Cis ponzi scheme,mutual fund ppt

63

Group NO . 3 Vinay Kumar Elegeti 16106A1045 Pritee Khade 16106A1047 Tejshree Manore 16106A1049 Manish Tiwari 16106A1051 Ashish Thakur 16106A1054 Kiran Agarwal 16106A1058 Nikhil Balai 16106A1059

-

Upload

manish-tiwari -

Category

Education

-

view

224 -

download

2

Transcript of Cis ponzi scheme,mutual fund ppt

Group NO. 3Vinay Kumar Elegeti 16106A1045

Pritee Khade 16106A1047

Tejshree Manore 16106A1049

Manish Tiwari 16106A1051

Ashish Thakur 16106A1054

Kiran Agarwal 16106A1058

Nikhil Balai 16106A1059

Collective Investment Scheme (CIS)

A Collective Investment Scheme (CIS), is an investment scheme wherein several

individuals come together to pool their money for investing in a particular asset(s)

and for sharing the returns arising from that investment as per the agreement

reached between them prior to pooling in the money.

Regulated by: -

“SEBI (Collective Investment Schemes) Regulations, 1999” for the regulation of CIS.

Development Collective investment scheme In India

CIS is not a new phenomenon for India.

Investor collect money and invest primarily in agro-related activities.

Large scale miss-utilization of funds fraudulent activities lead to establishing a regulated system for the operation of CIS.

The Government of India, on November 18, 1997, decided that an appropriate regulatory framework for regulating schemesthrough which instruments like agro- bonds, plantation bonds etc. are issued, has to be put in place and decided that the as“Collective Investment Schemes” coming under the provisions of the SEBI Act

The preliminary report and regulations were released by SEBI to the public on December 31, 1998. Dave Committee foundedto be appropriate for the transparent working of CISs were incorporated in the Final Report dated April 5, 1999.

Section 11AA was added to the SEBI Act and the CIS Regulations were framed.

One of committee recommendation: -

CIS shall be constituted in the form of a trust

Instrument of the trust shall be in the form of a deed registered under the provisions of the Indian Registration Act, 1908 andexecuted by the Collective Investment Management Company (CIMC) in favor of the trustees named in such an instrument.

CIS Participants

• Collective Investment Management Comp

• Trustee

• Fund Manager or Investment Manager

• Shareholders or Unitholders

Advantage of Collective Investment Schemes (CIS)

• Affordability

• Accessibility

• Diversification

• Scope for good return

• Professional Investments Management

• Liquidity

• Safety & Transparency

Disadvantages of a collective investment scheme

Paying for a fund manager

Lack of choice

Loss of owner's rights

Different Kinds of Collective Investment Schemes Available in The Market

Section 11AA of the SEBI Act, 1992 A Collective investment scheme is any scheme or arrangement, which satisfies the conditions, referred to in sub-section (2) of section 11AA of the Securities and Exchange Board of India Act, 1992 (SEBI Act).

The following conditions:

I The contributions, or payments made by the investors, by whatever name called, are pooled and utilized solely for the purposes of the scheme or arrangement

ii. The contributions or payments are made to such scheme or arrangement by the investors with a view to receive profits, income, produce or property, whether movable or immovable, from such scheme or arrangement

iii. The property, contribution or investment forming part of scheme or arrangement, whether identifiable or not, is managed on behalf of the investors

iv. The investors do not have day to day control over the management and operation of the scheme or arrangement.

Note: -The Securities Laws (Amendment) Act, 2014- any pooling of funds under any scheme or arrangement, which is not registered with SEBI, involving a corpus amount of one hundred crore rupees or more shall be deemed to be a collective investment scheme.

Schemes not treated as CIS

• Scheme offered by a co-operative society

• Scheme under which deposits are accepted by non-banking financial companies

• Any scheme or arrangement being a contract of insurance to which the Insurance Act,

applies

• Scheme such as, Pension Scheme or the Insurance Scheme framed under the Employees

Provident Fund and Miscellaneous Provisions Act, 1952

• Scheme under which deposits are accepted by a company declared as a Nidhi or a mutual

benefit society under section 620A of the Companies Act, 2013

Collective Investment Management Company

Intro : -

A Collective Investment Management Company, incorporated under the provisions of the Companies Act, 2013 and

registered with SEBI under the SEBI (CIS) Regulations, 1999, to organize, operate and manage a Collective Investment

Scheme.

Circumstances under which a company registered as a Collective InvestmentManagement Company can raise funds from the public

• A registered CIS is eligible to raise funds from the public by launching schemes.

• Schemes have to be compulsorily credit rated as well as appraised by an appraising agency.

• The schemes also have to be Approved by the Trustee and contain disclosures, as provided in the Regulations

• A copy of the offer document of the scheme has to be filed with SEBI

• Company is entitled to issue the offer document to the public for raising funds from them.

Circumstances under which an existing Collective Investment Scheme be wound up

An existing collective investment scheme which failed to make an application for registration

Not desirous of obtaining provisional registration

Not been granted provisional registration

Having obtained provisional registration fails to comply with the provisions as laid down in the Regulations

On the expiry of duration specified in the scheme or on the accomplishment of the purpose of the scheme.

If in SEBI’s opinion the continuation of the scheme would be prejudicial to the interest of the unitholders, then the

scheme can be wound up.

Eligibility Criteria for CIS Registration

The board shall not consider an application for the grant of a certificate unless the applicant satisfies the following condition: -

1- The applicant is set up and registered as a company under the Companies Act, 2013

2- The applicant has, in its Memorandum of Association specified the managing of collective investment scheme as one of its main objects

3- The applicant has a net worth of not less than rupees five crores at the time of making the application

4- The applicant shall have a minimum net worth of rupees three crores which shall be increased to rupees five crores within three years from the date of grant of registration

5- The applicant has adequate infrastructure to enable it to operate collective investment scheme in accordance with the provision of these regulations

6- The directors or key personnel of the applicant shall consist of persons having adequate professional experience in related field

7- Have not been convicted for an offence involving moral turpitude or for any economic offence or for the violation of any securities laws

8- At least fifty per cent of the directors of such Collective Investment Management Company shall consist of persons who are independent and are not directly or indirectly associated with the persons who have control over the Collective Investment Management Company;

9- No person, directly or indirectly connected with the applicant has in the past been refused registration by the Board under the Act.

Governance of collective investment schemes (cis) Collective Investment Schemes (CIS) have been one of the most significant developments in financial intermediation during the past few decades.

This Note covers Five areas:

Legislative and Regulatory Framework

Rights of Investors The Role of the Private Sector

The Internal Governance of the CIS

Transparency and Disclosure

(CIS) that are promoted to the investing public should be required to operate through a recognized legal and regulatory framework.

In india CIS are operated as per the guidelines provided by SEBI

Basic Rights : -• Insolvency • key issues related

to the CIS • use funds in

companies in which it has invested.

• Treat all investor class equally

Right to exit

Industry Associations, Self-Regulatory Organizations and Firms

Responsibilities of Distributors and Financial Advisers

Governance Structure

Conflicts of Interest

Custody and Valuation of Assets

Internal Policies, Controls and Compliance

Independent Review

The Prospectus and Periodic Reports

Fees, Commissions and Expenses

COLLECTIVE INVESTMENT SCHEMES OF COLLECTIVE INVESTMENT MANAGEMENT COMPANY

No guaranteed returns

Disclosures in the offer document

Advertisement material

Appraising Agency

Misleading Statements

Offer period

Allotment of Units and refunds of moneys Money to be kept in separate account

and utilization

Investments and segregation of funds

Listing of collective investment schemes

Winding up of collective investment scheme

GENERAL OBLIGATIONS

• To maintain proper books of account and records, etc.

• Financial year

• Dispatch of warrants and proceeds

• Statement of Accounts and Annual Report

• Auditor’s Report

• Publication of Annual Report and summary thereof

• Periodic and continual disclosures

• Quarterly disclosures

• Disclosures to the investors

• Calling of meeting of unit holders, transfer and transmission of units

EXISTING COLLECTIVE INVESTMENT SCHEMES

Any person who has been operating a collective investment scheme at the time ofcommencement of these regulations shall be deemed to be an existing collectiveinvestment scheme and shall also comply with the provisions of the securities andexchange board of india (collective investment schemes) regulations, 1999.

Ponzi Scheme

PONZI SCHEME

• A Ponzi scheme is a fraudulent investment operation that pays returns to its investors from their

own money or the money paid by subsequent investors, rather than profit earned by the

organization.

• Offering investment products with extreme high returns in investments that actually don’t exist.

• They don’t invest the money, but pay the promised returns with the investors own money.

• The money of new investors is being used to pay the old investors.

Key Elements to Investment

. Consistent returns

. High Investment return with no risk or little risk

. Unregistered investments

. Unlicensed sellers

. Difficulty in receiving payments.

PONZI SCHEME SCAMMER

THE SARADHA

CASE

THE SAHARA CASE

The Saradha Case

SARADHA GROUP

• Key People

• Sudipto Sen

• Originally a financial concern but invested heavily in brand building.

• Bengali film industry

• Local television channels

• Newspapers

Scam

• Started in 2006 with promises of astronomical returns in Ponzi Schemes. Started building

brand by buying and selling media channels

• Used nexus of companies for money laundering

• Collected money by using secured debentures and redeemable preferential bond

• SEBI challenged them for the first time in 2009

• Creation of more than 300 new companies

Cont’d

• SEBI persisted, in 2010, Saradha’s method of raising funds changed

• Collective Investment Schemes like tourism packages, real estate fund launched in the name of

Chit Fund

• In 2011, SEBI warned West Bengal government about the alleged schemes of the company as the

concept of chit fund is regulated by state governments and not by SEBI

• In 2012, SEBI identified that the group operated CIS and not Chit Fund.

• Saradha group started trading in stock market and siphoning off the proceeds

Action Taken

7 Dec. 2012

On 7 December 2012, RBI governor stated that the West Bengal government should initiate suo motu action against companies which were indulging in financial malpractices.

Apr. 2013

Sudipto Sen, wrote a confessional letter to CBI in April 2013 and fled. He was later arrested.

22 Apr. 2013

PIL was filed on 22nd April 2013 in Guwahati High Court and Calcutta High Court CBI investigation started

Currently

He is in jail in Kolkata.

The Sahara Scam

Sahara Group

SEBI Action• K M Abraham (IAS OFFICER) passed an order dated

23rd June, 2011 directing the two companies to refund the money so collected to the investors

• Restrained the promoters of the two companies Sahara India Real Estate Corporation, Sahara Housing Investment Corporation including Mr. Subrata Roy from accessing the securities market till further orders.

• Sahara then preferred an appeal before Securities Appellate Tribunal (SAT) against the order.

• SAT confirmed and maintained the order of the Whole Time Member by an order dated 18th October, 2011.

• Subsequently Sahara filed an appeal before the Supreme Court of India against the SAT order.

• Supreme Court-directed refund of Rs 24,000 crore to an estimated three crore investors.

• Finally, Supreme court of India passed the judgment in favor of SEBI.

• Ordered Sahara to repay the Rs24000 cr with 15% interest.

• Supreme Court allowed Sahara to pay whole amount in three instalments

• 120 crore immediately, 10,000 crore in January 2013 and remaining amount by February

2013

• But by February they failed to pay second and third installment.

• SEBI after getting permission from Supreme Court froze all bank and Demat accounts

and attaches properties of chief Subrata Roy and three directors.

• On October 28 2013, Supreme Court directed Sahara to submit title deeds of properties

worth Rs.20,000 crore to SEBI.

Introduction of Mutual Fund

Mutual fund is an investment

programme that pools money from

shareholders and invests in a variety

of securities, such as stocks, bonds

and money market instruments.

Investments in securities are spread

across a wide cross-section of

industries and sectors and thus the

risk is reduced

Concept of Mutual Funds:

A mutual fund is just the connecting bridge or a

financial intermediary that allows a group of

investors to pool their money together with a

predetermined investment objective. The mutual

fund will have a fund manager who is responsible

for investing the gathered money into specific

securities (stocks or bonds). When you invest in a

mutual fund, you are buying units or portions of the

mutual fund and thus on investing becomes a

shareholder or unit holder of the fund.

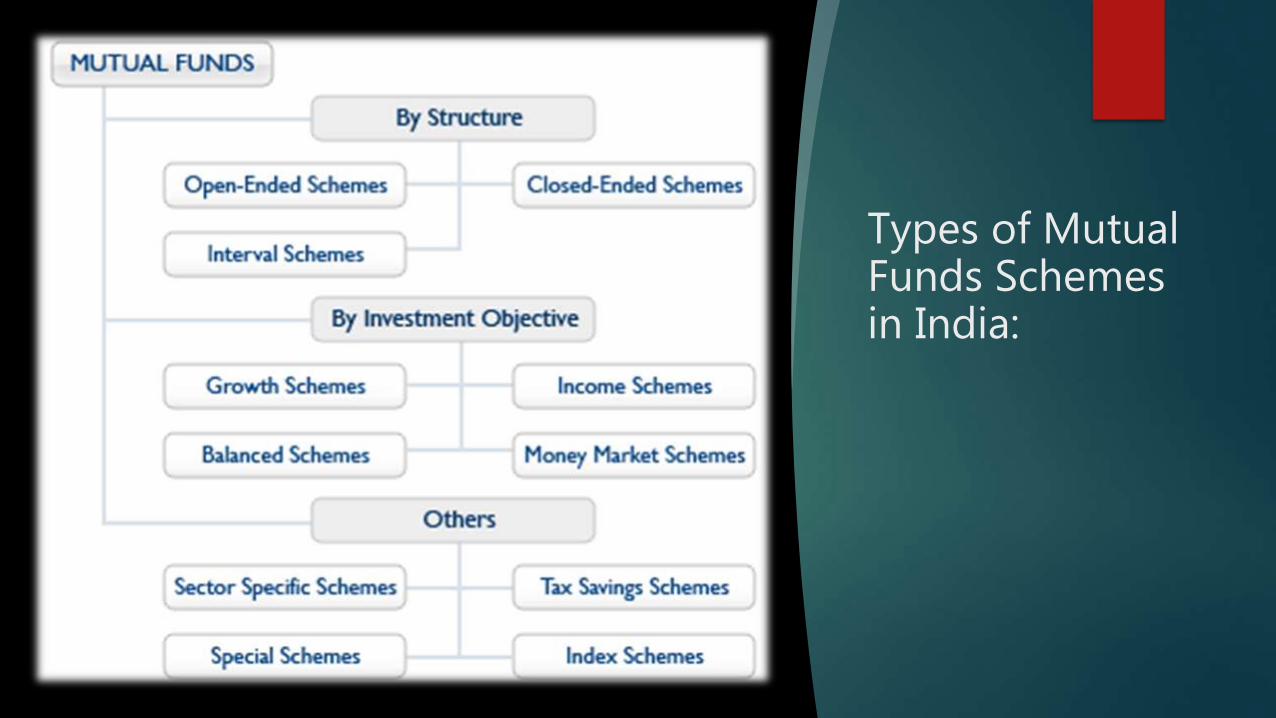

Types of Mutual Funds Schemes in India:

Regulations of Mutual Funds

SEBI

Why ?

• Increase Transparency

• Protects Investors Interests

• Avoid Financial Crime

SEBI (Mutual Funds) Regulations, 1996

Under Section 30 in the Securities

and Exchange Board of India Act,

1992

Advertisements of Mutual Funds in various mass media are flooded with variety of ads, enlightening

the people about the benefits of Mutual Funds, as to how it can be a lucrative investment alternate.

First Version “Mutual Fund investments are subject to market risks. Please read offer document carefully before investing.”

Second Version “Mutual Fund Investments are subject to market risks. Please read the Statement of Additional Information (SAI) and Scheme Information Document (SID) carefully before investing.”

Current Version “Mutual Fund investments are subject to market risks, read all scheme related documents carefully.”

• Which are the documents they are talking about?

• Scheme Information Document (SID)

• Statement of Additional Information (SAI)

• Key Information Memorandum (KIM)

• Monthly Factsheet

Why you should read these documents?

• Date of Issue

• Investment Objectives

• Investment Policies

• Risk Factors

• Information about the scheme

• Past Performance Data

• Fees and Expenses

• Key Personnel

• NAV and Valuation

• Tax Benefit Information

• Penalties and Litigations

• Rights of unit holders

• Redressal mechanism

Offer Document

Offer Document

Offer document is a document filed by the mutual fund with the regulator , SecuritiesExchange Board of India (SEBI).

Scheme Information DocumentStatement of Additional

Information

Scheme Information Document

(SID)

All Mutual Funds should use Form NS for filing an offer document pursuant to sub regulation (1) of Regulation 28 of

the SEBI (Mutual Funds) Regulations, 1996, along with filing fees as specified in the Second Schedule to these

Regulations.

Contents

I. Highlights of the Scheme

II. Introduction

III. Information about the Scheme

IV. Units and Offer

V. Fees and Expenses

VI. Rights of Unit Holders

VII. Penalties, Pending litigations or proceedings

• A Statement of Additional Information is a supplementary document to a mutual fund’s

prospectus that contains additional information about the fund and includes further

disclosure regarding its operation.

• Investors generally do not require to go through this document, as the information

contained in the Scheme Information Document provides all the information needed

Statement of Additional Information

(SAI)

Contents of the Statement of Additional Information

1. Information about Sponsor, AMC, and Trustee Companies

2. How to Apply

3. Rights of the Unit holders of the Scheme

4. Investment Valuation norms for Securities and other Assets

5. Tax & Legal & General Information

Trending topics in Mutual Funds

Mutual Fund’s Scheme Merger

• A circular for merging mutual fund schemes - G Mahalingam

• Regulator is looking to help investors cut through the clutter of 2,000 investment schemes

• Number of Schemes will be reduced by half

• The MF industry also needs to work on reducing the expense ratio - Mahalingam.

Linking Commodities Market with Mutual Funds

• Allowing Mutual Funds and portfolio management services PMS to trade in commodity services.

• Mr. Mrugank Paranjape, CEO MCX said” We can expect Mutual Funds and PMS to be allowed to invest in Commodities by the end of this fiscal year. “

CHIT FUNDS

• A Chit fund is a kind of savings scheme practiced in India.

• Under which a person enters into an agreement with a specified number of persons that every one of them shall subscribe a certain sum of money (or a certain quantity of grain instead) by way of periodical instalments over a definite period and that each such subscriber shall, in his turn, as determined by lot or by auction or by tender or in such other manner as may be specified in the chit agreement, be entitled to the amount.

ORIGIN

A totally Indian concept, the chit fund system has now been globally operated and won universal acclaim. In the villages of Kerala in India, many years ago, a small group of farmers operated a unique scheme.

Each farmer gave a fixed quantity of grains periodically to a selected trustee. The Trustee, after keeping aside a portion for himself, gave the rest to a member of the group to help him to meet his social commitments and other needs.

The farmer who received the lot continued to give the fixed quantity till every member of the group received his lot. The additional benefits when receiving the lot earlier led to competition. Some members were even willing to forgo a certain portion (like a discount) of the lot, in order to get an earlier chance. So, an auction was held and the lowest bidder got the lot.

This was the basis of what we know today as the “chit fund scheme”

TYPES OF CHIT FUNDS

There are three kinds of chit funds:

• Simple Chit

• Business Chit

• Prize Chit

KAJAL KUNDU

• Started with hotels & Entertainment then

he also set up Real Estate & Construction.

• In 2002 became a corporate agent of the LIC.

• Kajal Kundu along with his wife and son were

killed in an accident in 2003

GAUTAM KUNDU

• Chairman

• He owned a Bengali newspaper,

a TV channel and a jewellery

chain, among other things.

• He established Rose Valley

Media and Entertainment Wing in

2009.

WHAT WAS THE SCAM? The Rose Valley Group has been accused of

duping investors of about Rs 17,000 crores in different states.

SEBI found that the company offered plans with

interest rates ranging from 11.2% to 17.65%.

The subscription couldn’t be cancelled, and the

investor could not get money back before the end of

the tenure.

In July 2013, an investigation revealed suspicious expenditure in the profit and loss accounts of group companies.

It also revealed erratic “miscellaneous expenditures” with an almost nine fold increase in losses.

SEBI found out that the company did not follow due procedures.

RESULT

Kundu was arrested under criminal charges

and provisions of the Prevention of Money

Laundering Act.

The case was registered in June 2014 for

cheating, breach of trust, criminal breach by

public servant, criminal conspiracy, and

various sections of Prize Chits & Money

Circulation Schemes (Banning) Act, 1978.

FACTOR CHIT FUNDS MUTUAL FUNDS

DURATION Monthly periodic

RETURN ON

INVESTMENT12-16% Higher the risk , higher

the ROI

LIQUIDITY Higher than your paid-

value

Cannot get cash when required but based on

product performance.

RISK ELEMENT 0% risk due to guarantee

of funds.

100% risk since it is

totally market dependent

COLLECTIVE INVESTMENT SCHEME (CIS) MUTUAL FUND

Targeted for retail investors. Targeted for retail investors but majority of

investment are from non-retail investor.

Investment is very low. Minimum investment for Mutual funds is

500/-

Collective Investment Scheme confines its

investments to plantations and real estate.

Mutual Fund invests exclusively in

securities.

THANK YOU