CITIBANK CANADA - · PDF fileInterest Rate Risk in the Banking Book ... CITIBANK CANADA ......

37

CITIBANK CANADA Basel III Pillar 3 Disclosures As at December 31, 2014

Transcript of CITIBANK CANADA - · PDF fileInterest Rate Risk in the Banking Book ... CITIBANK CANADA ......

CITIBANK CANADA

Basel III Pillar 3 Disclosures As at December 31, 2014

CITIBANK CANADA

Table of Contents

1. Scope of Application .............................................................................................................................1

Qualitative disclosures ....................................................................................................................................1

2. Capital Structure ..................................................................................................................................2

Qualitative disclosures ....................................................................................................................................2 Quantitative disclosures ..................................................................................................................................2

3. Capital Adequacy ..................................................................................................................................3

Qualitative disclosures ....................................................................................................................................3 Quantitative disclosures ..................................................................................................................................5

4. Credit Risk – General Disclosures for all Banks ...............................................................................6

Qualitative disclosures ....................................................................................................................................6 Management of credit risk .......................................................................................................................6

Quantitative disclosures ..................................................................................................................................7

5. Credit Risk – Disclosures for Portfolios subject to the Standardized Approach and Supervisory Risk Weights in the IRB Approaches ......................................................................................................11

6. Credit Risk Mitigation ........................................................................................................................12

Qualitative disclosures ................................................................................................................................. 12 Quantitative disclosures ............................................................................................................................... 13

7. General Disclosures for Exposures Related to Counterparty Credit Risk ....................................14

Qualitative disclosures ................................................................................................................................. 14 Quantitative disclosures ............................................................................................................................... 15

8. Securitization .......................................................................................................................................15

9. Market Risk – Disclosures for Banks using the Internal Models Approach (IMA) for Trading Portfolios ....................................................................................................................................................16

Qualitative disclosures ................................................................................................................................. 16 Quantitative disclosures ............................................................................................................................... 19

10. Operational Risk .................................................................................................................................20

11. Equities – Disclosure for Banking Book Positions ...........................................................................21

12. Interest Rate Risk in the Banking Book ...........................................................................................22

Qualitative disclosures ................................................................................................................................. 22 Quantitative disclosures ............................................................................................................................... 22

13. Remuneration ......................................................................................................................................23

Governance .................................................................................................................................................. 23

CITIBANK CANADA

Table of Contents

Citi’s Compensation Philosophy .................................................................................................................. 24 Senior Management and Other Material Risk Takers .................................................................................. 24 Remuneration Structures ............................................................................................................................. 25 Performance measurement ......................................................................................................................... 29 Core Principle Statements ........................................................................................................................... 31 Quantitative disclosures ............................................................................................................................... 32

CITIBANK CANADA

1. Scope of Application

Qualitative disclosures This document addresses the Basel III Pillar 3 disclosure requirements for Citibank Canada (the “Bank”) and all its subsidiaries. There are no differences in the basis of consolidation for accounting and regulatory purposes. All intercompany transactions and balances have been eliminated. There are no specific restrictions on the transfer of funds or regulatory capital of the Bank’s subsidiaries except that necessary approvals from the Board of Directors and/or officers of the relevant entities are required prior to making changes and an OSFI regulated subsidiary of the Bank is required to follow the OSFI guidelines relating to regulatory capital.

The Bank is a wholly-owned indirect subsidiary of Citibank, N.A. and is licensed to operate as a bank in Canada with full banking powers under the Bank Act as a foreign bank subsidiary. The Bank’s immediate parent is Citibank Overseas Investment Corporation and the ultimate parent is Citigroup Inc.

The following disclosures have been prepared purely for explaining the basis on which the Bank has prepared and disclosed information about capital requirements, the management of certain risks, remuneration of senior management and for no other purpose. They do not constitute any form of financial statements and must not be relied upon in making any investment or judgment on the Bank or its parents, Citigroup Inc. and Citibank, N.A. Except as otherwise indicated, financial information presented in Canadian dollars has been rounded to the nearest thousand.

Page 1 of 34

CITIBANK CANADA

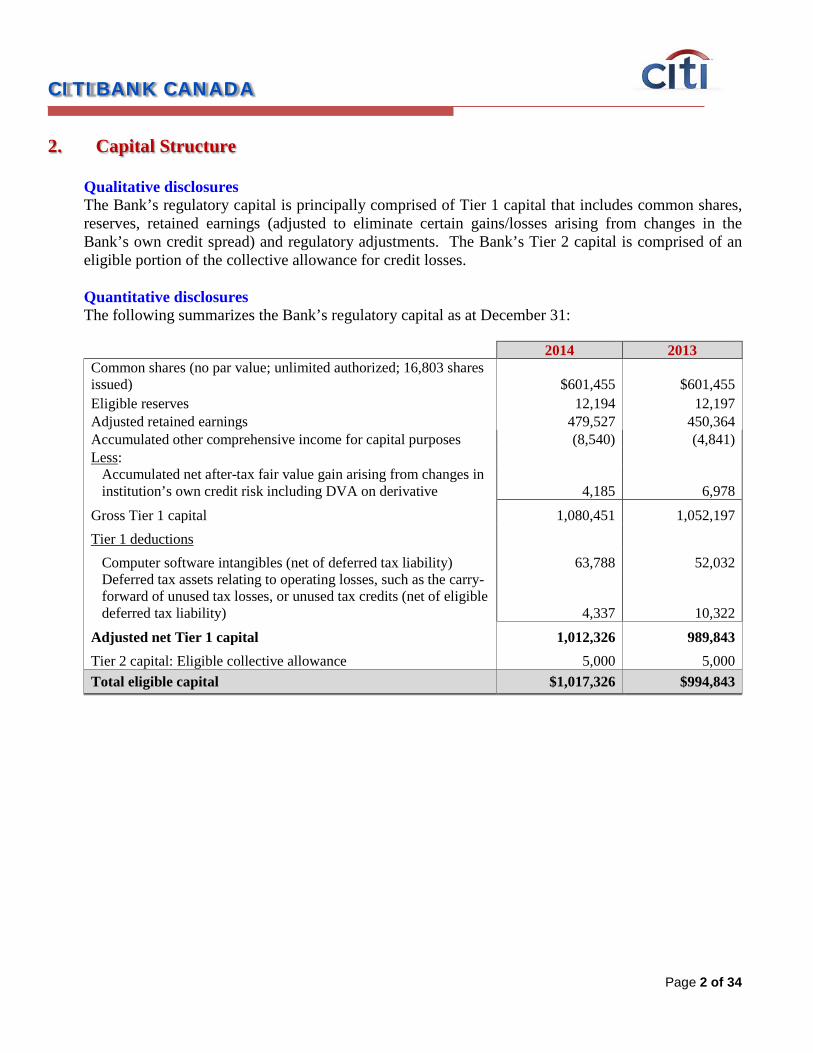

2. Capital Structure

Qualitative disclosures The Bank’s regulatory capital is principally comprised of Tier 1 capital that includes common shares, reserves, retained earnings (adjusted to eliminate certain gains/losses arising from changes in the Bank’s own credit spread) and regulatory adjustments. The Bank’s Tier 2 capital is comprised of an eligible portion of the collective allowance for credit losses.

Quantitative disclosures The following summarizes the Bank’s regulatory capital as at December 31:

2014 2013

Common shares (no par value; unlimited authorized; 16,803 shares issued) $601,455

$601,455

Eligible reserves 12,194 12,197 Adjusted retained earnings 479,527 450,364 Accumulated other comprehensive income for capital purposes (8,540) (4,841) Less:

Accumulated net after-tax fair value gain arising from changes in institution’s own credit risk including DVA on derivative 4,185 6,978

Gross Tier 1 capital 1,080,451 1,052,197 Tier 1 deductions

Computer software intangibles (net of deferred tax liability) 63,788 52,032 Deferred tax assets relating to operating losses, such as the carry-forward of unused tax losses, or unused tax credits (net of eligible deferred tax liability) 4,337 10,322

Adjusted net Tier 1 capital 1,012,326 989,843 Tier 2 capital: Eligible collective allowance 5,000 5,000 Total eligible capital $1,017,326 $994,843

Page 2 of 34

CITIBANK CANADA

3. Capital Adequacy

Qualitative disclosures Effective January 1, 2013, the Bank has adopted OSFI’s new guidelines which are based on “Basel III: A global regulatory framework for more resilient banks and banking systems – December 2010 (revised June 2011)” known as Basel III, issued by the Basel Committee on Banking Supervision (BCBS). Together with “Basel III International Framework for liquidity risk measurement standards and monitoring”, this presents the Basel Committee’s reforms to strengthen global capital and liquidity rules with the goal of promoting a more resilient banking sector.

OSFI’s new BCAR guidelines incorporate, among other changes, a new component of RWA i.e. Credit Valuation Adjustment (“CVA”) capital charge. The implementation of this new capital charge was January 1, 2014.

The Bank’s capital ratios under Basel III have been calculated using the Full Standardized Approach. Capital levels for Canadian banks are regulated pursuant to above guidelines. Regulatory capital is allocated to the following tiers: Common equity Tier 1 (CET1), Tier 1 and Total capital. Tier 1 capital is principally comprised of the more permanent components of capital and consists primarily of common shares, reserves and retained earnings. Tier 2 capital is comprised of an eligible portion of the total collective allowance for credit losses. Total capital is defined as the total of Tier 1 and Tier 2 capital less certain deductions as prescribed by OSFI.

The Bank has a capital management process in place to measure, deploy and monitor its available capital and assess its adequacy. The capital management process aims to achieve several objectives – exceed regulatory requirements and maintain a cost-effective capital structure that balances strong capital ratios with adequate returns to the Bank’s shareholder.

Appropriate levels of the Bank’s key capital ratios are maintained on a daily basis in compliance with OSFI’s guidelines. The Bank exceeded these regulatory capital requirements throughout 2014 and 2013. The Board of Directors of the Bank (Board) reviews these ratios on a quarterly basis.

Regulatory ratios are calculated by dividing CET1, Tier 1 and Total capital by risk-weighted assets (RWA). The calculation of RWA is determined by the OSFI-prescribed rules relating to on-balance sheet and off-balance sheet exposures and includes amounts for the market risk exposure associated with the Bank’s trading portfolios and operational risk exposure associated with the risk of loss resulting from inadequate or failed internal processes, people and systems, or from external events.

Page 3 of 34

CITIBANK CANADA

In addition, OSFI formally establishes risk-based capital minimums for deposit-taking institutions. These minimums are currently a CET1 capital ratio of 7% (2013 – 7.0%), Tier 1 capital ratio of 8.5% (2013 – 8.5%) and a Total capital ratio of 10.5% (2013 – 10.5%). In addition to the Tier 1 and Total capital ratios, Canadian banks are also required to ensure that their Leverage Ratio (“LR”), which is calculated by dividing Tier I capital by Total Exposure, exceeds a minimum. The calculation of Total Exposure is determined by OSFI-prescribed rules and includes on-balance sheet exposures, derivatives exposures, securities financing transaction exposures and other off-balance sheet exposures. The minimum LR requirement for the Bank is 4%.

Within our capital management framework, the Bank has an internal capital adequacy assessment process (ICAAP) that sets internal capital targets consistent with its risk profile, business plans and operating environment. The ICAAP is the primary process used by Citibank Canada for the assessment of capital levels in both normal and stressed operating conditions, taking into account internal and external factors and material risks that may impact Citibank Canada’s capital levels, as well as management’s determination as to capital adequacy. The Bank’s ICAAP framework is based on quantitative capital goals to ensure that it has sufficient capital to meet its strategic goals and all stakeholders are adequately protected from stress events. These goals include:

1. Capital Strength: Quantitative Capital Goals

• Base Case Capital: Maintain actual and forecasted capital levels above fully phased-in Basel III internal targets.

• Stressed Case Capital: Maintain projected capital ratios, under stress scenarios, above fully phased-in Basel III internal capital thresholds (as defined in the ICAAP process).

• Available Financial Resources (AFR) vs. Risk Capital: Maintain a level of AFR defined as equal to Citibank Canada’s Basel III Tier 1 Capital, above its Risk Capital inclusive of the Risk Capital buffer. Risk Capital usage by type (Credit, Market, and Operational) must be tracked and monitored.

• Liquidity: Maintain actual and forecasted base liquidity levels above internal thresholds, defined as (i) Liquidity Coverage Ratio (LCR) and (ii) Liquidity Scenario 2 / Severe Market Disruption (S2).

2. Earnings Power: Citibank Canada Risk Appetite Ratio • Citibank Canada calibrates risk-taking relative to the gross earnings power and expense base

such that the potential losses arising from a moderate stress event can be covered by the expected pre-tax net earnings, without compromising its capital. The Risk Appetite Ratio (RAR) is the ratio of earnings before taxes (the numerator) and the stress losses under a 1-in-10 year stress scenario (the denominator).

Market Risk, Operational Risk, Liquidity Risk, Credit Risk and Pillar 2 risks are the risk elements included in the Bank’s ICAAP framework.

Page 4 of 34

CITIBANK CANADA

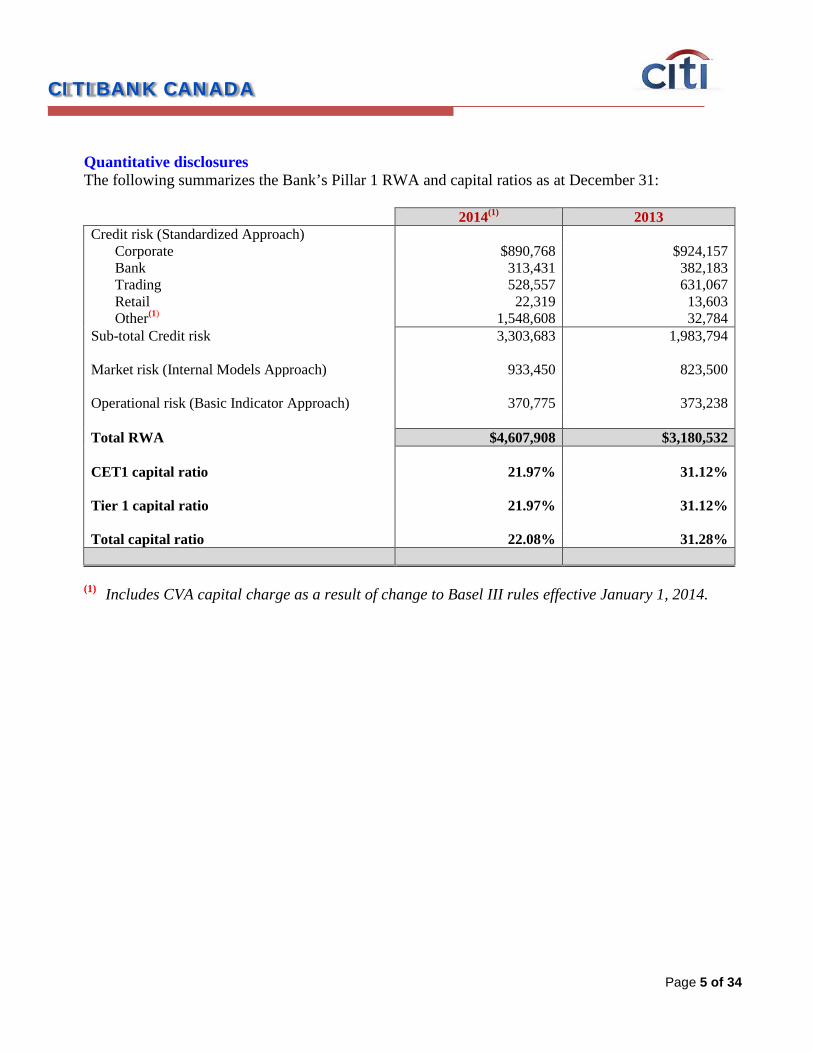

Quantitative disclosures The following summarizes the Bank’s Pillar 1 RWA and capital ratios as at December 31:

2014(1) 2013 Credit risk (Standardized Approach)

Corporate $890,768 $924,157 Bank 313,431 382,183 Trading 528,557 631,067 Retail 22,319 13,603 Other(1) 1,548,608 32,784

Sub-total Credit risk 3,303,683 1,983,794 Market risk (Internal Models Approach) 933,450 823,500 Operational risk (Basic Indicator Approach)

370,775

373,238

Total RWA $4,607,908 $3,180,532 CET1 capital ratio 21.97% 31.12% Tier 1 capital ratio 21.97% 31.12% Total capital ratio 22.08% 31.28%

(1) Includes CVA capital charge as a result of change to Basel III rules effective January 1, 2014.

Page 5 of 34

CITIBANK CANADA

4. Credit Risk – General Disclosures for all Banks

Qualitative disclosures Credit risk is the potential for financial loss resulting from the failure of a borrower or counterparty to honor its financial or contractual obligations. Credit risk arises in many of Citibank Canada’s business activities, including:

• Wholesale lending; • Capital markets derivative transactions; and • Repurchase agreements and reverse repurchase transactions. Credit risk also arises from settlement and clearing activities, when Citibank Canada transfers an asset in advance of receiving its counter-value or advances funds to settle a transaction on behalf of a client.

Management of credit risk Credit risk is one of the most significant risks Citibank Canada faces as an institution. As a result, the Bank has a well established framework in place for managing credit risk across all businesses. This includes a defined risk appetite, credit limits and credit policies, which are approved by the Board of Directors. The Bank’s credit risk management also includes processes and policies with respect to problem recognition, including, “watch lists”, portfolio review, updated risk ratings and classification triggers.

The Bank’s credit policies are based on the following fundamental principles: • Joint business and independent risk management responsibility for managing credit risks; • A single center of control for each credit relationship, which coordinates credit activities with

each client; • Portfolio limits to ensure diversification and maintain risk/capital alignment; • A minimum of two authorized credit officer signatures required on most extensions of credit, one

of which must be from a credit officer in credit risk management; • Risk rating standards, applicable to every obligor and facility; and • Consistent standards for credit origination documentation and remedial management

The maintenance of accurate and consistent risk ratings across the Corporate credit portfolio facilitates the comparison of credit exposure across all lines of business, geographic regions and products. Counterparty risk ratings reflect an estimated probability of default for a counterparty and are derived primarily through the use of validated statistical models, scorecard models and external agency ratings (under defined circumstances), in combination with consideration of factors specific to the obligor or market, such as management experience, competitive position and regulatory environment. Facility risk ratings are assigned that reflect the probability of default of the obligor and factors that affect the loss-given-default of the facility, such as support or collateral. Internal obligor ratings that generally correspond to BBB and above are considered investment grade, while those below are considered non-investment grade. Senior management of the Bank evaluates proposed business based on the Bank’s target market, return requirements, and capital levels and

Page 6 of 34

CITIBANK CANADA

must approve credits above certain limits. The Board of Directors approves all Credit Officer and Senior Credit Officer appointments. A series of checks and balances, including multiple reviews of credit approvals and independent reviews of credit performance by Internal Audit group, is in place to ensure the Bank’s marketing objectives are balanced against its credit objectives. Controls have been established to ensure that accountability for each aspect of the credit process is maintained. The portfolio and exceptions to industry and counterparty limits are reviewed at least quarterly with the Board.

Extensions of credit to individual relationships are subject to approvals, limits and monitoring procedures. In measuring the extension of credit to the client, the amount of risk on a derivative instrument is determined by the sum of the current replacement cost of the instrument and the potential increase in the replacement cost over the remaining life of the instrument.

At each reporting date the Bank assesses whether there is objective evidence that financial assets not carried at fair value through profit or loss are impaired. A financial asset is impaired when objective evidence demonstrates that a loss event has occurred after the initial recognition of the asset(s), and that the loss event has an impact on the future cash flows of the asset(s) that can be estimated reliably. The Bank considers evidence of impairment for loans at both an individual asset and collective level. All individually significant loans are assessed for specific impairment. All individually significant loans found not to be specifically impaired are then collectively assessed for any impairment that has been incurred but not yet identified. Loans that are not individually significant are collectively assessed for impairment by grouping together loans with similar risk characteristics. In assessing collective impairment the Bank uses statistical modelling of historical trends of the probability of default, timing of recoveries and the amount of loss incurred, adjusted for management’s judgement as to whether current economic and credit conditions are such that the actual losses are likely to be greater or less than suggested by historical modelling. Default rates, loss rates and the expected timing of future recoveries are regularly benchmarked against actual outcomes to ensure that they remain appropriate.

Quantitative disclosures The following table represents the Bank’s total gross credit risk exposures for financial instruments measured as the amount outstanding as at December 31:

2014 2013 Outstanding

amount Year to date

average Outstanding

amount Year to date

average Cash resources $306,455 $213,087 $492,820 $348,680 Trading securities 2,325,468 2,025,082 2,127,216 1,969,027 Available for sale securities 368,241 285,648 77,959 69,371 Loans, net of allowance for credit losses 1,814,747 1,432,204 1,387,680 1,383,852 Derivative financial instruments 5,453,191 4,789,732 4,636,180 5,408,775 Other assets 1,072,334 803,921 979,183 930,293 Total $11,340,436 $9,549,674 $9,701,038 $10,109,998

Page 7 of 34

CITIBANK CANADA

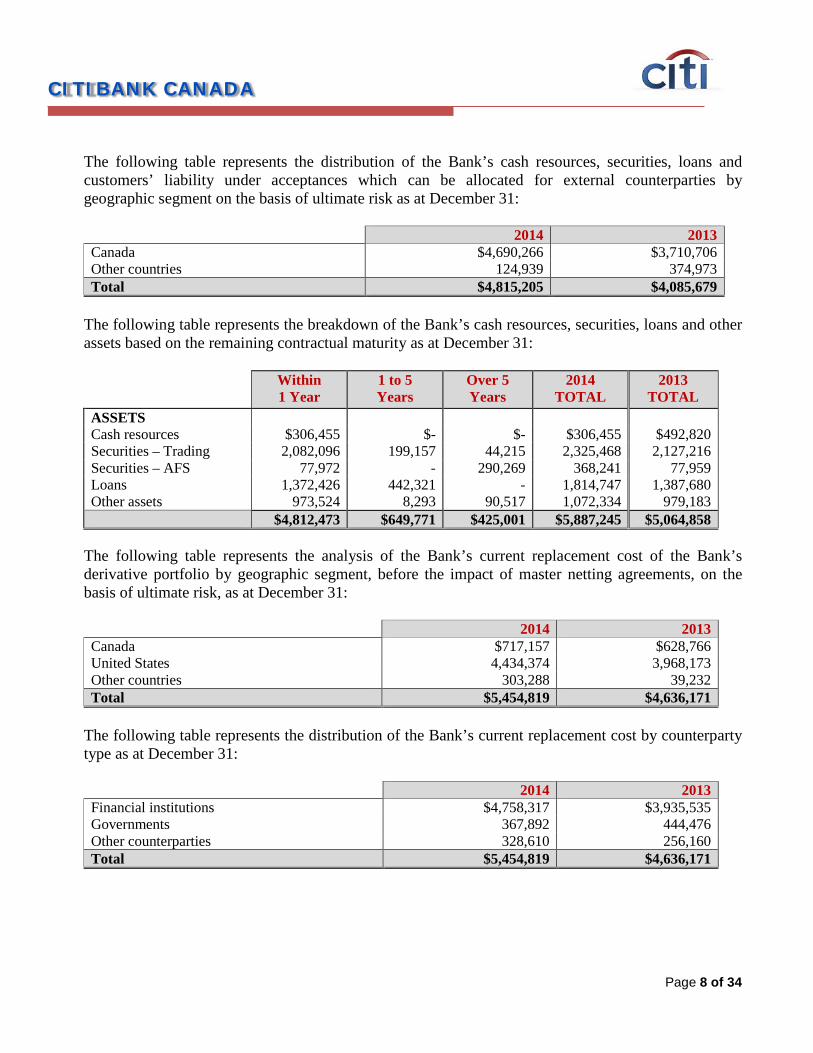

The following table represents the distribution of the Bank’s cash resources, securities, loans and customers’ liability under acceptances which can be allocated for external counterparties by geographic segment on the basis of ultimate risk as at December 31:

2014 2013 Canada $4,690,266 $3,710,706 Other countries 124,939 374,973 Total $4,815,205 $4,085,679

The following table represents the breakdown of the Bank’s cash resources, securities, loans and other assets based on the remaining contractual maturity as at December 31:

Within

1 Year 1 to 5 Years

Over 5 Years

2014 TOTAL

2013 TOTAL

ASSETS Cash resources $306,455 $- $- $306,455 $492,820 Securities – Trading 2,082,096 199,157 44,215 2,325,468 2,127,216 Securities – AFS 77,972 - 290,269 368,241 77,959 Loans 1,372,426 442,321 - 1,814,747 1,387,680 Other assets 973,524 8,293 90,517 1,072,334 979,183 $4,812,473 $649,771 $425,001 $5,887,245 $5,064,858

The following table represents the analysis of the Bank’s current replacement cost of the Bank’s derivative portfolio by geographic segment, before the impact of master netting agreements, on the basis of ultimate risk, as at December 31:

2014 2013 Canada $717,157 $628,766 United States 4,434,374 3,968,173 Other countries 303,288 39,232 Total $5,454,819 $4,636,171

The following table represents the distribution of the Bank’s current replacement cost by counterparty type as at December 31:

2014 2013 Financial institutions $4,758,317 $3,935,535 Governments 367,892 444,476 Other counterparties 328,610 256,160 Total $5,454,819 $4,636,171

Page 8 of 34

CITIBANK CANADA

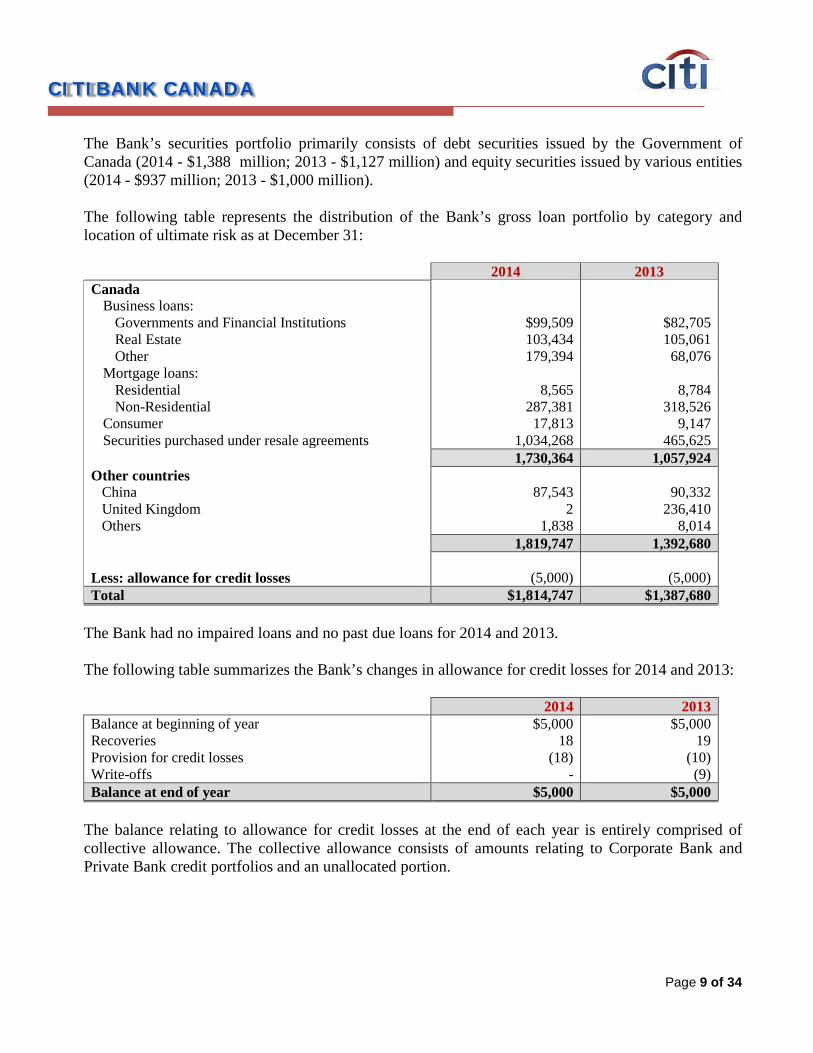

The Bank’s securities portfolio primarily consists of debt securities issued by the Government of Canada (2014 - $1,388 million; 2013 - $1,127 million) and equity securities issued by various entities (2014 - $937 million; 2013 - $1,000 million).

The following table represents the distribution of the Bank’s gross loan portfolio by category and location of ultimate risk as at December 31:

2014 2013

Canada Business loans:

Governments and Financial Institutions $99,509 $82,705 Real Estate 103,434 105,061 Other 179,394 68,076

Mortgage loans: Residential 8,565 8,784 Non-Residential 287,381 318,526

Consumer 17,813 9,147 Securities purchased under resale agreements 1,034,268 465,625

1,730,364 1,057,924 Other countries

China 87,543 90,332 United Kingdom 2 236,410 Others 1,838 8,014

1,819,747 1,392,680 Less: allowance for credit losses

(5,000)

(5,000)

Total $1,814,747 $1,387,680

The Bank had no impaired loans and no past due loans for 2014 and 2013.

The following table summarizes the Bank’s changes in allowance for credit losses for 2014 and 2013:

2014 2013 Balance at beginning of year $5,000 $5,000 Recoveries 18 19 Provision for credit losses (18) (10) Write-offs - (9) Balance at end of year $5,000 $5,000

The balance relating to allowance for credit losses at the end of each year is entirely comprised of collective allowance. The collective allowance consists of amounts relating to Corporate Bank and Private Bank credit portfolios and an unallocated portion.

Page 9 of 34

CITIBANK CANADA

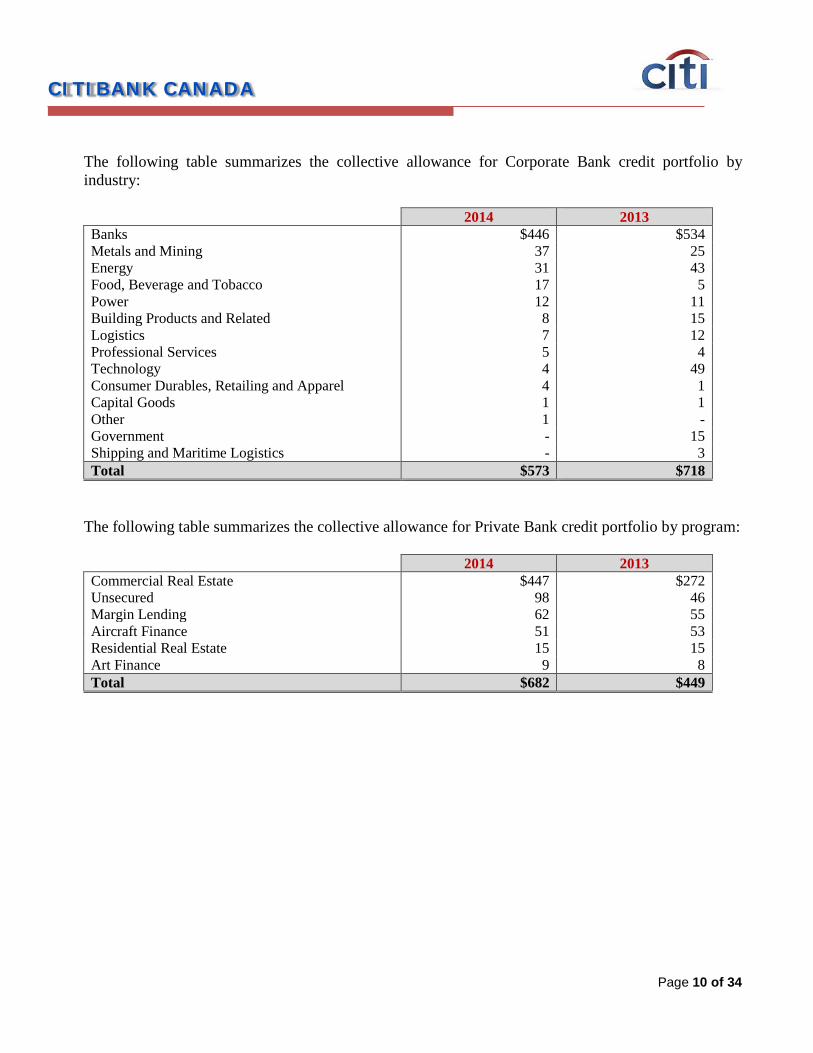

The following table summarizes the collective allowance for Corporate Bank credit portfolio by industry:

2014 2013

Banks $446 $534 Metals and Mining 37 25 Energy 31 43 Food, Beverage and Tobacco 17 5 Power 12 11 Building Products and Related 8 15 Logistics 7 12 Professional Services 5 4 Technology 4 49 Consumer Durables, Retailing and Apparel 4 1 Capital Goods 1 1 Other 1 - Government - 15 Shipping and Maritime Logistics - 3 Total $573 $718

The following table summarizes the collective allowance for Private Bank credit portfolio by program:

2014 2013 Commercial Real Estate $447 $272 Unsecured 98 46 Margin Lending 62 55 Aircraft Finance 51 53 Residential Real Estate 15 15 Art Finance 9 8 Total $682 $449

Page 10 of 34

CITIBANK CANADA

5. Credit Risk – Disclosures for Portfolios subject to the Standardized Approach

and Supervisory Risk Weights in the IRB Approaches

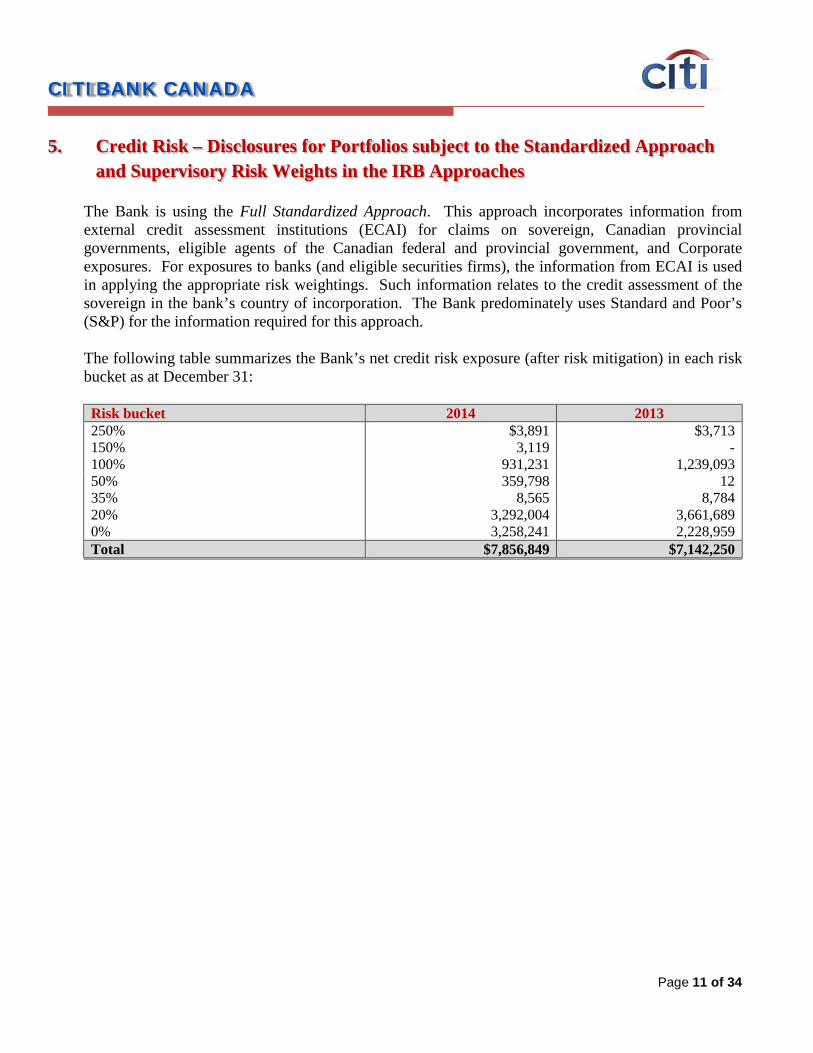

The Bank is using the Full Standardized Approach. This approach incorporates information from external credit assessment institutions (ECAI) for claims on sovereign, Canadian provincial governments, eligible agents of the Canadian federal and provincial government, and Corporate exposures. For exposures to banks (and eligible securities firms), the information from ECAI is used in applying the appropriate risk weightings. Such information relates to the credit assessment of the sovereign in the bank’s country of incorporation. The Bank predominately uses Standard and Poor’s (S&P) for the information required for this approach.

The following table summarizes the Bank’s net credit risk exposure (after risk mitigation) in each risk bucket as at December 31:

Risk bucket 2014 2013 250% $3,891 $3,713 150% 3,119 - 100% 931,231 1,239,093 50% 359,798 12 35% 8,565 8,784 20% 3,292,004 3,661,689 0% 3,258,241 2,228,959 Total $7,856,849 $7,142,250

Page 11 of 34

CITIBANK CANADA

6. Credit Risk Mitigation

Qualitative disclosures As part of its overall risk management activities, Citibank Canada utilizes collateral, guarantees and netting of derivative exposures to mitigate its credit risk.

To limit credit exposure to derivative counterparties, derivative transactions are customarily documented under industry standard master agreements and credit support annexes, which provide that following an uncured payment default or other event of default the non-defaulting party may promptly terminate all transactions between the parties and determine a net amount due to be paid to, or by, the defaulting party.

In the normal course of business, the Bank receives collateral on certain capital markets transactions to reduce its exposure to counterparty credit risk. The Bank is normally permitted to sell or re-pledge the collateral it receives subject to the obligation to return at the end of the agreements, under terms that are usual and customary to standard derivative, securities borrowing and reverse repurchase agreements.

For collateral used to offset capital markets transactions, the Bank follows the Institutional Clients Group (“ICG”) Margin Policy for Traded Products in conjunction with the ICG Margin Procedures for Traded Products. The policy describes the rules around margin pledged or transferred as a legally recognizable risk mitigant and requires that all margined over-the-counter (“OTC”) derivatives must be covered by an International Swaps and Derivatives Association Master Agreement, Credit Support Annex (“CSA”) or equivalent Master Agreements, if required by local laws.

The Bank holds collateral against loans in the form of mortgage interests over property, other registered securities over assets, and guarantees. Generally the collateral is reviewed at least annually, and upon any downgrade in classification of a secured facility to Pass Watch-list or worse.

For collateral held against loans, the Bank follows the ICG Banking Book Collateral Policy and Procedures. This policy describes the qualifying collateral pledged to support direct and contingent risk exposures, collateral valuation procedures, reporting processes and controls.

Valuation processes for cash and marketable securities differ than for physical assets. The monitoring of cash and marketable securities is typically more frequent than physical assets and may be based on product, geography and/or volatility of the security.

The Private Bank credit portfolio receives substantial guarantees against its exposures. These guarantees are primarily in the form of personal guarantees, guarantees from individuals controlling the obligor, and guarantees from entities affiliated with the obligor.

The Bank generally receives fewer guarantees against its Corporate Bank credit and OTC derivatives portfolios. The guarantors primarily consist of parent entities or affiliates of the obligor.

Page 12 of 34

CITIBANK CANADA

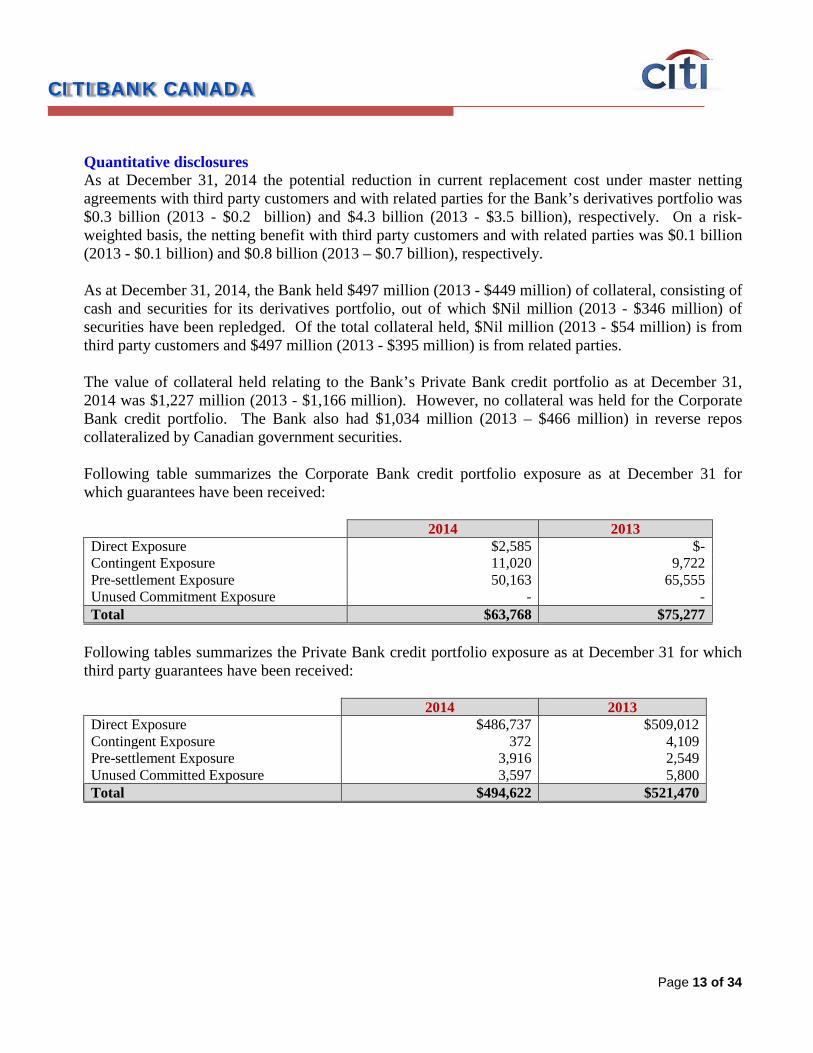

Quantitative disclosures As at December 31, 2014 the potential reduction in current replacement cost under master netting agreements with third party customers and with related parties for the Bank’s derivatives portfolio was $0.3 billion (2013 - $0.2 billion) and $4.3 billion (2013 - $3.5 billion), respectively. On a risk-weighted basis, the netting benefit with third party customers and with related parties was $0.1 billion (2013 - $0.1 billion) and $0.8 billion (2013 – $0.7 billion), respectively.

As at December 31, 2014, the Bank held $497 million (2013 - $449 million) of collateral, consisting of cash and securities for its derivatives portfolio, out of which $Nil million (2013 - $346 million) of securities have been repledged. Of the total collateral held, $Nil million (2013 - $54 million) is from third party customers and $497 million (2013 - $395 million) is from related parties. The value of collateral held relating to the Bank’s Private Bank credit portfolio as at December 31, 2014 was $1,227 million (2013 - $1,166 million). However, no collateral was held for the Corporate Bank credit portfolio. The Bank also had $1,034 million (2013 – $466 million) in reverse repos collateralized by Canadian government securities.

Following table summarizes the Corporate Bank credit portfolio exposure as at December 31 for which guarantees have been received:

2014 2013

Direct Exposure $2,585 $- Contingent Exposure 11,020 9,722 Pre-settlement Exposure 50,163 65,555 Unused Commitment Exposure - - Total $63,768 $75,277

Following tables summarizes the Private Bank credit portfolio exposure as at December 31 for which third party guarantees have been received:

2014 2013

Direct Exposure $486,737 $509,012 Contingent Exposure 372 4,109 Pre-settlement Exposure 3,916 2,549 Unused Committed Exposure 3,597 5,800 Total $494,622 $521,470

Page 13 of 34

CITIBANK CANADA

7. General Disclosures for Exposures Related to Counterparty Credit Risk

Qualitative disclosures The Bank manages Counterparty Credit Risk in accordance with the credit risk policies described earlier in section on Credit Risk – General Disclosures for all Banks.

Counterparty Credit Risk exposure is calculated to the maturity of the transactions in a portfolio using a Monte-Carlo simulation framework. The simulation models the behaviour of the underlying market factors in a way that captures the desired joint distribution of potential movements. At each point as we walk forward through time, the simulation process revalues each remaining transaction under the simulated scenario. Repeated simulations build up these distributions of potential future value and from these distributions, two measures are selected – (1) pre-settlement loan equivalent (PSLE), which is the expected positive exposure or average over the positive part of the distribution at each point in time; and (2) pre-settlement exposure (PSE) relating to derivatives, which is a high confidence level exposure. For the purposes of credit limits and monitoring of limit usage, the PSE measure is used. For purposes of monitoring outstanding exposure or usage against obligor limits, the exposure is measured on a PSLE basis.

Credit Reserves The Bank, pursuant to accounting guidance, incorporates a bilateral credit value adjustment in its accounting of counterparty risk. Refer to Market Risk section below for further details on CVA.

Wrong-Way Risk Wrong-way risk occurs where a movement in a market factor causes The Bank’s exposure to a counterparty to increase at the same time as the counterparty’s capacity to meet its obligations is decreasing. The Bank adheres to a Wrong Way Risk Policy, which sets guidelines for the identification, approvals, reporting and mitigation of Wrong-way Risk.

Collateral requirement due to Credit rating downgrade As at December 31, 2014, the maximum potential collateral requirement if the Bank is downgraded to zero threshold is $9 million (2013 - $32 million).

Counterparty Credit Risk Capital The Bank calculates risk capital for CVA on a unilateral basis, i.e. only the potential exposure to the Bank’s counterparties is considered. The risk capital is based on the unexpected loss resulting from spread changes of counterparties as well as default considerations during a stress period.

Page 14 of 34

CITIBANK CANADA

Quantitative disclosures The following table summarizes the Bank’s current replacement cost (CRC) and credit equivalent amounts (CEA) of its derivatives portfolio as at December 31:

2014 2013

CRC CEA CRC CEA Interest rate contracts $3,994,938 $5,318,971 $3,207,940 $4,223,378 Foreign exchange contracts 1,131,030 2,775,903 1,000,559 2,724,565 Equity, credit and commodity contracts 327,223 728,694 427,672 1,008,865 Total $5,453,191 $8,823,568 $4,636,171 $7,956,808

The table below presents the impact of master netting arrangement as at December 31:

2014 2013 Gross positive fair value of derivative contracts $5,453,191 $4,636,171 Netting benefit from master netting agreements (4,654,015) (3,744,825) Total net current credit exposure $799,176 $891,346

The Bank’s entire credit derivatives portfolio is in respect of intermediation activities as all customer trades are mirrored with back-to-back trades with the Bank’s indirect parent. As at December 31, 2014, the notional amount of these trades totalled $0.1 billion (2013 - $0.3 billion) and their current replacement cost totalled $3.4 million (2013 - $4.7 million).

8. Securitization

The Bank neither securitizes its own assets nor sponsors any securitization programs.

However, as at December 31, 2014, the Bank held a trading portfolio of securities issued by Canada Housing Trust (guaranteed by the Government of Canada) in its banking book with a fair value of $Nil million (2013 - $46 million). The Canada Housing Trust securities were risk weighted at 0%.

Page 15 of 34

CITIBANK CANADA

9. Market Risk – Disclosures for Banks using the Internal Models Approach (IMA)

for Trading Portfolios

Qualitative disclosures Market risk is the earnings risk from changes in interest rates, foreign exchange rates, and equity and commodity prices, and in their implied volatilities. The objective of market risk management is to manage and control market risk exposures within acceptable limits, while optimizing the return on risk.

Management of market risk The Bank manages market risk through specific policies, which are reviewed by the Risk Committee, approved by the Chief Risk Officer (CRO), senior management and the Board. These policies set out well-defined market risk responsibilities for business and corporate oversight groups, as well as limits and other processes to ensure that market risks remain well controlled. The Bank manages foreign exchange risk of non-trading assets and liabilities denominated in foreign currencies through hedging instruments such as forwards and cross currency swaps.

Market risks are measured in accordance with established standards to ensure consistency across businesses and the ability to aggregate risk. Each business is required to establish, with approval from independent market risk management and the CRO, a market risk limit framework for identified risk factors that clearly defines approved risk profiles and is within the parameters of the Bank’s overall risk appetite. In all cases, the businesses are ultimately responsible for the market risks they take and for remaining within their defined limits. These limits are reviewed annually by the Risk Committee and approved by the CRO, senior management and the Board. The CRO monitors all trading activity and market exposures on a daily basis to ensure risks remain within the established limits and policies.

In addition to the controls above, the risk management process is reviewed by Internal Audit on a periodic basis to ensure that market risk policies are being adhered to.

Exposure to market risks on trading portfolios Market risk in trading portfolios is monitored using a series of measures, including: • Factor sensitivities; • Value-at-risk (VaR); • Stressed value-at-risk (Stressed VaR); and • Stress testing.

Factor sensitivities are expressed as the change in the value of a position for a defined change in a market risk factor, such as a change in the value of a Treasury bill for a one-basis-point change in interest rates. The Bank’s independent market risk management ensures that factor sensitivities are calculated, monitored and limited, for all relevant risks taken in a trading portfolio.

Page 16 of 34

CITIBANK CANADA

Market Risk Model and Reporting VaR estimates the potential decline in the value of a position or a portfolio under normal market conditions. The Stressed VaR is a VaR-based risk measure subject to the same confidence level as applicable to a VaR measure but with model inputs calibrated to historical data from a continuous twelve-month period that reflects a period of significant financial stress appropriate to current portfolios. The Bank uses a single, independently approved Monte-Carlo simulation VaR model that has been designed to capture the risk sensitivities of various asset classes/risk types. VaR model is calibrated to incorporate the greater of short-term and long term (three years) market volatility. The Bank’s VaR is expressed as the risk to the Bank over a one-day holding period, at 99% confidence level. The Bank reports market risk exposures including factor sensitivities, VaR and Stressed VaR figures on a daily basis to senior management highlighting the risks the firm is exposed to and the usage against relevant market risk limits in place, as approved by the Board.

Each trading portfolio has its own market risk limit framework encompassing these measures and other controls, including permitted product lists and a new product approval process for complex products. Utilization of VaR limits and Stressed VaR limits are reviewed daily by the CRO and regular summaries are submitted to the Risk Committee and the Board.

Back Testing Backtesting is the comparison of ex-ante VaR to ex-post Profit & Loss (P&L). The performance of the Bank’s VaR model is tested through back testing, which involves the comparison of daily static P&L to One-day-VaR and tracks the number of breaches for a twelve-month period to assess the performance of the model. The static P&L is defined as hypothetical changes in portfolio value that would occur if end of the day positions remained unchanged. It, therefore, excludes bid-ask spreads, net interest income, intraday trading, and fees and commissions. The results of the back testing process are reported on a quarterly basis to the Risk Committee, the Board and OSFI.

Prudent Valuation Guidance The Bank has established adequate systems and controls to ensure that its fair estimates are prudent and reliable. These also include independent price verification procedures which are distinct from daily mark-to-market to ensure market prices or model inputs are regularly verified for accuracy. Further, these procedures also include consideration of valuation adjustments/reserves, as appropriate. For assets and liabilities carried at fair value, the Bank measures such value using the procedures set out below.

• When available, the Bank uses quoted market prices to determine fair value and classify such

items as Level 1. In some cases where a market price is not available, the Bank uses quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active and model-derived valuations in which all significant inputs and significant value drivers are observable in active markets to calculate fair value, in which case the

Page 17 of 34

CITIBANK CANADA

items are classified as Level 2.

• If quoted market prices are not available, fair value is based upon internally developed valuation

techniques that use, where possible, current market-based or independently sourced market parameters, such as interest rates, currency rates, option volatilities, etc. Items valued using such internally generated valuation techniques are classified as Level 2 or Level 3 depending on the observability of significant inputs to the model.

• CVA is applied to OTC derivative instruments, in which the base valuation generally discounts

expected cash flows using appropriate interest rate curves. Given that not all counterparties have the same credit risk as that implied by the relevant interest rate curve, a CVA is necessary to incorporate the market view of both counterparty credit risk and Citigroup’s own credit risk in the valuation.

The following methods and assumptions are used to estimate the fair values of on-balance sheet financial instruments:

• Trading and Available-for-sale Securities

When available, the Bank uses quoted market prices to determine the fair value of trading and AFS securities; such items are classified as Level 1 of the fair value hierarchy. Examples include certain government securities and exchange-traded equity securities. For other securities, the Bank generally determines fair value utilizing internal valuation techniques. Fair value estimates from internal valuation techniques are verified, where possible, to prices obtained from independent vendors. Securities priced using such methods are generally classified as Level 2.

• Derivative Assets and Liabilities

Exchange-traded derivatives are generally fair valued using quoted market (i.e. exchange) prices and so are classified as Level 1 of the fair value hierarchy.

The majority of derivatives entered into by the Bank are executed OTC and so are valued using internal valuation techniques as no quoted market prices exist for such instruments. The valuation techniques and inputs depend on the type of derivative and the nature of the underlying instrument. The principal techniques used to value these instruments are discounted cash flows, Black-Scholes and Monte Carlo simulation.

The key inputs depend upon the type of derivative and the nature of the underlying instrument and include interest rate yield curves, foreign exchange rates, the spot price of the underlying volatility and correlation.

A derivative contract is placed in either Level 2 or Level 3 depending on the observability of the significant inputs to the model. Correlation and items with longer tenors are generally less observable. Where appropriate, a valuation adjustment is made to cover counterparty credit risk, market liquidity and maintenance costs.

Page 18 of 34

CITIBANK CANADA

• Deposits The Bank determines the fair value of structured liabilities (where a call option is embedded) and hybrid financial instruments (performance linked to risks other than interest rates, inflation or currency risks) using the appropriate derivative valuation methodology (described above, including independent broker quotes) based on the nature of the embedded risk profile. Such instruments are classified as Level 2 or Level 3 depending on the observability of significant inputs to the model.

Stress Testing The Bank has in place a stress testing program that is applied to all trading desks in the Bank. The program, called global systemic stress testing (GSST), is comprised of historical scenarios and hypothetical scenarios. These scenarios are designed by the senior risk management team with input from senior business management. The macroeconomic variables reflect one-year changes and the market factors are defined as instantaneous shocks. From a trading book perspective the shocks in these scenarios are related to the main risk factor groups, such as equities, interest rate, foreign exchange, commodities and credit. Stress testing program includes a wide range of severities. The use of stress testing is linked to risk appetite monitoring, risk capital calculation and internal capital adequacy assessment process as described earlier in section on Capital Adequacy.

Market Risk Capital The market risk capital methodology is based on an integrated VaR and stress scenario methodology, which is consistent with the Basel II.5 guidelines.

Capital Adequacy Market Risk is a key part in the internal assessment of capital adequacy. The methodology and process for internal capital adequacy have been described earlier in section on Capital Adequacy.

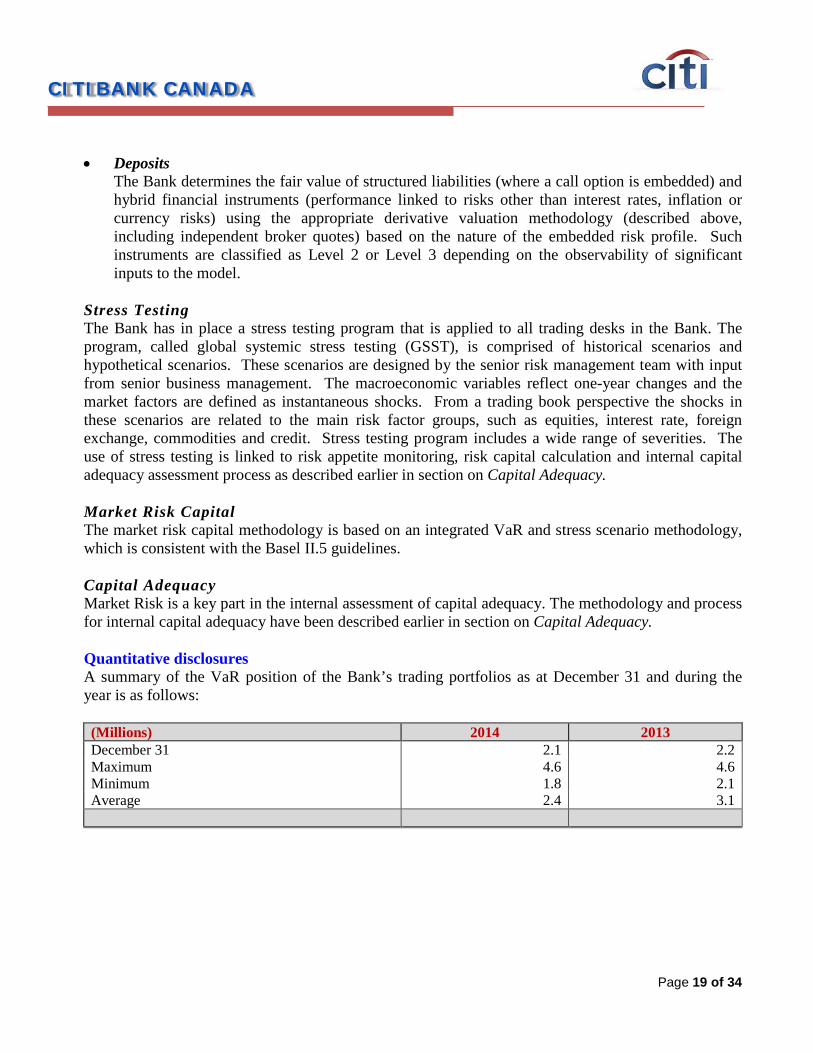

Quantitative disclosures A summary of the VaR position of the Bank’s trading portfolios as at December 31 and during the year is as follows:

(Millions) 2014 2013 December 31 2.1 2.2 Maximum 4.6 4.6 Minimum 1.8 2.1 Average 2.4 3.1

Page 19 of 34

CITIBANK CANADA

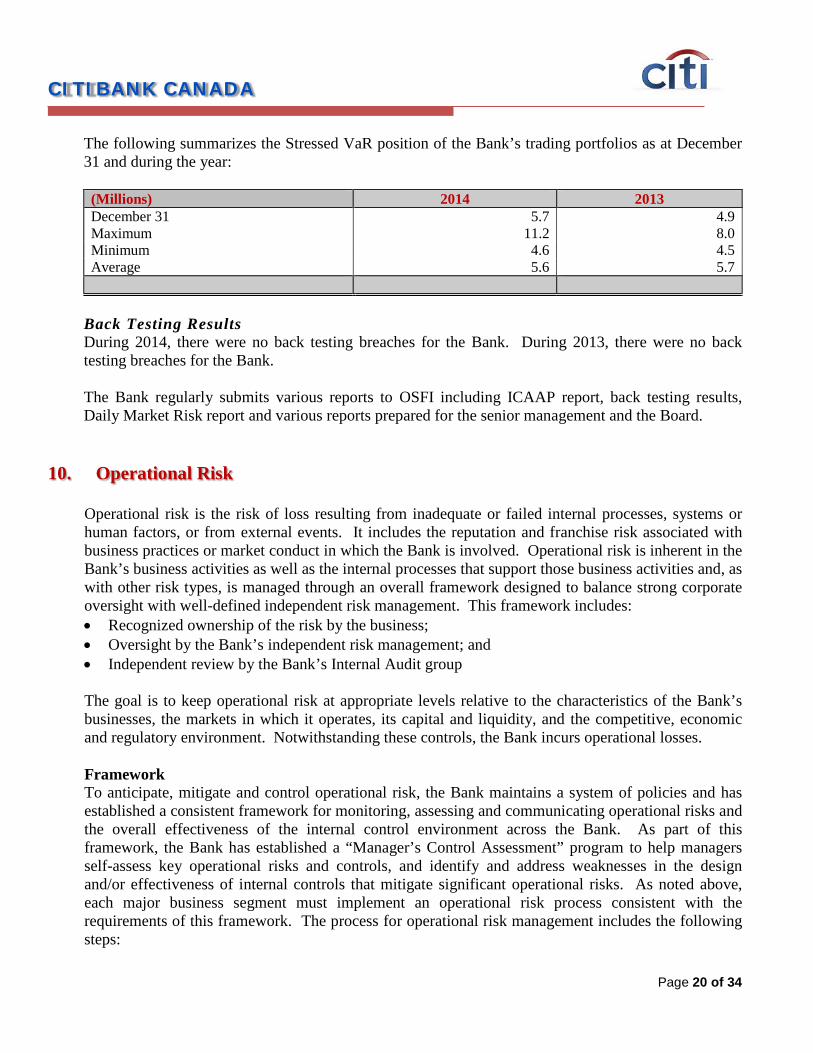

The following summarizes the Stressed VaR position of the Bank’s trading portfolios as at December 31 and during the year:

(Millions) 2014 2013 December 31 5.7 4.9 Maximum 11.2 8.0 Minimum 4.6 4.5 Average 5.6 5.7

Back Testing Results During 2014, there were no back testing breaches for the Bank. During 2013, there were no back testing breaches for the Bank.

The Bank regularly submits various reports to OSFI including ICAAP report, back testing results, Daily Market Risk report and various reports prepared for the senior management and the Board.

10. Operational Risk Operational risk is the risk of loss resulting from inadequate or failed internal processes, systems or human factors, or from external events. It includes the reputation and franchise risk associated with business practices or market conduct in which the Bank is involved. Operational risk is inherent in the Bank’s business activities as well as the internal processes that support those business activities and, as with other risk types, is managed through an overall framework designed to balance strong corporate oversight with well-defined independent risk management. This framework includes: • Recognized ownership of the risk by the business; • Oversight by the Bank’s independent risk management; and • Independent review by the Bank’s Internal Audit group The goal is to keep operational risk at appropriate levels relative to the characteristics of the Bank’s businesses, the markets in which it operates, its capital and liquidity, and the competitive, economic and regulatory environment. Notwithstanding these controls, the Bank incurs operational losses. Framework To anticipate, mitigate and control operational risk, the Bank maintains a system of policies and has established a consistent framework for monitoring, assessing and communicating operational risks and the overall effectiveness of the internal control environment across the Bank. As part of this framework, the Bank has established a “Manager’s Control Assessment” program to help managers self-assess key operational risks and controls, and identify and address weaknesses in the design and/or effectiveness of internal controls that mitigate significant operational risks. As noted above, each major business segment must implement an operational risk process consistent with the requirements of this framework. The process for operational risk management includes the following steps:

Page 20 of 34

CITIBANK CANADA

• Identify and assess key operational risks; • Design controls to mitigate identified risks; • Establish key risk and control indicators; • Implement a process for early problem recognition and timely escalation; • Produce a comprehensive operational risk report; and • Ensure that sufficient resources are available to actively improve the operational risk environment

and mitigate emerging risks.

The operational risk standards facilitate the effective communication and mitigation of operational risk both within and across businesses. As new products and business activities are developed, processes are designed, modified or sourced through alternative means and operational risks are considered. Information about the businesses’ operational risk, historical losses and the control environment is reported by each major business segment and the functional area, and is summarized and reported to senior management as well as the Board of Directors. Measurement and Basel II The Basic Indicator Approach is used for computing the operational risk for the purposes of regulatory capital.

Information Security and Continuity of Business Information security and the protection of confidential and sensitive customer data are a priority for the Bank. The Bank has implemented an Information Security Program. The Information Security Program is reviewed and enhanced periodically to address emerging threats to customers’ information. The Continuity of Business and Crisis Management group, with the support of senior management, coordinates preparedness and mitigates business continuity risks by reviewing and testing recovery procedures.

11. Equities – Disclosure for Banking Book Positions

The Bank has no exposure to equity investments in the banking book as at December 31, 2014 and 2013.

Page 21 of 34

CITIBANK CANADA

12. Interest Rate Risk in the Banking Book

Qualitative disclosures

Net interest revenue, for interest rate exposure purposes, is the difference between the yield earned on the non-trading portfolio assets (including customer loans) and the rate paid on the liabilities (including customer deposits or company borrowings). Net interest revenue is affected by changes in the level of interest rates, as well as the amounts of assets and liabilities, and the timing of repricing of assets and liabilities to reflect market rates.

Citibank Canada’s principal measure of risk to net interest revenue is interest rate exposure (IRE). IRE measures the change in expected net interest revenue in each currency resulting solely from unanticipated changes in forward interest rates. The Bank’s estimated IRE incorporates various assumptions including customer behavior, and the impact of pricing decisions. For example, in rising interest rate scenarios, portions of the deposit portfolio may be assumed to experience rate increases that are less than the change in market interest rates. IRE assumes that businesses and/or Citibank Canada Treasury make no additional changes in balances or positioning in response to the unanticipated rate changes.

In order to manage changes in interest rates effectively, the Bank may modify pricing on new customer loans and deposits, purchase fixed rate securities and enter into long/short term borrowing either fixed or floating. The Bank manages interest rate risk as a consolidated company-wide position. The Bank’s client-facing businesses create interest rate sensitive positions, including loans and deposits, as part of their ongoing activities. Citibank Canada Treasury (“Treasury department”) aggregates these risk positions and manages them centrally. Operating within established limits, the Treasury department makes positioning decisions and uses tools, such as the Bank’s investment securities portfolio and Long Term/Short Term borrowings to target the desired risk profile.

The market risks in the Bank’s non-traded portfolios, all of which are held within Treasury department, are estimated using a common set of standards that define, measure, limit and report the market risk. Treasury department is required to establish, with approval from the CRO, a market risk limit framework that clearly defines approved risk profiles and is within the parameters of the Bank‘s overall risk appetite. In all cases, Treasury department is ultimately responsible for the market risks it takes and for remaining within its defined limits. These limits are monitored by the CRO and asset/liability management committee on a monthly basis. All such limits are reviewed by the Risk Committee and approved by the CRO and the Board.

The Bank follows the Market Risk Management for Accrual Portfolios policy which includes the IRE measures for the firm and the need to perform stress testing for interest rate risk in the banking book. The stress testing is performed as part of the GSST process described above in section on Market Risk.

Quantitative disclosures The management of interest rate risk is based on monitoring the sensitivity of the Bank’s financial assets and liabilities to various standard and non-standard interest rate scenarios. Standard scenarios that are considered include a 100 basis point parallel fall or rise in all yield curves worldwide. As at

Page 22 of 34

CITIBANK CANADA

December 31, 2014, a 100 basis point upward interest rate shift would increase net income in the US dollar book by $4.63 million (2013 - $0.09 million increase) and decrease the Canadian dollar book by $4.15 million (2013 - $0.18 million increase) resulting in a net increase of $0.48 million (2013 - $0.27 million increase) over the next twelve months, assuming management takes no action. A 100 basis point downward shift would have a comparable, but opposite, impact on net income.

13. Remuneration

Governance Global Remuneration Committee Citigroup Inc.’s (“Citi”) Global Remuneration Committee which is known as the Personnel and Compensation (“P&C”) Committee is a duly constituted committee of the Board of Directors of the Bank’s ultimate parent, Citi. The P&C Committee draws on considerable experience of the non-executive directors of the Board of Directors of Citi, and is empowered to draw upon internal and external expertise and advice as it determines appropriate. The terms of reference of the P&C Committee are available online at: http://www.citigroup.com/citi/investor/data/percompcharter.pdf?ieNocache=783 Citi’s global compensation principles are developed and approved by the P&C Committee in consultation with management, independent consultants and Citi’s senior risk officers. The P&C Committee is comprised of independent directors who have experience evaluating compensation structures, especially for senior executives. Citi’s compensation principles are designed to advance Citi’s business strategy by attracting, retaining and motivating the best talent available to execute the strategy, while ensuring, among other things, unnecessary or excessive risk-taking is not encouraged.

For additional information on the global compensation principles and governance, refer to the Citi 2015 Proxy Statement available online at: http://www.citigroup.com/citi/investor/overview.html

Citibank Canada Governance Committee The Bank’s Board of Directors has constituted a Governance Committee comprising of five of its members, of which three are independent non-executive directors. The Governance Committee has the responsibility for overseeing the compensation practices of the Bank. These responsibilities include:

• Review and approve annually, the general compensation philosophy and guidelines for the

Bank’s senior management team, including its Chief Executive Officer. This includes incentive plan design and other remuneration.

• Take such action as the Committee deems necessary to highlight concerns on program and plan design, risk taking activities, etc. to influence compensation decisions related to specific programs or individuals.

Page 23 of 34

CITIBANK CANADA

Citi’s Compensation Philosophy Citi believes that compensation is a critical strategic lever in the successful execution of our goals. As long-term value creation requires balancing strategic goals, so does developing compensation programs that incentivize balanced behaviors.

Citi’s Compensation Philosophy includes designing compensation programs and structures that fulfill four primary objectives. These compensation objectives, as outlined below, have been developed and approved by the P&C Committee of the Board of Directors, in consultation with management, independent consultants and Citi’s senior risk officers. They have been specifically created to encourage prudent risk-taking, while attracting the world-class talent necessary to see the company through to success.

Citi’s Compensation Objectives are: • Align compensation programs, structures and decisions with shareholder interests • Manage risks to the firm by encouraging prudent decision-making • Implement evolving regulatory guidance • Attract and retain the best talent to lead the Company to success

For a full overview of what Citi’s compensation objectives mean, refer to the full statement available online at: http://www.citigroup.com/citi/investor/data/comp_phil_policy.pdf?ieNocache=570

Senior Management and Other Material Risk Takers • The Bank’s senior management personnel include its Chief Executive Officer, Heads of Global

Functions (Chief Financial Officer, General Counsel, Chief Compliance Officer, Chief Risk Officer, Head of Human Resources, and Head of Operations and Technology), Treasurer, and three business heads who lead the Bank’s global transaction services, global markets (derivatives) and private banking operations.

• In accordance with remuneration regulatory requirements, Citi undertakes an ongoing exercise to identify those employees whose professional activities have a material impact on the risk profile of the firm. In general, such employees may be subject to further obligations under relevant remuneration regulations. For US regulatory purposes, such employees are termed “Covered Employees”.

• Citi has developed a systematic framework for identifying employees who are Covered Employees across its businesses globally, based on a structural identification of the roles in managing key financial (including revenue and risk capital metrics) and non-financial risks (e.g., franchise risk): • Group 1 Covered employees are senior executives with firm-wide responsibilities known as

Section 16 executive officers for US regulatory purposes. There are no Group 1 Covered Employees in Canada.

• Group 2 Covered Employees are senior employees who can take, or influence the taking of, material risk for Citigroup or for a material business unit.

Page 24 of 34

CITIBANK CANADA

• Group 3 Covered Employees are employees in similar roles and with similar incentives who

could, acting as a group, create material risk for Citigroup or a material business unit, even though they are not likely capable of doing so if acting alone.

Remuneration Structures Link between pay and performance • Citi is committed to responsible compensation practices and structures. Citi seeks to balance the

need to compensate its employees fairly and competitively based on their performance, while assuring that their compensation reflects principles of risk management and performance metrics that reward long-term contributions to sustained profitability.

• Citi’s compensation programs aim to enhance stockholder value through the practice of responsible finance, facilitate competitiveness by attracting and retaining the best talent, promote meritocracy by recognizing employee contributions, and manage risk through sound incentive compensation practices.

Fixed Remuneration – Salary and Benefits • Citi’s fixed remuneration is set appropriately to attract, retain and motivate employees in line with

market practices and is benchmarked against market data. • Pension and other non-cash benefits are offered to Citi employees as part of an overall reward

package which is designed to be sufficiently competitive to attract, retain and motivate employees. Citi aims to provide common pension and other benefits across all units/business groups, which are competitive against the external market.

Ratio of fixed to variable remuneration • Citi seeks to balance the components of reward between fixed and variable, and between short

term and long-term components. Citi’s policy in regards to discretionary incentive and retention awards is to ensure that the scheme is wholly discretionary, and compensation is fully flexible and can be decreased as a result of negative performance, which may result in zero variable remuneration.

Variable compensation • The Discretionary Incentive and Retention Award (“DIRA”) Plan is Citi’s main variable

discretionary incentive and retention plan. It is designed to incentivize, reward and retain employees based on their current and prospective performance and contribution. Citi retains complete discretion as to the components of DIRA, which may include cash and/or equity or other share-linked instruments.

Page 25 of 34

CITIBANK CANADA

Use of stock as deferred variable compensation • In general, amounts subject to Citi’s mandatory deferral policy, are deferred into shares or share-

linked instruments. Subject to headroom limitations relating to Citi’s shareholder approved stock deferral plans, a portion of deferred remuneration may be in the form of deferred cash, Citi stock and/or phantom units related to Citi’s share price.

• The Capital Accumulation Program (“CAP”) and Citigroup Stock Award Program (“CSAP”) are the main programmes under which Citi may make awards of stock to selected employees.

• Certain senior executives are subject to stock ownership commitments, further aligning the executives’ interests with those of stockholders and other stakeholders.

• Deferred stock awards made to Covered Employees are subject to Performance Based Vesting (“PBV”). The trigger for application of a PBV reduction of a tranche of unvested deferred stock is the emergence of pre-tax losses in the relevant “reference business” of the individual. If there are pre-tax losses in the reference business, a portion of the deferred stock tranche is forfeited, the proportion of which is based on the extent of the losses and prior year net profits.

Use of deferred Cash as deferred compensation • Covered Employees may have a portion of their incentive compensation delivered in the form of

deferred cash awards, subject to performance based vesting PBV. PBV for the deferred cash portion of the award is a discretionary feature. If it is determined that a Material Adverse Outcome (“MAO”) has occurred, and that a given Covered Employee is deemed to have had “significant responsibility” for that MAO, then a discretionary reduction may be made to the unvested portion of the deferred cash award. Determinations of when a MAO has occurred, which (if any) Covered Employees have significant responsibility for the MAO, and what reductions to awards will be made, are all based on the facts and circumstances of a given outcome.

• The unvested cash portion of deferred incentive compensation will earn notional interest at a market rate.

Deferral periods and risk horizons • For non-Covered Employees, Citi operates a standard or “default” deferral policy period pro-rated

four years, which it considers captures the duration of most risks for nearly all employees.

Page 26 of 34

CITIBANK CANADA

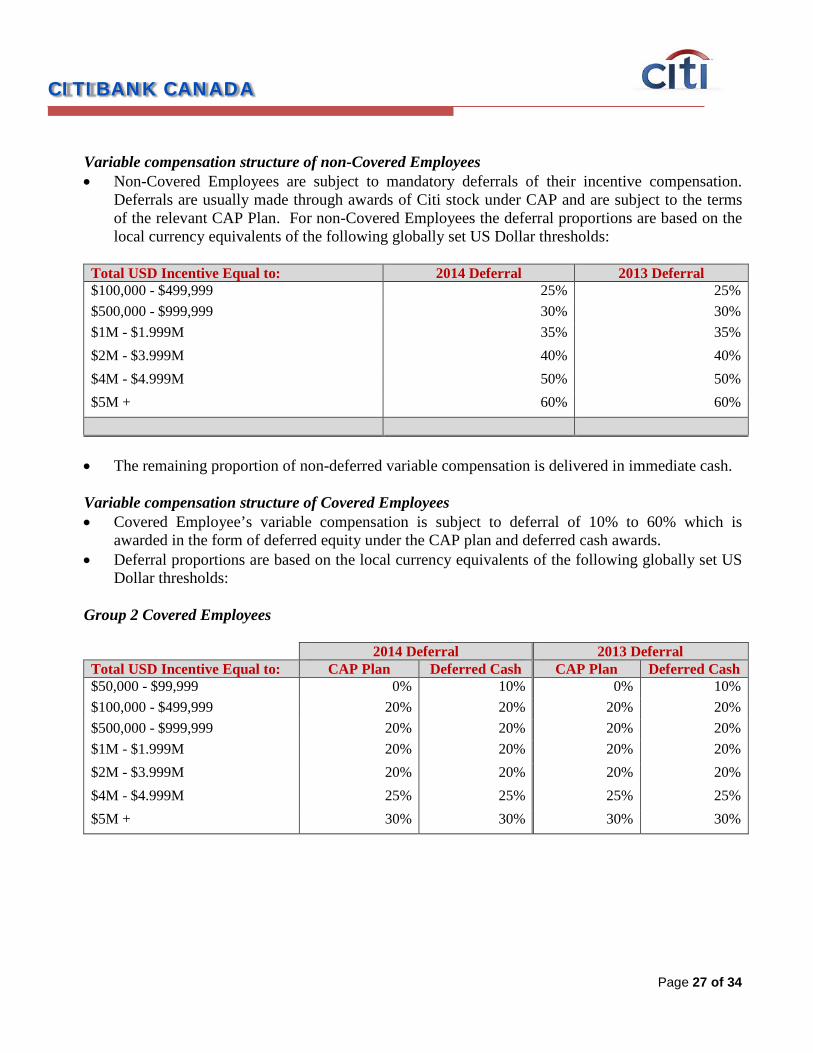

Variable compensation structure of non-Covered Employees • Non-Covered Employees are subject to mandatory deferrals of their incentive compensation.

Deferrals are usually made through awards of Citi stock under CAP and are subject to the terms of the relevant CAP Plan. For non-Covered Employees the deferral proportions are based on the local currency equivalents of the following globally set US Dollar thresholds:

Total USD Incentive Equal to: 2014 Deferral 2013 Deferral $100,000 - $499,999 25% 25% $500,000 - $999,999 30% 30% $1M - $1.999M 35% 35% $2M - $3.999M 40% 40% $4M - $4.999M 50% 50% $5M + 60% 60%

• The remaining proportion of non-deferred variable compensation is delivered in immediate cash.

Variable compensation structure of Covered Employees • Covered Employee’s variable compensation is subject to deferral of 10% to 60% which is

awarded in the form of deferred equity under the CAP plan and deferred cash awards. • Deferral proportions are based on the local currency equivalents of the following globally set US

Dollar thresholds: Group 2 Covered Employees

2014 Deferral 2013 Deferral Total USD Incentive Equal to: CAP Plan Deferred Cash CAP Plan Deferred Cash $50,000 - $99,999 0% 10% 0% 10% $100,000 - $499,999 20% 20% 20% 20% $500,000 - $999,999 20% 20% 20% 20% $1M - $1.999M 20% 20% 20% 20% $2M - $3.999M 20% 20% 20% 20% $4M - $4.999M 25% 25% 25% 25% $5M + 30% 30% 30% 30%

Page 27 of 34

CITIBANK CANADA

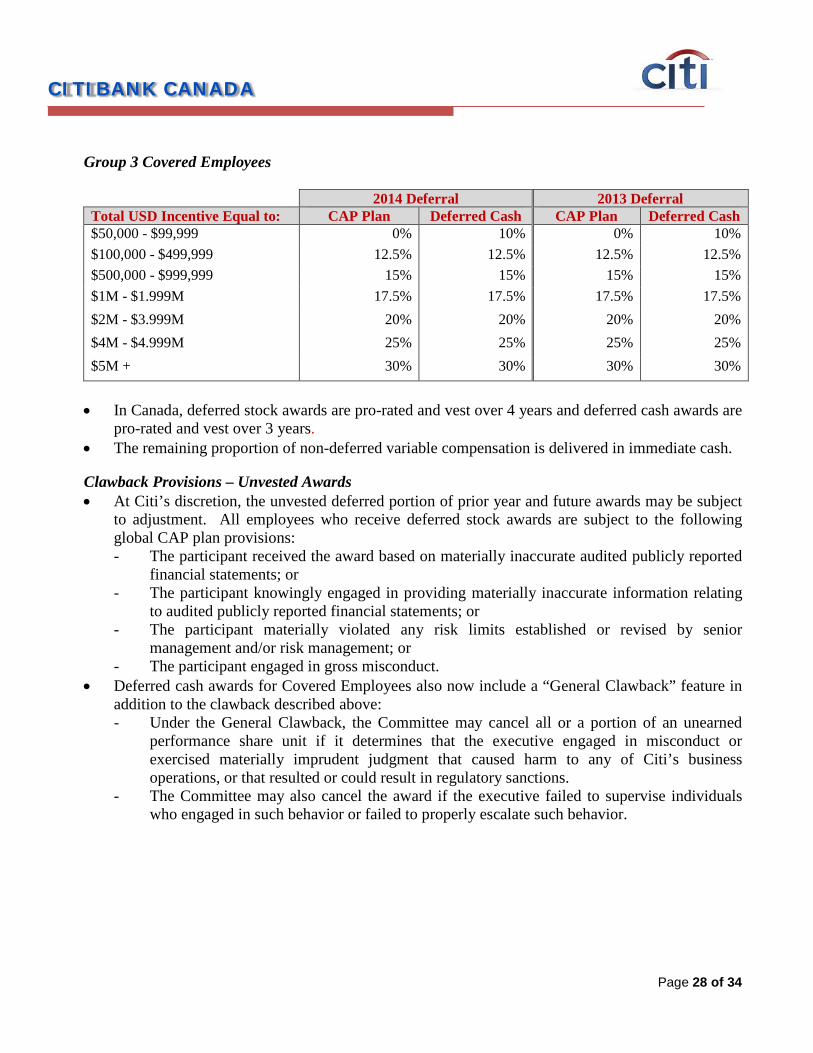

Group 3 Covered Employees

2014 Deferral 2013 Deferral Total USD Incentive Equal to: CAP Plan Deferred Cash CAP Plan Deferred Cash $50,000 - $99,999 0% 10% 0% 10% $100,000 - $499,999 12.5% 12.5% 12.5% 12.5% $500,000 - $999,999 15% 15% 15% 15% $1M - $1.999M 17.5% 17.5% 17.5% 17.5% $2M - $3.999M 20% 20% 20% 20% $4M - $4.999M 25% 25% 25% 25% $5M + 30% 30% 30% 30%

• In Canada, deferred stock awards are pro-rated and vest over 4 years and deferred cash awards are

pro-rated and vest over 3 years. • The remaining proportion of non-deferred variable compensation is delivered in immediate cash.

Clawback Provisions – Unvested Awards • At Citi’s discretion, the unvested deferred portion of prior year and future awards may be subject

to adjustment. All employees who receive deferred stock awards are subject to the following global CAP plan provisions: - The participant received the award based on materially inaccurate audited publicly reported

financial statements; or - The participant knowingly engaged in providing materially inaccurate information relating

to audited publicly reported financial statements; or - The participant materially violated any risk limits established or revised by senior

management and/or risk management; or - The participant engaged in gross misconduct.

• Deferred cash awards for Covered Employees also now include a “General Clawback” feature in addition to the clawback described above: - Under the General Clawback, the Committee may cancel all or a portion of an unearned

performance share unit if it determines that the executive engaged in misconduct or exercised materially imprudent judgment that caused harm to any of Citi’s business operations, or that resulted or could result in regulatory sanctions.

- The Committee may also cancel the award if the executive failed to supervise individuals who engaged in such behavior or failed to properly escalate such behavior.

Page 28 of 34

CITIBANK CANADA

Severance • Citi generally does not provide guaranteed levels of severance upon early termination of

employment. Severance pay is discretionary unless otherwise required by local law. Guarantees, Buyouts and Retention Payments • Guaranteed incentive and retention awards for all employees can only be made in exceptional

circumstances and by reference to the first year of service only. • Guaranteed awards made for the purposes of retaining employees can only be made in exceptional

circumstances, for example, during major restructuring, during a merger process; or where a business is winding down, such that particular staff need to be retained on business grounds.

Personal Hedging • Employees are prohibited by Citi from taking out insurance contracts or engaging in personal

hedging strategies or remuneration or liability related contracts of insurance that undermine or may undermine any risk alignment effects of their remuneration arrangements.

Performance measurement Determination of global bonus pools • Citi’s bonus pools are determined at a global level. For revenue generating business units,

incentive compensation pools reflect the reward that groups of employees should receive based on their economic value creation and distinct talent attributes. Bonus pool determinations will be driven by economic value creation measured on a risk-adjusted basis (including an explicit capital charge) calculated at a level that captures similar business dynamics and provides a structured framework to inform management discretion. Senior management will make discretionary risk adjustment based on factors not captured in the mechanical bonus pool determination, combined with adjustments for strategic factors (e.g., short term competitive pressures for talent, strategic importance of the franchise etc.) to determine final bonus pools. Incentive compensation pools of non-revenue generating and wind down business units are adjusted for Citi and business unit performance, business unit strategy and strategic positioning and competition for talent.

Page 29 of 34

CITIBANK CANADA

Individual performance assessment and award determination process • Citi has an annual performance management process which operates through the Global Talent

and Management System (“GTMS”). • The performance assessment of Canadian employees is based on individually tailored goals, and

an assessment against Citi’s Core Principles Statements, which incorporates risk management and non-financial performance factors by business area into the performance appraisal process (refer to core Principle Statements later in this section).

• Individuals complete a self-appraisal against their individual and Core Principle Statement goals. This is followed by a discussion between the individual and their manager. Managers complete their appraisal of the individual against their goals, and other metrics that may be pertinent to their business and record in GTMS the individual’s performance and contribution. A rating is then given based on the performance factors identified for the individual.

• Managers must carefully consider the risk metrics pertinent to their business unit when determining individual performance ratings, especially when applying any discretion that results in an individual compensation outcome varying from the level implied by the performance of their business unit.

• Covered Employees are subject to an additional independent risk review process under which the control functions (i.e., Compliance, Finance, Risk, Internal Audit, and Legal) provide an evaluation of their individual risk behaviours. The results of the independent risk review process are included in the performance evaluation system to inform the performance review conducted by the Covered Employee’s manager.

Risk assessment of compensation plans • Citi has developed processes to risk assess its compensation plans and is overseen by the Global

Incentive Council (“GIC”). The purpose of the GIC is to establish global policies and oversee the incentive design and administration process at Citi. The GIC has overall responsibility for creating incentive compensation plan standards that do not incentivize excessive risk taking.

Remuneration of control function employees • Citi takes several measures to avoid conflicts of interest between the business and Control

Functions. They are: - Employees engaged in control functions have direct reporting lines that are separate from

the business and those reporting lines within the control functions are responsible for the reward of those employees both in terms of year end compensation, salary increases and promotion.

- The control functions are allocated a bonus pool separate from the revenue generating businesses, and decisions about allocations of those pools are made within the Control Functions themselves.

- Compensation (both salary and variable incentive) for the Control Functions is regularly tested in line with external market data to gauge whether it is in keeping with the market. The level of variable remuneration for control function employees is determined by reference to performance against objectives that are set and assessed within their respective functions.

Page 30 of 34

CITIBANK CANADA

Core Principle Statements The performance assessment of Canadian employees is based on individually tailored goals, and an assessment against Citi’s Core Principles Statements, which incorporates risk management and non-financial performance factors by business area into the performance appraisal process. Citi’s Core Principle Statements are:

• Common Purpose

- Maintains client focus - understands client needs and drives customer satisfaction - Works as a partner and shares resources that could benefit other areas - Sets clear and challenging performance goals for self and team - Adjusts management and communication styles to effectively manage virtual team members

and matrix reports - Creates and maintains a strong network with internal colleagues and stakeholders - Keeps abreast of industry changes - Holds self and others accountable for results and decisions.

• Ingenuity - Encourages fresh bold ideas - Supports experimentation and learning from mistakes - Challenges the conventional and fosters healthy debate - Recognizes and rewards ingenuity - Adopts proactive, not reactive, approach - Offers creative solutions and strives for continuous improvement - Manages ambiguity; demonstrates optimism and agility during change

• Leadership - Rewards, recognizes, and promotes individuals based on performance - Actively teaches, coaches, and grows team members' skills and capabilities - Provides balanced and specific feedback to others in a proactive way - Fosters a positive team environment in which people of diverse backgrounds feel valued - Takes responsibility for addressing problems, finding solutions and making prudent

decisions - Conveys awareness of own strengths and development opportunities - Engages in open, honest dialogue with others and directly addresses conflict when it arises.

• Responsible Finance – manages Risk and Compliance - Appropriately assess risk/reward relationships when making business decisions,

demonstrating particular consideration for the firm's reputation and safeguarding the bank by applying sound ethical judgment regarding business practices.

- Identify and escalate risk inherent in particular situations or transactions. The impact of these risks on any part of the Citi organization should be adequately assessed, monitored, controlled and reported.

- Conduct business and day-to-day activities in a way that is consistent with Citi’s commitment to fairness in all dealings and practices, including affording appropriate treatment to consumers and clients throughout the entire product and service life cycle.

- Adhere to the Code of Conduct, corporate and business specific policies, and implement appropriate controls as part of day-to-day responsibilities.

Page 31 of 34

CITIBANK CANADA

- Contributes to a ‘no surprises’ compliance culture by managing control issues with

transparency and candor. Resolve issues, communicate clearly, engage others, and escalate in a timely fashion.

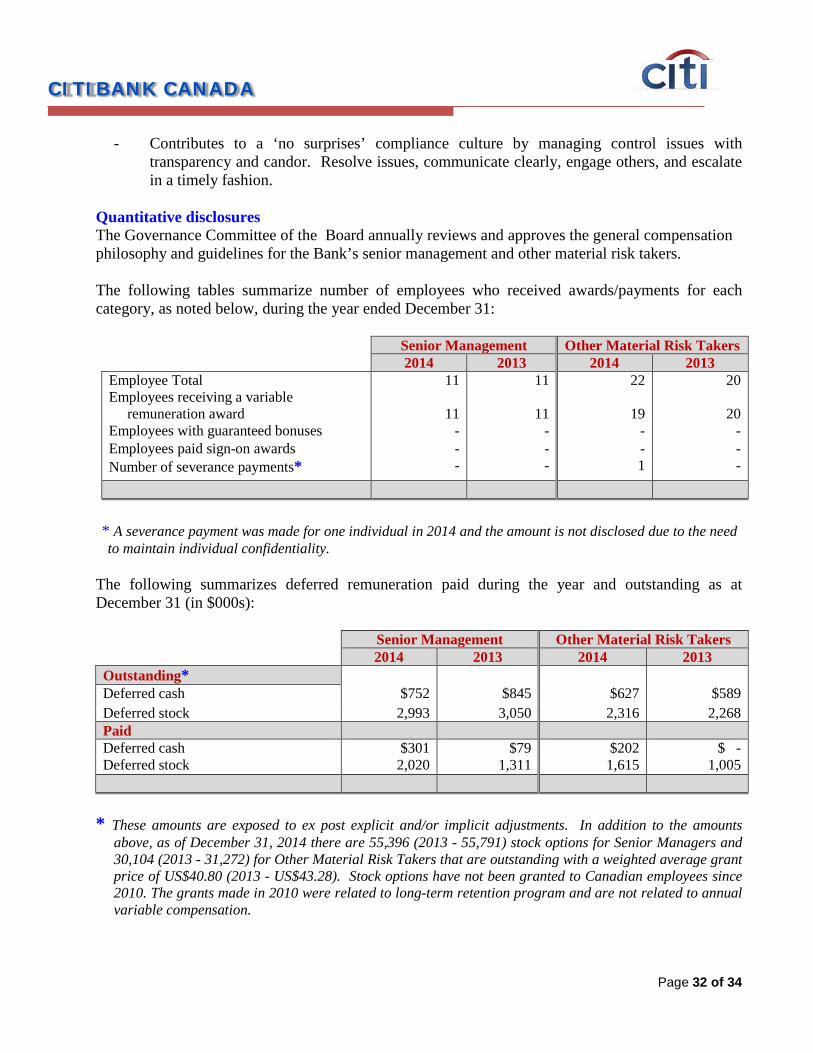

Quantitative disclosures

The Governance Committee of the Board annually reviews and approves the general compensation philosophy and guidelines for the Bank’s senior management and other material risk takers.

The following tables summarize number of employees who received awards/payments for each category, as noted below, during the year ended December 31:

Senior Management Other Material Risk Takers

2014 2013 2014 2013 Employee Total 11 11 22 20 Employees receiving a variable remuneration award

11

11

19

20

Employees with guaranteed bonuses - - - - Employees paid sign-on awards - - - - Number of severance payments* - - 1 -

* A severance payment was made for one individual in 2014 and the amount is not disclosed due to the need to maintain individual confidentiality.

The following summarizes deferred remuneration paid during the year and outstanding as at December 31 (in $000s):

Senior Management Other Material Risk Takers

2014 2013 2014 2013 Outstanding* Deferred cash $752 $845 $627 $589 Deferred stock 2,993 3,050 2,316 2,268 Paid Deferred cash $301 $79 $202 $ - Deferred stock 2,020 1,311 1,615 1,005

* These amounts are exposed to ex post explicit and/or implicit adjustments. In addition to the amounts

above, as of December 31, 2014 there are 55,396 (2013 - 55,791) stock options for Senior Managers and 30,104 (2013 - 31,272) for Other Material Risk Takers that are outstanding with a weighted average grant price of US$40.80 (2013 - US$43.28). Stock options have not been granted to Canadian employees since 2010. The grants made in 2010 were related to long-term retention program and are not related to annual variable compensation.

Page 32 of 34

CITIBANK CANADA

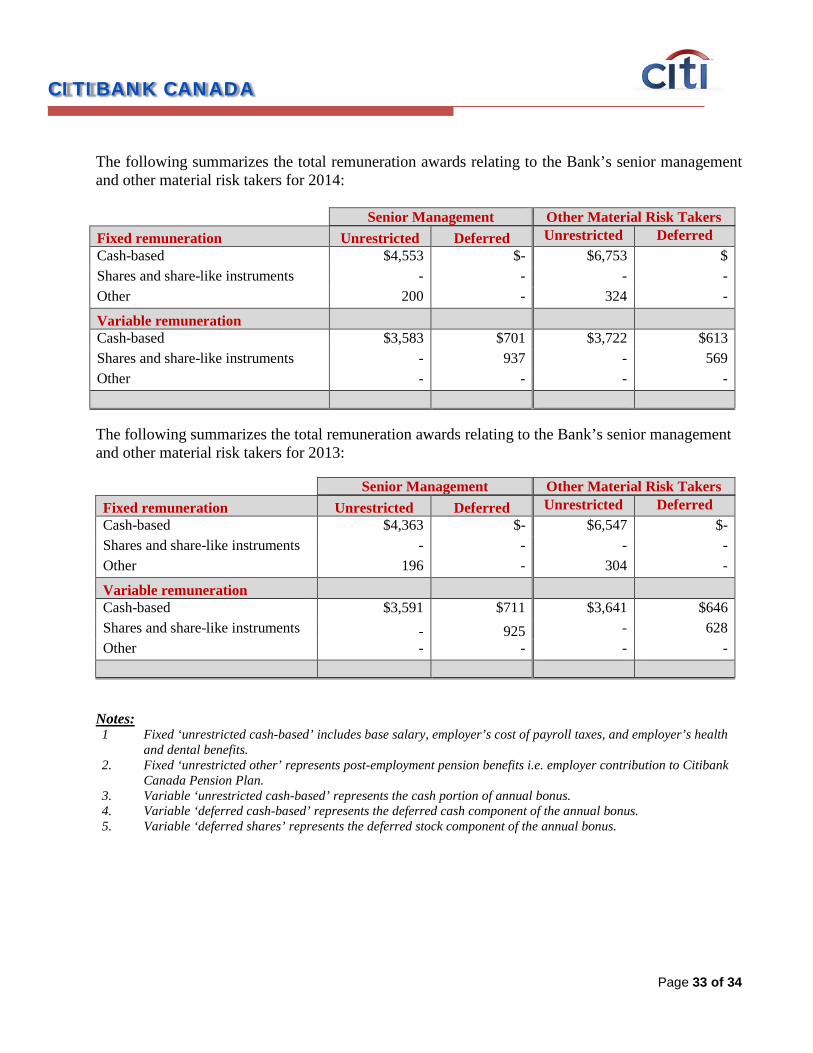

The following summarizes the total remuneration awards relating to the Bank’s senior management and other material risk takers for 2014:

Senior Management Other Material Risk Takers

Fixed remuneration Unrestricted Deferred Unrestricted Deferred Cash-based $4,553 $- $6,753 $ Shares and share-like instruments - - - - Other 200 - 324 -

Variable remuneration

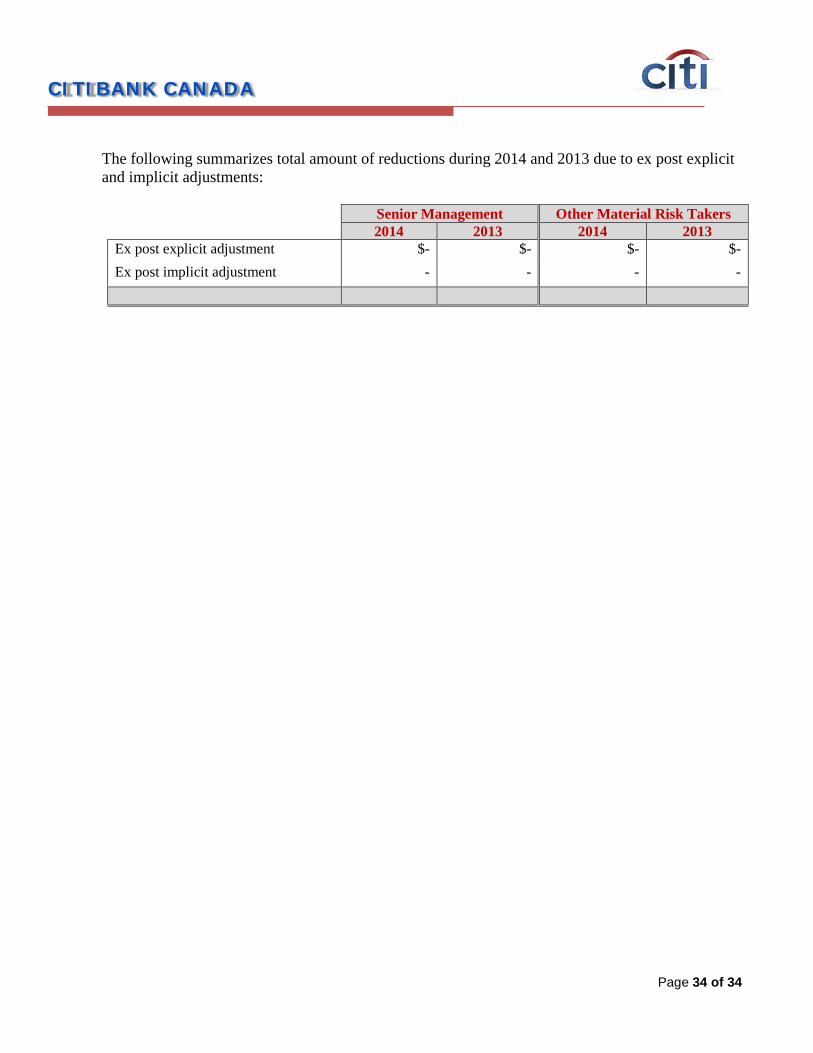

Cash-based $3,583 $701 $3,722 $613 Shares and share-like instruments - 937 - 569 Other - - - -