Chapter V: Special Topics Concerning Access to...

33

Conference Edition 126 Chapter V: Special Topics Concerning Access to Finance This Chapter looks at three special topics that are closely connected to issues of access to financial services, namely: Micro- Small- and Medium-sized Enterprises (MSMEs); international workers’ remittances; and mobile banking. The issues in each area are quite different, as are the policy options. V.1 MSMEs and Access to Finance 93 MSMEs are widely recognized as very important in any country’s economic development. The underlying reasons are clear: international evidence indicates that they account for some 98% of all enterprises; they employ about 60% or more of the private sector workforce; they create about 50% of value added; and they account for about 30% of direct exports. 94 In rural areas of large countries like Indonesia, where large enterprises are few in number, development of MSMEs is almost synonymous with sustainable poverty alleviation. Moreover, the micro enterprise component is the backbone of the informal sector, which accounts for some 70% of total employment in Indonesia. 95 Several international surveys regularly find that aspects related to financing are some of the critical constraints faced by MSMEs – ‘Cost and Access to Credit’ are usually a major problem. In the specific case of Indonesia, a Bank Indonesia survey, described in Section V.1.2, took a broader perspective and found variation within MSMEs. 96 For its part, The World Bank/IFC’s ‘Doing Business’ indicator 97 for 2009 ranked Indonesia 109th out of 181 countries in terms of ‘Getting Credit’, on a par with countries like Uganda, Nepal, Bolivia and Belarus. The OECD, in its 93 On Government of Indonesia definitions, a Micro Enterprise is a productive business unit owned by an Indonesian family or individual and with turnover up to Rp100 million per annum (Decree of the Minister of Finance No. 40/KMK.06/2003, issued on January 29, 2003). A Small Enterprise is any kind of business unit with net assets up to Rp200 million (excluding land and building for business site), or with turnover up to Rp1 billion per year, owned by an Indonesian, independent and not a branch or subsidiary of certain firms (Law No. 9 Year 1995 on Small Businesses). A Medium Enterprise is a business that has annual turnover of between Rp1 billion to Rp50 billion and with net assets between Rp200 million and Rp10 billion, excluding land and building for business location (Presidential Instruction No. 10/1999 on the Empowerment of Medium Businesses). 94 See APEC (2002). 95 For August 2008 on OECD definitions. See footnotes to Table 3.1 of OECD (2008) and http://wwww.bps.go.id/sector/employ/table3.shtml. 96 For example, almost all micro and small businesses, and all medium businesses, have used banking services. For credits, the main considerations are the interest rate and location; the main obstacle for micro businesses is collateral whereas for small and medium businesses, it is high interest rates. 97 See http://www.doingbusiness.org.

Transcript of Chapter V: Special Topics Concerning Access to...

Conference Edition

126

Chapter V: Special Topics Concerning Access to Finance This Chapter looks at three special topics that are closely connected to issues of access to financial services, namely: Micro- Small- and Medium-sized Enterprises (MSMEs); international workers’ remittances; and mobile banking. The issues in each area are quite different, as are the policy options. V.1 MSMEs and Access to Finance93

MSMEs are widely recognized as very important in any country’s economic development. The underlying reasons are clear: international evidence indicates that they account for some 98% of all enterprises; they employ about 60% or more of the private sector workforce; they create about 50% of value added; and they account for about 30% of direct exports.94 In rural areas of large countries like Indonesia, where large enterprises are few in number, development of MSMEs is almost synonymous with sustainable poverty alleviation. Moreover, the micro enterprise component is the backbone of the informal sector, which accounts for some 70% of total employment in Indonesia.95

Several international surveys regularly find that aspects related to financing are some of the critical constraints faced by MSMEs – ‘Cost and Access to Credit’ are usually a major problem. In the specific case of Indonesia, a Bank Indonesia survey, described in Section V.1.2, took a broader perspective and found variation within MSMEs.96 For its part, The World Bank/IFC’s ‘Doing Business’ indicator97 for 2009 ranked Indonesia 109th out of 181 countries in terms of ‘Getting Credit’, on a par with countries like Uganda, Nepal, Bolivia and Belarus. The OECD, in its

93 On Government of Indonesia definitions, a Micro Enterprise is a productive business unit owned by an Indonesian family or individual and with turnover up to Rp100 million per annum (Decree of the Minister of Finance No. 40/KMK.06/2003, issued on January 29, 2003). A Small Enterprise is any kind of business unit with net assets up to Rp200 million (excluding land and building for business site), or with turnover up to Rp1 billion per year, owned by an Indonesian, independent and not a branch or subsidiary of certain firms (Law No. 9 Year 1995 on Small Businesses). A Medium Enterprise is a business that has annual turnover of between Rp1 billion to Rp50 billion and with net assets between Rp200 million and Rp10 billion, excluding land and building for business location (Presidential Instruction No. 10/1999 on the Empowerment of Medium Businesses). 94 See APEC (2002). 95 For August 2008 on OECD definitions. See footnotes to Table 3.1 of OECD (2008) and http://wwww.bps.go.id/sector/employ/table3.shtml. 96 For example, almost all micro and small businesses, and all medium businesses, have used banking services. For credits, the main considerations are the interest rate and location; the main obstacle for micro businesses is collateral whereas for small and medium businesses, it is high interest rates. 97 See http://www.doingbusiness.org.

Conference Edition

127

pioneering Survey of Indonesia,98 asserted that access to credit is particularly difficult for SMEs, especially those operating in the informal sector. It took special note of the collateral issue.

As suggested by the preceding discussion, most financial studies of MSMEs focus almost exclusively on access to credit (that is, loans). By contrast, this study considers access to a much wider range of financial services, especially for Micro enterprises, which often operate in the informal economy at the household level (as indicated in the pyramid diagram, above).

V.1.1 Key Findings of Bank Indonesia’s Survey of MSMEs

The survey reported in Chapter III focused on households’ access to financial services rather than MSMEs’. However, much of the data reported in Chapter III (especially those for non-farm enterprises, freelance workers and the self-employed) are relevant for Micro and Small enterprises, because they mainly operate at the household level. To broaden the results—so as to include Medium enterprises or to ensure that only enterprises are included—it is useful to examine a survey targeted directly on MSMEs.

Bank Indonesia has done such a survey of MSMEs and their characteristics in Indonesia.99 The survey covered 11,000 respondents in 11 provinces and pursued many topics (such as 98 OECD (2008). 99 See Bank Indonesia (2005).

Large

Medium Enterprises

Small Enterprises

Micro EnterprisesHousehold Level (informal Economy)

Conference Edition

128

managerial issues, inputs and production, marketing, and manpower), and it includes a review of 6 other research studies on MSME problems in Indonesia. For the purposes of this report, the BI study is the main source of descriptive information on MSME issues in Indonesia. The highlights of the study are summarized immediately below, by topic area of special interest to this report; the interested reader is referred to Bank Indonesia (2005) for extensive details.

BI Survey Results: Legal Issues & Business Development

• Most MSMES do not have an official legal status, especially at the micro level. • Most micro businesses don’t have business licenses (TDI/TDP and SIUP) or a Tax Registry

Number (NPWP); half of small businesses have them; most medium-scale businesses have them.

• Costs, procedure and administrative requirements are not obstacles to obtaining business licenses and NPWP.

• The main reasons for having business licenses and NPWP is to obey government regulations and to obtain credit.

• Few micro and small businesses have cooperation agreements with big businesses, but they can see the advantages.

• Few MSMEs believe that they benefit from existing government programs. • Their greatest needs from the government are credit, training and market information.

BI Survey Results: Financing Issues

• Most MSMEs transact in cash. Nonetheless, almost all micro and small businesses, and all medium businesses, have used banking services.

• In choosing banks, safety is their main consideration for deposits; for credits, the main considerations are the interest rate and location.

• The main obstacle for micro businesses is collateral; for small and medium businesses, it is high interest rates.

• Most micro and small businesses believe that banks allocate insufficient credit for MSMEs. Medium businesses find the allocations fair.

BI Survey Results: Banks’ Policies towards MSMEs

• To increase credits to MSMEs, commercial banks believe that better credit analysis is the internal key, including training of their staff. BPRs believe the key is supervising and collecting payments.

• The external key for banks is linkage programs with BPRs and cooperation with the credit guarantee institution.

Conference Edition

129

• For micro credits, most banks do not require licenses (SIUP, NPWP, etc.). For small businesses, requirements are tighter; for medium businesses, almost all banks require all types of licenses.

• For micro businesses, most collateral is movable (e.g. cars and motorcycles). Small and medium businesses mainly use land and buildings.

BI Survey Results: The Main Constraints

• Human resources development, including in finance, marketing and production. • Legal development, especially in the area of easier licensing. • The credit guarantor institution (e.g., offices, premiums, and claim procedures)

In reviewing these results, three main points stand out from the rest. First, problems of access to finance become more difficult as the scale of the business decreases, despite efforts at increased flexibility on the part of the banks. Second, existing government programs are not working well. And third, manpower weaknesses (on the sides of the MSMEs, banks and possibly government institutions) look to be at the root of many of the most basic problems.

V.1.2 MSME Lending & Policies in Indonesia

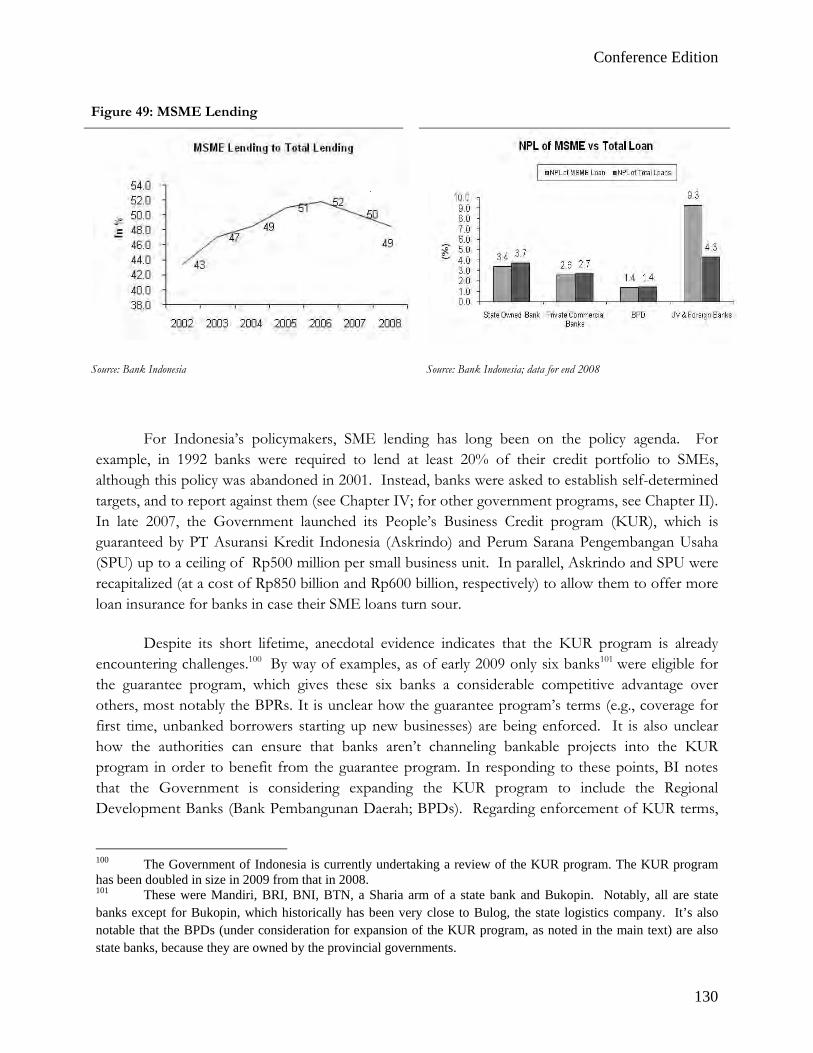

Notwithstanding the many problems mentioned in the previous Section, lending to MSMEs in Indonesia appears to have a relatively strong, established position in banks’ portfolios. Its share in total lending has been climbing in recent years, but may have stabilized around 50% (see Figure 49). This is just a bit lower than the 55% of GDP which they produce, according to the Minister of Cooperatives and Bank Indonesia. In addition, the quality of loans to MSMEs compares favorably with conventional loans, using the metric of non-performing loans (Figure 49, and a presentation by Bank Indonesia staff during field work for this report). This is consistent with the experience of BRI, which has 86% of their loan portfolio extended to MSMEs, while maintaining an NPL ratio that is a bit below the industry average (2.9% vs. industry’s 3.3%, as of September 2008).

Conference Edition

130

Figure 49: MSME Lending

Source: Bank Indonesia Source: Bank Indonesia; data for end 2008

For Indonesia’s policymakers, SME lending has long been on the policy agenda. For example, in 1992 banks were required to lend at least 20% of their credit portfolio to SMEs, although this policy was abandoned in 2001. Instead, banks were asked to establish self-determined targets, and to report against them (see Chapter IV; for other government programs, see Chapter II). In late 2007, the Government launched its People’s Business Credit program (KUR), which is guaranteed by PT Asuransi Kredit Indonesia (Askrindo) and Perum Sarana Pengembangan Usaha (SPU) up to a ceiling of Rp500 million per small business unit. In parallel, Askrindo and SPU were recapitalized (at a cost of Rp850 billion and Rp600 billion, respectively) to allow them to offer more loan insurance for banks in case their SME loans turn sour.

Despite its short lifetime, anecdotal evidence indicates that the KUR program is already encountering challenges.100 By way of examples, as of early 2009 only six banks101 were eligible for the guarantee program, which gives these six banks a considerable competitive advantage over others, most notably the BPRs. It is unclear how the guarantee program’s terms (e.g., coverage for first time, unbanked borrowers starting up new businesses) are being enforced. It is also unclear how the authorities can ensure that banks aren’t channeling bankable projects into the KUR program in order to benefit from the guarantee program. In responding to these points, BI notes that the Government is considering expanding the KUR program to include the Regional Development Banks (Bank Pembangunan Daerah; BPDs). Regarding enforcement of KUR terms,

100 The Government of Indonesia is currently undertaking a review of the KUR program. The KUR program has been doubled in size in 2009 from that in 2008. 101 These were Mandiri, BRI, BNI, BTN, a Sharia arm of a state bank and Bukopin. Notably, all are state banks except for Bukopin, which historically has been very close to Bulog, the state logistics company. It’s also notable that the BPDs (under consideration for expansion of the KUR program, as noted in the main text) are also state banks, because they are owned by the provincial governments.

Conference Edition

131

BI appears to rely heavily upon its Debtor Information System (SID) to check the borrower’s credit history and to see if the project has already received credit. In the course of its review of the KUR program, the government might consider allowing more banks to qualify for the program, including a good mixture of private banks and BPRs, not just state-owned banks. Also, the pricing structure of the guarantee could provide an incentive to increase the quantity and quality of small loans, and the terms should be designed ultimately to convince bank management that the guarantee is not needed.102 An exit strategy would also be useful.

As next steps, the Government could look at the other government programs run out of various ministries that attempt to channel financing into preferred sectors (see Chapter II.6). These programs are heavily dependent upon government financing and they crowd-out other micro-finance operations that are often struggling to be self-sustaining. Also, these programs’ subsidized nature invites corrupt administrative practices and encourages a culture of non-repayment. Like the KUR program, these would benefit from an independent, external assessment of their effectiveness. Participation could include local think tanks, industry associations and NGOs with special interests in the area.

Reflecting the ineffectiveness of these many programs, there are continuing controversies as to whether MSMEs have adequate access to finance. Proponents of this view argue ‘under-lending’ to MSMEs because they account for 99% of all business units and 96% of the employed labor force (Figure 50), but receive only around half of bank credits. Comparing output to lending by sector (Figure 50), SMEs operating in agriculture, construction, trade, transportation and business (financial) services are said to be particularly under-serviced. Proponents conclude that there are many untapped, potential investments that could be undertaken by MSMEs, if the financing were available. In this regard, they point to foreign-owned and joint venture banks as the main culprits;103 those banks account for 14% of total lending, but only 4% of lending to MSMEs. Proponents believe that an active SME lending policy would boost job creation and real sector growth in Indonesia.

This issue is partly explained by definitions; Bank Indonesia’s definitions do not match those of the Government.104 For practical reasons,105 Bank Indonesia currently defines small-scale credits by size of credit, not by size of the borrower. Consequently, roughly half of MSME credits are for

102 For example, the price of the guarantee could be proportional to the size of the MSME portfolio. And, the guarantee could only kick-in after a time threshold (say 3 months) when NPLs exceeded some pre-determined ratio (say 3%). 103 State-owned banks (SoB) are sometimes cited as neutral is this regard (see Figure 50), but this is only true for them as a group. The great majority of SoB lending to MSMEs is accounted for by BRI. 104 BI defines a micro credit as up to Rp50 million; a small credit is between Rp50 million and Rp500 million; and a medium-sized credit is between Rp500 million and Rp5 billion. (p. 79 of Bank Indonesia (2005)). According to BI staff, this definition is under review, with the intention of bringing it into line with the government’s definition. For GoI’s definition of an MSME, see footnote 116. 105 For example, it is very difficult to tell the difference between a motorcycle purchased for personal use and one that is purchased for small business purposes, like an ojek (a motor cycle taxi).

Conference Edition

132

consumption (that is, for consumer loans), not for investment.106 Effectively then, lending to MSMEs is only about half the amounts normally cited from official sources.

106 See Table 9.5 in Bank Indonesia (2007).

Figure 50: MSME Characteristics

MSME & Large Enterprise Business Units

MSME & Large Enterprise Employees

Breakdown by Loans Breakdown by Output

Breakdown of SME Lending by Type of Bank

Source: Bank Indonesia. Data for June 2007

Electricity, Gas, and Water

0%

Construction0%

Trade, Restaurants, and

Hotel27%

Transportation and

Communication6% Agriculture

53%

Services6% LEs

0.01%

Financial, Rental, and Business

Services0%

Manufacture Industry

7%

Mining1%

Electricity, Gas, and Water

0%

Construction1%

Trade, Restaurants, and

Hotel24%

Transportation and

Communication4%

Agriculture43%

Services11%

LEs4%

Financial, Rental, and Business

Services1%

Manufacture Industry

11%

Mining1%

By Lending

31%9% 20% 21% 31%

64%25% 30%

52%90%

69%91% 80% 79% 69%

36%75% 70%

48%10%

0%20%40%60%80%

100%

Agr

icul

ture

Min

ing

Man

ufac

turin

g

Elec

trici

ty,

Gas

, and

Wat

er

Cons

truct

ion

Trad

e

Tran

spor

tatio

n

Busin

ess

Serv

ices

Sosia

l Ser

vice

s

Oth

ers

(%)

SME LEs By GDP

87%

8% 13% 1%

44%75%

30% 17%40%

9%

3% 12%8%

22%

21%

24% 47% 8%

4%

89% 75% 92%

34%4%

46% 36% 52%

0%20%40%60%80%

100%A

gric

ultu

re

Min

ing

Man

ufac

ture

Indu

stry

Elec

trici

ty, G

as,

and

Wat

er

Build

ings

Trad

e,Re

staur

ants,

and

Tran

spor

tatio

nan

dFi

nanc

ial,

Rent

al, a

nd

Serv

ices

(%)

SEs MEs LEs

35% 34%

8% 14%

40%48%

14%4%3%

0%

20%

40%

60%

80%

100%

Total Lending SME Lending

Non-ForexCommercial Banks

JV and ForeignOwned Banks

Foreign ExchangeCommercial Banks

RegionalDevelopment Banks

State-owned Banks

Conference Edition

133

Another factor concerns the high overheads associated with conventional commercial bank lending, in part because they are subject to relatively strict regulatory oversight. More to the point, MSME lending is still risky unless there is strong loan supervision, which entails high administrative costs that can only be borne by institutions with a strong local presence. Even BRI, with one of the largest branching networks in the world, leaves the lower end of this segment to other players. For most conventional commercial banks—especially foreign and joint venture banks - this business is difficult, because they lack the requisite neighbourhood knowledge, relationships and trust. As technology brings costs down (see Box 56), the more aggressive commercial banks can be counted upon to move into these segments, because they will be attracted by the opportunities for profit. In the meantime, the real issue is how to bring down artificial barriers to faster progress; how to rationalize existing ineffective government programs; and how to find better ways to deliver financial services by institutions better-equipped to do the business.

V.2 Migrant Workers and Access to Finance

As mentioned in Chapter II, large numbers of Indonesians work abroad. In 2006, approximately 680,000 Indonesian migrant workers left Indonesia to work overseas, bringing the estimated total to about 4.3 million (World Bank, 2008). There are many issues associated with these migrant workers and this Section looks at two that fit well with the subject of this report. These are: some socio-economic characteristics of these migrant workers, using results of the household survey of Chapter III; and their difficulties in accessing financial services at different stages of their migration.

One striking aspect of this work is the disconnect between existing TKI financial products (e.g., insurance and savings) and the needs as expressed by the migrant workers themselves. In this context, it should be noted that the World Bank conducted a more extensive survey devoted expressly to migrant workers in late 2008. It will expand considerably upon the survey material of Chapter III.

V.2.1 A2F Findings on Indonesian Migrant Workers

This Section expands upon previous work (e.g., World Bank (2008a)), using the survey of Chapter II. This provides information on households that have a migrant worker living abroad, with a sample size of about 10% of total respondents (see the upper left panel in Figure 51). It is not a survey of migrant workers, per se, and for some sub-categories the number of observations is small, which reduces statistical reliability. With these qualifications in mind, the main patterns of these workers are as follows:

Conference Edition

134

Figure 51: Characteristics of Migrant Workers

How Many T imes Did Y ou Work Abroad?(in %)

0.00 20.00 40.00 60.00 80.00 100.00

Malays ia

B runei

S ingapore

Hongkong

Taiwan

S audi Arabia

K uwait

Other

One time Two times Three times More than three times

T otal Res pondentsby Mig rant Worker Abroad

10.1%

89.9%

Migrant Non Migrant

Mig rant Workers by Gender

29.6%

70.4%

Male F emale

Mig rant Workersby L evel of Education & Gender

(in% )

100.0

32.919.0

32.5 35.3

76.0

29.6

67.181.0

67.5 64.7

24.0

70.4

0.00

20.00

40.00

60.00

80.00

100.00

Never go tos chool

Did notcompleteP rimarys chool

P rimaryS chool

S econdaryS chool

S enior HighS chool

Univers ity Total

Male F emale

Conference Edition

135

• About 80% of the (legal) migrant workers are female, and more than 85% of them work in informal sector in relatively unskilled jobs, such as household domestics (e.g., maids and nannies; Figures 51 and 52).

• By education level, just over half (53%) have a primary school education or below, and males dominate the extremes, that is the well and very poorly educated (see the middle panel of Figure 51).

• 45% are repeat migrants, with Kuwait, Saudi Arabia, Hong Kong and Taiwan popular repeat destinations. Singapore is the least popular repeat destination (the lower panel in Figure 51).

Figure 52: Migrant Workers, by Type of Work and Legal Status

(in per cent)

The limited, available data suggest that many Indonesians work abroad illegally, which greatly complicates policy in this area.107 As illegal workers, they simply cross the border on foot or by boat, usually to a neighboring country, such as Malaysia. Results of this survey indicate that 10% are illegal workers, but that looks low based upon other available information.108 Most seem to be

107 Legal migrant workers are defined as those who register as a migrant worker to Ministry of Manpower and Transmigration, and hold a proper migrant workers’ passport and working permit in the destination country. 108 For example, see http://www.reliefweb.int where 600,000 were estimated to be in the state of Sabah alone in 2002. In 2005, the Government of Malaysia estimated that there were more than 1 million illegal migrant workers in the country, mainly from Indonesia and other countries in South and SE Asia (reported on http//burmalibrary.org). Joseph Liow (‘Malaysia’s Illegal Indonesian Migrant Labour Problem: In Search of

63.9

2.7

8.2

11.0

3.9

9.1

30.3

3.6

1.1

21.7

22.3

13.4

0.90.6

0.0 14.0 28.0 42.0 56.0 70.0

Domestic Worker

Industry Worker

F ac tory Worker

P lantation Worker

C onstruc tion Worker

S ervice Worker

Other

L egal Illegal

Conference Edition

136

men in Asia-Pacific destinations, dominantly Malaysia. It appears that they tend to work on construction projects, in plantations and service industries, including as domestic workers (Figure 52).

V.2.2 Migrants & Access to Financial Services

For purposes of this report, issues of migrant workers’ access to financial services are reviewed according to the different stages of the migration process, namely: i) pre-departure (pre-migration); ii) during migration; and iii) post-migration. This approach is useful because migrants’ needs are different at different stages of the process (see Figure 53).

Figure 53: Indonesian Migrant Workers and Access to Finance

Solutions’, on http://www.questia.com) writes that Indonesians into Malaysia are arguably the second largest flow of illegal immigrants in the world (after Mexicans into the United States).

Post-Migration Period

Migration Period

Pre-departure Preparation

Period

Recruited & Registered

Destination Country with Employer

Returning to Indonesia & the village PJTKIs

NEED CREDIT for: Placement Fees, Insurance, Transportation

NEED SAVINGS

NEED SAVINGS NEED INVESTMENT/CREDIT

NEED CHANNEL FOR REMITTANCES NEED SAVINGS for both TKIs overseas and for families in Indonesia

Conference Edition

137

V.2.3 The Pre-Departure Stage

Registration with PJTKI. Legally registered migrant workers are normally recruited either by a PJTKI109 (a licensed Indonesian Overseas Employment Agency) or by agents of PJTKI, usually referred to as ‘sponsors’. PJTKI’s functions are:

• To receive the placement request from overseas clients; • To recruit migrant workers in Indonesia; • To prepare all necessary documentation for migrant workers; and • To provide training, especially for those who plan to work as household domestics.

Depending on the type of job and the timing of the job order from overseas, migrant workers usually stay at PJTKI’s training center (with accommodations for migrant workers) from a few weeks (for repeat migrants) up to a year, before departing for the destination country.

Credit Needs during the Pre-departure Stage. As soon as they decide to work abroad, either formally or informally, most migrant workers face an immediate need for credit. The credit is needed to cover the cost of PJTKIs, agents of PJTKIs and sponsors.

In the case of PJTKIs, there are a series of administration services and training programs from PJTKI. These include: the administrative cost of a passport; government levy and working visa for their destination country; medical examination fees; insurance; transportation; and the fee for PJTKI. The cost varies by the destination country, but generally ranges from US$335 to US$950 for legally registered migrant workers.110

109 Perusahaan Jasa Tenaga Kerja Indondesia, popularly known as “PT” Indonesia (PJTKI), now is Perusahaan Penempatan Tenaga Kerja Indonesia Swasta (PPTKIS). 110 Fees for securing plantation and construction job are between $335 and $560. Clearly, the cost for illegal migrant workers is cheaper than for legals, which is part of the incentive for migrants to choose the illegal route (World Bank, 2008a).

Conference Edition

138

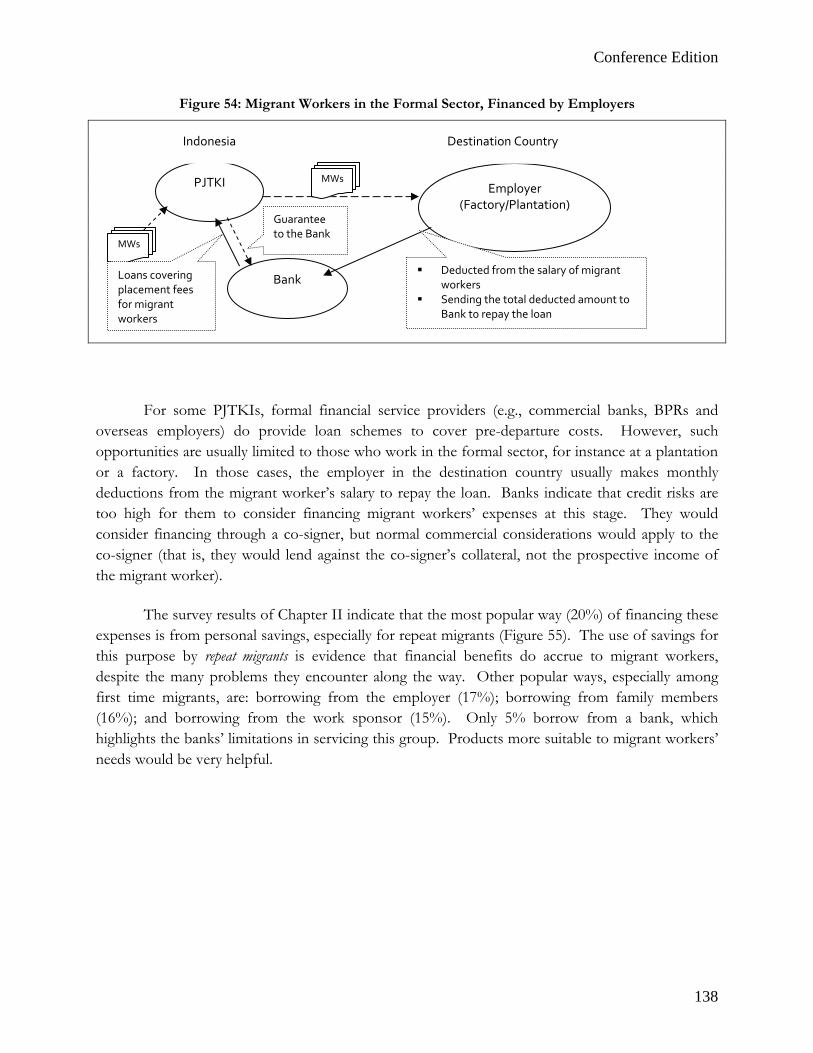

Figure 54: Migrant Workers in the Formal Sector, Financed by Employers

For some PJTKIs, formal financial service providers (e.g., commercial banks, BPRs and overseas employers) do provide loan schemes to cover pre-departure costs. However, such opportunities are usually limited to those who work in the formal sector, for instance at a plantation or a factory. In those cases, the employer in the destination country usually makes monthly deductions from the migrant worker’s salary to repay the loan. Banks indicate that credit risks are too high for them to consider financing migrant workers’ expenses at this stage. They would consider financing through a co-signer, but normal commercial considerations would apply to the co-signer (that is, they would lend against the co-signer’s collateral, not the prospective income of the migrant worker).

The survey results of Chapter II indicate that the most popular way (20%) of financing these expenses is from personal savings, especially for repeat migrants (Figure 55). The use of savings for this purpose by repeat migrants is evidence that financial benefits do accrue to migrant workers, despite the many problems they encounter along the way. Other popular ways, especially among first time migrants, are: borrowing from the employer (17%); borrowing from family members (16%); and borrowing from the work sponsor (15%). Only 5% borrow from a bank, which highlights the banks’ limitations in servicing this group. Products more suitable to migrant workers’ needs would be very helpful.

Employer (Factory/Plantation)

PJTKI

Bank

MWs

Indonesia Destination Country

Deducted from the salary of migrant workers

Sending the total deducted amount to Bank to repay the loan

Guarantee to the Bank

Loans covering placement fees for migrant workers

MWs

Conference Edition

139

Figure 55: How Migrant Workers Finance Pre-departure Expenses

As mentioned, the majority of Indonesian migrant workers are working in the informal sector (such as housemaids, baby-sitters or drivers) and there are very few loan products offered to these migrant workers by formal financial institutions. Despite the good income prospects from working abroad, the migrants are usually forced to obtain credit from informal providers who charge relatively high interest rates. From the banks’ perspective, these potential clients are very risky, because the loan recipient is physically abroad, which risks default without recourse by the lender. Also, the loan amounts are small, probably only Rp3-5 million, so the interest payments may not cover the bank’s administrative costs. This said, a few banks view migrant workers as a potential market and do have a special department to deal with remittances and migrant worker.

To assist with the shortage of credit for migrant workers, government of Indonesia through BP2TKI (The National Commission for Placement and Protection of Indonesian Migrant Workers), has initiated a credit scheme for migrant worker headed for Taiwan, in partnership with banks from Taiwan and Indonesia (Box 19). Interest rates and charges appear to be quite expensive.

0.00 20.00 40.00 60.00 80.00 100.00

S ale of as s ets

Us e of pers onal s aving

Borrowing from other family members

Borrowing from friends

Borrowing from a work s pons or

Borrowing from bank

Borrowing from employer

Other

Don't K now

F irs t Time Repeater

Conference Edition

140

Box 16: Case Study: Migrant Workers Bound for Taiwan

Indonesian migrant workers to Taiwan have access to finance through a mandatory credit scheme. It covers their placement fees, thanks to an initiative of the Indonesian and Taiwanese governments. PJTKI covers the placement fee for migrant workers going to Taiwan up front, in principle allowing Taiwan-bound migrant workers to register with PJTKI without having any initial credit. Prior to departure, migrant workers sign a loan document with one of several banks appointed by BP2TKI. (As of November 2008, these were: Hua Nan Commercial Bank; China Trust Overseas Bank; Sani Bank; First Bank; Bank Mandiri; BPR Tatakarya; and BPR Peranragmada). The loan document and job contract are submitted as supporting documents for visa application to the Taiwanese Embassy prior to their departure. Upon arrival in Taiwan, the migrant worker obtains the requisite local identification, assisted by the agent in Taiwan, who is usually contracted by banks. The migrant worker opens the bank account, with the signed loan agreement and other necessary documents. With proof that migrant workers are physically in Taiwan and have a legal status in Taiwan, the bank releases the loan proceeds to PJTKI, initially covering the cost of migration. Once migrant workers start working, the employer deposit the salary of migrant workers into the bank account, and the bank will deduct the agreed amount every month, usually for one year, to repay the loan.

It would be useful to review this credit scheme more closely, especially the prospects for transferability to other destination countries.

Conference Edition

141

Box 17: Perum Pegadaian (The State-owned Pawnshop) & Access to Credit Perum Pegadaian, the state-owned and only legal pawn shop in Indonesia, has a long history of providing lower income Indonesians with access to credit. It has a substantial presence in the Indonesian microfinance sector with around 900 branches nationwide, serving 16.7 million clients and providing Rp 22.8 trillion in loans in 2007. Migrant workers with certain physical assets are among those who use Pegadaian’s credit services. Once migrant workers are abroad, family members of the migrant workers pay the interest rate on the credit received from Pegadaian until the migrant worker remits earnings. Once family members receive the remittance, Perum Pegadaian is re-paid and the asset is returned. Example: The credit to cover migration costs: Rp 4 million The collateral: Gold jewellery Appraised value of the collateral: Rp 5 million Loan to be provided: 80% of appraisal (the percentage depends on the item): Rp 4 million Administration fee: 1% of Loan: Rp 40,000 (to be paid up-front) Interest Rate: 1.3% per 2 weeks: Rp 52,000 Maturity: 4 months Repayment by the end of 4th months: Rp4million + (Rp 4 million*1.3%*8) = Rp 4,416,000 Perum Pegadaian has recently established a corporate partnership with Western Union to provide money transfer services at their branches. This service started in 60 branches from early 2008. Perum Pegadaian also finances investment activities, such as farming, fisheries, and small scale industries and merchandising. Currently, these account for 25% of their customers. Pegadaian issues bonds which hold a AA+ credit rating by PT Pefindo, indicating a sound financial condition. Pegadaian is a government monopoly and a very profitable business. SourcPerum Pegadaian Annual Report, the Staff Field Interview at Perum Pegadaian Cibadak office, West Java, Indonesia.

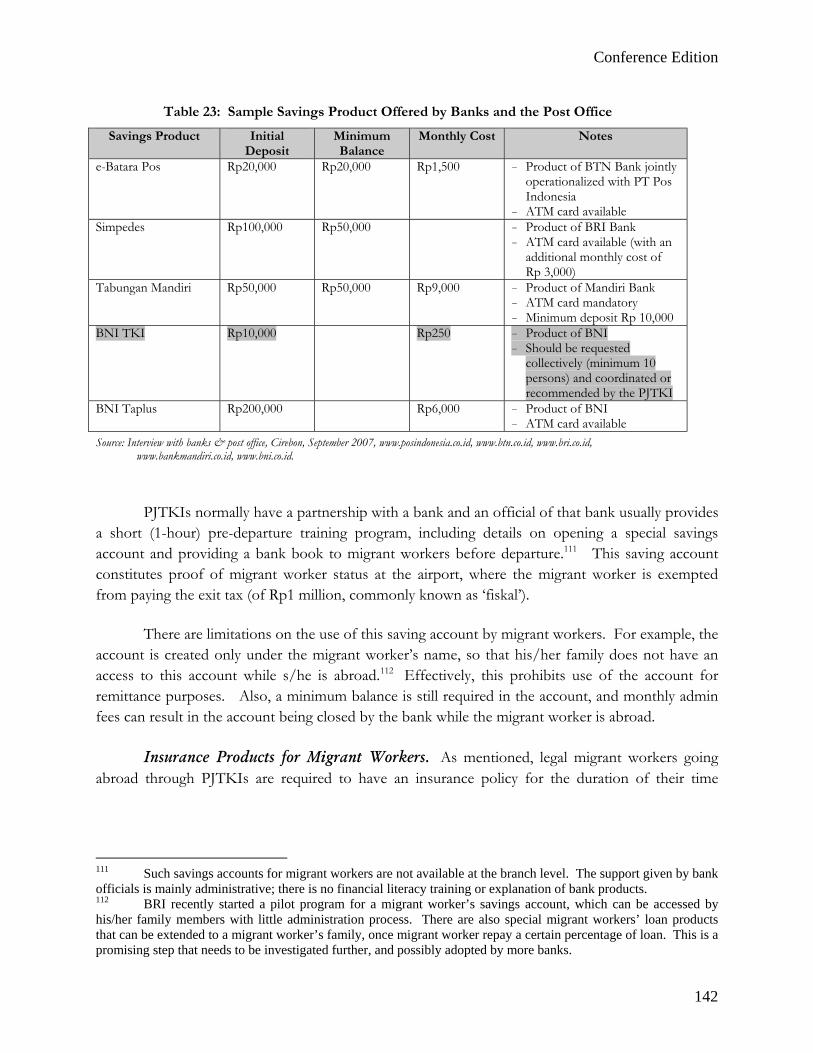

Needs for Saving Products during the Pre-departure Stage. By government regulation, migrant workers are required to open a savings account at a commercial bank and to buy an insurance policy prior to their departure (see the continued discussion of insurance products a few paragraphs below). Some commercial banks, such as Bank Negara Indonesia (BNI), have special saving accounts for migrant workers. These require a very low initial deposit and minimum balance, with low monthly admin fees (Table 24).

Conference Edition

142

Table 23: Sample Savings Product Offered by Banks and the Post Office

Savings Product Initial Deposit

Minimum Balance

Monthly Cost Notes

e-Batara Pos Rp20,000 Rp20,000 Rp1,500 - Product of BTN Bank jointly operationalized with PT Pos Indonesia

- ATM card available Simpedes Rp100,000 Rp50,000 - Product of BRI Bank

- ATM card available (with an additional monthly cost of Rp 3,000)

Tabungan Mandiri Rp50,000 Rp50,000 Rp9,000 - Product of Mandiri Bank- ATM card mandatory - Minimum deposit Rp 10,000

BNI TKI Rp10,000 Rp250 - Product of BNI - Should be requested

collectively (minimum 10 persons) and coordinated or recommended by the PJTKI

BNI Taplus Rp200,000 Rp6,000 - Product of BNI - ATM card available

Source: Interview with banks & post office, Cirebon, September 2007, www.posindonesia.co.id, www.btn.co.id, www.bri.co.id, www.bankmandiri.co.id, www.bni.co.id.

PJTKIs normally have a partnership with a bank and an official of that bank usually provides a short (1-hour) pre-departure training program, including details on opening a special savings account and providing a bank book to migrant workers before departure.111 This saving account constitutes proof of migrant worker status at the airport, where the migrant worker is exempted from paying the exit tax (of Rp1 million, commonly known as ‘fiskal’).

There are limitations on the use of this saving account by migrant workers. For example, the account is created only under the migrant worker’s name, so that his/her family does not have an access to this account while s/he is abroad.112 Effectively, this prohibits use of the account for remittance purposes. Also, a minimum balance is still required in the account, and monthly admin fees can result in the account being closed by the bank while the migrant worker is abroad.

Insurance Products for Migrant Workers. As mentioned, legal migrant workers going abroad through PJTKIs are required to have an insurance policy for the duration of their time

111 Such savings accounts for migrant workers are not available at the branch level. The support given by bank officials is mainly administrative; there is no financial literacy training or explanation of bank products. 112 BRI recently started a pilot program for a migrant worker’s savings account, which can be accessed by his/her family members with little administration process. There are also special migrant workers’ loan products that can be extended to a migrant worker’s family, once migrant worker repay a certain percentage of loan. This is a promising step that needs to be investigated further, and possibly adopted by more banks.

Conference Edition

143

overseas, as well as during the pre- and post-migration periods. As of early 2009, five consortiums of insurance companies provided insurance products to migrant workers.113

By regulation, every departing Indonesian migrant worker must pay Rp400,000 for insurance, which is included in their placement fee.114 However, there are serious issues as to whether these insurance policies provide reasonable service to the migrant worker. For instance, migrant workers are normally unfamiliar with insurance products, and are often unaware of their coverage; they tend to treat these expenses as just an overheard cost of working abroad. Consequently, in case of accident, illness or death during the insurance coverage period, claims are rarely submitted by the migrant worker and his/her family. Even if migrant workers do submit a claim, the process is often too long or too complicated for migrant workers.115 As a result, the claim rate by migrant workers and their families is low, according to discussions with representatives of the insurance consortium.

V.2.4 Financial Service Needs During Migration

The typical duration of migration for Indonesian migrants is two years. However, if both the employer and the migrant worker agree, there is the possibility of extending the contract for another one or two years. During the migration period, the workers often send some of their earnings back to their family in Indonesia, probably having saved up for 2-3 months or more (Box 21).

113 The biggest is Consortium Jasindo with 7 member of insurance companies lead by the Asuransi Jasindo. Another is the Konsorsium Asurasi TKI “Mitra Dhana Atmharakhsa”, currently a consortium of six insurance companies (PT. Asuransi Ramayana Tbk., Jasa Tania, General Insurance, BNI life, PT Asuransi Asoka Mas, PT. Fadent Mahkota Sahid General Insurance and Megalife Asuransi Jiwa). It has 19 offices throughout Indonesia and 6 international offices, in Kuwait, Bahrain, Malaysia, Singapore, Hong Kong and Taiwan. 114 This covers a total of 30 months of insurance, including the pre-departure, placement and post-placement stages. In the pre-departure stage, the insurance program covers death due to accidents or illness during training period; permanent partial disability; and medical treatment due to illness or accident. In the placement stage, insurance will cover accidents during and outside working hours; medical treatment expenses; death due to accident or illness (including expenses for burial and corpse repatriation); unpaid wages; and premature contract termination by the employer. During the post-placement stage, the insurance covers death due to accident or illness; permanent partial and total disabilities; and medical expenses due to accident. (Manpower and Transmigration Ministerial Decree no 157/MEN/2003, dated 9 June 2003). 115 There are instances where the PJTKI assists the migrant workers with the claim, but this is rare because the PJTKI’s responsibilities end when the migrant worker departs Indonesia for the destination country.

Conference Edition

144

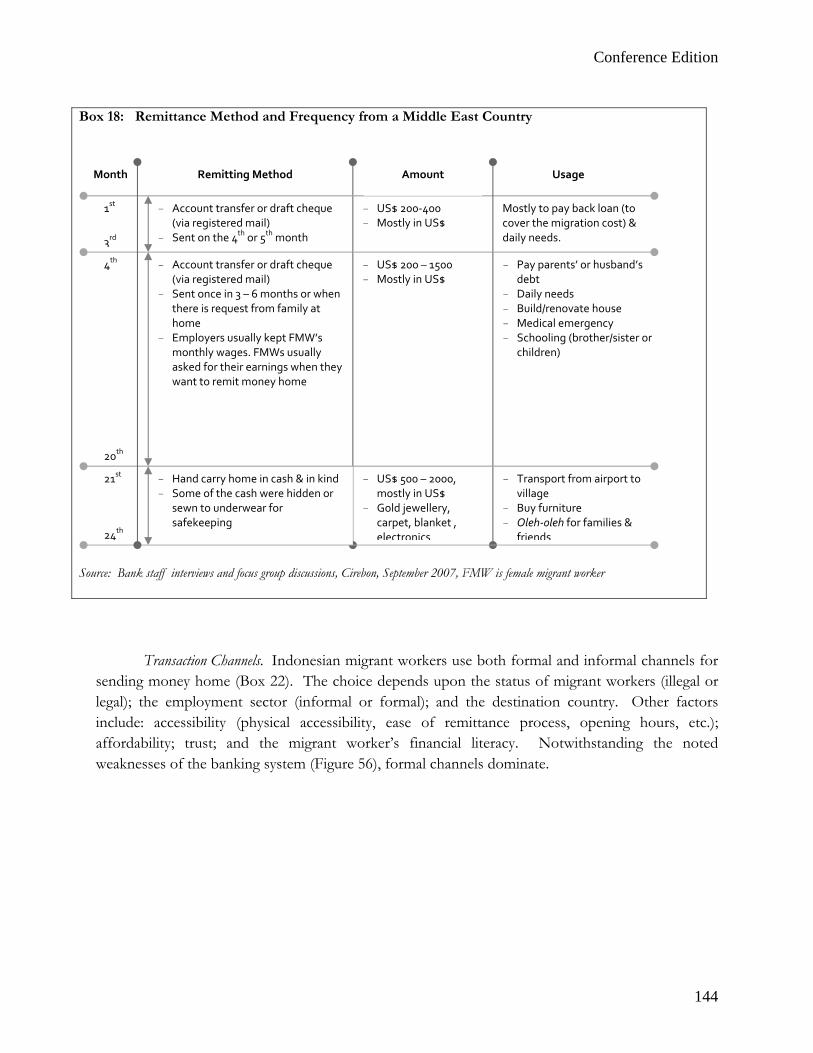

Transaction Channels. Indonesian migrant workers use both formal and informal channels for sending money home (Box 22). The choice depends upon the status of migrant workers (illegal or legal); the employment sector (informal or formal); and the destination country. Other factors include: accessibility (physical accessibility, ease of remittance process, opening hours, etc.); affordability; trust; and the migrant worker’s financial literacy. Notwithstanding the noted weaknesses of the banking system (Figure 56), formal channels dominate.

Box 18: Remittance Method and Frequency from a Middle East Country

Source: Bank staff interviews and focus group discussions, Cirebon, September 2007, FMW is female migrant worker

- US$ 500 – 2000, mostly in US$

- Gold jewellery, carpet, blanket , electronics

- US$ 200‐400 - Mostly in US$

- US$ 200 – 1500 - Mostly in US$

- Account transfer or draft cheque (via registered mail)

- Sent once in 3 – 6 months or when there is request from family at home

- Employers usually kept FMW’s monthly wages. FMWs usually asked for their earnings when they want to remit money home

Remitting Method

- Account transfer or draft cheque (via registered mail)

- Sent on the 4th or 5th month

- Transport from airport to village

- Buy furniture - Oleh‐oleh for families &

friends

Mostly to pay back loan (to cover the migration cost) & daily needs.

- Pay parents’ or husband’s debt

- Daily needs - Build/renovate house - Medical emergency - Schooling (brother/sister or

children)

24th

21st

20th

4th

3rd

1st

- Hand carry home in cash & in kind - Some of the cash were hidden or

sewn to underwear for safekeeping

Usage Month Amount

Conference Edition

145

Box 19 : The Methods of Remittance: Formal vs. Informal

With regard to gender issues in this area, female migrant workers in the Middle-East rarely remit money to Indonesia for social/cultural reasons. In that region, females are not allowed to go on the street unaccompanied by a male, and language is often a problem. As a result, they rely heavily on their employers to remit their salary to Indonesia.

Formal Remittances. The great majority of formal remittance inflows are through banks, with non-bank financial institutions accounting for the remainder (Figure 56). The overseas transaction does not require the sender to hold a bank account in the destination countries; the sender simply requests the transaction with the submission of certain documents, such as an ID card, to comply with Anti-Money Laundering regulations. The cost per transaction varies by institutions, by the amount remitted and the destination country (see Table 25). Further investigation into comparative costs by country would be very useful information, especially if the information could be made available to workers before going abroad.

Further issues related to formal remittances and mobile banking are discussed in Chapter V-3.

Formal Channel

Informal Channel

• Bank • Nonbank Financial Institutions

- Western Union - Money Gram - Licensed Foreign Exchange Shop. - Licensed Money Exchange Dealers

• Friends / neighbors / family members • Informal money exchange / foreign

exchange dealers

The methods of Rem

ittance (O

verseas money transfer)

Conference Edition

146

Table 24: Indicative Cost of Remitting Money from a Middle-East Country

Sending Method

Cost Borne by Duration Notes

Remitter Recipient Hand Carry None None 1-2 days - In the form of cash, gold, goods

- Policy on maximum amount of currencies leaving a destination country applies

Draft Cheque 20 Riyal 6 Riyal for mail

- Revenue stamp - ID photocopy - Indicative ‘gratitude

tip’ for post office

2-4 weeks - Cheque is sent via registered mail - Need valid ID to cash out - Post office called or sms migrant

family for incoming registered mail Account Transfer

25 Riyal None 2-3 days Need bank account & valid ID

Western Union

Rp 100 000 to transfer home Rp 1 million

- Formally none - Indicative ‘gratitude

tip’ for post office

1 hour - Need valid ID & PIN code - Can be cashed out in any WU outlet

(banks, post offices) - For post offices that are not yet

online, PIN code confirmation is done through phone calls with the Cirebon City Central Post Office

Source: Interviews and focus group discussions, Cirebon, September 2007

Figure 56: Method of Receiving Remittances, by Host Country

(in percent)

3.4

9.8

10.8

7.7 13.6

9.8

87.0

77.0

95.9

72.3

84.8

61.6

74.6

78.2

2.51

8.1

8.1

25.2

14.9

4.1

8.9

15.2

7.1

1.2

1.9

2.7

5.8

1.7

3.8

2.1

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0 90.0 100.0

Malaysia

Brune i

S ingapore

Hongkong

Ta iwan

S audi Arabia

Kuwa it

Other

Through a Pos t Offic e Bank c hec k s ent via a Wes tern unionBank wire trans fer Informal money travel Through relatives /friendCarries own money on Other

Conference Edition

147

Informal Remittances. The use of informal channels for overseas transactions is common for Indonesian migrant workers in Malaysia, where they are often illegal. The informal channels include hand delivery, informal agents, informal money changers and shops. The process tends to be simpler and quicker although the financial costs are usually higher. Illegal migrant workers are likely to use such informal channels due to the lack of proper ID, which is required by the formal channel.

There are also risks in using the informal channel. For example, migrant workers returning to Indonesia may carry money (or gold or jewellery) on behalf of others from the destination country. Before the couriers return home, they may be robbed; they may be charged higher fees for transportation; or they may be the target for corrupt immigration officials who know that returning migrant workers usually carry the cash on their person. Informal money changers and agents may also charge higher commissions of the recipient and the family of migrant workers.

Box 20: Voices of Hard Experience “I worked in a kedai minum in Kuching. I lived in a 3 X 4 m room that I rented for 150 Ringgit a month. I kept all my valuables and money in my room. It is safe, but I was once robbed by my own friend. I lost 2000 Ringgit (Rp 5,667,020),a necklace and a ring. I keep some of my money with my tauke now. I must be careful not to keep too much money there. When it amounted to 400 Ringgit, I have to cash it out because if he holds too much of my money, it would be more difficult for me to cash it out. He would say that he doesn’t have enough cash to give me my money.”

Rosalia, Sahan Village

“I worked in a kedai minum in Kuching. I send money home through a friend or by going home. I frequently go home. I always exchange my Ringgit at Ahie’s store. When sending money through a friend, I usually send around 100 Ringgit (Rp 283,350). Sometimes I send Rp by exchanging my Ringgit in Kuching. The two rates are very similar. We could also exchange our Ringgit in shops at the border.”

Dedek, Sahan Village

“I used to work in a kedai kopi in Kuching. I was paid monthly in cash. I always keep my own money; I never opened an account in Malaysia. I married a Malaysian in 2007 and now live in Malaysia. I send 200 – 300 Ringgit monthly to my parents through friends. Sometimes I asked my brother to go to the border in Sirikin. I will meet him there and hand over the money. It doesn’t cost us a thing.”

Mega, Sahan Village

“I worked in a plywood factory in Miri. I just completed my contract and will shortly go back to Malaysia to work again.What concerns me is what’s happening on the border: people are being cheated by the preman who forces returning TKI to exchange their Ringgit. They ran away before giving you the full amount Rp that was promised based on an exchange rate that you both agreed on. And this only happens on the Indonesian side of the border. The Malaysian side of the border is OK.”

Tadi, Sei Pangkalan I Village The World Bank staff interviews in Kalimantan, December 2007.

Conference Edition

148

In December 2006, Bank Indonesia issued a regulation that allows informal transfers by remittance agents. The regulation aims to prevent money laundering by allowing a gradual transition from registration to licensing of these agents. According to the regulation, existing agents are required to register by the end of 2008, and new agents will need to apply for a license from the beginning of 2009. Agents who are registered and/or licensed are obliged to record money transfer transaction, submit periodical and incidental reports to Bank Indonesia and to report any suspicious transactions to Bank Indonesia (World Bank, 2008b).

Saving During Migration. Migrant workers working in the formal sector are likely to have a bank account in the destination country, because their employer may transfer their salary to the bank account instead of paying the salary in cash. These migrant workers accumulate their savings in the bank account until the amount is large enough to send back to Indonesia. In the case of migrant workers in the informal sector (e.g., a housemaid or babysitter), the employer may keep the earnings on behalf of the migrant workers until they are ready to send their earnings home. Or the migrant workers simply keep their money themselves, for instance hiding it in their room. Typically, the migrant worker has limited free time; hours of banks’ operations may be a problem; and they are usually unfamiliar with the process of opening a bank account in the destination country. Consequently, migrant workers usually do not open a bank account unless their employer does it for them, and transfers their salary to the account.

V.2.5 The Post-Migration Period

Based on the evidence of this study, remittances are generally not used for investment, with the notable exception of building or renovating a house. Rather they go towards meeting the daily needs of family life in the village, re-paying loans, school and medical expenses and so forth. After returning home, many migrant workers find that their remitted earnings have been fully used up. Repeat migrant workers are likely to accumulate some assets (such as some savings or a better home) but there is limited evidence that their post-migration livelihood has improved much on a self-sustaining basis. Indeed, less than half (41%) of respondents reported that they had saved money from abroad.

In part, this reflects the dire on-going needs at home as well as the capacity of dependent family members to consume transfers from abroad, virtually as fast as the migrant worker can remit them. But it is also due to a lack of financial planning and financial management. As mentioned, the great majority of Indonesian migrant workers are from poor rural areas, with a lower education background. These migrant workers and their families tend to have little knowledge of financial services and products. This problem of low financial literacy is one of key constraints recognized by the Indonesian Government to improve migrant workers’ livelihood. Still, there are very few financial literacy education programs for migrant workers. Such information as migrant workers

Conference Edition

149

obtain comes from their own experience, friends, family members, the employer, neighbors or other migrant workers in the same destination country. Rarely does it arise from any form of proper, formal training, which would assist with making the best choices among the available financial services and products. Uninformed decisions early in the process often appear to trap the migrant into unfavorable loan arrangements, spending the bulk of their earnings to repay loans, rather than spending to improve their livelihood.

V.3 Mobile Banking

V.3.1 The International Context

Branchless banking, 116 whether it is mobile banking 117 or card-based transactions, 118 has considerable potential to provide access to financial services to the ‘unbanked’. For purposes of this study, mobile phone technology is particularly interesting because it provides a method for the unbanked to access financial services easily, conveniently and securely through a popular, existing delivery channel. Customers no longer have to travel a distance or wait for a long time to conduct a financial transaction; they can do it with their mobile phone, perhaps followed by a visit a nearby cash-in and cash-out agent.

There are two basic models of branchless banking, bank-based and non-bank based; both deliver financial services outside traditional bank branches. In the bank-based model, every customer has a direct contractual relationship with a prudentially licensed and supervised financial institution. In the non-bank based model, the customer buys an electronic store of value, the current value of which is tracked on the server of a non-bank, such a mobile phone operator or telecommunications company. If the system is mobile-phone based, customers only need to visit a retail agent to top-up the stored value or to convert the stored value back into cash (i.e., ‘cash-out’). These stored value instruments are referred to as e-money; effectively, they substitute for cash.

Recent years have seen a boom in mobile banking operations in some developing countries. In Kenya (a country of roughly 39 million people, where fewer than 4 million have bank accounts), the M-PESA mobile wallet service offered by Safaricom attracted 1 million registered users in 10 months.119 In the Philippines, the country’s two mobile network operators offer the functional

116 The term ‘branchless banking’ refers to financial transactions conducted by means other than formal bank branches or their field offices. For example, the transaction may be done through post offices or common retail outlets, like grocery stores or gas stations. 117 There is some disagreement over the term ‘mobile banking’. Some experts define mobile banking as any financial transactions conducted with the use of mobile phones, regardless of who provides the services. Others argue that banks must provide the underlying service; they believe that, if telecommunication companies provide the service, it should be called an ‘m-payment’ or something similar. 118 Card-based transactions include debit card or prepaid card transactions using a device that can transmit data over a network such as electronic data capturer (EDC) or by using a mobile phone. 119 See http://www.safaricom.co.ke/index.php?id=745.

Conference Edition

150

equivalent of small-scale transaction banking to an estimated 5.5 million customers.120 For the unbanked poor in countries like these, conducting transactions using a mobile phone is far cheaper than going to a bank branch, in terms of both time and out-of-pocket expenses.

These Kenyan and Filipino examples illustrate telco-led mobile banking operations that specifically target the unbanked; they are known as “transformational mobile banking”. Variations on this model include a joint venture between a telco and a bank, or a technology company with a bank, such as WIZZIT in South Africa (Box 24).

Box 21: Promising Technologial Advances – South Africa’s WIZZIT

There are good economic reasons to believe that the formal banking sector will extend its services to remote regions, if their cost of providing those servicing is sufficiently low. One promising technological advance in this regard is cell phone banking, introduced into South Africa under the branding of ‘WIZZIT’. The service is premised on the simple observation that even the poor in remote regions of the country have access to a cell phone these days. (As indicated in Chapter III, almost 95% of Indonesian households have a cellphone.) In South Africa, branchless banking through retail agents is permitted only for licensed financial institutions. (Non-banks are prohibited from accepting public deposits.) Consequently, mobile operators interested in branchless banking have created joint ventures with licensed banks to offer cell phone-based banking. WIZZIT, a third party technology company, became a division of the South African Bank of Athens in order to be able to offer cell phone- and card-based bank accounts for the unbanked. WIZZIT’s resulting product is a cellphone-based banking facility whose immediate target market is the estimated 16 million unbanked or underbanked South Africans (about 60 percent of the country's population). The initiative was conceived in early 2002 and commercially launched in March 2005. Once successful, the company plans to expand into the rest of Africa, and the company reports enquiries from Latin America and Asia. Because it is bank-based, WIZZIT can provide a wide range of regular bank services (e.g., deposit, withdrawal, payment and airtime reload services) through a mobile phone interface, ATMs, bank branches and post offices.

WIZZIT is compatible with early generation cell phones (which are popular in low-income communities), and it uses pay-as-you-go cellphones. In addition, WIZZIT account holders are issued debit cards that can be used at any ATM or in the formal retail sector. WIZZIT charges per-transaction fees that range from 99c (US$0.15) to R4.99 (US$0.78); it does not charge a monthly fee; there are no transaction limitations; and it does not require a minimum balance. WIZZIT employs over 800 "Wizz Kids" - typically unemployed university graduates from low-income communities to promote the product and help unbanked customers open accounts.

Sources: The World Resources Institute, http://www.nextbillion.net/archive/activitycapsule/wizzit and http://www.wizzit.co.za/

120 See Lyman, Porteous and Pickens (2008).

Conference Edition

151

Box 22: International Experience in Reducing the Cost of Mobile Banking In developed countries, commercial banks use ‘direct banking’ technology (e.g. ATMs and InterNet banking) to process transactions at 20% of the cost of a traditional bank teller. In other countries like Brazil, the Philippines and Kenya, banks are experimenting very successfully with technology to reduce transaction costs further. In Brazil, banks use point-of-sale (POS) terminals to deliver financial services in nearly every province at 0.5% of the cost of a bank branch. POS terminals are electronic devices connected to a telephone or other telecommunications network and placed at retail outlets for payments and disbursements. The device may read debit or credit cards or barcodes, or the device itself may be a mobile phone that can accept information transmitted by another mobile phone through short messaging service (SMS) or another protocol. Will POS staff of a retail outlet, or a postal clerk, build sufficient trust with a client on behalf of the bank to sell a wide range of banking services to customers? Recent information from Brazil suggests that this may be difficult. Thirty percent of the accounts opened at banking correspondents of Banco Popular do Brasil (a division of Banco do Brasil) never become active. After opening for business in June 2004 and attracting 1.05 million customers within six months, the division now maintains about 771,000 active accounts and is closing unprofitable banking correspondents. In the Philippines, a ‘G-Cash’ product is proving popular. It links the user’s cell phone to a cash account. The customer can deposit or withdraw cash from this wallet as needed, and credit can be transferred between mobile users. Registration and transactions (including inward remittances from Filipinos working overseas) are done by SMS; initially cash is deposited at a designated location and withdrawals require an acceptable ID. The cost per transaction is the standard SMS fee of about US¢2. However, cash deposits are a bit more expensive; the fee is 1% of the transaction value with a minimum of US¢19. It is too early to know whether the use of technology channels will be profitable enough to encourage banks to target low-income customers. No thorough profitability analysis of replacing bank branches with mobile phones or POS devices at retail outlets is available. Although using POS systems to move transactions outside the branch environment for existing customers reduces costs, this approach may take some tome before it helps banks acquire customers who live far from bank branches. Also, regulatory issues must be addressed (see Box 27) Ultimately, transaction costs still need to come down significantly for lower income groups to manage their own daily financial lives. To this end, current thinking is that the system should work for transactions of as little as $2—the daily income for many of the world’s truly poor—on agent commissions of not more than 2 percent. That means that customers’ transaction fees should be in the range of US¢2–4 (1–2 percent on a $2 transaction). Only then will the size of electronic transactions parallel the daily cash flow of the poor. In the specific case of Indonesia, costs look like they could be a small multiple of this amount, considering Indonesia’s level of per capita income, say very roughly US¢5-10 per transaction. Sources: “Using Technology to Build Inclusive Financial Systems”, CGAP Focus Note #32, January 2006; “Realizing the Potential of Branchless Banking: Challenges Ahead”, CGAP Focus Note #50, October 2008; and World Bank ‘Report on Access to Finance in Pakistan” (draft).

Transformational branchless banking—which is mostly operated by telcos with a limited banking license—usually offer only limited financial services, such as cash-in and cash-out, payment and person-to-person fund transfers. They cannot offer savings. Some countries have gone further, only allowing telco-led branchless banking to offer a cash-in payment, which limits the growth of

Conference Edition

152

branchless banking. Nonetheless, this is sufficient for many unbanked customers, because branchless banking is used mainly for payments, not for savings or credit, according to a CGAP report referenced above. For instance, in Brazil almost 78 percent of the 1.53 billion transactions conducted at more than 95,000 retail agents/merchants are for bill payments and for the payment of government benefits to individuals. Similarly, and even though WIZZIT offers a broader range of services, most of its customers use the service to buy airtime twice as often as they withdrew funds from a branch or ATM, and five times as often as they conduct money transfers.

With the number of people connected to mobile networks greatly exceeding the number of people with bank accounts, there is large potential for branchless banking, especially mobile banking, to reach unbanked customers. The main questions are: will the cost/unit of this service be reduced low enough to attract the unbanked poor (see Box 25)? And will the unbanked poor actually use these services once they are readily available on a cost-effective basis? Public education (by industry players) and transfer of knowledge (by early adopters of branchless banking) have a significant role to play in this regard.

V.3.2 The State of Mobile Banking in Indonesia

Indonesia is moving ahead quickly with mobile banking services (see Box 26). For instance, Bank Indonesia is relatively advanced in its thinking about e-money, and Indonesia is among the few countries with regulations allowing non-banks to issue e-money. As this report was being drafted, BI had just amended its current regulations, and the main issues are discussed in Box 26.

As of end-2007, twenty-three banks offered different kinds of mobile banking services to their customers.121 On the telco side, two mobile operators have been licensed by Bank Indonesia to allow them to operate mobile payment services to their customers, albeit with some limitations.

Mobile phone penetration is quite high in Indonesia, at 37 percent compared to 8.4 percent of fixed-line teledensity.122 Twelve mobile network operators are now competing for market share in Indonesia, with the big three (Telkomsel, Indosat and Excelcom) accounting for about 85% of the market with a total of 75 million customers at end-2007.

121 Information gathered in www.informasi-media.blogspot.com. 122 Paul Budde Communication. 2008. “Indonesia – Key Statistics, Telecommunications Market and Regulatory Overview.”

Conference Edition

153

Box 23: Mobile Banking Product Development in Indonesia

Among the commercial banks in Indonesia , Bank BCA and Bank Mandiri are the two biggest mobile banking operators (in term of number of users, number of transactions and volume of transactions). In reaching out to the unbanked, Bank Permata is probably the most innovative. Its customers can send money to an unbanked person with a mobile phone and that person can retrieve cash from a number of Bank Permata ATMs by pushing a button and keying-in a few data received via mobile phone. BCA has also launched Flazz, a prepaid electronic wallet targeted at young customers to offer an easy and convenient way to conduct transactions. Using radio frequency identification (RFID) technology and taking advantage of its vast ATM network, Flazz users only need to tap the card into an electronic reader (without PIN numbers, as would do done with a debit card). Flazz carries a limit of Rp1 million, or US$100, the same as other prepaid limit set by Bank Indonesia. Flazz can be reloaded in BCA branches or from any ATM. Telkomsel, the largest cellular operator in Indonesia, launched its mobile payment services in late 2007 called T-cash. Telkomsel customers can register to be a T-Cash user over the network or by coming into one of Telkomsel’s many centers or retail agents. The maximum wallet size is US$100, which looks small for purchasing and fund transfer. T-cash can only be used to cash in or convert cash to electronic money and to make payments or purchasing. Cashing out and person-to-person fund transfers are not allowed. Telkomsel signed up Fuji Image Plaza (a chain of photo processing kiosks) to be their first retail cash-in and retail agents. Subsequently, Telkomsel has been working with Indomaret, a chain of hundreds of mini markets, as retail agents. One year after its introduction, T-cash has approximately 80,000 users with some 500 retail agents. However, compared to the number of Telkomsel’s subscribers (55 million at end-2007), the number of T-cash adopters is quite small. Reasons include: a low limit of wallet size; restrictions on m-payment activities; and slow roll-out of retail agents that can handle cash-in and purchasing.

Indosat, the second biggest cellular provider in the country, also received a license to operate m-payments, but has yet to find a good strategy to reach potential customers. They only recently launched their m-payment service (called Dompetku, or My Wallet), and progress looks slow.

Bank Indonesia regulates all banking-related activity including mobile banking, whether it is banking- or telco-led, and banks have greater flexibility in offering services because they carry a full banking license. Under Bank Indonesia regulations,123 commercial banks in Indonesia can offer almost as many services over the internet and mobile banking platforms as they would over the bank branches, except opening a bank account.

123 Bank Indonesia Regulation (PBI) No. 9/15/2007 emphasized the importance of risk management in the use of ICT by commercial banks. This regulation governs, among others, the use of ATM, phone banking, electronic fund transfer, internet banking and mobile phone banking.

Conference Edition

154

Box 24: Weaknesses in the Regulatory Environment for Branchless Banking in Indonesia Despite Bank Indonesia’s relatively advanced thinking about e-money (described in the main text), there are few examples to date of the successful provision of financial services to low-income Indonesians through branchless banking. Some reasons are related to existing regulations, as summarized below. Policy recommendations are provided in Chapter VI. First, until very recently the regulatory regime limited the use of e-money to making retail payments. This happened because BI’s regulations treated e-money the same as prepaid card payment instrument, like credit, debit and ATM cards. BI changed its regulations in April 2009 (BI Regulation 11/12/2009), and the result appears to be a considerable improvement. However, the regulations do not secure the preferential claim of agents and customers over issuer creditors (for instance, in the case of bankruptcy of the e-money issuer). Also, non-banks are allowed to issue e-money, but the use is restricted to retail purchases. Second, any non-bank e-money provider that wants to extend its services to person-to-person (P2P) transfers (domestically or internationally) needs a remittance license from BI, and eligibility requirements are very tight. (For example, potential providers may need to change their articles of association, which may be difficult.) Effectively, the eligibility requirements are restricting new entry. Third, neither banks nor non-banks are currently allowed to use agents to provide financial services, like cash-out transactions. A network of agents is vital to operate on a sufficiently large scale to make a low-value transactions business commercially viable. Fourth, current Know Your Customer (KYC) regulations require banks that provide electronic banking services to meet the prospective customer, at least when the account is opened. This poses a barrier because sign-up of new customers can only be done in bank branch offices (or mobile branch offices). Effectively, banks cannot out-source their KYC procedures, which precludes customer acquisition beyond the reach of bank branches. Likewise, mobile banking cannot leverage off agents’ networks (or telecos) to sign up unbanked customers who are unable or unwilling to visit a traditional bank branch.

Source: ‘Diagnostic Report on the Legal and Regulatory Environment for Branchless Banking in Indonesia”, June 2009, by CGAP in cooperation with IFC and GTZ.

Looking at both the bank-led and telco-led model under current regulations, bank-led mobile banking looks more likely to provide a wide range of services to unbanked users. Nonetheless, most banks seem unable to extend these services beyond their existing customer base, partly because of regulatory issues (see Box 27). One of the solutions may lie in the Sharia banking system (see Box 6); important innovations are taking place in this segment and--because it’s Sharia-based-- some previously unbanked segments are being attracted by the service.

V.3.3 Mobile Banking to Improve Access to Financial Services

By contrast, the Telco-led model offers greater potential for reaching the unbanked poor in rural areas because of existing wide mobile network coverage. But the services don’t meet the needs of the poor, specifically no cash-out; no person-to-person fund transfer capabilities; and small wallet size.

Conference Edition

155

With Indonesia’s wide geographical spread, the main issue is how to reach the unbanked poor in remote, rural areas by cost-efficient means. Because of its reach, mobile banking offers much more promise than either internet banking or the costly brick and mortar of building additional branches. Telkomsel (which has applied to be a remittance agent) claims that its network has covered almost all districts (kacamatans) in Indonesia. The other players are currently expanding their networks rapidly, including by sharing base transceivers in the rural areas. These developments look likely to further reduce service providers’ costs significantly, especially for smaller players that want to focus their reach into rural areas.

On the side of customers, the price of handsets has dropped in recent years, making mobile phones more affordable for many low income people. These days, many operators even offer a bundling program, whereby the customer gets a low cost handset if s/he buys Rp300 thousand (US$30) worth of airtime.

These factors, of course, have to be supported by the regulatory environment (see Box 27) and by the services on offer, especially their convenience in conducting mobile banking transactions. Most people want the ability to cash-in and cash-out; send money to their families; make balance inquiries; reload airtime; and purchase goods. Considering the popularity of short messaging services (SMS), if banks or telcos were to offer mobile banking services using SMS as the transactions mechanism, there could be a huge take up, including from the unbanked poor segment of the market. Further work is needed to better access the prospects, including for helpful interventions of one form or another.

Remittances Using Mobile Banking. In some countries, person-to-person fund transfers are allowed under current regulations. For example, in the Philippines, remittances are one of the driving forces behind the success of mobile banking. Filipino migrant workers in Singapore, Hong Kong and the Middle East send millions of US dollars back home every month.

The same situation could unfold in Indonesia, if the regulatory framework permits. Currently, Telco-led mobile banking players are not allowed to conduct person-to-person fund transfer; only bank-account-to-bank-account transfers are permitted. Maxis, a cellular operator in Malaysia is able to provide remittance services to Indonesian migrant workers in Malaysia and Singapore. Indonesian migrant workers in the two countries can use Maxis services by sending money to their relatives providing their relatives have bank account in one of 5 banks that cooperate with Maxis in Indonesia.

At drafting of this report, two operators in Indonesia were working on a pilot with an Indonesia banks to allow Indonesian migrant workers in Malaysia and Hong Kong to remit money using Indonesian mobile operators. Beyond that, the mobile operators would need to build a chain of cash-out agents to allow for easy and convenient cash withdrawal. Under current circumstances, it looks quite difficult for small shops to apply to become remittance agents. To accelerate the

Conference Edition

156

process, there may be a role for a pilot program of some type, possibly in the form of a public-private partnership.

V.4 Policy Issues

MSMEs and Access to Finance. Unlike other parts of this report, the MSME issues of access to financial services are virtually one-dimensional, that is, they are almost exclusively credit-related. On the basis of available evidence, these problems of MSMEs get more difficult as the scale of the enterprise declines, with problems of access mainly arising at the micro level. At the micro-enterprise level, there are many problems, only one of which concerns their access to finance. Resolution of access-to-finance issues would certainly help micro-enterprises, but other, more basic problems need to be addressed, too, like manpower constraints.