Chapter 7 MARKETING OF PUBLIC ISSUES -...

31

189 CHAPTER-VII MARKETING OF PUBLIC ISSUES Issue management by merchant bankers mainly focuses on three basic functions viz, origination, underwriting and distribution of securities. Distribution services of lead managers include the activities and cost incurred in selling and delivering the securities to the investors. Along with performing the function as a bridge between the issuing company and the investors, merchant bankers also have to generate interest and build the confidence of the investors in the capital market. So distribution is a function of sale of securities to the ultimate investors. This service, managed by lead manager, is performed by brokers and dealers in securities who maintain regular direct contact with the ultimate investors. Merchant bankers make efforts for the promotion and marketing of the issue. They plan, co-ordinate and control the entire activities relating to public issues and direct different agencies to contribute to the successful marketing of securities. In India, lead managers do not own an issue before its distribution to general public. They simply underwrite and arrange the distribution through the underwriters. The liberalization and globalization of Indian capital market has widened the geographical and demographical range of investors. Now, issuing companies call the applications for their shares not only from domestic investors, but from the foreign investors. Similarly, efforts are on to include every strata of society in the list of investors. Advancement of technology in communication and data processing has posed a new challenge for the merchant bankers in the area of marketing of public issues. Today, merchant bankers need top care about being in the centre of ‘information flow’ rather than in the centre of ‘capital flow’. The present chapter aims to study the responsibilities of lead merchant bankers regarding marketing of public issues, SEBI Guidelines on public issue advertisement and the response of the investors for the public issues of equity and debt instruments during the period under review. 7.1 Market Design of Public Issues The market design of public issues is provided in the provisions of the Companies Act, 1956. It deals with the issue, listing and allotment of securities. In addition to this, SEBI Disclosures and Investor Protection Guidelines, 2000 as

Transcript of Chapter 7 MARKETING OF PUBLIC ISSUES -...

189

CHAPTER-VII

MARKETING OF PUBLIC ISSUES

Issue management by merchant bankers mainly focuses on three basic

functions viz, origination, underwriting and distribution of securities. Distribution

services of lead managers include the activities and cost incurred in selling and

delivering the securities to the investors. Along with performing the function as a

bridge between the issuing company and the investors, merchant bankers also have to

generate interest and build the confidence of the investors in the capital market. So

distribution is a function of sale of securities to the ultimate investors. This service,

managed by lead manager, is performed by brokers and dealers in securities who

maintain regular direct contact with the ultimate investors. Merchant bankers make

efforts for the promotion and marketing of the issue. They plan, co-ordinate and

control the entire activities relating to public issues and direct different agencies to

contribute to the successful marketing of securities. In India, lead managers do not

own an issue before its distribution to general public. They simply underwrite and

arrange the distribution through the underwriters.

The liberalization and globalization of Indian capital market has widened the

geographical and demographical range of investors. Now, issuing companies call the

applications for their shares not only from domestic investors, but from the foreign

investors. Similarly, efforts are on to include every strata of society in the list of

investors. Advancement of technology in communication and data processing has

posed a new challenge for the merchant bankers in the area of marketing of public

issues. Today, merchant bankers need top care about being in the centre of

‘information flow’ rather than in the centre of ‘capital flow’.

The present chapter aims to study the responsibilities of lead merchant bankers

regarding marketing of public issues, SEBI Guidelines on public issue advertisement

and the response of the investors for the public issues of equity and debt instruments

during the period under review.

7.1 Market Design of Public Issues The market design of public issues is provided in the provisions of the

Companies Act, 1956. It deals with the issue, listing and allotment of securities. In

addition to this, SEBI Disclosures and Investor Protection Guidelines, 2000 as

190

amended from time to time prescribe a series of disclosures about the issuing

company, management, promoters, project, risk factors and eligibility norms for

accessing the market.

7.1.1 Responsibilities of Lead Manager(s) in Marketing of Public Issue

The process of marketing of securities in primary market starts with the

preparation of prospectus. The success of public issue depends upon the excellent

marketing techniques worked out by the lead manager. It covers the institutional and

retail distribution capacity, equity research capability, retail distribution network,

advertising strategies and international distribution capability. A general standardized

methodology of marketing may not be ideal for all issues. It may be worked out on a

case to case basis depending on the nature of public issues in hand.

The responsibilities of lead merchant banker(s) for marketing of public issues

may be summarized as under:

(i) Deciding the time of floating the issue

Timing of the public issue is an important decision taken by lead manager. It

is an important marketing strategy and is a futuristic decision which involves the

expected market conditions during the time of the issue. It is very strategic decision to

determine the right time for the public issue.

The main considerations with lead manager for deciding the time of issue

include the present and probable future market conditions, research reports by

financial analysts, clashing with mega issues, major economic and political events in

the country and response of the investors to recent public issues. In the words of

Ritter, “Marketing timing ability of (lead manager) is manifested in the tendency for

firms to issue after high market returns and before low market returns.”1

(ii) Appointment of Printers for issue stationery

The printers are involved in the process of printing and distribution of issue

related stationery. Merchant bankers maintain a list of approved printers and the

company in consultation with the lead manager appoints printer after considering the

cost and quality of service. Lead merchant banker is responsible to ensure the printing

of prospectus, application forms, posters, brochures and other stationery. It must

ensure itself the accuracy of statements made and application form and confirm that

the prospectus is as per standard prescribed by the stock exchange. 1. Ritter, Investment Banking and Securities Issuance.

191

Main functions of the printer include the layout and design of the offer

document, application form, printing of prospectus, application form, brochures etc.

However, nowadays, a copy of the offer document is placed on the website of lead

managers and syndicate members associated with the issue. A copy of prospectus is

also made available on the website of SEBI.

(iii) Dispatch and Distribution of Issue Material

It is the duty of lead manager that the public issue offer document and other

issue related material is dispatched to the designated stock exchange(s), brokers,

underwriters, bankers to the issue etc. in advance as agreed upon. In case of rights

issue, lead manager must ensure that the abridged letter of offer is dispatched to all

shareholders at least three days before the date of opening of the issue.

(iv) Appointment of Advertising Agency

However sound the project is or the promoters of the issuer company are, the

success of the public issue can be attributed to the advertising agency and its

campaign for marketing the issue. Merchant bankers maintain a list of advertising

agencies having experience and expertise in the publicity of public issues. Normally,

merchant bankers call upon various agencies to make a presentation on their

advertising and publicity strategy. Based on their presentation and further

consultation, the advertising agency is selected. The Company decides on the size of

the advertising budget in consultation with the lead manager. Then the advertising

agency and lead manager draw up a publicity campaign.

(v) Publicity Campaign

The selected advertising agency is responsible for carrying on publicity

campaign for wide distribution of public issue. It covers the preparation of all

publicity material including prospectus, brochures, announcements, advertisements in

the media, hoardings etc. Lead merchant banker plays a key role by helping the choice

of media, determining the size and the publication in which the advertisement should

appear. Along with print media, audio-visual media, hoardings, banners, posters,

publicity campaign may also be carried through the followings:

(a) Road Shows

As a part of the marketing campaign, the issuer company may conduct

road shows at various places. In a road show, the lead manager accompanied

by a team of senior officials of the company hold conference and make

presentation in order to shift the demand schedule for the company’s security.

192

The groups of institutional investors, high net worth investors, brokers and

sub-brokers attend the road show. The team makes a presentation about the

issuing company and answers the questions raised by the participants.

Through road shows, the company comes in face to face with investors and

interacts with them. The points to be highlighted in the road shows cover the

performance of the company, reputation of the promoters and the projects of

the company.

(b) Research Coverage

Research coverage, forecasts and recommendations by financial

analysts are important tools in the marketing of securities especially in the

issue of equities. All reputed merchant bankers have their own research teams

and they publish research reports about the IPOs in various financial dailies.

(c) Press Conferences and Investors’ Conferences

Press conferences for public issues are organized by advertising

agency at different centres having concentration of investors. Sometimes,

visits by selected members of the press are also organized to the issuing

company and briefed about the importance of the project for wide publicity of

the issue.

Similarly, investors’ meetings are held at various cities where it is

expected that their interest could be invoked in the public issue. Cities with

stock exchanges are favourable centres for such meetings. Investors’ meetings

are also arranged in foreign countries to create interest of NRIs in the public

issue.

(d) Network of Merchant Bankers

Leading merchant bankers having specialization in the area of issue

management have wide network to create investors interest in public issue.

They maintain list of potential investors and generally have good links with

qualified institutional investors and high net worth investors. Some merchant

bankers have registered broking firms as their sister concerns having direct

link with the investors.

For example, Enam has a network of 5000 dedicated franchises, Karvy

has 448 branches and 275 business associates scattered all over India, SBI

Capital Markets and Kotak Mahindra Capital Company are the subsidiaries of

banks having a network of branches. IDBI Capital Markets Ltd operates

193

through 25 branches and 10,000 sub brokers/ agents spread across the country.

JM Morgan Stanley, DSP Merrill Lynch and HSBC Securities and Capital

Markets (India) Ltd have worldwide network. Private merchant bankers like

Edelweiss, Centrum and Allianz Securities have also wide network of sub

brokers in India.

7.1.2 SEBI Guidelines on Issue Advertisement Disclosure and Investor Protection Guidelines issued by SEBI in 2000 as

amended from time to time provide guidelines regarding advertisement for public

issues. The lead merchant banker has been made responsible to ensure compliance

with the guidelines on advertisement by the issuing company. As per SEBI guidelines,

an issue advertisement should have the following features:

It should be truthful, fair, and clear and should not contain any statement that

is untrue or misleading.

It should reproduce information contained in an offer document in full and

disclose all relevant facts and not be restricted to select extracts relating to that

item.

It should be set forth in a clear, concise and understandable language.

It should not contain statements which promise or guarantee rapid increase in

profits.

It shall not contain any information that is not contained in the offer document.

It should not appear in the form of crawlers i.e. the advertisement which runs

simultaneo`1usly with the programme in a narrow strip at the bottom of the

television screen.

No slogans, expletives or non factual and unsubstantial titles should appear in

the issue advertisement of offer document.

In case of issue advertisement on television screen (a) the risk factors should

not be scrolled on the screen (b) the advertisement should advise viewer to

refer to the red herring prospectus/ offer document for detail.

No issue advertisement should be released without giving ‘Risk Factors’ in

respect of the concerned issue, provided that an issue opening/ closing

advertisement which does not contain the highlights need not contain risk

factors.

194

If any advertisement carries any financial data, it should also contain data for

the past three years and include particulars relating to sales, gross profit, net

profit, share capital, reserves, earning per share, dividend and the book values.

All issue advertisements in newspapers, magazines, brochures and pamphlets

containing highlights relating to any issue should also contain risk factors

giving equal importance in all respects including the print size.

No advertisement shall include any issue slogans or brand name for the issue

except the normal commercial name of the company or commercial brand of

the product already in use.

No product advertisement of the issuer should contain any direct or indirect

reference to the performance of the issuer during the period (a) commencing

from the date of meeting of Board of Directors in which the issue is approved

till the filing of draft offer document with the SEBI, and (b) the period

commencing from the filing offer document with the SEBI till the date of

allotment of securities.

An advertisement should not be issued stating that the issue has been fully

subscribed or oversubscribed during the period the issue is open for

subscription, except to the effect that the issue is open or closed, (a)

announcement regarding closure of the issue should not be made except on the

last closing date, and (b) if the issue is fully subscribed before the last closing

date as stated in the offer document, the announcement should not be made

after the issue is fully subscribed and such announcement should also be made

on the date on which the issue is to be closed.

Announcement regarding closure of issue should be made only after the lead

merchant banker is satisfied that at least 90% of the issue has been subscribed

and a certificate has been obtained to that effect from the registrar to the issue.

No incentive, apart from the permissible underwriting commission and

brokerage, shall be offered through any advertisement to anyone associated

with marketing the issue.

In case there is a reservation for the NRIs, the issue advertisement should

specify the same and indicate the place in India from where the individual NRI

applicant can procure application forms.

195

7.1.3 Statutory Advertisements The following advertisements have to be statutorily released (1) Issue announcement advertisement at least 10 days before opening of the

issue. This advertisement contains an abridged version of the prospectus.

(2) Issue opening advertisement on the day of opening of the issue.

(3) Issue closing advertisement on the day of closing of the issue.

(4) The basis of allotment advertisement after finalization of allotment.

7.1.4 Lead Merchant Banker and Observance of Advertisement Code

The lead manager to the issue is responsible to ensure strict compliance with

the code of advertisement by the issuer company set out above and for that purpose

the lead manager should comply the following:

(1) To obtain undertaking from the issuer as part of Memorandum of

Understanding to be entered into by the lead merchant banker with the issuer

company to the effect that the issuer company shall not directly or indirectly

release, during any conference or at any other time, any material or

information which is not contained in the offer document.

(2) To ensure that the issuer company obtains approval in respect of all issue

advertisements and publicity materials from the lead merchant banker

responsible for marketing the issue and also ensure availability of copies of all

issue related materials with the lead merchant banker at least till the allotment

is completed.

(3) With respect to research reports, the lead merchant banker shall ensure that it

is prepared only on the basis of published information as contained in the offer

document and the advertisement code is observed while circulating the

research report and that the risk factors are reproduced wherever highlights are

given, as in case of an advertisement.

7.1.5 Recent Marketing Strategies for Public Issues Marketing strategies adopted for public issues aim at educating the investors

for active participation in capital market and reducing the cost of issue as also the risk

of investors and the issuer companies in the form of overpricing and under pricing

respectively. With these objectives in mind, marketing strategies are developed from

196

time to time to make Indian capital market more efficient. Some of the recent

marketing strategies adopted in new issue market in India are as follows:

(i) Marketing IPOs through Secondary Market ( e-IPO)

SEBI has approved a proposal of marketing IPOs through the stock exchange.

The system uses the existing infrastructure of stock exchange (terminals, brokers and

system) being used for secondary market transactions for marketing IPOs through

book building route. A company proposing to issue capital to public through on-line

system of stock exchange has to comply with section 55 to 68 A of the companies

Act, 1956 and DIP Guidelines of SEBI.

The on-line IPO system is designed to reduce information asymmetry between

bidders and allows the underwriters to aggregate orders and ‘build the book’. The

bidding begins simultaneously in several cities. The investors can see all the other

bids placed on the issue. The demand for the new issue is visible in real time to all

bidders on their computer screens and also available on the National Stock Exchange

(NSE) website. This new internet based IPO offering system is known as NEAT-

National Exchange Automated Trading.

On-line IPO system at NSE was launched with the book building issue of

Hughes Software Ltd in September, 1999 and got a good public response. Till March,

2007, a total of 199 issuer companies have used this NSE on-line IPO system.

Subsequently, the BSE also augmented its traditional book building offering

mechanism with an internet based bidding system, very similar to the NEAT-IPO

mechanism. This system reduces the cost of the issue as well as time for listing of

securities.

The lead manager is responsible for co-ordination of all the activities among

various intermediaries connected to the issue/ system. The names of brokers

appointed for the issue along with the names of other intermediaries should be

disclosed in the offer document and application from.

(ii) Green Shoe Option (Over Allotment of Securities)

The green shoe option is the most useful tactic strategy in an unanticipated

bull market. In a volatile market with little strong direction, provision of over

allotment is basically the best marketing device. The lead manager offers added

securities to syndicate members/ brokers with the expectation that they will put forth a

strong sales effort.

197

In India, provisions for green shoe option are stated in DIP Guidelines under

chapter VIII-A. It states that the issuing company shall appoint one of the merchant

bankers/BRLMs from among the issue management team, as the ‘Stabilization Agent’

(SA), who will be responsible for the price stabilization process, if required. The SA

shall enter into an agreement with the issuing company, prior to filing of offer

document with SEBI, clearly stating all the terms and conditions relating to this

option including the charges/expenses to be incurred by SA for this purpose.

The SA shall also enter into an agreement with the promoters or pre issue

shareholders who will lend their shares under the provisions of this chapter,

specifying the maximum number of shares that may be borrowed from promoters or

the shareholders, which shall not be in excess of 15% of the total issue size.

During the period of study, a number of issuing companies has availed of this

option. ICICI Bank is the first company to use this option for the public issue of

equity shares of Rs. 3050 crore in April, 2004.

(iii) Safety Net (Buy Back of Shares)

Safety net is the protection to investors against the fall in the market price of

the IPO below its offer price during a particular period of time. Promoters and

merchant bankers provide standby arrangement to buy shares from public if the

market quotations go below the offer price during the statutory period.

Safety net aims at wooing more and more potential investors to subscribe for

the IPOs. This mechanism helps the advertising agency to the issue and the lead

merchant banker in its campaign for marketing the IPOs. So safety net is actually a

put option given to the investors, but not by the issuing company. It gives the right but

not the obligation to the investors to sell the shares to the entity offering the option at

a particular price within a stipulated period.

Any safety net or buy back arrangement of shares proposed in any issue

should be finalized by the issuing company with the lead merchant banker in advance

and should be disclosed in the offer document.

Bangalore based Software Company Opto Circuits Ltd offered a safety net to

its shareholders for six months in its IPO. Other companies which offered safety net

mechanism during the period under review included TCS Ltd, Shree Renuka Sugars

Ltd and ICICI Bank.

198

(iv) Target Marketing/ Branding the financial Instrument

Lead merchant bankers have been using the strategy of targeting the different

segments of investors in the market and branding the securities to create interest of the

investors in the public issues.

Different innovative financial instruments have been witnessed in the Indian

capital market especially after post reform period. Some of the new financial

instruments are Zero Coupon Bonds, Deep Discount Bonds, Third party Convertible

Debentures, Zero Coupon Convertible Note, Tax Saving Bonds, Cumulative

Convertible Preference Shares, Convertible (Partly and Fully) Debentures, Debt for

Equity Swap, Floating Rate Bonds etc.

During the period under review, bond issues of two financial Institutions

namely ICICI Ltd and IDBI Ltd dominated the debt issues in India. ICICI Ltd raised

an aggregate amount of Rs.18876.62 crore from 41 debt issues of Bonds. These

unsecured bonds were branded as ‘ICICI Safety Bonds.’ To target the different

classes of investors, the bonds were classified as:

(a) Tax Saving Bonds – The issue of these bonds aimed at that segment of

investors who wanted to save tax.

(b) Regular Income Bonds- These were aimed at investors from middle class and

retired persons.

(c) Money Multiplier Bonds – These bonds targeted long term investors requiring

secured income.

(d) Child Growth Bonds – These were long term bonds with 16 to 19 years

maturity period suitable for young investors to secure the future of their

children.

Different options were given to the investors under each category of bonds.

JM Morgan Stanley performed the leading role as lead manager to these bond issues

with a group of other merchant bankers in the role of lead managers and co-managers.

Similarly IDBI Ltd came out with 21 public issues of bonds by raising an

aggregate amount of Rs. 17323.38 crore during this period. The bonds issued by the

IDBI Ltd were branded as ‘IDBI FLEXIBLE BONDS’. Different types of bonds

targeted different types of investors like:

(a) IDBI Regular Income Bonds – These bonds provided fixed rate of interest

payable annually or bi-annually.

199

(b) IDBI Growing Interest Bonds – These bonds provided increasing rate of

interest with the passage of time.

(c) IDBI Multiplier Bonds – Bonds on which Lump sum amount was payable at

the end of maturity period, that is, 6 years and 7 months.

(d) IDBI Infrastructure (Tax Saving) Bonds – Bonds with annual interest option

and cumulative option.

These bond issues were lead managed by a group of merchant bankers acting

as lead managers and co-managers with SBI Capital Markets Ltd at the apex.

7.2 Public Response to Public Issues The result of extensive campaign for marketing of public issues is the ultimate

response by the public for subscription of shares. The reputation of lead merchant

banker (s) as an issue manager is at stake in this respect. If the issuing company is not

able to get public subscription to the extent of 90% of total issue size, the issue has to

be withdrawn and the money received on applications is refunded. This adversely

affects the reputation not only of the issuing company, but the lead merchant banker

also.

Since the period of economic reforms in India, the primary capital market has

been witnessing a structural transformation. Liberalization and globalization has

resulted in the widening and deepening of the market. The number of investors as

well as the financial instruments has increased. Public response to capital issues is the

indication of the confidence of the investors in the primary market, thus leading to the

development of the capital market.

This part of the chapter analyses the trends of public response to the public

issues of equity and debt instruments. In this section, number of public issues

subscribed at different levels, mean annual subscription ratio and the subscription

ratio of public issues managed by different merchant bankers during the period 1997-

98 to 2008-09 has been analysed.

7.2.1 Public Response to Equity Issues New issue market for equity shares witnessed several ups and downs with

respect to response from public. Subscription by public to new issues depends upon a

number of factors and the major factor is the developments in the secondary market of

shares.

200

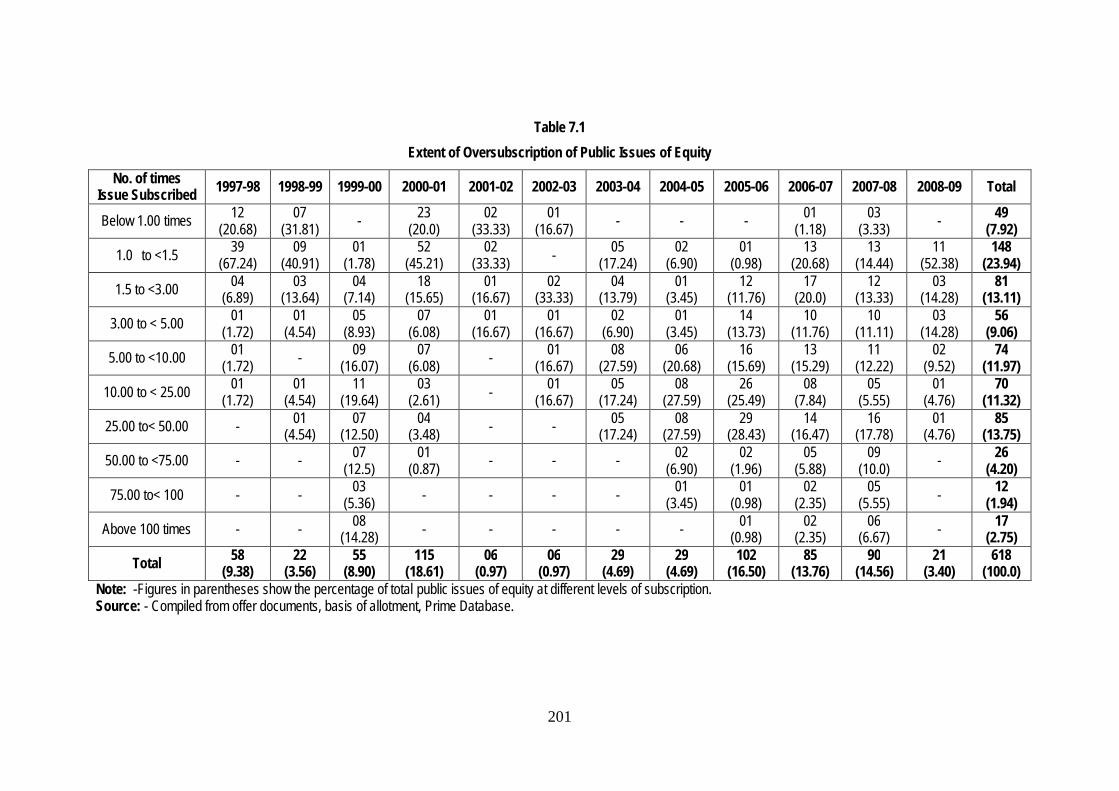

7.2.2 Overview of Subscription Level of Public Issues of Equity Shares

Annual public response to equity issues at various levels of subscription has

been presented in the table 7.1

Table depicts the number of public issues of equity shares along with percentage to total annual issues subscribed by public at different levels of subscription. As shown in the table, primary market in 1997-98 showed a dismal picture as far as the subscription of public issues is concerned. Out of 58 equity issues floated during the year, 12 issues (20.68%) were subscribed less than one time while 39 issues (67.24%) were subscribed between one and 1.5 time. Only three issues could get subscription of more than three times. Depressed secondary market conditions during 1993 -95, stringent entry barriers guidelines issued by SEBI and decline in industrial growth have been the major reasons for the lack of investors’ interest in the primary market. Introduction of free pricing of public issues led to fair pricing of issues. This resulted in decline in under pricing/ returns on listing and had an adverse effect on the subscription of shares by the general public. Declining trend of 1997-98 continued in 1998-99 also. Out of 22 public issues of equity floated during the period, seven issues (31.81%) were subscribed less than one time and subscription to 9 issues (40.91%) was more than one time but less than 1.5 times. Only one issue was found to have got subscription over 25 times and another one got in the range of 10 to 25 times.

A favourable response to the primary equity market has been found from the public in 1999-2000. This has been the period of information technology and software boom. Out of 56 equity issues in this year, as many as 8 issues (14.28%) were subscribed more than 100 times and another three (5.36%) were subscribed between 75 to100 times. Further, 11 issues (19.64%) were subscribed between 10 to 25 times.

During the year 2000-01, although there was a rush in the new issue market of equity shares from information technology companies with small size, but investors did not respond well to these issues. A total of 52 issues (45.21%) were subscribed in the range of 1.00 to less than 1.5 times. Only 8 issues (6.95%) were subscribed over 10 times during 2000-01. Crash in secondary market in April 2000, and overvaluation of information technology companies and media industry were the major cause for investors’ lack of interest in primary market during this year. As many as five companies have to refund the application money to investors for lack of minimum subscription and two equity issues partially devolved upon the underwriters during this year.

201

Table 7.1 Extent of Oversubscription of Public Issues of Equity

No. of times Issue Subscribed 1997-98 1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 Total

Below 1.00 times 12 (20.68)

07 (31.81) - 23

(20.0) 02

(33.33) 01

(16.67) - - - 01 (1.18)

03 (3.33) - 49

(7.92) 1.0 to <1.5 39

(67.24) 09

(40.91) 01

(1.78) 52

(45.21) 02

(33.33) - 05 (17.24)

02 (6.90)

01 (0.98)

13 (20.68)

13 (14.44)

11 (52.38)

148 (23.94)

1.5 to <3.00 04 (6.89)

03 (13.64)

04 (7.14)

18 (15.65)

01 (16.67)

02 (33.33)

04 (13.79)

01 (3.45)

12 (11.76)

17 (20.0)

12 (13.33)

03 (14.28)

81 (13.11)

3.00 to < 5.00 01 (1.72)

01 (4.54)

05 (8.93)

07 (6.08)

01 (16.67)

01 (16.67)

02 (6.90)

01 (3.45)

14 (13.73)

10 (11.76)

10 (11.11)

03 (14.28)

56 (9.06)

5.00 to <10.00 01 (1.72) - 09

(16.07) 07

(6.08) - 01 (16.67)

08 (27.59)

06 (20.68)

16 (15.69)

13 (15.29)

11 (12.22)

02 (9.52)

74 (11.97)

10.00 to < 25.00 01 (1.72)

01 (4.54)

11 (19.64)

03 (2.61) - 01

(16.67) 05

(17.24) 08

(27.59) 26

(25.49) 08

(7.84) 05

(5.55) 01

(4.76) 70

(11.32) 25.00 to< 50.00 - 01

(4.54) 07

(12.50) 04

(3.48) - - 05 (17.24)

08 (27.59)

29 (28.43)

14 (16.47)

16 (17.78)

01 (4.76)

85 (13.75)

50.00 to <75.00 - - 07 (12.5)

01 (0.87) - - - 02

(6.90) 02

(1.96) 05

(5.88) 09

(10.0) - 26 (4.20)

75.00 to< 100 - - 03 (5.36) - - - - 01

(3.45) 01

(0.98) 02

(2.35) 05

(5.55) - 12 (1.94)

Above 100 times - - 08 (14.28) - - - - - 01

(0.98) 02

(2.35) 06

(6.67) - 17 (2.75)

Total 58 (9.38)

22 (3.56)

55 (8.90)

115 (18.61)

06 (0.97)

06 (0.97)

29 (4.69)

29 (4.69)

102 (16.50)

85 (13.76)

90 (14.56)

21 (3.40)

618 (100.0)

Note: -Figures in parentheses show the percentage of total public issues of equity at different levels of subscription. Source: - Compiled from offer documents, basis of allotment, Prime Database.

202

Investment activities in the primary market of equity remained subdued in the

years 2001-02 and 2002-03 also. Only six equity issues in each year were floated.

Subscription level in 2001-02 showed that all the six issues were subscribed below

5.00 times while only one was subscribed above 10 times.

The year 2003-04 witnessed an upsurge in primary market activities. It was

induced by buoyant secondary market, political stability and economic recovery. 8

equity issues (27.59%) of total 29 issues were subscribed 5 to 10 times by the public

while 10 issues (34.48%) were subscribed more than 10 times. However, one issuing

company had to refund application money due to lack of minimum subscription

during this year.

Continuing the same trend, response to equity issues was good in 2004-05. Of

the 29 equity issues floated, 8 issues (27.59%) were subscribed more than 10 times

but less than 25 times whereas subscription to another 8 issues was found in the range

of 25 to 50 times. One equity issue was subscribed even more than 75 times.

In 2005-06, 29 issues ( 28.43%) were subscribed between 25 times to 50 times

while 26 issues ( 25.49%) were found to have been subscribed between 10 to 25

times. One equity issue was subscribed even in the range of 75 to 100 times and

another one was subscribed more than 100 times. Active participation of Foreign

Institutional Investors (FIIs), Qualified Institutional Buyers (QIBs), strong

fundamentals of economy, positive investment climate and buoyant secondary market

induced public to participate actively in the primary market activities during 2005-06.

Favourable response to public issue of equity during 2005-06 continued in

2006-07 and also. However, 14 issues (16.47%) failed to elicit much response from

the public (less than 1.5 times). 17 equity issues (20%) were subscribed 1.5 times to

3.00 times, while another 14 issues (16.47%) were subscribed in the range of 25 to

50 times and two equity issues were subscribed more than 100 times. Similarly in

2007-08, five issues (5.55%) were subscribed between 75 to 100 times and another

six issues (6.67%) got more than 100 times subscription. Primary equity market could

not sustain the same trend in 2008-09 and 11 (52.38%) out of total 21 issues were

subscribed less than 1.5 times while another three issues got subscription between 3 to

5 times. Only one issue could reach to subscription level of 25 to 50 times.

203

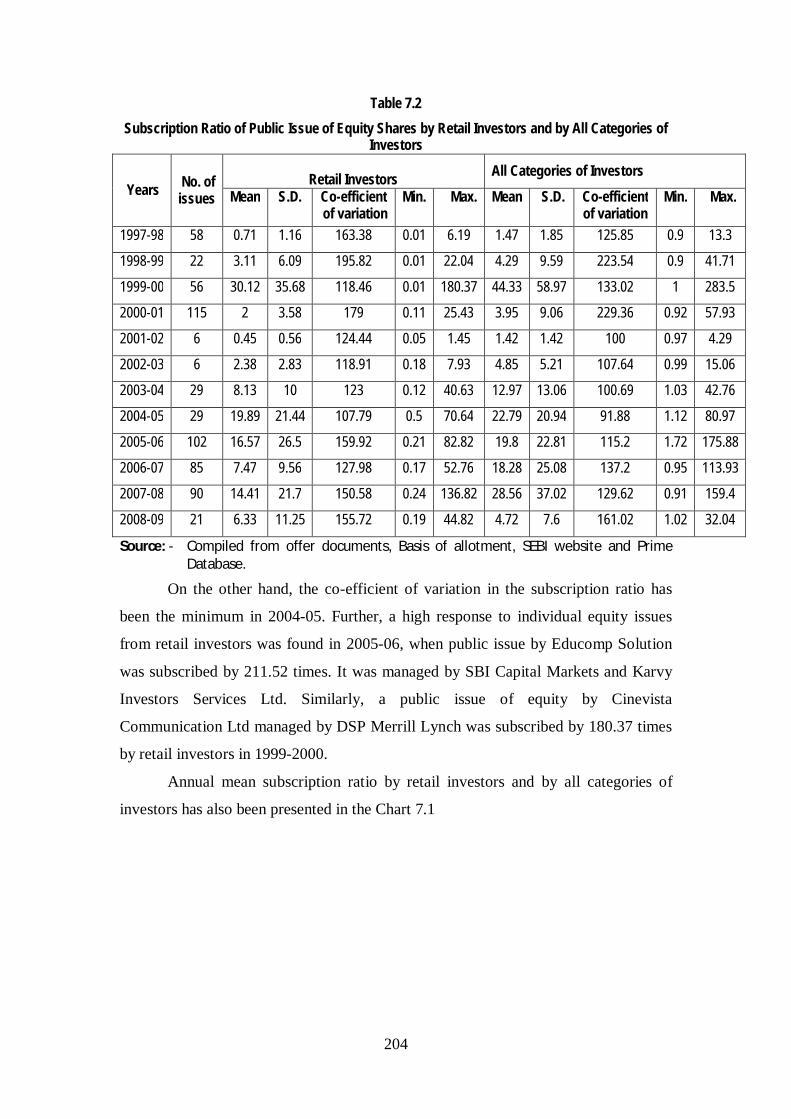

7.2.3 Subscription by Retail Investors vis-à-vis All Categories of Investors

Table 7.2 depicts the response from the retail vis-à-vis all categories of

investors to the public issue of equity shares during the period under review. As is

clear from the table, mean value of over subscription by all categories of investors

was highest (44.33 times) in 1999-2000. It was followed by mean subscription of

28.56 times in 2007-08 and 22.79 times in 2004-05. Investors also responded

favourably to the public issues of equity shares in 2005-06 and 2006-07, when

average of the shares subscription has been 19.80 and 18.28 times respectively. On

the other hand, investors did not respond well to equity issues in 1997-98 and 2001-

02, when mean subscription ratio was just 1.47 and 1.42 times respectively. Even the

number of public issues has been only six each in the year 2001-02 and 2002-03.

Thus, the response from the public was very dismal.

The table also shows the co-efficient of variation in the subscription ratio of

different equity shares floated during the particular year. A high co-efficient of

variation (229.30%) has been found in 2000-01 showing high dispersion in the

subscription level of 115 equity issues during the year. This has been followed by

223.54% in 1998-99. Co-efficient of variation has been minimum (91.88%) in 2004-

05, depicting less variation in the subscription level of public issues of equity. While a

high standard deviation of 58.97 has been found in the subscription level of different

equity issues in 1999-2000, the same has been only 1.42 in 2001-02. It showed that

the issues have been subscribed evenly during the year.

The analysis further shows that good response has been received from the

retail investors in the year 1999-2000 who subscribed 30.12 times to the equity issues

in that year. This was followed by 19.89 and 16.57 times in 2004-05 and 2005-06

respectively. On the other hand, retail investors have not responded well in 1997-98

and 2001-02, when mean subscription was only 0.71 and 0.45 times respectively.

A high variation in the subscription ratio by retail investors, as shown by co-

efficient of variation was found in 1998-99 and 1997-98 which stood at 195.82% and

163.38% respectively. It means retail investors have different response level for good

and average issues.

204

Table 7.2 Subscription Ratio of Public Issue of Equity Shares by Retail Investors and by All Categories of

Investors

Years No. of issues

Retail Investors All Categories of Investors

Mean S.D. Co-efficient of variation

Min. Max. Mean S.D. Co-efficient of variation

Min. Max.

1997-98 58 0.71 1.16 163.38 0.01 6.19 1.47 1.85 125.85 0.9 13.3

1998-99 22 3.11 6.09 195.82 0.01 22.04 4.29 9.59 223.54 0.9 41.71

1999-00 56 30.12 35.68 118.46 0.01 180.37 44.33 58.97 133.02 1 283.5

2000-01 115 2 3.58 179 0.11 25.43 3.95 9.06 229.36 0.92 57.93

2001-02 6 0.45 0.56 124.44 0.05 1.45 1.42 1.42 100 0.97 4.29

2002-03 6 2.38 2.83 118.91 0.18 7.93 4.85 5.21 107.64 0.99 15.06

2003-04 29 8.13 10 123 0.12 40.63 12.97 13.06 100.69 1.03 42.76

2004-05 29 19.89 21.44 107.79 0.5 70.64 22.79 20.94 91.88 1.12 80.97

2005-06 102 16.57 26.5 159.92 0.21 82.82 19.8 22.81 115.2 1.72 175.88

2006-07 85 7.47 9.56 127.98 0.17 52.76 18.28 25.08 137.2 0.95 113.93

2007-08 90 14.41 21.7 150.58 0.24 136.82 28.56 37.02 129.62 0.91 159.4

2008-09 21 6.33 11.25 155.72 0.19 44.82 4.72 7.6 161.02 1.02 32.04

Source: - Compiled from offer documents, Basis of allotment, SEBI website and Prime Database.

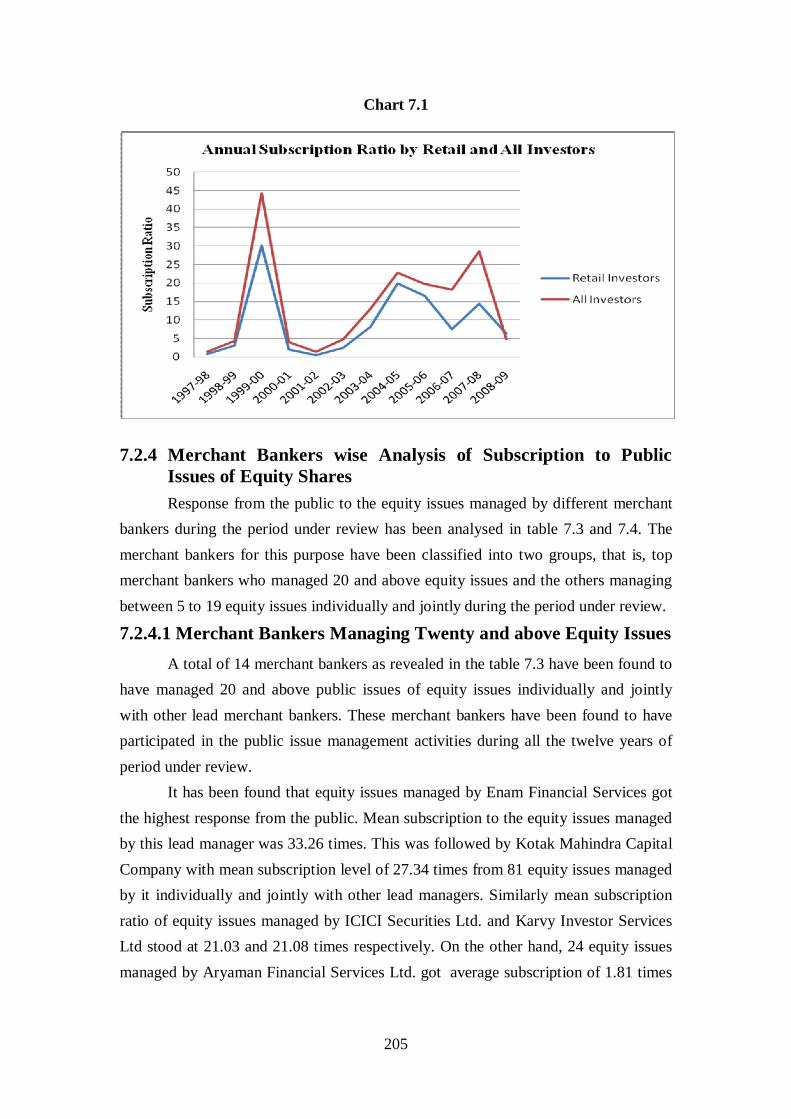

On the other hand, the co-efficient of variation in the subscription ratio has

been the minimum in 2004-05. Further, a high response to individual equity issues

from retail investors was found in 2005-06, when public issue by Educomp Solution

was subscribed by 211.52 times. It was managed by SBI Capital Markets and Karvy

Investors Services Ltd. Similarly, a public issue of equity by Cinevista

Communication Ltd managed by DSP Merrill Lynch was subscribed by 180.37 times

by retail investors in 1999-2000.

Annual mean subscription ratio by retail investors and by all categories of

investors has also been presented in the Chart 7.1

205

Chart 7.1

7.2.4 Merchant Bankers wise Analysis of Subscription to Public

Issues of Equity Shares

Response from the public to the equity issues managed by different merchant bankers during the period under review has been analysed in table 7.3 and 7.4. The merchant bankers for this purpose have been classified into two groups, that is, top merchant bankers who managed 20 and above equity issues and the others managing between 5 to 19 equity issues individually and jointly during the period under review.

7.2.4.1 Merchant Bankers Managing Twenty and above Equity Issues A total of 14 merchant bankers as revealed in the table 7.3 have been found to

have managed 20 and above public issues of equity issues individually and jointly with other lead merchant bankers. These merchant bankers have been found to have participated in the public issue management activities during all the twelve years of period under review.

It has been found that equity issues managed by Enam Financial Services got the highest response from the public. Mean subscription to the equity issues managed by this lead manager was 33.26 times. This was followed by Kotak Mahindra Capital Company with mean subscription level of 27.34 times from 81 equity issues managed by it individually and jointly with other lead managers. Similarly mean subscription ratio of equity issues managed by ICICI Securities Ltd. and Karvy Investor Services Ltd stood at 21.03 and 21.08 times respectively. On the other hand, 24 equity issues managed by Aryaman Financial Services Ltd. got average subscription of 1.81 times

206

only, while the 20 equity issues managed by IDBI Ltd and IDBI Capital Markets had mean subscription of 6.87 times.

The table further reveals that high variation in the public response to different

equity issues has been found in case of issues managed by Keynote Corporate

Services, Centrum Finance and IDBI Ltd and IDBI Capital Markets Ltd. Co-efficient

of variation in the subscription of issues managed by Keynote Corporate Service,

Centrum Finance and IDBI Ltd and IDBI Capital Markets stood at 242.42%, 222.24%

and 221.25% respectively. Least variation (99.28%) was found in the subscription of

equity issues managed by Enam Financial Services. On the basis of standard deviation

of subscription levels of equity issues also, a high dispersion was found in the

subscription of issues managed by Keynote Corporate Services, Allianz Securities and

Kotak Mahindra Capital Company Ltd.

The table further reveals that equity issues managed by karvy Investor Service,

Enam Financial Services and Centrum Finance Ltd found good response from retail

investors. Mean subscription of equity issues managed by these merchant bankers has

been found at 19.34, 14.75 and 13.74% times respectively. On the other hand, equity

issues managed by Aryaman Financial Services, IDBI Ltd, IDBI Capital Markets and

JM Morgan have not been responded favourably by retail investors. Aryaman

Financial Services Ltd. has been active in issue management during the initial years of

period under review, especially during 2000-01. There has been a moderate response

from retail investors to the equity issues managed by DSP Merrill Lynch, ICICI

Securities and IL&FS Investsmart etc.

High degree of standard deviation and co-efficient of variation has been found

in the retail investors’ subscription of the issues managed by DSP Merrill, SBI Capital

Markets and Centrum Finance Ltd. It shows the high variation in the response from

retail investors to different public issues managed by these merchant bankers.

207

Table 7.3 Subscription Ratio of Equity Public Issues Managed by Different Merchant Bankers

(Merchant Bankers Managing 20 and Above Equity Issues)

S. No. Merchant Bankers No. of issues

Retail Investor All Categories of Investors Mean S.D. Co-efficient

of variation (%)

Min. Max. Mean S.D.

Co-efficient of variation

(%)

Min. Max.

1. Enam financial Services. 86 14.75 18.8 127.45 0.13 90.76 33.26 33.02 99.28 0.99 131.8 2. Kotak Mahindra Capital Co. 81 10.47 15.13 144.51 0.19 80.32 27.34 33.07 120.95 1.48 115.32 3. SBI Capital Markets. 68 12.57 28.54 227.04 0.18 211.52 17.49 26.86 153.57 0.9 115.32 4. J.M. Morgan Stanley. 68 7.79 10.47 134.4 0.02 50.76 20.36 27.47 134.92 0.99 131.8 5 ICICI Securities. 62 9.71 12.31 126.77 0.01 45.72 21.03 24.77 117.78 0.9 115.32 6 DSP Merrill Lynch. 58 8.89 23.82 267.94 0.21 180.37 20.45 26.38 128.99 1.44 115.32 7. Karvy Investors. 41 19.34 35.15 181.74 0.44 211.52 21.08 25.58 121.34 0.9 114.11 8. UTI Securities Exchange 37 12.91 16.45 127.42 0.18 83.96 14.39 17.87 124.18 0.91 83.96 9. Keynote Corporate. 27 13.1 23.83 181.91 0.61 106.02 14.71 35.66 242.42 0.99 173.75

10. Aryaman Financial. 24 1.5 4.29 286 0.21 21.5 1.81 3.02 166.85 0.93 15.9 11. IL&FS Investsmart 20 9.74 9.75 100.1 0.22 34.74 16.43 16.95 103.16 1.45 54.85 12. IDBI, IDBI Capital Markets 20 4.85 9.28 191.34 0.01 36.69 6.87 15.2 221.25 0.9 61.49 13. Allianz Securities 20 12.07 20.66 171.68 1.05 81.92 17.96 38.88 216.48 0.95 175.88 14. Centrum Finance 20 13.74 30.15 219.43 0.49 136.82 14.61 32.47 222.24 0.98 145.57 Note: - No. of issues refers to the public issues of equity managed by respective lead merchant banker individually and jointly with other lead

managers. Source: - Compiled from offer documents, Basis of allotment, SEBI website and Prime Database.

208

Chart 7.2 also shows the mean subscription ratio of equity issues managed by

different merchant bankers (managing 20 and above equity issues) during the period

under review.

Chart 7.2

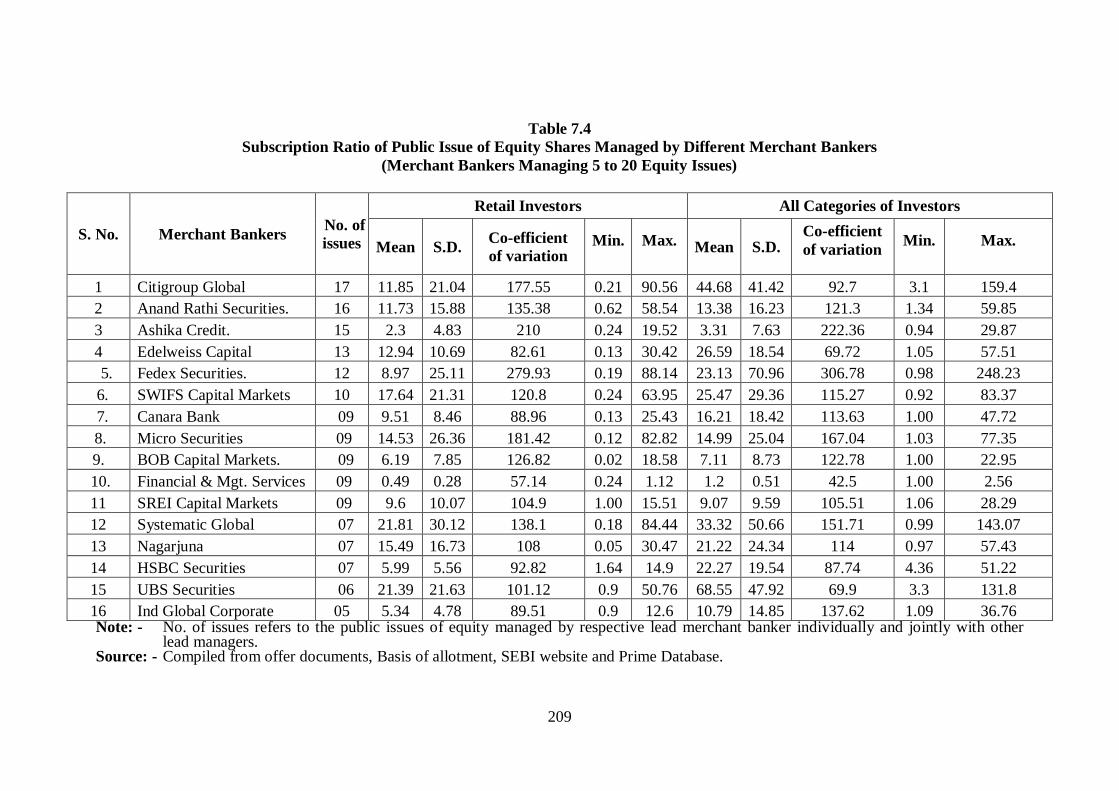

7.2.4.2 Merchant Bankers Managing 5 to 19 Equity Issues

Small sized merchant bankers, who occasionally participated in the services of

public issue management has been shown in table 7.4 A good public response to the

equity issues managed by UBS Securities, Citigroup Global, Systematic Global

Edelweiss Capital and SWIFS Capital Markets has been found from the analysis of

mean subscription ratio of all categories of investors.. Average subscription ratio for

the equity issues managed by these merchant bankers stood at 68.55, 44.68, 33.32,

26.59 and 25.47 times respectively. However, UBS Securities participated as lead

manager only during 2007-08 when primary market witnessed boom conditions and

public response to equity issues was highly favourable.

On the other hand, the equity issues managed by Financial and Management

Services, Ashika Credit, BOB Capital Markets and SREI Capital Markets could not

find much favour from the investors. Equity issues managed by Financial &

Management Services could secure subscription of only 1.2 times while the average

subscription to 9 equity issues managed by BOB Capital Markets stood at 7.11 times.

Financial & Management Services Ltd. participated in the initial years of study period

only when primary market was in depression.

209

Table 7.4 Subscription Ratio of Public Issue of Equity Shares Managed by Different Merchant Bankers

(Merchant Bankers Managing 5 to 20 Equity Issues)

S. No. Merchant Bankers No. of issues

Retail Investors All Categories of Investors

Mean S.D. Co-efficient of variation

Min. Max. Mean S.D. Co-efficient of variation Min. Max.

1 Citigroup Global 17 11.85 21.04 177.55 0.21 90.56 44.68 41.42 92.7 3.1 159.4 2 Anand Rathi Securities. 16 11.73 15.88 135.38 0.62 58.54 13.38 16.23 121.3 1.34 59.85 3 Ashika Credit. 15 2.3 4.83 210 0.24 19.52 3.31 7.63 222.36 0.94 29.87 4 Edelweiss Capital 13 12.94 10.69 82.61 0.13 30.42 26.59 18.54 69.72 1.05 57.51

5. Fedex Securities. 12 8.97 25.11 279.93 0.19 88.14 23.13 70.96 306.78 0.98 248.23 6. SWIFS Capital Markets 10 17.64 21.31 120.8 0.24 63.95 25.47 29.36 115.27 0.92 83.37 7. Canara Bank 09 9.51 8.46 88.96 0.13 25.43 16.21 18.42 113.63 1.00 47.72 8. Micro Securities 09 14.53 26.36 181.42 0.12 82.82 14.99 25.04 167.04 1.03 77.35 9. BOB Capital Markets. 09 6.19 7.85 126.82 0.02 18.58 7.11 8.73 122.78 1.00 22.95

10. Financial & Mgt. Services 09 0.49 0.28 57.14 0.24 1.12 1.2 0.51 42.5 1.00 2.56 11 SREI Capital Markets 09 9.6 10.07 104.9 1.00 15.51 9.07 9.59 105.51 1.06 28.29 12 Systematic Global 07 21.81 30.12 138.1 0.18 84.44 33.32 50.66 151.71 0.99 143.07 13 Nagarjuna 07 15.49 16.73 108 0.05 30.47 21.22 24.34 114 0.97 57.43 14 HSBC Securities 07 5.99 5.56 92.82 1.64 14.9 22.27 19.54 87.74 4.36 51.22 15 UBS Securities 06 21.39 21.63 101.12 0.9 50.76 68.55 47.92 69.9 3.3 131.8 16 Ind Global Corporate 05 5.34 4.78 89.51 0.9 12.6 10.79 14.85 137.62 1.09 36.76 Note: - No. of issues refers to the public issues of equity managed by respective lead merchant banker individually and jointly with other

lead managers. Source: - Compiled from offer documents, Basis of allotment, SEBI website and Prime Database.

210

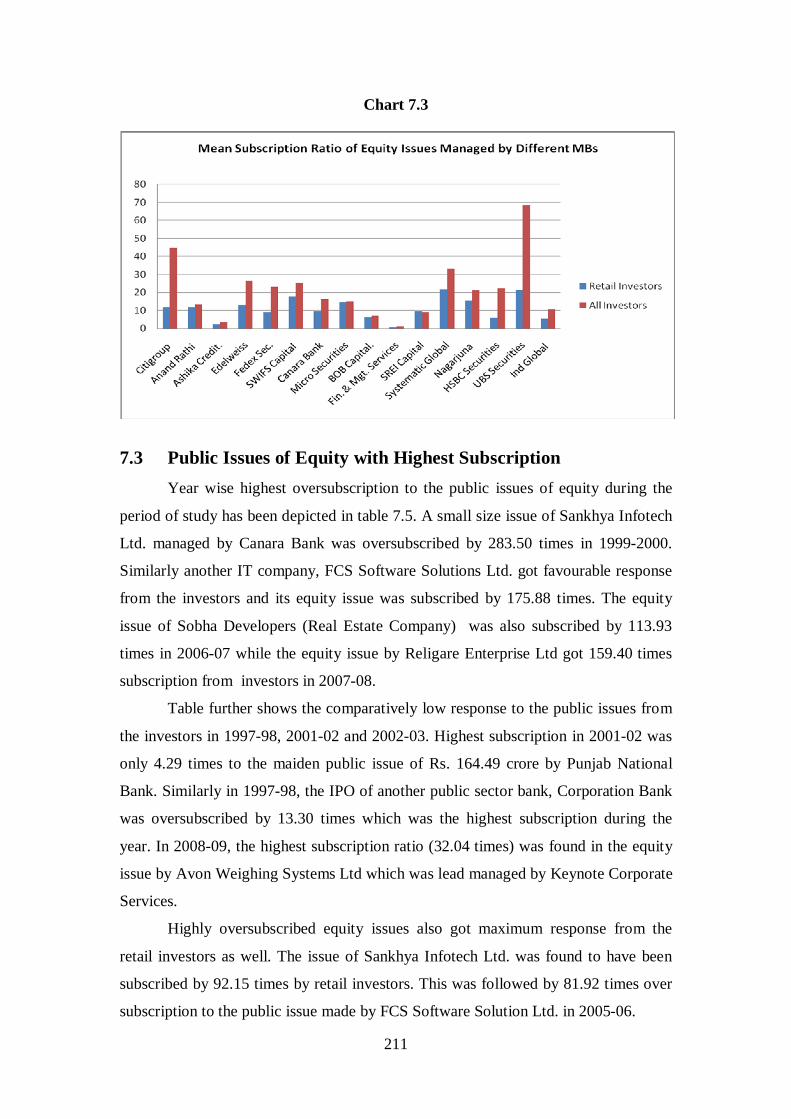

A high variation has been noticed in the co-efficient of variation and standard

deviation in the subscription ratio of equity issues managed by Fedex Securities,

Ashika Credit and Micro Securities. On the other hand, subscription to equity issues

managed by Financial & Management Services, UBS Securities, Citigroup Global,

HSBC Securities & Capital Markets and Anand Rathi Securities has been found to be

more consistent as shown by low co-efficient of variation and standard deviation.

The table further shows the response from Retail Investors to the equity issues

managed by different merchant bankers. A high mean subscription (signifying good

response from retail investors) has been found in case of issues managed by

Systematic Global (21.81times), UBS Securities (21.39%), SWIFS Capital Markets

(17.64 times) and Nagarjuna (15.49 times). The merchant bankers with low retail

investors’ response to their equity issues again included Financial & Management

Services (0.49 times), Ashika Credit (2.30 times) Ind Global (5.34 times) and HSBC

Securities & Capital Markets (5.99 times).

With respect to retail investors’ response also, a high co-efficient of variation

has been found in the subscription to equity issues managed by Fedex Securites (

279.93%), Ashika Credit (210%), Micro Securities (181.42%) and Citigroup Global

(177.55 %). A more consistency in subscription ratio by retail investors was found in

the equity issues managed by UBS Securities, SREI Capital, Nagarjuna, HSBC

Securities & Capital and Ind Global. Co-efficient of variation in subscription to public

issue of equity shares managed by these merchant bankers stood at 101.12%, 104.9%,

108%, 92.82%and 89.51% respectively.

Mean subscription ratio of equity issues managed by different merchant

bankers (managing less than 20 equity issues) during the period under review has also

been highlighted in chart 7.3

211

Chart 7.3

7.3 Public Issues of Equity with Highest Subscription

Year wise highest oversubscription to the public issues of equity during the

period of study has been depicted in table 7.5. A small size issue of Sankhya Infotech

Ltd. managed by Canara Bank was oversubscribed by 283.50 times in 1999-2000.

Similarly another IT company, FCS Software Solutions Ltd. got favourable response

from the investors and its equity issue was subscribed by 175.88 times. The equity

issue of Sobha Developers (Real Estate Company) was also subscribed by 113.93

times in 2006-07 while the equity issue by Religare Enterprise Ltd got 159.40 times

subscription from investors in 2007-08.

Table further shows the comparatively low response to the public issues from

the investors in 1997-98, 2001-02 and 2002-03. Highest subscription in 2001-02 was

only 4.29 times to the maiden public issue of Rs. 164.49 crore by Punjab National

Bank. Similarly in 1997-98, the IPO of another public sector bank, Corporation Bank

was oversubscribed by 13.30 times which was the highest subscription during the

year. In 2008-09, the highest subscription ratio (32.04 times) was found in the equity

issue by Avon Weighing Systems Ltd which was lead managed by Keynote Corporate

Services.

Highly oversubscribed equity issues also got maximum response from the

retail investors as well. The issue of Sankhya Infotech Ltd. was found to have been

subscribed by 92.15 times by retail investors. This was followed by 81.92 times over

subscription to the public issue made by FCS Software Solution Ltd. in 2005-06.

212

Table 7.5

Public Issues of Equity Shares with Highest Total Subscription

Year Issuer Company Issue Date Issue Size

( Rs. in crore)

Over Subscription

(No. of times) Retail

Investors

Over subscription (No. of times) All Investors

Lead Manager(s)

1997-98 Corporation Bank Oct. 03, 1997

304.00 6.19 3.30 ICICI Sec., IDBI Bank, SBI Caps, DSP Merrill, Kotak Mahindra, JM Financial.

1998-99 KPIT Systems Ltd. Feb. 02, 1999

11.61 22.04 41.71 Enam Securities.

1999-00 Sankhya Infotech Ltd.

March 23-27, 2000

1.67 92.15 283.50 Canara Bank

2000-01 Vantel TechnologiesLtd.

April 06-09, 2000

1.57 15.37 57.93 Karvy Investors, Ask Raymond

2001-02 Punjab National Bank

March 21-28,2002

164.49 1.45 4.29 ICICI Securities, SBI Caps, DSP Merrill, Kotak Mahindra

2002-03 Divi Laboratories Feb. 17-21,2003

44.86 7.93 15.06 IL&FS Investsmart, Kotak Manindra

2003-04 Power Trading Corporation

March 01-08 , 2004

93.60 40.63 42.76 SBI Caps, Enam Securities

2004-05 Spanco Telesystem Ltd.

Nov. 01-08, 2004

7.53 66.97 80.97 Keynote Corporate Services

2005-06 FCS Software Solutions Ltd.

Aug. 22-26, 2005

17.50 81.92 175.88 Allianz Securities

2006-07 Sobha Developers Ltd.

Nov. 23-27, 2006

569.17 20.48 113.93 Kotak Mahindra, Enam Securities

2007-08 Religare Enterprise Ltd.

Oct.19- Nov. 1, 2007

140.16 90.76 159.40 Enam Securities Citigroup Global.

2008-09 Avon Weighing System Ltd.

June 9-12, 2008

9.83 44.82 32.04 Keynote Corporate Services.

Source: - Compiled from offer documents, Basis of Allotment.

Retail investors’ poor interest was found in the public issues made by public

sector banks at different points of time. Punjab National Bank and Corporation Bank,

although the highest subscribed equity issues in different years, got 1.45 and 6.19

times subscription respectively from retail investors in 2001-02 and 1997-98. Kotak

Mahindra Capital Company and Enam Securities, as lead managers, were found to

have participated in four highest subscribed public issues of equity each. This was

followed by SBI Capital Markets Ltd in the management of three highest subscribed

equity issues. Four of the twelve of these equity issues were managed by individual

lead managers while eight issuers appointed multiple lead merchant bankers to

manage these issues.

213

Comparatively small issue size of highly subscribed equity shares during the

period under review signifies that the investors prefer small sized issues over the

issues with larger size.

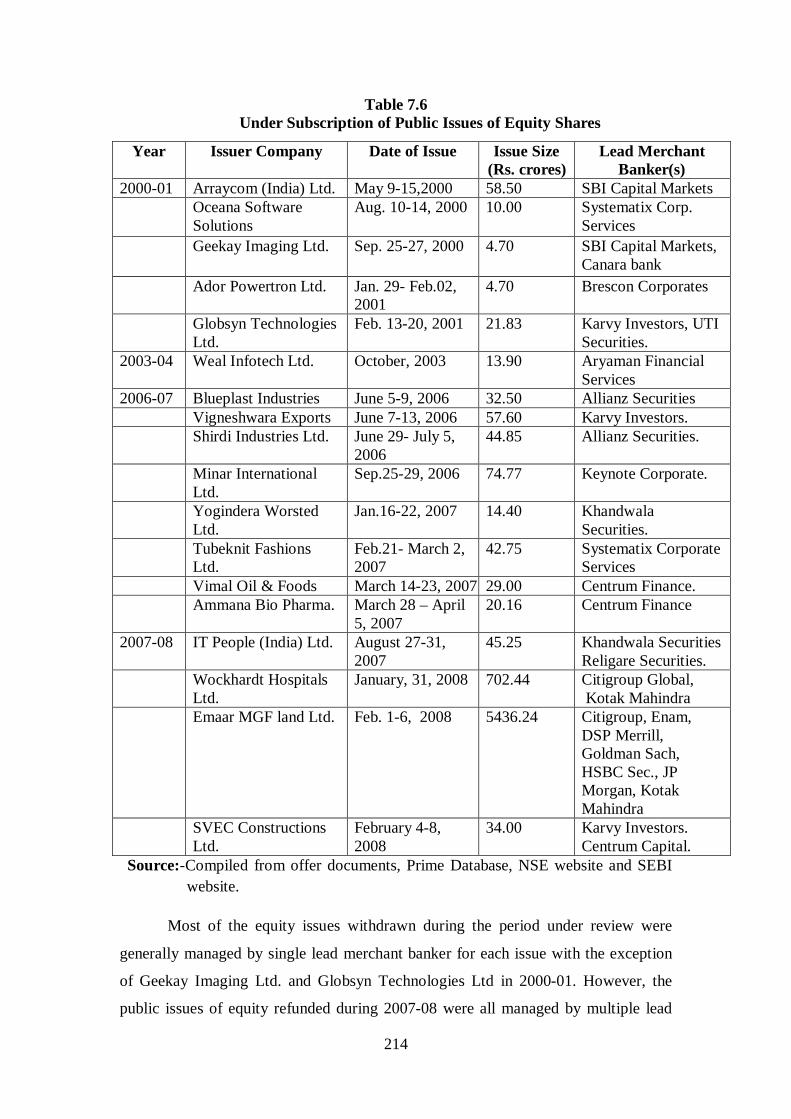

7.4 Under subscription of Public Issues of Equity As per provisions and directives of SEBI, if public issue of equity shares fails

to get 90% of the total issue amount, the issue is withdrawn and entire application

money has to be refunded. Table 7.6 shows the details of equity issues withdrawn due

to lack of investors’ response during the period under review.

The table shows that application money of five public issues of equity have to

be refunded in 2000-01 as the issuers companies could not get 90% subscription.

These issuer companies had not opted for underwriting of these issues. In addition to

this, two book building issues of SIP Technologies and Creative Eyes Ltd. had to be

withdrawn after launch due to poor response from public. Later on, Creative Eye Ltd.

re launched its issue with a lower price band. In 2003-04 also, one issue by Weal

Infotech has to refund the application money for the above stated reason.

Although investors responded favourably for the public issues of equity shares

in

2006-07, but eight equity issues have to be withdrawn due to lack of minimum

subscription. Out of these issues, three were floated in June 2006 and two issues in

March 2007. Depressed secondary market conditions were mainly responsible for

withdrawal of these public issues. Similarly, four issues were withdrawn/ refunded in

2007-08 due to poor response from the investors. Bearish secondary market in the

beginning of the year 2008 forced Wockhardt Hospitals Ltd, Emaar MGF Land Ltd

and SVEC Constructions Ltd to withdraw their equity issues from the market.

During the particular month or one month before the floatation of particular

equity issues to the public, a negative variation was found in BSE Sensex and NSE

Nifty index. For example, In May 2006 and February 2007, the percentage variation

in BSE Sensex has been -13.65% and -8.18% respectively. NSE Nifty varied between

-13.68% and -8.26% for the same period.

Most of the equity issues withdrawn for want of minimum subscription were

of medium size.The size of equity issues withdrawn ranged from Rs. 4.70 crore (Ador

Powerton & Geekay Imaging Ltd. each) to 74.77 crores of Minar International Ltd.

214

Table 7.6 Under Subscription of Public Issues of Equity Shares

Year Issuer Company Date of Issue Issue Size (Rs. crores)

Lead Merchant Banker(s)

2000-01 Arraycom (India) Ltd. May 9-15,2000 58.50 SBI Capital Markets Oceana Software

Solutions Aug. 10-14, 2000 10.00 Systematix Corp.

Services Geekay Imaging Ltd. Sep. 25-27, 2000 4.70 SBI Capital Markets,

Canara bank Ador Powertron Ltd. Jan. 29- Feb.02,

2001 4.70 Brescon Corporates

Globsyn Technologies Ltd.

Feb. 13-20, 2001 21.83 Karvy Investors, UTI Securities.

2003-04 Weal Infotech Ltd. October, 2003 13.90 Aryaman Financial Services

2006-07 Blueplast Industries June 5-9, 2006 32.50 Allianz Securities Vigneshwara Exports June 7-13, 2006 57.60 Karvy Investors. Shirdi Industries Ltd. June 29- July 5,

2006 44.85 Allianz Securities.

Minar International Ltd.

Sep.25-29, 2006 74.77 Keynote Corporate.

Yogindera Worsted Ltd.

Jan.16-22, 2007 14.40 Khandwala Securities.

Tubeknit Fashions Ltd.

Feb.21- March 2, 2007

42.75 Systematix Corporate Services

Vimal Oil & Foods March 14-23, 2007 29.00 Centrum Finance. Ammana Bio Pharma. March 28 – April

5, 2007 20.16 Centrum Finance

2007-08 IT People (India) Ltd. August 27-31, 2007

45.25 Khandwala Securities Religare Securities.

Wockhardt Hospitals Ltd.

January, 31, 2008 702.44 Citigroup Global, Kotak Mahindra

Emaar MGF land Ltd. Feb. 1-6, 2008 5436.24 Citigroup, Enam, DSP Merrill, Goldman Sach, HSBC Sec., JP Morgan, Kotak Mahindra

SVEC Constructions Ltd.

February 4-8, 2008

34.00 Karvy Investors. Centrum Capital.

Source:-Compiled from offer documents, Prime Database, NSE website and SEBI website.

Most of the equity issues withdrawn during the period under review were

generally managed by single lead merchant banker for each issue with the exception

of Geekay Imaging Ltd. and Globsyn Technologies Ltd in 2000-01. However, the

public issues of equity refunded during 2007-08 were all managed by multiple lead

215

merchant bankers. However, no public issue of equity was withdrawn due to lack of

minimum subscription for the remaining period.

In addition to the withdrawn issues of equity shown in the table, six public

issues of equity shares were cancelled by SEBI or withdrawn by the lead managers or

promoters on or before the opening of the subscription list during 1997-98. These

equity issues included:

S.No. Company Issues Rs. (Rs. in Crore)

1. Charishma Overseas Ltd. 7.10

2. Highways Users’ Centres (India) Ltd. 7.00

3. Orissa Securities Ltd. 0.27

4. Seer Finance Ltd. 3.25

5. Supreme Impex Ltd, 0.20

6. Tenashu Electronics & Tele Tech. Ltd. 0.855

Of these six companies, two (Orissa Securities and Supreme Impex) again

entered the primary market and got 1.03 times and 1.06 times subscription from the

public.

7.5 Response to Public Issues of Debt Corporate debt market is an important segment of capital market in any

economy. It provides an option to investors for diversification of risk. During the

period under study, corporate debt market was dominated by bond issues and many

innovations have been witnessed in the corporate bond issues over the years.

Primary corporate debt market, during the period under study, has been

dominated by domestic non banking companies and a very small amount of funds

have been raised by manufacturing and other service industries. Two domestic

financial institutions, ICICI Ltd and IDBI Ltd, have been the major fund raising

institutions through bond issues of various types.

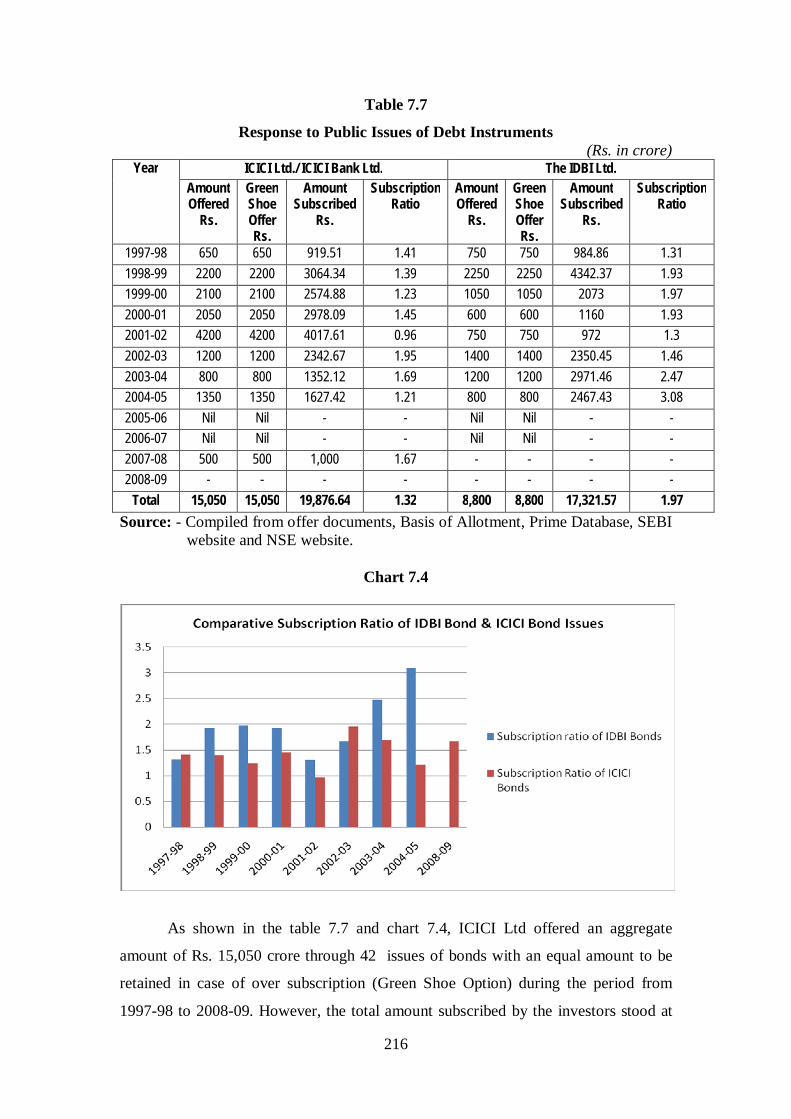

Table 7.7 presents the amount offered through bonds by ICICI Ltd and IDBI

Ltd along with Green Shoe offer. The table also shows the annual amount subscribed

by the public and thus the extent of subscription by investors.

216

Table 7.7

Response to Public Issues of Debt Instruments (Rs. in crore)

Year ICICI Ltd./ ICICI Bank Ltd. The IDBI Ltd. Amount Offered

Rs.

Green Shoe Offer Rs.

Amount Subscribed

Rs.

Subscription Ratio

Amount Offered

Rs.

Green Shoe Offer Rs.

Amount Subscribed

Rs.

Subscription Ratio

1997-98 650 650 919.51 1.41 750 750 984.86 1.31 1998-99 2200 2200 3064.34 1.39 2250 2250 4342.37 1.93 1999-00 2100 2100 2574.88 1.23 1050 1050 2073 1.97 2000-01 2050 2050 2978.09 1.45 600 600 1160 1.93 2001-02 4200 4200 4017.61 0.96 750 750 972 1.3 2002-03 1200 1200 2342.67 1.95 1400 1400 2350.45 1.46 2003-04 800 800 1352.12 1.69 1200 1200 2971.46 2.47 2004-05 1350 1350 1627.42 1.21 800 800 2467.43 3.08 2005-06 Nil Nil - - Nil Nil - - 2006-07 Nil Nil - - Nil Nil - - 2007-08 500 500 1,000 1.67 - - - - 2008-09 - - - - - - - -

Total 15,050 15,050 19,876.64 1.32 8,800 8,800 17,321.57 1.97 Source: - Compiled from offer documents, Basis of Allotment, Prime Database, SEBI

website and NSE website.

Chart 7.4

As shown in the table 7.7 and chart 7.4, ICICI Ltd offered an aggregate

amount of Rs. 15,050 crore through 42 issues of bonds with an equal amount to be

retained in case of over subscription (Green Shoe Option) during the period from

1997-98 to 2008-09. However, the total amount subscribed by the investors stood at

217

Rs. 19,876.64 crore resulting in the subscription ratio of 1.32 times. Thus, it could not

avail the green shoe option to the full extent.

Year wise break up of amount offered, amount subscribed and subscription

ratio of public issues of debt by ICICI Ltd. shows the poor response by investors in

the year 2001-02, when subscription ratio has been only 0.96 times. During this year,

the highest amount of Rs. 4,200 crores was offered to the public by ICICI Ltd through

bonds. However, investors subscribed 1.95 times to the bonds offerings of Rs. 1200

crores during 2002-03. This was followed by 1.41 times subscription to Rs. 1,350

crores bonds offer during 2004-05. Similarly, in 2007-08, Regular Income Bonds of

Rs. 500 crore with a green shoe option was made to investors. The Green shoe option

in this year was fully availed.

IDBI Limited, on the other hand, offered an aggregate amount of Rs. 8,800

crore to the public. An equal amount was offered through green shoe option. It was

able to raise a total amount of Rs. 17321.57 crore through 21 bond issues with an

aggregate subscription of 1.97 times. It has been shown in the table that IDBI Ltd

nearly availed the green shoe option in the years 1998-99, 1999-2000 and 2000-01.

The subscription ratio in these years was 1.93, 1.97 and 1.93 times of amount offered.

It has been the highest (3.08 times) during 2004-05 followed by 2.47 times in 2003-

04.

Comparison of public response to the debt issues by ICICI Ltd. and IDBI Ltd.

shows the comparatively good response to the bonds issues by IDBI Ltd. in all the

years except 1997-98 and 2002-03. This has also been clear from the chart 6.4

showing comparison of subscription ratio of bond issues by ICICI Ltd and IDBI Ltd.

An analysis of offer documents of bond issues by ICICI Ltd and IDBI Ltd.

shows that both these institutions filed an umbrella draft prospectus with SEBI for

public issue of bonds annually for an aggregate amount. That amount has been raised

through a number of tranches within the stipulated period of 365 days from SEBI’s

observation letter.

The issuer company had been given the option to retain any amount

oversubscribed in a particular tranche within the limits of annual aggregate amount of

bond issues approved by the SEBI.

In addition to ICICI Bonds and IDBI Bonds, other small companies who

raised funds through debt issues included Ahmedabad Municipal Corporation Ltd. in

1997-98 (Rs. 25 crore) and Krishna Bhagya Jala Nigam in 2001-02 (Rs. 350 crore).

218

Bonds issue by Ahmedabad Municipal Corporation Ltd got poor response from the

investors with subscription of only 0.25 times. It was managed by IF&FS Investsmart

Securities Ltd. and SBI Capital Markets. However, bonds issues by Krishna Bhagya

Jala Nigam got good response from investors and its bonds were subscribed by 1.80

times of amount offered. This issue was managed by SBI Capital markets Ltd.

A large size debt issue for Rs. 500 crore with green shoe option of Rs. 1,000

crore was made to investors by Tata Capital Limited in 2008-09. However,

subscription for Rs. 2,300 crore was made by investors resulting into 1.53 times

oversubscription. Two foreign based merchant bankers, Citigroup Global, DSP

Merrill and ICICI Securities were the lead managers for this debt issue.

Conclusion As a part of pre issue obligations of lead merchant banker, marketing and

distribution of public issues of securities is a major function of merchant bankers. The

success of public issue depends upon the effective marketing strategy followed by

lead merchant banker and the public response to the securities thereafter. The

obligations of lead merchant bankers with respect to marketing of public issues start

from deciding the time of floatation of issues.

For the protection of interest of investors, SEBI is striving hard for an efficient

and developed capital market. SEBI has made elaborate provisions and Guidelines

for advertisement for issue of securities to the public. Subscription of shares by the

investors is the result of hard work put by the lead manager and the issuing company.

Good public response to the issues enhances the reputation of both lead merchant

banker and the issuing company.

During the period under review, several ups and downs with respect to

response to new issue market of equity and debt has been noticed. Low public

response to new issue market has been found during the first half of period of study.

However, in the second part, a good public response has been noticed in the form of

higher mean subscription ratio both by retail investors and non retail investors. It has

been noted that new issue market generally swings with the secondary market

conditions.

An analysis of subscription ratio of public issue of equity managed by

different merchant bankers lead to the conclusion that the public issues of equity

managed by leading merchant bankers got more favourable response from investors.

219

Two domestic financial institutions, ICICI Ltd. and IDBI Ltd. have been found

to have dominant role in the public issue of debt. Comparative public response to debt

issues has been better to the bond issues of IDBI Ltd than the bond issues of ICICI

Ltd.