Code of Professional Conduct and Relevant Actuarial Standards of Practice March, 18, 2008 Ratemaking...

46

Code of Professional Conduct and Relevant Actuarial Standards of Practice March, 18, 2008 Ratemaking Seminar Boston

-

Upload

charity-owens -

Category

Documents

-

view

213 -

download

0

Transcript of Code of Professional Conduct and Relevant Actuarial Standards of Practice March, 18, 2008 Ratemaking...

Code of Professional Conduct and Relevant Actuarial Standards of Practice

March, 18, 2008Ratemaking SeminarBoston

Agenda

Code of Conduct/Code of Professional Ethics

Relevant Actuarial Standards of Practice

Case Studies

Code of Professional Conduct

Code of Professional Conduct

Definitions

Precepts & Annotations

Canadian Issues

Code of Ethics for Students

Key Definitions within Code

Actuarial Communication Actuarial Services Actuary Confidential Information Law Principal Recognized Actuarial Organization

Precepts and Annotations

Professional Integrity Qualification Standards Standards of Practice Communications and Disclosures Conflict of Interest Control of Work Product Confidentiality Courtesy and Cooperation Advertising Titles and Designations Violations of the Code of Professional Conduct

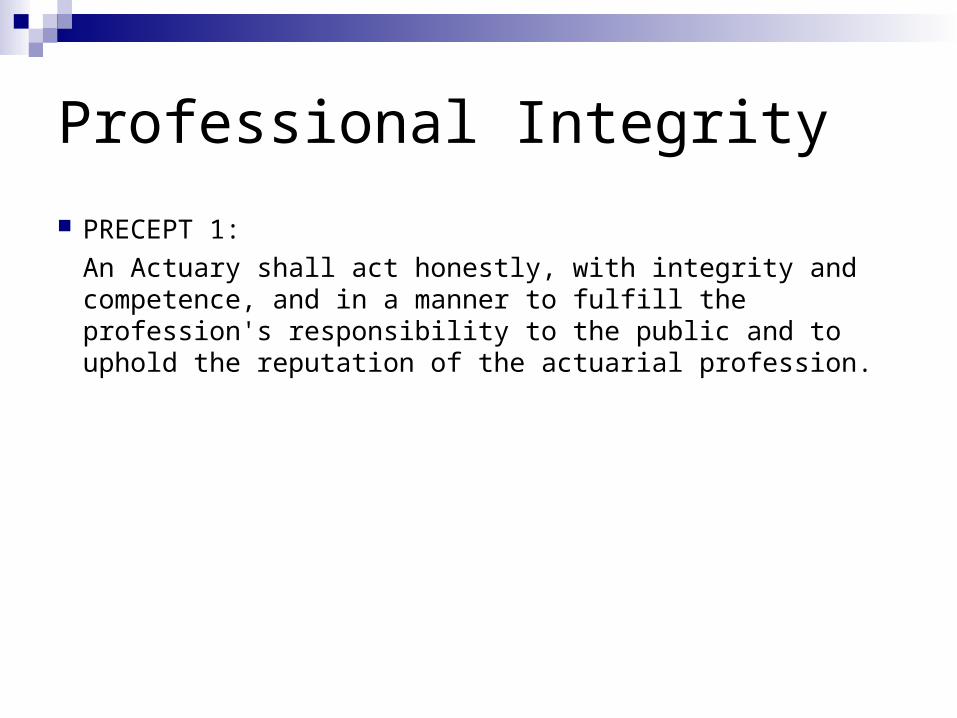

Professional Integrity

PRECEPT 1:

An Actuary shall act honestly, with integrity and competence, and in a manner to fulfill the profession's responsibility to the public and to uphold the reputation of the actuarial profession.

Qualification Standards

PRECEPT 2:

An Actuary shall perform Actuarial Services only when the Actuary is qualified to do so on the basis of basic and continuing education and experience and only when the Actuary satisfies applicable qualification standards.

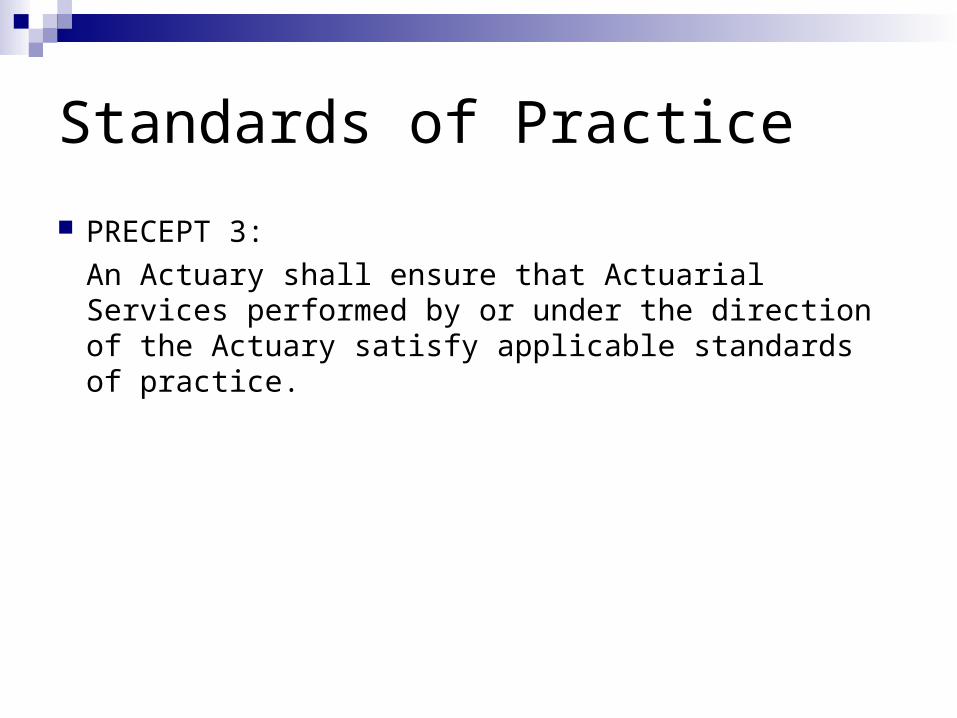

Standards of Practice

PRECEPT 3:

An Actuary shall ensure that Actuarial Services performed by or under the direction of the Actuary satisfy applicable standards of practice.

Communications and Disclosure

PRECEPT 4:

An Actuary who issues an Actuarial Communication shall take appropriate steps to ensure that the Actuarial Communication is clear and appropriate to the circumstances and its intended audience and satisfies applicable standards of practice.

Communications and Disclosure

PRECEPT 5:

An Actuary who issues an Actuarial Communication shall, as appropriate, identify the Principal(s) for whom the Actuarial Communication is issued and describe the capacity in which the Actuary serves.

Communications and Disclosure PRECEPT 6:

An Actuary shall make appropriate and timely disclosure to a present or prospective Principal of the sources of all direct and indirect material compensation that the Actuary or the Actuary's firm has received, or may receive, from another party in relation to an assignment for which the Actuary has provided, or will provide, Actuarial Services for that Principal. The disclosure of sources of material compensation that the Actuary's firm has received, or may receive, is limited to those sources known to, or reasonably ascertainable by, the Actuary.

Conflict of Interest

PRECEPT 7:An Actuary shall not knowingly perform Actuarial Services involving an actual or potential conflict of interest unless: the Actuary’s ability to act fairly is unimpaired; there has been disclosure of the conflict to all present

and known prospective Principals whose interests would be affected by the conflict; and

all such Principals have expressly agreed to the performance of the Actuarial Services by the Actuary.

Control of Work Product

PRECEPT 8:

An Actuary who performs Actuarial Services shall take reasonable steps to ensure that such services are not used to mislead other parties.

Confidentiality

PRECEPT 9:

An Actuary shall not disclose to another party any Confidential Information unless authorized to do so by the Principal or required to do so by Law.

Courtesy and Cooperation

PRECEPT 10:

An Actuary shall perform Actuarial Services with courtesy and professional respect and shall cooperate with others in the Principal's interest.

Advertising

PRECEPT 11:

An Actuary shall not engage in any advertising or business solicitation activities with respect to Actuarial Services that the Actuary knows or should know are false or misleading.

Titles and Designations

PRECEPT 12:

An Actuary shall make use of membership titles and designations of a Recognized Actuarial Organization only in a manner that conforms to the practices authorized by that organization.

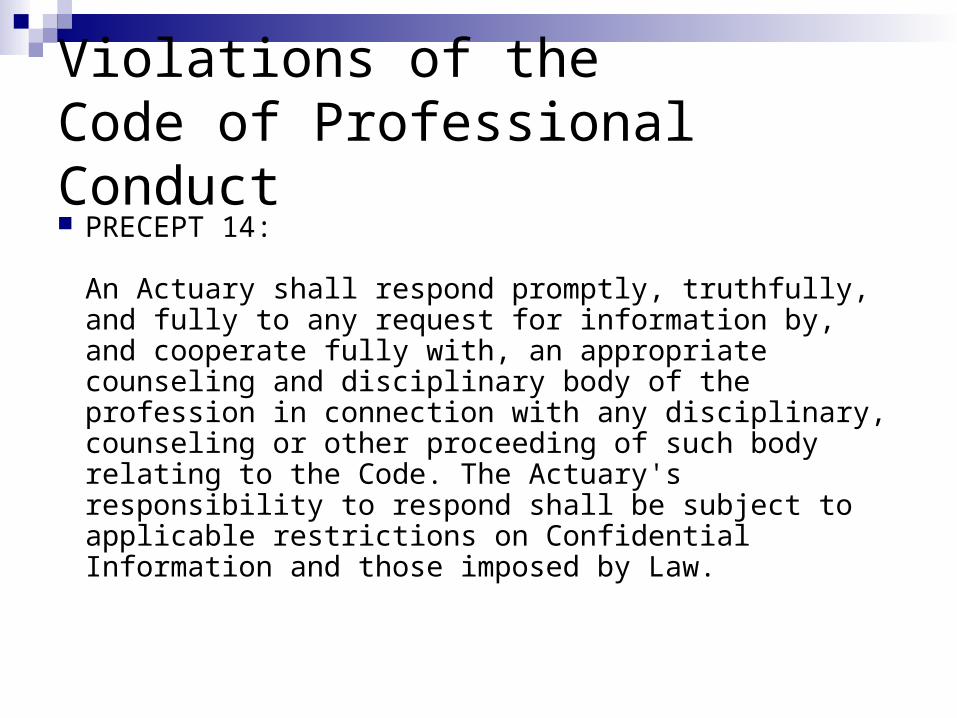

Violations of the Code of Professional Conduct PRECEPT 13:

An Actuary with knowledge of an apparent, unresolved, material violation of the Code by another Actuary should consider discussing the situation with the other Actuary and attempt to resolve the apparent violation. If such discussion is not attempted or is not successful, the Actuary shall disclose such violation to the appropriate counseling and discipline body of the profession, except where the disclosure would be contrary to Law or would divulge Confidential Information.

PRECEPT 14:

An Actuary shall respond promptly, truthfully, and fully to any request for information by, and cooperate fully with, an appropriate counseling and disciplinary body of the profession in connection with any disciplinary, counseling or other proceeding of such body relating to the Code. The Actuary's responsibility to respond shall be subject to applicable restrictions on Confidential Information and those imposed by Law.

Violations of the Code of Professional Conduct

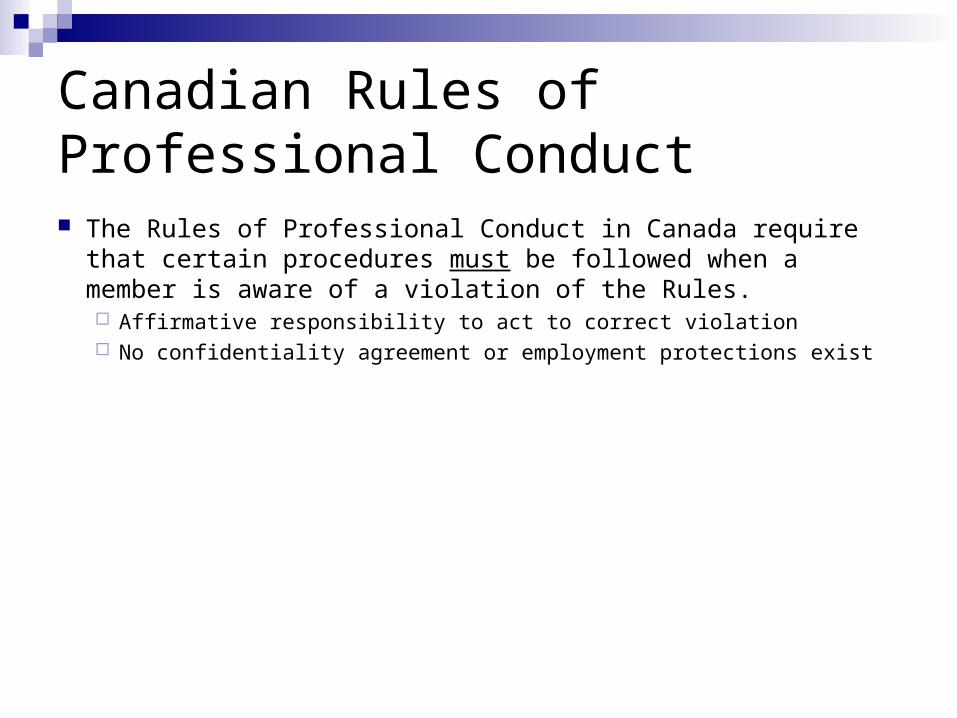

Canadian Rules of Professional Conduct The Rules of Professional Conduct in Canada require

that certain procedures must be followed when a member is aware of a violation of the Rules. Affirmative responsibility to act to correct violation No confidentiality agreement or employment protections exist

Code of Professional Ethics

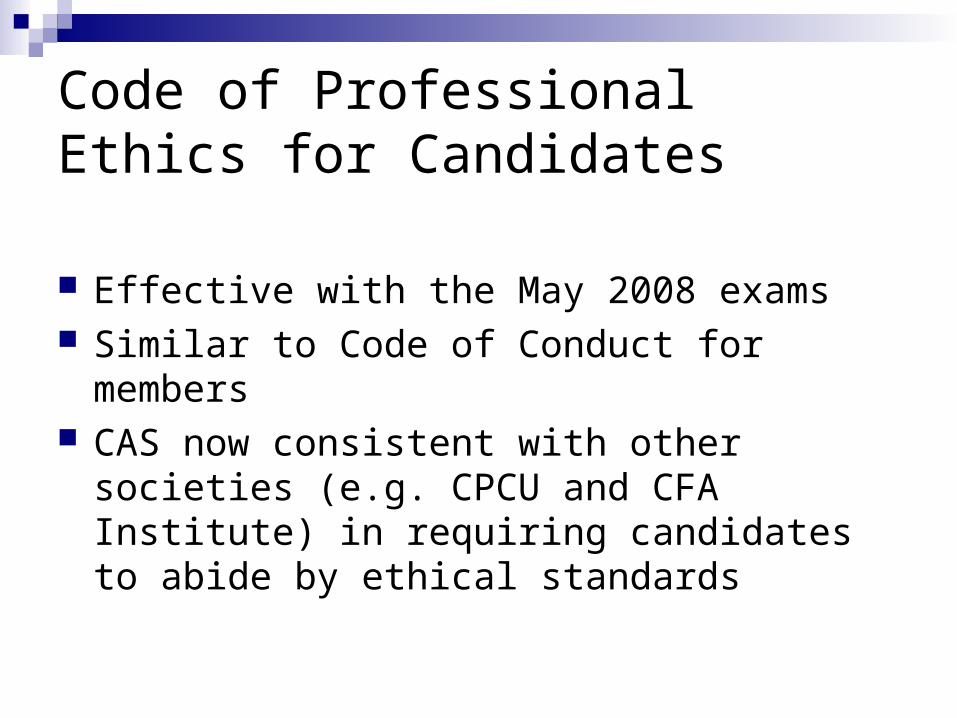

Code of Professional Ethics for Candidates

Effective with the May 2008 exams Similar to Code of Conduct for members CAS now consistent with other societies (e.g.

CPCU and CFA Institute) in requiring candidates to abide by ethical standards

Code of Professional Ethics for Candidates

Rules 1 & 2 = Precept 1: IntegrityRule 3 = Precept 10: CourtesyRule 4: Exam disciplineRule 5 = Precept 12: Titles/DesignationsRule 6 = Precept 9: ConfidentialityRule 7 = Precept 14: Respond

promptly/cooperate

Code of Professional Ethics for Candidates

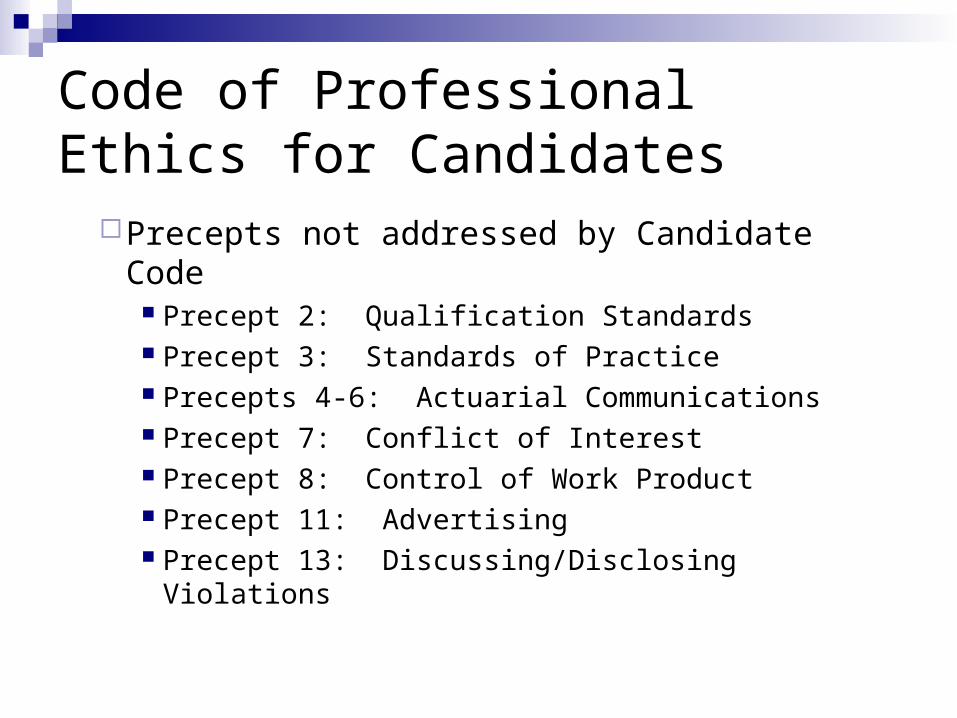

Precepts not addressed by Candidate Code Precept 2: Qualification Standards Precept 3: Standards of Practice Precepts 4-6: Actuarial Communications Precept 7: Conflict of Interest Precept 8: Control of Work Product Precept 11: Advertising Precept 13: Discussing/Disclosing Violations

Actuarial Standards of Practice

Actuarial Standards of Practice and Ratemaking

Actuaries need to be aware of the applicability of the different ASOPs to the work that they perform

The Council on Professionalism of the AAA has developed the “Applicability Guidelines for Actuarial Standards of Practice”

Applicability Guidelines

These guidelines are not meant to be exhaustive and only provide “non authoritative” guidance

Ultimately, it remains the actuary’s responsibility to identify the standards that apply to each assignment and to appropriately apply such requirements

These are updated periodically and it is the actuary’s responsibility to keep current with changes to ASOPs

The guidelines are not standards of practice These were not promulgated by the Actuarial Standards

Board

ASOPs Applicable to Ratemaking

Up to 10 ASOPs may apply to the different actuarial tasks related to product development/ratemaking/pricing # 9 Documentation and Disclosure # 12 Risk Classification # 13 Trending Procedures # 23 Data Quality # 25 Credibility Procedures # 29 Expense Provisions # 30 Treatment of Profit and Contingency Provisions and Cost of

Capital # 38 Using Model’s Outside Actuary’s Area of Expertise # 39 Treatment of Catastrophe Losses # 41 Actuarial Communications

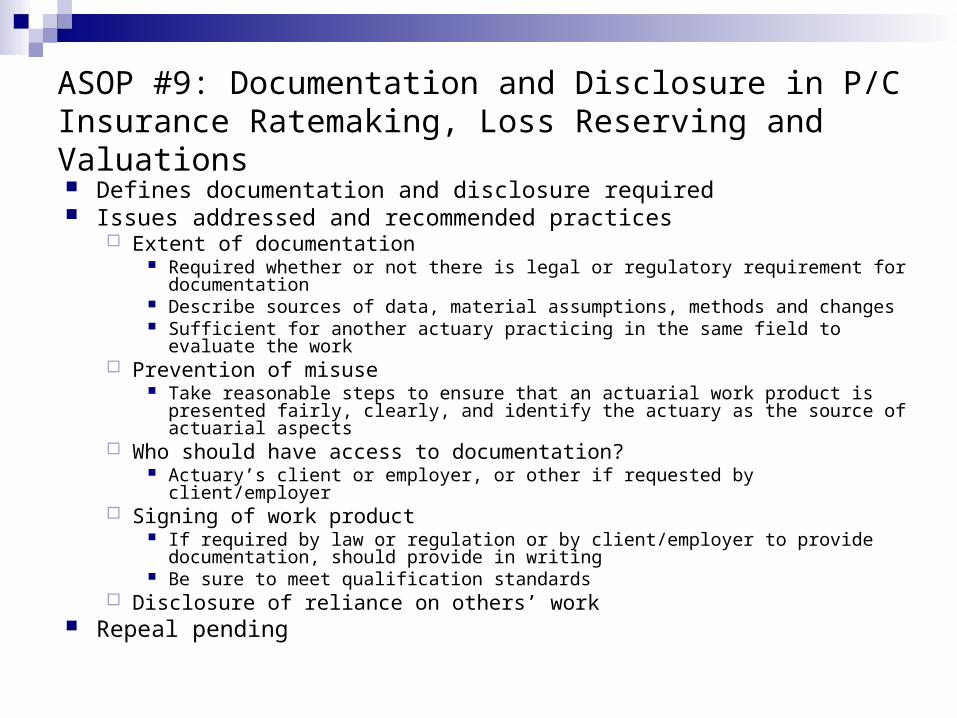

ASOP #9: Documentation and Disclosure in P/C Insurance Ratemaking, Loss Reserving and Valuations Defines documentation and disclosure required Issues addressed and recommended practices

Extent of documentation Required whether or not there is legal or regulatory requirement for

documentation Describe sources of data, material assumptions, methods and changes Sufficient for another actuary practicing in the same field to evaluate the work

Prevention of misuse Take reasonable steps to ensure that an actuarial work product is presented

fairly, clearly, and identify the actuary as the source of actuarial aspects Who should have access to documentation?

Actuary’s client or employer, or other if requested by client/employer Signing of work product

If required by law or regulation or by client/employer to provide documentation, should provide in writing

Be sure to meet qualification standards Disclosure of reliance on others’ work

Repeal pending

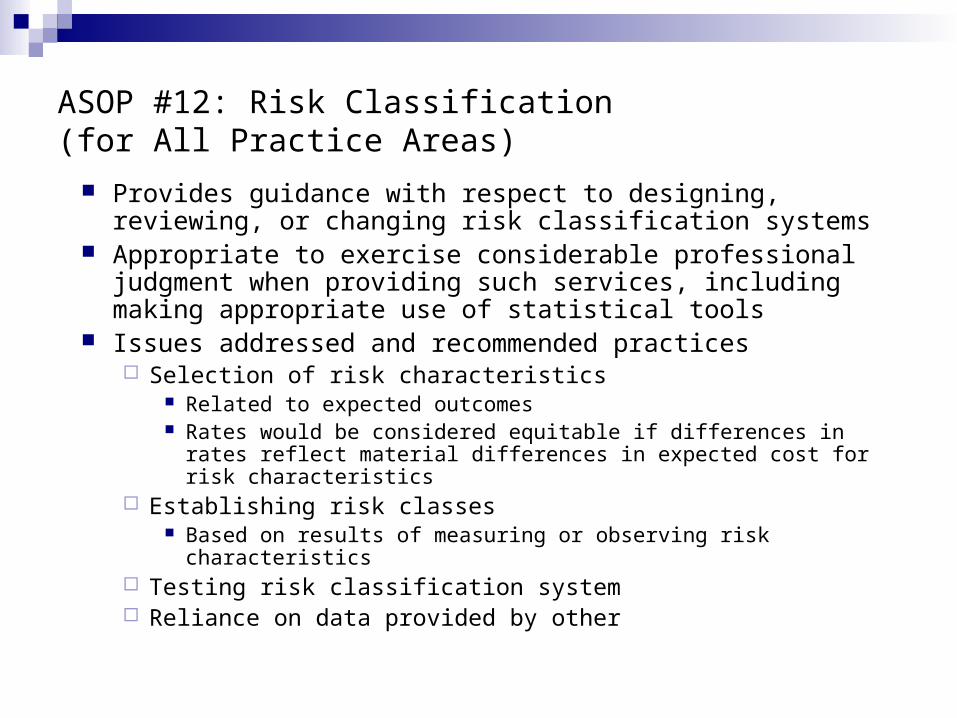

ASOP #12: Risk Classification(for All Practice Areas)

Provides guidance with respect to designing, reviewing, or changing risk classification systems

Appropriate to exercise considerable professional judgment when providing such services, including making appropriate use of statistical tools

Issues addressed and recommended practices Selection of risk characteristics

Related to expected outcomes Rates would be considered equitable if differences in rates

reflect material differences in expected cost for risk characteristics

Establishing risk classes Based on results of measuring or observing risk characteristics

Testing risk classification system Reliance on data provided by other

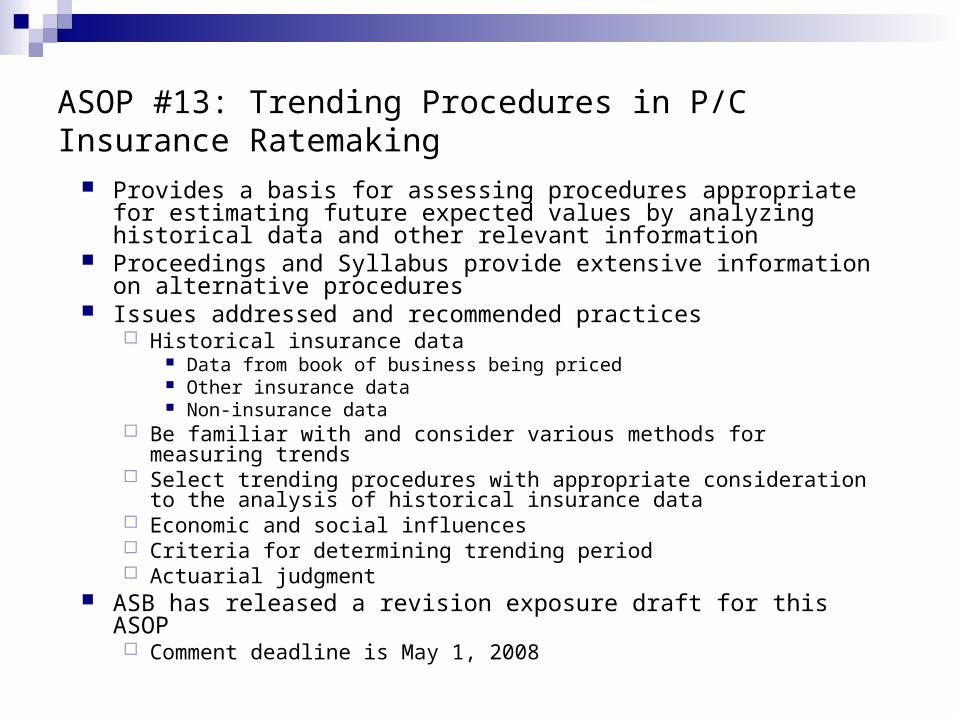

ASOP #13: Trending Procedures in P/C Insurance Ratemaking

Provides a basis for assessing procedures appropriate for estimating future expected values by analyzing historical data and other relevant information

Proceedings and Syllabus provide extensive information on alternative procedures

Issues addressed and recommended practices Historical insurance data

Data from book of business being priced Other insurance data Non-insurance data

Be familiar with and consider various methods for measuring trends Select trending procedures with appropriate consideration to the

analysis of historical insurance data Economic and social influences Criteria for determining trending period Actuarial judgment

ASB has released a revision exposure draft for this ASOP Comment deadline is May 1, 2008

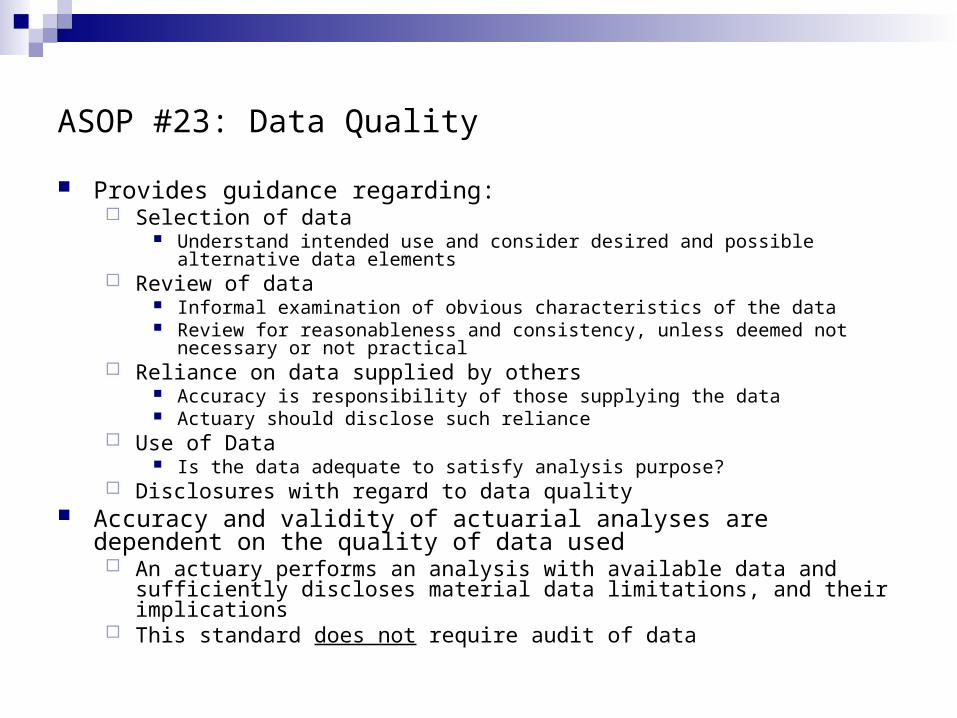

ASOP #23: Data Quality

Provides guidance regarding: Selection of data

Understand intended use and consider desired and possible alternative data elements Review of data

Informal examination of obvious characteristics of the data Review for reasonableness and consistency, unless deemed not necessary or not

practical Reliance on data supplied by others

Accuracy is responsibility of those supplying the data Actuary should disclose such reliance

Use of Data Is the data adequate to satisfy analysis purpose?

Disclosures with regard to data quality Accuracy and validity of actuarial analyses are dependent on the quality of

data used An actuary performs an analysis with available data and sufficiently discloses

material data limitations, and their implications This standard does not require audit of data

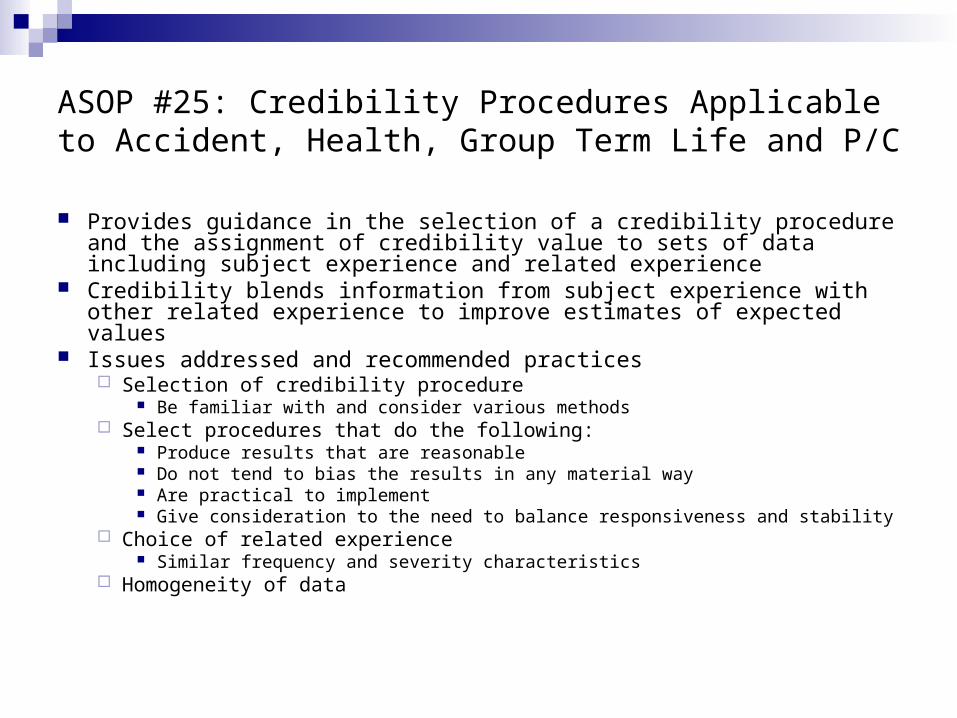

ASOP #25: Credibility Procedures Applicable to Accident, Health, Group Term Life and P/C

Provides guidance in the selection of a credibility procedure and the assignment of credibility value to sets of data including subject experience and related experience

Credibility blends information from subject experience with other related experience to improve estimates of expected values

Issues addressed and recommended practices Selection of credibility procedure

Be familiar with and consider various methods Select procedures that do the following:

Produce results that are reasonable Do not tend to bias the results in any material way Are practical to implement Give consideration to the need to balance responsiveness and stability

Choice of related experience Similar frequency and severity characteristics

Homogeneity of data

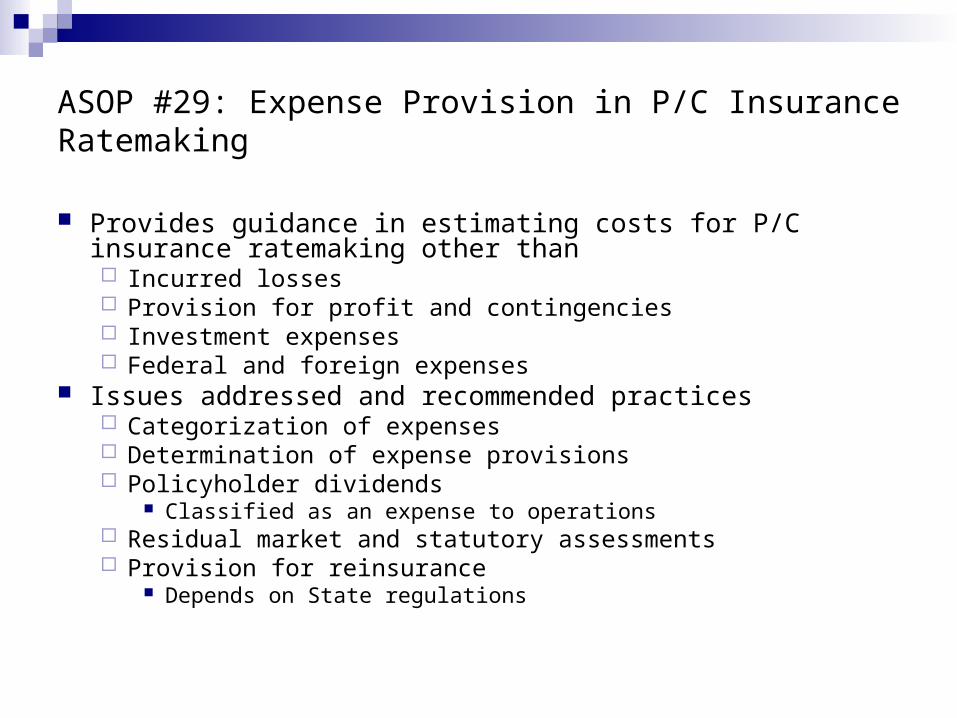

ASOP #29: Expense Provision in P/C Insurance Ratemaking

Provides guidance in estimating costs for P/C insurance ratemaking other than Incurred losses Provision for profit and contingencies Investment expenses Federal and foreign expenses

Issues addressed and recommended practices Categorization of expenses Determination of expense provisions Policyholder dividends

Classified as an expense to operations Residual market and statutory assessments Provision for reinsurance

Depends on State regulations

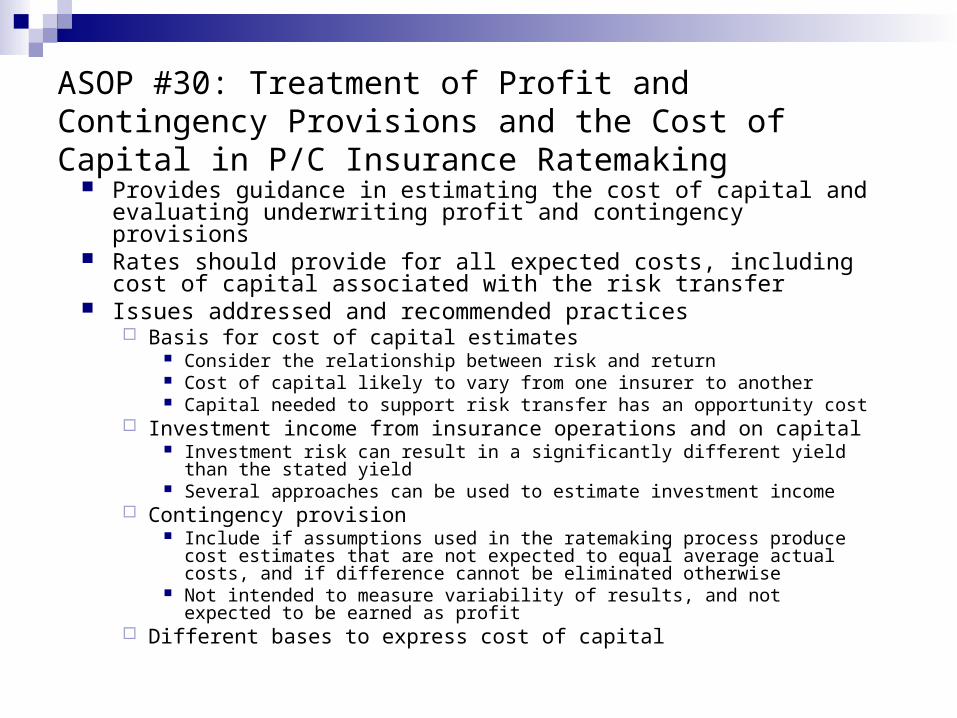

ASOP #30: Treatment of Profit and Contingency Provisions and the Cost of Capital in P/C Insurance Ratemaking

Provides guidance in estimating the cost of capital and evaluating underwriting profit and contingency provisions

Rates should provide for all expected costs, including cost of capital associated with the risk transfer

Issues addressed and recommended practices Basis for cost of capital estimates

Consider the relationship between risk and return Cost of capital likely to vary from one insurer to another Capital needed to support risk transfer has an opportunity cost

Investment income from insurance operations and on capital Investment risk can result in a significantly different yield than the

stated yield Several approaches can be used to estimate investment income

Contingency provision Include if assumptions used in the ratemaking process produce cost

estimates that are not expected to equal average actual costs, and if difference cannot be eliminated otherwise

Not intended to measure variability of results, and not expected to be earned as profit

Different bases to express cost of capital

ASOP #38: Using Models Outside of the Actuary’s Area of Expertise (P/C)

Provides guidance in using models that incorporate specialized knowledge outside the actuary’s own area of expertise when developing work product

Actuary’s level of effort in understanding and evaluating a model should be consistent with the intended use of the model and its materiality to the results of the actuarial analysis

Issues addressed and recommended practices Determine appropriate reliance on experts

May rely on experts if needed Basic understanding of models

Understand basic components, user input and output Evaluate whether the model is appropriate for intended application

Consider limitations, modifications and assumptions needed Determine that appropriate validation has occurred

User input: Review ASOP #23 “Data Quality” User output: Compare with alternate models, historical results and

review sensitivity Determine the appropriate use of the model

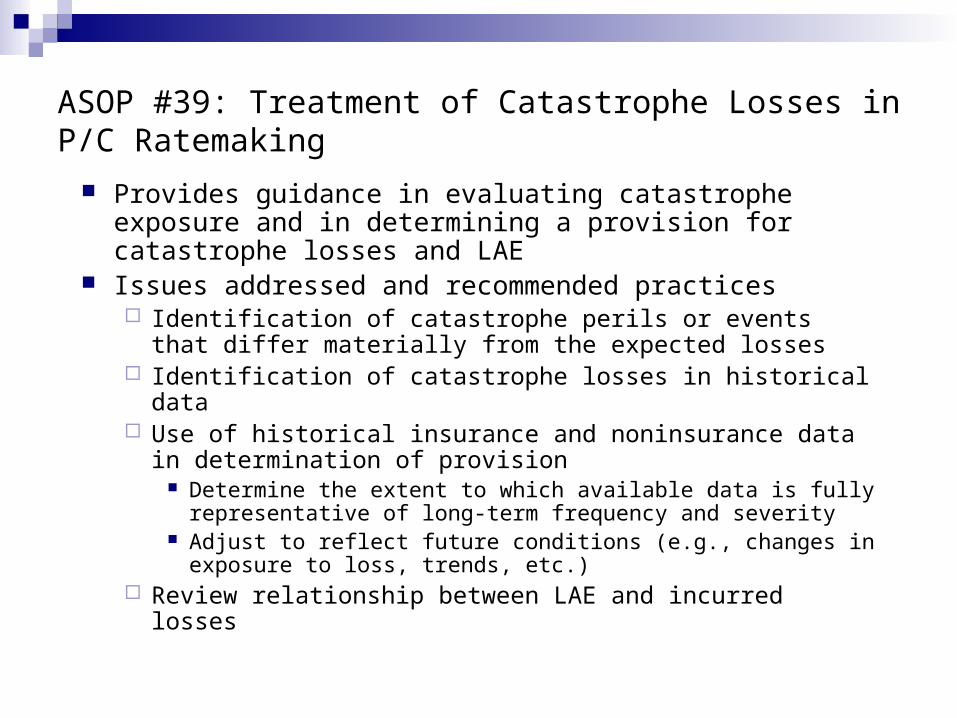

ASOP #39: Treatment of Catastrophe Losses in P/C Ratemaking

Provides guidance in evaluating catastrophe exposure and in determining a provision for catastrophe losses and LAE

Issues addressed and recommended practices Identification of catastrophe perils or events that differ

materially from the expected losses Identification of catastrophe losses in historical data Use of historical insurance and noninsurance data in

determination of provision Determine the extent to which available data is fully

representative of long-term frequency and severity Adjust to reflect future conditions (e.g., changes in exposure to

loss, trends, etc.) Review relationship between LAE and incurred losses

ASOP #41: Actuarial Communications(for All Practice Areas) Provides guidance for written, electronic or oral actuarial communications Applies to all actuarial communications, with some exceptions (e.g. testimony),

between an actuary and a principal Guidance applies to the extent practicable in the particular circumstances

Issues addressed and recommended practices General Requirements (as appropriate)

Identify Principal, clearly state scope and any limitations or constraints Form and content clear and appropriate to audience ASOP #41 establishes minimum requirements, other ASOPs may supersede

Requirements for Specific Communication Types Significant findings should be in writing or electronic form

Compliance with Other Standards Compliance with law, regulation, or another profession's standards may be

sufficient to deem compliance with this standard Responsibility to Other Users

Take reasonable steps to ensure the communication is clear and presented fairly

No obligation to communicate with any person other than the intended audience

Revisions currently considered by the ASB

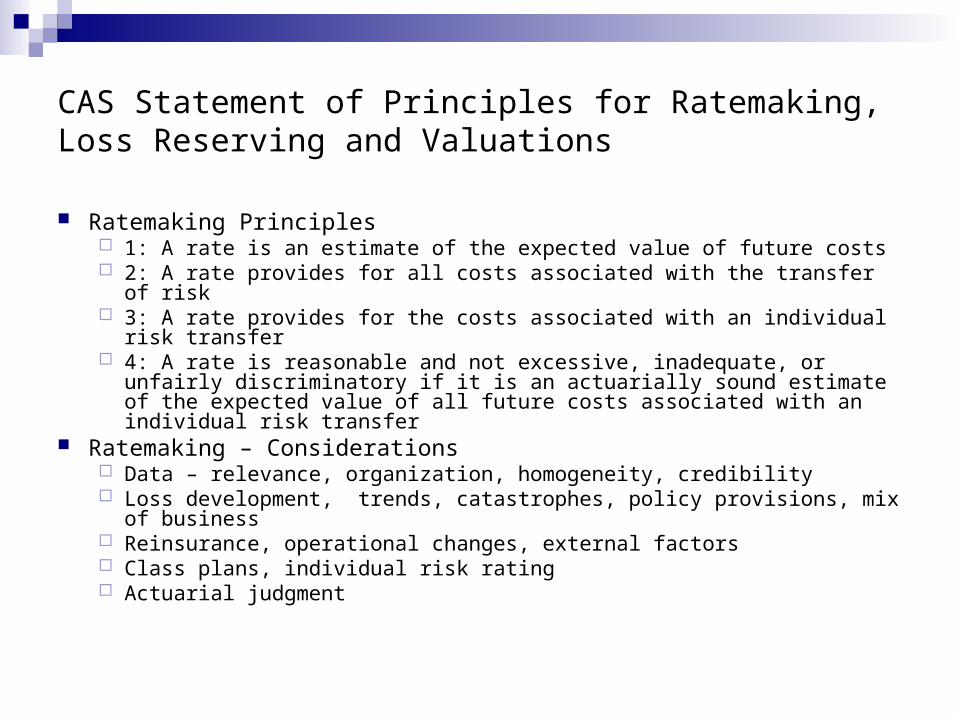

CAS Statement of Principles for Ratemaking, Loss Reserving and Valuations

Ratemaking Principles 1: A rate is an estimate of the expected value of future costs 2: A rate provides for all costs associated with the transfer of risk 3: A rate provides for the costs associated with an individual risk

transfer 4: A rate is reasonable and not excessive, inadequate, or unfairly

discriminatory if it is an actuarially sound estimate of the expected value of all future costs associated with an individual risk transfer

Ratemaking – Considerations Data – relevance, organization, homogeneity, credibility Loss development, trends, catastrophes, policy provisions, mix of

business Reinsurance, operational changes, external factors Class plans, individual risk rating Actuarial judgment

Case Studies

Assume that you filed a rate change of +10% and it is sitting in the Department of Insurance for quite a while (Prior Approval state/province). A new analyst decides to run a more current indication which utilizes two additional quarters of data that is not included in the 10% change waiting for approval. Thisnew indication shows a -2.0% need. The new analyst shares this information with you and you have seen the answer.

What do you do?

Case Study #1

Suppose your marketing department is really pushing a new business discount in order to get a boost in growth. You have no actuarial support for the discount because you do notcollect data on it. The competition does not have this discount either. As an actuary, would you file a discount that has no known support?

What would you do?

Case Study #2

You are an ACAS in the ratemaking department of ABCinsurance company. Your boss, an FCAS, asks you to puttogether a homeowners rate filing that he intends to sign.Your analysis results in a rate increase indication of 2.0%.Your boss reviews your work and says that managementwants a 5.0% increase and asks you to make some changesto some assumptions that will get the desired rate increase.You think these changes are somewhat arbitrary and thatthey result in a rate indication that is at, if not above, the veryhigh end of a reasonable range. Your boss is the only actuarysigning the rate filing report.

What do you do?

Case Study #3

You are doing the final review of a personal auto rate filing when you discover an error that not only was made in this filing, but also the prior filing which was approved by the Insurance Department and implemented.

Your prior indication was 17%, and you implemented the entire indication. Had this error been found the corrected indication would have been 4.5%.

What would you do?

Case Study #4

You are the actuary for a reinsurance company trying to set anexcess auto reinsurance rate for a small domestic companythat does not have credible data. You also reinsure a largercompany, which writes basically the same business in thesame state, and who has supplied you with ample data thatcould be used to set the rates for the smaller company.

Do you use the data, as a collateral source, to develop rates forthe smaller company?

Case Study #5