Click here to add image Global Trends and Swing Factors ...

42

Click here to add image Click here to add image Global Trends and Swing Factors And their impact on the agricultural complex

Transcript of Click here to add image Global Trends and Swing Factors ...

Click here to add imageClick here to add image

Global Trends and Swing Factors

And their impact on the agricultural complex

Introduction

2

I'm speaking today and tomorrow in Iowa for the IA Farm Bureau and I followed Sterling Liddell who gave a long range outlook. Super presentation. He has all the flamboyant showmanship of an economist, but still strangely likable.

John PhippsAgricultural Columnist

Food & Agribusiness Research and AdvisoryA global team of analysts – supporting knowledge based banking

Christchurch

Mexico City

New York

Sao Paulo

Mumbai

Melbourne

Utrecht

Shanghai

Buenos Aires

Fresno

Team of 80+ analysts

Specialist teams− Grains & oilseeds− Dairy− Animal protein− Retail− Beverages− Ag inputs− Sugar

London

Chicago

St Loius

Sydney

Singapore

Hong Kong

Beijing

Santiago

New Dehli

Click here to add image

Macro Conditions

Recipe for our Economic Perfect Storm: Lower Interest Rates

6Rabobank InternationalMarket Developments & Outlook

U.S. wage costs have barely budged over the last decade, while costs for Brazil are up 70% and up over 350% in China.

This changes the relative competitive landscape dramatically – especially when we think about whether China wil l import grain or meat.

Higher mean higher costs – but also more protein consumption.

Brazil, China and US Real Wage Index

Source: IBGE, BLS, Bloomberg, 2012

Labor: west improving relative cost competitiveness

7Rabobank InternationalMarket Developments & Outlook

Sovereign Debt Interest Rates - US and Brazil

Source: Bloomberg, 2012

Cost of capital: Big advantage vs. Brazil other developing economies

8

Systemic RiskRandom Risk

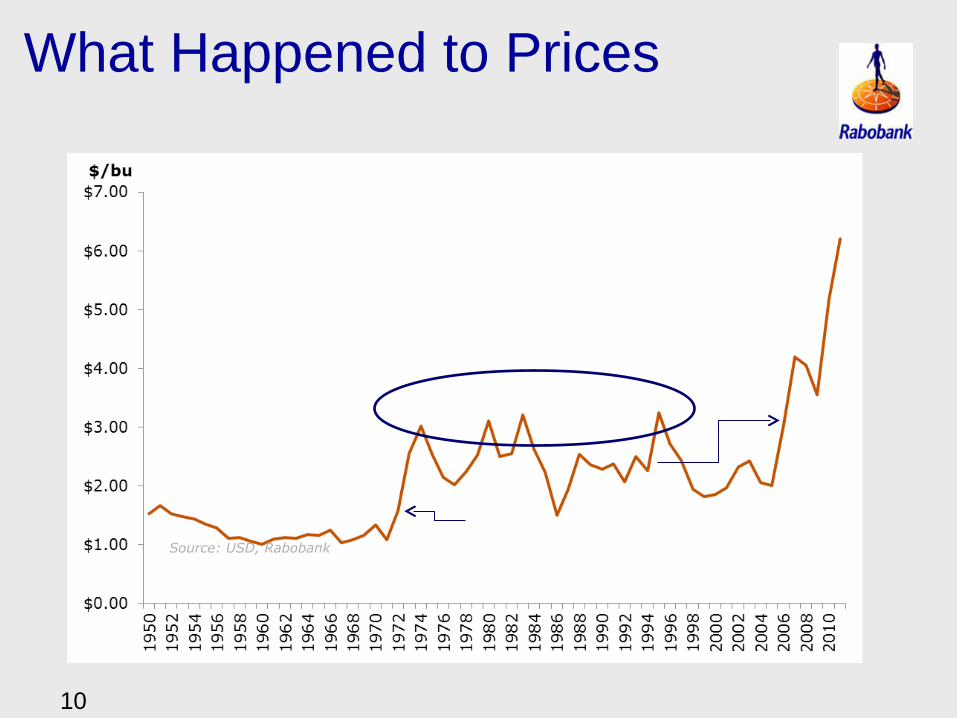

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.001950 1952 1954 1956 1958 1960 1962 1964 1966 1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Dollars/Bushel

Corn Price per Unit Average Corn Price

What Happened to Prices

10

Source: USD, Rabobank

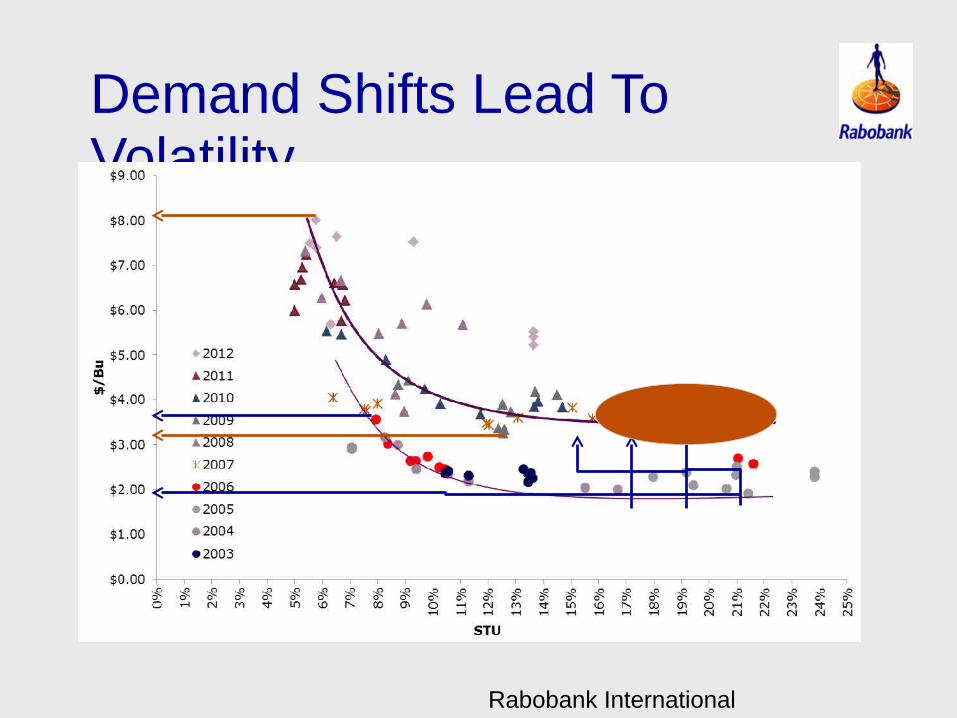

Demand Shifts Lead To Volatility

Rabobank International

Click here to add image

Understanding The Drivers:

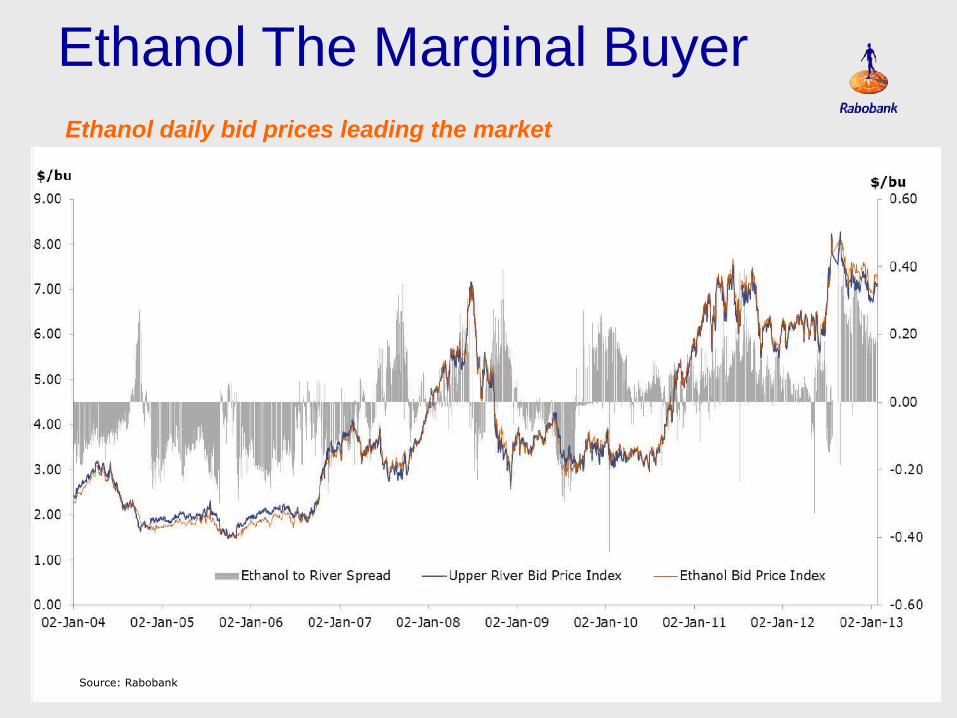

Ethanol Reversing Grain FlowsUS corn used for ethanol has increased by roughly 100MMT since 2005, while world grain demand has risen by about 300MMT.

Biodiesel is a factor as well. World demand for vegetable oil is growing by about 5 million tons per year. About 2 of that, or 40%, has been going to feed biodiesel demand.

Ethanol daily bid prices leading the market

Ethanol The Marginal Buyer

Source: Rabobank

Click here to add image

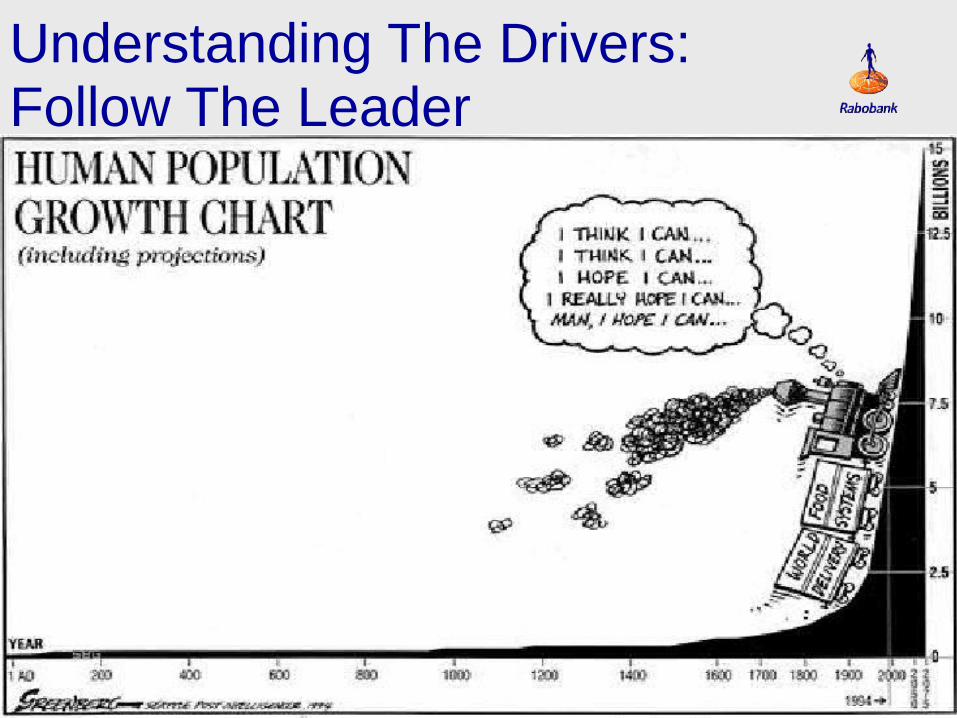

Understanding The Drivers: Follow The Leader

16Rabobank InternationalMarket Developments & Outlook

World GDP growth continues to outpace animal protein production growth – so demand is outstripping supply which leads to high meat prices.

Animal protein production is adapting to structurally higher and more volatile grain prices. Given the lag factor caused by anima l life-cycles, this process will take time.

The shorter life cycle for poultry, in addition to feed conversion advantages, provides a relative advantage to other proteins.

Especially that from developing markets

Sources: World Bank for GDP data and forecast, USDA for meat production, Rabobank for meat production forecast

Meat Production < GDP = Higher Meat Prices

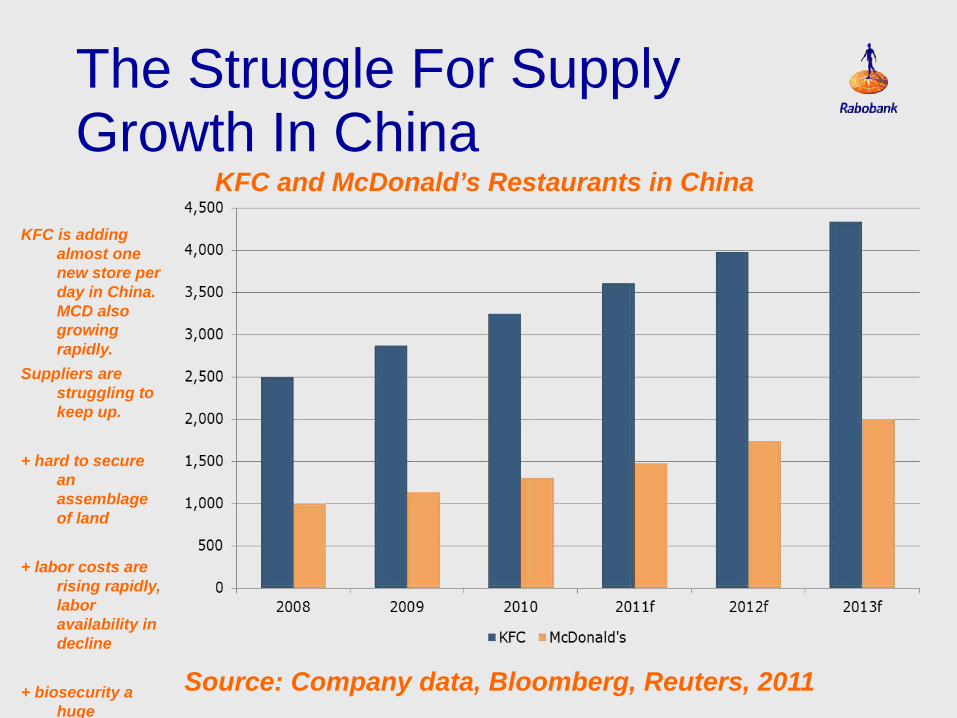

The Struggle For Supply Growth In China

KFC is adding almost one new store per day in China. MCD also growing rapidly.

Suppliers are struggling to keep up.

+ hard to secure an assemblage of land

+ labor costs are rising rapidly, labor availability in decline

+ biosecurity a huge challenge (disease, antibiotics)

+ these chains only use about 20% of the bird

KFC and McDonald’s Restaurants in China

Source: Company data, Bloomberg, Reuters, 2011

If industrial hog production grows from 55% to 60%, and modified from 11% to 21%, deficit expected to be 23 MMT by 2015

•Assuming 10 bu. of corn per pig

China Hog Production

Source: MOA, Rabobank, 2012

Industrialization Production Driving Demand

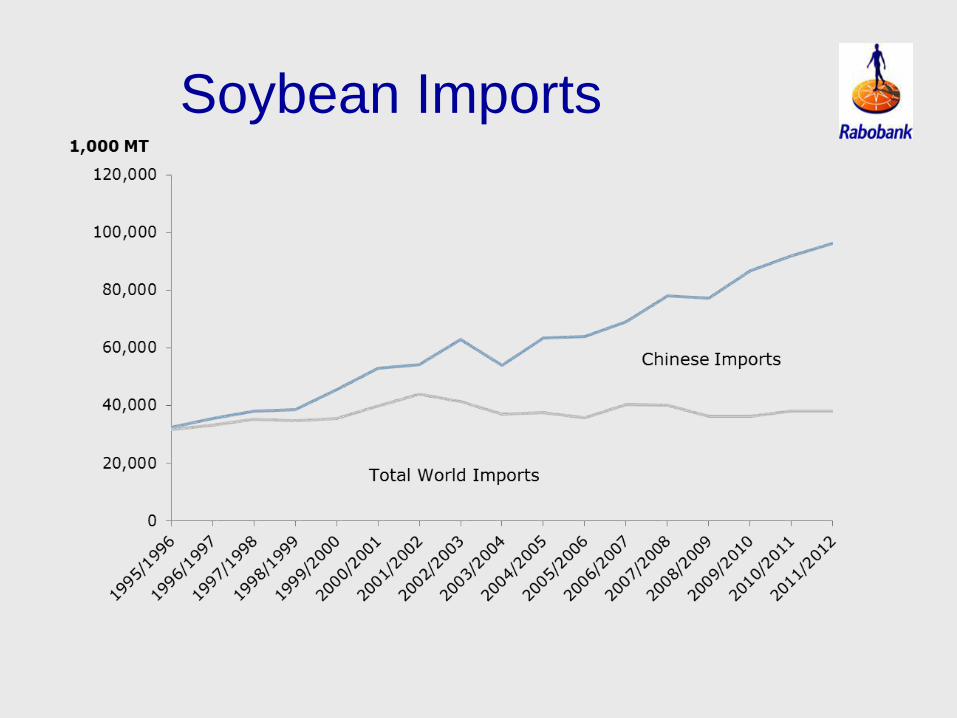

Soybean Imports

Despite a recovery of 60MMT of grain production from the FSU last year, the world grain still declined slightly.

Structurally, demand is growing faster than supply.

The world is still in a period of structural surplus to structural shortage.

World Grain Stocks to Use Ratio

Source: USDA, 2012

Grain Not Keeping Up With Structural Demand Growth

Click here to add image

Certainly We Have Tried To Over Produce

Click here to add image

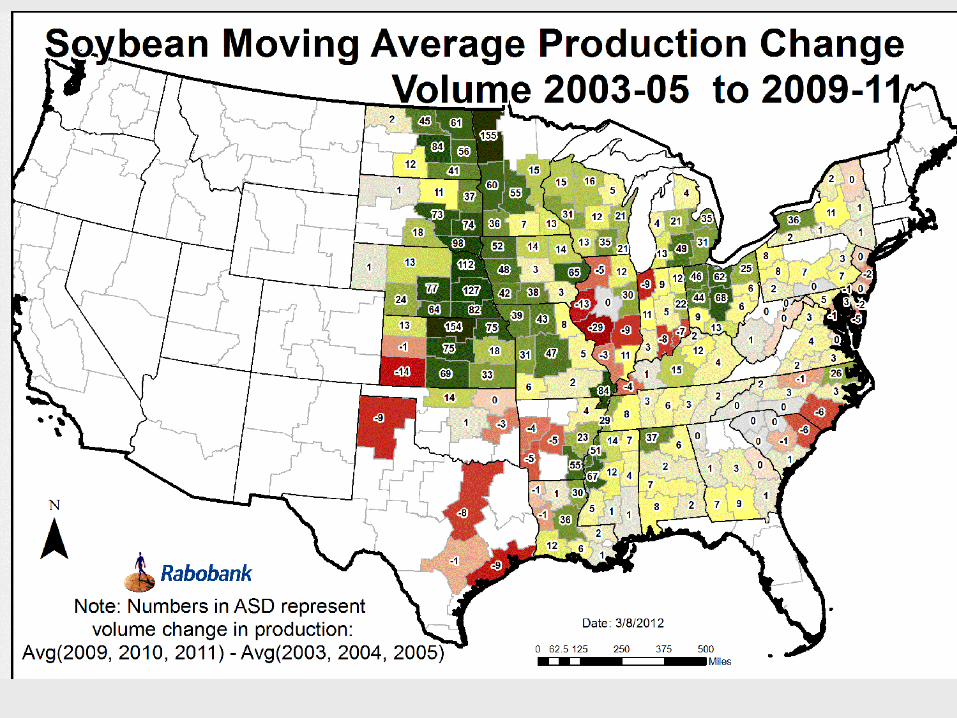

Understanding The Drivers: Changes In Supply Sources

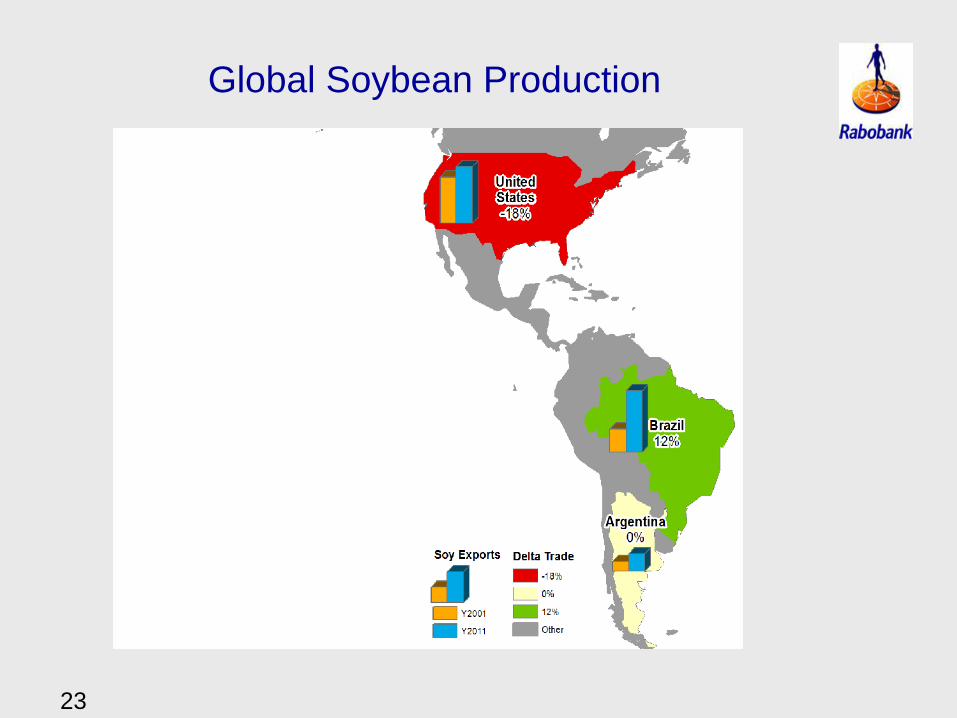

Global Soybean Production

23

Infrastructure Challenges

Investment in storage infrastructure has not matched the growth of corn and soybean production

19/03/13

19/03/1319/03/13

19/03/13

19

/0

3/

13

19

/0

3/

13

19/03/13

19

/0

3/

13

19/03/13

19

/0

3/

13

19/03/13

19

/0

3/

13

19/03/13

19/03/13

19

/0

3/

13

19/03/13

19

/0

3/

13

19/03/13

19/03/13

19

/0

3/

13

CAGR: 6%

19/03/13

19

/0

3/

13

19

/0

3/

13

19/03/13

19

/0

3/

13

19/03/13

19

/0

3/

13

19

/0

3/

13

19/03/1319/03/13

19/03/13

19/03/13

CAGR: 4%

[Million Metric Tons]

Source: Rabobank. Data from CONAB:2012.

154149

144

123

115119

123

101

155

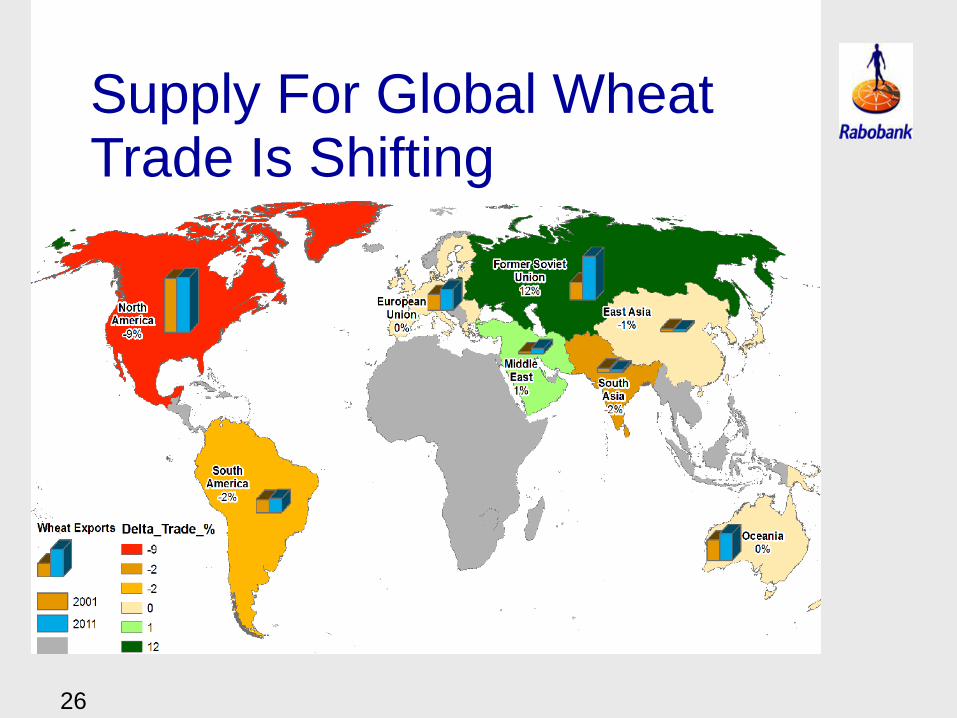

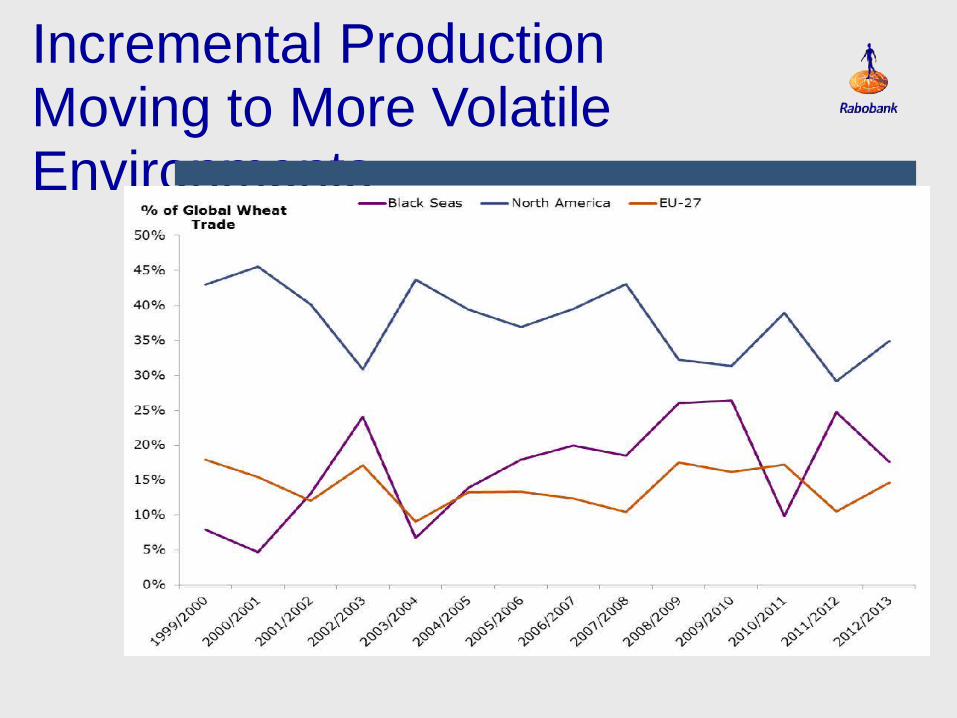

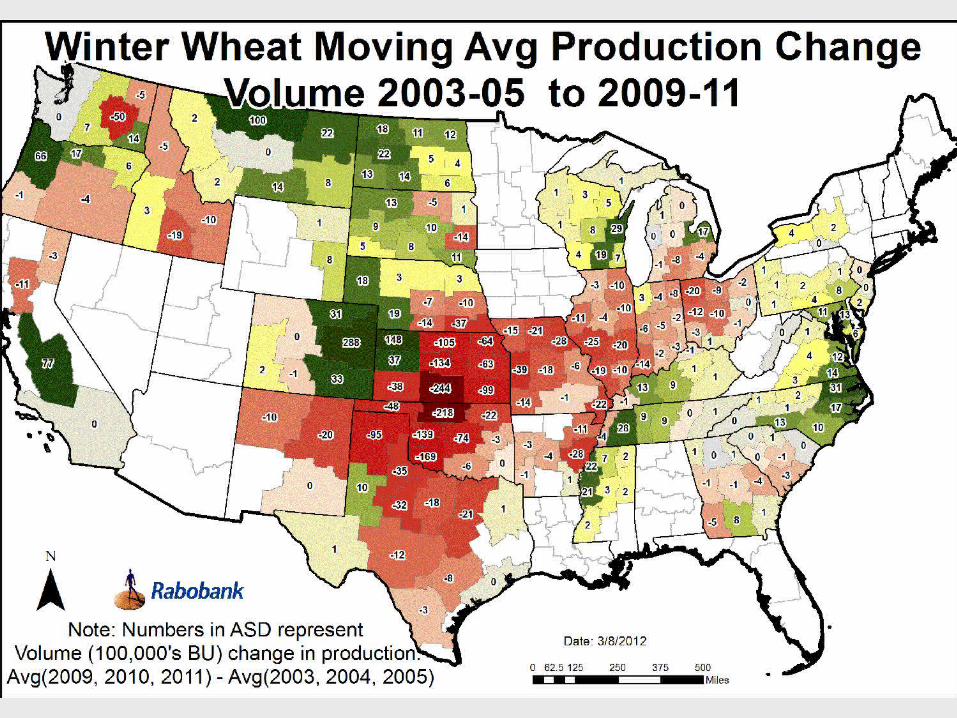

Supply For Global Wheat Trade Is Shifting

26

Incremental Production Moving to More Volatile Environments

What Does All of This Make Agriculture in 2013???

The Dog That Has Finally Caught the Car!

Outlook:

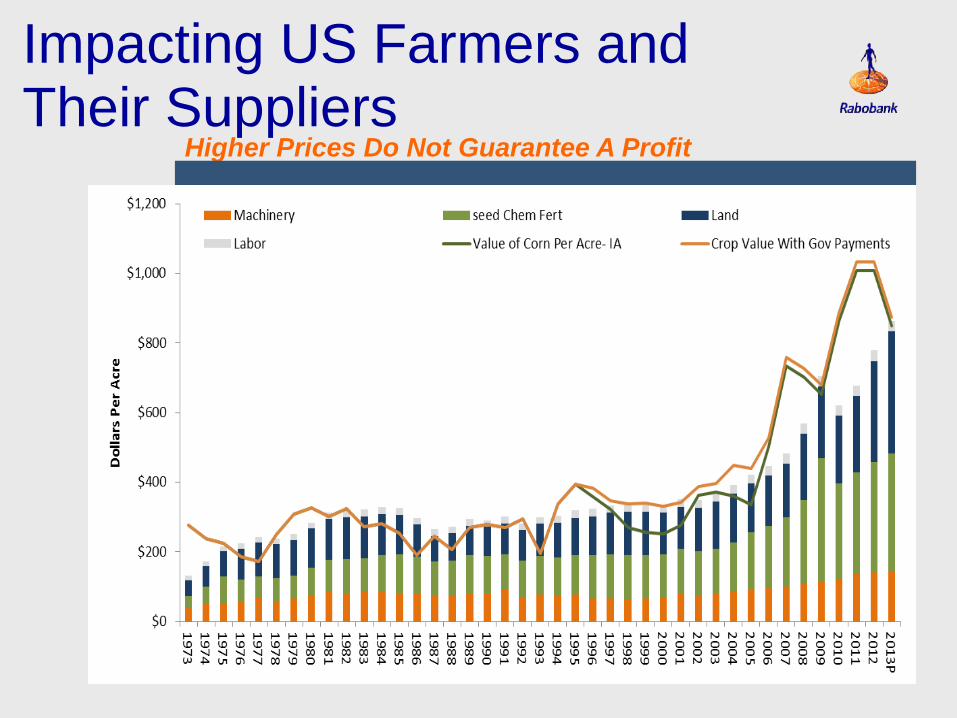

Higher Prices Do Not Guarantee A Profit

Impacting US Farmers and Their Suppliers

Confidence: The feeling just before you completely understand the situation

30

• Macro economy remains highly volatile• New trends of changing labor

rates and historically low cost of capital for developed economies

• New demand sources continue to grow• Developing economies demand

more protein• Food delivery systems force

changes• Although reduced from past

years, inelastic demand from bio fuels remains a key

• Supply will attempt to keep up• As crop production spreads

across the globe, weather will introduce additional volatility

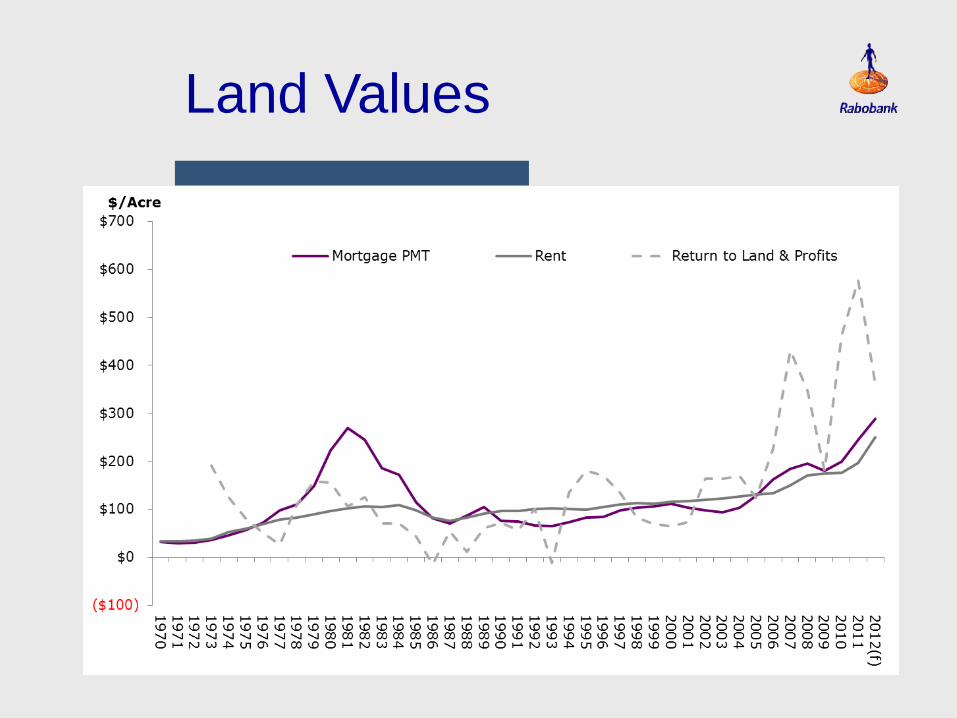

Land Values

32

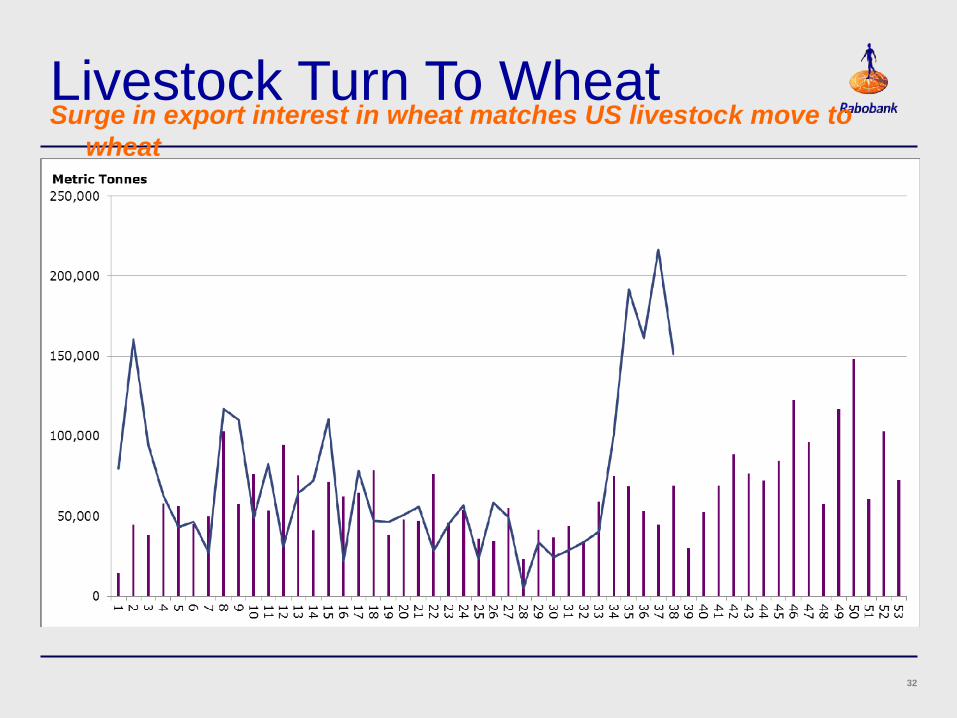

Livestock Turn To Wheat Surge in export interest in wheat matches US livestock move to

wheat

33

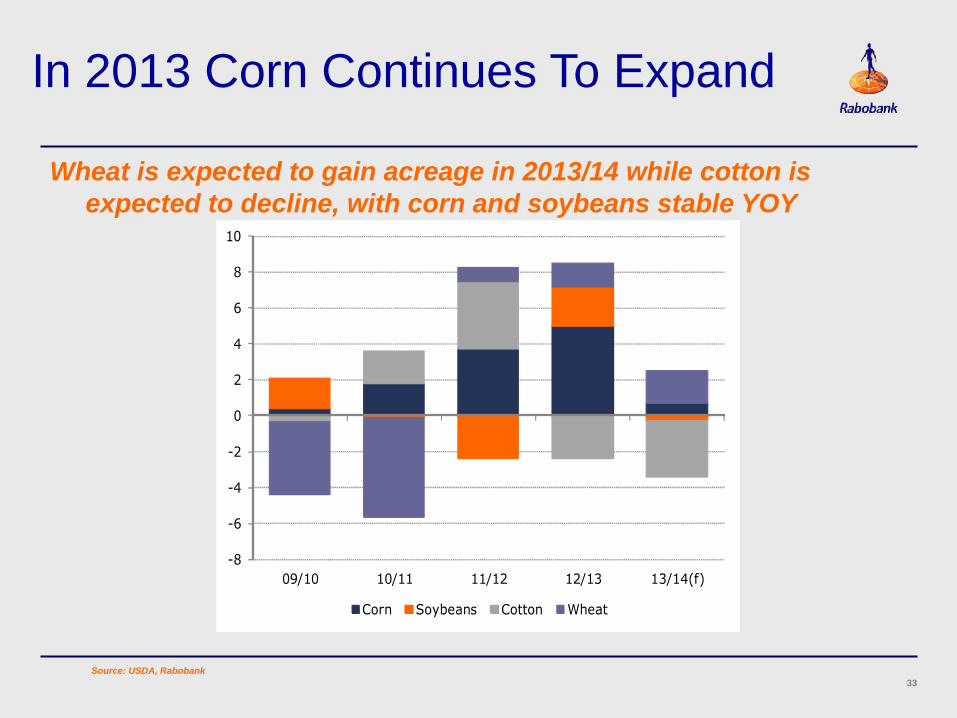

In 2013 Corn Continues To Expand

Wheat is expected to gain acreage in 2013/14 while cotton is expected to decline, with corn and soybeans stable YOY

Source: USDA, Rabobank

-8

-6

-4

-2

0

2

4

6

8

10

09/10 10/11 11/12 12/13 13/14(f)

Corn Soybeans Cotton Wheat

Click here to add imageClick here to add image

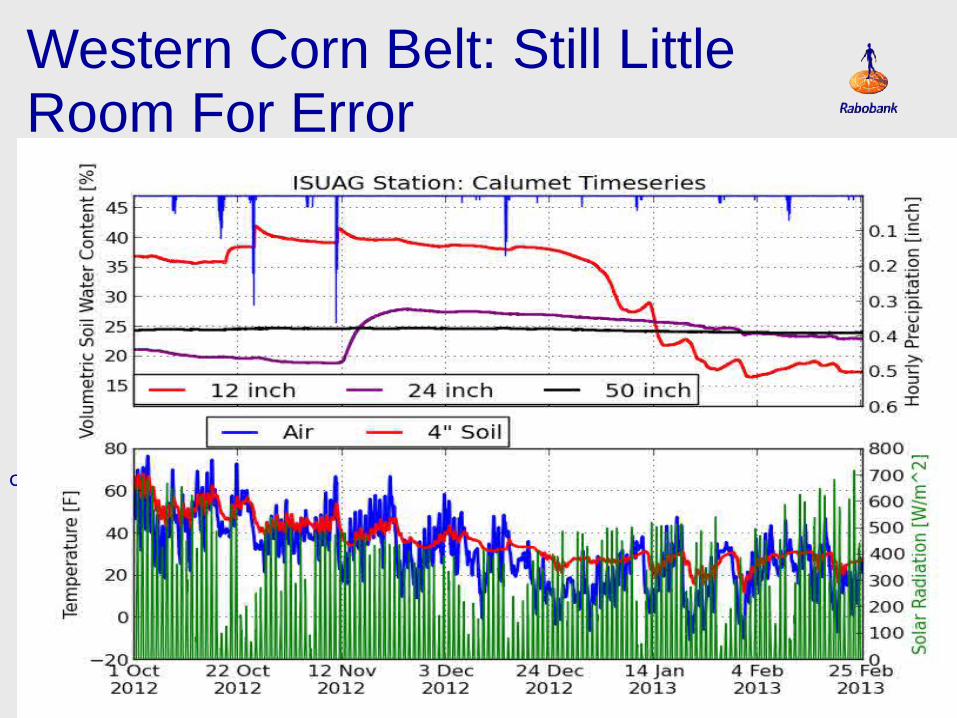

Western Corn Belt: Still Little Room For Error

Pivotal point in the future

Yield New Source of Uncertainty

50

70

90

110

130

150

170

190

10,000

15,000

20,000

25,000

30,000

35,000

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013(f) 2014(f) 2015(f) 2016(f) 2017(f)

Yield/ AcrePopulation/ Acre

Weighted PlantPopulation/AcreActual Yield

Expected yied basedon PPAYield at 1988 10-yearave weight/plantMax Capacity

Linear (Actual Yield)

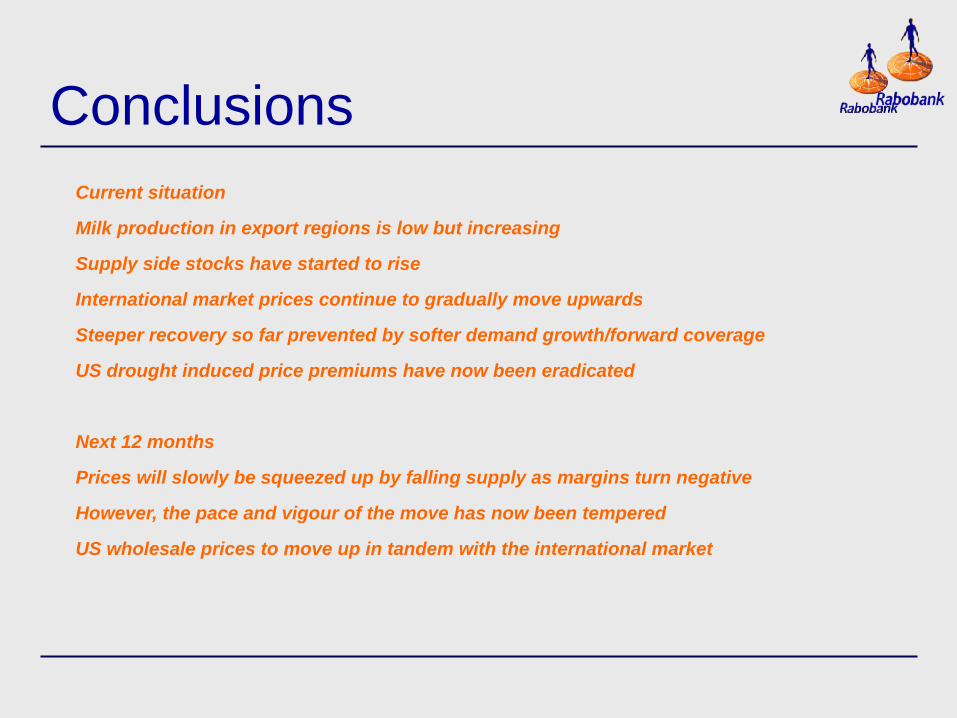

ConclusionsCurrent situation

Milk production in export regions is low but increasing

Supply side stocks have started to rise

International market prices continue to gradually move upwards

Steeper recovery so far prevented by softer demand growth/forward coverage

US drought induced price premiums have now been eradicated

Next 12 months

Prices will slowly be squeezed up by falling supply as margins turn negative

However, the pace and vigour of the move has now been tempered

US wholesale prices to move up in tandem with the international market

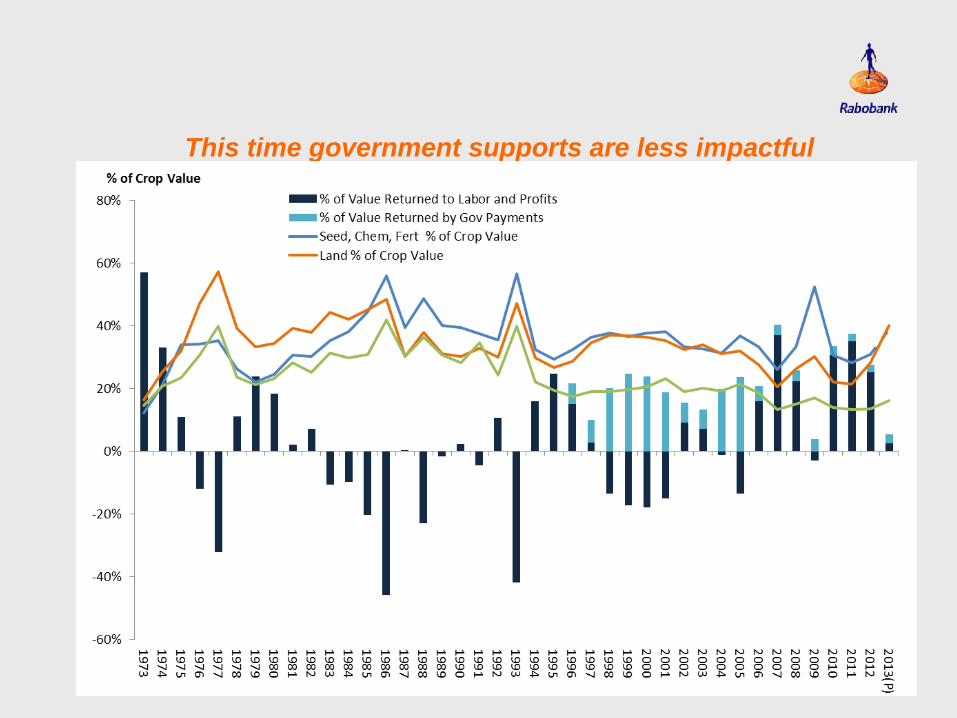

This time government supports are less impactful

All Wheat Accumulated Exports BY Week

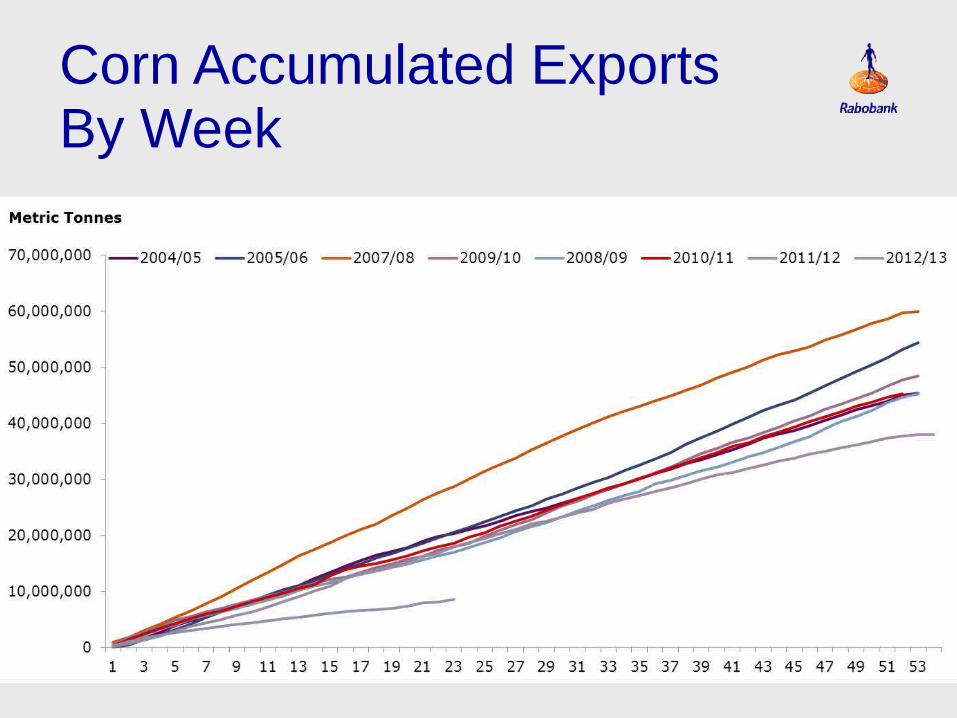

Corn Accumulated Exports By Week