Chapter 8 Corporate Combinations: Corporate Law Aspects · Chapter 8 Corporate Combinations:...

62

1 Chapter 8 Corporate Combinations: Corporate Law Aspects Copyright 2013, Stanley Siegel NOTE: Corporate Law in this draft reflects developments only as of 2000 I. INTRODUCTION A.The Importance of Form. This chapter examines the formal requirements, imposed primarily by state corporation law, for effectuating corporate combinations. Perhaps surprisingly, these requirements vary widely not only among jurisdictions, but also between the forms of corporate combination. Any of numerous structures may be devised to carry out a corporate combination, all with essentially or exactly the same economic and substantive end results. However, the legal rules applicable to these structures, including approval and disclosure formalities as well as shareholder and creditor protections, will often vary widely. From the planning perspective, therefore, form may be all important. Business combinations are referred to by many names -- merger, combination, acquisition, purchase, pooling, etc. -- which have varying and often ambiguous meanings, dependent upon the context in which they are used. In the literature and in practice, the two sides of the transaction are also referred to by a variety of terms, including the buying and selling corporations, the surviving and disappearing corporations, or the acquirer and the target. The corporate laws impose occasionally similar, but more often different, requirements on the two sides of the combination transaction. The choice of the form of combination, and in many instances of some of the economic and substantive terms, will be affected by the likelihood of satisfying these requirements and the costs that must be incurred to do so. For example, when one

Transcript of Chapter 8 Corporate Combinations: Corporate Law Aspects · Chapter 8 Corporate Combinations:...

1

Chapter 8 Corporate Combinations: Corporate Law Aspects

Copyright 2013, Stanley Siegel

NOTE: Corporate Law in this draft reflects developments only as of 2000 I. INTRODUCTION A.The Importance of Form. This chapter examines the formal requirements, imposed primarily by state corporation law, for effectuating corporate combinations. Perhaps surprisingly, these requirements vary widely not only among jurisdictions, but also between the forms of corporate combination. Any of numerous structures may be devised to carry out a corporate combination, all with essentially or exactly the same economic and substantive end results. However, the legal rules applicable to these structures, including approval and disclosure formalities as well as shareholder and creditor protections, will often vary widely. From the planning perspective, therefore, form may be all important. Business combinations are referred to by many names -- merger, combination, acquisition, purchase, pooling, etc. -- which have varying and often ambiguous meanings, dependent upon the context in which they are used. In the literature and in practice, the two sides of the transaction are also referred to by a variety of terms, including the buying and selling corporations, the surviving and disappearing corporations, or the acquirer and the target. The corporate laws impose occasionally similar, but more often different, requirements on the two sides of the combination transaction. The choice of the form of combination, and in many instances of some of the economic and substantive terms, will be affected by the likelihood of satisfying these requirements and the costs that must be incurred to do so. For example, when one

2

form of transaction (such as a statutory merger) requires the vote of stockholders of both corporations, while an equivalent alternative (such as a sale of assets) requires the vote of the stockholders of only one, the choice of the latter may result in significant savings of time and money. That two transactions which are economically and functionally equivalent are treated differently by the law poses important questions for the legal system, but leaves little choice for the business planner who is intent upon carrying out the interests of his or her client. The choice of form will not turn entirely on the corporate law formalities and protections examined in this chapter. Additional issues, including accounting treatment, disclosure and reporting requirements imposed by the Securities and Exchange Commission or by state law, federal and state income tax treatment, and the requirements of loan agreements or other contractual commitments, may significantly affect the form and substance of the transaction. However, the corporate law requirements come first, both logically and operationally: if the transaction cannot be approved pursuant to state law, it obviously cannot be implemented. B.Voting. The first line of legal protection for stockholders is ordinarily the right to vote on a transaction, the requirement that the transaction be approved by a stated proportion of the shares as a condition to its implementation. As applied to corporate combinations, this requirement generally consists of three parts: approval of the transaction by the board of directors, notice and disclosure of the transaction to the stockholders, and approval by stockholder vote.1 The important issues of which transactions require stockholder approval, and which corporation's stockholders are enfranchised are discussed further below. Most state corporation laws now require only a majority vote of stockholders to approve a corporate combination or other major corporate transaction, but that majority is measured by the number of shares entitled to vote,2 not merely by the number present at the meeting or actually voting. Some state laws retain larger majority requirements for certain transactions, typically 2/3 1..Model Bus. Corp. Act § 11.03.

2..Model Bus. Corp. Act § 11.03(e) (merger); § 12.02(e) (sale of assets); § 14.02(e) (dissolution); § 10.03(e) (amendment of articles of incorporation).

3

majority for approval of a merger,3 and all permit the articles of incorporation to provide for a greater than majority voting requirement.4 An additional issue is posed when, by the terms of the articles of incorporation5 or the state corporation law,6 the shares of a particular class of stock are entitled to vote separately on a transaction. Typically, class voting rights are imposed by statute when the transaction affects, normally adversely, the rights of a particular class of shares; this issue is discussed further later in this chapter. Counting of votes can be illustrated by example: Example 1: The boards of directors of Apex, Inc. and Boulder Corp. have approved a plan of

merger providing for Boulder to be merged into Apex. The 10,000 outstanding shares of voting common stock of Apex will remain outstanding without change. Each of Boulder's 5,000 outstanding shares of voting common stock will be exchanged for one share of Apex common stock; and each of Boulder's 200 outstanding shares of non-voting preferred stock will be exchanged for 10 shares of Apex common stock. Under the Model Business Corporation Act, what votes will be required to approve the plan?

Approval of the Apex-Boulder merger requires a majority of the votes of each voting group entitled to be cast on the plan.7 Apex has only one voting group, common stock, and the required vote will therefore be 5,001 shares in favor. Note that since the statute requires an affirmative vote of a majority of those entitled to vote, failure to appear at the meeting or by proxy, or failure to vote altogether, is the equivalent of a negative vote on the plan. Boulder Corp. has two classes of stock outstanding, and therefore has two voting groups within the contemplation of the Model Business Corporation Act. If the preferred stock had by its

3..E.g., N.Y. Bus. Corp. L. § 903.

4..Model Bus. Corp. Act § 7.27.

5..Model Bus. Corp. Act §§ 7.25, 7.27.

6..Model Bus. Corp. Act § 11.03(f) (merger); § 10.04 (amendment of articles of incorporation).

7..Model Bus. Corp. Act § 11.03(e).

4

own terms been entitled to a class vote on the merger, the statute would have enforced that right.8 Absent such a provision, the preferred stock would appear to have no voting rights. However, the statute grants a class voting right when a provision in the plan of merger would trigger class voting if contained in an amendment to the articles of incorporation.9 A change of preferred stock into common stock, as provided by the Apex-Boulder merger plan, would require such a class vote if contained in an articles amendment,10 and therefore a class vote is required on the merger itself. The approval requirement for the Boulder stockholders is a majority affirmative vote of each class: 2501 common shares and 101 preferred shares. This conclusion, in the Apex-Boulder merger and most similar transactions, appears obvious and is supported by the Official Comment to the Model Business Corporation Act.11 However, had the Boulder preferred stock been voting stock ab initio, both the statute and its commentary would support a critically different conclusion. In that instance, the required vote would have been a majority of all voting shares counted in the aggregate, plus a majority of the preferred stock counted separately.12 Apart from problems of determining the necessary majority, the Apex-Boulder example illustrates a recurring planning issue common to all the forms of business combination. When a corporation has multiple classes of stock outstanding, the class voting requirement creates the potential for a veto power by one group of stockholders. Often, the affected class may be convinced to vote in favor of the transaction by offering a favorable exchange rate. (If the Boulder preferred indicates dissatisfaction with the merger, perhaps an exchange ration of 11 or 12 to 1 will

8..Model Bus. Corp. Act § 11.03(e). This section similarly enforces greater-than-majority voting

provisions included in the articles of incorporation.

9..Model Bus. Corp. Act § 11.03(f)(1).

10..Model Bus. Corp. Act § 10.04(a)(2).

11..Model Bus. Corp. Act § 7.26 (official comment).

12..Thus, if the Boulder preferred had been voting stock, the required vote could have been satisfied by a favorable vote of 2401 common and 200 preferred. The total favorable vote (2,601) is a majority of all voting stock (5,200 shares), and the preferred favorable vote (200) is a majority of the class entitled to a separate class vote. See Model Bus. Corp. Act § 7.26 (official comment).

5

achieve their favorable vote.) In some instances, the extra price is too great, and in others the class may simply vote "no" on any transaction. An alternate solution to the problem, discussed below, is to restructure the plan so that the Boulder preferred, and perhaps even the Boulder common, is denied the right to vote altogether. A variation on the voting process, allowed by every corporation statute, is approval by unanimous consent of the stockholders.13 Particularly when a corporation has relatively few stockholders, and when notice and a meeting would be inconvenient or impracticable, written consents may be distributed and collected to obtain and document the required stockholder approval. A few states have extended the consent procedure to non-unanimous approval. For example, in Delaware a transaction may be approved by majority consent and in fact implemented prior to notifying the non-consenting stockholders.14 In most instances, the questions of voting will relate only to stock, but this is not invariably the case. The Model Business Corporation Act does not allow bonds to vote,15 but voting debt is not unknown in many states.16 Moreover, even though debt generally carries no formal voting power, covenants limiting mergers, asset sales and other major corporate transactions are normally included in bond trust indentures and bank loan agreements. The effects of these contractual limitations are the same as a class vote: unless the bank or the bond trustee agrees with the merger, it cannot go through. The remedy of the ignored creditor in this situation is drastic, since breach of the bond covenant or the loan agreement normally allows the creditor to demand immediate payment of the entire debt. Therefore, the consent of major creditors will normally be required as a precondition to a corporate combination, whether or not they hold the formal right to vote. II. FORMS OF COMBINATION 13..See Model Bus. Corp. Act § 7.04.

14..Del. Gen. Corp. Law § 228.

15..Model Bus. Corp. Act § 7.21(a); see Official Comment.

16..See, e.g., Del. Gen. Corp. Law § 221.

6

A. The Nature of the Combination: Corporate combinations differ in both form and substance. The first step in analysis of a proposed business combination is determination of its substantive character: the economic, financial, control and other business aspects of the transaction. Important legal, tax and financial considerations turn on whether the combination is in the nature of an acquisition, purchase or buyout or, alternatively, whether it represents the combination or pooling of continuing businesses under combined ownership. Like many other dichotomies in law and finance, this distinction is sharp at the extremes and blurred at the borders. Compare the facts of Example 1 (page 3, above), involving the Apex-Boulder combination, with the following illustration: Example 2: The boards of directors of Cory, Inc. and Darwin Corp. have approved a plan of merger

providing for Darwin to be merged into Cory. The 250,000 outstanding shares of voting common stock of Cory (which trades publicly at about $25 per share) will remain outstanding without change. Each of Darwin's 20,000 outstanding shares of voting common stock will be exchanged for $8.50 cash. An alternative plan is under consideration pursuant to which each share of voting common stock would be exchanged for $10 face amount of 11% subordinated debentures.

It will be seen in the discussion below that both examples are true mergers, in the legal sense. But they are more different than similar. The Apex-Boulder combination of Example 1 involves the combination of two businesses of roughly similar size, in which stockholders of each will remain as stockholders of the combined enterprise. The Cory-Darwin combination of Example 2 represents, in substance, the buy-out of a small corporation by a much larger corporation. The former stockholders of Darwin receive only cash, and have no continuing interest in the combined enterprise. Even in the alternative plan, former Darwin stockholders become only creditors, rather than equity participants, in the surviving company. We may for ease of reference refer to the Apex-Boulder transaction as a true business combination or pooling of interests, by contrast with the Cory-Darwin transaction, which we may refer to as a purchase or buy-out. Many business combinations can readily be categorized as one or the other. However, a variety of more complex transactions pose difficult questions of characterization. How does one characterize an Apex-Boulder combination when the Boulder

7

stockholders immediately sell their newly-received Apex stock? What is the character of a transaction in which part of the consideration is stock and part is cash or debt? What importance should be attached to the relative sizes of the combining enterprises? These questions are not academic. The discussion in this and succeeding chapters will demonstrate that characterization of the transaction will determine the nature of the legal safeguards associated with it, the tax consequences to the parties to the transaction, and the nature of the financial reporting of the transaction. To complicate matters further, the characterization will vary in each context: legal, tax and financial reporting. B.Combinations in the Nature of Acquisition or Purchase: 1.Factors favoring purchase-type acquisitions. A variety of considerations may weigh in favor of a purchase-type acquisition, any one or several of which may be definitive: (a) Excess cash or inadequate leverage. A cash rich corporation will seek investment prospects for its excess funds, as opposed to seeking acquisitions in which further equity securities will be issued. Similarly, a corporation whose management seeks additional leverage might look for acquisitions funded by the issuance of debt, whether that debt is issued directly to the stockholders of the acquired company or is issued publicly to raise cash for acquisitions. The tender offer boom of the 1980's was financed largely with debt, with the direct effect of dramatically increasing the leverage of the acquiring companies. (b) Avoidance of equity dilution. Acquisitions in the nature of pooling invariably require the issuance of stock. To the extent that the newly-issued stock is voting, the result is dilution of the voting control of the stockholders of the acquiring company. And if the newly-issued stock participates fully in combined earnings (e.g., common stock), the additional issuance has a dilutive effect on earnings-per-share of the acquired company.17

17..This point is somewhat oversimplified. In fact, if the ratio of the earnings of the acquired

corporation to the number of shares issued in the acquisition exceeds the earnings-per-share of the acquiring corporation, then the post-acquisition earnings-per-share of the

8

(c) Presence of favorable market conditions for issuance of new debt. When market interest rates are low, and similarly when unsecured or subordinated corporate debt is readily marketable, it may be to the advantage of an acquisition-minded company to issue long-term low-interest debt for acquisition purposes. The low fixed charge represented by low interest rates has the combined effect of minimizing the company's risk and maximizing the advantages of leverage.18 (d) Simplified acquisition structure. The discussion below will demonstrate that cash and debt financed acquisitions tend to avoid most compliance requirements (vote, appraisal remedy, etc.) under state corporate law, at least with respect to the acquiring corporation. (e) Minimize of SEC and state disclosure and filing requirements. Similarly, negotiated (as opposed to hostile) cash or debt financed acquisitions may minimize, or in some instances avoid entirely, certain SEC and state registration, filing and disclosure requirements, at least with respect to the acquiring corporation. (f) Tax advantages to one or both corporations. It is possible, though not common, that a purchase-type transaction might produce tax advantages in the form of higher basis for depreciable assets or inventories, without any adverse tax consequences. It is more likely that the parties will find no major tax disadvantages to the purchase-type acquisition in certain circumstances. (g) Desire of one group of stockholders to sell out. Commonly, a major reason for the purchase-type acquisition is that all or a substantial portion of the stockholders of the selling

company will actually increase. However, had the acquisition been financed with cash or debt, the increase in earnings-per-share would normally have been greater.

18..Suppose that the assets to be acquired have an expected long-term return of 14% based on their purchase price, and the acquiring company can publicly issue long-term bonds with an effective interest rate of 8.5% to finance the entire acquisition. Purchase-type acquisition in this instance provides the company with a 5.5% "free" return (14% - 8.5%), with relatively low risk, since the return on the assets would have to drop dramatically before the interest on the debt was not covered. In periods of low market interest rates, corporate debt financing tends to increase dramatically.

9

corporation wish to discontinue their association, as both management and owners, with the enterprise. (h) Hostile acquisition. It is possible to structure a hostile takeover in the form of either a purchase or a pooling type acquisition, but the pooling is both economically and tactically impracticable in such acquisitions. Moreover, since most hostile acquisitions look to removal of the management of the target, stock ownership by the target stockholders in the acquiring company would be at least undesirable if not dangerous. Hostile acquisitions are almost invariably for cash, debt or a combination thereof. The discussion below, illustrating the forms of purchase-type acquisitions, will be based on a variation of the facts of the Cory-Darwin acquisition, discussed earlier, as follows: Example 3: The presidents of Cory, Inc. and Darwin Corp. have agreed in principle to a plan of

acquisition providing for Cory to acquire Darwin, or alternatively to acquire all the assets and assume all the liabilities of Darwin. The purchase price will be either $170,000 cash, or $200,000 of 11% subordinated debentures, or some combination thereof. Cory has outstanding 250,000 shares of common stock, which trade publicly at about $25 per share. Darwin has outstanding 20,000 shares of voting common stock, which is closely held.

2.Asset Purchase. The simplest form of acquisition, asset purchase for cash, debt, or a combination thereof, may be diagrammed as follows:

10

Cash & Debt Assets & Liabilities (a)The buying corporation. From the viewpoint of Cory, the transaction involves acquisition of assets and assumption of liabilities in return for cash, debt or a combination thereof. Every element of the transaction is within the authority of the board of directors. Therefore, no part of this transaction will require notice, meeting or vote of the stockholders of Cory, Inc. (b)The selling corporation. Since the transaction involves Darwin's disposition of all its assets and liabilities, it has two steps: (i) Sale by Darwin to Cory of the assets, coupled with assumption by Cory of the liabilities, in exchange for stock, debt or a combination thereof; and (2) Probably, dissolution of Darwin and distribution of the proceeds of sale to its stockholders. The second step might not be part of the plan were Darwin to dispose of only a portion of its assets (such as an unwanted plant) and reinvest the proceeds. When the disposition involves all the assets, however, it is likely that the selling corporation will dissolve and distribute its assets. A corporation may normally dispose of a portion of its assets, even if the disposition is extraordinary, on the basis of approval by the board of directors. Corporation laws requiring

Cory, Inc.

Darwin Corp.

11

stockholder approval of sales of assets are invariably limited to those outside the normal course of business and comprising substantially all the assets. For example, the Model Business Corporation Act explicitly grants the board of directors, without stockholder approval, the authority to sell or otherwise dispose of all assets within the usual and regular course of business and to mortgage all assets whether or not in the usual and regular course of business.19 Moreover, the Model Act by both explicit statutory inclusion and negative implication excludes from the stockholder approval requirement sales of less than substantially all the assets.20 The Delaware decision excerpted below indicates, however, that the determination of "substantially all" may not always be a simple question. In any event Darwin's asset sale would under most state corporation statutes require board approval, notice to stockholders, and a majority vote of the stockholders entitled to vote,21 for approval of the transaction.22 Moreover, most states grant the right of appraisal to voting stockholders who elect to dissent from the transaction, although the Model Act denies appraisal when the sale is entirely for cash and the proceeds of sale are distributed within one year after the date of the sale.23 The operations of the appraisal remedy, and the problems occasioned by its application, are discussed later in this chapter. KATZ v. BREGMAN Delaware Court of Chancery 431 A.2d 1274 (c)Dissolution following the sale. 19..Model Bus. Corp. Act § 12.01. Provisions of this general substantive import are to be found

in nearly all contemporary state corporation statutes.

20..Model Bus. Corp. Act § 12.01 (official comment), § 12.02.

21..See the discussion of voting, earlier in this chapter, for discussion of how the majority is calculated.

22..Model Bus. Corp. Act § 12.02.

23..Model Bus. Corp. Act § 13.02 (a)(3).

12

Should Darwin elect to dissolve, it will be required to follow the statutory dissolution procedure, which invariably requires resolution of the board of directors, notice to stockholders, and majority affirmative vote of the voting stockholders.24 An interesting question is occasionally posed: does a stockholder vote authorizing dissolution automatically authorize sale of all assets? The Model Business Corporation Act appears to answer the question in the affirmative,25 but nevertheless preserves the appraisal remedy for dissenting stockholders unless the asset sale is for cash and the proceeds are distributed within one year.26 Dissolution is not a mere mechanical process. The Model Business Corporation Act, like all other corporation statutes, requires that claims against the corporation be discharged or that provision be made for their discharge.27 Failure to do so will occasion director and potential stockholder liability.28 Normally, in a Cory-Darwin type of acquisition, when the liabilities of a small corporation are assumed by a larger (and presumably more credit-worthy) corporation, creditors will accept assumption of their obligations as satisfactory provision. But this is not inevitable, and in some instances (including bank loans and mortgages), separate assumption provisions or even discharge of the debt may be required.

24..This procedure is detailed in Model Bus. Corp. Act § 14.02. Note that no class vote is

required for dissolution, since it is assumed that each class will receive its portion of the proceeds of liquidation in accordance with its interests. See Model Bus. Corp. Act § 14.05 (a)(4). If the plan of dissolution calls for a class of stock (e.g., preferred) to receive anything other than its rights as set forth in its terms, the plan will be treated as including an amendment of the articles of incorporation changing the rights, preferences or limitations of such shares. Such an amendment requires a class vote of the affected shares. Model Bus. Corp. Act § 10.04(a)(4).

25..Model Bus. Corp. Act § 14.05(a)(2) authorizes "disposing of its properties that will not be distributed in kind to its shareholders."

26..Model Bus. Corp. Act § 13.02(a)(4) extends the appraisal remedy to sales of all or substantially all the assets other than in the usual and regular course of business "including a sale in dissolution."

27..Model Bus. Corp. Act §§ 14.05(a)(3), 14.06 (known claims), 14.07 (unknown claims).

28..See Model Bus. Corp. Act §§ 6.40, 8.33.

13

In summary: (i) The purchase by Cory requires only board approval, whatever the terms of the transaction; (ii) The sale by Darwin will require majority stockholder approval, whether solely as a sale or as a sale coupled with dissolution. If the sale is for cash alone, and the cash is distributed within one year, no appraisal remedy will apply. But if all or part of the consideration consists of debt or other consideration, the appraisal procedure will be applicable. 3. Stock Purchase. The purchase of stock often has quite different effects from the purchase of assets. The transaction can be diagrammed as follows: Step 1 Step 2 Darwin Corp. 100% Stock Cash & Debt Stock Ownership Darwin Corp. Stockholders

(a)The buying corporation. From the viewpoint of Cory, the stock acquisition (like the asset acquisition discussed above) involves only the acquisition of assets (in this case, stock of another corporation) in return for cash, debt or a combination thereof. Every element of the transaction is within the authority of the board of directors. Therefore, no part of this transaction will require notice, meeting or vote of the

Cory, Inc.

Cory, Inc.

Darwin Corp.

14

stockholders of Cory, Inc. (b)The acquired corporation. From the viewpoint of Darwin, the transaction is a non-event. The Darwin Corp. takes no action to effect this transaction. Rather, the Darwin Corp. stockholders choose to give up their shares of stock in return for cash or debt. Thus, no vote or appraisal remedy is applicable. However, the Darwin Corp. stockholders must "vote with their feet," by electing to exchange their shares in return for the proffered consideration. If some of the stockholders are unwilling to accept, or are too lazy to send in their shares, or cannot be found, Cory might find itself owning less than all of the stock of Darwin. That result might be acceptable, or if unacceptable might be remediable by one of the techniques to be discussed later in this chapter.29 But the risk of an unacceptable result, and the potential costs of remedying it, render the stock-purchase transaction less desirable except in situations where the stock is held by few owners and all have evidenced in advance the desire to accept the deal. In some states, this difficulty in the stock-purchase transaction has been eliminated by the adoption of "share exchange" provisions in the state corporation law. These provisions, generally designed for share exchange mergers, are discussed in detail later in this chapter. At least some statutory provisions of this type would also be usable to achieve a stockholder-voted mandatory share purchase.30 After the first step in the transaction, assuming complete success, Darwin will be a wholly-owned subsidiary of Cory, as shown in step 2 of the diagram. An optional third step is available: dissolution of the acquired subsidiary. Although dissolution must be authorized by stockholder vote, Cory as the only stockholder of Darwin will be able to assure a favorable outcome of that vote should it desire to cause Darwin's dissolution.

29..These include short merger and freeze-out merger.

30..See Model Bus. Corp. Act § 11.02, which in subsection (b) permits the consideration for the share exchange to be cash or other property. Under this provision, a majority vote of the stockholders of Darwin could authorize a mandatory exchange of all Darwin stock for cash to be paid by Cory. See Model Bus. Corp. Act § 11.03(b).

15

In many if not most instances of stock acquisition, however, the wholly-owned subsidiary will not be dissolved, since there will be several important business advantages to retaining the separate subsidiary. Indeed, a principal reason for undertaking a stock acquisition (as opposed to an asset acquisition or a merger) is to assure retention of the acquired subsidiary. Primary among the advantages are the insulation of the acquiring corporation from the debts of the subsidiary. In only the rarest of cases will courts apply the doctrine of "lifting the corporate veil" to hold an acquiring parent corporation liable for the debts of an acquired subsidiary. Particularly when the subsidiary is engaged in liability-intensive activities (involving, for example, the risk of environmental disaster or product liability), retention of the subsidiary may be a critical element of the acquisition plan. Similarly, if the acquired corporation has significant contingent liabilities, the acquiring corporation can be most effectively protected against them by retaining the subsidiary. Retention of the subsidiary may also avoid the need to retitle property, pay various transfer taxes, renegotiate contracts and franchises and obtain new licenses, all of which would likely be attendant upon an asset acquisition or merger. Of course, there can be no assurance that some or all of these procedures will not be required; in any acquisition, the process of due diligence examination will unearth contract, filing or compliance problems that may or may not be avoided by choice of form. A further and not insignificant virtue of retention of the subsidiary may be preservation of certain favorable tax attributes. This issue is discussed in the next chapter. In summary: (i) The stock purchase plan has the considerable advantage of retaining the separate corporate structure of the acquired corporation; (ii) The stock purchase by Cory requires only board approval, whatever the terms of the transaction; (iii) The sale by Darwin stockholders requires no stockholder vote as such, but requires the more unwieldy process of convincing the Darwin stockholders to turn in their shares in return for cash; (iv) In some states, the problem of convincing the stockholders to turn in their shares has been statutorily solved by enactment of mandatory share exchange statutes. 4.Cash Merger.

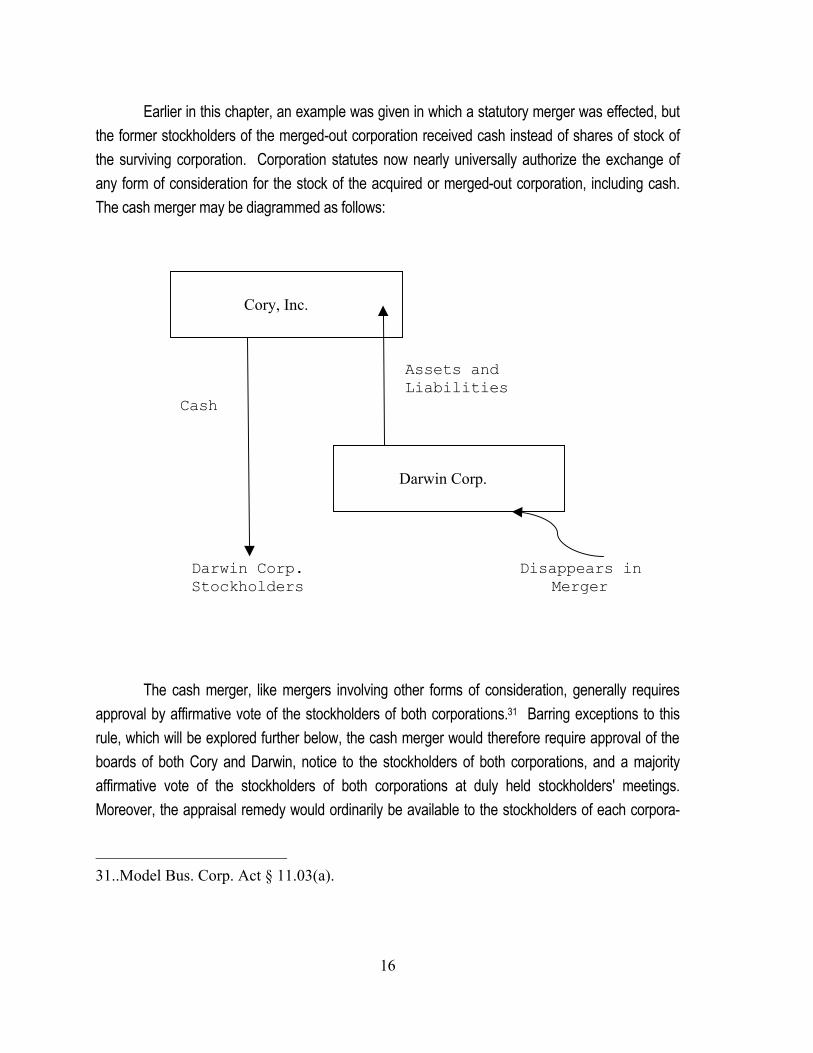

16

Earlier in this chapter, an example was given in which a statutory merger was effected, but the former stockholders of the merged-out corporation received cash instead of shares of stock of the surviving corporation. Corporation statutes now nearly universally authorize the exchange of any form of consideration for the stock of the acquired or merged-out corporation, including cash. The cash merger may be diagrammed as follows: Assets and Liabilities Cash Darwin Corp. Disappears in Stockholders Merger The cash merger, like mergers involving other forms of consideration, generally requires approval by affirmative vote of the stockholders of both corporations.31 Barring exceptions to this rule, which will be explored further below, the cash merger would therefore require approval of the boards of both Cory and Darwin, notice to the stockholders of both corporations, and a majority affirmative vote of the stockholders of both corporations at duly held stockholders' meetings. Moreover, the appraisal remedy would ordinarily be available to the stockholders of each corpora-

31..Model Bus. Corp. Act § 11.03(a).

Cory, Inc.

Darwin Corp.

17

tion who are entitled to vote on the plan of merger.32 The immediate question is then why such a plan would be considered, if its substantive effects can so readily be achieved by other plans not requiring a vote of both corporation's stockholders. The answer to this question lies in the mechanical operation of the statutory merger. First, it should be noted that when the constituent corporations are both closely held, it is often a minor matter to obtain approval of both groups of stockholders. Second, although the process of approval may be rendered more complex as a result of two stockholder votes, the implementation of a statutory merger is often simpler than the other acquisition or combination methods. A statutory merger automatically transfers title to all assets, and obligations on all liabilities, to the surviving corporation.33 No conveyances, title changes, notices to creditors or similar documents are necessary. Generally, the statutory merger form is more advantageous in pooling-type mergers as opposed to cash mergers. In practice, the statutory authorization to use cash as consideration in a merger is most widely used in two settings: (i) Cash is occasionally used either as partial consideration or as optional consideration for the shares of the merged-out corporation; (ii) The cash merger is widely used as a squeeze-out device in hostile acquisitions. Both of these uses are further described later in this chapter. In summary: (i) A cash merger of Darwin into Cory would normally require board approval, notice and stockholder vote by the stockholders of both corporations; (ii) The appraisal remedy would normally be available to the stockholders of both corporations; (iii) In return for these approval formalities, the merger offers considerably simplified implementation of the actual acquisition. 5.Multi-corporate variations: triangles and drop-downs. Mergers, like many other corporate transactions, may be used as components of larger multi-part business plans. In its simplest form, the multi-party merger involves the merger of the 32..Model Bus. Corp. Act § 13.02(a)(1). The appraisal remedy is discussed further later in this

chapter.

33..Model Bus. Corp. Act § 11.06(a)(2), (3).

18

acquired corporation into an existing or newly-created subsidiary of the acquiring corporation. Such a "triangular" cash merger may be diagrammed as follows:

19

Step 1 100% Stock Ownership Cash Assets and Liabilities Darwin Corp. Stockholders Merged into Cory Acquisition, Inc. Step 2 100% Stock Ownership

Cory, Inc.

Cory Acquisition, Inc.

Darwin Corp.

Cory, Inc.

Cory Acquisition, Inc.

20

The use of multi-party mergers (in both purchase and pooling type transactions) developed in response to the need to achieve certain results not obtainable by traditional combination or acquisition forms.34 Suppose that in the Darwin-Cory example it were essential to insulate Darwin from Cory's contingent product liabilities. Neither an asset acquisition nor a merger of Cory into Darwin would achieve this result. Suppose, too, that a significant minority of Cory's stockholders would simply not turn in their stock if offered cash in exchange. Therefore, Darwin would be faced with the Hobson's choice of either assuming all contingent liabilities or acquiring less than 100% of Cory.35 Use of the triangular cash merger in this setting would effectively satisfy all of Darwin's objectives. Since the transaction would take the form of a merger, a majority vote of Cory's stockholders would bind all of them. And since Cory would merge not into Darwin, but into a newly-formed subsidiary, its liabilities would never attach to Darwin. Authority to effectuate multi-party mergers appears in most state corporation laws in the description of the consideration permitted to be exchanged for the acquired corporation's stock. For example, the Model Business Corporation Act states that the plan of merger must set forth: "the manner and basis of converting the shares of each corporation into shares, obligations, or other

securities of the surviving or any other corporation or into cash or other property in whole or in part."36

The consideration, whether cash, shares or other property, may therefore flow from any corporation.

34..Asset acquisitions and stock acquisitions can similarly be effected through subsidiary

corporations. All of these forms can, as well, involve more than three corporations. To set some practical limits on the discussion, only three-party ("triangular") mergers are diagrammed and evaluated. Similar considerations apply to multi-party asset and stock acquisitions and to transactions involving additional entities.

35..This dilemma no longer exists in states that have adopted mandatory share-exchange provisions. See, e.g., Model Bus. Corp. Act § 11.02, discussed later in this chapter.

36..Model Bus. Corp. Act § 11.01(b)(3).

21

In the diagram, the merger occurs between Darwin Corp. and Cory Acquisition, Inc., the latter having been formed by Cory, Inc. for the specific purpose of the acquisition. And though Darwin is merged into Cory Acquisition, Inc. the consideration flows from Cory, Inc. An interesting side-effect of the triangular merger is that in most states it effectively eliminates the voting rights and the appraisal remedy of the parent corporation's stockholders (Cory, Inc., in the diagram). Note that the required stockholder vote is of the merging corporations, and in the diagram those are Darwin and Cory Acquisition. Since Cory Acquisition is a wholly-owned subsidiary of Cory, Inc., its shares are voted by Cory, Inc. And since Cory, Inc. is not merging with another corporation, its stockholders do not vote on the transaction.37 Moreover, since the appraisal remedy with respect to corporate mergers is in most states granted only to stockholders entitled to vote on the transaction,38 it is also denied to the stockholders of Cory, Inc. in the triangular merger. A variation on the theme of the triangular merger is the corporate acquisition followed by a "drop down" into a newly-formed or existing subsidiary of the acquiring corporation. The acquisition can take any form, asset acquisition, stock acquisition39 or statutory merger. Immediately following the acquisition, all or part of the acquired assets and liabilities are transferred to the subsidiary in exchange for all or a part of the subsidiary's stock.40 37..A few states by statute reject this analysis, and provide voting rights and the appraisal

remedy to the stockholders of a parent corporation whose subsidiary is a party to a triangular merger. See Cal. Gen. Corp. Law §§ 1200, 1201, requiring board and shareholder approval by the corporation in control of any constituent or acquiring corporation, the "parent party."

38..See Model Bus. Corp. Act § 13.02(a)(1). The appraisal remedy is discussed further later in this chapter.

39..Normally, a drop down is not required following a stock acquisition, since the acquired assets remain in a separate corporation. However, in some instances a portion of the assets of the newly-acquired corporation may be dropped down to yet another corporation to achieve further separation of ownership and liabilities.

40..This "drop down" of assets and liabilities will ordinarily be a tax-free transfer pursuant to IRC § 351(a). Details of the tax aspects of this transaction are discussed in the next chapter.

22

The drop-down has the advantage of insulating the acquiring corporation from future liabilities of the subsidiary. It has the disadvantage, relative to the triangular merger, that preexisting liabilities (including contingent and unasserted claims) attach to the acquiring corporation as of the acquisition. The subsequent dropping down of the assets does not relieve the acquiring company of ultimate liability on those claims. In summary: (i) Preservation of the separate corporate status of the acquired corporation, particularly when the share exchange cannot be effectively carried out, can be achieved by means of a triangular merger; (ii) A triangular merger of Darwin into a subsidiary of Cory would normally require stockholder vote only by the stockholders of Darwin; (iii) The appraisal remedy would normally be available only to the stockholders of Darwin; (iv) An alternative to the triangular merger, offering insulation only with respect to post-acquisition liabilities, is the asset purchase or cash merger followed by a drop-down of the acquired business or assets into a newly-formed subsidiary. 6. Hostile acquisition: the freeze-out merger. The preceding section illustrated the use of the multi-corporate (triangular) merger to achieve the results of a 100% stock acquisition while avoiding vote and appraisal by the acquiring corporation's stockholders. The same mechanism and the same diagram demonstrate that the multi-corporate merger can be used effectively as part of a plan to achieve a hostile takeover. Example 4: Suppose that Cory, Inc. decides to acquire all the stock of Darwin Corp., but that a

significant minority (40%) of the Darwin stockholders are unwilling to part with their shares at any price. Cory purchases 60% of the Darwin stock for cash from those stockholders who are willing to sell. What should be the next step?

One approach to the problem is a statutory merger of Darwin Corp. into Cory, Inc. As noted earlier in this chapter, the merger would require a majority vote of the stockholders of both corporations, and the appraisal remedy would be available to both groups of stockholders. Since Cory now owns a majority of the stock of Darwin, a favorable vote by the Darwin stockholders on the merger is a foregone conclusion.41 And the appraisal remedy results only in payment of cash to 41..Issues of fairness and business purpose, which may affect the terms of the merger, are

discussed later in this chapter.

23

dissenting stockholders, a result that was desired by Cory from the beginning. The statutory merger may not be the ideal answer to the problem, for the reasons discussed earlier in this chapter. It may be essential, for liability protection and other business purposes, to preserve the separate corporate status of Darwin following the acquisition. An alternative mechanism that achieves this objective would be the triangular merger. As step 1, Cory would establish a new subsidiary, Cory Acquisition, Inc., and transfer to it the previously acquired 60% of the stock of Darwin in return for 100% of the Cory Acquisition stock. Step 2 would be a cash merger of Darwin into Cory Acquisition, Inc., under the terms of which all remaining outstanding shares of Darwin Corp. would receive cash. The freeze-out is complete: Cory, Inc. now owns 100% of the stock of Cory Acquisition, Inc., which in turn is (as a result of the merger) the successor to all the assets and liabilities of Darwin. An important added virtue of the triangular merger, in this as in other settings, is that it can be achieved in most states without the vote or appraisal remedy of the stockholders of the parent corporation. An elegant variation on the freeze-out theme, the freeze-in merger, has been used to solve the problem of the reluctant preferred stockholders. This subject is discussed and illustrated in the section of this chapter on fairness. 7.Partial acquisitions: "thinning down" the acquired corporation. Not infrequently, the acquiring corporation wishes to obtain some, but not all, of the assets or business of another corporation. The simplest method of achieving this goal in many instances is to acquire a portion of the assets for cash. If the acquired business or assets pose potential liability problems, the acquisition can be made by a newly-created subsidiary of the acquiring corporation, into which sufficient cash has been transferred to finance the transaction. Alternatively, the transaction may be structured as a stock acquisition or as a triangular merger. The unwanted assets or business must then be disposed of, either before, concurrent with or after the acquisition. The process of "thinning down" the acquired corporation poses no unique corporate problems, since the sale or disposition of a portion of the corporation's assets will generally be within the discretion of the board of directors.42 The transaction may, however, pose 42..Model Bus. Corp. Act § 12.01.

24

interesting tax questions, which are discussed in the next chapter. C.Combinations in the Nature of Pooling: 1. Factors favoring pooling-type combinations. A variety of considerations may weigh in favor of a pooling-type combination, any one or several of which may be definitive: (a) Minimizing of cash drain. Pooling-type combinations are invariably effected through issuance of all or a substantial part of the consideration in the form of stock of the surviving corporation. Cash drain in the transaction is therefore limited to the legal, accounting and other costs of effecting the arrangement, plus any periodic dividend payments the board may make on the newly-issued stock after the acquisition. By contrast, the purchase acquisition will normally involve either direct cash payment for the acquired assets or stock, or mandatory dividend and principal payments on debt issued as part of the acquisition price. (b) Continuation of both managements and ownership interests. It is often in the interests of the parties to retain all or part of the existing management and ownership structure of the combining companies. Under these circumstances, combination by issuance of stock is generally the preferred approach. (c) Tax advantages. In many, if not most, instances, important tax advantages can be secured by using the pooling-type acquisition. These include avoidance of tax on the gain resulting from exchange of stock and securities in the transaction, as well as retention of certain desirable tax attributes of the constituent corporations. These tax considerations are discussed in the next chapter. (d) Accounting and reporting issues. Prior to revision of the accounting standards for business combinations, the required accounting disclosure for purchase-type transactions was considered undesirable by the business community. Under current standards, acquisition accounting requires that the acquirer restate the value of acquired assets and liabilities. The restatement of asset values often results in the creation of a substantial goodwill account on is

25

books. Details of this accounting treatment are discussed in the next chapter.43 (e) Creation of a broader public market for corporate securities. Quite commonly, a small publicly- or privately-held corporation merges with a larger publicly-held corporation with a major objective being to achieve broader public ownership and a more readily ascertainable market value for the shares held by the owners of the smaller company. (f) Presence of favorable market conditions for issuance of new stock. A strong stock-market condition for equity securities means that newly-issued stock will have maximum value (and therefore minimum dilutive effect). In such circumstances, particularly when coupled with high interest rates (rendering issuance of debt undesirable), stock-financed combinations tend to be favorable. The discussion below, illustrating the forms of pooling-type combinations, will be based on a variation of the facts of the Apex-Boulder combination, discussed earlier in this chapter, as follows: Example 5: The presidents of Apex, Inc. and Boulder Corp. have agreed in principle to a plan of

combination pursuant to which Boulder's assets and liabilities, or Boulder's stock, will be acquired by Apex; alternatively Boulder will be merged into Apex. The plan provides for the 10,000 outstanding shares of voting common stock of Apex to remain outstanding unchanged. Each of Boulder's 5,000 outstanding shares of voting common stock will receive one share of Apex voting common stock; and each of Boulder's 200 outstanding shares of non-voting preferred stock ($100 per share liquidation preference) will receive 10 shares of Apex voting common stock.

43..Much was made in the financial press about the relative advantages of pooling accounting

over purchase accounting. Whether the accounting differences were so consequential as to affect the form of the deal was never clear. Contemporary financial theorists are in agreement that the differences have no effect on the stock market.

26

2.Stock-for-Assets: The stock-for-assets combination involves the issuance by the acquiring corporation of stock (or a combination of stock and other consideration) in return for the assets of another corporation. In most instances, the liabilities of the other corporation are assumed in the same transaction, and in most instances the newly-issued stock and other consideration is distributed in liquidation of the selling corporation. This combination, like others to be discussed in this section of this chapter, is often referred to by reference to the section of the Internal Revenue Code that governs qualification for tax-free reorganization status. The stock-for-assets combination is governed by section 368(a)(1)(C), and is commonly known as a "C Reorganization." It can be diagrammed as follows: Step 1 Step 2 Apex Assets and Dissolved Stock Liabilities Apex Stock Boulder Corp. Stockholders

Apex, Inc.

Apex, Inc.

Boulder Corp.

Boulder Corp.

27

(a) The buying corporation. From the viewpoint of Apex, the transaction involves acquisition of assets and assumption of liabilities in return for newly-issued stock and -- possibly -- other consideration. If the articles of incorporation of Apex authorize a sufficient number of shares of the appropriate class or classes, the transaction on its face will be entirely within the authority of the board of directors and will not require notice, meeting or vote of the stockholders of Apex. Often, corporations in the position of Apex do not have sufficient authorized shares. Moreover, if a portion of the consideration is to be other than common stock, it may be necessary to authorize the additional class unless series authorization is already included in the articles of incor-poration.44 Authorization of additional shares, or of a new class of shares, requires amendment of the articles of incorporation, a process that will require resolution of the board of directors, notice to stockholders, and an affirmative majority vote on the amendment at a stockholders' meeting.45 Additionally, if the shares to be authorized carry rights or preferences with respect to distribution or dissolution that are prior, superior or substantially equal to those of an already outstanding class, that class will be entitled to vote separately on the transaction,46 pursuant to the procedure outlined earlier in this chapter. The notice to stockholders and the request for their vote on the amendment will clearly be proxy materials within the meaning of Section 14 of the Securities Exchange Act and the regulations thereunder. Among the material items required to be disclosed in the notice, apart from the terms of 44..The Model Business Corporation Act, like many recently revised corporation statutes, allows

inclusion in the articles of incorporation of a provision permitting the board of directors to designate the rights, preferences and limitations of any class or series before issuance thereof. See Model Bus. Corp. Act § 6.02. Acquisition minded corporations often include such a provision in their articles of incorporation, coupled with an ample authorization of preferred stock, to provide flexibility in future acquisitions or stock flotations.

45..Model Bus. Corp. Act §§ 6.01, 10.03.

46..Model Bus. Corp. Act § 10.04(a)(6).

28

the proposed amendment, will be any plans that the corporation is presently considering for issuance of the newly-authorized stock. In other words, if Apex must seek stockholder approval for authorization of additional shares, the required approval will in practical effect be not only of the authorization, but also of the acquisition in which the shares are to be issued. All of these considerations suggest strongly the importance of advance planning in the drafting of the articles of incorporation. Sufficient authorization of shares, together with series preferred authorization, will eliminate the need for any stockholder vote by Apex, except in the unlikely event of the application of the de facto merger doctrine, discussed further below. (b)The selling corporation. The procedures that must be followed by Boulder as the selling corporation are similar to those that were described earlier (with respect to Darwin Corp.) to authorize an asset sale for cash. The rights available to Boulder's stockholders and creditors may be somewhat different. The sale will be a disposition of all or substantially all the assets of Boulder, and will therefore require board approval, notice to stockholders, and a majority vote of the stockholders entitled to vote.47 Although Boulder has two classes of stock outstanding, the preferred stock is by its terms non-voting, and state corporation laws generally do not grant a statutory class vote on sale of assets. However, the Model Business Corporation Act, like many but not all state corporation laws, grants the appraisal remedy to stockholders dissenting from the sale.48 And in the case of the sale for stock, as opposed to a sale for cash followed by prompt distribution thereof,49 no exception to the appraisal remedy is granted. Boulder will also require authorization of dissolution and distribution of the stock received as consideration for the sale. The required procedure for dissolution -- board approval, notice to stockholders, and majority affirmative vote of the voting stockholders50 -- can be combined with the 47..Model Bus. Corp. Act § 12.02.

48..Model Bus. Corp. Act § 13.02(a)(3).

49..Ibid.

50..Model Bus. Corp. Act § 14.02.

29

vote to approve the asset sale. Again, no class vote is granted by statute to the Boulder preferred stockholders. In dissolution, however, each class of stock is entitled to receive proceeds in accordance with its terms.51 Therefore, upon dissolution the Boulder preferred stock would be entitled to $20,000 cash (200 shares x $100 per share liquidation preference). However, the proposed terms of the transaction call for Boulder to receive 7,000 shares of Cory common stock, and no cash, in exchange for its assets.52 It will therefore be necessary, as part of the plan, for Boulder to amend its articles of incorporation, changing the liquidation preference of the outstanding preferred stock from $100 cash per share to the sale consideration that will be distributed in liquidation: 10 shares of Apex common stock. This amendment will require a class vote of the Boulder preferred stock, since it changes the "designation, rights, preferences, or limitations" of the preferred stock.53 Thus, the stock-for-assets plan requires of the selling corporation three votes: (i) approval of the sale; (2) amendment of the articles changing the preferred stock liquidation preference; and (iii) approval of dissolution. The votes may, and should, be combined and made contingent upon approval of all simultaneously.54 The result of the combined votes will be that the Boulder stockholders will effectively have a class vote on the transaction, plus an appraisal remedy. (c)The problem of reluctant preferred stockholders. The preferred stockholders of Boulder may be unwilling to vote in favor of the plan. This problem may be solved in several ways. The most obvious and simple solution is to offer the preferred stock greater consideration, perhaps 11 or 12 shares of Apex common stock in return for 51..See Model Bus. Corp. Act § 14.05(a)(4).

52..The amount of stock to be issued by Cory in the acquisition can be calculated from the exchange ratios agreed to by the presidents of the two corporations, as follows:

5,000 common x 1 share each = 5,000 shares 200 preferred x 10 shares each = 2,000 shares Total 7,000 shares

53..Model Bus. Corp. Act § 10.04(a)(4).

54..See Goldman v. Postal Telegraph, Inc., 52 F. Supp. 763 (D.C. Del. 1943) (Delaware law), in which these three steps were combined successfully and were upheld by the court.

30

each preferred share. The plan might, however, still be unacceptable to the preferred stockholders. Moreover, the shifting of consideration to the preferred stockholders might be so great as to make the plan unacceptable to the common stockholders.55 It may in some instances be feasible to adopt a plan under which the common stock receives new common stock of the acquiring corporation, while the preferred stock receives cash equal to its liquidation preference. Since this plan would not change the liquidation preference of the preferred stock, they would have no vote on the plan whatever. But this plan has a number of serious problems, one of which is that the entire plan almost certainly will not qualify for advantageous tax-free reorganization treatment.56 Moreover, this plan calls for the preferred stock to be paid its full liquidation preference, which may in fact be greater than its value.57 Finally, in some instances the required cash payment may strain the cash resources of the acquiring company. Alternatively, the acquisition may be modified to provide that the preferred stock of Boulder will receive in the exchange identical preferred stock of Apex. Since in that case the terms of the preferred stock would be unchanged (though it would be stock in a different corporation) it might be possible to avoid a preferred stock class vote on the transaction.58 This approach has the possibly

55..The total consideration to be issued to Boulder (in Apex stock, cash or any other form) is a

function Apex's view of the value of Boulder. That value is independent of allocation of the consideration among the classes of Boulder stock. Therefore, increasing the consideration to one class of Boulder stock will correspondingly decrease the consideration to the other.

56..See Internal Revenue Code §§ 368(a)(1)(c), 368(a)(2)(B). This issue is discussed in detail in the next chapter.

57..On the other hand, particularly if the preferred stock carries a high dividend rate, its liquidation preference may be lower than its value. Indeed, in some instances it will be desirable to cash-out the preferred stock (possibly by pre-acquisition redemption by the issuing corporation) before the plan is implemented.

58..This point is not perfectly clear, and is not addressed directly by any corporation statute. For example, none of the statutory grants of class voting in Model Bus. Corp. Act § 10.04(a) applies to exchange of preferred stock for identical preferred stock of another corpora-tion. Moreover, if the stock issued in exchange is stock of a corporation with a greater asset base -- normally the case following a corporate combination -- the rights of the new

31

undesirable feature of leaving the Boulder preferred stock outstanding, retaining its full liquidation preference and its priority in dividends. Yet another alternative is to stand the transaction on its head: let Apex sell its assets to Boulder. Since the purchasing corporation requires no stockholder approval of the transaction (unless approval is required to authorize the stock to be issued), no vote will be required of any Boulder stock, common or preferred. This "reverse sale" strategy is also useful when it is difficult to obtain approval by the common stockholders of one of the combining corporations. Like other strategies, it too is not without problems. One difficulty is that the Boulder preferred stock remain outstanding under this plan. Another is that the reverse sale is a prime candidate for "de facto merger" treatment, as discussed below. (d)The de facto merger doctrine. The stock-for-assets combination, coupled as it almost invariably is with dissolution of the selling corporation, generally has exactly the same effects as a statutory merger. However, both voting procedures and appraisal rights are more extensive in mergers than in stock-for-assets combinations. The most important distinction is, in general, the denial of voting rights and the appraisal remedy to stockholders of the surviving corporation in a stock-for-assets combination. Another difference present in some jurisdictions is a lower vote requirement (generally majority) for authorization of sale of assets than for a merger (often two-thirds). The reasons underlying these statutory distinctions are unclear. They may, indeed, have had their origins in a drafting oversight, failure to foresee the use of the asset-sale authorization to achieve the results of a merger. Whatever the reasons for the differences, they led to widespread use of the stock-for-assets combination as a device to avoid the need for a stockholder vote and appraisal remedy for one group of stockholders. And, as suggested earlier in this chapter, occasionally the sale was reversed, so that the actual selling corporation became the putative purchasing corporation, and its stockholders were denied the vote.59

preferred stock are likely effectively superior to those of the stock it replaced. Cf. Dalton v. American Investment Co., 490 A.2d 574 (Del. Ch.), aff'd, 501 A.2d 1238 (Del. 1985), excerpted later in this chapter.

59..The most famous instance of such a transaction, and possibly the impetus for creation of the

32

The status of these transactions was occasionally contested by disenfranchised stockholders of the "buying" corporation. They sought, and occasionally obtained, voting and appraisal rights based on the theory that the transaction was, in fact, a merger. The "de facto merger" doctrine has been accepted in some cases60 and a few statutes, but rejected by many jurisdictions either in litigation or in legislation. In many jurisdictions, its status remains unclear. The Delaware and Pennsylvania decisions excerpted below demonstrate both judicial and legislative grounds for rejection of the doctrine. The excerpts of the California General Corporation Law represent the most expansive statutory enactment of the doctrine's underlying theory: that all reorganizations in whatever form should be subject to the same statutory requirements and protections. In summary: (i) The purchase by Apex requires only board approval, unless Apex has insufficient authorized shares; (ii) If Apex has insufficient authorized shares, or if the de facto merger doctrine is applicable by statute or case law, the full transaction will require board resolution, notice to stockholders, and majority stockholder approval; (iii) The sale, dissolution and distribution by Boulder will require majority stockholder approval and a class vote of the preferred stock, and will create an appraisal remedy for dissenting stockholders; (iv) A variety of techniques, with varying degrees of desirability, may be utilized to avoid a class vote or, if necessary, to disenfranchise the Boulder shareholders entirely. HARITON v. ARCO ELECTRONICS, INC. Delaware Court of Chancery, 1982 40 Del.Ch. 326, 182 A.2d 22 affirmed 41 Del.Ch. 74, 188 A.2d 123(1963) TERRY v. PENN CENTRAL CORP. United States Court of Appeals, Third Circuit, 1981

doctrine at least as it applies to stockholder rights, is Farris v. Glen Alden Corp., 393 Pa. 427, 143 A.2d 25 (1958). The subsequent history of the Farris doctrine in Pennsylvania is discussed in Terry, excerpted below.

60..See, e.g., Rath v. Rath Packing Co., 257 Iowa 1277, 136 N.W.2d 410 (1965).

33

668 F.2d 188 3.Stock-for-stock; share exchange: The stock-for-stock combination involves the issuance by the acquiring corporation of stock (or a combination of stock and other consideration) in return for the stock of another corporation. Since stock, rather than corporate assets, is acquired, the transaction takes place between the acquiring corporation and the stockholders of the acquired corporation. This combination is often referred to by reference to the section of the Internal Revenue Code that governs its qualification for tax-free reorganization, section 368(a)(1)(B). The transaction is therefore commonly known as a "B Reorganization." It can be diagrammed as follows: Step 1 Step 2 Apex Boulder 100% Stock Stock Stock Ownership Boulder Corp. Stockholders

Apex, Inc.

Apex, Inc.

Boulder Corp.

34

(a)The buying corporation. From the viewpoint of Apex, the stock-for-stock combination bears strong similarities to the stock-for-assets combination discussed above. Thus, if Apex has sufficient authorized shares of the necessary classes, and if the de facto merger doctrine is not applied to the transaction,61 the entire transaction can be effected solely on the basis of approval by the Apex board of directors. Two important differences distinguish the process of acquisition of stock the process of acquisition of assets. The first is that since the acquisition of shares is made from individual stockholders rather than the corporation, the acquisition can -- and in many instances must -- be made piecemeal by individual negotiations and purchases.62 The timing, as well as the price and other purchase terms, may vary among stockholders. The second difference turns on the requirements for qualification of the transaction as a tax-free reorganization. Central to these qualifications, which will be discussed in detail in the next chapter, is acquisition of "control" by means of the exchange solely of voting stock.63 Thus, if reorganization qualification is desired, as it often will be, the form of consideration permissible in the acquisition will be sharply limited. Issuance of non-voting stock, debt, cash or other consideration will disqualify the transaction for reorganization treatment. Moreover, the "control" test is severe: it requires ownership of 80% of the voting stock plus 80% of all other shares of stock of the acquired corporation.64 Therefore, in the Apex-Boulder transaction, Apex would be required to own 80% of both the common and the preferred stock of Boulder to meet the control test. (b)The exchanging shareholders. 61..For an example of application of the de facto merger doctrine to a stock-for-stock

acquisition, see Applestein v. United Board & Carton Corp., 60 N.J. Super 333, 159 A.2d 146 (Ch.), aff'd per curiam, 33 N.J. 72, 161 A.2d 474 (1960).

62..The strategy of slowly aggregating the controlling shares of stock by piecemeal acquisition is frequently referred to as a "creeping B reorganization."

63..Internal Revenue Code § 368(a)(1)(B).

64..Internal Revenue Code § 368(c).

35

From the viewpoint of Boulder, the transaction -- like the cash acquisition of shares discussed earlier in this chapter -- is a non-event. It is the Boulder Corp. stockholders who choose to give up their shares of stock in return for Apex common stock. Thus, no vote or appraisal remedy is applicable. However, if qualification of the transaction for reorganization status is to be achieved, 80% of both the common and the preferred stockholders of Boulder must elect to exchange their shares in return for Apex common stock. While partial success in the analogous cash acquisition of shares might be acceptable, the threshold for partial success in the share-for-share exchange will therefore ordinarily be 80%. (c)The statutory share exchange. It was noted earlier in this chapter that this difficulty in the stock-purchase transaction has in some states largely been eliminated by the adoption of "share exchange" provisions in the state corporation laws. These provisions operate similarly to state law requirements for sale of assets. Thus, under the Model Business Corporation Act a share exchange must be approved by the boards of directors of both corporations, but approved by an affirmative majority vote of the shareholders of only the corporation the shares of which will be exchanged in the transaction.65 A class vote by each class of shares exchanged is mandatory.66 As applied to the Apex-Boulder transaction, the Model Act provision would require majority approval of both the Boulder common stock and the Boulder preferred stock, since the plan calls for both classes to be exchanged for Apex common stock. The requirement of class voting, which grants an effective veto power to the preferred stockholders, poses familiar problems. Achieving the required class vote may require advance discussion and negotiation with the preferred stockholders. It may be necessary to offer them a more favorable exchange ratio in order to obtain their vote. It may, in some instances, simply be impossible to obtain their vote, in which case an alternative plan of combination may have to be considered.

65..Model Bus. Corp. Act §§ 11.02, 11.03(a).

66..Model Bus. Corp. Act § 11.03(f)(2).

36

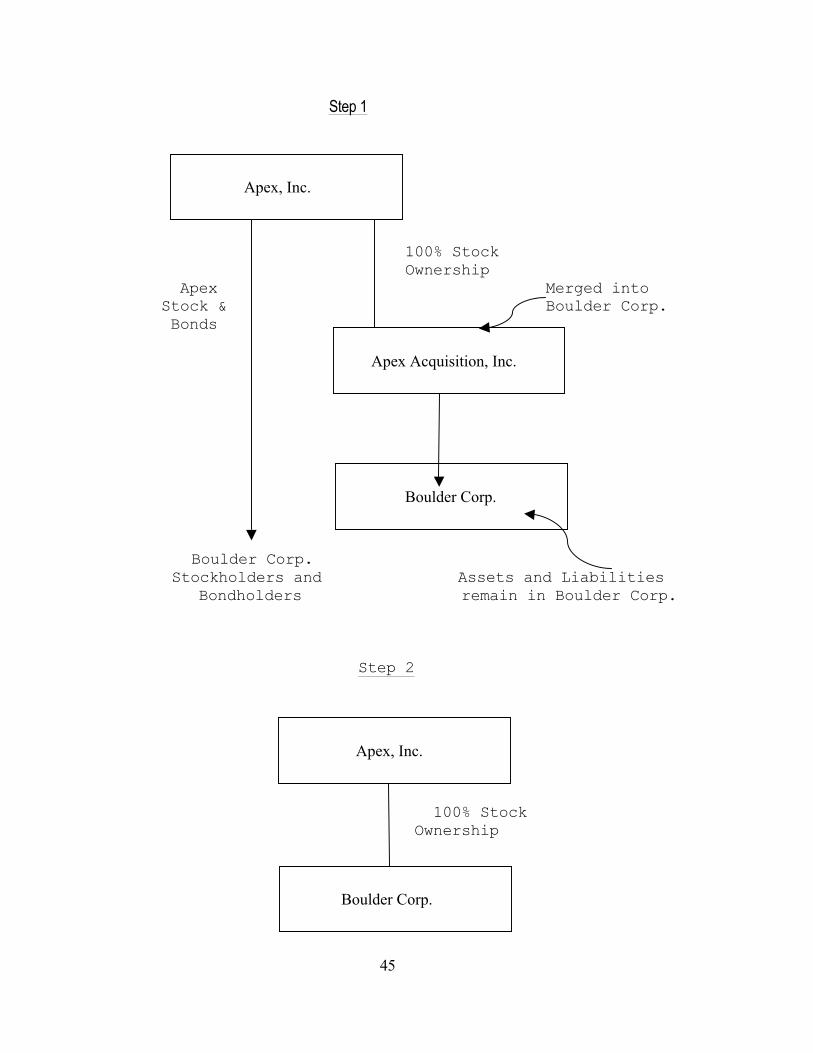

Following stockholder approval, the statutory share exchange is self-executing. The shares are deemed exchanged whether or not they are in fact tendered in return for new certificates, and they are treated thereafter as though they are the shares which were approved for exchange pursuant to the plan.67 The Model Business Corporation Act also grants appraisal to shareholders dissenting from the share exchange,68 thereby granting them effectively the option to receive cash in the exchange.69 (d)Dissolution or merger of the acquired corporation. Earlier in this chapter, the reasons for retention of the acquired corporation as a wholly-owned subsidiary were detailed. These included protection against existing and contingent liabilities, minimization of transfer formalities, and preservation of desirable tax attributes. Despite these advantages of maintaining the separate corporate status of the acquired corporation, there may be instances when dissolution of the acquired corporation -- or merger of that corporation into the parent or a subsidiary of the parent -- may be desirable.70 One such situation results from the acquisition (obviously not by means of statutory share exchange) of less than all the stock of the subsidiary. If it is undesirable or unacceptable to leave a minority outside interest in the subsidiary outstanding,71 a further step will be required.

67..Model Bus. Corp. Act § 11.06(b).

68..Model Bus. Corp. Act § 13.02(a)(2).

69..The exercise of the appraisal remedy may threaten qualification of the transaction as a reorganization under Internal Revenue Code § 368(a)(1)(B). This problem will be discussed in the next chapter.

70..A stock acquisition followed by a dissolution or a merger of the acquired subsidiary is likely to be characterized for tax purposes as an acquisition of assets; the implications of this recharacterization are discussed in the next chapter.

71..Among the reasons why the minority interest might be unacceptable are the following: (i) sufficient minority ownership to require continued compliance with the reporting requirements of the 1934 Securities Exchange Act; (ii) minority shareholder rights of inspection of corporate books under state law; (iii) minority objections to, and possible litigation over, corporate transaction that favor the parent.

37

The further step would normally have as its objective cashing out the minority stockholders. Dissolution of the subsidiary corporation probably cannot achieve this objective, since the minority shareholders may properly complain that it is impermissible in dissolution to convey the business to one group of shareholders (the majority, parent corporation) and cash to another.72 Merger of the subsidiary in any of various forms, including short merger and triangular merger, will however effectively eliminate the minority and generally be immune from judicial attack except on grounds of fairness. These techniques are discussed below. In summary: (i) The stock-for-stock exchange has the considerable advantage of retaining the separate corporate structure of the acquired corporation; (ii) The exchange by Apex requires only board approval, unless Apex has insufficient authorized shares; (iii) If Apex has insufficient authorized shares, or if the de facto merger doctrine is applicable by statute or case law, the full transaction will require board resolution, notice to stockholders, and majority stockholder approval; (iv) The exchange of shares by Boulder stockholders requires no stockholder vote as such, but requires the more unwieldy process of convincing them Darwin stockholders to turn in their shares in return for Apex stock; (v) In some states, the problem of convincing the stockholders to exchange their shares has been statutorily addressed by enactment of mandatory share exchange statutes, but these will generally require a class vote and grant appraisal remedies to the Boulder stockholders. 4.Statutory Merger: The statutory merger, which qualifies for reorganization treatment in accordance with § 368(a)(1)(A) of the Internal Revenue Code, is widely known as an "A" Reorganization. It can be diagrammed as follows:

72..See, e.g., Kellogg v. Georgia-Pacific Paper Corp., 227 F. Supp. 719 (W.D. Ark., 1964).

38

Apex All Assets and Stock & Bonds Liabilities Boulder Corp. Stockholders & Bondholders Disappears in Merger

(a)General statutory provisions applicable to the stockholders of the merging corporations. The statutory merger generally requires resolution of the boards of directors, notice to the stockholders, and approval by affirmative vote of the stockholders of both corporations.73 A class vote will be required on the plan of merger if it contains a provision that, if contained in an amendment to the articles of incorporation, would require a class vote.74 The term of the proposed Apex-Boulder merger calling for the exchange of Boulder preferred stock for Apex common stock would be such an amendment,75 and therefore a class vote of the Boulder preferred stock will be required to authorize the merger. Moreover, the appraisal remedy will ordinarily be available to the

73..Model Bus. Corp. Act § 11.03(a).

74..Model Bus. Corp. Act § 11.03(f)(1).

75..See Model Bus. Corp. Act § 10.04(a)(2) -- exchange of the shares of one class into shares of another class.

Apex, Inc.

Boulder Corp.

39

stockholders of each corporation who are entitled to vote on the plan of merger.76 The formal aspects of merger approval appear more onerous than the procedures required for other functionally equivalent forms of corporate combination. As a result, some corporate combinations have been, and continue to be, implemented by means of these alternative forms. However, a number of arguments may be made in favor of the statutory merger. It was noted earlier in this chapter that when the merging corporations are both closely held, obtaining approval of both groups of stockholders often presents no problem. And, since the statutory merger automatically transfers title to all assets, and obligations on all liabilities, to the surviving corpora-tion,77 no conveyances, title changes, notices to creditors or similar documents are necessary to implement the plan. More importantly, qualification of a statutory merger for reorganization treatment for tax purposes is considerably easier than qualification of the alternative forms of corporate combination. The statutory merger allows the surviving corporation to issue a broader range of permissible consideration (such as nonvoting stock, debt and other consideration) while preserving reorganization treatment. These advantages are further discussed in the next chapter. (b)Statutory elimination of the vote of stockholders of the surviving corporation. Despite its advantages, the statutory merger would likely have remained an unfavored form of corporate combination were it not for two relatively recent developments. The first has already been introduced in this chapter, and is discussed further below: the triangular or multi-party merger. The second, also of great importance, is statutory enactment of the no-vote merger. The no-vote merger, now part of the corporation statutes of many states, reflects what a reading of this chapter should make obvious: parties considering a corporate combination are not limited to the often onerous voting and appraisal requirements of a statutory merge. The same or equivalent results can be achieved by asset and stock acquisitions, for cash, stock or other consideration. And nearly all of these alternative approaches can be implemented without a vote of the stockholders of the surviving corporation. 76..Model Bus. Corp. Act § 13.02(a)(1). The appraisal remedy is discussed further later in this

chapter.

77..Model Bus. Corp. Act § 11.06(a)(2), (3).

40