Combating Trade-Based Money Laundering (TBML) in Your ...Combating Trade-Based Money Laundering...

66

Combating Trade-Based Money Laundering (TBML) in Your Institution Wednesday, 11 December 2013 13.30 -14.30 Moderator: Pattison Boleigha, Head Group Compliance & Internal Control, Access Bank Plc Speakers: Solomon Kofi Dawson, Head Compliance & AMLRO, UniBank Ghana Limited Reindorf Atta Gyamena, CAMS, Head of Compliance Unit, CAL Bank Ghana Bahlakona Shelile, Trade & Finance Expert, Economic Intellect Consulting

Transcript of Combating Trade-Based Money Laundering (TBML) in Your ...Combating Trade-Based Money Laundering...

Combating Trade-Based Money Laundering (TBML) in Your Institution

Wednesday, 11 December 2013 � 13.30 -14.30Wednesday, 11 December 2013 � 13.30 -14.30

Moderator: Pattison Boleigha, Head Group Compliance & Internal Control, Access Bank

Plc

Speakers:Solomon Kofi Dawson, Head Compliance & AMLRO, UniBank Ghana LimitedReindorf Atta Gyamena, CAMS, Head of Compliance Unit, CAL Bank GhanaBahlakona Shelile, Trade & Finance Expert, Economic Intellect Consulting

• Introduction & Statistics

• Identifying TBML Typologies

• Red Flags

• Case Study: Motor Vehicle Smuggling

• Mitigating Trade-based Money Laundering

Outline

23rd Annual AML & Financial Crime Conference, Africa

• Mitigating Trade-based Money Laundering Risks

• Control Measures

• Conclusions

• References

Introduction: Criminal’s Problem: How to move illicit

products without detectionIllicit product is ready for

sale

criminal organizations want illicit product

33rd Annual AML & Financial Crime Conference, Africa

How do I avoid detection and sell and pay for my product???

Introduction• Three main methods by which

criminal organisations and terrorist financiers move money for the purpose of disguising its origins

– Financial system

– Bulk Cash Smuggling and Cash couriers

43rd Annual AML & Financial Crime Conference, Africa

couriers

– Trading in goods and services.

• Trade-based money laundering is the use of otherwise legitimate trade transactions to earn, move and store proceeds of a crime.

• “The Impact of Switzerland’s Money Laundering Law on Capital Flows Through Abnormal Pricing in International Trade” by Dr.

John Zdanowicz

• Event Studied• April 1998: Federal Act on the Prevention of Money Laundering

in the Financial Sector – Money Laundering Act

• Time Period Studied – 1995 TO 2000• Before the Law: 1995, 1996, 1997

Why Focus on TBML

53rd Annual AML & Financial Crime Conference, Africa

• Before the Law: 1995, 1996, 1997

• After the Law: 1998, 1999, 2000

• Other Variables Evaluated• Interest Rates: Swiss and U.S.

• Exchange Rates: Swiss and U.S.

• Consumer Price Index: Swiss and U.S.

• Producer Price Index: Swiss and U.S.Source: Journal of Applied Financial Economics January 2005, 15, 217 - 230

Why Focus on TBML

Time Period $ Amount % of Trade Volume

Before the Law $ 252,863,571 28.93 %

Average Monthly Outflows – Before vs. After

63rd Annual AML & Financial Crime Conference, Africa

Before the Law $ 252,863,571 28.93 %

After the Law $ 628,437,709 57.76 %

Percent Increase

149 % 100 %

Why Focus on TBML

Results of Study

Other Variables had NO Impact on Movement of Money from Switzerland to U.S.

The only significant variable was the NEW LAW

73rd Annual AML & Financial Crime Conference, Africa

ConclusionIncreased Regulation of Financial Sector Shifts Money

Laundering to International Trade

POLICY IMPLICATIONSClose the Back Door – Monitor International Trade

Pricing

Why Focus on TBMLThe Back Door: Abnormal Pricing

The U.S government lost more than $53 billion in tax revenues in 2001 due to artificial over-pricing and under-

pricing of products entering and leaving the country.

Result of Research

83rd Annual AML & Financial Crime Conference, Africa

Result of Research The Research came up with a computer analysis that allows Financial Institutions to determine the normal weight characteristics for very product imported into

the U.S, identified a normal range, compared the weight to every imported product to the range and filtered out

for abnormal and suspicious transactions.Source: “Who is watching our back door? Business Accents Magazine College of Business Administration Florida International University

• FFIEC – Examination Manual - 2005, 2006, 2007

• ICE - Establishment Of Trade Transparency Units

• FATF Trade-based Money Laundering Report – 2006

Trade-based Money Laundering Increased Focus

93rd Annual AML & Financial Crime Conference, Africa

• FATF Best Practices Report – 2008

• IFSA - BAFT – Guidelines Trade Services – 2008

• Wolfsberg Group Trade Finance Principles - 2009

Regulatory Response in the U.S.A• Federal Financial Institutions Examination Council

• Board of Governors – Federal Reserve System

• Federal Deposit Insurance Corporation

• National Credit Union Administration

103rd Annual AML & Financial Crime Conference, Africa

• Office of Comptroller of the Currency

• Office of Thrift Supervision

• Bank Secrecy Act / Anti-money Laundering Examination Manual Revised 8/24/2007

Basic TBML Techniques

• Over and under invoicing for goods and services

• Over and under shipment of goods and services

113rd Annual AML & Financial Crime Conference, Africa

• Multiple invoicing of goods and services

• Falsely described goods and services

Trade-Based Money Laundering Implications

Money Moved out of the Country

• Under-valued Exports• Over-valued Imports

123rd Annual AML & Financial Crime Conference, Africa

Money Moved into the Country

• Over-valued Exports• Under-valued Imports

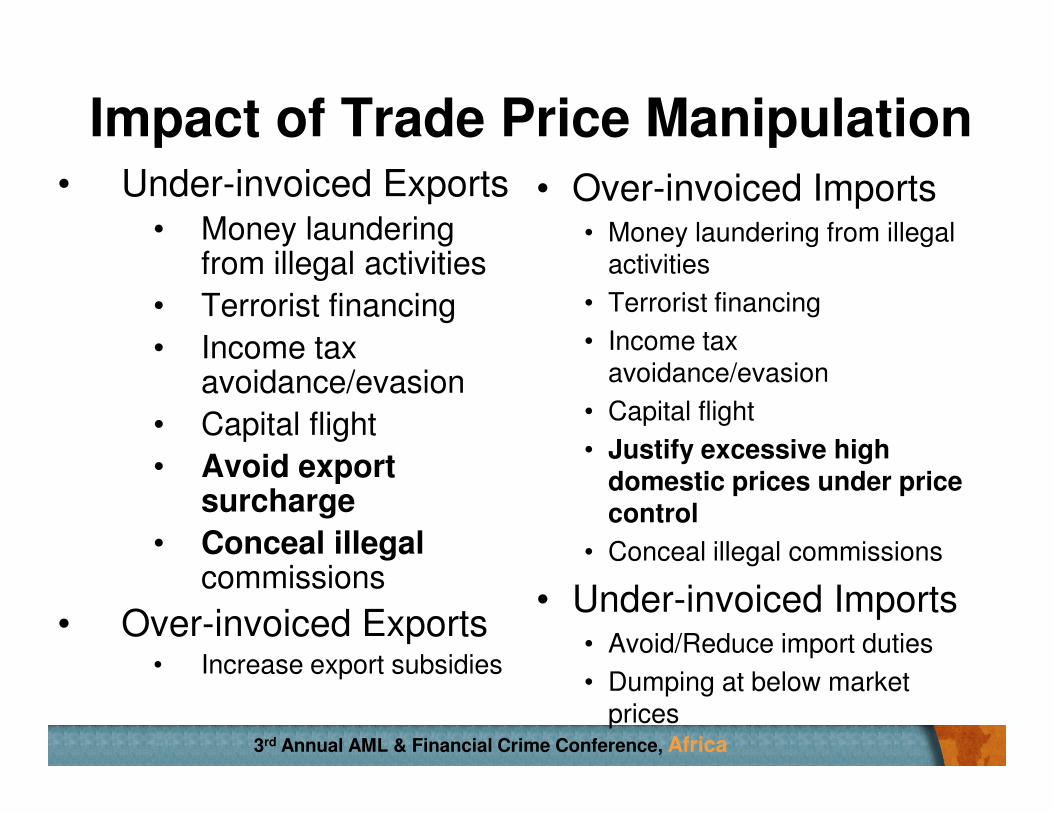

• Under-invoiced Exports• Money laundering

from illegal activities

• Terrorist financing

• Income tax avoidance/evasion

• Capital flight

Impact of Trade Price Manipulation• Over-invoiced Imports

• Money laundering from illegal activities

• Terrorist financing

• Income tax avoidance/evasion

• Capital flight

133rd Annual AML & Financial Crime Conference, Africa

• Capital flight

• Avoid export surcharge

• Conceal illegal commissions

• Over-invoiced Exports• Increase export subsidies

• Capital flight

• Justify excessive high domestic prices under price control

• Conceal illegal commissions

• Under-invoiced Imports• Avoid/Reduce import duties

• Dumping at below market prices

Red Flags• The shipment does not

make economic sense

• The transaction involves the receipt of cash or other payments form a third party entities that have no apparent

• The transaction involves the use of front or shell companies

• Customers are conducting business in high risk jurisdictions

• Customers are shipping

143rd Annual AML & Financial Crime Conference, Africa

have no apparent connection with the transaction

• The transaction involves the use of repeatedly amended or frequently extended LoC

• Customers are shipping items through high risk jurisdictions including transit through non-cooperative countries

• Customers are involved in potentially high risk activities (e.g. drugs, weapons, chemicals etc)

Red Flags• Customers are involved

in obvious over and under invoicing of goods or services

• Customers and/or issuing banks submit excessively amended LoC without reasonable

• Letters of credit with any of the following missing:

• Name and address of Applicant or Beneficiary

• Name and address of the issuing or advising banks

• Amount and type of currency

153rd Annual AML & Financial Crime Conference, Africa

LoC without reasonable justification

• Transactions are evidently designed to evade legal restrictions including evasion of necessary government licensing requirements

• Sight or time draft to be drawn

• Expiration date

• Description of merchandise

• Type and numbers of documents that must accompany letter of credit

Red Flags

• An unsigned letter of credit

• Numerous inquiries by Beneficiary regarding the LoC’s issuance ( a sense of urgency and/or angry complaints)

• LoC opened by telex when the fax has not been tested with the receiving bank

• LoC involving obscure ports and or locations that cannot be contacted

163rd Annual AML & Financial Crime Conference, Africa

angry complaints)

• Presentation of the LoC documents where the bank has no record of the credits existence

that cannot be contacted by telephone or email or fax

• Generic Character-based Analysis– Current Policies Procedures

– Customer Due Diligence

– Know Your Customer

– OFAC Lists

– PEP Lists

– Corruption Index List

Solution to TBML

173rd Annual AML & Financial Crime Conference, Africa

– PRODUCT Risk Index

– Training

– Obtain a method for checking precious metals

• Transaction Based Analysis –evaluation of prices

• Country Risk Analysis

– Country Risk Index

• Documentary Analysis

Conclusion• As International trade increases TBML can be

expected to become increasingly active.

• Basic Schemes: Fraudulent trade practices such as over and under invoicing will increase

• Trade-based money laundering is an important money laundering technique that has received

183rd Annual AML & Financial Crime Conference, Africa

money laundering technique that has received limited attention from policymakers in Africa.

• Building better awareness, strengthening measures to identify trade-based illicit activity and improving inter agency and international co-operation and provide Trade data is a way out.

• John S. Zdanowicz, Ph.D.

Florida International Bankers AssociationProfessor of FinanceFlorida International [email protected]

President – International Trade Alert, [email protected]

References

193rd Annual AML & Financial Crime Conference, Africa

• www. Interntionaltradealert.com

• The impact of Switzerland's money laundering law on capital flows through abnormal pricing in international trade

– Maria de Boyrie

– Simon Pak

– John S. Zdanowicz, Ph.D.

Questions & Questions &

IssuesIssues

203rd Annual AML & Financial Crime Conference, Africa

Pattison BoleighaBsc, MBA, FCA, ACIT, HCIB,CAMS,

Thank You

213rd Annual AML & Financial Crime Conference, Africa

Bsc, MBA, FCA, ACIT, HCIB,CAMS, CGEIT, CRMAChief Compliance OfficerAccess Bank [email protected]; [email protected]

Trade finance ML10 December 201310 December 2013

Solomon Kofi Dawson

Head, Compliance & AMLRO

uniBank Ghana

Introduction

• The Trade Finance Principles sets out thebackground to trade finance andaddresses the AML/CTF/Sanctions risks.Its also comments on the application ofcontrols in general and makes some

233rd Annual AML & Financial Crime Conference, Africa

controls in general and makes someobservations on the subject of future co-operation between relevant stakeholders.

-Wolfsberg group

Controls in trade finance

• Due diligence

• Reviewing

243rd Annual AML & Financial Crime Conference, Africa

• Reviewing

• Screening

• Monitoring

Due diligence

• This is used here to describe both theprocess for identifying and knowing thecustomer but also for risk based checks inrelation to parties who may not becustomers. Given the range of meanings

253rd Annual AML & Financial Crime Conference, Africa

customers. Given the range of meaningsapplied reference will be made asnecessary to “appropriate due diligence”,which may consist of risk based checksonly.

Reviewing

• This is defined here as any process (oftennot automated) to review relevantinformation in a transaction relating to therelevant parties involved, documentationpresented and instructions received.

263rd Annual AML & Financial Crime Conference, Africa

presented and instructions received.

• As will also be described under the RiskIndicators section certain information canand should be reviewed and checked beforetransactions are allowed to proceed.

Screening

• This is usually automated process tocompare information against referencesources such as terrorist lists. Screeningis normally undertaken at the same time

273rd Annual AML & Financial Crime Conference, Africa

is normally undertaken at the same timeas reviewing and prior to the completion ofthe specific activity subject to review. Itmay also be undertaken at the same timeas, or as part of, due diligence.

Monitoring

• Any activity to review completed or inprogress transactions for the presence ofunusual and potentially suspicious features.For trade transactions it should berecognised that it is impossible to introduce

283rd Annual AML & Financial Crime Conference, Africa

recognised that it is impossible to introduceany standard patterning techniques inrelation to account/transactional monitoringprocesses or systems. This is due to therange of variations which are present even innormal trading patterns.

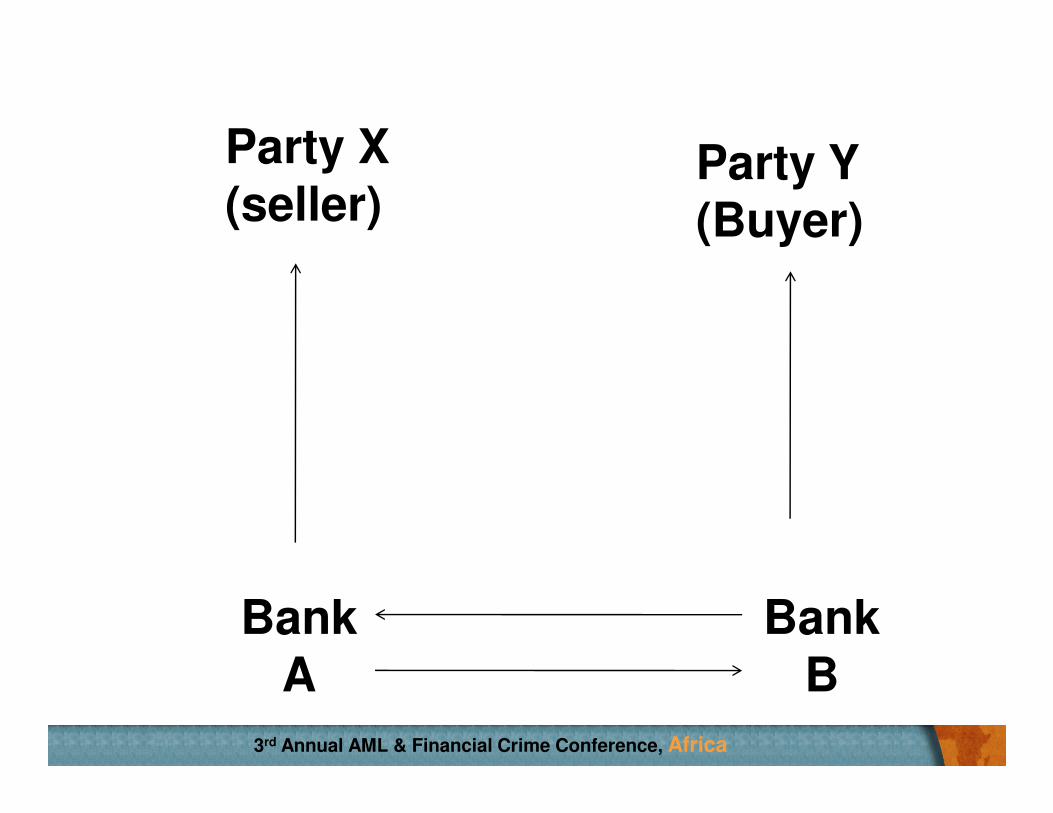

Simplified scenario

• Party X is selling goods to Party Y. Party X is willing to shipthe goods but does not want the documents which entitleParty Y to receive the goods to be released until Party Y haspaid for them or given specified payment undertakings.

• In this scenario it is assumed that Party X is the customer ofBank A and Party Y is the customer of Bank B.

293rd Annual AML & Financial Crime Conference, Africa

• Party X (the seller) instructs Bank A to collect payment inrelation to documents drawn on Party Y (the buyer). Bank Aselects (its correspondent bank or Party Y’s nominated bank)Bank B to present documents for payment to Party Y locallyin the other country.

Simplified scenario, cont’

• The delivery of documents to Party Y by Bank B is typically conditioned on:

• Payment (authorization to debit their account)by Party Y to Bank B, or

• Acceptance/Issuance by Party Y of a financial

303rd Annual AML & Financial Crime Conference, Africa

• Acceptance/Issuance by Party Y of a financialdocument (drafts, promissory notes, chequesor other similar instruments used for obtainingmoney) agreeing to pay Party X at a specifiedfuture date or

• Other stipulated terms and conditions

Simplified scenario, cont’

• The presentation terms (collectioninstruction) are determined by Party X andconveyed to Bank A, who in turn, providesthe collection instruction to Bank B at thetime of presentation of documents forcollection. Unless otherwise specifically

313rd Annual AML & Financial Crime Conference, Africa

collection. Unless otherwise specificallyagreed, neither bank incurs any liability tomake payment.

Simplified scenario, cont’

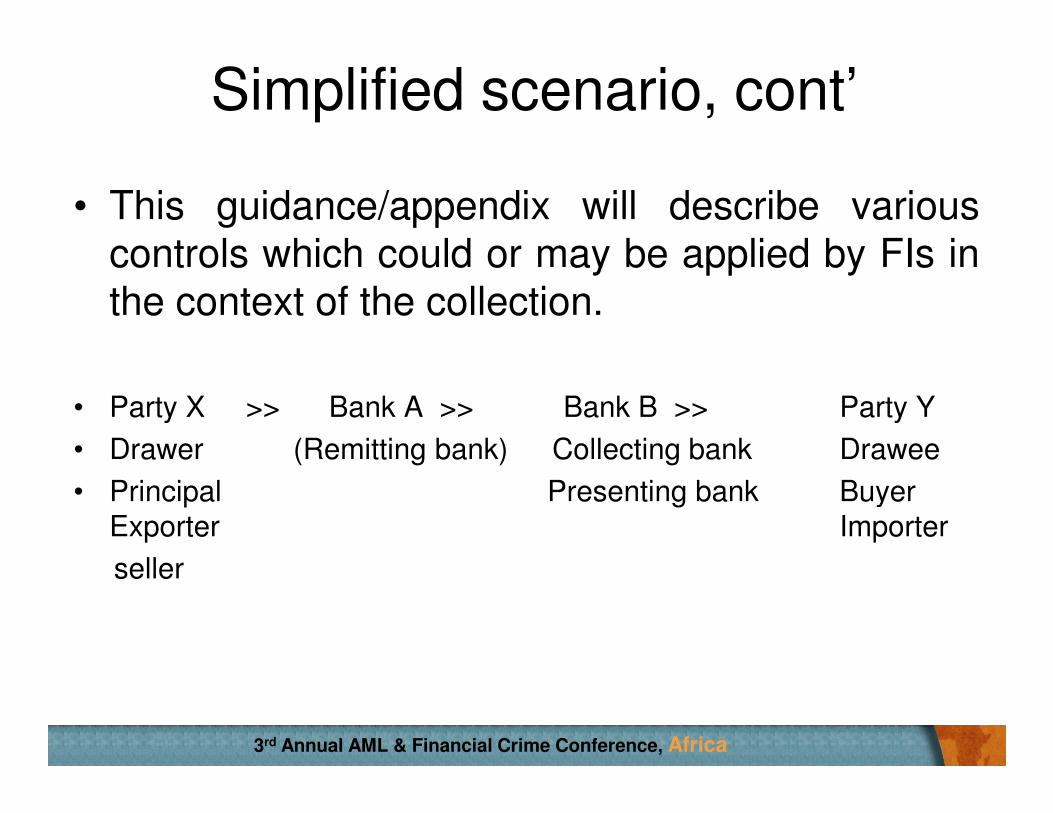

• This guidance/appendix will describe variouscontrols which could or may be applied by FIs inthe context of the collection.

• Party X >> Bank A >> Bank B >> Party Y

323rd Annual AML & Financial Crime Conference, Africa

• Party X >> Bank A >> Bank B >> Party Y

• Drawer (Remitting bank) Collecting bank Drawee

• Principal Presenting bank Buyer Exporter Importer

seller

Party X (seller)

Party Y (Buyer)

333rd Annual AML & Financial Crime Conference, Africa

Bank A

Bank B

Due Diligence Overview

• The banks will conduct due diligence whichwill normally follow the pattern describedbelow

• Bank A will conduct due diligence on Party X

• Bank A may conduct appropriate due

343rd Annual AML & Financial Crime Conference, Africa

• Bank A may conduct appropriate duediligence on Bank B

• Bank B may conduct appropriate duediligence on Bank A

• Bank B will conduct due diligence on Y

Party X (seller)

Party Y (Buyer)

353rd Annual AML & Financial Crime Conference, Africa

Bank ABank

B

Reviewing activity overview

• Once the BC is initiated the banks will then reviewthe transaction in accordance with standard bankingpractice at various stages through to the eventualpayment being made. This reviewing activity willnormally follow the pattern described below

• Bank A will review the collection instruction from X

363rd Annual AML & Financial Crime Conference, Africa

• Bank B will review the collection instruction receivedfrom Bank A

• Bank A and Bank B will review the payment (or other)instructions received.

Controls undertaken by Bank A• Party X Due diligence • Bank A should conduct appropriate due

diligence (Identification, verification screening &KYC) on Party X (who is a Customer of Bank A)prior to acceptance and execution of the originalinstruction. This is likely to involve a series ofstandardized procedures for account opening

373rd Annual AML & Financial Crime Conference, Africa

standardized procedures for account openingwithin Bank A.

• As the handling of BCs involves no directfinancial responsibility for Bank A and does notinvolve Bank A necessarily in any lending toParty X the normal due diligence for opening anaccount will generally apply.

Enhanced Due Diligence• An enhanced due diligence process should be

automatically applied where party X falls into ahigher risk category or where the nature of theirtrade as disclosed during the standard duediligence process suggests that enhanced duediligence would be prudent. The enhanced duediligence should be designed to understand the

383rd Annual AML & Financial Crime Conference, Africa

diligence should be designed to understand thetrade cycle and may involve establishing ;

• The countries where Party X trades

• The goods traded

• The type and nature of principal parties with whomParty X does business.

Enhanced Due Diligence, cont’

• The nature of business and the anticipatedtransactions as described and disclosed inthe initial due diligence stage may notnecessarily suggest a higher risk categorybut if this becomes apparent after

393rd Annual AML & Financial Crime Conference, Africa

but if this becomes apparent aftertransactions commence this may warrantadditional due diligence.

Bank B -Due Diligence

• Bank A should undertake appropriate due diligenceon Bank B. The due diligence may support anongoing relationship with Bank B which will besubject to a relevant risk based review cycle. Duediligence on Bank B is not therefore required inrelation to each subsequent transaction.

403rd Annual AML & Financial Crime Conference, Africa

• In other circumstances Bank B may neither have norneed to have a relationship with Bank A. Bank A willneed to decide when sending the BC to Bank Bwhether it should undertake any checks in relation toBank B or whether it should route the collectionthrough another intermediate Bank with whom arelationship already exists.

Reviewing

• The level of reviewing activity may be limited to that described as standard below. .

Standard • Appropriate reviewing may be conducted by Bank

A in relation to the BC instruction received fromParty X which may take account of the following.

• Sanctions & terrorist lists which may affect

413rd Annual AML & Financial Crime Conference, Africa

• Sanctions & terrorist lists which may affect • Any principal party as named target • The country in which Bank B and Party Y is

located• The goods involved

Reviewing, Cont’

• Enhanced • Enhanced reviewing is likely to be applied only to

transactions where there is a particular reason forcloser examination or scrutiny, and which may thentake account of the following

• The countries which are rated as high risk for otherreasons, as related to

423rd Annual AML & Financial Crime Conference, Africa

reasons, as related to• The countries where Bank B or Party Y are located • Transit countries through which the goods will be

shipped (only if visible on the collection instruction)• The goods described in the transaction to ensure that

the nature of these goods does not appearinconsistent with what is known of Party X

Reviewing, Cont’

Depending on the information arising from thisscreening process Bank A may need to;

• Make further internal enquires as to theappropriate course of action

• Request more information from Party X beforeagreeing to proceed with the transaction

433rd Annual AML & Financial Crime Conference, Africa

agreeing to proceed with the transaction• Allow the transaction to proceed but make a

record of the circumstances for review purposes• Decline the transaction if enquiries do not

provide reasonable explanations, and subject tocircumstances and local legal requirementssubmit a suspicious activity report

Monitoring

• For Bank B the monitoring opportunities arise from

• The normal procedures for monitoring theaccount and payment activity of Party Y.

• Patterns of activity observed from

443rd Annual AML & Financial Crime Conference, Africa

• Patterns of activity observed frombusiness as usual trade processing moregenerally

Limitations faced by bank A

• Bank B is not the originator of the transactionbut is requested to act on instructionsreceived by Bank A (although it is not obligedto do so).

• In accordance with established practice forhandling BCs, Bank B will have limited time

453rd Annual AML & Financial Crime Conference, Africa

handling BCs, Bank B will have limited timein which to act upon such instructions.

• In handling the BC Bank B’s role for the duediligence on Party X is limited to reviewing ofParty X’s name against sanctions andterrorist lists.

Risk Indicators -Pre and Post Event

• Since the full execution of each BC transaction is afragmented process involving a number of parties, eachwith varying degrees of information about the transaction, itis extremely rare for any one Bank to have the opportunityto review an overall trade financing process in completedetail given the premise of the trade business that banksdeal only in documents. Furthermore it is relevant to note

463rd Annual AML & Financial Crime Conference, Africa

deal only in documents. Furthermore it is relevant to notethat

• Different Banks have varying degrees of systems capabilitieswhich will lead to industry wide differences in theirreviewing abilities

• Commercial practices and industry standards determinefinite timescales in which to act.

Risk Indicators -Pre and Post Event

• In determining whether transactions aresuspicious due to over or under invoicing (orany other circumstances where there ismisrepresentation of value) it needs to beunderstood that Banks are not required to

473rd Annual AML & Financial Crime Conference, Africa

understood that Banks are not required tocheck the underlying documents presentedwith BCs.

Risk Indicators -Pre and Post Event

• it is important to distinguish between

1. Information which must be validated beforetransactions are allowed to proceed orcomplete and which may prevent suchcompletion (e.g. a terrorist name, UN

483rd Annual AML & Financial Crime Conference, Africa

completion (e.g. a terrorist name, UNsanctioned entity).

2. Information which ought to be used in postevent analysis as part of the investigationand suspicious activity reporting process

WHAT WHEN

S/N Activity or information connected with the BC

Pre or post

transaction

1

Goods • Applicable export or import controls may not be

complied with PRE

2

Goods • Manifest anomalies value v quantity (to the

extent reviewed and to the extent apparent) • Manifestly

out of line with customers known business PRE OR POST

3

Countries/principal parties • On the Sanctions/terrorist

list PRE

493rd Annual AML & Financial Crime Conference, Africa

4

Countries • On the Bank’s high risk list • Any attempt to

disguise/circumvent countries involved in the actual trade PRE OR POST

5Payment instructions • Illogical • Last minute changes PRE OR POST

6

Repayment arrangements • Third parties are funding or

part funding the collection PRE OR POST

7

Counterparties • Connected drawer/drawee, where

obvious PRE OR POST

8

Anomalies in instructions • Unexplained third parties •

Absence of transport documents PRE OR POST

THANK YOU

503rd Annual AML & Financial Crime Conference, Africa

THANK YOU

A word to a wise is enough

Investigating Criminal Activity in Motor Vehicle Smuggling and possible links to other crimes, possible links to other crimes, including terrorist financing…

Bahlakoana Shelile

Economic Intellect ConsultingLesotho

Contents

1. Background

2. Money laundering vulnerabilities related to illicit trade in and

smuggling of motor vehicles

3. Some offences related to illicit trade in and smuggling of motor

523rd Annual AML & Financial Crime Conference, Africa

3. Some offences related to illicit trade in and smuggling of motor

vehicles

4. Case Study – motor vehicle identity theft (cloning)

5. Some possible steps in motor vehicle anti – smuggling initiatives

Background

• The illicit trade in and smuggling of motor vehicles in nature are both

multi jurisdiction and multi industries criminal activities

• While trends in illicit trade in and smuggling of motor vehicles have

always been transforming, they seem to be leaning more towards

533rd Annual AML & Financial Crime Conference, Africa

always been transforming, they seem to be leaning more towards

“value for money”

ML vulnerabilities related motor vehicle smuggling

• Unregulated Motor Vehicle Industry

• Cash based nature of transactions

• Ineffective controls on bonded warehouses

• Insufficient cooperation with the vehicle manufacturers

543rd Annual AML & Financial Crime Conference, Africa

• Insufficient cooperation with the vehicle manufacturers

• Ineffective exchange of information amongst local and regional

LEAs

Some Offences related to MV smuggling

• False declaration/misclassification

• False registration

• Theft of motor vehicles

• Use of fraudulent documents

553rd Annual AML & Financial Crime Conference, Africa

• Use of fraudulent documents

• Illegal chop shops

• Cloning

Case study - cloning

• December 2008, a red Toyota Venture was stopped at the road

block between Durban, RSA and Swaziland by SAPS.

• Earlier, a Swazi family man purchased a brand new red Toyota

Venture from a Toyota dealership in Swaziland.

563rd Annual AML & Financial Crime Conference, Africa

Venture from a Toyota dealership in Swaziland.

• Motor vehicles criminal syndicate goes window shopping for vehicle

identity information.

• The Swaziland red Toyota Venture vehicle identification information is

stolen…

Case study – cloning…

• Investigation findings

• The criminal syndicate operated both in RSA and Swaziland

• Both red Toyota Ventures were purchased through a bank finance

facility

573rd Annual AML & Financial Crime Conference, Africa

facility

• Both red Toyota Ventures were purchased from licensed

authorised dealerships

• The syndicate, non Swazi Nationals had a front company in

Swaziland and property acquired using proceeds of illicit trade

Motor Vehicle – Anti Smuggling Initiatives

1. Increased information sharing among the regional LEAs,

(SARPCCO & EAPCO) – Preventative approach…

583rd Annual AML & Financial Crime Conference, Africa

(SARPCCO & EAPCO) – Preventative approach…

2. Use of third initiatives, “Business Against Crime”, e.g. International

Vehicle Identification Desk.

593rd Annual AML & Financial Crime Conference, Africa

Thank you…

Control Measures To Deal With Trade-based Money Laundering

Reindorf Atta Gyamena, CAMS, Head of Compliance Unit, CAL Bank Ghana

To develop your TBML controls you must have:

� Done your Risk Assessment to determine how your institution is

exposed to TBML.

� Determined some of the methodologies.

SOME POINTS TO NOTE

613rd Annual AML & Financial Crime Conference, Africa

� Determined some of the methodologies.

� Know that Tax evasion is the dominant predicate offence for TBML

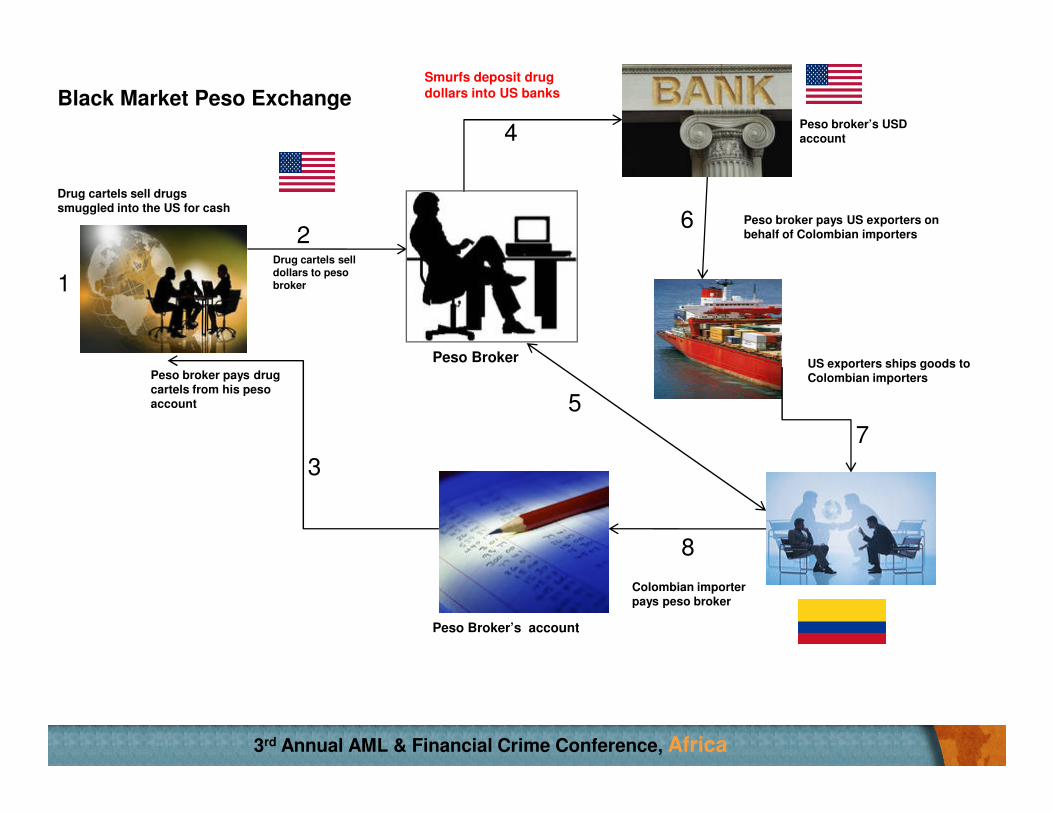

BLACK MARKET PESO EXCHANGE

ARRANGEMENTS

1

• Colombian drug cartel smuggles illegal drugs into the United States and sells them for cash.

2

• The drug cartel arranges to sell the US dollars at a discount to a peso broker for Colombian pesos.

• The peso broker pays the drug cartel with pesos from his

623rd Annual AML & Financial Crime Conference, Africa

3

• The peso broker pays the drug cartel with pesos from his bank account in Colombia which eliminates the drug cartel from any further involvement in the arrangement.

4

• The peso broker structures or smurfs the US currency into the US banking system to avoid reporting requirements and consolidates this money in his US bank account.

BLACK MARKET PESO EXCHANGE

ARRANGEMENTS

5

• The peso broker identifies a Colombian importer that needs US dollars to purchase goods from a US exporter.

6

• The peso broker arranges to pay the US exporter on behalf of the Colombian importer from his US bank account.

• The US exporter ships the goods to Colombia

633rd Annual AML & Financial Crime Conference, Africa

7• The US exporter ships the goods to Colombia

8

• The Colombian importer sells the goods, often high-value items such as personal computers, consumer electronics and household appliances, for pesos and repays the peso broker. This replenishes the peso brokers supply of pesos.

Drug cartels sell dollars to peso broker

Peso broker pays drug cartels from his peso account

Smurfs deposit drug dollars into US banks

Peso broker pays US exporters on behalf of Colombian importers

US exporters ships goods to Colombian importers

Peso Broker

2

4

6

5

Black Market Peso Exchange

Drug cartels sell drugs smuggled into the US for cash

1

Peso broker’s USD account

643rd Annual AML & Financial Crime Conference, Africa

account

Peso Broker’s account

Colombian importer pays peso broker

3

5

7

8

CONTROLS TO DEAL WITH TRADE

BASED MONEY LAUNDERING

It is the process of identifying and knowing the customer. It also

includes risk based checks in relation to parties who may not be

customers.

It involves reviewing relevant information in the transaction to

determine the relevant parties involved, documentation presented

and instructions received.

This is a process to compare information against reference sources

such as terrorist lists (world-check). Screening is normally

Due Diligence

Reviewing Transaction

653rd Annual AML & Financial Crime Conference, Africa

such as terrorist lists (world-check). Screening is normally

undertaken at the same time as reviewing and prior to the

completion of the specific activity subject to review.

It is any activity to review completed or in progress transactions for

the presence of unusual and potentially suspicious features.

Staff focused training is important for all the controls to be effective.

Screening

Monitoring

Training

Thank You!

663rd Annual AML & Financial Crime Conference, Africa66

Thank You!