Colombia Tax Guide 2013 - PKF - PKF International pkf tax guide 2013.pdf · PKF Worldwide Tax Guide...

13

Colombia Tax Guide 2013

Transcript of Colombia Tax Guide 2013 - PKF - PKF International pkf tax guide 2013.pdf · PKF Worldwide Tax Guide...

ColombiaTax Guide

2013

PKF Worldwide Tax Guide 2013 I

Fore

wor

d

foreword

A country’s tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there double tax treaties in place? How will foreign source income be taxed?

Since 1994, the PKF network of independent member firms, administered by PKF International Limited, has produced the PKF Worldwide Tax Guide (WWTG) to provide international businesses with the answers to these key tax questions. This handy reference guide provides clients and professional practitioners with comprehensive tax and business information for over 90 countries throughout the world.

As you will appreciate, the production of the WWTG is a huge team effort and I would like to thank all tax experts within PFK member firms who gave up their time to contribute the vital information on their country’s taxes that forms the heart of this publication.

I hope that the combination of the WWTG and assistance from your local PKF member firm will provide you with the advice you need to make the right decisions for your international business.

Richard SackinChairman, PKF International Tax CommitteeEisner Amper LLP [email protected]

PKF Worldwide Tax Guide 2013II

Disclaimer

important disclaimer

This publication should not be regarded as offering a complete explanation of the taxation matters that are contained within this publication.This publication has been sold or distributed on the express terms and understanding that the publishers and the authors are not responsible for the results of any actions which are undertaken on the basis of the information which is contained within this publication, nor for any error in, or omission from, this publication.

The publishers and the authors expressly disclaim all and any liability and responsibility to any person, entity or corporation who acts or fails to act as a consequence of any reliance upon the whole or any part of the contents of this publication.

Accordingly no person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice from an appropriately qualified professional person or firm of advisors, and ensuring that such advice specifically relates to their particular circumstances.

PKF International is a network of legally independent member firms administered by PKF International Limited (PKFI). Neither PKFI nor the member firms of the network generally accept any responsibility or liability for the actions or inactions on the part of any individual member firm or firms.

PKF Worldwide Tax Guide 2013 III

Pref

ace

preface

The PKF Worldwide Tax Guide 2013 (WWTG) is an annual publication that provides an overview of the taxation and business regulation regimes of the world’s most significant trading countries. In compiling this publication, member firms of the PKF network have based their summaries on information current on 1 January 2013, while also noting imminent changes where necessary.

On a country-by-country basis, each summary addresses the major taxes applicable to business; how taxable income is determined; sundry other related taxation and business issues; and the country’s personal tax regime. The final section of each country summary sets out the Double Tax Treaty and Non-Treaty rates of tax withholding relating to the payment of dividends, interest, royalties and other related payments.

While the WWTG should not to be regarded as offering a complete explanation of the taxation issues in each country, we hope readers will use the publication as their first point of reference and then use the services of their local PKF member firm to provide specific information and advice.

In addition to the printed version of the WWTG, individual country taxation guides are available in PDF format which can be downloaded from the PKF website at www.pkf.com

PKF INTERNATIONAL LIMITEDMAY 2013

©PKF INTERNATIONAL LIMITEDALL RIGHTS RESERVEDUSE APPROVED WITH ATTRIBUTION

PKF Worldwide Tax Guide 2013IV

Introduction

about pKf international limited

PKF International Limited (PKFI) administers the PKF network of legally independent member firms. There are around 300 member firms and correspondents in 440 locations in around 125 countries providing accounting and business advisory services. PKFI member firms employ around 2,270 partners and more than 22,000 staff.PKFI is the 11th largest global accountancy network and its member firms have $2.68 billion aggregate fee income (year end June 2012). The network is a member of the Forum of Firms, an organisation dedicated to consistent and high quality standards of financial reporting and auditing practices worldwide.

Services provided by member firms include:

Assurance & AdvisoryInsolvency – Corporate & PersonalFinancial Planning/Wealth managementTaxationCorporate FinanceForensic AccountingManagement ConsultancyHotel ConsultancyIT Consultancy

PKF member firms are organised into five geographical regions covering Africa; Latin America; Asia Pacific; Europe, the Middle East & India (EMEI); and North America & the Caribbean. Each region elects representatives to the board of PKF International Limited which administers the network. While the member firms remain separate and independent, international tax, corporate finance, professional standards, audit, hotel consultancy and business development committees work together to improve quality standards, develop initiatives and share knowledge and best practice cross the network.

Please visit www.pkf.com for more information.

PKF Worldwide Tax Guide 2013 V

Stru

ctur

e

structure of country descriptions

a. taXes payable

FEDERAL TAXES AND LEVIES COMPANY TAX CAPITAL GAINS TAX BRANCH PROFITS TAX SALES TAX/VALUE ADDED TAX FRINGE BENEFITS TAX LOCAL TAXES OTHER TAXES

b. determination of taXable income

CAPITAL ALLOWANCES DEPRECIATION STOCK/INVENTORY CAPITAL GAINS AND LOSSES DIVIDENDS INTEREST DEDUCTIONS LOSSES FOREIGN SOURCED INCOME INCENTIVES

c. foreiGn taX relief

d. corporate Groups

e. related party transactions

f. witHHoldinG taX

G. eXcHanGe control

H. personal taX

i. treaty and non-treaty witHHoldinG taX rates

PKF Worldwide Tax Guide 2013VI

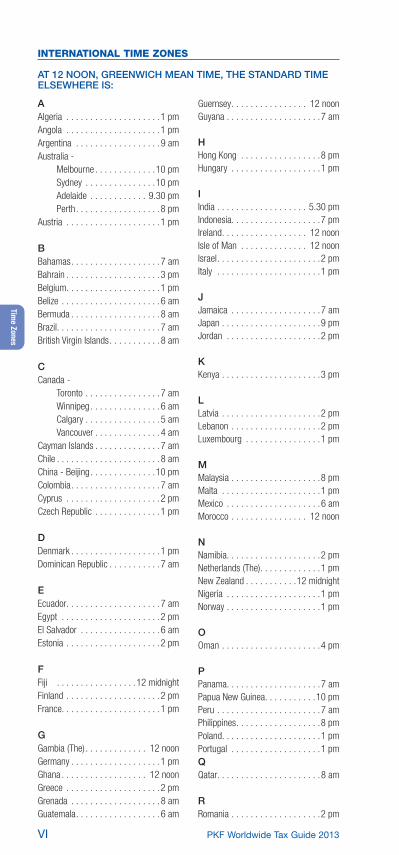

Time Zones

AAlgeria . . . . . . . . . . . . . . . . . . . .1 pmAngola . . . . . . . . . . . . . . . . . . . .1 pmArgentina . . . . . . . . . . . . . . . . . .9 amAustralia - Melbourne . . . . . . . . . . . . .10 pm Sydney . . . . . . . . . . . . . . .10 pm Adelaide . . . . . . . . . . . . 9.30 pm Perth . . . . . . . . . . . . . . . . . .8 pmAustria . . . . . . . . . . . . . . . . . . . .1 pm

BBahamas . . . . . . . . . . . . . . . . . . .7 amBahrain . . . . . . . . . . . . . . . . . . . .3 pmBelgium . . . . . . . . . . . . . . . . . . . .1 pmBelize . . . . . . . . . . . . . . . . . . . . .6 amBermuda . . . . . . . . . . . . . . . . . . .8 amBrazil. . . . . . . . . . . . . . . . . . . . . .7 amBritish Virgin Islands . . . . . . . . . . .8 am

CCanada - Toronto . . . . . . . . . . . . . . . .7 am Winnipeg . . . . . . . . . . . . . . .6 am Calgary . . . . . . . . . . . . . . . .5 am Vancouver . . . . . . . . . . . . . .4 amCayman Islands . . . . . . . . . . . . . .7 amChile . . . . . . . . . . . . . . . . . . . . . .8 amChina - Beijing . . . . . . . . . . . . . .10 pmColombia . . . . . . . . . . . . . . . . . . .7 amCyprus . . . . . . . . . . . . . . . . . . . .2 pmCzech Republic . . . . . . . . . . . . . .1 pm

DDenmark . . . . . . . . . . . . . . . . . . .1 pmDominican Republic . . . . . . . . . . .7 am

EEcuador . . . . . . . . . . . . . . . . . . . .7 amEgypt . . . . . . . . . . . . . . . . . . . . .2 pmEl Salvador . . . . . . . . . . . . . . . . .6 amEstonia . . . . . . . . . . . . . . . . . . . .2 pm

FFiji . . . . . . . . . . . . . . . . .12 midnightFinland . . . . . . . . . . . . . . . . . . . .2 pmFrance. . . . . . . . . . . . . . . . . . . . .1 pm

GGambia (The) . . . . . . . . . . . . . 12 noonGermany . . . . . . . . . . . . . . . . . . .1 pmGhana . . . . . . . . . . . . . . . . . . 12 noonGreece . . . . . . . . . . . . . . . . . . . .2 pmGrenada . . . . . . . . . . . . . . . . . . .8 amGuatemala . . . . . . . . . . . . . . . . . .6 am

Guernsey . . . . . . . . . . . . . . . . 12 noonGuyana . . . . . . . . . . . . . . . . . . . .7 am

HHong Kong . . . . . . . . . . . . . . . . .8 pmHungary . . . . . . . . . . . . . . . . . . .1 pm

IIndia . . . . . . . . . . . . . . . . . . . 5.30 pmIndonesia. . . . . . . . . . . . . . . . . . .7 pmIreland . . . . . . . . . . . . . . . . . . 12 noonIsle of Man . . . . . . . . . . . . . . 12 noonIsrael . . . . . . . . . . . . . . . . . . . . . .2 pmItaly . . . . . . . . . . . . . . . . . . . . . .1 pm

JJamaica . . . . . . . . . . . . . . . . . . .7 amJapan . . . . . . . . . . . . . . . . . . . . .9 pmJordan . . . . . . . . . . . . . . . . . . . .2 pm

KKenya . . . . . . . . . . . . . . . . . . . . .3 pm

LLatvia . . . . . . . . . . . . . . . . . . . . .2 pmLebanon . . . . . . . . . . . . . . . . . . .2 pmLuxembourg . . . . . . . . . . . . . . . .1 pm

MMalaysia . . . . . . . . . . . . . . . . . . .8 pmMalta . . . . . . . . . . . . . . . . . . . . .1 pmMexico . . . . . . . . . . . . . . . . . . . .6 amMorocco . . . . . . . . . . . . . . . . 12 noon

NNamibia. . . . . . . . . . . . . . . . . . . .2 pmNetherlands (The) . . . . . . . . . . . . .1 pmNew Zealand . . . . . . . . . . .12 midnightNigeria . . . . . . . . . . . . . . . . . . . .1 pmNorway . . . . . . . . . . . . . . . . . . . .1 pm

OOman . . . . . . . . . . . . . . . . . . . . .4 pm

PPanama. . . . . . . . . . . . . . . . . . . .7 amPapua New Guinea. . . . . . . . . . .10 pmPeru . . . . . . . . . . . . . . . . . . . . . .7 amPhilippines . . . . . . . . . . . . . . . . . .8 pmPoland. . . . . . . . . . . . . . . . . . . . .1 pmPortugal . . . . . . . . . . . . . . . . . . .1 pmQQatar. . . . . . . . . . . . . . . . . . . . . .8 am

RRomania . . . . . . . . . . . . . . . . . . .2 pm

international time Zones

AT 12 NOON, GREENwICH MEAN TIME, THE STANDARD TIME ELSEwHERE IS:

PKF Worldwide Tax Guide 2013 VII

Tim

e Zo

nes

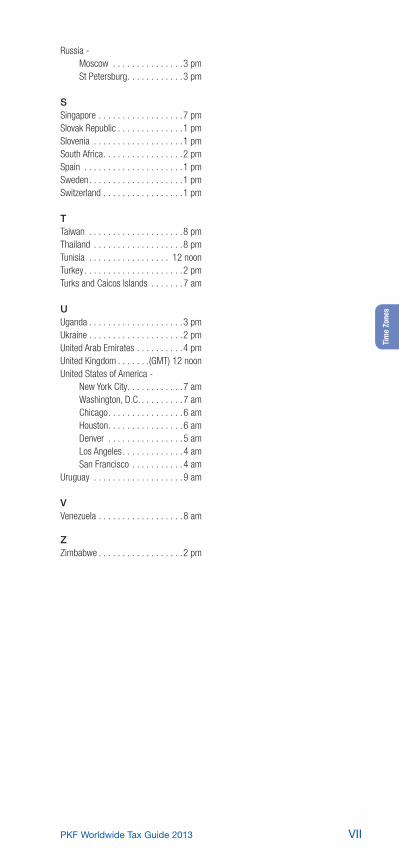

Russia - Moscow . . . . . . . . . . . . . . .3 pm St Petersburg . . . . . . . . . . . .3 pm

SSingapore . . . . . . . . . . . . . . . . . .7 pmSlovak Republic . . . . . . . . . . . . . .1 pmSlovenia . . . . . . . . . . . . . . . . . . .1 pmSouth Africa . . . . . . . . . . . . . . . . .2 pmSpain . . . . . . . . . . . . . . . . . . . . .1 pmSweden . . . . . . . . . . . . . . . . . . . .1 pmSwitzerland . . . . . . . . . . . . . . . . .1 pm

TTaiwan . . . . . . . . . . . . . . . . . . . .8 pmThailand . . . . . . . . . . . . . . . . . . .8 pmTunisia . . . . . . . . . . . . . . . . . 12 noonTurkey . . . . . . . . . . . . . . . . . . . . .2 pmTurks and Caicos Islands . . . . . . .7 am

UUganda . . . . . . . . . . . . . . . . . . . .3 pmUkraine . . . . . . . . . . . . . . . . . . . .2 pmUnited Arab Emirates . . . . . . . . . .4 pmUnited Kingdom . . . . . . .(GMT) 12 noonUnited States of America - New York City . . . . . . . . . . . .7 am Washington, D.C. . . . . . . . . .7 am Chicago . . . . . . . . . . . . . . . .6 am Houston . . . . . . . . . . . . . . . .6 am Denver . . . . . . . . . . . . . . . .5 am Los Angeles . . . . . . . . . . . . .4 am San Francisco . . . . . . . . . . .4 amUruguay . . . . . . . . . . . . . . . . . . .9 am

VVenezuela . . . . . . . . . . . . . . . . . .8 am

ZZimbabwe . . . . . . . . . . . . . . . . . .2 pm

PKF Worldwide Tax Guide 2013 1

colombia

Currency: Peso Dial Code To: 57 Dial Code Out: 09 (P)

Member Firm:City: Name: Contact Information:Bogotá Cristobal Uribe 1 2087500 [email protected]

a. taXes payable

FEDERAL TAxES AND LEVIESINCOME TAxCompanies resident in Colombia are subject to corporate income tax on their worldwide income. Resident corporations are those organised under Colombian law and that have their principal domicile in Colombia. The tax rate for which both domestic companies and branches of foreign companies are taxed is 25%. A reduced 15% rate applies in the ‘free-trade zone’ areas.

The last tax bill reform by congress created an additional annual income tax, . (locally called CREE), which came into force from 1 January 2013. Resident companies and foreign companies that are income tax payers will be subject to this new income tax. The general rate of this new tax is 8% but will be 9% during 2013, 2014 and 2015. The filing of this new tax is on annual basis (1 January – 31 December) so the first tax return to be filed will be during 2014.

It means that Colombian companies and branches are subject to both ordinary income tax at 25% and the new CREE income tax.

In addition, an exemption from SENA (national trainee services) contribution of 2% and ICBF (National familiar promotion entity) contribution of 3.5% (both payroll contributions) will apply for those new taxpayers of CREE. This exemption will apply from 1 July 2013 only for CREE taxpayers and for employees who earn less than ten (10) minimum mandatory wages.

CREE does not apply in free trade zones or for non-profit entities.

CAPITAL GAINSCapital gains are taxed as ordinary income except for a few types of capital gains that may be subject to special taxation (eg gains from lotteries and similar sources) or exempt from income taxation.

EQUITyA net worth tax (impuesto al patrimonio) was generated in 2011 and is payable between 2011 and 2014 by corporate and individual residents. The tax is imposed if the taxpayer’s wealth is equal to or exceeds COP 1 billion on 1 January 2011. The taxpayer’s net wealth includes both wealth located in Colombia and net wealth located abroad.

The tax rate starts at 1% on the value of the wealth between (COP $1.000.000.000 and $2.000.000.000), excluding the net worth of shares or interests in participations in national entities.

VALUE ADDED TAx (VAT)VAT is levied on taxable supplies of goods and services by a taxable person within Colombia and on the importation of goods into Colombia by any person. Exports (and some specific items) are zero rated. The standard rate of VAT is 16%.

Currently in Colombian there are only three VAT rates as follows: 16%, 5% and 0% (the last one for exempt services and goods).

PROPERTy TAxReal estate property is subject to municipal taxation (impuesto predial unificado).

The tax is usually levied at rates within a band of 1 to 16 per thousand, with reference to the cadastral value of each property. Undeveloped plots of land may be subject to increased tax rates.

Colombia

PKF Worldwide Tax Guide 20132

b. determination of taXable income

DEPRECIATIONTax deductions are available for reasonable depreciation rates which reflect the normal wear and tear or obsolescence of the property concerned. The straight-line and the declining-balance methods may be used, along with any other method of recognised technical value authorised by the Auditing Assistant Director of the General Direction of National Taxes.

STOCK/INVENTORyThe average, LIFO, FIFO, retail and specific identification methods may be used in order to value inventories and all are accepted for tax purposes as long as the relevant method is recorded in the accounting books.

LOSSESLosses incurred by a company in a tax year can be carried forward and deducted against ‘liquid income’ in subsequent tax years. Tax losses incurred before 31 December 2006 may be carried forward for only eight years and only 25% of the losses are available to offset each year. There are no group relief provisions.

DIVIDENDSDividends paid to resident shareholders are exempt from income tax if the dividends are distributed out of profits that have been previously taxed at the corporate level. If the distributed profits were not previously taxed at corporate level, they are subject to a withholding tax at the rate of 20% when paid to resident persons and 33% for non-residents.

INTEREST DEDUCTIONInterest is not deductible in full. Income tax payers may deduct an amount not exceeding the average result of a threefold increase in net worth of the previous year end.

FOREIGN SOURCE INCOMEColombia taxes resident companies on worldwide income from all domestic and foreign sources. This includes capital gains from the sale of stock of foreign corporations.

INCENTIVESSpecial tax incentives are provided to investors in certain specified industries such as agricultural plantations dedicated to the cultivation of fruits, anchovies, rubber and cacao, creation of hotels (new and remodeled), and publishing houses. There are also a number of ‘free-trade zones’ and ‘special import-export systems’ which provide for the duty-free entry of capital goods and materials to be used in the production of export goods.

The law 1429 of 2010 gave the following income tax benefits for new small businesses (natural or legal person) that constitute or formalise after this Act, and for inactive enterprises that are reactivated as a result of this law:

a) They do not have to present presumptive income tax in their first 10 years (depending on department to be installed)

b) They calculate the income tax at reduced rates (progressive rates - starting at 0%) for the first 10 years (depending on the department to be installed).

c. foreiGn taX relief

In most cases, double taxation is relieved unilaterally by the granting of a foreign tax credit (FTC) against Colombian corporate income tax.

Taxpayers may credit the amount of foreign tax paid on income from abroad, up to a maximum of the Colombian tax that would be due on the amount of income received from abroad.

Colombian resident companies receiving dividends from foreign companies may credit against both foreign withholding taxes paid on the dividends and also the amount of the underlying foreign income tax paid by the foreign company on the profits from which the dividends were paid.

Colombia

PKF Worldwide Tax Guide 2013 3

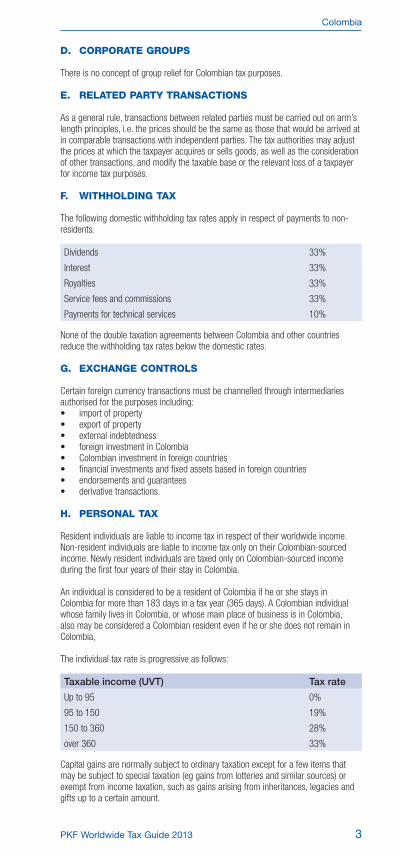

d. corporate Groups

There is no concept of group relief for Colombian tax purposes.

e. related party transactions

As a general rule, transactions between related parties must be carried out on arm’s length principles, i.e. the prices should be the same as those that would be arrived at in comparable transactions with independent parties. The tax authorities may adjust the prices at which the taxpayer acquires or sells goods, as well as the consideration of other transactions, and modify the taxable base or the relevant loss of a taxpayer for income tax purposes.

f. witHHoldinG taX

The following domestic withholding tax rates apply in respect of payments to non-residents.

Dividends 33%

Interest 33%

Royalties 33%

Service fees and commissions 33%

Payments for technical services 10%

None of the double taxation agreements between Colombia and other countries reduce the withholding tax rates below the domestic rates.

G. eXcHanGe controls

Certain foreign currency transactions must be channelled through intermediaries authorised for the purposes including:• importofproperty• exportofproperty• externalindebtedness• foreigninvestmentinColombia• Colombianinvestmentinforeigncountries• financialinvestmentsandfixedassetsbasedinforeigncountries• endorsementsandguarantees• derivativetransactions.

H. personal taX

Resident individuals are liable to income tax in respect of their worldwide income. Non-resident individuals are liable to income tax only on their Colombian-sourced income. Newly resident individuals are taxed only on Colombian-sourced income during the first four years of their stay in Colombia.

An individual is considered to be a resident of Colombia if he or she stays in Colombia for more than 183 days in a tax year (365 days). A Colombian individual whose family lives in Colombia, or whose main place of business is in Colombia, also may be considered a Colombian resident even if he or she does not remain in Colombia,

The individual tax rate is progressive as follows:

Taxable income (UVT) Tax rate

Up to 95 0%

95 to 150 19%

150 to 360 28%

over 360 33%

Capital gains are normally subject to ordinary taxation except for a few items that may be subject to special taxation (eg gains from lotteries and similar sources) or exempt from income taxation, such as gains arising from inheritances, legacies and gifts up to a certain amount.

Colombia

PKF Worldwide Tax Guide 20134

No inheritance (estate) or gift taxes are levied at the federal or the local level. However, certain gifts may be treated as income and therefore be subject to income tax in the hands of individual donees.

i. treaty and non-treaty witHHoldinG rates

Colombia has signed Double Taxation Agreements with Canada, Chile, Spain and Switzerland and the countries of the Andean Community. There is a treaty with Portugal that is not yet in effect.

Colombia

www.pkf.com