Commercial Bus Services in Ireland – 2016 Statistics · • Commercial Fleet Age Commercial Bus...

24

Statistical Bulletin Number: 03/2017 August 2017 Bulletin Topics: Overview of Commercial Bus Services • Number of Operators and Licences • Total Number of Passenger Journeys • Scheduled Vehicle Kilometres • Commercial Services Revenue and Ticketing • Free Travel Scheme Revenue and Passenger Journeys • Commercial Operator Fleet Size • Commercial Operating Fleet Accessibility and Scheduled Kilometres Operated by Accessible Vehicles • Automated Vehicle Location (AVL) Systems • Commercial Fleet Age Commercial Bus Services in Ireland (2016 statistics)

Transcript of Commercial Bus Services in Ireland – 2016 Statistics · • Commercial Fleet Age Commercial Bus...

Commercial Bus Statistics for Ireland | 1

Statistical Bulletin Number: 03/2017August 2017

Bulletin Topics:

Overview of Commercial Bus Services

•NumberofOperatorsand Licences

•TotalNumberofPassengerJourneys

•ScheduledVehicleKilometres

•CommercialServicesRevenueandTicketing

•FreeTravelSchemeRevenueandPassengerJourneys

•CommercialOperatorFleetSize

•CommercialOperatingFleetAccessibilityandScheduledKilometresOperatedbyAccessibleVehicles

•AutomatedVehicleLocation(AVL) Systems

•CommercialFleetAge

Commercial Bus Services in Ireland(2016 statistics)

2 | Commercial Bus Statistics for Ireland

Introduction ThisstatisticalbulletinisapublicationoftheNationalTransportAuthorityofIreland(“the Authority”).Itfocuseson bus statistics for licensed public bus passenger services operating to a regularschedulein Ireland.Licensedpublicbuspassengerservicesareoftencalled“commercial” bus services because they are operatedwithoutanypublicsubsidyfromthe Authority.Manyofthe services, however,receiveFreeTravelpaymentsfromthe Department of Social Protection in compensationfor the revenue foregone fromcarrying those entitledtoFree Travel.

These bus services are individually licensed bythe Authority. Under section 73 (Information, dataand statistics) of the Dublin Transport AuthorityAct 2008,amendedbysection75 oftheTaxiRegulationAct 2013,theAuthorityisrequiredto“collect, compile,analyse and prepare information, data or statistics”regardingpublictransportservicesin Ireland.

The bus services covered by this bulletin includeany licensed regular bus service with an origin,intermediate point, or adestinationwithin Ireland (i.e.essentially any service travelling through any part ofthe State).Busservicessubjecttoanauthorisationthataretravelling to,fromorthroughNorthernIrelandandthen into this State are also included in the bulletin.The licensed and authorised services in this bulletinare collectively refered to as regular commercial busservices.

Referencestocommercialbusservicesthereforeincludelicensed services operating wholly within the StateandbusserviceswhichcrosstheborderintoNorthernIrelandandaresubjecttoanauthorisation.

The Authority did not include information on certaincategories of licences such as Event or Venue licences,Temporary services, Demand Responsive services orSpecificTargetedservices(suchas tours,socialclub events,et cetera)becauseoftheadhocandirregularnatureofthesemainlyancillary services.

The data in this bulletin covers statistical informationfor all operators providing regular commercial services acrosstheStatefortheyears2013 to2016 andtheGreaterDublinArea(the“GDA”)1fortheyears2012 to2016 forcomparative purposes.HighlevelinformationonPublicServiceObligation(“PSO”) services,whicharesubsidisedservicesprovidedundercontract tothe Authority,hasalsobeenincludedforcomparative purposes.

Thiswillbethefourthyearthatdatahasbeenprovidedbyalllicensedoperatorsrunningserviceswithan origin,intermediate point, or destination in the State. ForoperatorswhohaveserviceswithintheGDAthiswillbe

1 TheGreaterDublinAreacomprisesthecityofDublinandthecountycouncilareasofSouth Dublin, Fingal,Dún Laoghaire-Rathdown, Kildare,WicklowandMeath

the fifth year that they have supplied data. Followingcomparisonofthedatasome figures,previously provided,havebeenrevisedby operators.Thedataexpressedinthisbulletinutilisesthemostuptodateinformationandsupercedestheprevious years’ bulletins.

Please note that the references to services as‘GDA Services’ refers to any service traveling to, fromor throughanyof theGDAcountiesof Dublin, Meath,Wicklow or Kildare. This includes services that travelwholly within the GDA as well as services that traveloutsidetheGDAcountiesbutwhichprovideevenpartof the service within the GDA. GDA Services includelicensedandauthorised services.

The services travelling wholly outside of the GDAcounties are referred to as ‘Non-GDA Services’ and,‘Nationally’referstothecombinedtotalofGDAandNon-GDAServicesrunning to,fromorthroughthe State,andthesearethemeaningsassignedtothemthroughoutthedocumentunlessotherwise stated.Againtheseservicesincludelicensedandauthorised services.

Readers should be aware that the two principalcontracted State funded bus operators, Bus Éireannand Dublin Bus, also provide licensed commercialbus services.TheseincludetheBusÉireannExpresswayServices and the Dublin Bus Airlink services and so,when relevant,theirlicensedfiguresareincludedinthelicensedcommercialbusservices data.

TheAuthorityhasproducedaseparatebulletinonStatefunded services covering bus services provided byDublin Bus, Bus Éireann, M&ACoaches Ltd,AndrewWhartonCoach Hire,BernardKavanagh&SonsLtdandthe Rural Transport Programme, as well State fundedrailservicesprovidedbyIarnródÉireannandLightRailservices provided by Transdev. This can be found onthe Authority’swebsite www.nationaltransport.ieundertheheadingPublications& Statistics.

Statistical Qualification - it is important to note thatthe figures used in this bulletin are provided by the operators and are intended to illustrate general features for licensed commercial public bus passenger services including patronage, passenger revenues and thecharacteristicsofthefleetandtheyarenotmeanttobereadasprecise calculations.Roundinghasbeingusedandthiscouldaffectoverall percentages.Itshouldalsobe noted that some figures from previous years havebeenrevisedbytheoperatorsthis year.Thishasbeenreflectedinthefiguresstatedinthis bulletin.

In publishing data theAuthority has been fully awareof its obligations regarding commercially sensitiveinformationandhas thereforeensured thatpatronageand revenues have been presented in a consolidatedandanonymised fashion.

AcknowledgementTheAuthoritywould like toextend itsappreciation tothe licensedandauthorisedcommercialbusoperatorsfor their co-operation and assistance in contributingto this bulletin.A 100% return was achieved from alloperators with active licences for every year save for2014 wherea 99%returnwas achieved.

Commercial Bus Statistics for Ireland | 3

Total Ticket Revenue

2016 Figures for Licensed Regular Bus Services

Total Scheduled Vehicle Kilometres

Total Passenger Journeys

22.74million

25.24million

11%

2015 2016

143.19million

155.62million

9%

2015 2016

86.28million

92.08million

7%

2015 2016

Table of Contents

Introduction 2

Overview Of Commercial Bus Services 5

1. Number Of Operators And Licences 6

2. Total Number Of Passenger Journeys 9

3. Scheduled Vehicle Kilometres 12

4. Commercial Bus Services Revenue And Ticketing 14

5. Free Travel Passenger Journeys 16

6. Commercial Operator Fleet Size 18

7. Commercial Operating Fleet Accessibility And Scheduled Kilometres

Operated By Accessible Vehicles 19

8. Automated Vehicle Location (AVL) Systems 22

9. Commercial Fleet Age 23

4 | Commercial Bus Statistics for Ireland

Commercial BusStatisticsforIreland|5

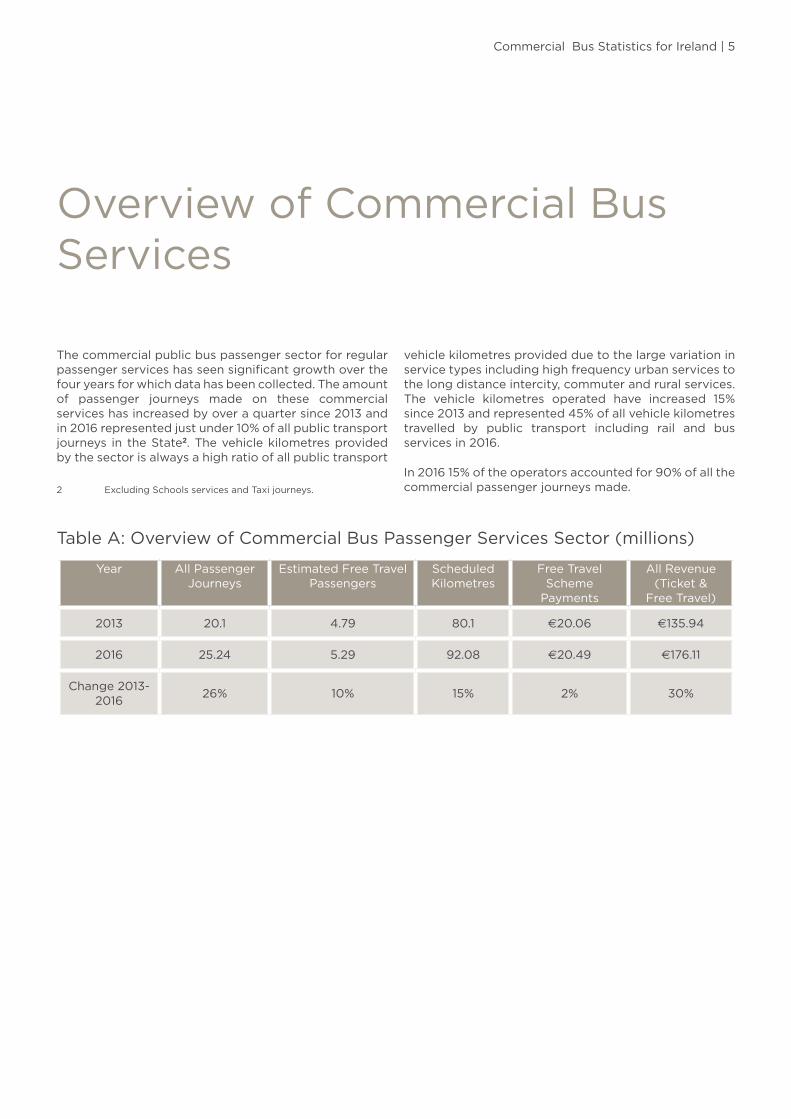

Overview of Commercial Bus Services

Thecommercialpublicbuspassengersectorforregularpassengerserviceshasseensignificantgrowthoverthefouryearsforwhichdatahasbeen collected.Theamountof passenger journeys made on these commercialserviceshasincreasedbyoveraquartersince2013 andin2016 representedjustunder 10%ofallpublictransportjourneys intheState2.Thevehiclekilometresprovidedbythesectorisalwaysahighratioofallpublictransport

2 ExcludingSchoolsservicesandTaxi journeys.

vehiclekilometresprovidedduetothelargevariationinservicetypesincludinghighfrequencyurbanservicestothelongdistance intercity,commuterandrural services.The vehicle kilometres operated have increased 15%since2013 andrepresented 45%ofallvehiclekilometrestravelled by public transport including rail and busservicesin 2016.

In2016 15%oftheoperatorsaccountedfor 90%ofallthecommercialpassengerjourneys made.

Table A: Overview of Commercial Bus Passenger Services Sector (millions)

Year AllPassengerJourneys

EstimatedFreeTravelPassengers

ScheduledKilometres

FreeTravelSchemePayments

AllRevenue (Ticket&

Free Travel)

2013 20.1 4.79 80.1 €20.06 €135.94

2016 25.24 5.29 92.08 €20.49 €176.11

Change 2013-2016

26% 10% 15% 2% 30%

1

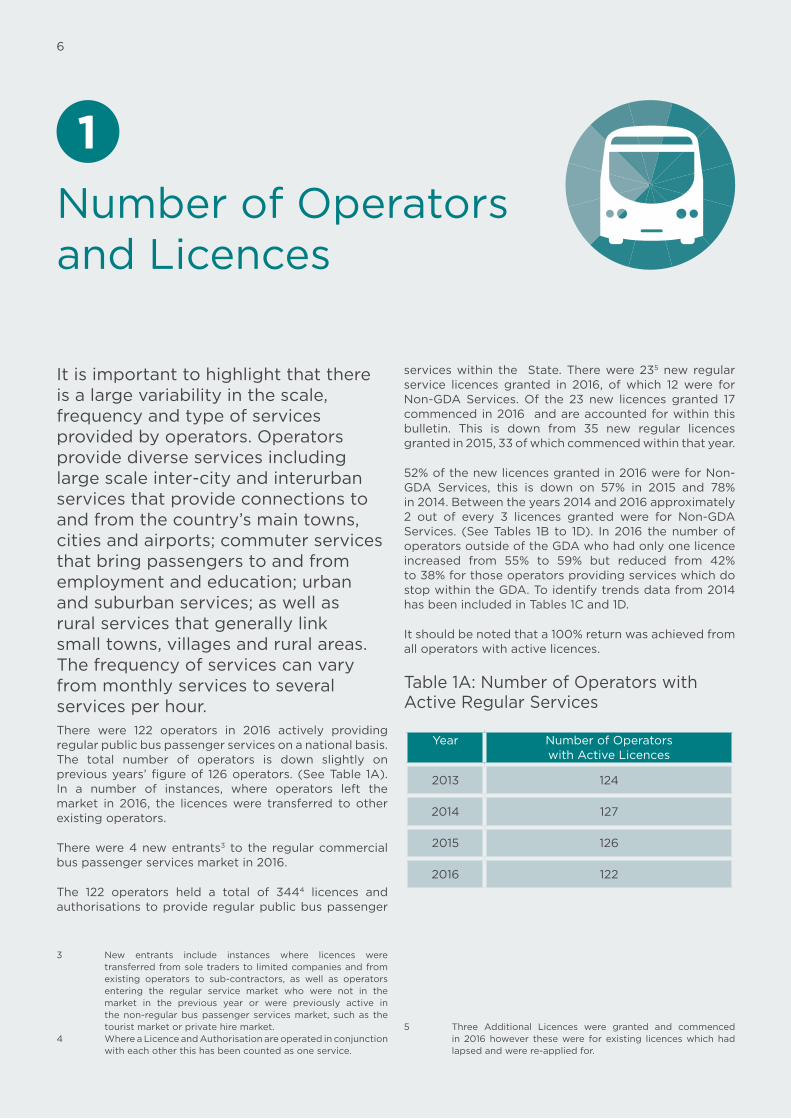

Number of Operators andLicences

Itisimportanttohighlightthatthereisalargevariabilityinthe scale,frequencyandtypeofservicesprovidedby operators.Operatorsprovide diverse services including largescale inter-cityandinterurbanservicesthatprovideconnectionstoandfromthe country’smain towns,citiesand airports;commuterservicesthatbringpassengerstoandfromemploymentand education;urbanandsuburban services;aswellasruralservicesthatgenerallylinksmall towns,villagesandrural areas.Thefrequencyofservicescanvaryfrommonthlyservicestoseveralservicesper hour.There were 122 operators in 2016 actively providingregularpublicbuspassengerservicesonanational basis.The total number of operators is down slightly onprevious years’ figureof 126 operators. (SeeTable 1A).In a number of instances, where operators left themarket in 2016, the licenceswere transferred tootherexisting operators.

Therewere4 newentrants3 to theregularcommercialbuspassengerservicesmarketin2016.

The 122 operators held a total of 3444 licences and authorisationstoprovideregularpublicbuspassenger

3 New entrants include instances where licences weretransferred from sole traders to limited companies and from existing operators to sub-contractors, as well as operatorsentering the regular service market who were not in themarket in the previous year or were previously active inthe non-regularbuspassengerservices market, suchas thetouristmarketorprivatehire market.

4 WhereaLicenceandAuthorisationareoperatedinconjunctionwitheachotherthishasbeencountedasone service.

serviceswithin the State.Therewere235 new regular service licences granted in 2016, ofwhich 12 were forNon-GDAServices.Of the 23 new licencesgranted 17commencedin2016 andareaccountedforwithinthis bulletin. This is down from 35 new regular licencesgrantedin2015,33ofwhichcommencedwithinthat year.

52%ofthenewlicencesgrantedin2016 wereforNon-GDA Services, this is down on 57% in 2015 and 78%in 2014.Betweentheyears2014 and2016 approximately2 out of every 3 licences granted were for Non-GDAServices. (SeeTables 1B to 1D). In2016 thenumberofoperatorsoutsideoftheGDAwhohadonlyonelicenceincreased from 55% to 59% but reduced from 42%to 38%forthoseoperatorsprovidingserviceswhichdostopwithinthe GDA.Toidentifytrendsdatafrom2014hasbeenincludedinTables1Cand1D.

Itshouldbenotedthata 100%returnwasachievedfromalloperatorswithactive licences.

Table 1A:NumberofOperatorswithActiveRegularServices

Year Number of Operators withActiveLicences

2013 124

2014 127

2015 126

2016 122

5 Three Additional Licences were granted and commencedin2016however thesewere forexisting licenceswhichhadlapsedandwerere-appliedfor.

6

Commercial Bus Statistics for Ireland | 7

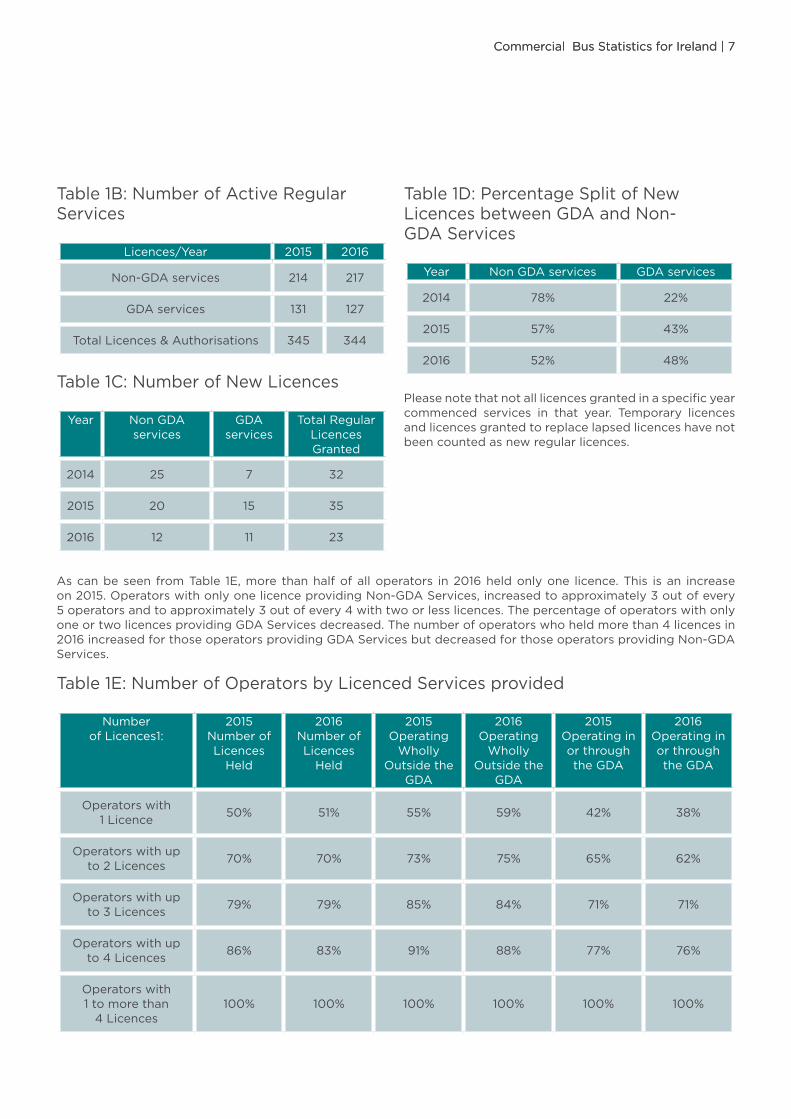

Table 1B:NumberofActiveRegularServices

Licences/Year 2015 2016

Non-GDAservices 214 217

GDAservices 131 127

TotalLicences&Authorisations 345 344

Table 1C:NumberofNewLicences

Year NonGDAservices

GDAservices

TotalRegular LicencesGranted

2014 25 7 32

2015 20 15 35

2016 12 11 23

Table 1D:PercentageSplitofNewLicencesbetweenGDAand Non-GDA Services

Year NonGDAservices GDAservices

2014 78% 22%

2015 57% 43%

2016 52% 48%

Pleasenotethatnotalllicencesgrantedinaspecificyearcommenced services in that year. Temporary licencesandlicencesgrantedtoreplacelapsedlicenceshavenotbeencountedasnewregular licences.

Table 1E:NumberofOperatorsbyLicencedServicesprovided

Number of Licences1:

2015 Number of Licences

Held

2016 Number of Licences

Held

2015Operating Wholly

OutsidetheGDA

2016Operating Wholly

OutsidetheGDA

2015Operating in orthroughtheGDA

2016Operating in orthroughtheGDA

Operatorswith1 Licence

50% 51% 55% 59% 42% 38%

Operatorswithupto2 Licences

70% 70% 73% 75% 65% 62%

Operatorswithupto3 Licences

79% 79% 85% 84% 71% 71%

Operatorswithupto4 Licences

86% 83% 91% 88% 77% 76%

Operatorswith1tomorethan4 Licences

100% 100% 100% 100% 100% 100%

Ascanbeseen fromTable 1E,morethanhalfofalloperators in2016 heldonlyone licence.This isan increaseon 2015.OperatorswithonlyonelicenceprovidingNon-GDAServices,increasedtoapproximately3 outofevery5 operatorsandtoapproximately3 outofevery4 withtwoorless licences.ThepercentageofoperatorswithonlyoneortwolicencesprovidingGDAServices decreased.Thenumberofoperatorswhoheldmorethan4 licencesin2016 increasedforthoseoperatorsprovidingGDAServicesbutdecreasedforthoseoperatorsprovidingNon-GDAServices.

Commercial Bus Statistics for Ireland | 7

8|Commercial Bus Statistics for Ireland

Figure 1.1:PercentageofOperatorsProvidingRegularServicesbyNumberofLicencesheld

Operators with 5 or more LicencesOperators with 4 LicencesOperators with 3 LicencesOperators with 2 LicencesOperators with 1 Licence

51%

17%

4%

9%

19%

Figure 1.2:PercentageofAllPassengerJourneysin2016byNumberofLicencesheld

Operators with 5 or more LicencesOperators with 4 LicencesOperators with 3 LicencesOperators with 2 LicencesOperators with 1 Licence

6%

68%

5%

3%

18%

Operatorswithonlyonelicenceaccountedfor6%ofallthepassengertripsnationallyin2016.Figures 1.1 and 1.2 givethepercentagebreakdownin2016 ofoperatorsbythenumberoflicencesheldandbypercentageofpassengertripsbynumberof licences.

ofAllPassengerJourneys

2

Total Number ofPassengerJourneys

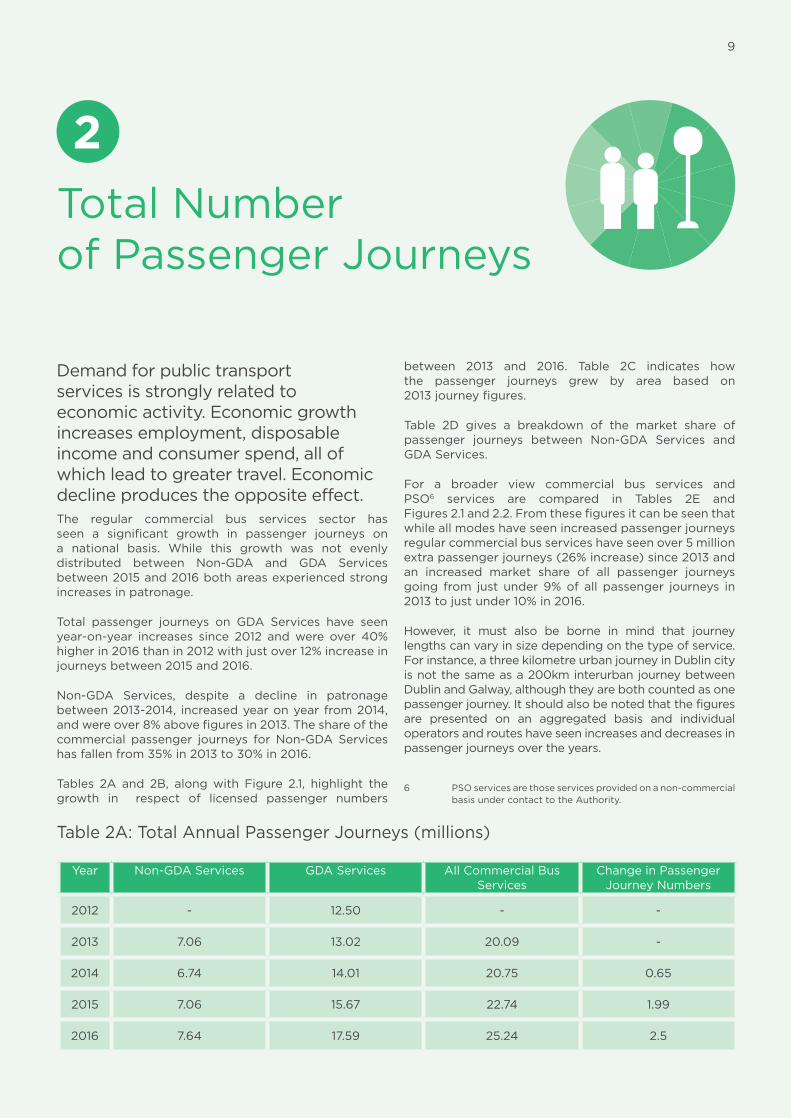

Demandforpublictransportservicesisstronglyrelatedtoeconomic activity.Economicgrowthincreases employment,disposableincomeandconsumer spend,allofwhichleadtogreater travel.Economicdeclineproducestheopposite effect.The regular commercial bus services sector hasseen a significant growth in passenger journeys ona national basis. While this growth was not evenlydistributed between Non-GDA and GDA Servicesbetween2015 and2016 bothareasexperiencedstrongincreasesin patronage.

Total passenger journeys on GDA Services have seenyear-on-year increases since 2012 andwere over 40%higherin2016 thanin2012 withjustover12%increaseinjourneysbetween2015 and 2016.

Non-GDA Services, despite a decline in patronagebetween 2013-2014, increasedyearonyearfrom2014,andwereover 8%abovefiguresin 2013.Theshareofthecommercial passenger journeys for Non-GDAServiceshasfallenfrom 35%in2013 to 30%in 2016.

Tables 2A and 2B, alongwith Figure 2.1, highlight thegrowth in respect of licensed passenger numbers

between 2013 and 2016. Table 2C indicates howthe passenger journeys grew by area based on2013 journey figures.

Table 2D gives a breakdown of the market share ofpassenger journeys between Non-GDA Services andGDA Services.

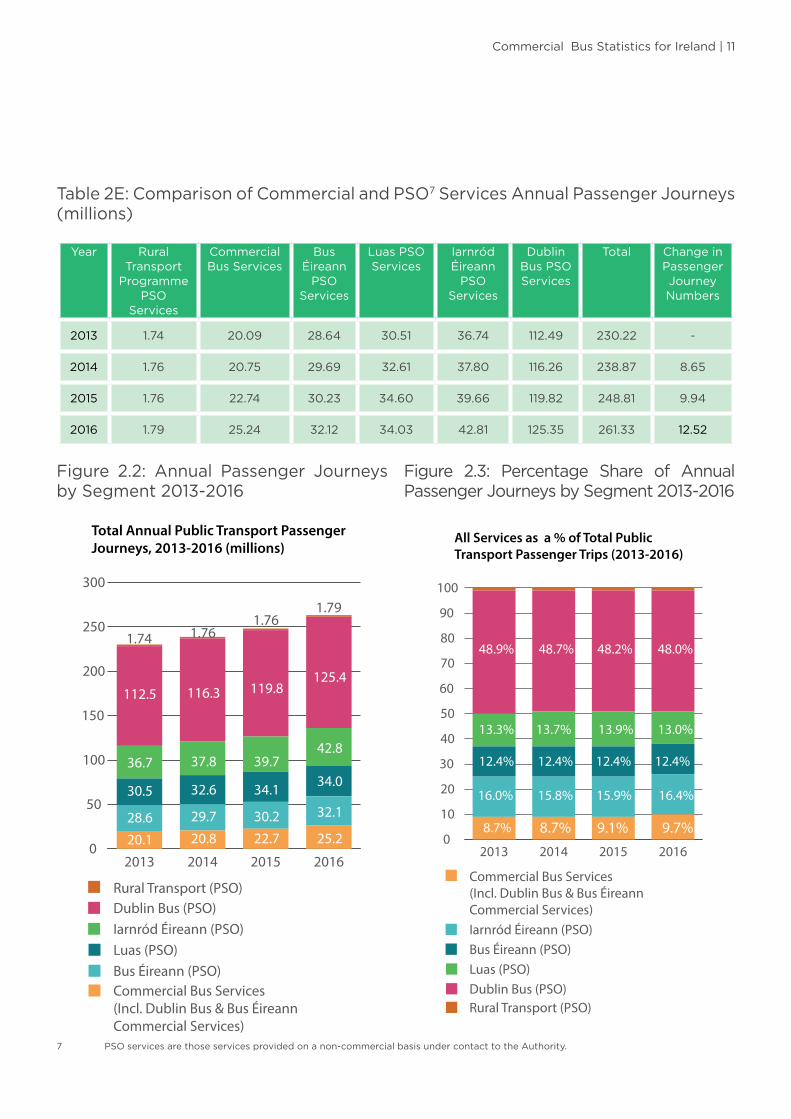

For a broader view commercial bus services andPSO6 services are compared in Tables 2E andFigures 2.1 and 2.2.Fromthesefiguresitcanbeseenthatwhileallmodeshaveseenincreasedpassengerjourneysregularcommercialbusserviceshaveseenover5 millionextrapassengerjourneys(26% increase)since2013 andan increased market share of all passenger journeysgoing from just under 9%of all passenger journeys in2013 tojustunder 10%in 2016.

However, it must also be borne in mind that journeylengthscanvaryinsizedependingonthetypeof service.For instance,athreekilometreurbanjourneyinDublincityisnotthesameasa200kminterurbanjourneybetweenDublinand Galway,althoughtheyarebothcountedasonepassenger journey.Itshouldalsobenotedthatthefiguresare presented on an aggregated basis and individual operatorsandrouteshaveseenincreasesanddecreasesinpassengerjourneysoverthe years.

6 PSOservicesarethoseservicesprovidedona non-commercialbasisundercontacttothe Authority.

Table 2A:TotalAnnualPassenger Journeys(millions)

Year Non-GDAServices GDAServices All Commercial Bus Services

ChangeinPassengerJourneyNumbers

2012 - 12.50 - -

2013 7.06 13.02 20.09 -

2014 6.74 14.01 20.75 0.65

2015 7.06 15.67 22.74 1.99

2016 7.64 17.59 25.24 2.5

9

10 | Commercial Bus Statistics for Ireland

Figure 2.1:ComparisonofTotalPassengerJourneysbyYear(millions)

Table 2B:PercentageChangeperYearinAnnualPassengerJourneys

Changefromprevious Year

Non-GDA

Services

GDAServices

All Commercial Bus Services

2014 -4.6% 7.6% 3.3%

2015 4.8% 11.9% 9.6%

2016 8.2% 12.2% 11.0%

Table 2C:PercentageChangefrom2013inAnnualPassengerJourneys

Changefrom 2013

Non-GDAServices

GDAServices

All Commercial Bus Services

2014 -4.6% 7.6% 3.3%

2015 0.0% 20.4% 13.2%

2016 8.2% 35.0% 25.6%

Table 2D:PercentageBreakdownintheStateofAnnualPassengerJourneys

Year Non-GDAServices GDAServices

2013 35% 65%

2014 32% 68%

2015 31% 69%

2016 30% 70%

All Commercial Bus Services GDA Services Non-GDA Services

0

5

10

15

20

25

30

2016201520142013

7.06

13.02

20.09

6.74

14.01

20.75

7.06 7.64

17.59

25.24

15.67

22.74

Total Annual Passenger Trips on Commercial Bus Services (millions)

Commercial Bus Statistics for Ireland | 11

Table 2E:ComparisonofCommercialandPSO7 Services Annual Passenger Journeys(millions)

Year RuralTransport

ProgrammePSO

Services

Commercial Bus Services

Bus ÉireannPSO

Services

LuasPSOServices

IarnródÉireannPSO

Services

DublinBusPSOServices

Total ChangeinPassengerJourneyNumbers

2013 1.74 20.09 28.64 30.51 36.74 112.49 230.22 -

2014 1.76 20.75 29.69 32.61 37.80 116.26 238.87 8.65

2015 1.76 22.74 30.23 34.60 39.66 119.82 248.81 9.94

2016 1.79 25.24 32.12 34.03 42.81 125.35 261.33 12.52

Figure 2.2: Annual Passenger Journeys bySegment 2013-2016

Figure 2.3: Percentage Share of AnnualPassengerJourneysbySegment2013-2016

Bus Éireann (PSO)Iarnród Éireann (PSO)

Commercial Bus Services (Incl. Dublin Bus & Bus Éireann Commercial Services)

Dublin Bus (PSO)Luas (PSO)

Rural Transport (PSO)

0

10

20

30

40

50

60

70

80

90

100

2016201520142013

48.9%

13.3%

12.4%

16.0%

8.7% 8.7% 9.1% 9.7%

48.7%

13.7%

12.4% 12.4% 12.4%

15.8%

48.2%

13.9%

15.9%

48.0%

13.0%

16.4%

All Services as a % of Total Public Transport Passenger Trips (2013-2016)

Iarnród Éireann (PSO)Dublin Bus (PSO)Rural Transport (PSO)

Bus Éireann (PSO)Luas (PSO)

Commercial Bus Services (Incl. Dublin Bus & Bus Éireann Commercial Services)

0

50

100

150

200

250

300

2016201520142013

112.5

1.74

36.7

30.5

28.620.1

116.3

1.76

37.8

32.6

29.720.8

119.8

1.761.79

39.7

34.1

30.222.7

125.4

42.8

34.0

32.1

25.2

Total Annual Public Transport Passenger Journeys, 2013-2016 (millions)

7 PSOservicesarethoseservicesprovidedona non-commercialbasisundercontacttothe Authority.

ScheduledVehicle Kilometres

‘ScheduledVehicleKilometres’indicatethenumberofvehiclekilometresthatabuscompanyplannedtooperateaspertheircumulative timetables.This measure has not increased significantly for Non-GDAservices.ForGDAServicestheincreasehasbeenpronounced, with 30% more kilometres scheduled in2016 than in 2012. Between 2013 and 2016 scheduledvehicle kilometres for GDA-Services have increased19%,whilepassenger journeyshave increasedby35%.Scheduled vehicle kilometres for Non-GDA Serviceshave increased by 3%, while passenger journeys haveincreasedby8.2%.

Table 3A provides the figures and Tables 3B-3Cshow the changes as a percentage. Tables 3D-3Eshow vehicle kilometres by each PSO operator andcommercial services.

Table 3A:AnnualScheduledVehicleKilometres(millions)

Year NonGDAServices

GDAServices All Commercial

Services

2012 - 55.10 -

2013 19.82 60.29 80.10

2014 19.32 62.83 82.15

2015 20.75 65.53 86.28

2016 20.40 71.68 92.08

Table 3B:PercentageBreakdownintheStateofTotalScheduledVehicleKilometres

Year NonGDAServices GDAServices

2013 25% 75%

2014 24% 76%

2015 24% 76%

2016 22% 78%

Table 3C:PercentageChangeinScheduledVehicleKilometresbyYear

Year NonGDAServices

GDAServices

All Commercial Bus Services On National Basis

2014 -2% 4% 3%

2015 7% 4% 5%

2016 -2% 9% 7%

2013-2016

3% 19% 15%

3

12

Commercial Bus Statistics for Ireland | 13

Table 3DOperated Vehicle Kilometres for PSO Services and Scheduled VehicleKilometresforCommercialBusServices(millions)

Year Luas IarnródÉireann BusÉireannPSO DublinBusPSO

All Commercial Bus Services Total

2013 3.54 15.97 33.34 50.30 80.10 183.25

2014 3.67 15.97 32.94 54.73 82.15 189.46

2015 3.66 15.97 33.76 55.34 86.28 195.01

2016 3.49 15.96 35.74 55.32 92.08 202.59

Table 3D shows scheduled vehicle kilometres forregular commercial bus services and compares thisto the operated vehicle kilometres for PSO Bus andRailservices. ‘Operatedvehiclekilometres’refertotheactual amount of vehicle kilometres that a bus or rail

companyhasoperatedforagivenperiod,asopposedtothe‘scheduledvehiclekilometres’whichwouldindicatethenumberofvehiclekilometresthattheyintendedtooperate.

Table 3E:PercentageChangeVehicleKilometresbyServiceType

Year Luas IarnródÉireann BusÉireannPSO DublinBusPSO All Commercial Bus Services

2013 2% 9% 18% 27% 44%

2014 2% 8% 17% 29% 43%

2015 2% 8% 17% 28% 44%

2016 2% 8% 18% 27% 45%

4

Commercial Bus ServicesRevenue andTicketing

Thevastmajorityoftheoveralllicensed commercial bus services revenueisfromticketrevenue(over 88%in 2016). FreeTravelSchemepaymentsaccountedforjustover 11%ofthetotalrevenuein 2016.Thisislowerthanin2013, whenFreeTravelSchemepaymentsrepresentedjustover 14%of revenue.TaxSaverTicketingwasofferedby 23%ofOperatorsin 2016.Regular commercial bus service revenue consists ofall revenue fromticket sales (including cash, TaxSaver,Leap Card, online&prepaid tickets) andpayments tooperators participating in the Department of SocialProtection’s Free Travel Scheme. Regular commercialbus services include licensed bus services operating wholly within the State and bus services which crosstheborder intoNorthern Irelandandaresubjecttoanauthorisation.

TaxSaverTicketing

The TaxSaver Commuter Ticket Scheme allowsemployees purchase annual/monthly public transportcommuterticketsiftheyaretravellingtoorfromworkby public transport. The scheme involves employersproviding employees with the facility to pay for theticketsover themonth/yearwhile savingonemployerPRSIpayments.Thescheme isgenerallyknownastheTaxSaver Scheme but other names can be used byindividualpublictransport operators.

SmartCardTicketing

Smartcards are the technological successor to magnetictickets. Smart cards contain a microchip that stores andtransmitsdataenablingthemtocommunicatewithasmart

card reading device without actually touching it. Periodticketssuchas Annual,MonthlyandWeeklyTickets,aswellas Pay-As-You-Gocreditcanbestoredonthe cards.ThetwomainsmartcardsaretheLeapCardandtheSmartlink card.TheLeapCard is theonly inter-operablepublic transportsmartcardwithinthe State.TheSmartlinkCardisavailablefrom Ulsterbus, who operate a number of cross-borderservices.

LeapCard

TheLeapCardwas first introduced in late2011 and isan integrated smart card which is available for bothpubliclysubsidisedandcommerciallylicensed services.In2014 theschemewasextendedtotheGreaterCorkArea and in 2016 includes services in Galway City,Limerick City, Waterford City and Wexford. TaxSaverTicketsarenowavailableontheLeapCard.In November 2016 the2 millionthLeapCardwas sold.

Therewere12operatorsin2016withLeapCardontheirregularcommercialbusservices.ThesewereSt.Kevin’sBus,AshbourneConnect,DualwayCoaches,CityDirectGalway,Citylink,CollinsCoaches,ExpressBus,MatthewsCoaches, Swords Express, Wexford Bus, Dublin BusandBusÉireann.(DublinBusandBusÉireannrunbothcommercialandPSOservices).

FreeTravelRevenue

Anumber of commercial bus services are part of theDepartmentofSocial Protection’sFreeTravel Scheme.OperatorsthatarepartoftheschemereceivepaymentsforthefareforgoneforcarryingpassengersentitledtoFree Travel.OverallFreeTravelPayments(listedas“FTPayments”inthetables)tocommercialoperatorsaresetoutbelowandincludepaymentsforFreeTravelwithinthestateforbothIrishandNorthernIrishpassengers,aswellaspaymentsforcrossborderFreeTravel.TheTotalAnnualFTPaymentsintheTablesincludepaymentsforBusÉireann’sExpresswayServices.

14

Commercial BusStatisticsforIreland|15

Table 4A shows the total ticket revenue and free travelschemepaymentsfortheregularcommercialbusservicessectorbetween2013 and 2016. This includes figures forthe licensed Bus Éireann Expressway and Dublin BusAirlink services.Thefreetravelpaymentsareinclusiveofpaymentsforcrossbordertravelandinternationalforeignfree travel payments. Table 4B shows the percentagechangeinrevenueperyearandTable4Cshowsthechange

between revenue, passenger journeys, and scheduledvehiclekilometresbetween2015 and 2016.

In 2016 of all operators providing regular commercialbusservices, 23%offeredoneormoretypesofTaxSaverTicket.

Table4DshowsthenumberandpercentageofoperatorsofferingTaxSaverTicketing.

Table 4A:AnnualPassengerRevenue(millions)

Year Total Annual TicketRevenue

TotalAnnualFTPayments

TotalRevenue FTPaymentsasaPercentofAllRevenue

2013 €115.889 €20.055 €135.944 14.8%

2014 €129.546 €20.101 €149.646 13.4%

2015 €143.187 €20.425 €163.612 12.5%

2016 €155.623 €20.487 €176.110 11.6%

Table 4B:PercentageChangeinRevenuebyYear

Year ChangeinAnnualTicket

Revenue

ChangeinAnnualFTPayments

Changein Total Revenue

2014 12% 0% 10%

2015 11% 2% 9%

2016 9% 0% 8%

Table 4C:PercentageChangeinTicketRevenue,VehicleKilometresandPassengerJourneys(millions)

Year TicketRevenue(Excl.FT Payments)

VehicleKilometres

PassengerJourneys

2016 9% 7% 11%

Table 4D:NumberofOperatorsofferingTaxSaverTicketing

Year Operators Offering 1 orMoreTaxSaver

Tickets

PercentofAllOperators Offering TaxSaverTickets

2013 17 14%

2014 27 21%

2015 25 20%

2016 28 23%

5

FreeTravel PassengerJourneys

TheDepartmentofSocial Protection’sFreeTravelSchemeisavailabletoallpersonsaged66 andoverlivingpermanentlyinthe State.Somepeopleunder66 mayalsoqualifysuchascarersinreceiptofa Carer’sAllowanceandcertainotherpersonsinreceiptofaDisabilityAllowanceorInvalidity Pension.Free travelwasavailableonState fundedbusand railtransport including Dublin Bus, Bus Éireann, IarnródÉireannandLuas services.Free travel isalsoavailableon a number of licensed commercial services operated by private bus companies and Bus Éireann. Since1995 Northern Ireland Senior Citizens aged 65+ havebeen eligible for limited cross border free travel from anypoint inNorthern Irelandtoanydestination intheRepublicof Ireland.

The provisionwas further expanded in 2007, to alloweligibleNorthernIreland65+SeniorSmartPass holders,to travel for free not only to a destination across theborder but also on internal public transport services whentheyarriveintheRepublicof Ireland.

AspartoftheAnnualBusOperatorReturnsoperatorsestimatethenumberofFreeTravelPassengerJourneysas a percentage of all journeys for each licenceand authorisation.TheestimatedtotalnumberofFreeTravel Passenger Journeys has risen between 2013 and2016 by 10%onanational basis,(SeeTable 5A).However,duetotheoverallgrowthlevelsinpassengerjourneysinthesameperiod(25.6%)thepercentageofallpassengerjourneyswhichwereFreeTravelPassengerJourneyshasdecreasedfrom 24%ofallcommercialbuspassengerjourneysin2013 to 21%in 2016.

These changes are not evenly distributed acrossthe State. In fact onNon-GDAServices,while overallpassengerjourneyshaveincreased 8.2%between2013 and2016 theestimatednumberofFreeTravelPassengerJourneyshasrisenbyanestimated 27%goingfrom 36%ofalljourneysin2013 to 43%in 2016.Thesameisnottrue

ofGDAServiceswhichhaveanestimated 9%decreaseinFreeTravelPassengerJourneysoverthesameperiodwiththepercentageofsuchjourneysreducingfrom 17%ofallcommercialbuspassengerjourneysin2013 to 12%in 2016. These reported changes mean that Non-GDA Services increased the percent share of all FreeTravelPassengerJourneys from 54%ofallFreeTravelPassengerJourneysonregularcommercialbusservicesin2013 to 62%in 2016.

Table 5A shows the estimated Free Travel PassengerJourney figures while Table 5B and 5C give thepercentages.

Table 5A:EstimatedNumberofFreeTravelPassengerJourneys(millions)

Year LicensedServices Nationally

Licensed Non-GDAServices

LicensedGDAServices

2013 4.79 2.57 2.22

2014 4.73 2.84 1.89

2015 4.92 2.94 1.98

2016 5.29 3.26 2.03

16

Commercial Bus Statistics for Ireland | 17

Table 5B:EstimatedFreeTravelPassengerJourneysasaPercentageofAllPassengerJourneys

Year LicensedServicesNationally Licensed Non-GDAServices

LicensedGDAServices

2013 24% 36% 17%

2014 23% 42% 13%

2015 22% 42% 13%

2016 21% 43% 12%

Table 5C:PercentageshareofEstimatedFreeTravelPassengerJourneys

Year Licensed Non-GDAServices LicensedGDAServices

2013 54% 46%

2014 60% 40%

2015 60% 40%

2016 62% 38%

Itshouldbenotedthatthesefigureshavebeencalculatedbymultiplyingthetotalnumberofpassengerjourneyswiththeestimatedpercentageoffreetravelpassengerjourneysprovidedbyoperators.Thefiguresshouldthereforebetakenasindicativeonlyratherthanprecise calculations.

6

Commercial OperatorFleetSize

Thenumberofvehiclesthatwereusedin2016 toprovideregularcommercialbusservicesintheStatewas 1371.TheAuthorityalsoaskedlicensedoperatorswhethertheirvehicleswerealsousedforotheractivitiesas well,toshownotonlyhowmanyvehiclesoperatorsusedtoprovidetheirregularcommercialbusservices,butalsohowmuchthesevehicleswereusedsolelyforrunningtheirregularcommercialbusservices services.For example,ifanoperatorhadjustonebusandthisbuswasused 70%ofthetimeforregularlicencedservicesand 30%ofthetimeforprivatehire services,thentheoperator would count that as 0.7 of a vehicle whenreportingtheirexactnumberofbuses used.

Usingthismethodofcalculationtherewere1125 busesusedonafulltimebasistoprovideregularpassenger services.Thisisup16%since2013.

Table 6A:NumberofVehiclesUsedtoProvideRegularCommercialBusServices

Number of Vehicles/Year

2013 2014 2015 2016

Number of vehiclesusedonfull time basis:

969 1,037 994 1,125

Number of vehiclesCounted:

1,062 1,227 1,223 1,371

Figure 6.1:PercentageofOperatorsbyNumberofVehiclesUsedtoProvideRegularCommercialBusServices

Operators using more than 10 vehiclesOperators Using 6 -10 vehiclesOperators using 3 -5 vehicles Operators Using 1-2 vehicles

11%

68%

13%

7%

Percentage of Operators by vehicles used

Vehiclesreferredtointhetablesincludeabroadvarietyof vehicles,suchas inter-city coaches, low-floorurbandouble and single decker buses, as well as midi andmini buses. These vehicles have a range of differentdesigns and passenger seat capacities. The vehiclesusedaregenerallytosuitthetypeofroutebeing served.

18

7

Commercial Operating FleetAccessibilityandScheduleKilometresOperatedbyAccessibleVehicles

Thepercentageofvehicleswhichare accessible is one measure of accessibilityofthefleet,howeveranotherkeyindicatoristheamountofscheduledvehiclekilometrestheseaccessiblevehiclesareusedtoprovide.Since2013thereportednumberofwheelchairaccessiblevehicles used on regular commercial services hasremainedatapproximately 2vehiclesforevery5vehiclesused. The number of vehicles which are reported asbeing low-floor suitable for wheelchair access hasincreasedfrom 13%in2013 to 16%in2016, butascanbeseen,remainslowasapercentageoftheoverall fleet.

WheelchairAccessibility

It is important to highlight that a vehicle can beeither low-floor wheelchair accessible or wheelchairaccessible through theuseofa lift.Thereareasmallnumberofvehicleswithinthisfleetthatareaccessibletowheelchairsbybeingboth low-floorandhavingtheuseofa lift,althoughthisisless common.Suchvehicleshavebeencountedasoneaccessible vehicle.

CommercialOperatingfleetthatarelowfloor vehicles suitable for wheelchairaccess

Low-floor wheelchair accessible vehicles are vehicleswhere access from the bus stop to part or all of thepassengerareaisdirectfromthebusstop apron.Therearenostepsinvolvedandawheelchair lift isnot used.Optionally, the vehicle may lower to kerb level andtheremaybeanentryandexitaccess ramp forquick

andsafewheelchair access.Thisenableseasieraccessfor wheelchair users and thosewith limited mobility.Accessing low-floor vehicles can also require thatappropriatebus stop infrastructure, for instance kerbsofaspecific height,arein place.

Commercial Operating fleet that haveliftssuitableforwheelchairaccess

Vehicles with wheelchair lifts raise the individual andtheirwheelchairabovethestepsofthebusandintothevehiclecorridorarea.Thisfeaturerequiresadeepspaceatthefootpathwhichisnotalwaysavailable.Theuseofwheelchairliftsincreasesthedwelltimeatbusstopsandmaynotbeaspreferableforthepassengerasthelow-floor, roll-on/roll-off option. Vehicles with wheelchairlifts are often only able to carry one passenger usingawheelchairatanygiventimeasonlyonedesignatedwheelchairspacemaybeavailable.

It can also be the case that the customer using awheelchairmayneedtoinformtheoperatorinadvancethat they wish to use the service because seatingmayneed tobe removed toprovide for a designatedwheelchair space.

ScheduledVehicleKilometresoperatedbywheelchairaccessiblevehicles

Estimatesofthescheduledvehiclekilometresoperatedbywheelchairaccessiblevehicleshavebeenset outinTables7Cand7D.ForbothGDAandNon-GDAServicesthere has been a trend of increased provision of theservices by accessible vehicles. On a National basisthefigures indicateanoverallchangefrom 39%ofallscheduledvehiclekilometresin2013beingprovidedbyaccessiblevehiclesto 61%in2016.

19

20 | Commercial Bus Statistics for Ireland

Thefiguressetoutbelowarederivedfromestimationsby operators. They are intended to be read as guidefigures to indicate trends as opposed to being exact calculations.

Forexample,ifanoperatorhadthreevehiclesandonewas wheelchair accessible (being either low floor orhavingawheelchair lift)thenyouwouldexpectthat 33%ofthetotalscheduledkilometreswouldbeoperatedwithaccessible vehicles. However,ifthewheelchairaccessiblevehiclewasregularlyusedforlicensed services,whereastheothervehicleswereusedlessoftenorusedas spares,

then you would expect the percentage to be muchhigherbecausemostoftheirserviceswouldbeprovidedwiththewheelchairaccessible vehicles.

Thepercentagesarearrivedatbymultiplyingtheoverallscheduled kilometres by the percentage of accessiblevehicles used. The percentage of accessible vehiclesusediscalculatedbasedonthetotalnumberofvehiclescountedbyan operator,ratherthanasapercentageofthenumberofvehiclesusedonafulltime basis,asdatahasbeenprovidedonthebasisofthetotalnumberofaccessiblevehicles available.

Table 7A:NumberofAccessibleVehicles

Year VehiclesthatareLow-FloorWheelchair

Accessible

VehicleswithliftssuitableforWheelchair

access

Total Accessible Vehicles

Total Number of Vehiclesused

2013 137 308 445 1062

2014 148 279 428 1227

2015 176 321 497 1223

2016 217 382 599 1371

Table 7B:PercentageofAllVehiclesusedwhichareAccessibleVehicles

Year VehiclesthatareLow-FloorWheelchairAccessible

VehicleswithliftssuitableforWheelchairaccess

TotalAccessibleVehicles

2013 13% 29% 42%

2014 12% 23% 35%

2015 14% 26% 41%

2016 16% 28% 44%

Table 7C: Estimation of Scheduled Vehicle Kilometres provided by AccessibleVehiclesbasedonDataprovidedbyOperators(millions)

Year AllNon-GDA

ServicesKM

AccessibleNon-GDAServicesKM

AllGDAServices

KM

AccessibleGDAServicesKM

NationallyAllScheduledKM

Accessible ScheduledKM

Nationally

2013 19.8 7.1 60.3 24.3 80.1 31.4

2014 19.3 7.6 62.8 28.3 82.2 35.9

2015 20.7 11.1 65.5 36.4 86.3 47.4

2016 20.4 11.9 71.7 44.0 92.1 55.8

Commercial Bus Statistics for Ireland | 21

Table 7D:PercentageofAllScheduledVehicleKilometresprovidedbyAccessibleVehiclesbasedonEstimations

Year AccessibleNon-GDAServicesScheduledKM

AccessibleGDAServicesScheduledKM

AccessibleScheduledKMNationally

2013 36% 40% 39%

2014 39% 45% 44%

2015 53% 55% 55%

2016 58% 61% 61%

8

Commercial Operating FleetwithAutomatic VehicleLocation(AVL) Systems

AutomaticVehicleLocation(AVL)isthetermusedforautomaticallydeterminingthegeographiclocationofavehicle.Vehiclesaregenerallytrackedbyplacingaglobalpositioningsystem(GPS)electronicdeviceinoronthevehicle.ThenumberofvehicleswithAVLisnowatapproximately70%ofallvehiclesusedtoprovideregularcommercialbusservices.(SeeTables8aand8B).

There are a number of benefits to AVL, especiallyin a public transport context. It allows an operator tomanagetheirfleetbetter,knowwherethevehiclesareatanygiventime,anditfacilitatestheprovisionofrealtimepassengerinformation(RTPI).

ItshouldbenotedthatalthoughmanyAVLsystemsmaybeofbenefittoanindividualoperator,onlyspecificAVLsystemsarecompatibletotheState’sRTPIfacilitythatis available throughon-streetdisplays,websites, apps,orSMSservice.ThereforehavingvehicleswithAVLonboard would not be a sufficient guide as to whethertheseservicescouldparticipateintheRTPIfacility.

Table8A:NumberofVehicleswithAVL

Year Number of Vehicleswith

AVL

TotalNumberofVehiclesused

2013 639 1062

2014 812 1227

2015 807 1223

2016 960 1371

Table8B:PercentageofAllVehiclesusedwhichhaveAVL

Year VehicleswithAVL

NumberofvehiclesusedtoprovideRegularServicesonaFulltime

basis

2013 60% 1062

2014 66% 1227

2015 66% 1223

2016 70% 1371

22

9

CommercialFleetAge

Theaverageageofafleetisanimportantmeasure,astheageofavehiclecaninfluenceaccessibilitystandards,vehicleemissionlevels,fuelefficiency,vehiclesafetyfeatures,maintenancerequirements,andreliability.Maintainingandattractingpassengers,whocanhavea preference for travelling on newer buseswithenhancedfeaturesanddesigns,mustalsobeconsidered.

Theaveragevehicleagehaschangedfrom6.8yearsto7yearsbetween2013and2016.Duringthesameperiodthe total number of vehicles used to provide regularcommercialbusservicesonafulltimebasisincreasedby156vehiclesfrom969vehiclesin2013to1,125vehiclesin2016.Thesefiguresdemonstratethatthereisinvestmentin the commercial fleet, which maintains an averagevehicleage.(SeeTable9A).

Table9A:AverageAgeofVehiclesusedto provide services

Year 2013 2014 2015 2016

AverageVehicleAge(Years)

6.8 6.6 6.8 7.0

23

Further information

Media enquiries: Statistical enquiries:

Dermot O’Gara Ciaran O’Gorman

T.+353 (0)18798346 T.+353 (0)1 8798363