Chapter 4 T1shackman/isye6225_Fall...Copyright © 2011 Pearson Prentice Hall. All rights reserved....

71

Copyright © 2011 Pearson Prentice Hall. All rights reserved. Chapter 4 The Time Value of Money

Transcript of Chapter 4 T1shackman/isye6225_Fall...Copyright © 2011 Pearson Prentice Hall. All rights reserved....

Copyright © 2011 Pearson Prentice Hall. All rights reserved.

Chapter 4

The Time Value of Money

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-2

Chapter Outline

4.1 The Timeline

4.2 The Three Rules of Time Travel

4.3 Valuing a Stream of Cash Flows

4.4 Calculating the Net Present Value

4.5 Perpetuities, Annuities, and Other Special Cases

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-3

Chapter Outline (cont’d)

4.6 Solving Problems with a Spreadsheet Program

4.7 Solving for Variables Other Than Present Value or Future Value

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-4

4.1 The Timeline

• A timeline is a linear representation of the timing of potential cash flows.

• Drawing a timeline of the cash flows will help you visualize the financial problem.

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-5

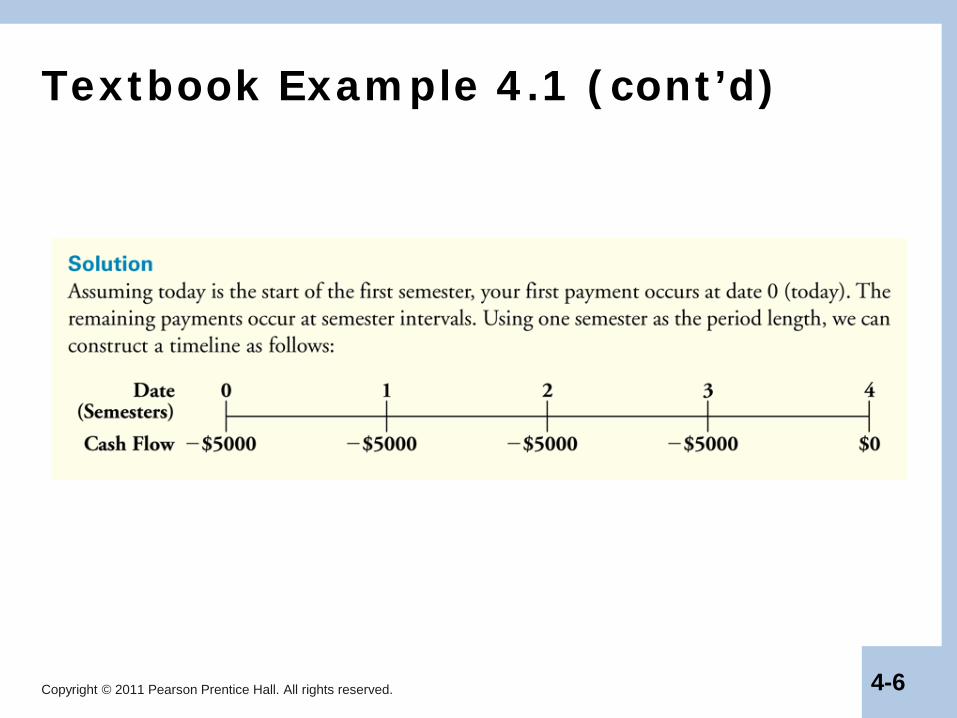

Textbook Example 4.1

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-6

Textbook Example 4.1 (cont’d)

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-7

4.2 Three Rules of Time Travel

• Financial decisions often require combining cash flows or comparing values. Three rules govern these processes.

Table 4.1 The Three Rules of Time Travel

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-8

The 1st Rule of Time Travel

• A dollar today and a dollar in one year are not equivalent.

• It is only possible to compare or combine values at the same point in time. – Which would you prefer: A gift of $1,000 today

or $1,210 at a later date? – To answer this, you will have to compare the

alternatives to decide which is worth more. One factor to consider: How long is “later?”

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-9

The 2nd Rule of Time Travel

• To move a cash flow forward in time, you must compound it. – Suppose you have a choice between receiving

$1,000 today or $1,210 in two years. You believe you can earn 10% on the $1,000 today, but want to know what the $1,000 will be worth in two years. The time line looks like this:

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-10

(1 ) (1 ) (1 ) (1 ) times

= × + × + × × + = × +

nnFV C r r r C r

n

The 2nd Rule of Time Travel (cont’d)

• Future Value of a Cash Flow

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-11

Textbook Example 4.2

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-12

Textbook Example 4.2 (cont’d)

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-13

Alternative Example 4.2

• Problem – Suppose you have a choice between receiving

$5,000 today or $10,000 in five years. You believe you can earn 10% on the $5,000 today, but want to know what the $5,000 will be worth in five years.

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-14

0 3 4 521

$5,000 $5, 500 $6,050 $6,655 $7,321 $8,053x 1.10 x 1.10 x 1.10 x 1.10 x 1.10

Alternative Example 4.2 (cont’d)

• Solution – The time line looks like this:

– In five years, the $5,000 will grow to: $5,000 × (1.10)5 = $8,053 – The future value of $5,000 at 10% for five years

is $8,053.

– You would be better off forgoing the gift of $5,000 today and taking the $10,000 in five years.

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-15

The 3rd Rule of Time Travel

• To move a cash flow backward in time, we must discount it.

• Present Value of a Cash Flow

(1 ) (1 )

= ÷ + =+

nn

CPV C rr

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-16

Textbook Example 4.3

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-17

Textbook Example 4.3

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-18

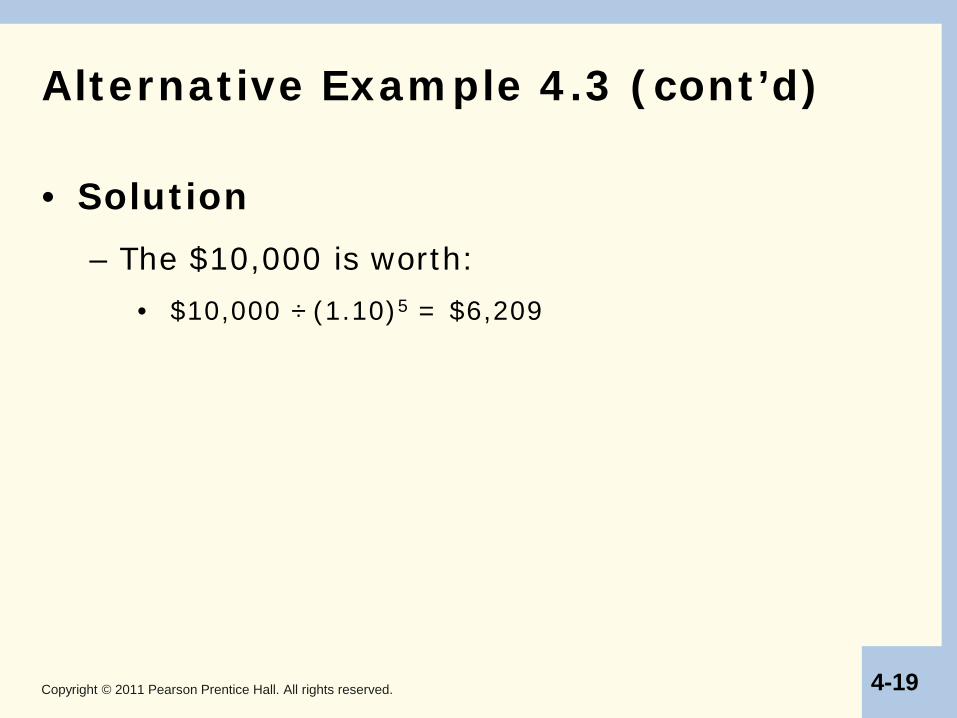

Alternative Example 4.3

• Problem – Suppose you are offered an investment that

pays $10,000 in five years. If you expect to earn a 10% return, what is the value of this investment today?

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-19

Alternative Example 4.3 (cont’d)

• Solution – The $10,000 is worth:

• $10,000 ÷ (1.10)5 = $6,209

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-20

Applying the Rules of Time Travel

• Recall the 1st rule: It is only possible to compare or combine values at the same point in time. So far we’ve only looked at comparing. – Suppose we plan to save $1000 today, and

$1000 at the end of each of the next two years. If we can earn a fixed 10% interest rate on our savings, how much will we have three years from today?

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-21

Applying the Rules of Time Travel (cont'd)

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-22

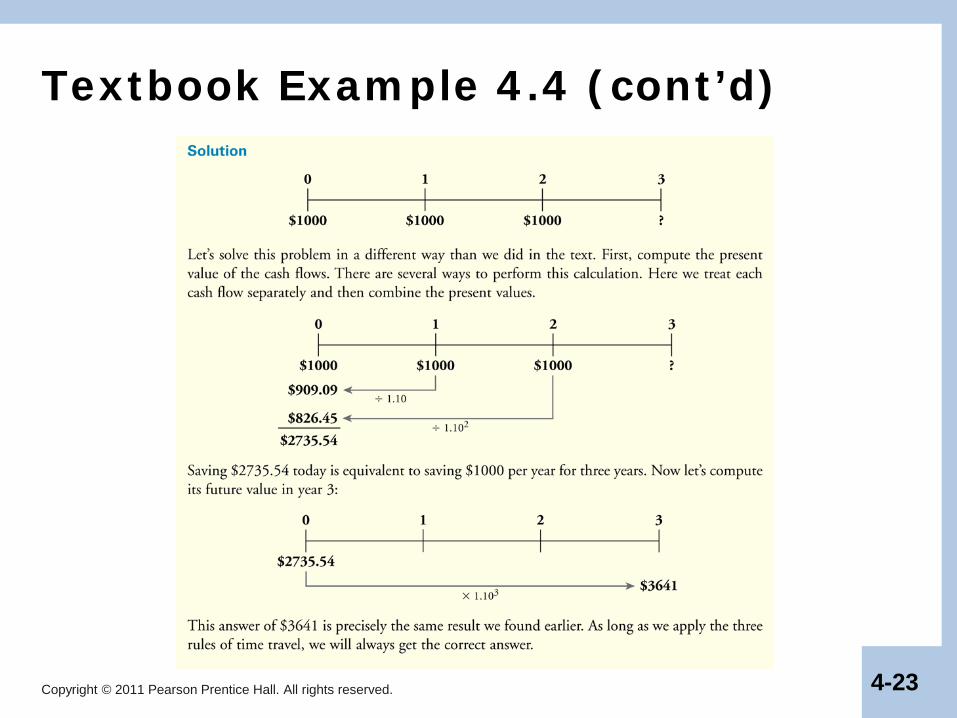

Textbook Example 4.4

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-23

Textbook Example 4.4 (cont’d)

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-24

0 3 4 521

$10,000$5,000

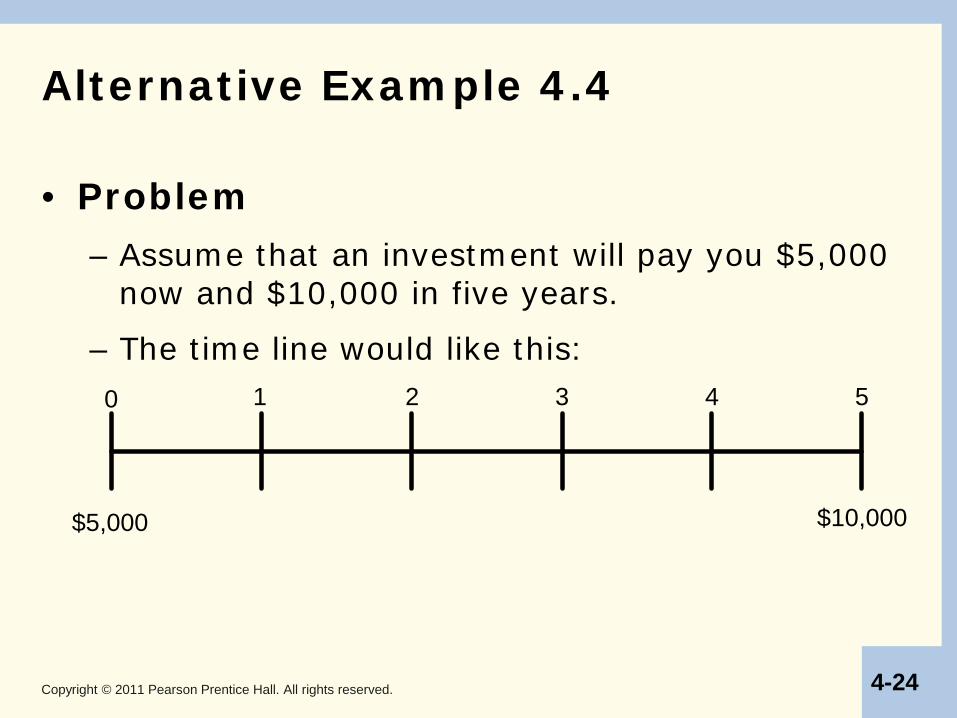

Alternative Example 4.4

• Problem – Assume that an investment will pay you $5,000

now and $10,000 in five years.

– The time line would like this:

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-25

0 3 4 521

$6,209 $10,000$5,000

$11,209 ÷ 1.105

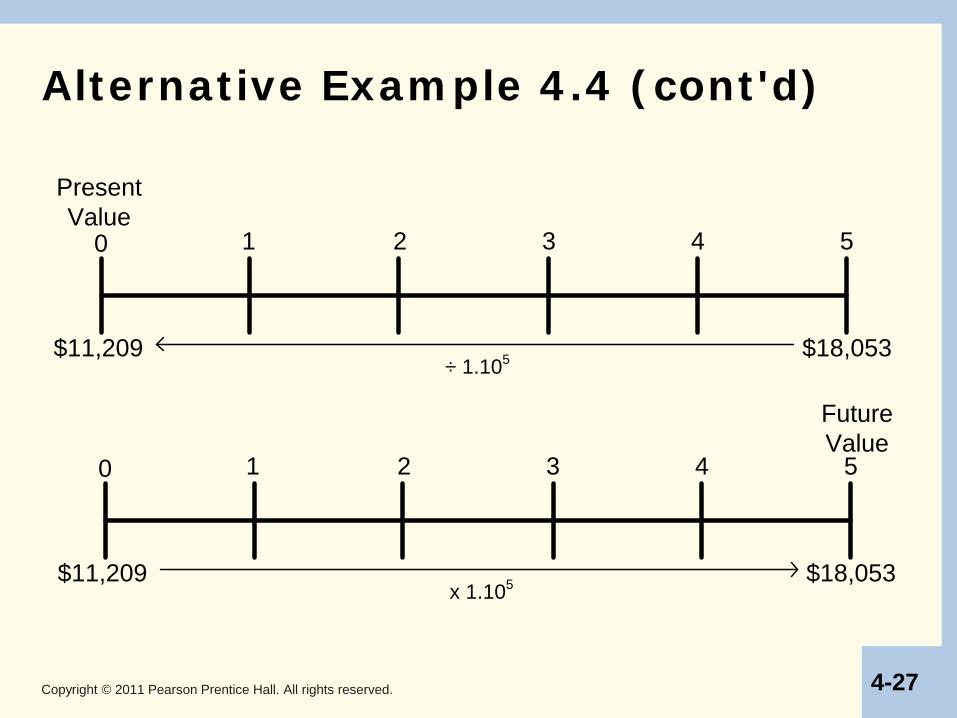

Alternative Example 4.4 (cont'd)

• Solution – You can calculate the present value of the combined cash

flows by adding their values today.

– The present value of both cash flows is $11,209.

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-26

Alternative Example 4.4 (cont'd)

• Solution – You can calculate the future value of the

combined cash flows by adding their values in Year 5.

– The future value of both cash flows is $18,053.

0 3 4 521

$5,000 $8,053x 1.105

$10,000

$18,053

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-27

0 3 4 521

$11,209 $18,053÷ 1.105

0 3 4 521

$11,209 $18,053x 1.105

Present Value

Future Value

Alternative Example 4.4 (cont'd)

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-28

4.3 Valuing a Stream of Cash Flows (cont’d)

• Present Value of a Cash Flow Stream

0 0 ( )

(1 )= =

= =+∑ ∑

N Nn

n nn n

CPV PV Cr

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-29

Textbook Example 4.5

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-30

Textbook Example 4.5 (cont’d)

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-31

(1 )= × + nnFV PV r

Future Value of Cash Flow Stream

• Future Value of a Cash Flow Stream with a Present Value of PV

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-32

Alternative Example 4.5

• Problem – What is the future value in three years of the

following cash flows if the compounding rate is 5%?

0 321

$2,000 $2,000 $2,000

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-33

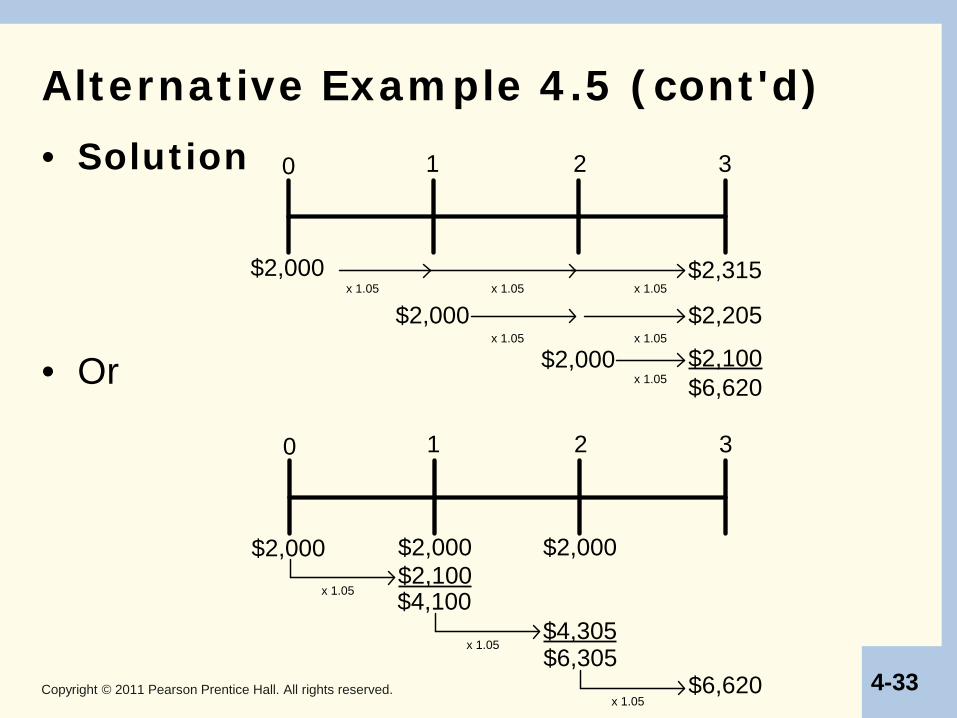

Alternative Example 4.5 (cont'd) • Solution

• Or

0 321

$2,000

$2,000x 1.05 x 1.05

$2,315x 1.05

$2,205

$2,000x 1.05 x 1.05

$2,100$6,620x 1.05

0 321

$2,000x 1.05 $4,100

$2,100

$4,305

$2,000 $2,000

x 1.05$6,305

x 1.05$6,620

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-34

4.4 Calculating the Net Present Value

• Calculating the NPV of future cash flows allows us to evaluate an investment decision.

• Net Present Value compares the present value of cash inflows (benefits) to the present value of cash outflows (costs).

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-35

Textbook Example 4.6

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-36

Textbook Example 4.6 (cont'd)

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-37

0 321

$1,000$3,000 $2,000

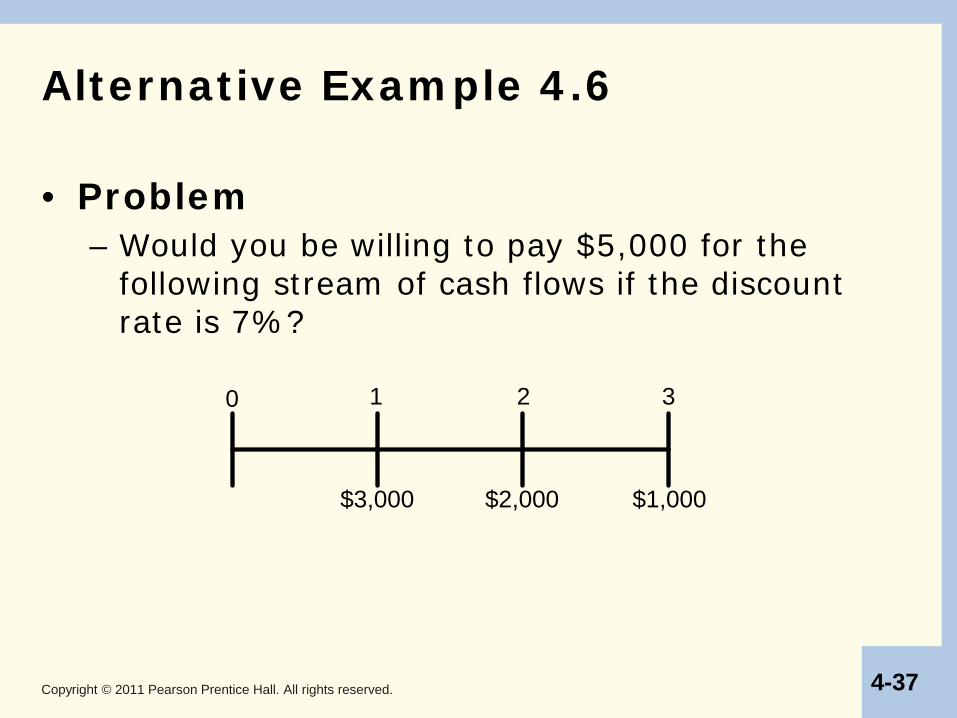

Alternative Example 4.6

• Problem – Would you be willing to pay $5,000 for the

following stream of cash flows if the discount rate is 7%?

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-38

Alternative Example 4.6 (cont’d)

• Solution – The present value of the benefits is: 3000 / (1.05) + 2000 / (1.05)2 + 1000 / (1.05)3 =

5366.91

– The present value of the cost is $5,000, because it occurs now.

– The NPV = PV(benefits) – PV(cost)

= 5366.91 – 5000 = 366.91

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-39

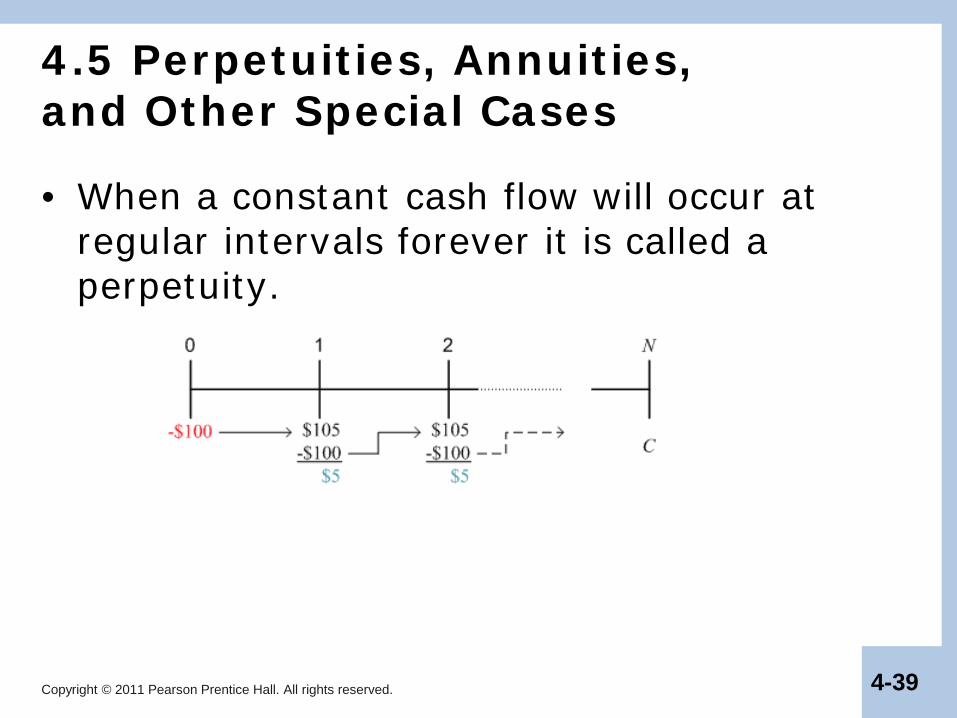

4.5 Perpetuities, Annuities, and Other Special Cases

• When a constant cash flow will occur at regular intervals forever it is called a perpetuity.

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-40

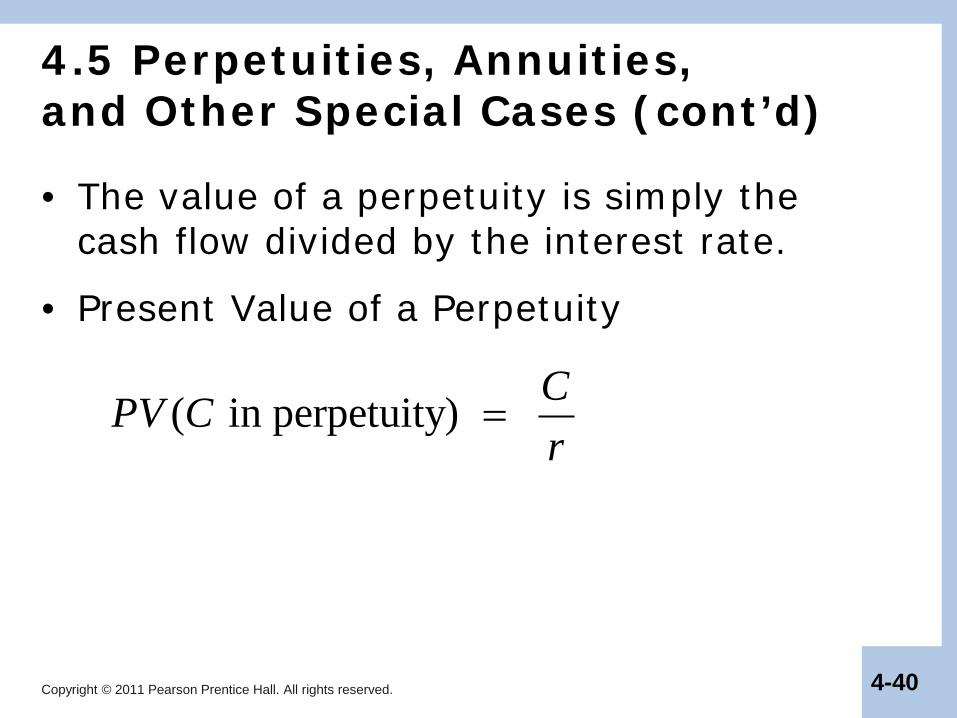

4.5 Perpetuities, Annuities, and Other Special Cases (cont’d)

• The value of a perpetuity is simply the cash flow divided by the interest rate.

• Present Value of a Perpetuity

( in perpetuity) =CPV Cr

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-41

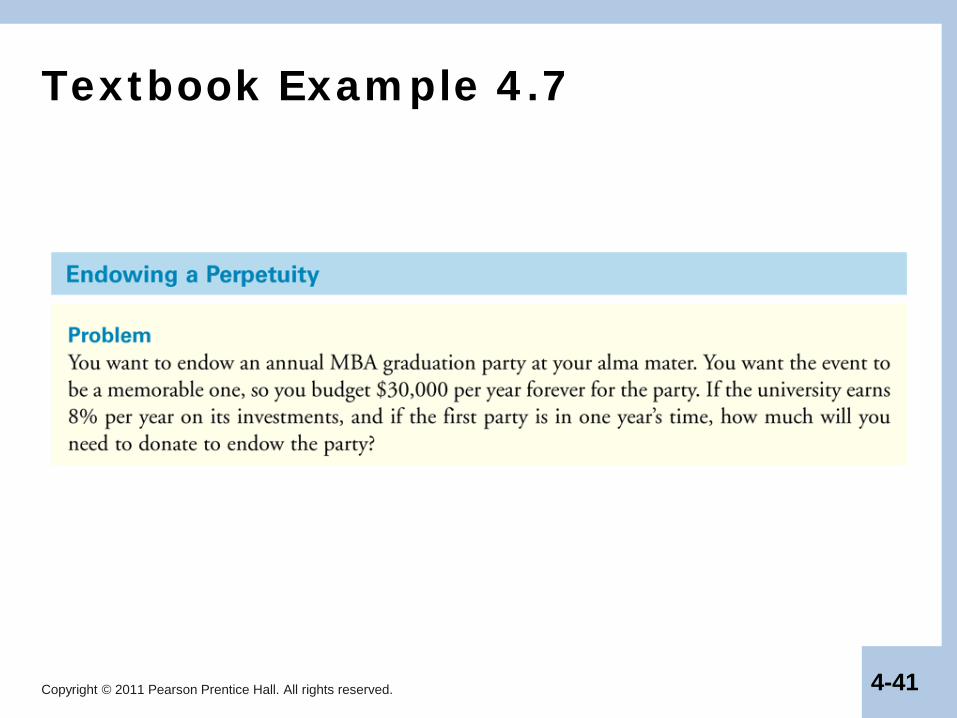

Textbook Example 4.7

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-42

Textbook Example 4.7 (cont’d)

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-43

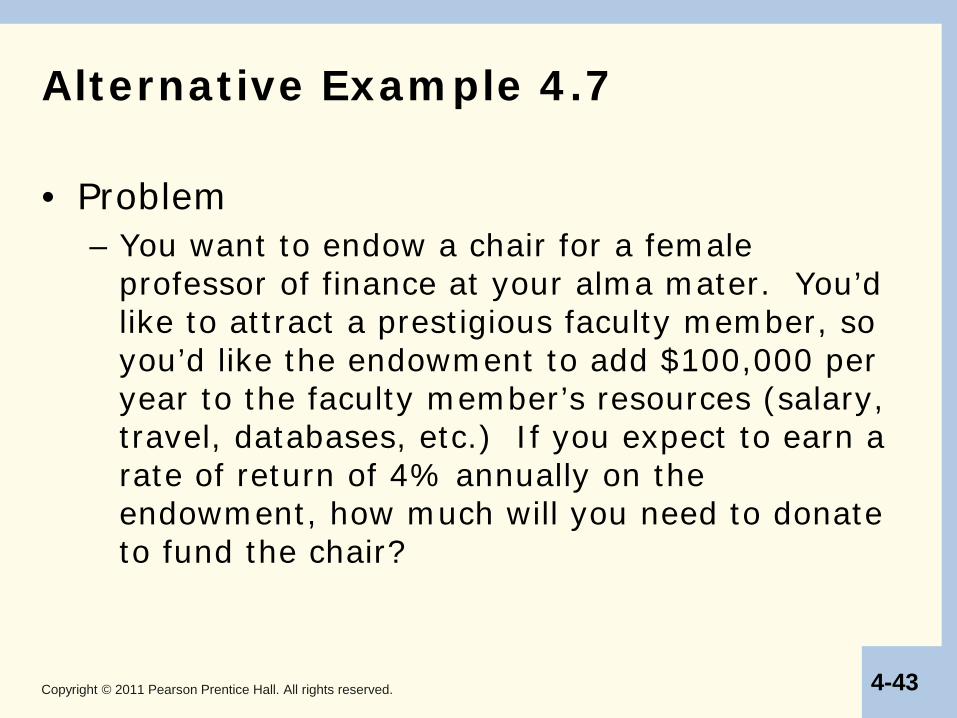

Alternative Example 4.7

• Problem – You want to endow a chair for a female

professor of finance at your alma mater. You’d like to attract a prestigious faculty member, so you’d like the endowment to add $100,000 per year to the faculty member’s resources (salary, travel, databases, etc.) If you expect to earn a rate of return of 4% annually on the endowment, how much will you need to donate to fund the chair?

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-44

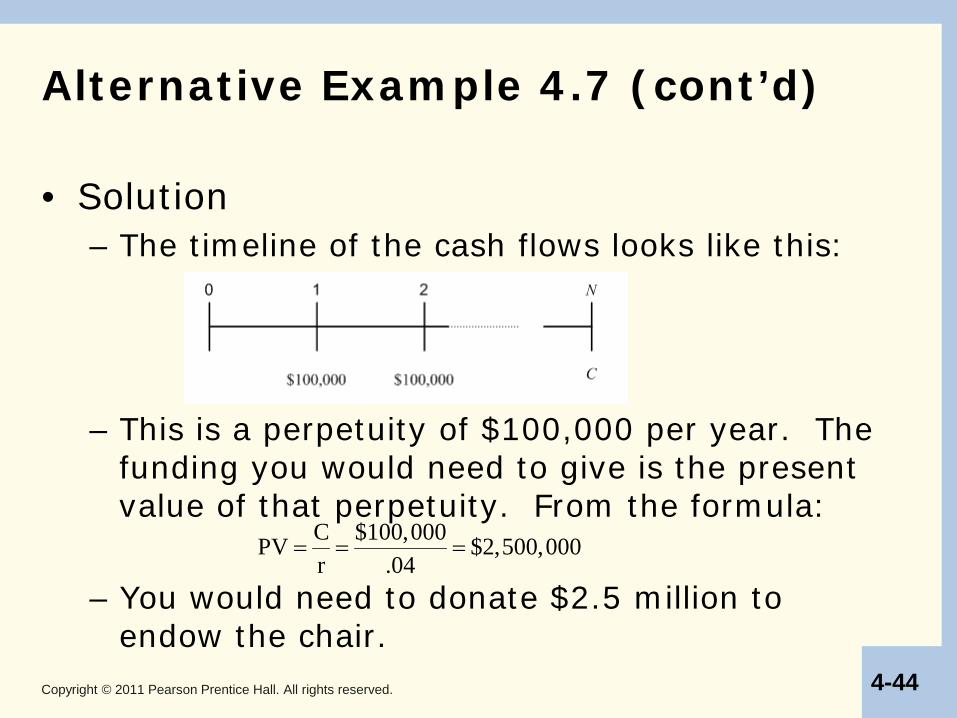

Alternative Example 4.7 (cont’d)

• Solution – The timeline of the cash flows looks like this:

– This is a perpetuity of $100,000 per year. The funding you would need to give is the present value of that perpetuity. From the formula:

– You would need to donate $2.5 million to endow the chair.

C $100,000PV $2,500,000r .04

= = =

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-45

Annuities

• When a constant cash flow will occur at regular intervals for a finite number of N periods, it is called an annuity.

• Present Value of an Annuity ∑

+=

+++

++

++

+=

=

N

1nnN32 )r1(

C)r1(

C...)r1(

C)r1(

C)r1(

CPV

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-46

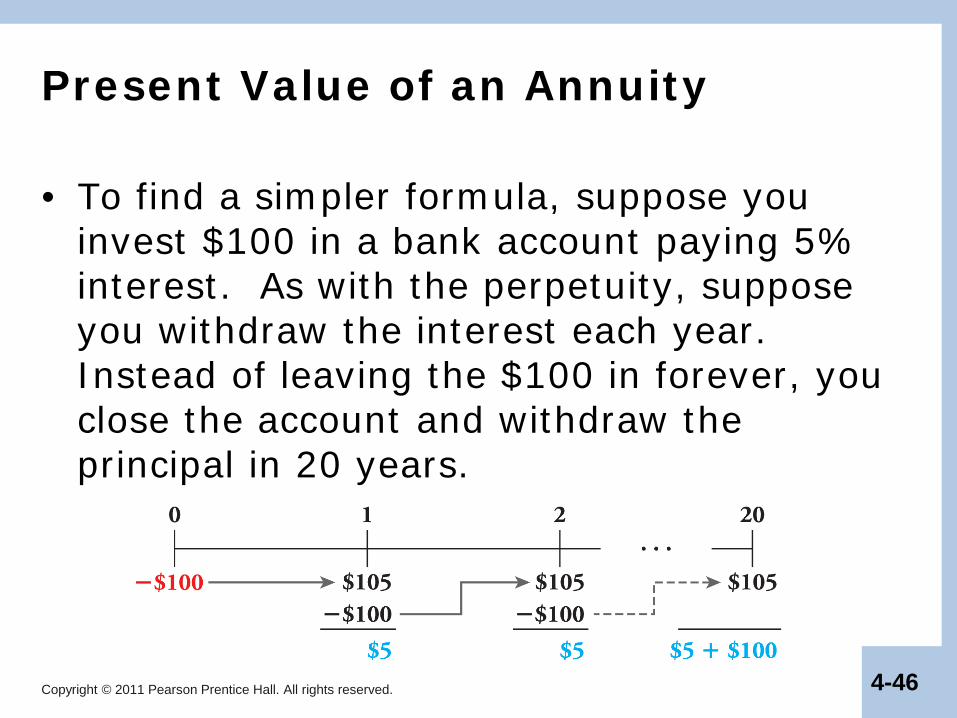

Present Value of an Annuity

• To find a simpler formula, suppose you invest $100 in a bank account paying 5% interest. As with the perpetuity, suppose you withdraw the interest each year. Instead of leaving the $100 in forever, you close the account and withdraw the principal in 20 years.

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-47

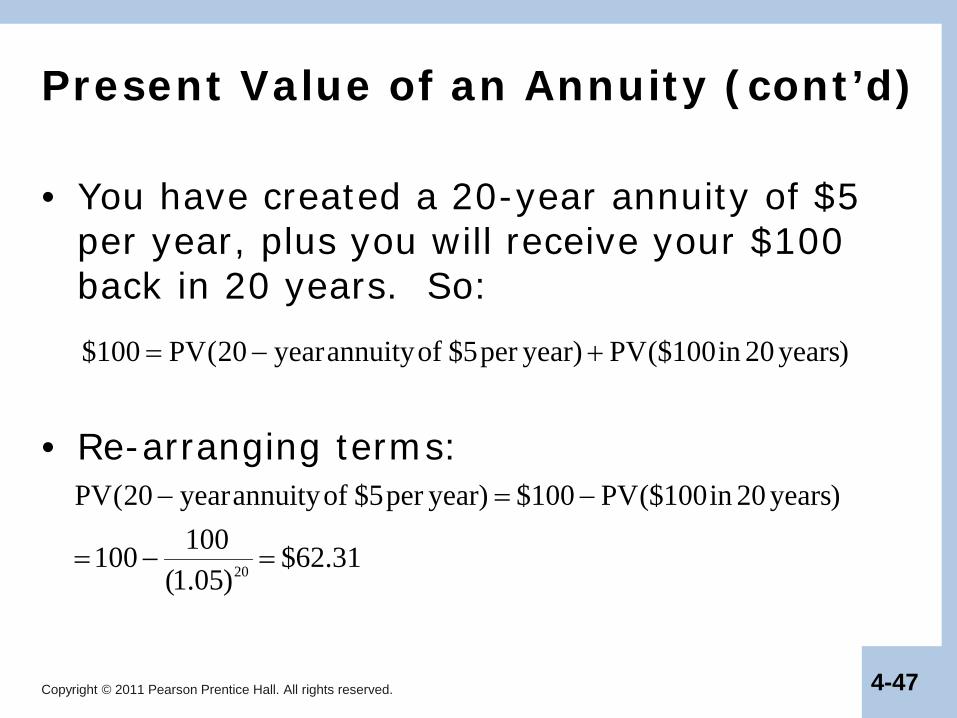

Present Value of an Annuity (cont’d)

• You have created a 20-year annuity of $5 per year, plus you will receive your $100 back in 20 years. So:

• Re-arranging terms:

)years20in100($PV)yearper5$ofannuityyear20(PV100$ +−=

31.62$)05.1(

100100

)years20in100($PV100$)yearper5$ofannuityyear20(PV

20 =−=

−=−

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-48

Present Value of an Annuity

• For the general formula, substitute P for the principal value and:

N N

PV(annuityof Cfor N periods)P PV(Pin period N)

P 1P P 1(1 r) (1 r)

= −

= − = − + +

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-49

Textbook Example 4.8

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-50

Textbook Example 4.8

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-51

Future Value of an Annuity

• Future Value of an Annuity

( )

(annuity) V (1 )

1 1 (1 )(1 )

1 (1 ) 1

= × +

= − × + +

= × + −

N

NN

N

FV P r

C rr r

C rr

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-52

Textbook Example 4.9

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-53

Textbook Example 4.9 (cont’d)

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-54

Growing Perpetuities

• Assume you expect the amount of your perpetual payment to increase at a constant rate, g.

• Present Value of a Growing Perpetuity

(growing perpetuity)

=−CPV

r g

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-55

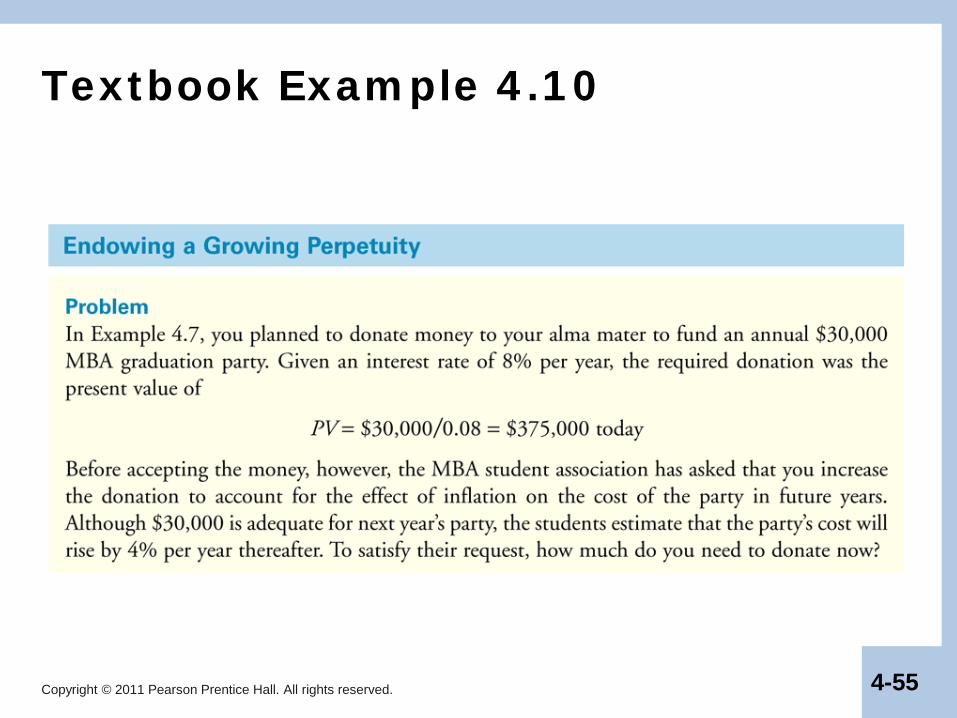

Textbook Example 4.10

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-56

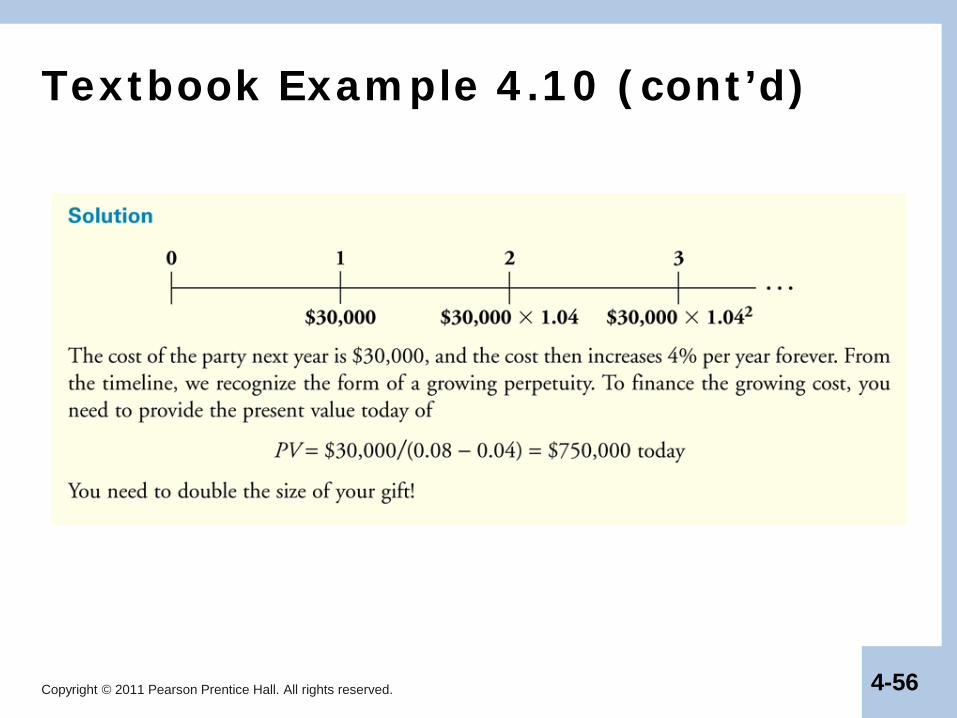

Textbook Example 4.10 (cont’d)

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-57

Alternative Example 4.10

• Problem – In Alternative Example 4.7, you planned to

donate money to endow a chair at your alma mater to supplement the salary of a qualified individual by $100,000 per year. Given an interest rate of 4% per year, the required donation was $2.5 million. The University has asked you to increase the donation to account for the effect of inflation, which is expected to be 2% per year. How much will you need to donate to satisfy that request?

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-58

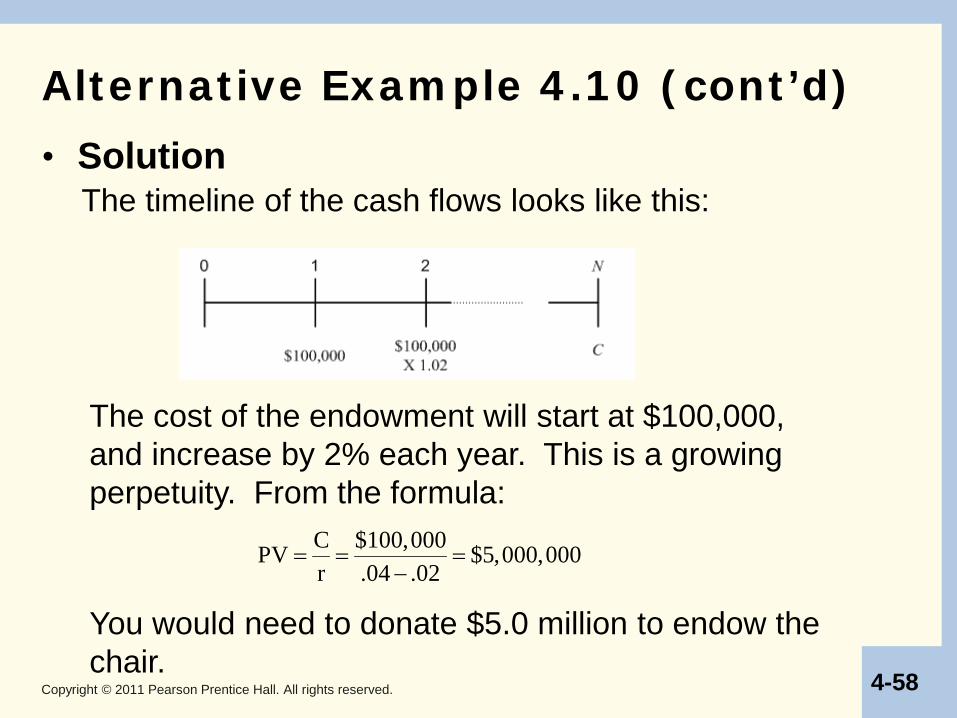

Alternative Example 4.10 (cont’d)

The timeline of the cash flows looks like this:

The cost of the endowment will start at $100,000, and increase by 2% each year. This is a growing perpetuity. From the formula:

C $100,000PV $5,000,000r .04 .02

= = =−

You would need to donate $5.0 million to endow the chair.

• Solution

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-59

Growing Annuities

• The present value of a growing annuity with the initial cash flow c, growth rate g, and interest rate r is defined as: – Present Value of a Growing Annuity

1 1 1 ( ) (1 )

+ = × − − +

NgPV C

r g r

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-60

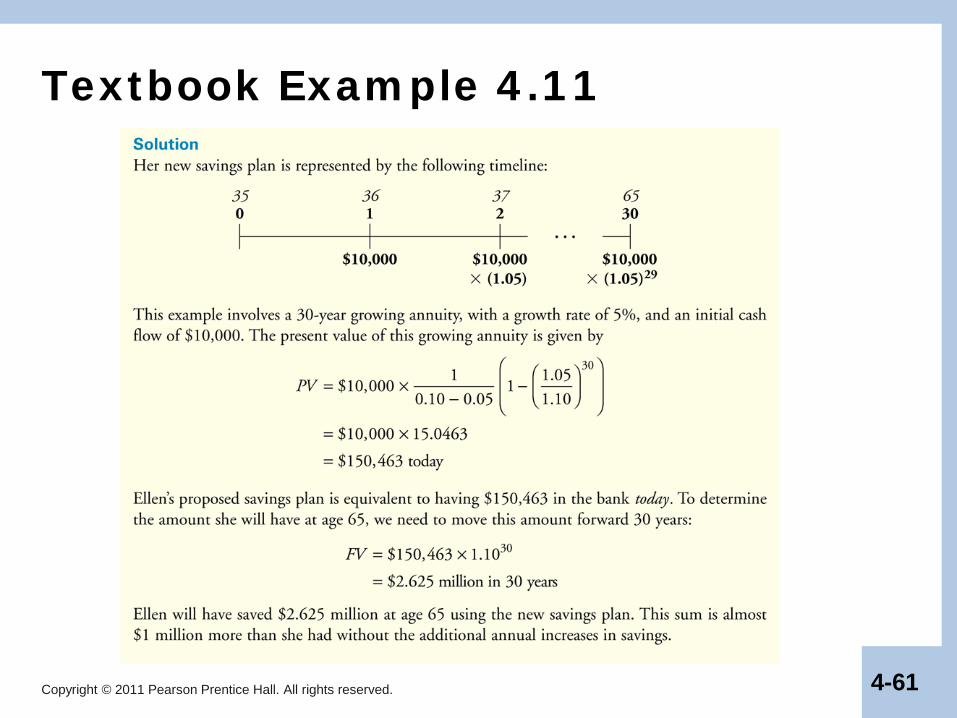

Textbook Example 4.11

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-61

Textbook Example 4.11

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-62

4.7 Solving for Variables Other Than Present Values or Future Values

• Sometimes we know the present value or future value, but do not know one of the variables we have previously been given as an input. For example, when you take out a loan you may know the amount you would like to borrow, but may not know the loan payments that will be required to repay it.

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-63

Textbook Example 4.14

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-64

Textbook Example 4.14 (cont’d)

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-65

4.7 Solving for Variables Other Than Present Values or Future Values (cont’d)

• In some situations, you know the present value and cash flows of an investment opportunity but you do not know the internal rate of return (IRR), the interest rate that sets the net present value of the cash flows equal to zero.

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-66

Textbook Example 4.15

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-67

Textbook Example 4.15 (cont’d)

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-68

Textbook Example 4.16

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-69

Textbook Example 4.16 (cont’d)

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-70

Textbook Example 4.17

Copyright © 2011 Pearson Prentice Hall. All rights reserved. 4-71

Textbook Example 4.17

![[Pearson - Prentice Hall] Fisica 1 - Antonio Lara](https://static.fdocuments.net/doc/165x107/55cf98a6550346d03398dee0/pearson-prentice-hall-fisica-1-antonio-lara.jpg)