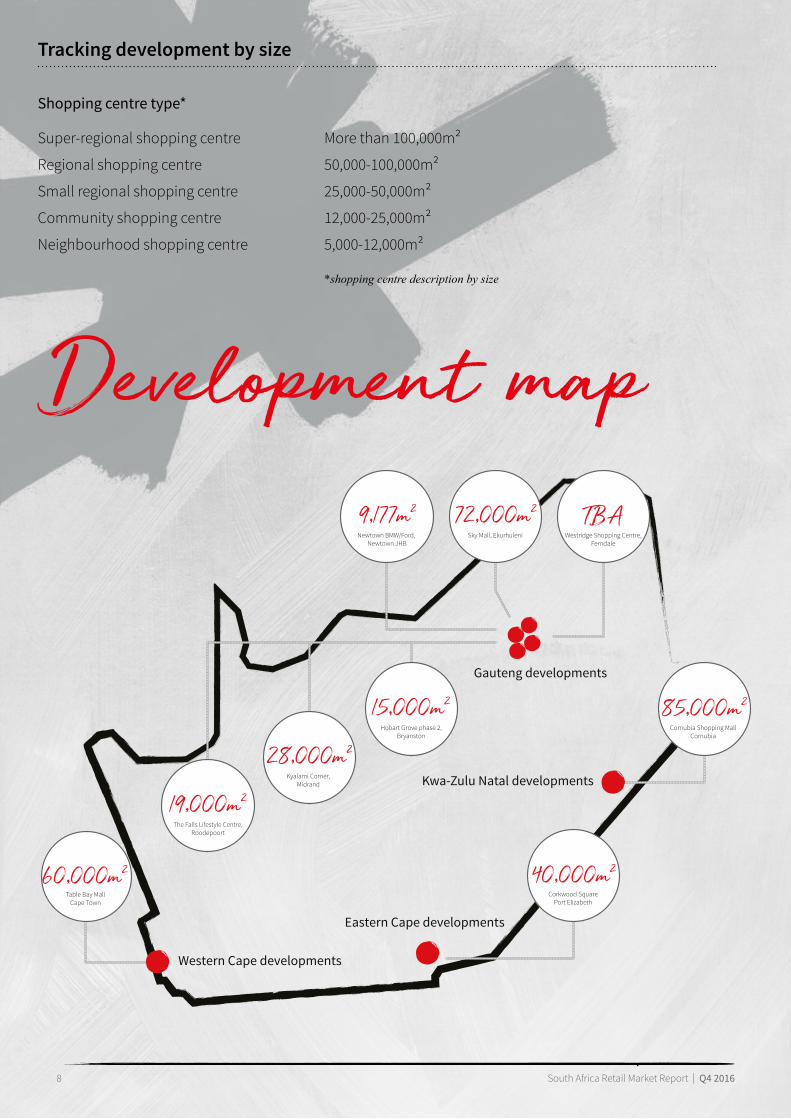

Super-regionalshoppingcentre

Regionalshoppingcentre

Smallregionalshoppingcentre

Communityshoppingcentre

Neighbourhoodshoppingcentre

Tracking development by size

Morethan100,000m²

50,000-100,000m²

25,000-50,000m²

12,000-25,000m²

5,000-12,000m²

Shopping centre type*

*shopping centre description by size

Table Bay MallCape Town

60,000m²

Kwa-Zulu Natal developments

Gauteng developments

Eastern Cape developments

Corkwood SquarePort Elizabeth

40,000m²

Western Cape developments

85,000m²Cornubia Shopping Mall

Cornubia

19,000m²The Falls Lifestyle Centre,

Roodepoort

28,000m²Kyalami Corner,

Midrand

Hobart Grove phase 2,Bryanston

15,000m²

Newtown BMW/Ford, Newtown JHB

9,177m²Sky Mall, Ekurhuleni

72,000m²Westridge Shopping Centre,

Ferndale

TBA

Development map

9 CentralLondonOfficeMarketReport | Q3 2016

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. The information contained in this document is proprietary to JLL and shall be used solely for the purposes of evaluating this proposal. All such documentation and information remains the property of JLL and shall be kept confidential. Reproduction of any part of this document is authorised only to the extent necessary for its evaluation. It is not to be shown to any third party without the prior written authorisation of JLL. All information contained herein is from sources deemed reliable; however, no representation or warranty is made as to the accuracy thereof.

JLL South AfricaJohannesburg3rd Floor, The FirsCnr Biermann & Cradock AveRosebank, South Africa, 2196Phone: +27 11 507 2200

Tom MundyHead: Research, Sub-Saharan [email protected]

Zandile MakhobaHead: Research, South [email protected]

www.jll.co.zawww.jllpropertysearch.co.za

Contact us

With other regional offices in Dubai, Abu Dhabi, Riyadh, Jeddah, Al Khobar, Cairo, Casablanca, Lagos and Nairobi

![TOWN AND NEIGHBOURHOOD CENTRES [DESCRITION] 2011...TOWN AND NEIGHBOURHOOD CENTRES Collet Park Precinct (North Parramatta) 4.1.2 Collet Park Precinct (North Parramatta) Desired Future](https://static.fdocuments.net/doc/165x107/60181b45296da74e693f9c5d/town-and-neighbourhood-centres-descrition-2011-town-and-neighbourhood-centres.jpg)