CMI Limited Annual Report 2007 - … adding to the already well established Brisbane office. ......

88

CMI Limited Annual Report 2007 CMI LIMITED ANNUAL REPORT 2007

Transcript of CMI Limited Annual Report 2007 - … adding to the already well established Brisbane office. ......

CMI Limited Annual Report 2007

CM

I LIM

Ite

d A

nn

uA

L R

epo

Rt

2007

CMI LIMITED ANNUAL REPORT 2007

ContentS2007 Highlights 2

Chairman’s Review 3

Group Business overview 4

2007 operational Review 5

directors & Senior Management 7

CMI Locations 9

Financial Report 11

Shareholder Information 80

Corporate directory 83

the Annual General Meeting of CMI Limited will be held at the Brisbane Riverview Hotel, Clayfield Albion Room, cnr Kingsford-Smith drive and Hunt Street, Hamilton on Monday, 12 november 2007 at 10.00 am. the business of the meeting is outlined in the formal notice and proxy Form that is enclosed with this report.

FINANCIAL CALENDAR

Financial year end 30 June 2007ASX announcement of results and dividend 31 August 2007Annual General Meeting 12 november 2007

ANNUAL GENERAL MEETING

CMI LIMITED ANNUAL REPORT 2007 �

CMI Limited is a diversified company which operates through three major business streams:

• Engineered and 4WD Components – manufacture and distribution of metal-based products for a diverse range of industry sectors including automotive, 4WD accessories, heavy transport, water fittings, white goods, energy, rural and housing.

• Electrical Components – manufacture and distribution of specialty cables, high voltage cables, flexible cables, plugs and couplers for the mining, communication, film, sound and lighting industries.

• Financial Services – consumer and commercial finance through the finance brokerage company, Capitalcorp Finance & Leasing Pty Ltd (“Capitalcorp”), which operates from 40 branches nationally.

The company’s operations, which are based throughout Australia, New Zealand and the United States of America, generated revenue of $265.4 million.

With its head office in Brisbane, CMI employs approximately 1,058 people as at 30 June 2007.

CMI

CMI LIMITED ANNUAL REPORT 20072

2007 Highlights

Financial Overview

• Revenue decreased by 4.8% to $265.4 million.

• Operating profit after tax decreased prior to impairment write down by 16.3% to $13.4 million.

• Significant growth in our Electrical business with sales increasing by 55.1% to $49.3 million and profit before tax increasing by 66% to $15 million.

• Acquisition of the business of XLPE Cables on 11 July 2006 to add high voltage cables to our Electrical division’s product range.

• Acquisition of the business of 4WD Warehouse on 1 June 2007 consisting of retail outlets at Kings Park, Penrith and Orange and 4WD Megastores advertising and purchasing group.

Operational Overview

• The Engineering division has been affected by the trend away from locally manufactured six cylinder cars in favour of smaller imported cars. The market statistics for the seven months to July 2007 indicate that 80% of new car sales are imported cars.

• The production volumes of the Original Equipment manufacturers supplied by CMI decreased during the year which has impacted on volumes at the Engineering Division’s Campbellfield and Kensington plants.

• Engineering Division’s margins were subject to cost pressures increasing raw material prices, the strong Australian dollar and low cost overseas component suppliers.

• The Electrical Division significantly increased revenue and profit through an expanded product range and distribution base. The division has been successful in increasing the sales of the Minto mining products and Aflex Cables range whilst integrating the XLPE high voltage cable range into the distribution network.

• TJM recorded revenue and profit before tax in line with the prior year. The SUV market has remained buoyant with the increase in sales on 4WD utilities compensating for any decrease in sales of other large 4WD’s. On 1 June 2007 TJM purchased the business of 4WD Warehouse Pty Ltd consisting of three retail stores and the 4WD Megastores advertising and purchasing group.

• Capitalcorp’s Business Finance capability was strengthened with particular emphasis on the Sydney and Melbourne markets adding to the already well established Brisbane office.

• Capitalcorp has opened eight new points of representation during the past 12 months.

• CMI Springs New Zealand has continued to trade in line with forecasts despite increased competition within the local market from Chinese suppliers. The business of Curtis Springs acquired in May 2006 was fully integrated into the existing operations during the year increasing the customer base and product range.

Financial Summary 2003 2004 2005 2006 2007 % $’000 $’000 $’000 $’000 $’000 Change

Group Revenue �96,045 275,604 284,040 278,704 265,397 (5)

Earnings before Depreciation, Interest & Tax �9,655 26,976 28,80� 27,750 6,540 (76)Depreciation & Amortisation (5,678) (7,285) (7,37�) (7,730) (7,379) (5)Earnings before Interest & Tax �3,977 �9,69� 2�,430 20,020 (839) (�04)Interest & Finance Charges (3,�97) (3,674) (3,705) (4,060) (4,397) 8Operating Profit (Loss) before Tax �0,780 �6,0�7 �7,725 �5,960 (5,236) (�33) Operating Profit (Loss) after Tax 7,229 �0,585 �2,�59 ��,�97 (3,840) (�34)

Earnings per Share

- Basic (Cents) �8.29 26.4� 22.89 23.45 (2�.6�) (�92)

Dividends

- Ordinary ($’000) 2,704 2,989 4,295 4,335 3,�83 (27)- Preference ($’000) 2,548 3,406 4,5�5 N/a N/a N/a- Class A ($’000) N/a N/a N/a 2,738 3,786 38

Dividends per Share

- Ordinary (Cents) �0.00 �2.00 �2.00 �2.00 9.00 (25)- Preference (Cents) * �2.50 �3.25 �4.00 3.50 N/a N/a- Class A (Cents) * N/a N/a N/a �0.50 �4.00 N/a

Shareholders Funds ($’000) 65,6�9 70,�77 84,296 87,985 79,5�5 (�0)Net Tangible Assets per Ordinary Share (Dollars) 0.90 0.44 �.45 �.57 �.39 (��)Number of Employees �,�46 �,3�� �,272 �,�26 �,058 (6)

* All issued Preference Shares were converted to Class A shares during the 2006 year.

CMI LIMITED ANNUAL REPORT 2007 3

Chairman’s Review

2007 has been a year of significant change for the company. Mr Max Hofmeister, the Chairman and CEO since the company was listed on the ASX in 1993, retired from all positions in the company during the year. Over that long term, he built the company from small beginnings to the company that it is today.

CMI today has three major business units: engineering, electrical and finance.

The engineering businesses have been the core of the company for the whole period of its existence and have been substantive suppliers of components to the car manufacturers and to the after-market. The Australian car manufacturing industry has changed greatly in the last few years and continues to change with the challenge of lower cost imports competing with the local engineering businesses. Those cost challenges have caused a significant reduction in the profitability of the CMI engineering businesses and the Board does not believe that any of those challenges will diminish in the next year.

The electrical businesses have continued to grow and to increase profitability. Much of the electrical sales are into the resources sector and the Board expects those markets to continue to grow over the next year.

The finance business has been impacted by increased competition in its market. The business has significant volumes and has an extensive distribution network of branches. The Board expects that trading conditions will continue to be difficult in this year.

Following the retirement of the former CEO, Mr Ray Catelan was appointed Managing Director. He has substantial experience in operating successful trading businesses and he is working with other management and the Board to finalise and implement the future strategy for the company.

I acknowledge the retirement of former directors Mr Maurie Maughan and long serving Mr John Johnson during the year.

Colin Ryan

Chairman

CMI LIMITED ANNUAL REPORT 20074

Group Business Overview

Engineered Components & 4WD Components Electrical Components USA Operations Financial Services

BUSINESS ACTIVITY

• Manufacture of precision engineered components for end manufacturers

• Manufacture and marketing of accessories for 4WD and light commercial vehicles

• Manufacture and distribution of specialist cabling and electrical products

• Distribution of CMI manufactured heavy transport, brake and 4WD components

• Consumer and commercial brokerage

BUSINESS NAMES

• CMI Operations

• CMI Forge

• CMI Water

• CMI Springs

• Curtis Springs

• Toowoomba Metal Technologies

• Toowoomba Engine Products

• TJM

• 4WD Megastores

• 4WD Warehouse

• CMI Electrical Products

• Hartland Cables

• Minto Industrial Products

• Aflex Cables

• XLPE Cables

• CMI Operations

• TJM USA

• Capitalcorp Financial Services

• Capitalcorp Finance & Leasing

PRODUCTS • Seat belt, suspension and brake components, inlet and exhaust manifolds and axle components

• Passenger airbag components, light truck mirror assemblies, drive train components and high performance disc brakes

• Truck, trailer and bus brake drums, wheel assemblies

• Water reticulation fittings, centrifugal pumps, water tanks

• Cylinder Heads

• Turbine Blades

• Vehicle Frontal Protection Systems (VFPS), canopies, side/rear protection bars, roof racks, water tanks, winches, suspension, rear bars, snorkels and other specialist accessories

• Power and communication cables/assemblies, computer cabling, mining plugs and high voltage couplers

• Brake components and select range of 4WD components

• Truck and trailer brake drums, hubs and wheel assemblies

• Personal loans – car loans, boat loans, unsecured personal loans

• Commercial finance – leases, hire purchases, operating and rental finance, novated leases and business loans.

• Home loans

• Insurance – motor vehicle insurance, personal loan protection insurance, gap cover insurance

INDUSTRY SECTORS

SUPPLIED

• Car & Component Manufacturing, Whitegoods, Energy, Agricultural, Heavy Transport, Water Supply, Building and Construction

• 4WD Accessory, Retailers & Distributors, Car Manufacturing

• Mining, Communications, Sound & Lighting and Power

• 4WD Accessory, Retailers and Distributors,

• Car and Component Manufacturing

• Consumers and Small, Medium Entities (SMEs)

MAJOR CUSTOMERS

• Holden, Ford, General Motors Brazil, Autoliv, Bosch Australia, PBR, Drivetrain Sustems International, Bendix Mintex, Cooper Standard, Dana, Unidrive, Schefenacker, BIC, Fisher and Paykel, Gallagher Group, Arvin Meritor, Transpec BPW, Tyco

• 4WD Specialist Distributors for after-market products

• Original Equipment market – Nissan, Mazda and Ford

• Specialist electrical distributors and OEM’s

• 4WD Specialist Distributors for after-market products

• Direct – PBR (Pacifica Limited subsidiary)

• Indirect – Ford, General Motors

Major Finance Providers

• GE Automotive Financial Services, Esanda, Westpac, ANZ, NAB and St George

OPERATING LOCATIONS

• Ballarat, Horsham, Campbellfield, Kensington, Footscray, Toowoomba, Auckland, Christchurch

• Brisbane and distribution in all capital cities and major provincial areas

• Sydney, Melbourne, Brisbane, Rockhampton, Perth

• Knoxville, Tennessee, Columbia, South Carolina

40 branches throughout Australia

CMI LIMITED ANNUAL REPORT 2007 5

2007 Operational ReviewENGINEERED AND 4WD COMPONENTS

The year under review was adversely affected by decreased sales of Australian manufactured 6 cylinder vehicles and a decline in large 4WD sales. The difficult trading conditions, which included increased raw material costs, large increases to petrol prices, reduced demand in the North American market and an increasingly competitive market, resulted in a 12.7% decline in sales revenue.

CMI Campbellfield

Despite the commencement of the supply of components for the mirror assembly of light trucks in North America and Australia, CMI’s Campbellfield manufacturing facility has endured a difficult year due to the decrease in the number of vehicles produced locally by a major customer, Ford. The ongoing demand for locally built 6 cylinder Ford vehicles over the next twelve months remains unknown.

CMI Kensington

CMI’s Kensington manufacturing plant returned a reduced contribution to the prior year whilst exceeding its budget. The reduction in the performance from the prior year related to a decrease in the demand for machined components for General Motor’s Family Two engines that are exported to Korea, China and Brazil and the impact of Ford’s reduced build rate on the components associated with the work won from the ION plant in New Zealand.

CMI Forge

This business, continued to perform below budgeted and prior year levels due to the reduced demand for locally produced cars, particularly for large 6 cylinder cars and the turbine blade business for GE generating below forecast sales. The business has also been impacted by increasing raw material costs and the strong Australian dollar.

CMI Forge has consolidated the majority of the operations from the two sites to one site during the year. The integration of the two sites is expected to be completed in the first half of 2007/2008.

The business has also incurred significant redundancy costs during the year associated with the reduced sales levels and the integration of the two sites.

As a fully accredited supplier to GE, CMI Forge is well positioned to meet any additional orders from GE to supply turbine blades for land-based wind generators in the USA. This business is now an integral part of its core operations.

Toowoomba Metal Technologies (TMT)

TMT sales volumes were in line with budget for the year. The profitability of the business suffered from the effect of scrap metal price increases and an increase in the Australian dollar against the US dollar.

The supply of heavy transport product to North America slowed during the second half of the year due to the increase in the Australian dollar against the US dollar and a major customer Dana entering into Chapter 11 in North America.

TMT has maintained its supply of after market cylinder heads through a USA based distributor despite the increase in the exchange rate.

Demand for TMT’s heavy transport products continues to remain strong.

CMI Horsham

CMI Horsham performed in line with budget in 2006/2007 despite higher scrap metal prices and a decrease in the Ford build rates. The primary driver behind the business’ performance was the continued supply of automotive components supplied to CMI Kensington and solid general engineering demand.

CMI New Zealand

CMI New Zealand has continued to consistently perform at close to budgeted levels despite ongoing pressure from overseas competition particularly from China.

The 2006/2007 result was an improvement on the prior year due to the impact of a favourable exchange rate movement as well as being the first full year of the incorporation of the business of Curtis Springs acquired on 1 May 2006. The business is expected to continue to face pressure from overseas competition in 2007/2008.

CMI USA

The first half of the year was impacted by reduced vehicle production volumes in North America by General Motors as a result of model run outs and increased fuel prices.

Demand from General Motors for the brake components we supply via our contract with Pacifica’s USA subsidiary PBR, increased during the second half with the introduction of the GMT 900 platform, although sales gained were at decreased margins.

Sales of TJM’s 4WD accessories in the USA were affected by a decrease in large vehicle sales due to increased fuel prices. The coming year will see the introduction of sales of TJM’s air operated differential locker into USA markets with the first two models scheduled for release in the first half of the year. Whilst this product will take some time to establish within the USA market we are confident that sales will grow following the model range’s progressive expansion.

CMI Ballarat

The Ballarat plant supplies brake components for export to the USA, and as such was affected by the decrease in volumes in the first half of the year associated with the runout of the GMT 800 platform and the reduced margins encountered in the second half following the introduction of the GMT 900 platform.

CMI Water

CMI Water was established during the year. The division manufactures polyethylene water tanks at its factory in Bundaberg, Queensland. The division whilst profitable in its first year of operation did not contribute significantly to the results of the company.

CMI LIMITED ANNUAL REPORT 20076

TJM

TJM sales performance was in line with our expectations with sales down 3% and profit up by 6% compared to the prior year. The increase in the profitability is a direct result of a focus on the costs within the business and the fact TJM has continued to increase its sourcing of products from overseas to supplement local production in order to control overall costs.

During the year TJM purchased the businesses of 4WD Megastores and 4WD Warehouse consisting of retail outlets at Kings Park NSW, Penrith NSW and Orange NSW and an advertising and marketing business.

TJM focus will continue on the control of costs and on new product development and the expansion of its existing product range.

We remain confident that TJM will continue to maintain current levels of orders. To ensure the business remains competitive we will continue out-sourcing production of some selected TJM designed and tooled components offshore. This initiative is to enable us to cost-effectively extend the range of TJM accessories which can be offered to the market both in Australia and overseas.

ELECTRICAL COMPONENTS

CMI Electrical

The CMI Electrical business has performed above our expectations, with sales revenue up 55.1% to $49.3 million and profit before tax increasing by 66% to $15 million. The year included the results of NSW based cabling business, XLPE Cables for the first time (purchased in July 2006).

Headed by Jeff Heslington, this division now employs around 83 staff based in offices at Sydney, Melbourne, Brisbane, Rockhampton and Perth. The operational structure has been built around the acquisition and successful integration of several separate businesses including Minto Industrial Products, Hartland Cables, Aflex Cables and XLPE Cables.

The division has continued to focus on consolidating the product range around a core of proven locally manufactured lines supplemented by a an increase in number of imported products. Major product lines now sold throughout Australia, and in selected areas overseas, comprise power and communication cables/assemblies, computer cabling, plugs and high voltage couplers.

The division’s operations are structured around the following five business units:

• Aflex Cables;

• Cable Assemblies;

• Hartland Cables;

• Minto Industrial Products; and

• XLPE Cables.

Each of the five Electrical Components business units focuses on one or two industry sectors and the cumulative reach of the division’s product range now extends across mining, industrial, electrical appliance, niche data, flexible cabling and high voltage cabling.

With the global resources sector continuing to grow during the year ended 30 June 2007 and the Australian coal mining sector remaining buoyant, the division has achieved further sales growth from its mining products. Growth is predicted to

continue from the division’s mining products, flexible and medium to high voltage cabling operations.

FINANCIAL SERVICES

Capitalcorp

The past year has seen a further expansion of the Branch distribution network taking to 40 our points of representation. Our Business Finance capability was strengthened with particular emphasis on the Sydney and Melbourne markets adding to the already well established Brisbane office. Capitalcorp has opened eight new points of representation during the past 12 months.

• Silverwater, Sydney

• Homebush, Sydney

• Caloundra

• Coffs Harbour

• Lismore

• Geelong West

• Sydney and Melbourne Business Finance

Capitalcorp now boasts 40 Points of representation offering the full suite of Consumer, Business Finance and Home loan products.

We have improved our capability of financing vehicles on line with the introduction of Autocapital, a web based used car search and online application facility linked to Capitalcorp accredited dealers.

The result for the Financial Services Division was affected by issues that adversely impacted the core business, which is providing finance for used motor vehicles.

Down Turn in Used Motor Sales

Many consumers are continuing to prefer the purchase of new rather than used motor vehicle due to the strong A$ and particularly the availability of new, cheaper, smaller, fuel efficient imported motor vehicles. This has affected used car sales across the board, but particularly from used motor dealers where a significant portion of the Capitalcorp core consumer finance and insurance business emanates.

Costs Incurred In Restructure

Substantial costs have been incurred with the restructuring of the delivery channels in our two largest markets; Sydney and Melbourne. We have moved our distribution model from predominantly a single independent contractor to mainly corporate controlled branches. This will produce improved profits in the medium term, and also reduce reliance on singular independent operators.

Margin and Interest Rate Pressure

As the used car market contracted during the past two years interest margins have reduced and and competition has increased with introducers and referrers of new business now demanding a larger percentage of available commissions.

The ensuing 12 months will focus on strongly growing our direct Sydney and Melbourne presence. Further, we will build on the now established commercial lending opportunities and the Autocapital online initiative.

2007 Operational Review

CMI LIMITED ANNUAL REPORT 2007 7

Directors and Senior Management

Colin Ryan AM

Chairman

Colin Ryan joined the board on 28 February 2007 as the non-executive chairman and independent director. Colin is currently: Chairman of the Brisbane Airport Corporation Ltd, Chairman of Capital + Merchant Finance Ltd (New Zealand), Chairman of Cymbis Finance Australia Ltd, Director of Softlink International Ltd and Chairman of the Royal Children’s Hospital Foundation.

Colin is the former Queensland managing partner of Arthur Andersen and former Deputy Chairman of the Port of Brisbane. He holds bachelor degrees in Commerce and Law, is a Fellow of the Institute of Chartered Accountants and a Fellow of the Australian Institute of Company Directors.

Raymond Catelan

Managing Director

Ray Catelan joined the board as a director on 18 May 2007 and as managing director on 3 July 2007. Ray has extensive commercial and management experience both in public and private company environments including more than 12 years in the IT industry. Ray founded RP Data in 1991 and was the managing director. RP Data was first listed on the Australian Stock Exchange in May 2000.

Ray is also a non-executive director of Bigair Group Limited.

Danny Herceg

Non-Executive Director

Danny Herceg joined the board on 9 March 2007 as an independent director. Danny is a senior corporate and commercial lawyer with a specialisation in capital raisings, mergers and acquisitions, privatisations, restructurings and venture capital. Danny commenced practise in 1990 after completing degrees in science and law. He was a capital raisings partner of Gilbert + Tobin before establishing Herceg Lawyers in 2002. In addition to Danny’s capital raisings expertise, Danny advises on various commercial and corporate law issues, including prospectus issues, corporate governance and employee share and option plans, as well as joint ventures and non-equity funding.

Danny is also the Chairman and a non-executive director of Bigair Group Limited.

Mark Laidlaw

Chief Financial Officer and Company Secretary

Mark Laidlaw joined CMI in 1997. He is a former audit manager of international accountancy firm, Deloitte Touche Tohmatsu. Mark worked for Deloitte in both Australia and the USA and was responsible for the CMI audit from 1991 to 1997. He is a member of the Institute of Chartered Accountants in Australia. He holds a Bachelor of Commerce (Honours) from the University of Queensland.

Dan Gallagher

Executive General Manager – Engineering

Dan Gallagher is responsible for the management of the company’s Engineered Components manufacturing operations in Australia and New Zealand. He has extensive experience in the automotive manufacturing sector, having held positions with Ford and Autoliv before joining CMI in 1993.

Dan has played a key part in maximising the company’s production efficiencies, and has been responsible for the restructure and implementation of lean manufacturing through many of CMI’s manufacturing facilities.

He is a member of the Australian Industry Group and the Federation of Automotive Products Manufacturers.

Ian Whittle

Managing Director – Financial Services

Ian Whittle was appointed Managing Director of Capitalcorp by CMI in November 2003. Ian has over 29 years experience in the financial services industry, including 8 years as a member of the Bank of Queensland’s Senior Executive Team. Prior to joining Capitalcorp he was the Bank of Queensland’s General Manager, Business Acquisition, with a focus on acquiring new commercial and high net worth individual customers.

CMI LIMITED ANNUAL REPORT 20078

Vince Misztowt

Vice President – USA Division

Vince Misztowt has managed CMI’s USA Division which is based in Knoxville, Tennessee, since its establishment in 1997. Besides managing the distribution of CMI’s products to PBR’s Tennessee and South Carolina brake manufacturing operations, Vince also has responsibility for distributing the company’s 4WD accessories in the USA market.

Jeff Heslington

General Manager – Electrical Components Division

Jeff Heslington joined CMI’s Hartland Cables business in 1999. Since then he has focused on strengthening the Electrical Components Division’s product range, including new design development.

Jeff, who is based in Sydney, was appointed General Manager of the Electrical Components Division in 2002. He has over 20 years experience in the electrical industry having worked for a range of companies including MM Cables where he was heavily involved in exports and government contracts.

Neil Saxon

Division Manager – TJM

Neil joined TJM in 2007. Neil has extensive experience in manufacturing and over seven years in the 4WD industry having previously held a senior position within ARB as their manufacturing manager overseeing their Australian and Thailand plants.

Neil is a mechanical engineer who has a focus on cost control, productivity improvements and product sourcing.

Geoff Fussell

Corporate Finance Manager

Geoff Fussell joined CMI in February 2003. He is a former client director of an international Chartered Accounting Firm – Assurance and Advisory division. He has also worked as a Senior Manager in the Corporate Finance division of Deloitte Touche Tohmatsu in the United Kingdom.

He is a member of the Institute of Chartered Accountants in Australia and holds a Bachelor of Commerce from the University of Queensland.

Allan Thomson

Manager – Tax and Treasury

Allan Thomson joined CMI in 2000. He is a former tax manager of Deloitte Touche Tohmatsu.

Allan is a member of the Institute of Chartered Accountants in Australia and the Taxation Institute of Australia and holds a Bachelor of Commerce and Bachelor of Law from the University of Queensland.

Ian Shelton

Information Systems Manager

Ian Shelton joined CMI in May 2000. Ian’s previous experience includes 10 years in the audit section of Deloitte Touche Tohmatsu, 15 years in senior financial and administration positions in both public and private companies and prior to joining CMI, he was responsible for ERP system implementations with Pronto Software.

Directors and Senior Management

CMI LIMITED ANNUAL REPORT 2007 9

Engineered and 4WD Components

Ballarat903 Latrobe StreetBallarat VIC 3350Telephone: 03 5335 8121Facsimile: 03 5335 5446Email: [email protected]

Melbourne (Campbellfield)76-106 National BoulevardCampbellfield VIC 3061Telephone: 03 9358 8300Facsimile: 03 9358 8350Email: [email protected]

Melbourne (Kensington)133 – 165 Kensington RoadKensington VIC 3031Telephone: 03 9687 6801Facsimile: 03 9689 9627Email: [email protected]

Melbourne (West Footscray)465 Somerville RoadWest Footscray VIC 3012Telephone: 03 8325 5200Facsimile: 03 8325 5299Email: [email protected]

HorshamPalm AvenueHorsham VIC 3400Telephone: 03 5382 0094Facsimile: 03 5382 0938Email: [email protected]

Toowoomba259 Ruthven StreetToowoomba QLD 4350Telephone: 07 4690 2200Facsimile: 07 4638 3559Email: [email protected]

Bundaberg (CMI Water)5 Charlie Triggs CrescentBundaberg QLD 4670Telephone: 07 4151 6822Facsimilie: 07 4151 8827

Brisbane (4WD Components)150 Robinson RoadGeebung QLD 4034Telephone: 07 3865 9999Facsimile: 07 3865 3677Email: [email protected]

Auckland 7A Carmont PlaceMt Wellington, Auckland NZTelephone: + 649 579 4089Facsimile: + 649 579 2595Email: [email protected]

Christchurch 25 Lunns RoadChristchurch NZTelephone: + 643 343 4460Facsimile: + 643 343 4469Email: [email protected]

US Operations

Knoxville, Tennessee2510 Quality LaneKnoxville, Tennessee 37931 USATelephone: +1 865 670 1556Facsimile: +1 865 670 1993Email: [email protected]

Columbia, South Carolina1025 Technology DriveWest Columbia, SC 29170 USATelephone: +1 803 822 0655Facsimile: +1 803 822 0654

Email: [email protected]

Electrical Components

Sydney18 - 20 Railway RoadMeadowbank NSW 2114Telephone: 02 9807 6155Facsimile: 02 9808 2033

XLPE Cables87 Malta StreetFairfield NSW 2165Telephone: 02 9723 2300Facsimile: 02 9723 2322

Melbourne (Aflex Cables)3-5 Dissik StCheltenham Vic 3192Telephone: 03 9532 1233Facsimile: 03 9553 3502

Brisbane150 Robinson RoadGeebung QLD 4034Telephone: 07 3865 4745Facsimile: 07 3865 7494

RockhamptonUnit 2/253 Bolsover StreetRockhampton QLD 4700Telephone: 07 4921 0978Facsimile: 07 4921 0981

Perth5 Runyon RoadMidvale WA 6056Telephone: 08 9250 5933Facsimile: 08 9250 5722

CMI Locations

CMI LIMITED ANNUAL REPORT 2007�0

Financial Services

Brisbane (Head Office)Garden City Office Park, Building 52404 Logan RoadUpper Mt Gravatt Qld 4122Telephone: 07 3112 2222Facsimile: 07 3112 2229Email: [email protected]

Points of Representation

40 throughout Australia as at right.

(details available

www.capitalcorp.com.au)

QLD

Bundaberg

Brisbane

Cairns

Chermside

Gold Coast

Home Loans

Ipswich

Mt Gravatt

Mackay

Rockhampton

Sunshine Coast

Toowoomba

Townsville

Underwood

NSW

Sydney - Business Finance

Albury

Capital Coast

Coffs Harbour

Homebush

Lismore

Newcastle

Orange

Penrith

Wollongong

NT

Darwin

VIC

Ballarat

Bendigo

Geelong West

Geelong South

Melbourne - Commercial

Ringwood

Shepparton

ACTCanberra

SAAdelaideMt GambierPort Lincoln

TASBurnieLauncestonHobart

WAPerth

CMI Locations

CMI LIMITED ANNUAL REPORT 2007 ��

Corporate Governance Statement 12

Directors’ Report 15

Independence Declaration by Auditors 21

Independent Audit Report 22

Directors’ Declaration 24

Income Statement 25

Balance Sheet 26

Statement of Changes in Equity 27

Cash Flow Statement 29

Notes to the Financial Statements 30

Financial Report

CMI LIMITED ANNUAL REPORT 2007�2

The Board of Directors (“Board”) is responsible for the corporate governance practices of the Company. Following the release of the Principles of Good Corporate Governance and Best Practice Recommendations by the ASX Corporate Governance Council, the Board formalised a Corporate Governance Charter in 2004. The summary of the Corporate Governance Charter is available on the Company’s website (www.cmilimited.com.au).

The following statement sets out the main corporate governance practices adopted by the Board and discloses any instances of non-compliance with, and reasons for not adopting, the best practice recommendations of the ASX Corporate Governance Council.

Lay Solid Foundations for Management and Oversight

The Board is responsible for, and has the authority to determine, all matters relating to the running of the Company including the policies, practices, management, operations and objectives of the Company. It is the role of management to manage the Company in accordance with the directions of the Board. The functions reserved to the Board, and those delegated to management, are disclosed in the Corporate Governance Charter.

Structure the Board to Add Value

As at the date of this statement, the Board comprises three directors - one executive and two non-executives. Details of the directors, including their skills, expertise, length of service and independence, are set out in the Directors’ Report.

The Board acknowledges the ASX Corporate Governance Council recommendation that the board should consist of a majority of independent directors and as such the Board consists of a majority of independent non-executive directors.

The Company complies with the ASX Corporate Governance Council recommendation of having different people in the roles of Chairman and Managing Director. The Chairman is also an independent director.

The Board considers that two directors are independent. An independent director is one who is free from any interest and any business or other relationship which could, or could reasonably be perceived to materially interfere with the director’s ability to act with a view to the best interests of the company.

The non-executive directors were appointed during the year as indicated within the Directors’ Report.

With the prior approval of the Board, each director has the right to seek independent legal and other professional advice at the Company’s expense concerning any aspect of the Company’s operations or undertakings in order to fulfil his duties and responsibilities.

The Board established an Audit Committee in 1994 and a Remuneration Committee in 1998. Each has had a formal charter since that time. A summary of the charters is available on the Company’s website.

The Board performs the duties of the Nomination Committee. There is no established formal Nomination Committee. Due to the small number of directors it is unlikely that the company would obtain additional benefits from a formal committee structure.

Promote Ethical and Responsible Decision Making

It is part of the philosophy of the Company that it will at all times comply with the law and behave ethically.

The Company has a Code of Ethics to guide directors, the Managing Director, and other executives as to the practices necessary to maintain confidence in the Company’s integrity, and the responsibility and accountability of individuals for reporting and investigating reports of unethical practices.

The directors and employees must be aware of, and comply with the provisions of, the Corporations Act 2001 in relation to insider trading. The Company has Security Transaction Rules that set out the policy of the Company on dealing in shares and securities by directors and employees. These are formally acknowledged by all directors and relevant employees of the Company.

A summary of The Code of Ethics and the Security Transaction Rules are available on the Company’s website.

Safeguard Integrity in Financial Reporting

The Managing Director and Chief Financial Officer verify in writing to the Board and to the Auditors that the financial reports of the Company present a true and fair view, in all material respects, of the Company’s financial condition and operational results, and are drawn up in accordance with relevant Accounting Standards.

The Audit Committee consists of one executive director and two independent non-executive directors. The Chairman of the Audit Committee is a non-executive director. The Board acknowledges the ASX Corporate Governance Council recommendation that the Audit Committee should consist of at least three members, all of whom are non-executive directors. Consideration has been given as to how and when this can be achieved, however the Board is currently of the view that this would require the appointment of an additional director which would be an unnecessary cost to the Company and the shareholders.

The Committee’s responsibility is to independently verify and safeguard the integrity of the Company’s financial reporting and oversee the independence of the external auditors. Details of the names and qualifications of the members of the Audit Committee, and their attendance at meetings, are disclosed in the Directors’ Report.

A formal charter which outlines the audit committee’s role, responsibilities, composition, structure and membership requirements and a summary of its main provision has been published on the Company’s website.

Corporate Governance Statement

CMI LIMITED ANNUAL REPORT 2007 �3

Make Timely and Balanced Disclosures

The Board complies with the continuous disclosure obligations of the Australian Stock Exchange (“ASX”) and, in so doing, immediately notifies the market by disclosing any information in relation to the business of the Company that a reasonable person would expect to have a material effect on, or lead to a substantial movement in, the price or value of the Company’s shares. The Company Secretary is responsible for communications with the ASX including responsibility for ensuring compliance with the continuous disclosure requirements in the ASX Listing Rules and overseeing information released to the ASX and shareholders.

Respect the Rights of Shareholders

In addition to market disclosure, the Company has a policy to ensure shareholders are able to gain access to information about the Company.

The principal communication with shareholders is through the provision of the Annual Report and Financial Statements, through the interim reports and at the Annual General Meeting. Shareholders are encouraged to participate at general meetings. There is also the Company’s website, which includes major briefings and announcements, the Corporate Governance Charter, other policies and committee charters and terms of reference.

The Board of Directors requests that the Company’s external auditor attends all Annual General Meetings and be available to answer shareholders’ questions about the conduct of the audit and the preparation and content of the auditor’s report thereon.

Recognise and Manage Risk

The Board recognises that the management of risk is an integral part of the management process and adheres to the general principles of Standards Australia Risk Management Standard 4360:1999. The Managing Director and Chief Financial Officer advise the Board in writing that the integrity of financial systems is founded on a sound system of risk management and internal compliance and control, which adheres to the policies adopted by the Board, and that the Company’s risk management and internal compliance and control system is operating efficiently and effectively in all material respects.

Encourage Enhanced Performance

The Managing Director is a key member of the Board and the key employee of the Company. An Operating Report is provided monthly to each of the directors. The report keeps them informed of the Company’s activities and performance.

The Remuneration Committee undertakes a detailed evaluation of the Managing Director’s performance on an annual basis. This evaluation utilises both quantitative and qualitative measures, and is judged against approved plans.

In addition, the Remuneration Committee, in conjunction with the Managing Director, reviews in a similar manner the performance of the senior executives of the Company who report directly to the Managing Director.

The results of these evaluations are tabled to the Board as part of the Remuneration Committee’s report. At this meeting, the Board and Managing Director discuss and agree goals (both quantitative and qualitative) for the coming year.

Remunerate Fairly and Responsibly

In accordance with its charter, the Remuneration Committee supports and advises the Board on appropriate remuneration policies, designed to meet the needs of the Company and enhance corporate and individual performance, as well as to attract and retain competent new talent.

It is responsible for reviewing and recommending salary package arrangements for the Managing Director, senior executives and directors, having regard to the performance of the Company and the individuals. Details of the names and qualifications of the members of the Remuneration Committee, and their attendance at meetings during the financial year, are disclosed in the Directors’ Report.

In recommending remuneration levels for the Managing Director, senior executives and directors, the committee considers several factors. The Company believes that it is imperative that these levels are commensurate with current market trends in relevant businesses, so as to ensure that high calibre employees and directors are attracted to and retained by the Company.

Other than for directors, remuneration packages usually include bonus and option elements, thus providing maximum benefits to both the Company and its shareholders.

In accordance with the Company’s Constitution, the total remuneration payable to non-executive directors is not to exceed $390,000 per annum as approved by the shareholders at a general meeting.

The policy on bonuses for the Managing Director and senior executives takes into account both quantitative and qualitative measures and, while profit performance is a key factor, revenue, market share, production hours, customer satisfaction and achievement of strategic objectives are considered, as well as the individual’s performance. Payment is always at the discretion of the Board, which takes into account the Company’s overall financial and strategic performance.

The Company operates the CMI Employee Incentive Scheme, approved by the shareholders in accordance with the requirements of the ASX. The intention of the Scheme is to assist in the attraction and retention of employees and executives. The Board will determine in its absolute discretion the eligibility and the number of options to be offered, having regard to length of service, contribution, and potential contribution to the Company. Further detail is contained in the Directors’ Report and the Financial Statements.

Details of directors’ and senior executives’ remuneration are disclosed in the Directors’ Report.

Corporate Governance Statement

CMI LIMITED ANNUAL REPORT 2007�4

Recognise the Legitimate Interests of Stakeholders

The Company has developed a Code of Conduct to guide compliance with legal and other obligations of legitimate shareholders. This Code of Conduct is available on the Company’s website.

The directors are responsible for the corporate governance practices of the company. This statement sets out the main corporate governance practices that were in operation throughout the financial year, except where otherwise indicated.

Corporate Governance Statement

CMI LIMITED ANNUAL REPORT 2007 �5

The directors of CMI Limited submit herewith the annual financial report for the financial year ended 30 June 2007. In order to comply with the provisions of the Corporations Act 2001, the directors report as follows:

The name and particulars of the directors of the company during or since the end of the financial year are:

Name Particulars

Colin G. Ryan Chairman and Non-Executive Director – Appointed 28 February 2007

Mr Ryan, AM, BCom, LLB, FCA, FAICD, is a former Queensland managing partner of an international chartered accounting firm. He is currently Chairman of the Brisbane Airport Corporation Ltd, Chairman of the Royal Children’s Hospital Foundation, Chairman of Cymbis Finance Australia Ltd and Director of Softlink International Ltd. Mr Ryan was awarded the Order of Australia in 2004 for his services to the health industry and corporate governance.

During the financial year he attended 2 of the 2 directors’ meetings held since his appointment.

Danny Herceg Non-Executive Director – Appointed 9 March 2007

Mr Herceg is a senior corporate and commercial lawyer with a particular specialisation in capital raisings, mergers and acquisitions, privatisations, restructurings and venture capital.

During the financial year he attended 1 of the 2 directors’ meetings held since his appointment.

Raymond D. Catelan Managing Director – Appointed 3 July 2007; Director - Appointed 18 May 2007

Mr Catelan has had extensive commercial and management experience both in the public and private company environments, particularly in providing property and equipment information services.

During the financial year there were no directors’ meetings held subsequent to his appointment.

Maxwell J. Hofmeister Executive Director – Appointed 20 June 1991

Mr Hofmeister founded the company in 1991, following an extensive involvement with other successful rural products, engineering and manufacturing companies.

During the financial year he attended 11 of the 11 directors’ meetings held and 4 of the 4 audit committee meetings.

Maurice C. Maughan Non Executive Director – Appointed 27 October 2005

Mr Maughan, FCA, has had extensive experience as a former partner in an international chartered accounting firm.

During the financial year he attended 11 of the 11 directors’ meetings held and 4 of the 4 audit committee meetings.

John J.A. Johnson Non Executive Director – Appointed 25 February 1993

Mr Johnson has had extensive marketing and business development experience.

During the financial year he attended 8 of the 9 directors’ meetings held and 4 of the 4 audit committee meetings.

Warren V. Hill Non Executive Director – Appointed 22 September 2003

Mr Hill was appointed Chief Operating Officer of CMI Limited in November 2002 and was responsible for the company’s Australian and New Zealand operations. Mr Hill resigned as Chief Operating Officer on 28 February 2006. The Board granted Mr Hill six months leave of absence effective 1 March 2006.

During the financial year he attended 4 of the 4 directors’ meetings held.

The above named directors held office during and since the end of the financial year except for:

Mr W.V. Hill – resigned 28 November 2006 Mr C.G. Ryan – appointed 28 February 2007 Mr J.J.A. Johnson – resigned 28 February 2007 Mr D. Herceg – appointed 9 March 2007 Mr R.D. Catelan – appointed 18 May 2007 Mr M.J. Hofmeister – resigned 8 June 2007 Mr M.C. Maughan – resigned 2 July 2007

Mr R.D. Catelan and Mr D. Herceg were appointed Directors of BigAir Group Limited in July 2007. The directors do not hold any other listed company directorships.

Details of directors’ shareholdings as at the date of this report:

NameFully Paid Ordinary

SharesPartly Paid Ordinary

SharesFully Paid Class A

SharesExecutive Share

Options

R.D. Catelan as:

RP Prospects Pty Limited as trustee for the M & L Trust 10,274,943 – 964,067 –

Directors’ Report

CMI LIMITED ANNUAL REPORT 2007�6

Company Secretary

Mark D. Laidlaw Joined CMI Limited in 1997 as Chief Financial Officer. He is a former audit manager of international accountancy firm, Deloitte Touche Tohmatsu. He is a member of the Institute of Chartered Accountants in Australia and holds a Bachelor of Commerce (Honours) from the University of Queensland.

Principal Activities

The consolidated entity’s principal activities in the course of the financial year were the manufacture and marketing of precision engineered components, particularly for the automotive industry, the manufacture and marketing of components and parts for 4WD, light commercial and heavy transport vehicles, the manufacture and marketing of specialist cabling and electrical products for a range of industry sectors and the provision of chattel finance to both consumer and commercial borrowers.

Review Of Operations

Consolidated revenue for the year was $265,397 thousand (2006: $278,704 thousand). The consolidated entity’s loss before tax was $5,236 thousand (2006 profit: $15,960 thousand) and the loss after tax was $3,840 thousand (2006 profit: $11,197 thousand). Refer to the Chairman’s Review and the Operational Review for more details.

Changes In State Of Affairs

During the financial year there was no significant change in the state of affairs of the consolidated entity other than that referred to in the financial statements or notes thereto.

Future Developments

Disclosure of information regarding likely developments in the operations of the consolidated entity in future financial years and the expected results of those operations is likely to result in unreasonable prejudice to the consolidated entity. Accordingly, this information has not been included in this report.

Subsequent Events

There has not been any matter or circumstance, other than that referred to above, in the financial statements or notes thereto, that has arisen since the end of the financial year, that has significantly affected, or may significantly affect, the operations of the consolidated entity, the results of those operations, or the state of affairs of the consolidated entity in future financial years.

Environmental Regulations

The consolidated entity’s operations are subject to various environmental regulations governed by State, Federal and Local legislation. The impact on the business is constantly reviewed to ensure it complies with and exhibits best practice within the following areas of environmental regulation: air, water, noise, hazardous chemicals and contaminated land waste.

Appropriate licenses have been obtained where necessary and procedures implemented to ensure that the consolidated entity operates under the conditions imposed by the license or regulation. During the year, no areas of non-compliance were identified.

Dividends

All dividends stated below are whole numbers and are not rounded to the nearest thousand dollars.

In respect of the financial year ended 30 June 2006, as detailed in the directors’ report for that financial year, a final dividend of $912,688 (3.5 cents per share) franked to 100% at 30% corporate income tax rate was paid to the holders of fully paid Class A shares on 4 September 2006.

In respect of the financial year ended 30 June 2006, as detailed in the directors’ report for that financial year, a final dividend of $2,170,510 (6 cents per share) franked to 100% at 30% corporate income tax rate was paid to the holders of fully paid and partly paid ordinary shares on 2 November 2006.

In respect of the financial year ended 30 June 2007, an interim dividend of $912,688 (3.5 cents per share) franked to 100% at 30% corporate income tax rate was paid to the holders of fully paid Class A shares on 4 December 2006.

Directors’ Report

CMI LIMITED ANNUAL REPORT 2007 �7

In respect of the financial year ended 30 June 2007, interim dividends of $980,188 (3.5 cents per share) franked to 100% at 30% corporate income tax rate were paid to the holders of fully paid Class A shares on 2 March 2007 and 4 June 2007.

In respect of the financial year ended 30 June 2007, an interim dividend of $1,012,579 (3 cents per share) franked to 100% at 30% corporate income tax rate was paid to the holders of fully paid ordinary shares on 2 May 2007.

In respect of the financial year ended 30 June 2007, the directors recommend the payment of a final dividend of $980,188 (3.5 cents per share) franked to 100% at 30% corporate income tax rate to the holders of fully paid Class A shares on 3 September 2007.

In respect of the financial year ended 30 June 2007, the directors do not recommend the payment of a final dividend to the holders of fully paid ordinary shares.

Indemnification Of Officers And Auditors

During the financial year, the company paid a premium in respect of a contract insuring the directors of the company (as named above), the company secretary and all executive officers of the company and of any related body corporate against a liability incurred as such a director, secretary or executive officer to the extent permitted by the Corporations Act 2001. The contract of insurance prohibits disclosure of the nature of the liability and the amount of the premium.

The company has not otherwise, during or since the financial year, indemnified or agreed to indemnify an officer or auditor of the company or of any related body corporate against a liability incurred as such an officer or auditor.

Remuneration Report

The remuneration report is set out under the following main headings:

A. Principles used to determine the nature and amount of remuneration

B. Service agreements

C. Details of remuneration

D. Share-based compensation

A. Principles Used to Determine the Nature and Amount of Remuneration

The remuneration committee reviews the remuneration packages of all directors and executives on an annual basis and makes recommendations to the board. Remuneration packages are reviewed and determined with due regard to current market rates and are benchmarked against comparable industry salaries, adjusted by a performance factor to reflect changes in the performance of the company.

The objective of the company’s remuneration reward framework is to ensure reward for performance is competitive and appropriate for the results delivered. The framework aligns reward with achievement of strategic and financial objectives and the creation of wealth for shareholders.

In order to retain and attract executives of sufficient calibre to facilitate the efficient and effective management of the company’s operations, the remuneration committee seeks the advice of external advisers in connection with the structure of remuneration packages.

The overall level of executive reward takes into account the performance of the consolidated entity over a number of years. Over the past five years, the consolidated entity’s profit from ordinary activities after income tax (but prior to the impairment loss) has grown by 87.7%, and total equity has grown by 55.8%. During the same period, directors and executives remuneration (included in part C below) has grown by 130.8%. Refer to the Financial Summary in the 2007 Highlights for more details.

In accordance with the company’s constitution, the total remuneration payable to non-executive directors is not to exceed $390,000 per annum as approved by the shareholders at a general meeting.

One non-executive director received payment upon retirement of three times their annual director fee.

Remuneration packages contain the following key elements:

a) Short-term employee benefits - salary/fees, bonuses and non monetary benefits including the provision of motor vehicles, accommodation and interest not charged on loans provided by the company;

b) Post-employment benefits - including superannuation and prescribed benefits; and

c) Share-based payment – shares issued during the financial year and share options granted under the director and employee share option plans approved by shareholders on 23 August 1999, and

d) Long-term benefits – including long service leave and retirement benefits.

Directors’ Report

CMI LIMITED ANNUAL REPORT 2007�8

Short-term employee benefits – directors and executives listed in part C below are offered a competitive remuneration that comprises the components of base pay and benefits. Base pay for executives is reviewed annually to ensure the executive’s pay is competitive with the market. An executive’s pay is also reviewed on promotion. Specific key management personnel are paid cash bonuses based on performance criteria. The performance criteria used to determine the amount of compensation include revenue, net profit before tax and inventory targets.

Other benefits – executives receive benefits including long service leave and superannuation as required by the laws in the various jurisdictions in which the company operates. In certain circumstances, additional benefits (e.g. travel, car parking and accommodation) may also be provided.

Equity - further details of the employee incentive scheme are disclosed in note 23 to the financial statements.

None of the directors or executives listed in part C below received any profit based or performance based compensation by way of bonus or other compensation.

B. Service Agreements

Directors and executives are employed through contracts for service which contain the following key conditions:

• Reviewed annually on or about 1 September;

• Require a six month notice period; and

• If employment is terminated by the company before the term of the contract expires, the specified director or executive is entitled to a termination payment based on up to two years of the contract, or the remaining contract period, whichever is greater.

C. Details of Remuneration

The directors of the company and the consolidated entity are detailed below as are the five executives who received the highest remuneration for the year ended 30 June 2007:

Directors

C.G. Ryan (appointed 28 February 2007) D. Herceg (appointed 9 March 2007) R.D. Catelan (appointed 18 May 2007) M.J. Hofmeister (resigned 8 June 2007) M.C. Maughan (resigned 2 July 2007) J.J.A. Johnson (resigned 28 February 2007) W.V. Hill (resigned 28 November 2006)

Five highest remunerated executives

P.R. Meurer (Chief Executive – Engineering Division), resigned 16 November 2006 D.J. Gallagher (Manufacturing Manager – Engineering Division) I.C. Whittle (Managing Director – Capitalcorp Finance & Leasing Pty Ltd) M.D. Laidlaw (Chief Financial Officer/Company Secretary) J.L. Heslington (General Manager – Electrical Components Division)

Directors’ Report

CMI LIMITED ANNUAL REPORT 2007 �9

The following tables disclose the remuneration of the directors and five highest remunerated executives of the company and the consolidated entity.

2007

Short-term Employee Benefits Post Employment Benefits Share-based payment

Total $

Salary/Fees

$Bonus

$

Non-monetary

$Other

$Superannuation

$Other

$Shares

$Options

$

C.G. Ryan 53,776 - - - - - - - 53,776

D. Herceg 22,667 - - - 2,040 - - - 24,707

R.D. Catelan - - - - - - - - -

M.J. Hofmeister 1,018,500 - - 241,644 - - - - 1,260,144

J.J.A. Johnson 36,666 - - 8,209 - - - - 44,875

W. V. Hill - - - - - - - - -

M.C. Maughan 89,905 - - - - - - - 89,905

P.R. Meurer 147,791 - - - 33,355 329,047 - - 510,193

D.J. Gallagher 157,586 - 15,000 13,608 103,320 218,866 - - 508,380

I.C. Whittle 300,000 - - 594 - - - - 300,594

M.D. Laidlaw 244,648 - - 19,708 22,019 - - - 286,375

J.L. Heslington 216,333 - 15,000 29,331 19,470 - - - 280,134

Total 2,287,872 - 30,000 313,094 180,204 547,913 - - 3,359,083

2006

Short-term Employee Benefits Post Employment Benefits Share-based payment

Total $

Salary/ Fees

$Bonus

$

Non-monetary

$Other

$Superannuation

$Other

$Shares

$Options

$

M.J. Hofmeister 880,000 - - 89,609 - - 53,584 - 1,023,193

J.J.A. Johnson 55,000 - - 10,654 - - - - 65,654

W. V. Hill 168,314 - - 15,429 - - - - 183,743

M.C. Maughan 34,005 - - - - - - - 34,005

V. Misztowt 345,485 - - 16,394 - - - - 361,879

I.C. Whittle 300,000 - - 609 - - - - 300,609

P.R. Meurer 275,229 - - - 24,771 - - - 300,000

D.J. Gallagher 160,329 - 15,000 13,788 100,296 - - - 289,413

M.D. Laidlaw 207,951 - - 19,070 18,716 - - - 245,737

Total 2,426,313 - 15,000 165,553 143,783 - 53,584 - 2,804,233

(i) Further disclosure is contained in notes 23 and 27 to the financial statements.

D. Share Based Compensation

The Remuneration Committee makes recommendations to the Board regarding the granting of options to directors and executives as part of their remuneration package based on the company’s performance and as an incentive to improve the performance of the company. Options issued to directors require approval by a general meeting of shareholders. Options issued to executives are in accordance with the company’s employee incentive scheme.

Share Options Granted to Key Management Personnel

No options were granted to directors or executives during and since the end of the financial year.

Directors’ Report

CMI LIMITED ANNUAL REPORT 200720

Share Options Exercised During the Year

On 20 December 2006, 1,000,000 fully paid ordinary shares were issued to Mr M.J. Hofmeister pursuant to the exercise of unquoted options.

Share Options Lapsed During the Year

200,000 share options lapsed during the financial year.

The Percentage of Remuneration Consisting of Options During the Year

As no options were issued during the year, the percentage of remuneration consisting of options for directors and for the five highest remunerated executives during the year was zero.

Share Options on Issue to Directors and the Five Highest Remunerated Executives

The following options were on issue at year end:

Individual Issuing EntityNumber of Shares

Under Option Class of Share Exercise PriceExpiry Date of

Options

M.D. Laidlaw CMI Limited 100,000 Ordinary $2.22 28/10/09

J.L. Heslington CMI Limited 10,000 Ordinary $2.22 27/4/09

Employee Incentive Scheme

In accordance with the provisions of the employee incentive scheme, as at the date of this report, employees are entitled to purchase an aggregate of 42,500 ordinary shares of CMI Limited at an issue price of $2.22 per ordinary share during the period of 5 years after 27 April 2004 and 100,000 ordinary shares of CMI Limited at an issue price of $2.22 per ordinary share during the period of 5 years after 29 October 2004.

Further details of the employee incentive scheme are disclosed in note 23 to the financial statements.

Non-audit Services

The directors are satisfied that the provision of non-audit services, during the year, by the auditor (or by another person or firm on the auditor’s behalf) is compatible with the general standard of independence for auditors imposed by the Corporations Act 2001. Details of amounts paid or payable for non-audit services provided during the year by the auditor are outlined in note 25 to the financial statements.

Independence Declaration By Auditors

The auditor’s independence declaration is included on page 21.

Rounding Off Of Amounts

The company is a company of the kind referred to in ASIC Class Order 98/0100, dated 10 July 1998, and in accordance with that Class Order amounts in the directors’ report and the financial report have been rounded off to the nearest thousand dollars, unless otherwise stated.

Signed in accordance with a resolution of the directors made pursuant to section 298(2) of the Corporations Act 2001.

On behalf of the Directors

C.G. RyanChairman

R.D. CatelanDirector

BRISBANE

Dated: 12 September 2007

Directors’ Report

CMI LIMITED ANNUAL REPORT 2007 2�

CMI LIMITED ANNUAL REPORT 200722

CMI LIMITED ANNUAL REPORT 2007 23

CMI LIMITED ANNUAL REPORT 200724

The directors declare that:

a) In the directors’ opinion, there are reasonable grounds to believe that the company will be able to pay its debts as and when they become due and payable;

b) In the directors’ opinion, the attached financial statements and notes thereto are in accordance with the Corporations Act 2001, including compliance with accounting standards and giving a true and fair view of the financial position and performance of the company and the consolidated entity; and

c) The directors have been given the declarations required by section 295A of the Corporations Act 2001.

At the date of this declaration the company is within the class of companies affected by ASIC Class Order 98/1418. The nature of the deed of cross guarantee is such that each company which is party to the deed guarantees to each creditor payment in full of any debt in accordance with the deed of cross guarantee.

In the directors’ opinion, there are reasonable grounds to believe that the company and the companies to which the ASIC Class Order applies, as detailed in Note 28 to the financial statements, will as a group, be able to meet any obligations or liabilities to which they are, or may become, subject by virtue of the deed of cross guarantee.

Signed in accordance with a resolution of the directors made pursuant to section 295(5) of the Corporations Act 2001.

On behalf of the Directors

C.G. Ryan

Chairman

R.D. Catelan

Director

BRISBANE

Dated: 12 September 2007

Directors’ DeclarationFOR THE FINANCIAL YEAR ENDED 30 JUNE 2007

CMI LIMITED ANNUAL REPORT 2007 25

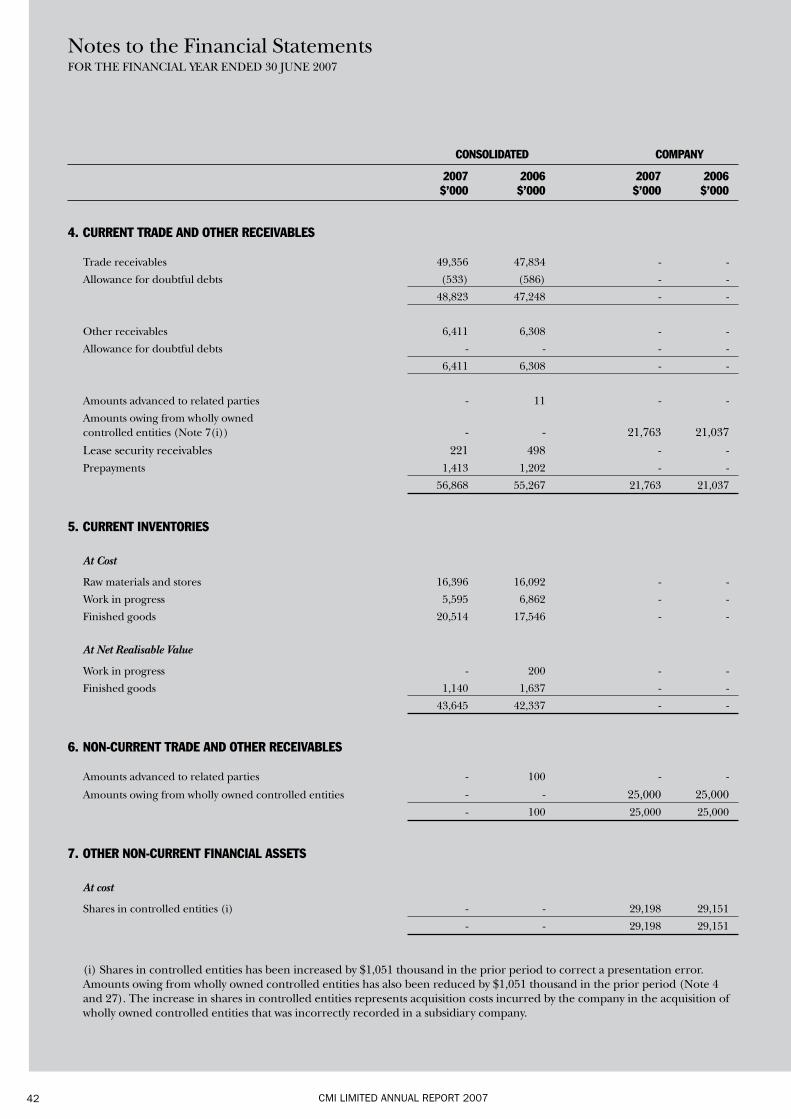

NOTE CONSOLIDATED COMPANY

2007 2006 2007 2006 $’000 $’000 $’000 $’000

Revenue 2 265,397 278,704 10,226 10,549

Other income 2 2,701 2,416 3 3

Changes in inventories (1,476) (4,679) - -

Raw materials expense (116,518) (112,415) - -

Sub-contractors expense (7,537) (14,122) - -

Employee benefits expense (79,906) (84,250) (218) (93)

Repairs, maintenance and consumables expense (9,458) (10,530) - -

ASX and share register expense (215) (219) (215) (219)

Occupancy expense (11,810) (11,410) (86) (318)

Travel and communication expense (4,272) (4,002) - -

Freight and cartage expense (5,546) (5,589) - -

Depreciation and amortisation expense (7,379) (7,730) - -

Finance costs (4,397) (4,060) - -

Impairment of non-current assets (18,601) - - -

Other expenses (6,219) (6,154) - (4)

Profit/(Loss) before income tax 2 (5,236) 15,960 9,710 9,918

Income tax 3 1,396 (4,763) (2,711) (2,831)

Profit/(Loss) from continuing operations (3,840) 11,197 6,999 7,087

Profit/(Loss) attributable to members of the parent entity (3,840) 11,197 6,999 7,087

Earnings per share:

Basic (cents per share) 21 (21.61) 23.45

Diluted (cents per share) 21 (21.61) 23.09

Notes to the financial statements are included on pages 30 to 79.

Income StatementFOR THE FINANCIAL YEAR ENDED 30 JUNE 2007

CMI LIMITED ANNUAL REPORT 200726

NOTE CONSOLIDATED COMPANY

2007 2006 2007 2006 $’000 $’000 $’000 $’000

CURRENT ASSETS

Cash and cash equivalents 4,724 3,461 - -

Trade and other receivables 4 56,868 55,267 21,763 21,037

Inventories 5 43,645 42,337 - -

Current tax assets 3 1,189 - 1,171 -

106,426 101,065 22,934 21,037

Non-current assets classified as held for sale 34 1,032 - - -

TOTAL CURRENT ASSETS 107,458 101,065 22,934 21,037

NON-CURRENT ASSETS

Trade and other receivables 6 - 100 25,000 25,000

Other financial assets 7 - - 29,198 29,151

Property, plant and equipment 8 43,354 61,876 - -

Goodwill 9 10,176 6,309 - -

Other intangible assets 10 22,351 24,215 - -

Deferred tax assets 3 212 209 74 161

TOTAL NON-CURRENT ASSETS 76,093 92,709 54,272 54,312

TOTAL ASSETS 183,551 193,774 77,206 75,349

CURRENT LIABILITIES

Trade and other payables 11 31,798 32,872 - 165

Borrowings 12 52,295 7,610 7,069 6,616

Current tax payables 3 - 406 - 445

Provisions 13 7,289 11,746 - -

TOTAL CURRENT LIABILITIES 91,382 52,634 7,069 7,226

NON-CURRENT LIABILITIES

Borrowings 14 6,008 45,325 - -

Deferred tax liabilities 3 1,231 5,625 - -

Provisions 15 5,415 2,205 - -

TOTAL NON-CURRENT LIABILITIES 12,654 53,155 -

TOTAL LIABILITIES 104,036 105,789 7,069 7,226

NET ASSETS 79,515 87,985 70,137 68,123

EQUITY

Issued capital 18 70,103 67,999 70,103 67,999

Reserves 19 91 (144) - 120

Retained earnings 20 9,321 20,130 34 4

TOTAL EQUITY 79,515 87,985 70,137 68,123

Notes to the financial statements are included on pages 30 to 79.

Balance SheetAS AT 30 JUNE 2007

CMI LIMITED ANNUAL REPORT 2007 27

NOTE CONSOLIDATED

Issued Capital Reserves Retained Earnings Total Equity $’000 $’000 $’000 $’000

At 1 July 2005 68,067 223 16,006 84,296

Adjustment on adoption of AASB 132 and AASB 139 1(u) (20,401) - - (20,401)

Adjustment on conversion of convertible preference shares to Class A shares 1(u) 20,401 - - 20,401

Translation of foreign operations: Exchange differences taken to equity - (420) - (420)

Net Income Recognised Directly in Equity - (420) - (420) Profit for the period - - 11,197 11,197

Total Recognised Income and Expense for the Period - (420) 11,197 10,777

Transactions with equity holders in their capacity as equity holders:

Contributions of equity - - - -

Share buy-back (68) - - (68)

Employee equity-settled benefits - 53 - 53 Dividends provided for or paid - - (7,073) (7,073)

At 1 July 2006 67,999 (144) 20,130 87,985

Translation of foreign operations: Exchange differences taken to equity - 355 - 355

Net Income Recognised Directly in Equity - 355 - 355 Profit/(Loss) for the period - - (3,840) (3,840)

Total Recognised Income and Expense for the Period - 355 (3,840) (3,485)

Transactions with equity holders in their capacity as equity holders:

Contributions of equity – ordinary shares 4,350 - - 4,350

Contributions of equity – Class A shares 2,063 - - 2,063

Ordinary share buy-back (3,954) - - (3,954)

Equity adjustment on share buy-back (424) - - (424)

Ordinary share buy-back costs (98) - - (98)

Employee equity-settled benefits - 47 - 47

Employee equity-settled benefits reserve transferred to issued capital 167 (167) - -

Dividends provided for or paid - - (6,969) (6,969)

At 30 June 2007 70,103 91 9,321 79,515

Notes to the financial statements are included on pages 30 to 79.

Statement of Changes in EquityFOR THE FINANCIAL YEAR ENDED 30 JUNE 2007

CMI LIMITED ANNUAL REPORT 200728

NOTE COMPANY

Issued Capital Reserves Retained Earnings Total Equity $’000 $’000 $’000 $’000

At 1 July 2005 68,067 67 (10) 68,124

Adjustment on adoption of AASB 132 and AASB 139 1(u) (20,401) - - (20,401)

Adjustment on conversion of convertible preference shares to Class A shares 1(u) 20,401 - - 20,401

Profit for the period - - 7,087 7,087

Total Recognised Income and Expense for the Period - - 7,087 7,087

Transactions with equity holders in their capacity as equity holders:

Contributions of equity - - - -

Share buy-back (68) - - (68)

Employee equity-settled benefits - 53 - 53

Dividends provided for or paid - - (7,073) (7,073)

At 1 July 2006 67,999 120 4 68,123

Profit for the period - - 6,999 6,999

Total Recognised Income and Expense for the Period - - 6,999 6,999

Transactions with equity holders in their capacity as equity holders:

Contributions of equity – ordinary shares 4,350 - - 4,350

Contributions of equity – Class A shares 2,063 - - 2,063

Ordinary share buy-back (3,954) - - (3,954)

Equity adjustment on share buy-back (424) - - (424)

Ordinary share buy-back costs (98) - - (98)

Employee equity-settled benefits - 47 - 47

Employee equity-settled benefits reserve transferred to issued capital 167 (167) - -

Dividends provided for or paid - - (6,969) (6,969)

At 30 June 2007 70,103 - 34 70,137

Notes to the financial statements are included on pages 30 to 79.

Statement of Changes in EquityFOR THE FINANCIAL YEAR ENDED 30 JUNE 2007

CMI LIMITED ANNUAL REPORT 2007 29

NOTE CONSOLIDATED COMPANY

2007 2006 2007 2006 $’000 $’000 $’000 $’000 Inflow Inflow Inflow Inflow (Outflow) (Outflow) (Outflow) (Outflow)

Cash flows from operating activities:

Receipts from customers 292,496 316,688 - -

Payments to suppliers and employees (269,509) (282,148) - -

Interest paid (3,862) (3,284) - -

Dividends received - - 523 481

Income tax paid (4,374) (6,996) (4,342) (6,814)

Net cash provided by/(used in) operating activities 30(b) 14,751 24,260 (3,819) (6,333)

Cash flows from investing activities:

Interest received 254 278 - -

Payment for intangible assets - (188) - -

Payment for deferred expenditure (1,313) (1,337) - -

Amounts received from/(advanced) to related parties 4,450 - 13,239 14,384

Payment for plant and equipment (2,702) (3,190) - -

Payment for purchase of businesses 30(c) (8,808) (1,297) - -

Proceeds from sale of plant and equipment 2,001 92 3 3

Net cash (used in)/provided by investing activities (6,118) (5,642) 13,242 14,387

Cash flows from financing activities:

Proceeds from issue of equity securities - - - -

Share issue expenses (140) - (140) -

Payment for share buy-back (2,314) (68) (2,314) (68)

Dividends paid (6,969) (7,986) (6,969) (7,986)

Proceeds from borrowings 8,000 - - -

Repayment of borrowings (6,010) (10,452) - -

Net cash provided by/(used in) financing activities (7,433) (18,506) (9,423) (8,054)

Net increase/(decrease) in cash and cash equivalents held 1,200 112 - -

Cash and cash equivalents at the beginning of the financial year 3,433 3,336 - -

Effect of exchange rate changes on the balance of cash held in foreign currencies 29 (15) - -

Cash and cash equivalents at the end of the financial year 30(a) 4,662 3,433 - -

Notes to and forming part of the financial statements are included on pages 30 to 79.

Cash Flow StatementFOR THE FINANCIAL YEAR ENDED 30 JUNE 2007

CMI LIMITED ANNUAL REPORT 200730

1. SUMMARY OF ACCOUNTING POLICIES

Statement of Compliance

The financial report is a general purpose financial report which has been prepared in accordance with the Corporations Act 2001, Accounting Standards and Interpretations, and complies with other requirements of the law. The financial report includes the separate financial statements of the company and the consolidated financial statements of the Group. Accounting Standards include Australian equivalents to International Financial Reporting Standards (‘A-IFRS’). Compliance with the A-IFRS ensures that the financial statements and notes of the company and the Group comply with International Financial Reporting Standards (‘IFRS’). The parent entity financial statements and notes also comply with IFRS except for the disclosure requirements in IAS 32 Financial Instruments: Disclosure and Presentation as the Australian equivalent Accounting Standard, AASB 132 Financial Instruments: Disclosure and Presentation does not require such disclosures to be presented by the parent entity where its separate financial statements are presented together with the consolidated financial statements of the consolidated entity.

The financial statements were authorised for issue by the directors on 12 September 2007.

Basis of Preparation

The financial report has been prepared on the basis of historical cost. Cost is based on the fair values of the consideration given in exchange for assets. All amounts are presented in Australian dollars, unless otherwise noted.

The company is a company of the kind referred to in ASIC Class Order 98/0100, dated 10 July 1998, and in accordance with that Class Order amounts in the directors’ report and the financial report have been rounded off to the nearest thousand dollars, unless otherwise stated.

In the application of CMI Limited (“Group”) accounting policies, management is required to make judgments, estimates and assumptions about carrying values of assets and liabilities that are not readily apparent from other sources. The estimates and associated assumptions are based on historical experience and various other factors that are believed to be reasonable under the circumstance, the results of which form the basis of making the judgments. Actual results may differ from these estimates. The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimate is revised if the revision only affects that period, or in the period of the revision and future periods if the revision affects both current and future periods.

Judgments made by management in the application of the Group’s accounting policies that have significant effects on the financial statements and estimates with a significant risk of material adjustments in the next year are disclosed, where applicable, in the relevant notes to the financial statements.

Accounting policies are selected and applied in a manner which ensures that the resulting financial information satisfies the concepts of relevance and reliability, thereby ensuring that the substance of the underlying transactions or other events is reported.

The following significant accounting policies have been adopted in the preparation and presentation of the financial report.

Significant Accounting Policies

a) Borrowings