Claims by acquirers sellers and unsuccessful bidders

68

Claims by Acquirers, Sellers, and Unsuccessful Bidders Presented by: Mary M. Bannister, Matthew S. Knoop and Robert V. Spake, Jr.

-

Upload

polsinelli-pc -

Category

Law

-

view

365 -

download

0

Transcript of Claims by acquirers sellers and unsuccessful bidders

Claims by Acquirers, Sellers, and

Unsuccessful Bidders

Presented by:

Mary M. Bannister, Matthew S. Knoop

and Robert V. Spake, Jr.

CONTRACT INDEMNITY

Robert V Spake, Jr. is an attorney in Polsinelli’s

Business Litigation department. Bob combines his

strong advocacy skills, business minded practice,

and specialized knowledge of Delaware corporate

law to partner with clients and effectively resolve

business disputes. His practice focuses on complex

business, derivative, securities, and shareholder

class action litigation in both federal and state

courts throughout the country.

Robert V. Spake, Jr.

Associate

Contract Indemnity

� Representations and warranties provide

information to the buyer and create the basic

structure for allocating risk between the buyer and

seller.

� Indemnification provisions provide the extent to

which a party will defend, hold harmless, and

indemnify the other party for breaches of those

representations and warranties.

Contract Indemnity

� Sellers want to limit contractual indemnity.

� Buyers want to expand contractual indemnity.

� Negotiate, among other things, the timing,

process, payment of claims, and limitations on

liability.

Contract Indemnity

� Often exclusive remedy (“EOR” or “exclusivity of

remedies”)

� Handful of common carve-outs

– Fraud

– Intentional misrepresentation

– Equitable remedies

Contract Indemnity

� Frequently negotiated claims

– Survival Period

• Timeframe for bringing indemnification claims

• 1 to 2 years most common

– Cap

• Overall limit on indemnity claims (set dollar

amount or percentage of the deal value)

Contract Indemnity

� Frequently negotiated claims

– Eligible Claim Threshold

• Excludes individual and unrelated claims under a

certain dollar amount

– Baskets and Deductibles

• Excludes immaterial claims

Contract Indemnity

� Frequently negotiated claims

– Sandbagging

• Addresses buyer’s remedies based on knowledge

of inaccuracy or breach before closing

– Escrow / Holdback

• Portion of purchase price to cover future

indemnification claims

BREACHES OF REPRESENTATIONS

AND WARRANTIES

Matt Knoop focuses his practice on preparing and trying civil litigation matters in state and federal courts throughout the country. His experience spans a variety of commercial litigation matters, including those related to mergers and acquisitions, data processing, telecommunications, and manufacturing.

Matthew S. Knoop

Shareholder

What are Reps and Warranties?

� Representations and warranties generally

serve to allocate risk among parties to

merger and acquisition agreements.

� Some are “boilerplate”, others are very

specific and negotiated vigorously.

What are Reps and Warranties?

� A representation within an agreement

induces the contract and historically

functioned as a “condition” of the contract.

� If false, the buyer could repudiate or rescind

the contract.

� Important protection against fraud

What are Reps and Warranties?

� Examples of representations in M&A

agreements:

– All contingent liabilities have been disclosed.

– Historical financial statements have been

prepared in accordance with GAAP.

What are Reps and Warranties?

A warranty is an assurance that a fact is true or

that certain acts have been performed

OR

A promise that something will happen in the

future

What are Reps and Warranties?

A warranty serves as a promise of indemnity if

a statement of fact is false.

Unlike a representation, the beneficiary of

the promise does not have to believe that the

statement is true.

The purpose of a warranty is to relieve the

beneficiary from the obligation of determining

whether the statement is true or not.

What are Reps and Warranties?

� Examples of warranties in M&A agreements:

– Seller is in good standing with all contractual

obligations.

– Seller has informed Buyer of all potentially

material claims that exist.

What are Reps and Warranties?

� Certain covenants also may be found in

M&A agreements (e.g., covenants that

individual sellers will not compete).

– A covenant is a promise that a party has (or has

not) done something or will (or will not) do

something.

What are Reps and Warranties?

� If a party materially breaches a covenant

contained in a merger or acquisition

agreement, it may excuse the performance

of the non-breaching party.

Negotiating Reps and Warranties

� In formulating transaction terms:

– Identify potential future losses

– Consider specific scenarios

– Categorize/prioritize risk

– What are appropriate remedies?

– Are there alternative means to resolve disputes?

� Negotiate appropriate reps and warranties

� Balance between the “ideal” contract and closing timely and in a cost-effective manner

Negotiating Reps and Warranties

� Reps and Warranties Insurance

– Available for both buyers and sellers

– Covers certain risks

– Reliable source of funds to satisfy claims

– Certainty for sellers

– Consider exclusions and coverage limits

– Cost may be prohibitive

Negotiating Reps and Warranties

� Protections for buyers:

– “Strong” representations and warranties

– Escrow released only after survival period(s) for

reps and warranties expire(s)

– Purchase price holdback or offset

– Liquidated damages provision

– Damages limitation provision “carve outs”

Negotiating Reps and Warranties

� Protections for sellers:

– “Weak” representations and warranties

– Damages limitation provisions

• “Basket” (i.e., deductible)

• Caps

• Exclusions

Litigating Reps and Warranties

� Potential claims and remedies may differ depending on whether the buyer/seller breached a representation, warranty or covenant

� Generally have a breach of contract claim

– Damages directly flowing from the breach

– Benefit of the bargain

– Unlikely to recover attorney fees unless explicitly provided for in the agreement

Litigating Representations

� Litigating representations:

– Often require only substantial compliance

– If intentionally false, claims for

• Deceit

• Fraud/fraudulent misrepresentation

– If unintentionally false, buyer/seller still may

have a negligent misrepresentation claim

Litigating Representations

� Proving fraud:

– Materiality

– Scienter (knowledge or conscious ignorance of

the falsity of a representation)

– Intent to induce reliance

– Justifiable reliance

Litigating Representations

� Broader remedies for a breach of a

representation:

– Rescission (return parties to pre-contract status)

• Must be timely

• Must tender all obtained through contract

• Often difficult post-acquisition/merger

(“unscrambling the eggs”)

Litigating Representations

� Remedies for breach of representation (continued)

– Alternatively, affirm the contract and sue for damages

• Compensatory damages

• Sometimes only out-of-pocket damages

– Potential for punitive damages (if permitted under applicable law) where proof of fraud or other intentional misconduct

– Potential to recover attorney fees

Litigating Warranties

� Litigating warranties:

– Generally require strict compliance

– In many states, a plaintiff may rely on a

warranty even if it knew that the statement was

not true when made

Litigating Warranties

� Easier to prove but more limited damages:

– Need not prove scienter or justifiable reliance

– Rescission and punitive damages not available

– Direct or benefit-of-the-bargain damages (or

negotiated remedy)

Litigation Considerations

� Is litigation worth it?

– What’s the amount at risk?

– What limitations on damages exist in the

subject agreement?

– Can the defendant(s) pay?

Litigation Considerations

� Expense

– Discovery (electronic, paper, testimony)

– Opportunity cost

– Adverse publicity (particularly if tried)

– Cost of enforcement (locating and collecting

funds to satisfy judgment)

Litigation Considerations

� Time bars

– Statutes of limitation may differ

– Survival period for representations and warranties

� Business operations and relationships

– Litigation disruption

– Any seller still employed?

– Industry

– Adverse effect on future mergers/acquisitions

SPECIFIC PERFORMANCE

Robert V Spake, Jr. is an attorney in Polsinelli’s

Business Litigation department. Bob combines his

strong advocacy skills, business minded practice,

and specialized knowledge of Delaware corporate

law to partner with clients and effectively resolve

business disputes. His practice focuses on complex

business, derivative, securities, and shareholder

class action litigation in both federal and state

courts throughout the country.

Robert V. Spake, Jr.

Associate

Specific Performance

� Equitable remedy – compelling a party to do

something, rather than suing for money damages.

� Enforced when there is no adequate remedy at law

(e.g., non-compete, non-solicit, and enforcement

of deal closing). Note: Delaware generally honors

a contractual stipulation that a breach of the

acquisition agreement will cause irreparable harm.

Specific Performance

� Specific performance is a common remedy in an

acquisition agreement.

� Protects a seller if the deal does not close due to a

buyer’s breach or a financing failure.

Specific Performance

� Drafting note

– In addition to including language that “The Parties agree

that money damages would not be a sufficient

remedy…”

– Consider the distinction between “shall be entitled to

seek specific performance” and “shall be entitled to

specific performance”

– Latter is more common and creates a stronger right to

specific performance

Specific Performance

� Buyer’s breach or buyer’s remorse

� Force closing

� Common in deals that do not require debt

financing, whether buyer is private equity or

strategic

� Strategic buyers may still offer specific

performance, even when there is debt financing

� Private equity less likely to do so

Specific Performance

� Financing failure

� Force buyer to draw equity and debt financing

(provided debt financing is available)

� If conditions to debt financing are met, seller can

sue buyer to require buyer to enforce the debt

commitment against the banks.

Specific Performance

� Full specific performance

� Conditional specific performance

� Limited specific performance

� No specific performance

Specific Performance

� Full specific performance – seller has the

unconditional right to enforce all of the buyer’s

obligations and close the deal.

Specific Performance

� Conditional specific performance

– Unconditional obligations and obligations conditioned

on funding

– Breadth of condition on funding

Specific Performance

� Limited specific performance

– Right to enforce the funding, but not the buyer’s

obligation to close the deal

Specific Performance

� No specific performance

– Seller has no right to specific performance

– Remedy is terminate the agreement and accept reverse

break-up fee or sue for money damages

LETTERS OF INTENT AND

MEMORANDA OF UNDERSTANDING

Mary Bannister is known for achieving successful

and timely closings of complex business

transactions. She provides strategic legal advice

whether the structure or negotiation involves

acquisition, divestiture, financing or strategic

alliance. Mary has more than 20 years of experience

in a wide range of transactions in the manufacturing

and service industries.

Mary M. Bannister

Shareholder

Letters of Intent

� Letters of Intent (LOI) set forth the key terms of the

proposed transaction as agreed on by the parties

in principle

� An LOI usually is entered to at the beginning of a

transaction before the drafting of transaction

documents

� An LOI usually is not intended to be binding with

respect to the terms of the proposed transaction

Should there be a Letter of Intent?

� No consensus among transaction attorneys as to

desirability

� There is a general understanding that they benefit

Buyers more than Sellers, due to exclusivity

provisions

� Sellers sometimes want them because they are

entered into at a time of Sellers’ greatest leverage

when the Seller can negotiate the best terms

Advantages

� Focuses the negotiations especially if terms are

complicated

� Identifies deal breakers early

� May create a “moral” commitment to the deal terms

making it difficult for a party to change terms later

� May start the waiting period for regulatory approvals (ex:

US antitrust approval)

� May contain important binding provisions (e.g.: exclusivity,

confidentiality)

� Helpful with prospective financing sources

Disadvantages

� Cost

� Negotiation may impair deal momentum

� May create disclosure obligations for public companies

� May unintentionally create a binding commitment

� May create a duty to negotiate in good faith, limiting the

ability to just walk away

� May create “moral” obligations, making it difficult to

change terms later or walk away

Unintentionally Creating a Binding

Agreement

� An LOI typically is intended to be a non-binding expression

of the parties’ then-current understanding of the structure

and terms of the proposed transaction

� Silence as to the non-binding nature may cause a court to

find that it is a binding agreement. The parties

clearlyshould state the LOI is non-binding or risk a breach of

contract claim

� Rarely, a party with great bargaining power insists on a fully

binding LOI

– Later issues arise if the parties cannot agree to the terms of a

definitive agreement; court can impose commercially reasonable

terms to enforce the LOI

Binding Provisions

� Parties may intend that certain provisions of

the LOI be binding.

� Examples:– Exclusivity

– Confidentiality

– Governing Law

– Expenses

– No Third Party Beneficiaries

– Due Diligence Procedures

– Break Up Fees

Binding Provisions

� The binding portions of the LOI must meet

the legal requirements for a binding contract

– Sufficiently certain terms

– Consideration

� Consider which binding provisions will

survive the termination of the LOI

Determination of Binding Nature

� Whether an LOI is binding or not is a question of intent. The language

of the LOI is good evidence of intent and properly should reflect the

intentions of the parties.

� Factors that courts consider:

– LOI language (most important)

– Context

– Are terms definite?

– Partial performance?

– Subject matter of the discussions

� Provisions that are intended to be binding should be specifically

identified and excluded from the portions of the letter that will be

deemed non-binding.

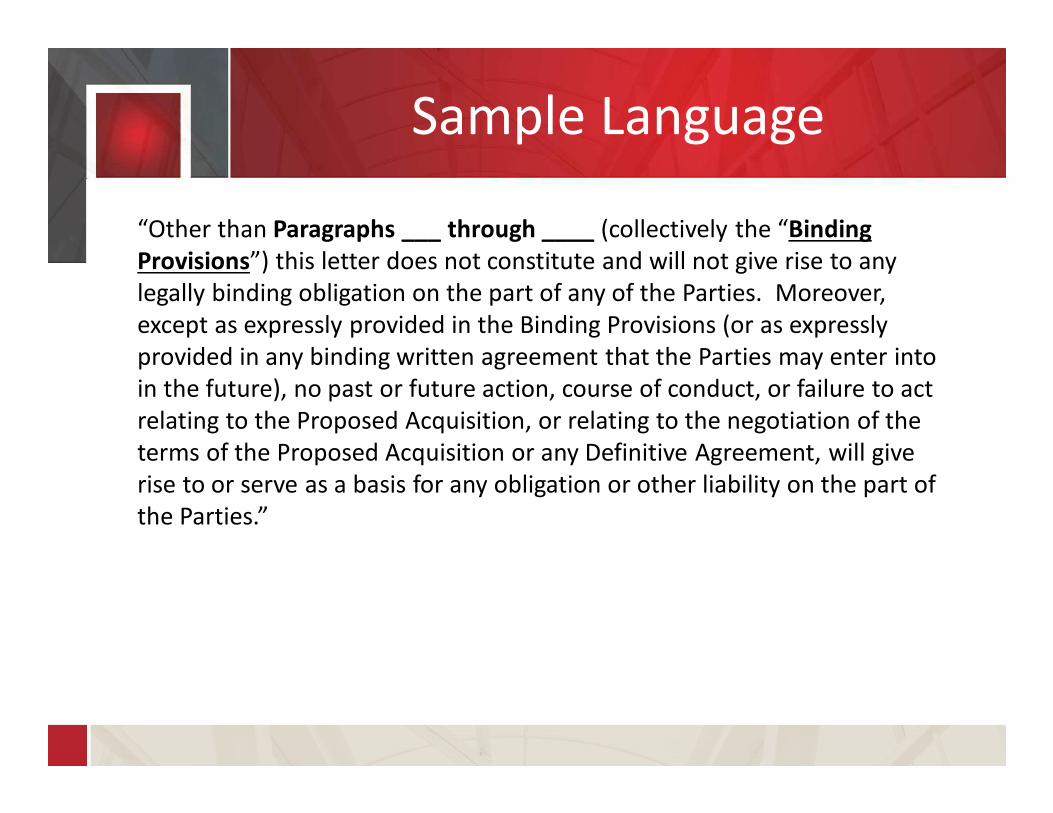

Sample Language

“Other than Paragraphs ___ through ____ (collectively the “Binding

Provisions”) this letter does not constitute and will not give rise to any

legally binding obligation on the part of any of the Parties. Moreover,

except as expressly provided in the Binding Provisions (or as expressly

provided in any binding written agreement that the Parties may enter into

in the future), no past or future action, course of conduct, or failure to act

relating to the Proposed Acquisition, or relating to the negotiation of the

terms of the Proposed Acquisition or any Definitive Agreement, will give

rise to or serve as a basis for any obligation or other liability on the part of

the Parties.”

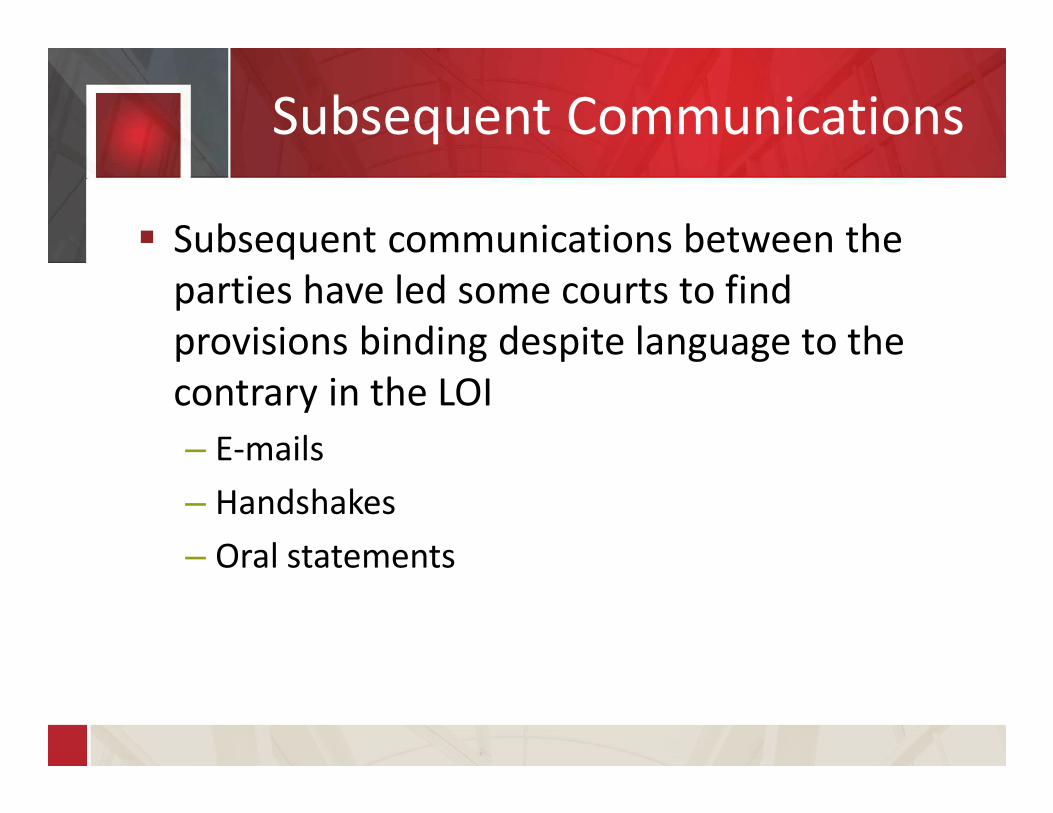

Subsequent Communications

� Subsequent communications between the

parties have led some courts to find

provisions binding despite language to the

contrary in the LOI

– E-mails

– Handshakes

– Oral statements

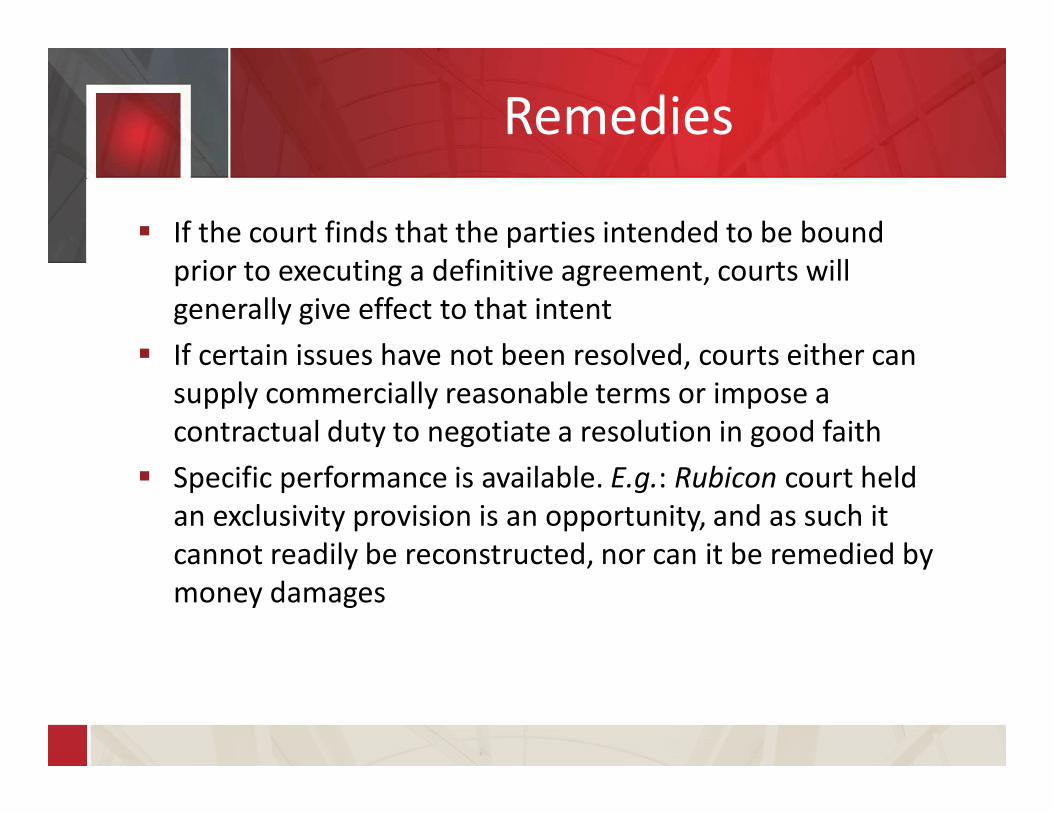

Remedies

� If the court finds that the parties intended to be bound

prior to executing a definitive agreement, courts will

generally give effect to that intent

� If certain issues have not been resolved, courts either can

supply commercially reasonable terms or impose a

contractual duty to negotiate a resolution in good faith

� Specific performance is available. E.g.: Rubicon court held

an exclusivity provision is an opportunity, and as such it

cannot readily be reconstructed, nor can it be remedied by

money damages

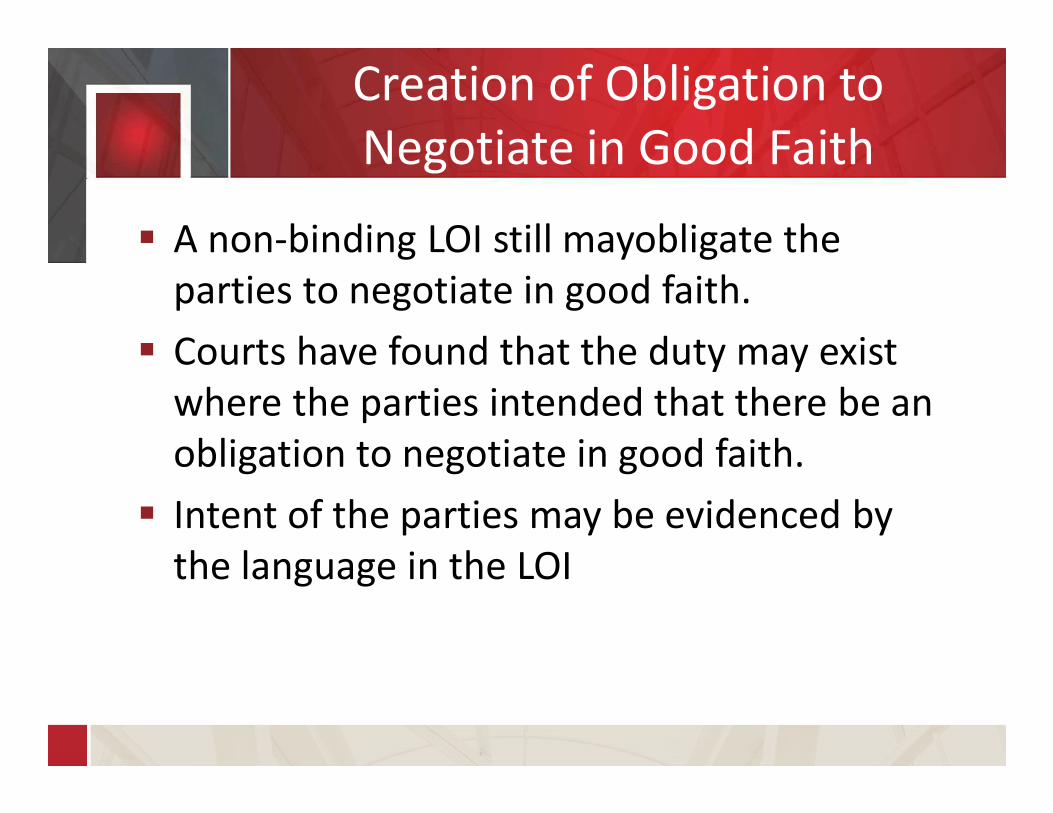

Creation of Obligation to

Negotiate in Good Faith

� A non-binding LOI still mayobligate the

parties to negotiate in good faith.

� Courts have found that the duty may exist

where the parties intended that there be an

obligation to negotiate in good faith.

� Intent of the parties may be evidenced by

the language in the LOI

Disclaimer of Obligation to

Negotiate in Good Faith

Sample Language

“The parties hereby waive and disclaim the

obligation to negotiate in good faith in

furtherance of its obligations under this letter

of intent.”

Disclaimers

� If adding a disclaimer of the obligation to

negotiate in good faith:

– Include the disclaimer in the binding provisions

– Consider whether it should be disclaimed by

both parties or only one party

Inclusion of a

Good Faith Obligation

� Include any obligation to negotiate in good faith in the

binding provisions

� If you include an obligation to negotiate in good faith:

– No need to complete the transaction to fulfill the duty

– But if parties fail to come to an agreement they may

have to show they did not act in “bad faith”

– Consider adding a definition of “bad faith”

� “radio silence is not negotiating in good faith.” See,

Rubicon

Global Asset Capital v. Rubicon

� Global bid to acquire 12 office buildings owned by Rubicon

contemplating a sale through a bankruptcy supervised auction

� Parties entered into an LOI with an affirmative obligation to negotiate

in good faith to complete a Plan Support Agreement and a no- shop

clause (exclusivity) as well as confidentiality agreements

� Del. Ch. Court stated that it regarded letters of intent, as well as the

duty to negotiate in good faith, as rights of commercial importance and

rights that the Court would protect

� The Court noted that to the extent that parties wish to enter into

nonbinding letters of intent, they can do so by expressly stating that the

agreement is to be nonbinding

� Global Asset Capital, LLC v. Rubicon US Reit, Inc., C.A. No. 5071-VCL

(Del. Ch. Nov. 16, 2009)

“Bad Faith”

� Examples of what could constitute Bad Faith

– Violate exclusivity clause

– Lack of cooperation in due diligence

– Failure to use reasonable efforts to obtain

financing

– Other actions specific to your transaction

Silence Regarding Good Faith

� Depending on the applicable state law, there

may be a duty to negotiate in good faith

even where there is no express obligation to

negotiate in good faith.

� In general, the circumstances must show

that the parties intended such an obligation

even though the LOI is silent.

Remedies – Money Damages

� Generally limited to money damages

– Reliance Damages (expenses of negotiation)

– Expectation Damages (lost profits from failed

transaction)

• Would the agreement have been reached but for

the breaching party’s bad faith negotiations?

Remedies - Specific Performance

� Specific performance generally is not

ordered.

� Exception for where the duty requires a

party to take specified actions such as

providing information

SIGA Technologies Case

� Under Delaware law, agreements to negotiate in good faith, even in

preliminary agreements, are enforceable.

� Proposing deal terms that deviate materially from terms set out in a

term sheet may be deemed to evidence bad faith in negotiations;

� If an obligation to negotiate in good faith is breached, and the

aggrieved party is able to establish that a final, binding agreement

would have been reached absent the other’s bad faith negotiations, the

aggrieved party is entitled to “expectation” or “benefit of the bargain”

damages (e.g., lost profits) rather than simply “reliance” damages (e.g.,

costs and expenses of the failed negotiation).

� Per the court, bad faith “contemplates a state of mind affirmatively

operating with furtive design or ill will.”

� SIGA Technologies v. PharmAthene, 67 A.3d 330 (Del. 2013).

Memoranda of Understanding

and Term Sheets

� Same rules apply as with Letters of Intent.

� No matter the name of the document, have

an attorney review

� Even if unsigned, a disclaimer of intention to

be bound and disclaimer of any legal

obligation of the parties should be included

� If there are binding provisions, best practice

is to use a signed letter of intent

Claims by Acquirers, Sellers and

Unsuccessful Bidders

Thank you, and we hope that you will join us

for our next webinar on March 22, 2016

entitled, M&A Stockholder Claims.

real challenges. real answers. sm

Contact Information

Polsinelli PCwww.polsinelli.com

� Follow us on: – Twitter: @polsinelli– LinkedIn: https://www.linkedin.com/company/polsinelli?trk=company_logo– SlideShare: http://www.slideshare.net/Polsinelli_PC

real challenges. real answers. sm

About Polsinelli

Polsinelli provides this material for informational purposes only. The material provided herein is general and is not intended to be legal advice. Nothing herein should be relied upon or used without consulting a lawyer to consider your specific circumstances, possible changes to applicable laws, rules and regulations and other legal issues. Receipt of this material does not establish an attorney-client relationship.

Polsinelli is very proud of the results we obtain for our clients, but you should know that past results do not guarantee future results; that every case is different and must be judged on its own merits; and that the choice of a lawyer is an important decision and should not be based solely upon advertisements. © 2015 Polsinelli PC. In California, Polsinelli LLP.

Polsinelli is a registered mark of Polsinelli PC

Polsinelli is an Am Law 100 firm with more than 750 attorneys in 17 offices, serving corporations, institutions, entrepreneurs and individuals nationally. Ranked in the top five percent of law firms for client service*, the firm has risen more than 100 spots in Am Law's annual firm ranking over the past six years. Polsinelli attorneys provide practical legal counsel infused with business insight, and focus on health care and life sciences, financial services, real estate, technology and biotech, mid-market corporate, and business litigation. Polsinelli attorneys have depth of experience in 100 service areas and 70 industries. The firm can be found online at www.polsinelli.com. Polsinelli PC. In California, Polsinelli LLP.

*2016 BTI Client Service A-Team Report