China / Hong Kong Monthly Chart Book HK Property

32

Page 1 ed TH / sa- AH Hotel supply in focus Hotel inventory concentrated in Yau Tsim Mong Hotel room supply growth to moderate slightly Major hotels in the pipeline located in North Point, Wan Chai & Tsim Sha Tsui Hotel inventory concentrated in Yau Tsim Mong. As at June 2016, there were 259 hotels in Hong Kong with a total of 74,155 rooms. High Tariff A and High Tariff B hotels accounted for 24.4% and 37.3% of total inventory of hotel rooms. Medium Tariff hotels made up 31.6% of the total with the balance made up of unclassified hotels. In terms of locations, Yau Tsim Mong (Yau Ma Tei/Tsim Sha Tsui/Mongkok) is most concentrated hotel district in Hong Kong with 23,200 rooms, representing 31.3% of the total hotel stock as at June 2016. This is followed by Wan Chai (13.3%) and Central and Western districts (11.6%). Moreover, Kowloon City and Eastern Hong Kong account for 9.1% and 6.7% of the total hotel room inventory. Kwai Tsing, Shatin, Tsuen Wan and Island districts each made up of 4-6% of hotel rooms available. Including guesthouses, there are 86,074 rooms available as at June 2016. Hotel room supply growth to moderate slightly Our analysis suggests that hotel room supply will increase at 5-year CAGR of 3.5% between 2015 and 2020. The growth rate is envisaged to be slightly slower than in the past five or ten years. In 2006-2015, hotel supply room increased at 10-year CAGR of 5.3%, with growth stronger during 2006-10 at 6.6%, moderating to 4.1% between 2011-15. Major hotels in the pipeline. Shangri-la Asia will launch Kerry Hotel Hong Kong (546 rooms) on the Hung Hom harbourfront in late-2016, marking the fourth hotel owned by this hotel group in Hong Kong. Two hotels are being built along the North Point waterfront sites acquired via government tender, to provide 1,520 units upon completion in 2018-19, representing c.30% of existing supply in the Eastern Hong Kong. New World Development is constructing a 3m square foot mixed-use project on the Tsim Sha Tsui waterfront. About one-third of the gross floor area will be earmarked for hotel use. Superstructure works are currently underway. This hotel will be launched under the “Rosewood” brand and open for business in 2018. Harbour Centre Development is converting an iconic Murray Building into an urban chic hotel, with total investment of around HK$7bn. Targeted for opening in late 2017, this luxury hotel will operate under the Niccolo brand, offering 336 guest rooms. This hotel will also be the first High Tariff A hotel in Central/Admiralty since the opening of Upper House at Pacific Place in 2009. Hopewell Holdings is developing Hopewell Centre II in Wan Chai, which includes a conference hotel with 1,024 rooms. Targeted to start operations in 2019, this hotel will be the largest conference hotel in Hong Kong with comprehensive conference facilities. HSI: 22,811 ANALYST Jeff YAU CFA +852 2820 4912 [email protected] Andrew LAM Andrewr_lam@ hk.dbsvickers.com Hotel room supply 0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016F 2017F 2018F 2019F 2020F Source: HKTB, DBS Vickers estimates Hotel room supply by district (Jun-16) Central/We stern HK 12% Easter HK 7% Souther HK 2% Wan Chai 13% Kowloon city 9% Kwun Tong 2% Sham Shui Po 0% Wong Tai Sin 1% Yau Tsim Mong 31% Kwai Tsing 4% Sai Kung 1% Sha Tin 4% Tsuen Wan 5% Tuen Mun 1% Yuen Long 2% Islands 6% Source: HKTB DBS Group Research . Equity 3 Nov 2016 China / Hong Kong Monthly Chart Book HK Property (Issue No. 81) Refer to important disclosures at the end of this report

Transcript of China / Hong Kong Monthly Chart Book HK Property

Page 1

ed TH / sa- AH

Hotel supply in focus Hotel inventory concentrated in Yau Tsim Mong

Hotel room supply growth to moderate slightly

Major hotels in the pipeline located in North Point, Wan Chai & Tsim Sha Tsui

Hotel inventory concentrated in Yau Tsim Mong. As at June 2016, there were 259 hotels in Hong Kong with a total of 74,155 rooms. High Tariff A and High Tariff B hotels accounted for 24.4% and 37.3% of total inventory of hotel rooms. Medium Tariff hotels made up 31.6% of the total with the balance made up of unclassified hotels. In terms of locations, Yau Tsim Mong (Yau Ma Tei/Tsim Sha Tsui/Mongkok) is most concentrated hotel district in Hong Kong with 23,200 rooms, representing 31.3% of the total hotel stock as at June 2016. This is followed by Wan Chai (13.3%) and Central and Western districts (11.6%). Moreover, Kowloon City and Eastern Hong Kong account for 9.1% and 6.7% of the total hotel room inventory. Kwai Tsing, Shatin, Tsuen Wan and Island districts each made up of 4-6% of hotel rooms available. Including guesthouses, there are 86,074 rooms available as at June 2016. Hotel room supply growth to moderate slightly Our analysis suggests that hotel room supply will increase at 5-year CAGR of 3.5% between 2015 and 2020. The growth rate is envisaged to be slightly slower than in the past five or ten years. In 2006-2015, hotel supply room increased at 10-year CAGR of 5.3%, with growth stronger during 2006-10 at 6.6%, moderating to 4.1% between 2011-15. Major hotels in the pipeline. Shangri-la Asia will launch Kerry Hotel Hong Kong (546 rooms) on the Hung Hom harbourfront in late-2016, marking the fourth hotel owned by this hotel group in Hong Kong. Two hotels are being built along the North Point waterfront sites acquired via government tender, to provide 1,520 units upon completion in 2018-19, representing c.30% of existing supply in the Eastern Hong Kong. New World Development is constructing a 3m square foot mixed-use project on the Tsim Sha Tsui waterfront. About one-third of the gross floor area will be earmarked for hotel use. Superstructure works are currently underway. This hotel will be launched under the “Rosewood” brand and open for business in 2018. Harbour Centre Development is converting an iconic Murray Building into an urban chic hotel, with total investment of around HK$7bn. Targeted for opening in late 2017, this luxury hotel will operate under the Niccolo brand, offering 336 guest rooms. This hotel will also be the first High Tariff A hotel in Central/Admiralty since the opening of Upper House at Pacific Place in 2009. Hopewell Holdings is developing Hopewell Centre II in Wan Chai, which includes a conference hotel with 1,024 rooms. Targeted to start operations in 2019, this hotel will be the largest conference hotel in Hong Kong with comprehensive conference facilities.

HSI: 22,811 ANALYST Jeff YAU CFA +852 2820 4912 [email protected] Andrew LAM Andrewr_lam@ hk.dbsvickers.com

Hotel room supply

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

F20

17F

2018

F20

19F

2020

F

Source: HKTB, DBS Vickers estimates

Hotel room supply by district (Jun-16)

Central/Western HK

12%

Easter HK7%

Souther HK2%

Wan Chai13%

Kowloon city9%

Kwun Tong2%Sham Shui

Po0%

Wong Tai Sin1%

Yau Tsim Mong31%

Kwai Tsing4%

Sai Kung1%

Sha Tin4%

Tsuen Wan5%

Tuen Mun 1%

Yuen Long2%

Islands6%

Source: HKTB

DBS Group Research . Equity 3 Nov 2016

China / Hong Kong Monthly Chart Book

HK Property (Issue No. 81) Refer to important disclosures at the end of this report

China / Hong Kong Monthly Chart Book

HK Property

Page 2

Hotel Project in North Point Estate Lane/Shu Kuk Street

Hotel Project in Oil Street, North Point

Murray Building Hotel Project

Rosewood Hong Kong, Tsim Sha Tsui

Hopewell Centre II

Kerry Hotel, Hong Kong

Source: DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 3

TABLE OF CONTENTS

Share price performance 4

What were the transaction trends in primary and secondary markets? 9

What are the factors affecting residential demand and supply? 11

What projects were launched? 13

Where are the upcoming projects? 14

How about the office market? 15

How about the retail market? 16

What did corporates do? 18

Discount to NAV – Property developers & investors 20

Discount to NAV band – Property developers & investors 23

Price to book NAV band - REITs 26

Historical yield band - REITs 27

Any important dates to look out for? 28

Our past publications 29

China / Hong Kong Monthly Chart Book

HK Property

Page 4

Share price performance

Property developer index vs HSI Property developer index vs HSI (6 month)

0

50

100

150

200

250

300

350

Jan/

01

Jan/

02

Jan/

03

Jan/

04

Jan/

05

Jan/

06

Jan/

07

Jan/

08

Jan/

09

Jan/

10

Jan/

11

Jan/

12

Jan/

13

Jan/

14

Jan/

15

Jan/

16

HK property developers share price index HSI

Rebased (01 Jan 01 = 100)

70

80

90

100

110

120

130

Apr

/16

May

/16

Jun/

16

Jul/1

6

Aug

/16

Sep/

16

Oct

/16

HK property developers share price index HSI

Rebased (29 Apr 16 = 100)

Property investor vs HSI Property investor index vs HSI (6 month)

0

100

200

300

400

500

600

Jan/

01

Jan/

02

Jan/

03

Jan/

04

Jan/

05

Jan/

06

Jan/

07

Jan/

08

Jan/

09

Jan/

10

Jan/

11

Jan/

12

Jan/

13

Jan/

14

Jan/

15

Jan/

16

HK property investors share price index HSI

70

80

90

100

110

120

130

140

Apr

/16

May

/16

Jun/

16

Jul/1

6

Aug

/16

Sep/

16

Oct

/16

HK property investors share price index HSI

REIT vs HSI REIT index vs HSI (6 month)

40

90

140

190

240

290

340

Jan/

07Ju

l/07

Jan/

08Ju

l/08

Jan/

09Ju

l/09

Jan/

10Ju

l/10

Jan/

11Ju

l/11

Jan/

12Ju

l/12

Jan/

13Ju

l/13

Jan/

14Ju

l/14

Jan/

15Ju

l/15

Jan/

16Ju

l/16

REITs share price index HSI

Rebased (29 Dec 06 = 100)

70 75 80 85 90 95

100 105 110 115 120

Apr

/16

May

/16

Jun/

16

Jul/1

6

Aug

/16

Sep/

16

Oct

/16

REITs share price index HSI

Rebased (29 Apr 16 = 100)

Source: Thomson Reuters; DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 5

Valuation – Property developers

Disc. to

Mkt Last 12-m PE PE J ul-17 J ul-17 Y ield Y ieldCompany Code F YE Cap Price target Recom F Y16 F Y17 NA V NA V F Y16 F Y17

HK$bn HK$ HK$ x x HK$ % % %

Henderson Land 12 HK Dec 168 46.25 51.75 Buy 12.2 16.2 79.6 (42) 3.5 3.5

K Wah Int'l 173 HK Dec 13 4.24 4.50 Buy 6.1 8.0 11.2 (62) 4.0 4.0Kerry Props 683 HK Dec 35 24.45 25.70 Buy 9.8 7.1 73.4 (67) 3.7 3.7

Lai Sun Dev 488 HK Jul 3 0.159 0.220 Buy 12.2 14.2 0.6 (75) 1.2 1.2

MTR Corp 66 HK Dec 253 42.90 40.45 Hold 27.0 26.2 46.6 (8) 7.6 7.6New World Dev 17 HK Jun 91 9.73 11.20 Buy 12.9 12.6 22.4 (57) 4.5 4.5

Sino Land 83 HK Jun 78 12.70 15.40 Buy 14.5 15.1 23.7 (46) 4.0 4.0

SHKP 16 HK Jun 340 117.30 132.00 Buy 14.0 13.7 203.1 (42) 3.3 3.3Tai Cheung 88 HK Mar 4 6.58 7.89 Buy 18.0 12.6 19.7 (67) 4.6 4.6

Wheelock & Co. 20 HK Dec 98 48.15 46.35 Buy 9.3 9.1 57.9 (17) 2.5 2.5

Wing Tai Properties 369 HK Dec 6 4.81 5.46 Buy 16.3 15.7 15.8 (70) 3.1 3.1

^ ^

^ Included proposed special dividend Source: Thomson Reuters, DBS Vickers

Valuation – Property investors

Disc . t oM k t Last 12- m PE PE J u l- 17 J u l- 17 Y ield Y ield

Company Code F Y E Cap Price t arget Recom F Y 16 F Y 17 NA V NA V F Y 16 F Y 17

HK $bn HK $ HK $ x x HK $ % % %

Hang Lung Props 101 HK Dec 76 17.00 15.40 Hold 15.1 14.5 34.2 (50) 4.4 4.4

HK Land @ HKL SP Dec 16 6.62 7.87 Buy 18.0 16.7 12.1 (45) 2.9 2.9Hysan Dev 14 HK Dec 37 35.25 35.65 Hold 15.8 15.6 64.8 (46) 3.9 3.9

Swire Props 1972 HK Dec 129 22.00 26.45 Buy 19.0 17.1 40.7 (46) 3.2 3.2Wharf 4 HK Dec 179 59.00 56.00 Hold 14.1 13.7 86.2 (32) 3.5 3.6

@ denominated in USD

Source: Thomson Reuters, DBS Vickers

Valuation – REITs

M k t Last 12- m Y ield Y ield Y ield Price/

REIT Code F Y E Cap Pric e T arget Recom F Y 15A F Y 16F F Y 17F BV

HK $m HK $ HK $ % % % (x )

Champion REIT* 2778 HK Dec 25,512 4.40 4.94 Buy 4.5 5.1 5.1 0.51

J inmao Investments* 6139 HK Dec 7,960 3.98 4.93 Hold 10.9 9.3 9.3 0.99

Langham Hospitality^ 1270 HK Dec 6,388 3.09 n.a. NR 8.1 7.9 7.5 0.54

New Century REIT^ 1275 HK Dec 2,397 2.52 n.a. NR 12.9 7.7 6.9 0.88

Regal REIT^ 1881 HK Dec 6,678 2.05 n.a. NR 7.5 n.a. n.a. 0.50

Spring REIT^ 1426 HK Dec 3,632 3.22 n.a. NR 8.3 7.7 7.5 0.50

Sunlight REIT* 435 HK J un 7,837 4.78 5.22 Buy 4.6 5.1 5.1 0.58

Link REIT* 823 HK Mar 122,166 54.75 60.30 Buy 3.3 3.8 4.1 0.96

Yuexiu REIT^ 405 HK Dec 12,656 4.43 n.a. NR 6.3 6.8 6.6 0.80 @ denominated in RMB ^ DPU based on consensus Source: Thomson Reuters, *DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 6

Trading range comparison – Property developers and investors

LastPrice

F Y16FP/E atHighPrice

F Y16FP/E at

LowPrice

Discountto NAVat High

Price

Discountto NAVat Low

PriceHighPrice

LowPrice

HighPrice

LowPrice

HighPrice

LowPrice

HK$ x x % % HK$ HK$ HK$ HK$ HK$ HK$

Property dev elopers

Henderson Land 12 HK 46.25 12.5 11.9 -41% -44% 47.40 45.15 47.40 45.15 46.90 45.15

K Wah Int'l 173 HK 4.24 6.3 5.5 -60% -64% 4.38 3.88 4.38 4.10 4.34 4.12

Kerry Properties 683 HK 24.45 10.3 8.5 -65% -71% 25.50 21.05 25.50 22.60 25.40 24.15

Lai Sun Dev 488 HK 0.159 13.0 10.4 -72% -78% 0.17 0.14 0.17 0.15 0.17 0.16

MTR Corp 66 HK 42.90 27.6 26.4 -3% -7% 43.85 41.90 43.85 41.90 43.80 42.10

New World Dev 17 HK 9.73 13.7 11.7 -52% -59% 10.34 8.82 10.34 9.56 10.18 9.56

Sino Land 83 HK 12.70 16.4 14.5 -39% -46% 14.34 12.70 14.34 12.70 14.12 12.70

SHKP 16 HK 117.30 14.4 12.7 -39% -47% 120.90 106.10 120.90 111.90 118.40 113.20

Tai Cheung 88 HK 6.58 18.4 16.7 -66% -69% 6.74 6.11 6.65 6.11 6.65 6.22

Wheelock & Co 20 HK 48.15 9.4 7.8 -18% -32% 48.70 40.35 48.70 43.90 48.70 44.75

Wing Tai Properties 369 HK 4.81 16.8 15.7 -68% -70% 4.98 4.64 4.98 4.78 4.89 4.78

Property inv estors

Hang Lung Props 101 HK 17.00 17.0 14.6 -43% -51% 19.10 16.36 19.10 17.00 17.80 17.00

HK Land^ HKL SP 6.62 19.6 16.6 -37% -46% 7.19 6.12 7.19 6.43 7.15 6.62

Hysan Dev 14 HK 35.25 17.2 15.8 -42% -46% 38.35 35.25 38.35 35.25 37.60 35.25

Swire Properties 1972 HK 22.00 20.4 18.5 -40% -46% 23.70 21.40 23.70 21.80 22.85 21.90

Wharf 4 HK 59.00 14.3 12.1 -33% -43% 59.95 50.75 59.95 54.25 59.95 54.25

Sector Av erage - Dev elopers 14.3 12.8 -34% -39%Sector Av erage - Inv estors 17.7 15.5 -38% -46%Hang Seng Index 13.0 11.8

- - Last 1 month - -- - Last 2 month - -- - Last 3 month - - - - Last 3 month - - - - Last 3 month - -

^ denominated in USD

Source: Thomson Reuters; DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 7

Trading range comparison – REITs

LastPrice

F Y16FDiv y ield

at HighPrice

F Y16FDiv

y ield atLowPrice

P/BV atHigh Price

P/BV atLow Price

HighPrice

LowPrice

HighPrice

LowPrice

HighPrice

LowPrice

HK$ % % x x HK$ HK$ HK$ HK$ HK$ HK$

REIT s

Champion REIT 2778 HK 4.40 4.5 5.1 0.58 0.51 5.00 4.40 4.98 4.40 4.75 4.40

J inmao Investments 6139 HK 3.98 8.4 9.4 1.10 0.98 4.42 3.95 4.42 3.95 4.24 3.98

Langham Hospitality 1270 HK 3.09 7.5 8.8 0.57 0.49 3.26 2.77 3.26 3.06 3.13 3.07

New Century REIT 1275 HK 2.52 7.5 9.0 0.91 0.75 2.60 2.16 2.60 2.16 2.52 2.22

Regal REIT 1881 HK 2.05 n.a. n.a. 0.53 0.49 2.19 2.04 2.19 2.04 2.08 2.05

Spring REIT 1426 HK 3.22 7.0 7.7 0.56 0.50 3.57 3.22 3.57 3.22 3.45 3.22

Sunlight REIT 435 HK 4.78 4.8 5.1 0.61 0.57 5.02 4.74 5.02 4.74 4.97 4.74

Link REIT 823 HK 54.75 3.6 3.8 1.02 0.96 58.00 54.45 58.00 54.45 58.00 54.45

Yuexiu REIT 405 HK 4.43 5.6 6.6 0.92 0.80 5.14 4.43 5.08 4.43 4.74 4.43

Sector A v erage - REIT s 6.1 6.8 0.74 0.67Hang Seng Index 3.4 3.8

@ denominated in RMB

Source: Thomson Reuters; DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 8

Share price movement comparison (%)

1- w k 2- w k 1- mt h 3- mt h 6- mth 1- y r Y T D 2012 2013 2014 2015

Henderson Land (0.4) 1.8 0.5 (0.6) 4.9 5.0 7.1 41.7 (11.0) 35.0 (3.8)K Wah Int'l (2.3) 2.4 0.2 7.0 17.8 31.9 32.7 89.3 26.0 (10.0) (15.6)

Kerry Properties (2.2) 0.2 (3.7) 14.5 15.6 7.2 15.6 56.6 (33.2) 4.6 (24.9)

Lai Sun Development (3.0) 0.0 2.6 10.4 37.1 16.1 39.5 192.0 (31.2) (15.9) (32.5)

MTR Corp (0.8) (0.7) 0.5 (1.7) 11.7 22.6 11.7 21.3 (3.8) 8.3 20.8New World Dev (0.2) 0.7 (3.5) 6.5 25.7 19.5 27.0 92.0 (16.3) (3.2) (14.1)

Sino Land (4.4) (2.8) (7.4) (9.8) 3.9 8.5 11.8 26.0 (24.0) 18.1 (9.3)

SHKP 1.6 2.2 0.2 6.1 19.6 16.6 25.3 19.4 (15.4) 20.3 (20.9)

Tai Cheung 0.3 2.7 5.8 1.9 10.8 5.8 6.0 33.7 (7.6) 8.7 (2.7)Wing Tai Properties 0.0 (0.8) (1.4) 3.7 2.3 8.8 7.4 106.1 (5.7) 5.0 (10.4)Wheelock and Co. 1.0 4.0 5.2 16.3 33.8 36.0 47.5 102.7 (8.6) 1.5 (9.8)

Hang Lung Properties (2.3) 0.0 (2.5) (0.2) 9.8 (8.5) (3.6) 39.4 (20.5) (11.2) (18.9)

HK Land (2.4) (3.9) (6.8) 5.9 4.3 (10.5) (5.4) 54.0 (15.6) 14.6 3.6Hysan Development (3.7) (1.4) (3.0) (1.8) 2.6 3.1 11.0 46.1 (10.3) 3.7 (8.4)

Swire Properties (2.7) (1.6) (3.1) 1.9 8.9 (4.3) (1.8) n.a. (24.2) 16.8 (2.2)

Wharf Holdings 1.5 6.2 4.5 9.5 40.1 28.3 37.2 72.6 (2.1) (5.6) (23.2)

Champion REIT (1.6) (2.0) (6.4) (3.3) 5.8 8.9 13.4 27.1 (7.5) 5.0 7.8Yuexiu REIT (1.8) (2.6) (6.1) (5.7) 3.0 7.8 6.5 7.3 2.7 2.9 6.9

Link REIT (2.6) (2.3) (3.9) (3.6) 16.1 16.5 18.0 35.3 (2.8) 29.1 (4.4)

Regal REIT (0.5) 0.0 (0.5) (0.5) 3.0 4.1 5.7 24.0 0.5 (8.1) (5.4)

Sunlight REIT 0.4 (2.2) (3.2) (2.4) 16.9 21.3 24.8 48.6 (9.1) 16.7 9.4Spring REIT (3.0) (4.2) (4.5) (8.3) (4.7) 3.5 6.3 n.a. n.a. 15.5 (17.2)

New Century REIT 3.3 7.2 12.0 (0.8) (6.7) (17.1) (13.1) n.a. n.a. (9.3) (12.1)

Great Eagle 0.4 0.1 (1.2) (4.5) 9.0 35.5 35.8 68.6 3.3 (4.9) 0.2

Far East Consort.Intl. (1.6) (1.9) 1.3 20.9 27.0 16.6 11.5 90.1 40.7 8.9 3.5

HSI Index (2.2) (2.1) (2.1) 3.1 8.3 2.0 4.1 22.9 2.9 1.3 (7.2)

HSP Index 0.3 1.1 (2.3) 0.7 12.4 9.1 11.6 37.6 (9.2) 7.2 (2.1)

Source: Thomson Reuters

China / Hong Kong Monthly Chart Book

HK Property

Page 9

Residential

What were the transaction trends in primary and secondary markets?

Primary market transaction volume

Primary market transaction value

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11A

pr-1

1Ju

l-11

Oct

-11

Jan-

12A

pr-1

2Ju

l-12

Oct

-12

Jan-

13A

pr-1

3Ju

l-13

Oct

-13

Jan-

14A

pr-1

4Ju

l-14

Oct

-14

Jan-

15A

pr-1

5Ju

l-15

Oct

-15

Jan-

16A

pr-1

6Ju

l-16

No of units Sep-16

113.7% m-o-m

118.7% y-o-y

9M16

-1.7% y-o-y

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11A

pr-1

1Ju

l-11

Oct

-11

Jan-

12A

pr-1

2Ju

l-12

Oct

-12

Jan-

13A

pr-1

3Ju

l-13

Oct

-13

Jan-

14A

pr-1

4Ju

l-14

Oct

-14

Jan-

15A

pr-1

5Ju

l-15

Oct

-15

Jan-

16A

pr-1

6Ju

l-16

HK$mSep-16

99.7% y-o-y

85.9% m-o-m

9M16

-5.6% y-o-y

Source: Centaline Property Agency Source: Centaline Property Agency

Secondary market transaction volume

Secondary market transaction value

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11A

pr-1

1Ju

l-11

Oct

-11

Jan-

12A

pr-1

2Ju

l-12

Oct

-12

Jan-

13A

pr-1

3Ju

l-13

Oct

-13

Jan-

14A

pr-1

4Ju

l-14

Oct

-14

Jan-

15A

pr-1

5Ju

l-15

Oct

-15

Jan-

16A

pr-1

6Ju

l-16

No of units Sep-16

5.5% m-o-m63% y-o-y

9M16

-24% y-o-y

0 5,000

10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11A

pr-1

1Ju

l-11

Oct

-11

Jan-

12A

pr-1

2Ju

l-12

Oct

-12

Jan-

13A

pr-1

3Ju

l-13

Oct

-13

Jan-

14A

pr-1

4Ju

l-14

Oct

-14

Jan-

15A

pr-1

5Ju

l-15

Oct

-15

Jan-

16A

pr-1

6Ju

l-16

HK$mSep-16

49.1% y-o-y

10% m-o-m

9M16

-26.1% y-o-y

Source: Centaline Property Agency Source: Centaline Property Agency

China / Hong Kong Monthly Chart Book

HK Property

Page 10

Confirmor – Overall

Confirmor – Over HK$7m

0%1%2%3%4%5%6%7%8%9%10%

0 200 400 600 800

1,000 1,200 1,400 1,600 1,800

Jul-9

5Ju

l-96

Jul-9

7Ju

l-98

Jul-9

9Ju

l-00

Jul-0

1Ju

l-02

Jul-0

3Ju

l-04

Jul-0

5Ju

l-06

Jul-0

7Ju

l-08

Jul-0

9Ju

l-10

Jul-1

1Ju

l-12

Jul-1

3Ju

l-14

Jul-1

5Ju

l-16

No. of cases of confirmor (LHS)

As a % of total secondary registrations (RHS)

Sep-16 0, 0%

Aug-16 0, 0%

0%

5%

10%

15%

20%

25%

30%

0

50

100

150

200

250

300

350

Jul-9

5Ju

l-96

Jul-9

7Ju

l-98

Jul-9

9Ju

l-00

Jul-0

1Ju

l-02

Jul-0

3Ju

l-04

Jul-0

5Ju

l-06

Jul-0

7Ju

l-08

Jul-0

9Ju

l-10

Jul-1

1Ju

l-12

Jul-1

3Ju

l-14

Jul-1

5Ju

l-16

No. of cases of confirmor (LHS)

As a % of over $7m secondary registrations (RHS)

Sep-16 0, 0%

Aug-16 0, 0%

Source: Centaline Property Agency Source: Centaline Property Agency

Centa-City leading index (Secondary market price index)

Residential rents (Based on saleable area)

(4)

(2)

0

2

4

6

8

50

70

90

110

130

150

170

Jan-

09M

ay-0

9Se

p-09

Jan-

10M

a y-1

0Se

p-10

Jan-

11M

a y-1

1Se

p-11

Jan-

12M

a y-1

2Se

p-12

Jan-

13M

a y-1

3Se

p-13

Jan-

14M

a y-1

4Se

p-14

Jan-

15M

a y-1

5Se

p-15

Jan-

16M

a y-1

6Se

p-16

Mom growth (RHS) CCL Index (LHS)

%

3.5% m-o-m

6.1% ytd

Sep-16

5 10 15 20 25 30 35 40 45

Jan-

07Ju

l-07

Jan-

08Ju

l-08

Jan-

09Ju

l-09

Jan-

10Ju

l-10

Jan-

11Ju

l-11

Jan-

12Ju

l-12

Jan-

13Ju

l-13

Jan-

14Ju

l-14

Jan-

15Ju

l-15

Jan-

16Ju

l-16

Hong Kong KowloonNew Territories East New Territories WestOverall

HK$psf Sep-16

Overall: 0.5% m-o-m-3.2% y-o-y

Source: Centaline Property Agency Source: Centaline Property Agency

China / Hong Kong Monthly Chart Book

HK Property

Page 11

What are the factors affecting residential demand and supply?

Real GDP growth

Unemployment rate

(10)

(8)

(6)

(4)

(2)

0

2

4

6

8

10

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

1Q15

3Q15

1Q16

%2Q16: 1.7% y-o-y

2

3

4

5

6

7

8

9

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

Jan-

16

%Jul-16 -Sep-16: 3.4%

Jun-16 -Aug-16: 3.4%

Source: CEIC Source: CEIC

3-mth HIBOR vs Prime rate

Effective mortgage rate

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0 9.0

Jan-

07Ju

l-07

Jan-

08Ju

l-08

Jan-

09Ju

l-09

Jan-

10Ju

l-10

Jan-

11Ju

l-11

Jan-

12Ju

l-12

Jan-

13Ju

l-13

Jan-

14Ju

l-14

Jan-

15Ju

l-15

Jan-

16Ju

l-16

3-mth HIBOR HK Prime rate

% Sep-16

3-mth HIBOR: 0.59%Prime rate: 5%

0

2

4

6

8

10

12

Jan-

96Ja

n-97

Jan-

98Ja

n-99

Jan-

00Ja

n-01

Jan-

02Ja

n-03

Jan-

04Ja

n-05

Jan-

06Ja

n-07

Jan-

08Ja

n-09

Jan-

10Ja

n-11

Jan-

12Ja

n-13

Jan-

14Ja

n-15

Jan-

16

% Sep-16: 1.67%

Aug-16: 1.65%

Source: CEIC Source: CEIC, DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 12

Housing affordability – private households

Rental yields (mass market projects) (Based on Saleable Area)

0%

20%

40%

60%

80%

100%

120%

Jan-

94Ja

n-95

Jan-

96Ja

n-97

Jan-

98Ja

n-99

Jan-

00Ja

n-01

Jan-

02Ja

n-03

Jan-

04Ja

n-05

Jan-

06Ja

n-07

Jan-

08Ja

n-09

Jan-

10Ja

n-11

Jan-

12Ja

n-13

Jan-

14Ja

n-15

Jan-

16

Prime base HIBOR base

Prime base HIBOR base

Sep-16

Aug-16 50.1

51.6

48.2%

49.4%

3%

4%

5%

6%

7%

Jul-9

5Ju

l-96

Jul-9

7Ju

l-98

Jul-9

9Ju

l-00

Jul-0

1Ju

l-02

Jul-0

3Ju

l-04

Jul-0

5Ju

l-06

Jul-0

7Ju

l-08

Jul-0

9Ju

l-10

Jul-1

1Ju

l-12

Jul-1

3Ju

l-14

Jul-1

5Ju

l-16

Sep-163.34%

Source: Centaline Property Agencys Source: Centaline Property Agency

Yield spread

Housing supply

(10)

(8)

(6)

(4)

(2)

0

2

4

6

Jan-

96Ja

n-97

Jan-

98Ja

n-99

Jan-

00Ja

n-01

Jan-

02Ja

n-03

Jan-

04Ja

n-05

Jan-

06Ja

n-07

Jan-

08Ja

n-09

Jan-

10Ja

n-11

Jan-

12Ja

n-13

Jan-

14Ja

n-15

Jan-

16

%

Jun-03

Max:

3.77%

0 5,000

10,000 15,000 20,000 25,000 30,000 35,000 40,000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

E20

17E

2018

E20

19E

2020

E

Completion No of primary units sold

Average

No of units

Average completion (96-15)

17,988 units

Source: CEIC, Centaline Property Agency, DBS Vickers Source: DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 13

What projects were launched?

Project launches (Oct 2016)

e

Launch Project s Locat ion Dev eloper TotalUnit s

Unit ssold

% sold A SP(HK$psf )

Oct-16 Seven V ictory Avenue Ho Man Tin Henderson Land 250 80 32% 22,000

Oct-16 Island Garden Shau Kei Wan Nan Fung 470 35 7% 19,500

Oct-16 Marina South Ap Lei Chau 114 73 64% 25,000

Oct-16 Zumurud Ho Man Tin 224 51 23% 20,000

Oct-16 Park One Sham Shui Po Henderson Land 129 32 25% 15,200

Oct-16 23-39 Blue Pool Road Happy Valley Hang Lung Props 18 1 6% 63,071

Oct-16 The Met.Bliss Ma On Shan Wang On Group 364 273 75% 15,000

Oct-16 Alto Residences Tseung Kwan O Lai Sun Development/Walter 605 359 59% 14,200

Oct-16 NAPA Tuen Mun Wheelock 460 85 18% 10,500

Oct-16 2Gether Tuen Mun HKR Int'l 222 164 74% 12,800

Note: ASPs are based on saleable area. Source: DBS Vickers

Occupation permits issued (Aug 2016)

Project s Locat ion Locat ion Dev elopers No of unit s

Greenhill Private developer HK Happy Valley 86

Hoi Fung Path, Stanley Private Developer HK Island South 1Heya Crystal HK Housing Society KL Cheung Sha Wan 350

187-191 Portland Street Rise Win Corporation KL Yau Ma Tei 3733 South Lantau Road Swire Properties NT Islands 2

Hung Kiu Lane, Kau To Shan Private developer NT Sha Tin 1

The Wings IIIB SHKP NT Tseung Kwan O 326 Source: Buildings Department

China / Hong Kong Monthly Chart Book

HK Property

Page 14

Where are the upcoming projects?

Pre-sale consent granted (Sep 2016)

Project Dev elopers Locat ion Locat ion No. of unitThe Met. Bliss Wang On-led consortium NT Ma On Shan 364Alto Residences Lai Sun Consortium NT Tseung Kwan O 605Crescendo NT Yuen Long 67

Source: Lands Department

Pre-sale consent pending approval (Sep 2016)

Project Dev elopers Locat ion Locat ion No. of unitIL8949 (Ph1) HK Mid-levels 115IL 2302 Chinese Estates HK Mid-levels 24IL 8920 HK North Point 378IL 9027 RP (Ph1) SHKP HK North Point 355RBL 1190 Nan Fung Group HK Shouson Peak 54Cullinan West SHKP Kln West Kowloon 1,050NKIL 6527 Poly Property Group Kln Kai Tak 930NKIL 6526 K Wah Int'l Kln Kai Tak 900NKIL 6525 K&K Property Kln Kai Tak 822NKIL 6541 Wheelock & Co. Kln Kai Tak 648One Kai Tak II Kln Kai Tak 624STTL 574 NT Ma On Shan 454STTL 581 (ph 1) SHKP NT Ma On Shan 354STTL 581 (ph 2) SHKP NT Ma On Shan 67Lot 1588 in DD 243 V ice Chairman of Agile NT Sai Kung 8STTL 567 Wing Tai Props/Manhattan Realty NT Shatin 158STTL 565 Wing Tai Props/Manhattan Realty NT Shatin 69La Cresta HKR/Nan Fung Group NT Shatin 61STTL 566 SHKP NT Shatin 59Mount V ienna Hanison Construction Holdings Ltd NT Shatin 12Lot 2640 in DD 92 Henderson Land NT Sheung Shui 590TKOKL 126 Wheelock & Co. NT Tseung Kwan O 926TWTL 401 (3A) NT Tsuen Wan 1,436The Pav ilia Bay New World/Vanke NT Tsuen Wan 983TWTL 401 NT Tsuen Wan 970TWTL 417 Chinachem/MTRC NT Tsuen Wan 953NAPA Wheelock & Co. NT Tuen Mun 4602 Tsing Min Path Chun Wo consortium NT Tuen Mun 3562GETHER HKR NT Tuen Mun 222CPTL 18 and TMTL 99 New World NT Tuen Mun 1008 Kwun Fat Street Emperor International NT Tuen Mun 14

14,152

Source: Lands Department

China / Hong Kong Monthly Chart Book

HK Property

Page 15

How about the office market?

Office rentals

Office capital values

0

50

100

150

200

250

Aug

-07

Dec

-07

Apr

-08

Aug

-08

Dec

-08

Apr

-09

Aug

-09

Dec

-09

Apr

-10

Aug

-10

Dec

-10

Apr

-11

Aug

-11

Dec

-11

Apr

-12

Aug

-12

Dec

-12

Apr

-13

Aug

-13

Dec

-13

Apr

-14

Aug

-14

Dec

-14

Apr

-15

Aug

-15

Dec

-15

Apr

-16

Aug

-16

Premium Central Traditional Central

HK$psf/mth P remium Central

Sep-16: 0.2% m-o-m

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Sep-

07Ja

n-08

May

-08

Sep-

08Ja

n-09

May

-09

Sep-

09Ja

n-10

May

-10

Sep-

10Ja

n-11

May

-11

Sep-

11Ja

n-12

Ma y

-12

Sep-

12Ja

n-13

Ma y

-13

Sep-

13Ja

n-14

May

-14

Sep-

14Ja

n-15

May

-15

Sep-

15Ja

n-16

Ma y

-16

Overall Central

HK$psf/mth Sep-16

HK$29,252psf, 2.1% m-o-mOverall Ce ntral

Source: Knight Frank Source: Knight Frank

Office vacancy

Expectations to hire

1.5

2.42.0 2.3

7.3

4.1

1.5

2.7 2.7 2.6

7.2

4.2

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Cen

tral

Wan

chai

/ C

ause

way

Bay

HK

Eas

t

Tsim

shat

sui

Kow

loon

Eas

t

Ove

rall

Aug-16 Sep-16%

0

10

20

30

40

50

60

70

80

4Q01

2Q02

4Q02

2Q03

4Q03

2Q04

4Q04

2Q05

4Q05

2Q06

4Q06

2Q07

4Q07

2Q08

4Q08

2Q09

4Q09

2Q10

4Q10

2Q11

4Q11

2Q12

4Q12

2Q13

4Q13

2H14

2H15

2H16

%2H16

15.7%

Source: Jones Lang LaSalle Source: Hudson Global Resources (HK)

China / Hong Kong Monthly Chart Book

HK Property

Page 16

How about the retail market?

Private retail rent index

Private retail price index

80

100

120

140

160

180

200

Jan/

93Ja

n/94

Jan/

95Ja

n/96

Jan/

97Ja

n/98

Jan/

99Ja

n/00

Jan/

01Ja

n/02

Jan/

03Ja

n/04

Jan/

05Ja

n/06

Jan/

07Ja

n/08

Jan/

09Ja

n/10

Jan/

11Ja

n/12

Jan/

13Ja

n/14

Jan/

15Ja

n/16

Rental Index (1999=100)

Aug-16-0.6% m-o-m

-4.5% y-o-y

50

150

250

350

450

550

Jan/

93Ja

n/94

Jan/

95Ja

n/96

Jan/

97Ja

n/98

Jan/

99Ja

n/00

Jan/

01Ja

n/02

Jan/

03Ja

n/04

Jan/

05Ja

n/06

Jan/

07Ja

n/08

Jan/

09Ja

n/10

Jan/

11Ja

n/12

Jan/

13Ja

n/14

Jan/

15Ja

n/16

Price Index (1999=100)Aug-16

-0.1% m-o-m-10.2% y-o-y

Source: Rating and Valuation Department Source: Rating and Valuation Department

Overall retail sales growth

Monthly retail sales growth of jewelleries/watches

(30)

(20)

(10)

0

10

20

30

40

Jan-

08Ju

l-08

Jan-

09Ju

l-09

Jan-

10Ju

l-10

Jan-

11Ju

l-11

Jan-

12Ju

l-12

Jan-

13Ju

l-13

Jan-

14Ju

l-14

Jan-

15Ju

l-15

Jan-

16Ju

l-16

Yoy, % Aug-16: -10.5% y-o-y

8M16: -10.2% y-o-y

(40)

(20)

0

20

40

60

80

Jan-

Feb

08Ju

n-08

Oct

-08

Mar

-09

Jul-0

9N

ov-0

9A

pr-1

0A

ug-1

0D

ec-1

0M

ay-1

1Se

p-11

Jan-

Feb

12Ju

n-12

Oct

-12

Mar

-13

Jul-1

3N

ov-1

3A

pr-1

4A

ug-1

4D

ec-1

4M

ay-1

5Se

p-15

Jan-

Feb

16Ju

n-16

Yoy, % Aug-16: -26.6% y-o-y

8M16: -22.5% y-o-y

Source: CEIC Source: CEIC

China / Hong Kong Monthly Chart Book

HK Property

Page 17

Monthly retail sales growth of consumer durable goods

Monthly retail sales growth of supermarket items

(30)

(20)

(10)

0

10

20

30

40

50

Jan-

Feb

08Ju

n-08

Oct

-08

Mar

-09

Jul-0

9N

ov-0

9A

pr-1

0A

ug-1

0D

ec-1

0M

a y-1

1Se

p-11

Jan-

Feb

12Ju

n-12

Oct

-12

Mar

-13

Jul-1

3N

ov-1

3A

pr-1

4A

ug-1

4D

ec-1

4M

ay-1

5Se

p-15

Jan-

Feb

16Ju

n-16

Yoy, % Aug-16: -23.9% y-o-y

8M16: -23.6% y-o-y

(2)0 2 4 6 8

10 12 14 16 18

Jan-

Feb

08Ju

n-08

Oct

-08

Mar

-09

Jul-0

9N

ov-0

9A

pr-1

0A

u g-1

0D

ec-1

0M

a y-1

1Se

p-11

Jan-

Feb

12Ju

n-12

Oct

-12

Mar

-13

Jul-1

3N

ov-1

3A

pr-1

4A

ug-1

4D

ec-1

4M

a y-1

5Se

p-15

Jan-

Feb

16Ju

n-16

Yoy, % Aug-16: -0.9% y-o-y

8M16: 0.9% y-o-y

Source: CEIC Source: CEIC

Visitor arrivals growth – overall

Visitor arrivals growth – China

(30)

(20)

(10)

0

10

20

30

40

50

Jan/

08Ju

l/08

Jan/

09Ju

l/09

Jan/

10Ju

l/10

Jan/

11Ju

l/11

Jan/

12Ju

l/12

Jan/

13Ju

l/13

Jan/

14Ju

l/14

Jan/

15Ju

l/15

Jan/

16Ju

l/16

Yoy, % Sep-16: -3% y-o-y-6.1% y-o-y9M16:

(40)

(30)

(20)

(10)

0

10

20

30

40

50

60

Jan/

08Ju

l/08

Jan/

09Ju

l/09

Jan/

10Ju

l/10

Jan/

11Ju

l/11

Jan/

12Ju

l/12

Jan/

13Ju

l/13

Jan/

14Ju

l/14

Jan/

15Ju

l/15

Jan/

16Ju

l/16

Yoy, %Sep-16: -5% y-o-y

-8.7% y-o-y9M16:

Source: CEIC Source: CEIC

China / Hong Kong Monthly Chart Book

HK Property

Page 18

What did corporates do?

Major corporate actions

Date Ev ent

30-Sep Lands Department announced the sale of a residential site located at Off Sin Fat Road, Kwun Tong, Kowloon through publictender which will close on 11 November. Total permissible gross floor area (GFA) for the residential site is 826,538sf.

30-Sep Lands Department announced the sale of a commercial site located at Kai Tak, Kowloon through public tender which will closeon 18 November. Total permissible GFA for the residential site is 1,097,315sf.

30-Sep Eleven developers submitted tenders for the residential site located at Beacon Hill, Kowloon.30-Sep Lai Sun Dev elopment sold 52 units in 93 Pau Chung Street, To Kwa Wan on the first day of its initial launch. This

represented 39% of the total units offered for sale02-Oct Henderson Land sold 33 units in Seven V ictory Avenue, Homantin on the first day of its initial launch. This represented

49% of the total units offered for sale04-Oct Wharf agreed to sell Wharf T&T to a consortium equally owned by MBK Partners Fund III, L.P. and TPG for HK$9.5bn05-Oct Eleven developers submitted tenders for URA's redevelopment project in Kowloon Road/Kiu Yam Road, Sham Shui Po.05-Oct Kerry Propert ies won the tender for the residential site in Kowloon, Beacon Hill for HK$7.269bn or HK$21,206psf.07-Oct Lands Department announced the sale of a residential site located at Lo Fai Road, Tai Po, New Territories through public tender

which will close on 4 November. Total permissible GFA for the residential site is 336,081sf.07-Oct Lands Department announced the sale of a residential site located at Lo Fai Road, Tai Po, New Territories through public tender

which will close on 4 November. Total permissible GFA for the residential site is 161,211sf.07-Oct Twenty four developers submitted tenders for the commercial site in Wong Chuk Hang11-Oct Three office floors (c.49,554sf) in Convention Office Plaza Tower, Wanchai was sold for a consideration of HK$1.39bn or

c.HK$28,000psf12-Oct A consortium comprising Sino land (60%) and Empire Group (40%) won the tender for the commercial site in Wong Chuk

Hang for a consideration of HK$2,528m or HK$8872psf.18-Oct Henderson Land sold 28 units in Park One, Sham Shui Po in the first day of its initial launch, representing 56% of the total

units on offer.20-Oct An office space (c.8,690sf) at IFC One in Central was leased to The Executive Centre at a monthly rent of HK$1.39m or

HK$160psf.23-Oct Wheelock sold 70 units in NAPA, Tuen Mun in the first day of its initial launch, representing 76% of the total units on offer.25-Oct Lai Sun Dev elopment and Walter Kwok sold 359 units in Alto Residence, Tseung Kwan O in the first two days of its initial

launch, representing 99% of the total units on offer.25-Oct Sino Land wins development rights for URA’s Kowloon Road/Kiu Yum Road redevelopment project in Sham Shui Po28-Oct Twenty developers submitted tenders for the residential site in Kai Tak28-Oct Link REIT intends to dispose five of its existing properties by way of tender which is scheduled to close on 15 Dec 2016.

These five properties comprises of a total internal floor area (IFA) of 420,225sf and an appraised value of HK$2,743m.28-Oct Sw ire Propert ies has agreed to sell its Kowloon Bay office property on en bloc basis for HK$6,528m or HK$11,761psf.29-Oct HKR Int'L sold 164 units in 2GETHER, Tuen Mun in the first day of its initial launch, representing 74% of the total units on

offer.

Source: DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 19

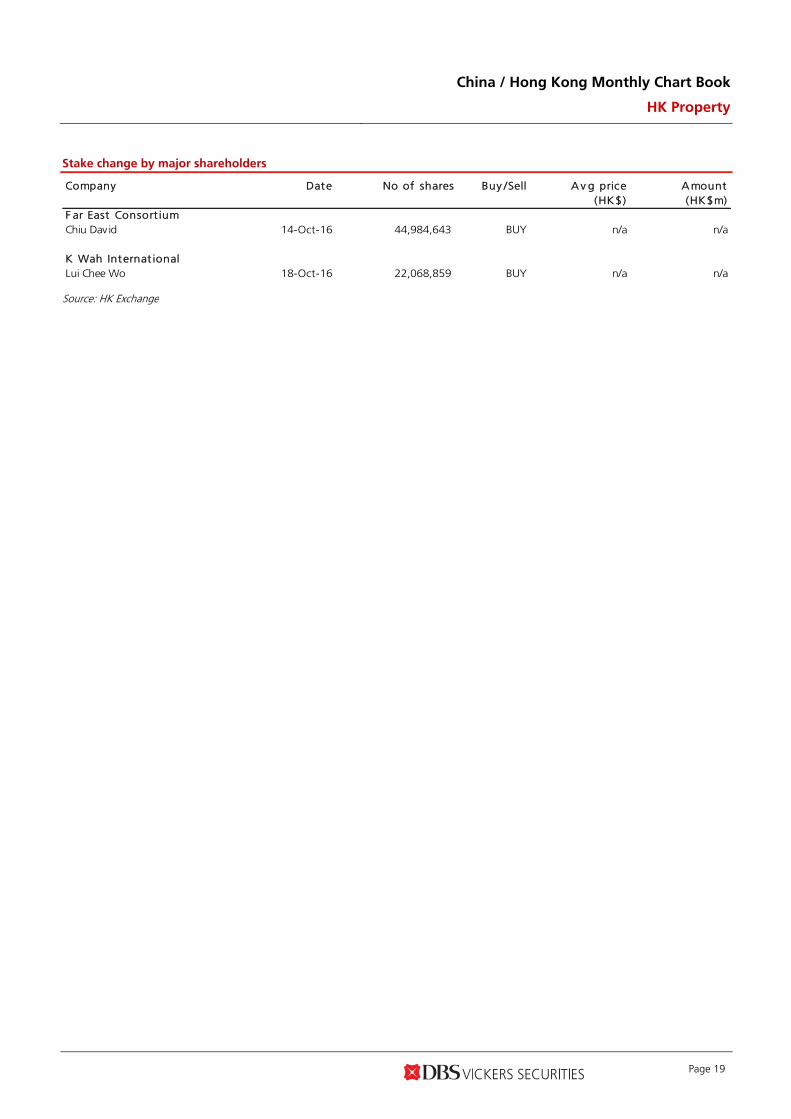

Stake change by major shareholders

Company Date No of shares Buy /Sell A v g price A mount(HK$) (HK$m)

F ar East Consort iumChiu David 14-Oct-16 44,984,643 BUY n/a n/a

K Wah Internat ionalLui Chee Wo 18-Oct-16 22,068,859 BUY n/a n/a

Source: HK Exchange

China / Hong Kong Monthly Chart Book

HK Property

Page 20

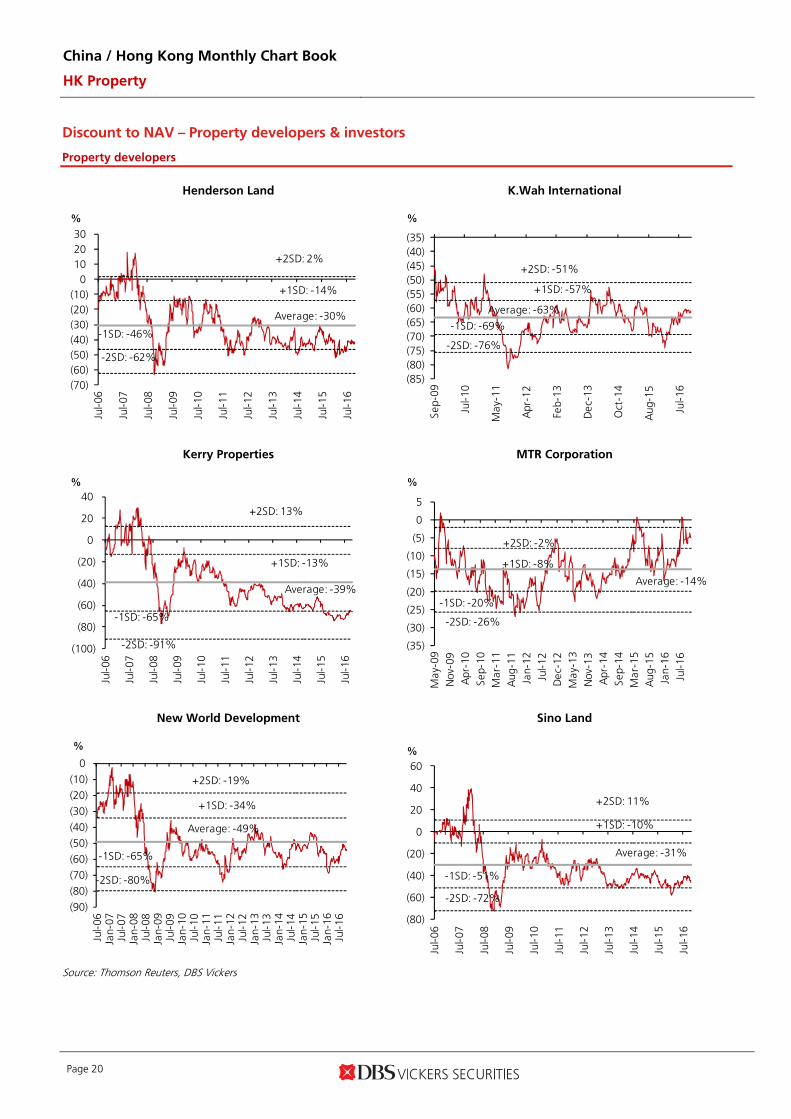

Discount to NAV – Property developers & investors

Property developers

Henderson Land K.Wah International

(70)(60)(50)(40)(30)(20)(10)

0 10 20 30

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

%

Average: -30%

+2SD: 2%

+1SD: -14%

-1SD: -46%

-2SD: -62%

(85)(80)(75)(70)(65)(60)(55)(50)(45)(40)(35)

Sep-

09

Jul-1

0

May

-11

Apr

-12

Feb-

13

Dec

-13

Oct

-14

Aug

-15

Jul-1

6

%

Average: -63%

+2SD: -51%

+1SD: -57%

-1SD: -69%

-2SD: -76%

Kerry Properties MTR Corporation

(100)

(80)

(60)

(40)

(20)

0

20

40

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

%

Average: -39%

+2SD: 13%

+1SD: -13%

-1SD: -65%

-2SD: -91%

(35)

(30)

(25)

(20)

(15)

(10)

(5)

0

5

May

-09

Nov

-09

Apr

-10

Sep-

10M

ar-1

1A

ug-1

1Ja

n-12

Jul-1

2D

ec-1

2M

ay-1

3N

ov-1

3A

pr-1

4Se

p-14

Mar

-15

Aug

-15

Jan-

16Ju

l-16

%

Average: -14%

+2SD: -2%

+1SD: -8%

-1SD: -20%

-2SD: -26%

New World Development Sino Land

(90)

(80)

(70)

(60)

(50)

(40)

(30)

(20)

(10)

0

Jul-0

6Ja

n-07

Jul-0

7Ja

n-08

Jul-0

8Ja

n-09

Jul-0

9Ja

n-10

Jul-1

0Ja

n-11

Jul-1

1Ja

n-12

Jul-1

2Ja

n-13

Jul-1

3Ja

n-14

Jul-1

4Ja

n-15

Jul-1

5Ja

n-16

Jul-1

6

%

Average: -49%

+2SD: -19%

+1SD: -34%

-1SD: -65%

-2SD: -80%

(80)

(60)

(40)

(20)

0

20

40

60

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

%

Average: -31%

+2SD: 11%

+1SD: -10%

-1SD: -51%

-2SD: -72%

Source: Thomson Reuters, DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 21

Property developers (continued)

Sun Hung Kai Properties Tai Cheung

(80)

(60)

(40)

(20)

0

20

40

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

%

Average: -25%

+2SD: 14%

+1SD: -5%

-1SD: -44%

-2SD: -64%

(90)

(80)

(70)

(60)

(50)

(40)

(30)

(20)

Jan-

07Ju

l-07

Feb-

08A

ug-0

8Fe

b-09

Sep-

09M

ar-1

0Se

p-10

Apr

-11

Oct

-11

Apr

-12

Oct

-12

May

-13

Nov

-13

May

-14

Dec

-14

Jun-

15D

ec-1

5Ju

l-16

%

Average: -62%

+2SD: -46%

+1SD: -54%

-1SD: -70%

-2SD: -78%

Wheelock & Co. Sector average

(60)

(50)

(40)

(30)

(20)

(10)

0

10

20

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

%

Average: -29%

+2SD: -3%

+1SD: -16%

-1SD: -42%

-2SD: -55%

(60)

(50)

(40)

(30)

(20)

(10)

0

10

20

30

Jul/0

6

Jul/0

7

Jul/0

8

Jul/0

9

Jul/1

0

Jul/1

1

Jul/1

2

Jul/1

3

Jul/1

4

Jul/1

5

Jul/1

6

%

+2SD: 3%

+1SD: -11%

Average: -26%

-1SD: -40%

-2SD: -54%

Source: Thomson Reuters, DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 22

Property investors

Great Eagle Hang Lung Properties

(90)

(80)

(70)

(60)

(50)

(40)

(30)

(20)

(10)

0

Jul-0

6

Mar

-08

Nov

-09

Aug

-11

Apr

-13

Dec

-14

Aug

-16

%

Average: -56%

-2SD: -76%

-1SD: -66%

+1SD: -45%

+2SD: -35%

(80)

(60)

(40)

(20)

0

20

40

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

%

Average: -19%

+2SD: 26%

+1SD: 4%

-1SD: -41%

-2SD: -63%

Hysan Swire Properties

(80)

(70)

(60)

(50)

(40)

(30)

(20)

(10)

0

Jul-0

6

Jul-0

8

Aug

-10

Aug

-12

Aug

-14

Sep-

16

%

Average: -39%

-2SD: -59%

-1SD: -49%

+1SD: -29%

+2SD: -18%

(55)(50)(45)(40)(35)(30)(25)(20)(15)(10)(5)

Jan-

12

Jun-

12

Nov

-12

Apr

-13

Sep-

13

Jan-

14

Jun-

14

Nov

-14

Apr

-15

Sep-

15

Feb-

16

Jul-1

6

%

Average: -34%

-2SD: -52%

-1SD: -43%

+1SD: -25%

+2SD: -16%

Wharf Sector average

(70)

(60)

(50)

(40)

(30)

(20)

(10)

0

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

%

Average: -30%

-2SD: -56%

-1SD: -43%

+1SD: -16%

+2SD: -3%

(70)

(60)

(50)

(40)

(30)

(20)

(10)

0

10

20

Jul/0

6

Jul/0

7

Jul/0

8

Jul/0

9

Jul/1

0

Jul/1

1

Jul/1

2

Jul/1

3

Jul/1

4

Jul/1

5

Jul/1

6

%

Average: -26%

+2SD: 4%

+1SD: -10%

-1SD: -37%

-2SD: -51%

Source: Thomson Reuters, DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

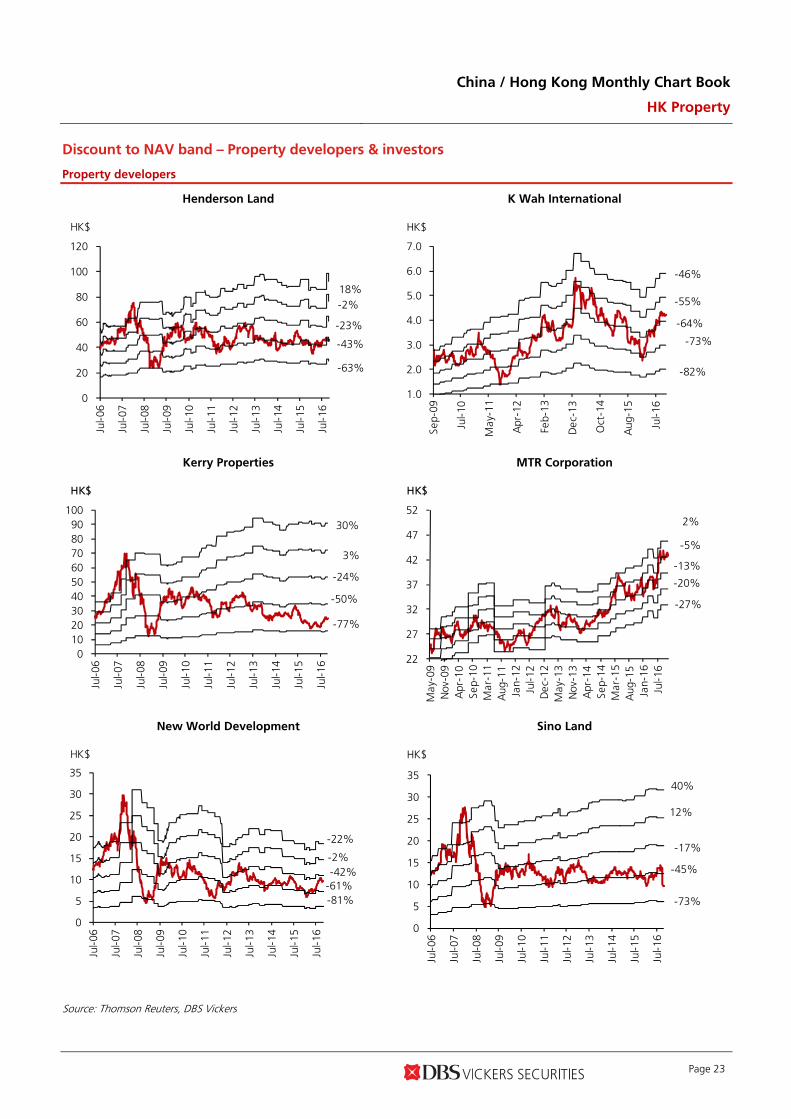

Page 23

Discount to NAV band – Property developers & investors

Property developers

Henderson Land K Wah International

0

20

40

60

80

100

120

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

HK$

-63%

-43%

-23%

-2%18%

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Sep-

09

Jul-1

0

May

-11

Apr

-12

Feb-

13

Dec

-13

Oct

-14

Aug

-15

Jul-1

6

HK$

-82%

-73%

-64%

-55%

-46%

Kerry Properties MTR Corporation

0 10 20 30 40 50 60 70 80 90

100

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

HK$

-77%

-24%

3%

30%

-50%

22

27

32

37

42

47

52

May

-09

Nov

-09

Apr

-10

Sep-

10M

ar-1

1A

ug-1

1Ja

n-12

Jul-1

2D

ec-1

2M

ay-1

3N

ov-1

3A

pr-1

4Se

p-14

Mar

-15

Aug

-15

Jan-

16Ju

l-16

HK$

-27%

-20%

-13%

-5%

2%

New World Development Sino Land

0

5

10

15

20

25

30

35

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

HK$

-81%-61%-42%

-22%

-2%

0

5

10

15

20

25

30

35

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

HK$

-73%

-45%

-17%

12%

40%

Source: Thomson Reuters, DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 24

Property developers (continued)

Sun Hung Kai Properties Tai Cheung

20

70

120

170

220

270

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

HK$

-58%

-14%

8%

30%

-36%

0

2

4

6

8

10

12

14

Jan-

07Ju

l-07

Feb-

08A

ug-0

8Fe

b-09

Sep-

09M

ar-1

0Se

p-10

Apr

-11

Oct

-11

Apr

-12

Oct

-12

May

-13

Nov

-13

May

-14

Dec

-14

Jun-

15D

ec-1

5Ju

l-16

HK$

-83%

-38%

-49%

-61%

-72%

Wheelock & Co.

0

10

20

30

40

50

60

70

80

90

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

HK$

-47%-31%-15%

1%17%

Source: Thomson Reuters, DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 25

Property investors

Great Eagle Hang Lung Properties

0

10

20

30

40

50

60

Jul-0

6Ja

n-07

Jul-0

7Ja

n-08

Jul-0

8Ja

n-09

Jul-0

9Ja

n-10

Jul-1

0Ja

n-11

Jul-1

1Ja

n-12

Jul-1

2Ja

n-13

Jul-1

3Ja

n-14

Jul-1

4Ja

n-15

Jul-1

5Ja

n-16

Jul-1

6

HK$

-82%

-67%

-53%

-39%

-25%

0

10

20

30

40

50

60

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

HK$

-61%

-37%

35%

13%

-9%

Hysan Swire Properties

3

13

23

33

43

53

63

Jul-0

6

Mar

-08

Nov

-09

Jul-1

1

Mar

-13

Nov

-14

Aug

-16

HK$

-69%

-54%

-40%

-25%

-10%

15

20

25

30

35

40

Jan-

12

Jun-

12

Nov

-12

Apr

-13

Sep-

13

Jan-

14

Jun-

14

Nov

-14

Apr

-15

Sep-

15

Feb-

16

Jul-1

6

HK$

-51%

-42%

-32%

-23%

-13%

Wharf

0 10 20 30 40 50 60 70 80 90

100

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

HK$

-66%

-1%

-17%

-33%

-50%

Source: Thomson Reuters, DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

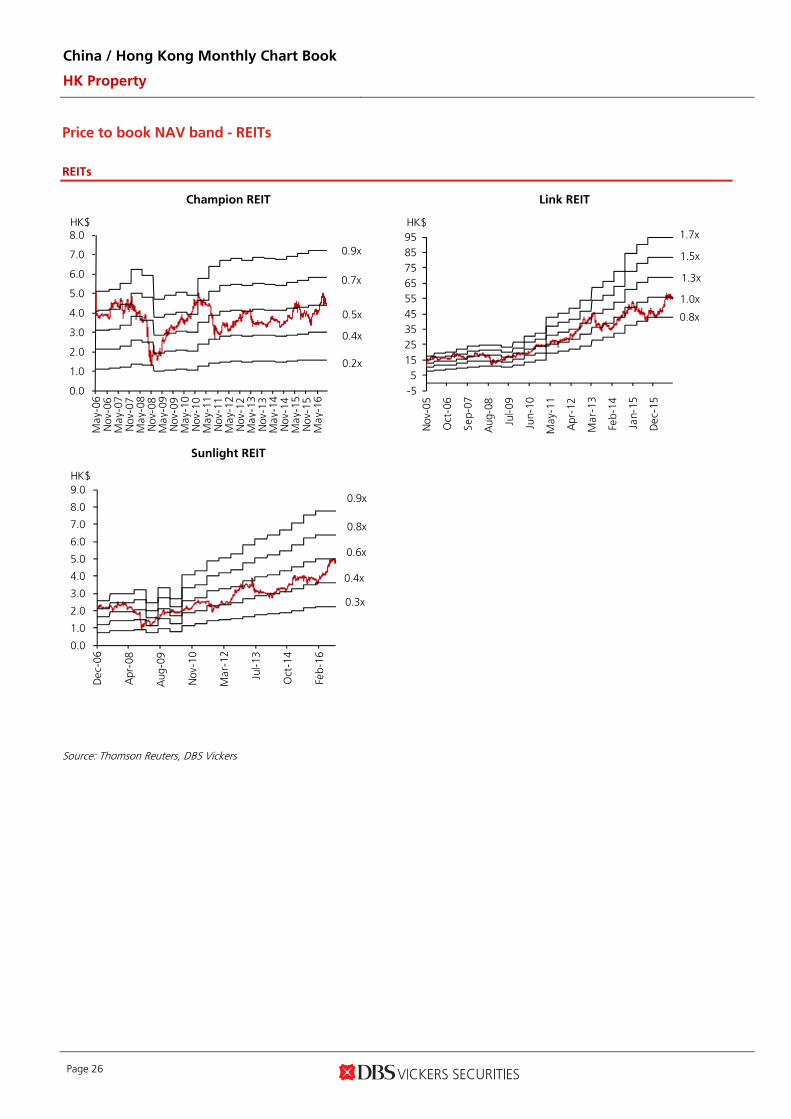

Page 26

Price to book NAV band - REITs

REITs

Champion REIT Link REIT

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

May

-06

Nov

-06

Ma y

-07

Nov

-07

Ma y

-08

Nov

-08

Ma y

-09

Nov

-09

Ma y

-10

Nov

-10

May

-11

Nov

-11

Ma y

-12

Nov

-12

Ma y

-13

Nov

-13

Ma y

-14

Nov

-14

Ma y

-15

Nov

-15

May

-16

HK$

0.2x

0.4x

0.5x

0.7x

0.9x

-55

152535455565758595

Nov

-05

Oct

-06

Sep-

07

Aug

-08

Jul-0

9

Jun-

10

May

-11

Apr

-12

Mar

-13

Feb-

14

Jan-

15

Dec

-15

HK$

0.8x

1.0x

1.3x

1.5x

1.7x

Sunlight REIT

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Dec

-06

Apr

-08

Aug

-09

Nov

-10

Mar

-12

Jul-1

3

Oct

-14

Feb-

16

HK$

0.3x

0.4x

0.6x

0.8x

0.9x

Source: Thomson Reuters, DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 27

Historical yield band - REITs

REITs

Champion REIT Link REIT

0

1

2

3

4

5

6

7

8

9

May

-06

Nov

-06

May

-07

Nov

-07

May

-08

Nov

-08

May

-09

Nov

-09

May

-10

Nov

-10

May

-11

Nov

-11

May

-12

Nov

-12

May

-13

Nov

-13

May

-14

Nov

-14

May

-15

Nov

-15

May

-16

HK$

Floor 24%

Ceiling 4%

Champion REIT

Mid 14%

5

15

25

35

45

55

65

75

Nov

-05

Oct

-06

Sep-

07

Aug

-08

Jul-0

9

Jun-

10

May

-11

Apr

-12

Mar

-13

Feb-

14

Jan-

15

Dec

-15

HK$

Link REIT

Ceiling 3% Mid 5%

Floor 7%

Sunlight REIT

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Dec

-06

Apr

-08

Aug

-09

Nov

-10

Mar

-12

Jul-1

3

Oct

-14

Feb-

16

HK$

Sunlight REIT

Ceiling 5%

Mid 15%

Floor 25%

Source: Thomson Reuters, DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 28

Any important dates to look out for?

Major upcoming events

3-Nov Retail statistics for Sep 20164-Nov TPTL 223 Tender Close4-Nov TPTL 229 Tender Close11-Nov GDP 3Q1611-Nov NKIL 6584 Tender Close17-Nov Unemployment rate Aug 2016 - Oct 201618-Nov NKIL 6557 Tender Close22-Nov CPI October 2016

1-Dec Retail statistics for Oct 201619-Dec Unemployment rate Sep 2016 - Nov 201620-Dec CPI November 2016

3-Jan Retail statistics for Nov 201619-Jan Unemployment rate Oct 2016 - Dec 201623-Jan CPI December 2016

December 2016

J anuary 2016

Nov ember 2016

Source: Census and Statistics Department, Lands Department, HK Exchange, DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 29

Our past publications

Date Publicat ion

1 Aug (Hysan Development ) 1H16 result preview 3 Aug (Hysan Development ) Higher dividend amidst challenging retail scene 3 Aug (HK Property) Pak Shek Kok ?a source of residential supply 5 Aug (Champion REIT) 1H16 result preview 8 Aug (MTR Corporation) 1H16 result preview 8 Aug (Wharf Holdings) 1H16 result preview 9 Aug (HK Property Sector) Replenishing land banks 10 Aug (MTR Corporation) Fairly priced 10 Aug (Champion REIT) Harvest time for Three Garden Road 11 Aug (Wharf Holdings) Firm rental performance despite market challenges 12 Aug (Wheelock) 1H16 result preview 15 Aug (Swire Properties ) 1H16 result preview 16 Aug (Great Eagle ) 1H16 result preview 16 Aug (Wheelock) Wheelock & Co 18 Aug (Great Eagle ) Core business operations improving 18 Aug (Kerry Properties ) 1H16 result preview 19 Aug (Swire Properties ) Expanding rental asset base 19 Aug (K Wah International) 1H16 result preview 22 Aug (Henderson Land ) 1H16 result preview 23 Aug (Kerry Properties ) China project sales is a bright spot 23 Aug (K Wah International) Robust development earnings 24 Aug (Henderson Land ) Steady climb 25 Aug (Sino Land ) Enviable balance sheet strength 29 Aug (Wing Tai Properties) 1H16 result preview 31 Aug (Wing Tai Properties) Strong asset backing 31 Aug (HK Property) Growing office supply in Kowloon East

1 Sep (HK Property) Growing office supply in Kowloon East 2 Sep (Sunlight REIT) FY16 Results Preview 6 Sep (Sunlight REIT) Ongoing revitalisation initiatives to unlock hidden value 7 Sep (SHKP ) FY16 results preview 9 Sep (SHKP ) Firing on all cylinders 19 Sep (Lai Sun Development) New project launch to unlock embedded value 19 Sep (Henderson Land ) Windfall profit from property disposal 22 Sep (New World Development) Right direction 28 Sep (Far East Consortium) Encouraging project sales, recovering hotel operations

4 Oct (Hong Kong Property Sector) Retail supply in focus 5 Oct (Wharf Holdings) Realising the value of telecom business 6 Oct (Link REIT) Solid retail leasing performance 13 Oct (Sunlight REIT) Asset enhancement initiative to bear fruit soon 20 Oct (Lai Sun Development) Harvest season is coming 24 Oct (Wharf Holdings) Mount Nicholson apartments well sought after 25 Oct (Lai Sun Development) Overwhelming response to the Alto Residences launch 25 Oct (Tai Cheung) To benefit from robust demand for luxury homes

October 2016

September 2016

August 2016

Source: DBS Vickers

China / Hong Kong Monthly Chart Book

HK Property

Page 30

DBSVHK recommendations are based an Absolute Total Return* Rating system, defined as follows:

STRONG BUY (>20% total return over the next 3 months, with identifiable share price catalysts within this time frame)

BUY (>15% total return over the next 12 months for small caps, >10% for large caps)

HOLD (-10% to +15% total return over the next 12 months for small caps, -10% to +10% for large caps)

FULLY VALUED (negative total return i.e. > -10% over the next 12 months)

SELL (negative total return of > -20% over the next 3 months, with identifiable catalysts within this time frame)

Share price appreciation + dividends Completed Date: 3 Nov 2016 15:03:20 Dissemination Date: 3 Nov 2016 15:22:26

GENERAL DISCLOSURE/DISCLAIMER This report is prepared by DBS Vickers (Hong Kong) Limited (“DBSVHK”). This report is solely intended for the clients of DBS Bank Ltd., DBS Vickers Securities (Singapore) Pte Ltd. (“DBSVS”) and DBSVHK, its respective connected and associated corporations and affiliates only and no part of this document may be (i) copied, photocopied or duplicated in any form or by any means or (ii) redistributed without the prior written consent of DBSVHK. The research set out in this report is based on information obtained from sources believed to be reliable, but we (which collectively refers to DBS Bank Ltd., DBSVS and DBSVHK, its respective connected and associated corporations, affiliates and their respective directors, officers, employees and agents (collectively, the “DBS Group”)) do not make any representation or warranty as to its accuracy, completeness or correctness. Opinions expressed are subject to change without notice. This document is prepared for general circulation. Any recommendation contained in this document does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. This document is for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate independent legal or financial advice. The DBS Group accepts no liability whatsoever for any direct, indirect and/or consequential loss (including any claims for loss of profit) arising from any use of and/or reliance upon this document and/or further communication given in relation to this document. This document is not to be construed as an offer or a solicitation of an offer to buy or sell any securities. The DBS Group, along with its affiliates and/or persons associated with any of them may from time to time have interests in the securities mentioned in this document. The DBS Group may have positions in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking services for these companies. Any valuations, opinions, estimates, forecasts, ratings or risk assessments herein constitutes a judgment as of the date of this report, and there can be no assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or risk assessments. The information in this document is subject to change without notice, its accuracy is not guaranteed, it may be incomplete or condensed, it may not contain all material information concerning the company (or companies) referred to in this report and the DBS Group is under no obligation to update the information in this report. This publication has not been reviewed or authorized by any regulatory authority in Singapore, Hong Kong or elsewhere. There is no planned schedule or frequency for updating research publication relating to any issuer. The valuations, opinions, estimates, forecasts, ratings or risk assessments described in this report were based upon a number of estimates and assumptions and are inherently subject to significant uncertainties and contingencies. It can be expected that one or more of the estimates on which the valuations, opinions, estimates, forecasts, ratings or risk assessments were based will not materialize or will vary significantly from actual results. Therefore, the inclusion of the valuations, opinions, estimates, forecasts, ratings or risk assessments described herein IS NOT TO BE RELIED UPON as a representation and/or warranty by the DBS Group (and/or any persons associated with the aforesaid entities), that: (a) such valuations, opinions, estimates, forecasts, ratings or risk assessments or their underlying assumptions will be achieved, and (b) there is any assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or risk assessments

stated therein. Please contact the primary analyst for valuation methodologies and assumptions associated with the covered companies or price targets. Any assumptions made in this report that refers to commodities, are for the purposes of making forecasts for the company (or companies) mentioned herein. They are not to be construed as recommendations to trade in the physical commodity or in the futures contract relating to the commodity referred to in this report. DBS Vickers Securities (USA) Inc ("DBSVUSA"), a U.S.-registered broker-dealer, does not have its own investment banking or research department, has not participated in any public offering of securities as a manager or co-manager or in any other investment banking transaction in the past twelve months and does not engage in market-making.

China / Hong Kong Monthly Chart Book

HK Property

Page 31

ANALYST CERTIFICATION The research analyst(s) primarily responsible for the content of this research report, in part or in whole, certifies that the views about the companies and their securities expressed in this report accurately reflect his/her personal views. The analyst(s) also certifies that no part of his/her compensation was, is, or will be, directly or indirectly, related to specific recommendations or views expressed in the report. The DBS Group has procedures in place to eliminate, avoid and manage any potential conflicts of interests that may arise in connection with the production of research reports. As of 3 November 2016, the analyst(s) and his/her spouse and/or relatives who are financially dependent on the analyst(s), do not hold interests in the securities recommended in this report (“interest” includes direct or indirect ownership of securities). The research analyst(s) responsible for this report operates as part of a separate and independent team to the investment banking function of the DBS Group and procedures are in place to ensure that confidential information held by either the research or investment banking function is handled appropriately.

COMPANY-SPECIFIC / REGULATORY DISCLOSURES 1. DBSVHK and its subsidiaries do not have a proprietary position in the securities recommended/mentioned in this report as of 02 Nov

2016.

2. DBS Bank Ltd., DBSVS, DBSVHK, DBSVUSA, their subsidiaries and/or other affiliates have a net long position exceeding 0.5% of the total issued share capital in Jinmao Investments & Jinmao (China) (6139 HK) and Yuexiu Real Estate Investment Trust (405 HK) recommended in this report as of 01 Nov 2016.

3. DBS Bank Ltd., DBSVS, DBSVHK, DBSVUSA, their subsidiaries and/or other affiliates beneficially own a total of 1% of any class of common equity securities of Yuexiu Real Estate Investment Trust (405 HK) as of 01 Nov 2016.

4. Compensation for investment banking services: DBS Bank Ltd., DBSVS, DBSVHK, their subsidiaries and/or other affiliates of DBSVUSA have received compensation, within the past 12 months for investment banking services from Link Real Estate Investment Trust (823 HK), Yuexiu Real Estate Investment Trust (405 HK) and Far East Consortium International Limited (35 HK) as of 30 Sep 2016. DBS Bank Ltd., DBSVS, DBSVHK, their subsidiaries and/or other affiliates of DBSVUSA have managed or co-managed a public offering of securities for Far East Consortium International Limited (35 HK) in the past 12 months, as of 30 Sep 2016. DBSVUSA does not have its own investment banking or research department, nor has it participated in any public offering of securities as a manager or co-manager or in any other investment banking transaction in the past twelve months. Any US persons wishing to obtain further information, including any clarification on disclosures in this disclaimer, or to effect a transaction in any security discussed in this document should contact DBSVUSA exclusively.

RESTRICTIONS ON DISTRIBUTION

General This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

Australia This report is being distributed in Australia by DBS Bank Ltd. (“DBS”) or DBS Vickers Securities (Singapore) Pte Ltd (“DBSVS”) or DBS Vickers (Hong Kong) Limited (“DBSVHK”), which are exempted from the requirement to hold an Australian Financial Services Licence under the Corporation Act 2001 (“CA”) in respect of financial services provided to the recipients. Both DBS and DBSVS are regulated by the Monetary Authority of Singapore under the laws of Singapore, and DBSVHK is regulated by the Securities and Futures Commission of Hong Kong under the laws of Hong Kong, which differ from Australian laws. Distribution of this report is intended only for “wholesale investors” within the meaning of the CA.

Hong Kong This report is being distributed in Hong Kong by DBSVHK which is licensed and regulated by the Hong Kong Securities and Futures Commission.

Indonesia This report is being distributed in Indonesia by PT DBS Vickers Securities Indonesia.

Malaysia This report is distributed in Malaysia by AllianceDBS Research Sdn Bhd ("ADBSR"). Recipients of this report, received from ADBSR are to contact the undersigned at 603-2604 3333 in respect of any matters arising from or in connection with this report. In addition to the General Disclosure/Disclaimer found at the preceding page, recipients of this report are advised that ADBSR (the preparer of this report), its holding company Alliance Investment Bank Berhad, their respective connected and associated corporations, affiliates, their directors, officers, employees, agents and parties related or associated with any of them may have positions in, and may effect transactions in the securities mentioned herein and may also perform or seek to perform broking, investment banking/corporate advisory and other services for the subject companies. They may also have received compensation and/or seek to obtain compensation for broking, investment banking/corporate advisory and other services from the subject companies.

Wong Ming Tek, Executive Director, ADBSR

China / Hong Kong Monthly Chart Book

HK Property

Page 32

Singapore This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) or DBSVS (Company Regn No. 198600294G), both of which are Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd and/or DBSVS, may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 6327 2288 for matters arising from, or in connection with the report.

Thailand This report is being distributed in Thailand by DBS Vickers Securities (Thailand) Co Ltd. Research reports distributed are only intended for institutional clients only and no other person may act upon it.

United Kingdom