Club Link Annual Report - 2010

76

Your Passport to more ! Clubhouse at Club Renaissance ANNUAL REPORT 20 10

-

Upload

sutton-compliance-communications -

Category

Investor Relations

-

view

408 -

download

7

Transcript of Club Link Annual Report - 2010

15675 Dufferin Street,King City, Ontario,Canada L7B 1K5

Tel 905 841 3730Fax 905 841 1134

CLUBLINKENTERPRISESLIMITED

Your Passport tomore !

Clubhouse at Club Renaissance

ANNUAL REPORT 2010

Photo courtesy of The Greg Wilson Group

CONTENTS1 Financial Highlights2 Chairman’s Message4 ClubLink Establishes a Florida Region5 Heron Bay Golf Club – Florida6 ClubLink in Sun City Center – Florida8 Glendale Joins ClubLink

10 Your Passport to More Excitement at White Pass12 Map of Canadian Golf Club and Resort Locations13 Golf Club and Resort Property Listing14 Management’s Discussion and Analysis of Financial Condition and Results of Operations47 Management’s Responsibility for Financial Reporting47 Independent Auditor’s Report48 Consolidated Balance Sheets49 Consolidated Statements of Earnings and Comprehensive Earnings49 Consolidated Statements of Retained Earnings and Accumulated Other Comprehensive Loss50 Consolidated Statements of Cash Flows51 Notes to Consolidated Financial Statements73 Board of Directors, Senior Officers, Corporate Information and Location of Annual Meeting of Shareholders

ClubLink Enterprises Limited has a strategic objective tomaximize shareholder value over a five to ten year horizon,though the Company may monetize an investment when businessconditions present a suitable opportunity.

ClubLink is engaged in golf club and resort operations underthe trademark “ClubLink One Membership More Golf”. ClubLinkis Canada’s largest owner and operator of golf clubs with 48½,18-hole equivalent championship and six 18-hole equivalentacademy courses at 41 locations, primarily in Ontario, Quebecand Florida.

ClubLink is also engaged in rail, tourism and port operationsbased in Skagway, Alaska, which operates under the trade name“White Pass & Yukon Route.” The railway stretches approximately177 kilometres (110 miles) from Skagway, Alaska, through BritishColumbia to Whitehorse, Yukon. In addition, ClubLink operatesthree docks primarily for cruise ships.

BOARD OF DIRECTORS SENIOR OFFICERS

PATRICK S. BRIGHAM (b, c)

PAUL CAMPBELL (b, c)

DAVID A. KING (a)

JOHN LOKKER (a)

SAMUEL J.B. POLLOCK (a, b)

K. (RAI) SAHI

DONALD W. TURPLE (c)

JACK D. WINBERG (b, c)

(a) Audit Committee

(b) Corporate Governance and Compensation Committee

(c) Environmental, Health and Safety Committee

ClubLink Enterprises Limited

K. (RAI) SAHIChairman and Chief Executive Officer

ROBERT VISENTINChief Financial Officer

EUGENE N. HRETZAYVice President, General Counsel and SecretaryPresident, White Pass and Yukon Route

ROBERT WRIGHTVice President

Golf Club and Resort Operations

EDGE M. CARAVAGGIOVice President, Operations

SCOTT DAVIDSONVice President, Corporate Operations

CHARLES F. LORIMERVice President, Sales & Marketing

NEIL E. OSBORNEVice President, Clubhouse Operations

Rail, Tourism and Port Operations

MICHAEL D. BRANDTSenior Vice President, Planning & Administration

ED C. HANOUSEKSuperintendent, Rail Operations

Annual Meeting of ShareholdersAnnual Meeting of Shareholders of ClubLink EnterprisesLimited will be held at 11 a.m. on May 19, 2011 at King ValleyGolf Club, 15675 Dufferin Street, King City, Ontario, L7B 1K5.

CORPORATE INFORMATION

Executive Office15675 Dufferin StreetKing City, Ontario L7B 1K5Tel: (905) 841-3730Fax: (905) 841-1134

Websites:clublinkenterprises.ca/comclublink.ca/comwpyr.com

Investor RelationsContact: Robert VisentinTel: 905-841-5360Fax: 905-841-1134Email: [email protected]

BankersHSBC Bank CanadaWells Fargo Bank Alaska

AuditorsDeloitte & Touche LLP

Stock Exchange ListingsCommon shares: TSX: CLK

Transfer AgentCanadian Stock Transfer Company, Inc.

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

73

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

1

FINANCIAL HIGHLIGHTS

The following table summarizes the consolidated financial results of the Company:

For the Years Ended December 31 2010 2009 2008 2007 (4) 2006 (4)

OPERATIONSOperating revenue ($000) 189,903 190,212 196,532 160,710 40,506

Net operating income ($000) (1) 49,858 51,437 55,035 50,595 18,589

Operating margin (%) (1) 26.3 27.0 28.0 31.5 45.9

Net membership fee income ($000) (1) 13,781 12,829 12,327 6,724 –

Earnings before other items, income taxes andnon-controlling interest ($000) (1) 63,639 64,266 67,362 57,319 18,589

Net earnings ($000) 11,842 11,155 6,125 8,869 18,071

Cash flow from operations ($000) (1) 36,299 27,912 35,516 40,873 25,332

OPERATING DATA

ClubLink One Membership More Golf

Championship rounds – Canada (2) 1,064,000 1,020,000 975,000 1,004,000 886,000

18-hole equivalent championship golf courses – Canada (2, 3) 40.5 40.5 38.5 38.5 35.0

Average number of championship roundsper 18-hole golf course – Canada (2, 3) 26,272 25,185 25,325 26,078 25,314

Championship rounds – U.S. (2) 58,000 11,000 13,000 14,000 13,000

18-hole equivalent championship golf courses – U.S. (2, 3) 7.0 1.0 1.0 1.0 1.0

White Pass & Yukon Route

Rail passengers 368,000 396,000 438,000 461,000 431,000Port passengers from cruise ships 697,000 781,000 779,000 820,000 760,000

MEMBERSHIP DATA

Sales and transfer fees ($000) 9,752 15,214 15,225 23,399 18,182

Sales (Members) 1,456 1,477 1,194 2,230 1,001

Resignations and terminations ($000) 4,726 4,595 3,685 2,893 2,624

Resignations and terminations (Members) 1,100 1,075 766 513 599

Golf Members at year end (Members) 18,917 17,049 16,647 16,219 14,502

Cash collected, net of origination costs ($000) 11,803 11,951 15,514 12,248 –Deferred membership fees at year end ($000) 57,356 59,334 60,212 57,025 –

FINANCIAL POSITION

Total assets ($000) 611,412 627,753 641,300 626,765 154,378

Total debt ($000) 359,813 375,702 388,692 380,371 21,706

Shareholders’ equity ($000) 155,797 154,560 109,625 104,188 112,407Total debt to shareholders’ equity ratio 2.31 2.43 3.55 3.65 0.19

PER COMMON SHARE DATA ($)

Basic and diluted earnings 0.42 0.44 0.27 0.39 0.79

Basic and diluted cash flow from operations (1) 1.30 1.11 1.55 1.79 1.10Eligible cash dividends 0.30 0.27 0.24 0.24 0.24

COMMON SHARE DATA (000)

Shares outstanding 27,903 28,057 22,909 22,739 22,939Weighted average shares outstanding 27,976 25,113 22,887 22,784 22,933

(1) Net operating income, operating margin, net membership fee income, earnings before other items, income taxes and non-controlling interest, cash flow from operations, and basicand diluted cash flow from operations per share are not recognized measures under Canadian generally accepted accounting principles (GAAP). Management believes that thesemeasures are useful supplemental information. Investors should be cautioned, however, that these measures should not be construed as an alternative to net earnings determinedin accordance with GAAP as an indicator of the Company’s performance or to cash flows from operating, investing and financing activities, as a measure of liquidity and cash flows.ClubLink’s method of calculating these measures is consistent from year to year, but may be different than those used by other companies (see “Management’s Discussion andAnalysis of Financial Condition and Results of Operations”).

(2) Excluding academy courses.

(3) 18-hole equivalent championship golf courses operating during the year ended December 31, excluding Glendale Golf and Country Club (acquired December 2010).

(4) The 2007 results include the consolidation of ClubLink Corporation’s results for seven months. During 2006, the investment in ClubLink Corporation was accounted for as an equityinvestment. Operating and Membership data for ClubLink Corporation display 100% of the operating results, consolidation commenced in 2007.

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

2

CHAIRMAN’S MESSAGE

Your Passport to

ClubLink ended the year at 18,917 golf members – up 1,868 golfmembers or 11% from 17,049 golf members at the end of 2009.Our golf membership has grown by almost five thousand members(or 34%) over the last five years.

K. (Rai) SahiChairman & ChiefExecutive Officer

2010 represented a year of opportunity. On September 3rd, ClubLink announced that it had entered the Florida marketplace bypurchasing eight 18-hole equivalent golf courses in Sun City Center, Florida. This acquisition was supplemented by the acquisitionof Heron Bay Golf Club near Fort Lauderdale on October 21st. These acquisitions created ClubLink’s first region outside of Canada.

Driven by a depressed Florida real estate market with plenty of opportunities and our desire to continually add value to our Canadiangolf memberships, these acquisitions represent the beginning of ClubLink’s presence and operating model in Florida.

We believe that the Florida golf market is a logical extension to our current Ontario/Quebec focus. Based on our members surveys, manyof our Canadian members travel to Florida on golf vacations, have winter homes in the state or will be purchasing a vacation home in thenear future. This will allow them to receive additional value from their current ClubLink membership.

Late in 2010, ClubLink acquired Glendale Golf and Country Club in Hamilton, Ontario. Glendale was founded in 1919and was one of the first private golf clubs in the Hamilton area. Glendale will provide a natural complement to nearby Heron Point GolfLinks in Ancaster.

ClubLink’s strong financial position has allowed this expansion. After spending $13 million on these acquisitions, we closed the year withliquidity of $41 million, virtually unchanged from the end of 2009. Our debt to equity ratio also declined from 2.43 in 2009 to 2.31in 2010.

We believe that our balance sheet has allowed us to continue to expand in a prudent manner.

ClubLink was able to realize strong growth in its golf club and resort operations segment during 2010. Net operating income increased8.2% to $35.2 million from $32.6 million in 2009. Even with the loss of a strong contribution from the 2009 RBC Canadian Open, hostedby Glen Abbey Golf Club, we were able to capitalize on the modest economic recovery from the 2009 recession which provided increasesin most operational metrics.

more!

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

3

Other operational highlights for thegolf club and resort operations in2010 included:

• The opening of a new $5 millionclubhouse at the 36 hole GreyHawkGolf Club at the beginning of the2010 golf season. This investmenthas enhanced the value of anOttawa area membership;

• The inaugural 2010 MontrealChampionship (Champions TourEvent) was successfully hosted atour Club de Golf Le Fontainebleau.Plans are already in place for thereturn of this event in 2011; and

• The conversion of the 18-holechampionship daily fee golf courseat Rolling Hills Golf Club into aHybrid-Silver Golf Club named“Bethesda Grange”.

Rail, tourism and port operations netoperating income decreased to $17.3million in 2010 from $20.6 millionin 2009.

The rail, tourism and port operationresults were impacted by two factors.Significantly fewer cruise ship visits toAlaska resulted in a decline in portpassengers to our docks in Skagway,Alaska and therefore a decline in ourrail passengers. Secondly, a strongerCanadian dollar resulted in a declineof $1.3 million in the segment’sCanadian dollar net operating income.

The decline in cruise ship visits was areaction to the State of Alaska HeadTax imposed on each cruise ship tourist.With the partial repeal of this tax in2010, we expect to see modestincreases in cruise ship visits startingin 2011. The arrival of Disney, Crystaland Oceania cruise lines to Alaska in2011 are exciting new additions to theAlaskan tourism market. These new2011 additions will offset previouslyannounced reductions of 6% over2010 sailings.

Helping to offset these factors wasan improved capture rate and loweroperating costs. The capture rate ofcruise passengers to rail passengersincreased to 43.2% from 40.8% in2009. A decline of 5.1% in US dollaroperating costs helped to offset theoperating revenue decrease in 2010.

Two repowered locomotives wereadded to the fleet in 2010 with anadditional two being added in theSpring of 2011 bringing the totalrepowered locomotives in our fleetto six. Repowered locomotives reducefuel emissions by 90% and are alsosignificantly more efficient – tworepowered locomotives do the samework as three older locomotives, withsignificant savings in fuel and repairsand maintenance costs.

Consolidated EBITDA for 2010declined 1.0% to $63.6 million from$64.3 million in 2009 due to thedecline in the net operating incomefrom rail, tourism and port operationsin US dollars and a stronger Canadiandollar. These declines were offset byimproved operating results from thegolf club and resort operations.

Decreases in other categories suchas amortization, interest and otherexpense helped to improve netearnings to $11.8 million in 2010from $11.2 million in 2009. Earningsper share declined to 42 cents from44 cents in 2010.

Effective strategy and prudentmanagement has resulted in a numberof positive metrics over the last threeyears. The business combination in2009 which privatized ClubLinkCorporation has been a majorcontributor to improving ourresults since the end of 2007:

• Net earnings increased 93%;

• EPS increased 56%;

• Cash dividends per shareincreased 25%; and

• Debt to equity ratio declined 37%.

Overall, 2010 was a year in whichwe were able to capitalize oncertain opportunities in the Floridamarketplace to add value to our golfmembers and to you, our shareholders.As we expand in this marketplace andour strategy takes hold, we expect tosee the results of this strategy helpdrive the above metrics even more.

In closing, I would like to thank allour employees for their dedicationincluding a special thank you to thoseinvolved with the integration of ourFlorida acquisitions and our directorsfor their counsel and experience duringthese exciting times.

K. (Rai) SahiChairman & ChiefExecutive Officer

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

4

CLUBLINKESTABLISHESA FLORIDA REGION

In the fall of 2010, ClubLink established itsFlorida Region with the acquisition of fiveoperating 18-hole equivalent championshipgolf clubs and two academy golf clubs in SunCity Center, south of Tampa, and the 18-holeHeron Bay Golf Club in Coral Springs, adjacentto Fort Lauderdale.

The Florida Region represents an opportunityto establish a membership base underpinned byClubLink’s unique “one membership, more golf”business model which offers members reciprocalaccess to all of its golf clubs, as well ascapitalizing on the increasing number ofCanadians travelling to and buying secondhomes in Southern Florida.

To maximize this opportunity, our TravelLinkprogram was launched, which providesOntario/Quebec Region members with reciprocalaccess to ClubLink golf clubs in the Florida Region,and vice versa. The program offers a variety ofoptions, including one whereby members canjoin a “second home club” in another region,an attractive choice for Canadian snowbirds.

5

4

7

2

6

13

FLORIDA

Your Passport to

ACADEMY CLUB

SILVER MEMBER CLUB

GOLD MEMBER CLUB

HYBRID-PLATINUM CLUB

Championship AcademyFlag # Golf Holes Golf Holes

FLORIDA GOLF CLUBSHybrid-Platinum1 Club Renaissance, Sun City Center 18 –2 Heron Bay Golf Club, Coral Springs 18 –Gold3 Scepter Golf Club, Sun City Center 18 –Silver4 Falcon Watch Golf Club, Sun City Center 27 –5 Sandpiper Golf Club, Sun City Center 27 –Academy6 Caloosa Greens Golf Club, Sun City Center – 187 Kings Point Golf Club, Sun City Center – 18

more golf !

TAMPA

SARASOTA

MIAMI

FORT LAUDERDALE

ORLANDO

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

5

For six years (1997–2002), the PGA Tour’s Honda Classic called Heron Bay home, crowning champions StuartAppleby, Mark Calcavecchia, Vijay Singh, Dudley Hart, Jesper Parnevik and Matt Kuchar.

When the 7,268-yard course opened in 1996 as the TPC at Heron Bay, it was named one of America’s 10 best newpublic golf courses by Golf Digest. Golf Magazine ranks it one of the top 10 daily-fee courses in Florida. Designed by10-time PGA Tour winner Mark McCumber, it is home to the Heron Bay Golf Academy, an outstanding 40-acre practicefacility, and is the home course of the NHL’s Florida Panthers. Heron Bay also plays host to one of America’s oldest andmost prestigious amateur tournaments, the Dixie Amateur, whose fields have featured stars such as Tiger Woods andSergio Garcia.

Heron Bay Golf Club is adjacent to the Fort Lauderdale Marriott Coral Springs Hotel and Convention Center, providingan ideal venue for visiting golfers taking advantage of stay-and-play packages. ClubLink members receive preferredpricing when staying at the hotel.

2

HERON BAY GOLF CLUB

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

6

ClubLink’s initial foray into Florida was the acquisitionin September 2010 of the courses in Sun City Center,Florida approximately 50 kilometres (30 miles) southof Tampa. The operating championship golf clubs areClub Renaissance (18 holes), Sandpiper Golf Club (27holes), Scepter Golf Club (18 holes), and Falcon WatchGolf Club (27 holes). Two 18-hole academy (executive-length) clubs were also included: Kings Point Golf Cluband Caloosa Greens Golf Club. North Lakes Golf Club,which was closed in 2009, was also part of theportfolio, as was an undeveloped two-acre parcelof commercially zoned land.

The jewel in the Sun City Center crown is ClubRenaissance. The excellent 6,700-yard golf course,designed by Chip Powell in 2002, is complemented bya stunning 43,000 square-foot Mediterranean-inspiredclubhouse. Clubhouse amenities include a largeswimming pool and hot tub, full-service spa with fiveservice rooms, and a two-room wellness centre withthe latest in fitness equipment, personal training andexercise classes. There are two dining rooms, each of2,700 square feet, an 800 square-foot golf shop, andcovered patio.

Within the ClubLink family, Club Renaissance is a hybridgolf club, combining Platinum-level membership withpremium daily-fee golf.

1

CLUBLINK IN SUN CITY CENTERScepter Golf Club, a Chip Powell design that openedin 2005, is 6,717 yards in length. It features numerouswater hazards, strong bunkering and pushed-up greensites with roll-off collars and swales that demandaccurate approach shots. Scepter is a Gold-levelmember club.

Sandpiper Golf Club is comprised of three nine-holecourses, each with a par of 36: The Lakes (3,258yards), the Oaks (3,154 yards) and the Palms (3,170yards). The original 18 holes, designed by MarkMahanna, were built in 1968. Renowned Floridaarchitect Ron Garl designed the third nine in 1985.

Garl designed all three nines at Falcon Watch: Sands(par 36, 3,210 yards), Cypress (par 36, 3,265 yards),and Challenge (par 36, 3,280 yards). They opened in1981, 1984, and 1988, respectively.

Both Sandpiper and Falcon Watch are ClubLinkSilver-level clubs.

ClubLink members visiting Sun City Center receivepreferred pricing on accommodations at the nearbyResort and Club at Little Harbor.

Photos courtesy of The Greg Wilson Group

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

7

3

4

5

Photos courtesy of The Greg Wilson Group

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

8

GLENDALE JOINS CLUBLINK

On December 15th, ClubLink announced it had acquiredGlendale Golf and Country Club in Hamilton, Ontario.Glendale became ClubLink’s 23rd golf club in the GreaterToronto Area, and brought the Company’s total golf clubportfolio to 48.5 18-hole equivalent championship coursesand six 18-hole equivalent academy courses.

Glendale, founded in 1919, was one of the first private clubsin the Hamilton area. More than 500 of the club’s originalmembers volunteered over several months to build the course,which has had a vigorous and entertaining history. Forexample, found on the property is Smugglers Cave, abrick-lined cavern purported to be used by rumrunnersduring Prohibition.

Glendale has been the site of many important amateur andprofessional tournaments, including the 2001 Canadian PGAWomen’s Championship won by Lorie Kane in brilliantfashion, as she shot a final-round 63, a competitive courserecord that still stands today.

At 6,321 yards, the par-72 Glendale courseis not overly long by modern standards but thetree-lined fairways and elevation changes makeit a challenging experience for golfers of allabilities. Several holes on the front nine wereredesigned in 2005 by well-known Canadianarchitect Ian Andrew.

The classic clubhouse is home to a 300-seatbanquet facility in addition to the usual amenitiesand a six-sheet curling rink built in 1960.

Within the ClubLink family, Glendale iscategorized as a Gold-level Member Club.

Photos courtesy of Brent Long

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

9

Photos courtesy of Brent Long

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

10

Three new high-end luxury cruise lines — Disney, Crystaland Oceania — will be coming to Alaska and Skagwayin 2011, adding nearly 54,000 passengers, offsettingpreviously announced reductions by Holland Americaand Princess.

Disney will dramatically change the demographics of themarket by bringing over 40,000 passengers — many ofthem children — to Skagway aboard the Disney Wonder.As a result, White Pass will develop new product offeringsand marketing materials that are family-centric, interactiveand educational.

One of the key programs will be the exclusive youthactivity car available as an upgrade for families. This isan enhanced round trip Summit Excursion. Once arrivedat the Summit, kids will be escorted to their exclusiveactivity car for the southbound journey of sing alongs,I-Spy, activities and stories of the Klondike Gold Rush.On their private car, they’ll be joined by an exclusiveRailroader Guide. Meanwhile, the rest of the familywill enjoy a champagne toast and receive a souvenirmedallion, to welcome them into the “White PassSummit Club”.

YOUR PASSPORT TOMORE EXCITEMENT AT WHITE PASS

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

11

During the last week of April 2011, White Pass will hosta historic event: the clearing of the line with our historicrail equipment. Rotary Snowplow No. 1 built for WhitePass in 1898, by the Cooke Locomotive and MachineryCompany of Paterson, New Jersey, will head the RotaryFleet. Behind Rotary Snowplow No. 1 will be SteamEngine No. 73, a fully restored 1947 Baldwin 2-8-2Mikado Class steam locomotive joined by No. 69,a Baldwin 2-8-0 built for White Pass in 1907.

Media, railfans, and other guests will travel behindthe Rotary Fleet on a chase train consisting of diesellocomotives and comfortable, vintage passengercoaches. Throughout the adventure, passengers willhave the opportunity to disembark their train, wheresafety allows, to capture the Rotary Snowplow hard atwork, a view rarely seen by anyone but our locomotiveengineers and our maintenance-of-way workers. TheRotary Snowplow with its 10 huge blades pushes andclears heavy winter snow accumulations of up to 12 feetsending the snow flying out to the side of the tracks bycentrifugal force in spectacular fashion.

159

7

16

17

813

146 5

23

18

3235

34

1

12

34

2

39

38

37

36

10

11

26

24

20

30

2831

29

21

27

22

33

19

25

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

12

DAILY FEE CLUB

RESORT

SILVER MEMBER OR HYBRID CLUB

GOLD MEMBER OR HYBRID CLUB

PLATINUM MEMBER CLUB

PRESTIGE MEMBER OR HYBRID CLUB

TORONTO LAKE ONTARIO

LAKE ERIE

LONDON

MONTREAL

MONT TREMBLANT

Q U E B E C

O N T A R I O

OTTAWA

PICKERING

HUNTSVILLE

GEORGIAN BAY

Map of Canadian Golf Club and Resort Locations

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

13

Championship Academy Future Current SurplusGolf Holes Golf Holes Golf Holes Rooms Land in Acres

ONTARIO/QUEBEC REGION (see map on page 12)Prestige

1 Greystone Golf Club, Milton, Ontario 18 – – – –2 King Valley Golf Club, The Township of King, Ontario 18 – – – –3 RattleSnake Point Golf Club, Milton, Ontario 36 9 – – –

Hybrid – Prestige4 Glen Abbey Golf Club, Oakville 18 – – – –

Platinum5 Club de Golf Islesmere, Laval, Quebec (a) 27 – – – –6 Club de Golf Le Fontainebleau, Blainville, Quebec 18 – – – –7 DiamondBack Golf Club, Richmond Hill, Ontario 18 – – – –8 Eagle Creek Golf Club, Dunrobin, Ontario 18 – – – –9 Emerald Hills Golf Club, Whitchurch-Stouffville, Ontario 27 – – – –10 Glencairn Golf Club, Milton, Ontario 27 – – – –11 Grandview Golf Club, Huntsville, Ontario 18 – 18 – –12 Heron Point Golf Links, Ancaster, Ontario 18 – – – –13 Kanata Golf & Country Club, Kanata, Ontario 18 – – – –14 Le Maitre de Mont-Tremblant, Mont-Tremblant, Quebec 18 – – – –15 King’s Riding Golf Club, The Township of King, Ontario 18 – – – –16 Rocky Crest Golf Club, Mactier, Ontario 18 – 18 – –17 The Lake Joseph Club, Port Carling, Ontario 18 9 – – –18 Wyndance Golf Club, Uxbridge, Ontario 18 9 – – –

Gold19 Blue Springs Golf Club, Acton, Ontario 18 9 – – –20 Caledon Woods Golf Club, Bolton, Ontario 18 – – – –21 Cherry Downs Golf & Country Club, Pickering, Ontario 18 9 18 – –22 Club de Golf Hautes Plaines, Gatineau, Quebec 18 – – – –23 Club de Golf Val des Lacs, Ste. Sophie, Quebec 18 – – – –24 Eagle Ridge Golf Club, Georgetown, Ontario 18 – – – –25 Glendale Golf and Country Club, Hamilton, Ontario 18 – – – –26 Greenhills Golf Club, London, Ontario (a) 18 9 – – –27 GreyHawk Golf Club, Ottawa, Ontario 36 – – – –28 National Pines, Innisfil, Ontario (a) 18 – – – –29 Station Creek Golf Club, Whitchurch-Stouffville, Ontario 36 – – – –30 The Country Club, Woodbridge, Ontario (a) 36 9 – – –

Hybrid – Gold31 The Club at Bond Head (a) 36 – – – –

Hybrid – Silver32 Bethesda Grange, Whitchurch-Stouffville, Ontario 18 – – – –33 Highland Gate Golf Club, Aurora, Ontario 18 – – – –

Daily Fee34 Grandview Inn Course, Huntsville, Ontario – 9 – – –35 Rolling Hills Golf Club, Whitchurch-Stouffville, Ontario 36 – – – –

MUSKOKA, ONTARIO RESORTS36 Delta Grandview Resort, Huntsville, Ontario – – – 151 –37 The Lake Joseph Club, Port Carling, Ontario – – – 251 –38 Delta Rocky Crest Resort/Lakeside at Rocky Crest, Mactier (b) – – – 84 –39 Delta Sherwood Inn, Port Carling, Ontario – – – 49 –

OTHERLake Chesdin Golf Club, Richmond, Virginia 18 – 18 – –King Haven, The Township of King – – – – 278Harwood, Montreal – – 36 – –

FLORIDA REGION (see map on page 4)Hybrid – Platinum

1 Club Renaissance, Sun City Center, Florida 18 – – – –2 Heron Bay Golf Club, Coral Springs, Florida 18 – – – –

Gold3 Scepter Golf Club, Sun City Center, Florida 18 – – – –

Silver4 Falcon Watch Golf Club, Sun City Center, Florida 27 – – – –5 Sandpiper Golf Club, Sun City Center, Florida 27 – – – –

Other6 Caloosa Greens Golf Club, Sun City Center, Florida – 18 – – 27 Kings Point Golf Club, Sun City Center, Florida – 18 – – –North Lakes Golf Club, Sun City Center, Florida (c) – – 18 – –

Total 18-hole Equivalent Courses, Rooms, Acres 48.5 6.0 7.0 309 280Notes:

(a) Operated by ClubLink under long-term leases.

(b) Delta Rocky Crest Resort consists of 65 units and Lakeside at Rocky Crest consists of 19 units.

(c) North Lakes Golf Club was closed by the previous owner. Management is reviewing alternatives for this facility.

GOLF CLUB AND RESORT PROPERTY LISTING

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

14

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

This management’s discussion and analysis of financial condition and results of operations (“MD&A”) should be read in conjunction withClubLink Enterprises Limited’s (“ClubLink” or the “Company”) audited consolidated financial statements and accompanying notes for theyear ended December 31, 2010. This MD&A has been prepared as at March 1, 2011 and all amounts are in Canadian dollars unless otherwiseindicated. In this document, unless otherwise indicated, all financial data are prepared in accordance with Canadian Generally AcceptedAccounting Principles (“GAAP”).

Forward-Looking Statements

This annual report contains certain forward-looking information and statements relating but not limited to, operations, anticipated orprospective financial performance, results of operations, business prospects and strategies of ClubLink. Forward-looking information typicallycontains statements with words such as “consider”, “anticipate”, “believe”, “expect”, “plan”, “intend”, “may”, “likely”, or similar wordssuggesting future outcomes or statements regarding an outlook, or other expectations, beliefs, plans, objectives, assumptions, intentions orstatements about future events or performance. Readers should be aware that these statements are subject to known and unknown risks,uncertainties and other factors that could cause actual results, performance or achievements of ClubLink to differ materially from thosesuggested by the forward-looking statements, some of which may be beyond the control of management.

Although ClubLink believes it has a reasonable basis for making the forecasts or projections included in this MD&A, readers are cautionednot to place undue reliance on such forward-looking information. By its nature, ClubLink’s forward-looking information involves numerousassumptions, inherent risks and uncertainties, both general and specific, that contribute to the possibility that the predictions, forecasts andother forward-looking statements will not occur. These factors include, but are not limited to, availability of credit, weather conditions, theeconomic environment, environmental regulation and competition.

The above list of important factors affecting forward-looking information is not exhaustive, and reference should be made to the other risksdiscussed in ClubLink’s filings with Canadian securities regulatory authorities. ClubLink undertakes no obligation, except as required by law,to update publicly or otherwise any forward-looking information, whether as a result of new information, future events or otherwise, or theabove list of factors affecting this information.

Business Strategy and Corporate Overview

The Company has a strategic objective to maximize shareholder value over a five to ten year horizon, though the Company may monetizean investment when business conditions present a suitable opportunity. The Company acquired its increasing share interest in ClubLinkCorporation from 2001 through July 2009 – with control being acquired and full consolidation commencing on June 1, 2007. ClubLinkCorporation became a wholly-owned subsidiary on July 28, 2009.

The privatization of ClubLink Corporation on July 28, 2009 has provided a stable environment to allow for continued growth and enhancedprofitability from golf club and resort operations. An experienced management team and a strategic focus which offers customers a widevariety of high quality facilities and flexible membership programs has resulted in ClubLink Corporation establishing itself as the golfindustry leader in Canada. Operating synergies and continued cost reduction through economies of scale will improve operating performanceand financial returns.

Management has been actively looking at acquisition opportunities in southern Florida. The Company made two acquisitions in late 2010.The first acquisition involved a portfolio of six 18-hole equivalent championship and two 18-hole academy golf courses in Sun City Center,Florida. The second investment was the purchase of Heron Bay Golf Club in the Fort Lauderdale area. These investments created ClubLink’sfirst region outside of Ontario and Quebec.

ClubLink’s continued investment in programs to build the core operating business at White Pass & Yukon Route (“White Pass”) has historicallybeen the Company’s key to profitability. As a standalone entity, White Pass has an experienced on-site management team and has been ableto generate growth in the passenger traffic and corresponding U.S. dollar revenue since acquisition in 1997. Significant initiatives in thisbusiness segment have included capitalizing on historical relationships with cruise lines, supporting investments to create one of the leadingport facilities in southeast Alaska, investing to repower our locomotive fleet to reduce environmental emissions and ongoing operating costsand continuing to offer Alaska’s premier shore excursion experience to the travelling public.

Overview of Business Segments

ClubLink operates in two distinct business segments: (a) golf club and resort operations and (b) rail, tourism and port operations. In addition,the corporate operations segment oversees the two business segments.

Clublink_AR2010_pgs14-72_v2.3.qxd:AR 2010 4/4/11 10:08 AM Page 14

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

15

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

Overview of Business Segments (cont’d)

The quarterly earnings performance of the Company reflects the highly seasonal nature of both business segments. The majority of operatingrevenue and net operating income from these businesses occur during the second and third quarters of the year. Accordingly, the quarterlyreported net earnings of the Company will fluctuate with those of the underlying business segments. This seasonality will be mitigatedsomewhat by ClubLink’s recent expansion into the Florida marketplace, as the primary golf season in Florida is from November to April.

Golf Club and Resort Operations Segment

ClubLink is engaged in golf club and resort operations under the trademark “ClubLink One Membership More Golf ”. ClubLink is Canada’slargest owner and operator of golf clubs with 48.5, 18-hole equivalent championship and six 18-hole equivalent academy courses, at 41locations primarily in Ontario, Quebec and Florida.

ClubLink’s golf clubs are strategically organized in clusters that are located in densely populated metropolitan areas and resort destinationsfrequented by those who live and work in these areas. By operating in these areas, ClubLink is able to offer golfers a wide variety of uniquemembership, corporate event and resort opportunities. ClubLink is also able to obtain the benefit of operating synergies to maximize revenueand achieve economies of scale to reduce costs.

Revenue at all golf club and resort properties is enhanced by cross-marketing, as the demographics of target markets for each are substantiallysimilar. Revenue is further improved by corporate golf events, business meetings and social events that utilize golf capacity and relatedfacilities at times that are not in high demand by ClubLink’s members.

Member and Hybrid Golf Club revenue is maximized by the sale of flexible personal and corporate memberships that offer reciprocalplaying privileges at ClubLink golf clubs and, on payment of an additional fee, inter-regional play within ClubLink and ClubCorp ofAmerica golf clubs. Daily fee golf club revenue is maximized through unique and innovative marketing programs. Resort revenue ismaximized by the integration of high quality golf facilities, which are recognized throughout the leisure industry as the key amenity forsuccessfully attracting corporate groups and leisure guests.

(a) Canada

ClubLink’s Ontario/Quebec Region is organized into two clusters: the major metropolitan areas of Southern Ontario and Muskoka,Ontario’s premier resort area, extending from London to Huntsville to Pickering, with a particularly strong presence in the Greater TorontoArea; and Quebec/Eastern Ontario, extending from the National Capital Region to Montreal, including Mont-Tremblant, Quebec’s premierresort area.

In 2011, ClubLink will operate 29 Ontario/Quebec Region Member Golf Clubs in three categories as follows:

Prestige: Greystone, King Valley, RattleSnake Point

Platinum: DiamondBack, Eagle Creek, Emerald Hills, Fontainebleau, Glencairn, Grandview, Heron Point, Islesmere,Kanata, King’s Riding, Lake Joseph, Le Maitre, Rocky Crest, Wyndance

Gold: Blue Springs, Caledon Woods, Cherry Downs, Country Club, Eagle Ridge, Glendale, Greenhills, GreyHawk,Hautes Plaines, National Pines, Station Creek, Val des Lacs

On December 15, 2010, ClubLink announced the acquisition of Glendale Golf and Country Club in Hamilton, Ontario. Glendale is the23rd golf club in the Greater Toronto Area. It was founded in 1919 and was one of the first private golf clubs in the Hamilton area. Glendalewill operate as a Gold Member Golf Club. ClubLink has committed to $1,500,000 in capital upgrades over three years for cart paths,bunkers, a practice facility and clubhouse improvements.

In 2011, ClubLink will operate four Ontario/Quebec Region Hybrid Golf Clubs in three categories as follows:

Hybrid – Prestige: Glen Abbey

Hybrid – Gold: The Club at Bond Head

Hybrid – Silver: Bethesda Grange, Highland Gate

Hybrid Golf Clubs are available for daily fee (public) play, reciprocal access by Members and provide a home club for Members withreciprocal access to the ClubLink system.

On June 10, 2010, ClubLink announced the conversion of the 18-hole championship daily fee golf course at Rolling Hills into a Hybrid –Silver Golf Club named Bethesda Grange. Golf course upgrades commenced in 2010, as part of this conversion, are expected to becompleted by the end of 2011.

Clublink_AR2010_pgs14-72_v2.3.qxd:AR 2010 4/4/11 10:08 AM Page 15

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

16

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

Overview of Business Segments (cont’d)

Golf Club and Resort Operations Segment (cont’d)

(a) Canada (cont’d)

In 2011, ClubLink will operate two Ontario/Quebec Region Daily Fee Golf Clubs as follows:

Daily Fee: Grandview Inn, Rolling Hills

ClubLink owns sufficient land to develop an additional 18 holes at Cherry Downs Golf Club in Pickering, Grandview Golf Club in Muskokaand Rocky Crest Golf Club in Muskoka and sufficient land in the Greater Montreal Area to develop a 36-hole golf club.

In 2011, ClubLink will operate The Lake Joseph Club while Delta Hotels and Resort (“Delta”) will manage Delta Grandview Resort, DeltaRocky Crest Resort and Delta Sherwood Inn on ClubLink’s behalf.

The Lake Joseph Club and Delta Rocky Crest Resort operate seasonally from May to October. Delta Sherwood Inn has undergonerenovations after the resort was damaged by a fire and closed in September 2009 and was reopened in June 2010. Delta Grandview Resortoperates year round. Delta’s responsibilities include management of rooms, recreation programs and food and beverage outlets. This includesthe management of food and beverage operations at Rocky Crest and Grandview Golf Clubs, while ClubLink remains responsible formanagement of the golf operations at these properties.

Delta’s sales and marketing efforts for ClubLink’s Muskoka Resorts are focused on increasing corporate clientele through direct mail programs,telemarketing campaigns, e-commerce promotions and cross promotions to all ClubLink, ClubCorp, Toronto Board of Trade and DeltaPrivilege Members.

ClubLink’s remaining Muskoka land holdings, excluding golf course development sites, include zoned and serviced land that are capable ofsupporting a substantial number of resort rooms/villas, conference facilities and residential homes.

(b) United States

ClubLink’s golf clubs in the United States consist of a Florida Region and the Lake Chesdin Golf Club, located near Richmond, Virginia.The Florida Region includes six 18-hole equivalent championship and two 18-hole equivalent academy golf courses.

On September 3, 2010, ClubLink acquired eight 18-hole golf courses in Sun City Center, Florida for US $8,700,000. The operatingchampionship golf courses are Club Renaissance (18 holes), Sandpiper Golf Course (27 holes), Scepter Golf Club (18 holes), and Falcon WatchGolf Club (27 holes). Two 18-hole academy courses are also included: Kings Point Golf Club and Caloosa Greens Golf Club. North Lakes GolfClub, which was closed in 2009 and remains closed, is also part of the portfolio, as is an undeveloped two-acre parcel of commercially zonedland. The golf courses, about 50 kilometres (30 miles) south of Tampa, range from a full-service country club to academy courses.

On October 21, 2010, ClubLink acquired Heron Bay Golf Club in Coral Springs, Florida, 30 minutes from downtown Fort Lauderdale, forUS $2,900,000. From 1997 to 2002, Heron Bay hosted the PGA Tour’s Honda Classic, crowning champions Stuart Appleby, MarkCalcavecchia, Vijay Singh, Dudley Hart, Jesper Parnevik and Matt Kuchar.

For the 2011 operating season, ClubLink will operate five Florida Region Golf Clubs in three categories as follows:

Hybrid – Platinum: Club Renaissance, Heron Bay

Gold: Scepter

Silver: Falcon Watch, Sandpiper

These investments created ClubLink’s first region outside of Ontario and Quebec.

Under GAAP the results of the United States golf clubs are considered integrated and their monetary assets/liabilities and earnings aretranslated into Canadian currency using average exchange rates during the period. Non-monetary assets/liabilities are translated usinghistorical exchange rates. Changes in average exchange rates will impact the net earnings of the Company.

(c) TravelLink

The TravelLink program offers three levels that allow ClubLink members inter-regional access. The first level provides all ClubLink membersinter-regional access with preferred pricing. Levels 2 and 3 are optional and provide ClubLink members greater inter-regional access for fixedannual fees.

Clublink_AR2010_pgs14-72_v2.3.qxd:AR 2010 4/4/11 10:08 AM Page 16

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

17

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

Overview of Business Segments (cont’d)

Rail, Tourism and Port Operations Segment

ClubLink is also engaged in rail, tourism and port operations based in Skagway, Alaska which operate under the trade name of “White Pass& Yukon Route”. This includes a tourist railway stretching approximately 177 kilometres (110 miles) from Skagway, Alaska through BritishColumbia to Whitehorse, Yukon. Presently, approximately 110 kilometres (67.5 miles) of the railway is in active service.

The railway was constructed by White Pass during the Klondike Gold Rush of 1898/1899 and completed in 1900. From 1900 until 1982,it was used for the carriage of general freight, ore concentrates, petroleum products and passengers. Railway operations were suspended in1982 when a major ore concentrate customer shut down its mine. The South Klondike Highway between Whitehorse and Skagway,subsequently constructed in 1985, transferred the transportation of ore concentrates from rail to road service. The railway reopened in 1988and has since been operating as a seasonal passenger tourism railway. ClubLink acquired White Pass in 1997.

White Pass operates three docks in Skagway, which provide four berths for cruise ships operating west coast schedules throughout the Mayto September tourist season. The largest of the three docks, with two berths, is owned while the two remaining docks are situated on stateand city property and operate under long-term tideland leases.

The primary market is the cruise industry, which recognizes Skagway as a marquee port for its Alaskan cruises. White Pass maintains asymbiotic relationship with the cruise lines – carrying almost half of all cruise passengers – making it Alaska’s premier shore excursion anda high volume, highly rated and profitable shore excursion for the cruise lines. The relationship is supported with an existing incentiveprogram and extensive cooperative pre-cruise and on-board promotion. White Pass also markets to motorcoach tour companies andindependent travellers who arrive via ferry and the South Klondike Highway.

Under GAAP, the results of White Pass are self-sustaining and its US operations are translated into Canadian currency using averageexchange rates during the period. Changes in average exchange rates will impact the net earnings of the Company.

Corporate Operations Segment

ClubLink’s objective at the corporate level is to identify opportunities to generate incremental returns and cash flow. Historically, the natureof these investments included debt and equity instruments in both public and private organizations. Currently, management is focused onimproving the returns of both operating business segments.

Business Combination

On July 28, 2009, the Company acquired the remaining 28.1% common share interest in ClubLink Corporation that it did not already own.

ClubLink issued 1.1 common shares for each common share of ClubLink Corporation acquired, resulting in the issuance of 5,164,015common shares of the Company. The ClubLink common shares issued were valued at $44,669,000, based on an independent third partyvaluation. In addition, the Company incurred $951,000 of transaction costs which have been included in the cost of the purchase. Theacquisition has been accounted for under the purchase method of accounting. Accordingly, the Company allocated the purchase price to theidentifiable assets and liabilities acquired based on their estimated fair values at the time of acquisition. The operations of ClubLinkCorporation have been included in the consolidated statements of earnings and comprehensive earnings and cash flows on a 100% basis sinceJuly 28, 2009.

As part of the accounting treatment for this transaction, the Company allocated the purchase price to the identifiable assets and liabilitiesof the acquisition which resulted in an increase to intangible assets of $14,857,000 and a decrease to capital assets in the amount of$14,700,000.

Selected Financial Information

The table below sets forth selected financial data relating to the Company’s fiscal years ended December 31, 2010, December 31, 2009 andDecember 31, 2008. This financial data is derived from the Company’s audited consolidated financial statements, which are prepared inaccordance with GAAP.

For the Years Ended December 31, % Change % Change(thousands of dollars, except per share amounts) 2010 2009 2008 2010/2009 2009/2008

CHAMPIONSHIP GOLF ROUNDS 1,122,000 1,031,000 988,000 8.8% 4.4%

RAIL PASSENGERS 368,000 396,000 438,000 -7.1% -9.6%

PORT PASSENGERS 697,000 781,000 779,000 -10.8% 0.3%

OPERATING REVENUE $ 189,903 $ 190,212 $ 196,532 -0.2% -3.2%COST OF SALES AND OPERATING EXPENSES 140,045 138,775 141,497 0.9% -1.9%

NET OPERATING INCOME 49,858 51,437 55,035 -3.1% -6.5%

Operating margin (%) 26.3% 27.0% 28.0% -2.6% -3.6%

Amortization of membership fees 15,292 14,784 13,965 3.4% 5.9%Direct costs of originating membership fees 1,511 1,955 1,638 -22.7% 19.4%

NET MEMBERSHIP FEE INCOME 13,781 12,829 12,327 7.4% 4.1%

Earnings before other items, income taxes andnon-controlling interest (EBITDA) 63,639 64,266 67,362 -1.0% -4.6%

Amortization of capital and intangible assets (20,789) (21,533) (20,774) -3.5% 3.7%

Land lease rent (5,285) (5,024) (4,182) 5.2% 20.1%

Interest, net (22,108) (23,397) (25,283) -5.5% -7.5%

Other income (expense) 344 (1,807) (292) N/A N/A

Current income taxes recovery (provision) 1,811 (5,313) (6,432) N/A N/A

Future income taxes recovery (provision) (5,770) 3,311 (3,276) N/A N/ANon-controlling interest – 652 (998) N/A N/A

NET EARNINGS $ 11,842 $ 11,155 $ 6,125 6.2% 82.1%

WEIGHTED AVERAGE SHARES OUTSTANDING (000) 27,976 25,113 22,887 11.4% 9.7%

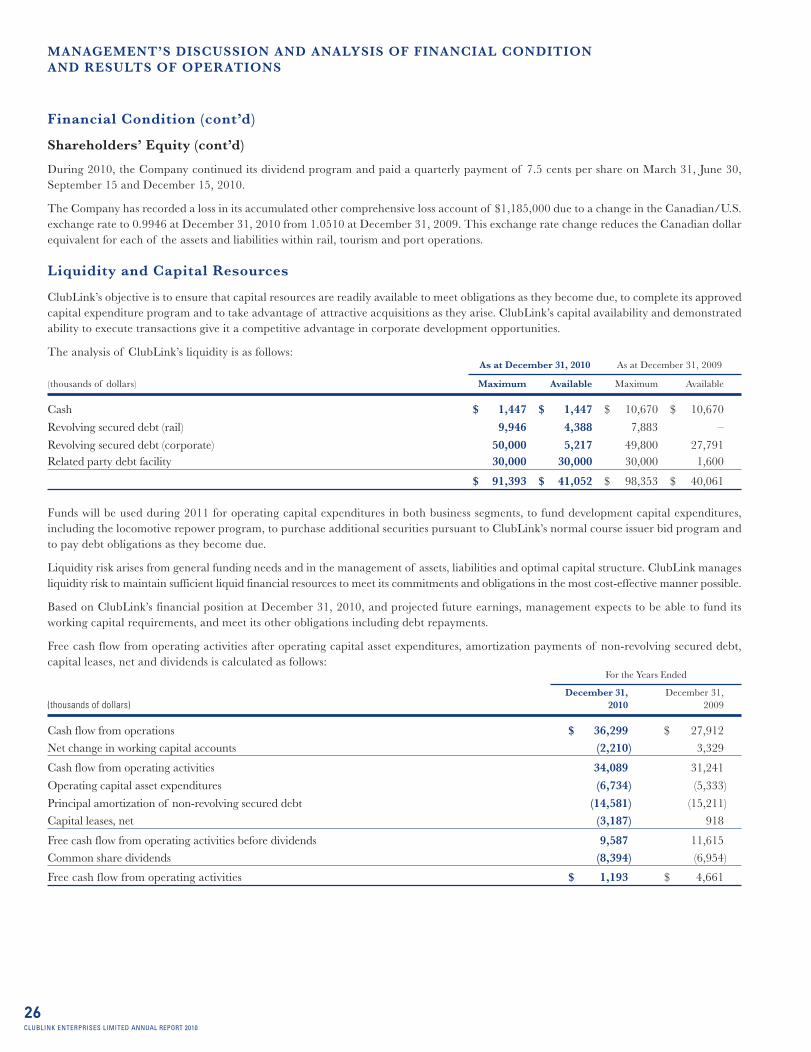

BASIC AND DILUTED EARNINGS PER SHARE $ 0.42 $ 0.44 $ 0.27 -4.5% 63.0%

CASH FLOW FROM OPERATIONS $ 36,299 $ 27,912 $ 35,516 30.0% -21.4%

BASIC AND DILUTED CASH FLOW FROMOPERATIONS PER SHARE $ 1.30 $ 1.11 $ 1.55 17.1% -28.4%

TOTAL ASSETS $ 611,412 $ 627,753 $ 641,300 -2.6% -2.1%

TOTAL LIABILITIES $ 455,615 $ 473,193 $ 484,729 -3.7% -2.4%

ELIGIBLE CASH DIVIDENDS PER SHARE $ 0.30 $ 0.27 $ 0.24 11.1% 12.5%

Summary of Canadian/U.S. Exchange Rates Used for Translation Purposes

The following exchange rates translate one U.S. dollar into the Canadian dollar equivalent.

2010 2009 2008

Balance Sheet, at December 31 0.9946 1.0510 1.2217

Statement of Earnings, average for the years ended December 31 1.0299 1.1326 1.0678

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

18CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

Clublink_AR2010_pgs14-72_v2.3.qxd:AR 2010 4/4/11 10:08 AM Page 18

2010 Consolidated Operating Highlights

Consolidated operating revenue decreased 0.2% to $189,903,000 for the year ended December 31, 2010 from $190,212,000 in 2009 primarilydue to a decline in the rail, tourism and port operations revenue. The operating revenue from this segment has declined due to: (i) a 10.8%decline in port passengers; (ii) a 7.1% decline in rail passengers and (iii) a stronger Canadian dollar per US dollar (1.0299 compared to1.1326 in 2009). This decrease was offset by revenue generated by ClubLink’s expansion into the Florida golf marketplace and improvedCanadian golf club and resort operations. Consolidated operating revenue decreased 3.2% to $190,212,000 in 2009 from $196,532,000 in2008 due to a decline in golf club and resort operations revenue resulting from reduced discretionary spending during the 2009 recession.

Championship golf rounds increased 8.8% to 1,122,000 championship rounds from 1,031,000 championship rounds in 2009, including58,000 rounds from our US golf clubs, including the Florida golf clubs acquired late in 2010. This compares to 988,000 championshiprounds in 2008.

Port passengers from cruise ships decreased 10.8% to 697,000 from 781,000 in 2009. The decline in cruise ship visits was a reaction to thehead tax imposed by the State of Alaska. Port passengers in 2008 amounted to 779,000. Rail passengers declined 7.1% to 368,000 in 2010from 396,000 in 2009. The number of rail passengers decreased 9.6% to 396,000 in 2009 from 438,000 in 2008 due primarily to two separateinterruptions in rail service.

Consolidated cost of sales and operating expenses increased 0.9% to $140,045,000 in 2010 from $138,775,000 in 2009 due to additionaloperating costs incurred relating to the Company’s expansion into Florida offset by a stronger Canadian dollar used to convert costs fromrail, tourism and port operations. The cost of sales and operating expenses in 2008 amounted to $141,497,000.

Net membership fee income increased 7.4% to $13,781,000 from $12,829,000 in 2009 primarily due to a 2.1% increase in Canadianmembers and a 22.7% decrease in direct costs of originating membership fees. This compares to $12,327,000 in 2008.

Consolidated EBITDA decreased 1.0% for the year ended December 31, 2010 to $63,639,000 from $64,266,000 in 2009. This decrease isdue primarily to the decline in rail, tourism and port operations EBITDA and a stronger Canadian dollar. Consolidated EBITDA declinedfrom $67,362,000 in 2008 due to the decline in discretionary spending in golf club and resort operations during the 2009 recession.

Amortization of capital and intangible assets decreased 3.5% to $20,789,000 for the year ended December 31, 2010 from $21,533,000 in2009 and compares to $20,774,000 in 2008.

Land lease rent increased 5.2% to $5,285,000 for the year ended December 31, 2010 from $5,024,000 in 2009 due to a full year of rent forThe Club at Bond Head, which became a ClubLink property on April 7, 2009. Land lease rent for 2008 was $4,182,000.

Interest, net decreased 5.5% to $22,108,000 for the year ended December 31, 2010 from $23,397,000 in 2009. This reduction was causedby a 4.2% decline in debt levels, a stronger Canadian dollar and a lower average borrowing rate in 2010. Interest, net has decreased from$25,283,000 in 2008.

Other expense changed to income of $344,000 in 2010 from an expense of $1,807,000 in 2009 primarily due to costs incurred in 2009relating to the golf club and resort operations property tax appeal process. A total of $873,000 (2009 – nil) in business combination transactioncosts have been charged to other expense during the year in conjunction with the change in GAAP requiring business combination transactioncosts to be expensed.

The overall effective tax rate for 2010 was 25.1% as compared to 16.0% in 2009. This increase was due to a future income tax recovery of$3,483,000 from previous unrecognized operating losses in 2009. This compares to an effective tax rate of 57.7% in 2008 which was higherthan the statutory tax rate due to unrecognized operating losses in that year.

Consolidated net earnings increased to $11,842,000 for the year ended December 31, 2010 from $11,155,000 in 2009 primarily due to thedecline in interest, net and other expense and compares to $6,125,000 in 2008.

Weighted average shares for the year ending December 31, 2010 increased to 27,976,000 as compared to 25,113,000 in 2009 primarily dueto the 5,164,015 common shares issued by the Company on July 28, 2009 as part of the business combination with ClubLink Corporation.Weighted average shares for the year ending December 31, 2008 was 22,887,000.

Earnings per share decreased to 42 cents per share in 2010, compared to 44 cents per share in 2009 and 27 cents per share in 2008.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

19CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

Clublink_AR2010_pgs14-72_v2.3.qxd:AR 2010 4/4/11 10:08 AM Page 19

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

20

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

Results of Operations by Business Segment

The review of operations by business segment should be read in conjunction with the segmented information contained in note 17 of theaudited consolidated financial statements for the year ended December 31, 2010.

The following is a summary of the results of operations.For the Years Ended

December 31, December 31, %(thousands of dollars) 2010 2009 Change

Operating revenue by segment

Golf club and resort operations $ 153,366 $ 147,414 4.0%Rail, tourism and port operations 36,537 42,798 -14.6%

$ 189,903 $ 190,212 -0.2%

Net operating income by segment

Golf club and resort operations $ 35,247 $ 32,586 8.2%

Rail, tourism and port operations 17,270 20,577 -16.1%Corporate operations (2,659) (1,726) -54.1%

49,858 51,437 -3.1%

Net membership fee incomeGolf club and resort operations 13,781 12,829 7.4%

EBITDA $ 63,639 $ 64,266 -1.0%

Review of Golf Club and Resort Operations for the Year Ended December 31, 2010

On April 7, 2009, ClubLink entered into a long-term 21 golf-season lease for The Club at Bond Head. Bond Head, just west of Highway400, north of Toronto, consists of two superb 18-hole championship courses designed by the renowned architectural firm of Hurdzan Fry.Bond Head operated as a Premium Daily Fee facility in 2009. In June 2009, ClubLink announced that it was selling Gold Level Membershipsto Bond Head commencing in 2010 with interim playing privileges in 2009. In 2010, Bond Head operated as a Hybrid – Gold Golf Clubavailable for daily fee (public) play, reciprocal access by members and provided a home club for Bond Head members with reciprocal access.

ClubLink announced on September 3, 2010 that it had acquired eight 18-hole golf courses in Sun City Center, Florida for US $8,700,000. Theoperating championship golf courses are Club Renaissance (18 holes), Sandpiper Golf Course (27 holes), Scepter Golf Club (18 holes), andFalcon Watch Golf Club (27 holes). Two 18-hole academy courses are also included: Kings Point Golf Club and Caloosa Greens Golf Club. NorthLakes Golf Club, which was closed in 2009 and remains closed, is also part of the portfolio, as is an undeveloped two-acre parcel of commerciallyzoned land. The courses, about 50 kilometres (30 miles) south of Tampa, range from a full-service country club to academy courses.

ClubLink announced on October 21, 2010 that it had acquired Heron Bay Golf Club in Coral Springs, Florida, 30 minutes from downtownFort Lauderdale, for US $2,900,000. From 1997 to 2002, Heron Bay hosted the PGA Tour’s Honda Classic, crowning champions StuartAppleby, Mark Calcavecchia, Vijay Singh, Dudley Hart, Jesper Parnevik and Matt Kuchar.

The Sun City and Heron Bay acquisitions created ClubLink’s first region outside of Ontario and Quebec.

On December 15, 2010, ClubLink announced the acquisition of Glendale Golf and Country Club in Hamilton, Ontario. Glendale is the 23rd golfclub in the Greater Toronto Area. It was founded in 1919 and was one of the first private golf clubs in the Hamilton area. Glendale will operate as aGold Member Golf Club. ClubLink has committed to $1,500,000 in capital upgrades over 3 years for cart paths, bunkers, a practice facility andclubhouse improvements.

Summary of Golf Club and Resort OperationsFor the Years Ended

December 31, December 31, %(thousands of dollars) 2010 2009 Change

Operating revenue $ 153,366 $ 147,414 4.0%Operating costs (118,119) (114,828) 2.9%

Net operating income 35,247 32,586 8.2%

Operating margin % 23.0% 22.1% 4.1%

Amortization of membership fees 15,292 14,784 3.4%Direct costs of originating membership fees (1,511) (1,955) -22.7%

Net membership fee income 13,781 12,829 7.4%

EBITDA $ 49,028 $ 45,415 8.0%

Clublink_AR2010_pgs14-72_v2.3.qxd:AR 2010 4/4/11 10:08 AM Page 20

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

21

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

Results of Operations by Business Segment (cont’d)

Review of Golf Club and Resort Operations for the Year Ended December 31, 2010 (cont’d)

Golf Club and Resort Operating Revenue

Golf club and resort operating revenue is recorded as follows:For the Years Ended

December 31, December 31, %(thousands of dollars) 2010 2009 Change

Annual dues $ 60,678 $ 57,710 5.1%

Corporate events, guest fees and cart rentals 36,050 35,262 2.2%

Food and beverage 42,370 40,167 5.5%

Resort rooms 3,260 3,361 -3.0%

Merchandise and other 11,008 10,914 0.9%

Total operating revenue $ 153,366 $ 147,414 4.0%

Championship golf rounds increased 8.8% to 1,122,000 championship rounds from 1,031,000 championship rounds in 2009, including58,000 championship rounds from our US golf clubs, including the Florida golf clubs acquired late in 2010.

Total operating revenue increased 4.0% to $153,366,000 from $147,414,000 in 2009 primarily due to operating revenue from the Floridagolf clubs acquired late in 2010. This resulted in increases in all areas with the exception of resort rooms.

Resort occupancy levels were 45.1% in 2010 compared to 44.2% in 2009 and operating revenue per available room increased to $159 from$142 in 2009. Resort room revenue declined 3.0% due to the closure of Delta Sherwood Inn from September 2009 to June 2010 as a resultof a fire.

Golf Club and Resort Operating Costs

Golf club and resort operating costs are recorded as follows:

For the Years Ended

December 31, December 31, %(thousands of dollars) 2010 2009 Change

Cost of sales $ 20,363 $ 20,266 0.5%

Labour 54,526 52,118 4.6%

Direct operating costs 20,555 19,312 6.4%

Insurance 1,859 1,331 39.7%

Utilities 7,367 6,908 6.6%

Property taxes 5,186 5,017 3.4%

Sales and marketing 2,361 2,075 13.8%

Administration and provincial capital taxes 5,902 7,801 -24.3%

Total operating costs $ 118,119 $ 114,828 2.9%

Gross margin on food and beverage sales was 68.1% in 2010 compared to 68.3% in 2009.

Gross margin on merchandise sales was 26.0% in 2010 compared to 22.3% in 2009. This increase is due to a change in mix of sales, focusingon higher margin items.

Increases in all operating cost categories are primarily due to the addition of the Florida golf clubs late in 2010.

Administration and provincial capital taxes have decreased 24.3% to $5,902,000 in 2010 from $7,801,000 in 2009 due to (a) a decline inadministrative costs from the business combination and privatization of ClubLink Corporation, (b) a decline in both Ontario and Quebeccapital tax rates and (c) the transfer of certain head office costs from golf club and resort operations to corporate operations.

Clublink_AR2010_pgs14-72_v2.3.qxd:AR 2010 4/4/11 10:08 AM Page 21

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

22

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

Results of Operations by Business Segment (cont’d)

Review of Golf Club and Resort Operations for the Year Ended December 31, 2010 (cont’d)

Membership Fees

Total golf members increased 11.0% to 18,917 on December 31, 2010 from 17,049 on December 31, 2009 primarily due to the acquisitionof 1,512 Sun City Center, Florida members. New membership sales for the year ended December 31, 2010 decreased 34.3% to $8,278,000(1,456 members) from $12,602,000 (1,477 members) during the year ended December 31, 2009. Transfer and upgrade fees during 2010decreased to $1,474,000 from $2,612,000 in 2009. Resignations and terminations increased to $4,726,000 (1,100 members or 6.5% of golfmembers at December 31, 2009) in 2010 from $4,595,000 (1,075 members or 6.5% of golf members at December 31, 2008) in 2009.Membership fee instalments received in cash decreased 4.3% to $13,314,000 from $13,906,000 in 2009 as a number of membership contractshave been paid in full.

In recent years, ClubLink’s membership growth has been driven, in part, by: (a) long-term lease arrangements, (b) the addition of newproduct through the conversion of daily fee golf clubs into member or hybrid golf clubs, (c) the acquisition of operating golf course propertiesand (d) the development of greenfield sites into member golf clubs.

The opportunity to add new product through the conversion of daily fee golf clubs has diminished because ClubLink has only two remainingdaily fee golf clubs (Glen Abbey and Rolling Hills Golf Clubs) which may be converted if market demand warrants. ClubLink has sixadditional greenfield sites on which seven 18-championship hole equivalent golf courses could be built if demand warrants. The developmentof a greenfield site requires an investment of approximately $15 to $18 million to open, on a turn-key basis, an 18-championship hole golfclub for play including a clubhouse and furniture, fixtures and equipment where required. Management currently has no plans to proceedwith development at any of the properties within its budgeting horizons. Acquisitions, including long-term leasing opportunities, will beconsidered if the opportunity arises on terms acceptable to ClubLink.

In the absence of new product, management anticipates that membership sales will stabilize at between $9.5 and $12 million per year,comprised of sales to new members of between $8 and $9 million and transfer fees from existing members between $1.5 and $3 million.

Membership fees are amortized over the estimated weighted average remaining life of memberships purchased each year. This is determinedby subtracting the average age of members that joined in that year from 70 and dividing the result by 2. The amortization period is reviewedannually and any adjustments are made prospectively. Membership fee revenue recognized in 2010 increased 3.4% to $15,292,000 from$14,784,000 in 2009.

Details on amortization period in years, member resignations and amortization of membership fee revenue is broken down by member joinyear as follows:

Amortization Amortizationof of

Amortization Amortization Resignations Resignations Membership MembershipPeriod (yrs) Period (yrs) (Members) (Members) Fees ($000) Fees ($000) %

Member Join Year 2010 2009 2010 2009 2010 2009 change

1994–2001 4 5 258 305 $ 3,988 $ 3,884 2.7%

2002 5 6 94 78 2,609 2,595 0.5%

2003 7 8 56 70 1,222 1,215 0.6%

2004 8 9 48 67 1,162 1,166 -0.3%

2005 7 8 132 158 2,073 2,102 -1.4%

2006 10 11 49 52 883 887 -0.5%

2007 10 11 161 202 1,281 1,336 -4.1%

2008 12 13 99 143 723 770 -6.1%

2009 13 14 203 – 766 829 -7.6%2010 13 – – – 585 – N/A

1,100 1,075 $ 15,292 $ 14,784 3.4%

Clublink_AR2010_pgs14-72_v2.3.qxd:AR 2010 4/4/11 10:08 AM Page 22

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

23

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

Results of Operations by Business Segment (cont’d)

Review of Golf Club and Resort Operations for the Year Ended December 31, 2010 (cont’d)

Membership Fees (cont’d)

The following is an age analysis of ClubLink’s golf members:2010 2009 % Change

Under 30 years 1,274 1,199 6.3%

31 – 40 years 1,534 1,706 -10.1%

41 – 50 years 4,858 5,099 -4.7%

51 – 60 years 5,629 5,386 4.5%

61 – 70 years 2,920 2,638 10.7%

71 and over 612 498 22.9%

Not available 578 523 10.5%

Canadian golf members 17,405 17,049 2.1%

Florida golf members 1,512 – n/a

Total golf members 18,917 17,049 11.0%

The average age of a Canadian golf member as at December 31, 2010 is 50.8 years as compared to 50.2 years as at December 31, 2009.

Direct Costs of Originating Membership Fees

Direct costs of originating membership fees decreased 22.7% to $1,511,000 from $1,955,000 in 2009 primarily due to no new majormembership marketing campaigns undertaken in 2010 and the completion of the successful Bond Head marketing campaign in 2009.

Review of Rail, Tourism and Port Operations for the Year Ended December 31, 2010

Summary of Rail, Tourism and Port OperationsFor the Years Ended

December 31, December 31, %2010 2009 Change

Operating revenue $ 35,313 $ 38,131 -7.4%

Operating costs 18,672 19,668 -5.1%

Net operating income (US dollars) 16,641 18,463 -9.9%

Exchange 629 2,114 -70.2%

Net operating income (Cdn dollars) $ 17,270 $ 20,577 -16.1%

Net operating income decreased to US $16,641,000 in 2010 from US $18,463,000 in 2009 due to the decline in rail and port passengers.

Rail, Tourism and Port Operating Revenue

Rail, tourism and port operating revenue is recorded as follows:For the Years Ended

December 31, December 31, %(thousands of dollars) 2010 2009 Change

Railroad $ 26,042 $ 27,981 -6.9%

Port 6,966 7,858 -11.4%

Gift shop and other 2,305 2,292 0.6%

Subtotal (US dollars) 35,313 38,131 -7.4%

Exchange 1,224 4,667 -73.8%

Total (Cdn dollars) $ 36,537 $ 42,798 -14.6%

The number of rail passengers has decreased 7.1% to 368,000 in 2010 as compared to 396,000 in 2009. The decline in rail passengers was less thanexpected due to an improved port passenger capture rate and the loss of rail passengers in 2009 relating to two separate interruptions in rail service.

The number of port passengers has decreased 10.8% to 697,000 in 2010 as compared to 781,000 in 2009. A 12% decline in each category wasexpected as a reaction by the cruise industry to the head tax imposed by the State of Alaska.

Clublink_AR2010_pgs14-72_v2.3.qxd:AR 2010 4/4/11 10:08 AM Page 23

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

24

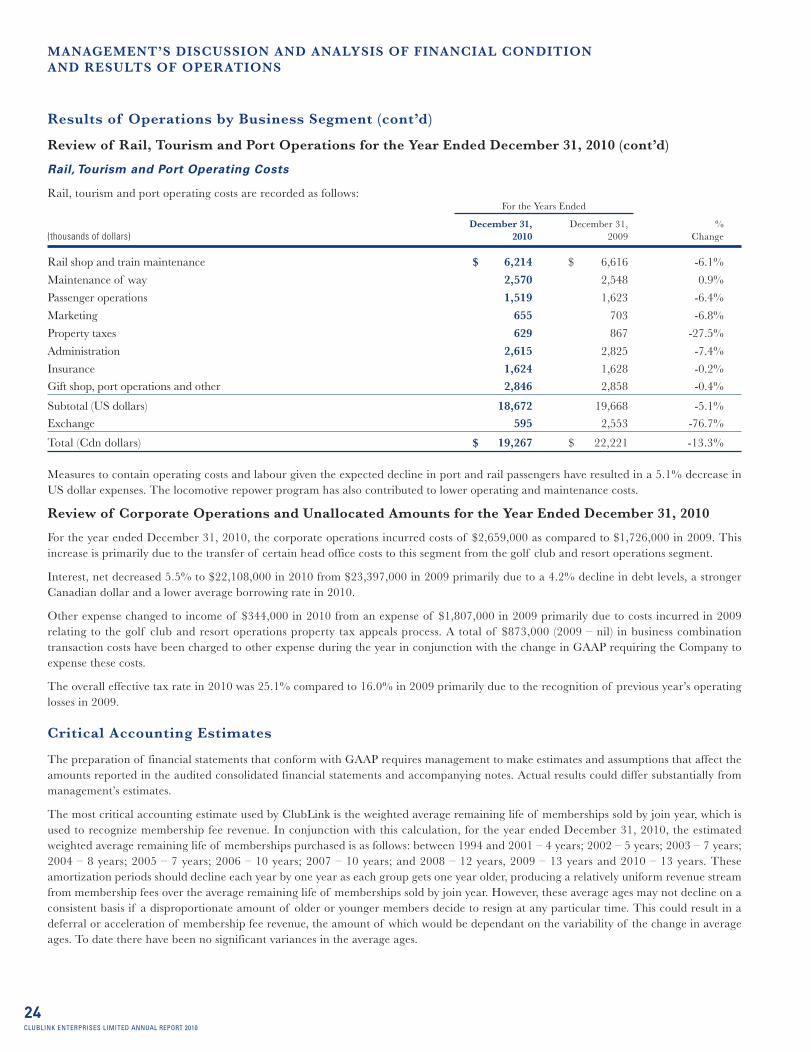

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

Results of Operations by Business Segment (cont’d)

Review of Rail, Tourism and Port Operations for the Year Ended December 31, 2010 (cont’d)

Rail, Tourism and Port Operating Costs

Rail, tourism and port operating costs are recorded as follows:For the Years Ended

December 31, December 31, %(thousands of dollars) 2010 2009 Change

Rail shop and train maintenance $ 6,214 $ 6,616 -6.1%

Maintenance of way 2,570 2,548 0.9%

Passenger operations 1,519 1,623 -6.4%

Marketing 655 703 -6.8%

Property taxes 629 867 -27.5%

Administration 2,615 2,825 -7.4%

Insurance 1,624 1,628 -0.2%

Gift shop, port operations and other 2,846 2,858 -0.4%

Subtotal (US dollars) 18,672 19,668 -5.1%

Exchange 595 2,553 -76.7%

Total (Cdn dollars) $ 19,267 $ 22,221 -13.3%

Measures to contain operating costs and labour given the expected decline in port and rail passengers have resulted in a 5.1% decrease inUS dollar expenses. The locomotive repower program has also contributed to lower operating and maintenance costs.

Review of Corporate Operations and Unallocated Amounts for the Year Ended December 31, 2010

For the year ended December 31, 2010, the corporate operations incurred costs of $2,659,000 as compared to $1,726,000 in 2009. Thisincrease is primarily due to the transfer of certain head office costs to this segment from the golf club and resort operations segment.

Interest, net decreased 5.5% to $22,108,000 in 2010 from $23,397,000 in 2009 primarily due to a 4.2% decline in debt levels, a strongerCanadian dollar and a lower average borrowing rate in 2010.

Other expense changed to income of $344,000 in 2010 from an expense of $1,807,000 in 2009 primarily due to costs incurred in 2009relating to the golf club and resort operations property tax appeals process. A total of $873,000 (2009 – nil) in business combinationtransaction costs have been charged to other expense during the year in conjunction with the change in GAAP requiring the Company toexpense these costs.

The overall effective tax rate in 2010 was 25.1% compared to 16.0% in 2009 primarily due to the recognition of previous year’s operatinglosses in 2009.

Critical Accounting Estimates

The preparation of financial statements that conform with GAAP requires management to make estimates and assumptions that affect theamounts reported in the audited consolidated financial statements and accompanying notes. Actual results could differ substantially frommanagement’s estimates.

The most critical accounting estimate used by ClubLink is the weighted average remaining life of memberships sold by join year, which isused to recognize membership fee revenue. In conjunction with this calculation, for the year ended December 31, 2010, the estimatedweighted average remaining life of memberships purchased is as follows: between 1994 and 2001 – 4 years; 2002 – 5 years; 2003 – 7 years;2004 – 8 years; 2005 – 7 years; 2006 – 10 years; 2007 – 10 years; and 2008 – 12 years, 2009 – 13 years and 2010 – 13 years. Theseamortization periods should decline each year by one year as each group gets one year older, producing a relatively uniform revenue streamfrom membership fees over the average remaining life of memberships sold by join year. However, these average ages may not decline on aconsistent basis if a disproportionate amount of older or younger members decide to resign at any particular time. This could result in adeferral or acceleration of membership fee revenue, the amount of which would be dependant on the variability of the change in averageages. To date there have been no significant variances in the average ages.

Clublink_AR2010_pgs14-72_v2.3.qxd:AR 2010 4/4/11 10:08 AM Page 24

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

25

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

Critical Accounting Estimates (cont’d)

Amortizable intangible assets consist of amounts expended on below market rent terms, brand and membership base. These assets areamortized based on estimates of their useful lives.

Operating capital assets are amortized over their useful lives on a straight-line basis. The Company assesses on an annual basis the usefullife of all capital assets which is used in the calculation of amortization expense. The useful lives assigned by type of capital asset are disclosedin note 2 to the audited consolidated financial statements. Due to the relatively large proportion of these assets to total assets, the selectionof the method of amortization and length of amortization period could have a material impact on amortization expense and net book valueof capital assets.

Capital assets, intangible assets and goodwill are reviewed for impairment whenever events or changes in the circumstances indicate that thecarrying amount of an asset may not be recoverable. Goodwill is also tested on an annual basis at the end of each fiscal year. Recoverabilityof assets to be held and used is measured by comparing the carrying amount of the assets to the anticipated future net cash flows. If suchassets are considered to be impaired, the impairment to be recognized is measured by the amount that the carrying amount of the assetexceeds the fair value of the asset.

ClubLink records income taxes using the liability method of accounting. Under this method, future income tax assets and liabilities aredetermined according to differences between the carrying amounts and tax bases of the assets and liabilities. Management uses judgmentand estimates in determining the appropriate rates and amounts to record for future taxes, giving consideration to timing and probability.Previously recorded tax assets and liabilities are remeasured using tax rates in effect when these differences are expected to reverse inaccordance with enacted laws or those substantively enacted as at the date of the financial statements.

Financial Condition

Assets

Consolidated assets at December 31, 2010 totalled $611,412,000 compared with $627,753,000 at December 31, 2009.

Capital assets employed in golf club and resort operations and rail, tourism and port operations account for all of the Company’s capitalassets. The book value of these capital assets was $468,771,000 and $72,264,000, respectively, at December 31, 2010 ($464,717,000 and$72,007,000, respectively, at December 31, 2009). The increase in the golf club and resort capital assets is due to the three acquisitions inthis segment during the year.

Liabilities

Total liabilities decreased to $455,615,000 at December 31, 2010 from $473,193,000 at December 31, 2009 primarily due to the amortizationpayments decreasing the Company’s secured debt.

Shareholders’ Equity

Consolidated shareholders’ equity at December 31, 2010 totalled $155,797,000 or $5.58 per share, compared to $154,560,000 or $5.51 pershare at December 31, 2009. The number of common shares outstanding decreased to 27,902,618 shares as at December 31, 2010 from28,057,479 as at December 31, 2009 primarily due to shares repurchased and cancelled.

The following is a summary of the common share activity:For the Years Ended

December 31, December 31,(number of shares) 2010 2009

Balance, beginning of year 28,057,479 22,909,437

Shares issued pursuant to dividend reinvestment plan 3,389 5,567

Shares issued as consideration for business combination with ClubLink Corporation – 5,164,015

Exercise of stock options – 3,000

Shares purchased and cancelled through normal course issuer bid program (64,200) (24,540)

Shares repurchased and cancelled (94,050) –

Balance, end of year 27,902,618 28,057,479

Clublink_AR2010_pgs14-72_v2.3.qxd:AR 2010 4/4/11 10:08 AM Page 25

CLUBLINK ENTERPRISES LIMITED ANNUAL REPORT 2010

26

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

Financial Condition (cont’d)

Shareholders’ Equity (cont’d)

During 2010, the Company continued its dividend program and paid a quarterly payment of 7.5 cents per share on March 31, June 30,September 15 and December 15, 2010.

The Company has recorded a loss in its accumulated other comprehensive loss account of $1,185,000 due to a change in the Canadian/U.S.exchange rate to 0.9946 at December 31, 2010 from 1.0510 at December 31, 2009. This exchange rate change reduces the Canadian dollarequivalent for each of the assets and liabilities within rail, tourism and port operations.

Liquidity and Capital Resources

ClubLink’s objective is to ensure that capital resources are readily available to meet obligations as they become due, to complete its approvedcapital expenditure program and to take advantage of attractive acquisitions as they arise. ClubLink’s capital availability and demonstratedability to execute transactions give it a competitive advantage in corporate development opportunities.

The analysis of ClubLink’s liquidity is as follows:As at December 31, 2010 As at December 31, 2009

(thousands of dollars) Maximum Available Maximum Available

Cash $ 1,447 $ 1,447 $ 10,670 $ 10,670

Revolving secured debt (rail) 9,946 4,388 7,883 –

Revolving secured debt (corporate) 50,000 5,217 49,800 27,791Related party debt facility 30,000 30,000 30,000 1,600

$ 91,393 $ 41,052 $ 98,353 $ 40,061

Funds will be used during 2011 for operating capital expenditures in both business segments, to fund development capital expenditures,including the locomotive repower program, to purchase additional securities pursuant to ClubLink’s normal course issuer bid program andto pay debt obligations as they become due.

Liquidity risk arises from general funding needs and in the management of assets, liabilities and optimal capital structure. ClubLink managesliquidity risk to maintain sufficient liquid financial resources to meet its commitments and obligations in the most cost-effective manner possible.

Based on ClubLink’s financial position at December 31, 2010, and projected future earnings, management expects to be able to fund itsworking capital requirements, and meet its other obligations including debt repayments.