CHORASA NHAMO R105938P

135

AN EVALUATION OF THE INTERNAL CONTROL SYSTEMS AT ZIMBABWE ELECTRICITY TRANSMISSION AND DISTRIBUTION COMPANY (ZETDC) ON SERVICE DELIVERY (2009 – 2012) By Nhamo Chorasa Registration Number R105938P Dissertation submitted in partial fulfilment for the degree of Master of Administration Graduate School of Management University of Zimbabwe Supervisor : Dr N. KASEKE July 2012

Transcript of CHORASA NHAMO R105938P

AN EVALUATION OF THE INTERNAL CONTROL SYSTEMS AT ZI MBABWE

ELECTRICITY TRANSMISSION AND DISTRIBUTION COMPANY ( ZETDC) ON

SERVICE DELIVERY (2009 – 2012)

By Nhamo Chorasa

Registration Number R105938P

Dissertation submitted in partial fulfilment for t he degree of

Master of Administration

Graduate School of Management

University of Zimbabwe

Supervisor : Dr N. KASEKE

July 2012

i

DECLARATION

I Nhamo Chorasa, do hereby declare that this dissertation is the result of my own

investigation and research, except to the extent indicated in the

acknowledgements, references and by comments included in the body of the

report, and that it has not been submitted in part or in full for any other degree to

any other University.

……………………………………………… ……………………………

SIGNATURE DATE

SUPERVISOR

SIGNATURE………………………………… DATE………………………..

i

DEDICATION

To my wife Chipo, and our children, Joshua, Junior and Jonathan, you were a pillar

of support and a beacon of love and may the love of God always be with you Amen.

ii

ACKNOWLEDGEMENTS

The researcher extends gratitude to the following people for making this study

possible:

Dr N. Kaseke my supervisor, for providing the guidance, wisdom and

encouragement.

Mr O. Dondo and Mr T. Mushangwe, my workmates at ZESA Holdings for the

support, understanding, and for the fruitful discussions and idea sharing.

Mrs F Musimbo for editing and other support service.

Members of Hope Community Church, for the spiritual and moral support including

prayer and supplications.

iii

ABSTRACT

The aim of this study is to evaluate the internal control system in ZETDC (Zimbabwe

Electricity Transmission and Distribution Company) on service delivery with regards

to the period 2009 to 2012. This is the period when Zimbabwe, as a country

commenced using the US dollar and other foreign currencies after experiencing

several years of devastation by a record inflation, on the local Zimbabwean currency.

Most services were expected to improve with the stability in the economy. ZETDC is

a subsidiary of ZESA Holdings (Zimbabwe Electricity Supply Authority), the electricity

utility service provider in Zimbabwe.

The COSO framework on internal controls as noted by Chambers and Rand (2011)

articulates that internal controls should provide reasonable assurance regarding the

achievements of objectives on the effectiveness and efficiency of operations, the

reliability of financial reporting and compliance with applicable laws and regulations.

Authors such as Hopkin (2012), Warren (2012) and Graham (2010) in supporting

the COSO framework, notes that there are five elements of internal controls that

form an umbrella over the business to protect it from control threats and these

include, the control environment, risk assessment , control procedures, monitoring

and information communication. A good internal control system should have three

forms of controls as noted by Hall (2010), which include preventative, detective and

corrective controls. As noted by Harrer (2010), strong controls put up roadblocks for

fraud, bad decisions, human error and help to minimise pitfalls and surprises. On the

other hand, poor internal controls were noted to negatively affect service delivery

and Braiota, Gazzaway, Colson, Colson and Ramamoorti (2010) believe that an

organisation cannot produce reliable services or products without good internal

controls. Obtaining sufficient resources, recruiting and retaining the right expertise

and maintaining good communications and relations are some of the challenges in

implementing effective internal controls highlighted by Hightower (2008).

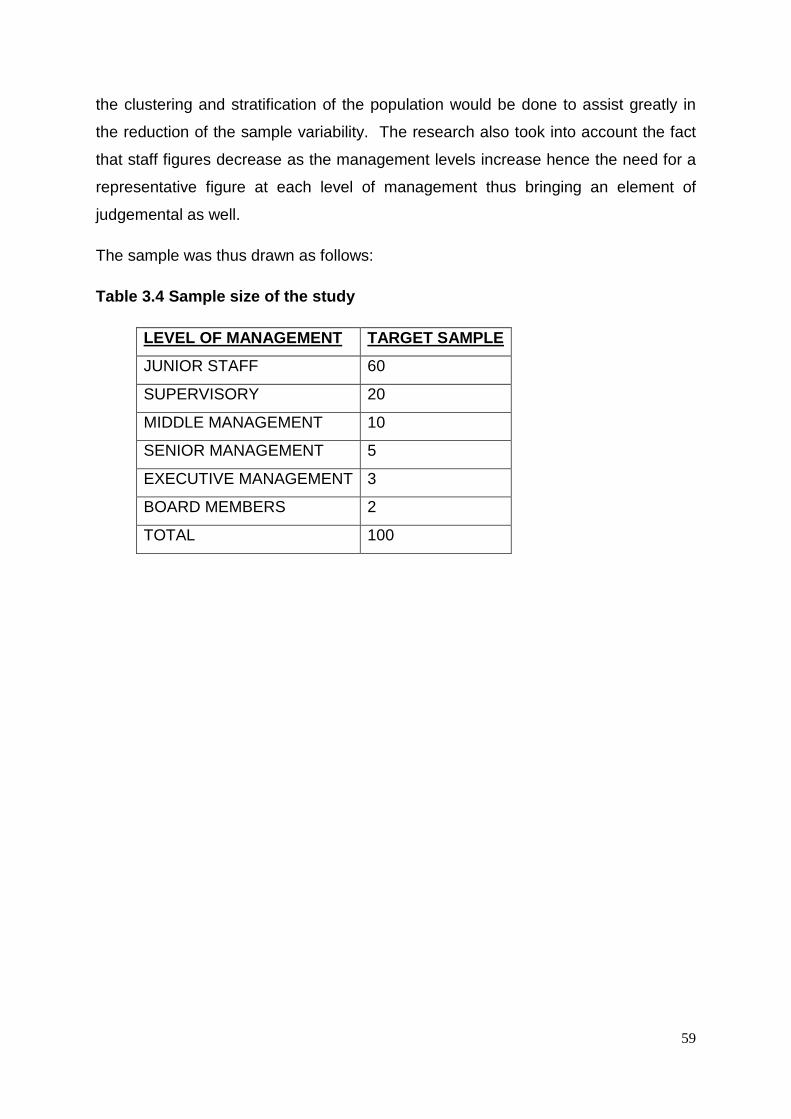

The target population for the study consist of ZETDC staff members estimated at

5,000 inclusive of board members.

A sample of 100 staff members was selected using multistage random sampling to

ensure a fair representation of all hierarchical levels of staff in ZETDC on the

iv

sample. Data was collected through a survey questionnaire which was distributed to

staff members in ZETDC including board members. A 55% response rate was

obtained from the distributed questionnaires.

The major findings were that ZETDC has an internal control system that is company

devised with some elements of a good internal control system, which however are

not modelled along any known frameworks. The internal control system was found to

be regularly breached as evidenced by common activities such as assets abuse,

electricity bill adjustments and illegal power connections. These internal control

breaches negatively affected service delivery in that service provision in many

instances was sub standard, was not done, was delayed and cost more. ZETDC

faced staff resistance as a major challenge in implementing internal control systems,

furthermore, it lacked the strategy to implement internal control systems.

The research concluded that ZETDC had an ineffective internal control system that

resulted in poor service delivery.

It is recommended that ZETDC should adopt the COSO framework on internal

controls to enhance its internal control system.

v

Table of Contents

DECLARATION ..................................................................................................................................... i

DEDICATION ......................................................................................................................................... i

ACKNOWLEDGEMENTS ................................................................................................................... ii

ABSTRACT .......................................................................................................................................... iii

LIST OF TABLES .............................................................................................................................. viii

LIST OF FIGURES .............................................................................................................................. ix

ABBREVIATIONS ................................................................................................................................ x

CHAPTER 1 .......................................................................................................................................... 1

INTRODUCTION AND BACKGROUND TO THE STUDY ............................................................ 1

1.INTRODUCTION ............................................................................................................................... 1

1.1 BACKGROUND OF THE STUDY ............................................................................. 2

1.1.1 OVERVIEW ......................................................................................................................... 2

1.1.2 BACKGROUND TO THE COMPANY - ZETDC ...................................................... 5

1.1.3 STRATEGIC PLANNING .......................................................................................... 11

1.1.4 THE CONTROL ENVIRONMENT ........................................................................... 13

1.1.5 FINANCIAL PERFOMANCE .................................................................................... 15

1.1.6 SWOT ANALYSIS ...................................................................................................... 16

1.1.7 PEST ANALYSIS........................................................................................................ 18

1.1.8 ZETDC’S INTERNAL CONTROL DEFICIENCIES ............................................... 20

1.2 PROBLEM STATEMENT .............................................................................................. 22

1.3 RESEARCH OBJECTIVES .......................................................................................... 22

1.4. RESEARCH QUESTIONS ............................................................................................ 23

1.5 RESEARCH PROPOSITION ........................................................................................ 23

1.6 SIGNIFICANCE OF THE STUDY ................................................................................ 23

1.7 SCOPE OF RESEARCH AREA ................................................................................... 24

1.8 DISSERTATION OUTLINE ........................................................................................... 24

1.9 CHAPTER SUMMARY .................................................................................................. 25

CHAPTER 2 ........................................................................................................................................ 26

LITERATURE REVIEW ..................................................................................................................... 26

2.1 INTRODUCTION ............................................................................................................ 26

2.2 INTERNAL CONTROL SYSTEM ................................................................................. 26

2.3 FORMS OF INTERNAL CONTROL SYSTEMS ........................................................ 31

vi

2.4 FRAMEWORK FOR EVALUATING INTERNAL CONTROLS ................................ 35

2.5 THE IMPORTANCE OF INTERNAL CONTROL SYSTEMS ................................... 38

2.6 FACTORS INFLUENCING INTERNAL CONTROL SYSTEMS .............................. 40

2.7 SERVICE DELIVERY .................................................................................................... 42

2.8 EFFECTIVE INTERNAL COTROL SYSTEMS AND SERVICE DELIVERY ......... 46

2.9 CHALLENGES IN IMPLEMENTING INTERNAL CONTROL SYSTEMS .............. 47

2.11 CONCEPTUAL FRAMEWORK .................................................................................... 50

2.10 CHAPTER SUMMARY .................................................................................................. 50

CHAPTER 3 ........................................................................................................................................ 51

RESEARCH METHODOLOGY ........................................................................................................ 51

3.1 INTRODUCTION ............................................................................................................ 51

3.2 RESEARCH DESIGN .................................................................................................... 51

3.3 RESEARCH PHILOSOPHY ......................................................................................... 52

3.4 POPULATION AND SAMPLING TECHNIQUES ...................................................... 53

3.5 RESEARCH APPROACH ............................................................................................. 60

3.6 RESEARCH METHODS ............................................................................................... 60

3.7 DATA COLLECTION METHODS .............................................................................. 61

3.8 DATA ANALYSIS AND PRESENTATION .................................................................. 66

3.9 ETHICAL CONSIDERATIONS ..................................................................................... 66

3.10 RESEARCH LIMITATIONS .......................................................................................... 66

3.11 CHAPTER SUMMARY .................................................................................................. 67

CHAPTER 4 ........................................................................................................................................ 68

FINDINGS AND DISCUSSION ........................................................................................................ 68

4.0 INTRODUCTION ............................................................................................................ 68

4.1 RESPONSE RATE ......................................................................................................... 68

4.2 DEMOGRAPHIC RESPONSE ..................................................................................... 69

4.3 ELEMENTS OF THE INTERNAL CONTROL SYSTEM .......................................... 71

4.4 STATE OF THE INTERNAL CONTROL SYSTEM ................................................... 75

4.5 IMPACT ON SERVICE DELIVERY ............................................................................. 84

4.6 INTERNAL CONTROL IMPLEMENTATION CHALLENGES .................................. 87

CHAPTER SUMMARY .............................................................................................................. 90

CHAPTER 5 ........................................................................................................................................ 91

CONLUSION AND RECOMMENDATIONS ................................................................................... 91

5.0 INTRODUCTION ............................................................................................................ 91

vii

5.1 CONCLUSION ................................................................................................................ 91

5.1.1 STATE OF INTERNAL CONTROL SYSTEM IN ZETDC ..................................... 91

5.1.2 INTERNAL CONTROL BREACHES ....................................................................... 92

5.1.2 IMPACT ON SERVICE DELIVERY ......................................................................... 92

5.1.3 INTERNAL CONTROL IMPLEMENTATION CHALLENGES .............................. 92

5.2 TEST OF THE STUDY PROPOSITION ................................................................. 92

5.3 RECOMMENDATIONS ............................................................................................. 93

5.3.1 INTERNAL CONTROL FRAMEWORK .................................................................. 93

5.3.2 ORGANISATIONAL STRUCTURE ......................................................................... 93

5.3.3 INTERNAL CONTROL CHALLENGES .................................................................. 93

5.4 AREA OF FURTHER STUDY .................................................................................. 93

REFERENCES ........................................................................................................................... 94

APPENDIX 1.1.1A HARARE SUMMER LOAD SHEDDING TIME TABLE .................. 106

APPENDIX 1.1.1B HARARE WINTER LOAD SHEDDING TIME TABLE .................... 107

APPENDIX 1.1.1C SCHEDULE OF SURBURB CODES IN HARARE REGION........ 108

APPENDIX 1.1.2A ELECTRICITY TARIFFS EFFECTIVE FEBRUARY 2009 ............ 109

APPENDIX 1.1.2B ELECTRICITY TARIFFS EFFECTIVE JUNE 2010 ........................ 110

APPENDIX 1.1.2C ELECTRICITY TARIFFS EFFECTIVE SEPTEMBER 2011 ......... 111

APPENDIX 1.1.4A ZETDC STATEMENT OF FINANCIAL POSITION 2011 .............. 112

APPENDIX 1.1.4B ZETDC COMPREHENSIVE INCOME STATEMENT 2011 .......... 113

APPENDIX 1.1.4C ZETDC STATEMENT OF CASH FLOWS 2011 ............................ 114

APPENDIX 1.1.4D ZETDC RATIO ANALYSIS 2011 ...................................................... 115

APPENDIX 4.1 RESEARCH QUESTIONAIRE ................................................................ 116

viii

LIST OF TABLES

Table 1.1 Tipp Off reports for ZETDC

Table 1.2 Power Generation Statistics

Table 1.3 Power Imports Statistics

Table 1.4 ZETDC Application Systems

Table 2.1 Definitions of Internal Control

Table 2.2 Preventative and Detective Procedures

Table 3.1 Sample Size of the Study

Table 4.1 Response Summary

Table 4.3 Response on Integrity and Ethical values

ix

LIST OF FIGURES

Figure 1.1.1 Harare Region Service Evaluation

Figure 1.1.2 Tip-off Reports for ZETDC

Figure 2.3.1 Preventative, Detective and Corrective Controls

Figure 2.4.1 The COSO Internal Control Cube

Figure 4.2.1 Response by years of experience

Figure 4.2.2 Response by level of education

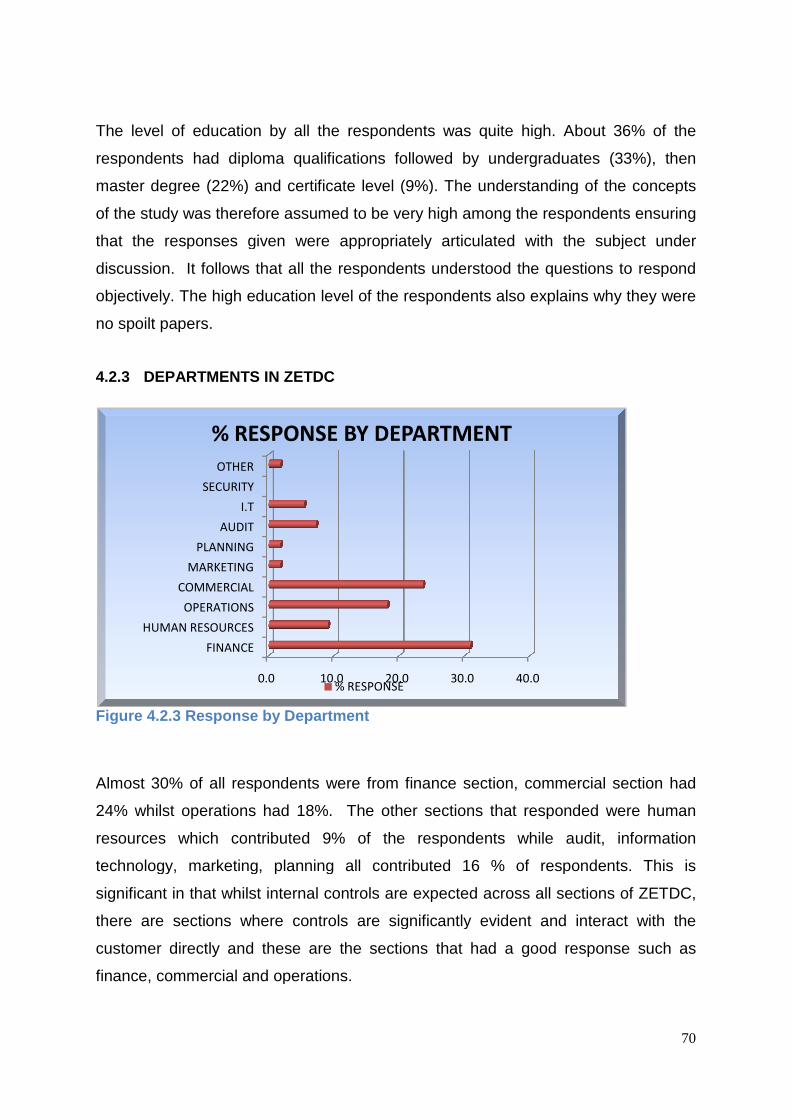

Figure 4.2.3 Response by department

Figure 4.3.2 Management philosophy

Figure 4.3.3 Response on organisational structure

Figure 4.4.1 Percentage response on type of controls

Figure 4.4.2 Response on internal control frameworks

Figure 4.4.3 Yes responses to internal control reviews

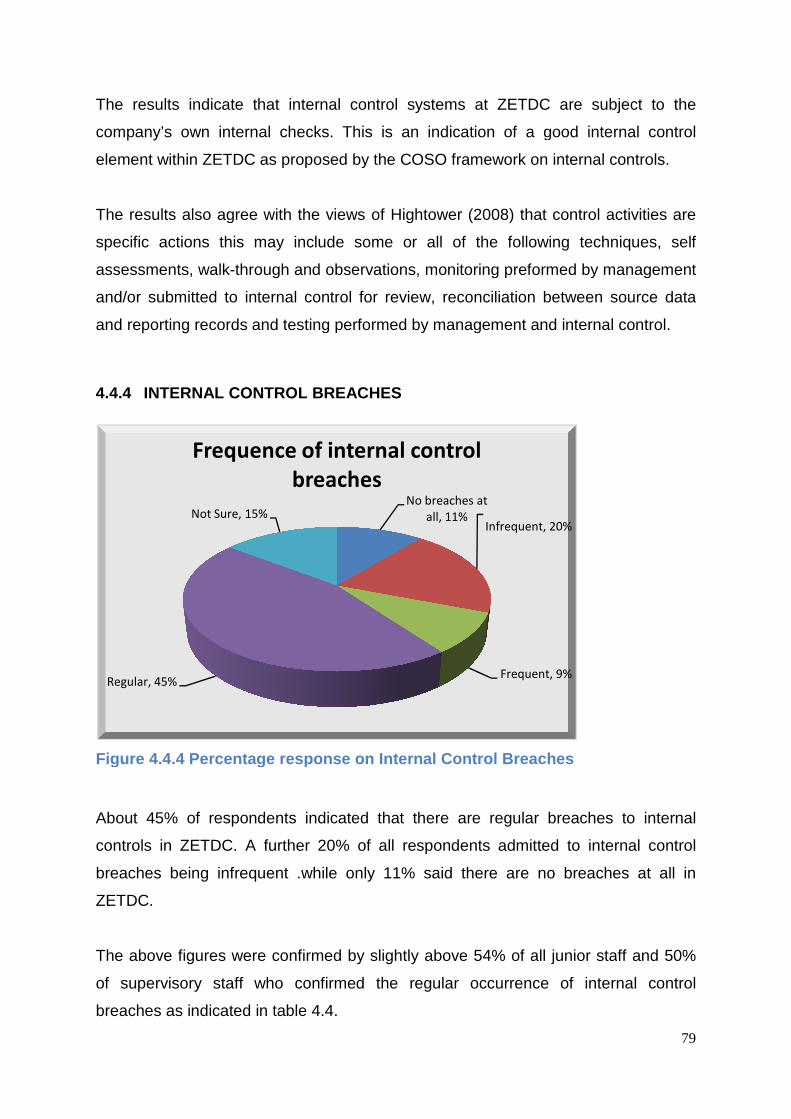

Figure 4.4.4 Percentage response on internal control breaches

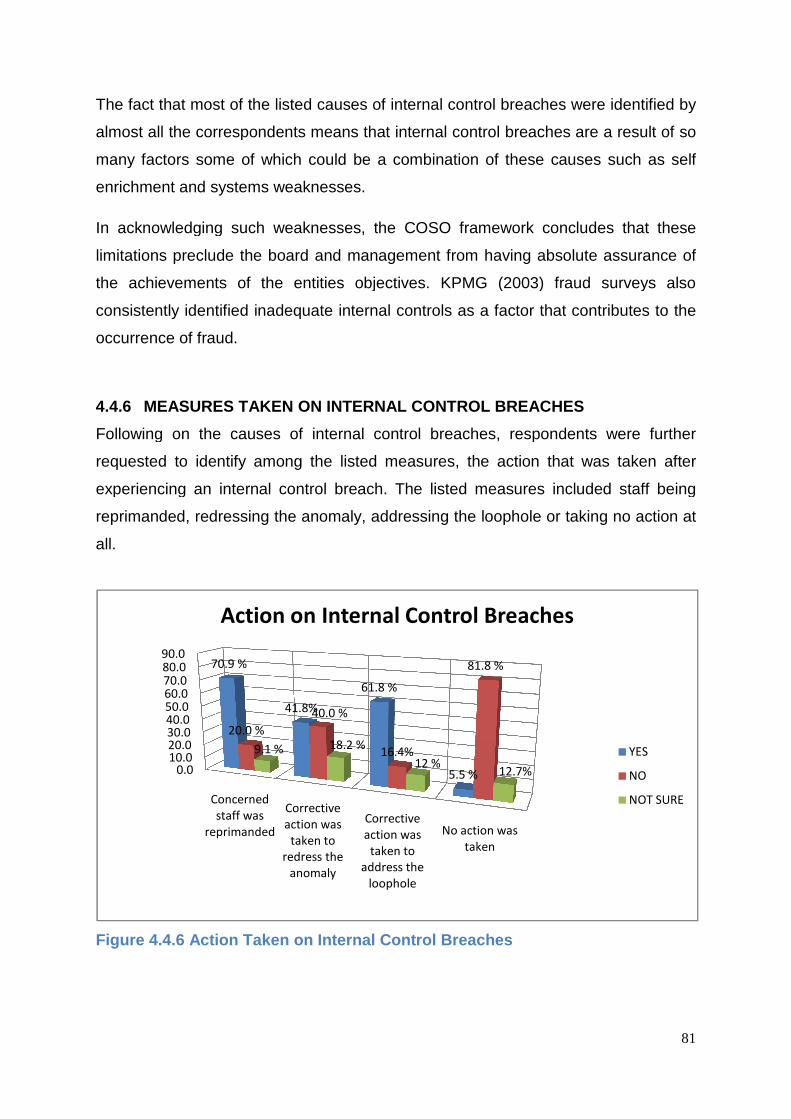

Figure 4.4.6 Action taken on internal control breaches

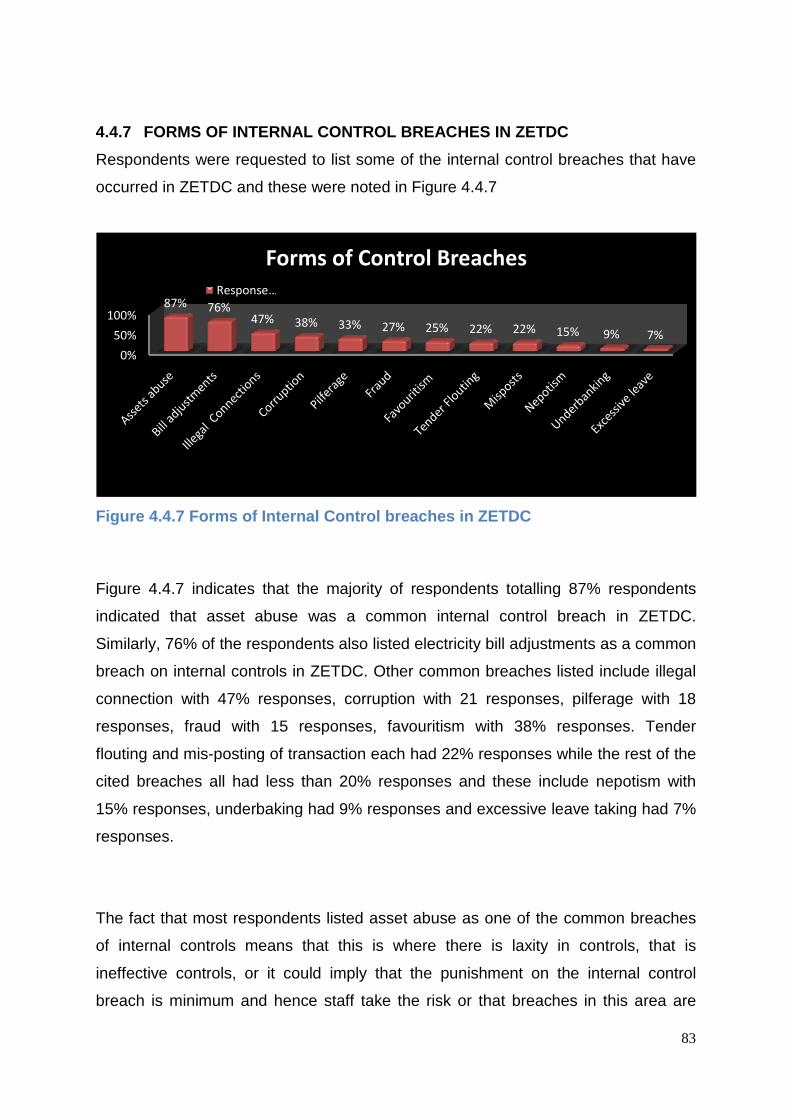

Figure 4.4.7 Occurrence of internal control breaches

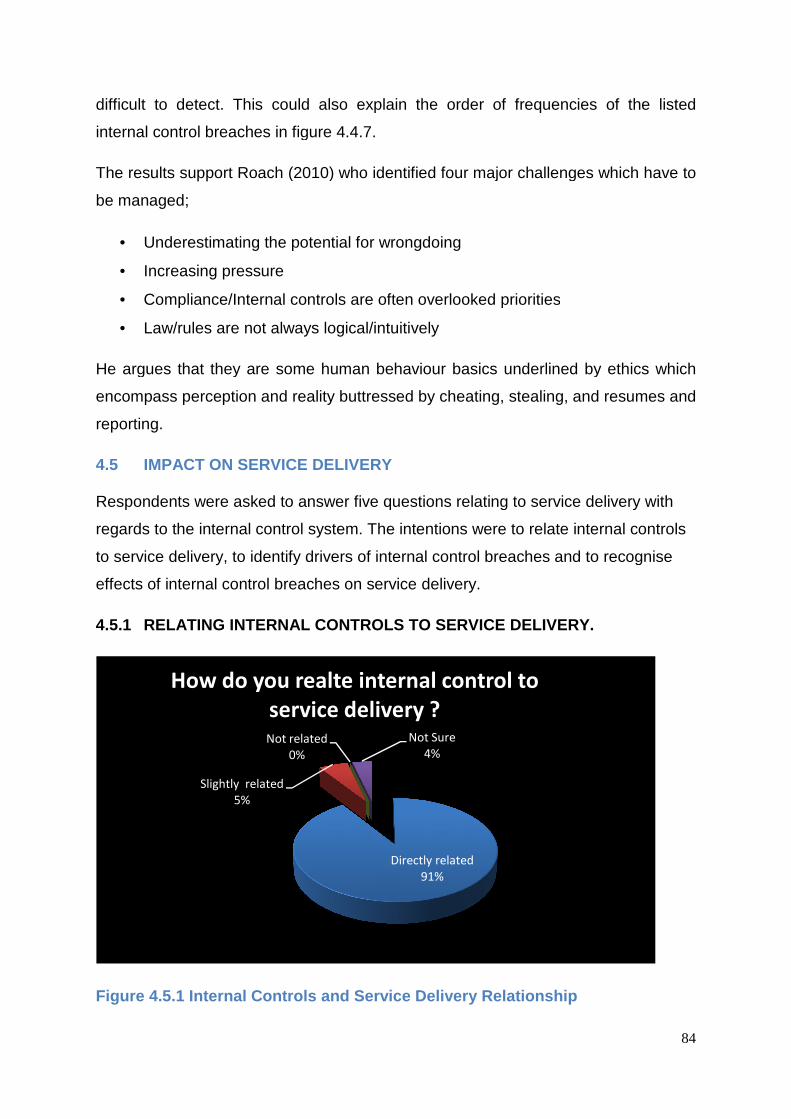

Figure 4.5.1 Response on internal control and service delivery

Figure 4.5.2 Services affected by internal control breaches

Figure 4.5.3 Impact on service delivery

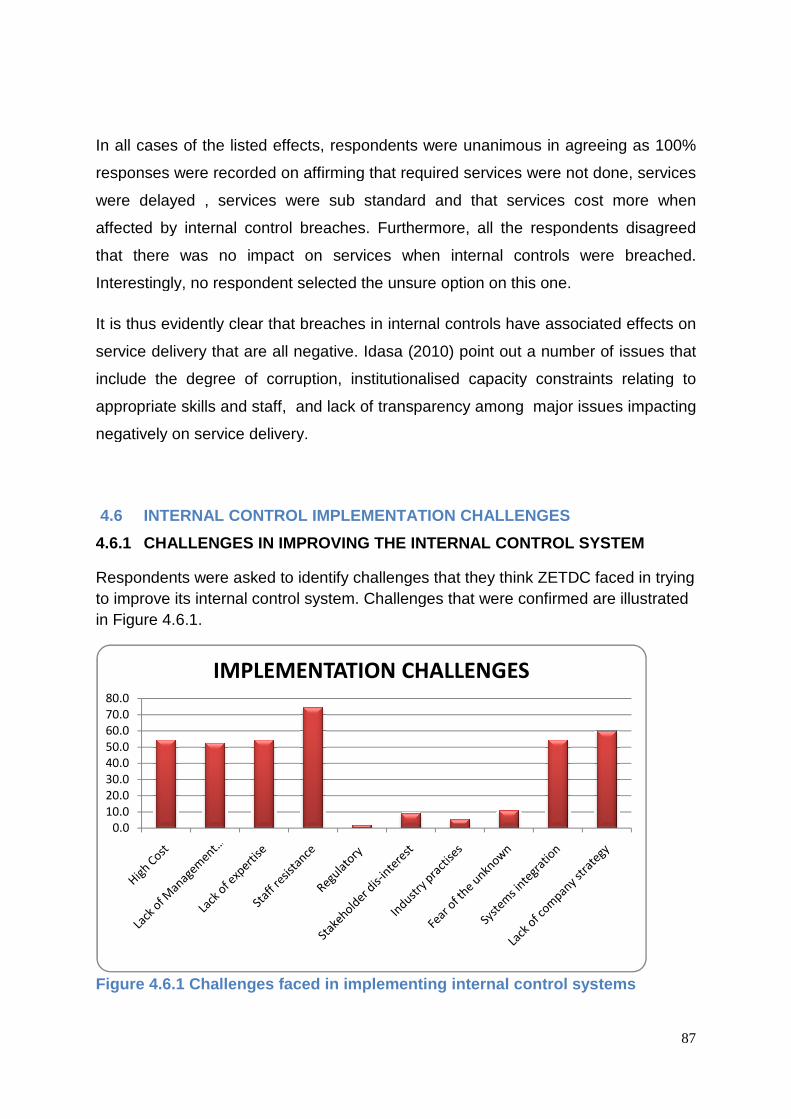

Figure 4.6.1

Challenges faced in implementing internal control

systems

Figure 4.6.2 Responses to ZETDC technology adoption

x

ABBREVIATIONS

4G Fourth Generation

CCZ Consumer Council of Zimbabwe

CFL Compact Fluorescent Lamps

CoCo Criteria of Control

COSO Committee of Sponsoring Organizations of the Treadway

Commission

CPA Certified Public Auditor

ERP Enterprise Resource Planning

GNU Government of National Unity

GWh Gigawatt hour

ICS Integrated Customer Service

IIA Institute of Internal Auditors

ITC Incomes and Tariff Commission

KWh Kilowatt hour

KV Kilovolts

MD and A Management Discussion and Analysis

POTRAZ Postal and Telecommunications Regulatory Authority of

Zimbabwe

SADC Southern African Development Community

SAP Systems Application and Products

SAPP Southern Africa Power Pool

SPSS Statistical Package for the Social Sciences

STEM Short Term Energy Market

xi

USD United States Dollar

ZEDC Zimbabwe Electricity Distribution Company

ZEDC Zimbabwe Electricity Distribution Company

ZENT ZESA Enterprises

ZERA Zimbabwe Energy Regulation Authority

ZESA Zimbabwe Electricity Supply Authority

ZETC Zimbabwe Electricity Transmission Company

ZETDC Zimbabwe Electricity Transmission and Distribution Company

ZIMSTATS Zimbabwe Statistical Agency

ZPC Zimbabwe Power Company

1

CHAPTER 1

INTRODUCTION AND BACKGROUND TO THE STUDY

1. INTRODUCTION

The world economy has experienced various business scandals and corporate

failures such as the Enron accounting fraud, the Deutsche Bank spying scandal, the

Royal Dutch Shell overstatement of oil reserves, the WorldCom overstatement of

cash flows, the Olympus Corporation accounting scandal. Zimbabwe has also

experienced the Renaissance Merchant Bank (RMB) and Genesis Investment Bank

insolvency, the collapse of Ziscosteel and Air Zimbabwe among several other

corporate crisis. In view of this, focus has now shifted to the individual company’s

internal control system. A company’s internal control system has become

fundamental in various ways. Proponents of corporate governance have exerted

pressure to ensure that an effective internal control system forms part of the

corporate governance initiatives. There is growing perception that effective internal

controls help prevent and detect fraud, that reliable financial reporting is underpinned

by effective internal control system and that good internal controls will ultimately

deliver a quality product or service.

It is with this in mind that this research endeavours to evaluate one of the most vital

utility companies in Zimbabwe, the Zimbabwe Electricity Supply Authority (ZESA)

through its subsidiary company, the Zimbabwe Electricity Transmission and

Distribution Company (ZETDC) which is the sole supplier of electricity services in

the country. The study seeks to evaluate the internal control system, explore internal

control breaches, identify implementation challenges and find best practises that can

assist ZETDC in its mandate to deliver a quality service. This chapter provides the

background of the study, introduces the company under study - ZETDC, states the

problem statement, the research objectives and questions, the research proposition

and provides the significance, scope and the outline of the research.

2

1.1 BACKGROUND OF THE STUDY

1.1.1 OVERVIEW

There has been an unprecedented public outrage on the shoddy services obtaining

from Zimbabwe Electricity Supply Authority (ZESA) through its subsidiary company,

Zimbabwe Electricity and Distribution Company (ZETDC). Recently, Zimbabwean

readers have woken up to screaming front page newspaper headlines on ZESA such

as ‘ZESA billing woes to stay’ (Gumbo, 2012), ‘ZESA: A Thorn in flesh’ (Bwititi,

2011), ‘ZESA fails to import power’ (Nkala, 2011), ‘ZESA billing system chaotic’

(Harare Residents Trust, 2012), “Consumers Slam ZESA tariff hike”, (2011), ‘ZESA

attacked for load shedding’ (Ndlovu, 2010), ‘ZESA fears collapse’ (Mushava, 2011),

‘Hundreds march through Bulawayo to protest ZESA failures’ (Sibanda, 2011),

‘Disband ZESA’ (Zvauya and Kadirire, 2011), ‘Nerve racking power bills from ZESA’

(Mapimhidze, 2012) and many more such headlines. ZESA has fought hard to

manage a lot of public outrage. According to these newspaper reports, consumers

have bitterly and emotionally complained about the poor service quality offered by

ZETDC. The Consumer Council of Zimbabwe (CCZ) executive director Ms

Rosemary Siyachitema believes ‘ZESA has tossed electricity users from the frying

pan straight into the fire’ (Bwititi, 2011). Such is the frustration by electricity

consumers on power availability that they have even gone to the extent of changing

the acronym of ZESA from Zimbabwe Electricity Supply Authority to Zimbabwe

Electricity Sometimes Available (SW Radio Africa, 2011).

Most of the reported complaints from electricity consumers include unreasonable

bills sent to customers. Some bills as high as US $2 million were at one time

received by some domestic consumers and could possibly have arisen mainly from

continuous meter estimations that seem to go on forever as noted by the consumers.

Others have cited the non delivery of the bills with most consumers going for long

periods without being advised of their electricity dues which is not expected from any

reasonable supplier. Complaints have also been made on unfair load shedding.

Whilst the shortage of power has been widely publicised as a regional challenge and

many have had to accept the challenge, it is the manner of power allocation of the

available power which has irked many consumers.

3

Most complaints have cited long periods of load shedding going for as much as 8

hours to three days in some areas and these areas have been observed to be in the

high density suburbs. Consumers have also cried foul on power fault attendances by

ZESA staff as taking far too long with one cited area going with a fault for three

months unattended. On the other hand, the business community also complained of

unsustainable electricity tariffs.

It was on the basis of some of these consumer concerns that ZESA Holdings was

investigated by the Competition Tariff Commission (CTC) in 2011 which found ZESA

Holdings guilty of abusing its monopoly power particularly on services rendered

through ZETDC.

Research carried out by ZETDC titled “Customer Survey Monitor” in 2011, on

customer’s perception on some services offered by ZETDC in Harare region also

revealed increasing negative dispositions by customers on service delivery. The

details are illustrated in Figure 1.1.1

Figure 1.1.1 Harare Region Service Evaluation .Adapted from

ZETDC.”CUSTOMER SERVICE MONITOR HARARE REGION”. (2011)

a) Negative Opinions on Ratings b) Mean Opinion Ratings

0 %

20 %

40 %

60 %

80 %

100 %

B\Hall Rating

Timeliness

Service vs Charge

ChargePublic OpinionStaff

Upper Negative

Limit

30

40

50

60

70

80

90

M e a n P e r c en t

Banking Hall

Service Charge

Timeliness

4

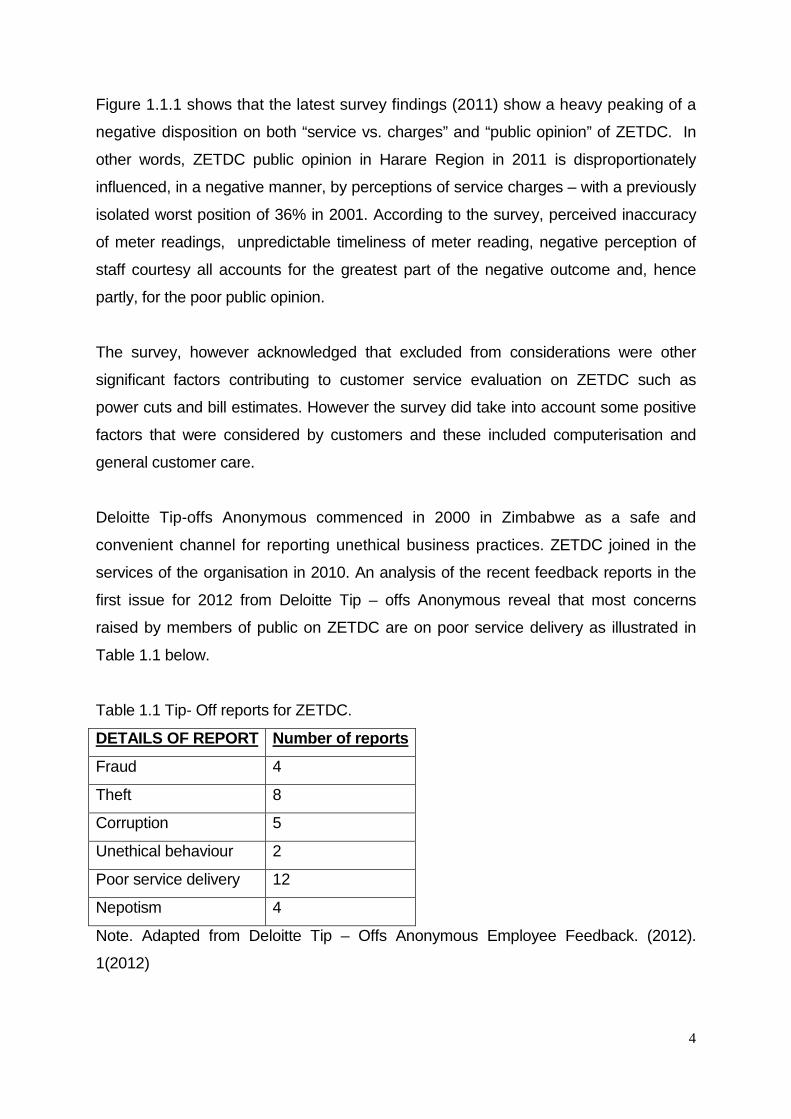

Figure 1.1.1 shows that the latest survey findings (2011) show a heavy peaking of a

negative disposition on both “service vs. charges” and “public opinion” of ZETDC. In

other words, ZETDC public opinion in Harare Region in 2011 is disproportionately

influenced, in a negative manner, by perceptions of service charges – with a previously

isolated worst position of 36% in 2001. According to the survey, perceived inaccuracy

of meter readings, unpredictable timeliness of meter reading, negative perception of

staff courtesy all accounts for the greatest part of the negative outcome and, hence

partly, for the poor public opinion.

The survey, however acknowledged that excluded from considerations were other

significant factors contributing to customer service evaluation on ZETDC such as

power cuts and bill estimates. However the survey did take into account some positive

factors that were considered by customers and these included computerisation and

general customer care.

Deloitte Tip-offs Anonymous commenced in 2000 in Zimbabwe as a safe and

convenient channel for reporting unethical business practices. ZETDC joined in the

services of the organisation in 2010. An analysis of the recent feedback reports in the

first issue for 2012 from Deloitte Tip – offs Anonymous reveal that most concerns

raised by members of public on ZETDC are on poor service delivery as illustrated in

Table 1.1 below.

Table 1.1 Tip- Off reports for ZETDC.

DETAILS OF REPORT Number of reports

Fraud 4

Theft 8

Corruption 5

Unethical behaviour 2

Poor service delivery 12

Nepotism 4

Note. Adapted from Deloitte Tip – Offs Anonymous Employee Feedback. (2012).

1(2012)

5

Table 1.1 indicates that out of the 35 reports on ZETDC received in the first quarter in

2012, the majority of them,12 (34%) were on poor service delivery.

Furthermore, ZETDC the power distributer has had to ration the available inadequate

power through load shedding since 2007. However, in recent times (since 2009), it

has had to increase its load shedding frequency since power supply failed to meet

the increasing demand as highlighted in its load shedding programme. The load

shedding programme indicates that mostly residential areas will be without power

during the morning and evening peak periods. However, ZETDC has failed to

implement the load shedding as per schedule, a concern that has also irked

electricity consumers.

It is mostly when a company has collapsed or is in dire operational challenges that

questions begin to be asked as to what could have possibly gone wrong. Most

pointers will be in the direction of a breakdown in the system of internal controls and

this may not be far-fetched. In recent years, the relevance and objectives of Internal

Controls, have expanded far beyond the traditional ambit of protection against theft

and fraud, well into the areas of effectiveness, accountability and operational

efficiency of the organisation, hence the need for an evaluation of the system of

internal controls at ZETDC.

1.1.2 BACKGROUND TO THE COMPANY - ZETDC

Zimbabwe Electricity Transmission and Distribution Company (ZETDC), belongs to a

diversified group of companies whose core business is electricity generation,

transmission and distribution in Zimbabwe.

The Electricity Amendment Act Number 3 of 2003 provided for the setting up of a

company to hold shares of the state in the successor companies of the Zimbabwe

Electricity Supply Authority which company was registered under the Companies Act

[ Chapter 24;03] as ZESA Holdings (Private) Limited. The successor companies that

comprise the ZESA Holdings Group of companies are Zimbabwe Power Company

(ZPC), Zimbabwe Electricity Transmission and Distribution Company (ZETDC),

6

ZESA Enterprises and Powertel Communications. Each of the successor companies

is incorporated under the Companies Act (Chapter 24:03) and has its own board of

directors appointed by ZESA Holdings (Private) Limited as the shareholder. ZESA

Holdings (Private) Limited is the Holding company and is also run by a Board of

Directors. The company is wholly owned by the Government of Zimbabwe.

The Zimbabwe Electricity Transmission and Distribution Company (ZETDC) is a

subsidiary of ZESA Holding (Pvt) Ltd that is involved in the business of bulk

purchasing of electricity from power producers locally and regionally, transporting it

to load centres across the country for distribution and retail to end user customers.

Its major functions as highlighted on the ZESA website (2012) include : Electricity

retailing - Network planning, development, operation and maintenance -

Development, Operation and Maintenance of the transmission infrastructure within

Zimbabwe - Power System Operations - Bulk Power Purchases and System

Planning for Long Term Capacity.

ZETDC has its Head Office in Harare and Five regional offices in Harare (Harare

Region), Bulawayo (Western Region), Mutare (Eastern Region), Gweru (Southern

Region) and Chinhoyi (Northern Region). Each Regional office has several district

offices spread throughout the region stationed in city centres

CORE BUSINESS

Zimbabwe Electricity Transmission and Distribution Company (ZETDC) is mandated

in terms of the Electricity Act (Cap 13:09), to carry out the following activities which

are also outlined in its 2010 Annual report.

i) Transmission and Distribution Infrastructure Mai ntenance and

Development

The company develops, operates and maintains transmission and distribution

facilities within Zimbabwe. It receives power at 330 kilovolts (kv) from ZPC

(Zimbabwe Power Company)’ s Hwange, Bulawayo , Munyati and Harare Thermal

Power stations and Kariba Hydro-electrical Power station. It also gets import power

7

from Mozambique’s Carbora Bassa at 400 kv through the Bindura 330kv/132kv/33kv

substation.

Other regional power imports from South Africa’s Eskom and Democratic Republic of

Congo’s SNEL supplied at 420kv come through Insukamini Interconnector

Substation in Bulawayo.

It is this power which is then transmitted at high voltages of 330kv, 132kv, 88kv and

66kv to power users called load centres. Transmission lines span long distances with

the Kariba substation to Alaska substation (Chinhoyi) running more than 200

kilometres and Hwange substation to Marvel substation (Bulawayo) spanning 300

kilometres.

Before power is received by a consumer it has to be transformed to a lower voltage.

Voltage transformation is done at a substation using transformers. Power is

transformed from 330kv to 132kv and further down to 88kv and 33kv for distribution

to users.

Maintenance work involves the fixing, repairing and overhauling or servicing of the

physical assets which are the transformers, circuit breakers and the isolators. When

power supplies are lost due to a line that has fallen to the ground as a result of a

pylon which has collapsed, maintenance staff restores power by erecting a new

pylon or reconstructing the collapsed one.

ii) Electrical power system operations.

The company ensures that supply and demand match on a minute-by-minute basis.

ZETDC also monitors the power system and ensures safety of personnel and

equipment during switching operations of any equipment connected to the grid. This

may also be necessary to allow for maintenance of certain sections or for load

shedding purposes.

8

Due to the constrained power supply availability in Zimbabwe, ZETDC has had to

manage the demand side through load shedding and has continuously drawn a load

shedding programme for the various centres across Zimbabwe.

There are different load shedding programmes for the two distinct seasons in

Zimbabwe one for summer where power demand is comparatively low and one for

winter where power demand is high. According to a notice by ZETDC for 2010 Load

Shedding in the press (The Herald, 2010) essential services loads are exempted

from load shedding and these were classified as follows;

• Major Referral Hospitals

• Major Water and Sewer installations

• National security establishments

• Major airports

• Major Central business districts with high rise buildings

• Winter wheat farming belts to receive priority supplies.

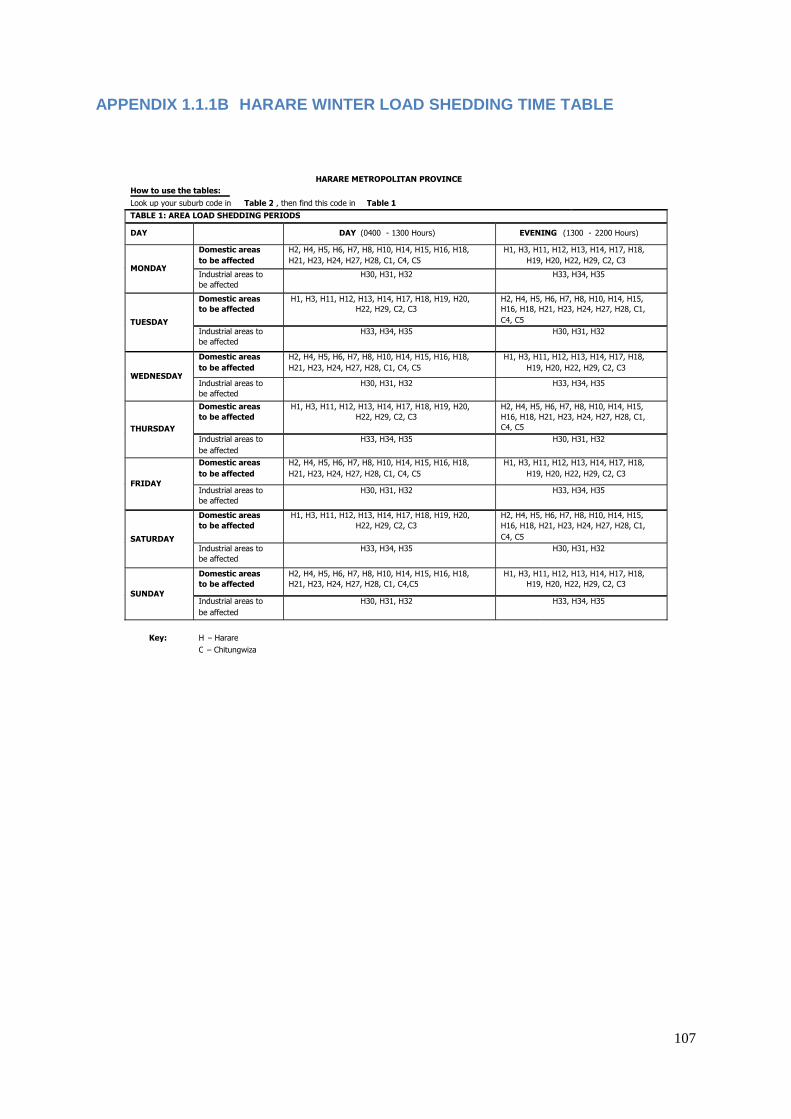

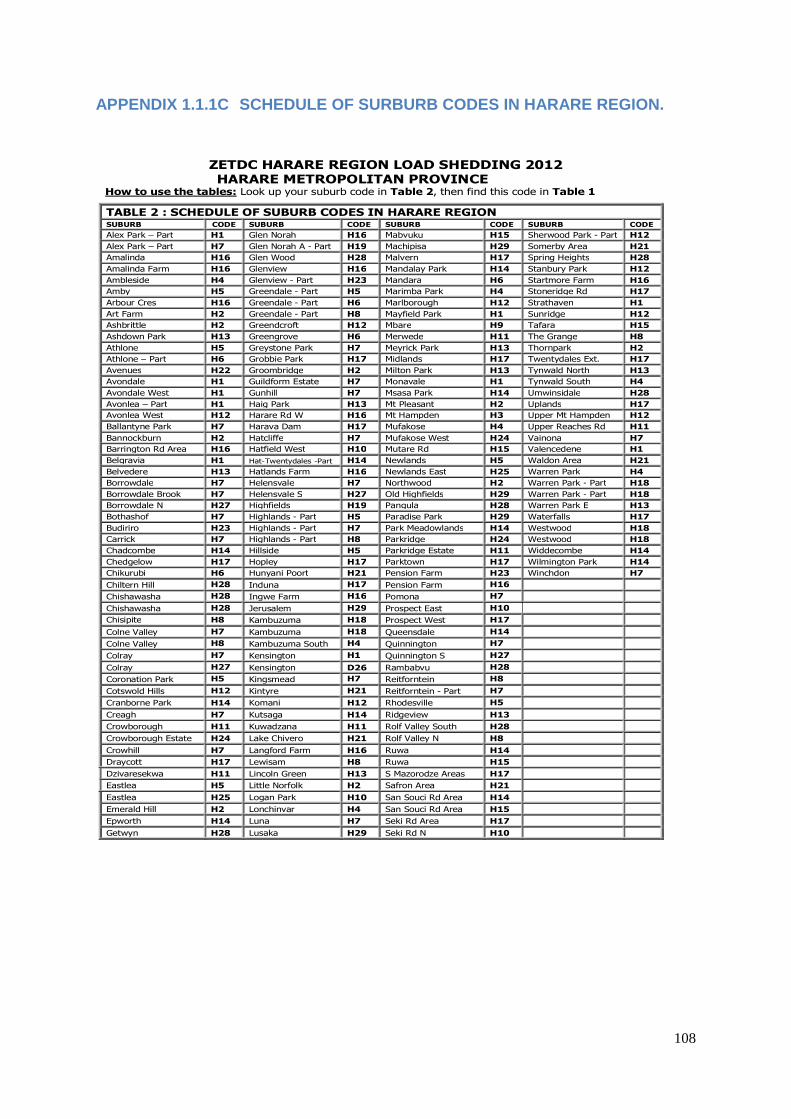

Appendix 1.1.1A, Appendix 1.1.1B and Appendix 1.1.1 C shows the load shedding

programme during summer for 2010 and winter for 2012 for Harare region. On a

normal operations assumption taking the summer 2010 load shedding schedule,

each point on the schedule is shed during the morning peak period (between

0600hrs and 0800hrs) and during the evening peak period (between 1800hrs and

2200hrs). Consequently, each area should be shed a total of 22 hours weekly.

iii) Electricity Trading

The company purchases bulk electrical power from internal sources (Hwange, Kariba,

Harare, Munyati and Bulawayo Power Stations and Independent Power Producers) as

well as from neighbouring countries (Mozambique, Democratic Republic of Congo,

South Africa and Zambia) for sale to local consumers and also trading on the Southern

African Power Pool (SAPP).

However, ZETDC’s sources of power supply have remained depressed over the last

few years as a result of ZPC’s operational challenges coupled with regional supply

shortfalls. As at 11 May 2012, generation statistics showed that electricity production

9

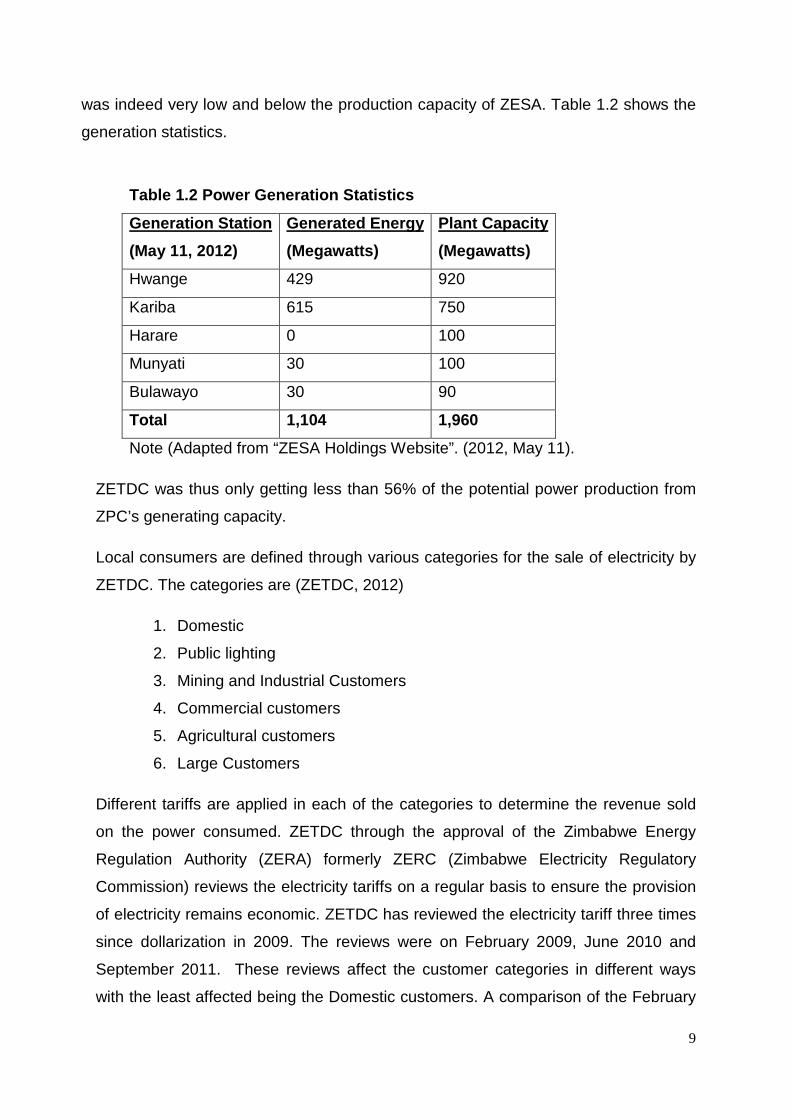

was indeed very low and below the production capacity of ZESA. Table 1.2 shows the

generation statistics.

Table 1.2 Power Generation Statistics

Generation Station

(May 11, 2012)

Generated Energy

(Megawatts)

Plant Capacity

(Megawatts)

Hwange 429 920

Kariba 615 750

Harare 0 100

Munyati 30 100

Bulawayo 30 90

Total 1,104 1,960

Note (Adapted from “ZESA Holdings Website”. (2012, May 11).

ZETDC was thus only getting less than 56% of the potential power production from

ZPC’s generating capacity.

Local consumers are defined through various categories for the sale of electricity by

ZETDC. The categories are (ZETDC, 2012)

1. Domestic

2. Public lighting

3. Mining and Industrial Customers

4. Commercial customers

5. Agricultural customers

6. Large Customers

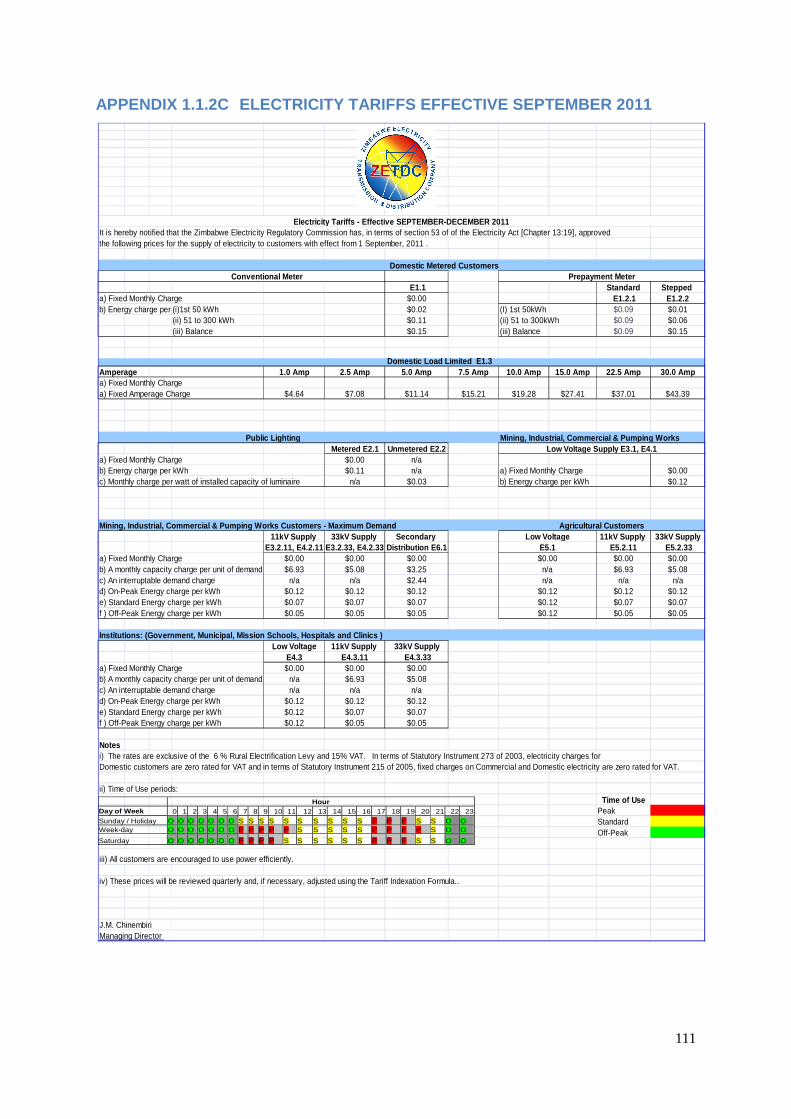

Different tariffs are applied in each of the categories to determine the revenue sold

on the power consumed. ZETDC through the approval of the Zimbabwe Energy

Regulation Authority (ZERA) formerly ZERC (Zimbabwe Electricity Regulatory

Commission) reviews the electricity tariffs on a regular basis to ensure the provision

of electricity remains economic. ZETDC has reviewed the electricity tariff three times

since dollarization in 2009. The reviews were on February 2009, June 2010 and

September 2011. These reviews affect the customer categories in different ways

with the least affected being the Domestic customers. A comparison of the February

10

2009 tariff review with the September 2011 indicate that on overage the price for the

domestic customer increased from US 7 cents to US 10 cents, a 43% increase.

The February 2009, June 2010 and September 2011 tariff reviews are indicated on

Appendix 1.1.2A, Appendix 1.1.2B and Appendix 1.1.2C respectively.

iv) Power System Planning

The company undertakes long-term supply and demand studies in order to develop a

national least cost System Development Plan that also takes cognisance of regional

developments. This involves identifying the need for new generating plants and

expansion of the grid to meet load growth and transfer power from new generation

plants to load centres.

v) Regional Cooperation

The company’s Transmission Division, as the Zimbabwe representative in SAPP, plays

a key role I n regional integration through its strategically positioned power grin that

provides critical links between Southern and Northern parts of the SAPP

interconnected power system. This makes the company the hub of transactions

between DRC, Zambia and Mozambique on one end and Botswana, South Africa,

Swaziland, Namibia and Lesotho on the other end. The wheeling services provided to

SAPP by the company facilitate electricity trading in the region.

The supply of power imports from SAPP has however remained restricted as the

SADCC region (Southern African Development Community) grapples with power

shortages. This, coupled with cash flow challenges, has seen ZETDC failing to obtain

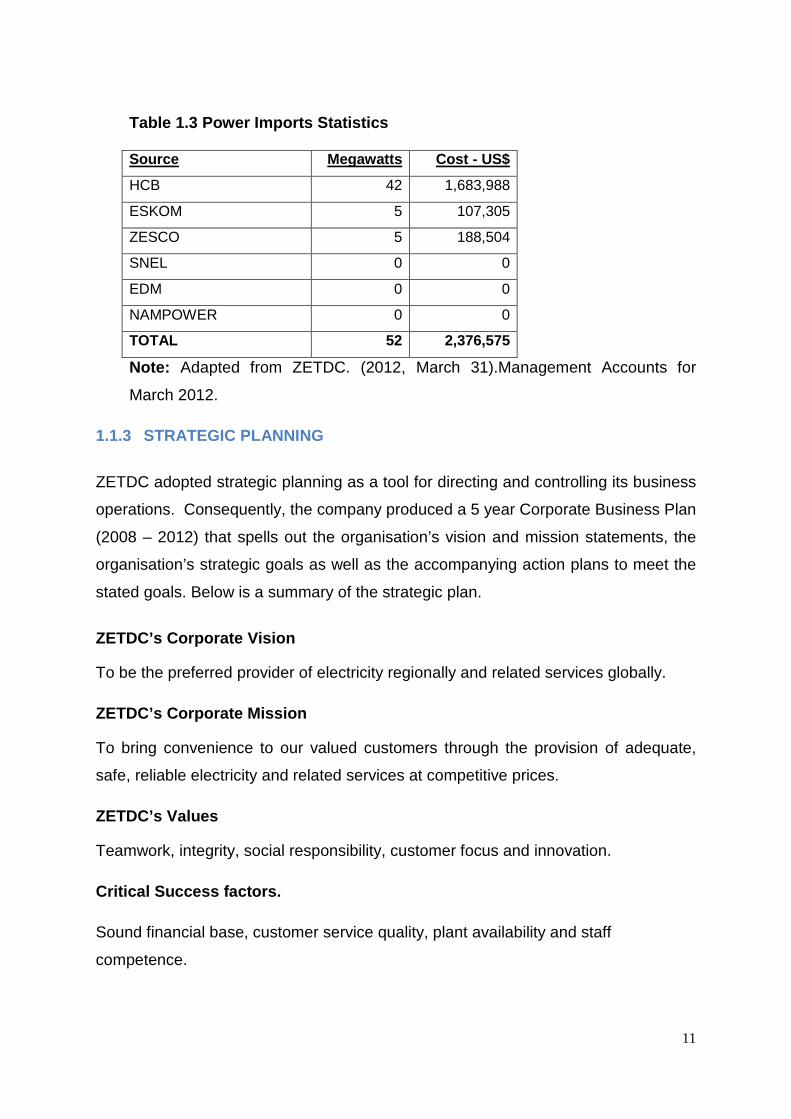

extra power from its neighbouring power utilities. The table 1.3 indicates the sources of

imports for ZETDC as at 31 March 2012.

11

Table 1.3 Power Imports Statistics Source Megawatts Cost - US$

HCB 42 1,683,988

ESKOM 5 107,305

ZESCO 5 188,504

SNEL 0 0

EDM 0 0

NAMPOWER 0 0

TOTAL 52 2,376,575

Note: Adapted from ZETDC. (2012, March 31).Management Accounts for

March 2012.

1.1.3 STRATEGIC PLANNING

ZETDC adopted strategic planning as a tool for directing and controlling its business

operations. Consequently, the company produced a 5 year Corporate Business Plan

(2008 – 2012) that spells out the organisation’s vision and mission statements, the

organisation’s strategic goals as well as the accompanying action plans to meet the

stated goals. Below is a summary of the strategic plan.

ZETDC’s Corporate Vision

To be the preferred provider of electricity regionally and related services globally.

ZETDC’s Corporate Mission

To bring convenience to our valued customers through the provision of adequate,

safe, reliable electricity and related services at competitive prices.

ZETDC’s Values

Teamwork, integrity, social responsibility, customer focus and innovation.

Critical Success factors.

Sound financial base, customer service quality, plant availability and staff

competence.

12

Core Competencies

The core competencies required in order to achieve the vision are strong technical

skills, sound financial management skills; professionalism, strong management

skills, and entrepreneurial skills.

ZETDC’s STRATEGIC BUSINESS OBJECTIVES

As outlined in its 2008 to 2012 business strategy, ZETDC has defined a set of

strategic objectives for its main functional business areas which are Transmission,

Distribution, Finance and Human resources. These are then translated into business

action strategies for Transmission, Distribution and Head Office. The strategic

objectives are listed as:-

• Financial Goals:

o Ensuring cost effective tariffs;

o Improving working capital;

o Improving financial management;

o Ensuring attainment of break-even point;

o Increasing revenue base and

o Ensuring revenue collection maximization.

• Customer Goals:

o Ensuring safe use of electricity;

o Improving Corporate Image;

o Improving customer communication;

o Improving availability of electricity to customers;

o Improving service delivery and customer satisfaction and

o Improving environmental management.

• Operational Goals:

o Improving system reliability;

o Improving productivity;

o Reducing accidents;

o Improving communication;

13

o Improving quality of supply and

o Improving operational efficiency.

• Human Capital Goals:

o Ensuring high employee productivity;

o Improving staff health and safety;

o Ensuring staff motivation and retention;

o Ensuring adequate and competent staff;

o Ensuring a good business culture and

o Ensuring a good industrial relations climate.

1.1.4 THE CONTROL ENVIRONMENT

1.1.4.1 ORGANIZATIONAL STRUCTURE

The organisational structure is made up of elements of the control systems logical

structure. The elements are the organisational units used to structure business

functions for reporting.

ZETDC is headed by a Managing Director who reports to the Group chief executive

officer at ZESA Holdings. There is also a board of directors at ZETDC the majority of

whom are non executive independent directors. The ZETDC Managing Director

heads an executive committee comprising the finance director, the commercial

director, the transmission services director, all at head office, and five regional

general managers for Harare, Western, Southern, Eastern and Northern Regions.

The regional managers overseer power distribution and revenue collection in each of

the regional centres in Zimbabwe through various district offices in their regions. An

internal audit unit at ZESA Holdings monitors the activities at ZETDC through regular

internal audits of all ZETDC centres and reports directly to the board audit

committee.

Each district is headed by a network manager responsible for the supply of power

and maintenance of the distribution networks and a sales manager responsible for

power sales and revenue collections.

14

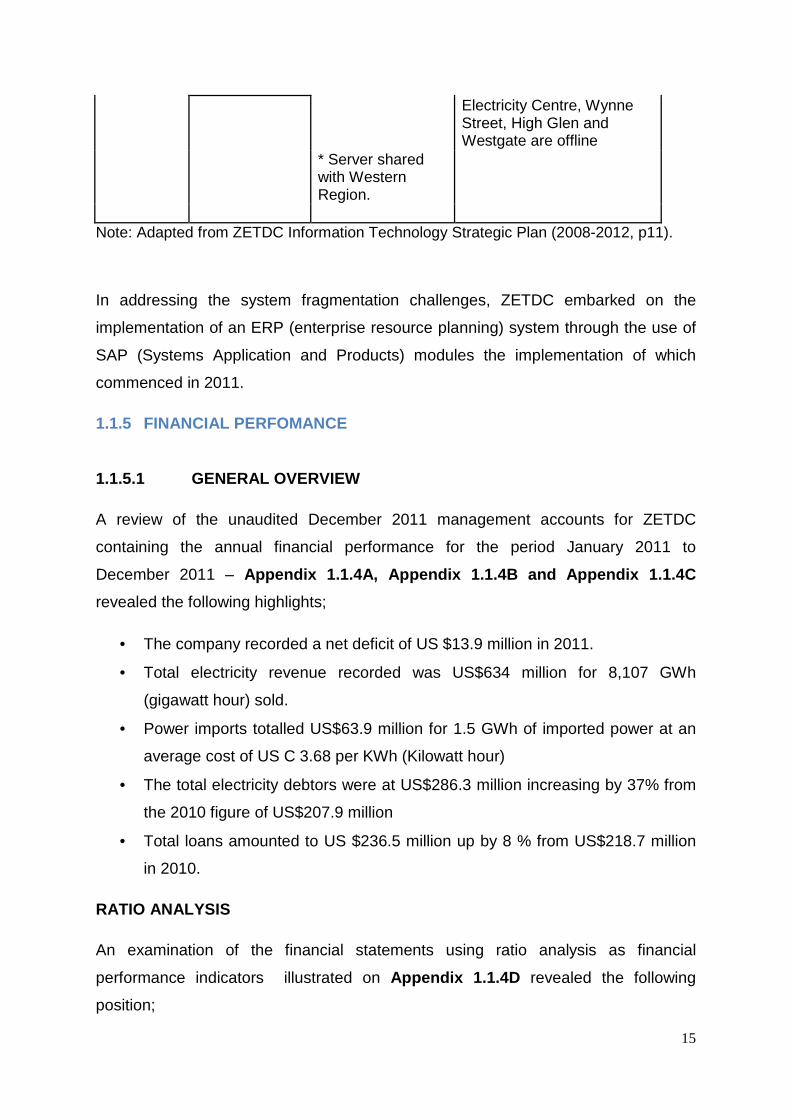

1.1.4.2 APPLICATION SYSTEMS

The current internal control systems in ZETDC is characterised by fragmented

systems with varying degrees of business coverage and utilisation. (ZETDC I.T

Business Plan, 2009). This state of affairs is a result of limitations in data

communications facilities, partial implementation of some systems, high staff

turnover in user and IT departments as well as the amalgamation of ZETCO

(Zimbabwe Electricity Transmission Company) and ZEDC (Zimbabwe Electricity

Distribution Company).

An overview of the current IT application systems currently in place at ZETDC head

office and Harare region is highlighted in table 1.4.

Table 1.4 ZETDC Application Systems

LOCATION APPLICATION PLATFORM COVERAGE ZETDC Head Office

SAP Financials Sun Solaris Both Distribution and Transmission at Head Office.

Finance Oracle database Control Sales and

Dist. * Server rented from Dexel and shared with Powertel.

Materials Management.

Harare Region

JBA Business/400

IBM OS/400 Entire Region where comms facilities are available.

General Ledger

DB2/400 database

Cash Book Purchase

Ledger * Dedicated AS/400 server.

Vision 2000 – Soluziona

Sun Solaris Entire Region where comms facilities are available.

IPMS Oracle database DCS Utilisation for MMS and IMS

almost at nil. MMS * Server shared

with Western and Southern as well as ZPC entities.

IMS

ICS - Soluziona Sun Solaris Entire Region where comms facilities are available.

Oracle database All Banking Halls except

15

Electricity Centre, Wynne Street, High Glen and Westgate are offline

* Server shared with Western Region.

Note: Adapted from ZETDC Information Technology Strategic Plan (2008-2012, p11).

In addressing the system fragmentation challenges, ZETDC embarked on the

implementation of an ERP (enterprise resource planning) system through the use of

SAP (Systems Application and Products) modules the implementation of which

commenced in 2011.

1.1.5 FINANCIAL PERFOMANCE

1.1.5.1 GENERAL OVERVIEW

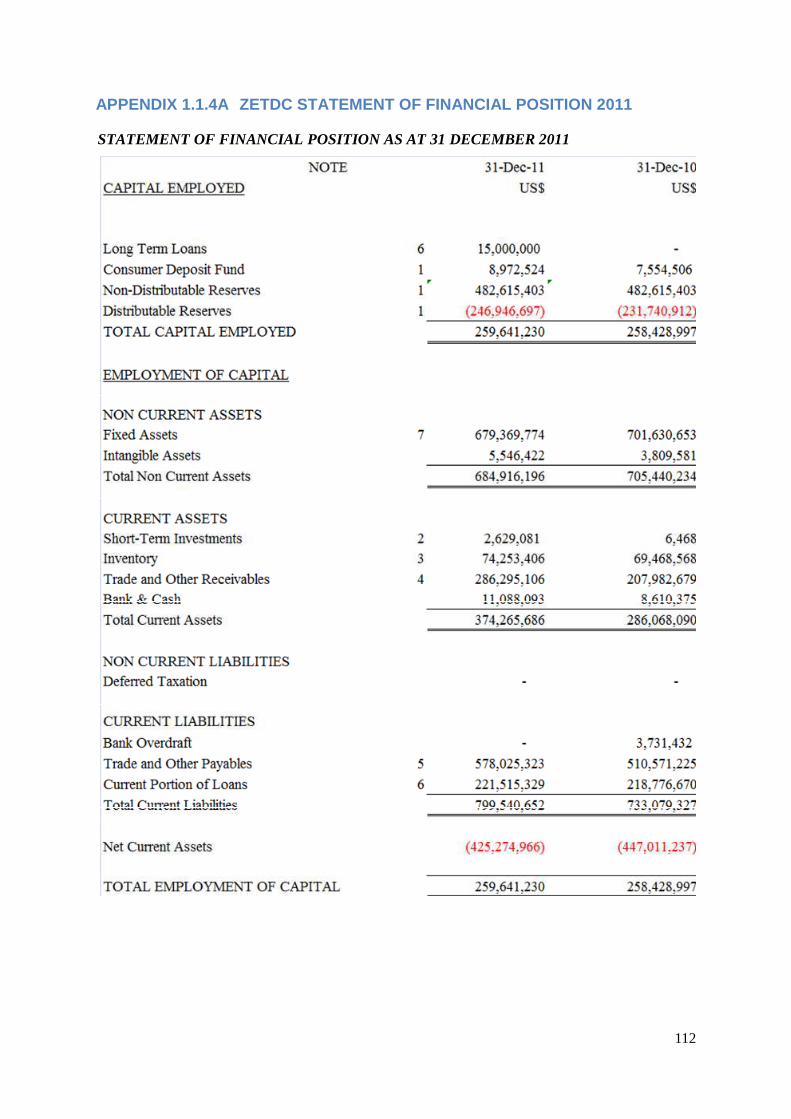

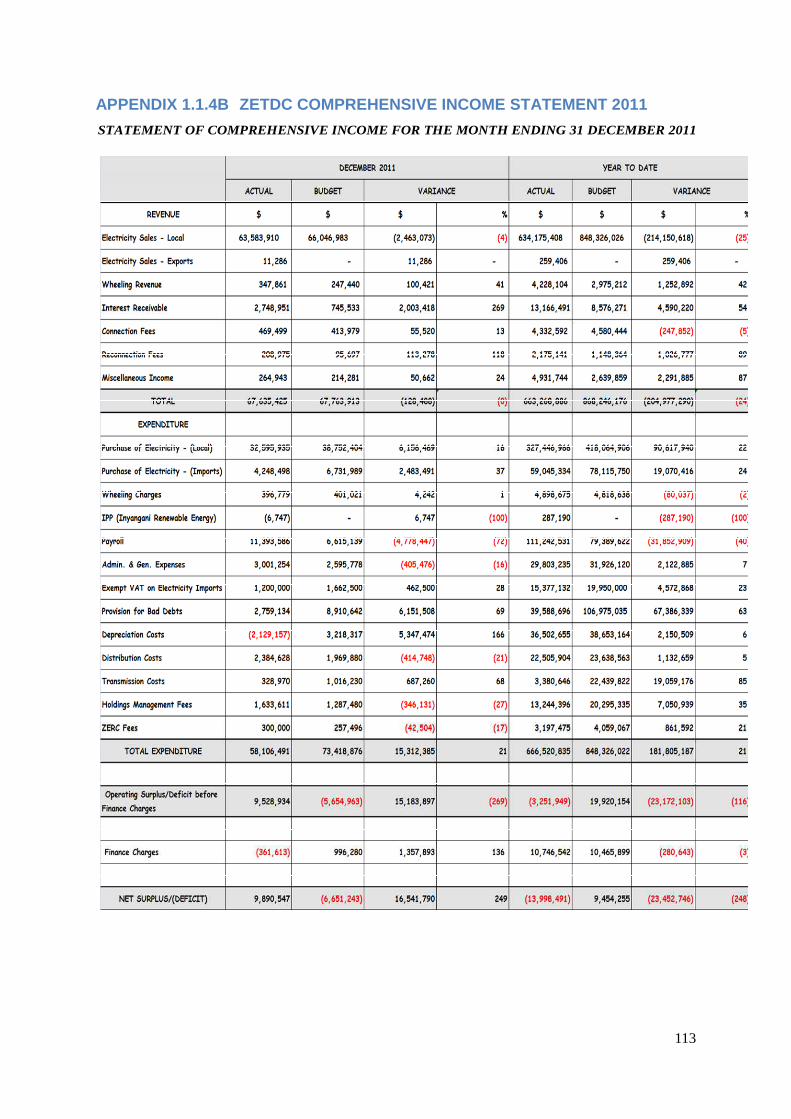

A review of the unaudited December 2011 management accounts for ZETDC

containing the annual financial performance for the period January 2011 to

December 2011 – Appendix 1.1.4A, Appendix 1.1.4B and Appendix 1.1.4 C

revealed the following highlights;

• The company recorded a net deficit of US $13.9 million in 2011.

• Total electricity revenue recorded was US$634 million for 8,107 GWh

(gigawatt hour) sold.

• Power imports totalled US$63.9 million for 1.5 GWh of imported power at an

average cost of US C 3.68 per KWh (Kilowatt hour)

• The total electricity debtors were at US$286.3 million increasing by 37% from

the 2010 figure of US$207.9 million

• Total loans amounted to US $236.5 million up by 8 % from US$218.7 million

in 2010.

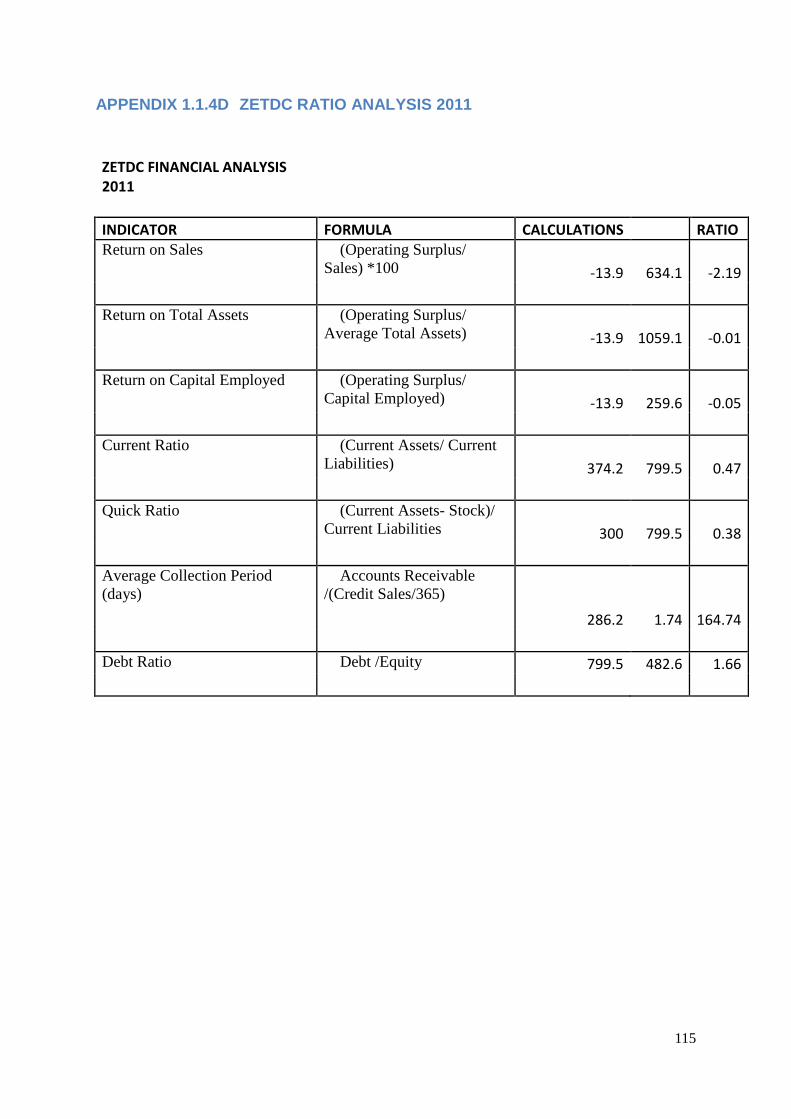

RATIO ANALYSIS

An examination of the financial statements using ratio analysis as financial

performance indicators illustrated on Appendix 1.1.4D revealed the following

position;

16

PROFITABILITY RATIOS

• Return on sales recorded a negative 2%. This means that sales are

generating a negative return in that from every dollar of sales 2 cents is lost.

• Return on total assets was at -0.013%. The assets are not getting a return for

their use. The company is losing 1 cent on every dollar of the assets.

• Return on capital employed was a negative .05%. An indication that 5 cents is

lost from every $1 invested into the company.

LIQUIDITY RATIOS

• The current ratio was 0.4. The company can only meet 40 cents from every

$1 on its current obligations. This is a far outcry from the standard

recommended ratio of 2 :1

• The quick ratio recorded 0.3. The liquid resources available to settle

immediate obligations are only 30 cents for every dollar owing. The standard

recommended ratio is 1:1

• Debtors collection period showed 278 days. The company is taking over a

year to collect money from its revenue. It is effectively funding other entities at

the expense of its own cash flows.

DEBT MANAGEMENT RATIO

• Debt to equity ratio was at 1.6. The company is heavily funded by outsiders in

that for every $1 that the shareholders own in ZETDC, $1.60 is owed to

creditors.

These highlights reveal that ZETDC made a huge loss from its operations and is

increasingly funding its debtors whilst borrowing heavily to keep operating. It is also

apparent that it cannot meet its current obligation. Its assets are under-utelised. This

scenario puts the company’s going concern perspective into questions.

1.1.6 SWOT ANALYSIS

A SWOT analysis (Strength, Weaknesses, Opportunities and Threats) is a valuable

tool to quickly analyse various aspects of the current state of the business process

17

undergoing change. It is a framework for strategic planning, opportunity analysis,

competitive analysis, business and product development (Brennan, 2009).

STRENGTHS

i. State owned – ZETDC is a government wholly owned state enterprise giving

it a distinct advantage in the influence of policies that can safeguard its

interest.

Furthermore, it is able to utilise government guarantees to access offshore

funding and also government is able to guarantee its going concern basis.

ii. Huge capital base – The asset base of ZETDC covers the geographical

spread of the entire country of Zimbabwe and even interlocks with

neighbouring power utilities. This enables ZETDC to reach as many

customers as possible with its national distribution grid. The nature and cost

of the asset base are a barrier of entry to possible competitors.

iii. Sole supplier – ZETDC currently enjoys a monopoly over the supply of

power emanating from the historical legal set up. This therefore means that it

currently has no competition except from fuel powered generators which

serve as a substitute in the event of ZETDC failing to supply.

WEAKNESSES

i. Aged infrastructure – The transmission and distribution assets were

installed in the 1960’s and are thus over 50 years old. This has consequently

resulted in frequent breakdown leading to a high number of faults in power

supply.

ii. Poor Image – As a result of the frequent power outages due to asset

breakdown and load shedding due to constrained supply, customers do not

have confidence in ZETDC. This has also been compounded by the

haphazard billing system, high power tariffs, poor workmanship on faults and

selective credit control policies on ‘political heavyweights’ leaving the

reputation of ZETDC in a battered state.

iii. High Cost structure – The aged asset infrastructure which is also very huge,

results in very high maintenance costs forcing ZETDC to operate at very high

levels of costs thus eroding profit margins.

18

OPPORTUNITIES

i. Unfulfilled customer needs – Many customers remain without power due to

ZETDC’s inability to connect all potential customers leading to some

customers illegally connecting themselves and thus existing outside of

ZETDC’s billing system.

ii. New Technologies – Prepaid meters are being installed in place of the

conventional meters . This will do away with estimated meter reading at the

same time providing advance cashflows eliminating electricity debtors.

iii. Privatisation – The possibility of ZETDC being privatised will give it the

impetus to operate on a more sound commercial basis drawing upon

investors to expand and maximise on revenue.

THREATS

i. Controlled tariff – The power tariff is regulated through control by ZERA

(Zimbabwe Energy Regulation Authority) . This means that ZETDC has no

total control over what it charges to the customer as this has to be determined

through ZERA. It cannot literally share most of its cost with the customer.

ii. Substitutes – The possibilities of gas found in Lupane being fully exploited

can result in many customers substituting electricity for gas for a competitive

price. Furthermore, subject to fuel prices declining, consumers can easily turn

to generators in the event that electricity tariffs become uncompetitive.

iii. Deregulation - The electricity industry is undergoing deregulation to allow

other private players to enter the industry. This may bring in competition which

ZETDC may be ill prepared to deal with.

1.1.7 PEST ANALYSIS

(i) POLITICAL AND LEGAL ENVIRONMENT

A government of national unity (GNU) was formed by the three popular political

formations in Zimbabwe in February 2009 following a condemned electoral process

in 2008. This is pending elections which are anticipated after the completion of a new

constitution which is under consideration. Ministerial positions are shared between

the political formations. A recently enacted indigenisation and empowerment act

19

which seeks to economically empower previously disadvantaged locals is under

implementation. The energy sector is partially liberalised and is regulated by a

statutory body the Zimbabwe Energy Regulation Authority (ZERA) which was set up

in October 2011.

These developments are likely to impact directly on the leadership and direction of

ZETDC itself being a state enterprise. Government policies have a direct bearing on

ZETDC being an essential utility service provider in terms of both tariff charges and

the electricity supply environment.

(ii) SOCIO –ECONOMIC ENVIRONMENT

There is a prevailing stable economic environment in Zimbabwe buttressed by a

steady economic growth which, according to the minister of finance, is focused to

grow by 9.4% in 2012 as outlined in the 2012 National Budget Statement (Ministry of

Finance Zimbabwe, 2012). Inflation was reported by Zimbabwe Statistical Agency

(ZIMSTAT) at 4% on year on year whilst the monthly inflation was at 0.2% during the

month of April 2012 (Zimstat, 2012). However, the country is experiencing a liquidity

crunch with most banks struggling to get any cash let alone issue loans and

government through the Reserve Bank of Zimbabwe adopted measures to improve

the situation in February 2012 (Reserve Bank of Zimbabwe, 2012). There are

currently no official statistics for the unemployment rate but experts have estimated it

to be at 95% per 2009 estimates (index mundi, 2012). Energy production is currently

depressed with only 1,200 megawatts available against a demand of 2,200

megawatt. (ZESA Megawatt bulletin, 2012). This has resulted in load shedding

across the country.

ZETDC as a utility service provider will need to balance expectations from the public

who largely depend on the services of the utility company for all their energy needs.

(iii) TECHNOLOGICAL ENVIRONMENT

Zimbabwe has moved with the rest of the world in adopting recent technological

advancements and ZETDC is no exception. Such technological advances have

demanded a lot of integration between technologies and between organisations. Bill

payment systems between banks and other organisations are now in high demand

using 4G (fourth generation) cell phone technologies. Technological integration

20

between systems technologies in various organisations is now vital and the

challenge faced by ZETDC towards this is great.

1.1.8 ZETDC’S INTERNAL CONTROL DEFICIENCIES

They are some recorded publicised cases at ZETDC where there have been

incidences of internal control deficiencies. The following cases highlight some of the

recorded publicised deficiencies.

Case 1 - US $3 million fraud

In September 2010 ZETDC lost over US $3 million to two workers of a Spanish

computer firm which it had contracted to develop new computer systems and render

technical assistance in its billing (Farawo, 2010). The two would enter false amounts

into the system on the pretext that a customer has paid up when in actual fact they

would have intercepted through collusion with some ZETDC staff the payment by the

customers and converted it to their own use. The money was supposed to be paid

to the company but the two allegedly concealed the offence by reducing amounts of

the bills in the system to zero using an unauthorised Harare BATCH, as a financial

programme in the national server. ZETDC suffered an actual prejudice in the sum of

US$3,635,927.59 and nothing was recovered.

Case 2 - Reconnection scam

The Chronicle on 17 February 2012 reported that ZETDC could be losing thousands

of dollars in electricity bills by consumers who were either deleted from the billing

system or had their power fraudulently reconnected. ((ZESA unearths reconnection

scam, 2012)). The power utility had unearthed a scam in which some of its

employees were prejudicing the company by either deleting some consumers from

the system or were reconnecting defaulters and getting paid kickbacks.

Case 3 - Ministers’ ZESA scandal

ZETDC was reportedly failing to collect money from high ranking government

officials for electricity bills owing and was also not disconnecting them. According to

Newsday of 14 February 2012, (Langa, 2012 ), cabinet ministers, senior civil

servants and MPs were bleeding the Zimbabwe Electricity Supply Authority (ZESA)

dry by refusing to pay electricity bills at their private properties and using political

21

muscle to avoid being switched off. Some of the officials named who were owing

very huge amounts included the Manicaland governor, whose outstanding bill was

US $145 000, and Secretary for Energy and Power Development who owed

US$20 000 among several high ranking government officials also named in the

report. At the time the power utility was owed US$537 million by both its industrial

and domestic customers highlighting ZETDC’s poor debt management.

Case 4 - Inaccurate electricity bills sent to custo mers

Incidence of suspiciously erroneous electricity bills that were received by some

customers was noted by the Newsday (Mapimhidze, 2012). The report highlighted

incidences of inaccurate bills sent to customers by the power utility. In July 2011, a

tenant in Harare’s Avenues area received a US$5 bill for a month’s uninterrupted

supply of electricity whilst a tenant in the adjacent flat even rejoiced more for not

paying for the power he used because his apartment number did not appear in

ZESA’s database at all! In another case, a company executive received a US$5,000

bill and ZESA employees threatened to discontinue supplies if he failed to pay. It

was reported that the man had to pay an officer at the power utility US$100 to “sort

out the mess”.

Case 5 – ZESA Boss Fired

In September 2010, ZETDC fired its then managing director Mr Ernest Muchayi for

helping himself to a US $25,000.00 loan and paying out unsanctioned allowances to

top managers (Zesa Boss fired, 2010).

Case 6 – ZETDC accounts qualified

The external auditors who conducted an audit of ZETDC’s accounts for the financial

period 2010 did not agree with ZETDC’s valuation of its revenue. The auditors

therefore qualified the accounts on the basis that part of ZETDC’s revenue (US $3

million) was based on estimates which could not be conclusively verified (ZETDC

Annual Statements 2010)

The above cases serve to highlight the magnitude of the loopholes that exist at

ZETDC that put the company into perspective on its ability to self regulate and

safeguard its service delivery without compromising on quality.

22

1.2 PROBLEM STATEMENT

The introduction of the multicurrency system in 2009 which curbed the spiralling

inflation was a relief to the Zimbabwean economy which had been battered and

bruised by the record galloping inflation over the last three years. After so many

excuses for poor performance premised on the lack of foreign currency, ZETDC was

expected to show signs of service improvement with the improving economy as was

the case with most Zimbabwean companies, commencing 2009. However,

electricity customers remain sceptical on the services obtaining from ZETDC.

Electricity Bills are fraught with many errors, bill estimations continue unhindered,

load shedding continues outside the advertised schedules, power tariff are increased

on a regular interval, many customers remain outside of the billing system and

continue to enjoy free electricity. Reports of the company’s staff involvement in

abuse and prejudice of company resources continue to surface, and the company

continues to record losses in its annual accounts. All these issues point to a

systems failure within the organisation. ZETDC is the sole essential power utility

service provider in Zimbabwe and any failures on its part has a consequence on the

entire economy of the country. Whilst the final service delivery is evident, as in

services obtaining, it became apparent that the internal processes that give rise to

these unpalatable services needed some interrogation in order to fully comprehend

ZETDC’s commitment to service delivery. Why is ZETDC continuing in failing its

customers? Does ZETDC have a control mechanism of ensuring good quality

service? What needs to be answered is an assurance on whether the public can

place reliance on ZETDC and its ability to self correct the apparent deficiencies that

continue to clog it. Furthermore, management need to be assisted in identifying

areas of concern within their processes in order for the company to obtain the best

value and plug off the unpalatable services reaching the customers.

The research therefore seeks to evaluate the control systems in ZETDC and their

influences on the services obtaining from the utility company to the public customer.

1.3 RESEARCH OBJECTIVES

In pursuance of the above problem, the research therefore attempts to pursue the

following objectives;

23

PRIMARY OBJECTIVE

1.3.1 The primary objective of this research is to evaluate the internal control

systems in ZETDC

SECONDARY OBJECTIVES

1.3.1 To explore the effects of internal control breaches in ZETDC on

service delivery

1.3.2 To assess the influence of the internal control system on service

delivery

1.3.3 To identify challenges in implementing the internal control systems

1.3.4 To recommend ideal internal control practises

1.4. RESEARCH QUESTIONS

The research will seek to answer the following vital questions;

1.4.1 What are the internal control systems in ZETDC?

1.4.2 What are the effects of internal control breaches in ZETDC?

1.4.3 How is service delivery affected by the internal control systems?

1.4.4 What problems are faced in implementing internal control systems?

1.4.5 What can be done to improve the internal control systems?

1.5 RESEARCH PROPOSITION

The study maintains that ZETDC has an ineffective internal control system that has

resulted in poor service delivery.

1.6 SIGNIFICANCE OF THE STUDY

There is significantly little research that exists evaluating the internal controls that

ultimately give rise to the final products of companies more so at ZETDC, a vital

utility service provider in Zimbabwe. Management are increasingly facing

responsibilities through corporate governance pressure, to evaluate internal controls

and assess the potential risks.

24

The study intends to extend the knowledge of internal control systems, which is

established as an effective management tool through which an organisation

enhances its performance. The research will explore the essential elements of a

sound internal control system, drawing upon experience in established situations.

The significance of the research is to outline a number of principles for use by

supervisory authorities when implementing internal control systems. The study will

also assist in obtaining the internal control environment existing in ZETDC for the

sake of all stake holders, chief among them electricity customers. Furthermore,

researchers will benefit on possible further areas of study that may need more

probing.

1.7 SCOPE OF RESEARCH AREA

The Sampling Frame for the study will be ZETDC and the focus will be the period

existing from January 2009 and thereafter to 2012. This study will only address the

function of an internal control system in relation to commercial activities. Although

engineers also need to evaluate an internal control system in terms of its

effectiveness in assuring reliable operations, this is not the concern of this study.

1.8 DISSERTATION OUTLINE

There are five chapters in this study

Chapter 1

Gives the introduction and background to the study as well as outlining the area of

study. Also in this chapter is the problem statement, research objectives, questions,

scope and justifications of the study.

Chapter 2

Outlines the literature review on internal control systems defining and giving

concepts and basis on internal controls as well as challenges. It is the theoretical

framework of the study that draws conclusions from authoritative sources on internal

control systems.

Chapter 3

25

States the methodology for the research including the research design, sample

frame and the research instruments for the study as well as justification for the

research design.

Chapter 4

Presents and analyses results of the study as well as interpreting the findings there

of in relation to the underlying basis. Gives answers to the research questions.

Chapter 5

Concludes on the findings giving practical recommendations and areas needing

further studies

1.9 CHAPTER SUMMARY

In this chapter the events leading to the study were introduced. The overall subject of

study was also introduced and details outlined culminating in the problem statement

which was stated. Five objectives where identified and matched to the requisite

research questions. Also clearly stated was the research hypothesis and the

significance and justification of the study. The underlying scope was defined and the

overall research structure was outlined.

26

CHAPTER 2

LITERATURE REVIEW

2.1 INTRODUCTION

This chapter will demonstrate the theoretical framework of the study as highlighted

by various authors. The importance of literature review as explained by Dawidowicz

(2010) is to examine scholarly information and research based information to acquire

understanding of the topic under study of what has already been done, how it was

researched, and the key issues involved. The chapter seeks therefore to lay the

theoretical foundation of the study. The literature review will attempt to expose the

related areas that have not been explored significantly enough to draw conclusions.

2.2 INTERNAL CONTROL SYSTEM

2.2.1 WHAT IS AN INTERNAL CONTROL SYSTEM?

The current issue of the CPA (Certified Public Auditor) Exam review by Delaney and

Whittington (2012) define internal controls using the widely accepted American

Committee of Sponsoring Organizations of the Treadway Commission (COSO)

framework. This framework defines internal control system as noted by Chambers

and Rand (2011), as a process effected by the entity’s body of directors,

managements, and other personnel designed to provide reasonable assurance

regarding the achievement of objectives in the category of reliability of financial

reporting, effectiveness and efficiency of operations and compliance with applicable

laws and regulations.

A similar approach is followed by Collier and Agyei- Ampomah (2009) who define

internal control system as including all policies and procedures adopted by the

directors and management of an entity to assist in achieving their objectives of

ensuring , as far as practicable, the orderly and efficient conduct of a business

including adherence to internal policies, the safeguarding of assets, the prevention

and detection of fraud and error, the accuracy and completeness of the amounting

records and the timely preparation of reliable financial information.

27

A more comprehensive definition of internal control systems is the one by Menzies

(as cited in Mooler, 2008), who defines internal control systems as consisting of

regulations for the guidance of company activities (internal guidance systems) and

regulations for the supervision of these regulations (internal supervision system). He

however notes further that the internal supervision system consist of process-

integrated and not process oriented supervision activities.

Hopkin (2012) summarises definition from some of the major accounting bodies as

depicted in the table 2.1.

Table 2.1 - Definitions of Internal Control

ORGANISATION DEFINITION OF INTERNAL CONTROL SYSTEM

COCO (Criteria of

Control)

All the elements of an organisation that, taken together,

support people in the achievement of the organisation’s

objectives. The elements include resources, systems,

processes, culture, structure and tasks.

COSO A process, effected by an entity’s board of directors,

management and other personnel, designed to provide

reasonable assurance regarding the achievements of

objectives in the following categories;

• Effectiveness and efficient of operations

• Reliability of financial reporting

• Compliance with applicable laws and regulations

IIIA (Institute of

Internal Auditors)

A set of processes ,functions, activities sub systems ,and

people who are grouped together or consciously segregate to

ensure the effective achievement of objective and goals

Note; Adapted from Fundamentals of risk management: Understanding evaluating,

and implementing effective risk management (2nd Edition). (p.334). Hopkin. (2012).

Great Britain. Kogan Page Publishers.

It can be summed up that from the definitions in table 2.1 by Hopkin (2012) that

internal control system includes internal control activities and the structure and

responsibilities that relate to them.

28

The purpose of which is to enable directors to drive the organisation with confidence

in both good and bad times, safeguarding the organisation’s resources and ensuring

adequacy of records and systems accountability.

2.2.2 ELEMENTS OF INTERNAL CONTROL

Graham (2010) notes that the COSO internal control framework identifies five

components of internal control:

i. Control environment

ii. Risk assessment

iii. Control procedures

iv. Information and communication

v. Monitoring

This view is also supported by Delaney and Whittington (2012) who contend that

internal controls can be viewed as including five components mentioning those

alluded to in the COSO framework. Warren (2012) notes that elements of internal

control form an umbrella over the business to protect it from control threats. He

identifies five internal control elements that aim at achieving the internal control

objectives which tallies with those of Delaney and Whittington (2012) and the COSO

framework as noted by Graham (2010), as the control environment, risk assessment,

control procedures, monitoring, and information communication.

i) THE INTERNAL CONTROL ENVIRONMENT

The purpose of the internal control environment is to ensure consistence responses

to risks that materialises (Hopkin, 2012). Warren (2012) adds that the internal control

environment is the overall attitude of management and employees about the

importance of internal controls. On the other hand Hopkin (2012) describes it taking

from the COSO framework viewpoint as a measure of the risk culture within the

organisation whereas Rittenberg, Johnstone and Gramling (2011) sees it as referring

to the overall governance of the organisation starting by the tone developed at the

top level of the organisation.

29

However, Hightower (2008) views the internal control environment as including

statements that define and/or reinforce the tone from the top expressing value to the

company and authority to act. She emphasises that senior leadership within the

company must ensure there are suitable and consistent activities to support the

control environment such as communication, providing adequate resources and

time to implement, and holding process owners accountable and responsible for

process outcomes.

II) RISK ASSESSMENT

Understanding and management of the risk environment is a basic element of the

internal control foundation, and an enterprise should have a process in place to

evaluate the potential risk that may impact attainment of its objectives (Moeller,

2009). In making reference to the COSO framework Moeller (2009) describes risk

assessment as a three step process beginning with 1. Estimation of the significance

of the risk. 2. Assessing the likelihood or frequency of the risk occurring and 3.

Considering how the risk should be managed and assessing what actions must be

taken. (p. 39). Put differently Leitch (2008) notes that the objectives of risk control

are simply two fold. 1 to help people take off their mental blinkers and see the true

range of possibilities they face and 2, to help people behave competently in a way

that is consistent with that wider view.

III) CONTROL ACTIVITIES

Control activities are indicated as the policies and procedures that help ensure that

management directives are carried out (Dauber, 2009). They help ensure that the

necessary actions are taken to address risks to the achievement of the entity’s

objectives. However Hightower (2008) views control activities as specific actions

designed to produce evidence in support of the control objectives indicating that this

may include some or all of the following techniques:

• Self assessments performed by process owners using predefined self

assessment or audit readiness checklist

• Walk-through and observations performed by peer groups and/or internal

control representatives.

30

• Monitoring preformed by management and/or submitted to internal control for

review

• Reconciliation between source data and reporting records including period to

period roll forward and period over period analysis.

• Testing performed by management and internal control representatives using

statistical or random sampling techniques.

• Quarterly sub certification submitted by executive leadership, process owners

and selected business area executives attesting to compliance with company

policies, procedures, and internal control requirements.

• Remediation of action items resulting from internal control and internal audit

reviews.

(p. 45)

IV) INFORMATION COMMUNICATION

Needles, Powers, and Crosson (2010) view information communication as pertaining

to the accounting system established by management, to the way the system

gathers and treats information about the company’s transaction and how it

communicates individual responsibilities within the system. They argue that

employees must understand exactly what their functions are. This is aptly summed

up by Vilsanoiu and Serban (2010) whose view is that information and

communication requires that financial reporting information should have reliability

and should be communicated in a timely and accurate manner to managers and

decision makers. A more comprehensive view is proffered by Heintz and Parry

(2010) who contend that Information and communication system is the set of

procedures, processes and records used to initiate, process, record and report the

business transactions.

V) MONITORING

As internal control process is implemented, management should monitor the

operation of controls to provide assurance that all five components continue to

operate effectively (Rittenberg, Johnstone and Gramling, 2011). Ramos (2008)

emphasises that ongoing and separate evaluations enable management to

determine whether internal control over financial reporting is present.

31

He argues that internal control deficiencies are identified and communicated in a

timely manner to those partied responsible for taking corrective action, and to

management and the board as appropriate.

2.3 FORMS OF INTERNAL CONTROL SYSTEMS

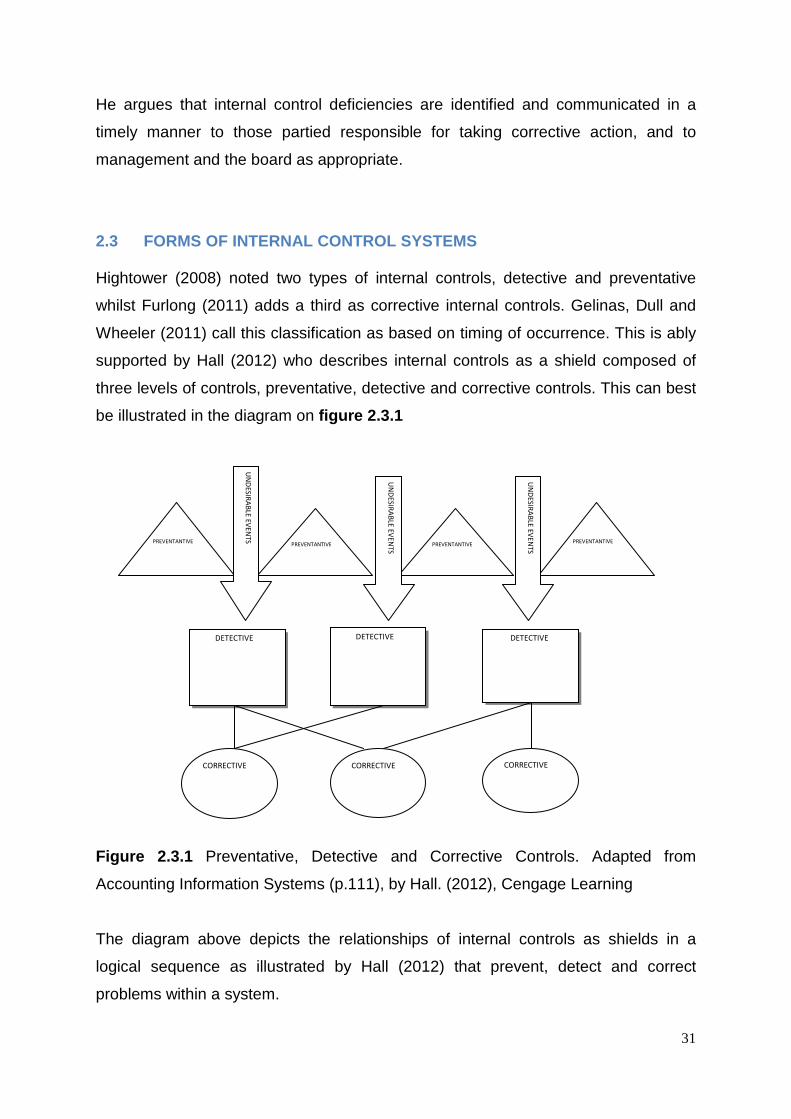

Hightower (2008) noted two types of internal controls, detective and preventative

whilst Furlong (2011) adds a third as corrective internal controls. Gelinas, Dull and

Wheeler (2011) call this classification as based on timing of occurrence. This is ably

supported by Hall (2012) who describes internal controls as a shield composed of

three levels of controls, preventative, detective and corrective controls. This can best

be illustrated in the diagram on figure 2.3.1

Figure 2.3.1 Preventative, Detective and Corrective Controls. Adapted from

Accounting Information Systems (p.111), by Hall. (2012), Cengage Learning

The diagram above depicts the relationships of internal controls as shields in a

logical sequence as illustrated by Hall (2012) that prevent, detect and correct

problems within a system.

PREVENTANTIVE PREVENTANTIVE

PREVENTANTIVE

PREVENTANTIVE

DETECTIVE DETECTIVE DETECTIVE

CORRECTIVE CORRECTIVE

CORRECTIVE

UN

DE

SIR

AB

LE E

VE

NT

S

UN

DE

SIR

AB

LE E

VE

NT

S

UN

DE

SIR

AB

LE E

VE

NT

S

32

2.3.1 PREVENTANTIVE CONTROLS

According to Hall (2012), preventative controls force compliance with prescribed or

desired actions and thus screen out aberrant events. He notes that when designing

internal control systems an ounce of prevention is most certainly worth a pound of

cure. Both Hightower (2008) and Furlong (2011) agree that these are controls that

are put into place to keep errors and irregularities from happening as simply stated

by Gelinas Jr, Dull and Wheeler (2011), that they stop problems from occurring.