Choice of Business Entity Jack Cohen, CPA Asset Protection IncSmart.biz Inc.

31

Choice of Business Entity Jack Cohen, CPA Asset Protection IncSmart.biz Inc

-

date post

19-Dec-2015 -

Category

Documents

-

view

216 -

download

0

Transcript of Choice of Business Entity Jack Cohen, CPA Asset Protection IncSmart.biz Inc.

Choice ofBusiness Entity

Jack Cohen, CPA

Asset Protection

IncSmart.biz Inc

Types of Entities

C CORPORATION

SOLE PROPRIETOR

S CORPORATION

PARTNERSHIPLLC

Identifying the Objectives Items To consider

What’s at Risk?

Tax SavingsAsset ProtectionManagementCapitalizationExit Strategies

Chances of IRS AuditF.Y. 06

Form 1040 Sch. ‘C’ > $100,000 = 3.90%1120 < 10 Mill. Assets = .80%1120-S = .38% 1065 = .36%

Tax Savings

Income Tax

Payroll Taxes

Self Employment

Gift and Estate Taxes

Asset Protection From:

Business Activities Risk

Management Actions

Employee Actions

Management

Will management be expanded?

How will management disputes be resolved?

How will they be compensated? Equity participation Compensation Additional fringe benefits

Capitalization – What Form Should it Take?

Initial Capitalization

Debt Bank loans Home equity loans Family and friends

Equity Corporation- stock Partnership- partner interest Limited liability company- member

interest

DebtPros Interest tax deductible No ownership dilution Flexible rates and terms Increases return on equity Establishes credit ratingCons Personal guarantees Monthly periodic payments

EquityPros Minimum cash outflows Ease of transfer Large source of capitalCon Ownership dilution

Tax Tip

On corporations capitalize for the least amount possible.

Have company “borrow money” from you.Example

$1,000 Stock$99,000 Loan

$100,000 Total Capital

Exit StrategiesCompany

Stock redemptions

Competitor

Merger

Acquisition

Asset sale

Stock sale

Family members

Gifting

Death transfers

Acquisition

Management

Management buy-out (MBO)

Management buy-in (MBI)

Proprietorships – Non Tax Considerations

Simplicity of form

Unlimited personal liability

Continuity of existence and transferability of ownership

Limited ownership

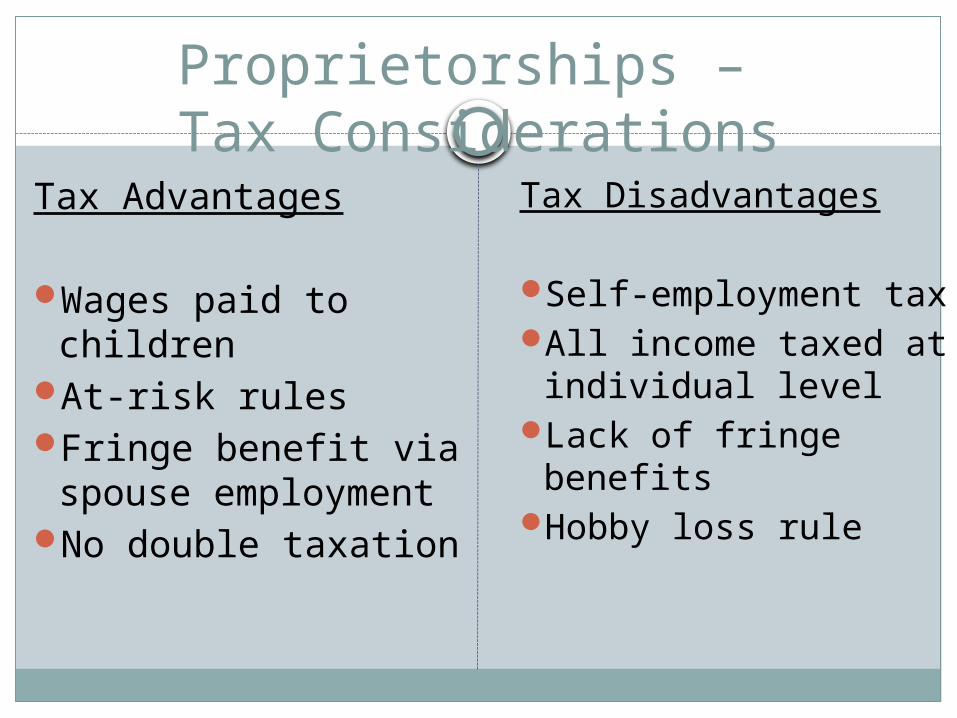

Proprietorships – Tax Considerations

Tax Advantages

Wages paid to children

At-risk rulesFringe benefit via

spouse employmentNo double taxation

Tax Disadvantages

Self-employment taxAll income taxed at

individual levelLack of fringe

benefitsHobby loss rule

Proprietorships – Taxation

Tax rate depends on filing statusNo withholding requirements15.3% self-employment taxTotal net income determines income tax & Social

Security liabilitiesFile Schedule C with 1040: Business profit & loss

Taxation of LLCSingle Member LLC: Disregarded Entity

Rev Ruling 99-5; 99-6 SMLLC – Husband or Husband & Spouse Reported on Form 1040 Can not have any other unrelated owner

“Check the Box” Rules Partnership taxation is default (minimum two members) May choose to be taxed as a corporation

S Corp or C Corp

Real Estate Tip

For Maximum Asset Protection Separate SMLLC for each property.

Put Real Estate in SMLLC.

Partnership – Formation Issues

Partnership agreement or operating agreement Buy/Sell agreement Contributions of Assets Limited Life Liability Issues LLP vs. General Partnership

Partnership – Tax Considerations

Tax AdvantagesTax basis from debtBasis adjustment when

partnership interest acquired

Tax-free contributions and distributions of property

Ability to make special elections

No entity level of tax

Tax DisadvantagesInability to reduce payroll

taxesUnfavorable tax treatment

of fringe benefitsLack of flexibility to select

a tax year endTechnical Termination

Partnership Taxation – Summary

IRS Form 1065Generates K-1No “double taxation”Self-employment taxInformational tax return: entity does not pay taxTaxed at partner levelIncome is taxable for FICA

S Corporation – Tax Considerations

Tax AdvantagesNo double taxationPass-through to shareholdersNo excessive compensationAbility to reduce payroll taxesAbility to use cash methodTax-free withdrawals of equityPossible ordinary loss

treatment for stock losses

Tax DisadvantagesFringe benefitsTax year-endBuilt-in gains taxExcess passive incomeBasis is reduced even if

no tax benefit

‘S’ CorporationWho Can Be Shareholder?

U.S. citizenEstatesSingle Member LLC 501 (c) (3) CharitiesQualified Pension plansQualified Profit Sharing plans

‘S’ CorporationWho Can not Be shareholder?

CorporationsPartnershipsLLC’s (not SMLLC)IRA’S & Roth’sSep IRA’s & SIMPLE IRA’sNon-Resident Aliens

S Corporation Taxation – Summary

Must make election: Form 2553Files Form 1120-SGenerates K-1Informational returnTaxed at shareholder levelIncome tax only on proportionate share of income:

No FICANo corporate tax on sale of assets or liquidation

Partnership vs. S Corp– Treatment

Social Security

General partners pay FICA on K-1 income

Shareholders S Corp K-1 income: no FICA

Social SecurityHow Much Does Sub ‘S’ Owner Pay?

In 2000 78.9% of ‘S’ - more than 50% owned by single shareholder.

Compensation To be Reasonable36,00 taxpayers > $100,000 profits = 0

compensation.2001 – Owner salaries 41.5% of operating profits.2000 – ‘S’ corporations paid 5.7 billion less than if

sole proprietors

Partnership vs. S Corp – TreatmentDistributionsPartnership:

disproportionate distributions allowed

S Corp: no disproportionate distributions

Ownership InterestS Corp: ownership restrictedNo more than 100 shareholdersIndividuals, estates, certain

types of trustsNo foreign shareholdersOnly one class of stock allowedPartnership: no restrictions

C Corporations – Non Tax Considerations

Limited liabilityAdministrative burdenManagement and controlContinuity of existence and transferability of

ownership

C Corporations – Tax Considerations

Tax AdvantagesLower tax rates at

many income levelsNet income not

subject to Social Security

Takes maximum advantage of fringe benefit deductions

Tax Disadvantages

Double taxation of corporate earnings

Excessive compensationPersonal service corporate

limitationsPersonal holding company

accumulated earnings tax- penalty taxes

Limitations caused by corporate ownership changes

C Corporation – Employee Benefits

SalariesReasonable salariesGarnishment limitations

Medical benefitsMedical reimbursement plansHealth savings accounts

Retirement benefitsEducational benefitsOther benefits

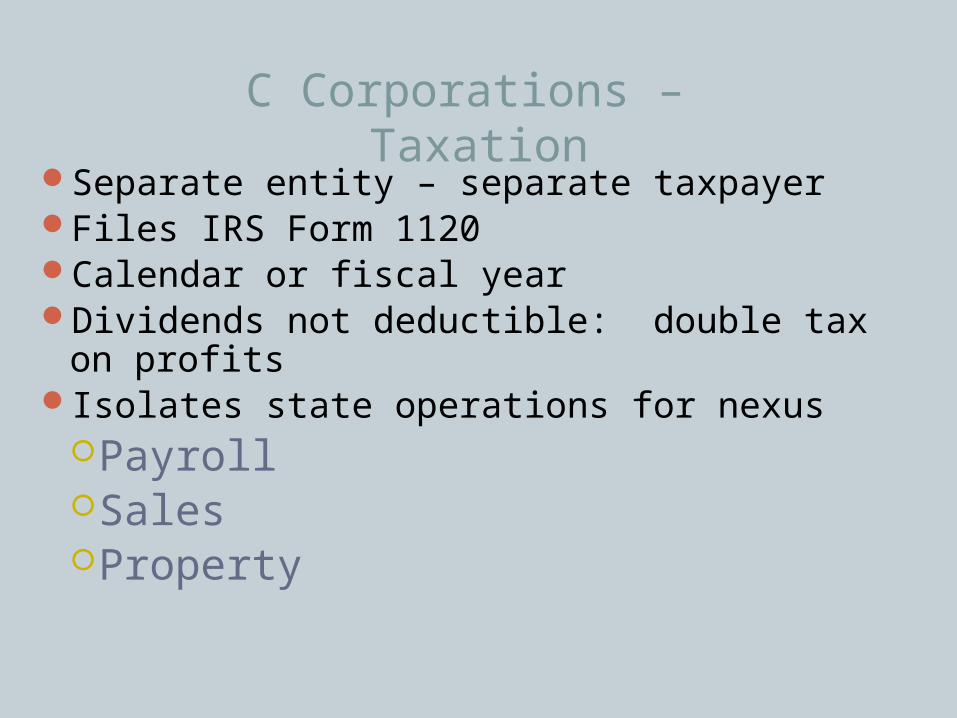

C Corporations – Taxation

Separate entity – separate taxpayerFiles IRS Form 1120Calendar or fiscal yearDividends not deductible: double tax on profitsIsolates state operations for nexus

PayrollSalesProperty

Proprietorship

S Corporati

on

C Corporat

ion

Business Income $90,000 $90,000 $90,000

W-2 Income - $45,000 $45,000

Net Business Income

$90,000 $45,000 $45,000

Corporate Tax $ - $ - $6,750

Personal Tax $10,136 $11,736 $3,564

FICA & Medicare $12,718 $6,885 $6,885

TOTAL TAXES $22,854 $18,621 $17,199

MFJ, SD, & Expt

Making the Decision

THANK YOU

For more information, visithttp://incsmart.biz