China - Peoples Republic of Cotton and Products Annual GAIN Publications/Cotton...continue to...

23

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Date: GAIN Report Number: Approved By: Prepared By: Report Highlights: MY14/15 forecast planting area of 4.41 million hectares (MHa) and production of 6.5 million tons are both down from last year as a support policy change lessens incentives for planting. Government cotton purchases over the past three years have built domestic stocks to a record high 12.3 million tons through MY13/14 which, when coupled with weak consumption growth of 8.2 million tons, further reduces demand for imports which are expected to fall to 1.8 million tons in MY14/15. The U.S., with 1.3 million tons of cotton exported to China in MY12/13, was China's top supplier but faces increasing competition from India and Australia. M. Melinda Meador and Wu Xinping Michael Riedel Cotton and Products Annual China - Peoples Republic of CH14015 4/1/2014 Required Report - public distribution

Transcript of China - Peoples Republic of Cotton and Products Annual GAIN Publications/Cotton...continue to...

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY

USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT

POLICY

Date:

GAIN Report Number:

Approved By:

Prepared By:

Report Highlights:

MY14/15 forecast planting area of 4.41 million hectares (MHa) and production of 6.5 million tons are

both down from last year as a support policy change lessens incentives for planting. Government cotton

purchases over the past three years have built domestic stocks to a record high 12.3 million tons through

MY13/14 which, when coupled with weak consumption growth of 8.2 million tons, further reduces

demand for imports which are expected to fall to 1.8 million tons in MY14/15. The U.S., with 1.3

million tons of cotton exported to China in MY12/13, was China's top supplier but faces increasing

competition from India and Australia.

M. Melinda Meador and Wu Xinping

Michael Riedel

Cotton and Products Annual

China - Peoples Republic of

CH14015

4/1/2014

Required Report - public distribution

China’s official cotton market information collection system covers cotton and yarn production,

however, the lack of reliable data (production, consumption, and stocks) has been more pronounced in

recent years due to the rapid expansion and diversified scales of production. The numerous players

continue to diversify ownership in the industry chain, including the large number of cotton farmers, gins,

merchants and mills. All these entities contribute to making the collection of reliable production

statistics in China an extremely difficult task.

Executive Summary:

MY14/15 forecast planting area of 4.41 million hectares and production of 6.5 million tons are 7.1

percent and 6.2 percent down, respectively, over the estimated 7 million tons and 4.7 MHa last year. A

change in government support policy for cotton is widely expected to lower farmer payments and

financial incentives for planting. The government’s new cotton production support policy for MY14/15

narrows eligibility to Xinjiang farmers only and pays a direct subsidy based on a target price instead of

price support purchases. In MY14/15, these program changes are expected to prompt a reduction in

cotton planting intentions, particularly in Yangtze and Yellow River regions, due to the loss of

government production support altogether and the option of more profitable, alternative crops.

Government cotton crop purchases at record prices over the past three years have built domestic stocks

to a record high 12.3 million tons through MY13/14. MY 13/14 cotton consumption is forecast at

recover slightly to 8.2 million tons from an estimated 8.04 million tons in MY13/14. China’s ability to

manipulate domestic supply resources through state reserve auctions and tariff rate quotas continues to

impact import demand. The U.S., with 1.3 million tons of cotton exports to China in MY12/13, was

China's top supplier but faces increasing competition from suppliers like India and Australia as China's

imports fall to a projected 1.8 million tons in MY14/15.

Production

MY14/15 domestic production will fall to 6.5 million tons based on planted area of 4.41 MHa, both

down 7.1 percent and 6.2 percent, respectively, over the estimated 7 million tons and 4.7 MHa in the

previous year. A recent change in MY14/15 government policy that supplants a nation-wide price

support policy with a narrower eligibility pool and direct payments based on a target price has lowered

overall profit expectations.

China's policy change reflects a reassessment of its measures to encourage production through ensuring

positive returns by paying artificially high prices to cotton farmers. In retrospect, as a result of this

support policy, the government has absorbed vast expenses for handling and storage, the textile industry

has endured inflated, above market cotton costs and in return, the policy returns in cotton acreage and

production gains have been negligible. Going forward, instead of purchasing cotton at a high floor price

in all cotton-producing regions, the government will provide a direct subsidy based on a target price

only to Xinjiang farmers. Without the government support payments, farmers in the Yangtze and

Yellow River production regions are expected to switch to alternative crops, thus decreasing overall

cotton acreage and production.

Estimates of China’s total cotton production (area and yields) continue to differ among sources. For

MY13/14 example, China’s National Statistics Bureau (NSB) estimates MY13/14 production at 6.31

million tons based on planted area of 4.35 MHa with yields of 1,450 Kg/Ha. Industry sources, however,

estimate MY13/14 production at around 7 million tons, believing Xinjiang planted area remains under-

reported. Further clouding the forecast picture, statistics based on official classification data could be

skewed by the repeated classification of domestic cotton or even classification of imported cotton (to

take advantage of the price difference between imported and domestic cotton). Adding to the difficulty

in accurately forecasting production with data inconsistencies, the changes in government policy for

MY14/15 also muddy the profit picture and impair accurate forecasting by province. Nevertheless,

below is a table of estimates by various sources for MY13/14 and MY14/15 production.

For Xinjiang, in mid-January, the Xinjiang government released estimates that MY13/14 cotton

production was 3.4 million tons (based on planted area of 1.57 MHa, both up slightly by 45,000 Ha and

20,000 tons over the previous year). This figure is significantly below the China Fiber Inspection

Bureau (CFIB) classified volume for Xinjiang, as of March 16th, of 4.68 million tons (out of the

nation’s total 7.28 million tons). (See table 10 and more in GAIN CH10033 on inconsistencies in

Xinjiang’s reported planted area).

For the eastern production regions, MY13/14 production data bears additional explanation. CFIB data

shows MY13/14 classified volume for Henan at 75,000 tons (as of Mid-March). However, industry

sources suggest that a portion of Henan production is likely being reported under Shandong and Hubei

province volume. Large traders/mills purchase seed cotton in Henan which is baled and classified in

Shandong/Hubei provinces and reported under their production figures. Additionally, MY13/14 Hubei’s

stable production seems to be supported by improved profits received in the previous year. Based on all

these factors, Post adjusted MY13/14 production estimates for these provinces accordingly.

The following table reflects production estimates/forecasts for MY13/14 and MY14/15 by major

industry source.

Cotton Production Estimate/Forecast by Various Sources (million tons)

CCA NCMMN CNCE CAAS NSB Post

MY13/14 production 7.0 6.99 6.85 7.0 6.31 7.0

MY14/15 area change -10.5% -14.2% -10% -10.7% -7%** -6.2%

MY14/15 Production NA NA NA NA NA 6.5

[CCA- China Cotton Association, NCMMN- National Cotton Market Monitoring Network,

CNCE- China National Cotton Exchange, CAAS- China Academy of Ag Science]

(**MOA March intention survey results)

Planted Area

Cotton planted area is expected to continue its downward trend as rising production costs, variable

profits and alternative crops influence planting decisions. Post forecasts MY14/15 cotton planted area

will fall to 4.41 MHa from an estimated 4.7 MHa last year.

The Ministry of Agriculture (MOA) estimates MY14/15 planted area will decrease by 7 percent over the

previous year based on its March planting intention survey on farmers.

In addition, a China Academy of Agricultural Science Cotton Research Cotton Institute (CAAS)

January forecast shows a 10.7 percent fall in MY14/15 cotton planting to 4.37 MHa, a drop from its

estimated area of 4.9 MHa in MY13/14, with the Yangtze River region down 12.1 percent, the Yellow

River region down 17.4 percent, and the northwest region down 4.9 percent (with north Xinjiang down

5.8 percent, south Xinjiang down 4.8 percent).

A recent China Cotton Association (CCA) survey also indicates MY14/15 cotton planting intention will

decline by 10.5 percent over last year to 4.17 MHa. The survey showed the Yellow River planting

intentions were down 22 percent with Henan, Shandong both down more than 20 percent and Hebei

down 29 percent as higher profits to competing crops pull acreage from cotton. For example, farmers

planting both wheat and corn had a profit of RMB6, 600/Ha in Shandong compared to farmers planting

cotton who had a negative profit in MY12/13 (chart 2).

More recently, the National Cotton Market Monitoring Network (NCMMN) released a March 27th

forecast that MY14/15 planted area will be down by 14.2 percent to 4.13 MHa and readjusted its

MY13/14 production data to 6.99 million tons. A China National Cotton Exchange (CNCE) forecast

agrees that MY14/15 cotton area will fall by 10 percent over the previous year.

Similar to the national experts, local industry forecasts also show varying forecasts. In Yiyang/Hunan,

farmers expect a 13.3 percent decline in cotton planting intention in MY14/15 following comparatively

low profit as drought and typhoon conditions lowered yield and quality in the previous year. Farmers in

Heze and Liaocheng/Shandong province expect cotton planting intentions to be down 7.7 percent and

25 percent, respectively, in MY14/15.

(See Table 10 for details)

Chart 1- China Cotton Planted Area and Production

(2011-2014, in MHa and million tons)

Source: FAS/Beijing)

In MY13/14, low yield, labor shortages and low profits in both the Yellow River rand Yangtze River

regions further eroded cotton prospects. The withdrawal of government price support in MY14/15 is

expected to further accelerate an eastern region planting decline, as indicated in Chart 2, and exacerbate

profit and labor issues.

For the northwest, the Xinjiang Development and Reform Commission reported a 3 percent decline in

cotton planting intentions in MY14/15 due to uncertainties following changes in government support

policy. Post forecasts, though, that MY14/15 planted area will remain stable at 2.2 MHa. A record of

positive profits, which peaked in MY10/11 due to a surge in world prices, has continued strong at

RMB8,550 (or $1,357)/Ha in MY11/12 and RMB8,820 (or $1,420)/Ha in MY12/13. Furthermore, the

government has reportedly purchased a majority of Xinjiang’s relatively high yielding MY 13/14 crop

(4.6 million tons as of March 9) at above world market prices (RMB20, 400 or $3,290). Thus, Xinjiang

cotton farmers are expected to continue their profitable record which should keep planting intentions

high for MY14/15.

Chart 2 - Comparison of Average Net Profit from Cotton Planting

(2009-2012; RMB/Ha)

Source: NDRC

Yield

China’s average cotton yield varies significantly by individual province/autonomous region, ranging

from 976Kg/Ha in Anhui to 1,815Kg/Ha in Xinjiang (see Chart 3). Overall, MY14/15 cotton yield is

forecast above average at 1,474Kg/Ha with Xinjiang yield forecast at 1,909 Kg/Ha. MY13/14 cotton

yield averaged 1,450 Kg/Ha (NSB total production divided by planted area), with Xinjiang's yield

topping 2,009Kg/Ha, according to the Xinjiang Agricultural Working Conference Report.

Chart 3 – NSB Yield by Province

(Kg/Ha; MY08/09 to MY12/13)

1,815

1,061 1,006 1,039 991 9761,106

1,382 1,3641,283

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Source: NSB

Yellow River provinces of Henan, Hebei, Shandong, and Anhui Provinces could potentially see 100

percent use of Bt variety cotton in the near future which reduces pest-related yield losses. Weather

uncertainties in the Yangtze River and Yellow River region though continue to impact yields.

In Xinjiang’s dry climate, Bt cotton is less prevalent due to fewer pests. Conventional varieties with

specific traits, such as dwarf plant size and early maturity, continue to raise yields in Xinjiang. The

Xinjiang Production and Construction Corp (PCC) farms, which are organized on a larger scale than

other typical cotton farms, incorporate particular agronomic practices, such as high density sowing,

plastic sheet covering, and drip irrigation technology, to improve yields.

Stocks

Government purchases of more than 6.24 million tons of the MY13/14 cotton crop (as of March 24)

raises state-held reserves to a record level approaching 12.3 million tons at the end of MY13/14, a

sizeable increase from an estimated 11 million tons of beginning stocks.

Post forecasts ending stocks could reach 12.4 million tons at the end of MY14/15, depending on the

consumption recovery rate and the price gap between the domestic and world market. The stock to use

ratio remains high at above 150 percent in MY13/14 and 14/15.

Record high stock levels prompted recent government auctions of state reserve cotton but the response

has been lackluster. As of March 24th, the government had only sold 715,000 tons of reserve cotton,

roughly 39 percent of the volume offered for sale at RMB18,000/ton. This reaction reflects stagnation in

cotton demand and/or an unwillingness by the textile sector to pay the inflated price. In an attempt to

stimulate purchases, the government will lower the state cotton release price from RMB18, 000/ton to

RMB17, 250/ton (Grade 328) beginning April 1st, according to the China Cotton Association.

Cotton Trade

Note: Annual import volume is controlled by the government through a tariff rate quota (TRQ) system.

This policy facilitates the government's ability to regulate the supply of cotton imports.

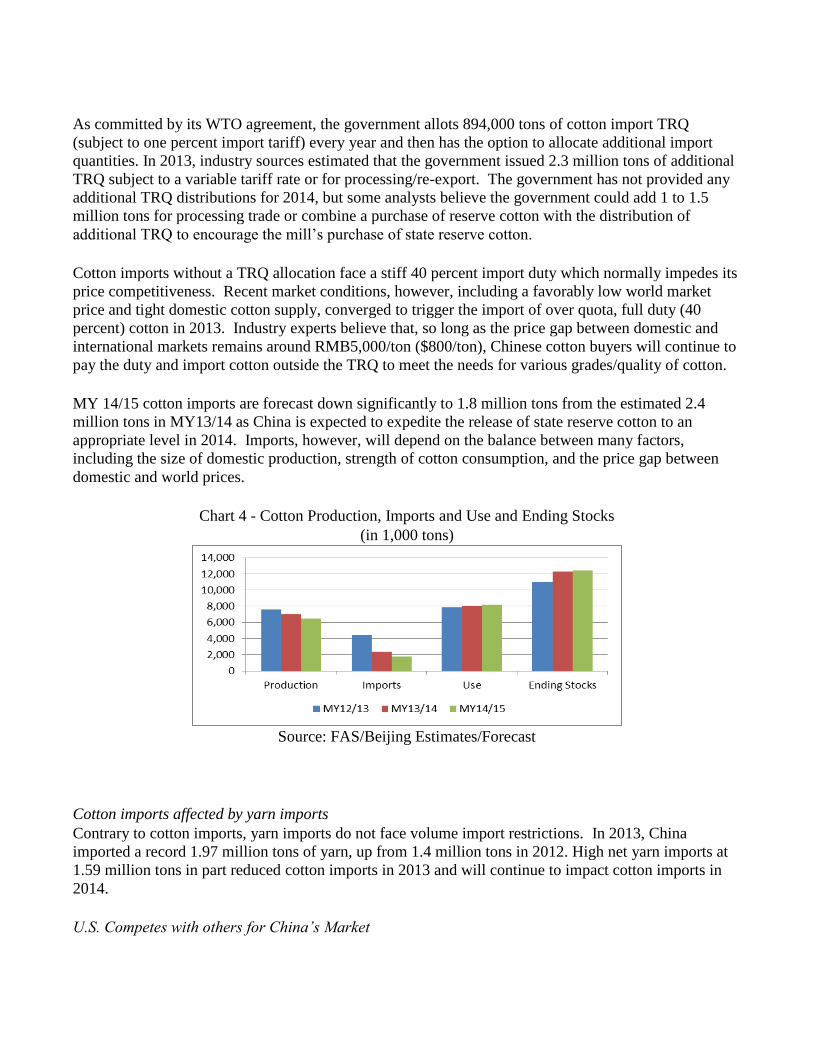

As committed by its WTO agreement, the government allots 894,000 tons of cotton import TRQ

(subject to one percent import tariff) every year and then has the option to allocate additional import

quantities. In 2013, industry sources estimated that the government issued 2.3 million tons of additional

TRQ subject to a variable tariff rate or for processing/re-export. The government has not provided any

additional TRQ distributions for 2014, but some analysts believe the government could add 1 to 1.5

million tons for processing trade or combine a purchase of reserve cotton with the distribution of

additional TRQ to encourage the mill’s purchase of state reserve cotton.

Cotton imports without a TRQ allocation face a stiff 40 percent import duty which normally impedes its

price competitiveness. Recent market conditions, however, including a favorably low world market

price and tight domestic cotton supply, converged to trigger the import of over quota, full duty (40

percent) cotton in 2013. Industry experts believe that, so long as the price gap between domestic and

international markets remains around RMB5,000/ton ($800/ton), Chinese cotton buyers will continue to

pay the duty and import cotton outside the TRQ to meet the needs for various grades/quality of cotton.

MY 14/15 cotton imports are forecast down significantly to 1.8 million tons from the estimated 2.4

million tons in MY13/14 as China is expected to expedite the release of state reserve cotton to an

appropriate level in 2014. Imports, however, will depend on the balance between many factors,

including the size of domestic production, strength of cotton consumption, and the price gap between

domestic and world prices.

Chart 4 - Cotton Production, Imports and Use and Ending Stocks

(in 1,000 tons)

Source: FAS/Beijing Estimates/Forecast

Cotton imports affected by yarn imports

Contrary to cotton imports, yarn imports do not face volume import restrictions. In 2013, China

imported a record 1.97 million tons of yarn, up from 1.4 million tons in 2012. High net yarn imports at

1.59 million tons in part reduced cotton imports in 2013 and will continue to impact cotton imports in

2014.

U.S. Competes with others for China’s Market

In MY12/13, the United States resumed its status as the number one cotton supplier to China with total

export volume of 1.3 million tons, followed by India and Australia with export volume of 987,000 tons

and 887,000 tons, respectively. While the quality and reliability of U.S. cotton appeals to China’s end-

users, India’s price and transportation advantages provide serious competition. India’s cotton

production is expected to increase as it incorporates new technology, expands Bt cotton dissemination

and actively promotes its product. Competition from India and other suppliers, coupled with expected

low demand for imports, is expected to reduce demand for US cotton exports to China in MY13/14 and

MY14/15.

Consignment Trade

Due to strong demand for alternatives to high-priced domestic cotton since late 2011, consignment trade

has been on the rise. China’s small to medium-sized mills choose consignment purchases due to the

flexibility they offer, including short delivery time, convenient quality verification and lower financial

commitment. However, due to the lack of import TRQ, most mills pay the full duty to take delivery of

the cotton on consignment being held in bonded warehouses. Consignment trade is expected to remain a

viable source until the world cotton price changes making the cost of import plus full duty unattractive

for Chinese mills. Industry sources indicated as of the end of February, total cotton in the bonded zone

of Qingdao and Zhangjiagang/Jiangsu ports was about 205,000 tons.

Cotton exports insignificant

China’s cotton exports average about 10,000 tons annually, insignificant compared to total cotton use.

Yarn exports increased slightly to 387,000 tons, making net yarn imports 1.59 million tons in 2013

showing a significantly rise from 500,000 tons in 2011.

Consumption

MY14/15 cotton consumption is forecast at 8.2 million tons, up from an estimated 8 million tons in

MY13/14. Although demand from developed markets, like the US and EU, remains sluggish due to

recovering economic performance, strengthening demand from developing countries, and especially

China, raises expectations for consumption of apparel and textile products.

On the other hand, industry experts anticipate that the share of synthetic fibers and other fibers in cotton

yarn production may continue to rise in 2014 due to high domestic cotton prices while the price for

synthetic fiber may remain relatively low and competitive. Historically, the price of cotton fiber runs

approximately 20 percent higher than that of synthetic fiber. According to NSB, total chemical fiber

production in 2013 was 41.22 million tons, up 7.9 percent over the previous year.

China's Textile Sector Production/Investment Trends

Year/Item 2010

2011

2012

2013

2013/2012

Change %

Yarn Production (million tons) 27.17 28.7 29.84 32.0 +7.2

Fabrics Production (Million Meters) 800 814 841 883 +4

Chemical Fiber Production (million tons) 30.9 33.9 38 41.2 +7.4

Fixed Asset Investment in Textile Sector (RMB billion) 257 366.9 397.1 NA NA

Source: China Economic and Social Development Report by NSB

(Exchange Rate: 2012-$1=RMB6.3; 2013-$1=RMB6.2)

New Challenges for textile sector impact cotton use

The textile industry in China employs over 23 million people and is considered an economic pillar

industry. In China’s 12th Five Year (2011-2015) Plan, the government confirmed its support to

upgrading this sector. According to NSB, while fixed asset investment in the textile industry in 2012

reached $64 billion, up 8 percent over 2011, this figure is significantly lower than the 30.9 percent

growth in 2011. The investment value in 2013 is not available, but NSB indicated that the fixed asset

investment in general manufacturing industry increased by 18.5 percent over the previous year. Total

profit for the sector in 2013 increased 15.8 percent over 2012. The sector’s marketing profit margins

averaged 5.5 percent, up slightly (0.2 percentage) over the previous year.

Despite this financial influx, the textile industry faces significant challenges, including declining orders

from overseas, appreciating Chinese currency and rising production costs for key inputs such as raw

materials and labor. Industry statistics show that in 2013 mills paid more than RMB 4,000/ton ($645)

above the world price for domestic cotton.

In addition to high prices for raw materials, Chinese Ministry of Labor indicated 27

provinces/municipalities adjusted the minimum wage level in 2013 with average growth up by 18

percent over the previous year. High electricity price coupled with environmental pressure (emission

limit) not only adds to production costs, but also inhibits facility expansion.

To address these ongoing hurdles, textile industry leaders use different approaches. Some mills are

improving efficiency and productivity to maintain profits. Others have moved operations towards

China’s central and western regions (Henan, Sichuan, Anhui, Jiangxi, Xinjiang and Ningxia Provinces)

and foreign countries (Vietnam and Cambodia etc.) in search of lower raw material/labor inputs and a

favorable investment climate. For example, China’s industry reported the construction of a 150,000 ton

annual spinning capacity project in North Carolina in February which is expected to be operational in

October 2014. A Zhejiang Textile Group began a $136 million spinning investment in Vietnam at the

end of 2013 that is expected to reduce costs in raw material, labor, logistics and duties, and facilitate

access to Southeast Asian Markets. China’s industry associations are also organizing trips to Southeast

Asia countries for talks on textile investment.

Recovery of exports support moderate growth of cotton use

According to NSB, total textile and apparel exports were valued at $283.9 billion in 2013, up 11.4

percent over the previous year. Specifically, textile export value increased by 11.7 percent to $106.9

billion, and apparel export value increased by 11.3 percent to $177 billion, both figures reflecting

growth rates in excess of those in 2012. Although total textile and apparel export value in the first two

months of 2014 fell slightly (by four percent) over the previous year (mainly due to China’s Spring

Festival vacation, analysts reported), China’s industry experts remain optimistic regarding export

growth prospects in 2014 given a moderate recovery of overseas markets and lowering of domestic

cotton price due to policy changes.

Chart 5 - Textile and Apparel Exports (Value in $100 million)

Source: NSB

Domestic demand support cotton use

According to the China Textile Industry Association (CTIA), the domestic market accounted for more

than 83 percent of the sector’s total sales value in 2012. However, the general sales trend remained

weak in 2013. The estimated low cotton use of 8.04 million tons in MY13/14, however, is expected to

rebound to a forecast 8.2 million tons in MY14/15. In addition to an anticipated fall in cotton prices,

and constant high GDP growth of 7.7 percent in 2013 and likely 7.5 percent in 2014, higher disposable

income and rising living standards of Chinese consumers are driving retail consumption to the benefit of

cotton products. For example, as indicated in Chart 6, the 2012 per capita expenditures on clothing

increased for both urban and rural residents, with urban resident’s still far outspending rural

counterparts. High urbanization is expected to continue in 2014 (with newly added urban residents at

19.29 million in 2013). The market potential for China’s 629.6 million rural residents to increase textile

related purchases is expected to rise as rural incomes grow as well. This will support continued demand

for domestic cotton products.

Chart 6 - Per Capita Expenditures on Clothing

By Urban and Rural Resident (in RMB/year)

Source: NSB

Misreporting of yarn categories and volume continue

A long standing problem in consumption forecasting is the lack of reliable data to connect cotton

consumption data with finished product numbers. For example, according to NSB, total yarn

production for 2011 was reported at 29 million tons, of which 22 million tons (accounting for 75.4

percent) was reported as pure cotton yarn, with the remainder as blended yarn and synthetic yarn. These

figures are problematic when compared to China’s average cotton consumption of 10 million tons

annually in recent years, plus other fibers available for spinning, which cumulatively cannot produce the

volume of yarn as reported. Over-reporting of total yarn and pure cotton yarn production and under-

reporting of synthetic fiber ratios and cotton consumption, or some combination thereof, distorts

accurate analysis. China’s industry insiders acknowledge misreporting of yarn categories and volume

by mills is the basis of the problem.

Policy

Domestic cotton support policy amended

The State Purchase of Domestic Cotton Program, established three years ago to boost income and

stimulate production through fixed price supports and the cotton TRQ regime (sliding scale and

processing scale quotas) are government programs enacted to maintain domestic cotton supply/demand

balance. The minimum cotton purchase price for domestic cotton started at RMB19, 800/ton in

MY11/12 and rose to RMB20, 400/ton in MY12/13 and MY13/14 (approximately $3,100-3,300 per

ton). During this same period, world cotton prices declined significantly to an average $2,000/ton in

2014 (based on Global Trade Atlas/China import price), far below the internal cotton price set by the

government. The inflated domestic price depressed consumption of domestic cotton thus forcing the

government to purchase the majority of the MY12/13 crop. This massive purchase added 6.46 million

tons of expensive cotton to state reserve storage facilities. In MY13/14, the government purchased

another 6.24 million tons (as of March 24, out of estimated 7 million tons total production in MY13/14)

which will push state reserves levels to a record high 12.3 million tons by the end of MY13/14. The

policy resulted in an unsustainable situation with huge government stocks and limited stimulus to cotton

production.

In 2014, China’s government announced an adjustment in this policy to transition toward less market

distortion and government intervention. Beginning in MY14/15, only Xinjiang cotton farmers will

receive an acreage based subsidy based on a target price (which would exceed world price). The

nationwide fixed purchase price policy will be eliminated.

As of this report, the government target price for cotton remains unknown although information

suggests it will be RMB19, 400/ton. In general, this policy change will have limited impact on Xinjiang

cotton planting intention based on analysis of production costs and yield expectation in this region, but

is likely to reduce planting intentions in other cotton-producing regions where alternative crops are an

option.

As such, China’s total cotton planting area is expected to shrink in the short term (due to the

government’s significant stocks, a moderate small crop in next few years is desirable for policy makers).

However, as an NDRC official hinted, the government’s resumption of the state purchase program is

possible in the future if the government deems it necessary.

Over the next two years, government decision makers will be deciding whether a Xinjiang only support

policy will produce sufficient cotton for domestic needs while staying consistent with its policy of

having imported cotton primarily the domain of textile use for export. Policy leaders are unlikely to

accept a situation where a regionalized support policy puts domestic needs and government stock levels

into a position where they could be perceived to be vulnerable to imports.

Seed Subsidy

Large seed producers/traders currently compete for the $34/Ha subsidy provided for selected “high

quality variety” seeds to improve quality cotton coverage. Total expenditure in 2013, though

unpublished, is believed to exceed $155 million (if based on the NSB’s 5.04 MHa planted area for

MY13/14).

Registration System for Overseas Cotton Suppliers

Overseas cotton suppliers must be registered with China’s General Administration of Quality

Supervision, Inspection and Quarantine (AQSIQ) to export cotton to China (CH8075 and CH9004). On

January 18, 2013, AQSIQ published Decree No.151 on "Supervision and Administration Measures for

Inspection of Import Cotton." The measures took effect on February 1, 2013. Preliminary comparison

between the draft and final versions shows only slight modifications in Article 26 (CH13003). The

impact of the Measures on cotton trade is expected to be limited.

Traders are also recommended to register with AQSIQ to export cotton to China based on these

requirements. AQSIQ keeps updating the newly registered or renewed overseas cotton supplier list on

its website with the latest dated on December 13, 2013. Post received no complaints on this

registration.

Official cotton classification

According to CFIB, as of March 16, 2014, total cotton baled and classed under the new classification

system has reached 7.28 million tons, up from 5.56 million tons in MY11/12. The government

requirement that only classified cotton qualifies for its purchase support program is stimulating the

increase in classified cotton. Although the intent behind requiring classification was to simultaneously

upgrade the quality of China’s ginning sector and facilitate the collection of production data, the reality

is not so clear cut. Industry sources report that some cotton may be presented repeatedly for

classification and purchase and even some imported cotton may also be presented for classification to

take advantage of the import/domestic price difference. The inclusion of multiple repeat purchases or

imported cotton skews the overall production data. The new purchase program for MY14/15 is expected

to eliminate some problems in that without the government purchase program, mills may not request

ginners to provide official classification data.

Targeted Loans

In MY13/14, the Agriculture Development Bank of China (ADBC) continued to provide targeted loans

with favorable terms for the purchase of seed cotton. This program facilitated the marketing of seed

cotton when market prices remained weak and demand for cotton was stagnant. Xinjiang government

information indicated that total loans exceeded RMB66.3 billion in My13/14, up RMB5.7 billion over

the previous year. ADBC will continue to provide financial assistance for domestic cotton marketing in

MY14/15.

Marketing

The government continues to provide a transportation subsidy of RMB500/ton ($80) in MY13/14 (up

from RMB 400/ton in MY11/12) for Xinjiang origin cotton shipped to mills in coastal and southern

cities. Xinjiang province provides 40 percent of China’s domestic cotton production yet there is only

one rail line to move the raw product cross-country to the textile production areas. Harvest time can be

a bottleneck. The shipping congestion improved slightly in MY12/13 and MY13/14 when the

government purchased most of the Xinjiang cotton for reserve and stored it locally, thus reducing the

pressure on rail transportation.

U.S. cotton exporters interested in exporting cotton to China in need of marketing assistance may

contact USDA/FAS’s Agricultural Trade Offices (ATO) in Beijing, Chengdu, Guangzhou, Shanghai

and Shenyang. They can be contacted via email at, [email protected], [email protected],

[email protected], [email protected], and [email protected], respectively.

Cotton Council International (CCI) is also actively involved in promoting U.S. cotton in China and

throughout Asia. CCI serves China regionally from its Hong Kong Office. CCI can be reached via

email at [email protected]. Both CCI and the ATO’s organize events designed to bring U.S.

cotton exporters in close contact with Chinese buyers.

The China International Cotton Conference, a biannual event sponsored by CCA and MOA attracts a

worldwide audience from the cotton/textile industry. The 2013 conference was held in June in Qingdao,

Shandong Province. CCA, in collaboration with China National Cotton Exchange also holds an annual

event, the China Cotton Industry Development Forum, which focuses on analysis and outlook of the

market situation. The 2014 Forum will be held in May in Xiamen, Fijian Province.

Tables

Production, Supply and Demand (PSD)

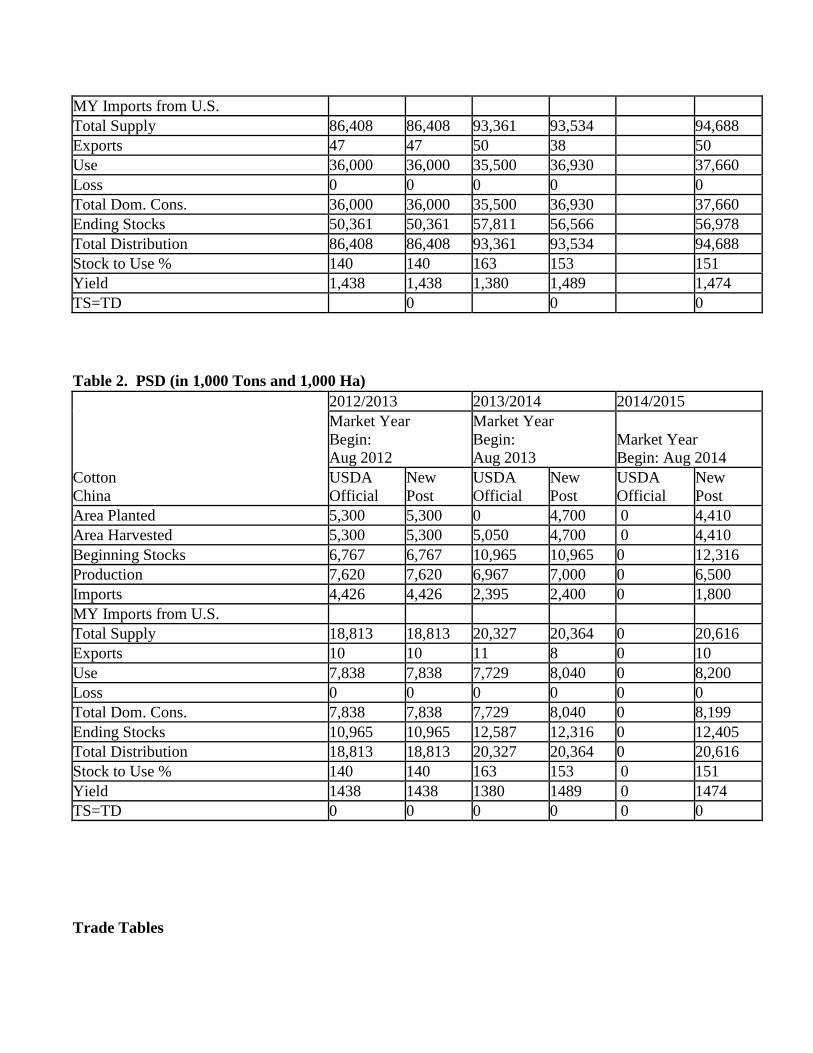

Table 1. PSD (in 1,000 Bales and 1,000 Ha)

Cotton

China

2012/2013 2013/2014 2014/2015

Market Year

Begin:

Aug 2012

Market Year

Begin:

Aug 2013

Market Year

Begin: Aug 2014

USDA

Official

New

Post

USDA

Official

New

Post

USDA

Official

New

Post

Area Planted 5,300 5,300 5,050 4,700 4,410

Area Harvested 5,300 5,300 5,050 4,700 4,410

Beginning Stocks 31,081 31,081 50,361 50,361 56,566

Production 35,000 35,000 32,000 32,150 29,855

Imports 20,327 20,327 11,000 11,023 8,267

MY Imports from U.S.

Total Supply 86,408 86,408 93,361 93,534 94,688

Exports 47 47 50 38 50

Use 36,000 36,000 35,500 36,930 37,660

Loss 0 0 0 0 0

Total Dom. Cons. 36,000 36,000 35,500 36,930 37,660

Ending Stocks 50,361 50,361 57,811 56,566 56,978

Total Distribution 86,408 86,408 93,361 93,534 94,688

Stock to Use % 140 140 163 153 151

Yield 1,438 1,438 1,380 1,489 1,474

TS=TD 0 0 0

Table 2. PSD (in 1,000 Tons and 1,000 Ha)

Cotton

China

2012/2013 2013/2014 2014/2015

Market Year

Begin:

Aug 2012

Market Year

Begin:

Aug 2013

Market Year

Begin: Aug 2014

USDA

Official

New

Post

USDA

Official

New

Post

USDA

Official

New

Post

Area Planted 5,300 5,300 0 4,700 0 4,410

Area Harvested 5,300 5,300 5,050 4,700 0 4,410

Beginning Stocks 6,767 6,767 10,965 10,965 0 12,316

Production 7,620 7,620 6,967 7,000 0 6,500

Imports 4,426 4,426 2,395 2,400 0 1,800

MY Imports from U.S.

Total Supply 18,813 18,813 20,327 20,364 0 20,616

Exports 10 10 11 8 0 10

Use 7,838 7,838 7,729 8,040 0 8,200

Loss 0 0 0 0 0 0

Total Dom. Cons. 7,838 7,838 7,729 8,040 0 8,199

Ending Stocks 10,965 10,965 12,587 12,316 0 12,405

Total Distribution 18,813 18,813 20,327 20,364 0 20,616

Stock to Use % 140 140 163 153 0 151

Yield 1438 1438 1380 1489 0 1474

TS=TD 0 0 0 0 0 0

Trade Tables

Table 3. China’s Monthly Cotton Imports

Unit: Tons

Month 2009 2010 2011 2012 2013 2014

January 77,993 301,359 391,590 326,468 457,490 292,485

February 93,083 221,046 184,216 616,048 378,842

March 98,763 323,807 276,459 625,196 528,822

April 145,560 323,819 210,453 509,694 430,878

May 151,524 197,955 144,569 501,855 345,779

June 168,619 177,248 120,017 475,971 269,793

July 131,440 168,882 157,087 405,842 337,799

August 109,711 240,172 207,048 305,556 275,885

September 102,162 200,806 252,739 262,924 201,270

October 118,604 96,136 252,315 272,067 141,185

November 112,866 126,203 378,152 303,643 173,122

December 216,776 461,657 790,402 532,187 608,606

TOTAL 1,527,101 2,841,100 3,367,058 5,137,451 4,151,484

Marketing

Year

Aug/09-

Jul/10

Aug/10-

Jul/11

Aug/11-

Jul/12

Aug/11-

Jul/12

Aug/13-

Jul/14

TOTAL 2,374,346 2,609,365 5,341,730 4,425,780

Unit: 480-lb Bales

Month 2009 2010 2011 2012 2013

January 358,222 1,384,142 1,798,573 1,499,468 2,101,252 1,343,384

February 427,529 1,015,264 846,104 2,829,508 1,740,021

March 453,619 1,487,246 1,269,776 2,871,525 2,428,879

April 668,557 1,487,301 966,611 2,341,025 1,979,023

May 695,952 909,207 664,005 2,305,020 1,588,163

June 774,466 814,100 551,238 2,186,135 1,239,159

July 603,702 775,675 721,501 1,864,032 1,551,511

August 503,901 1,103,110 950,971 1,403,419 1,267,140

September 469,232 922,302 1,160,830 1,207,610 924,433

October 544,749 441,553 1,158,883 1,249,604 648,463

November 518,392 579,650 1,736,852 1,394,632 795,149

December 995,653 2,120,391 3,630,316 2,444,335 2,795,327

TOTAL 7,013,974 13,041,950 15,464,897 23,596,312 19,067,766

Marketing

Year

Aug/09-

Jul/10

Aug/10-

Jul/11

Aug/11-

Jul/12

Aug/12-

Jul/13

Aug/13-

Jul/14

TOTAL 10,905,371 11,984,813 24,534,566 20,327,608

Source: Global Trade Atlas

Table 4. China’s Quarterly Cotton Imports by Country of Origin

Unit: Tons

Marketing Year: 2011/2012

Country Jul-Sep /10 Oct-Dec /10 Jan-Mar/11 Apr-Jun/11 TOTAL

India 78,544 602,910 778,250 421,102 1,880,806

United States 98,835 147,563 424,256 584,886 1,255,540

Australia 280,665 208,774 30,258 108,580 628,277

Brazil 17,674 191,260 87,778 46,986 343,698

Uzbekistan 43,257 47,600 111,853 60,442 263,152

Burkina Faso 26,098 22,893 10,397 46,895 106,283

Mali 20,855 10,122 4,774 28,746 64,497

Cameroon 11,153 6,665 5,459 29,973 53,250

Pakistan 7,154 23,471 15,901 24,482 71,008

Other 32,639 159,611 98,785 135,428 426,463

TOTAL 616,874 1,420,869 1,567,711 1,487,520 5,092,974

Marketing Year: 2012/2013

Country Jul-Sep /11 Oct-Dec /11 Jan-Mar/12 Apr-Jun/12 TOTAL

India 91,159 148,171 605,491 173,408 1,018,229

United States 255,847 198,658 398,347 465,747 1,318,599

Uzbekistan 57,670 79,788 93,590 83,863 314,911

Brazil 43,500 188,815 76,950 17,925 327,190

Australia 352,003 327,752 56,454 144,505 880,714

Mexico 5,774 15,875 18,698 12,364 52,711

Tanzania 22 15,180 15,701 3,106 34,009

Zimbabwe 1,608 15,411 15,619 1,646 34,284

Zambia 5,820 21,548 10,056 3,441 40,865

Mali 48,838 25,042 2,202 8,627 84,709

Cameroon 28,942 7,118 1,044 19,733 56,837

Other 83,139 64,540 71,002 112,085 330,766

TOTAL 974,322 1,107,898 1,365,154 1,046,450 4,493,824

Marketing Year: 2013/2014

Country Jul-Sep /12 Oct-Dec /12 Jan-Mar/13 Apr-Jun/13 TOTAL

Australia 391,661 204,232 595,893

India 59,257 355,375 414,632

United States 173,606 114,114 287,720

Uzbekistan 49,661 36,500 86,161

Brazil 10,852 53,862 64,714

Burkina Faso 29,415 21,873 51,288

Mali 23,953 17,981 41,934

Cameroon 25,352 19,658 45,010

Other 51,197 99,317 150,514

TOTAL 814,954 922,912 1,737,866

Source: Global Trade Atlas

Table 5. China’s Monthly Cotton Exports

Unit: Tons

Month 2010 2011 2012 2013 2014

January 86 3,641 0 70 440

February 0 5,108 472 0

March 578 1,908 617 211

April 1,136 5,240 42 990

May 1,474 6,124 1,512 715

June 461 1,058 5,919 495

July 86 820 1,653 507

August 1,052 1,097 1,389 348

September 1,240 456 3,007 959

October 255 0 1,168 1,409

November 55 90 502 717

December 31 157 1,277 313

TOTAL 8,464 27,710 17,558

Marketing Year Aug/10-Jul/11 Aug/11-Jul/12 Aug/12-Jul/13 Aug/13-Jul/14

TOTAL 5,084

Unit: 480-lb Bales

Month 2010 2011 2012 2013 2014

January 395 16,723 0 322 2,021

February 0 23,461 2,168 0

March 2,655 8,763 2,834 969

April 5,218 24,067 193 4,547

May 6,770 28,128 6,945 3,284

June 2,117 4,859 27,186 2,274

July 395 3,766 7,592 2,329

August 4,832 5,039 6,380 1,598

September 5,695 2,094 13,811 4,405

October 1,171 0 5,365 6,472

November 253 413 2,306 3,293

December 142 721 5,865 1,438

TOTAL 38,875 127,272 80,644 40,175

Marketing Year Aug/10-Jul/11 Aug/11-Jul/12 Aug/12-Jul/13 Aug/13-Jul/14

TOTAL 121,861

Source: Global Trade Atlas

Table 6. China’s Monthly Cotton Yarn and Thread Imports

Unit: Tons

Month 2010 2011 2012 2013 2014

January 102,478 90,812 65,637 162,971 172,173

February 58,667 50,986 114,922 94,457

March 103,588 78,041 113,610 185,939

April 93,393 53,412 99,090 151,011

May 85,614 43,123 114,747 158,033

June 74,473 40,781 97,851 136,010

July 75,036 54,851 126,778 187,801

August 80,202 63,562 143,086 194,228

September 82,571 75,369 129,565 193,729

October 75,846 83,269 116,731 176,786

November 94,145 79,225 134,442 168,870

December 102,953 90,537 149,506 163,395

TOTAL 1,030,976 805,979 1,405,965 1,973,230

Marketing Year Aug/10-Jul/11 Aug/11-Jul/12 Aug/12-Jul/13 Aug/13-Jul/14

TOTAL

847,723 1,124,597

1,749,552

Source: Global Trade Atlas

Table 7. China’s Monthly Cotton Yarn and Thread Exports

Unit: Tons

Month 2010 2011 2012 2013 2014

January 39,795 30,243 19,420 44,249 33,120

February 24,800 20,323 24,823 22,549

March 48,377 48,893 41,244 40,903

April 44,305 35,205 28,122 37,983

May 49,254 23,469 27,809 27,927

June 48,430 21,395 24,670 23,431

July 39,325 18,717 19,824 25,594

August 29,464 18,998 23,196 29,836

September 24,584 18,095 29,497 32,314

October 28,400 19,404 31,207 28,577

November 35,875 17,802 31,866 36,263

December 28,083 22,684 41,230 37,459

TOTAL 442,702 297,239 342,908 387,085

Marketing Year Aug/10-Jul/11 Aug/11-Jul/12 Aug/12-Jul/13 Aug/13-Jul/14

TOTAL

344,651

355,118 447,211

Source: Global Trade Atlas

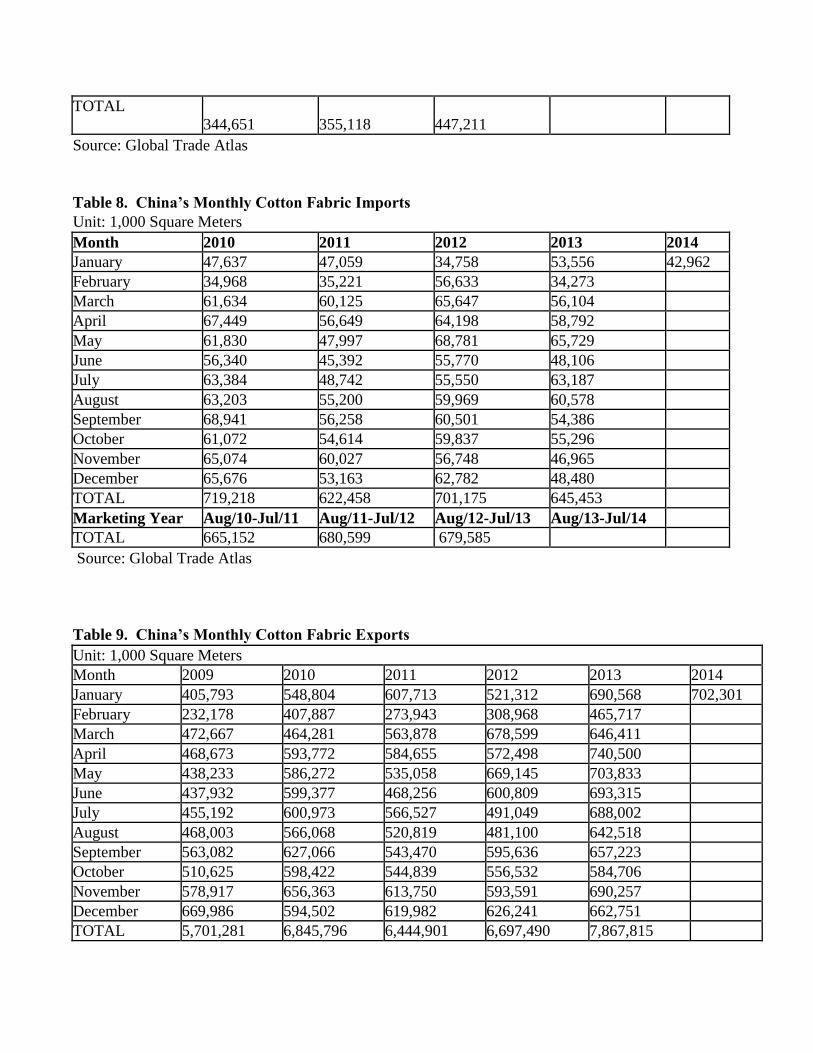

Table 8. China’s Monthly Cotton Fabric Imports

Unit: 1,000 Square Meters

Month 2010 2011 2012 2013 2014

January 47,637 47,059 34,758 53,556 42,962

February 34,968 35,221 56,633 34,273

March 61,634 60,125 65,647 56,104

April 67,449 56,649 64,198 58,792

May 61,830 47,997 68,781 65,729

June 56,340 45,392 55,770 48,106

July 63,384 48,742 55,550 63,187

August 63,203 55,200 59,969 60,578

September 68,941 56,258 60,501 54,386

October 61,072 54,614 59,837 55,296

November 65,074 60,027 56,748 46,965

December 65,676 53,163 62,782 48,480

TOTAL 719,218 622,458 701,175 645,453

Marketing Year Aug/10-Jul/11 Aug/11-Jul/12 Aug/12-Jul/13 Aug/13-Jul/14

TOTAL 665,152 680,599 679,585

Source: Global Trade Atlas

Table 9. China’s Monthly Cotton Fabric Exports

Unit: 1,000 Square Meters

Month 2009 2010 2011 2012 2013 2014

January 405,793 548,804 607,713 521,312 690,568 702,301

February 232,178 407,887 273,943 308,968 465,717

March 472,667 464,281 563,878 678,599 646,411

April 468,673 593,772 584,655 572,498 740,500

May 438,233 586,272 535,058 669,145 703,833

June 437,932 599,377 468,256 600,809 693,315

July 455,192 600,973 566,527 491,049 688,002

August 468,003 566,068 520,819 481,100 642,518

September 563,082 627,066 543,470 595,636 657,223

October 510,625 598,422 544,839 556,532 584,706

November 578,917 656,363 613,750 593,591 690,257

December 669,986 594,502 619,982 626,241 662,751

TOTAL 5,701,281 6,845,796 6,444,901 6,697,490 7,867,815

Marketing

Year

Aug/09-

Jul/10

Aug/10-

Jul/11

Aug/11-

Jul/12

Aug/12-

Jul/13

Aug/13-

Jul/14

TOTAL

6,591,978 6,642,450

6,444,901 7,481,447

Source: Global Trade Atlas

Other Tables

Table 10. Cotton Planted Area and Production by Province

Planted Area (in 1,000 Ha)

Year MY11/12 MY12/13 MY13/14 MY14/15

Xinjiang 1,980 2,160 2,250 2,200

Shandong 766 740 610 525

Hebei 633 550 400 385

Hubei 489 473 450 440

Henan 390 250 220 195

Anhui 340 305 200 180

Jiangsu 220 171 100 88

Hunan 192 202 175 152

Gansu 48 71 70 70

Other 322 353 225 175

Total 5,380 5,275 4,700 4,410

Production (in 1,000 tons)

Year MY11/12 MY12/13 MY13/14 MY14/15

Xinjiang 3,500 4,430 4,450 4,200

Shandong 785 698 650 560

Hebei 653 571 385 395

Hubei 523 571 540 455

Henan 382 269 200 190

Anhui 378 270 180 175

Jiangsu 247 210 95 95

Hunan 227 251 192 180

Gansu 78 107 108 100

Other 429 223 200 150

Total 7,202 7,600 7,000 6,500

Average Yield (Kg/Ha) 1,339 1,441 1,489 1,474

Note: FAS/Beijing estimate and forecast

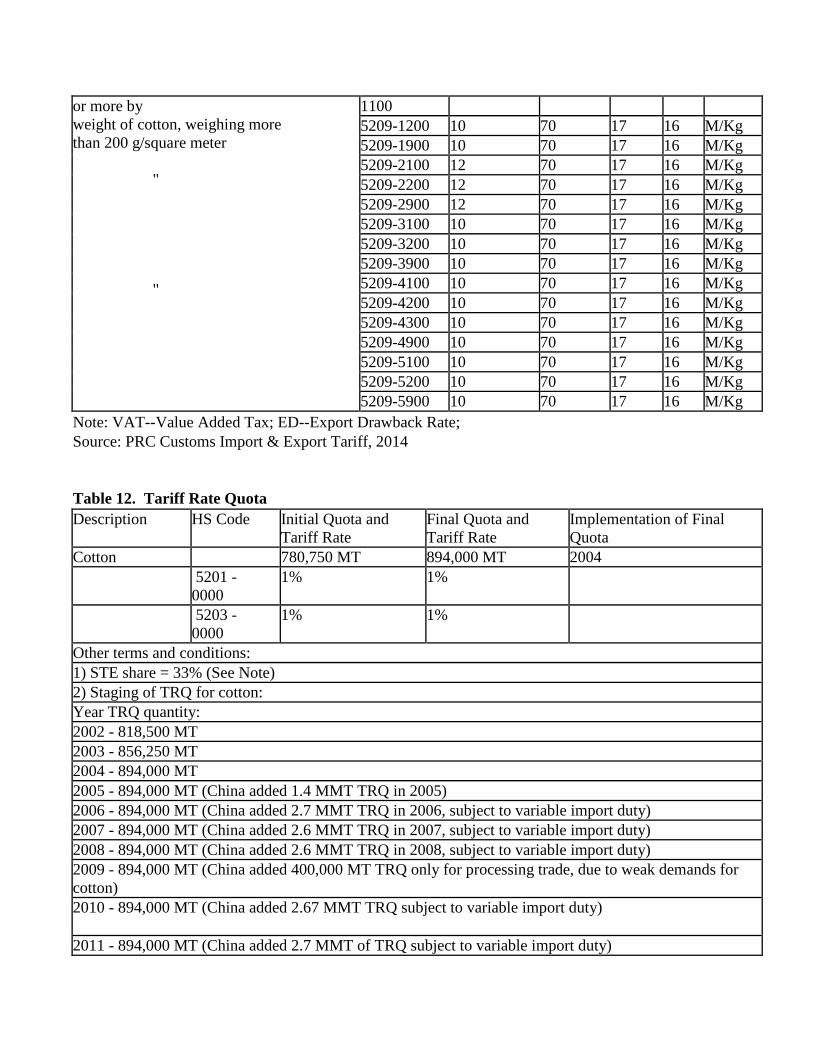

Table 11. Cotton Tariffs as of January 1, 2014 (continued)

Description HS Code M.F.N.(%) Gen(%) VAT ED Unit

Cotton, not carded or combed 5201-0000 Kg

Cotton, not carded or combed, including

degreased cotton -in quota

5201-

0000.01

1 125

13 13

Cotton, not carded or combed, including

degreased cotton - tariff and out of

quota, interim

5201-

0000.80

40(*) 0

13 13

Cotton, not carded or combed, including

degreased cotton -out of quota

5201-

0000.90

40 125

13 13

Cotton waste, yarn waste 5202-1000 10 30 17 13 Kg

Cotton waste, garnetted stock 5202-9100 10 30 17 13 Kg

Cotton waste, other 5202-9900 10 30 17 13 Kg

Cotton, carded or combed 5203-0000 125 17 13 Kg

Cotton, carded or combed, in quota 5203-

0000.01

1 125

17 13

Cotton, carded or combed, out of quota 5203-

0000.90

40 125

17 13

Cotton sewing thread, containing 5204-1100 5 40 17 16 Kg

85% or more by weight of cotton

Other 5204-1900 5 40 17 16 Kg

Put up for retail sale 5204-2000 5 50 17 16 Kg

Cotton yarn (other than sewing 5205-1100 5 40 17 16 Kg

thread), containing 85% or more to

by weight of cotton, not for retail sale 5205-4800

Cotton yarn (other than sewing thread)

containing less than 85% by weight of

cotton, not put for retail sale

5206-1100

to 5206-

4500

5 40

17 16 Kg

Cotton yarn (other than sewing 5207-1000 6 50 17 16 Kg

thread), containing 85% or more 5207-9000 6 50 17 16 Kg

Note: (*) subject to sliding tariff rate based on a formula; VAT--Value Added Tax; ED--Export

Drawback Rate; Source: PRC Customs Import & Export Tariff, 2014

Table 11. Cotton Tariffs as of January 1, 2014 (continued)

Description HS Code M.F.N.(%) Gen(%) VAT ED Unit

Woven fabrics of cotton,

containing 85% or more by weight of

cotton, weighing not more than 200

g/square meter

5208-

1100

to

5208-

5990*

10

70

17 16 M/Kg

*Except:

5208-2300

12 70

17 16 M/Kg

Woven fabrics of cotton, containing 85% 5209- 10 70 17 16 M/Kg

or more by

weight of cotton, weighing more

than 200 g/square meter

"

"

1100

5209-1200 10 70 17 16 M/Kg

5209-1900 10 70 17 16 M/Kg

5209-2100 12 70 17 16 M/Kg

5209-2200 12 70 17 16 M/Kg

5209-2900 12 70 17 16 M/Kg

5209-3100 10 70 17 16 M/Kg

5209-3200 10 70 17 16 M/Kg

5209-3900 10 70 17 16 M/Kg

5209-4100 10 70 17 16 M/Kg

5209-4200 10 70 17 16 M/Kg

5209-4300 10 70 17 16 M/Kg

5209-4900 10 70 17 16 M/Kg

5209-5100 10 70 17 16 M/Kg

5209-5200 10 70 17 16 M/Kg

5209-5900 10 70 17 16 M/Kg

Note: VAT--Value Added Tax; ED--Export Drawback Rate;

Source: PRC Customs Import & Export Tariff, 2014

Table 12. Tariff Rate Quota

Description HS Code Initial Quota and

Tariff Rate

Final Quota and

Tariff Rate

Implementation of Final

Quota

Cotton 780,750 MT 894,000 MT 2004

5201 -

0000

1% 1%

5203 -

0000

1% 1%

Other terms and conditions:

1) STE share = 33% (See Note)

2) Staging of TRQ for cotton:

Year TRQ quantity:

2002 - 818,500 MT

2003 - 856,250 MT

2004 - 894,000 MT

2005 - 894,000 MT (China added 1.4 MMT TRQ in 2005)

2006 - 894,000 MT (China added 2.7 MMT TRQ in 2006, subject to variable import duty)

2007 - 894,000 MT (China added 2.6 MMT TRQ in 2007, subject to variable import duty)

2008 - 894,000 MT (China added 2.6 MMT TRQ in 2008, subject to variable import duty)

2009 - 894,000 MT (China added 400,000 MT TRQ only for processing trade, due to weak demands for

cotton)

2010 - 894,000 MT (China added 2.67 MMT TRQ subject to variable import duty)

2011 - 894,000 MT (China added 2.7 MMT of TRQ subject to variable import duty)

2012 - 894,000 tons (China added 1.32 million tons of TRQ subject to variable import duty)

2013 - 894,000 tons (China added an estimated 2.3 million tons additional TRQ subject to variable duty

or for processing trade)

2014 - 894,000 tons (as of this report, no additional TRQ has been allocated; China’s WTO commitment

does NOT mandate a TRQ for CY05 and after, but China maintained an identical quantity of TRQ as

CY04. In addition to those volumes, based on market demand, China adds TRQs yearly. The added

TRQs are subject to a variable import duty)

![Cipaganti [ whats next ] Focus or Diversify?](https://static.fdocuments.net/doc/165x107/547951b15906b576048b46c1/cipaganti-whats-next-focus-or-diversify.jpg)