chubb Annual Report 2007

151

THE CHUBB CORPORATION Annual Report 2007 Service: The Chubb Difference

-

Upload

finance18 -

Category

Economy & Finance

-

view

135 -

download

9

Transcript of chubb Annual Report 2007

THE CHUBB CORPORATION

Annual Report 2007

TH

EC

HU

BB

CO

RP

OR

ATIO

N•

Annual

Report

20

07

Service:The Chubb Difference

THE CHUBB CORPORATION15 Mountain View RoadWarren, New Jersey 07059Telephone (908) 903-2000www.chubb.com

2007 AR Covers_gac2.26:Layout 1 2/29/08 1:57 PM Page 1

Chubb celebrated its 125th anniversary in 2007.In 1882, Thomas Caldecot Chubb and his son Percyopened a marine underwriting business in theseaport district of New York City. The Chubbs wereadept at turning risk into success, often by helpingpolicyholders prevent disasters before they occurred.By the turn of the century, Chubb had establishedstrong relationships with the insurance agents and

brokers who placed their clients’ business with Chubb underwriters.“Never compromise integrity,” a Chubb principle, captures the spirit of

our company. Each member of the Chubb organization seeks to satisfycustomers by bringing quality, fairness and integrity to each transaction.

The Chubb Corporation was formed in 1967 and was listed on the NewYork Stock Exchange in 1984. Today, Chubb stands among the largestproperty and casualty insurers in the world. Chubb’s 10,600 employees servecustomers from offices in North America, South America, Europe and Asia(see page 8).

The principles of financial stability, product innovation and excellentservice combined with the high caliber of our employees have been themainstays of our organization for 125 years.

Contents1 Letter to Shareholders8 Chubb Worldwide Locations9 Service: The Chubb Difference

24 Employee Profiles26 Corporate Directory29 Form 10-K

On the cover: Chubb is proud to insure Salamander Farm, the Virginia homeof Sheila C. Johnson and her husband, the Hon. William T. Newman, Jr.See pages 14–15.

Some of the statements in this report may be considered forward-lookingstatements as defined in the Private Securities Litigation Reform Act of 1995.We caution investors that these forward-looking statements are not guaranteesof future performance. Various risks and uncertainties may cause actual results todiffer materially. These risks and uncertainties include those discussed inour 2007 Annual Report on Form 10-K (which forms a part of this document),in our Quarterly Reports on Form 10-Q and in the other filings we make withthe Securities and Exchange Commission. Forward-looking statements speakonly as of the date made, and we assume no obligation to update such forward-looking statements.

��Portions of this report discuss operating income and property and casualtyinvestment income after tax, both of which are “non-GAAP financialmeasures” (as defined by the Securities and Exchange Commission). Foradditional information regarding these non-GAAP financial measures, pleaserefer to the inside back cover of this report.

The Chubb Corporation The Chubb Corporation15 Mountain View RoadWarren, New Jersey 07059Telephone (908) 903-2000www.chubb.com

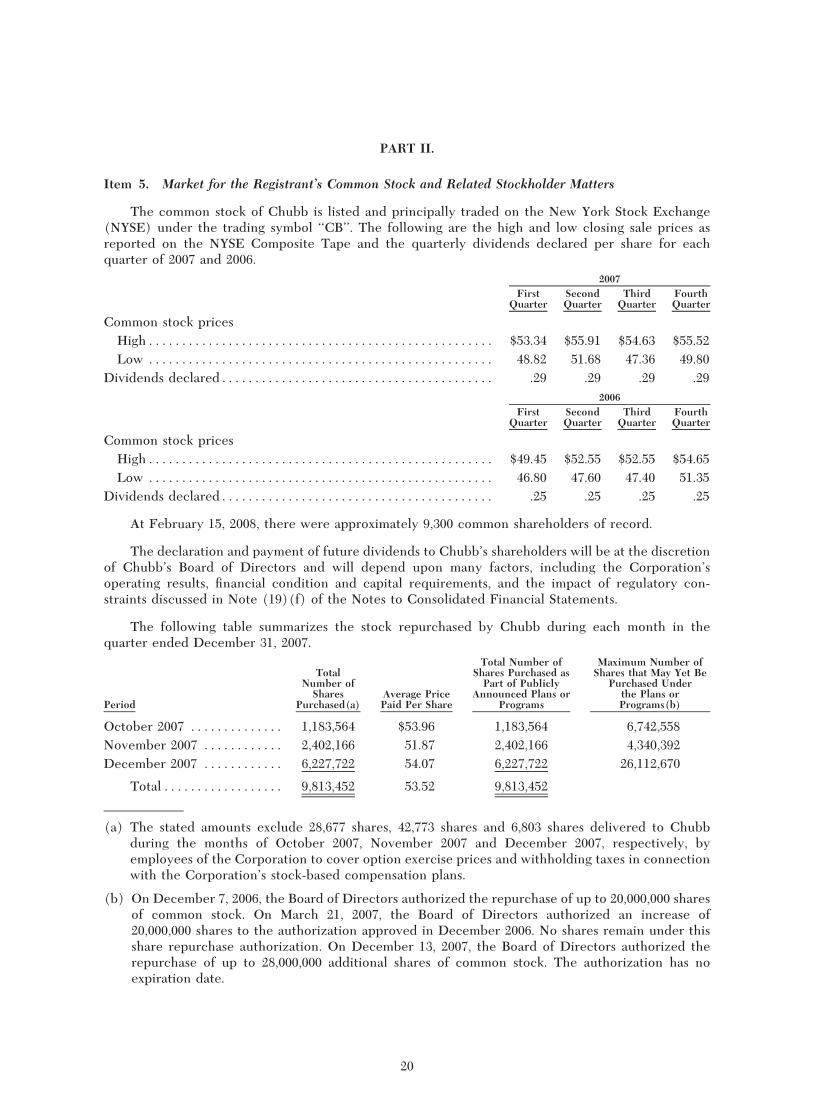

Stock ListingThe common stock of theCorporation is traded on theNew York Stock Exchangeunder the symbol CB.

Dividend Agent, TransferAgent and RegistrarBNY MellonShareholder Services480 Washington BoulevardJersey City, New Jersey 07310Telephone (877) 251-3569www.bnymellon.com

SEC and NYSECertificationsChubb has included as exhibits toits Annual Report on Form 10-Kfor the year ended December 31,2007 filed with the Securities andExchange Commission certificatesof its Chief Executive Officer andChief Financial Officer certifyingthe quality of Chubb’s internalcontrols over financial reportingand disclosure controls. Chubb hassubmitted to the New York StockExchange (NYSE) a certificate ofits Chief Executive Officercertifying that he is not awareof any violation by Chubb of theNYSE’s corporate governancelisting standards.

Photography Randy Duchaine, Peter Vidor, Joseph Lynch, Carlos Villalon and Mark Leong.

Operating income, a non-GAAP financialmeasure, is net income excluding after-taxrealized investment gains and losses.Management uses operating income,among other measures, to evaluate itsperformance because the realization ofinvestment gains and losses in any givenperiod is largely discretionary as to timingand can fluctuate significantly, which coulddistort the analysis of trends.

Property and casualty investment incomeafter income tax, a non-GAAP financialmeasure, is property and casualtyinvestment income after giving effect toapplicable income tax. Management usesproperty and casualty investment incomeafter income tax to evaluate its investmentperformance because it reflects the impactof any change in the proportion of theproperty and casualty investment portfolioinvested in tax-exempt securities and istherefore more meaningful for analysispurposes than property and casualtyinvestment income before income tax.

Explanation of Non-GAAP Financial Measures

2007 AR Covers_gac2.26:Layout 1 3/4/08 8:10 AM Page 2

Dear Fellow Shareholder:

I am pleased to report that 2007 was the fifth consecutive year of

record earnings for Chubb. In a slow-growth environment marked by

intense competition for market share, all our strategic business units

performed outstandingly well.

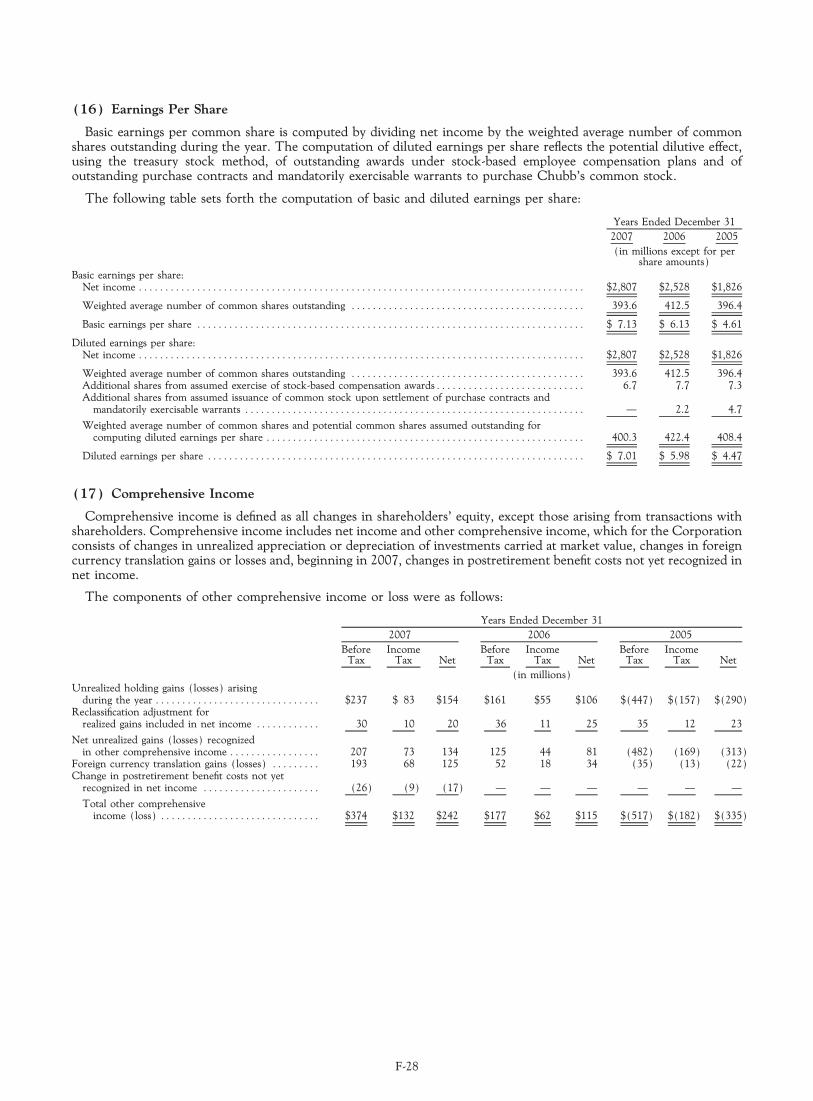

Net income grew to $2.8 billion from $2.5 billion in 2006, and net

income per share increased to $7.01 from $5.98. Operating income,

Letter to Shareholders

John D. FinneganChairman, President and Chief Executive Officer

Net Income per Share

$5.98

$4.01

2003 2004 2005 2006 2007

$4.47

$7.01

$2.23

2007 AR Text_gac2.26:Layout 1 2/29/08 2:02 PM Page 1

which we define as net income excluding realized investment gains and

losses, increased to $2.6 billion from $2.4 billion. Operating income per

share grew 14% to a record $6.41 from $5.60.

Net written premiums in 2007 declined 1% to $11.9 billion,

reflecting the impact of the transfer of our ongoing reinsurance assumed

business to Harbor Point in December 2005. Premiums for the

insurance business increased 1%; for the reinsurance assumed business,

premiums declined 65%.

Underwriting income grew 11% to $2.1 billion. The combined

loss and expense ratio for 2007 improved to 82.9% from 84.2% in 2006.

The expense ratio was 30.1% in 2007 and 29.0% in 2006, reflecting

growth in certain product lines outside the United States for which

commission rates are high.

Catastrophe losses in 2007 accounted for 3.0 percentage points of

the combined ratio, compared to 1.4 points in 2006. Excluding

catastrophe losses, the combined ratio improved 2.9 percentage points

in 2007 to an extraordinary 79.9% from 82.8% in 2006.

Property and casualty investment income pre-tax increased 9% to

$1.6 billion, reflecting strong cash flow from both investments and

underwriting; after taxes, it increased 9% to $1.3 billion.

Book value per share grew 14% in 2007. Over the past five years,

book value per share has grown at a compound average annual rate of 14%.

2

Combined Loss &Expense RatioPercentage of premium dollarsspent on claims and expenses

82%

84%

88%

86%

92%

90%

98%

96%

94%

100%

92.3% 92.3%

2003 2004 2005 2006 2007

82.9%

84.2%

98.0%

2007 was the fifth

consecutive year of

record earnings for

Chubb. In a slow-growth

environment marked

by intense competition

for market share, all

our strategic business

units performed

outstandingly well.

2007 AR Text_gac2.26:Layout 1 2/26/08 8:05 PM Page 2

For the five years ended

December 31, 2007,

Chubb’s compound

average annual total

return was 18.4%, far

better than the S&P 500

Index and nearly double the

total return of the S&P

Property & Casualty Index.

Total Return for Chubb Shareholders

Although 2007 was not a particularly good year in the stock

market, Chubb shareholders enjoyed a total return (stock appreciation

plus reinvested dividends) of 5.5%, nearly identical with the return of

the Standard & Poor’s 500 Index and much better than the Standard &

Poor’s Property & Casualty Index, which had a negative 13.2% return

in 2007.

For the five years ended December 31, 2007, Chubb’s compound

average annual total return was 18.4%, far better than the S&P 500

Index’s 12.8% and nearly double the 9.5% total return of the S&P

Property & Casualty Index. Chubb’s market capitalization at the end

of 2007 was still a modest 1.4 multiple of book value.

John J. Degnan, Vice Chairmanand Chief Administrative Officer

Thomas F. Motamed, Vice Chairmanand Chief Operating Officer

Michael O’Reilly, Vice Chairmanand Chief Financial Officer

3

2007 AR Text_gac2.26:Layout 1 2/29/08 12:49 PM Page 3

Operations Review

Chubb Personal Insurance (CPI) net written premiums grew 5%

to $3.7 billion. As a result of higher catastrophe losses in 2007, the

combined ratio in 2007 was 84.8% compared to 81.7% in 2006.

Excluding catastrophes, CPI’s combined ratio was 78.5% in 2007,

compared to 78.0% in 2006.

CPI specializes in insuring the homes, autos, yachts, jewelry, art,

antiques, collectibles and other possessions of affluent customers in the

United States, Canada, the United Kingdom, Australia and Brazil. CPI

also offers personal excess liability insurance and group accident

insurance.

Chubb Commercial Insurance (CCI) net written premiums

declined 1% to $5.1 billion. The combined ratio was 85.8% in 2007,

compared to 83.1% in 2006. Excluding catastrophe losses, the combined

ratio was 83.2% in 2007, compared to 82.5% in 2006. Margin

compression due largely to competitive pricing pressures was mitigated

by improved loss experience.

CCI is a global provider of multiple peril, monoline casualty and

property, excess liability and workers’ compensation coverages, with

special expertise in serving the local insurance needs of companies

wherever in the world they do business. In an industry often regarded as

fully commoditized, Chubb continues to rise above the competition

4

In an industry often

regarded as fully

commoditized, Chubb

continues to rise above

the competition with

specialized coverages,

loss-control expertise,

outstanding claim service

and highly selective

underwriting criteria.

2007 AR Text_gac2.26:Layout 1 3/3/08 11:54 AM Page 4

with specialized coverages, loss-control expertise, outstanding claim

service and highly selective underwriting criteria.

Chubb Specialty Insurance (CSI) net written premiums remained

virtually unchanged at $2.9 billion — but the combined ratio improved

to 77.4% from 87.5%. In our Professional Liability (PL) book, which

includes, among others, directors & officers (D&O) and errors &

omissions (E&O) insurance coverages, premiums declined 1%, and the

combined ratio improved to 82.4% from 91.8% in 2006.

Our PL book of business was formerly dominated by Fortune 500

companies. Following heavy losses in 2000 through 2002, we shifted our

emphasis to middle-market insureds and reduced our limits per insured.

These and other underwriting decisions, together with a decline in class

action litigation and favorable court decisions, have resulted in

dramatically lower losses and improved profitability despite declining

rates.

CSI also includes our Surety business, which had premium growth

of 13% and a combined ratio of 35.4%.

Returning Capital to Our Shareholders

As part of our capital management program, we returned over

$2.6 billion of excess capital to our shareholders in 2007: $451 million

in dividends and $2.2 billion through share repurchases. In March 2007,

5

Shareholders’ Equity($ in billions)

$13.9$14.4

$10.1

2003 2004 2005 2006 2007

$12.4

$8.5

We returned over

$2.6 billion of excess

capital to our shareholders

in 2007. In March 2007,

the Board raised the

dividend by 16%, and in

December, the Board

approved a new share

repurchase program.

2007 AR Text_gac2.26:Layout 1 2/28/08 3:54 PM Page 5

our Board of Directors raised the dividend by 16%, marking Chubb’s

25th consecutive annual dividend increase. In December 2007, the

Board approved a new 28-million-share repurchase program, which we

expect to complete by the end of 2008, subject to market conditions.

Managing Risk

Dominating the headlines since mid-2007 has been the global

credit crisis precipitated by the sub-prime mortgage meltdown. I am

pleased to report that our investment portfolio has not had and does not

have any direct exposure to either sub-prime mortgages or collateralized

debt obligations. Regarding our tax-exempt bonds, 43% of our portfolio

is insured. It’s our view that even if the insurance ceased to exist, the

underlying quality of the bonds is so strong that the aggregate mark-to-

market impact on our financial condition would not be material. As for

6

Our portfolio has not had

and does not have any

direct exposure to either

sub-prime mortgages or

collateralized debt

obligations.

200720062005200420032002$15.00

$30.00

$45.00

$60.00

$26.10

$19.93

Market Value per Share

$54.58

Book Value per Share

$38.56

2002 2003 2004December 31

2005 2006 2007

Book Value and Market Value per Share

2007 AR Text_gac2.26:Layout 1 3/3/08 9:25 AM Page 6

our mortgage-backed securities, 98% of our portfolio was rated AAA at

year end.

We are in the business of assuming risk. However, expert investing

and underwriting — knowing which risk (and how much of it) to

assume — are fundamental to long-term success in the insurance

business. Having just celebrated our 125th anniversary with a year of

record earnings, we intend to pursue actions and behaviors that will

enable us to prosper for another 125 years.

My thanks to our customers, agents, brokers, employees and

shareholders for your efforts and support all through the year.

John D. FinneganChairman, President and Chief Executive Officer

February 21, 2008

7

We are in the business of

assuming risk. However,

expert investing and

underwriting — knowing

which risk (and how much

of it) to assume — are

fundamental to long-term

success in the insurance

business.

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

$22,000

$24,000 Chubb$23,300

S&P 500$18,300

S&P P&C$15,600

2002 2003 2004December 31

2005 2006 2007

Value of $10,000 invested on December 31, 2002 in Chubb common stock,S&P 500 Index and S&P Property & Casualty Index, including share priceappreciation and reinvested dividends. Past results are no guarantee of future returns.

Total Return

2007 AR Text_gac2.26:Layout 1 2/28/08 3:56 PM Page 7

Seamless Global Service

UNITED STATES

Mid-AtlanticBaltimore, MDChesapeake, VAFlorham Park, NJHarrisburg, PANew York, NYPhiladelphia, PAPittsburgh, PARichmond, VAWashington, DCWhitehouse Station, NJNortheastAlbany, NYBoston, MALong Island, NYNew Haven, CTPortsmouth, NHRochester, NYSimsbury, CTWestchester, NYWestDenver, COLos Angeles, CANewport Beach, CAPhoenix, AZPleasanton, CAPortland, ORSalt Lake City, UTSan Diego, CASan Francisco, CASeattle, WA

NorthChicago, ILCincinnati, OHCleveland, OHColumbus, OHDes Moines, IAGrand Rapids, MIIndianapolis, INItasca, ILKansas City, MOLouisville, KYMilwaukee, WIMinneapolis, MNSt. Louis, MOTroy, MISouthAtlanta, GAAustin, TXBirmingham, ALCharlotte, NCColumbia, SCDallas, TXHouston, TXJackson, MSMaitland, FLNashville, TNRaleigh, NCSan Antonio, TXSunrise, FLTampa, FLTulsa, OK

CANADACalgary, ABMontréal, PQToronto, ONVancouver, BC

BERMUDAHamilton

LATIN AMERICAArgentinaBuenos AiresBrazilBelo HorizonteBrasiliaCuritibaPorto AlegreRio de JaneiroSão PauloChileSantiagoColombiaBarranquillaBogotáCaliMedellínMéxicoGuadalajaraMéxico CityMonterrey

EUROPEAustriaViennaBelgiumBrusselsDenmarkCopenhagenFranceBordeauxLilleLyonParisGermanyDüsseldorfHamburgMunichIrelandDublinItalyMilan

NetherlandsAmsterdamNorwayOsloSpainBarcelonaMadridSwedenStockholmSwitzerlandZurichUnited KingdomBelfastBirminghamGlasgowLeedsLondonManchesterReading

ASIA/PACIFICAustraliaBrisbaneMelbournePerthSydneyChinaBeijingHong KongShanghaiJapanTokyoKoreaSeoulSingaporeTaiwanTaipeiThailandBangkok

Worldwide Headquarters: Warren, NJ

8

2007 AR Text_gac2.26:Layout 1 2/28/08 4:02 PM Page 8

C hubb’s commitment to superior service, whichhas always been the essence of our reputation,

continues to guide us in a world that has changed dra-matically since the company opened its doors in 1882.Early on, we distinguished ourselves from competitors byproviding principled claim handling and expert loss pre-vention advice. It was a focus thatdemonstrated our personal interest inthe success and well-being of the indi-viduals and businesses we insure, as wellas our respect for the agents and brokerswith whom we partner. Those core val-ues continued to guide us as we built aworldwide branch network that not onlyallowed us to provide an increasingly so-phisticated range of services, but alsohelped us remain a local company withstrong ties to each of the communities inwhich we operate.

In a business as complex as property and casualtyinsurance, superior service is predicated on specializedexpertise. Chubb’s underwriting, claim and loss preven-tion specialists spend years developing deep knowledgeand businesses relationships in their selected industry seg-ments or areas of expertise. Our customers trust Chubb’sspecialists to understand and protect what they value —whether it’s a personal art collection, a biotechnologylaboratory, bank information systems or a wineryvineyard.

We also recognize the need to balance our quest forincreased speed and efficiency with our commitment toworking closely with our producers and customers aroundthe world. Because technology has the potential to dis-tance companies from those they serve, we take greatcare to use it in ways that add value and dimension to

our relationships. In addition to stream-lining the routine services associatedwith the insurance transaction, technol-ogy has provided new opportunities forus to partner with our customers on lossprevention efforts, claim handling, fi-nancial management and service needsunique to their homes or businesses.

Of course the most meaningfulmeasure of the service provided by anyinsurer is its ability and willingness to paypromptly and fairly in the event of a loss.

Chubb’s outstanding financial strength, which has con-sistently earned the highest rating from A.M. Best, as-sures our customers that our claim handling integrity isbacked by more than 125 years of responsible financialmanagement.

Insurance is fundamentally a promise, made tangi-ble not only by fair dealing when a claim occurs, but alsoby the quality of the overall service relationship an in-surer has with its customers. The pages that follow offerprofiles of customers, agents and brokers who have ex-perienced first-hand what service means to Chubb.

9

Our customers

trust Chubb’s

specialists

to understand and

protect what

they value.

Service: The Chubb Difference

Photo at left: 5 & 7 South WilliamStreet, circa 1897. In 1892, PercyChubb and Charles Myers bought theland and building at 5 & 7 South WilliamStreet and moved the firm there. Here agroup of employees stand in front of theold building, which served as Chubb’sheadquarters until 1901.

2007 AR Text_gac2.26:Layout 1 2/28/08 4:03 PM Page 9

10

O n paper, it appears like a perfect fit — two globalcorporations with impeccable reputations work-

ing together to help maintain and enhance those repu-tations.

Christie’s, the venerable London-based auction house with operations in43 countries, and Chubb, the highlyrated insurance carrier with offices in 28countries, first teamed up in 2004.Chubb provides Christie’s property andcasualty insurance on a global basis andis a participating insurer for other cov-erages, such as directors and officersliability.

But Christie’s and Chubb arelinked by more than just insurance policies. The twocompanies have formed a close bond by working togetheron a global basis to help identify and mitigate potential

problems and ensure that Christie’s has appropriate andsufficient insurance protection wherever it does business.

Chubb secures locally admitted insurance policiesin many countries where Christie’s has operations andalso provides coverage on a non-admitted basis wherenecessary. These policies are combined under a con-trolled master policy to help close coverage gaps.

“Because Christie’s is all over the world, we needto be flexible and creative,” said Erika Bloor, who super-vises risk-management accounts at ChubbUnited King-dom. “Christie’s has offices and showrooms in manycountries, and, in some countries, there may be just oneperson working from home. The challenge is making sureChristie’s is protected wherever it does business.”

Claim handling also is critical for a multinationalorganization. Chubb helps keep Christie’s risk manage-ment team informed by consolidating loss data from

around the world and delivering them ina single quarterly report to the Londonheadquarters. “Knowing what is happen-ing in its overseas operations helps giveChristie’s risk managers peace of mind,”Bloor said.

Tim Lloyd, Risk Manager forChristie’s, said Chubb’s global networkwas one of the deciding factors when itselected an insurer. “In addition, we werelooking for a respected, financially soundcarrier with a track record of dealing

with claims promptly and fairly,” Lloyd said. “Chubb hasa reputation for working effectively with risk-managedbusinesses.”

Chubb Service: Global Capability, Prompt and Fair Claim Handling

Photo at right: Brian Holland, Group Insurance Director ofChristie’s, is photographed at a Christie’s showroom in London.

Photo at left: At Christie’s in London are (from left) Erika Bloor,Chubb United Kingdom Manager for Risk Management; GrahamMedcalf, Chubb United Kingdom Property Manager; and TimLloyd, Christie’s Risk Manager.

“We were looking for a

respected, financially

sound carrier with a

track record of dealing

with claims promptly

and fairly.”

2007 AR Text_gac2.26:Layout 1 2/28/08 4:06 PM Page 10

11

2007 AR Text_gac2.26:Layout 1 2/26/08 8:07 PM Page 11

12

As Chief Financial Officer for one of the leaders inluxury travel, business and lifestyle accessories,

Tumi’s Mike Mardy places a high premium on productquality, functionality and innovation— and he expects the same from Tumi’sinsurer.

Since 1975, New Jersey-basedTumi has relied on innovation in high-quality products to achieve success.Ranging from luggage, business cases andhandbags to electronics, pens andwatches, its award-winning products aredesigned to meet the evolving needs ofconsumers worldwide.

Tumi’s relationship with Chubbbegan with the purchase of a single excess liability policyin 1999. Today, Chubb provides a uniquely tailored prop-erty and casualty insurance program, which Chubb un-

derwriters adapt to fit Tumi’s changing needs. But thecompany’s choice of Chubb extends beyond quality ofcoverage: “Chubb takes the time to understand our busi-ness and its exposures and then partners with us to im-plement effective loss prevention measures,” explainedMardy.

While Tumi’s operations include 75 stores in majorcities throughout the world, Chubb’s loss-control effortsare focused on Vidalia, Georgia, where 182 employeeswork at Tumi’s 260,000-square-foot distribution, productrepair and customer service facility. Chubb has workedwith Tumi to reduce workplace injuries through er-gonomic assessments, Occupational Safety and HealthAdministration employee training, a formal safety com-mittee and loss control inspections.

“Since our first visit to Vidalia, it was evident thatthe local staff was eager to develop a more thorough pro-gram to address their exposures while caring for employ-ees,” said Chubb Property and Casualty Risk EngineerDexter Sturdivant, who helped develop a baggage-repairworkbench to reduce repetitive motion injuries.

Peter Closs, Tumi’s Director ofCorporate Finance, said that Chubb’sloss mitigation efforts have helped im-prove Tumi’s workers’ compensationaccident experience rate by a third, sig-nificantly reducing claim frequency andseverity.

While Tumi values Chubb’s prod-uct quality and risk management expert-ise, Mardy noted that claim handling iswhat sets Chubb apart. “When you in-sure a business or underwrite a casualty

risk with Chubb, you can be assured there will be nohassle getting the claim resolved quickly and effectivelyto get you back in business.”

Chubb Service: Understanding the Insured’s Business

Photo at right: Tumi’s Mike Mardy, Chief Financial Officer(seated) and Peter Closs, Director of Corporate Finance, ina showroom at the company’s South Plainfield, New Jerseyheadquarters.

Photo at left: At the baggage repair center of Tumi’s Vidalia,Georgia warehouse are (from left) Dexter Sturdivant, ChubbProperty and Casualty Risk Engineer; Tina Weeks, Tumi’sHuman Resources Coordinator; Richard Lawrence, VicePresident of Tumi’s Georgia operations; and Barbara Lawrence,Manager of Tumi’s After Sales Service.

“...with Chubb, you

can be assured there

will be no hassle

getting the claim

resolved quickly and

effectively to get you

back in business.”

2007 AR Text_gac2.26:Layout 1 2/28/08 4:07 PM Page 12

13

2007 AR Text_gac2.26:Layout 1 2/26/08 8:08 PM Page 13

In addition to doubling the size of the existingstructure, the project included the addition of a tenniscourt, landscaped spaces to accommodate outdoor en-tertaining and the construction of an equestrian centerfor her daughter Paige. “The renovation of SalamanderFarm was a masterful integration of architectural, land-scape and interior design,” said Matt Burgey, Chubb Per-sonal Lines Manager in Washington, D.C. “It’s a uniqueproperty that requires the type of custom loss-preventionservices Chubb excels at providing.”

During the renovation, Chubb Technical Special-ist Rick Albers worked closely with Ms. Johnson’s con-tractor and Nick Bretz, Operations Director for Ms.Johnson’s Family Office at Salamander Farm, to design astate-of-the-art fire and security system that included in-stallation of a 10,000-gallon water tank on the property.“By incorporating the tank in our fire-protection plan,we essentially installed our own hydrant — which could

be critical in the event of a fire, given thesize and location of the farm,” said Bretz.“We have not only the piece of mindthat comes from knowing we have doneeverything possible to safeguard Ms.Johnson’s home, but the added benefit ofa substantial premium credit in return foracting on Chubb’s loss-prevention rec-ommendations.”

Chubb’s emphasis on expertise andsuperior service made it the clear choicefor Ms. Johnson, a customer since 1996.

“I’m a perfectionist who doesn’t like leaving things tochance,” she said. “I expect the same from my insurancecompany.”

Photo at right: Sheila C. Johnson and the Honorable William T.Newman, Jr. in the living room of the main house atSalamander Farm.

Photo at left: Matt Burgey, Chubb’s Personal Lines Managerin Washington, D.C. (left), and Nick Bretz, Operations Directorfor the Johnson Family Office at Salamander Farm, outside oneof the farm’s stables with Dominique, one of Paige Johnson’sshow horses.

14

S heila C. Johnson — a founder of Black Enter-tainment Television, President and Managing

Partner of the Women’s National Bas-ketball Association’s Washington Mys-tics, CEO of Salamander Hospitality,philanthropist, educator and entrepre-neur — is above all a visionary. In 2002,Ms. Johnson pictured her 100-year-oldstone farmhouse in the rolling hills ofVirginia transformed into a Tuscan-stylevilla graced by gardens, ponds and fruittrees. Accustomed to making her dreamscome true, she launched a three-yearrenovation project that quickly became apassion. Named “Salamander Farm,” the property is nowhome to Ms. Johnson and her husband, Arlington, Vir-ginia, Chief Judge William T. Newman, Jr.

Chubb Service: Technical Loss-Prevention Expertise

“I’m a perfectionist

who doesn’t like

leaving things to

chance. I expect the

same from my

insurance company.”

2007 AR Text_gac2.26:Layout 1 2/28/08 4:13 PM Page 14

1515

2007 AR Text_gac2.26:Layout 1 2/28/08 4:16 PM Page 15

16

As a leading agribusiness group based in Singapore

with facilities in 20 countries, Wilmar needs an

insurer that has the insurance, IT and

risk management capabilities to support

its growing international operations.

Since 1991, Wilmar has become

the largest global processor and mer-

chandiser of palm and lauric oils, deliv-

ering products to more than 50

countries. While Chubb provides pro-

tection for Wilmar’s directors and offi-

cers, our primary assignment is to support

the transportation of Wilmar’s cargo

with coverage and loss-prevention solutions.

After learning in 2004 about Chubb’s reputation as

an ocean cargo specialist and leader in loss control,

Wilmar senior management chose Chubb to develop a

cargo coverage programwhich was tailored to meet their

unique exposures.

One of the biggest benefits to Wilmar’s insurance

process, explained ShippingManager Shannonjeet Kaur,

is the Chubb Certificate Issuance System (CCIS), which

was specifically designed to meetWilmar’s needs. When

Wilmar’s products are purchased, the trades are often fi-

nanced by banks, and certificates are necessary to

demonstrate proof of insurance.

“Before CCIS, we had to manually issue and verify

insurance certifications,” said Kaur. “Chubb’s system

saves our staff time by enabling the au-

tomatic issuance of certifications and de-

velopment of customized reports.”

Chubb’s loss control department is

currently working to reduce Wilmar’s

marine transport exposures and also as-

sessing Wilmar’s vessel selection and

chartering best practices, which will help

streamline the worldwide distribution of

the company’s products.

Chubb continues to earnWilmar’s

business with comprehensive coverages, first-class service

and loss-control leadership.

Chubb Service: Customized Solutions for Unique Needs

Photo at right: At the entrance to Wilmar’s Singaporeheadquarters are Shannonjeet Kaur, Shipping Manager (left),and Carol Wong Choy Lan, Operations and DocumentationsManager.

Photo at left: Valerie Lee, Wilmar Operations Executive(seated), uses the Chubb Certificate Issuance System on acomputer station at Chubb’s Singapore office with Jessie Siow,Chubb Senior Marine Underwriting Assistant.

“Chubb’s system

saves our staff time

by enabling the

automatic issuance

of certifications and

development of

customized reports.”

2007 AR Text_gac2.26:Layout 1 2/29/08 12:58 PM Page 16

1717

2007 AR Text_gac2.26:Layout 1 2/26/08 8:09 PM Page 17

18

In 2007, Chubb continued todemonstrate how its loss control ex-pertise could help protect TastefullySimple employees. The addition of

two warehouse conveyor lines resulted in increased fork-lift traffic and more chances for accidents. With the in-crease in business, employees had also begun toexperience an increase in repetitive stress injuries. ChubbLoss Control worked with Tastefully Simple’s risk man-ager to help develop and implement changes to forklift

traffic patterns and to packaging andhandling procedures.

“By providing all of Tastefully Sim-ple’s insurance coverages and loss-control services, we’re able to offer truecontinuity of service,” said Chubb’sKrista Ksicinski, Commercial InsuranceSpecialty Senior Underwriter.

“Tastefully Simple has very highstandards,” noted Founding Partner andChief Operating Officer Joani Nielson.“We want to work with the best of the

best; that’s how we’re going to grow. Whether it’s a foodvendor or our insurance carrier, everyone we work withis an extension of our image. Chubb’s commitmentto offering quality products and service truly aligns withTastefully Simple’s culture and philosophy of doingbusiness.”

Photo at right: In the atrium of theTastefully Simple headquarters inAlexandria, Minnesota, are Jill BlashackStrahan, Founder and Chief ExecutiveOfficer (left), and Joani Nielson, FoundingPartner and Chief Operating Officer.

Photo at left: Pictured among boxes ofgourmet food in the Tastefully SimpleAlexandria, Minnesota, warehouse areJason Berger, Property and CasualtyRisk Engineer in Chubb’s Minneapolisbranch (left), and Richard Miller, ChiefFinancial Officer, Tastefully Simple.

W hen Minnesota-based Tastefully Simplebegan selling gourmet food through home

taste-testing parties in 1995, its founder reported to workat a small shed with no running water and packed orderson a pool table. Today, the company’s 340 employeeswork in a state-of-the-art 200,000square-foot office/warehouse. Accordingto Founder and Chief Executive OfficerJill Blashack Strahan, “Our amazingheadquarters team and our 26,000 con-sultants have been critical in getting thecompany to the next level.” She alsonoted that “vendors and serviceproviders play an important role in help-ing us exceed expectations.”

With this in mind, Tastefully Sim-ple’s Chief Financial Officer, Rick Miller,turned to Chubb in 2002 for property and casualty insur-ance protection, as well as critical loss control services.“Chubb has the ability and resources to help us as we buildthis business,” noted Miller. “Its expertise in all areas of in-surance — especially loss control — enables Chubb tobring solutions to the table that are in our best interest.”

Chubb Service: Broad Coverages, Loss Control

“Its expertise in all

areas of insurance —

especially loss control

— enables Chubb to

bring solutions to the

table that are in our

best interest.”

2007 AR Text_gac2.26:Layout 1 2/26/08 8:10 PM Page 18

1919

2007 AR Text_gac2.26:Layout 1 2/26/08 8:10 PM Page 19

20

W ith roots that run deep in the agriculturalcommunity, Agricredit Acceptance, LLC, in

Johnston, Iowa, and AGCO Finance,LLC, in Duluth, Georgia, provide fi-nancing options for the agriculture andfood production industry. Agricredit Ac-ceptance and AGCO Finance have acommon parent company, De Lage Lan-den, a subsidiary of Rabobank Neder-land, formed in the 1890’s as a collectionof small rural banks financing local farm-ers in the Netherlands.

Since Agricredit Acceptanceopened its doors to the agribusiness com-munity 50 years ago, many aspects of theindustry have evolved. According to Agricredit Accept-ance Chief Executive Officer Dennis J. Fedosa, “Thegreatest challenge for companies servicing this industry

is market segmentation. More people are living in ruralareas, and their needs are different from the large-scalecommercial farmer. We need to have a comprehensivefinance offering that is easily explained to our customersbut that can be tailored to their individual needs.”

In 2005, Agricredit Acceptance and AGCO Fi-nance sought an insurance partner that fully understoodtheir needs and had the flexibility to offer a product thatwould enhance each company’s finance offering. Insur-ance is required for all financed or leased purchases ofagricultural equipment. “Agricredit Acceptance andAGCO Finance needed a partner that could integratethe insurance offering into the finance quote process ina seamless manner,” noted Pat Stoik, Vice President andGlobal Commercial InlandMarine Manager for Chubb.“We met their criteria.”

Chubb provides property insurance protection forinstallment sales and leasing deals for agricultural equip-ment for Agricredit Acceptance and AGCO Finance

customers. But what really impressed ex-ecutives at the two companies was thedevelopment of a tailored automatedprocess to transfer financial data betweenthe company, its insurance agent,Holmes Murphy & Associates, andChubb.

AGCO Finance Chief ExecutiveOfficer Amy Ventling said, “Chubb’swillingness to listen and understand ourneeds has made this partnership a win forAgricredit Acceptance and AGCO Fi-nance. The transition to Chubb was

easy. Our experience with payment on losses has beenvery impressive, and our dealers and customers are quitesatisfied with our program.”

Chubb Service: Listening to the Customer

Photo at right: Viewing farm equipment at the Iowa PowerFarming Show in Des Moines are Amy Ventling, Chief ExecutiveOfficer, AGCO Finance, LLC, Duluth, Georgia (left), and Dennis J.Fedosa, Chief Executive Officer, Agricredit Acceptance, LLC,Johnston, Iowa.

Photo at left: L. Pat Stoik, Vice President and GlobalCommercial Inland Marine Manager (left) visits Richard Mauk,Vice President and Branch Manager, at Chubb’s Des Moines,Iowa, office.

“Chubb’s willingness to

listen and understand

our needs has made

this partnership a

win for Agricredit

and AGCO.”

2007 AR Text_gac2.26:Layout 1 2/26/08 8:11 PM Page 20

2121

2007 AR Text_gac2.26:Layout 1 2/26/08 8:11 PM Page 21

At Chubb, we understand that our reputation is onlyas good as that of the independent agents and

brokers who sell our products. That’s whyChubb places a high value on agency ed-ucation and offers many opportunitiesfor agents and brokers to advance theireducation in sales, management andleadership.

In 2001, Chubb partnered with theWharton School of the University ofPennsylvania to offer a program to edu-cate insurance agency executives. Thepartnership has grown steadily over theyears, and today the Chubb/WhartonRecognized Insurance Leader Program offers a robust cur-riculum for agents and brokers throughout the year.

The curriculum is geared toward agency executivesand begins with a five-day Executive Leadership

Development Program. Among the many courses offeredare growth through innovation, financial analysis, nego-tiating skills, and mergers and acquisitions.

“This is not about Chubb, and sometimes it’s noteven about insurance,” said Elizabeth McDaid, AgencyEducation Manager for Chubb. “It’s about making agencyleaders more successful as business people.”

Many agency executives return to further their ed-ucation, and they can earn a Chubb/Wharton Certifi-cate of Leadership Development and RecognizedInsurance Leader designation by accumulating pointsthrough participation in the programs over a three-yearperiod.

William Pridgeon, Senior Vice President and ChiefFinancial Officer of Hylant Group in Toledo, Ohio, par-ticipated in the Chubb/Wharton executive program in2003 and completed three-day advanced leadership

training on the Gettysburg battlefield in2004. Pridgeon said the biggest benefitof the five-day introductory training wasthe ability to think strategically insteadof tactically for a week. “I left with a listof things to start doing at work, but alsoa list of things to stop doing,” he said.

Susan Daley, Area President,Arthur J. Gallagher & Co., Aliso Viejo,California, said the training helped herto find her “blind spots” and surroundherself with people who can help make

her more productive. “The Chubb/Wharton program wasthe single most beneficial adult learning experience Ihave ever had.”

22

Chubb Service: Agency Education

Photo at right: Pictured behind a statue of Benjamin Franklinat the University of Pennsylvania in Philadelphia are (from left)William Pridgeon, Senior Vice President and Chief FinancialOfficer of Hylant Group, Toledo, Ohio; Jeffrey Perlman, Partner,Borden Perlman, Lawrenceville, New Jersey; and Susan Daley,Area President, Arthur J. Gallagher & Co., Aliso Viejo, California.

Photo at left: Pictured at the University of Pennsylvania inPhiladelphia are (from left) Sandhya Karpe, Senior Directorof Executive Programs at the Wharton School of the Universityof Pennsylvania; Elizabeth McDaid, Vice President, AgencyEducation Manager, Chubb; and Neil Doherty, Frederick H.Ecker Professor and Chairperson, Insurance and RiskManagement at the Wharton School.

“The Chubb/Wharton

program was

the single most

beneficial adult

learning experience

I have ever had.”

2007 AR Text_gac2.26:Layout 1 2/28/08 4:35 PM Page 22

2323

2007 AR Text_gac2.26:Layout 1 2/26/08 8:12 PM Page 23

Chubb’s success depends on theperformance of each employee. Meetsix leaders whose accomplishmentsillustrate the many individual successesthat have contributed to Chubb’sextraordinary results in 2007.

S tarting her career shortlyafter Chubb de Colombia

first became a wholly ownedChubb subsidiary 18 years ago,Claudia Vargas has contributed toChubb de Colombia’s results fromthe very beginning. She now servesas Vice President and CommercialUnderwriting Manager.

During the last five years,Claudia has helped guide Chubb’sColombian commercial operationsto superior results — an averagecombined ratio of 62% andcumulative premium growth of53%. Her contributions are notlimited to financial results; she hasalso led Chubb de Colombia’sdiversity group since 2003.

“The respect the corporationgives to its employees throughtraining, equal opportunity andrecognition makes us a verycommitted group, oriented to thecompany’s goals,” said Claudia.“This is one of the reasons thatChubb de Colombia has beenvoted ‘The Number One Propertyand Casualty Insurance Companyin Colombia’ by producers for fiveconsecutive years.”

I n his role as Assistant VicePresident and Commercial

Underwriting Manager in Seoul,building the profitability andgrowth of Chubb in Korea isChang Tae Noh’s primary goal.He also forges strategic alliancesto maximize Chubb’s businessopportunities there.

“I’ve worked to developChubb’s marine business in Koreathrough the country’s growth inglobal exports and local marketchange,” said Chang. “UsingChubb’s underwriting expertiseand global capability, we have beenable to introduce product liabilitycoverage to local manufacturersgoing global and technology

insurance to IT-related companiesthat currently make up asubstantial portion of the KoreanGDP.”

In addition to expandingChubb’s ability to provide a diversearray of products in Korea, Chang’smanagement talents have enabledChubb’s commercial operations inKorea to grow at a double-digit ratein 2007 while remaining profitable.

J oining Chubb immediatelyafter graduating from

Western Michigan University, KenStephens has held nine positionsof increasing responsibility duringhis 21-year career at Chubb. Hehas risen to Senior Vice Presidentand Manager of Chubb’s NorthCentral United States specialtybusiness, representing nearly a fifthof Chubb’s specialty businessworldwide.

When Ken began his currentassignment, he was challenged toreturn the region’s specialtybusiness to profitability whileshifting its underwriting focus ina marketplace of intense pricecompetition. Since then, his regionhas surpassed the average annualprofitability of Chubb’s specialtybusiness worldwide with a highcustomer-retention rate.

Ken credits his success tothe many leaders he has workedfor, and he seeks to pass on hisknowledge and experience throughhis leadership of Chubb’s MinorityDevelopment Council.

“I’m proud to work at acompany that is sincere about itscommitment to diversity,” saidKen. “My belief is that the morediverse individuals progress toleadership, the more thecorporation will benefit from adiversity of thought andleadership.”

24

Employee Profiles

2007 AR Text_gac2.26:Layout 1 2/29/08 12:51 PM Page 24

Although new to Chubb,Denise Lewis is no

newcomer to the insuranceindustry. Currently Assistant VicePresident and Human ResourcesManager for Chubb’s Atlanta andBirmingham offices, Denise hasmore than two decades of industry

experience in marketing andoperations.

Since 2005, Denise hashelped create a talent developmentinitiative to increase employeeleadership skills in the southernUnited States. Every year, hertalent management team carefullyselects high-potential employees toreceive leadership education. Aftertraining, these individuals formteams and suggest ideas to developnew products and increaseefficiency.

“This program has enabledparticipants to grow and developdynamic leadership abilities, andtheir suggestions are enhancingChubb’s operations,” said Denise.“I value the opportunity tocontribute to talent developmentand add to Chubb’s intellectualcapital.”

She has also worked toimprove new-hire performanceand retention while supportingthe Atlanta branch’s diversity andcharitable activities.

U sing her skills gleaned fromfour years as a broker and

11 as a personal lines underwriter,Tara Parchment knows how tobalance the needs of brokers withChubb’s continued expensereduction initiatives.

As Assistant Vice Presidentand Producer DevelopmentManager for the United Kingdomand Ireland, Tara recentlyimplemented a broker incentiveprogram, based on the currentmodel in the United States,whereby brokers who bring Chubbmore profitable business receivehigher incentives.

“By grouping our brokersbased on performance, we canmake sure that we’re putting ourlimited resources where we get thebest results,” explained Tara.

The broker incentive programenabled Chubb to both signifi-cantly reduce expenses and show

brokers how to reach the nextperformance level. By training thesales team to deliver a consistentmessage about the financial reasonsfor incentive structure adjustments,Tara also helped to retain all 550 ofthe region’s personal lines brokers— a tremendous accomplishmentconsidering the local soft market,rate increases and competitorincentives.

O ver the last two decades,Senior Vice President and

International Chief InformationOfficer Rick Gray has spent moretime abroad than in his nativeUnited States.

Previously on assignmentin Singapore, Hong Kong andLondon, he cites his internationalexperience as the key to hismanagement success. As theInternational CIO, Rick ensuresthat, wherever possible, the 200employees he manages integrateChubb’s international IToperations very closely with thosein the United States.

“I view Chubb as a companythat thinks globally but oftentimeshas to act locally,” explained Rick.“Although our primary focus iscompany-wide solutions, thingsdo work differently in differentmarketplaces, and we need to beagile enough to adapt.”

In his last position as Europe’sCIO, Rick helped to outsourcesome of Chubb Europe’s policyadministration and financeactivities to the Czech Republicand India. The project is expectedto result in significant annualsavings and enhanced operationalefficiency.

25

2007 AR Text_gac2.26:Layout 1 2/26/08 8:12 PM Page 25

26

Officers

Chairman andChief Executive OfficerJohn D. Finnegan

President andChief Operating OfficerThomas F. Motamed

Executive Vice PresidentsRobert C. CoxJohn J. DegnanJune E. DrewrySunita HolzerPaul J. KrumpAndrew A. McElwee, Jr.Harold L. Morrison, Jr.Michael O’ReillyDino E. RobustoJanice M. Tomlinson

Executive Vice President andGeneral CounselMaureen A. Brundage

Administrative CommitteeW. Brian BarnesMaureen A. BrundageTerrence W. CavanaughRobert C. CoxJohn J. DegnanJune E. DrewryJohn D. FinneganMark E. GreenbergSunita HolzerPaul J. KrumpAndrew A. McElweeHarold L. MorrisonThomas F. MotamedMichael O’ReillyDino E. RobustoHenry B. SchramJanice M. Tomlinson

Senior Vice PresidentsValerie A. AguirreJames E. AltmanJohn C. AndersonJoel D. AronchickWilliam D. ArrighiGregory P. BarabasDonald E. BarbJohn A. BarrettMark L. BerthiaumeJon C. BidwellPeter G. BoccherJulia T. BolandJames P. BronnerDeborah L. BronsonAlan C. BrownR. Jeffery BrownTimothy D. BuckleyGerard M. ButlerJohn F. CasellaMichael J. CasellaTerrence W. CavanaughGardnerR.Cunningham, Jr.Robert F. DaddDavid S. DaltonJames A. DarlingGary R. DelongChristopher N. Di SipioTimothy R. DiveleyKathleen M. DubiaMark D. DugleAlexis R. Durcan, Jr.

Mary M. ElliottKathleen S. EllisTimothy T. EllisMichele N. FincherPhilip W. FiscusThomas V. FitzpatrickPhilip G. FolzPaul W. FranklinAnthony S. GalbanThomas J. GanterMichael GarceauJames E. GardnerJohn C. Gibson, Jr.Christopher J. GilesJohn H. GillespieBaxter W. GrahamJeffrey S. GrangeRick A. GrayMark E. GreenbergDonna M. GriffinCharles S. GunterMarc R. HacheyJames R. HamiltonSteven D. HernandezJeffrey HoffmanKevin G. HoganKim D. HogrefePatricia A. HurleyGerald A. IppolitoHope JarvisDoris M. JohnsonBettina F. KellyJohn J. KennedyJames P. KnightMark P. KorsgaardEric T. KrantzUlli KrellJohn B. KristiansenAndrew N. LaGraveneseJames V. LalorKathleen S. LangnerPaul A. LarsonKevin J. LeidwingerPaul L. LewisRobert A. LippertBeverly J. LuehsAmelia C. LynchMichael J. MaloneyMichael L. MarinaroKathleen P. MarvelRobert A. MarzocchiDavid P. Mc KeonMichelle D. MiddletonRobert P. MidwoodJohn J. MizziEllen J. MooreFrank MorelliLynn S. NevilleFrances D. O’BrienMoses I. OjeisekhobaMichael W. O’MalleyMichael D. OppeRolando A. OramaDaniel A. PaciccoNancy D. Pate-NelsonJane M. PetersonGary C. PetrosinoSteven R. PozziEdward J. RadzinskiBarbara RingChristoph C. RittersonEric M. RiveraJames C. RomanelliEvan J. RosenbergJudith A. Sammarco

Timothy M. ShannahanRichard I. SimonMichael A. SlorKevin G. SmithGail W. SojaRichard P. SojaJody E. SpechtEdward G. SpellScott R. SpencerKurt R. StemmlerKenneth J. StephensJohn M. SwordsTimothy J. SzerlongJoel M. TealerClifton E. ThomasBruce W. ThorneKathleen M. TierneyGary TrustPeter J. TuckerWilliam P. TullyWilliam C. Turnbull, Jr.Michele E. TwymanJeffrey A. UpdykeSusan M. VellaPeter H. Vogt, IICharles J. WalkonisSusan C. WaltermireCarole J. WeberJames L. WestJeremy N.R. Winter

Senior Vice President andChief Accounting OfficerHenry B. Schram

Senior Vice President andChief ActuaryW. Brian Barnes

Senior Vice Presidents andActuariesJames E. BillerLinda M. GrohRobert J. HopperAdrienne B. KaneMichael F. McManusKeith R. Spalding

Senior Vice President andDeputy General CounselJudith A. Heim

Senior Vice Presidents andAssociate General CounselsMatthew CampbellSuzanne JohnsonKirk J. RaslowskyLinda F. Walker

Senior Vice President andTreasurerDouglas A. Nordstrom

Vice PresidentsJames R. AbercrombieJill A. AbereDerek R. AdamsWilliam M. AdamsElizabeth A. AguinagaJames D. AlbertsonBrenda I. AlbiarGeorge N. AllportAngela W. AlperMary S. AquinoMichael Arcuri

Ronald J. ArigoBrendan ArnottDorothy M. BadgerSybil O. BaffoeKirk O. BaileyGregory W. BangsAchiles I. BarbatsoulisDavid A. BarclayFrances M. BarfootCynthia L. BarkmanRichard W. BarnettWilliam E. Barr, Jr.David BaumanJohn L. BayleyArthur J. BeaverWilliam R. Bell, IIIDonna A. BelvedereR. Kerry BesniaDavid H. BissellStanley V. BloomJulie BondOdette M. BonvouloirCharles A. BordaDaniel J. BosoldDennis L. Bostedo, Jr.Jeffrey M. BrownJeff H. BrundrettJohn E. Bryer, IIIJohn A. Burkhart, IIIJames D. ButchartSabine B. CainWalter K. CainRonald CalavanoW. Michael CamfieldJames M. CarsonJohn C. CavanaughMichael A. ChangBarnes L. ChatelainKenneth ChungRichard A. CiulloThomas C. ClansenLaura B. ClarkFrank L. ClaybrooksArthur W. CohenRichard N. ConsoliJudith A. CookRoberta CorbettBrian B. CottoneEdwin E. CreterRaymond L. Crisci, Jr.William S. CrowleyTimothy E. DadikChristine A. DartMichael D. DaughertyMark W. DavisJanet DecostroDavid S. DeetsCarol A. DeFranceMichael C. DeMarcoPhillip C. DemmelSusan Devries AmelangJoanne C. DiamondDebra A. DikenJames S. DobsonRobert J. DonnellyBrian J. DouglasWendy J. DowdAlfred C. DrowneKeith M. DunfordLeslie L. EdsallRichard J. EdsallTimothy G. EhrhartJames P. EkdahlRobert C. Ellis, Jr.Victoria S. Esposito

Heather S. EvansCraig M. FarinaTimothy J. FarrThomas J. FazioDrew A. FeldmanAmy L. FellerKaren E. FeuerhermJeffrey B. FischerJames A. FiskeBrian J. FlynnPeter A. FlynnPatrick G. FoucheJill A. FrancisJohn B. FuossFrederick W. GaertnerEileen L. GallagherTrevor S. GandyWallace W. Gardner, Jr.Donald M. Garvey, Jr.Mark D. GatliffIrene T. GaughanPatrick GerrityNed I. GerstmanRalph GiordanoKaren R. GladdenAaron GoldsteinChristine GomesEugene B. GoodridgeFrank F. GoudsmitAnne S. GouinPerry S. GranofCraig M. GrantJoseph Gresia, Jr.Patricia L. HallNancy Halpin-BirknerRobert A. HamburgerNoel P. HannonRichard W. HaranPatricia F. HarrisPeter J. HarrisonWilliam R. HarrisonGary L. HeardMichael W. HeembrockLynne J. HeidelbachRandolph L. HeinLorraine C. HeinenRaymond HendricksonFrederick P. HessenthalerSteven M. HillPamela D. HoffmanEdward I. HowardMichael S. HoweyThomas B. HowlandJoaquin O. HoyosAnthony IovineRobert A. IskolsMichael E. JacksonSteven JakubowskiMark S. JamesJohn M. JeffreyColleen A. JenningsBradley M. JohnLatrell JohnsonKenneth C. JonesLisa M. JonesJohn J. Juarez, Jr.Celine E. KacmarekArvind KapoorDennis C. KearnsJames R. KebbekusDavid L. KeenanDebra Ann KeiserRobert G. KellyTimothy J. KellyAmy F. Kendall

Thomas R. KerrElsbeth KirkpatrickJeffrey KneeshawCille KochJoseph M. KorkuchDieter W. KorteKathleen W. KoufacosJoseph E. KozlowskiEdgar KroezeRalph La CannaKathleen V. LafeminaAnne La FontaineBarbara J. LangioneTerri L. LathanMary M. LeahyJames W. LenzKelly LewisRobert D. LindbergFrederick W. LobdellMark A. LockeDonna M. LombardiMatthew E. LubinJohn W. LuthringerRobert LynchDavid E. MackMichael G. ManginiLeona E. MantieKeith D. MarksJohn C. MarquesPatricia S. MartzBrian MatesEileen G. MathewsRichard D. MaukAnthony McCullerElizabeth McDaidSandra K. Mc DanielFrances K. Mc GuinnPenny L. McGuireMichelle MclaughlinEdward J. McLoughlin, Jr.Neil W. McPhersonDenise B. MelickRobert MeolaAllison W. MetaScott D. MeyersAnn M. Minzner ConleyJoseph D. MiskellTimothy L. MoehlenpahAndrea M. MollicaGregory E. MonroeTerry D. MontgomeryMichael K. MooneyPaul N. MorrissetteRichard P. MunsonPatrick P. MurphyJeffery A. NeighborsRuth T. NelsonJennifer K. NewsomCatherine J. NikodenDavid B. Norris, Jr.Nancy A. O’DonnellStephen S. OhKelly P. O’LearyThomas P. OlsonJohn A. O’MaraKathleen A. OrenczakJohn S. OsabenMark C. PaccioneCatherine M. PadalinoPeter PalermoMichael PalumboChristopher ParkerLouise T. PatregnaniJoanna B. PerronAudrey L. Petersen

Chubb & Son, a division of Federal Insurance Company

OfficersChairman, President andChief Executive OfficerJohn D. Finnegan

Lead DirectorJoel J. Cohen

Vice Chairman andChief Operating OfficerThomas F. Motamed

Vice Chairman andChief Administrative OfficerJohn J. Degnan

Vice Chairman andChief Financial OfficerMichael O’Reilly

Executive Vice PresidentsNed I. GerstmanMarjorie D. Raines

Executive Vice President andGeneral CounselMaureen A. Brundage

Senior Vice PresidentsDaniel J. ConwayFrederick W. GaertnerPaul R. GeyerMark E. GreenbergAndrew A. McElwee, Jr.Glenn A. MontgomeryHenry B. SchramRobert M. Witkoff

Vice PresidentsStephen A. FullerMarc R. HacheyMarylu KorkuchRobert A. MarzocchiThomas J. Swartz, IIISteven M. Versaggi

Vice President, CorporateCounsel and SecretaryW. Andrew Macan

Vice President and TreasurerDouglas A. Nordstrom

The Chubb Corporation

2007 AR Text_gac2.26:Layout 1 2/28/08 4:42 PM Page 26

00

Officers

Jeffrey PetersonIrene D. PetilloDonaldW. PetrinMichael S. PhillipsMary Beth PittingerRobert J. PriceRamona D. PringleScott F. PringleJennifer L. ProceJames H. ProferesWilliam J. PuleoDanette PurkisDavid L. PychRobert S. RaffertyMarjorie D. RainesRichard D. ReedRichard P. ReedRobert ReedyWalead A. RefaiMichael K. Reicher, IIJames L. RhynerMerrily RiesebeckGary V. Rispoli

Nicholas RizziMark J. RobinsonAnne RoccoEdward F. RochfordBeatriz RodriguezThomas J. RoesselJorge A. RosasJune A. RoseVictoria S. RossettiJeffrey W. RyanRuth M. RyanCarolyn M. SalapaBarbara N. SandelandsFranklin D. Sanders, Jr.Robert F. SantoroEric D. SchallMelissa P. SchefflerAnthony C. SchiavoneRobert F. SchmidMichael A. SchraerRobert D. SchuckRussell J. SchurenMark L. Schussel

Roma K. SeudatMary T. SheridanLeigh A. ShermanKristine A. ShieldsAnthony W. ShineDonald L. Siegrist, Jr.Jason SkrantPatricia S. SmithScott E. SmithT. Clarke Smith, IIIRichard E. SoleauVeronica SomarribaVictor J. SordilloPeter D. SpicerMario A. StassiBrian J. SteeleVictor C. StewmanLloyd J. StoikMichael C. StrakhovBeth A. StrappDorit D. StrausRobert K. StreeterJacquelyn C. Strobel

Patrick F. SullivanScott B. TellerJames S. ThieringerJonathan ThomasCharles E. ThompsonEric W. ThompsonPeter J. ThompsonJohn J. TomaineDionysia G. ToregasRichard E. TowleJoel S. TownsendJ. Tracy TuckerJohn T. TuckerRoy C. Tyson, IIIRichard L. UghettaPaula C. UmreikoLouise E. ValleeNivaldo VenturiniBennett C. VernieroTracey A. VispoliJohn T. VolanskiRichard VreelandKevin M. Waldron

Christine WartellaWalter B. WashingtonMaureen B. WaterburyRyan L. WatsonGregory WellsJanece E. WhitePatricia S. WhitehouseDavid B. WilliamsGrenes Eugene WilliamsOwen E. WilliamsThomas R. Wing, Jr.Suzanne L. WittBarbara A. WittickBert Wolff, Jr.Archyne S. WoodardGary C. WoodringSteven YacikJack S. ZachariasJohn J. ZanzalariStephen J. ZappasAnn H. ZapraznyCynthia ZegelDominick Zenzola

Vice President and SecretaryW. Andrew Macan

Vice Presidents andActuariesPeter V. BurchettJoseph E. FreedmanHye-Sook KangKevin A. KesbyShu C. LinKraig P. Peterson

Vice President andCoverage CounselLouis Nagy

Vice Presidents andAssociate CounselsGail ArkinJames W. GunsonJames Sharkey

Chubb & Son, a division of Federal Insurance Company (continued)

Officers

Chief Executive OfficerJohn D. Finnegan

Chairman, President andChief Operating OfficerThomas F. Motamed

Senior Vice President andChief Administrative OfficerJohn J. Degnan

Senior Vice President andChief Financial OfficerMichael O’Reilly

Senior Vice President andGeneral CounselMaureen A. Brundage

Senior Vice PresidentsBrendon R. AllanStephen BlasinaStanley V. BloomPaul ChapmanMichael CollinsIan CookAndre DallaireChristopher J. GilesChristopher HamiltonMark T. LingafelterFrederick W. LobdellKevin O’ShielGary C. PetrosinoDoreen Yip

Vice PresidentsJames E. AltmanPaul BaldacchinoKemsley BrennanRoger C.P. BrookhouseJ. Airton CarvalhoMichael J. CasellaTerrence W. CavanaughJackie ChangBay Hon ChinWilliam C. ClarksonAnn Maree CookStephen De GruchyMario DelrossoGregory D. DoddsJonathan Doherty

Matthew T. DoquileFrederick W. GaertnerShasi GangadharanNed I. GerstmanPaul R. GeyerAndrew R. GourleyBaxter W. GrahamRick A. GrayJason HowardMichael S. HoweyGeorge X.Z. HuangKaren A. HumphreysJames E. KernsHelen KoustasChristopher R. LeesIrene LiangAmelia C. Lynch

Robert A. MarzocchiDermot McComiskeyDavid P. Mc KeonMark B. MitchellGlenn A. MontgomeryDavid B. Norris, Jr.Rolando A. OramaSteven J. OrdEmma OsborneMatthew PasterfieldMarjorie D. RainesJorge A. RosasFrancis RowAndrew RussellLeo A. SchmidtHenry B. SchramJohn X. Stabelos

Jik C. TayJanice M. TomlinsonStephen P. WarrenKyle WilliamsRobert M. WitkoffEsther WongKiyoshi Yamamoto

Vice President and ActuaryW. Brian Barnes

Vice President and SecretaryW. Andrew Macan

Vice President and TreasurerDouglas A. Nordstrom

Federal Insurance Company

Officers

ChairmanJanice M. Tomlinson

President andChief Executive OfficerEllen J. Moore

Senior Vice President andChief Financial OfficerGeoffrey D. Shields

Senior Vice President,General Counsel andSecretaryJohn F. Cairns

Senior Vice PresidentsJean BertrandNicole BrouillardGiovanni DamianoPaul N. MorrissetteJames V. Newman

Andrew SteenSusanWattsDavid B. Williams

Vice PresidentsBarry BlackburnLeeAnn Boyd

Dale ChowPatricia EwenPaul JohnstoneGale LewisMary MaloneyJeffrey MaritChristina Mcavella

Robert MurrayMichel Rousseau

Vice President andActuaryPhilip Jeffery

Chubb Insurance Company of Canada

Officers

President andChief Executive OfficerChristopher J. Giles

Senior Vice PresidentsPaul ChapmanGardnerR.Cunningham, Jr.Thierry DaucourtJohannes EttenCarolyn HamiltonAndrew McKeeCarlos MerinoMoses I. Ojeisekhoba

Jalil RehmanFred ShurbajiBernardus VanDer VossenPaul R. Van PeltSimonWood

Senior Vice President andChief Financial OfficerKevin O’Shiel

Senior Vice President andActuaryColin Crouch

Vice President, GeneralCounsel and SecretaryRanald T. I. Munro

Vice PresidentsDavid AdamsJan AuerbachRon BakkerHubert BelangerThierry BourguignonBernhard BuddeRobert CageDavid CasementFiona CoxBijan Daftari

Guillaume DealMark EdmondsonHalcyon EllisRichard EveleighAndrew FrancisDavid GibbsMarta Gomez-LlorenteBrian HardwickErik HasselSimon HayterIsabelle HilaireMonique KooijmanNeil Lee-AmiesPhilippe Leostic

Andreas LuberichsDaniel MaurerJeremy MilesSimon MobeyMiguel MolinaTom NewarkRene NieuwlandStuart PayneBjorn PetersenHugh PollingtonJonathan PooleJohn RoomeFeliciano RuizVittorio Scala

Henrik SchwieningCovington ShacklefordAlan SheilVeronica SomarribaChris TaitPeter ThomasMichael ThyssenLynn TwinnMonique Van Der LindenSophie Van T’il LeedhamBrian VoslohBerndWiemannNigel WilliamsMiles Wright

Chubb Insurance Company of Europe, S.A.

27

2007 AR Text_gac2.26:Layout 1 2/28/08 4:43 PM Page 27

28

Directors

Zoë BairdPresidentThe Markle Foundation

Sheila P. BurkeResearch FacultyJ.F. Kennedy School ofGovernment,Harvard University

James I. Cash, Ph.D.Professor EmeritusHarvard Business School

Joel J. CohenLead DirectorThe Chubb CorporationChairman andCo-Chief Executive OfficerSagent Advisors Inc.

John D. FinneganChairman, President andChief Executive OfficerThe Chubb Corporation

Dr. Klaus J. MangoldFormer Member of the BoardDaimler AG

Martin G. McGuinnRetired Chairman andChief Executive OfficerMellon Financial Corp.

Sir David G. Scholey, CBESenior AdvisorUBS Investment Bank

Lawrence M. SmallFormer SecretarySmithsonian Institution

Jess SØderbergRetired Partner andGroup CEOA.P. Moller-Maersk

Daniel E. SomersRetired Vice ChairmanBlaylock and Partners LP

Karen Hastie WilliamsRetired PartnerCrowell & Moring LLP

Alfred W. ZollarGeneral ManagerTivoli SoftwareIBM Corporation

The Chubb Corporation

Committees of the Board

Audit CommitteeJoel J. Cohen (Chair)Zoë BairdMartin G. McGuinnDaniel E. SomersAlfred W. Zollar

Organization & Compensation CommitteeDaniel E. Somers (Chair)Sheila P. BurkeMartin G. McGuinnKaren Hastie WilliamsAlfred W. Zollar

Executive CommitteeJohn D. Finnegan (Chair)James I. Cash, Ph.D.Joel J. CohenDaniel E. Somers

Finance CommitteeJohn D. Finnegan (Chair)Sheila P. BurkeDr. Klaus J. MangoldSir David G. Scholey, CBEJess SØderberg

Corporate Governance & Nominating CommitteeJames I. Cash, Ph.D. (Chair)Zoë BairdJoel J. CohenLawrence M. SmallKaren Hastie Williams

Pension & Profit Sharing CommitteeSheila P. BurkeDr. Klaus J. MangoldSir David G. Scholey, CBEJess SØderberg

2007 AR Text_gac2.26:Layout 1 2/29/08 2:05 PM Page 28

UNITED STATES SECURITIES AND EXCHANGE COMMISSIONWashington, D. C. 20549

FORM 10-K≤ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2007

OR

n TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIESEXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO

Commission File No. 1-8661

The Chubb Corporation(Exact name of registrant as speciÑed in its charter)

New Jersey 13-2595722(State or other jurisdiction of incorporation or organization) (I.R.S. Employer IdentiÑcation No.)

15 Mountain View RoadWarren, New Jersey 07059

(Address of principal executive oÇces) (Zip Code)

(908) 903-2000(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

(Title of each class) (Name of each exchange on which registered)

Common Stock, par value $1 per share New York Stock ExchangeSeries B Participating Cumulative New York Stock ExchangePreferred Stock Purchase Rights

Securities registered pursuant to Section 12(g) of the Act:

None(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as deÑned in Rule 405 ofthe Securities Act. Yes ®„© No ® ©

Indicate by check mark if the registrant is not required to Ñle reports pursuant to Section 13 orSection 15(d) of the Exchange Act. Yes ® © No ®„©

Indicate by check mark whether the registrant (1) has Ñled all reports required to be Ñled bySection 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or forsuch shorter period that the registrant was required to Ñle such reports), and (2) has been subject tosuch Ñling requirements for the past 90 days. Yes ®„© No ® ©

Indicate by check mark if disclosure of delinquent Ñlers pursuant to Item 405 of Regulation S-K isnot contained herein, and will not be contained, to the best of the registrant's knowledge, in deÑnitiveproxy or information statements incorporated by reference in Part III of this Form 10-K or anyamendment to this Form 10-K. ® ©

Indicate by check mark whether the registrant is a large accelerated Ñler, an accelerated Ñler, anon-accelerated Ñler, or a smaller reporting company. See the deÑnitions of ""large accelerated Ñler,''""accelerated Ñler'' and ""smaller reporting company'' in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated Ñler ®„© Accelerated Ñler ® ©

Non-accelerated Ñler ® © Smaller reporting company ® ©(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as deÑned in Rule 12b-2 of theExchange Act). Yes ® © No ®„©

The aggregate market value of common stock held by non-aÇliates of the registrant was$21,242,705,472 as of June 30, 2007, computed on the basis of the closing sale price of the commonstock on that date.

370,249,648Number of shares of common stock outstanding as of February 15, 2008

Documents Incorporated by Reference

Portions of the deÑnitive Proxy Statement for the 2008 Annual Meeting of Shareholders areincorporated by reference in Part III of this Form 10-K.

CONTENTS

ITEM DESCRIPTION PAGE

PART I 1 Business 3

1A Risk Factors 12

1B Unresolved StaÅ Comments 17

2 Properties 17

3 Legal Proceedings 17

4 Submission of Matters to a Vote of Security Holders 19

PART II 5 Market for the Registrant's Common Stock andRelated Stockholder Matters 20

6 Selected Financial Data 22

7 Management's Discussion and Analysis of Financial Conditionand Results of Operations 23

7A Quantitative and Qualitative Disclosures About Market Risk 61

8 Consolidated Financial Statements and Supplementary Data 64

9 Changes in and Disagreements with Accountantson Accounting and Financial Disclosure 64

9A Controls and Procedures 64

9B Other Information 65

PART III 10 Directors and Executive OÇcers of the Registrant 67

11 Executive Compensation 67

12 Security Ownership of Certain BeneÑcial Owners and Managementand Related Stockholder Matters 67

13 Certain Relationships and Related Transactions 67

14 Principal Accountant Fees and Services 67

PART IV 15 Exhibits, Financial Statements and Schedules 67

Signatures 68

Index to Financial Statements and Financial Statement Schedules F-1

Exhibits Index E-1

2

PART I.

Item 1. Business

General

The Chubb Corporation (Chubb) was incorporated as a business corporation under the laws ofthe State of New Jersey in June 1967. Chubb and its subsidiaries are referred to collectively as theCorporation. Chubb is a holding company for a family of property and casualty insurance companiesknown informally as the Chubb Group of Insurance Companies (the P&C Group). Since 1882, theP&C Group has provided property and casualty insurance to businesses and individuals around theworld. According to A.M. Best, the P&C Group is the 11th largest U.S. property and casualty insurancegroup based on 2006 net written premiums.

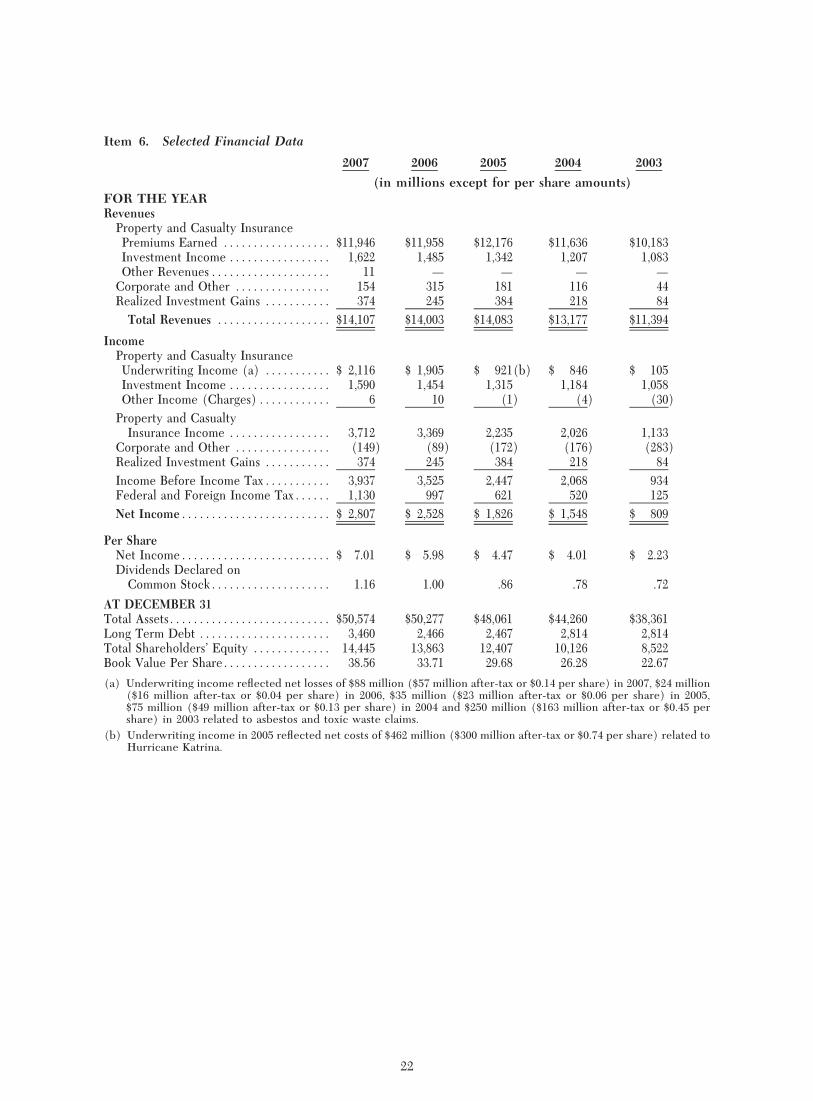

At December 31, 2007, the Corporation had total assets of $51 billion and shareholders' equity of$14 billion. Revenues, income before income tax and assets for each operating segment for the threeyears ended December 31, 2007 are included in Note (12) of the Notes to Consolidated FinancialStatements. The Corporation employed approximately 10,600 persons worldwide on December 31, 2007.

The Corporation's principal executive oÇces are located at 15 Mountain View Road, Warren, NewJersey 07059, and our telephone number is (908) 903-2000.

The Corporation's internet address is www.chubb.com. The Corporation's annual report onForm 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to thosereports Ñled or furnished pursuant to Section 13(a)of the Securities Exchange Act of 1934 are availablefree of charge on this website as soon as reasonably practicable after they have been electronicallyÑled with or furnished to the Securities and Exchange Commission. Chubb's Corporate GovernanceGuidelines, charters of certain key committees of its Board of Directors, Restated CertiÑcate ofIncorporation, By-Laws, Code of Business Conduct and Code of Ethics for CEO and Senior FinancialOÇcers are also available on the Corporation's website or by writing to the Corporation's CorporateSecretary.

Property and Casualty Insurance

The P&C Group is divided into three strategic business units. Chubb Commercial Insurance oÅersa full range of commercial insurance products, including coverage for multiple peril, casualty, workers'compensation and property and marine. Chubb Commercial Insurance is known for writing nichebusiness, where our expertise can add value for our agents, brokers and policyholders. Chubb SpecialtyInsurance oÅers a wide variety of specialized professional liability products for privately and publiclyowned companies, Ñnancial institutions, professional Ñrms and healthcare organizations. ChubbSpecialty Insurance also includes our surety business. Chubb Personal Insurance oÅers products forindividuals with Ñne homes and possessions who require more coverage choices and higher limits thanstandard insurance policies.

In December 2005, the Corporation transferred its ongoing reinsurance assumed business toHarbor Point Limited. For a transition period of about two years, Harbor Point underwrote speciÑcreinsurance business on the P&C Group's behalf. The P&C Group retained a portion of this businessand ceded the balance to Harbor Point.

The P&C Group provides insurance coverages principally in the United States, Canada, Europe,Australia, and parts of Latin America and Asia. Revenues of the P&C Group by geographic area for thethree years ended December 31, 2007 are included in Note (12) of the Notes to Consolidated FinancialStatements.

The principal members of the P&C Group are Federal Insurance Company (Federal), PaciÑcIndemnity Company (PaciÑc Indemnity), Vigilant Insurance Company (Vigilant), Great NorthernInsurance Company (Great Northern), Chubb Custom Insurance Company (Chubb Custom), ChubbNational Insurance Company (Chubb National), Chubb Indemnity Insurance Company (ChubbIndemnity), Chubb Insurance Company of New Jersey (Chubb New Jersey), Texas PaciÑc Indemnity

3

Company, Northwestern PaciÑc Indemnity Company, Executive Risk Indemnity Inc. (Executive RiskIndemnity) and Executive Risk Specialty Insurance Company (Executive Risk Specialty) in the UnitedStates, as well as Chubb Atlantic Indemnity Ltd. (a Bermuda company), Chubb Insurance Company ofCanada, Chubb Insurance Company of Europe, S.A., Chubb Insurance Company of Australia Limited,Chubb Argentina de Seguros, S.A. and Chubb do Brasil Companhia de Seguros.

Federal is the manager of Vigilant, PaciÑc Indemnity, Great Northern, Chubb National, ChubbIndemnity, Chubb New Jersey, Executive Risk Indemnity and Executive Risk Specialty. Federal alsoprovides certain services to other members of the P&C Group. Acting subject to the supervision andcontrol of the boards of directors of the members of the P&C Group, Federal provides day to dayexecutive management and operating personnel and makes available the economy and Öexibilityinherent in the common operation of a group of insurance companies.

Premiums Written

A summary of the P&C Group's premiums written during the past three years is shown in thefollowing table:

Direct Reinsurance Reinsurance NetPremiums Premiums Premiums Premiums

Year Written Assumed(a) Ceded(a) Written

(in millions)

2005ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ $12,180 $1,120 $1,017 $12,2832006ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 12,224 954 1,204 11,9742007ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 12,432 775 1,335 11,872

(a) Intercompany items eliminated.

The net premiums written during the last three years for major classes of the P&C Group'sbusiness are included in the Property and Casualty Insurance Ì Underwriting Results section ofManagement's Discussion and Analysis of Financial Condition and Results of Operations (MD&A).

One or more members of the P&C Group are licensed and transact business in each of the50 states of the United States, the District of Columbia, Puerto Rico, the Virgin Islands, Canada,Europe, Australia, and parts of Latin America and Asia. In 2007, approximately 78% of theP&C Group's direct business was produced in the United States, where the P&C Group's businessesenjoy broad geographic distribution with a particularly strong market presence in the Northeast. TheÑve states accounting for the largest amounts of direct premiums written were New York with 12%,California with 9%, Texas with 5%, New Jersey with 5% and Florida with 5%. No other state accountedfor 5% of such premiums. Approximately 11% of the P&C Group's direct premiums written wasproduced in Europe and 5% was produced in Canada.

Underwriting Results

A frequently used industry measurement of property and casualty insurance underwriting resultsis the combined loss and expense ratio. The P&C Group uses the combined loss and expense ratiocalculated in accordance with statutory accounting principles applicable to property and casualtyinsurance companies. This ratio is the sum of the ratio of losses and loss expenses to premiums earned(loss ratio) plus the ratio of statutory underwriting expenses to premiums written (expense ratio) afterreducing both premium amounts by dividends to policyholders. When the combined ratio is under100%, underwriting results are generally considered proÑtable; when the combined ratio is over 100%,underwriting results are generally considered unproÑtable. Investment income is not reÖected in thecombined ratio. The proÑtability of property and casualty insurance companies depends on the resultsof both underwriting and investments operations.

4

The combined loss and expense ratios during the last three years in total and for the major classesof the P&C Group's business are included in the Property and Casualty Insurance Ì UnderwritingOperations section of MD&A.

Another frequently used measurement in the property and casualty insurance industry is the ratioof statutory net premiums written to policyholders' surplus. At December 31, 2007 and 2006, the ratiofor the P&C Group was .91 and 1.05, respectively.

Producing and Servicing of Business

The P&C Group does not utilize a significant in-house distribution model for its products. Instead,in the United States, the P&C Group offers products through approximately 5,000 independent insuranceagencies and accepts business on a regular basis from approximately 500 insurance brokers. In mostinstances, these agencies and brokers also offer products of other companies that compete with theP&C Group. The P&C Group's branch and service offices assist these agencies and brokers in producingand servicing the P&C Group's business. In addition to the administrative offices in Warren andWhitehouse Station, New Jersey, the P&C Group has zone, branch and service offices throughout theUnited States.

The P&C Group offers products through approximately 3,000 insurance brokers outside the UnitedStates. Local branch offices of the P&C Group assist the brokers in producing and servicing the business.In conducting its foreign business, the P&C Group mitigates the risks relating to currency fluctuations bygenerally maintaining investments in those foreign currencies in which the P&C Group has loss reservesand other liabilities. The net asset or liability exposure to the various foreign currencies is regularlyreviewed.

Business for the P&C Group is also produced through participation in certain underwriting poolsand syndicates. Such pools and syndicates provide underwriting capacity for risks which an individualinsurer cannot prudently underwrite because of the magnitude of the risk assumed or which can be moreeffectively handled by one organization due to the need for specialized loss control and other services.

Reinsurance Ceded

In accordance with the normal practice of the insurance industry, the P&C Group cedes reinsur-ance to other insurance companies. Reinsurance is ceded to provide greater diversification of risk and tolimit the P&C Group's maximum net loss arising from large risks or from catastrophic events.