China Consumer - · PDF fileChina | Consumer China Consumer 10 July 2014 China Consumer Hard...

78

China | Consumer China Consumer 10 July 2014 China Consumer Hard Choices: The Impact of E-commerce EQUITY RESEARCH CHINA Jessie Guo, PhD * Equity Analyst +852 3743 8036 [email protected] Edwin Fan, CFA * Equity Analyst +852 3743 8037 [email protected] Kevin Chee, CFA * Equity Analyst 852 3743 8022 [email protected] Jeffrey Zeng * Equity Associate +852 3743 8009 [email protected] * Jefferies Hong Kong Limited Key Takeaway This research unveils the business model evolution of a consumer sector facing an E-commerce boom. We find that E-commerce poses a serious threat to most traditional retailers but benefits certain sectors/brands: dept. stores and domestic apparel/footwear get hit most; leading global apparel brands seem to leverage it to enhance branding; sportswear uses it as an effective tool for cleaning out inventory; restaurants and jewelers have held up relatively well. What makes this research different? We conducted large-scale data-mining to unveil the business model evolution and key characteristics of traditional retailing in the era of E-commerce. We studied more than 100,000 items sold online, covering almost all major consumer subsectors. Our research studies not only the competitive landscape change caused by E-commerce and brands’ marketing strategy but also makes thorough comparisons amongst E-tailers and traditional retailers covering a wide range of areas such as ASPs, profitability, consumer feedback, etc. We also refer to a survey led by Southwestern University of Finance and Economics, studying households' online spending behaviour through in-depth face-to-face interviews with more than 22,000 Chinese households. We expect our study from a supply perspective and CHFS’s survey from a demand perspective to provide investors with a comprehensive angle to understand E-commerce’s impact on consumer sectors. Key findings. Online shopping is fast changing people’s daily purchasing behaviour and the competitive landscape of consumer sectors: 1) Online cosmetics retailing gains momentum and poses a serious challenge to traditional cosmetics retailing and even cosmetics brands with self-owned stores. 2) Restaurants could benefit since online group- purchasing moderately stimulates traffic and does not hurt margins. 3) Jewelers could boost their branding through online channels which also enjoys higher margins than retail stores. 4) Mass-market department stores are heavily losing customers to online retail and face structural issues and a dilemma: aggressive participation in E-commerce will cause price cannibalization and lower margins; not doing so means worse market share-loss. 5) Traditional supermarkets are losing consumers as well but those with a larger proportion of fresh products and with large numbers of CVS are relatively less impacted. 6) We think a solution for electronics retailers lies in the integration of logistics management and after-sales service into online platforms. 7) We observe that apparel and footwear brands get hurt most. Online sales will further gain market share and offline stores have to lower ASPs and face decelerating margins in the future. In contrast, international brands take market share from local brands and gain popularity through online platforms. 8) Local sportswear is better off than local apparel and footwear brands due to relatively higher entry barriers. We believe this sector has troughed as indicated by lower inventory days and reduced promotions. Sector and stock implications. We maintain a positive view on sportswear; a neutral view on staples, jewellery and electronics distributors; and a negative view on apparel, footwear, department stores, supermarkets and traditional cosmetics distributors. Staples trade at 21x 12-month forward PE vs. a historical median of 24x. Retailers trade at 13.5x 12- month forward PE vs. a historical median of 17x, whereas apparel trades at 13x 12-month forward PE vs. a historical median of 18-20x. Staples underperformed HSCEI by 2% in the past month, while retailers and apparel outperformed by 2% and 1% , respectively. Top Buys: Anta (2020 HK), CTF (1929 HK), CMD (1117 HK), Biostime (1112 HK) and Tingyi (322 HK). Top Sells: Belle (1880 HK), Sasa (178 HK), Tsingtao (168 HK, 600600 CH), Vinda (3331 HK), Parkson (3368 HK) and Giordano (709 HK). Jefferies does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that Jefferies may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 74 to 78 of this report.

Transcript of China Consumer - · PDF fileChina | Consumer China Consumer 10 July 2014 China Consumer Hard...

China | Consumer

China Consumer 10 July 2014

China ConsumerHard Choices: The Impact of E-commerce

EQU

ITY R

ESEARC

H C

HIN

A

Jessie Guo, PhD *Equity Analyst

+852 3743 8036 [email protected] Fan, CFA *

Equity Analyst+852 3743 8037 [email protected]

Kevin Chee, CFA *Equity Analyst

852 3743 8022 [email protected] Zeng *Equity Associate

+852 3743 8009 [email protected]

* Jefferies Hong Kong Limited

Key Takeaway

This research unveils the business model evolution of a consumer sector facingan E-commerce boom. We find that E-commerce poses a serious threat tomost traditional retailers but benefits certain sectors/brands: dept. stores anddomestic apparel/footwear get hit most; leading global apparel brands seemto leverage it to enhance branding; sportswear uses it as an effective tool forcleaning out inventory; restaurants and jewelers have held up relatively well.

What makes this research different? We conducted large-scale data-mining to unveilthe business model evolution and key characteristics of traditional retailing in the eraof E-commerce. We studied more than 100,000 items sold online, covering almost allmajor consumer subsectors. Our research studies not only the competitive landscapechange caused by E-commerce and brands’ marketing strategy but also makes thoroughcomparisons amongst E-tailers and traditional retailers covering a wide range of areas suchas ASPs, profitability, consumer feedback, etc. We also refer to a survey led by SouthwesternUniversity of Finance and Economics, studying households' online spending behaviourthrough in-depth face-to-face interviews with more than 22,000 Chinese households. Weexpect our study from a supply perspective and CHFS’s survey from a demand perspectiveto provide investors with a comprehensive angle to understand E-commerce’s impact onconsumer sectors.

Key findings. Online shopping is fast changing people’s daily purchasing behaviourand the competitive landscape of consumer sectors: 1) Online cosmetics retailing gainsmomentum and poses a serious challenge to traditional cosmetics retailing and evencosmetics brands with self-owned stores. 2) Restaurants could benefit since online group-purchasing moderately stimulates traffic and does not hurt margins. 3) Jewelers couldboost their branding through online channels which also enjoys higher margins than retailstores. 4) Mass-market department stores are heavily losing customers to online retailand face structural issues and a dilemma: aggressive participation in E-commerce will causeprice cannibalization and lower margins; not doing so means worse market share-loss. 5)Traditional supermarkets are losing consumers as well but those with a larger proportionof fresh products and with large numbers of CVS are relatively less impacted. 6) We thinka solution for electronics retailers lies in the integration of logistics management andafter-sales service into online platforms. 7) We observe that apparel and footwear brandsget hurt most. Online sales will further gain market share and offline stores have to lowerASPs and face decelerating margins in the future. In contrast, international brands takemarket share from local brands and gain popularity through online platforms. 8) Localsportswear is better off than local apparel and footwear brands due to relatively higherentry barriers. We believe this sector has troughed as indicated by lower inventory days andreduced promotions.

Sector and stock implications. We maintain a positive view on sportswear; a neutralview on staples, jewellery and electronics distributors; and a negative view on apparel,footwear, department stores, supermarkets and traditional cosmetics distributors. Staplestrade at 21x 12-month forward PE vs. a historical median of 24x. Retailers trade at 13.5x 12-month forward PE vs. a historical median of 17x, whereas apparel trades at 13x 12-monthforward PE vs. a historical median of 18-20x. Staples underperformed HSCEI by 2% in thepast month, while retailers and apparel outperformed by 2% and 1% , respectively. TopBuys: Anta (2020 HK), CTF (1929 HK), CMD (1117 HK), Biostime (1112 HK) and Tingyi (322HK). Top Sells: Belle (1880 HK), Sasa (178 HK), Tsingtao (168 HK, 600600 CH), Vinda (3331HK), Parkson (3368 HK) and Giordano (709 HK).

Jefferies does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that Jefferies may have aconflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investmentdecision. Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 74 to 78 ofthis report.

Table of contents

Executive summary: Methodology and key findings 3

The era of E-commerce 15

The impact of E-commerce

Cosmetics 19

Restaurants 29

Jewellery 34

Electronic goods 42

Apparel, footwear and sportswear 50

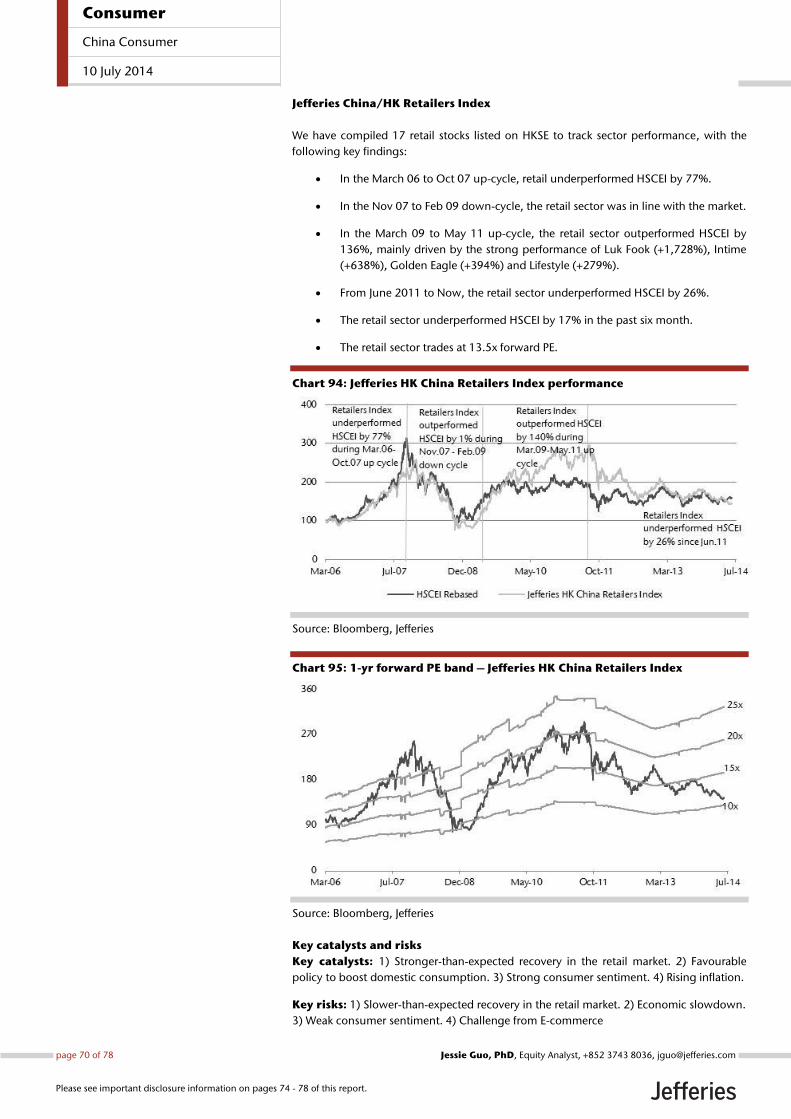

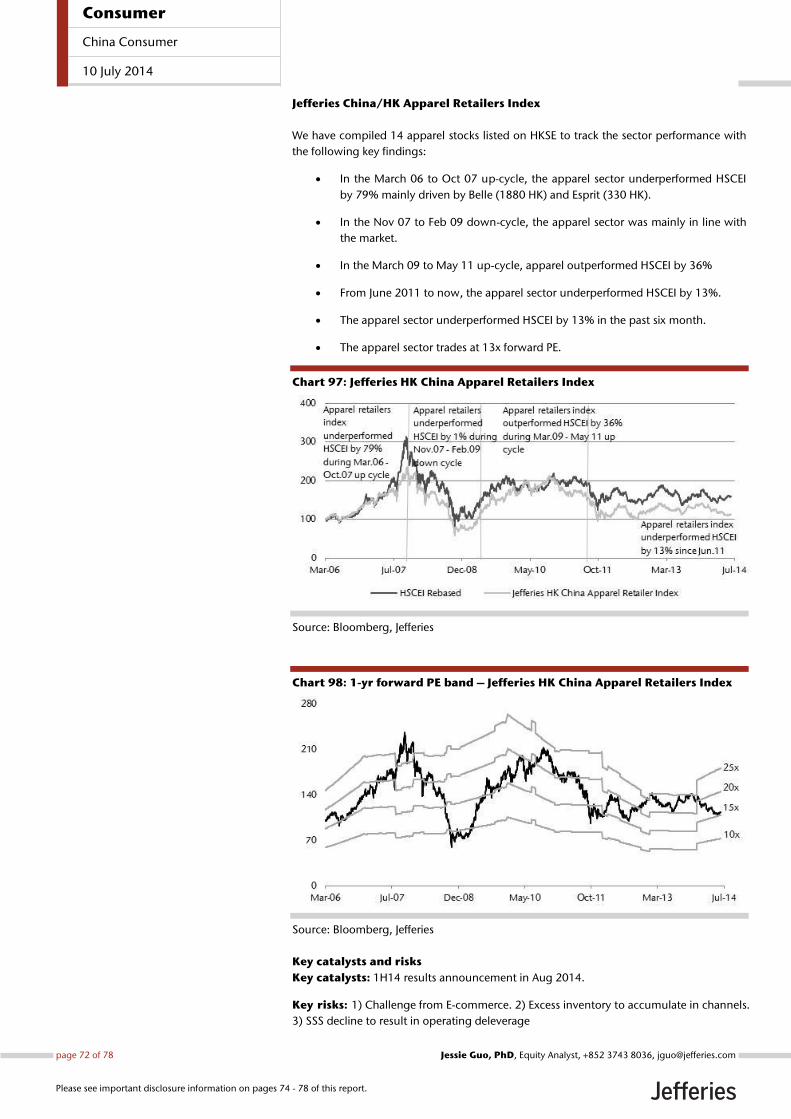

Sector performance and valuation 67

Consumer

China Consumer

10 July 2014

page 2 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

Executive summary Key takeaway

Through large-scale data-mining, this study seeks to unveil the business model evolution

of the consumer sector in the face of the E-commerce boom. We find that E-commerce

poses a serious threat to most traditional retailers but benefits certain sectors/brands:

department stores and domestic apparel/footwear get hit most; leading global apparel

brands seem to leverage it to enhance branding recognition; sportswear uses it as an

effective tool for cleaning up inventory; and restaurants and jewellers have held up

relatively well.

We maintain a positive view on sportswear; a neutral view on staples, jewellery and

electronics retailers; and a negative view on apparel, footwear, department stores,

supermarkets and traditional cosmetics retailers. Top Buys: CTF (1929 HK), Anta (2020

HK), Biostime (1112 HK), CMD (1117 HK), Tingyi (322 HK). Top Sells: Belle (1880 HK),

Sasa (178 HK), Tsingtao (168 HK, 600600 CH), Vinda (3331 HK), Parkson (3368 HK), and

Giordano (709 HK).

Research Methodology We studied all major online retail platforms with a wide array of coverage: from

household products, apparel, footwear, sportswear and jewellery to cosmetics and

restaurants. Our samples exceed 100,000 items and cover almost all major brands in each

consumer subsector. Through large-scale data-mining we try to compare the different

performance and business model evolution of both E-tailers and traditional retailers and

consumer brands covering a wide array of areas such as ASP, profitability, consumer

feedback, etc. We also take a qualitative approach to explain the current competitive

landscape and predict its future trajectory. Last but not least, we draw conclusions on

sector preferences and stock recommendations.

In this research, we also refer to databases from iResearch and the US Department of

Commerce, as well as research led by Southwestern University of Finance and Economics.

The 2nd round of the China Household Finance Survey (CHFS) 2013 studies households’

online spending behaviour through in-depth face-to-face interviews with more than

22,000 households. In order to reduce sample bias, this study considers a sound mixture

of survey participants including rural vs. urban households, communities with different

wealth status and professional backgrounds; geographical selections and educational

background.

We expect our large-scale online data-mining from a supply perspective and studies by

other authorities from a demand perspective to provide investors with a comprehensive

understanding of the penetration of E-commerce in the consumer sector.

Key findings E-commerce is coming, at a pace faster than expected

China has become the largest online retail market and its penetration grows at a much

faster pace than other developed economies. We observe the following key features: 1) as

consumers become more sophisticated and counterfeit products become a concern, the

B2C format is quickly overriding the C2C format; 2) the B2C market is set to undergo

consolidation; thus, building up a successful and sustainable platform requires a wide

range of strategies and strong execution; 3) O2O integration provides better consumer

satisfaction and can be a meaningful competitive advantage for both retailers and E-

tailers; 4) mobile/Wechat-made retail gains stronger momentum from PC-made retail.

Online cosmetics retailing gains momentum

Online distribution of cosmetic products is becoming a strong competitive force to

traditional retail channels. Penetration of online sales of cosmetics (out of total retail sales

of cosmetics) increased from 3.8% in 2011 to 6.6% in 2012 and 10.2% in 2013. It is

expected to reach 21.9% in 2018e. This will increasingly pose challenges to traditional

Consumer

China Consumer

10 July 2014

page 3 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

department stores and offline cosmetics retailers such as Sasa (178 HK, Underperform),

Bonjour (653 HK, NC), Colourmix (owned by Veeko Holdings; 1173 HK, NC), Sephora

(owned by LVMH group; MC FP, NC), and even brands with self-owned stores such as

L’Occitaine (973 HK, Hold), Body Shop (owned by L’Oreal; OR FP, Hold), etc.

We believe Sasa is less competitive compared with Jumei (JMEI US, NC) and Vipshop (VIPS

US, Buy). The fundamentals and growth potential of Jumei in particular are likely to

outstrip Vipshop and Sasa due to its wide product range and relatively low pricing that

meets the needs of a stable/rising consumer base with monthly income of RMB5,000-

8,000.

Vipshop (VIPS, Buy) has its niche serving sophisticated consumers with higher purchasing

power. In contrast, Sasa’s business model is facing a serious challenge: its online channel

is much less competitive than close rivals. It can hardly help to offset headwinds that its

retail stores face: a slowdown in the number of mainland travellers, a weak Hong Kong

retail environment and difficulty in raising ASP.

Restaurants could benefit from online platforms

We believe online group-purchasing moderately stimulates traffic of conventional

restaurants, in particular those with mass market positioning. It does not pose a challenge

to overall margins of participating restaurants due to its small portion of sales

contribution (0.7% in 2013), albeit with heavy discounts for those items.

Online offerings are smartly used by restaurants; in particular those newly opened, as an

effective marketing tool to enhance brand awareness. It is also used to encourage visits in

non-peak hours and to specific locations. (74% and 90% of the deals on Dianping and

Meituan are restricted to certain hours or locations).

However, the online channel does not seem to be an effective tool for mainstream chain

stores such as KFC (owned by YUM! Brands YUM US, Hold), McDonald’s (MCD US, Hold),

Ajisen (538 HK, NC), Starbucks (SBUX US, Buy), Café De Coral (341 HK, NC), Tsui Wah

(1314 HK, NC), and Fairwood (52 HK, NC). This is because 1) They already have a wide

range of retail store coverage while online consumers are more inclined to try new

restaurants/cuisine types; 2) They already have strong brand awareness.

E-commerce boosts jewellery branding

The penetration of e-commerce sales in jewellery in China is as low as c1-2% of total

jewellery sales but we expect E-commerce to become a platform to boost sales and

enhance brand image. Gold products sold better than gem-set jewellery due to the

homogeneity of gold products vs gem-set jewellery. In addition, gold products sold on

line are at a lower ASP vs gem-set jewellery.

The EBIT margin from online sold gold/jewellery products is higher than those sold offline.

This phenomenon is different from the apparel, footwear and sportswear brands, mainly

because jewellery brands are reluctant to offer significant price discounts for an identical

product sold online, while offline stores have to bear heavy fixed costs.

We prefer the business model of self-operated stores which has the potential to leverage

online channels to enhance its branding image to stimulate both online and offline sales.

In contrast, brands adopting a franchisee model are conservative in online expansion

since they try to protect licensees from potential cannibalization of online sales.

We favour CTF (1929 HK, Buy, PT HKD13) and CSS (116 HK, Hold, PT HKD21.3) to Luk

Fook (590 HK, Hold, PT HKD23.1). We believe CTF and Chow Sang Sang are well-

positioned for online expansion due to their business model of self-operated stores.

According to CTF, e-commerce retail sales rose 91% YoY in FY14 while the company had

an overall 122,000 online visitors in FY14 (+51% YoY). Luk Fook (590 HK, Hold) is much

more conservative with online expansion in order to protect franchisees’ business.

Consumer

China Consumer

10 July 2014

page 4 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

A mixed picture for supermarkets

It was rather surprising to see as high as c30% of people surveyed by CHFS did online

shopping for daily FMCG products such as toothpaste, tissue paper and shampoo, which

are a significant proportion of supermarkets’ turnover. However, online shopping for

finished F&B goods is high- single digit to low-teens; and fruits and vegetables are only

low single digit. The implication is that traditional supermarkets with a larger proportion

of fresh products and supermarket operators with a large number of CVS’ won’t be

impacted meaningfully in the future. We expect Sunart (6808 HK, NC), Lianhua (980 HK,

NC), and Wumart (1025 HK, NC) to face rising competition from online. In contrast, CRE

(291 HK) is relatively better off due to its multi-format strategies (with CVS, high-end

supermarkets, beer businesses).

A serious threat to mass-market department stores

Shopping malls and department stores with mass-market positioning are losing

customers to E-shops. We found that 75% of items sold online are priced below RMB300

and online shoppers are highly price sensitive. In addition, the aggressive expansion that

the sector experienced in the past few years (at >20% CAGR for GFA increase) as well as

the government’s anti-waste/corruption policy put pressure on sales growth. We believe

this sector is facing structural headwinds with high-end department stores and beauty

salons being exceptions.

We believe Intime (1833 HK, Hold) and Lifestyle (1212 HK, Buy) are relatively better

positioned than other department stores such as Parkson (3368 HK, Underperform).

On/offline integration is key to electronics retailers

Standardized products are at the forefront of the competition. We think the solution lies in

online/offline integration. Challenges to traditional electronic goods retailers such as

Gome (493 HK, Buy) and Suning (002024 CH, Hold) have existed for a few years.

However, we think they have advantages of inventory and logistics management and

after-sales service, which are not easy to replace.

Local apparel/footwear brands get hit most

We believe online sales of apparel and footwear will further gain share from retail stores

due to cheaper prices offered by online channels, convenience for consumers, and easier

logistics arrangement. Local brands face a structural challenge due to the large price gap

between online and offline. Local brands’ ASP in traditional retail stores are 30-40%

higher than e-retailers. As a result, retail stores generate higher EBIT margins at 13-14%

compared with 9-10% from online. We believe this trend is unsustainable and expect

offline channels to cut price so as to narrow gaps with online channels. This will

unavoidably lower their margins (given constant other factors). Such a structural

headwind has no ready-made prescription, unfortunately.

This situation applies to almost all major local brands: Belle (1880 HK, Underperform),

Giordano (709 HK, Underperform), Daphne (210 HK, Hold), Trinity (891 HK, Hold), China

Lilang (1234 HK, Hold), Metersbonwe (002269 CH, NC), Semir (002563 CH, NC) and

Septwolves (002029 CH, NC).

….yet international apparel/footwear brands reap the harvest

International apparel and footwear brands take market share from local brands and gain

rising popularity from Chinese consumers in 1st and 2nd tier cities; in particular, brands

like Zara (Inditex, ITX SM, Hold), H&M (HMB SS, Underperform) and Uniqlo (Fast Retailing,

9983 JP, NC). This is due to better product offering, stronger marketing and better

consumer services. We expect online channels to become important channels for

international brands to further enhance their presence.

Sportswear troughed and held up relatively well

Local sportswear held up relatively well compared with local apparel and footwear brands

in the face of E-commerce penetration. The entry barrier to this industry is higher than

apparel. Large brands make serious efforts in brand-enhancement. We believe the sector

Consumer

China Consumer

10 July 2014

page 5 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

has troughed as indicated by lower inventory days and reduced promotions. Thus we take

a positive view on sportswear.

We have Buy ratings on Anta (2020 HK, Buy, PT HKD13.5), Li Ning (2331 HK, Buy, PT

HKD7.5) and Xtep (1368 HK, Buy, PT HKD4.5). We have an Underperform rating on Belle

(1880 HK, PT HKD6.8) and Giordano (709 HK, PT HKD3.9), and Hold ratings on Daphne

(210 HK, Hold, PT HKD3.2), Trinity (891 HK, Hold, PT HKD1.9) and China Lilang (1234 HK,

Hold, PT HKD4.6). The following sessions introduce our research methodology and data

analysis.

Sector valuation and stock picks We maintain a positive view on sportswear; a neutral view on staples, jewellery and

electronics retailers; and a negative view on apparel, footwear, department stores,

supermarkets and traditional cosmetics retailers.

Staples trade at 21x 12-month forward PE vs. a historical median of 24x. Retailers trade at

13.5x 12-month forward PE vs. a historical median of 17x, whereas apparels trade at 13x

12-month forward PE vs. a historical median of 18-20x. Staples underperformed the HSCEI

by 2% in the past one month, retailers outperformed by 2% and apparels outperformed

by 1%.

Top Picks: Anta (2020 HK), CTF (1929 HK), Biostime (1112 HK), CMD (1117 HK), Tingyi

(322 HK).

Top Sells: Belle (1880 HK), Sasa (178 HK), Tsingtao (168 HK, 600600 CH), Vinda (3331

HK), Parkson (3368 HK) and Giordano (709 HK).

Chart 1: E-commerce impact and investment view on sub-sectors

Source: Jefferies

Consumer Subsector Impact from e-commerce

Mass-market department stores Heavily negative

Traditional electronics retailers Moderately negative K

Traditional supermarkets Negative

Consumer staples Neutral K

Domestic apparel and footwear Heavily negative

Global apparel and footwear Moderately positive

Domestic sportswear Netural to moderately positive

Traditional cosmetics retailers Negative

Global cosmetics brands Positive

Jewellers Positive K

Restaurants Positive

Our investment

view

Consumer

China Consumer

10 July 2014

page 6 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

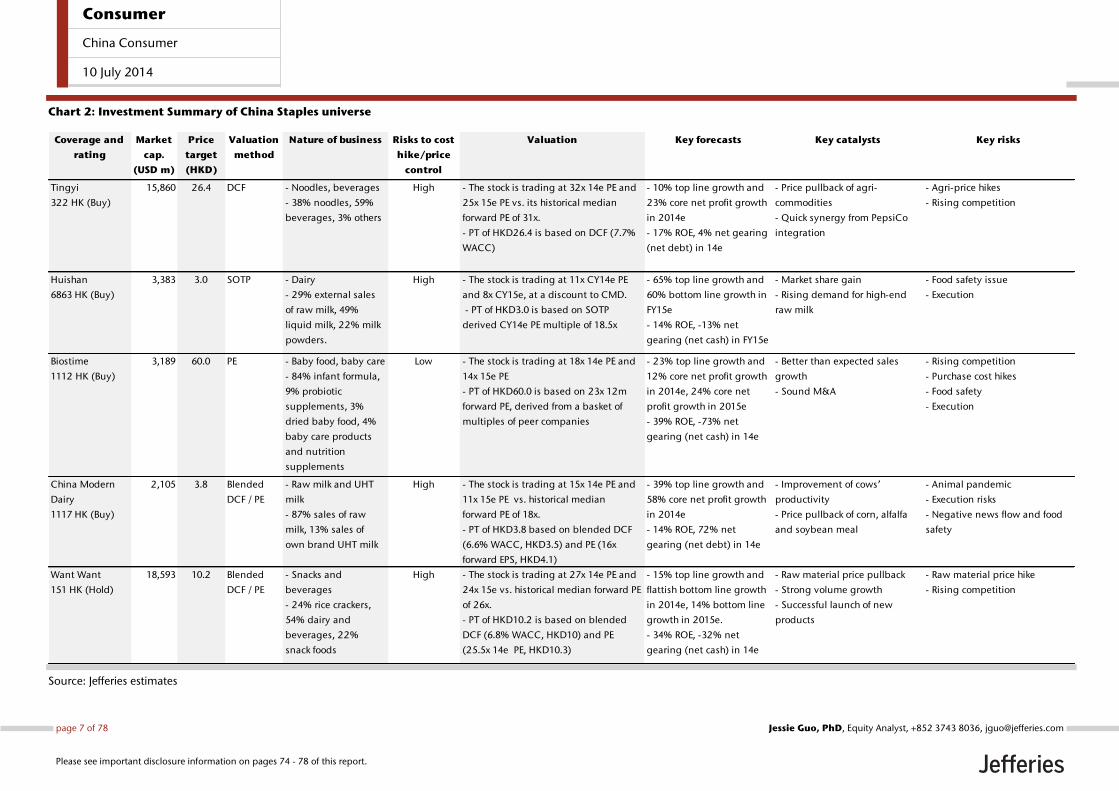

Chart 2: Investment Summary of China Staples universe

Source: Jefferies estimates

Coverage and

rating

Market

cap.

(USD m)

Price

target

(HKD)

Valuation

method

Nature of business Risks to cost

hike/price

control

Valuation Key forecasts Key catalysts Key risks

Tingyi

322 HK (Buy)

15,860 26.4 DCF - Noodles, beverages

- 38% noodles, 59%

beverages, 3% others

High - The stock is trading at 32x 14e PE and

25x 15e PE vs. its historical median

forward PE of 31x.

- PT of HKD26.4 is based on DCF (7.7%

WACC)

- 10% top line growth and

23% core net profit growth

in 2014e

- 17% ROE, 4% net gearing

(net debt) in 14e

- Price pullback of agri-

commodities

- Quick synergy from PepsiCo

integration

- Agri-price hikes

- Rising competition

Huishan

6863 HK (Buy)

3,383 3.0 SOTP - Dairy

- 29% external sales

of raw milk, 49%

liquid milk, 22% milk

powders.

High - The stock is trading at 11x CY14e PE

and 8x CY15e, at a discount to CMD.

- PT of HKD3.0 is based on SOTP

derived CY14e PE multiple of 18.5x

- 65% top line growth and

60% bottom line growth in

FY15e

- 14% ROE, -13% net

gearing (net cash) in FY15e

- Market share gain

- Rising demand for high-end

raw milk

- Food safety issue

- Execution

Biostime

1112 HK (Buy)

3,189 60.0 PE - Baby food, baby care

- 84% infant formula,

9% probiotic

supplements, 3%

dried baby food, 4%

baby care products

and nutrition

supplements

Low - The stock is trading at 18x 14e PE and

14x 15e PE

- PT of HKD60.0 is based on 23x 12m

forward PE, derived from a basket of

multiples of peer companies

- 23% top line growth and

12% core net profit growth

in 2014e, 24% core net

profit growth in 2015e

- 39% ROE, -73% net

gearing (net cash) in 14e

- Better than expected sales

growth

- Sound M&A

- Rising competition

- Purchase cost hikes

- Food safety

- Execution

China Modern

Dairy

1117 HK (Buy)

2,105 3.8 Blended

DCF / PE

- Raw milk and UHT

milk

- 87% sales of raw

milk, 13% sales of

own brand UHT milk

High - The stock is trading at 15x 14e PE and

11x 15e PE vs. historical median

forward PE of 18x.

- PT of HKD3.8 based on blended DCF

(6.6% WACC, HKD3.5) and PE (16x

forward EPS, HKD4.1)

- 39% top line growth and

58% core net profit growth

in 2014e

- 14% ROE, 72% net

gearing (net debt) in 14e

- Improvement of cows’

productivity

- Price pullback of corn, alfalfa

and soybean meal

- Animal pandemic

- Execution risks

- Negative news flow and food

safety

Want Want

151 HK (Hold)

18,593 10.2 Blended

DCF / PE

- Snacks and

beverages

- 24% rice crackers,

54% dairy and

beverages, 22%

snack foods

High - The stock is trading at 27x 14e PE and

24x 15e vs. historical median forward PE

of 26x.

- PT of HKD10.2 is based on blended

DCF (6.8% WACC, HKD10) and PE

(25.5x 14e PE, HKD10.3)

- 15% top line growth and

flattish bottom line growth

in 2014e, 14% bottom line

growth in 2015e.

- 34% ROE, -32% net

gearing (net cash) in 14e

- Raw material price pullback

- Strong volume growth

- Successful launch of new

products

- Raw material price hike

- Rising competition

Consumer

China Consumer

10 July 2014

page 7 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

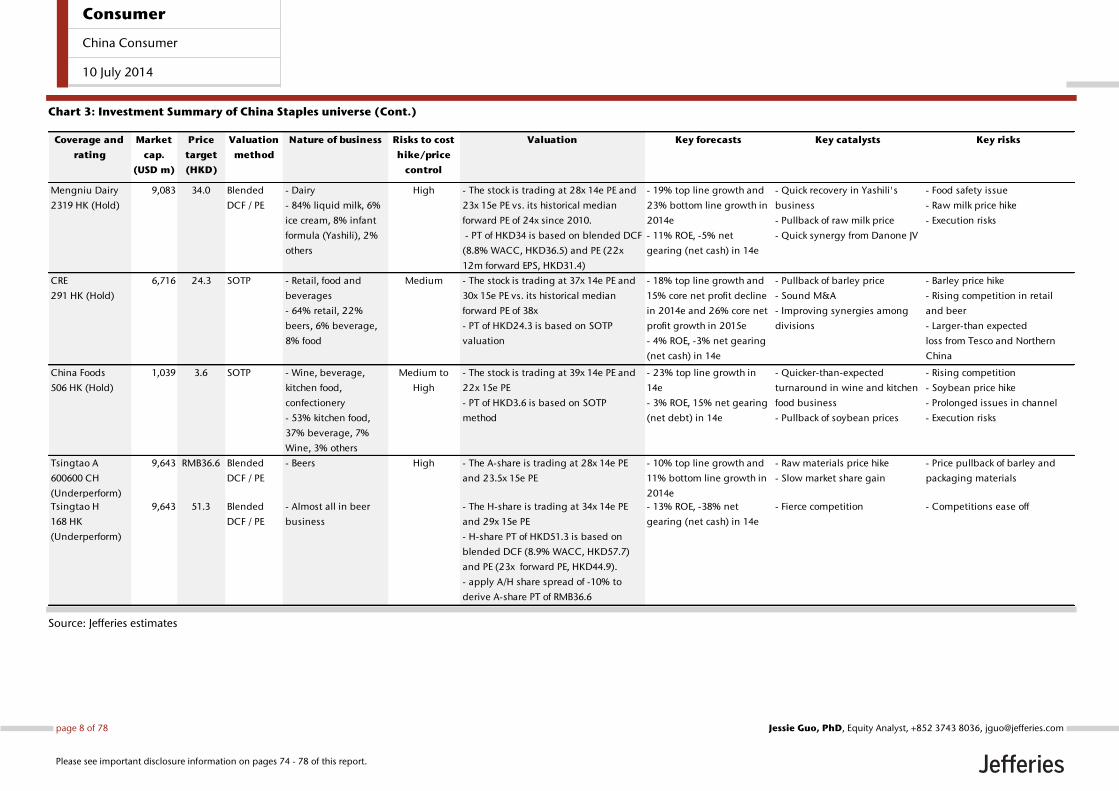

Chart 3: Investment Summary of China Staples universe (Cont.)

Source: Jefferies estimates

Coverage and

rating

Market

cap.

(USD m)

Price

target

(HKD)

Valuation

method

Nature of business Risks to cost

hike/price

control

Valuation Key forecasts Key catalysts Key risks

Mengniu Dairy

2319 HK (Hold)

9,083 34.0 Blended

DCF / PE

- Dairy

- 84% liquid milk, 6%

ice cream, 8% infant

formula (Yashili), 2%

others

High - The stock is trading at 28x 14e PE and

23x 15e PE vs. its historical median

forward PE of 24x since 2010.

- PT of HKD34 is based on blended DCF

(8.8% WACC, HKD36.5) and PE (22x

12m forward EPS, HKD31.4)

- 19% top line growth and

23% bottom line growth in

2014e

- 11% ROE, -5% net

gearing (net cash) in 14e

- Quick recovery in Yashili's

business

- Pullback of raw milk price

- Quick synergy from Danone JV

- Food safety issue

- Raw milk price hike

- Execution risks

CRE

291 HK (Hold)

6,716 24.3 SOTP - Retail, food and

beverages

- 64% retail, 22%

beers, 6% beverage,

8% food

Medium - The stock is trading at 37x 14e PE and

30x 15e PE vs. its historical median

forward PE of 38x

- PT of HKD24.3 is based on SOTP

valuation

- 18% top line growth and

15% core net profit decline

in 2014e and 26% core net

profit growth in 2015e

- 4% ROE, -3% net gearing

(net cash) in 14e

- Pullback of barley price

- Sound M&A

- Improving synergies among

divisions

- Barley price hike

- Rising competition in retail

and beer

- Larger-than expected

loss from Tesco and Northern

China

China Foods

506 HK (Hold)

1,039 3.6 SOTP - Wine, beverage,

kitchen food,

confectionery

- 53% kitchen food,

37% beverage, 7%

Wine, 3% others

Medium to

High

- The stock is trading at 39x 14e PE and

22x 15e PE

- PT of HKD3.6 is based on SOTP

method

- 23% top line growth in

14e

- 3% ROE, 15% net gearing

(net debt) in 14e

- Quicker-than-expected

turnaround in wine and kitchen

food business

- Pullback of soybean prices

- Rising competition

- Soybean price hike

- Prolonged issues in channel

- Execution risks

Tsingtao A

600600 CH

(Underperform)

9,643 RMB36.6 Blended

DCF / PE

- Beers High - The A-share is trading at 28x 14e PE

and 23.5x 15e PE

- 10% top line growth and

11% bottom line growth in

2014e

- Raw materials price hike

- Slow market share gain

- Price pullback of barley and

packaging materials

Tsingtao H

168 HK

(Underperform)

9,643 51.3 Blended

DCF / PE

- Almost all in beer

business

- The H-share is trading at 34x 14e PE

and 29x 15e PE

- H-share PT of HKD51.3 is based on

blended DCF (8.9% WACC, HKD57.7)

and PE (23x forward PE, HKD44.9).

- apply A/H share spread of -10% to

derive A-share PT of RMB36.6

- 13% ROE, -38% net

gearing (net cash) in 14e

- Fierce competition - Competitions ease off

Consumer

China Consumer

10 July 2014

page 8 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

Chart 4: Investment Summary of China Staples universe (Cont.)

Source: Jefferies estimates

Coverage and

rating

Market

cap.

(USD m)

Price

target

(HKD)

Valuation

method

Nature of business Risks to cost

hike/price

control

Valuation Key forecasts Key catalysts Key risks

Hengan

1044 HK (Hold)

13,122 84.6 Blended

DCF and PE

Tissue, disposable

diapers and sanitary

napkins

- 47% tissue products,

30% sanitary napkins,

13% disposable

diapers, 16% others

High - The stock is trading at 26x 14e PE and

22x 15e PE, vs. its historical median

forward PE of 26x (3 years average).

- PT of HKD84.6 is based on blended

DCF (6.6% WACC, HKD100.4) and PE

(20x 12m forward PE, HKD68.8)

- 14% sales growth and 5%

net profit growth in 2014e

- 23% ROE, -5% net

gearing (net cash)

- Wood pulp and petro-chemical

cost pullback

- Pricing pressure eases on

rational competition

- Better-than-expected 1H14

results

- Wood pulp cost hike

- Intensifying competition

- Price competition in mid-low

end diapers market

- Worse-than-expected 1H14

results

Vinda

3331 HK

(Underperform)

1,463 9.6 Blended

DCF and PE

Tissue High - The stock is trading at 23x 14e PE and

19x 15e PE, vs. historical median

forward PE of 20x (3 years average)

- PT of HKD9.6 is based on blended DCF

(7.3% WACC, HKD10.1) and PE (17x

12m forward PE, HKD9.2)

- 10% sales growth and 8%

net profit decline in 2014e

- 10% ROE, 50% net

gearing (net debt) for

2014e

- Wood pulp cost hike

- Intensifying competition

- ASP pressure due to industry

overcapacity issue

- Worse-than-expected result in

1H14

- Wood pulp cost pullback

- Quick ramp up in the sanitary

napkin and baby diapers

business under associate

company

- Large synergy from potential

cooperation with SCA

- Better-than-expected 1H14

results

Consumer

China Consumer

10 July 2014

page 9 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

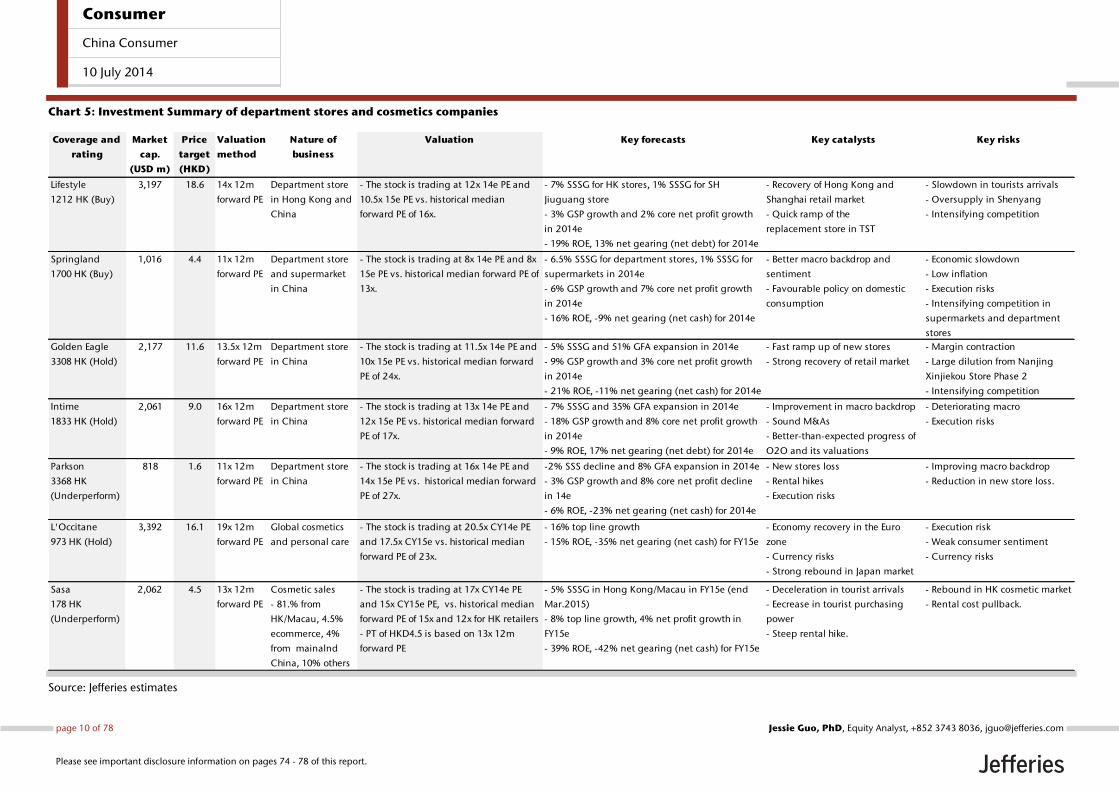

Chart 5: Investment Summary of department stores and cosmetics companies

Source: Jefferies estimates

Coverage and

rating

Market

cap.

(USD m)

Price

target

(HKD)

Valuation

method

Nature of

business

Valuation Key forecasts Key catalysts Key risks

Lifestyle

1212 HK (Buy)

3,197 18.6 14x 12m

forward PE

Department store

in Hong Kong and

China

- The stock is trading at 12x 14e PE and

10.5x 15e PE vs. historical median

forward PE of 16x.

- 7% SSSG for HK stores, 1% SSSG for SH

Jiuguang store

- 3% GSP growth and 2% core net profit growth

in 2014e

- 19% ROE, 13% net gearing (net debt) for 2014e

- Recovery of Hong Kong and

Shanghai retail market

- Quick ramp of the

replacement store in TST

- Slowdown in tourists arrivals

- Oversupply in Shenyang

- Intensifying competition

Springland

1700 HK (Buy)

1,016 4.4 11x 12m

forward PE

Department store

and supermarket

in China

- The stock is trading at 8x 14e PE and 8x

15e PE vs. historical median forward PE of

13x.

- 6.5% SSSG for department stores, 1% SSSG for

supermarkets in 2014e

- 6% GSP growth and 7% core net profit growth

in 2014e

- 16% ROE, -9% net gearing (net cash) for 2014e

- Better macro backdrop and

sentiment

- Favourable policy on domestic

consumption

- Economic slowdown

- Low inflation

- Execution risks

- Intensifying competition in

supermarkets and department

stores

Golden Eagle

3308 HK (Hold)

2,177 11.6 13.5x 12m

forward PE

Department store

in China

- The stock is trading at 11.5x 14e PE and

10x 15e PE vs. historical median forward

PE of 24x.

- 5% SSSG and 51% GFA expansion in 2014e

- 9% GSP growth and 3% core net profit growth

in 2014e

- 21% ROE, -11% net gearing (net cash) for 2014e

- Fast ramp up of new stores

- Strong recovery of retail market

- Margin contraction

- Large dilution from Nanjing

Xinjiekou Store Phase 2

- Intensifying competition

Intime

1833 HK (Hold)

2,061 9.0 16x 12m

forward PE

Department store

in China

- The stock is trading at 13x 14e PE and

12x 15e PE vs. historical median forward

PE of 17x.

- 7% SSSG and 35% GFA expansion in 2014e

- 18% GSP growth and 8% core net profit growth

in 2014e

- 9% ROE, 17% net gearing (net debt) for 2014e

- Improvement in macro backdrop

- Sound M&As

- Better-than-expected progress of

O2O and its valuations

- Deteriorating macro

- Execution risks

Parkson

3368 HK

(Underperform)

818 1.6 11x 12m

forward PE

Department store

in China

- The stock is trading at 16x 14e PE and

14x 15e PE vs. historical median forward

PE of 27x.

-2% SSS decline and 8% GFA expansion in 2014e

- 3% GSP growth and 8% core net profit decline

in 14e

- 6% ROE, -23% net gearing (net cash) for 2014e

- New stores loss

- Rental hikes

- Execution risks

- Improving macro backdrop

- Reduction in new store loss.

L'Occitane

973 HK (Hold)

3,392 16.1 19x 12m

forward PE

Global cosmetics

and personal care

- The stock is trading at 20.5x CY14e PE

and 17.5x CY15e vs. historical median

forward PE of 23x.

- 16% top line growth

- 15% ROE, -35% net gearing (net cash) for FY15e

- Economy recovery in the Euro

zone

- Currency risks

- Strong rebound in Japan market

- Execution risk

- Weak consumer sentiment

- Currency risks

Sasa

178 HK

(Underperform)

2,062 4.5 13x 12m

forward PE

Cosmetic sales

- 81.% from

HK/Macau, 4.5%

ecommerce, 4%

from mainalnd

China, 10% others

- The stock is trading at 17x CY14e PE

and 15x CY15e PE, vs. historical median

forward PE of 15x and 12x for HK retailers

- PT of HKD4.5 is based on 13x 12m

forward PE

- 5% SSSG in Hong Kong/Macau in FY15e (end

Mar.2015)

- 8% top line growth, 4% net profit growth in

FY15e

- 39% ROE, -42% net gearing (net cash) for FY15e

- Deceleration in tourist arrivals

- Eecrease in tourist purchasing

power

- Steep rental hike.

- Rebound in HK cosmetic market

- Rental cost pullback.

Consumer

China Consumer

10 July 2014

page 10 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

Chart 6: Investment Summary of jewellery and watch retailers

Source: Jefferies estimates

Coverage and

rating

Market

cap

(USD m)

Price

target

(HKD)

Valuation

method

Nature of business Risk to gold

price

fluctuation

Valuation Key forecasts Key catalysts Key risks

Chow Tai Fook

1929 HK (Buy)

15,380 13.0 1-year

forward PE

- Sells gold, gem-set jewellery and

watches in HK, Macau and China

through self-operated shops and

franchisee stores.

- Revenue contribution: China 55%,

HK/Macau and others 45%

Low: Company

hedges 70% of

gold inventory

- The stock is trading at

17x CY14e and 15x

CY15e PE, vs historical 1-

year forward PE of 16x.

- PT of HKD13.0 is based

on 18x 1-year forward PE

- 7% revenue drop and 4% net

profit drop for FY15e, but 11%

revenue growth and 16% net profit

growth in FY16e (end March).

- 18% ROE and 11% gearing for

FY15e; 19% ROE and 12% gearing

for FY16e

1QFY15e

operational

updates in Jul14

- Downside risks: Gold price

drop may cause valuations

to de-rate, despite CTF

hedges 70% of gold.

- Sales may further drop in

HK on lower tourist

spending.

Luk Fook

590 HK (Hold)

1,832 23.1 1-year

forward PE

- Sells gold, gem-set jewellery and

watches in HK, Macau and China

through self-operated and licensee

shops.

- Revenue contribution: China self-

operated shops: 9%, HK/Macau 76%,

licensing fees: 3%, wholesaling 12%

High: Company

hedges 20% of

gold inventory

- The stock is trading at

9x CY14e and 8x CY15e

PE, vs 3-year average 1-

year forward PE at 10x.

- PT of HKD23.1 is based

on 8.5x 1-year forward PE

- 13% revenue drop and 17% net

profit drop for FY15e, but 7%

revenue growth and 16% net profit

growth in FY16e (end March).

- 19% ROE and -24% gearing (net

cash) for FY15e; 20% ROE and -28%

gearing for FY16e

1QFY15e

operational

updates in Jul14

- Upside risk: jewellery

sales to recover in HK, Luk

Fook benefits the most

- Downside risk: Gold price

drop may cause valuations

to de-rate.

Chow Sang Sang

116 HK (Hold)

1,777 21.3 1-year

forward PE

- Sells gold, gem-set jewellery and

watches in HK, Macau and China

through self-operated shops only. Also

wholesales precious metals to smaller

scale HK-based jewellery retailers.

- Revenue contribution: HK/Macau

49%, China 30%, Taiwan 2%,

wholesale and others 25%

Medium:

Company hedges

40% of gold

inventory

- The stock is trading at

11x CY14e and 10x

CY15e PE, vs 3-year

average 1-year forward

PE at 12x.

- PT of HKD21.3 is based

on 11x 1-year forward PE

- 6% revenue drop and 5% net

profit growth for 2014e, and 7%

revenue growth and 11% net profit

growth in 2015e (end Dec).

- 15% ROE and 4% gearing for

2014e; 15% ROE and 1% gearing

for 2015e

1H14 results

announcement in

Aug14

- Upside risk: jewellery

sales to recover in HK

- Downside risk: Gold price

drop may cause valuations

to de-rate.

Hengdeli

3389 HK (Hold)

855 1.5 1-year

forward PE

- Sells luxury and mass market Swiss

watches in Greater China

- Revenue contribution: China 40%,

HK/Macau: 33%, Taiwan 2%,

wholesale and customer services: 25%

Low: according to

the Federation of

Swiss Watch

Industry, less

than 2% of Swiss

watches' raw

material are from

gold

- The stock is trading at

10x CY14e and 10x

CY15e PE, vs 3-year

average 1-year forward

PE at 14x.

- PT of HKD1.5 is based

on 11x 1-year forward PE

- 3% revenue growth and 29% net

profit growth for 2014e, and 4%

revenue growth and 6% net profit

growth in 2015e (end Dec).

- 9% ROE and 28% gearing for

2014e; 9% ROE and 23% gearing

for 2015e

1H14 results

announcement in

Aug14

- Upside risk: Relief in anti-

corruption measures which

may result in rebound of

Swiss watch sales.

- Downside risk:

Continuous slowdown in

demand for luxury watches;

Consumer

China Consumer

10 July 2014

page 11 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

Chart 7: Investment Summary of sportswear companies

Source: Jefferies estimates

Coverage

and rating

Market

cap

(USD m)

Price

target

(HKD)

Valuation

methodNature of business Risk to cost hike Valuation Key forecasts Key catalysts Key risks

Anta Sports

2020 HK

(Buy)

4,193 13.5 Blended

DCF/ PE

- Manufactures and wholesales

domestic sportswear products under

Anta Brand and Fila in China

- Revenue contribution: 47% from

footwear, 49% from apparel, 4% from

accessories, c95% of revenue are

generated from wholesaling

Medium: Company can

improve product mix to

mitigate labour cost

growth

- The stock is trading at 18x

CY14e PE and 15x CY15e PE

vs. 3-year average 1-year

forward PE of 13x.

- Based on blended DCF/14x

1-year forward ex-cash PE,

we derive PT of HKD13.5 for

Anta, equivalent to 16.5x 1-

year forward PE

- 11% revenue growth and 15% net

profit decline for 2014e, and 8%

revenue growth and 15% net profit

growth in 2015e (end Dec).

- 20% ROE and -70% gearing (net

cash) for 2014e

1H14 financial

results and 1Q15e

trade fair orders in

Aug14

- E-retailing cannibalizes

traditional channels;

- Competition from

international and local

sportswear brands;

- Growing rental and retail

staff costs.

Li Ning

2331 HK

(Buy)

976 7.5 DCF - Manufactures and wholesales

domestic sportswear products under Li

Ning Brand in China

- Company plans to focus on self-

operated shops and close down

unprofitable franchisee shops in China

- Revenue contribution: 67% from

wholesaling to distributors and

franchisees, 33% from self-operated

shops

Medium: Company can

improve product mix to

mitigate labour cost

growth

- The stock is trading at 2.8x

CY14e PB and 2.4x CY15e PB

vs. 3-year average 1-year

forward PB of 2.7x.

- Based on DCF (WACC

9.7%, terminal growth rate

2%), we derive PT of

HKD7.5, which is equivalent

to 3.7x 14e PB and 3.2x 15e

PB

- 13-14% revenue growth for 2014e-

15e, while Li Ning to deliver a net

profit of RMB192mn in 14e and

RMB525 in 15e vs a loss of

RMB392mn in 13 (end Dec).

- 7% ROE and -7% gearing (net cash)

for 2014e

1H14 financial

results in Aug14

- Failure of new product

sales in lower tier cities;

- Growing rental and retail

staff costs;

- Competition from

international and local

sportswear brands;

- Relationship with

distributors and franchisees

may deteriorate.

Xtep

1368 HK

(Buy)

924 4.5 DCF - Manufactures and wholesales

domestic sportswear products under

Xtep Brand in China

- Revenue contribution: 52% from

footwear, 46% from apparel, 2% from

accessories, c99% of revenue are

generated from wholesaling,

remaining c1% is from self-owned e-

commerce stores

Medium-to-high:

Company may improve

product mix to mitigate

labour cost growth,

however it has less room

to pass through cost hike

due to mass market

positioning

- The stock is trading at 10x

CY14e PE and 9x CY15e PE

vs. 3-year average 1-year

forward PE of 9x.

- Based on DCF (WACC

11.5%, terminal growth rate

2%), we derive PT of

HKD4.5, which is equivalent

to 13x 1-year forward PE.

- 1% revenue drop and 1% net profit

decline for 2014e, but 7% revenue

growth and 7% net profit growth in

2015e (end Dec).

- 13% ROE and -59% gearing (net

cash) for 2014e;

1H14 financial

results and 1Q15e

trade fair orders in

Aug14

- E-retailing cannibalizes

traditional channels;

- Competition from

international and local

sportswear brands;

- Growing rental and retail

staff costs.

Consumer

China Consumer

10 July 2014

page 12 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

Chart 8: Investment Summary of apparel and footwear companies

Source: Jefferies estimates

Coverage and

rating

Market

cap

(USD m)

Price

target

(HKD)

Valuation

methodNature of business Risk to cost hike Valuation Key forecasts Key catalysts Key risks

China Lilang

1234 HK

(Hold)

820 4.6 1-year

forward PE

- Wholesales menswear and lifestyle

products in China

- Revenue contribution: 90% from Lilanz

(menswear brand), 10% from L2

(lifestyle apparel brand)

Medium to high:

Lilang's product ASP is

on a declining trend in

CY14-15e

- The stock is trading at 10x CY14e

PE and 9x CY15e PE, vs 3-year

average forward PE of 13x.

- PT at HKD4.6 is based on 8.5x 1-

year forward PE

- 6% revenue growth and

flattish net profit growth in

14e

- 20% ROE and -41% gearing

(net cash) in 14e

1H14 results and 4Q14

(winter 2014) trade

fair announcement in

Jul-Aug14

- Upside risk: apparel

sector to recover from

2Q14 on better demand.

- Downside risk: retail

inventory may

accumulate as peers

offer serious discounts.

Daphne

210 HK

(Hold)

658 3.2 1-year

forward PE

- Retails mass market footwear products

under brands Daphne and Shoebox,

and retails licensed brands (such as

Aldo and Aee) in department stores.

- Revenue contribution: 93% from core

brands, 6% from licensed brands, 1%

from OEM and other income

High: In CY14-15e,

footwear products' ASP

may decline by 2-3%

while manufacturing

labour and retail staff

cost continue to

increase by 10-15%

- The stock is trading at 10x CY14e

PE and 8x CY15e PE vs 3-year

average forward PE of 18x.

- PT at HKD3.2 is based on 11x 1-

year forward PE

- 2% revenue growth and

59% net profit growth in 14e,

and 4% revenue growth and

16% net profit growth in 15e

(end Dec).

- 10% ROE and -20% gearing

(net cash) in 14e

2Q14 operational

updates in Jul14

- Upside risk: Better than

expected business

performance from 2Q14

onwards.

- Downside risk: Further

cannibalization by e-

commerce.

Trinity

891 HK

(Hold)

425 1.9 1-year

forward PE

- Retails luxuxy menswear brands

- Core brands include Kent & Curwen,

Gieves and Hawkes, Cerruti

- Revenue contribution: China 50%,

HK/Macau 32%, Taiwan 7%, others

(including retailing in Europe and UK)

11%

Low to medium: 10-15%

retail staff cost inflation

may put margin

pressure on Trinity

- The stock is trading at 11x CY14e

PE and 10x CY15e PE vs 3-year

average forward PE of 19x.

- PT at HKD1.9 is based on 11x 1-

year forward PE

- 2% revenue growth but 5%

net profit decline in 14e, and

3% revenue growth and 10%

net profit growth in 15e (end

Dec).

- 8% ROE and -0.3% gearing

(net cash) in 14e

Potential acquisitions

of menswear brands;

1H14 results

announcement in

Aug14

- Upside risk: Loosening

of anti-corruption

measures in China

- Downside risk:

Declining brand equity

of Trinity’s core brands

Belle

1880 HK

(Underperform)

9,533 6.8 1-year

forward PE

- Manufactures and retails mid-high

end footwear products under various

brands (Belle, Teenmix, Staccato, etc);

and distributes and retails international

sportswear (mainly Nike and Adidas)

- Revenue contribution: 61% from

footwear, 39% from sportswear

High: In 14e, footwear

products' ASP may

decline by 1-2% while

manufacturing labour

and retail staff cost

continue to increase by

10-15%

- The stock is trading at 15x CY14e

PE and 15x CY15e PE vs 3-year

average forward PE of 21x.

- PT at HKD6.8 is based on 11.5x 1-

year forward PE

- 6% revenue growth but a

10% net profit drop for FY15e,

and 7% revenue growth and

2% net profit growth in FY16e

(end Feb).

- 14.5% ROE and -32.4%

gearing (net cash) for FY15e

Jun-Aug14 operational

statistics in Sep14,

1HFY15e results

announcement in

Oct14; potential

acquisition of apparel

and footwear brands

Upside risk: SSSG may

rebound, which results

in operating leverage,

and valuation re-rating

Giordano

709 HK

(Underperform)

944 3.9 DCF - Wholesales and retails lifestyle apparel

products

- Revenue contribution: China 30%,

HK/Taiwan 29%, Rest of Asia Pacific

25%, Middle East 11%, Manufacturing

and others: 15%

Medium: manufacturing

cost in China will

continue to increase; it

may face currency risk

as SE Asian currency

may depreciate

- The stock is trading at 15x CY14e

PE and 14.5x CY15e PE vs. 3-year

average forward PE of 15x.

- PT at HKD3.9 is based on DCF,

(9.4% WACC, 2% terminal growth);

equivalent to 12x forward PE.

- 5% revenue drop and 26%

net profit decline in 14e, and

2% revenue growth and 2%

net profit growth in 15e

- 16% ROE and -31% gearing

(net cash) in 14e

1H14 results in Aug14 - Upside risks. Improving

apparel sales in HK, TW,

China and SE Asia; SE

Asian currency

appreciation to create

operating leverage.

Consumer

China Consumer

10 July 2014

page 13 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

Chart 9: Investment Summary of electrical appliances retailers

Source: Jefferies estimates

Coverage

and rating

Market

cap

(USD m)

Price

target

(HKD)

Valuation

methodNature of business

Risk to cost

hikeValuation Key forecasts Key catalysts Key risks

Gome

493 HK

(Buy)

2,845 1.8 DCF - Retails household appliances and

consumer electronic products across

different tiers of cities in China

- Revenue contribution: 91% from

offline channels vs 9% from online

channels in 2014e

Medium to

high, as GPM is

thin for home

appliance and

consumer

electronics

retailing

- The stock is trading at 14x

14e PE and 12x 15e PE vs. 1-

year average forward PE of

13x.

- Based on DCF (13.3%

WACC, 2% terminal growth

rate), we derive PT of

HKD1.8 for Gome,

equivalent to 19x 1- year

forward PE

- 12% revenue growth and 43% net

profit increase for 2014e

- 8% ROE and -31% gearing (net

cash) for 2014e

- 1H14e results

announcement in

Aug14

- additional shares

buyback

Downside risks:

- Slowdown in demand for

electrical appliances

- Cannibalization between

online and offline channel

results in product price cuts

and lower profit margin

- Less than expected cost

saving through the

enhancement of supply chain

Suning

002024 CH

(Hold)

7,785 RMB7.0 DCF - Retail chain stores to sell household

appliances, electronic products,

office equipment, and

communication products across

China.

- Revenue contribution: 80% from

offline channels and services vs 20%

from online channels in 2014e

Medium to

high, as GPM is

thin for home

appliance and

consumer

electronics

retailing

- The stock is trading at 1.8x

CY14e PB and 1.8x CY15e PB

vs. 3-year average forward

PB of 2.2x.

- Based on DCF (13.3%

WACC, 2% terminal growth

rate), we derive PT of

RMB7.0, which is equivalent

to 1.9x 1-year forward PB

- 3% revenue decline in 14e.

Company is expected to turn from

NP RMB372mn in 13 to net loss of

RMB1.2bn on declining GPM and

inflating operating costs.

- -4% ROE and -47% gearing (net

cash) for 2014e;

- 1H14e results

announcement in

Aug14

Downside risks

- further market share loss on e-

retailing

Upside risks:

- strong recovery in the

demand for home appliances

- Cost synergy between online

and offline as revenue resumes

growth in both channels

Consumer

China Consumer

10 July 2014

page 14 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

The era of E-commerce China has become the largest online retail market and its penetration grows at a much

faster pace than other developed economies. We observe the following key features: 1) as

consumers become more sophisticated and counterfeit products become a concern, B2C

format is quickly overriding C2C format; 2) The B2C market is set to undergo

consolidation; thus, building up a successful and sustainable platform requires a wide

range of strategies and strong execution; 3) O2O integration provides better consumer

satisfaction and can be a meaningful competitive advantage for both retailers and E-

tailers; 4) mobile/Wechat-made retail gains stronger momentum from PC-made retail.

China as the largest online retail market According to iResearch, China’s overall e-commerce market is expected to reach RMB4.5

trillion in 2017e. This implies 24.7% 13-17e CAGR, much higher than the 9.8% CAGR

generated by traditional offline retail for the same period of time. However, traditional

retail’s overall market size (RMB21.6trn in 13 to RMB31.4trn in 17e) is/will still be much

bigger than that of online retail. China’s online retail penetration rate reached 6.4% in

2012, surpassing the US market, and is expected to further go up to 12.4% in 2017e.

Chart 10: China retail sales from online and offline

Source: iResearch, Jefferies

Chart 11: Online retail penetration comparison: China vs US

Source: comScore, US Department of Commerce, iResearch, Jefferies

Year Online

retail sales

(RMBbn)

YoY % of total

retail

sales

Offline

retail sales

(RMBbn)

YoY % of total

retail

sales

Total

retail sales

(RMBbn)

YoY

2009 263 105.5% 2.1% 12,271 14.5% 97.9% 12,534 15.5%

2010 461 75.3% 3.0% 14,994 22.2% 97.0% 15,455 23.3%

2011 785 70.2% 4.3% 17,306 15.4% 95.7% 18,091 17.1%

2012 1,320 68.3% 6.4% 19,396 12.1% 93.6% 20,717 14.5%

2013 1,841 39.4% 7.9% 21,597 11.3% 92.1% 23,438 13.1%

2014e 2,420 31.5% 9.1% 24,173 11.9% 90.9% 26,593 13.5%

2015e 3,119 28.9% 10.4% 26,871 11.2% 89.6% 29,990 12.8%

2016e 3,790 21.5% 11.5% 29,167 8.5% 88.5% 32,957 9.9%

2017e 4,450 17.4% 12.4% 31,437 7.8% 87.6% 35,887 8.9%

13-17e CAGR 24.7% 9.8% 11.2%

Consumer

China Consumer

10 July 2014

page 15 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

Massive online shopping pool According to iResearch, the number of internet users in China is expected to increase from

230mn in 12 to 400mn in 16e, at 14.8% CAGR. In contrast, a similar figure in the US will

only increase from 150m in 12 to 175m to 16e, at 4.0% CAGR. Online shoppers’

penetration in China (as a % of total population) is expected to grow from 16.7% in 12 to

28.4% in 16e, while the same figure in US will only grow from 47.2% in 12 to 53.4% in

16e.

Chart 12: Online Shoppers’ comparison: China vs US (mn)

Source: iResearch, United Nations Department of Economics and Social Affairs, Jefferies

Household behaviour According to the China Household Finance Survey (CHFS), online shopping per domestic

household crossed RMB5,200 in 2013; in cities it was RMB5,600 and in rural areas

RMB2,600. This survey was conducted exclusively with Jefferies’ research team. About

20% of households surveyed purchased products online and the E-shopping ratio for

apparel products was as high as 80%. Although there is a large gap between rural and

urban areas, we expect rural areas to catch up in e-commerce with the help of improving

logistics facilities and accelerated urbanization.

We were surprised to see as many as c30% of the people surveyed had shopped online

for daily FMCG products such as toothpaste, tissue paper and shampoo, which are a

significant proportion of supermarkets’ turnover. In Eastern China, the ratio rose as high

as 37%. However, while online shopping for finished F&B goods ranges from single digits

to low teens, that for fruits and vegetables is only in the low single digits.

Chart 13: Domestic household online shopping, 2013

Source: Jefferies, China Household Finance Survey 2013

US China US China US China

2010 140 150 202 456 44.8% 11.0%

2011 143 190 204 469 45.5% 13.9%

2012 150 230 209 505 47.2% 16.7%

2013 156 270 214 542 48.8% 19.5%

2014e 163 310 219 583 50.4% 22.2%

2015e 169 360 223 636 51.9% 25.7%

2016e 175 400 229 687 53.4% 28.4%

12-16e CAGR 4.0% 14.8% 2.3% 8.0% 3.1% 14.2%

Number of e-shoppers Online population Penetration (%)

China

overall

Urban Rural

Per household online spending in 2013 (RMB) 5,237 5,606 2,584

% of household with online shopping

experience in 2013

22.6% 35.1% 6.4%

Footwear, apparel, sportswear 80.2% 80.0% 81.0%

Daily articles (Shampoo, paper, detergent, etc.) 33.1% 34.7% 21.9%

Consumer electronics (incl. 3C) 22.7% 23.6% 16.5%

Books and videos 20.5% 22.1% 9.5%

Home appliances 15.5% 16.6% 7.8%

Mother and baby items 13.0% 13.9% 7.0%

F&B, tobacco 12.5% 13.5% 5.7%

Furniture and cooking utensils 10.3% 11.3% 3.8%

Autos and parts 6.9% 7.3% 3.8%

Fruits and vegetables 1.9% 2.0% 0.7%

Consumer

China Consumer

10 July 2014

page 16 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

Trajectory of E-commerce From C2C (consumer to consumer) to B2C (business to consumer)

As consumers become more sophisticated and counterfeit products become a concern,

the B2C format is quickly overriding the C2C format. Contribution to online retail revenue

from B2C format increased from 7.8% in 2009 to 36.2% in 2013 and this figure is further

expected to reach 52.7% by 17e. In contrast, contribution from C2C will reduce to 47.3%

in 2017e from 63.8% in 2013, as illustrated in the table below.

Chart 14: Online sales from B2C and C2C

Source: iResearch, Jefferies

B2C market consolidation

The B2C market is set to undergo consolidation. Building up a successful and sustainable

platform requires the following criteria, in our view: 1) a rich collection of brands and

large number of SKUs with Tmall (Alibaba) as the best example; 2) strong specialization

in certain products with Suning as the most well-known electrical appliances retailer; 3)

User-friendly websites or and mobile phone apps attracting visiting volume, with Alibaba

and Tencent as the best examples; and 4) integration of rich experience in

logistics/inventory management into online platform. We believe all retailers are making

serious efforts towards this direction but none including Suning, Gome, Alibaba, Tecent,

has made a successful integration. Our study suggests that certain B2C platforms such as

Newegg China (新蛋网), Vincl (凡客诚品), etc. face challenges to keep their market shares.

We expect this industry to consolidate and weaker players will be phased out.

Chart 15: B2C market share breakdown in 2013

Source: i-Research, Jefferies

B2C sales

(RMBbn)

YoY % of total

online

sales

C2C sales

(RMBbn)

YoY % of total

online

sales

Online

retail sales

(RMBbn)

YoY

2009 21 102.9% 7.8% 243 105.7% 92.2% 263 105.5%

2010 63 207.8% 13.7% 398 64.0% 86.3% 461 75.3%

2011 198 214.3% 25.3% 586 47.3% 74.7% 785 70.2%

2012 403 102.9% 30.5% 918 56.6% 69.5% 1,320 68.3%

2013 666 65.5% 36.2% 1,175 28.0% 63.8% 1,841 39.4%

2014e 980 47.1% 40.5% 1,440 22.6% 59.5% 2,420 31.5%

2015e 1,410 43.8% 45.2% 1,709 18.7% 54.8% 3,119 28.9%

2016e 1,880 33.3% 49.6% 1,910 11.8% 50.4% 3,790 21.5%

2017e 2,345 24.8% 52.7% 2,105 10.2% 47.3% 4,450 17.4%

13-17e CAGR 37.0% 15.7% 24.7%

Consumer

China Consumer

10 July 2014

page 17 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

Chart 16: Background of major E-tailers

Source: Company, Jefferies

O2O (offline/online) integration

According to a survey conducted by Bain & Company in 2013, Chinese shoppers prefer

retailers to have both an e-commerce platform and brick-and-mortar retail stores (such as

Suning) over pure platforms with no retail stores (such as Tmall and JD360). The reasons

are as follows: 1) many consumers prefer the ‚touch and feel‛ at a brick-and-mortar store,

in particular for expansive goods. 2) Consumers have concerns about quality issues of

products bought online.

Mobile/Wechat-made retail gains momentum from PC-made retail

With the increasing popularity of smartphones and digital notepads, mobile online

shopping is expected to enjoy a significantly faster growth rate than PC platform.

According to iResearch, mobile-made retail sales reached RMB170bn in 13, which is a

much smaller size than PC-made retail sales at RMB1,671bn. However, mobile-made retail

sales CAGR for 13-17e period could reach 59%, whereas that for PC is much lower at

19.2%. Mobile-made retail sales proportion in total online sales is estimated to rise to

24.2% in 2017e from 9.2% in 2013.

Chart 17: Mobile e-commerce (B2C & C2C) vs PC e-commerce

Source: iResearch, Jefferies

The following part studies the impact of E-commerce on consumer subsectors.

Name Est. Year Major products offering Largest shareholders

Tmall 2008 All products, largest in apparel Softbank: 36.7%, Yahoo: 24%, Jack Ma and partners: 13%

JD360 2007 All products, largest in electronic goods Liu Qiangdong: 20.2%, Tencent: 17.8%, Tiger Funds: 15.6%

Tencent 2006 All products Nasper: 34%, Ma Huateng 10%

Suning 2005 All products, 3rd largest in electronic goods Zhang Jindong: 34%

Amazon China 1999 All products Amazon US: 100%

Dangdang 1999 All products, largest in books Yu Yu & Guoqing Li 82.9%

Gome 2011 All products Wong Kwong Yu: 32.1%, Bain Capital 9.9%

VIP shop 2008 Discount items Eric Shen 16%, Arthur Hong 12.3%, Sequoia 16.8%, US DCM 14.4%

Yihaodian 2008 Supermarket items Walmart: 51%, Gang Yu and Junling Liu: 49%

Vancl 2007 Apparel Chen Nian: 23%

Yixun (by Tencent) 2006 Electronic goods Nasper: 34%, Ma Huateng 10%

Newegg China 2001 All products Newegg US: 100%

M18 1996 Apparel Mecox Lane: 50%, Giosis: 50%

Mobile-

made sales

(RMBbn)

YoY % of total

online

sales

PC/tablets-

made sales

(RMBbn)

YoY % of total

online

sales

Online

retail sales

(RMBbn)

YoY

2011 11 397.6% 1.5% 773 68.5% 98.5% 785 70.2%

2012 63 450.7% 4.8% 1,257 62.6% 95.2% 1,320 68.3%

2013 170 168.5% 9.2% 1,671 32.9% 90.8% 1,841 39.4%

2014e 324 91.2% 13.4% 2,096 25.4% 86.6% 2,420 31.5%

2015e 524 61.6% 16.8% 2,595 23.8% 83.2% 3,119 28.9%

2016e 777 48.3% 20.5% 3,013 16.1% 79.5% 3,790 21.5%

2017e 1,077 38.6% 24.2% 3,373 11.9% 75.8% 4,450 17.4%

13-17e CAGR 58.7% 19.2% 24.7%

Consumer

China Consumer

10 July 2014

page 18 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

The impact of E-commerce Through large-scale data-mining, this study seeks to unveil the business model evolution

of the consumer sector in the face of the E-commerce boom. We find that E-commerce

poses a serious threat to most traditional retailers but benefits certain sectors/brands:

department stores and domestic apparel/footwear get hit most; leading global apparel

brands seem to leverage it to enhance branding recognition; sportswear uses it as an

effective tool for cleaning up inventory; and restaurants and jewellers have held up

relatively well.

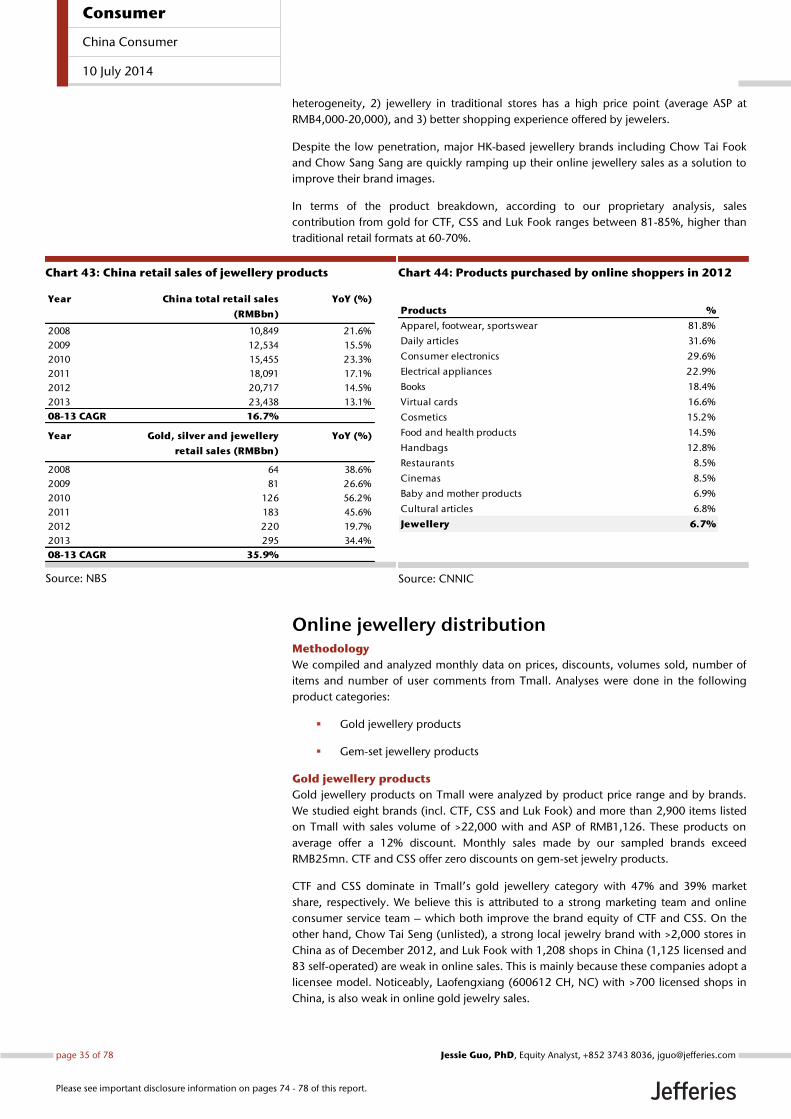

Cosmetic Goods Through large-scale data-mining and in-depth study of business models of online and

offline cosmetics retailers, we draw the following conclusions:

Online distribution of cosmetic products is becoming a strong competitive force

to traditional retail channels. Penetration of online sales of cosmetics (out of

total retail sales of cosmetics) increased from 3.8% in 2011 to 6.6% in 2012 and

10.2% in 2013. It is expected to reach 21.9% in 2018e. This will increasingly

pose a challenge to traditional department stores and offline cosmetics retailers

such as Sasa (178 HK, Underperform), Bonjour (653 HK, NC), Colourmix (owned

by Veeko Holdings; 1173 HK, NC), Sephora (owned by LVMH group; MC FP,

NC), and even brands with self-owned stores such as L’Occitaine (973 HK,

Hold), The Body Shop (owned by L’Oreal; OR FP, Hold), etc.

The online distribution channel is not a fatal challenge to high-end department

stores and beauty salons. We found that 76% of items are sold online are priced

below RMB300 and online shoppers are highly price sensitive. For expensive

items, consumers are more sophisticated and prefer trials and even beauty

consultancy in retail stores.

We believe Sasa is less competitive compared with Jumei (JMEI US, NC) and

Vipshop (VIPS US, Buy). The fundamentals and growth potential of Jumei in

particular is likely to outstrip Vipshop and Sasa due to its wide product range

and relatively low pricing that meets the needs of a stable/rising consumer base

with monthly income of RMB5,000-8,000. Vipshop has its niche serving

sophisticated consumers with higher purchasing power. In contrast, Sasa’s

business model is facing a serious challenge: its online channel is much less

competitive than close rivals, and can hardly help to offset headwinds that its

retail stores face: a slowdown in the number of mainland travelers, a weak Hong

Kong retail environment and difficulty in raising ASP.

The following sessions introduce our research methodology and data analysis.

Overview of cosmetics industry Cosmetic products have enjoyed stronger growth than the overall retail market in the past

few years due to further penetration of cosmetic products and product mix upgrade

driven by rising disposable income. The overall retail sales of cosmetic products grew at a

CAGR of 17.5% in 2010-13 to reach RMB221bn in 2013, according to Frost and Sullivan.

It is expected to grow at a CAGR of 14.3% in 2013-18e to reach RMB432bn in 2018e.

Online sales of cosmetic product have been growing rapidly in the past few years, thanks

to the further penetration of internet and fast growing online retailers that provide

attractive prices for cosmetic goods. It is the third largest product category in ecommerce

after apparel and home appliance & consumer electronics, according to iResearch. Online

sales of cosmetics grew from RMB1.7bn in 2010 to RMB22.6bn in 2013, at a CAGR of

137%. Online sales accounted for 10.2% of total retail sales of cosmetics in 2013, up from

6.6% in 2012 and 1.2% in 2010. Frost and Sullivan expects the Online cosmetic market to

Consumer

China Consumer

10 July 2014

page 19 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

grow at a CAGR of 33% in 2013-18e to reach RMB94.6bn in 2018e, and account for

21.9% of the overall cosmetic market in 2018e.

According to research from AC Nielsen on consumers who purchased cosmetics on 11

November 2013 (‚Single’s Day‛ Promotion), 83% of the cosmetic e-shoppers are aged

between 20-39 years old, while unsurprisingly 93% of them are female. In terms of the

income distribution of cosmetic e-shoppers, 53% of them have a monthly salary of

RMB5,000-8,000, 30% have a monthly income exceeding RMB8,000, while the remaining

17% e-shoppers have income lower than RMB5,000 per month.

Chart 18: Overall retail sales of cosmetic products in China

Source: Frost and Sullivan

Chart 19: Online B2C sales of cosmetic products in China

Source: Frost and Sullivan

Chart 20: Penetration of online cosmetic sales

Source: Frost and Sullivan

Chart 21: Income distribution of cosmetic consumers

purchasing on 11November 2013

Source: AC Nielsen

Online cosmetic distribution Methodology

We compiled and analyzed information on prices, discounts, volumes, number of SKUs

and quantity sold from four online cosmetic sales platforms:

Vipshop: online discount outlet

Jumei: specialty cosmetic online retailer

Sasa.com: e-commerce platform of traditional cosmetic retailer, and

Official flagship stores operated by various cosmetic brands in Tmall

We looked at similar brands across different platforms, which helped to provide useful

comparison and analysis on the positioning, characteristics and potential of these

platforms.

Monthly salary % of e-shoppers

RMB5,000-8,000 53%

>RMB8,000 30%

Others 17%

Total 100%

Consumer

China Consumer

10 July 2014

page 20 of 78 , Equity Analyst, +852 3743 8036, [email protected] Guo, PhD

Please see important disclosure information on pages 74 - 78 of this report.

Vipshop

We analyzed the product offerings on Vipshop’s Shanghai regional site. Our analysis of 11

skincare brands shows that Vipshop on average provided 21% discounts on these skincare

products. Its average selling price (ASP) after discount is RMB465, with an average of 51

SKU offerings per brand.

In the analysis of 5 key brands for makeup products, they have an average discount of

21%, similar to that of skincare products. The ASP (after discount) of makeup is RMB238,

with an average of 66 SKUs available per brand.

Vipshop provided a high discount of 33% on average for perfumes on 6 brands surveyed.

Its perfume offerings have an ASP of RMB476 with an average volume of 58ml and 8 SKUs

per brand.

Chart 22: Skincare products on Vipshop

Source: Vipshop, Jefferies

Chart 23: Makeup products on Vipshop

Source: Vipshop, Jefferies

Chart 24: Perfumes on Vipshop

Source: Vipshop, Jefferies

Brand ASP before

discount

(RMB)

ASP after

discount

(RMB)

Average

discount

%

Average

volume

(ml)

# of SKUs

available

Dior 1,485 1,188 -19.9% 90 24

Lancome 1,292 987 -22.1% 89 23

SK II 1,231 902 -24.7% 97 45

Clarins 572 441 -23.5% 90 25

Shu Uemura 454 354 -22.8% 169 43

Biotherm 401 314 -21.6% 106 61

L'Occitane 360 286 -20.9% 142 44

Kiehl's 305 269 -11.7% 137 47

Olay 214 159 -25.0% 72 98

L'Oreal 174 143 -17.6% 85 100

Maybelline 86 69 -19.8% 64 47

Average 598 465 -20.9% 100 51

Brand ASP before

discount (RMB)

ASP after

discount (RMB)

Average

discount %

# of SKUs

available

Dior 520 383 -24.9% 3

Lancome 481 379 -21.2% 8