Commercial Banking System

44

Commercial Banking System

-

Upload

rohit-kochhar -

Category

Economy & Finance

-

view

21 -

download

0

Transcript of Commercial Banking System

Commercial Banking System

Commercial Banking System

• Topics– Definition and Nature– Evolution– Functions of Commercial Banks– Products of commercial banks

Definition and Nature

Definition of Commercial Banks

• Definition of banks take into account what types of task is performed by the banks. – According to the Indian Banking Company Act

1949, “A banking company means any company which transacts the business of banking. Banking means accepting of deposits from the public, for the purpose of lending or investment, payable on demand or otherwise withdraw able by cheque, draft or otherwise.”

Nature of Commercial Banks

• Commercial banks are an organisation which normally performs certain financial transactions. It performs the twin task of accepting deposits from members of public and make advances to the needy and worthy people from the society.

Evolution

Evolution – Phase I

• Phase I - Pre Nationalisation Phase(prior to 1955)– The first banks were

• The General Bank of India – started in 1786• The Bank of Hindustan – started in 1790

– Both are now defunct

• The East India Company established – Bank of Bengal – 1809– Bank of Bombay – 1840– Bank of Madras – 1843

• as independent units and called it Presidency Banks.• The three Presidency Banks merged to form Imperial Bank of India –

1921(which, upon India’s independence, became the State Bank of India).

Evolution – Phase I (Contd….)

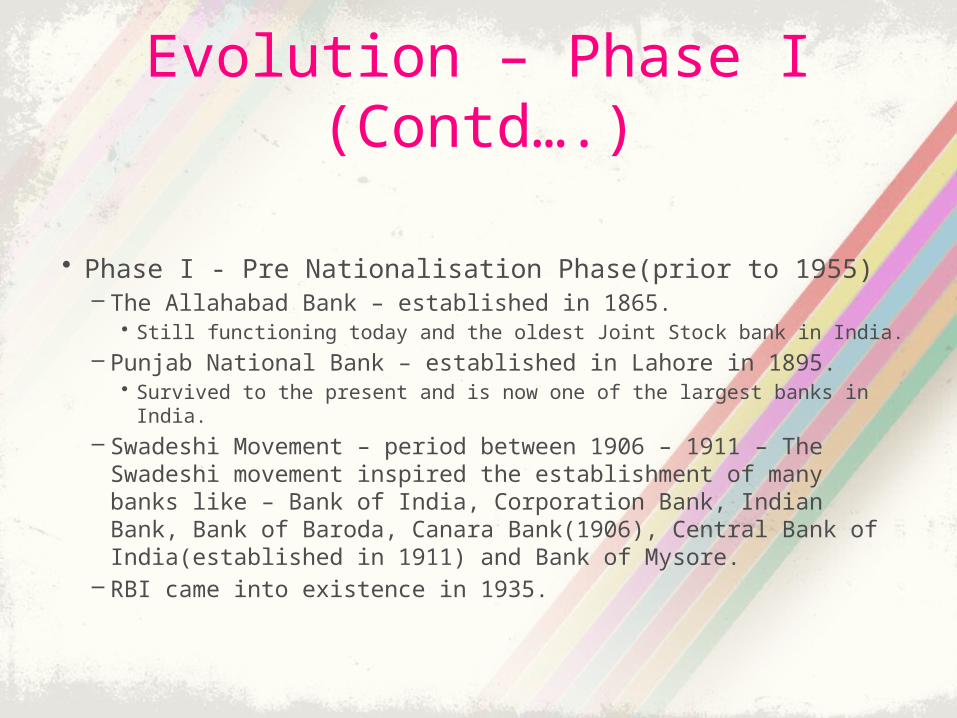

• Phase I - Pre Nationalisation Phase(prior to 1955)– The Allahabad Bank – established in 1865.

• Still functioning today and the oldest Joint Stock bank in India.

– Punjab National Bank – established in Lahore in 1895.• Survived to the present and is now one of the largest banks in India.

– Swadeshi Movement – period between 1906 – 1911 – The Swadeshi movement inspired the establishment of many banks like – Bank of India, Corporation Bank, Indian Bank, Bank of Baroda, Canara Bank(1906), Central Bank of India(established in 1911) and Bank of Mysore.

– RBI came into existence in 1935.

Evolution – Phase I (Contd….)

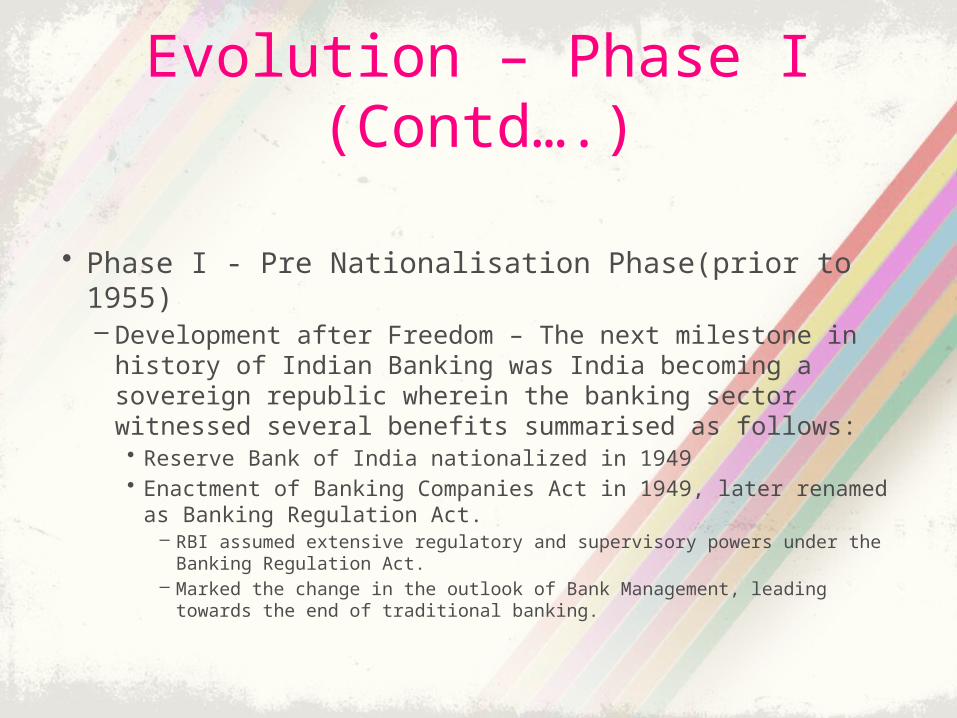

• Phase I - Pre Nationalisation Phase(prior to 1955)– Development after Freedom – The next milestone in history

of Indian Banking was India becoming a sovereign republic wherein the banking sector witnessed several benefits summarised as follows:• Reserve Bank of India nationalized in 1949• Enactment of Banking Companies Act in 1949, later renamed as

Banking Regulation Act.– RBI assumed extensive regulatory and supervisory powers under the

Banking Regulation Act.– Marked the change in the outlook of Bank Management, leading towards

the end of traditional banking.

Evolution – Phase II

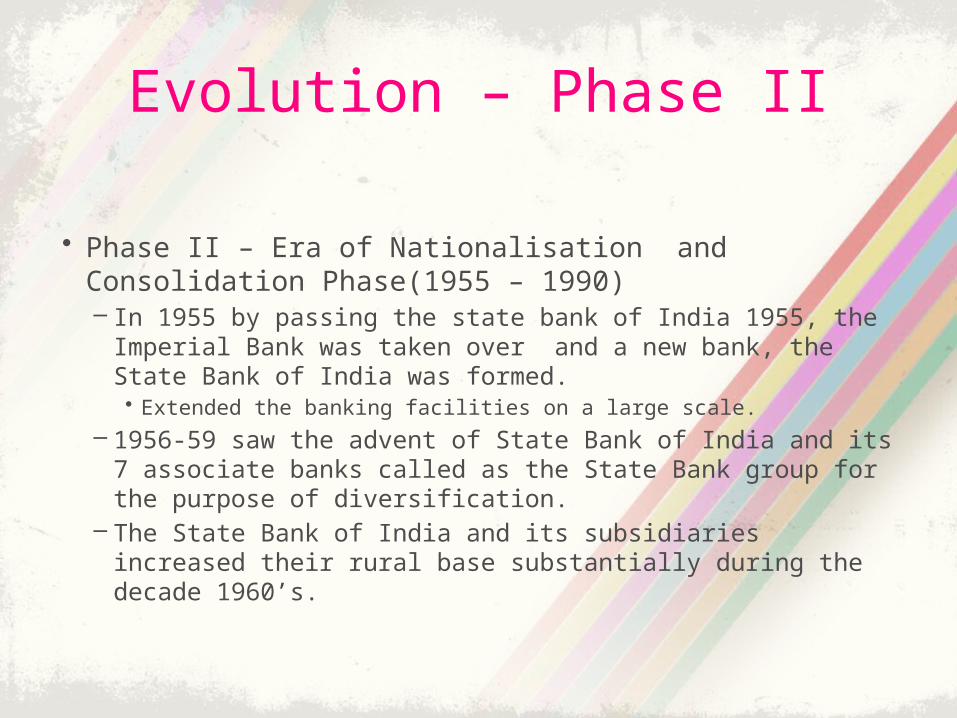

• Phase II – Era of Nationalisation and Consolidation Phase(1955 – 1990)– In 1955 by passing the state bank of India 1955, the Imperial

Bank was taken over and a new bank, the State Bank of India was formed.

• Extended the banking facilities on a large scale.

– 1956-59 saw the advent of State Bank of India and its 7 associate banks called as the State Bank group for the purpose of diversification.

– The State Bank of India and its subsidiaries increased their rural base substantially during the decade 1960’s.

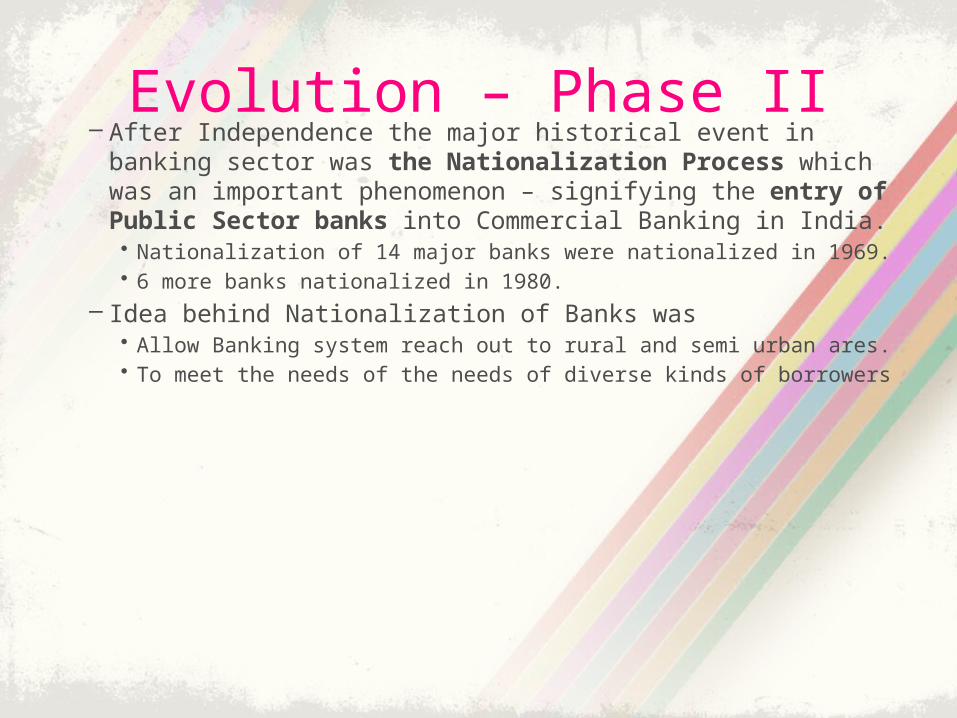

Evolution – Phase II– After Independence the major historical event in banking

sector was the Nationalization Process which was an important phenomenon – signifying the entry of Public Sector banks into Commercial Banking in India.• Nationalization of 14 major banks were nationalized in 1969.• 6 more banks nationalized in 1980.

– Idea behind Nationalization of Banks was• Allow Banking system reach out to rural and semi urban ares.• To meet the needs of the needs of diverse kinds of borrowers

Evolution – Phase II

– The nationalization of the Banks marked the beginning of the expansion phase of the Indian Banking Industry.• Objective of the expansion phase – expand the Banking facilities in

deficit areas and reduce inter-state and inter-district disparities to support development activities.

• The expansion phase was marked by geographical and numerical increase of the Bank branches.

– Consolidation Phase – • 1985 – series of policy measures introduced by RBI to strengthen

Public Sector Banks.• Emphasis on internal control, customer services, credit

management, staff productivity, and profitability of banks.

Evolution – Phase II

– In 1990 – Balance of Payment Crisis occurred showing that the economic policies were out of line with the changing environments.

– This crisis facilitated major changes in 1990’s

Evolution – Phase III

• Phase III – Liberalisation Phase(1990 onwards)– 1990’s – Narasimha Rao Government embarked on a

policy of liberalisation and licensing of a small number of Private Sector Banks.• The Private Sector Banks came to be known as New

Generation Tech savvy Banks.• New generation banks included

– Global Trust Bank(later amalgamated with Oriental Bank of Commerce).– Axis Bank(earlier as Unit Trust of India)– Industrial Credit and Investment Corporation of India Bank(ICICI)– Housing Development Finance Corporation Limited Bank(HDFC)

Evolution – Phase III

– Relaxation in the norms related to Foreign Direct Investment.

– This phase witnessed the liberal entry of Private and Foreign Banks, operational freedom, deregulation of the interest rates, reduction in the SLR and CRR.

– Brought in competitiveness and helped in improving profitability.

– Another significant instance of this phase was the entry of mass Computerisation to handle increased volumes of business effectively and to improve customer service.

Evolution – Phase III

– 1992 onwards –Banking Sector reforms undertaken in India – primarily aimed at the safety and soundness of the financial system and to make the Banking industry strong, efficient and competitive.

– Indian Banking Industry categorized into Scheduled Banks and Non-Scheduled Banks.

– Scheduled Banks constituted of Commercial Banks and Co-operative Banks.

– Year 1998 onwards – New delivery channels developed – ATM, Phone Banking, Internet Banking etc.

– Need for centralised database – due to alternate delivery channels – solution was Core Banking Solutions(CBS)

Evolution – Phase III

– As a part of financial sector reforms State Banks were given operational flexibility and functional autonomy by diluting the stake of the Indian Government to 51 percent.

– 2004 – Reforms in monetary and credit policy introduced.– Another major emphasis in this phase was to have international

accounting standards – introduced in phased manner with a view to make the Indian Banks internationally competitive with sound capital base.

– During this phase the RBI stressed on objectives like• Strengthening of prudential and supervisory norms for Banks, Improving

credit delivery system, Developing technological and institutional infrastructure for efficient financial sector, Ensuring stability, Modernising the payment system.

Functions of Commercial Banks

Functions of Commercial Banks

• Commercial Banks perform a variety of functions broadly classified as – Primary Functions– Secondary Functions

Functions of Commercial Banks

• Primary Functions or Banking Functions– Accepting deposits– Making Advances– Credit Creation

• Secondary Functions or Non Banking Functions– Agency Services– General utility services

Functions of Commercial Banks• Primary Functions or Banking Functions

– Commercial Banks performs various primary functions :• Accepting Deposits – Commercial bank accepts various

types of deposits from public especially from its clients. It includes Savings account deposits, recurring account deposits, fixed deposits etc. These deposits are payable at certain time periods.

• Making Advances – The commercial banks provide loans and advances in various forms. It includes an over draft facility, cash credit, bill discounting etc. They also give demand and term loans to all types of clients against property security.

Functions of Commercial Banks

• Credit Creation – It is the most significant function of the Commercial Banks. While sanctioning a loan to a customer, a bank does not provide cash to the borrower. Instead it opens a deposit account from where the borrower can withdraw. In oter words while sanctioning a loan a bank automatically creates deposits. This is known as a credit creation from commercial banks.

Functions of Commercial Banks• Secondary Functions

– The secondary functions of commercial banks can be divided into agency functions and utility functions:• Agency Functions – Banks perform certain functions on

behalf of their customers. While performing these services, banks act as agents to their customers and hence these are called agency services.Various agency functions of commercial banks are:

– To collect and clear cheques, dividends , interest warrants and any other receipts which are to be received by the customer. For these services banks charge a nominal amount.

– Banks make payments on behalf of their customers like paying rent, insurance premiums, taxes, elecricity, phone bills etc for which commission is charged.

Functions of Commercial Banks– To deal in foreign exchange transactions– To purchase and sell securities – As per customers

instructions banks undertake sale and purchase of securities, shares and any other financial assets for nominal charges.

– To act as trusty, attorney, correspondent and executor – As a trustee, banks become custodian and manager of customer funds. Bank also act as executor of deceased customer’s will. As an attorney the Banks sign the documents on behalf of the customer.

– To accept tax proceeds and tax returns

Functions of Commercial Banks• General Utility Functions – The General Utility functions of

the commercial banks include– To provide safety locker facility to customers– To provide money transfer facility– To issue traveller’s cheque.– To act as referees. – Banks supply information about business

transactions and financial standing of their customers on enquiries made by third parties.

– To accept various bills for payment eg. Phone bills, gas bills, water bills etc.

– To provide merchant banking facility. – This is the function of underwriting of securities. They underwrite a portion of the Public issue of shares, debentures and bonds. Such underwriting ensures the expected minimum subcription and also convey to the public about the quality of the company issuing the securities.

– To provide various cards such as credit cards, debit cards, smart cards etc.

Products of Commercial Banks

Products of Commercial Banks• The products of the Banking industry broadly

include: – deposit products, – credit products and – customized banking services.

• Most banks offer the same kind of products with minor variations. The basic differentiation is attained through quality of service and the delivery channels that are adopted.

Products of Commercial Banks• Deposit Products – Deposit Products are of 2

types– Time Deposit – These are deposits repayable

after a certain fixed period. These deposits are can not be withdraw by cheque, draft or by other means. It includes the following• Fixed Deposits –

– Deposits can be withdrawn only after expiry of certain period.– High rate of interest depending on amount and period of

time.– In times of urgent needs, premature closure of FD allowed

by paying interest at reduced rate.

Products of Commercial Banks• Recurring Deposits –

– Customer opens account deposit certain sum of money every month

– After certain period, accumulated amount along with interest paid to customers.

– Interest paid is generally on cumulative basis– Useful mechanism for regular savers of money.

• Cash Certificate – – Issued to public for longer period of time– Its maturity value is in multiples of sum invested– Attractive and high yielding investment– These are generally issued at discount to the face value

Products of Commercial Banks– Demand Deposit - These are deposits payable on

demand either through cheque or otherwise. Demand Deposit may serve as medium of exchange, because their ownership may be transferred from person to person through cheques. It includes the following:• Savings Deposits –

– Can only be held by individuals– Rate of interest is lower than that of time deposits– Restrictions on withdrawals– Advantage of liquidity(as in CA) and small income in the form of

interests

• Current Account Deposits –– Business firms and institutions– No interest paid on current deposits– No restriction on withdrawals

Products of Commercial Banks• Credit Products – The commercial banks

provide credits in the following forms:– Overdraft –

• Facility given to holders of Current A/cs only• Arrangement with the bankers thereby the customer is

allowed to draw money over and above the balance in his/her account.

• Overdrawing facility Pre-arranged with the bank upto a certain limit

• Short-term temporary fund facility • Interest charged on the amount overdrawn• Facility available to business firms and companies

Products of Commercial Banks– Cash Credit –

• Form of working capital credit to the business firms• Customer opens an account and sactioned amount

credited with the account• Customer can operate the account within the

sanctioned limit as and when required• It is made against secutiry of goods, personal security

etc.• Bank charges interest only on the amount utilized nd

not on the total amount sanctioned/ credited• Slowly phased out from banks and replaced by loan

accounts.

Products of Commercial Banks– Discounting of Bills –

• Banks purchase inland and foreign bills at discounted values

• The bills are purchased by the bank at face value less the interest at the current rate till the time when the bill falls due.

• Bankers reserve rights to debit accounts of the customers in case the bills are dishonoured

• Banks discount only genuine Commercial bills i.e., those drawn against sale of goods against credit

Products of Commercial Banks– Loans and Advances

• Short Term – granted to meet the working capital requirements

• Long Term – granted to meet the capital expenditure– Direct loans and advances given to all types of customers

mainly to businessmen and investors against personal security or goods of movable or immovable in nature.

– Loan amount can be paid in cash or by credit to the customer account which the customer can draw at any time

– Interest is charged for the full amount whether he withdraws the money from his account or not

Products of Commercial Banks– The following types of loans can be availed

from the banks• Home Loan• Car Loan• Education Loan• Personal Loans – Bank grant credit to household

in a limited amount to buy some durable customer goods like TV, refrigerators, washing machine etc. Such loans are repaid in installments.

Products of Commercial Banks

• Other Customised Banking Services and Products - – Letters of Credit:

• Letter of Credit is a payment document provided by the buyer's banker in favour of seller. This document guarantees payment to the seller upon production of document mentioned in the Letter of Credit evidencing dispatch of goods to the buyer.

• The letter of credit is an important method of payment mostly used in international trade.

• There are primarily 4 parties to a letter of credit. The buyer or importer, the bank which issues the letter of credit, known as opening bank, the person in whose favour the letter of credit is issued or opened (The seller or exporter, known as 'Beneficiary of Letter of Credit'), and the credit receiving/advising bank.

• The Letter of Credit is generally advised/sent through the seller's bank, known as Negotiating or Advising bank.

Products of Commercial Banks– Travellers Cheques:

• Banks issue travellers cheques to help carry money safely while travelling within India or abroad. Thus, the customers can travel without fear, theft or loss of money.

– Money Transfer :• Many banks provide simple and convenient, online

remittance facility.• The money can be sent to accounts at all the

branches of the banks across India.

Products of Commercial Banks– Credit cards:

• Banks have introduced credit card system. Credit cards enable a customer to purchase goods and services from certain specified retail and service establishments up to a limit without making immediate payment. In other words, purchases can be made on credit basis on the strength of the credit card.

– Debit Cards : • Like a Credit card a debit card too is a payment

mechanism which allows its holder to make purchases without making any immediate payment.

• At the time of making payment through a debit card, the amount is instantly debited to the customer’s account.

Products of Commercial Banks– Merchant Banking:

• The commercial banks provide valuable services through their merchant banking divisions or through their subsidiaries to the traders. This is the function of underwriting of securities. They underwrite a portion of the Public issue of shares, Debentures and Bonds of Joint Stock Companies.

• Such underwriting ensures the expected minimum subscription and also convey to the investing public about the quality of the company issuing the securities. Currently, this type of services can be provided only by separate subsidiaries, known as Merchant Bankers as per SEBI regulations.

Products of Commercial Banks– Advice on Financial Matters:

• The commercial banks also give advice to their customers on financial matters particularly on investment decisions such as expansion, diversification, new ventures, rising of funds etc.

– Safety Locker facility:• Safekeeping of important documents, valuables like jewels are one

of the oldest services provided by commercial banks. 'Lockers' are small receptacles which are fitted in steel racks and kept inside strong rooms known as vaults. These lockers are available on rental basis.

• The bank merely provides lockers and the key but the valuables are always under the control of its users.

• Only customers of safety lockers after entering into a register his name account number and time can enter into the vault.

Products of Commercial Banks– Internet Banking Services :

• Internet banking is the ability to use ones’s personal computer to communicate with one’s bank.

• It enables the customers to execute bank transations from the PC through financial software of the bank.

• It is being used as a distribution channel to build up customer contracts in a systematic way in order to inform, counsel, and sell products and services.

• Internet banking provides anywhere and anytime banking as services are provided round the clock, easy access to recent and historical data, direct consumer control of movement of funds, greater processing speed and accuracy.

Products of Commercial Banks– ATM Services:

• An automated teller machine or automatic teller machine(ATM) is a computerised telecommunication device that provides a bank’s customers a secure method of performing financial transactions in a public space without a human clerk or bank teller.

• Under this system the customers can withdraw their money easily and quickly and 24 hours a day.

• A consumer can use an ATM for : deposits/withdrawals of cash, making balance enquiry, obtaining account statement, inter account transfer of funds, making utility payments of bills e.g., electricity, telephone etc. , requisition of cheque books

Products of Commercial Banks– Mobile Banking :

• Also known as M-Banking, sms Banking etc., refers to provision and availment of banking and financial services with the help of mobile telecommunication devices.

• The scope of offered services may include facilities to conduct bank and stock market transactions, to administer accounts and to access customized informations.

– Demand Draft:• It is a written order for making payments.• The person making payments is called drawee and the

recipient is alled payee. The bank providing the service is called payer.

![Modern commercial banking []](https://static.fdocuments.net/doc/165x107/55a494801a28ab081b8b4639/modern-commercial-banking-wwwbconnect24com.jpg)