CHAPTER-4 CAPITAL STRUCTURE & ITS COMPONENTS ...

37

122 CHAPTER-4 CAPITAL STRUCTURE & ITS COMPONENTS (TRENDS & PATTERNS) 4.1 TRENDS IN CORPORATE CAPITAL STRUCTURE AND ITS ANALYSIS. The financial decision occupy a pivotal role in the overall finance function in a corporate firm which mainly concern itself with an efficient utilization of the funds provided by the owners or obtained from external sources together with those retained or ploughed back out of surplus or undistributed profits. These decisions are mainly in the nature of planning the capital structure, working capital sand mechanism through which funds can be raised from the capital market whenever required. The financing decision explain how to plan an appropriate financing mix the least cost, how to raise long term funds, and how to mobilize the funds for working capital within a short span of time. Such a financing policy provides an appropriate backdrop for formulating effective policies for investment of funds as well as management of earnings. It contributes to magnifying the earnings on equity as profitability (expressed as return on equity), to a large extent, is dependent on the degree of leverage in the capital structure. Besides this valuation and structure of physical assets depends fundamentally on the financing mix. This makes it necessary for the management of a firm to propose a well thought out financing policy, which ought to be framed initially, incorporating, among things the proportion of debt and equity, types of debt and owned funds to be used and volume of funds to be raised from each source or combination of sources, to unable the firm to have a proper capitalization or under capitalization impending its smooth financial functioning. It is obvious that financing decisions are extremely important for corporate firms. Such decisions, in management parlance, are termed as capital structure decisions. 4.2 Capital Structure Capital structure ordinarily implies the proportion of debt and equity in total capital of a company. Since a company may tap any one or more of the different available

Transcript of CHAPTER-4 CAPITAL STRUCTURE & ITS COMPONENTS ...

122

CHAPTER-4

CAPITAL STRUCTURE & ITS COMPONENTS

(TRENDS & PATTERNS)

4.1 TRENDS IN CORPORATE CAPITAL STRUCTURE AND ITS

ANALYSIS.

The financial decision occupy a pivotal role in the overall finance function in a

corporate firm which mainly concern itself with an efficient utilization of the funds

provided by the owners or obtained from external sources together with those retained

or ploughed back out of surplus or undistributed profits. These decisions are mainly in

the nature of planning the capital structure, working capital sand mechanism through

which funds can be raised from the capital market whenever required. The financing

decision explain how to plan an appropriate financing mix the least cost, how to raise

long term funds, and how to mobilize the funds for working capital within a short

span of time. Such a financing policy provides an appropriate backdrop for

formulating effective policies for investment of funds as well as management of

earnings. It contributes to magnifying the earnings on equity as profitability

(expressed as return on equity), to a large extent, is dependent on the degree of

leverage in the capital structure. Besides this valuation and structure of physical assets

depends fundamentally on the financing mix. This makes it necessary for the

management of a firm to propose a well thought out financing policy, which ought to

be framed initially, incorporating, among things the proportion of debt and equity,

types of debt and owned funds to be used and volume of funds to be raised from each

source or combination of sources, to unable the firm to have a proper capitalization or

under capitalization impending its smooth financial functioning.

It is obvious that financing decisions are extremely important for corporate firms.

Such decisions, in management parlance, are termed as capital structure decisions.

4.2 Capital Structure

Capital structure ordinarily implies the proportion of debt and equity in total capital of

a company. Since a company may tap any one or more of the different available

123

source of funds to meet its total financial requirements. The total capital of a company

may, thus, be composed of all such tapped sources. The term structures have been

associated with the term capital. The term capital may be defined as the long term

funds of the firm. Capital is the aggregation of the items appearing on the left hand

side of the balance sheet minus current liabilities. In other words capital may also be

expressed as follows: Capital = Total Assets – Current Liabilities. Further, capital of

the company may broadly be categorized into ‘equity’ and ‘debt’.

• Equity consists of the following:

Equity share capital + Preference share capital + Share premium + Free reserves +

Surplus profits + Discretionary provisions for contingency + Development rebate

reserve.

• Debt consists of Following:

All borrowing from Government, Semi Government, statutory financial corporation

and other agencies + Term Loans from Banks, Financial institutions etc. + Debentures

+ All deferred Payment Liabilities.

4.3 Salient Features of Various Sources of Funds.

The salient features of the aforesaid sources of funds are outline as follows:

4.3.1 Sources of Owned Capital.

This comprises equity, preference share capital and retained earnings.

(1) Equity Capital: Equity shareholders are the owner of a corporate firm.

They share its profits and also participate in residual earnings and

properties which are left after meeting other expenses including financial

changes and taxes. It is also describe as risk capital because at time of

liquidation of a corporate firm equity shareholders receive only the balance

amount payable after the all charges. Thus the risk is higher in case of

equity capital both in respect of repayment of principal and return thereon.

The issue of equity capital is expected to provide a sound base not only

from keeping a desired “debt/equity ratio” but also to exploit it to

maximize benefits to the shareholders by allowing greater scope for

trading on equity. Following this reasoning, corporate firms have shown

124

greater interest in this source, even though it does not confer any tax

benefits.

(2) Preference Share Capital: Preference shareholders enjoy preferential rights

as compared to equity shareholders both in respect of dividends and

repayment of capital either during the life time or on winding up of the

corporate firm. On certain attributes of this source such as fixed dividend

rate and absence of any tax benefits, it is considered to be a relatively

weak corporate security. Accordingly this source has become unpopular

amongst the corporate firms. As most of the companies have not issued

preference share capital, this is excluded from the study.

(3) Retained earnings: A corporate firm can finance its developmental

activities from internal surpluses. That means instead of allocating the

entire profits for distribution as dividends, portion of the profits is kept in

the firm for financing the future plans for growth. Being a part of profit

earned by the firm, retained earnings belong to the owners of the firm.

Therefore, this source forms a part of equity fund. The percentage of

profits to be retained in the firm depends on a variety of factors such as the

nature of industry, magnitude of profitability, tax burden, expectation of

shareholders and attitude of the management towards allocation of profits,

etc.

4.3.2 Borrowed Funds

A corporate firm could also avail itself of funds from borrowed sources for meeting

the financial requirements of long term as well as short term duration. Most of the

growing and well established corporate firms invariably favor employing borrowed

funds as they are relatively less costly sources of finance. They lead to savings in

corporate income tax and help to avoid dilution of voting power. These sources

broadly include debenture capital, term loans, differed credit and public deposits, etc.

(1) Debentures: A corporate firm may be issue convertible or non-convertible

debentures. The debentures are converted at the option of the holders in to

ordinary shares under specific terms and conditions. Ordinarily, debentures are

issued for a longer period, say seven to fifteen years, provided they are

redeemable. Theoretically, irredeemable debenture issues could also be

125

attempted. It is surprising to note that most of the companies in Andhra

Pradesh have not issued debentures. Most of the companies are depending on

the other forms of debt.

(2) Term Loan: this source represents borrowing from domestic or international

financial institutions against security of fixed assets. Term loans are generally

repayable in sixteen to eighteen equal half-yearly installments after a grace

period of two or three years. This has become an important source for rising

long term funds for newly established firms in view of the very limited scope

for raising funds from the capital market.

(3) Deferred Credit: A company can resort to credit facilities extended by the

foreign suppliers to import capital asset or technology. It has to pay in

installments spread over periods ranging from seven to fifteen years. The

suppliers obtain promissory notes signed by the buyer for each installment and

they discount it with their bankers, the buyer is required to execute promissory

notes and obtain a ban guarantee.

(4) Public Deposits: A corporate firm can accept deposits which represent

unsecured borrowings form the public at large. The maturity period for public

deposit is usually one to three days. With the help of this source, it is possible

to mobilize sufficient funds by attracting certain classes of investors due to

higher interest rates thereon than the prevailing rate of return on bank deposits

other instruments such as preference shares. This form of debt is also not

present in the sampled units.

(5) Cash Credits and Bank Overdrafts: A corporate firm can obtained short-term

credit facilities from commercial banks to meet working capital requirements.

This credit facility is obtained either in the form of cash credit bank overdraft

wherein interest is changed normally on the amount actually drawn or used. In

addition, the corporate firm can also avail itself of temporary loan facility by

discounting commercial papers with the banks. Considering the ease of access,

ready availability of funds and relative cost, all discounting has become a

customary practice for corporate firms for using necessary short-term capital

from the commercial banks.

126

(6) Total Debt: Debentures issued by the companies, bank loans, other secured

loans are included under the total debt. The average total debt of the

companies for the study of 7 years is presented in table 4.1 and 4.3 of all the

18 units of the sample of cement and Automobile industries.

4.4 Constraints on Capital Structure Decision:

In view of availability on numerous sources of funds, the planning of capital structure

involves decision making about three basic issues, namely, should be the debt/equity

ratio, which sources of borrowed and owned funds should be used, and the other

criteria to be applied to strike optimality. These decisions could be taken after giving

due thought to the following constraints.

4.5 Factors Influencing Capital Structure

1. Tax Advantage of Debt: The first factor the tax advantage of debt. Interest

paid on is deductible from income and reduces a firm’s tax liabilities,

therefore, debt has a tax advantage over equity and by increasing the amount

of debt issued, and a firm increases its earnings available to shareholders.

2. Investors’ attitude to risk and return: The second factor is related to segmented

market, with different sets of investors measuring risk differently or simply

charging different rates on the capital that they invest. By choosing the

instrument that taps the cheapest market, firms lower their cost of capital.

However the trade off in terms of availability of funds always exists.

3. Financing decision and firm’s risk exposure: The third factor is the impact of

financing decisions on the riskiness of a firm. As firms pile or more and more

debt, their ability to meet fixed interest payments out of current earnings

diminished. This affects the profitability of bankruptcy and as a result, the cost

(or risk premium) of both debt and equity. Firms that adjust their capital

structure in order to keep the riskiness of their debt and equity reasonable

should have a lower cost of capital.

4. Flexibility: It is more important consideration with the raising of debt is

flexibility. As and when the funds required, the debt may be raised and it can

be paid off and when desired. But in case of equity, once the fund rose through

issue of equity shares, it cannot ordinarily be reduces except with the

127

permission of the court and compliance with lot of legal provisions. Hence,

debt capital has to get the characteristic of greater flexibility than equity

capital, which will influence the capital structure decisions.

5. Timing: The timing at which the capital structure decision is taken will be

influenced by the boom or recession conditions of the economy. In times of

boom, it would be easier for the firm to raise equity, but in times of recession,

the equity investors will not show much of interest in investing. Then the firm

is to rely in raising debt.

6. Legal Provisions: Legal provisions in raising capital will also play a

significant role in planning capital structure. Rising of equity capital is more

complicated than raising debt.

7. Profitability of the Company: A Company with higher profitability will have

low reliance on outside debt and it will meet its additional requirement

through internal generation.

8. Growing companies: The growing companies will require more than more

funds for its. Expansion schemes, which will be met through raising debt.

4.6 Analysis of the Capital Structure.

It is essential to know how to analyze the concept of capital structure. One approach

to this is to use leverage terminology. As stated earlier, leverage presents the use of

fixed cost bearing securities such as debt and preference capital lieu of equity for

raising funds. Therefore, the degree of leverage could be employed both for

examining the proportion of debt fund in the capital structure as well as for analyzing

its impact on the benefits to the shareholders as normally it is expected that the use of

debt should be beneficial to the shareholders.

The magnitude of the debt finance in the capital structure could be combined by using

three different ratios namely debt/equity ratio, debt to capital employed ratio and

interest coverage ratio. But hare the study is affected to the debt to capital employed

ratio only.

128

4.6.1 Debt to capital employed ratio: This ratio represents the degree of relationship

between debt and capital employed and is expressed in percentage as below

���

������ ���� ��� � 100

As the debt may be considered as long term and short term either independently or

combine, debt to capital employed ratio could be classified in to three categories.

Short term debt to capital employed ratio: Wherein capital employed is comprised

of net worth and short term debt only.

Long term debt to capital employed ratio: Wherein capital employed is comprised

of net worth and long term debt only.

Total debt to capital employed ratio: Wherein capital employed is comprised of net

worth, short term and long term debt only.

Of the above three ratios, the second ration namely long term debt to capital

employed is used in macro analysis as the debt/equity norm, which is inspected to be

used as a focal point for arriving at desired debt/equity ratio, is always fixed with

respect to long term debt equity ratio only. On the other hand, the third ratio debt to

capital employed is used in micro study.

4.6.2 Equity to capital employed:

There is yet another alternative way of expressing basic relationship between debt and

equity. If one wants to know, how much funds are contributed together by the lenders

and owners for each rupee of owner’s contribution? This can be found out by

calculating the ratio of equity to capital employed or net worth to assets. Here equity

means shareholders fund or net worth calculated as follows.

Paid-up share capital + share premium + reserves and surplus – accumulated losses

and miscellaneous not written off.

In light of above information, the researcher analyses the data of sample companies of

steel and automobile industry in the following manner.

Table No: 4.1 Total debt of sampled companies of Automobile Industry

Sr. No.

Name of the company

2008

1 Ashok Leyland Ltd.

887.50

2 Bajaj Auto Ltd.

1334.34

3 Hero Motorcorp Ltd.

132.00

4 Mahindra & Mahindra Ltd.

2587.06

5 Maruti Suzuki India Ltd.

900.20

6 Tata Motors Ltd.

6280.52

7 TVS Motors 666.34

Average - Year wise 1826.85

Source: Ace Analyser Database

As we can see from the table that average debt of automobile companies is 3309.39

crores over the period of study. Further we can say that average debt of Tata Motors is

327 % more than average debt of industry. Moreover we can also see that rest of all

the companies have average debt size which is less than industry average debt.

Moreover from the above figu

borrowing debt by automobile companies over the years.

Chart no. 4.1

129

Table No: 4.1 Total debt of sampled companies of Automobile Industry (Rs. In Crores.)

2009 2010 2011 2012 2013

887.50 1961.99 2267.99 2568.26 3097.89 4355.43

1334.34 1570.00 1338.58 325.14 125.03 88.44

132.00 78.49 66.03 2164.39 1730.83 943.74

2587.06 4052.76 2883.61 2404.47 3580.76 3488.59

900.20 698.90 821.40 309.20 1236.90 1389.20

6280.52 13329.68 16594.54 15915.43 15880.57 16798.95

666.34 908.95 1003.37 767.82 831.09 628.16

1826.85 3228.68 3567.93 3493.53 3783.30 3956.07

Source: Ace Analyser Database

As we can see from the table that average debt of automobile companies is 3309.39

of study. Further we can say that average debt of Tata Motors is

327 % more than average debt of industry. Moreover we can also see that rest of all

the companies have average debt size which is less than industry average debt.

Moreover from the above figures we can also say that there is upward trend on

borrowing debt by automobile companies over the years.

Chart no. 4.1 - Total debt of automobile companies

Table No: 4.1 Total debt of sampled companies of Automobile Industry

2013 Average - Company

wise

4355.43 2523.18

88.44 796.92

943.74 852.58

3488.59 3166.21

1389.20 892.63

16798.95 14133.28

628.16 800.96

3956.07 3309.39

As we can see from the table that average debt of automobile companies is 3309.39

of study. Further we can say that average debt of Tata Motors is

327 % more than average debt of industry. Moreover we can also see that rest of all

the companies have average debt size which is less than industry average debt.

res we can also say that there is upward trend on

130

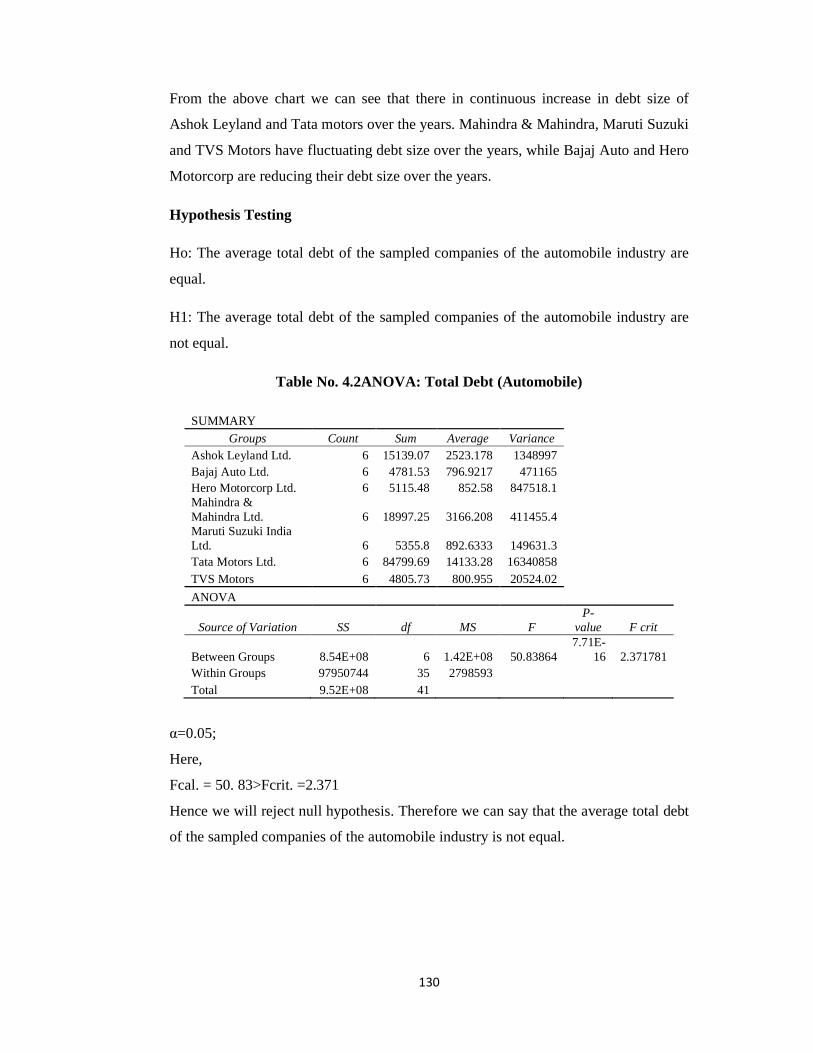

From the above chart we can see that there in continuous increase in debt size of

Ashok Leyland and Tata motors over the years. Mahindra & Mahindra, Maruti Suzuki

and TVS Motors have fluctuating debt size over the years, while Bajaj Auto and Hero

Motorcorp are reducing their debt size over the years.

Hypothesis Testing

Ho: The average total debt of the sampled companies of the automobile industry are

equal.

H1: The average total debt of the sampled companies of the automobile industry are

not equal.

Table No. 4.2ANOVA: Total Debt (Automobile)

SUMMARY Groups Count Sum Average Variance

Ashok Leyland Ltd. 6 15139.07 2523.178 1348997 Bajaj Auto Ltd. 6 4781.53 796.9217 471165

Hero Motorcorp Ltd. 6 5115.48 852.58 847518.1 Mahindra &

Mahindra Ltd. 6 18997.25 3166.208 411455.4 Maruti Suzuki India Ltd. 6 5355.8 892.6333 149631.3

Tata Motors Ltd. 6 84799.69 14133.28 16340858 TVS Motors 6 4805.73 800.955 20524.02

ANOVA

Source of Variation SS df MS F P-

value F crit

Between Groups 8.54E+08 6 1.42E+08 50.83864 7.71E-

16 2.371781 Within Groups 97950744 35 2798593

Total 9.52E+08 41

α=0.05;

Here,

Fcal. = 50. 83>Fcrit. =2.371

Hence we will reject null hypothesis. Therefore we can say that the average total debt

of the sampled companies of the automobile industry is not equal.

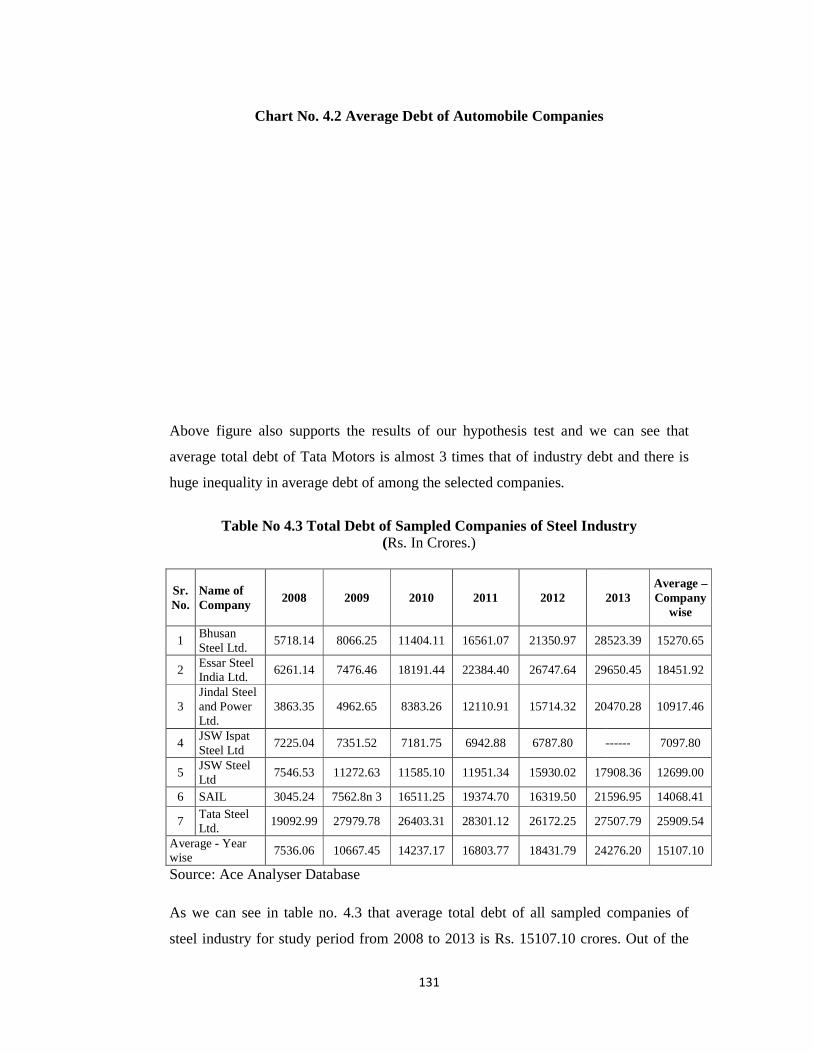

Chart No. 4.2 Average Debt of

Above figure also supports the results of our hypothesis test and we can see that

average total debt of Tata Motors is almost 3 times that of industry debt and there is

huge inequality in average debt of among the selected companies

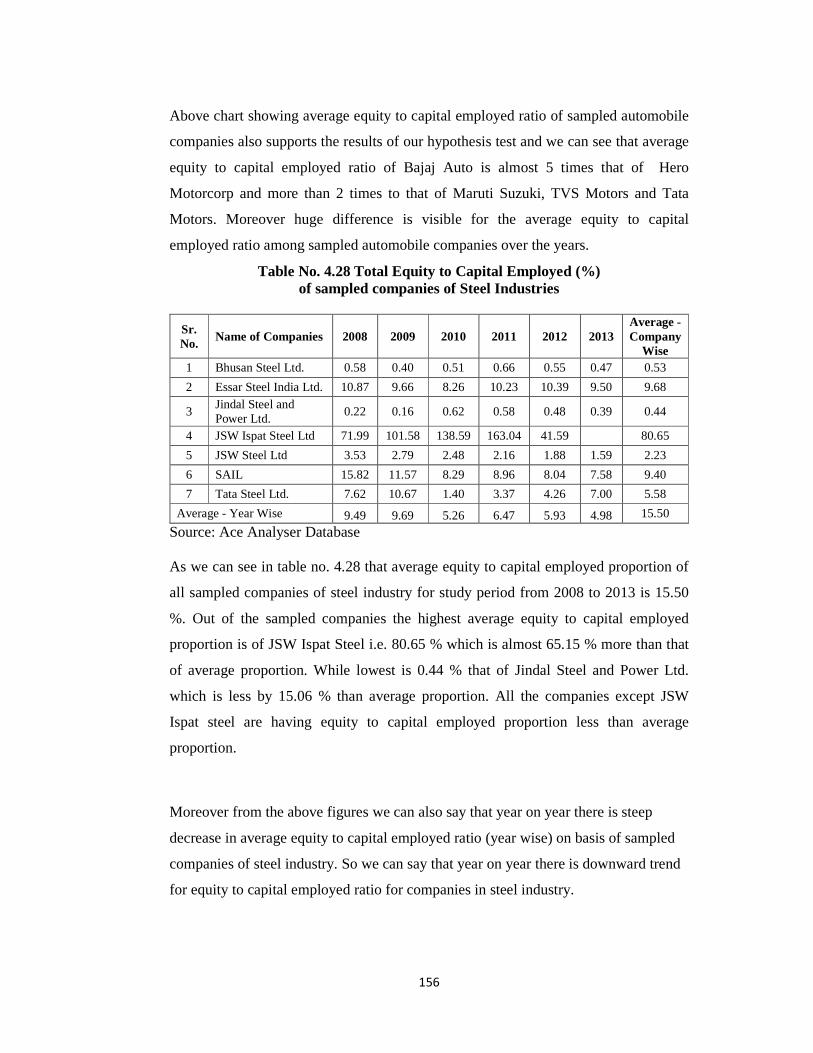

Table No 4.3 Total Debt of Sampled Companies of Steel Industry

Sr. No.

Name of Company

2008

1 Bhusan Steel Ltd.

5718.14

2 Essar Steel India Ltd.

6261.14

3 Jindal Steel and Power Ltd.

3863.35

4 JSW Ispat Steel Ltd

7225.04

5 JSW Steel Ltd

7546.53

6 SAIL 3045.24

7 Tata Steel Ltd.

19092.99

Average - Year wise

7536.06

Source: Ace Analyser Database

As we can see in table no. 4.3 that average total debt of all sampled companies of

steel industry for study period from 2008 to 2013 is Rs. 15107.10 crores. Out of the

131

Chart No. 4.2 Average Debt of Automobile Companies

Above figure also supports the results of our hypothesis test and we can see that

average total debt of Tata Motors is almost 3 times that of industry debt and there is

huge inequality in average debt of among the selected companies.

Table No 4.3 Total Debt of Sampled Companies of Steel Industry (Rs. In Crores.)

2009 2010 2011 2012 2013

8066.25 11404.11 16561.07 21350.97 28523.39

7476.46 18191.44 22384.40 26747.64 29650.45

4962.65 8383.26 12110.91 15714.32 20470.28

7351.52 7181.75 6942.88 6787.80 ------

11272.63 11585.10 11951.34 15930.02 17908.36

7562.8n 3 16511.25 19374.70 16319.50 21596.95

27979.78 26403.31 28301.12 26172.25 27507.79

10667.45 14237.17 16803.77 18431.79 24276.20

Source: Ace Analyser Database

As we can see in table no. 4.3 that average total debt of all sampled companies of

steel industry for study period from 2008 to 2013 is Rs. 15107.10 crores. Out of the

Above figure also supports the results of our hypothesis test and we can see that

average total debt of Tata Motors is almost 3 times that of industry debt and there is

Table No 4.3 Total Debt of Sampled Companies of Steel Industry

2013 Average – Company

wise

28523.39 15270.65

29650.45 18451.92

20470.28 10917.46

------ 7097.80

17908.36 12699.00

21596.95 14068.41

27507.79 25909.54

24276.20 15107.10

As we can see in table no. 4.3 that average total debt of all sampled companies of

steel industry for study period from 2008 to 2013 is Rs. 15107.10 crores. Out of the

sampled companies the highest average debt is borrowed by Tata Steel Ltd. i.e. Rs.

25909.54 crores which is more by 10802.44 crores and approximately 171 % more by

overall average. Apart from it Bhusan steel also have average debt size more than

industry average by Rs. 163.55 crores i.e. 2% more than industry average debt. While

rest of all the companies have average debt size less than that of industry average.

Moreover from the above figures we can also say that there is upward trend on

borrowing debt by steel companies over the years.

Chart No 4.3 Total Debt of Steel Companies

From the above chart we can see that there in continuous increase in debt size of

Bhusan Steel, Essar Steel India Ltd., Jindal Steel and Power Ltd. And JSW Steel over

the years. SAIL and Tata Steel have fluctuating debt size over the years, while debt

size of JSW Ispat Steel is fairly stable which was merged with JSW Steel from year

2013.

Hypothesis Testing

Ho: The average total debt of the sampled companies of the steel industry

H1: The average total debt of the sampled companies of the steel industry is not equal.

132

pled companies the highest average debt is borrowed by Tata Steel Ltd. i.e. Rs.

25909.54 crores which is more by 10802.44 crores and approximately 171 % more by

overall average. Apart from it Bhusan steel also have average debt size more than

age by Rs. 163.55 crores i.e. 2% more than industry average debt. While

rest of all the companies have average debt size less than that of industry average.

Moreover from the above figures we can also say that there is upward trend on

steel companies over the years.

Chart No 4.3 Total Debt of Steel Companies

From the above chart we can see that there in continuous increase in debt size of

Bhusan Steel, Essar Steel India Ltd., Jindal Steel and Power Ltd. And JSW Steel over

SAIL and Tata Steel have fluctuating debt size over the years, while debt

size of JSW Ispat Steel is fairly stable which was merged with JSW Steel from year

Ho: The average total debt of the sampled companies of the steel industry

H1: The average total debt of the sampled companies of the steel industry is not equal.

pled companies the highest average debt is borrowed by Tata Steel Ltd. i.e. Rs.

25909.54 crores which is more by 10802.44 crores and approximately 171 % more by

overall average. Apart from it Bhusan steel also have average debt size more than

age by Rs. 163.55 crores i.e. 2% more than industry average debt. While

rest of all the companies have average debt size less than that of industry average.

Moreover from the above figures we can also say that there is upward trend on

From the above chart we can see that there in continuous increase in debt size of

Bhusan Steel, Essar Steel India Ltd., Jindal Steel and Power Ltd. And JSW Steel over

SAIL and Tata Steel have fluctuating debt size over the years, while debt

size of JSW Ispat Steel is fairly stable which was merged with JSW Steel from year

Ho: The average total debt of the sampled companies of the steel industry is equal.

H1: The average total debt of the sampled companies of the steel industry is not equal.

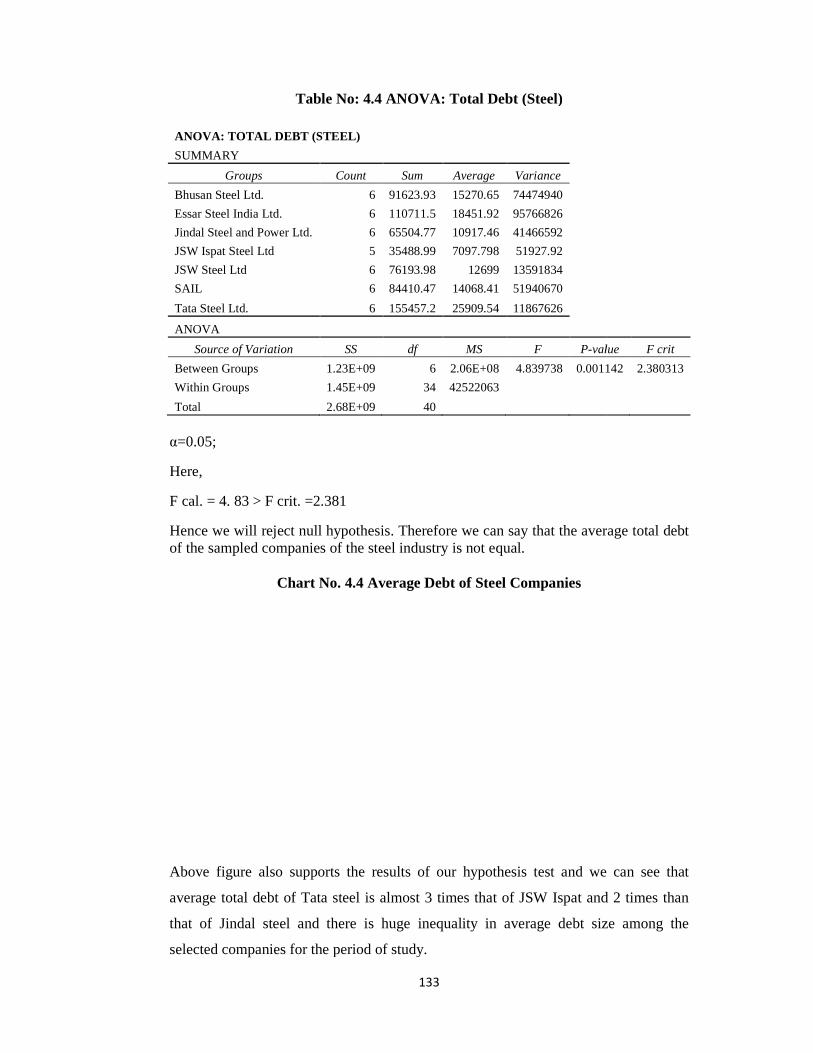

Table No: 4.4 ANOVA: Total Debt (Steel) ANOVA: TOTAL DEBT (STEEL)

SUMMARY

Groups

Bhusan Steel Ltd.

Essar Steel India Ltd.

Jindal Steel and Power Ltd.

JSW Ispat Steel Ltd

JSW Steel Ltd

SAIL

Tata Steel Ltd.

ANOVA

Source of Variation

Between Groups

Within Groups

Total

α=0.05;

Here,

F cal. = 4. 83 > F crit. =2.381

Hence we will reject null hypothesis. Therefore we can say that the average total debt of the sampled companies of the steel industry is not equal.

Chart No. 4.4 Average Debt of Steel Companies

Above figure also supports the results of our hypothesis test and we can see that

average total debt of Tata steel is almost 3 times that of JSW Ispat and 2 times than

that of Jindal steel and there is huge inequality in average debt size among the

selected companies for the period of study.

133

Table No: 4.4 ANOVA: Total Debt (Steel)

ANOVA: TOTAL DEBT (STEEL)

Count Sum Average Variance

6 91623.93 15270.65 74474940

6 110711.5 18451.92 95766826

6 65504.77 10917.46 41466592

5 35488.99 7097.798 51927.92

6 76193.98 12699 13591834

6 84410.47 14068.41 51940670

6 155457.2 25909.54 11867626

SS df MS F P-value

1.23E+09 6 2.06E+08 4.839738 0.001142

1.45E+09 34 42522063 2.68E+09 40

F cal. = 4. 83 > F crit. =2.381

Hence we will reject null hypothesis. Therefore we can say that the average total debt of the sampled companies of the steel industry is not equal.

Chart No. 4.4 Average Debt of Steel Companies

also supports the results of our hypothesis test and we can see that

average total debt of Tata steel is almost 3 times that of JSW Ispat and 2 times than

that of Jindal steel and there is huge inequality in average debt size among the

or the period of study.

value F crit

0.001142 2.380313

Hence we will reject null hypothesis. Therefore we can say that the average total debt

also supports the results of our hypothesis test and we can see that

average total debt of Tata steel is almost 3 times that of JSW Ispat and 2 times than

that of Jindal steel and there is huge inequality in average debt size among the

134

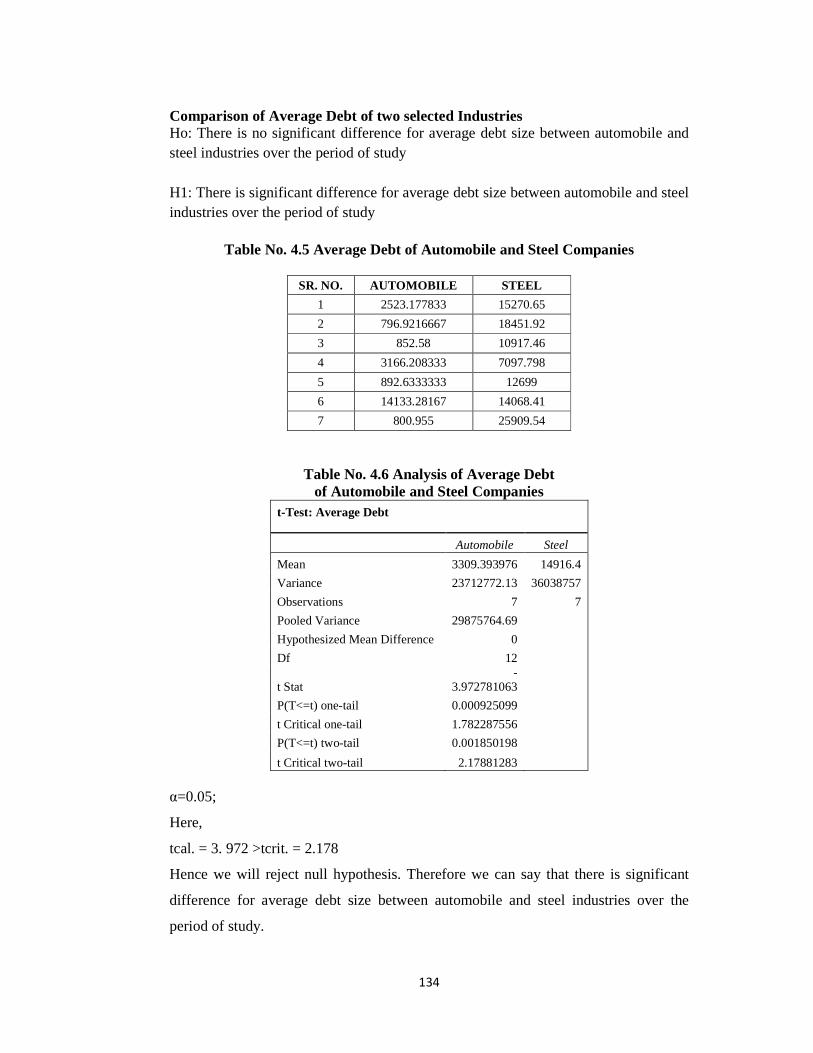

Comparison of Average Debt of two selected Industries Ho: There is no significant difference for average debt size between automobile and steel industries over the period of study H1: There is significant difference for average debt size between automobile and steel industries over the period of study

Table No. 4.5 Average Debt of Automobile and Steel Companies

SR. NO. AUTOMOBILE STEEL

1 2523.177833 15270.65

2 796.9216667 18451.92

3 852.58 10917.46

4 3166.208333 7097.798

5 892.6333333 12699

6 14133.28167 14068.41

7 800.955 25909.54

Table No. 4.6 Analysis of Average Debt of Automobile and Steel Companies

t-Test: Average Debt

Automobile Steel

Mean 3309.393976 14916.4

Variance 23712772.13 36038757

Observations 7 7

Pooled Variance 29875764.69 Hypothesized Mean Difference 0

Df 12

t Stat -

3.972781063

P(T<=t) one-tail 0.000925099 t Critical one-tail 1.782287556

P(T<=t) two-tail 0.001850198 t Critical two-tail 2.17881283

α=0.05;

Here,

tcal. = 3. 972 >tcrit. = 2.178

Hence we will reject null hypothesis. Therefore we can say that there is significant

difference for average debt size between automobile and steel industries over the

period of study.

135

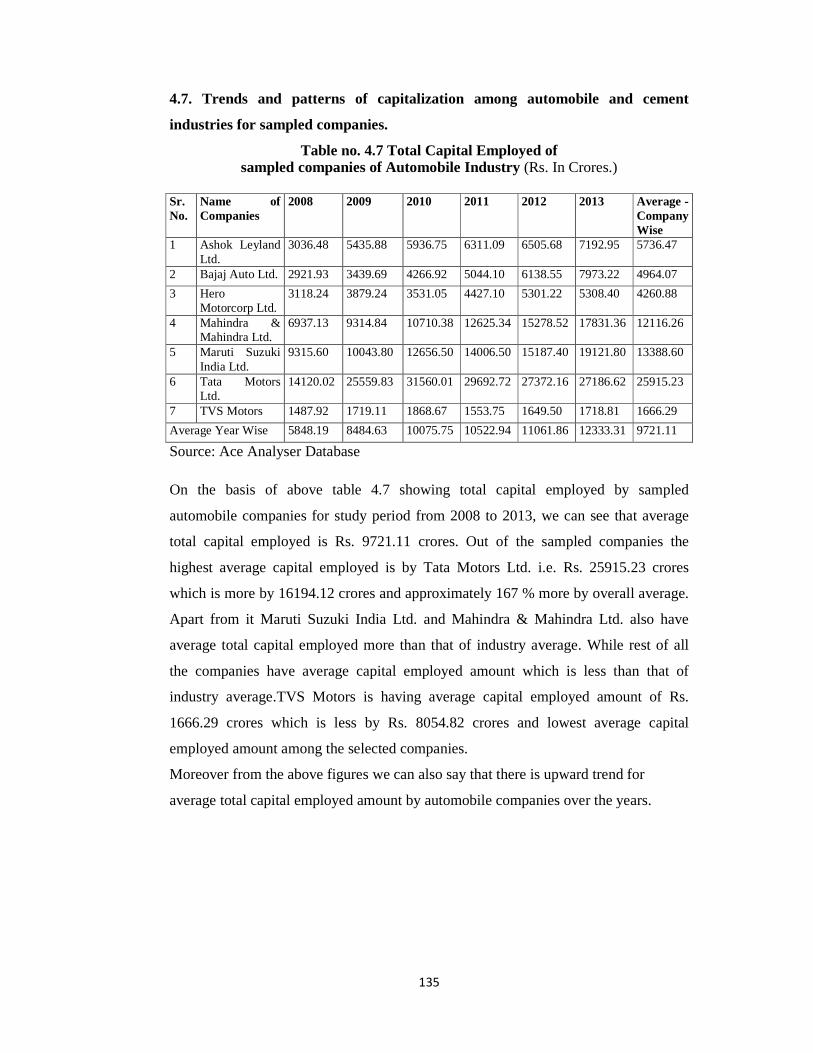

4.7. Trends and patterns of capitalization among automobile and cement

industries for sampled companies.

Table no. 4.7 Total Capital Employed of sampled companies of Automobile Industry (Rs. In Crores.)

Sr. No.

Name of Companies

2008 2009 2010 2011 2012 2013 Average - Company Wise

1 Ashok Leyland Ltd.

3036.48 5435.88 5936.75 6311.09 6505.68 7192.95 5736.47

2 Bajaj Auto Ltd. 2921.93 3439.69 4266.92 5044.10 6138.55 7973.22 4964.07

3 Hero Motorcorp Ltd.

3118.24 3879.24 3531.05 4427.10 5301.22 5308.40 4260.88

4 Mahindra & Mahindra Ltd.

6937.13 9314.84 10710.38 12625.34 15278.52 17831.36 12116.26

5 Maruti Suzuki India Ltd.

9315.60 10043.80 12656.50 14006.50 15187.40 19121.80 13388.60

6 Tata Motors Ltd.

14120.02 25559.83 31560.01 29692.72 27372.16 27186.62 25915.23

7 TVS Motors 1487.92 1719.11 1868.67 1553.75 1649.50 1718.81 1666.29

Average Year Wise 5848.19 8484.63 10075.75 10522.94 11061.86 12333.31 9721.11

Source: Ace Analyser Database

On the basis of above table 4.7 showing total capital employed by sampled

automobile companies for study period from 2008 to 2013, we can see that average

total capital employed is Rs. 9721.11 crores. Out of the sampled companies the

highest average capital employed is by Tata Motors Ltd. i.e. Rs. 25915.23 crores

which is more by 16194.12 crores and approximately 167 % more by overall average.

Apart from it Maruti Suzuki India Ltd. and Mahindra & Mahindra Ltd. also have

average total capital employed more than that of industry average. While rest of all

the companies have average capital employed amount which is less than that of

industry average.TVS Motors is having average capital employed amount of Rs.

1666.29 crores which is less by Rs. 8054.82 crores and lowest average capital

employed amount among the selected companies.

Moreover from the above figures we can also say that there is upward trend for

average total capital employed amount by automobile companies over the years.

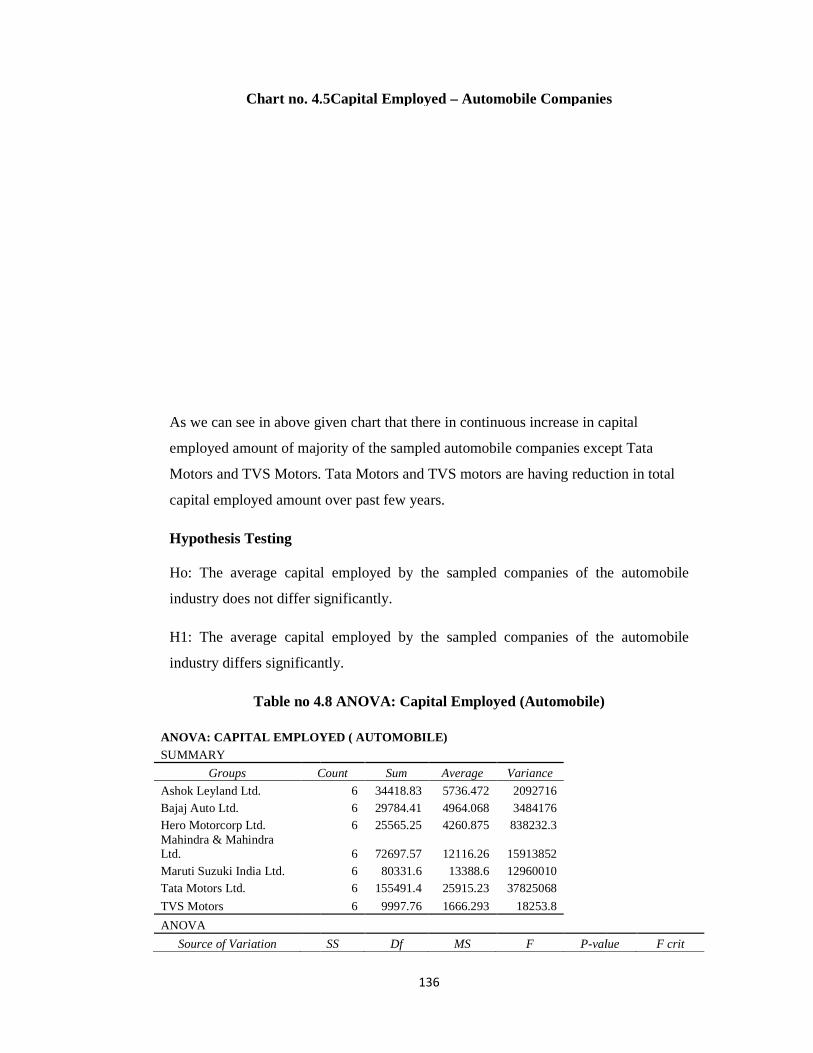

Chart no. 4.5Capital Employed

As we can see in above given chart that there in continuous increase in capital

employed amount of majority of the sampled automobile companies except Tata

Motors and TVS Motors. Tata Motors and TVS motors are having reduction in total

capital employed amount over past few years.

Hypothesis Testing Ho: The average capital employed by

industry does not differ significantly.

H1: The average capital employed by the sampled companies of the automobile

industry differs significantly.

Table no 4.8

ANOVA: CAPITAL E MPLOYED ( AUTOMOBILE)SUMMARY

Groups Count

Ashok Leyland Ltd. Bajaj Auto Ltd. Hero Motorcorp Ltd. Mahindra & Mahindra Ltd. Maruti Suzuki India Ltd. Tata Motors Ltd.

TVS Motors

ANOVA

Source of Variation

136

Chart no. 4.5Capital Employed – Automobile Companies

As we can see in above given chart that there in continuous increase in capital

employed amount of majority of the sampled automobile companies except Tata

Motors and TVS Motors. Tata Motors and TVS motors are having reduction in total

capital employed amount over past few years.

Ho: The average capital employed by the sampled companies of the automobile

industry does not differ significantly.

H1: The average capital employed by the sampled companies of the automobile

industry differs significantly.

Table no 4.8 ANOVA: Capital Employed (Automobile)

MPLOYED ( AUTOMOBILE)

Count Sum Average Variance

6 34418.83 5736.472 2092716 6 29784.41 4964.068 3484176 6 25565.25 4260.875 838232.3

6 72697.57 12116.26 15913852 6 80331.6 13388.6 12960010 6 155491.4 25915.23 37825068

6 9997.76 1666.293 18253.8

SS Df MS F P-value

Automobile Companies

As we can see in above given chart that there in continuous increase in capital

employed amount of majority of the sampled automobile companies except Tata

Motors and TVS Motors. Tata Motors and TVS motors are having reduction in total

the sampled companies of the automobile

H1: The average capital employed by the sampled companies of the automobile

value F crit

Between Groups 2.49E+09Within Groups 3.66E+08Total 2.85E+09

α=0.05;

Here,

Fcal. = 39. 68 > Fcrit. =2.371

Hence we will reject null hypothesis. Therefore we can say that the average capital

employed by the sampled companies of the automobile industry differs significantly.

Chart No. 4.6Average Capital Employed

Above chart showing average capital employed amount by different sampled

automobile company also supports the results o

that average capital employed amount of Tata motors is almost 15 times that of TVS

Motors and 2 times than that of Mahindra and Mahindra. Moreover huge difference is

visible for the average capital employed amount by di

the years.

137

2.49E+09 6 4.15E+08 39.68785 3.38E3.66E+08 35 10447473 2.85E+09 41

Fcal. = 39. 68 > Fcrit. =2.371

Hence we will reject null hypothesis. Therefore we can say that the average capital

the sampled companies of the automobile industry differs significantly.

Chart No. 4.6Average Capital Employed – Automobile Companies

Above chart showing average capital employed amount by different sampled

automobile company also supports the results of our hypothesis test and we can see

that average capital employed amount of Tata motors is almost 15 times that of TVS

Motors and 2 times than that of Mahindra and Mahindra. Moreover huge difference is

visible for the average capital employed amount by different sampled companies over

3.38E-14 2.371781

Hence we will reject null hypothesis. Therefore we can say that the average capital

the sampled companies of the automobile industry differs significantly.

Automobile Companies

Above chart showing average capital employed amount by different sampled

f our hypothesis test and we can see

that average capital employed amount of Tata motors is almost 15 times that of TVS

Motors and 2 times than that of Mahindra and Mahindra. Moreover huge difference is

fferent sampled companies over

138

Table No. 4.9 Total Capital Employed of Sampled companies of Steel Industry (Rs. In Crores.)

Sr No

Name of Companies

2008 2009 2010 2011 2012 2013 Average - Company Wise

1 Bhusan Steel Ltd. 7343.46 10500.89 15395.78 16865.75 23308.15 30712.31 17354.39

2 Essar Steel India Ltd.

10892.47 12252.12 27316.80 25138.72 25718.00 29921.43 21873.26

3 Jindal Steel and Power Ltd.

7619.73 10377.97 15129.26 16049.05 19339.33 24208.99 15454.06

4 JSW Ispat Steel Ltd

3186.60 2237.06 1605.54 2057.68 7216.29 -------- 3260.63

5 JSW Steel Ltd 15223.78 19231.88 21291.44 26093.17 30025.58 35371.63 24539.58

6 SAIL 26108.81 35711.05 49827.95 46122.03 51397.98 54510.19 43946.34

7 Tata Steel Ltd. 81408.60 58156.04 63365.11 72943.68 76249.56 46393.72 66419.45

Average - Year Wise 21683.35 21209.57 27704.55 29324.30 33322.13 36853.05 27549.67

Source: Ace Analyser Database

As we can see in table no. 4.9 that average total capital employed of sampled steel

companies for the period of study is Rs. 27549.67 crores. Out of the sampled

companies the highest average capital employed is by Tata Steel Ltd. i.e. Rs.

66419.45 crores which is more by Rs. 38869.78 crores and approximately 141 %

more by overall average. Apart from it SAIL also have average total capital employed

of Rs. 43946.34 crores which is more than that of industry average by Rs. 16396.67

crores. While rest of all the companies have average capital employed amount which

is less than that of industry average.JSW Ispat Steel Ltd. is having average capital

employed amount of Rs. 3260.63 crores which lowest average capital employed

amount among the selected companies.

Moreover from the above figures, we can also observe that except year 2009 there is

constant increase in average capital employed by sampled companies each year. So,

we can say that there is upward trend for average total capital employed amount by

steel companies over the years.

Chart No. 4.7Capital Employed

In above chart showing total capital employed by different sampled steel companies

over the years, we can see that there in continuous increase in total capital employed

of Bhusan Steel Ltd., Jindal Steel and Power Ltd. and SW Steel Ltd. over the years.

Essar Steel India Ltd., JSW Ispat Steel Ltd, SAIL and Tata Steel have fluctuating

pattern for total capital employed over the years.

Hypothesis Testing Ho: The average capital employed by the sampled companies of the steel industry

does not differ significantly.

H1: The average capital employed by the sampled companies of the steel industry differs significantly.

Table No. 4.10

ANOVA: CAPITAL EMPLOYED ( STEEL)

SUMMARY

Groups

Bhusan Steel Ltd.

Essar Steel India Ltd.

Jindal Steel and Power Ltd.

JSW Ispat Steel Ltd

JSW Steel Ltd

SAIL

Tata Steel Ltd.

139

Chart No. 4.7Capital Employed – Steel Companies

total capital employed by different sampled steel companies

over the years, we can see that there in continuous increase in total capital employed

of Bhusan Steel Ltd., Jindal Steel and Power Ltd. and SW Steel Ltd. over the years.

SW Ispat Steel Ltd, SAIL and Tata Steel have fluctuating

pattern for total capital employed over the years.

Ho: The average capital employed by the sampled companies of the steel industry

does not differ significantly.

apital employed by the sampled companies of the steel industry

Table No. 4.10 ANOVA: Capital Employed (Steel)

ANOVA: CAPITAL EMPLOYED ( STEEL)

Count Sum Average Variance 6 104126.3 17354.39 73029132

6 131239.5 21873.26 66598901

6 92724.33 15454.06 35869409

5 16303.17 3260.634 5221708

6 147237.5 24539.58 55069873

6 263678 43946.34 1.18E+08

6 398516.7 66419.45 1.69E+08

total capital employed by different sampled steel companies

over the years, we can see that there in continuous increase in total capital employed

of Bhusan Steel Ltd., Jindal Steel and Power Ltd. and SW Steel Ltd. over the years.

SW Ispat Steel Ltd, SAIL and Tata Steel have fluctuating

Ho: The average capital employed by the sampled companies of the steel industry

apital employed by the sampled companies of the steel industry

ANOVA

Source of Variation

Between Groups

Within Groups

Total

α=0.05;

Here,

Fcal. = 33.37 > Fcrit. =2.38

Hence we will reject null hypothesis. Therefore we can say that the average capital

employed by the sampled companies of the steel industry differs significantly.

Chart No 4.8Average Capital Employed

Above chart showing average capital employed amount by different sampled steel

company also supports the results of our hypothesis test and we can see that average

capital employed amount of Tata steel is almost 20 times that of JSW Ispat Steel Ltd.

and more than 2 times for rest of all the companies except SAIL. Moreover huge

difference is visible for the average capital employed amount by different sampled

companies over the years.

140

SS Df MS F P-value

1.54E+10 6 2.56E+09 33.37165 7.18E-

2.61E+09 34 76725993

1.8E+10 40

Fcal. = 33.37 > Fcrit. =2.38

Hence we will reject null hypothesis. Therefore we can say that the average capital

employed by the sampled companies of the steel industry differs significantly.

Chart No 4.8Average Capital Employed – Steel Companies

Above chart showing average capital employed amount by different sampled steel

company also supports the results of our hypothesis test and we can see that average

capital employed amount of Tata steel is almost 20 times that of JSW Ispat Steel Ltd.

ore than 2 times for rest of all the companies except SAIL. Moreover huge

difference is visible for the average capital employed amount by different sampled

companies over the years.

value F crit

-13 2.380313

Hence we will reject null hypothesis. Therefore we can say that the average capital

employed by the sampled companies of the steel industry differs significantly.

Steel Companies

Above chart showing average capital employed amount by different sampled steel

company also supports the results of our hypothesis test and we can see that average

capital employed amount of Tata steel is almost 20 times that of JSW Ispat Steel Ltd.

ore than 2 times for rest of all the companies except SAIL. Moreover huge

difference is visible for the average capital employed amount by different sampled

141

Comparison of Average Capital Employed Between Automobile and Steel Industries

Table No. 4.11 Average Capital Employed of Automobile and Steel Industry

SR. NO. AUTOMOBILE STEEL

1 5736.472 17354.39

2 4964.068 21873.26

3 4260.875 15454.06

4 12116.26 3260.634

5 13388.6 24539.58

6 25915.23 43946.34

7 1666.293 66419.45

Average 9721.114 27549.67

Ho: There is no significant difference for average capital employed between

automobile and steel industries over the period of study

H1: There is significant difference for average capital employed between automobile

and steel industries over the period of study

Table No. 4.12 Analysis of Average Capital Employed of Automobile and Steel Companies

t-Test: Capital Employed

Automobile Steel

Mean 9721.114 27549.67

Variance 69106279 4.44E+08

Observations 7 7

Pooled Variance 2.56E+08

Hypothesized Mean Difference 0

Df 12

t Stat -2.08334

P(T<=t) one-tail 0.029636

t Critical one-tail 1.782288

P(T<=t) two-tail 0.059271

t Critical two-tail 2.178813 α=0.05;

Here,

tcal. = -2.08334>tcrit. = -2.178

Hence we will fail to reject null hypothesis. Therefore we can say that there is no

significant difference for average capital employed between automobile and steel

industries over the period of study.

142

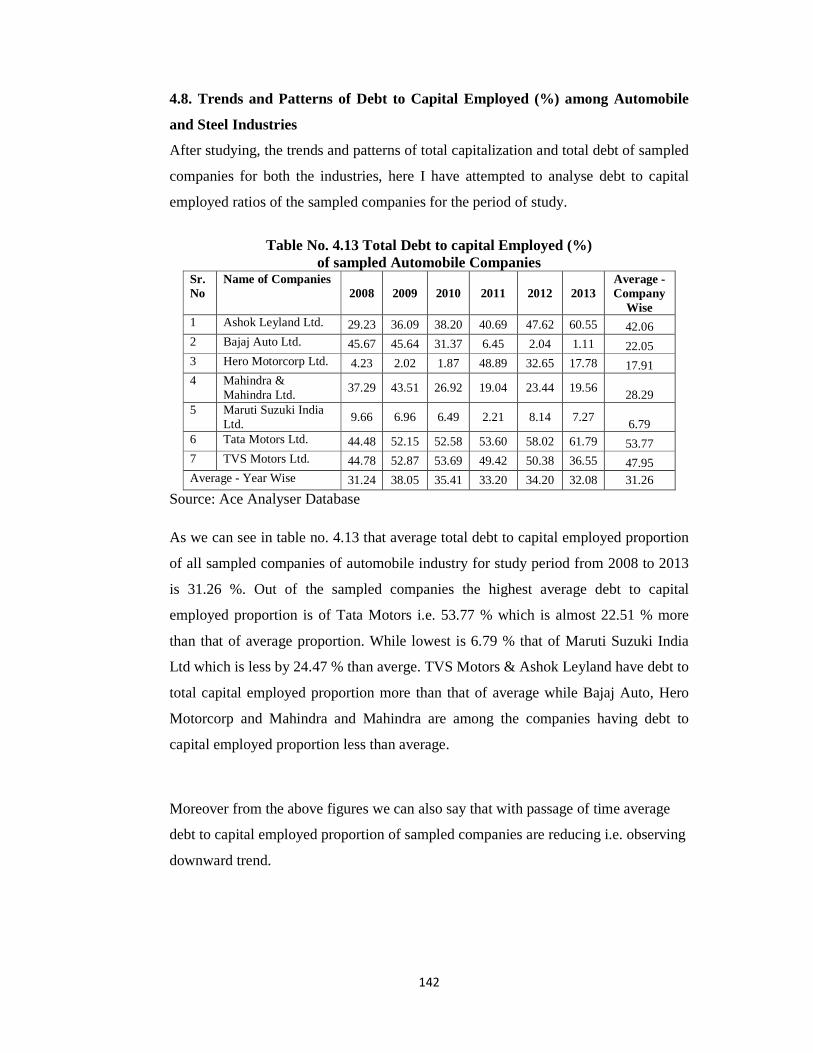

4.8. Trends and Patterns of Debt to Capital Employed (%) among Automobile

and Steel Industries

After studying, the trends and patterns of total capitalization and total debt of sampled

companies for both the industries, here I have attempted to analyse debt to capital

employed ratios of the sampled companies for the period of study.

Table No. 4.13 Total Debt to capital Employed (%)

of sampled Automobile Companies Sr. No

Name of Companies 2008 2009 2010 2011 2012 2013

Average - Company

Wise 1 Ashok Leyland Ltd. 29.23 36.09 38.20 40.69 47.62 60.55 42.06 2 Bajaj Auto Ltd. 45.67 45.64 31.37 6.45 2.04 1.11 22.05 3 Hero Motorcorp Ltd. 4.23 2.02 1.87 48.89 32.65 17.78 17.91 4 Mahindra &

Mahindra Ltd. 37.29 43.51 26.92 19.04 23.44 19.56

28.29 5 Maruti Suzuki India

Ltd. 9.66 6.96 6.49 2.21 8.14 7.27

6.79 6 Tata Motors Ltd. 44.48 52.15 52.58 53.60 58.02 61.79 53.77 7 TVS Motors Ltd. 44.78 52.87 53.69 49.42 50.38 36.55 47.95 Average - Year Wise 31.24 38.05 35.41 33.20 34.20 32.08 31.26

Source: Ace Analyser Database

As we can see in table no. 4.13 that average total debt to capital employed proportion

of all sampled companies of automobile industry for study period from 2008 to 2013

is 31.26 %. Out of the sampled companies the highest average debt to capital

employed proportion is of Tata Motors i.e. 53.77 % which is almost 22.51 % more

than that of average proportion. While lowest is 6.79 % that of Maruti Suzuki India

Ltd which is less by 24.47 % than averge. TVS Motors & Ashok Leyland have debt to

total capital employed proportion more than that of average while Bajaj Auto, Hero

Motorcorp and Mahindra and Mahindra are among the companies having debt to

capital employed proportion less than average.

Moreover from the above figures we can also say that with passage of time average

debt to capital employed proportion of sampled companies are reducing i.e. observing

downward trend.

Chart No. 4.9Average Debt to Capital Employed

From the above chart we can see that debt to equity proportion of Ashok Leyland and

Tata Motors are continuously increasing

reducing their debt to capital employed proportion. There is a sharp rise in debt to

capital employed ratio of Hero Motor Corp in 2011immediately after termination of

joint venture with Honda corp, post that they h

Mahindra & Mahindra, Maruti Suzuki and TVS Motors have fluctuating debt to

capital employed proportion over the years.

Hypothesis Testing

Ho: The average debt to capital employed ratio of the sampled companies of the

automobile industry are equal.

H1: The average debt to capital employed ratio of the sampled companies of the automobile industry are not equal.

Table No. 4.14 ANOVA: Debt to Capital EmployedSUMMARY

Groups

Ashok Leyland Ltd.

Bajaj Auto Ltd.

Hero Motorcorp Ltd.

Mahindra & Mahindra Ltd.

Maruti Suzuki India Ltd.

Tata Motors Ltd.

TVS Motors

143

Chart No. 4.9Average Debt to Capital Employed – Automobile Companies

From the above chart we can see that debt to equity proportion of Ashok Leyland and

Tata Motors are continuously increasing over the years. While Bajaj Auto keeps on

reducing their debt to capital employed proportion. There is a sharp rise in debt to

capital employed ratio of Hero Motor Corp in 2011immediately after termination of

joint venture with Honda corp, post that they have reduced their ratio drastically.

Mahindra & Mahindra, Maruti Suzuki and TVS Motors have fluctuating debt to

capital employed proportion over the years.

Ho: The average debt to capital employed ratio of the sampled companies of the

tomobile industry are equal.

to capital employed ratio of the sampled companies of the automobile industry are not equal.

ANOVA: Debt to Capital Employed (Automobile)

Count Sum Average Variance 6 252.38 42.06333 117.964

6 132.28 22.04667 456.6997

6 107.44 17.90667 374.7922

Mahindra & Mahindra Ltd. 6 169.76 28.29333 99.96463

6 40.73 6.788333 6.277017

6 322.62 53.77 34.55128

6 287.69 47.94833 41.04574

Automobile Companies

From the above chart we can see that debt to equity proportion of Ashok Leyland and

over the years. While Bajaj Auto keeps on

reducing their debt to capital employed proportion. There is a sharp rise in debt to

capital employed ratio of Hero Motor Corp in 2011immediately after termination of

ave reduced their ratio drastically.

Mahindra & Mahindra, Maruti Suzuki and TVS Motors have fluctuating debt to

Ho: The average debt to capital employed ratio of the sampled companies of the

to capital employed ratio of the sampled companies of the

(Automobile)

ANOVA

Source of Variation

Between Groups

Within Groups

Total

α=0.05;

Here,

Fcal. = 10.9692 >Fcrit. =2.371

Hence we will reject null hypothesis. Therefore we can say that the average debts to

capital employed ratio of the sampled companies of the automobile industry are not

equal.

Chart No. 4.10Average Debt to Capital Employed

Above chart showing average debt to capital employed ratio of sampled automobile

companies also supports the results of our hypothesis test and we can see that average

debt to capital employed

and more than 2 times to that of Hero Motor corp and Bajaj Auto. Moreover huge

difference is visible for the average debt to capital employed ratio by different

sampled companies over the years.

144

SS Df MS F P-value

10636.64 6 1772.773 10.96921 7.42E-07

5656.473 35 161.6135

16293.11 41

Fcal. = 10.9692 >Fcrit. =2.371

Hence we will reject null hypothesis. Therefore we can say that the average debts to

capital employed ratio of the sampled companies of the automobile industry are not

4.10Average Debt to Capital Employed – Automobile Companies

Above chart showing average debt to capital employed ratio of sampled automobile

companies also supports the results of our hypothesis test and we can see that average

ratio of Tata Motors is almost 7 times that of Maruti Suzuki

and more than 2 times to that of Hero Motor corp and Bajaj Auto. Moreover huge

difference is visible for the average debt to capital employed ratio by different

sampled companies over the years.

value F crit

07 2.371781

Hence we will reject null hypothesis. Therefore we can say that the average debts to

capital employed ratio of the sampled companies of the automobile industry are not

Automobile Companies

Above chart showing average debt to capital employed ratio of sampled automobile

companies also supports the results of our hypothesis test and we can see that average

ratio of Tata Motors is almost 7 times that of Maruti Suzuki

and more than 2 times to that of Hero Motor corp and Bajaj Auto. Moreover huge

difference is visible for the average debt to capital employed ratio by different

145

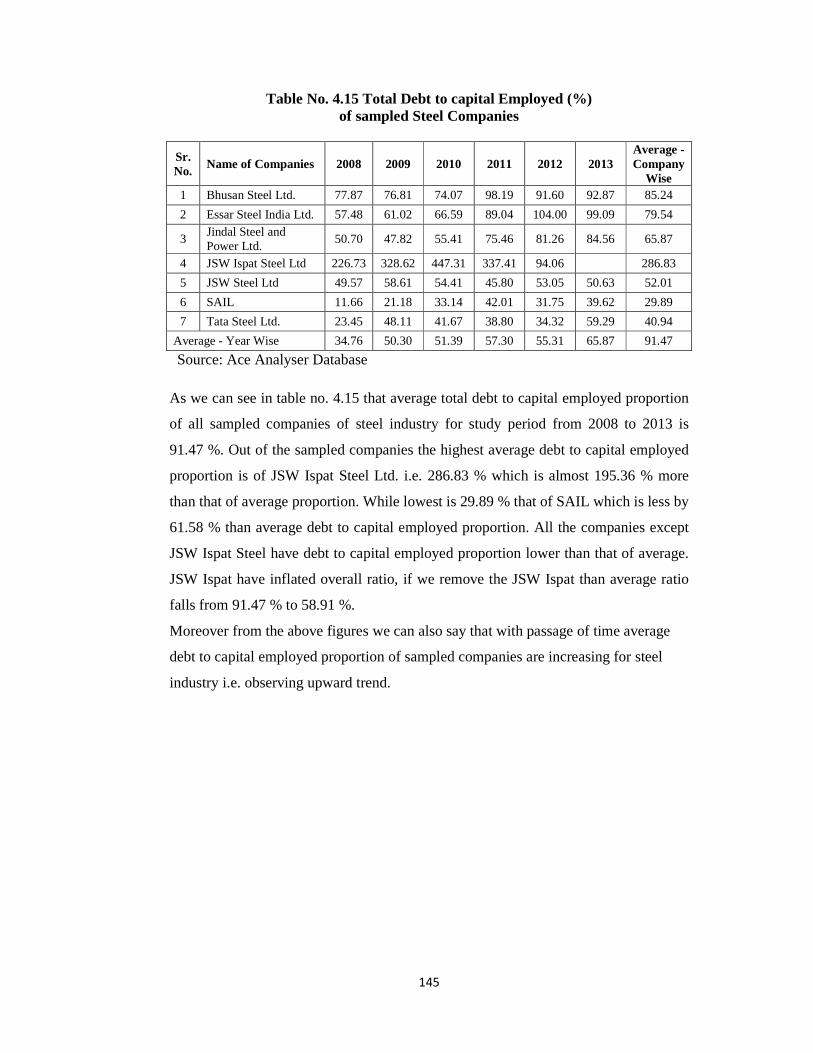

Table No. 4.15 Total Debt to capital Employed (%) of sampled Steel Companies

Sr. No.

Name of Companies 2008 2009 2010 2011 2012 2013 Average - Company

Wise 1 Bhusan Steel Ltd. 77.87 76.81 74.07 98.19 91.60 92.87 85.24

2 Essar Steel India Ltd. 57.48 61.02 66.59 89.04 104.00 99.09 79.54

3 Jindal Steel and Power Ltd.

50.70 47.82 55.41 75.46 81.26 84.56 65.87

4 JSW Ispat Steel Ltd 226.73 328.62 447.31 337.41 94.06

286.83

5 JSW Steel Ltd 49.57 58.61 54.41 45.80 53.05 50.63 52.01

6 SAIL 11.66 21.18 33.14 42.01 31.75 39.62 29.89

7 Tata Steel Ltd. 23.45 48.11 41.67 38.80 34.32 59.29 40.94

Average - Year Wise 34.76 50.30 51.39 57.30 55.31 65.87 91.47

Source: Ace Analyser Database

As we can see in table no. 4.15 that average total debt to capital employed proportion

of all sampled companies of steel industry for study period from 2008 to 2013 is

91.47 %. Out of the sampled companies the highest average debt to capital employed

proportion is of JSW Ispat Steel Ltd. i.e. 286.83 % which is almost 195.36 % more

than that of average proportion. While lowest is 29.89 % that of SAIL which is less by

61.58 % than average debt to capital employed proportion. All the companies except

JSW Ispat Steel have debt to capital employed proportion lower than that of average.

JSW Ispat have inflated overall ratio, if we remove the JSW Ispat than average ratio

falls from 91.47 % to 58.91 %.

Moreover from the above figures we can also say that with passage of time average

debt to capital employed proportion of sampled companies are increasing for steel

industry i.e. observing upward trend.

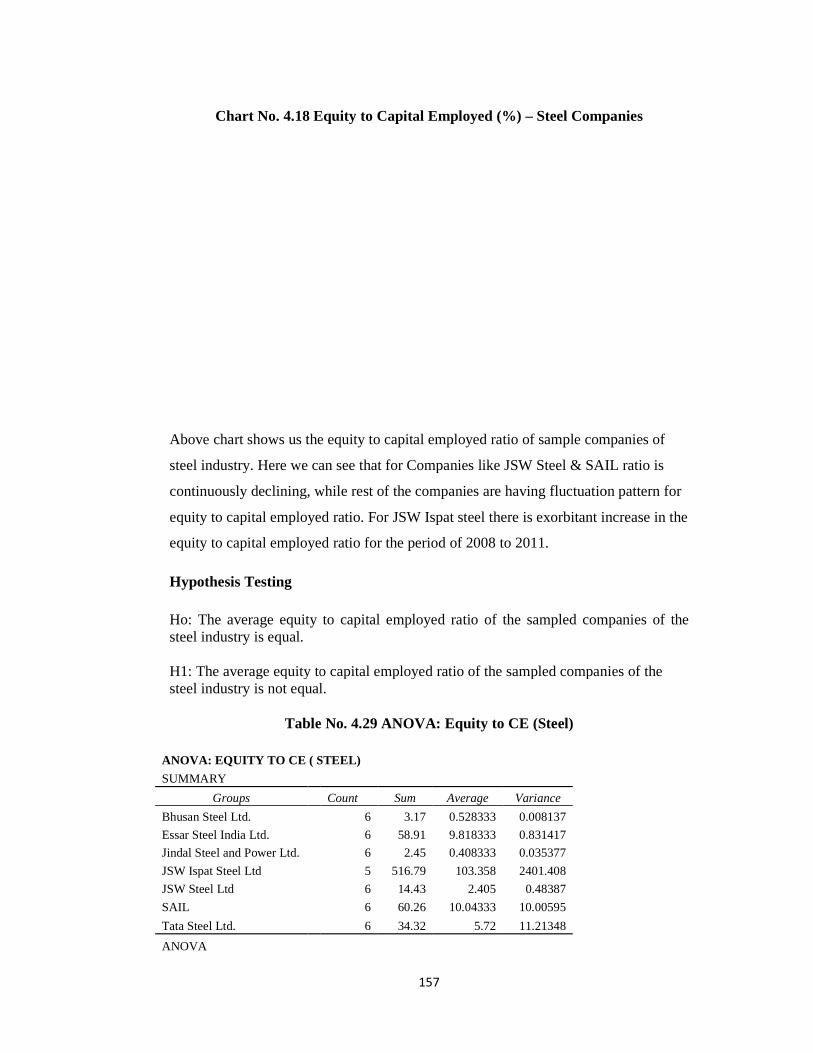

Chart No. 4.11Debt to Capital Employed (%)

From the above chart we can see that debts to capital employed proportion of majority

of the sampled companies

years. JSW Ispat steel is an exceptional sample in above figure having very high

proportion of debt to capital employed over the years until its takeover. SAIL and

JSW Steel have fluctuating debt to

Hypothesis Testing Ho: The average debts to capital employed ratio of the sampled companies of the steel

industry are equal.

H1: The average debts to capital employed ratio of the sampled companies of the steelindustry are not equal.

Table No. 4.16

ANOVA: DEBT TO CAPITAL EMPLOYED ( STEEL)

SUMMARY

Groups

Bhusan Steel Ltd.

Essar Steel India Ltd.

Jindal Steel and Power Ltd.

JSW Ispat Steel Ltd

JSW Steel Ltd

SAIL

Tata Steel Ltd.

ANOVA

146

Chart No. 4.11Debt to Capital Employed (%) – Steel Companies

From the above chart we can see that debts to capital employed proportion of majority

of the sampled companies from steel industry are continuously increasing over the

years. JSW Ispat steel is an exceptional sample in above figure having very high

proportion of debt to capital employed over the years until its takeover. SAIL and

JSW Steel have fluctuating debt to capital employed proportion over the years.

Ho: The average debts to capital employed ratio of the sampled companies of the steel

H1: The average debts to capital employed ratio of the sampled companies of the steel

Table No. 4.16 ANOVA: Debt to Capital Employed (Steel)

ANOVA: DEBT TO CAPITAL EMPLOYED ( STEEL)

Count Sum Average Variance 6 511.41 85.235 103.3039

6 477.22 79.53667 413.6161

6 395.21 65.86833 268.6959 5 1434.13 286.826 17707.71

6 312.07 52.01167 19.36474 6 179.36 29.89333 132.7573

6 245.64 40.94 148.5937

Steel Companies

From the above chart we can see that debts to capital employed proportion of majority

from steel industry are continuously increasing over the

years. JSW Ispat steel is an exceptional sample in above figure having very high

proportion of debt to capital employed over the years until its takeover. SAIL and

capital employed proportion over the years.

Ho: The average debts to capital employed ratio of the sampled companies of the steel

H1: The average debts to capital employed ratio of the sampled companies of the steel

ANOVA: Debt to Capital Employed (Steel)

Source of Variation

Between Groups

Within Groups

Total

α=0.05;

Here,

Fcal. = 18.00 >Fcrit. =2.380

Hence we will reject null

capital employed ratio of the sampled companies of the steel industry are not equal.

Chart No. 4.12Average Debt to Capital Employed

Above chart showing average debt to capital

companies also supports the results of our hypothesis test and we can see that average

debt to capital employed ratio of JSW Ispat Steel is almost 10 times that of SAIL and

higher from all other companies. Moreover huge di

debt to capital employed ratio among other sampled companies over the years

147

SS Df MS F P-value

242322.1 6 40387.02 18.00568 2.85E-09

76262.51 34 2243.015

318584.6 40

Fcal. = 18.00 >Fcrit. =2.380

Hence we will reject null hypothesis. Therefore we can say that the average debts to

capital employed ratio of the sampled companies of the steel industry are not equal.

Chart No. 4.12Average Debt to Capital Employed – Steel Companies

Above chart showing average debt to capital employed ratio of sampled steel

companies also supports the results of our hypothesis test and we can see that average

debt to capital employed ratio of JSW Ispat Steel is almost 10 times that of SAIL and

higher from all other companies. Moreover huge difference is visible for the average

debt to capital employed ratio among other sampled companies over the years

F crit

2.380313

hypothesis. Therefore we can say that the average debts to

capital employed ratio of the sampled companies of the steel industry are not equal.

Steel Companies

employed ratio of sampled steel

companies also supports the results of our hypothesis test and we can see that average

debt to capital employed ratio of JSW Ispat Steel is almost 10 times that of SAIL and

fference is visible for the average

debt to capital employed ratio among other sampled companies over the years

148

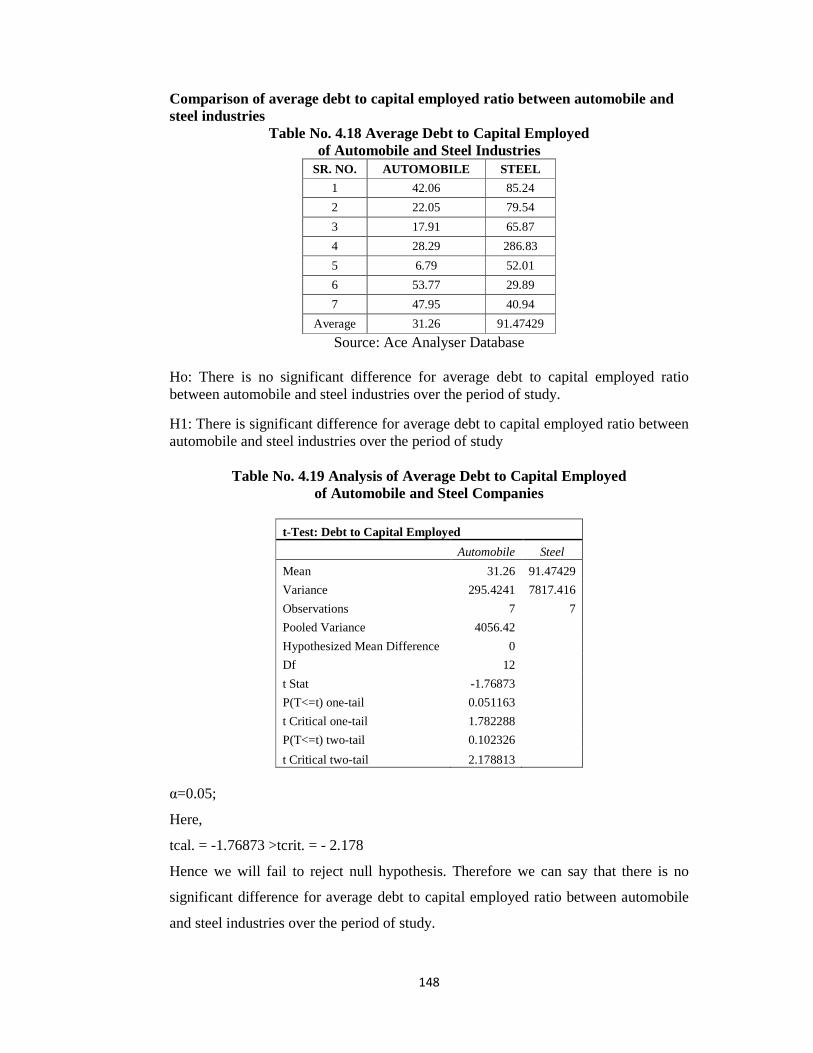

Comparison of average debt to capital employed ratio between automobile and steel industries

Table No. 4.18 Average Debt to Capital Employed of Automobile and Steel Industries

SR. NO. AUTOMOBILE STEEL

1 42.06 85.24

2 22.05 79.54

3 17.91 65.87

4 28.29 286.83

5 6.79 52.01

6 53.77 29.89

7 47.95 40.94

Average 31.26 91.47429

Source: Ace Analyser Database

Ho: There is no significant difference for average debt to capital employed ratio between automobile and steel industries over the period of study.

H1: There is significant difference for average debt to capital employed ratio between automobile and steel industries over the period of study

Table No. 4.19 Analysis of Average Debt to Capital Employed

of Automobile and Steel Companies

t-Test: Debt to Capital Employed

Automobile Steel

Mean 31.26 91.47429

Variance 295.4241 7817.416

Observations 7 7

Pooled Variance 4056.42

Hypothesized Mean Difference 0 Df 12

t Stat -1.76873 P(T<=t) one-tail 0.051163

t Critical one-tail 1.782288 P(T<=t) two-tail 0.102326

t Critical two-tail 2.178813 α=0.05;

Here,

tcal. = -1.76873 >tcrit. = - 2.178

Hence we will fail to reject null hypothesis. Therefore we can say that there is no

significant difference for average debt to capital employed ratio between automobile

and steel industries over the period of study.

149

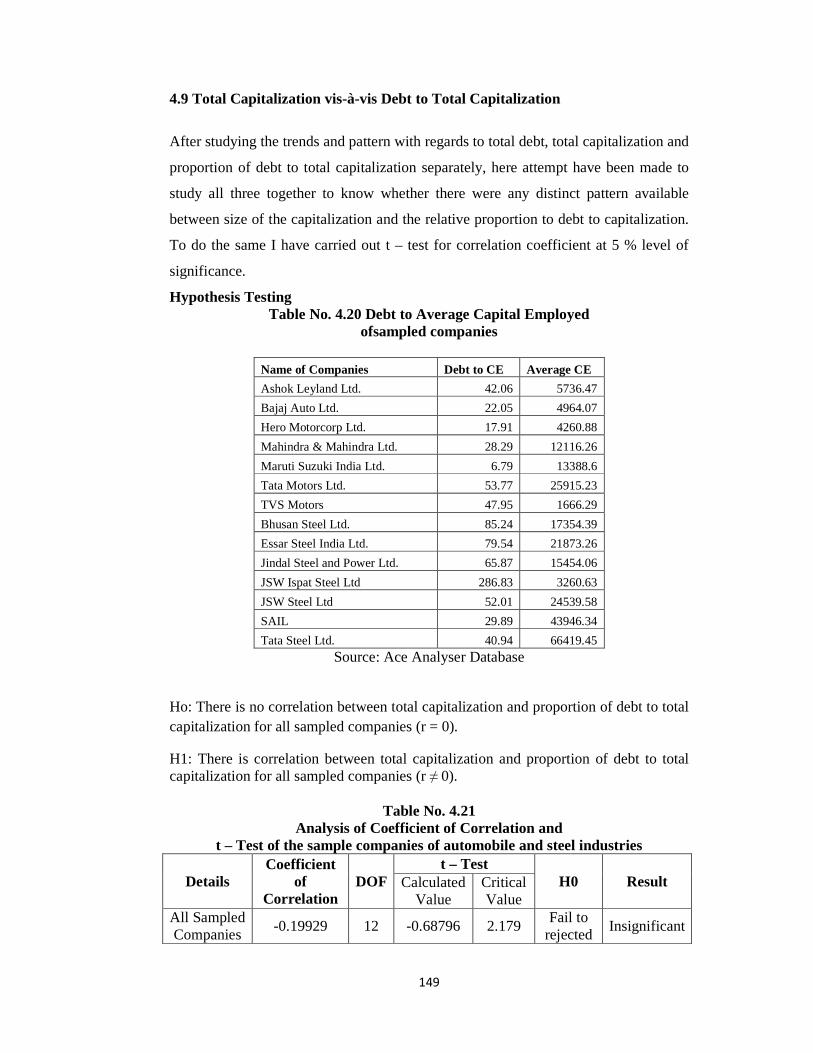

4.9 Total Capitalization vis-à-vis Debt to Total Capitalization

After studying the trends and pattern with regards to total debt, total capitalization and

proportion of debt to total capitalization separately, here attempt have been made to

study all three together to know whether there were any distinct pattern available

between size of the capitalization and the relative proportion to debt to capitalization.

To do the same I have carried out t – test for correlation coefficient at 5 % level of

significance.

Hypothesis Testing Table No. 4.20 Debt to Average Capital Employed

ofsampled companies

Name of Companies Debt to CE Average CE

Ashok Leyland Ltd. 42.06 5736.47

Bajaj Auto Ltd. 22.05 4964.07

Hero Motorcorp Ltd. 17.91 4260.88

Mahindra & Mahindra Ltd. 28.29 12116.26

Maruti Suzuki India Ltd. 6.79 13388.6

Tata Motors Ltd. 53.77 25915.23

TVS Motors 47.95 1666.29

Bhusan Steel Ltd. 85.24 17354.39

Essar Steel India Ltd. 79.54 21873.26

Jindal Steel and Power Ltd. 65.87 15454.06

JSW Ispat Steel Ltd 286.83 3260.63

JSW Steel Ltd 52.01 24539.58

SAIL 29.89 43946.34

Tata Steel Ltd. 40.94 66419.45 Source: Ace Analyser Database

Ho: There is no correlation between total capitalization and proportion of debt to total capitalization for all sampled companies (r = 0).

H1: There is correlation between total capitalization and proportion of debt to total capitalization for all sampled companies (r ≠ 0).

Table No. 4.21 Analysis of Coefficient of Correlation and

t – Test of the sample companies of automobile and steel industries

Details Coefficient

of Correlation

DOF t – Test

H0 Result Calculated Value

Critical Value

All Sampled Companies

-0.19929 12 -0.68796 2.179 Fail to

rejected Insignificant

α=0.05;

Here,

tcal. = -0.68796 > tcrit. =

Hence we will fail to reject null hypothesis.

correlation between total capitalization and proportion of debt to total capitalization

for all sampled companies (r = 0).

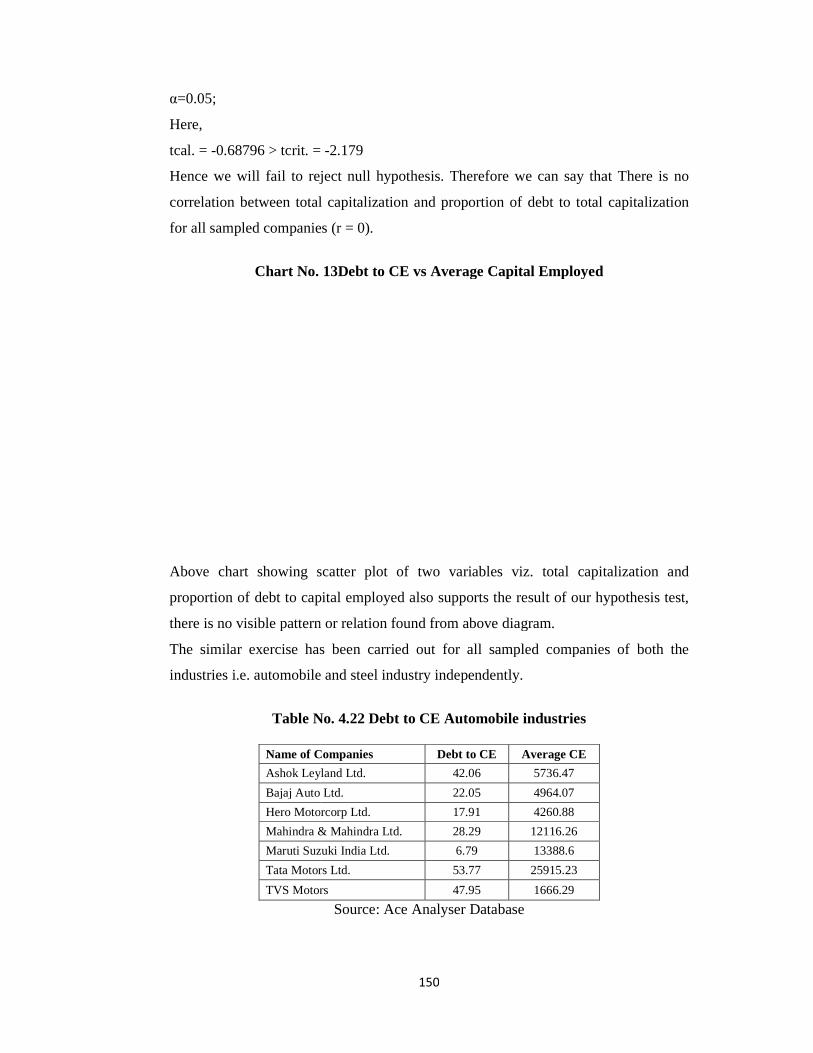

Chart No. 13Debt to CE vs Average Capital Employed

Above chart showing scatter plot of two

proportion of debt to capital employed also supports the result of our hypothesis test,

there is no visible pattern or relation found from above diagram.

The similar exercise has been carried out for all sampled comp

industries i.e. automobile and steel industry independently.

Table No. 4.22 Debt to CE

Name of Companies

Ashok Leyland Ltd.

Bajaj Auto Ltd.

Hero Motorcorp Ltd.

Mahindra & Mahindra Ltd.

Maruti Suzuki India Ltd.

Tata Motors Ltd.

TVS Motors

150

tcrit. = -2.179

Hence we will fail to reject null hypothesis. Therefore we can say that There is no

correlation between total capitalization and proportion of debt to total capitalization

for all sampled companies (r = 0).

Chart No. 13Debt to CE vs Average Capital Employed

Above chart showing scatter plot of two variables viz. total capitalization and

proportion of debt to capital employed also supports the result of our hypothesis test,

there is no visible pattern or relation found from above diagram.

The similar exercise has been carried out for all sampled companies of both the

industries i.e. automobile and steel industry independently.

Table No. 4.22 Debt to CE Automobile industries

Name of Companies Debt to CE Average CE

Ashok Leyland Ltd. 42.06 5736.47

Bajaj Auto Ltd. 22.05 4964.07

Hero Motorcorp Ltd. 17.91 4260.88

Mahindra & Mahindra Ltd. 28.29 12116.26

Maruti Suzuki India Ltd. 6.79 13388.6

Tata Motors Ltd. 53.77 25915.23

TVS Motors 47.95 1666.29

Source: Ace Analyser Database

Therefore we can say that There is no

correlation between total capitalization and proportion of debt to total capitalization

variables viz. total capitalization and

proportion of debt to capital employed also supports the result of our hypothesis test,

anies of both the

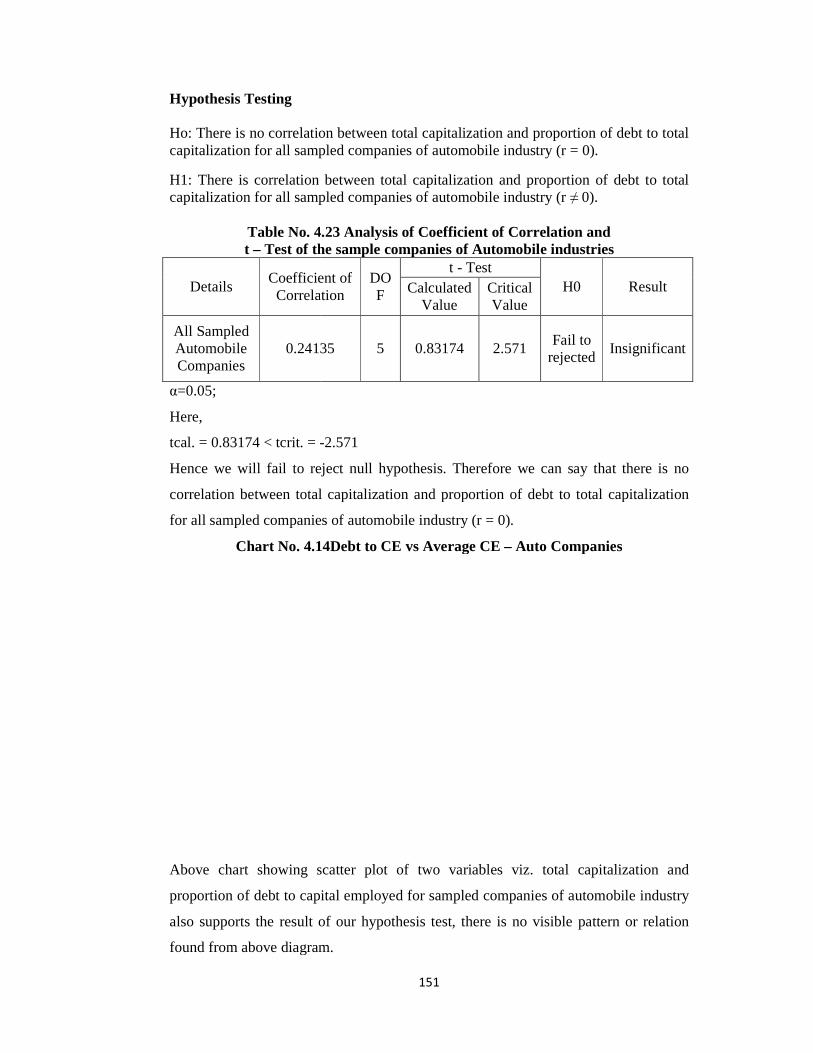

Hypothesis Testing Ho: There is no correlation between total capitalization for all sampled companies of automobile industry (r = 0).

H1: There is correlation between total capitalization and proportion of debt to total capitalization for all sampled companies of

Table No. 4.23 t – Test of the sample companies of Automobile industries

Details Coefficient of Correlation

All Sampled Automobile Companies

0.24135

α=0.05;

Here,

tcal. = 0.83174 < tcrit. = -

Hence we will fail to reject null hypothesis. Therefore we can say that there is no

correlation between total capitalization and

for all sampled companies of automobile industry (r = 0).

Chart No. 4.14Debt to CE vs Average CE

Above chart showing scatter plot of two variables viz. total capitalization and

proportion of debt to capital employed for sampled companies of automobile industry

also supports the result of our hypothesis test, there is no visible pattern or relation

found from above diagram.

151

Ho: There is no correlation between total capitalization and proportion of debt to total capitalization for all sampled companies of automobile industry (r = 0).

H1: There is correlation between total capitalization and proportion of debt to total capitalization for all sampled companies of automobile industry (r ≠ 0).

Table No. 4.23 Analysis of Coefficient of Correlation andTest of the sample companies of Automobile industries

Coefficient of Correlation

DOF

t - Test H0 Calculated

Value Critical Value

0.24135 5 0.83174 2.571 Fail to

rejected

-2.571

Hence we will fail to reject null hypothesis. Therefore we can say that there is no

correlation between total capitalization and proportion of debt to total capitalization

for all sampled companies of automobile industry (r = 0).

Chart No. 4.14Debt to CE vs Average CE – Auto Companies

Above chart showing scatter plot of two variables viz. total capitalization and

ebt to capital employed for sampled companies of automobile industry

also supports the result of our hypothesis test, there is no visible pattern or relation

found from above diagram.

capitalization and proportion of debt to total

H1: There is correlation between total capitalization and proportion of debt to total

Analysis of Coefficient of Correlation and Test of the sample companies of Automobile industries

Result

Insignificant

Hence we will fail to reject null hypothesis. Therefore we can say that there is no

proportion of debt to total capitalization

Auto Companies

Above chart showing scatter plot of two variables viz. total capitalization and

ebt to capital employed for sampled companies of automobile industry

also supports the result of our hypothesis test, there is no visible pattern or relation

152

Table No. 4.24 Debt to CE of Steel industries

Name of Companies Debt to CE Average CE

Bhusan Steel Ltd. 85.24 17354.39

Essar Steel India Ltd. 79.54 21873.26

Jindal Steel and Power Ltd. 65.87 15454.06

JSW Ispat Steel Ltd 286.83 3260.63

JSW Steel Ltd 52.01 24539.58

SAIL 29.89 43946.34

Tata Steel Ltd. 40.94 66419.45

Source: Ace Analyser Database Hypothesis Testing Ho: There is no correlation between total capitalization and proportion of debt to total capitalization for all sampled companies of steel industry (r = 0). H1: There is correlation between total capitalization and proportion of debt to total capitalization for all sampled companies of steel industry (r ≠ 0).

Table No. 4.25 Analysis of Coefficient of Correlation and t – Test of the sample companies of Steel industries

Details Coefficient of Correlation

DOF t - Test

H0 Result Calculated Value

Critical Value

All Sampled Steel

Companies -0.70727 5 -2.23638 2.571

Fail to rejected

Insignificant

α=0.05;

Here,

tcal. = -2.236 < tcrit. = 2.571

Hence we will fail to reject null hypothesis. Therefore we can say that there is no

correlation between total capitalization and proportion of debt to total capitalization

for all sampled companies of steel industry (r = 0).

Chart No. 4.15Debt to CE Average Capital Employed – Steel Companies

Above chart showing scatter plot of two variables viz. total capitalization and

proportion of debt to capital employed for sampled companies of steel industry also

supports the result of our hypothesis test, there is no visible pattern or relation found

from above diagram. Moreover we can see an extreme outlier (JSW Ispat Steel) in the

above diagram.

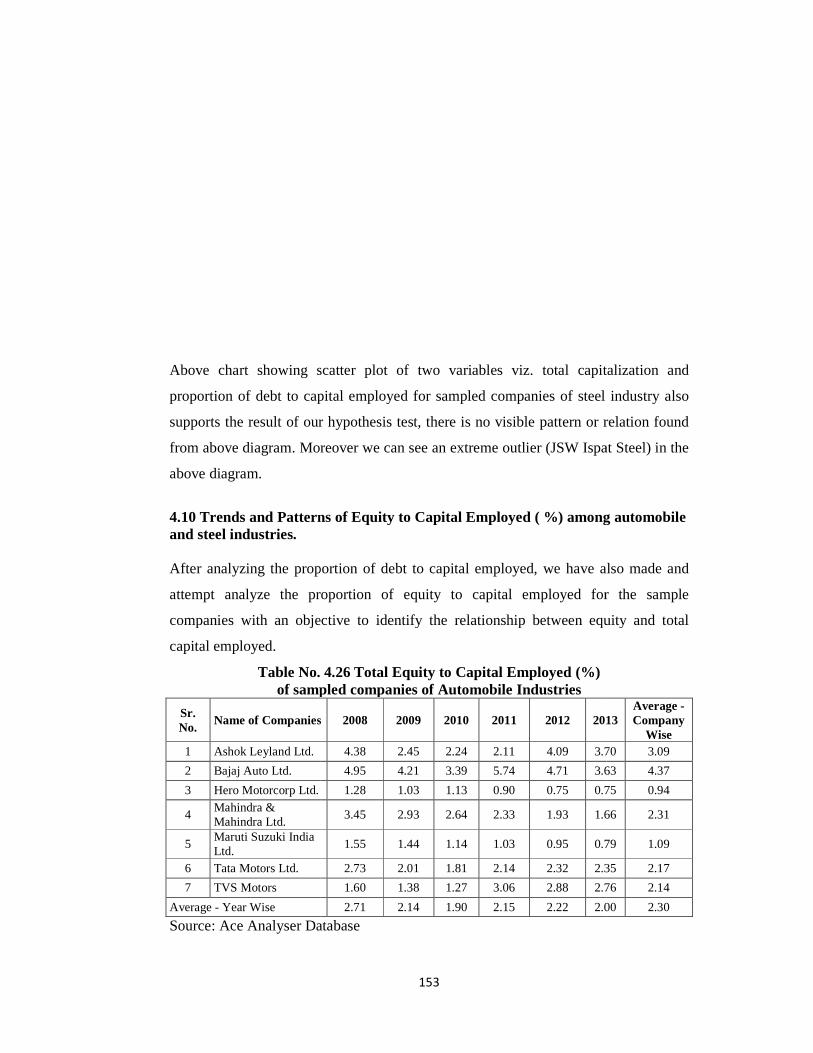

4.10 Trends and Patterns of Equity to Capital Employed ( %) among automobile and steel industries. After analyzing the proportion of debt to capital employed, we have al

attempt analyze the proportion of equity to capital employed for the sample

companies with an objective to identify the relationship between equity and total

capital employed.

Table No. 4.26 of sampled compa

Sr. No.

Name of Companies

1 Ashok Leyland Ltd.

2 Bajaj Auto Ltd.

3 Hero Motorcorp Ltd.

4 Mahindra & Mahindra Ltd.

5 Maruti Suzuki India Ltd.

6 Tata Motors Ltd.

7 TVS Motors

Average - Year Wise

Source: Ace Analyser Database

153

showing scatter plot of two variables viz. total capitalization and

proportion of debt to capital employed for sampled companies of steel industry also

supports the result of our hypothesis test, there is no visible pattern or relation found

gram. Moreover we can see an extreme outlier (JSW Ispat Steel) in the

4.10 Trends and Patterns of Equity to Capital Employed ( %) among automobile

After analyzing the proportion of debt to capital employed, we have al

attempt analyze the proportion of equity to capital employed for the sample

companies with an objective to identify the relationship between equity and total

Table No. 4.26 Total Equity to Capital Employed (%) of sampled companies of Automobile Industries

Name of Companies 2008 2009 2010 2011 2012 2013

4.38 2.45 2.24 2.11 4.09 3.70

4.95 4.21 3.39 5.74 4.71 3.63

1.28 1.03 1.13 0.90 0.75 0.75

3.45 2.93 2.64 2.33 1.93 1.66

1.55 1.44 1.14 1.03 0.95 0.79

2.73 2.01 1.81 2.14 2.32 2.35

1.60 1.38 1.27 3.06 2.88 2.76

2.71 2.14 1.90 2.15 2.22 2.00

Source: Ace Analyser Database

showing scatter plot of two variables viz. total capitalization and

proportion of debt to capital employed for sampled companies of steel industry also

supports the result of our hypothesis test, there is no visible pattern or relation found

gram. Moreover we can see an extreme outlier (JSW Ispat Steel) in the

4.10 Trends and Patterns of Equity to Capital Employed ( %) among automobile

After analyzing the proportion of debt to capital employed, we have also made and

attempt analyze the proportion of equity to capital employed for the sample

companies with an objective to identify the relationship between equity and total

2013 Average - Company

Wise 3.70 3.09

3.63 4.37

0.75 0.94

1.66 2.31

0.79 1.09

2.35 2.17

2.76 2.14

2.00 2.30

As we can see in table no. 4.25 that average equity to capital employed proportion of

all sampled companies of automobile industry for study period from 2008 to 2013 is

2.30 %. Out of the sampled companies the highest average equity to capital employed

proportion is of Bajaj Auto i.e. 4.37 % which is almost 2.07 % more than that of

average proportion. While lowest is 0.94 % that of Hero Motorcorp which is less by

1.36 % than average proportion. Ashok Leyland and Mahindra & Mahindra have

equity to total capital employed proportion more than that of average while Tata

Motors, TVS Motors and Maruti Suzuki are among the companies having equity to

capital employed proportion le

Moreover from the above figures we can also say that year on year there is fluctuating

pattern of average equity to capital employed ratio (year wise) on basis of sampled

companies of automobile industry.

Chart No. 4.16 Equity t

Above chart shows us the equity to capital employed ratio of sample companies of

automobile industry. Here we can see that for Companies like Mahindra & Mahindra,

Maruti Suzuki and Hero Motorcorp ratio is contin

companies are having fluctuation pattern for equity to capital employed ratio.

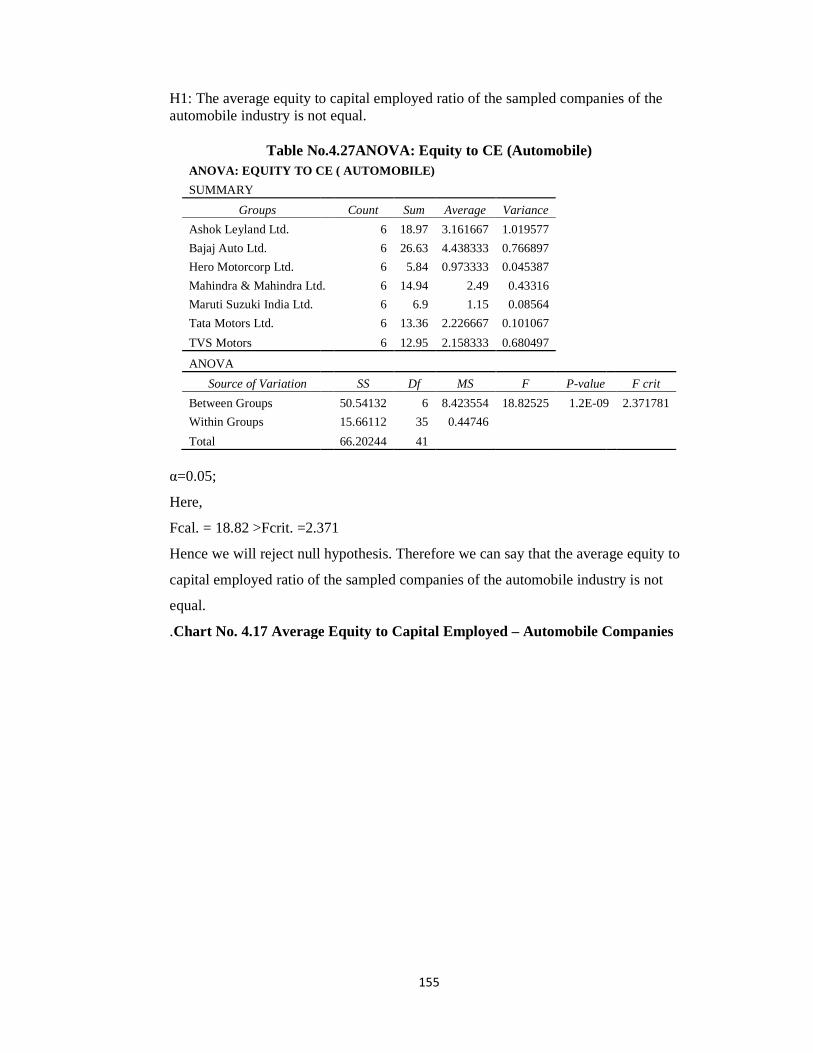

Hypothesis Testing

Ho: The average equity to capital employed ratio of the sampled companies of the

automobile industry is equal.

154

As we can see in table no. 4.25 that average equity to capital employed proportion of

all sampled companies of automobile industry for study period from 2008 to 2013 is

2.30 %. Out of the sampled companies the highest average equity to capital employed

proportion is of Bajaj Auto i.e. 4.37 % which is almost 2.07 % more than that of

average proportion. While lowest is 0.94 % that of Hero Motorcorp which is less by

han average proportion. Ashok Leyland and Mahindra & Mahindra have

equity to total capital employed proportion more than that of average while Tata

Motors, TVS Motors and Maruti Suzuki are among the companies having equity to

capital employed proportion less than average proportion.

Moreover from the above figures we can also say that year on year there is fluctuating

pattern of average equity to capital employed ratio (year wise) on basis of sampled

companies of automobile industry.

Chart No. 4.16 Equity to Capital Employed – Automobile Companies

Above chart shows us the equity to capital employed ratio of sample companies of

automobile industry. Here we can see that for Companies like Mahindra & Mahindra,

Maruti Suzuki and Hero Motorcorp ratio is continuously declining, while rest of the

companies are having fluctuation pattern for equity to capital employed ratio.

Ho: The average equity to capital employed ratio of the sampled companies of the

automobile industry is equal.

As we can see in table no. 4.25 that average equity to capital employed proportion of

all sampled companies of automobile industry for study period from 2008 to 2013 is

2.30 %. Out of the sampled companies the highest average equity to capital employed

proportion is of Bajaj Auto i.e. 4.37 % which is almost 2.07 % more than that of

average proportion. While lowest is 0.94 % that of Hero Motorcorp which is less by

han average proportion. Ashok Leyland and Mahindra & Mahindra have

equity to total capital employed proportion more than that of average while Tata

Motors, TVS Motors and Maruti Suzuki are among the companies having equity to

Moreover from the above figures we can also say that year on year there is fluctuating

pattern of average equity to capital employed ratio (year wise) on basis of sampled

Automobile Companies

Above chart shows us the equity to capital employed ratio of sample companies of

automobile industry. Here we can see that for Companies like Mahindra & Mahindra,

uously declining, while rest of the

companies are having fluctuation pattern for equity to capital employed ratio.

Ho: The average equity to capital employed ratio of the sampled companies of the

H1: The average equity to capital employed ratio of the sampled companies of the automobile industry is not equal.

Table No.ANOVA: EQUITY TO CE ( AUTOMOBILE)

SUMMARY

Groups

Ashok Leyland Ltd.

Bajaj Auto Ltd.

Hero Motorcorp Ltd.

Mahindra & Mahindra Ltd.

Maruti Suzuki India Ltd.

Tata Motors Ltd.

TVS Motors

ANOVA

Source of Variation

Between Groups

Within Groups

Total

α=0.05;

Here,

Fcal. = 18.82 >Fcrit. =2.371

Hence we will reject null hypothesis. Therefore we can say that the average equity to

capital employed ratio of the sampled companies of the automobile industry is not

equal.

.Chart No. 4.17 Average

155

average equity to capital employed ratio of the sampled companies of the automobile industry is not equal.

Table No.4.27ANOVA: Equity to CE (Automobile) ANOVA: EQUITY TO CE ( AUTOMOBILE)

Count Sum Average Variance 6 18.97 3.161667 1.019577

6 26.63 4.438333 0.766897

6 5.84 0.973333 0.045387

Mahindra & Mahindra Ltd. 6 14.94 2.49 0.43316

6 6.9 1.15 0.08564

6 13.36 2.226667 0.101067

6 12.95 2.158333 0.680497

SS Df MS F P-value

50.54132 6 8.423554 18.82525 1.2E-09

15.66112 35 0.44746 66.20244 41

Fcal. = 18.82 >Fcrit. =2.371

Hence we will reject null hypothesis. Therefore we can say that the average equity to

capital employed ratio of the sampled companies of the automobile industry is not

Average Equity to Capital Employed – Automobile Companies

average equity to capital employed ratio of the sampled companies of the

F crit

09 2.371781