Chapter 9 The Production Business Process. Presentation Outline I.Files and Reports in a Production...

36

Chapter 9 The Production Business Process

-

Upload

kerry-emil-bradley -

Category

Documents

-

view

219 -

download

5

Transcript of Chapter 9 The Production Business Process. Presentation Outline I.Files and Reports in a Production...

Chapter 9The Production Business Process

Presentation Outline

I. Files and Reports in a Production System

II. Production Control Application System

III. Property Accounting Applications

IV. Quick-Response Manufacturing Systems

I. Files and Reports in a Production System

A. Production Order

B. Bill of Materials

C. Master Operations List

D. Materials Requisitions

E. Job Time Cards

F. Resource Availability Reports

G. Production Status Reports

A. Production Order

Production control issues production orders to authorize production departments to make

certain products.

We are ready to begin this

order.

B. Bill of Materials

A bill of materials is a listing of the

ingredients that go into making a product.

It lists of all the required parts and their descriptions.

What materials do we need to make this product?

C. Master Operations List

A master operations list specifies the

sequencing of all labor and/or machine

operations that are necessary to produce a

product.

D. Materials Requisitions

Production control prepares materials

requisitions to authorize the release of raw materials from inventory for use in

production.

E. Job Time Cards

Job time cards are used to document the

amount of labor time that is spent on each production order or

job.

F. Resource Availability Reports

Inventory status reports detail the material

resources available in inventory for production.

Factor availability reports communicate the

availability of labor and machine resources for

production.

We have the materials, but may have to schedule some

overtime for this job.

G. Production Status Reports

Production status reports detail the work completed on individual production

orders as they move through production.

Open production orders are monitored and

departmental production schedules are revised as

necessary.

II. Production Control Application System

A. The Role of Production Control

B. Accounting for the Factors of Production

C. Completion of the Production Order

D. Inventory Control

E. Just-In-Time Production

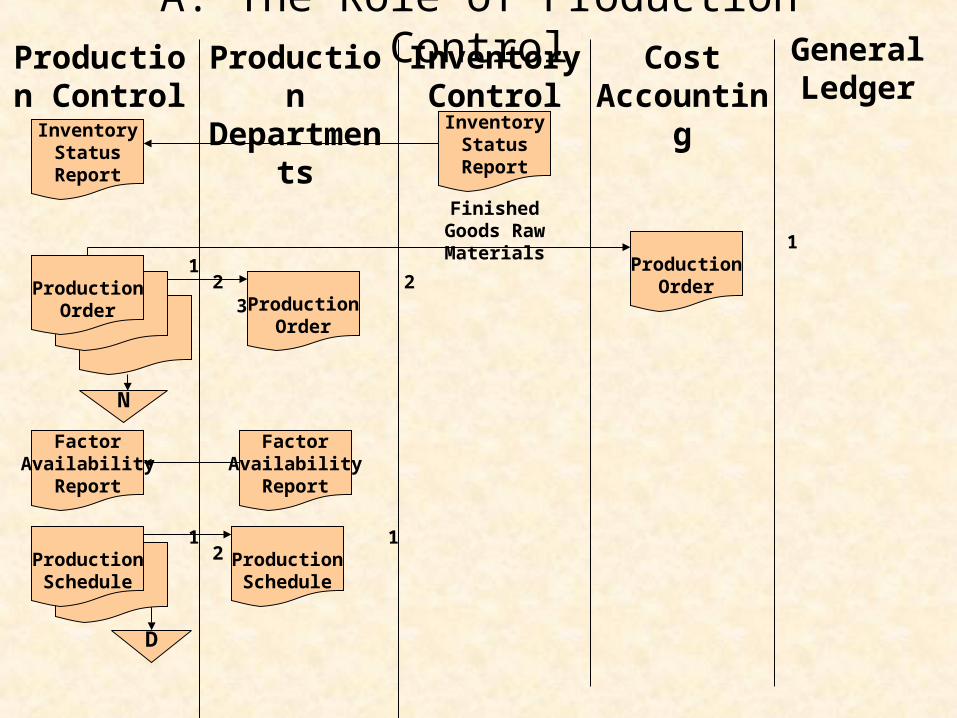

A. The Role of Production Control

1Production

Order 3

2

Production Departments

Production Control

Inventory Control

Cost Accounting

General Ledger

1Production

Order

2Production

Order

N

InventoryStatusReport

Finished Goods Raw Materials

InventoryStatusReport

FactorAvailability

Report

FactorAvailability

Report

2 1ProductionSchedule

D

1ProductionSchedule

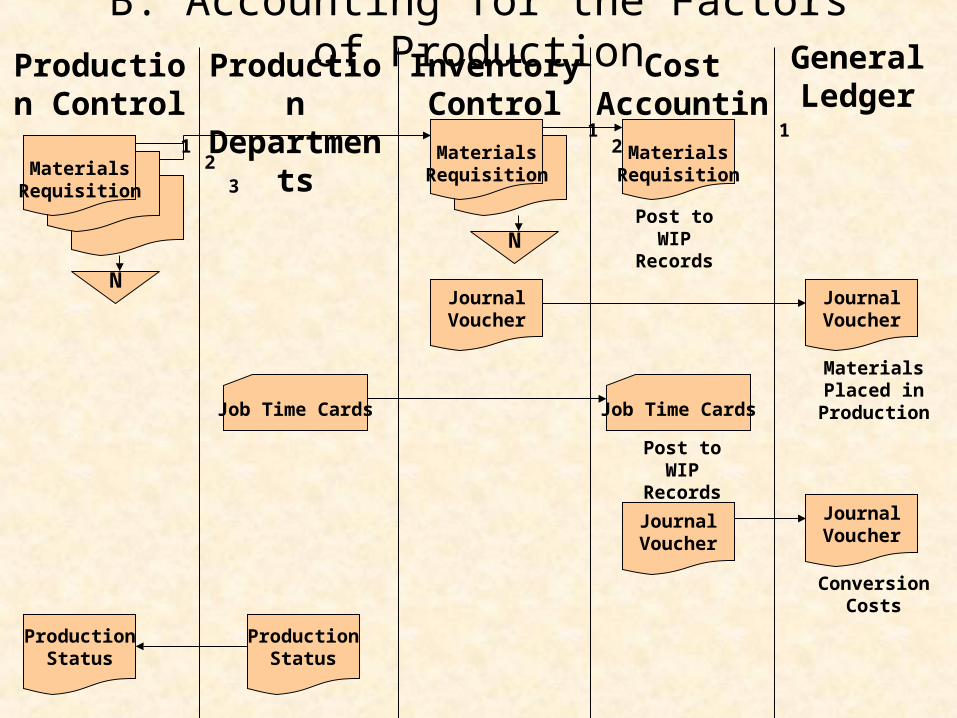

B. Accounting for the Factors of ProductionProduction

DepartmentsProduction

ControlInventory Control

Cost Accounting

General Ledger

3 2

1Materials

Requisition

N

2 1

MaterialsRequisition

1Materials

Requisition

NPost to WIP

Records

JournalVoucher

JournalVoucher

Materials Placed in Production

ProductionStatus

ProductionStatus

Job Time Cards Job Time Cards

Post to WIP Records

JournalVoucher

JournalVoucher

Conversion Costs

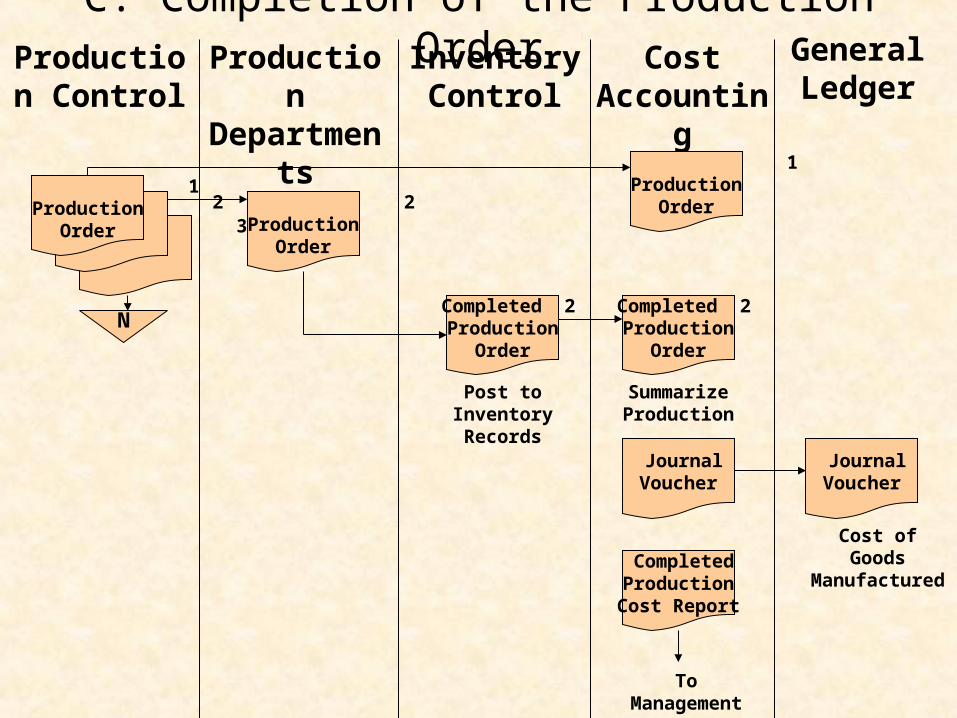

C. Completion of the Production Order

3 2

Production Departments

Production Control

Inventory Control

Cost Accounting

General Ledger

1Production

Order

1Production

Order 2Production

Order

N Completed 2

ProductionOrder

Post to Inventory Records

Completed 2Production

Order

Summarize Production

JournalVoucher

JournalVoucher

Cost of Goods Manufactured Completed

ProductionCost Report

To Management

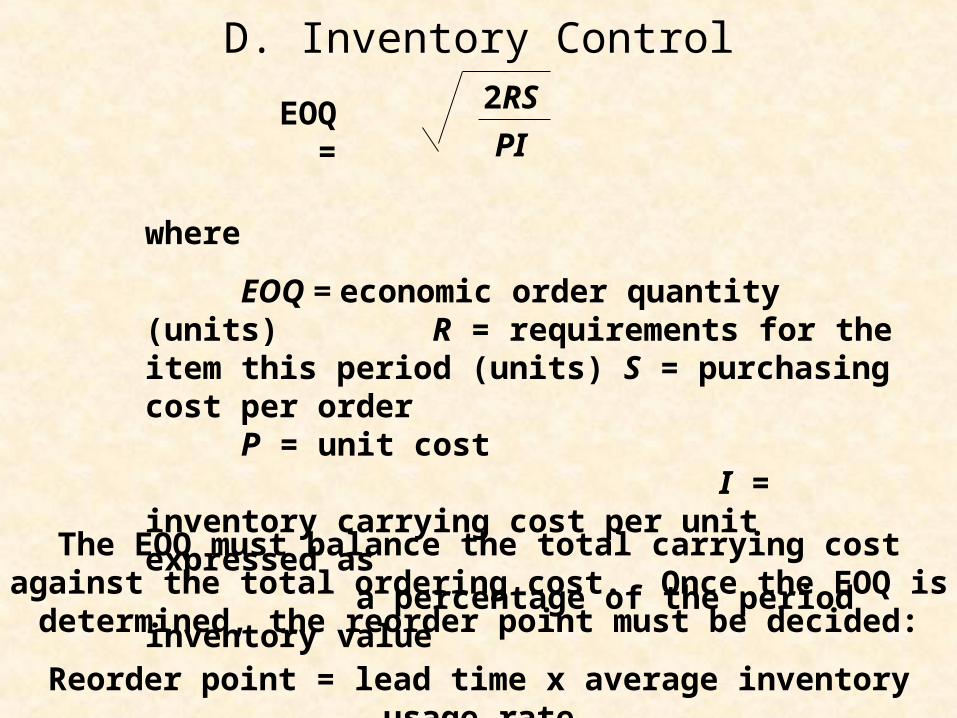

D. Inventory Control2RS

PIEOQ =

where

EOQ = economic order quantity (units) R = requirements for the item this period (units)S = purchasing cost per order P = unit cost I = inventory carrying cost per unit expressed as

a percentage of the period inventory value

The EOQ must balance the total carrying cost against the total ordering cost. Once the EOQ is determined, the reorder point must

be decided:

Reorder point = lead time x average inventory usage rate

E. Just-In-Time Production

Just-in-time (JIT) production describes a production system in which parts are only

produced as required in subsequent operations.JIT systems differ from conventional production

systems in that inventories of work-in-process, raw materials, and finished goods are minimized

or totally eliminated.

III. Property Accounting Applications

Fixed Assets Maintain adequate records

that identify assets with description cost, and physical

location. Provide for appropriate

depreciation and/or amortization calculations for

book and tax purposes. Provide for reevaluation for

insurance and replacement-cost purposes.

Provide management with reports for planning and controlling the individual

asset items.

InvestmentsA common control practice

with respect to the physical handling of

investment securities is to require two people to

be present when the firm’s safe deposit box or other depository is

entered.

IV. Quick-Response Manufacturing Systems

A. Defining Quick-Response Manufacturing Systems

B. The Physical Manufacturing System

C. The Manufacturing Resource Planning (MRP) System

D. MRP II versus MRP

E. Advanced Integration Technologies

F. Internal Control Considerations

G. Activity-Based Costing

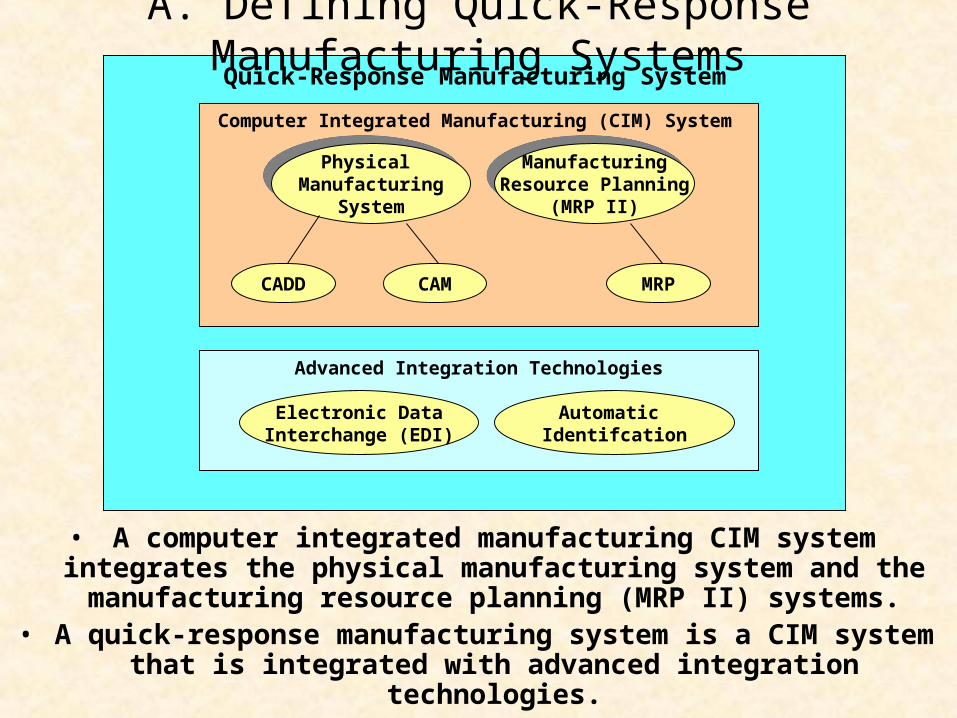

Quick-Response Manufacturing System

A. Defining Quick-Response Manufacturing Systems

• A computer integrated manufacturing CIM system integrates the physical manufacturing system and the manufacturing resource

planning (MRP II) systems.• A quick-response manufacturing system is a CIM system that is

integrated with advanced integration technologies.

Physical Manufacturing

System

Physical Manufacturing

System

CADD CAM

ManufacturingResource Planning

(MRP II)

ManufacturingResource Planning

(MRP II)

MRP

Computer Integrated Manufacturing (CIM) System

Electronic DataInterchange (EDI)

Automatic Identifcation

Advanced Integration Technologies

B. The Physical Manufacturing System

1. Computer-Aided Design and Drafting (CADD)

2. Computer-Aided Manufacturing (CAM)

1. Computer-Aided Design and Drafting (CADD)CADD uses computer software to

perform engineering functions.Designers can store product

designs on computer. These designs can be recalled and

manipulated as needed.Solids modeling is the

mathematical representation of a part as a solid object in computer

memory.Finite element analysis is a

mathematical model used to determine mechanical

characteristics, such as stresses of structures under load.

2. Computer-Aided Manufacturing (CAM)CAM systems are useful in

planning and obtaining feedback from the

manufacturing process.Statistical process control

considers whether process outputs are within

acceptable variations from engineering specifications.

A type of CAM known as a flexible manufacturing

system is a programmable production process that can be quickly reconfigured to produce different products.

There seems to be a problem with the stamping process.

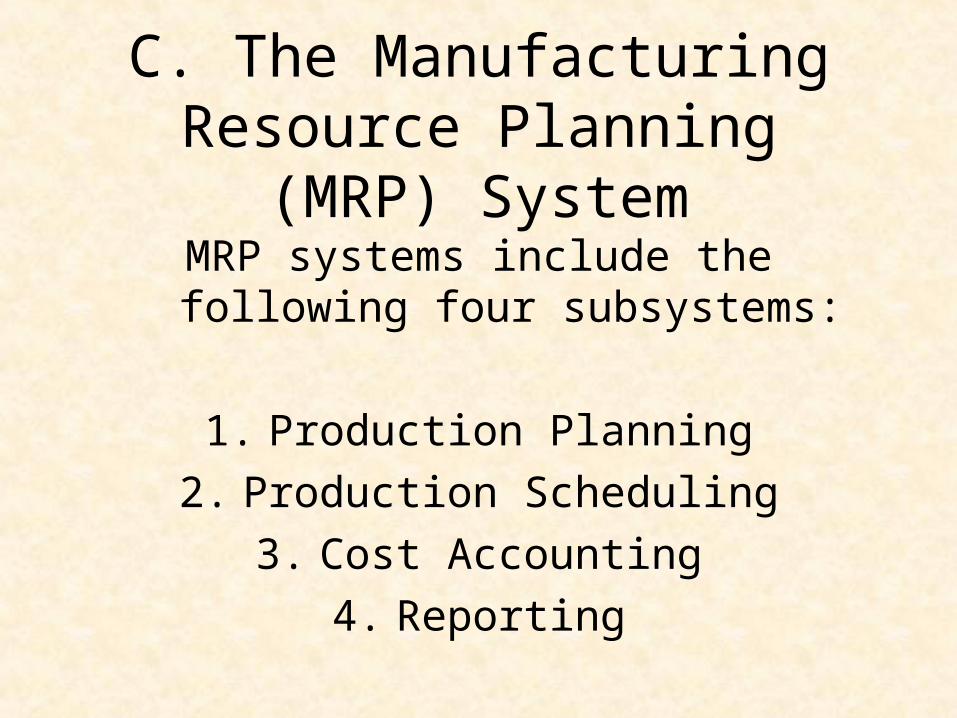

C. The Manufacturing Resource Planning (MRP) System

MRP systems include the following four subsystems:

1. Production Planning

2. Production Scheduling

3. Cost Accounting

4. Reporting

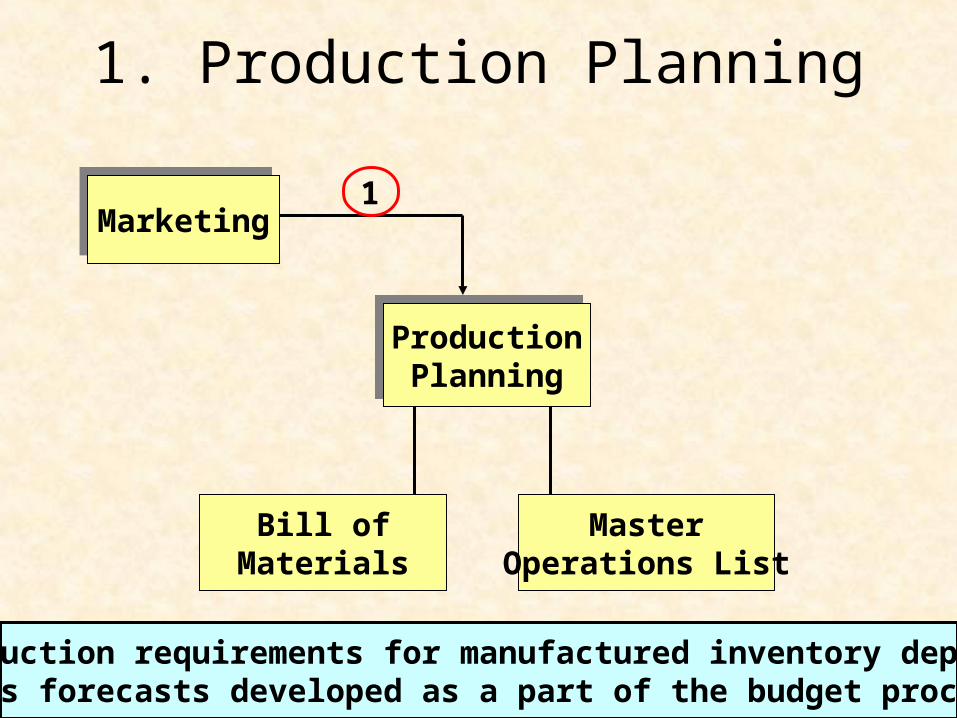

1. Production Planning

MarketingMarketing

ProductionPlanningProductionPlanning

1

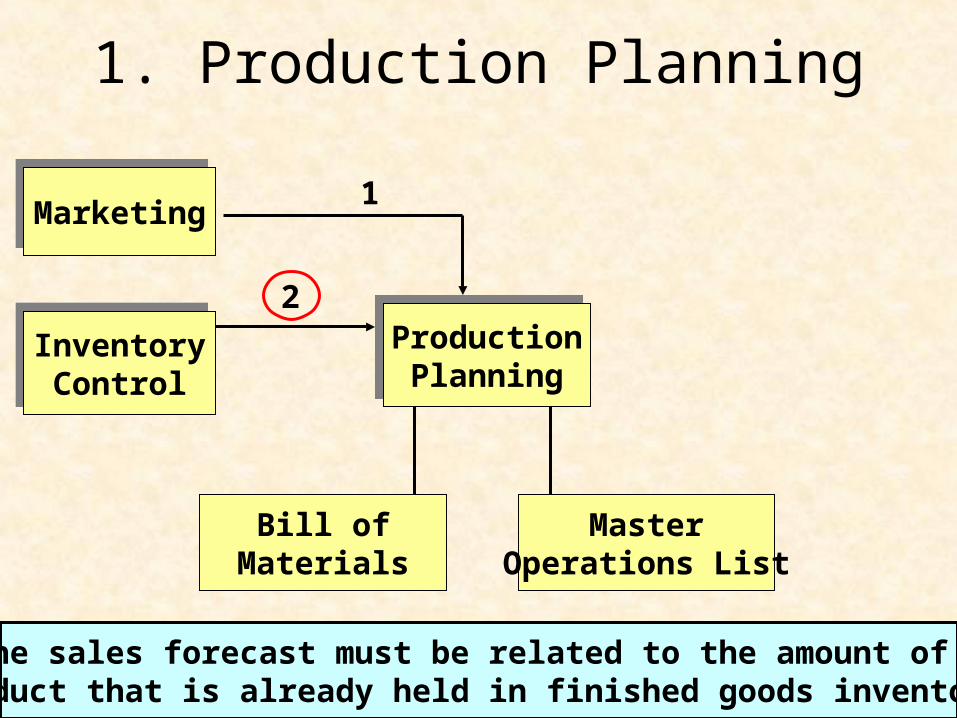

1. Production requirements for manufactured inventory depend on sales forecasts developed as a part of the budget process.

Bill ofMaterials

MasterOperations List

1. Production Planning

MarketingMarketing

ProductionPlanningProductionPlanning

1

2. The sales forecast must be related to the amount of eachproduct that is already held in finished goods inventory.

InventoryControlInventoryControl

2

Bill ofMaterials

MasterOperations List

1. Production Planning

MarketingMarketing

ProductionPlanningProductionPlanning

1

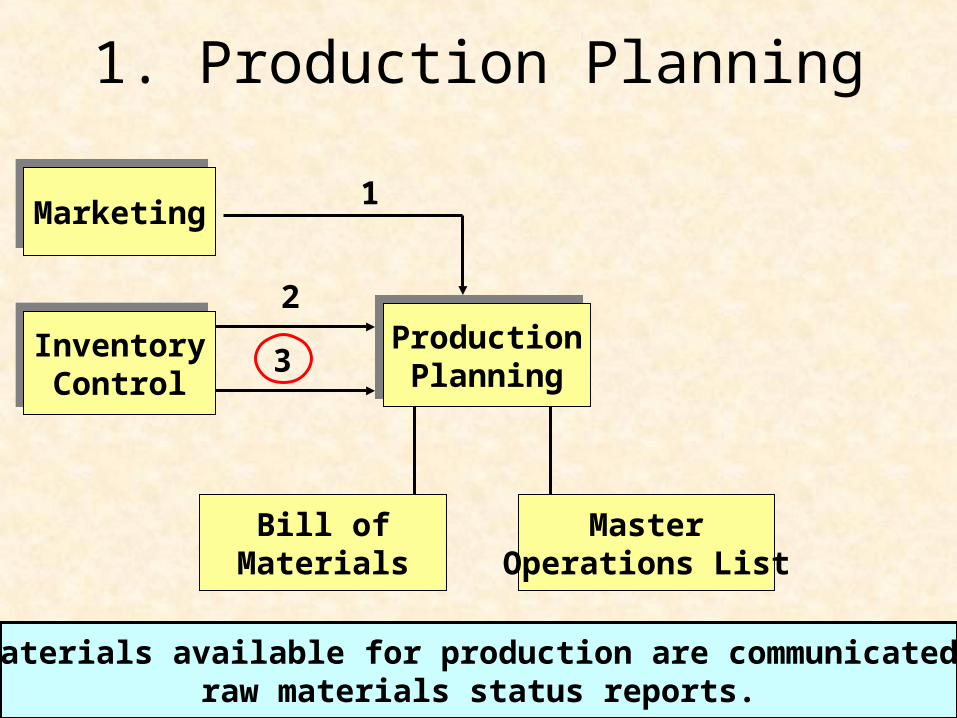

3. Raw materials available for production are communicated throughraw materials status reports.

InventoryControlInventoryControl

2

3

Bill ofMaterials

MasterOperations List

1. Production Planning

MarketingMarketing

ProductionPlanningProductionPlanning

1

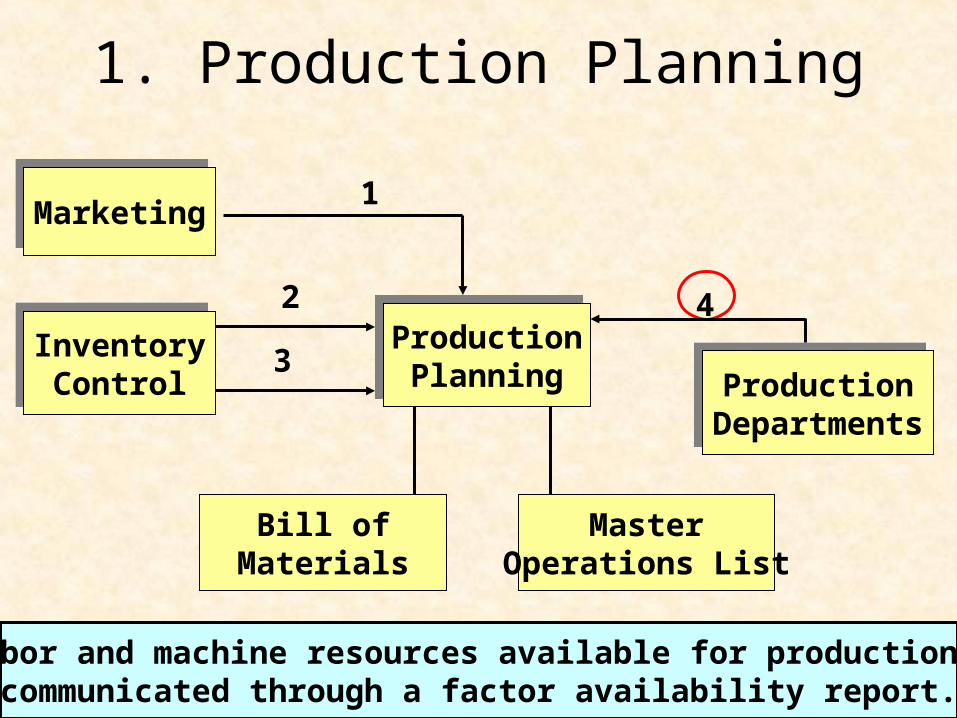

4. Labor and machine resources available for production are communicated through a factor availability report.

InventoryControlInventoryControl

2

3 ProductionDepartments

ProductionDepartments

4

Bill ofMaterials

MasterOperations List

1. Production Planning

MarketingMarketing

ProductionPlanningProductionPlanning

1

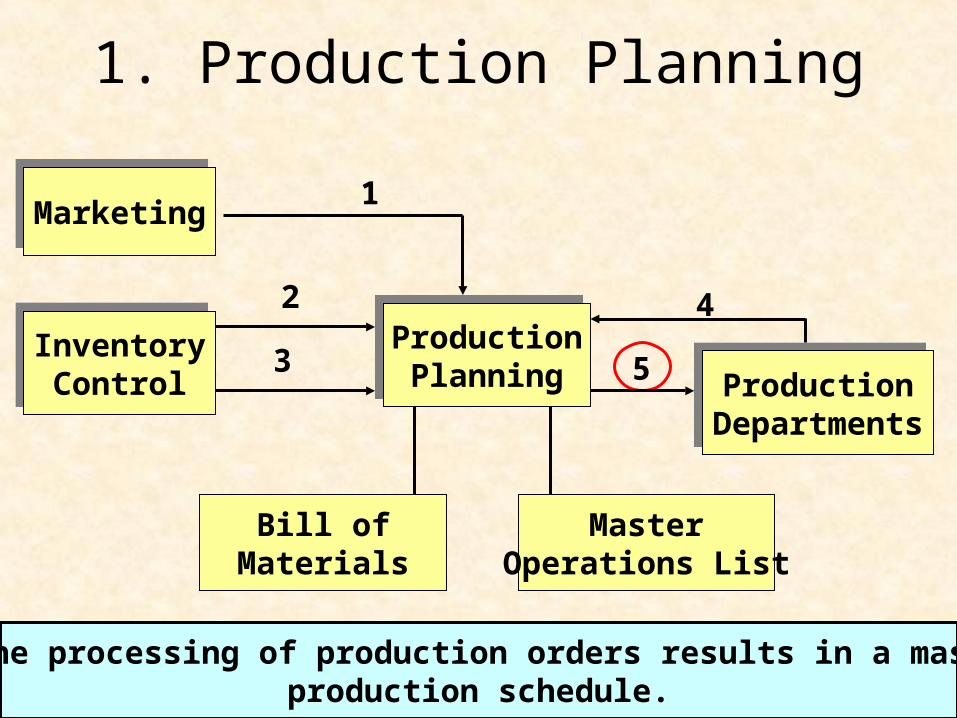

5. The processing of production orders results in a master production schedule.

InventoryControlInventoryControl

2

3 ProductionDepartments

ProductionDepartments

4

5

Bill ofMaterials

MasterOperations List

2. Production Scheduling

Routings (RTGs) indicate the sequence of operations required to manufacture a product and contain information about the work center, length of time, and tooling required

to perform each task.Each RTG contains a production order number. As tasks are completed information is input into the computer system

to update the production status file.A scheduling application program uses linear programming

and other techniques to determine the optimal assignment of available resources to production.

3. Cost Accounting

The central feature of the cost-accounting application

is the updating of the production-status (Work-

in-Process) file.As orders are completed, the related work-in-process

record is closed and a record is created to update the finished inventory file.

4. ReportingThe completed production-

order file lists all cost data for completed production

orders. Outputs of processing this file include an updated finished goods inventory file and a stock

status report.Variances between standard and actual costs are determined to assist in

control of production.

D. MRP II versus MRP

An MRP II system includes the major processing modules of MRP. Some extensions added with MRP II

include:Extensions to bill-of-materials processing might

include maintenance of engineering/product drawings from a CADD system.

Extensions to routings filings might include expanded information concerning work center capacity data and

maintenance of machine tooling data.

E. Advanced Integration Technologies

1. Automatic identification enhances integration

by putting machine-readable codes on products

and materials.

2. EDI enhances integration by integrating the

systems of suppliers and customers.

3. Distributed processing enhances integration by

combining geographically dispersed resources

into a single system.

F. Internal Control Considerations

In quick-response manufacturing systems, internal control can become a problem because transactions can be completed with no human intervention. Since it is not feasible to install

controls after implementation, controls must be implemented during systems design and

implementation .

G. Activity-Based Costing

CIM integrates the physical manufacturing system and manufacturing resource planning (MRP II) systems.

Activity-based costing (ABC) is particularly well suited to a CIM environment because

both ABC and CIM consider the processes that go into making a product, and

CIM’s use of technology results in a less labor-intensive manufacturing environment. This can

increase the need for more accurate overhead allocations.

SummaryProduction System Forms and ReportsThe Production Application System

Physical Manufacturing SystemMaterial Requirements Planning (MRP)

Advanced Integration TechnologiesInternal Control Considerations

Computer-Integrated Manufacturing and Activity-Based Costing