COGENERATION POTENTIAL IN JAMAICA - …jamaicasugar.org/wist/Presentations/Cogeneration Potential...

48

COGENERATION POTENTIAL IN COGENERATION POTENTIAL IN JAMAICA JAMAICA WITH AN EMPHASIS ON THE SUGAR INDUSTRY Presented by Mr. Fitzroy A. Vidal Senior Energy Engineer

Transcript of COGENERATION POTENTIAL IN JAMAICA - …jamaicasugar.org/wist/Presentations/Cogeneration Potential...

COGENERATION POTENTIAL IN COGENERATION POTENTIAL IN JAMAICAJAMAICA

WITH AN EMPHASISON THE SUGAR INDUSTRY

Presented byMr. Fitzroy A. Vidal

Senior Energy Engineer

7 May 2008 Prepared by the Energy Division, MITEC 2

PRESENTATION OUTLINEPRESENTATION OUTLINE

Introduction What is Cogeneration?The Cogeneration ProcessHistory of Cogeneration in Jamaica Current Cogeneration Plants and Potential for ExpansionCogeneration Potential in the Sugar Cane IndustryBenefits of CogenerationEthanol ProductionReplacement of MTBE as Fuel EnhancerThe Way Forward

7 May 2008 Prepared by the Energy Division, MITEC 3

INTRODUCTIONINTRODUCTION

Improving Plant EfficiencyIncreasing Global Ambient TemperatureMelting Of Solar Cap Increasing Frequency And Magnitude Of Natural Disasters

7 May 2008 Prepared by the Energy Division, MITEC 4

WHAT IS COGENERATION?WHAT IS COGENERATION?

Otherwise called Combined Heat and Power (CHP)The simultaneous production of electric power and other forms of useful energy, like heat or process steam, from the same facilityThe process by which an industrial facility uses its waste energy to produce heat and electricity.– Efficient, clean, and reliable approach to generating

power and thermal energy from a single fuel source– Conventional plant efficiency, 20-33%– CHP increases plant efficient up to 85%

7 May 2008 Prepared by the Energy Division, MITEC 5

bagasse

electricity

Sugar & Ethanol plants produce their own thermal & electric energy using bagasse as a fuel in cogeneration systems and sell excess electricity to the public grid.

THE COGENERATION PROCESS

Source: UNICA

thermal

7 May 2008 Prepared by the Energy Division, MITEC 6

HISTORY OF COGENERATION IN JAMAICAHISTORY OF COGENERATION IN JAMAICA

The Role of Sugar in Pre - Independent JamaicaThe Emergence of Bauxite and the Mining SectorPost – Independent Jamaica

• 1962 – 1982• 1982 – Present

The Energy CrisesVulnerability of Jamaica’s Energy SectorEnvironmental Considerations

7 May 2008 Prepared by the Energy Division, MITEC 7

Bauxite - Alumina sector Sugar sectorJPSCo. Bogue Power PlantOther Plants:– Jamaica Broilers– Petrojam Refinery– Caribbean Cement Company

CURRENT COGENERATION PLANTS AND CURRENT COGENERATION PLANTS AND THEIR POTENTIAL FOR EXPANSIONTHEIR POTENTIAL FOR EXPANSION

7 May 2008 Prepared by the Energy Division, MITEC 8

Cogeneration In The Bauxite SectorCogeneration In The Bauxite Sector

Alumina Refineries

Company Location Alumina Existing Capacity

Production Possible Expansion

Existing Cogen Capacity

Potential

Million tones/yr MW

1 Jamalco Halse Hall 1.3 1.3 50 Currently supply 5-6 MW to JPSCo.Expansion will enable an additional 55 MW to JPS

2 Windalco Ewarton 0.6 0.4 25 Requires 4.5 MW from Grid for emergency.

3 Windalco Kirkvine 0.6 0.1 25 Requires 6 MW from Grid for emergency.

4 Alpart St. Elizabeth 1.65 0.3 50 Operate at 60 Hz

Sub-Total 4.15 2.1 150

Table 1 Sources: National Integrated Electricity Expansion Plan and Study for Jamaica.

7 May 2008 Prepared by the Energy Division, MITEC 9

Cogeneration In The Sugar SectorCogeneration In The Sugar SectorSugar Refineries Potential

SCJCompany

Installed CogenCapacity

CapacityDiesels

JPSCOPurchases(million KWh)

notes

MW

1 Frome 5.5 3.1 None SCJ factories use bagasse and HFO (over 2 million liters/yrs)

Mukherji repot indicated a potential of 20-30 MW of cogeneration capacity, hence reduced HFO consumption

2 Monymusk 4 1.8

3 Bernard Lodge

2.5 1.2

4 St. Thomas 1.5 0.6

5 Long Pond 1.6 1.4

6 Appleton 3.25 2 yes Operates at 60HZ

7 Worthy Park N/Av N/Av N/Av

Sub Total 18.35 5.1 5

7 May 2008 Prepared by the Energy Division, MITEC 10

Other Cogeneration PlantsOther Cogeneration Plants

Others Producer

Company InstalledCogenCapacity

Capacity Diesels

JPSCOPurchases(million MWh)

Potential

MW

1 Jamaica Broiler

17.5 no Plan for expansion

2 Caribbean Cement

None 2 yes Purchase 13.8 MW from grid. Expansion requires 20 MW and a 30 MW unit will be installing.

3 Petrojam 1.4 yes Phase one- Expansion required 10-15 MW and this will enable 5 MW for export to the grid.Phase one- Expansion required 80 MW and this will provide 60-65 MW and a 10 MW for export to the grid.

Sub Total 18.9

7 May 2008 Prepared by the Energy Division, MITEC 11

BENEFITS OF COGENERATIONBENEFITS OF COGENERATIONEconomic – Enhance plant efficiency– Utilize generated waste (bagasse and heat) – Utilize indigenous materials– Increase production output– Increase revenue– Increase CO2 production– Increase Carbon trading potential – Produce Ethanol

• Replace MTBE as fuel enhancer• Increase export potential

– Save Foreign Currency– Earn Foreign Currency

Environmental

7 May 2008 Prepared by the Energy Division, MITEC 12

Cogeneration Environmental Benefits Each additional 100 million tonnes of cane produced will avoid 1Each additional 100 million tonnes of cane produced will avoid 12.6 million tonnes of CO2.6 million tonnes of CO22 --

(ethanol, bagasse and surplus electricity)(ethanol, bagasse and surplus electricity)

76

Szwarc, A.

Sugar Cane and the CO2 Cycle

EthanolElectric Energy

Neat Ethanol or Blends

Co-generation

Sugar

CO

Bagasse

Ethanol

Sugar

CO2

CO2

Sugar Cane Field

Photosynthesis

CO2

Ethanol

7 May 2008 Prepared by the Energy Division, MITEC 13

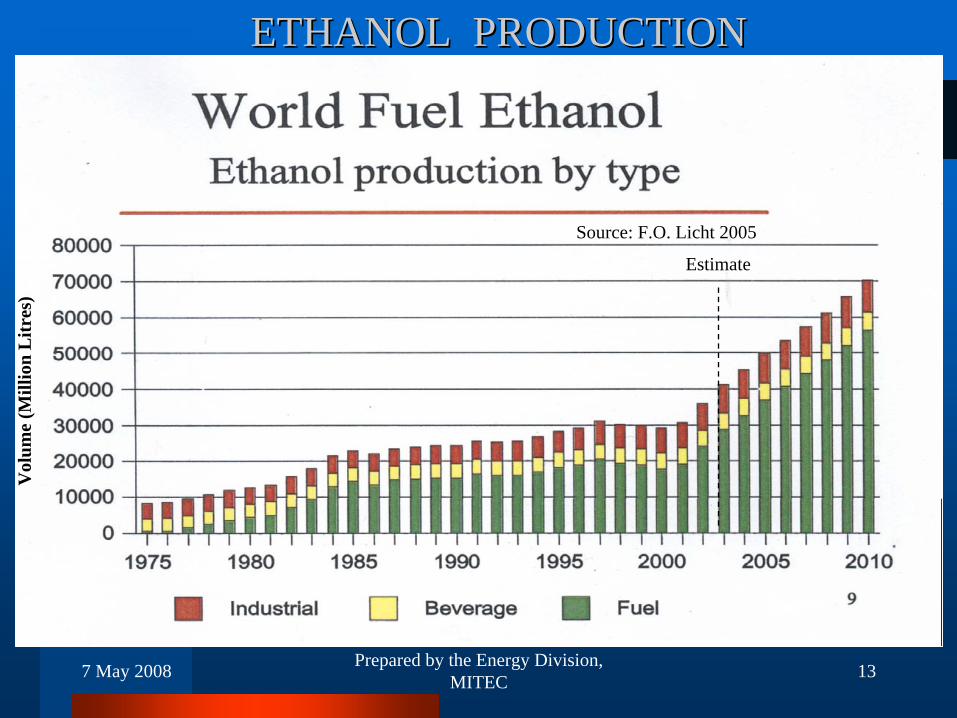

ETHANOL PRODUCTIONETHANOL PRODUCTION

Source: F.O. Licht 2005

Estimate

Vol

ume

(Mill

ion

Litr

es)

7 May 2008 Prepared by the Energy Division, MITEC 14

Annual Ethanol Exports To The USA

Million Gallons/Year

7 May 2008 Prepared by the Energy Division, MITEC 15

2005 (million liters)

US Supply & Demand – Imports from CBI

2005 (billion liters)

Total: 391.7

Source: F.O.Licht, Coimex

7 May 2008 Prepared by the Energy Division, MITEC 16

Sugar Cane Production & Conversion To Ethanol

50

100

150

200

250

300

350

400

45075

/76

76/7

777

/78

78/7

979

/80

80/8

181

/82

82/8

383

/84

84/8

585

/86

86/8

787

/88

88/8

989

/90

90/9

191

/92

92/9

393

/94

94/9

595

/96

96/9

797

/98

98/9

999

/00

00/0

101

/02

02/0

303

/04

04/0

505

/06

Mill

ion

Tonn

es

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

% C

onve

rsio

n

Cane Production % Cane to EthanolSource: UNICA

The trend is to convert a higher percentage of cane to ethanol: 58% of 575 Mt in 2010

7 May 2008 Prepared by the Energy Division, MITEC 17

21

Szwarc, A.

Brazilian Concept of Integrated Sugar & Ethanol Production

Sugarcane Transport,Cleaning & Crushing

JuiceTreatment

Fermentation

SugarProduction

Distillation

Dehydration

HydrousEthanol

AnhydrousEthanol

Process Heat &Cogeneration

Bagasse

Molasses

PrimaryJuice

Secondary + Filter Juice

SUGAR, ETHANOL, ENERGY, DRY YEASTS, CARBON DIOXIDE, FUSEL OIL, FILTER CAKE

7 May 2008 Prepared by the Energy Division, MITEC 18

Brazil Thailand India USA EU

Cane

Wheat

Beet

CornCane

Cane Cassava

2004 - Ethanol Cost Of Production

Source: F.O.Licht, Coimex

US$

/lite

r

7 May 2008 Prepared by the Energy Division, MITEC 19

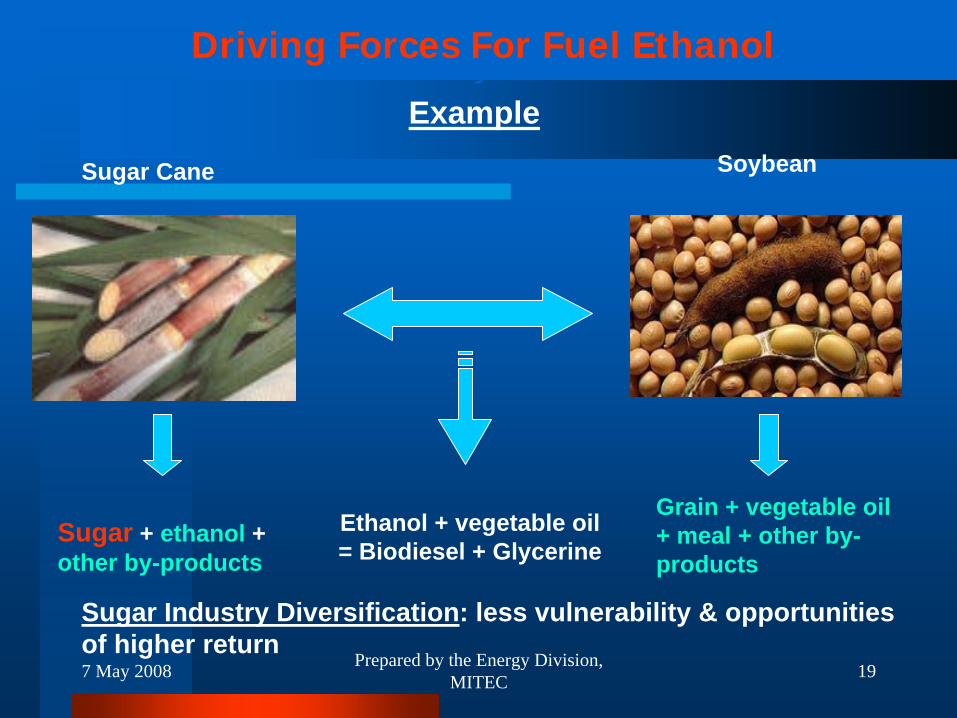

MOTIVAÇÃO

Sugar Industry Diversification: less vulnerability & opportunities of higher return

Ethanol + vegetable oil = Biodiesel + Glycerine

Sugar + ethanol + other by-products

Grain + vegetable oil + meal + other by- products

SoybeanSugar Cane

Driving Forces For Fuel Ethanol

Example

7 May 2008 Prepared by the Energy Division, MITEC 20

METHY TERTIARYMETHY TERTIARY--BUTYL ETHER (MTBE)BUTYL ETHER (MTBE)

Economic Impact– Foreign Exchange

SavingsEnvironmental impact– Non- biodegradable– Ground water

contamination

Jamaica MTBE IMPORT

YearVolume Cost

Barrel x 1000 US$M

2004 49.6 3.2

2005 68.5 4.4

Jan-June 2006 94.6 7.7

7 May 2008 Prepared by the Energy Division, MITEC 21

Production Of Ethanol And MTBE In The Production Of Ethanol And MTBE In The USAUSA

0.0

0.1

0.2

0.3

0.4

0.5Ja

n-02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Forecast

Year Ethanol MTBEJan 2006 0.288 0.120Jan 2007 0.350Jan 2008 0.416

Ethanol

MTBE

Considerable number of refiners are expected to halt MTBE use by May 2006

Source: EIA, April 2006

Vol

ume

(Mill

ion

Bbl

s/da

y)

7 May 2008 Prepared by the Energy Division, MITEC 22

•Diversify the National Fuel Base

•Modernize, Diversify and Expand the Sugar Industry

•Save Jobs and Create Employment

•Increase Production of Ethanol

•Promote Opportunities For New Investments

•Implement the New National Energy Policy

•Complete the Replacement of MTBE

•Harness all Available Resources of Tradition,

• Know-how, Land, Climate, and Labour

•Reduce Green-House Emissions

•Earn Foreign Exchange - Exports and Carbon Trading

WAY FORWARD

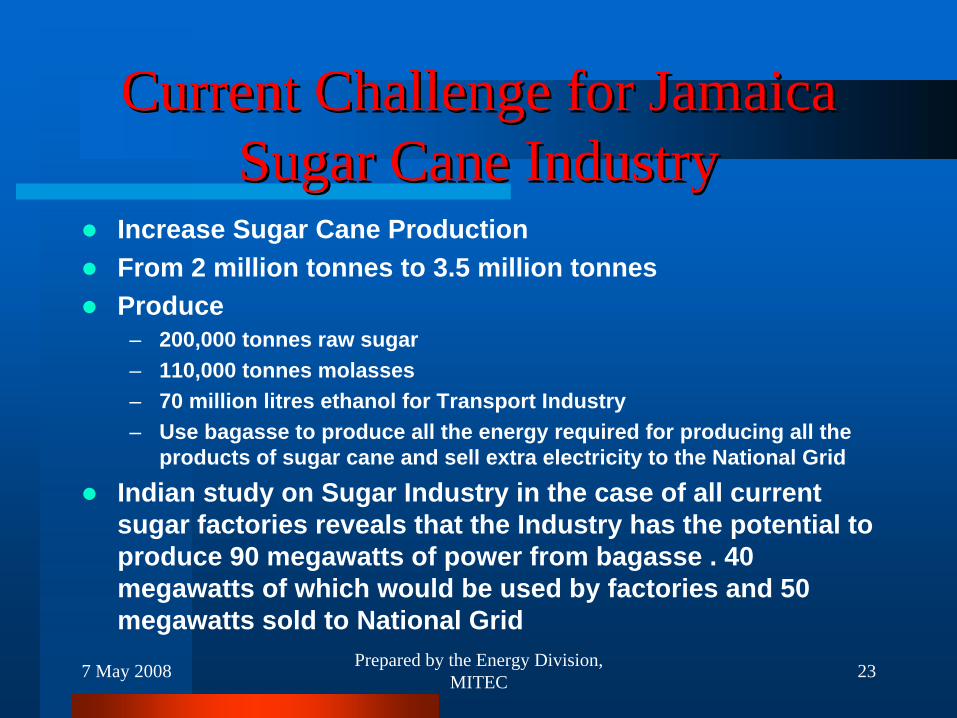

Current Challenge for Jamaica Current Challenge for Jamaica Sugar Cane Industry Sugar Cane Industry

Increase Sugar Cane ProductionFrom 2 million tonnes to 3.5 million tonnesProduce

– 200,000 tonnes raw sugar– 110,000 tonnes molasses – 70 million litres ethanol for Transport Industry– Use bagasse to produce all the energy required for producing all the

products of sugar cane and sell extra electricity to the National Grid

Indian study on Sugar Industry in the case of all current sugar factories reveals that the Industry has the potential to produce 90 megawatts of power from bagasse . 40 megawatts of which would be used by factories and 50 megawatts sold to National Grid

7 May 2008 Prepared by the Energy Division, MITEC 23

Replacing MTBE with EthanolReplacing MTBE with EthanolIncrease in popularity of ethanol in transport gasoline globally

– Renewable – Can produce locally– Environmentally friendly– Earning carbon credits

Jamaica plans ethanol addition to fuel at 10% levelProduction from local sugar cane within 3 yearsTarget 18 million gallons annuallyCan produce ethanol competitively in Jamaica

– Ethanol produced from local feed stock enters EU and USA duty free and quota free

– Ethanol can be added in different percentages popular ones between E10 and E85

7 May 2008 Prepared by the Energy Division, MITEC 24

PRODUCTION OF ETHANOL PRODUCTION OF ETHANOL ANDAND

POSSIBILTIES FOR JAMAICAPOSSIBILTIES FOR JAMAICA

EXPLORATION OF ALTERNATIVE EXPLORATION OF ALTERNATIVE ENERGYENERGY

Oil priced having reached US$100 per barrel forced many countries to explore alternative source of energy.

Emphasis is then placed on renewable energy.

ALTERNATIVE ENERGYALTERNATIVE ENERGYETHANOL- Has attracted greatest interest

Ethanol can be produced from:– Sugarcane– Corn– Sorghum– Cassava– and a wide range of cellulosic material

PRODUCERS OF ETHANOLPRODUCERS OF ETHANOL

USA - World leading producer Brazil - Largest Exporter

Other producers are:– Thailand – Nigeria– China– Jamaica

SOURCES OF RAW MATERIAL SOURCES OF RAW MATERIAL USED BY PRODUCERSUSED BY PRODUCERS

Most countries use sugar cane as their source of raw material.

Thailand and Nigeria use cassavaUSA and China use corn Jamaica uses sugarcane.

POSSIBILITIES FOR JAMAICAPOSSIBILITIES FOR JAMAICAThe experience gained in producing rum will prove very useful in the production of Ethanol.

However, Jamaica will not be starting from scratch, technologically.

In the 1980’s they have produced ethanol from sugarcane molasses and sweet sorghum.

The first requirement is to significantly increase the production of sugarcane.

POSSIBILITES FOR JAMAICAPOSSIBILITES FOR JAMAICA

Jamaica should produce over 2 million tonnes of cane for the current crop.

The first target, however, is to produce 3 million tonnes by 2010.

The next target - Produced 18 million gallons of ethanol to replace MTBE in local transport fuel.

POSSIBILITIES FOR JAMAICAPOSSIBILITIES FOR JAMAICA

Calculations show that we can produce Anhydrous ethanol for under US$2.00 per gallon.

The current price, delivered to New York Harbour, is US$2.45 per gallon.

United States having a new energy bill mandating greater mix of ethanol in gasolene in many more states, there will be a greater demand for ethanol.

POSSIBILITIES FOR POSSIBILITIES FOR JAMAICAJAMAICA

In an attempt to service the 5 million flexi-fuel cars that are expected to be on the roads in the USA, there is an expectation that additional outlets will be available for the sale of :

– Ethanol mixed gasoline–E-10–E-85

POSSIBILITIES FOR POSSIBILITIES FOR JAMAICAJAMAICA

Florida is believed to be the next state to fully launch ethanol use in gasolene.

Jamaica, being in close proximity to that State is expected to have greater volumes going there.

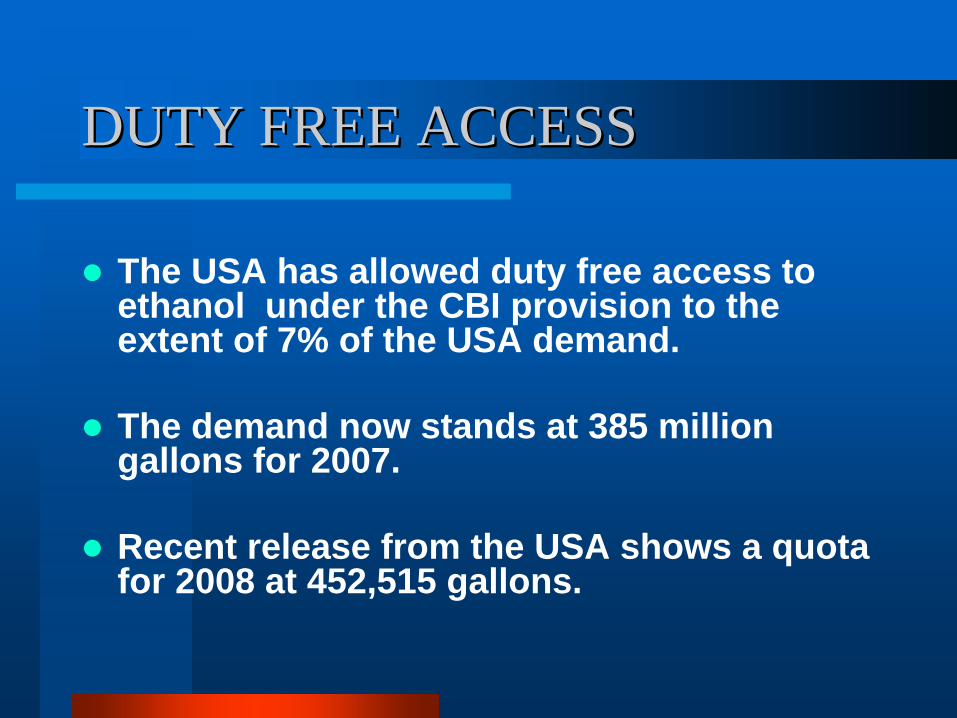

DUTY FREE ACCESS DUTY FREE ACCESS

The USA has allowed duty free access to ethanol under the CBI provision to the extent of 7% of the USA demand.

The demand now stands at 385 million gallons for 2007.

Recent release from the USA shows a quota for 2008 at 452,515 gallons.

DUTY FREE ACCESSDUTY FREE ACCESS

The highest delivery from all CBI countries was 260 million gallons in 2006.

In 2007, delivery is projected to be well below the 2006 amount due to the softness of the USA ethanol market during the first half of the year.

DUTY FREE ACCESSDUTY FREE ACCESS

The 7% cap on duty free access applies only to ethanol produced from feedstock imported from out of the region. If it is produced from locally grown sugarcane there is no limit on the quantity that is allowed to enter the USA duty free.

DUTY FREE ACCESSDUTY FREE ACCESS

The same provision applies to the EU if the ethanol is produced from local feedstock.

The production of the 18 million gallons for the local transport industry must be seen as first target.

ECONOMICS OF SUPPLYING ECONOMICS OF SUPPLYING SUGAR TO THE EU MARKETSUGAR TO THE EU MARKET

We must be aware that when the price of sugar delivered to the EU market is reduced by 36% as of 2010, we will have to examine the economics of continuing to supply raw sugar to them.

However, as the price is being drastically reduced, there is a massive increase in the cost to deliver the sugar to the EU.

ECONOMICS OF SUPPLYING ECONOMICS OF SUPPLYING SUGAR TOSUGAR TO THE EU MARKETTHE EU MARKET

Cost per tonne for freight in 2007 was €32 per tonne to the UK - this is most of the sugar is delivered.

For the 2008 delivery period, the cost will be €73 per tonne as a result of the jump in oil price.

ECONOMICS OF SUPPLYING SUGARECONOMICS OF SUPPLYING SUGAR TO THE EU MARKETTO THE EU MARKET

In 2010 when the sugar price is reduced to €335 per tonne, if the freight remains at the 2008 rate, net to the Jamaican producer will be €262 per tonne sugar.

If the exchange rate is US$1.40 to the Euro, the price will be US$336.80 per tonne or US$.1664¢per lb.

ECONOMICS OF SUPPLYING ECONOMICS OF SUPPLYING SUGAR SUGAR TO THE EU MARKETTO THE EU MARKET

It may be better business for the Jamaican Sugar Industry to produce more ethanol than sugar.

The demand for ethanol worldwide is projected to keep increasingly significantly each year as the search for renewable energy intensifies.

Sugar is still regarded as the most efficient producer of ethanol among all sources.

ETHANOL AS A ETHANOL AS A ‘‘SUNRISESUNRISE’’ INDUSTRYINDUSTRY

In the midst of very high oil prices and the desire by more countries to become greener, ethanol from sugarcane is considered a ‘sunrise’ industry that will make all the difference to the Sugarcane Industry in Jamaica.

Once we begin to produce ethanol from local sugarcane we will then have the flexibility to move easily between sugar and ethanol as the economics dictate.

VALUE OF ETHANOL TO THEVALUE OF ETHANOL TO THE SUGAR INDUSTRYSUGAR INDUSTRY

$6,000.00 per tonne molasses = US$84.50 @ J$71.00 300 litres ethanol per tonne Blackstrap molasses;

• J$20 per litre @71.00:US$1.00 = US$28.17¢

–

3.75 litres

per gallon = $1.056 per gallon

–

Material is 60% of cost of ethanol produced, therefore:–

Price =

US$1.76 per gallon

–

Cost of dehydrating

=

.18¢

per gallon

–

Total Cost

=

US$1.94 per gallon–

Selling price @ $2.00 per gallon

–

Value added is US$.06¢

per gallon

–

Value added per tonne

molasses = US$4.80 per tonne

–

Value in local currency = J$340.80 -

62% at 12 tonnes

cane TC/TS

–

Additional income to farmers -

J$17.60 per tonne

cane

Every 0.6¢ increase in price yields $17.70 per tonne cane to farmers.

VALUE OF ETHANOL TO THEVALUE OF ETHANOL TO THE SUGAR INDUSTRYSUGAR INDUSTRY

In the 2007 crop average earnings by cane farmers was $2,212.55 per tonne cane delivered. Of this amount, molasses contributed $154.45 , leaving sugar to account for $2,058.10.

The illustration on preceding slide showed an additional earning of J$17.60 per tonne cane if ethanol was produced from some molasses and sold at US$2.30 per gallon FOB Kingston.

VALUE OF ETHANOL TO THE VALUE OF ETHANOL TO THE SUGAR INDUSTRYSUGAR INDUSTRY

The additional earning for cane farmers would be:

• $17.60 x 6 = $105.60 per tonne cane

His total earning would therefore be:• $154.45 + $105.60 = $260.05 tonnes cane

delivered

VALUE OF ETHANOL TO THE VALUE OF ETHANOL TO THE SUGAR INDUSTRYSUGAR INDUSTRY

Payment to the sugarcane producer should reflect the improved earnings from ethanol.

This will be an incentive to keep increasing the production of sugarcane, thus ensuring rural stability and reduction of the rural-urban drift.

In addition to the above, there will be savings on foreign exchange outflows and while the country adds ethanol to the gasolene, we will be helping to save the environment.

7 May 2008 Prepared by the Energy Division, MITEC 48

THANK YOU FOR YOUR ATTENTIONTHANK YOU FOR YOUR ATTENTION

QUESTIONS?QUESTIONS?