Climate Change and Business: A Climate SWOT Analysis Tool for ...

24

Climate Change and Business: A Climate SWOT Analysis Tool A Climate SWOT Analysis Tool for SME’s Susanna Horn School of Business and Economics University of Jyväskylä, Finland

Transcript of Climate Change and Business: A Climate SWOT Analysis Tool for ...

Climate Change and Business:A Climate SWOT Analysis ToolA Climate SWOT Analysis Tool

for SME’s

Susanna HornSchool of Business and Economics

University of Jyväskylä, Finland

f hi iContents of this presentation

Climate Change and Business – An overview

Climate SWOT as a tool

Results of the studies:– Tool

Content– Content

Climate Change and Business: Strategies

How will climate change affect the business environment: Markets? Prices? Resources?

What action is needed?

How will the markets in the future look like? How will the markets in the future look like?

What are the opportunities in the uncertainty?

What about competitors? at about co pet to s

→ Strategic assessment for a market transition (present, near future, long‐term)

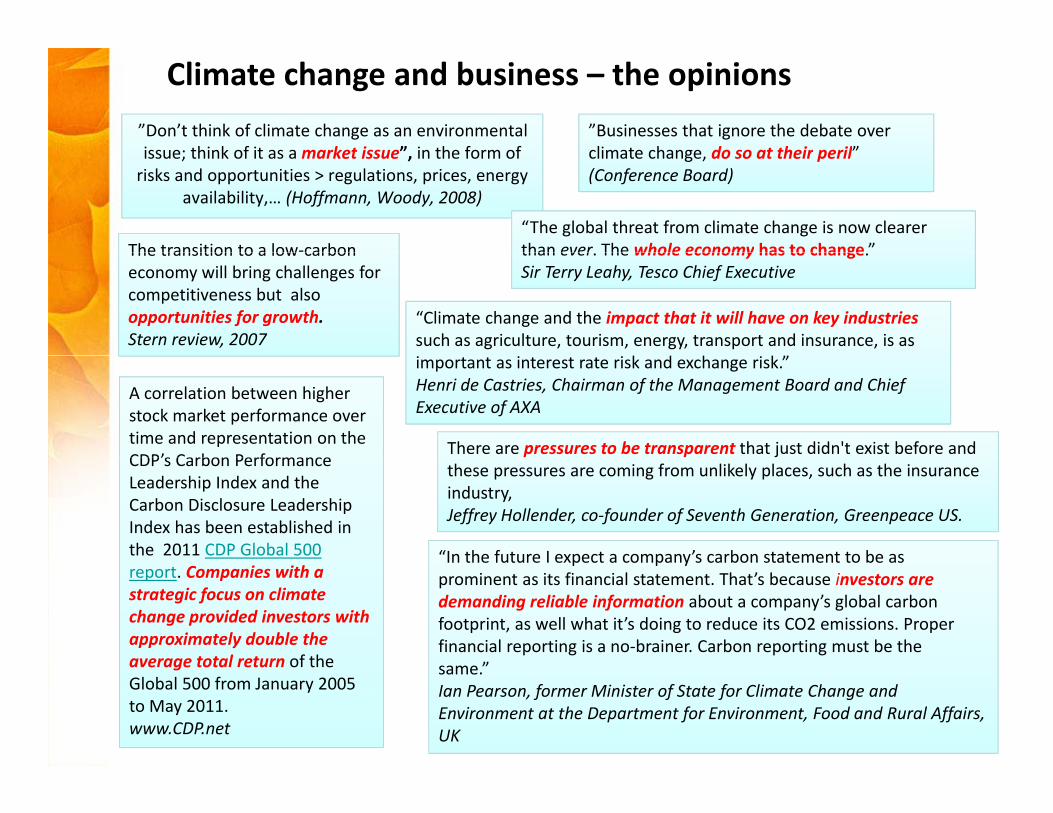

”Don’t think of climate change as an environmentalissue; think of it as amarket issue” in the form of

”Businesses that ignore the debate overclimate change do so at their peril”

Climate change and business – the opinions

issue; think of it as amarket issue”, in the form of risks and opportunities > regulations, prices, energy

availability,… (Hoffmann, Woody, 2008)

climate change, do so at their peril” (Conference Board)

“The global threat from climate change is now clearer than ever The whole economy has to change ”The transition to a low‐carbon than ever. The whole economy has to change.Sir Terry Leahy, Tesco Chief Executive

“Climate change and the impact that it will have on key industriessuch as agriculture, tourism, energy, transport and insurance, is as

The transition to a low carbon economy will bring challenges for competitiveness but also opportunities for growth.Stern review, 2007

important as interest rate risk and exchange risk.”Henri de Castries, Chairman of the Management Board and Chief Executive of AXA

There are pressures to be transparent that just didn't exist before and

A correlation between higher stock market performance over time and representation on the CDP’s Carbon Performance

“In the future I expect a company’s carbon statement to be as

these pressures are coming from unlikely places, such as the insurance industry, Jeffrey Hollender, co‐founder of Seventh Generation, Greenpeace US.

CDP s Carbon Performance Leadership Index and the Carbon Disclosure Leadership Index has been established in the 2011 CDP Global 500 In the future I expect a company s carbon statement to be as

prominent as its financial statement. That’s because investors are demanding reliable information about a company’s global carbon footprint, as well what it’s doing to reduce its CO2 emissions. Proper financial reporting is a no‐brainer. Carbon reporting must be the

”

report. Companies with a strategic focus on climate change provided investors with approximately double the average total return of the same.”

Ian Pearson, former Minister of State for Climate Change and Environment at the Department for Environment, Food and Rural Affairs, UK

average total return of the Global 500 from January 2005 to May 2011.www.CDP.net

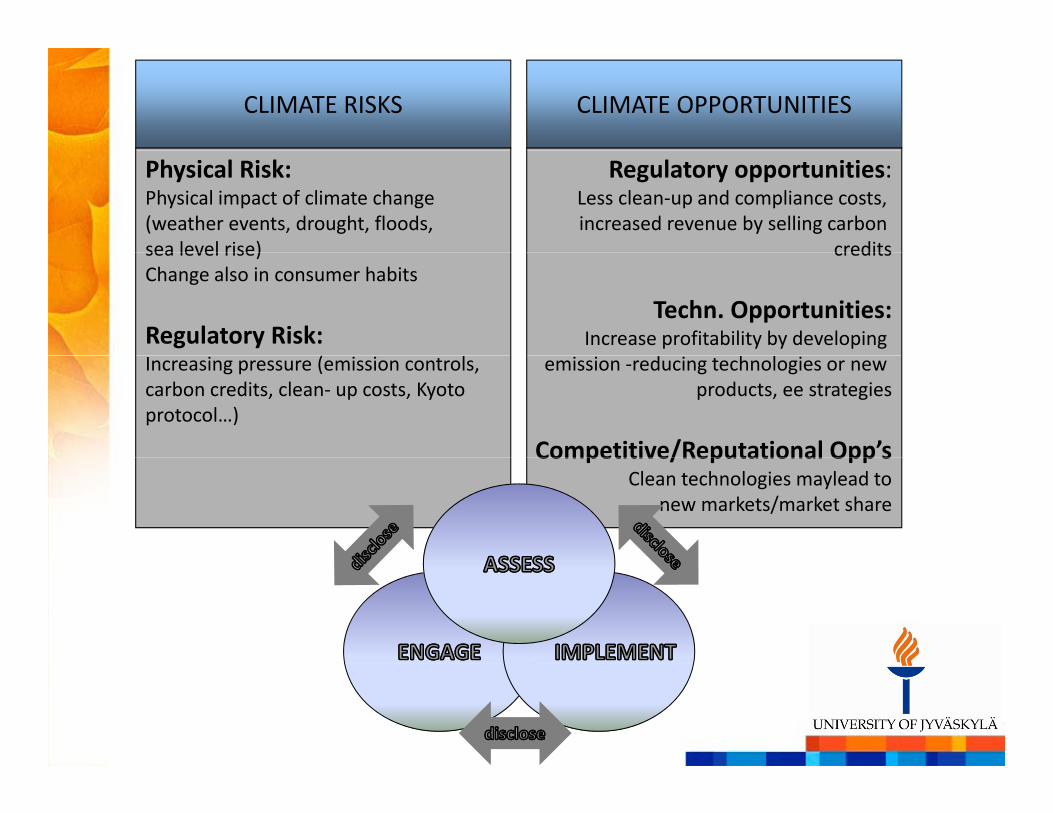

From a business perspective you don’t need to look at theFrom a business perspective, you don t need to look at the science of climate change and make up your mind whetherto believe it or not:

The framework (regulations), markets (e.g. prices, investment community’s interests), competitors, demandis changing so the companies should act on theseis changing, so the companies should act on these

CLIMATE RISKS CLIMATE OPPORTUNITIES

Physical Risk:Physical impact of climate change(weather events, drought, floods,sea level rise)

Regulatory opportunities:Less clean‐up and compliance costs, increased revenue by selling carbon

creditssea level rise)Change also in consumer habits

Regulatory Risk:

credits

Techn. Opportunities:Increase profitability by developing

Increasing pressure (emission controls, carbon credits, clean‐ up costs, Kyotoprotocol…)

emission ‐reducing technologies or new products, ee strategies

Competitive/Reputational Opp’sCompetitive/Reputational Opp sClean technologies maylead to

new markets/market share

Climate SWOT

Two basic ideas combined

1. SWOT analysis• Quadrivial analysis is a common and simple method to assess e.g. your business (or parts of it) ‐ risk assessment

• Strength – Weakness – Opportunity – ThreatStrength Weakness Opportunity Threat

• In present (SW) and in future (OT)

• Internal (SW) and external (OT)

St th th hi h b tili d k• Strengths are those resources which can be utilised, weaknessesthose which must be improved. Opportunities and threats mustbe known approximately

2 Lif l i2. Life cycle perspective• Consider all life cycle steps

Goal and Scope Definition

LCA steps (ISO 14040):LIFE CYCLE ASSESSMENT

Goal and Scope Definition

Inventory analysis

ionan

d

Impact assessment

Interpretat

Repo

rting

StrengthsStrengthsGlobal

WeaknessesWeaknessesHigh cost structure

SWOT

Strong R&DSpecific competitive advantageHighly qualified personnelHigh re‐sale valueEfficient processLocationS i l k ti ti

Too narrow focusAbsence of strongmarketing/accounting expertisePoor access to distributionUnreliable serviceHigh wagesP ft l iSpecial marketing expertise Poor after sales servicePoor quality product

OpportunitiesOpportunitiesPotential to diversify into relatedmarketsChanges in government actions

ThreatsThreatsLow cost competitorsEconomic slowdownChanges in government actions

Change in population ageAlternative delivery modelsInternet salesMergers, acquisitions etc.Larger international markets

Change in population ageCompetitor with a new subsituteproductCompetitor’s access to betterdistribution channelsNew taxes

Climate Strategies Based on Climate SWOTBased on Climate SWOT

1. Identification of Product Life Cycle Stages

2. Identification of Climate Impactsa) Now

b) In the future year Xb) In the future, year X

3. Significance Assessment of the Climate Impacts

4. Compilation of the Climate SWOTp

5. Climate Strategy Options

6. Strategy Formulation

Hanna-Leena Pesonen, 2011

1. Identification of Product Life Cycle StagesProduct Life Cycle Stages

Typical Model of a Product Life Cycle

Raw MaterialsProduction

Production Transportation Trade UseRecycling and

Waste Management

Example: Life Cycle of a Car

Production of Steel, Plastic,

and Other Raw Materials

Component Production

Car Production Car Sales

Car Use,Driving

Recycling and Waste

Management

Example: Life Cycle of a Car

Example: Life Cycle of a Newspaper

ForestryPulp

ProductionPaper

ProductionPrinting Distribution Use, Reading

Newspaper

Paper Recycling and

Waste Management

T lli Skii dExample: Life Cycle of a Vacation in Ski Resort

Travel Reservation

Travelling to/from Ski

ResortAccommodation Slope

MaintenanceSkiing and

Other Outdoor Activities

Hanna-Leena Pesonen, 2011

2. Identification of Climate Impacts

Raw MaterialsProduction

Production Transportation Trade UseRecycling and

Waste Management

Impact A + Impact B -Impact C +

Consider climate impacts for all life cycle stages a) in the current situation and b) in the future:Both positive and negative aspects“Inside‐out”: impacts of the activities of each life cycle stage on the climate i e greenhouse gas emissions caused

Impact D -stage on the climate, i.e. greenhouse gas emissions caused by use of energy, traffic, transportation, location and land use, etc.“Outside‐in”: how the changing climate may affect the activities of each life cycle stage

Use GHG Inventories

Impact E +

Use Climate Scenarios

Hanna-Leena Pesonen, 2011

3. Significance Assessment of the Climate Impactsof the Climate Impacts

Assess the significance of each identified impact on scaleAssess the significance of each identified impact on scale 1‐3– Minor impact 1– Medium impact 2p– Major impact 3In assessing the significance consider the nature of your impacts against your competitors’ impacts:– Environmental impacts (fragility of the environment, size and

frequency of the aspect)– Financial impacts

I t f th i t t k h ld ( li t l– Importance of the issue to your stakeholders (clients, employees etc.)

– Requirements of legislation concerning climate issues

Hanna-Leena Pesonen, 2011

4. Compilation of the Climate SWOT

Raw MaterialsProduction

Production Transportation Trade UseRecycling and

Waste Management

Strengths

I t A

Weaknesses

I t B Impact A

Impact C

Impact B

O t iti Th t

Opportunities

Impact E

Threats

Impact D

Hanna-Leena Pesonen, 2011

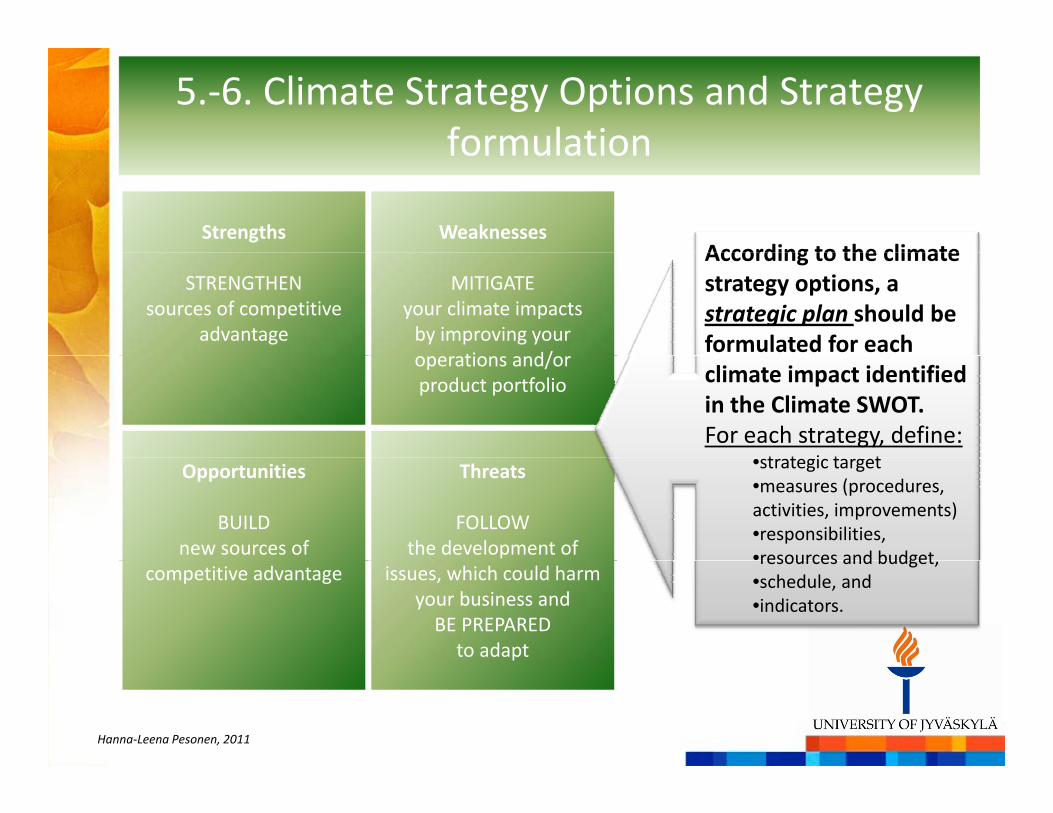

5.‐6. Climate Strategy Options and Strategy formulationformulation

Strengths WeaknessesAccording to the climate

STRENGTHENsources of competitive

advantage

MITIGATEyour climate impacts by improving your

ti d/

According to the climate strategy options, a strategic plan should be formulated for each

operations and/orproduct portfolio climate impact identified

in the Climate SWOT. For each strategy, define:

t t i t tOpportunities

BUILDnew sources of

Threats

FOLLOWthe development of

•strategic target•measures (procedures, activities, improvements)•responsibilities,•resources and budget

competitive advantage issues, which could harm your business andBE PREPARED

to adapt

resources and budget,•schedule, and•indicators.

Hanna‐Leena Pesonen, 2011

Two studies are made about the ClimateSWOTSWOT

First: Methodological scope, developing the toolTwo target groups: student group (24 students) and BalticClimate’s commissioners

Students prepared the Climate SWOT’s for the given productsystems in the Baltic area

The results were communicated to the Commissioners in the spring

Two surveys: one to the students (how easy/logical the tool wasto use) and one to the Commissioners (if the results hadgenerated any changes)

Results: encouraging in terms of usability, some minor changeswere implemented (product system, time scope, policy‐levelimpacts, data sources)

Second: The results of the Climate SWOT’s

Agriculture and Forestry

Refining and Industrial

OperationsTransport Retail Use

Recycling and Waste

Management

Climate Strategy Options for SME’s in Agriculture and Forestry in the Baltic Region:

StrengthsProduction of bioenergy, often as byproductProduction of bioenergy, often as byproduct

WeaknessesEnergy intensive industriesT t ti b d f il f l

y Operations Management

Production of bioenergy, often as byproduct

Recyclable materialsTransportation based on fossil fuelsCurrently retail not strongly supporting local food

OpportunitiesTwo harvests per season, more yield on agriculture

ThreatsLogging more complicated in winter

p , y gLonger growing season for forests, which can increase forestry yieldIncreasing freshwater resources due to precipitationNew plant species or new races for animal husbandryIncreasing wind creates opportunities for wind energy

Logging more complicated in winterFlooding because of increasing precipitation, increasing soil moisture and weakening soil quality, erosionMore winter kills in both agriculture and forestry due to no snow

Increasing wind creates opportunities for wind energy

Use of bioenergy increasingUse of biofuels increasingChanges in diet favoring local or organic foodNew markets for agricultural products due to negative climate effects in other regions

due to no snowMore and new species of pest and plant diseasesHealth problems for farmers and livestockMore forest fires when summers are hotterMore expensive fuel , more expensive transport

climate effects in other regions

•Invest in developing options for bioenergy (as a producer and user)•Invest in energy efficiency to avoid impact of increasing fuel prices

•Be prepared to react promptly on changes in traditional timing of agricultural and forestry( )operations (e.g. two harvests)

•Promote the ongoing change in diets towards local and organic food

•Follow the development of the natural threats caused by climate change and be preparedto act by e.g. introducing new, more resistant species

Raw Material Production RefiningTransportation

to Refining Distribution Use

Climate Strategy Options for SME’s in Bioenergy in the Baltic Region:

StrengthsRenewable raw materialsAvailability of wood, agribiomass and biowaste as rawmaterial

WeaknessesInefficient production technologies and supply chain management=> life cycle energy balance of biofuels/bioenergy in some cases negative

materialDecreasing transportation, if local materials usedGHG neutral fuel or energy source

bioenergy in some cases negativeCurrently often higher production prices compared to fossil fuelsLack of distribution network for biofuelsLack of infrastructure to accommodate use of new biofuels or bioenergy, e.g. biogas as vehicle fuel

gy, g g

OpportunitiesLarger scale, more efficient production=> increasing eco‐efficiency of biofuels life cycle environmental impactsSupport for increasing use of biofuels/bioenergy in( ) l l

ThreatsBiodiversity concerns related to growing raw materialsfor bioenergy and biofuelsAvailability of raw materials

f h l

(European) legislationDecreasing production prices with economies of scale andlearning => increasing price competitivenessImproved technologies enabling new raw materials (egwood based raw materials in F‐T technologies)=> moreefficient raw material production=> increasing price

No interest from car owners to switch to alternative fuels or from car industry to develop biofuel vehicles=> no demand for biofuelsNo policy framework to support change

efficient raw material production=> increasing price competitivenessChanges in fuel & energy taxation favoring biofuels/‐energy

•Invest in developing local raw material production

P ti i t i d l i di t ib ti t k d i f t t t d t f bi f l /bi•Participate in developing distribution network and infrastructure to accommodate use of new biofuels/bioenergy

•Follow changes in legislation and political support for bioenergy and be prepared to develop your business accordingly

•Be active in promoting the use of bioenergy

Raw Material Extraction and

ProcessingTransport Building Use and

MaintenanceRecycling and

Waste Management

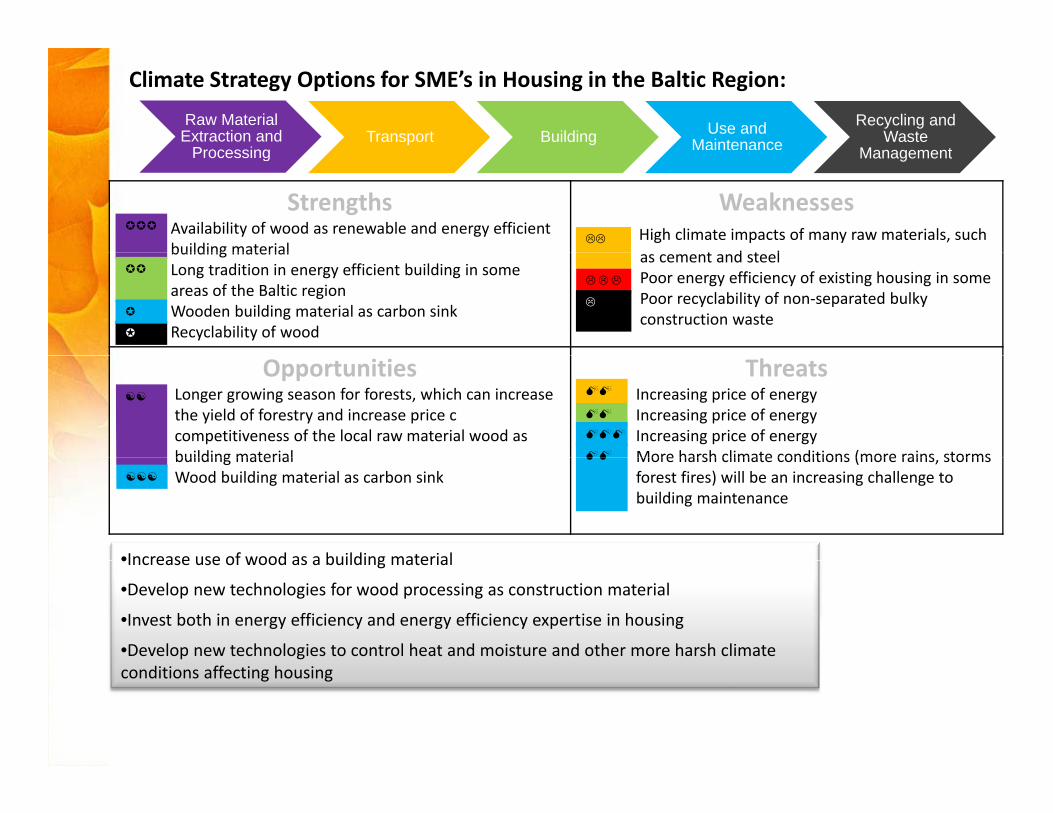

Climate Strategy Options for SME’s in Housing in the Baltic Region:

StrengthsAvailability of wood as renewable and energy efficientbuilding material

WeaknessesHigh climate impacts of many raw materials, such

t d t l

Processing Management

building materialLong tradition in energy efficient building in someareas of the Baltic regionWooden building material as carbon sinkRecyclability of wood

as cement and steelPoor energy efficiency of existing housing in some Poor recyclability of non‐separated bulky construction waste

OpportunitiesLonger growing season for forests, which can increasethe yield of forestry and increase price ccompetitiveness of the local raw material wood as building material

ThreatsIncreasing price of energyIncreasing price of energyIncreasing price of energyMore harsh climate conditions (more rains storms

building materialWood building material as carbon sink

More harsh climate conditions (more rains, stormsforest fires) will be an increasing challenge to building maintenance

•Increase use of wood as a building material

•Increase use of wood as a building material

•Develop new technologies for wood processing as construction material

•Invest both in energy efficiency and energy efficiency expertise in housing•Develop new technologies to control heat and moisture and other more harsh climateconditions affecting housing

Marketing Travelling to/ from Resort

Summer Activities

Winter Activities

Infrastructure and Facilities

Climate Strategy Options for SME’s in Tourism in the Baltic Region:

StrengthsPristine nature in many areas of the Baltic region,cleanair and water

WeaknessesLong distance from foreign market areas, expensive transport

from Resort Activities Activitiesand Facilities

air and waterShorter distance for local travelers compared to foreignresorts, cheaper transportTraditions in relatively energy efficient building (insula‐tions etc.)

expensive transportEnergy intensity in accommodation and other facilities (heating, lighting etc.)Energy intensity in winter sports maintenance (snow making, skiing lifts, lighting, etc.)

OpportunitiesChanging tourism culture bringing more opportunitiesfor local tourismLonger season for summer tourism through risingtemperatures

ThreatsIncreasing fuel prices decreasing travellingIncreasing costs of accommodation because of increasing heating, cooling, electricity costs => price competitiveness suffers

temperatures price competitiveness suffersIncreasing precipitation, i.e. more rain, might causeproblems for summer tourismRising sea level threat for seaside hotels and infrastructureLack of snow and rising temperatures causing

Lack of snow and rising temperatures causingshorter winter season

•Stress the pristine nature, clean air and water in communication

•Strengthen marketing efforts to local travelers

•In winter travel study options for renewable energy•Winter resorts might have to start looking for new innovations how to enable traditionalwinter sports and activities (cooperation with technological partners, create alternative, non‐winter (or year‐round) activities

Road TransportShip

Transportation and Port

Public TransportationRail Transport

Climate Strategy Options for SME’s in Transportation and Mobility in the Baltic Region:

StrengthsRelatively good railroad network in the Baltic RegionTradition of using waterways for transportation

WeaknessesUse of fossil fuels and high fuel pricesHigh replacement cost for alternative fuel vehicles

and Port Operations

Transportation

Tradition of using waterways for transportationHigh energy efficiency of public transportationRelatively good public transportation network in someareas of the Baltic region, in bigger cities and densely populatedareas

Use of fossil fuels and high fuel pricesUse of fossil fuels and high fuel pricesLimited infrastructure for public transportation, eg limitedbiking routesPoor quality and image of public transportationHigh prices of public transportation

Accessibility of public transportation (especially for handi‐capped and the elderly

OpportunitiesMore energy efficient vehicles using alternative fuelsTax support or other forms of subsidies for alternative fuel

ThreatsIncreasing problems in road construction and maintenance:temperature fluctuation around 0°C degrade roads

Tax support or other forms of subsidies for alternative fuel consuming vehiclesIf winters get milder, no spikes are needed in tires, which woulddecrease the stress on road surfaceIncreasing attractiveness of rail transport with rising fuel pricesIncreasing opportunities to use waterways for transportation ast t i

temperature fluctuation around 0 C degrade roadsIncreasing problems in railroad construction and maintenance because of temperature fluctuationsMore storms and floods causing problems for ship transportsFailure to attract travelers to shift to public transport modes

temperature risesIncreasing attractiveness and demand on public transport, when increasing fuel prices make private car ownership expensive

•Local cooperation between different transportation modes and actors

•Prepare for rising fossil fuel prices by compensating the current fleet with models using alternative renewable fuels•Prepare for rising fossil fuel prices by compensating the current fleet with models using alternative renewable fuels

•Investments for infrastructure, e.g. biking routes and public transportation infrastructure would offer new opportunities for SME’s in construction sector

•In areas with good inland waterways, develop new year‐round water transportation services

SummaryI i il h iImpacts similar across the region:– Rising temperatures

– Increasing precipitationg p p

– Decreasing snow cover

ChallengesN i t di ( i lt &f t )– New species, pests, diseases (agriculture&forestry)

– Development of alternative RE sources, energy efficiency (energyand transportation)

– New needs of maintenance due to changing climate (housing)

– Shortening of winter season (tourism)

Opportunities:– New markets for green tech (indoor skiing, nanotechnology,

new mobility services)

– New species in agriculture and forestry

– Energy efficiency, RE

– Wood construction

Common features:Common features:– Locality

– Significance of wood

– Importance of energy saving and efficiency

– More cooperation needed between all stakeholders

Contact information:

Thanks!

Susanna [email protected]

School of Business and EconomicsUniversity of Jyväskylä

P O Box 35P.O. Box 35 40014Finland