Columbia Real Estate Office Report - 2Q 2011

4

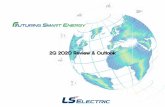

0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 30.00% 0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 30.00% Q203 Q204 Q205 Q206 Q207 Q208 Q209 Q210 Q410 Q211 CBD Class A Vacancy CBD Vacancy Market Vacancy RESEARCH & FORECAST REPORT COLUMBIA, SOUTH CAROLINA www.colliers.com/columbia Activity in the Columbia, South Carolina, office market continued to show promise of economic recovery as leasing activity expanded into the suburban markets during the second quarter of 2011. The majority of the leasing volume during the previous three quarters was primarily limited to the Central Business District due to the aggressiveness of downtown landlords to attract and retain tenants. During the second quarter of 2011, however, CBD rental rates started to increase for the first time in 18 months, while suburban rates further declined by an average of $0.58 per square foot. This divergence of rental rates between the CBD and suburban markets can be largely attributed to suburban landlords being more aggressive in rental rates to capture tenant activity. Absorption in the suburban markets totaled 37,461 square feet during in the second quarter of 2011. Leasing activity in the suburban markets was largely concentrated in Columbia’s largest suburban submarket, St. Andrews. This positive absorption is noteworthy because the St. Andrews area had experienced a continual decline in occupancy from the onset of the last economic downturn through the first quarter of 2011. Renewed activity in this submarket signals an encouraging trend in traditional suburban office space primarily occupied by regional and national corporate tenants. MARKET INDICATORS QUICK UPDATES Q2 2011 Forecast VACANCY NET ABSORPTION CONSTRUCTION — — RENTAL RATE — — Q2 2011 | OFFICE 2003 - 2011 Vacancy Rates • THE ST. ANDREWS MARKET EXPERIENCED POSITIVE ABSORPTION FOR THE FIRST TIME SINCE THE ONSET OF THE RECESSION • TENANTS REMAIN VALUE CONSCIENCE IN THEIR DECISIONS AND ARE ASKING FOR HIGHER QUALITY FINISHES • LANDLORDS WHO ARE AGGRESSIVE WITH RENTAL RATES ARE EXPERIENCING GREATER ACTIVITY

-

Upload

colliers-international -

Category

Real Estate

-

view

239 -

download

4

description

Columbia Real Estate Office Report - 2Q 2011

Transcript of Columbia Real Estate Office Report - 2Q 2011

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Q203 Q204 Q205 Q206 Q207 Q208 Q209 Q210 Q410 Q211

CBD Class A Vacancy CBD Vacancy Market Vacancy

RESEARCH & FORECAST REPORTCOLUMBIA, SOUTH CAROLINA

www.colliers.com/columbia

Activity in the Columbia, South Carolina, office market continued to show promise of economic recovery as leasing activity expanded into the suburban markets during the second quarter of 2011. The majority of the leasing volume during the previous three quarters was primarily limited to the Central Business District due to the aggressiveness of downtown landlords to attract and retain tenants. During the second quarter of 2011, however, CBD rental rates started to increase for the first time in 18 months, while suburban rates further declined by an average of $0.58 per square foot. This divergence of rental rates between the CBD and suburban markets can be largely attributed to suburban landlords being more aggressive in rental rates to capture tenant activity. Absorption in the suburban markets totaled 37,461 square feet during in the second quarter of 2011.

Leasing activity in the suburban markets was largely concentrated in Columbia’s largest suburban submarket, St. Andrews. This positive absorption is noteworthy because the St. Andrews area had experienced a continual decline in occupancy from the onset of the last economic downturn through the first quarter of 2011. Renewed activity in this submarket signals an encouraging trend in traditional suburban office space primarily occupied by regional and national corporate tenants.

MARKET INDICATORS

QUICK UPDATES

Q2 2011 Forecast

VACANCY

NET ABSORPTION

CONSTRUCTION — —

RENTAL RATE — —

Q2 2011 | OFFICE

2003 - 2011 Vacancy Rates

• THE ST. ANDREWS MARKET EXPERIENCED POSITIVE ABSORPTION FOR THE FIRST TIME SINCE THE ONSET OF THE RECESSION

• TENANTS REMAIN VALUE CONSCIENCE IN THEIR DECISIONS AND ARE ASKING FOR HIGHER QUALITY FINISHES

• LANDLORDS WHO ARE AGGRESSIVE WITH RENTAL RATES ARE EXPERIENCING GREATER ACTIVITY

Columbia’s Central Business District experienced a 17,238-square-foot decline in occupied space during the second quarter of 2011. This negative absorption can be largely attributed to downsizing by the South Carolina state government, which is an anticipated result of the state’s continued financial pressure to cut operational expenses. Although the CBD experienced an overall decline in occupied space during the second quarter, activity among private sector tenants remained strong as the insurance and legal sectors continued to expand. Activity among these sectors should result in positive absorption in the coming quarters.

Leasing activity during the second quarter was much stronger in office properties where landlords

demonstrated aggressiveness in attracting tenants. Tenants have remained value-conscience in searching for space and continue to work towards increasing efficiencies, thereby reducing square footage requirements and rental expenses. Office users are now increasing the number of employees per square foot of space, sometimes by as much as 25% more than levels traditionally experienced. With the perception of a “buyer’s market” still present, landlords should be cautious about raising asking rental rates.

As employers look to increase efficiencies, and with more employees per office, the demand for parking spaces required per square foot of space leased will rise. As this demand increases, it will become more difficult

DEFINITIONS

Absorption (Net) The net change in occupied space over a given period of time, calculated by summing all the positive changes in occupancy and subtracting all the negative changes in occupancy.

Vacancy Rate A percentage of the total amount of physically vacant space divided by the total amount of existing inventory.

Vacant Space Space that is not currently occupied by a tenant, regardless of any lease obligation on the space.

Sublease Space Space that has been leased by a tenant and is being offered for lease back to the market by the tenant with the lease obligation.

Deliveries Buildings that complete construction during a specified period of time. A certificate of occupancy must have been issued for the property for it to be considered delivered.

Leasing Activity The volume of square footage that is committed to and signed for under a lease obligation for a specific building or market in a given period of time. It includes direct leases, subleases and renewals of existing leases. It also includes any pre-leasing activity for buildings under construction or planned.

Build-to-Suit A term describing property that was developed specifically for a certain tenant to occupy. Can be either leased or owned by the tenant.

Average Asking Rental Rate Rental rates are calculated based on a weighted average of available space in each submarket. Therefore, fully leased buildings do not impact the average asking rate within the market, and properties with large blocks of available space have greater influence on market rates.

Columbia, South Carolina Office Submarkets

P. 2 | COLLIERS INTERNATIONAL

RESEARCH & FORECAST REPORT | Q2 2011 | OFFICE | COLUMBIA

MARKET UPDATES Buildings Inventory Direct VacantDirect Vacancy Rate

Sublease Total Vacant Vacancy Rate Mid Year 2010

Six Month Absorption

Average Asking Rate

CBD

A 12 2,004,680 279,374 13.9% 67,368 346,742 13.1% (12,506) $19.52

B 17 1,616,799 182,247 11.3% 42,506 224,753 10.5% (17,453) $16.40

C 27 1,424,707 630,794 44.3% - 630,794 46.3% 12,721 $15.87

Total 56 5,046,186 1,092,415 21.6% 109,874 1,202,289 21.2% (17,238) $16.89

SUBURBAN SECTION:

CAYCE/WEST COLUMBIA

A 2 63,000 14,400 22.9% - 14,400 32.2% 5,900 $18.67

B 8 296,928 26,802 9.0% - 26,802 10.8% 5,335 $13.07

C 5 147,889 40,016 27.1% - 40,016 28.3% 1,847 $12.03

Total 15 507,817 81,218 16.0% - 81,218 18.6% 13,082 $13.55

EAST COLUMBIA (DEVINE STREET)

Total (Class C Only) 6 84,483 17,006 24.6% - 17,006 24.59% 5,632 $10.99

FOREST ACRES

A 1 23,700 1,500 6.3% - 1,500 7.4% 250 $17.00

B 7 305,725 86,250 28.2% - 86,250 31.6% 10,253 $15.82

C 11 393,632 65,961 16.8% - 65,961 14.3% (9,813) $13.64

Total 19 723,057 153,711 21.3% - 153,711 21.4% 690 $14.90

NORTHEAST

A 8 399,292 78,674 19.7% - 78,674 14.6% (20,459) $16.33

B 9 595,113 89,769 15.1% - 89,769 15.6% 3,366 $15.10

C 7 209,967 56,920 27.1% - 56,920 23.3% 2,734 $12.15

Total 24 1,204,372 225,363 18.7% - 225,363 16.6% (14,359) $14.79

ST ANDREWS

A 5 402,472 52,411 13.0% - 52,411 16.09% 12,334 $17.04

B 20 1,089,298 167,959 15.4% - 167,959 18.15% 20,316 $14.00

C 16 855,169 233,669 27.3% - 233,669 27.96% 5,398 $11.77

Total 41 2,346,939 454,039 19.3% - 454,039 21.37% 38,048 $13.20

SUBURBAN TOTAL

A 16 888,464 146,985 16.5% - 146,985 16.3% (1,975) $16.82

B 44 2,287,064 370,780 16.2% - 370,780 18.3% 39,270 $14.62

C 45 1,606,657 396,566 24.7% - 396,566 24.0% 166 $12.16

Total 105 4,782,185 914,331 19.1% - 914,331 19.9% 37,461 $13.91

MARKET TOTAL

A 28 2,893,144 426,359 14.7% 67,368 493,727 14.0% (14,481) $18.59

B 61 3,903,863 553,027 14.2% 42,506 595,533 15.3% 21,817 $15.21

C 72 3,031,364 1,027,360 33.9% - 1,027,360 34.2% 12,887 $14.44

Total 161 9,828,371 2,006,746 20.4% 109,874 2,116,620 20.6% 20,223 $15.53

RESEARCH & FORECAST REPORT | Q2 2011 | OFFICE | COLUMBIA

COLLIERS INTERNATIONAL | P. 3

for landlords to accommodate parking needs. Thus, landlords that control their own parking and buildings that offer free parking will likely have an advantage in attracting tenants.

Along with increased efficiencies, tenants have started requesting higher quality finishes in their respective spaces. Increased tenant improvement costs for higher quality finishes have resulted in longer lease commitments from tenants. Many of the significant transactions that have occurred thus far in 2011 have lease terms beyond the typical five-year term, extending to seven- to 10-year terms. This is of particular importance in the long-term forecast because the traditional five-year turnover experienced in Columbia will not be as substantial in 2015 and 2016.

The Columbia office market will continue to expand through the end of 2011, although absorption in the third quarter may be nominal due to limited activity during the summer months. While activity is expected to increase along with job growth, absorption numbers will likely not reach the levels

experienced prior to the last economic downturn due to many tenants’ desire to increase efficiencies and reduce their square footage requirements.

Rental rates will likely remain stable across the Columbia market through the end of 2011, although fluctuations will occur as landlords work to aggressively attract and retain tenants. This trend will likely continue in the suburban markets into 2012, but the CBD will likely see consistent increases in asking rates within six to nine months.

Demand for office space in the third and fourth quarters of 2011 will be primarily concentrated in the Class A and Class B markets, where tenants are able to get quality space at what is perceived to be a good value. Landlords who have invested in improvements to their properties, including upgrades to common areas and amenities, will experience a higher level of interest in their respective properties.

• $1.6 billion in annual revenue

• 672.9 million square feet under management

• Over 15,000 professionals

This market report is a research document of Colliers International. Information herein has been deemed reliable and no representation is made as to the accuracy thereof. Colliers International South Carolina, Inc., and certain of its subsidiaries, is an independently owned and operated business and a member firm of Colliers International Property Consultants, an affiliation of independent companies with over 480 offices throughout more than 61 countries worldwide.

www.colliers.com/columbia

Accelerating success.

FOR MORE INFORMATION:

David C. Lockwood, III, CCIM, SIORSenior Vice President South Carolina1301 Gervais StreetSuite 600Columbia, South Carolina 29201TEL +1 803 401 4211FAX +1 803 401 4211

Ryan Hyler, LEED Green AssociateVice President | Research & MarketingSouth Carolina1301 Gervais StreetSuite 600Columbia, South Carolina 29201TEL +1 803 401 4269FAX +1 803 401 4269

480 offices in 61 countries on 6 continentsUnited States: 135Canada: 39Latin America: 17Asia Pacific: 194EMEA: 95

RESEARCH & FORECAST REPORT | Q2 2011 | OFFICE | COLUMBIA