Chief Executive Magazine

76

How simple giving is evolving into good business REIMAGINING CORPORATE CITIZENSHIP Securing Your Data CEOs share cyber safety tips— corporate and personal, p. 54 Making Mergers Work What CEOs can learn from deal guru Irwin Simon, p. 36 Private CEO Comp How does public and private sector pay compare? p. 43 Private Aviation Guide How to navigate the expanding world of private jet options, p. 64 SEPTEMBER/OCTOBER 2015

-

Upload

chief-executive-group -

Category

Documents

-

view

226 -

download

0

description

September / October 2015

Transcript of Chief Executive Magazine

How simple giving is evolving into good business

REIMAGINING CORPORATE CITIZENSHIP

Securing Your Data

CEOs share cyber safety tips— corporate and personal, p. 54

Making Mergers WorkWhat CEOs can learn from deal

guru Irwin Simon, p. 36

Private CEO Comp

How does public and private sector pay compare? p. 43

Private Aviation GuideHow to navigate the expanding

world of private jet options, p. 64

SEPTEMBER/OCTOBER 2015

September/October 2015 No. 278

FEATURES

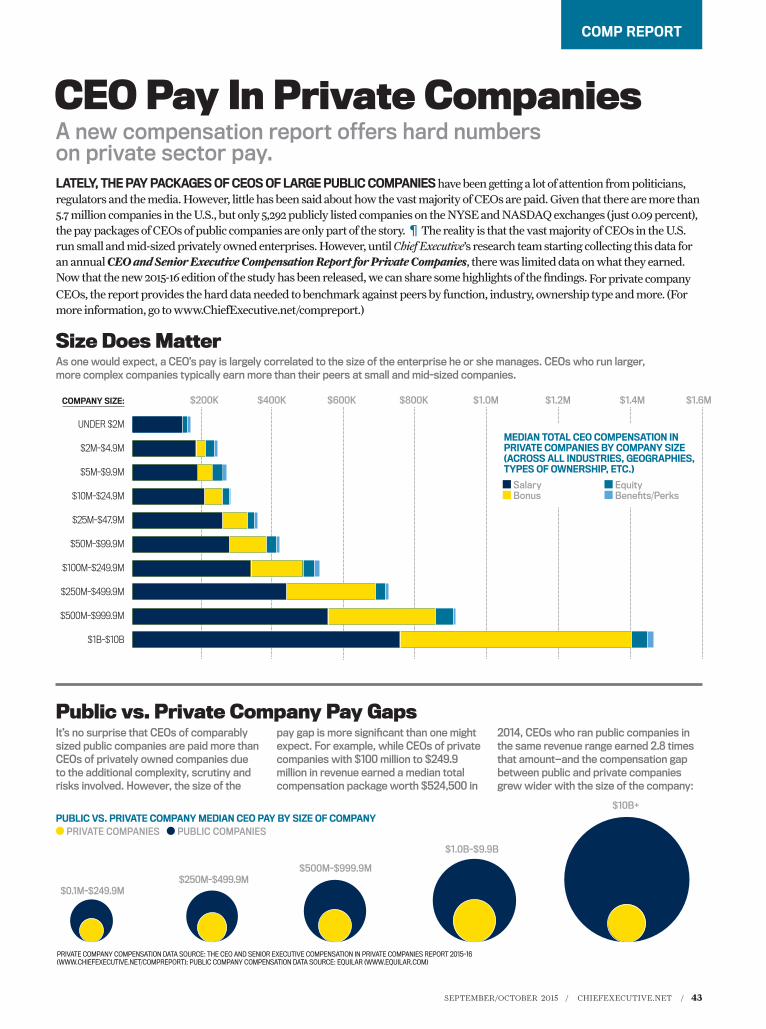

30 Corporate Philanthropy Lessons in Good Giving How companies who prioritize social change are using philanthropy to make it happen—and what they’re getting back. By C.J. Prince

36 Mergers & Acquisitions Piecing Together a Natural-Foods Empire Deal guru Irwin Simon, founder and CEO of Hain Celestial, knows how to make mergers work. By Warren Strugatch

46 Economic Development Regional Report: The Southeast With further automotive wins, the Southeast continues rolling along. By Warren Strugatch

COVER ILLUSTRATION BY THE HEADS OF STATE02 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

46

51

36

30

CONTENTS

S P E C I A L E V E N T C O V E R A G E

51 CEO OF THE YEAR

Boeing’s Jim McNerney Recognized for smoothing out Boeing’s bumpy

flight plan, Jim McNerney was chosen by a panel of CEO peers for this annual award recognizing stellar leadership.

54 CEO ROUNDTABLE Understanding and Thwarting Cyber Threats

With great connectivity comes great risk—and an imperative to protect critical data and safeguard systems from attack.

57 CEO ROUNDTABLE The Data-Enabled CEO

CEOs share their experiences unlocking key insights to accelerate business performance.

8 Editor’s Note

10 CEO Watch • CSL Bhering’s Paul Perreault on pharma innovation

• Citizens Bank’s Bruce Van Saun on surviving a spinoff

• Red Hat’s Jim Whitehurst on open management

• CEO Confidence: Optimistic Outlook

22 Chief Concern Fifty Shades of Gray: The Real World of the CEO

By Thomas J. Saporito

24 Mid-Market Report Growth Softens for the

Middle Market

26 Making Technology Work

The Rewards of Right-Sourcing Why IT sourcing matters to CEOs

and boards. By Tom Pettibone

28 Sonnenfeld The King is Dead, Long Live the King Always tricky, leadership transitions

get even tougher when a CEO departs the world along with the job. By Jeff Sonnenfeld

CONTENTS

04 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

Chief Executive (ISSN 0160-4724 & USPS # 431-710), Number 278, September/October 2015. Established in 1977, Chief Executive is published bimonthly by Chief Executive Group, LLC at One Sound Shore Drive, Suite 100, Greenwich, CT 06830-7251, USA, 203.930.2700. Wayne Cooper, Executive Chairman, Marshall Cooper, CEO. © Copyright 2014 by Chief Executive Group, LLC. All rights reserved. Published and printed in the United States. Reproduction in whole or in part without permission is strictly prohibited. Basic annual subscription rate is $99. U.S. single-copy price is $33. Back issues are $33 each. Periodicals postage paid at Greenwich, CT and additional mailing offices. POSTMASTER: Send all UAA to CFS. NON-POSTAL AND MILITARY FACILITIES: send address corrections to Chief Executive, P.O. Box 15306, North Hollywood, CA 91615-5306.

Subscription Customer Service: p | 818.286.3119 e | [email protected] w | chiefexecutive.net/magazine

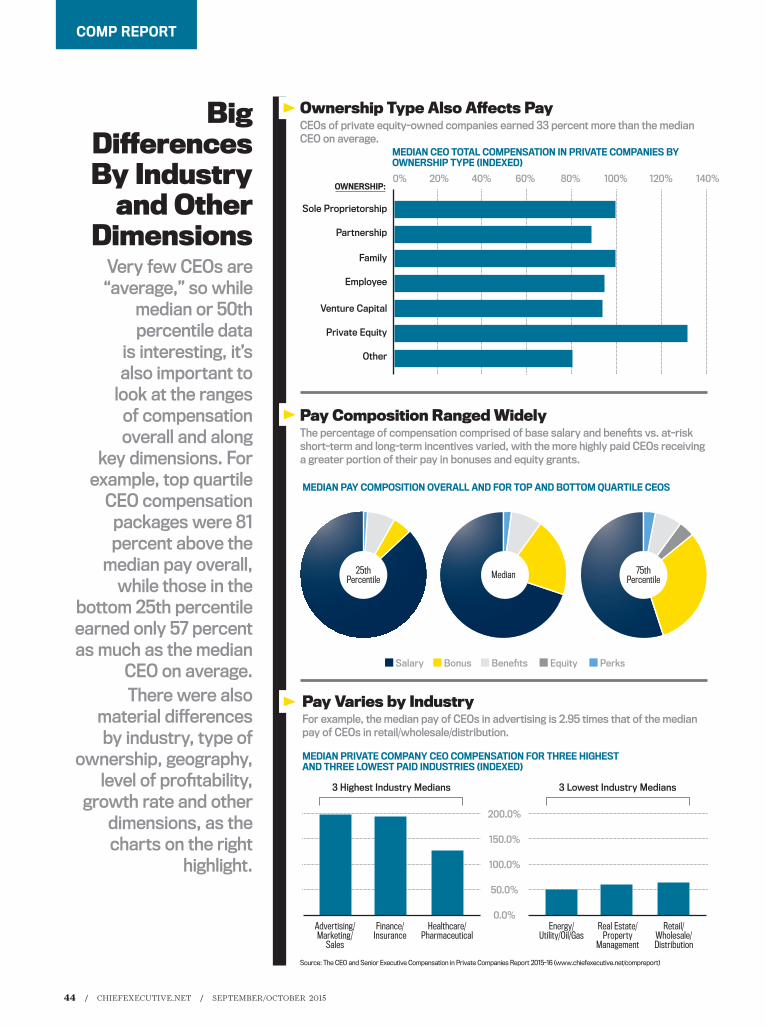

43 Comp Report CEO Pay in Private Companies

62 CEO Passions Collecting Earthly Treasures

Presented in partnership with PURE Insurance, our sixth column on CEOs who are notable collectors features SAS’s Jim Goodnight. By George Nicholas

64 Executive Life Private Aviation Report Riding out the turbulence of 2008’s U.S. recession was no easy trick, but the business aviation sector has made a steady comeback thanks to options for every flier’s needs. By Michael Gelfand

72 Flip Side It’s All Greek, All the Time

Why is Greece suddenly getting all the glory? By Joe Queenan

DEPARTMENTS

Wayne Cooper Chairman & President

Marshall Cooper Chief Executive

One Sound Shore Drive, Suite 100 Greenwich, CT 06830, 203/930-2700

Editor in ChiefJ.P. Donlon

Editor at LargeJennifer Pellet

Creative DirectorMarne A. Mayer

Production DirectorRose Sullivan

Chief CopyeditorRebecca M. Cooper

Associate CopyeditorCarl Levi

Contributing EditorsMichael Gelfand

Bill HolsteinGeorge Nicholas

C.J. PrinceJoe Queenan

Dr. Thomas J. SaporitoProf. Jeff Sonnenfeld

Online EditorLynn Russo Whylly

VP, Associate PublisherChristopher J. Chalk

Director, Business DevelopmentLisa Cooper203/889-4983

Director, Business DevelopmentLiz Irving

Director, Business DevelopmentMarc Richards

Vice PresidentPhillip Wren

Marketing DirectorJason Golden

Back Issues Back issues are $33 each. For back issue

availability and additional order information, please contact us at: Phone: 203.930.2701

Subscription Customer ServiceChief Executive, P.O. Box 15306

North Hollywood, CA 91615-5306Phone: 818.286.3119 | Fax: 800.869.0040

64

DAN GLASER President and Chief Executive,

Marsh & McLennan

FRED HASSAN Chairman, Zx Pharma

Partner/Managing Director, Healthcare, Warburg Pincus

ROBERT IGER Chairman and Chief Executive,

The Walt Disney Company 2014 Chief Executive of the Year

CHRISTINE JACOBS Former Chief Executive,

Theragenics Director, McKesson

TAMARA LUNDGREN President and Chief Executive,

Schnitzer Steel Industries

ROBERT NARDELLI Chief Executive, XLR-8

WILLIAM R. NUTI Chairman and Chief Executive, NCR

THOMAS J. QUINLAN III President and Chief Executive,

RR Donnelley

JEFFREY SONNENFELD President and Chief Executive,

The Chief Executive Leadership Institute, Yale School

of Management

MARK WEINBERGER Chairman and Chief Executive, EY

MAGGIE WILDEROTTER Executive Chairman,

Frontier Communications Solutions

CONTACT USCorporate Office

Chief Executive Group, LLCOne Sound Shore Drive, Suite 100

Greenwich, CT 06830Phone: 203.930.2700 | Fax: 203.930.2701

www.chiefexecutive.net

Letters to the [email protected]

Advertising, Custom Publishing, Events, Roundtables

& ConferencesPhone: 847.730.3662 | Fax: 847.730.3666

ReprintsPhone: 203.889.4974

CHIEF EXECUTIVE OF THE YEAR

2015 SELECTION COMMITTEE

DAILY BEST OF THE WEBWe scour dozens of websites so you don’t have to.

Top stories for CEOs to help you start your day

CEOS IN THE NEWSAdvice from successful CEOs, along with news and

information about your industry peers

CEO INSIGHTSInsider information from experts on leadership, strategy,

operations, marketing, sales, manufacturing and much more

PLUSImportant lists and rankings you can reference all year long, including:

Best & Worst States for Business • Best Companies for LeadersCEO Confidence Index • CEO of the Year • Annual Wealth Creators

CHIEF EXECUTIVE ON THE GOChiefExecutive.net content is available anytime, anywhere through your mobile device! Also, magazine subscribers can download digital editions of the magazine on their iPad, iPhone or Android phone.

What you need, when you need it. www.ChiefExecutive.net

ChiefExecutive.netTIMELY CONTENT

TO HELP YOU RUN YOUR BUSINESS

The Impending Talent Crisis

Building a Performance and Recognition Culture

Retaining Your Top Talent

Developing Leaders In a Rapidly

Complex and Changing World

How Data and Analytics Will Reshape Your Workforce

2015 CEO Talent SummitSeptember 30-October 1 • Dallas, TX

Hosted by Southwest Airlines

CEOTALENT.CHIEFEXECUTIVE.NET

Solutions for Your Growing

Talent Gap

Chief Executive’s

2015 CEO Talent Summit copy.indd 7 8/26/15 5:24 PM

EDITOR’S NOTE

08 / CHIEFEXECUTIVE.NET / SEPTEMBER / OCTOBER 2015

WILL ROBOTS AND AUTOMATION DIS-PLACE WORKERS FOREVERMORE? It’s a worry shared by many, including CEOs participating in a recent roundtables held in conjunction with our celebration of our 30th Chief Executive of the Year, Boeing’s Jim McNerney. Our discussion centered on technology’s impact on innovation and how disruptive technologies such as the Internet of Things (IoT) are changing everyone’s operations and go-to-market strategies.

Along the way, two CEOs representing high-tech and low-tech industries re-spectively—McNerney and Ethan Allen’s Farooq Kathwari—expressed concern that as technology becomes ever more capable of doing work once thought only doable by employees, there will be fewer and fewer jobs available. Both CEOs felt that business leaders will be asked to solve this social issue and had better start thinking about it seriously. Both also said that while they want to keep as much manufacturing as practical within the U.S., from a competi-tive standpoint factories will still be needed around the world. Furthermore, manu-facturing jobs are unlikely to continue to account for more than 12 percent of overall employment. Agriculture, which repre-sented 92 percent of U.S. employment in the late 18th Century now represents just 2 percent thanks to automation.

“There are lots of examples of rou-tine, middle-skilled jobs that are being eliminated the fastest,” reports Erik Brynjolfsson, professor of information technology at MIT Sloan School of Man-agement. “Those kinds of jobs are easier for our friends in the artificial intelligence community to design robots to handle, ” he told 60 Minutes. Indeed recent de-velopments indicate robots—or smart

machines—will be taking not just manual jobs, but also intellectual jobs. Consider Watson, IBM’s computer, which played—and won—on Jeopardy! During the tour-nament, Watson not only came up with correct answers, but also learned why his incorrect answers are wrong. It improved rate faster than any human could.

Brynjolfsson adds that “technology is always creating jobs. It’s always destroy-ing jobs. But right now the pace is accel-erating. It’s faster, we think, than ever before in history. As a consequence, we are not creating jobs at the same pace we need to.” This is what worries CEOs like Kathwari and McNerney. Will advances in technology outpace the ability of Amer-ica’s businesses to create new jobs for people, and will there be a backlash when businesses find they can’t keep up?

Brynjolfsson isn’t pessimistic. At a recent TED Talk he stated that “technology is not destiny; we shape our own destiny. We’re going to need to reinvent our organizations and even our whole economic system.”

Supporting this view is Fortune senior editor-at-large Geoff Colvin, who in his recent book, Humans Are Underrated, argues that despite growing anxiety about technology putting people out of work, the reality is that we will always want other people to do a range of tasks—even if a computer can do them better for less money. Creativity, he argues, can never be replaced by automation. This is why Goo-gle, for example, “is fanatical about forcing people to connect in person.” Colin writes that the most valuable people will not just be knowledge workers, but simultaneous-ly “relationship workers” who create the kind of social value that people will always desire. Let’s hope he’s right.

As technology becomes ever more capable of doing work once thought only doable by employees, there will be fewer and fewer jobs available.

The Next Big Challenge for CEOAddressing automation’s impact on employment may fall to CEOs. By J.P. Donlon

ILL

US

TR

AT

ION

BY

TIM

TO

MK

INS

ON

J.P. Donlon

10 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

IN THE PHARMA INDUSTRY, a company’s future prospects are every-thing. One can only ride the wave of a blockbuster drug for so long before it goes off patent and generic versions edge in. But as anyone familiar with the rollercoaster-like road to FDA approval well knows, drug develop-ment is an expensive and extremely iffy endeavor. At any point along the process—from Phase 1’s early human studies and Phase 2’s efficacy testing on through navigating healthcare reimbursement programs—even the most promising compound can implode.

That’s a risk that pharma CEOs like Paul Perreault, CEO of CSL Behring, face regularly. “Our biggest business challenge is picking the right things,” he says. “It’s looking for those key items that you have insight into from a science perspective so that you’re not wasting R&D money, because that’s easy to do. You get enthralled with the neat stuff out there.”

In that sense, pharma is some-thing of a microcosm for the broader corporate world, where intensifying global competition and commoditi-zation have bred an “innovate or die trying” environment. At the same time, getting led astray by fear of being left behind or pursuit of the “next big thing” can be just as dangerous as inertia.

Thus far, Perreault, who took the CEO role at CSL in July of 2013, has avoided both fates, having success-

fully launched or registered (meaning introduced existing products in new countries) 22 new products around the globe in CSL’s last reporting financial year. Going forward, however, he has more ambitious innovation plans for the King of Prussia, Pennsylva-nia-based company, which makes plasma-derived and recombinant ther-apies for rare conditions like bleeding disorders and immune deficiencies.

“I want to look beyond the product and think about how we can innovate also the delivery and the infomatics that are being required in healthcare now,” he explains, noting that patient

CEO WATCH

CEO INSIGHT / CSL BEHRING’S PAUL PERREAULT

Driving Disciplined R&D The pursuit of new drugs is just one way to navigate the “innovate or exit” pharma world. By Jennifer Pellet

compliance is one of the challenges of treating children with hemophilia. Naturally reluctant to get a shot in the arm, kids who feel fine decide to skip their medicine. “If you can collect that information about compliance via a Bluetooth device and send it directly to the healthcare provider and the payers, you’ll have greater control over both the disease and management of its cost. That’s innovation.”

Information is becoming a bigger piece of the innovation puzzle on other levels as well. For example, some new treatments have made it all the way through FDA-type gauntlets only to

We don’t acquire things we don’t know anything about.

That’s where companies get into trouble.

“”

There is a lot of information (and hype) about the shifts inmarketing and sales tactics for consumer products and software

companies. However, little hard data has been available to help CEOs and senior executives from B2B companies benchmark

their sales and marketing activities—until now.

Chief Executive Group is pleased to announcethe release of the new

B2B SALES AND MARKETING:KEY BENCHMARKS AND BEST PRACTICES REPORT

With more than 120 charts and graphs, the report provides insight on the e� ectiveness and use of nearly all sales

and marketing channels and tactics.

Price: $1,495 $1,295Save $300 by entering source code CESub1107 when ordering through

ChiefExecutive.net/B2B

BENCHMARK YOUR B2B COMPANY’S MARKETING AND SALES ACTIVITIES

B2B.indd 11 8/26/15 5:24 PM

12 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

CEO WATCH

perish at the hands of insurers who refused to cover their use. “In Germany, there was a case where a new pharmaceutical that cost $200 million to bring to market was approved, but the governing body said ‘there’s no benefit over the current therapy so we’re not going to re-imburse for it,’” explains Perreault. “To spend all that money and not have thought about how you’ll get it paid for is a huge mistake.”

To guard against that outcome, CSL focuses not only on developing new treatments but on gathering data to show a benefit over what’s current-ly available. “We have to get better at making sure we deliver the data to the regulators that justifies the cost of the medicines,” says Perreault. “All

$275 million, a move that catapulted it into the big leagues in that busi-ness. Should the deal go through—it remains subject to regulatory approv-als in a number of jurisdictions—CSL Behring will become the second larg-est-influenza vaccine manufacturing company, giving it economies of scale and strong pandemic capabilities in the U.S., UK, Australia and Germany.

But Perreault is quick to note that acquisitions won’t be the company’s principle growth strategy. “I looked at 200 possibilities last year; we did one,” he asserts. “We don’t acquire things we don’t know anything about. That’s where companies get into trouble. They spend billions getting into an area and then billions getting out. When we do something, we do it in areas where we have expertise in it, adjacencies around it or the capability to improve it. I tell people that we do one big deal every decade because that situation is hard to find.”

WHO

Paul Perreault, CEO of CSL Behring

WHAT

$5.5 billion specialty biotherapeutics company

WHERE

King of Prussia, PA

RECENTLY READ

I Moved Your Cheese, by Deepak Malhotra; The

Power of Noticing, by Max Basemann, Mao’s Last

Dancer, by Li Cunxin

BUSINESS PHILOSOPHY

“Work every day like someone’s life depends

upon it—because it usually does.”

CEO CONFIDENCE

CEOS AND THE BUSINESSES they lead have endured many ups and downs over the last few months, from global economic distress in places like Greece and China to increasing terrorist concerns worldwide, a strong U.S. dollar, low oil and gas prices, increased healthcare costs, staffing challenges and more. So it’s not altogether unexpected that CEOs’ confidence about future business conditions is down from the beginning of the year, when prospects for future business were stronger. Also adding to CEOs’ concerns is antici-pation over who will be elected the next president of the United States, and where that candidate stands on issues that affect business.

CEOs collectively reported a 6.14 out of 10 points in August with regard to their expectations about overall business conditions one year from now compared with 6.71 points in January, an 8.5 percent reduction in confidence over the eight-month period.

JAN ’156.71%

FEB ’15 6.45%

MAR ’15 6.48%

APR ’15 6.52%

JUN ’15 6.25%

MAY ’15 6.41%

JUL ’15 6.33%

AUG ’15 6.14%

6.00

6.25

6.50

6.75

THE TAKEAWAY

Confidence down 8.5% since

January

that work has to be done up front.”

At the same time, the company is continuing to develop new ther-apies. One promising area is a reconstituted high-density lipopro-tein (RHDL)—aka good cholesterol—that will be used for patients who develop acute cor-onary syndrome after experiencing a heart at-tack. “From Hour Zero to Day 60 after a heart

attack is when plaque is most unstable and you’re at the most risk of a second attack,” explains Perreault. “These molecules actually attract plaque from an affected artery and metabolize it through the body.”

CSL is also working to finalize its October 2014 acquisition of Novartis’ global influenza vaccine business for

Volatile Market Conditions Continue to Erode CEO Confidence

14 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

CEO WATCH

CEO CASE STUDY / CITIZENS FINANCIAL’S BRUCE VAN SAUN

Banking on Steering a SpinoffApproaching its IPO anniversary, Citizens Financial is forging an independent future. By Jennifer Pellet

The ChallengeYou’re the group finance director of a foreign bank, which you’ve spent the past five years bringing back from the brink of failure, a gargantuan task given the circumstances. Now you’ve been tapped to spin the U.S. arm of that still-recuperating financial institution off into a healthy public company—and to do it in a year flat.

The ContextWhen Bruce Van Saun stepped in as its CEO, Providence, Rhode Island-based Citizens Financial was still part of the Royal Bank of Scot-land, although its days as such were numbered. Under pressure from reg-ulators to make good on a government bailout loan, RBS needed to unload a hefty portion of its majority stake in Citizens Financial. Van Saun was charged with the dubious task of tak-ing an underperforming company public.

The first step of that task was accomplished on September 24, 2014 in what turned out to be the biggest financial services IPO in U.S. history, a $3.5 billion transaction for Citizens. A second stock sale in March of 2015—valued at $3.7 billion—further reduced RBS’s stake to less than 50 percent of the bank. But while the sales firmly established Citizens’ independence, Van Saun’s work had just begun.

“Our returns were not where they should be, and our efficiency ratio was high,” recounts Van Saun. “We had the right level of expenses but the alloca-tion of those dollars was not optimal. We needed to put a lot of effort into becoming more effective and efficient so that we could invest back into areas where we saw growth opportunities.”

The ResolutionEarly on, the company homed in on boosting returns in sectors like mort-gages, business banking and student lending, as well as fee-based business-es like wealth management services. During Van Saun’s tenure, Citizens steadily built out its commercial lend-ing business, a success he attributes to a relationship acquisition approach.

“To me the most intelligent way to grow market share is to bring in people with pre-existing relationships,” he says. “We have a big capital position on the balance sheet, which gives us loan capacity. So if we bring in good people, hopefully their [clients] think, ‘I like what that bank is doing and I want to keep a good relationship with Joe or Sally.’ That’s been a

successful formula for us.”The company also focused on

developing an expertise in industries like franchising, energy and technol-ogy, where it can add value. “We try

to bring a big bank approach to really understanding our customers and showing up with ideas,” explains Van Saun. “I never want to visit without being able to say ‘Here’s how I think you can be more successful,’ whether that’s an opportunity in your capital structure, cash management or an M&A prospect.”

In its effort to build industry verti-cals, Citizens has been particularly suc-cessful in the franchising sector, where it counts Dunkin’ Donuts, McDonald’s and Taco Bell as partners. “Initially our franchise finance group had six people, today we have 44,” says Van Saun, who explains that the bank has been able to take financing arrangements that begin regionally national. “McDonald’s said, ‘We like your approach, we like the quality of your people, why don’t you come national with us?’ Now we’re probably the No. 2 lender in the U.S. to their franchisees.”

The HurdleIn building the bank’s commercial business, Van Saun struggled with a which-comes-first-chicken-or-egg dilemma in hiring industry specialists to build its coverage group. “Great coverage people want to make sure you have good product capabilities so they can serve their clients well—but great product people [or specialists on trans-actional models] want to make sure

WHO

Bruce Van Saun, Chairman and CEO

WHAT

Citizens Financial Group

WHERE

Providence, Rhode Island

SIZE

$137.3 billion in assets

BIGGEST INFLUENCE

“My parents. They taught me a good work ethic.”

ADVERTISEMENT

FOUR YEARS AGO THIS MONTH, the United States embarked upon broad patent reform with the America Invents Act, seeking to curb skyrocketing patent litigation, costs and perceived abuses—particularly by non-practicing entity “trolls.”

The new laws appear seaworthy. According to PricewaterhouseCoopers, U.S. patent infringement suits dropped for the first time in five years, from a crest of almost 6,500 in 2013, to less than 5,700 in 2014; and fewer of those suits are from trolls. Conversely, patent validity challenges before the U.S. Patent & Trademark Office, particularly newly enacted Inter Partes Reviews, rose to almost 1,900 in 2014. These challenges are swift, laser-focused and less-costly—they are now standard-operating-procedure for accused infringers striking back against patentees.

Four other developments have further reshaped U.S. patents in these four years. First, winning litigants are getting less money—court-awarded damages to patentees that prevail are down to their second-lowest level in 20 years. Second, accused infringers have a better shot at reclaiming attorneys’ fees from patentees behind spurious suits, in the wake of the Supreme Court’s Octane and Highmark rulings. Third, that high court’s Alice ruling has increased scrutiny of claims to business method software. And fourth, you now have to be “first-to-file” a patent application, rather than “first-to-invent”—thus the new “race to the patent office.” In sum, those attempting to gain and enforce patents in America are facing rougher seas.

Still, it is a huge ocean out there, with patent stakes higher than ever: intellectual property-intensive U.S. industries account for over $5 trillion in value-added each year—almost 35 percent of

U.S. gross domestic product. Accordingly, more U.S. patents

are pursued than ever before—330,000 were granted in 2014 alone, an all-time high.

Trimming your company’s sails for the new patent seas is clearly a worthy endeavor—three new compass points to guide by:

1. Reengineer your patent portfolio process— to best harvest and enhance your technological edge. Expedite invention disclosure (and review) to be first-to-file. And draft patent claims away from scrutinized business methods, toward more patentable technology—focus on the hardware, for instance, at least as much as the software.

2. Modernize patent enforcement— rigorously develop claims to withstand USPTO validity challenges. Particularly avoid claims to computer implementation of long-standing abstract ideas. Provision your litigation to weather a stay pending a validity challenge, as now happens in most U.S. District Court suits. Or, bring your complaint to the U.S. International Trade Commission to block infringing imports, as these expedited proceedings are generally not stayed for validity challenges. On defense, always consider challenging validity at the USPTO, but take heed: a failed challenge can bullet-proof a patent for litigation. And look for ill-founded allegations, as you are now more likely to win back attorneys’ fees for a forceful defense, or at least to contain damages such that the ship stays afloat.

3. Communicate your patent course— both internally, to foster a culture of capturing innovation, and externally, to attract investment. And consider aligning against trolls: innovative new collaborations are pioneering creative tactics.

As the America Invents Act turns four, some seas remain unsettled, with Congress considering even further patent reform. But new compass points have indeed emerged, opening new blue-ocean opportunities.

Patent Sea ChangesNew compass points four years into the America Invents Act

By Josh Pond

JOSH POND is a patent litigator, strategist and partner at Kilpatrick Townsend in Washington, D.C. He is also a sailor.

16 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

CEO WATCH

you’re adding good coverage people so they have more swings at bat and a bigger book,” he explains. “We’ve been on a journey to invest in both.”

The EndgameCitizens’ first-quarter earnings were $209 million, up 27 percent from a year ago, and beat analyst expecta-tions. The market has noticed. At press time, Citizens’ stock price was a healthy $26.70, a considerable bump from its IPO offering price of $21.50.

“We’re on a good trajectory,” says Van Saun. “I tell my commercial guys, ‘Our customers love us; we just need more customers.’ That’s always the way when you’re plotting expansion. The perception of the people who haven’t used you yet isn’t as high as that of the people who use you and know you and love you. So we just need to continue to bring good people onto the platform.” The LessonsFor Van Saun, batting cleanup for a floundering foreign bank underscored the dangers of a growth-by-acquisition strategy. “Both RBS, and also Citizens indirectly through RBS owning Citi-zens, prized acquisition-led growth,” he explains. “They were both always looking for the next deal. So there was insufficient investment in organic growth and investing in the necessary technology to be successful and in stitching everything together in a co-herent delivery model for customers.”

It’s a mistake he’s determined to avoid repeating by developing a comprehensive plan, building team buy-in and focusing on execution. “My lessons are: make sure that the bank from an organic standpoint is running well and take care of customers so you have a firm franchise and foundation and it’s sustainable,” he says. “Then to also keep some dry powder because there will be acquisition opportunities that can further your agenda—but they shouldn’t be the be-all and end-all, which is what they became at RBS and Citizens before.”

CEO POV / RED HAT’S JIM WHITEHURST

On Becoming an Open Organization LeaderRed Hat CEO Jim Whitehurst believes he’s latched onto the best way of leading an organi-zation and solving problems. Open management challenges conventional ideas of what companies are. But is it for everyone? By J.P. Donlon

BEFORE JIM WHITEHURST became president and CEO of Red Hat, the largest open-source software company in the world with nearly $2 billion in revenues, he held various positions at Delta Airlines. Most recently, he served as COO, responsible for opera-tions, sales and customer service, network and revenue management and corporate strategy. Before that he was a partner at The Boston Consulting Group and held vari-ous leadership roles in its Chicago, Hong Kong, Shanghai and Atlanta offices. Not bad for a guy raised in rural Georgia.

Before he took the helm at Red

Hat, Whitehurst was being wooed primarily by big industrial com-panies interested in turnarounds. “They were literally sending private planes and taking me to five-star dinners and all that mess,” he recalls. But one day, a recruiter convinced him to fly to Red Hat’s headquarters in Raleigh, North Carolina on a Sunday. He arrived at the building to find it locked and no one in sight. Was this a gag? As Whitehurst pondered going back to the airport, Matthew Szulik, the company’s CEO drove up in his car, rolled down the window and asked, “Want to grab some coffee?” The conversation went well until Szulik

18 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

QCEO WATCH

JW: At first it seemed like chaos. I thought, “Oh my God, this place is more of a train wreck than I thought.” There was no order; no structure. How do things get done? I didn’t know the industry either.

Then I was out talking to custom-ers and investors and, during that time, the organization made a series of decisions that at Delta would have been made by the executive commit-tee. I went to the team and asked, “Do you guys not trust me?” They replied, “What do you mean?” Soon I began to realize that people here make a number of decisions and there’s more buy-in because they’ve made them.

Red Hat was an open organization long before I came on board. I made my mark as a quintessential top-down kind of leader. The company changed me and taught me how to be a better leader. At the same time I’ve put enough structure in place that focuses people’s passion towards specific purposes. Overall, I’ve just gotten more comfortable. Ambiguity is good if you have smart people.

Here’s the danger, though. You’ve probably read about the chaos that developed with Zappos, where it experimented with their version of open (i.e. leaderless) management they call “holacra-cy.” Chaos degenerated into anarchy and then civil war to the point where people were resign-ing in droves. How do you con-trast what you describe in your book with this?

JW: I hope the book describes that managers play a really important role. The problem is middle managers have gotten a bad rap because middle managers used to be the people who

went for his wallet to pick-up the tab and realized he didn’t have it. Could Whitehurst spring for the coffee?

Next, Szulik asked Whitehurst to meet with Michael Cunningham, the company’s general counsel, at a local Mexican eatery. He did and had another great conversation, after which the restaurant informed them that its credit card machine was broken. Cash-poor, Cunningham turned to Whitehurst and asked him to cover the bill. To make matters worse, Cunningham offered to take Whitehurst to the airport but first had to get gas because his car was “running on fumes.” You guessed it. The gas station didn’t accept credit cards. Whitehurst had to pull out his wallet a third time.

Despite the inauspicious begin-ning, Whitehurst, the product of top-down, traditional, hierarchical organizations, soon embraced what he terms an “open organization” which he defines as one that “engag-es participative communities both inside and out—responds to oppor-tunities more quickly, has access to resources and talent outside the organization and inspires, motivates and empowers people at all levels.” He recently set forth these ideas in a book, The Open Organization.

Much has been written about “crowdsourcing,” which attempts to harness mass participation to generate big ideas and solve complex prob-lems. The Linux operating system, which played a key role in Red Hat’s start, is an open-source system where communities of people self-organize a problem or activity. The power of open networks has been championed by such gurus as Don Tapscott and inno-vation evangelist Henry Chesbrough. Companies such as Whole Foods, Pix-ar, Zappos and Starbucks are said to have implemented open organization precepts. But how does it really work and can it be scaled for most organiza-tions? That what we asked Whitehurst when he recently visited New York.

It probably spooked you when you joined Red Hat as CEO in 2007, having been an executive at traditional companies such as Delta Airlines and Boston Consulting Group. What did you find?

controlled the information flow.What I suspect happened at Zap-

pos was trying to have a leaderless organization without having any man-agers to direct things. It is a little bit like having a brain that has neurons, but not synapses.

How do you connect? How do you create meaning around strategy? How do you decide how much leash people get, and how do you connect and look for patterns? That’s what managers have to do. They need to enable. So, if you say in the old world any manager’s or leader’s job was to drive performance, today I would argue it’s still about performance, but it’s around how do you create the context in which your people can perform well.

If you’re saying you don’t have people to help create the context in which people perform well, it seems to me like it’s chaos. Again, maybe I’m wrong, but I think people need a degree of structure and that’s what managers provide. I’m not proposing a new grand theory of management. I’m just saying here’s a structure that works really, really well and has scale.

Is what you practice servant leadership?

JW: No, but it’s very similar. Servant leadership misses what I call the cat-alytic part of what I need to do as a leader. If serving is what one does to create the environment where good performance happens, I would agree. But I also try to catalyze direction by using what I talk about and the people I put in place and other things to catalyze a general direction. An example would be how we get to be more customer-focused, but still be

JAMES MATTISFOUR STAR GENERAL

Battle tested leadership lessons

from NATO’s Supreme Allied Commander &

Commander of the U.S. Joint Forces Command—

who led and inspired over 200,000 troops.

www.ChiefExecutiveLeadershipSummit.com

The premier event for mid-market CEOs and senior executives, focused

on practical take-home ideas with real bottom-line value for you & your

company’s leadership team.

Featured Speakers Include:

LEADERSHIP SUMMIT 2015NOVEMBER 5-6 • HILTON HEAD ISLAND, SC

Sponsored byCHIEF EXECUTIVE

FOR MORE INFORMATION ABOUT THE SUMMIT, GO TO

CHRIS MCCHESNEY

BEST-SELLING AUTHOR & GLOBAL PRACTICE

LEADER OF EXECUTION FOR FRANKLIN COVEY

How the best companies out-perform

their competitors by adopting

“The 4 Disciplines of Execution.”

LARRY LIGHT

FORMER GLOBAL MARKETING HEAD AT

MCDONALDS

Author of “Six Rules for Brand

Revitalization” will share a blueprint for leading

your brands to growth and

prosperity.

2015_CE_JA_LeadershipAd.indd 19 8/26/15 5:24 PM

20 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

a technology company. I didn’t go out and say we’re running a project to figure out how we get more cus-tomer-focused. I just started talking about it and people started to do things. Think of a coral reef. Plant a stick near the ocean shallows and walk away. Before you know it organ-ic life forms all around it.

You write that employee engage-ment has nothing to do with morale—something you learned at Delta Airlines when it filed for bankruptcy. Explain.

The Delta bankruptcy experience taught me that people really want to understand context more than anything. They want to understand the direction of the company and the role they play in it. Most of what we were doing at Delta was negative: cutting pay, laying people off, cutting benefits. I remember going into a meeting to talk about the direction of the company. Everyone’s initial reaction was to try to make people happy or tell them it’s going to be okay. Wrong. A leader’s job is to impart the facts so they know what’s coming and they can make informed decisions for themselves.

I was asked by a flight attendant what are we going to do about our morale? And my answer was “noth-ing.” Surprisingly I got a round of ap-plause. I said, “Look, my goal is to get the planes out on time, build a stable company, give you a great work envi-ronment so you serve the customer

well. I’m hoping if we do all those things you’ll be happier, but your morale ain’t my goal. My goal is to build a great company and hopefully that will make you happy.”

Engagement goes off track when you try to make employees happy versus saying here’s the strategy and how you fit into it. By imparting context and information, you end up doing different things and communicating different things than if it’s a morale exercise, which comes off as disingenuous. It generally becomes an HR-led thing versus a CEO-led thing.

What is it that you do that your nearest competitor cannot do or do as well?Our advantage looks a lot like Toy-ota. What I mean by that is Toyota’s source of advantage is its production system called Kaizen. They have been doing it for years and said to Ford, GM, and others, come look at how we do it. Yet, it’s hard for others to fully duplicate it because it’s a capabili-ties-based advantage. Our advantage is centered on being able to work in open source communities to deliver great technology. Sounds easy but one reason it’s hard to replicate, is that engineers like control and open

source immediately flips the model around because you don’t have control. You have to trust that the com-munities are going to do the right things.

Some traditional software companies think open-source is interesting and all that’s required is open-

ing up their code. But if you open up your code, but don’t make it inclusive, people don’t join or you make chang-es that go upstream. As a result, your engineers get frustrated and start doing their own thing.

There are 100 reasons why people aren’t successful doing it. Many tradi-tional software companies start with a brilliant CTO making an educated guess on where the world is going. Our model is completely different. We look outside and see what the most technically sophisticated people are doing. They’re probably doing it in open source because the Googles and Amazons are all doing that. We glom onto those things. We bring a consumable version of what Google or Twitter is doing to the enterprise. We don’t assume that we know where the future of technology is going. We make sure that we’re involved in the right communities to bring the right things.

THE ENVIRONMENTAL PROTECTION AGENCY spilled 3 million gallons of toxic sludge into a tributory of the Animas River in Colorado. The stinky yellow flume of old mine waste—rife with cancer-causing mercury and

arsenic—threatens to pollute the drinking and recreational water of three states. Had a private oil company acted so incompetently and negligently, it would have been fined bil-lions of dollars by the same EPA and its executives possibly subject to criminal prosecutions. The business’s reputation would have been tarnished for years. Just ask BP officials what the Obama Administration did to the corporation after the Deepwater Horizon oil spill of 2010 in the Gulf of Mexico.

Presidential contender BERNIE SANDERS deserves credit for his transparency as a socialist, but he frequently points to Sweden specifically and Scandinavia generally as utopian ideals. Yet, as Kelly McDonald argues in

The Federalist, in some ways Sweden is now less progress- ive than the U.S. Wealth inequality is more pronounced in Scandinavian countries than it is in the U.S. In Sweden, Denmark, Finland and Norway, the top decile of earners own between 65 and 69 percent of the country’s total wealth, an astonishing figure. Sanders is apparently unaware of this reality, given that one of his reasons for praising Scandinavia is its supposed low levels of wealth inequality.

THORNS ROSES

THORNS AND ROSES

Tarred by a Brush With Toxicity Sanders’ Scandinavian Sensibilities

WHO

Jim Whitehurst, CEO Red Hat Software

WHAT

$2 billion provider of open-source solutions

WHERE

Raleigh, NC

BUSINESS PRACTICE

“I answer every email I get.”

RECENT READS

Blindspot: Hidden Biases of Good People, by Mahzarin R. Banaji and Anthony G.

Greenwald; The Innovators, by Walter Isaacson

CEO WATCH

22 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

CHIEF CONCERN

DR. THOMAS J. SAPORITO is chairman and CEO of the consulting firm RHR International. This column is part of a series on leadership.

heavily involved in recruiting her. In this case, eventually the newer exec-utive was selected over the company veteran. The new CEO wanted to retain the veteran, expanding the role and addressing compensation with hopes of retention. But that led to another difficult situation, and the new CEO’s skills will be put to the test as the world of gray continues.

This story puts in high relief where the job of just about any big-compa-ny CEO resides: in the lonely, often murky “gray zone.” As Doug Conant, chairman of Avon and former CEO of Campbell Soup says, “The black-and-white, right-or-wrong decisions happen before they reach the CEO’s office. The gray area is where the CEO lives and proves his or her worth.”

This means that CEOs face less-clear-cut decisions on strategy, direction, and people. They have to proceed with the nuance, flexibility and maturity to navigate complex human variables that have as much to do with inference and, say, assessing levels of trust among colleagues as hard analysis.

The rub is that while the gray zone

is where the CEO position sits, it is not always the comfort zone.

I knew an exceptional CEO who got fired after executing a decision he knew was right for the company, but which went against the personal priorities and ingrained business values of the board chairman, whose family had founded the company. Although the CEO ana-lyzed the facts and thought the answer was clear, he failed to consider the un-derlying dynamics in the organization and on the board.

As Dominic Pileggi, former chair-man and CEO of Thomas & Betts, puts it, “When reacting and making decisions at the top, you have to oper-ate more like a dimmer switch than a simple on-off switch. Things are rarely black and white.”

So, how can CEOs prepare for the gray zone? They must continually ask, “Where is it necessary to have agreement among constituencies for an outcome to go well, even if I’m right and I’m the top boss?” They should also build a strong team of advisors who have license to challenge them.

And what can be done to ensure that top CEO candidates can thrive in the realm of the gray? Most important, smart boards must determine whether the potential leader is an agile thinker. Can she apply wisdom, nuance and a human element into decisions concern-ing trust, communication and power?

It is proven that this kind of agility is critical in the gray zone. According to a recent Harvard Business Review article, research showed that people who got high scores at “learning agility”—being able to adjust on the fly to changing conditions, process information quickly and effectively challenge the status quo—are also high performers in top leadership roles.

Hence, a maxim for CEO success might be: Seek out the best imperfect solution—the one that you can make work.

IT WOULD BE NICE for CEOs if deci-sions involved simply examining hard data and making the tough decisions. However, what constitutes the “right” decision is often unclear. Today’s CEOs sit in a world of nuances that require judgement, insight and the ability to weigh in on the soft issues—not just the hard ones. Whether it is strategy, handling complex nego-tiations, orchestrating senior team dynamics, handling a major customer relationship or CEO succession, CEOs must lead in a world of gray.

Take a financial services company faced with a CEO succession dilemma. The transition came at a difficult time for the company, as it struggled to meet new competition. On top of this, the board needed a candidate with the right balance of continuity and change.

Two strong internal candidates seemed prepared to take the reins. The first candidate was a company veteran, very close to board members. The sec-ond was newer to the firm and favored by board members who had been most

Fifty Shades of Gray: The Real World of the CEO

By Thomas J. Saporito

10%

6%

8%

4%

4% 40%

5%

3% 30%

2% 20%2%

1% 10%

-2%

0%

0% 0%

20% 30% 40% 50%

50%2Q 2014

24 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

MID-MARKET REPORT

THE RATE OF MIDDLE-MARKET revenue growth slipped this quarter, according to a recent survey of 1,000 c-suite executives by the National Center for the Middle Market, which also reported that expectations for future rates of revenue and employment growth declined for the second straight quarter. On average, mid-market companies reported second quarter revenue growth of 6.6 percent, down from 7.4 percent in Q1.

The middle market is also less enthusiastic about prospects for profits than it was at the start of the year. Though a respectable majority (86 percent) expect profit margins to grow or stay the same over the next year, the average projected increase in profitability is down from 3.1 percent to 2.4 percent. Concern about the availability and pricing of labor due to both minimum wage increases and a tighter labor market is one factor fueling this less optimistic outlook. Other issues include a dip in confidence about economic conditions and the business climate and the potential impact of an interest rate hike and/or higher energy prices. The statistics, tables and charts to follow offer a snapshot of how the middle market is performing and what’s in store for the rest of the year.

Growth Softens for the Middle Market Workforce issues and concern about economic growth and the

business climate are dampening gains.

Long Term Challenges (next 12 months)Employment issues—including hiring, retention and workforce qualifications—remain the top internal challenges facing companies over the coming year. Externally, leaders express growing concerns related to competition and the impact of government regulations.

A dip in confidence about economic conditions, business climate concerns and the potential impact of an interest rate hike are hampering hiring.

Staff/Employees

Business Growth

Finances

Costs

Government Regulations

Government Regulations

Competition

Costs

Economy

Business Growth

Finances

2Q 2014 2Q 2015

Revenue Growth Rate Outpaces the S&P For two years running, the mid-market has beaten the S&P in revenue growth.

Mid-Market Company Hiring Slows

MIDDLE-MARKET EMPLOYMENT GROWTH

INTERNAL CHALLENGES

EXTERNAL CHALLENGES

RESPONDENTS WHO PLANNED TO ADD JOBS

SOURCE: THE OHIO STATE UNIVERSITY FISHER COLLEGE OF BUSINESS, THE NATIONAL CENTER FOR THE MIDDLE MARKET

MIDDLE MARKET

S&P500

47%

22%

15%

17%

5%

24%

19%

14%

14%

13%

11%

3.9%47%

2.7%38%

LAST 12 MONTHS(MEAN)

NEXT 12 MONTHS (EXPECTED)

2Q 2015

THE AVERAGE PROJECTED INCREASE IN PROFITABILITY

AMONG MID-MARKET FIRMS HAS DROPPED FROM 3.1% TO 2.4%

% OF RESPONDENTS CITING THIS AS A TOP CHALLENGE

REVENUE GROWTH

26 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

FOR 30 YEARS, companies have sought to outsource and offshore information technology as a way to reduce costs and/or quickly improve performance. Mega-deals were done in the ’90s and then, after that market was saturated, lesser deals ensued. IT outsourcing deals are some of the largest financial commitments companies make, total-ing as much as $5 billion. What’s more, they often encompassed a company’s “crown jewels”—those mission-critical proprietary systems that provide a competitive advantage.

Recently, however, companies are insourcing that which was once outsourced. Why does one CEO outsource while another insources? What should CEOs consider when weighing their options?

THE DRIVE TO OUTSOURCE While there are many reasons compa-nies opt to outsource and send work offshore, cost-cutting typically tops the list of drivers. The promise of 20 to 25 percent savings to the bottom line is a powerful driver. Outsourcing can shift fixed costs to variable or, better yet, en-able contracts can be “financially engi-neered” to pull savings ahead, creating a windfall for current management.

Outsourcing can also enable a com-pany to quickly acquire new technical capability and capacity to expand, move into new markets or overcome inter-nal inertia. Outsourcing also becomes attractive when IT issues consume unreasonable amounts of management time and attention. However, there are pitfalls of which you should be aware.

PROBLEMS AND PITFALLSAn outsourcing contract defines your flexibility. How well or poorly the contract is written determines how nimble you can be. Many years ago, in the Ross Perot days, GM outsourced its IT. Recently, GM’s current CIO, Randy Mott, famously said, “When we have an urgent need for IT changes, I don’t call the programmers, I call the lawyers.” When systems provide a competitive advantage, this inflexibility becomes particularly problematic. The need for speed and control is one reason we’ve seen CEOs move to in-source. For exam-ple, JP Morgan canceled its $5 billion IT outsourcing deal with IBM and brought everything in house in 2004, as did Bank One a few years earlier.

Anticipated savings often go un-realized because contracts are badly written, poorly defining current and future situations. Frequently, busi-ness changes are not anticipated and vendors charge extra for each change. In addition, the skills necessary for maintaining and enhancing the sys-tems are often underestimated. During a recent network outage, the CEO of a

MAKING TECHNOLOGY WORK

high-volume financial payment proces-sor asked why the company’s technical expert was so slow to respond. “He was terminated last week as part of our outsourcing deal,” he was informed.

Furthermore, management sometimes squeezes vendors during negotiations. To break even, the vendor responds by strictly following contract

language and performs the bare min-imum, resulting in poor service.

Outsourcing and offshoring can also provoke social unrest within the company. Organization struc-ture and jobs change and people get

laid off. While this may be inten-tional to jog the organization into a

new operating paradigm, it invariably results in mistrust, passive-aggres-sive behavior and a dip in loyalty and productivity.

Finally, IT outsourcing is often a one-way street with supplier lock-in. During the transition, the vendor capitalizes on the talent and spreads it across multiple clients. Once lost, this technical expertise is difficult to re-acquire. Those folks are now gone and one has the challenge to find and train new talent to support the old custom systems.

CEO RESPONSIBILITYFor these reasons, CEOs and boards must carefully assess the rationale and consequences of both outsourcing and insourcing IT and be sure to craft a good contract. The benefits can look great particularly in the short run—but the pitfalls can cause significant damage later in the game.

Because the vendor has crafted hundreds of these deals, they are ex-perts at contract negotiation and have the upper hand. Your goals and theirs are different—you seek responsive, low-cost service. They seek profits. So, before you jump, it may be prudent to seek the advice of an experienced and independent advisor who is 100 percent focused on your goals.

The Rewards of Right-SourcingWhy IT sourcing matters to CEOs and boards. by Tom Pettibone

TOM PETTIBONE is a founding partner of Reston, Virginia-based Transition Partners, an IT management consulting firm and business.

26 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

SONNENFELD

JEFFREY SONNENFELD is senior associate dean for leadership studies; Lester Crown professor of leadership practice, Yale School of Management; president of the Yale Chief Executive Leadership Institute, and author of The Hero’s Farewell and Firing Back.

28 / CHIEFEXECUTIVE.NET / SEPTEMBER / OCTOBER 2015

THE TRADITIONAL CHANT when a new monarch ascends to the throne has been the unsentimental proclamation, “The king is dead, long live the king”—to instantly reas-sure all of the continuity of command. Such consolation is just as essential in business, where companies are often caught unpre-pared for the impact of a leader’s demise.

Silicon Valley was grief stricken when Survey Monkey’s CEO Dave Goldberg died suddenly May 1, while exercising during a family vacation. His wife, Facebook COO Sheryl Sandberg, had often cited her husband’s model of partnership in sharing their personal and professional lives as her “rock” and referred to him as “the love of my life.” The ripples of trauma, however, spread widely outside of their family and friends. Goldberg had taken the company from 12 employees to 450 and to a $2 billion valuation. To his colleagues and fellow tech titans, he was not a replaceable part on an assembly line of talent.

That sentiment is common after the unexpected demise of a business leader. Several analysts held out hope that Steve Jobs would reappear from his deathbed during Tim Cook’s first Apple keynote in October 2011. Every industry experiences its share of losses—which come in many forms. Last year, Autumn Radtke, the 28-year-old CEO of Bitcoin exchange First Meta, jumped to her death in Singapore. Arrowstream founder Steven LeVoie was shot by one of his own top lieutenants at age 54 in 2014. Arthur Gold-berg, 58, a fitness buff whose casino portfolio included Caesars and Bally’s, died in 2000. In heavy industry, Michael Walsh, age 51 and CEO of Tenneco, succumbed to brain cancer.

In the food industry, McDonald’s 60-year-old CEO, Jim Cantalupo, died of a heart at-

tack in 2004. The board hastily replaced him with 43-year-old Charlie Bell, who died nine months later. Wendy’s CEO Gordon Teter died at age 56 in 1999; his predecessor, James Near, had died in 1996 at age 58.

Over the past few months, Survey Mon-key has demonstrated how businesses can rally in the wake of such tragedy by:Mourning without defining the enter-prise by its past. Business had to go on—as Goldberg would have wanted. As Executive Chairman Zander Lurie, who stepped in as acting CEO, commented, “He truly was an egalitarian man who would give without ego. He just cared about investing in everything he was doing.”Projecting the leader’s legacy into the future. Goldberg’s widow, Sandberg, joined the Survey Monkey board a month after his death. She explained, “I am looking forward to working with the board and this amazing team and helping to realize Dave’s vision of building a lasting company that impacts the way we all do business for years to come.”Bringing in respectful but fresh and cred-ible new leadership. A major search firm worked with the board to size up internal and external candidates. By July, industry veteran Bill Veghte was named the new CEO. Veghte, a cloud expert who had held top jobs at Microsoft and HP, has the skills to fulfill the firm’s new direction. Equally important, he had been a friend of Goldberg’s for 30 years and considered him a mentor. Rather than seek to minimize grief, redirecting it into a purposeful mission. Veghte declined Goldberg’s office, stating, “I share in the loss that everyone feels. For me, from out of this searing sadness comes fierce determination.” Employees applauded with tears and cheers.

Several analysts held out hope that Steve Jobs would reappear from his deathbed during Tim Cook’s first Apple keynote.

The King is Dead,Long Live the KingAlways tricky, leadership transitions get even tougher when a CEO departs the world along with the job. By Jeffrey Sonnenfeld

ILL

US

TR

AT

ION

BY

TIM

TO

MK

INS

ON

Jeffrey Sonnenfeld

NEGOTIATE WITH

KNOWLEDGE

Save $500 by ordering directly through

ChiefExecutive.net/CompReport

CEO & SENIOR EXECUTIVE

COMPENSATION REPORT

FOR PRIVATE COMPANIES

2015-2016

Pre-order today. The report will be released

on August 17th.Price: $2,995

$2,495

Attract the best candidates

Retain your top talentMotivate your team

to drive your business’ results

Align executive pay with the strategic goals

of the business

CORPORATE PHILANTHROPY

30 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

Lessons in Good Giving

How companies that prioritize social change are using philanthropy to make it happen—and what they’re getting backby C.J. Prince

ILLUSTRATION BY THE HEADS OF STATE

SEPTEMBER/OCTOBER 2015 / CHIEFEXECUTIVE.NET / 31

Lessons in Good Giving

Key Takeaways

Make it Personal Identify and leverage the unique skills or

expertise your organization can bring to bear to benefit the cause

Encourage Volunteerism Giving employees one day per year to

volunteer with the charity their choice can boost enthusiasm and productivity

Get Involved Employees will take it seriously if they

see the CEO participating

Ask Employees Invite employees to submit suggestions for

worthy causes and host a companywide vote to choose the charity you will support

1 2

43

GIVING ON THE RISEWhile still not at pre-recession levels, corporate giving rose by 12 percent in 2014 over the prior year to $17.8 billion, according to “Giving USA,” an annual report on American philan-thropy. The report attributed some of that upswing to faster growth in cor-porate pre-tax profits and the gross domestic product, but at least some of the increase can be attributed to more companies across the spectrum participating with in-kind donations and volunteer hours counting along with cash.

“Passing out United Way checks is faceless, nameless and, frankly, meaningless for creating a culture of helping people,” says Tony Aquila, founder and CEO of Solera, a 10-year-old, $1.3 billion provider of risk and asset management software and services to the insurance industry. Instead, Solera funds six philanthrop-ic expeditions per year that allow em-ployees to take up to a six-month paid sabbatical to work on an approved project.

Aquila believes that this deeply personal work benefits his employees

and the company’s culture at least as much as those they help. “This is not about ‘corporate philanthropy,’” he asserts, noting that he objects to the term. “It’s about giving not only to those lives that you touch but the lives within your company that you allow to touch them.”

More and more often, companies are seeing the causal relationship between giving back to the commu-nity, whether local or global, and the company’s own health. “What’s changed over the years is that it used to be a ‘nice to do,’” says Daryl

NOT LONG AGO, a company’s philanthropic strategy largely boiled down to a decision about which large, generic charity would receive a donation and how big of a check should be cut. Employees were seldom involved save for very high levels and the giving, done overwhelmingly by big companies with deep pockets, had little to do with the rest of the company’s strategy for growth. ¶ But times have changed. Although companies are still writing checks, they’re doing it in the context of carefully crafted strategies that target specific causes based on geography and/or alignment with business goals. When they do write checks, they expect transparency and results-oriented data. They supplement cash contributions with product donation, skills-based volunteering and long-term relationship building with nonprofit organizations to provide ongoing resources. The choice of cause to support is no longer dictated by the CEO’s passion but rather by company strategy, with employees contributing their vision for making the world a better place.

32 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

Brewster, CEO of CECP, a coalition of 150 Fortune 500 CEOs who believe that investing in societal engage-ment brings a critical return. “We’re approaching an emerging sea change as leading companies move from occasional check-writing to increased community engagement, viewing so-cietal advancement as a key measure of business success.”

The market has responded in kind. Brewster points to the 2012 study by Babson professor Raj Sisodia, which looked at 28 companies identified as the most conscious—“firms of endearment” as Sisodia calls them—based on characteristics such as their stated purpose, compensation, quality of customer service, investment in their communities and impact on the environment. Out of the 28, the 18 companies that are publicly traded outperformed the S&P 500 index by a factor of 10.5 over the years 1996-2011.

Jane Madden, managing di-rector and head of U.S. Corporate Responsibility for global PR firm Burson-Marsteller, says the outper-formance of socially responsible com-panies isn’t so much about investors rewarding companies for their good deeds as it is that those companies

that invest in their environments and communities make better strategic decisions. “If you are measuring and managing your environment, includ-ing social and governance impact, you’re just a smarter company. You’re minimizing risk and maximizing opportunity and that has a definite positive impact on the bottom line.”

MORE WAYS TO GIVEJohn Ferdinandi makes it a practice to get engaged in the local communities in which his company, Milano Restau-rants, operates. With 43 restaurants and 18 franchises located primarily in California, Milano habitually approaches local communities to find out what they most need. That pres-ence and involvement gives Milano an advantage vis-à-vis other fast-casual restaurant chains.

“We want the consumer to know that we’re more than just a chain coming in,” says Ferdinandi. “It’s the idea that we’re not just here to sell you a good or service, but to partici-pate. Your issues are our issues, and a stronger community is a benefit both to the community at large and to the business operating within it.”

The data show that consumers in-creasingly do make purchasing deci-sions based on a company’s corporate citizenship. According to Nielsen’s 2014 corporate social responsibility survey, 55 percent of global respon-dents said they are willing to pay

extra for products and services from companies that are committed to pos-itive social and environmental impact, up from 50 percent in 2012 and 45 percent in 2011.

Milano has primarily focused on youth-oriented philanthropy and projects that feed the poor, and is an example of the creativity companies are using to design efficient ways to give back to communities. Most recently, Blast 825 Pizza, a quick-fired pizza concept and division of Milano Restaurants, opened a new restaurant in Rocklin, California, and initiated a program called “Blast Buddies” to support pet-centric causes in each restaurant’s local area. Represen-tatives from the charity come in and design their own custom pizza. Then, for a month, that pie stays on the menu with proceeds going to the charity and Blast 825 matching. For the Rocklin opening, the Placer SPCA designed a signature pizza they dubbed the “Pet Lover’s Pizza,” which raised more than $6,000 for the charity.

Ferdinandi notes that due to tech-nology and social media the public is more aware and involved in different causes. “We can get more information out to more people about a subject like feeding the poor or helping animals than we could 10 years ago,” he says.

For customer-facing retail food service companies like Milano, it may be relatively easy to find a charitable cause that integrates well with the company’s mission. Others have to reach outside their core competencies, but they operate on the same princi-ple that a better world means a better world for business as well. “If you had a factory in Guatemala or Mexico, and you were surrounded by villages who were very hostile to you, it would be to your best interest to go out and cre-ate prosperity and stability in those villages, so you would have more freedom to operate and wouldn’t have the pressure of security, or the need to move your factory at great expense,”

When you do this stuff, you end up reaping these ancillary benefits YOU DIDN’T ANTICIPATE WHEN YOU STARTED OUT.”

- David Sanford, WinterWyman

CORPORATE PHILANTHROPY

SEPTEMBER/OCTOBER 2015 / CHIEFEXECUTIVE.NET / 33

2014 CORPORATE GIVING, UP 12% FROM LAST YEAR

PEOPLE WHO WOULD PAY EXTRA FOR PRODUCTS AND SERVICES FROM PHILANTHROPIC COMPANIES

55 PERCENT

SIXTY-ONE

$17.8 BILLIONsays Stephen Miller, CEO of Dillon Gage Metals, who objects to the term “giving back.” “It kind of implies that business people have taken things and now we’re feeling guilty, so we’re going to give it back to the poor folks. Most of the men and women I know in business have worked their tails off and sacrificed a great deal for the success they enjoy. So, for me, this kind of work is not a social payback. It’s just plain smart business.”

In 1984, Miller cofounded the non-profit HELPS International to provide relief and development services for the country of Guatemala. The organization also provides loans to farmers to purchase quality fertilizer and tools to grow corn more efficient-ly. Executives and employees at Dillon Gage support HELPS by participating in community projects, including installing new stoves and water filters in homes, which save villages hun-dreds of thousands of dollars each year. Other employees participate by raising money or covering for employ-ees who travel to Central America to donate time and service.

A RECRUITING ADVANTAGEMiller notes that people genuinely like to work for “good” companies. “They like to know that the people who em-ploy them are concerned about others and are developing programs that give back and allow employees to give back,” he says. The more connected they feel to their employer, outside of their normal job description duties, the longer they’ll remain with the company, which ultimately saves the company thousands of dollars in turnover costs.

Miller is among many CEOs find-ing that good corporate citizenship is increasingly an advantage in the ongoing war for talent. A 2011 Deloitte Volunteer Impact study found that 61 percent of Millennials consider a com-pany’s commitment to the community when making a job decision.

“One of the things I’ve seen in the

Millennial generation is that they have a real desire to give back to the community. But it’s also intensely personal for them,” says Joe Schum-acher, president and CEO of Goddard Systems, which operates the Goddard School franchise. Schumacher insti-tuted a program to offer the compa-ny’s 140 corporate-office employees “volunteer time off,” or eight VTO hours to help the charity of their choice. “I’m not an expert on the evo-lution of this, but 10 or 20 years ago, corporations would say, ‘This is what we’re doing.’ I felt that empowering employees to make their own choices would be more meaningful.”

Bob Boudreau, CEO of WinterWy-man, a global recruiting firm, agrees. When he formalized the compa-ny’s giving strategy 10 years ago by creating a new role for community development and employee engage-ment and establishing a new commit-tee to develop philanthropic projects and execute them, he was clear on one thing: “I said, ‘I don’t want this to be the Bob Boudreau philanthropic club. I want it to be what you guys want it

to be’. I do not have veto power.” Even as a recruitment firm,

WinterWyman’s senior team did not expect the new strategy to impact its own recruiting. “That wasn’t even on our radar screen,” says David San-ford, EVP, client relations. “[Doing good] was our initial driver, but what we found was that when you do this stuff, you end up reaping these an-cillary benefits you didn’t anticipate when you started out. As we were working the marketplace and trying to attract people, 20- and 30-some-things, that became an important part of why they wanted to come here.”

Bill Austin, founder and CEO of Starkey Hearing Technologies, puts it simply: “People like to be served by people who care.” Starkey, a Minnesota-based, 4,100-employee company that is the largest hearing aid manufacturer in the U.S., has its own foundation that has pledged, as part of the Clinton Global Initiative, to fit one million people across the globe with hearing aids this decade. Austin spends the majority of his time doing hearing aid fittings for

PERCENTAGE OF MILLENNIALS WHO CONSIDER A COMPANY’S COMMITMENT TO THE COMMUNITY WHEN MAKING A JOB DECISION

34 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

Tell us about your company’s initiative and be eligible for Chief Executive’s first-ever Corporate Citizenship Awards honoring those that:

•RECOGNIZE key employees involved in citizenship efforts

•DEMONSTRATE CEO leadership and commitment toward citizenship efforts

•HONOR and bring attention to the causes they care about

•INSPIRE other CEOs to improve our communities

Winners will be judged by a volunteer committee comprised of peer CEOs. Thirty companies in three categories (small, medium and large) will be honored in the magazine and at an event to be held in New York in Spring 2016.

challenging cases around the globe, and freely admits the company could be earning more if he worked more hours on the business side. “But then I’d have no life. So I traded money for life,” he says, pointing out that many younger employees are all too happy to make that same tradeoff today. That might not work as well, he adds, if his company were not privately owned. “I would be sued by my shareholders if I was public,” he says.

Edwards Lifesciences is a public company, but CEO Michael Mus-sallem says they’ve been able to keep the board happy by watching global-giving norms among high performing companies. “We try to stay mindful of that and responsible from a shareholder point of view.” That means creating clear goals with measurable results. Last year, the Edwards Lifesciences Fund celebrat-ed its 10th anniversary by launching a new initiative called “Every Heartbeat Matters,” with a 2020 goal to impact the global burden of heart valve disease by supporting the education, screening and treatment of 1 million

underserved people. The fund will support 25-plus nonprofit partner or-ganizations selected to help Edwards Lifesciences reach its target.

“We expect, in return, that they will be able to tell us what their results are,” Mussallem says. “How many people who were underserved did you treat, how many were screened and so on. We keep score on that.” The company also has a challenge that every one of its 9,500 employees participate in at least one

charitable activity per year. They’re close to 75 percent now, and Mussal-lem is confident they will reach full participation.

Mussallem notes that for a long time, the prevailing wisdom was that it might be idealistic to think you could have both a rewarding return for shareholders and be a great place to work. But, as it turns out, the two really go hand in hand. As Boudreau puts it, “It’s not rocket science. It’s just got to matter to you.”

Passing out United Way checks is faceless, nameless and, frankly, MEANINGLESS FOR CREATING A CULTURE OF HELPING PEOPLE.”—Tony Aquila, Solera

Visit chiefexecutive.net/SOPhilanthropy to learn about Edwards Lifesciences philanthropic work under CEO Mike Mussallem.

Do You Have a Great Corporate Citizenship Effort?

CORPORATE PHILANTHROPY

Whether your efforts are local, national or global, visitwww.chiefexecutive.net/corporatecitizenship

to tell us your story to recognize your people and inspire others.

MERGERS & ACQUISITIONS

“Simon says: Don’t push

round pegs into square holes.”

A

TOGETHER

PIECING

FOODS

Deal guru IRWIN SIMON, founder and CEO of Hain Celestial, knows how to make mergers work. By Warren Strugatch

NATURAL

EMPIRE

LAST APRIL WAS A BUSY TIME AT HAIN CELESTIAL GROUP. At its corporate headquarters on Long Island, not far from Manhattan, the organic and natural foods company was fast approaching its first $2 billion sales year. Irwin D. Simon–founder, chairman, CEO and president—was as usual perusing roll-up deals. At the moment, Simon was hot on the trail of an organic bakery called Rudi’s in Boulder, Colorado. Rudi’s was located near the Celestial Seasonings tea line he bought in 2000. Later that month, Simon shook hands with the Charter Equity Partners deal team, paid the PE firm $61.3 million in cash and common stock and walked away owning an organic bakery. The bolt-on acquisition gave Hain Celestial about 60 new better-for-you products, including wraps, pizza crusts, breads and bagels. Simon was happy to enter the fast-growing market for whole-grain, organic and gluten-free baked products without having to develop a product line from scratch.

SEPTEMBER/OCTOBER 2015 / CHIEFEXECUTIVE.NET / 37

38 / CHIEFEXECUTIVE.NET / SEPTEMBER/OCTOBER 2015

That might be a stretch, but clearly scouting deals at industry forums and gatherings is one way Simon keeps his deal pipeline full. A major stop every year is the Expo West Natural Products tradeshow held in Anaheim in March. At shows like Expo West, the curly-haired, effusive Simon is the most recognizable figure in today’s nat-ural and organic food sector, a walking exit plan for health-food company founders around the world.

“Irwin is very approachable,” says Siegel. “And he’s very fair. He strikes a reasonable deal. That reputation helps him get more deals.” While founders and key managers are often welcomed into the fold to oversee the post-deal integration, most do not stay on after the companies have blended.

In 2013, during a conversation at Simon’s headquarters in Lake Success, New York—he bought and moved into the sprawling structure built for the United Nations in the late 1940s—the acquisitive founder expounded on his approach to deal-making and his overall management philosophy. “At Hain Celestial, we’ve built out a strong infrastructure of sales, marketing and manufacturing,” he began. “My philosophy is that if we can find great companies that need these functions, and we can buy them and bring them into Hain, we can do better than if

we started from scratch. All these acquired companies—their payables, their collections, their customer service, all their processes—can be run out of here. This makes for a lot of savings and enormous synergies. When these conditions are met, we are going to see a lot of growth.”

Many of Simon’s deals have been for small companies that seemed to hit invisible ceilings, then got energized within Hain’s global sales and distri-bution channels. A key part of Simon’s deal-making acumen is his ability to see M&A as a two-way street. Not only does he plug new acquisitions into his global network, but he absorbs the networks he’s just acquired and works those channels.