Chapter Brealey, Myers, and Allen Principles of Corporate Finance 11th Edition REAL OPTIONS 22...

26

Chapter Brealey, Myers, and Allen Principles of Corporate Finance 11th Edition REAL OPTIONS 22 Copyright © 2014 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

-

Upload

sarina-heady -

Category

Documents

-

view

247 -

download

8

Transcript of Chapter Brealey, Myers, and Allen Principles of Corporate Finance 11th Edition REAL OPTIONS 22...

Chapter

Brealey, Myers, and Allen

Principles of Corporate Finance

11th Edition

REAL OPTIONS

22

Copyright © 2014 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

22-2

22-1 VALUE OF FOLLOW-ON INVESTMENT OPPORTUNITIES

• Four Types of Real Opinions • Opportunity to expand, make follow-up investments

• Opportunity to wait, invest later

• Opportunity to shrink or abandon project

• Opportunity to vary firm’s output or production methods

• Value of real option = NPV with option

− NPV without option

22-3

TABLE 22.1 CASH FLOW AND FINANCIAL ANALYSIS OF MARK I MICROCOMPUTER

• Mark I Microcomputer in Millions

22-4

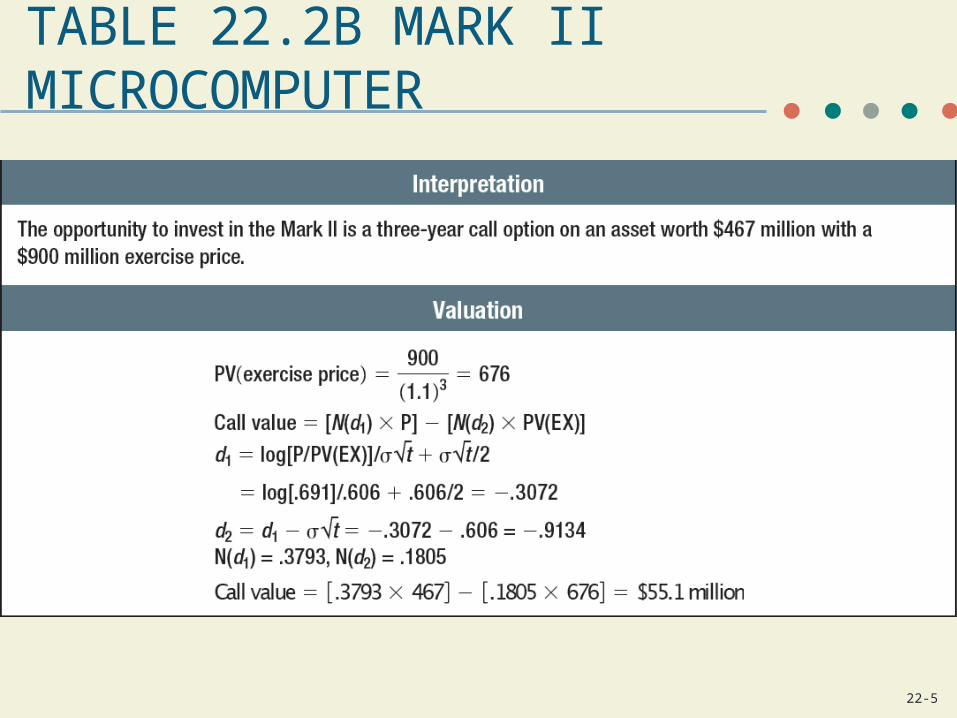

TABLE 22.2A MARK II MICROCOMPUTER

22-5

TABLE 22.2B MARK II MICROCOMPUTER

22-6

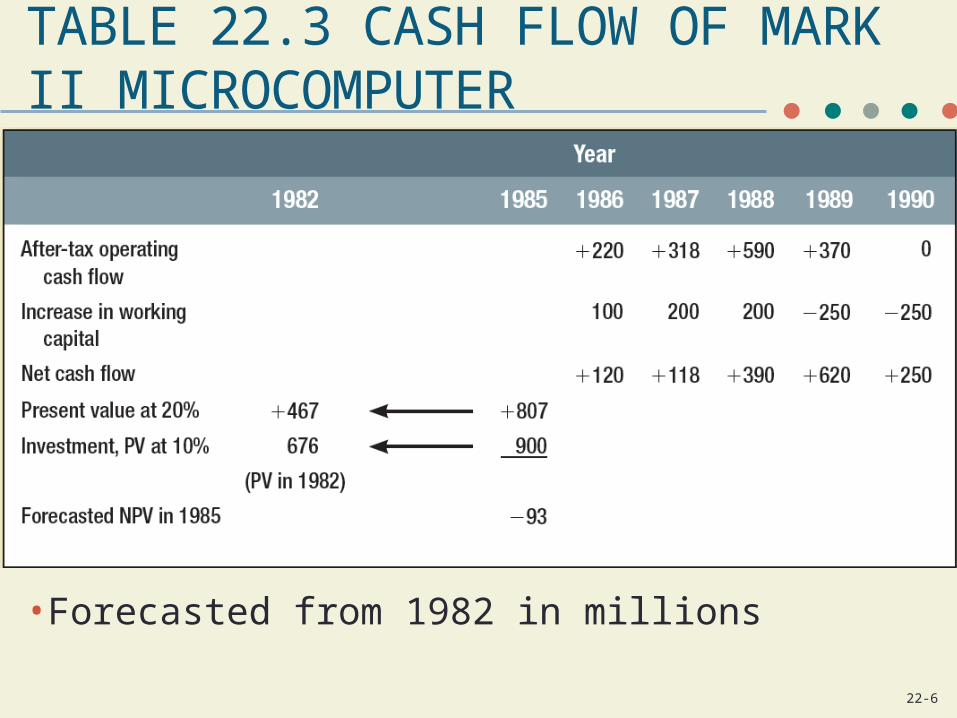

TABLE 22.3 CASH FLOW OF MARK II MICROCOMPUTER

• Forecasted from 1982 in millions

22-7

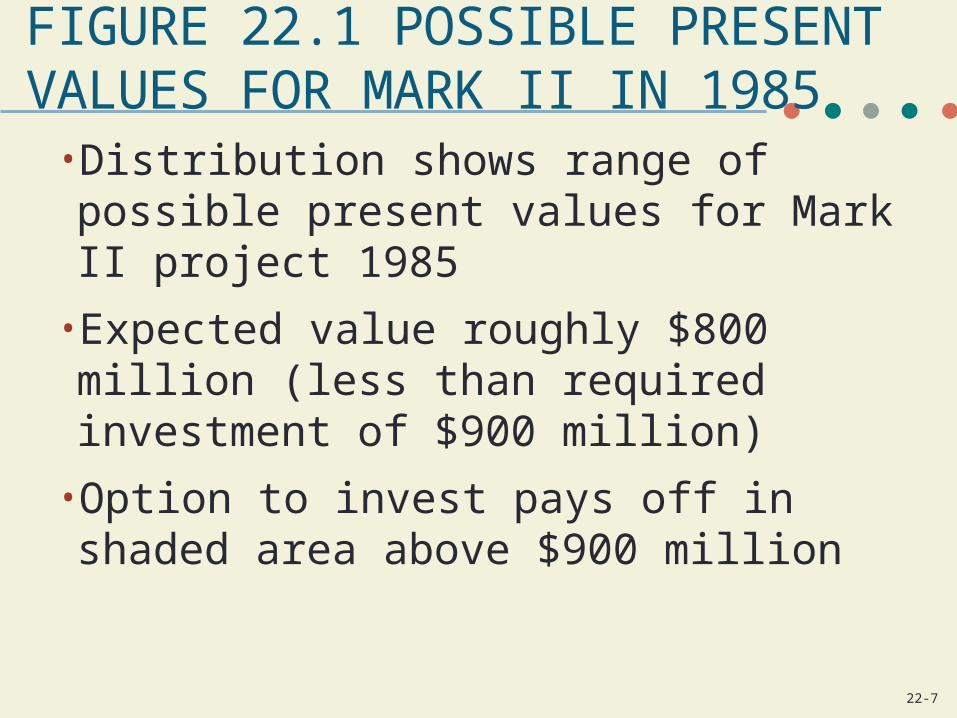

FIGURE 22.1 POSSIBLE PRESENT VALUES FOR MARK II IN 1985

• Distribution shows range of possible present values for Mark II project 1985

• Expected value roughly $800 million (less than required investment of $900 million)

• Option to invest pays off in shaded area above $900 million

22-8

FIGURE 22.1 POSSIBLE PRESENT VALUES FOR MARK II IN 1985

22-9

22-2 TIMING OPTIONO

ptio

n p

rice

Intrinsic value

Stock price

•Option to Wait

22-10

22-2 TIMING OPTION

• Intrinsic value plus time premium equals option value

• Time premium equals value of being able to wait

Opt

ion

pric

e

Stock price

22-11

22-2 TIMING OPTION

• Option to Wait• More time equals more value

Stock price

Opt

ion

pric

e

22-12

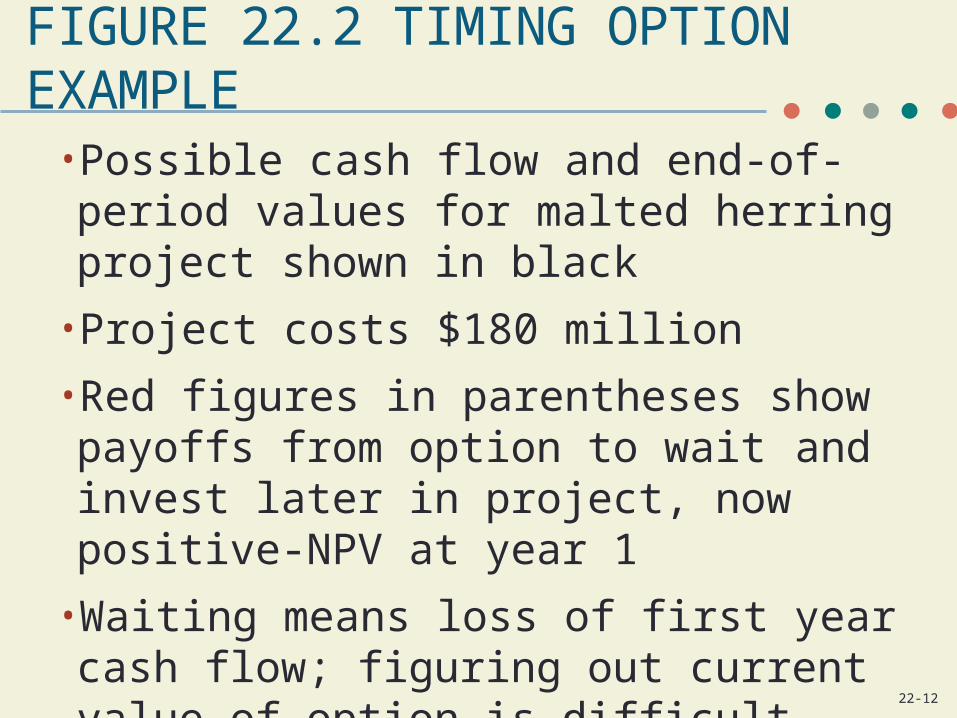

FIGURE 22.2 TIMING OPTION EXAMPLE

• Possible cash flow and end-of-period values for malted herring project shown in black

• Project costs $180 million

• Red figures in parentheses show payoffs from option to wait and invest later in project, now positive-NPV at year 1

• Waiting means loss of first year cash flow; figuring out current value of option is difficult

22-13

FIGURE 22.2 TIMING OPTION EXAMPLE

22-14

22-2 TIMING OPTION

• High demand generates $25 million, $250 million value at end of year

• Low demand generates $16 million with no value

High Demand Low Demand

375.

1200

)25025(return Total

12.

1200

)16016(return Total

Risk neutral return

22-15

22-2 TIMING OPTION

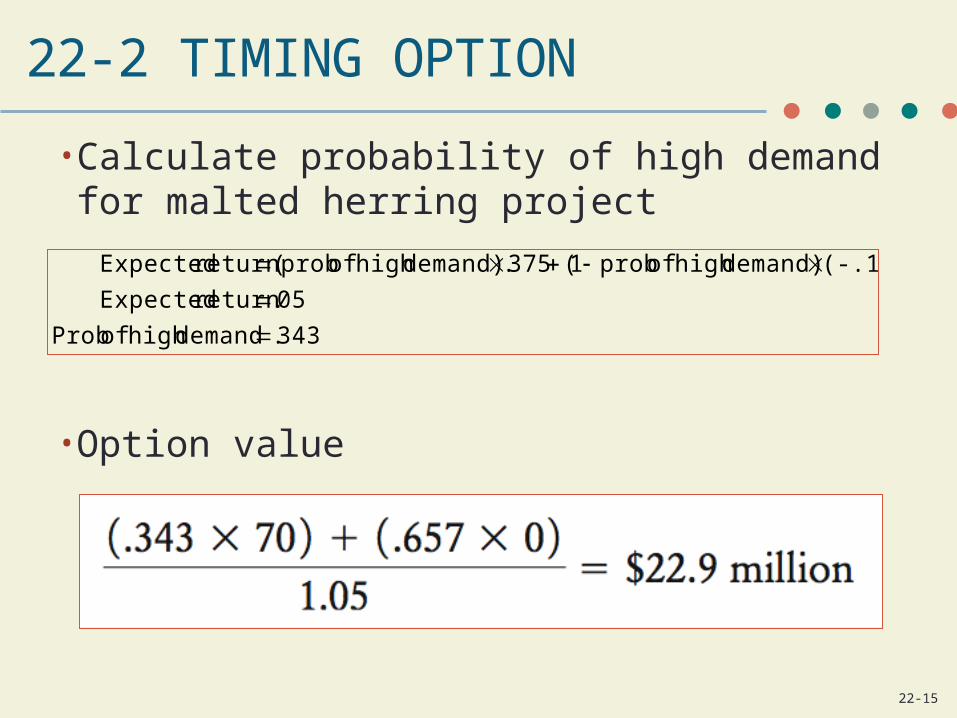

• Calculate probability of high demand for malted herring project

• Option value

343. demandhigh of Prob

05.return Expected

(-.12)demand)high of prob1(375.demand)high of prob(return Expected

22-16

FIGURE 22.3 DEVELOPMENT OPTION FOR VACANT LAND

22-17

22-3 ABANDONMENT OPTION

• Example • Mrs. Mulla gives nonretractable offer to buy company for $150 million at anytime within next year

• Given possible outcomes

• What is value of offer?

• What is most Mrs. Mulla could charge for that option?

• Use discount rate of 10%

22-18

22-3 ABANDONMENT OPTION

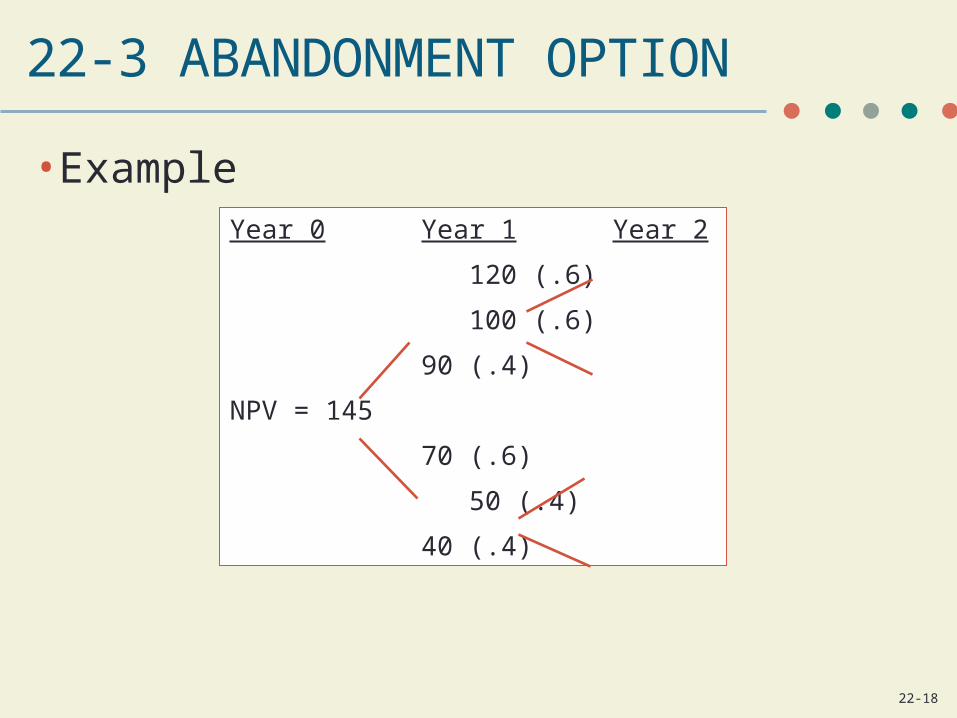

Year 0 Year 1 Year 2

120 (.6)

100 (.6)

90 (.4)

NPV = 145

70 (.6)

50 (.4)

40 (.4)

•Example

22-19

22-3 ABANDONMENT OPTION

Year 0 Year 1 Year 2

120 (.6)

100 (.6)

90 (.4)

NPV = 162

150 (.4)

Option value =

162 − 145 =

$17 Million

22-20

FIGURE 22.4 VALUE OF TANKER

22-21

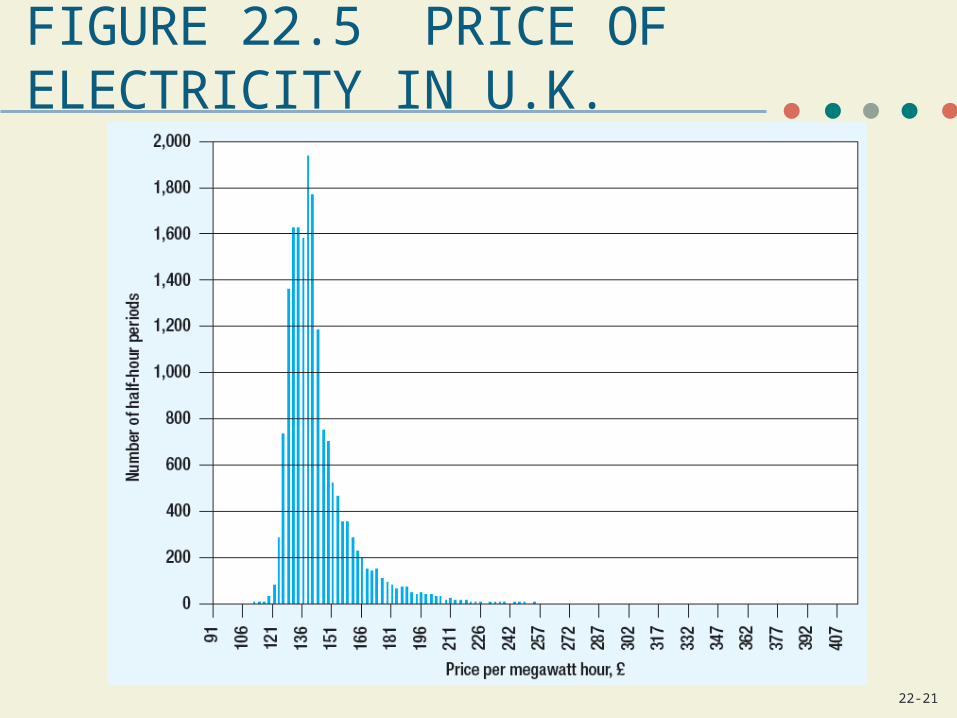

FIGURE 22.5 PRICE OF ELECTRICITY IN U.K.

22-22

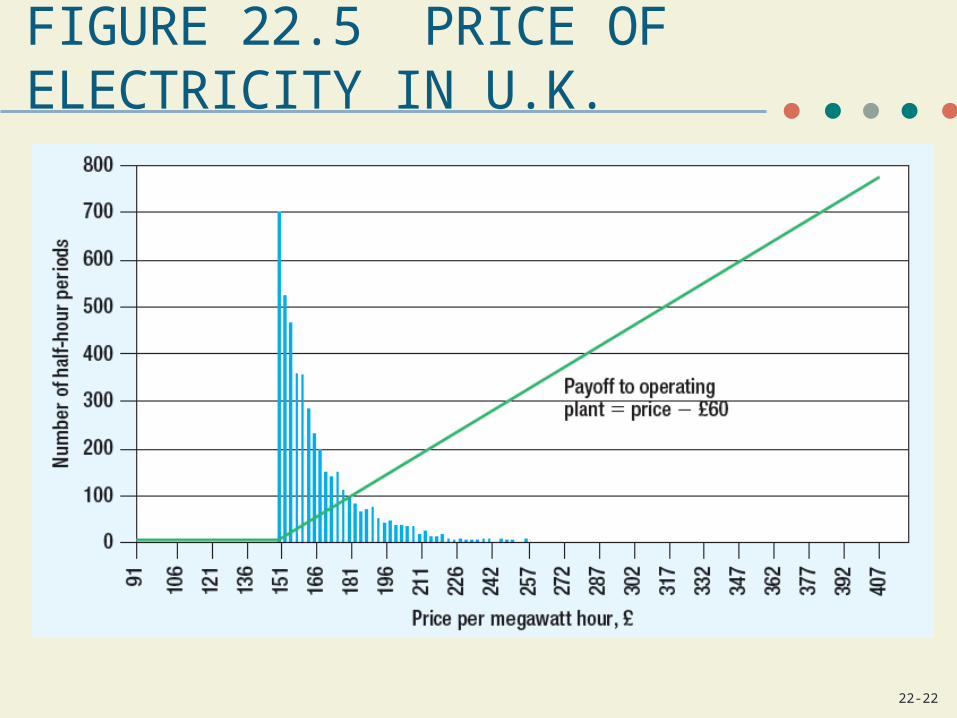

FIGURE 22.5 PRICE OF ELECTRICITY IN U.K.

22-23

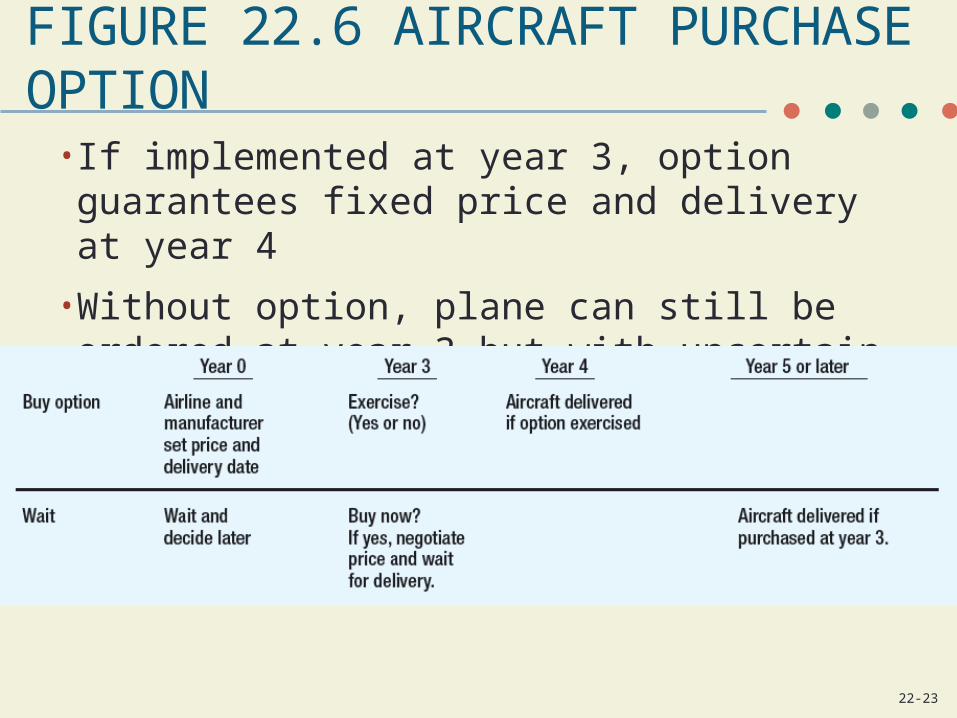

FIGURE 22.6 AIRCRAFT PURCHASE OPTION

• If implemented at year 3, option guarantees fixed price and delivery at year 4

• Without option, plane can still be ordered at year 3 but with uncertain price and delivery

22-24

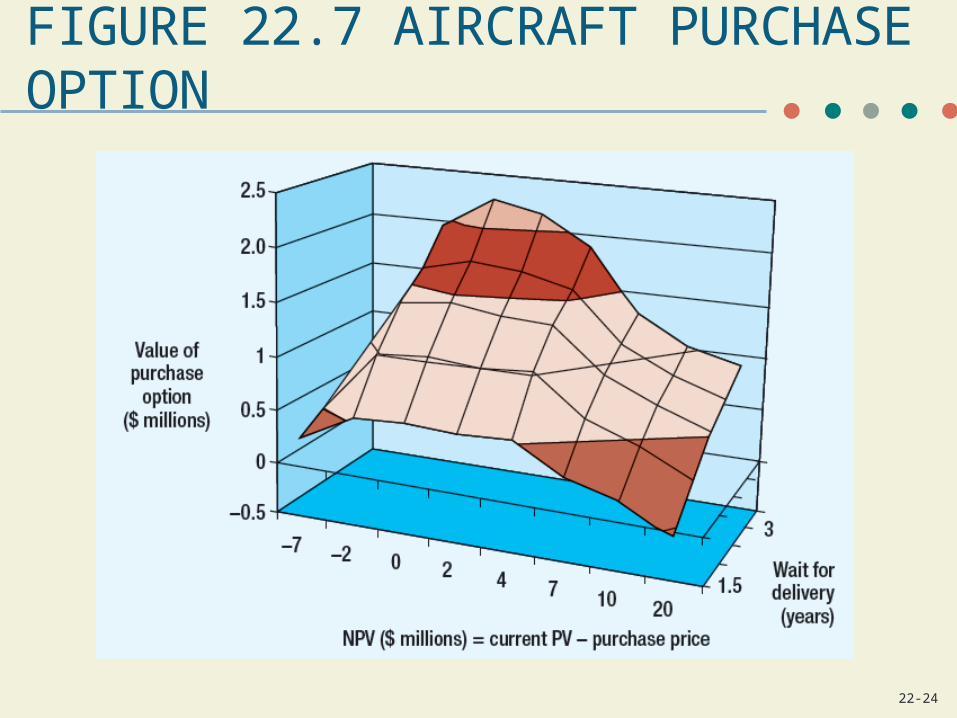

FIGURE 22.7 AIRCRAFT PURCHASE OPTION

22-25

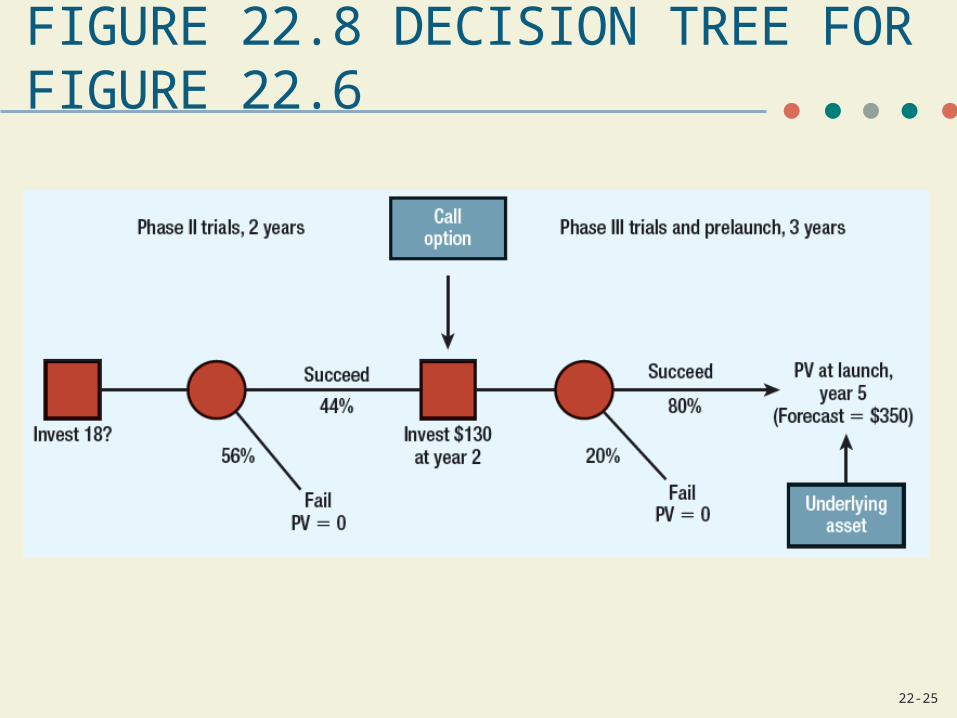

FIGURE 22.8 DECISION TREE FOR FIGURE 22.6

22-26

22-6 CONCEPTUAL PROBLEM

• Real options are not always feasible to use• Options can be complex; it is sometimes impossible to arrive at “perfect” answer

• No clear structure to path and cash flows

• Competitors have real options, which alter option values by altering underlying assumptions and environment that serves as basis of valuation