Chapter Twelve Foreign Currency Risk Management

29

177 177 Chapter Twelve Foreign Currency Risk Management Foreign currency risk is caused by the change in the spot rate that can cause a gain or a loss. There are THREE types of risk: ! Translation ! Economic ! Transaction 1. Translation Exposure 1.1 Risk caused by change in the value of a Forex asset or liability over the long term. Class Illustration – Translation Risk Botham Co Botham Co has a US subsidiary worth $10m. Extract from the SOFP 20X1 at $1.50 £6.67m 20X2 at $1.75 £5.71m Loss to equity (£0.96m) The recognised way to hedge this risk is to MATCH the FX asset with an equivalent liability.

Transcript of Chapter Twelve Foreign Currency Risk Management

177

177

Chapter Twelve

Foreign Currency Risk Management Foreign currency risk is caused by the change in the spot rate that can cause a gain or a loss. There are THREE types of risk:

! Translation ! Economic ! Transaction

1. Translation Exposure 1.1 Risk caused by change in the value of a Forex asset or liability

over the long term. Class Illustration – Translation Risk

Botham Co

Botham Co has a US subsidiary worth $10m. Extract from the SOFP

20X1 at $1.50 £6.67m

20X2 at $1.75 £5.71m

Loss to equity (£0.96m)

The recognised way to hedge this risk is to MATCH the FX asset with an equivalent liability.

178

178

Funded by a $10m loan.

20X1 at $1.50 £6.67m

20X2 at $1.75 £5.71m

Gain to equity £0.96m

1.2 This not a cash risk, only due to financial reporting regulations. 2 Economic Exposure 2.1 When a company has operations based in foreign countries, the returns earned by that entity would be subject to the variations in economic factors of the relevant country. For example, the foreign cash flows converted back into the home currency may fall due to changes in the exchange rate. 2.2 The recommended method of hedging is to have many operations based all over the world – GLOBAL DIVERSIFICATION. This is because when one economy is performing badly, another is moving in the polar opposite direction. 3 Transaction Exposure 3.1 This is the main concern. When an entity has to make a FX payment or is due to receive a FX receipt at a point in the future this will be converted at the spot rate prevailing on that date. The future spot rate is highly unlikely to be the same as the one today – TRANSCTION RISK. 3.2 There are many ways to hedge this risk and these will be considered below.

179

179

4 Exchange Rates 4.1 Rates will be presented as:

(Bid) (Offer) $1.5000 - $1.5555 / £

£0.6429 - £0.6667 / $ (Bid) (Offer) 4.2 Choosing the correct rate is CRITICAL. Here is a quick way:

! If the SPOT Rates are FX/Home Currency

! We are RECEIVING FX then

! Use the right hand rate

5 Hedging Transaction Risk – “Simple Hedges” 5.1 Invoice /transact only in the home currency

! All transactions in home currency

! Transfer risk to the other party

! Monopoly power-over our customers or suppliers 5.2 Foreign currency bank accounts

! Held in the main currencies ($, Euro)

! Pool all transactions in same FX

Reciprocal and cross over!!!!!

180

180

5.3 Leading and Lagging This a method used by many IMPORTERS who are due to make a FX payment in the near future. They can either pay now or in the near future (LEADING). Alternatively, they can delay the payment (LAGGING) as the exchange rate is predicted to lead to a lower payment value. This can be described as hedging with an element of risk as the future spot rate has to be predicted. However, the risk is no too great due to the short time period involved and the currencies used been widely traded. 5.4 Netting “Basic” is to match all FX transactions that occur on the same day and in the same currency. For example

Today 30 Sep

€200K = Expected Receipt (€ 120K)=Expected Payment €80K)

181

181

6 Hedging Transaction Risk – Main Hedging Methods 6.1 Multigroup Netting This is used when a large group is can remove the transaction risk by have its entire group FX transactions converted into just one currency. Apart from reducing or removing the FX risk, there will be a reduction in transaction costs.

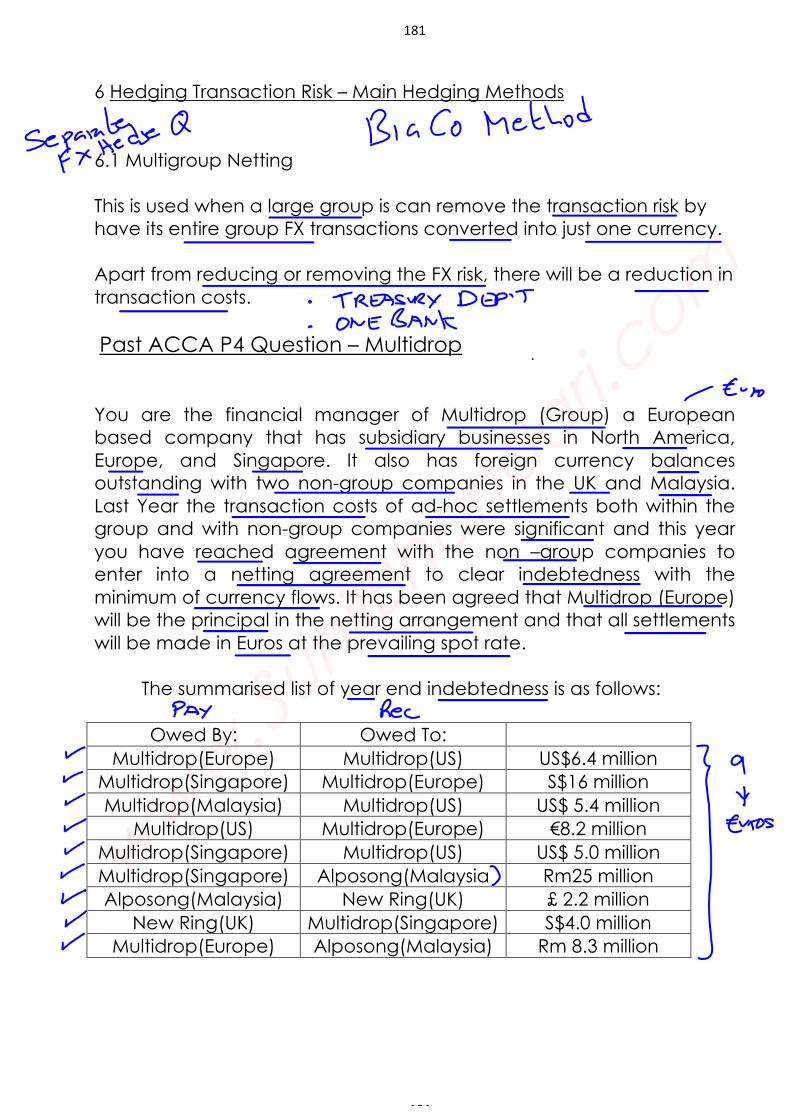

Past ACCA P4 Question – Multidrop You are the financial manager of Multidrop (Group) a European based company that has subsidiary businesses in North America, Europe, and Singapore. It also has foreign currency balances outstanding with two non-group companies in the UK and Malaysia. Last Year the transaction costs of ad-hoc settlements both within the group and with non-group companies were significant and this year you have reached agreement with the non –group companies to enter into a netting agreement to clear indebtedness with the minimum of currency flows. It has been agreed that Multidrop (Europe) will be the principal in the netting arrangement and that all settlements will be made in Euros at the prevailing spot rate.

The summarised list of year end indebtedness is as follows: Owed By: Owed To:

Multidrop(Europe) Multidrop(US) US$6.4 million Multidrop(Singapore) Multidrop(Europe) S$16 million Multidrop(Malaysia) Multidrop(US) US$ 5.4 million

Multidrop(US) Multidrop(Europe) €8.2 million Multidrop(Singapore) Multidrop(US) US$ 5.0 million Multidrop(Singapore) Alposong(Malaysia Rm25 million Alposong(Malaysia) New Ring(UK) £ 2.2 million

New Ring(UK) Multidrop(Singapore) S$4.0 million Multidrop(Europe) Alposong(Malaysia) Rm 8.3 million

182

182

Currency cross rates (mid-market) are as follows: Currency Euro 1UK£ = 1.0653 1US$ = 0.7296 1Euro = 1.0000 1Sing$ = 0.4843 1Rm = 0.2004 You may assume settlement will be at the mid-market rates quoted. Required: a) Calculate the inter group and inter-company currency transfers that will be required for settlement by Multidrop (Europe)

183

183

Past ACCA P4 Question – Multidrop (Solution)

184

184

185

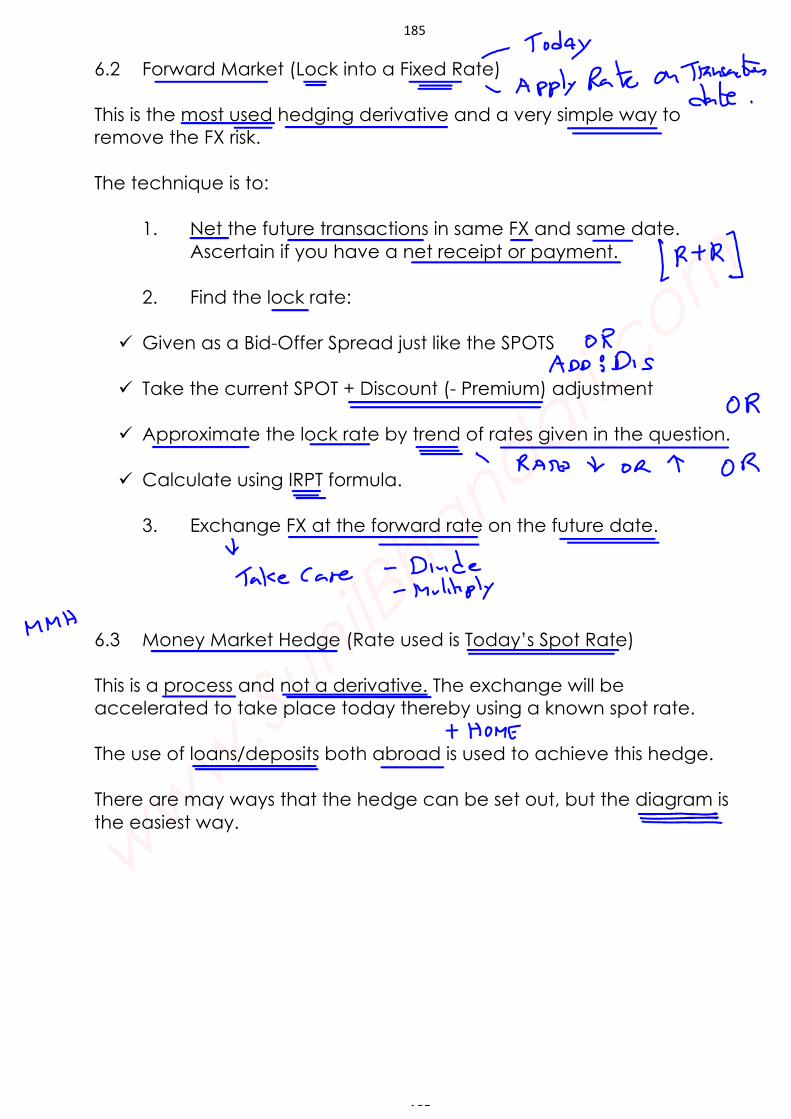

185

6.2 Forward Market (Lock into a Fixed Rate) This is the most used hedging derivative and a very simple way to remove the FX risk.

The technique is to:

1. Net the future transactions in same FX and same date.

Ascertain if you have a net receipt or payment.

2. Find the lock rate:

! Given as a Bid-Offer Spread just like the SPOTS

! Take the current SPOT + Discount (- Premium) adjustment

! Approximate the lock rate by trend of rates given in the question.

! Calculate using IRPT formula.

3. Exchange FX at the forward rate on the future date. 6.3 Money Market Hedge (Rate used is Today’s Spot Rate) This is a process and not a derivative. The exchange will be accelerated to take place today thereby using a known spot rate. The use of loans/deposits both abroad is used to achieve this hedge. There are may ways that the hedge can be set out, but the diagram is the easiest way.

186

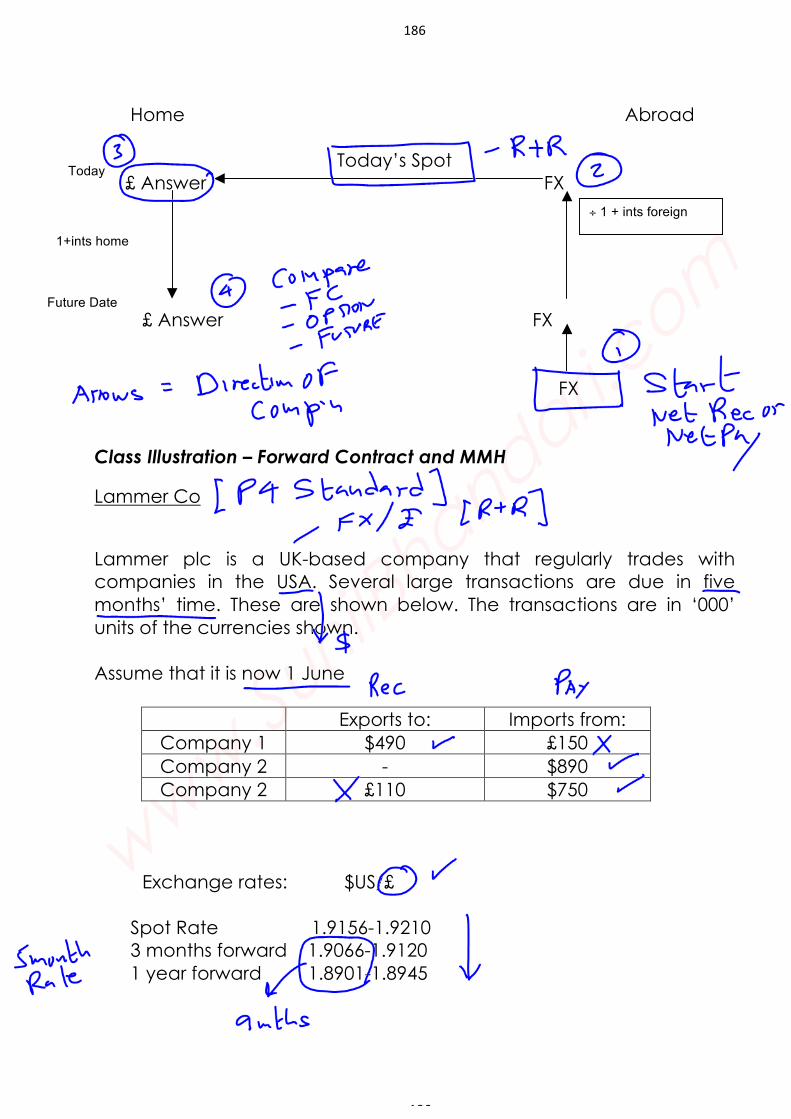

186

Home Abroad Today’s Spot £ Answer FX

£ Answer FX

FX

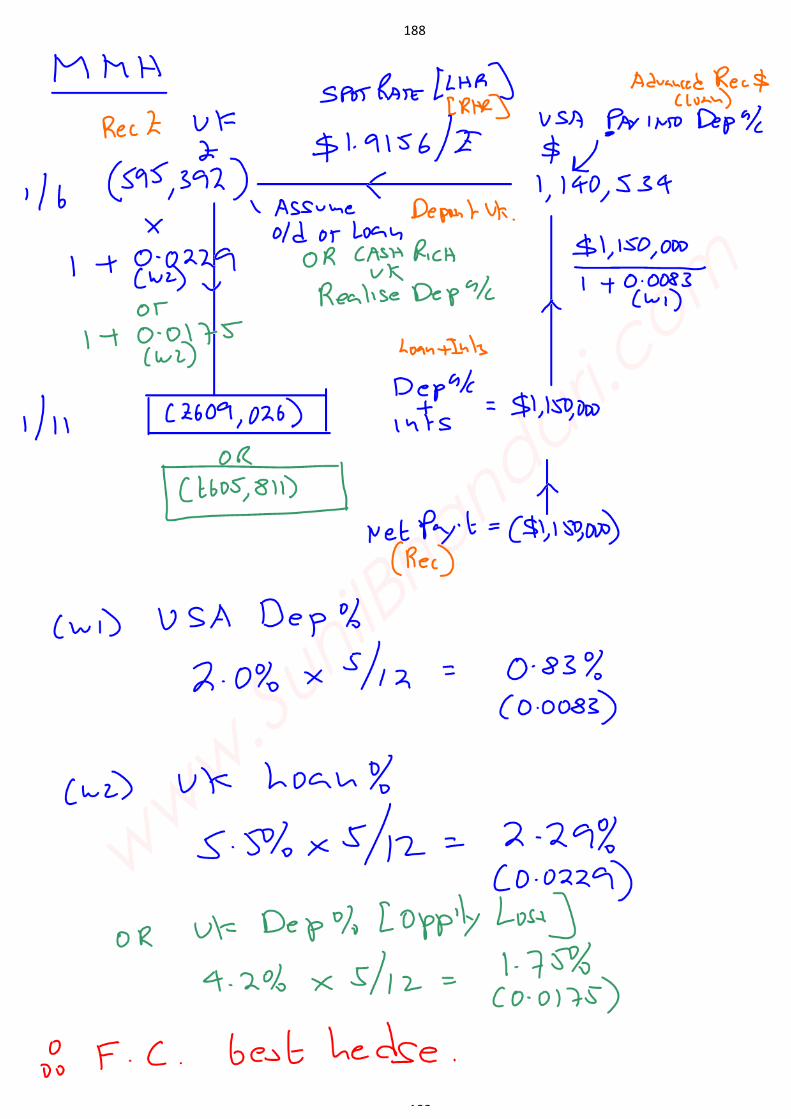

Class Illustration – Forward Contract and MMH

Lammer Co

Lammer plc is a UK-based company that regularly trades with companies in the USA. Several large transactions are due in five months’ time. These are shown below. The transactions are in ‘000’ units of the currencies shown.

Assume that it is now 1 June

Exports to: Imports from:

Company 1 $490 £150 Company 2 - $890 Company 2 £110 $750

Exchange rates: $US/£

Spot Rate 1.9156-1.9210 3 months forward 1.9066-1.9120 1 year forward 1.8901-1.8945

Today

1+ints home

Future Date

÷ 1 + ints foreign

187

187

Annual interest rates available to Lammer plc

Borrowing Deposit Sterling up to 6 months 5.5% 4.2% Dollar up to 6 months 4.0% 2.0%

188

188

189

189

6.4 Currency Options (Remove the downside risk only) The currency option is the RIGHT to use an exchange rate that is chosen today. However, a premium has to be paid for that right. These products can be obtained from a bank – known at an OTC option. These are more expensive. More likely they can be obtained from one of several major futures and option exchanges located in major cities. For traded options please note:

! Available from SIMEX, LIFFE, CME, NYBOT etc

! Each market sets the currency of the contract (cc) it trades options in. E.g. $125,000

! A PUT is the right to SELL the CC and the CALL the right to buy

the CC

! There will be choice of exercise or strike rates to choose from.

! Care must be taken when computing the premium. It must be paid up from in the currency the market commands.

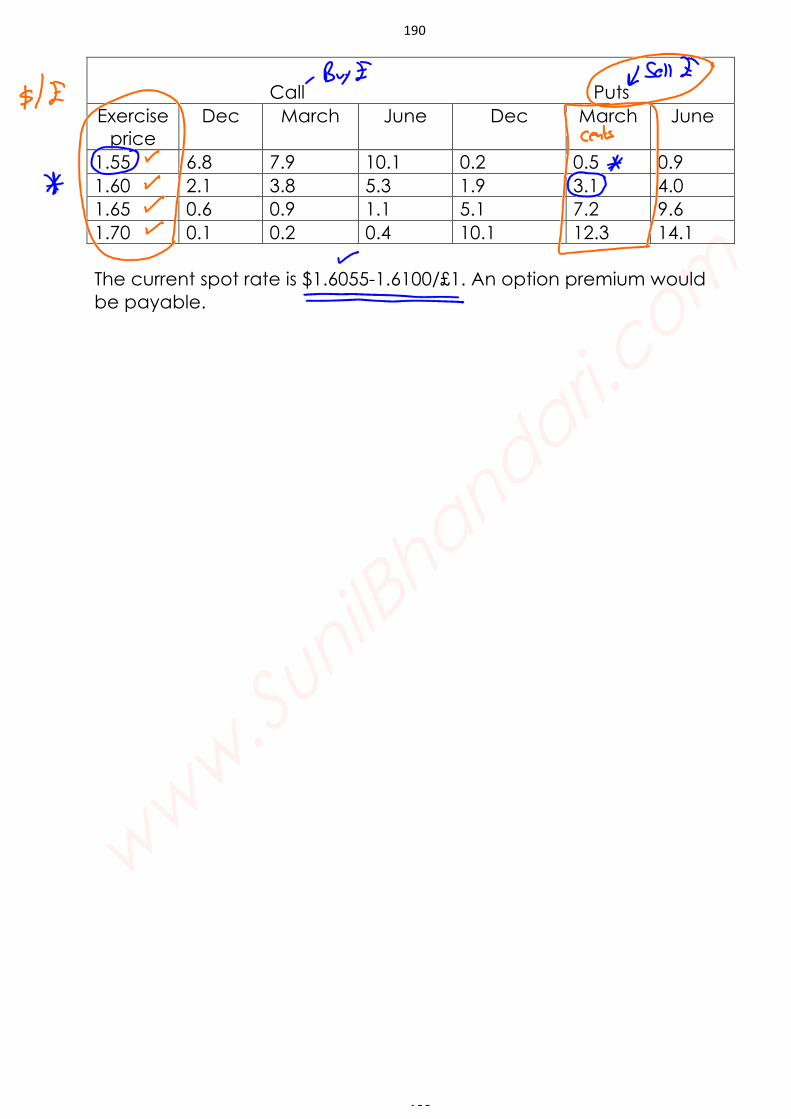

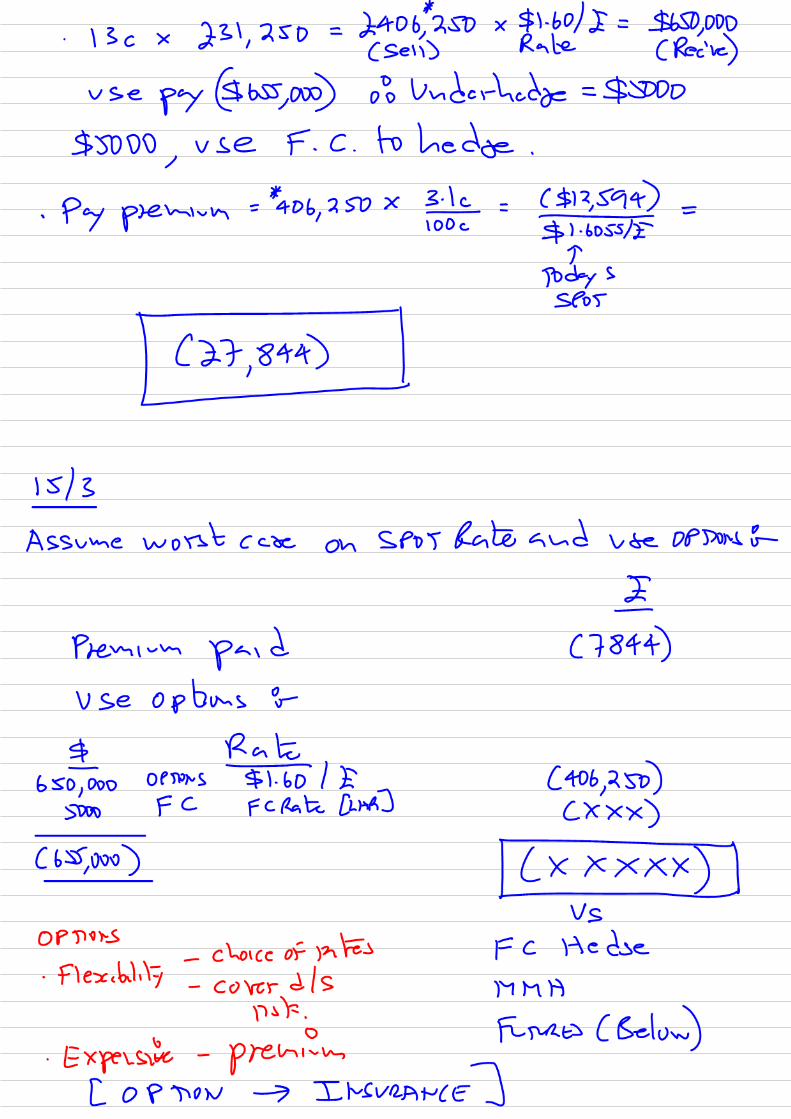

Class Illustration – Currency Options

Giggs Co Giggs Co based in the UK is expecting to pay $655,000 on 15th March. Today is 1st January. It wishes to use a traded currency option available on the CME. Current option prices are: Sterling contacts, £31,250 contracts size. Premium is in US cents per £1.

190

190

Call Puts Exercise

price Dec March June Dec March June

1.55 6.8 7.9 10.1 0.2 0.5 0.9 1.60 2.1 3.8 5.3 1.9 3.1 4.0 1.65 0.6 0.9 1.1 5.1 7.2 9.6 1.70 0.1 0.2 0.4 10.1 12.3 14.1 The current spot rate is $1.6055-1.6100/£1. An option premium would be payable.

191

191

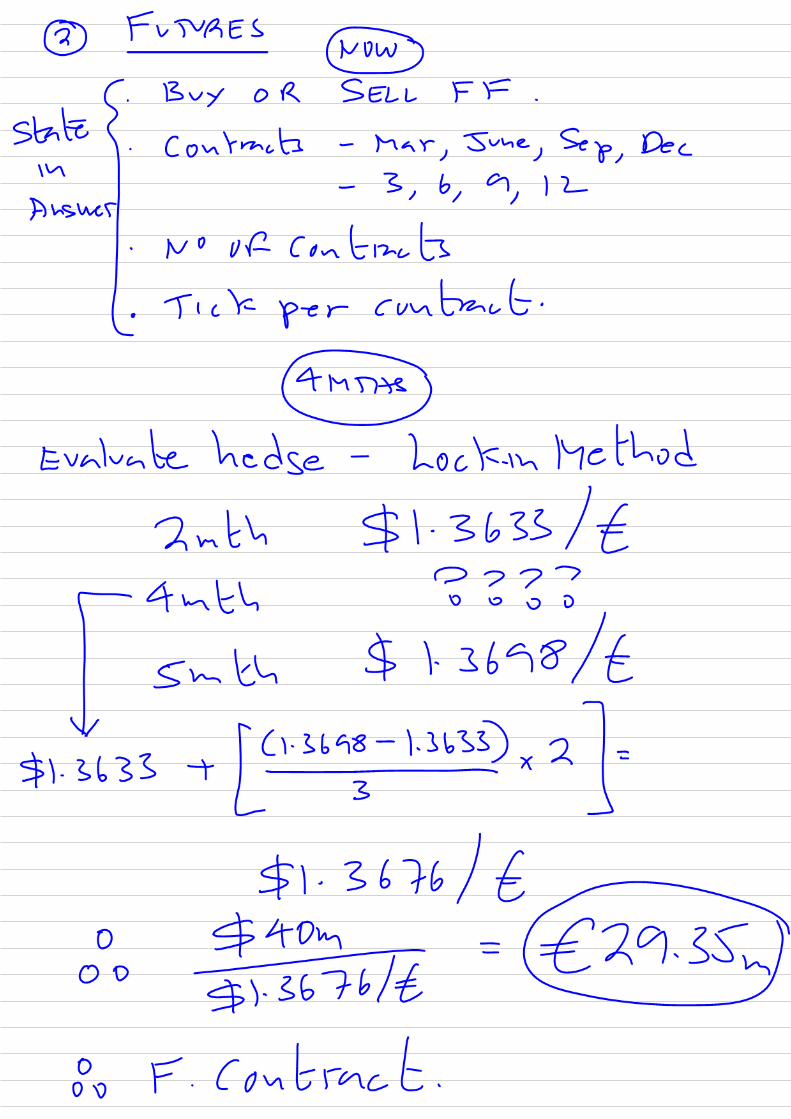

6.5 Futures (Lock into a rate that will approximately equal today’s Spot Rate)

This is regarded as the most complicated of the hedging methods. The markets mentioned above trade both FUTURES and OPTIONS. Futures are a speculative derivative – in effect a spread betting product where the terminology is key. “SELL” is to bet on the Derivative will FALL in value and “BUY” is to bet on a RISE. Other details that need to be known:

! Futures exist for “products” and “index” numbers like Oil, wheat, pork bellies, CURRENCIES and INTEREST RATES

! Key factor is that derivative values FOLLOW IN SAME DIRECTION as primary market values. For instance, if the price of oil were to rise on the world markets, the OIL FUTURES DERIVATIVE price will also RISE.

! Futures markets set:

" Contract sizes and dates – which will be given

" Ticks – the minimum change in the value of a currency and the derivative.

" Margins – as this is a betting the market, traders must show that they can cover their losses and so the markets demand a deposit be left with them to pay out in case of a loss.

" Basis – the value of the primary and its derivative are NOT exactly the same on any date except for the last day of trading of those futures. The difference is called basis.

192

192

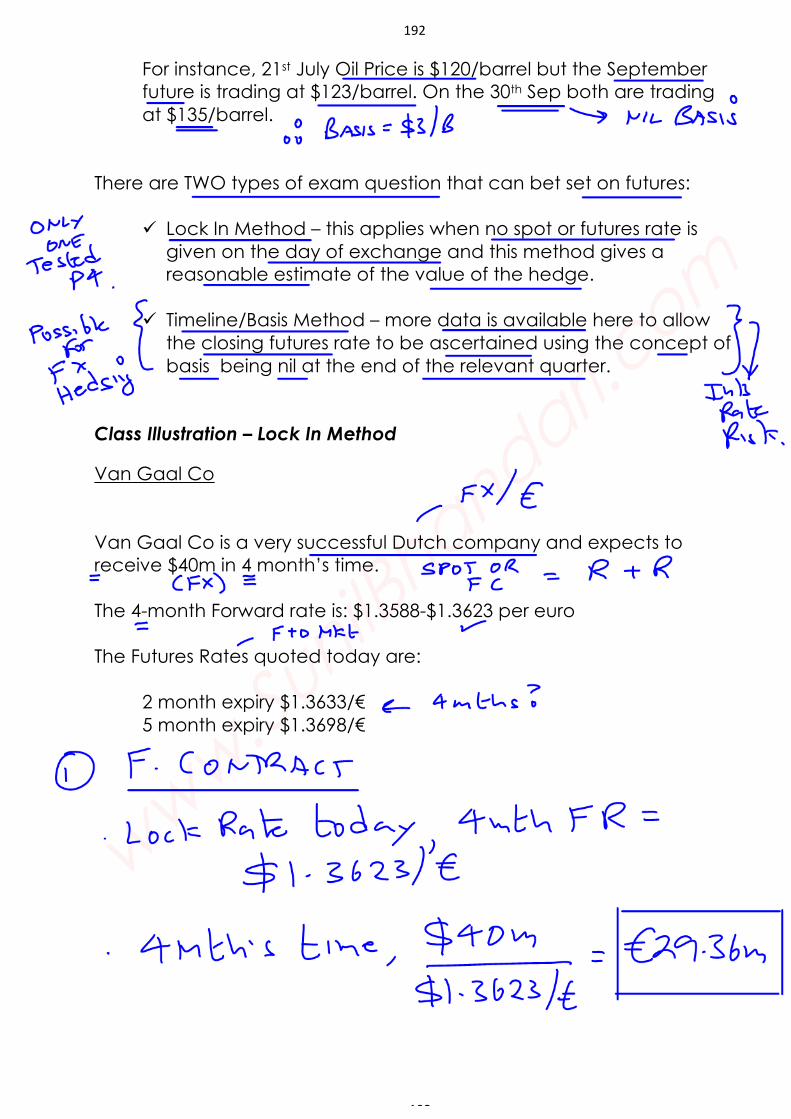

For instance, 21st July Oil Price is $120/barrel but the September future is trading at $123/barrel. On the 30th Sep both are trading at $135/barrel.

There are TWO types of exam question that can bet set on futures:

! Lock In Method – this applies when no spot or futures rate is given on the day of exchange and this method gives a reasonable estimate of the value of the hedge.

! Timeline/Basis Method – more data is available here to allow

the closing futures rate to be ascertained using the concept of basis being nil at the end of the relevant quarter.

Class Illustration – Lock In Method

Van Gaal Co Van Gaal Co is a very successful Dutch company and expects to receive $40m in 4 month’s time. The 4-month Forward rate is: $1.3588-$1.3623 per euro The Futures Rates quoted today are:

2 month expiry $1.3633/€ 5 month expiry $1.3698/€

193

193

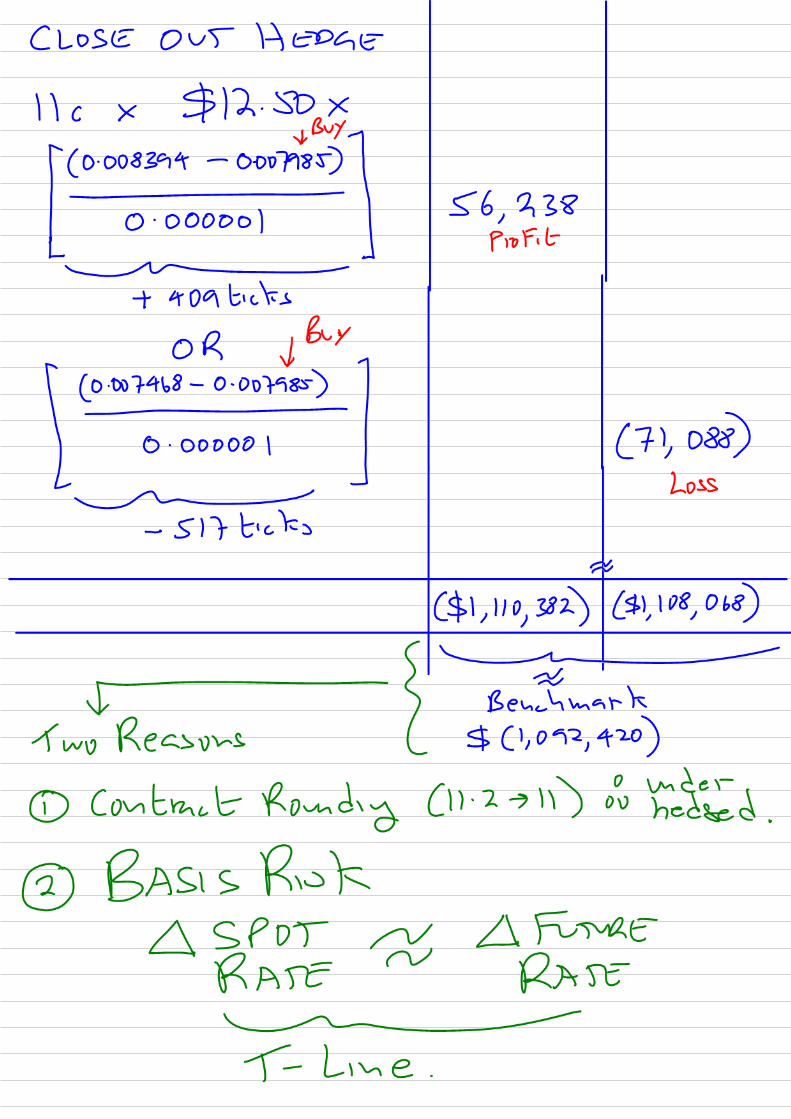

Class Illustration – Basis Method

KYT Inc Assume that it is now 30 June. KYT Inc is a company located in the USA THAT HAS A CONTRACT TO PURCHASE GOODS FROM Japan in two months’ time, on 1 September. The payment is to be made in yen and will total 140 million yen.

The managing director of KYT Inc wishes to protect the contract against adverse movements in foreign exchange rates, and is considering the use of currency futures. The following data are available.

Spot foreign exchange rate:

Yen/$ 128.15

Yen currency futures contracts on SIMEX (Singapore Monetary Exchange):

Contract size 12,500,000 yen. Contract prices are in US$ per yen

Contract prices: September 0.007985 December 0.008250 Assume that futures contracts mature at the end of the month.

Please note Spot Rate on 1st Sep is Yen 120/$ or Yen 135/$.

194

194

195

195

196

196

7 Pros & Cons

Pros Cons Forward Market

• Fixed Rate, certainty • Easy • Cheap • Tailored

• Inflexible/contract • Lose out on the upside • Must ensure FX receipts

arrive MMH

• Convert today • Cheap • Tailored • Flexible

• Complicated • May not apply for FX

receipt

Futures • Effectively fix rate • No cost • Small gain

• Complicated • Small loss • Need cash for margin • No tailoring

Options • Best hedge – cover d/s

risk only • Flexibility • Lots of choice

• Complicated • No tailoring • Expensive

197

197

8. SWAPS 8.1 In forex swap, the parties agree to swap equivalent amounts of currency for a period and then re-swap them at the end of the period at an agreed swap rate. The swap rate and amount of currency is agreed between the parties in advance. Thus it is called a ‘fixed rate/fixed rate’ swap.

The main objectives of a forex swap are:

! To hedge against forex risk, possibly for a longer period than is possible on the forward market.

! Access to capital markets, in which it may be impossible to

borrow directly.

! Forex swaps are especially useful when dealing with countries that have exchange controls and /or volatile exchange rates.

Class Illustration – SWAPS

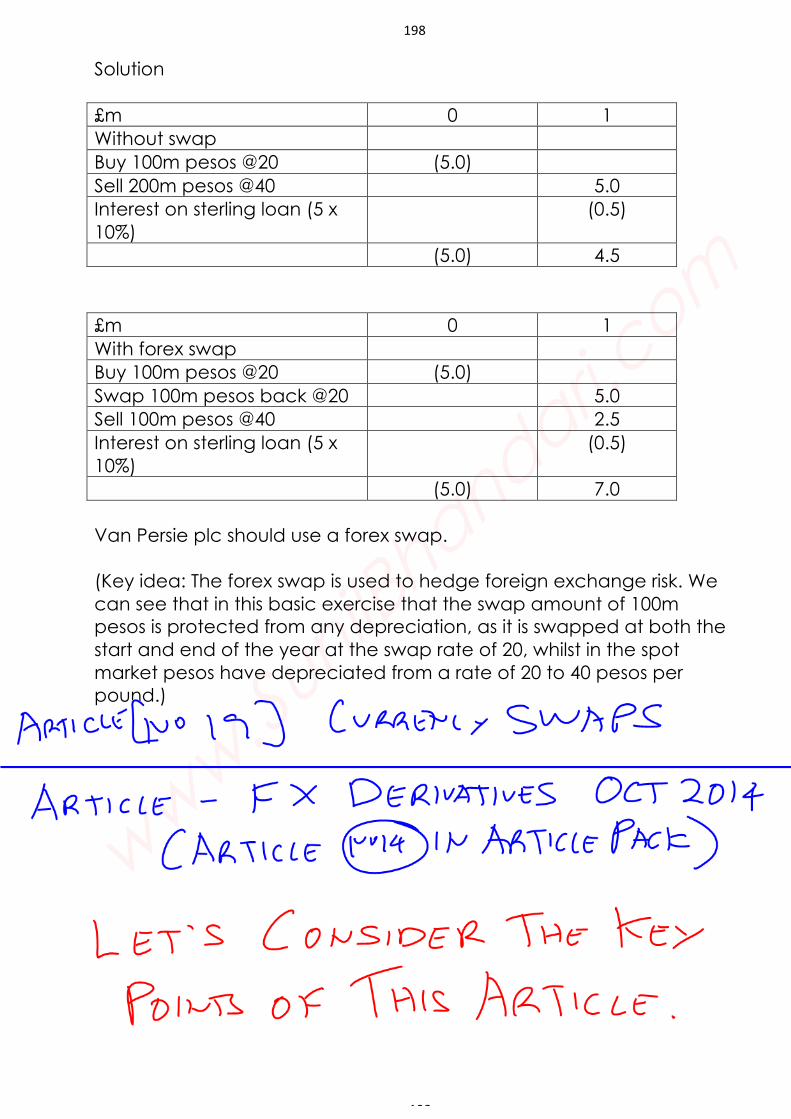

Van Persie Say Van Persie is contracted to build a bridge that will require an initial investment of 100m pesos and is will be sold for 200m pesos in one year’s time. The currency spot rate is 20 pesos/£, and the government has offered a forex swap at 20 pesos/£. Van Persie cannot borrow pesos directly and there is no forward market available. The estimated spot rate in one year is 40 pesos/£. The current UK borrowing rate is 10%. Determine whether Van Persie should do nothing or hedge its exposure using the forex swap.

198

198

Solution £m 0 1 Without swap Buy 100m pesos @20 (5.0) Sell 200m pesos @40 5.0 Interest on sterling loan (5 x 10%)

(0.5)

(5.0) 4.5 £m 0 1 With forex swap Buy 100m pesos @20 (5.0) Swap 100m pesos back @20 5.0 Sell 100m pesos @40 2.5 Interest on sterling loan (5 x 10%)

(0.5)

(5.0) 7.0 Van Persie plc should use a forex swap. (Key idea: The forex swap is used to hedge foreign exchange risk. We can see that in this basic exercise that the swap amount of 100m pesos is protected from any depreciation, as it is swapped at both the start and end of the year at the swap rate of 20, whilst in the spot market pesos have depreciated from a rate of 20 to 40 pesos per pound.)